fee policy statement kit: best practices for managing plan expenses - brian bouchard

TRANSCRIPT

Q4 2014

TP476

2015

Fee Policy Statement: Best Practices for

Managing Plan Expenses Under ERISA

1974

ERISA

1980’s

401(k)Plans

2000 - 2002

Corporate Fiduciary Governance

Enron, WorldCom Tyco

2002

fi360 Fiduciary Best Practices –

Investment Policy Statement

2006

Pension Protection

Act

2012

408(b)2The Game Changer

2014

Fee Policy

Statement

Evolution of DC Plan Governance

2 This material is not for distribution to plan participants.

Opening “Pandora’s Box” – Fee Documentation Process

8 This material is not for distribution to plan participants.

Basic Fiduciary Duties

▪Acting solely in the interests of the participants & their beneficiaries

▪Being “prudent”

▪Paying only reasonable and necessary expenses of the plan

▪Following the terms of the plan

▪Not engaged in prohibited transactions

Source: U.S. Department of Labor (DoL)4 This material is not for distribution to plan participants.

Investment Policy Statement & The Investment Committee

How to Write an Investment Policy StatementThe IPS is the cornerstone of a prudent process.

Most important fiduciary task

Defines roles and responsibilities

Defines a prudent process

Paper trail of a prudent investment process

How can a fiduciary follow a process that has not been defined in writing?

Best Practices for Investment CommitteesInvestment committees purpose and objectives

5 This material is not for distribution to plan participants.

Establish plan policies and procedures for investment fiduciaries

Establish and document formal process to make investment decisions

Create and execute Investment Policy Statement

Regulatory / Judicial Landscape

Regulatory Landscape

New regulations are designed to provide

plan sponsors and employees with more information from which to make better-informed decisions.

Jason C. Roberts, Esq Partner at Retirement Law Group, PC & CEO of Pension Resource Institute, LLC

Quotes are for information only and should not be considered an endorsement, testimonial or recommendation of any product or viewpoint.

7 This material is not for distribution to plan participants.

Regulatory Disclosures – 408(b)(2) & 404(a)(5)

Source: Pension Resource InstitutePhotos and quotes are for information only and should not be considered an endorsement, testimonial or recommendation of any product or viewpoint.

ERISA Sec. 408(b)(2)▪ Disclosures to plan sponsors

▪ Effective July 1, 2012 for all new and existing contracts

▪ Disclosure by all Covered Service Providers (CSP)

▪ Compensation for services rendered

▪ Fees must be reasonable

▪ Benchmarking

ERISA Sec. 404(a)(5)

▪ Disclosures to eligible employees

▪ Effective August 30, 2012 (calendar year plans)

▪ Plan more than 100 participant, add’l disclosure

▪ Non-event?

The disclosures required under these regulations have the potential to

highlight gaps in current fee allocation policies.

8 This material is not for distribution to plan participants.

New Regulations Impacting Fee Allocation

Source: Pension Resource Institute

Covered Service Providers

Required to provide disclosures into a service contract/agreement. Any changes must be disclosed

no later than 60 days from the date the service provider is notified of such change.

Form 5500/Schedule C Participant Disclosures

9 This material is not for distribution to plan participants.

Plan Sponsors

Required to be filed

annually

Must be provided prior to eligible

employees annually and

participants quarterly

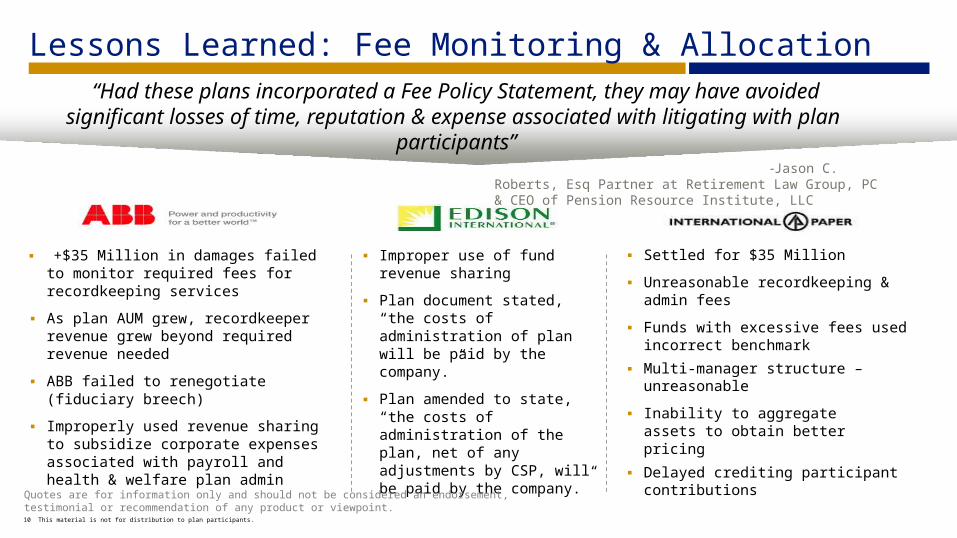

▪ Settled for $35 Million

▪ Unreasonable recordkeeping & admin fees

▪ Funds with excessive fees used incorrect benchmark

▪ Multi-manager structure – unreasonable

▪ Inability to aggregate assets to obtain better pricing

▪ Delayed crediting participant contributions

10 This material is not for distribution to plan participants.

▪ Improper use of fund revenue sharing

▪ Plan document stated, “the costs of administration of plan will be paid by the company.”

▪ Plan amended to state, “the costs of administration of the plan, net of any adjustments by CSP, will be paid by the company.”

▪ +$35 Million in damages failed to monitor required fees for recordkeeping services

▪ As plan AUM grew, recordkeeper revenue grew beyond required revenue needed

▪ ABB failed to renegotiate (fiduciary breech)

▪ Improperly used revenue sharing to subsidize corporate expenses associated with payroll and health & welfare plan admin

“Had these plans incorporated a Fee Policy Statement, they may have avoidedsignificant losses of time, reputation & expense associated with litigating with plan

participants”-Jason C. Roberts,

Esq Partner at Retirement Law Group, PC & CEO of Pension Resource Institute, LLC

Lessons Learned: Fee Monitoring & Allocation

Quotes are for information only and should not be considered an endorsement, testimonial or recommendation of any product or viewpoint.

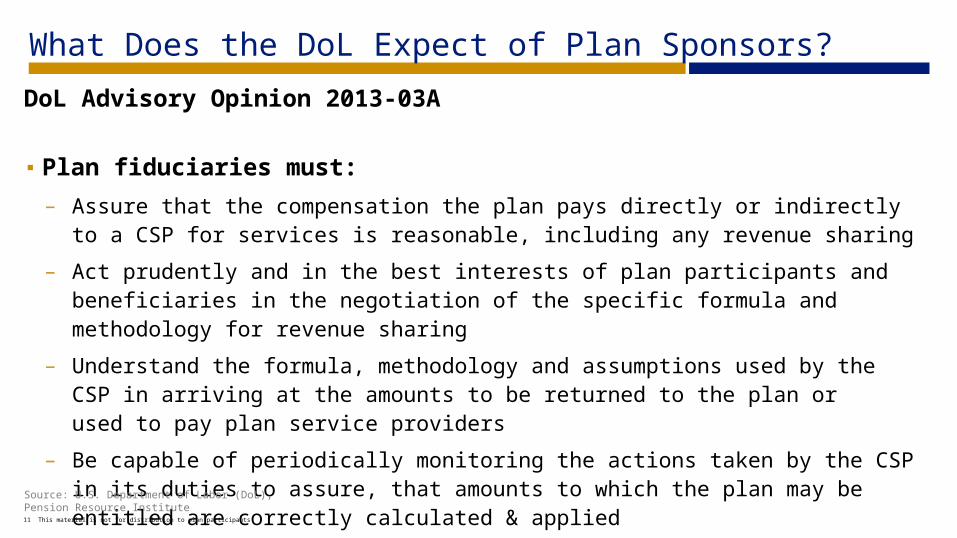

What Does the DoL Expect of Plan Sponsors?

DoL Advisory Opinion 2013-03A

▪Plan fiduciaries must:

– Assure that the compensation the plan pays directly or indirectly to a CSP for services is reasonable, including any revenue sharing

– Act prudently and in the best interests of plan participants and beneficiaries in the negotiation of the specific formula and methodology for revenue sharing

– Understand the formula, methodology and assumptions used by the CSP in arriving at the amounts to be returned to the plan or used to pay plan service providers

– Be capable of periodically monitoring the actions taken by the CSP in its duties to assure, that amounts to which the plan may be entitled are correctly calculated & applied

Source: U.S. Department of Labor (DoL), Pension Resource Institute11 This material is not for distribution to plan participants.

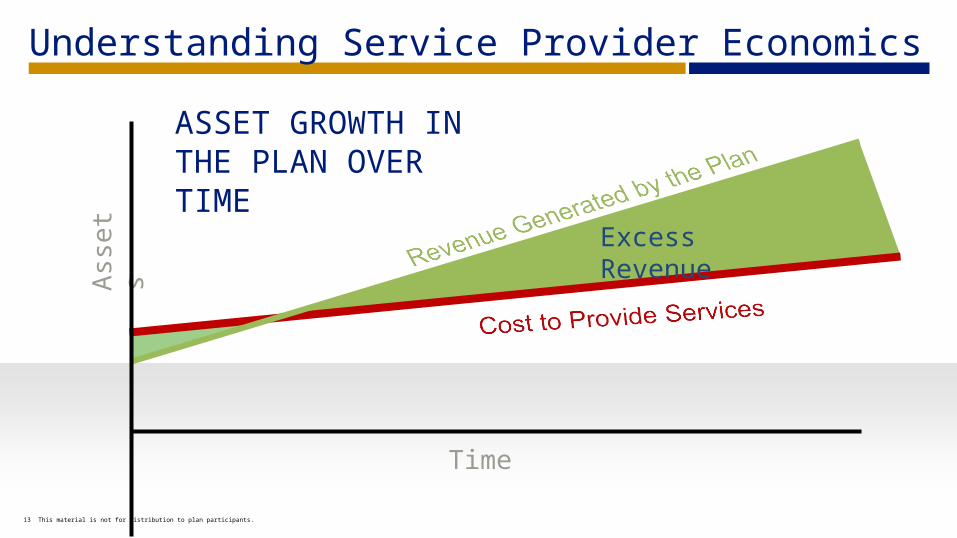

Refresher: Understanding Plan Costs & Revenue Sharing

Most of a plan’s costs are offset by the investments in a practice known as “revenue sharing” here’s how it works:

12 This material is not for distribution to plan participants.

Understanding your plan's costs:

Investment expenses(Expense ratios and management fees)

+ Recordkeeping and administration fees

+ Advisory expenses(Investment advisors, consultants, accountants, attorneys)

= Total Plan Cost

Understanding Service Provider Economics

ASSET GROWTH INTHE PLAN OVERTIME

Ass

ets

Time

13 This material is not for distribution to plan participants.

Excess Revenue

Fee Policy Statement:

Controlling and Allocating Plan Expenses

What is a Fee Policy Statement?

▪A plan governance tool to provide plan fiduciaries with a documented and systematic approach to making decisions affecting the management of the plan.– Who is paying the fee to the recordkeeper of the plan?

– How are plan expenses paid or allocated?

– How is excess revenue being captured and allocated?

– How often are fees monitored?

15 This material is not for distribution to plan participants

Creating a Fee Policy

▪Purpose

– To satisfy ERISA and prudently discharge duties to pay expenses

▪Fee policies

– How to pay for and allocate plan expenses

▪Monitoring frequency

▪Method of revenue sharing recapturing

– PERA / ERISA account

– Fee equalization

– Ensure CSPs are following the policy

16 This material is not for distribution to plan participants

The Fee Documentation Process

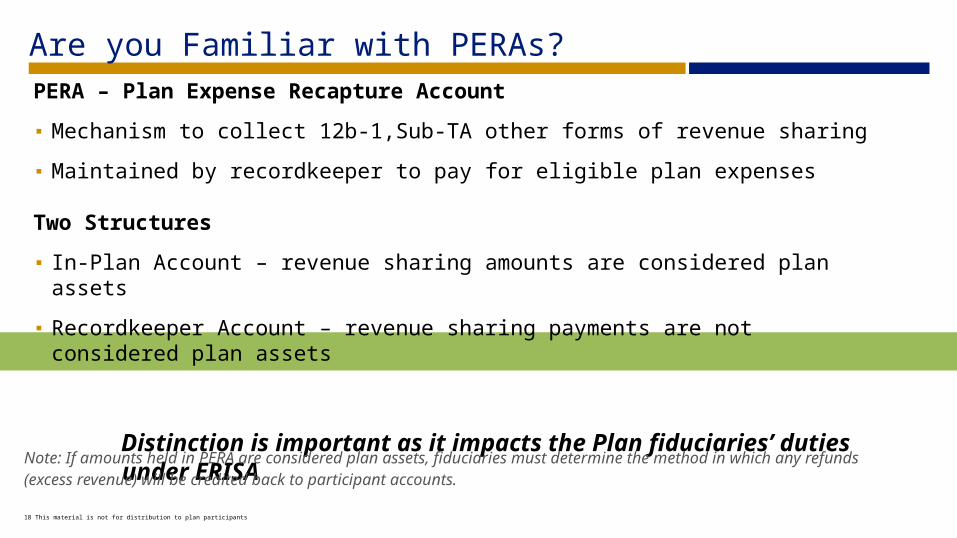

Are you Familiar with PERAs?PERA – Plan Expense Recapture Account

▪ Mechanism to collect 12b-1,Sub-TA other forms of revenue sharing

▪ Maintained by recordkeeper to pay for eligible plan expenses

Two Structures

▪ In-Plan Account – revenue sharing amounts are considered plan assets

▪ Recordkeeper Account – revenue sharing payments are not considered plan assets

Distinction is important as it impacts the Plan fiduciaries’ duties under ERISA

Note: If amounts held in PERA are considered plan assets, fiduciaries must determine the method in which any refunds (excess revenue) will be credited back to participant accounts.

18 This material is not for distribution to plan participants

19 This material is not for distribution to plan participants

Settlor v. Non-Settlor Expenses

What are eligible plan expenses under ERISA?

Source: Jason Roberts, PRI

The following fees typically are considered non-settlor fees and can be paid from plan assets:

Recordkeeping fees Participant education fees

Trustee fees Legal fees (related to non-settlor functions, i.e. preparation of required ongoing plan amendments)

Custodial fees Investment management fees

Plan accounting fees Plan fidelity bond fees

Plan audit fees Fees associated with IRS determination letter application

Plan actuarial service fees Loan administration fees

Reporting fees (Form 5500, etc.)

QDRO fees

Participant communication fees

The following fees typically are considered settlor fees and cannot be paid from plan assets:

Plan design or other fees associated with the establishment of the plan

EPCRS/VCP compliance fee

Plan termination fees VFC correction fees

Fees associated with discretionary plan amendments

Amendment of plan for a merger or spin-off

Audit CAP sanctions

Does the Provider Offer a Recapture Account or Other Equalization Method?

20 This material is not for distribution to plan participants

Questions▪ If PERA, then how are credits accounted for (e.g. on books of provider vs.

unallocated plan account)?

▪What process does the plan have to monitor the credits?

▪ If equalized, how does the method affect various classes of participants?

▪ Is the arrangement reasonable?

Expense Allocation Methods

Background: Expense Allocation Methods

22 This material is not for distribution to plan participants

Traditional methods for allocating plan expenses include:

▪ Solely paid for by the company (from corporate assets)

▪ By the company less any credits received from investments (revenue sharing)

▪ Solely paid by the plan’s participants

Methods for administrative expenses paid by the plan/participants:

▪ CSPs billing plan directly deducting expenses from participants’ accounts or from forfeiture accounts

▪ CSPs offsetting fees with revenue sharing, deducting additional cost from participants

▪ Use of PERA to collect revenue sharing to pay CSPs directly and excess revenue sharing returned to Plan or retained by the recordkeeper.

Fiduciaries must determine if the expense is properly paid from plan assets and fee allocation method among participants (e.g. on pro rata or per capita basis).Source: Jason Roberts, PRI

Allocating Expenses and/or Credits

23 This material is not for distribution to plan participants

▪ Pro Rata: allocated on the basis of the account size of the participant in relation to the plan’s total assets

▪ Per Capita: spread out equally among all participants

▪ Hybrid Method: combined pro rata & per capita approach

▪ Fee Equalization: recordkeeping costs are applied evenly across all funds in the plan

▪ Individual Charges: charges to individuals who receive specific services, such as loan fees, QDROs, etc.

Source: Jason Roberts, PRI

Which Approach is Reasonable? - Appropriate? - Fair?

Source: Callan

DoL’s FAB 2003-3:

Choosing dollar or basis point fee deemed “most appropriate” depends on what is “solely in the

interest of participants”. It can disfavor one class of participants - “provided that a rational

basis exists for the selected method”.

Flat dollar into basis point charge

24 This material is not for distribution to plan participants

Fees assessed on a percentage basis

Hypothetical Plan

Example: Plan Assets:

$100M

# Participants: 2,000

Admin Costs: $100k

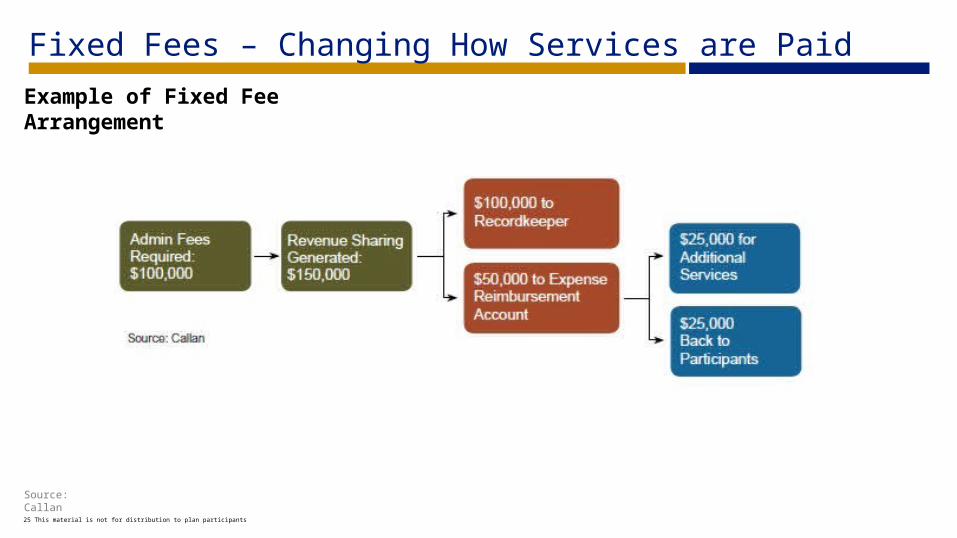

Fixed Fees – Changing How Services are Paid

Example of Fixed Fee Arrangement

Source: Callan25 This material is not for distribution to plan participants

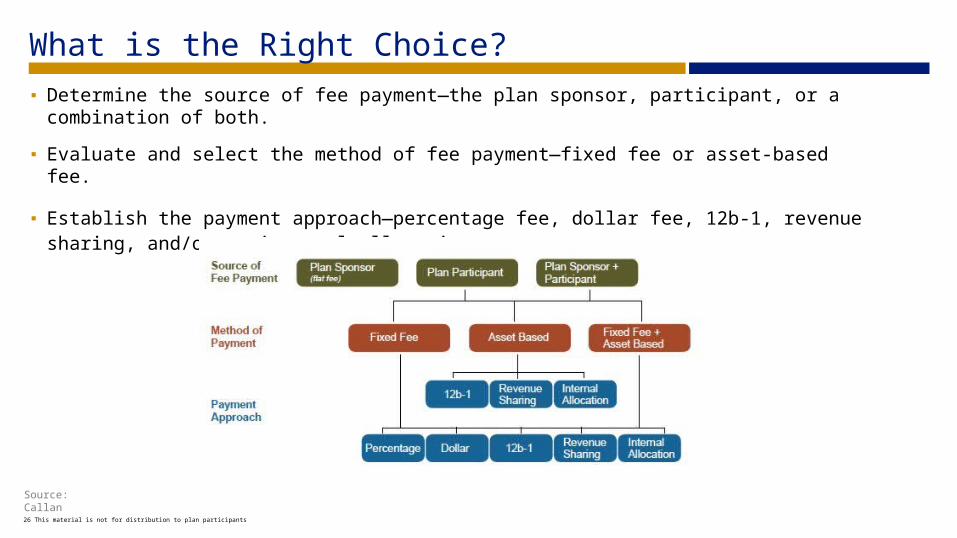

What is the Right Choice?▪ Determine the source of fee payment—the plan sponsor, participant, or a combination of both.

▪ Evaluate and select the method of fee payment—fixed fee or asset-based fee.

▪ Establish the payment approach—percentage fee, dollar fee, 12b-1, revenue sharing, and/or an internal allocation.

Source: Callan26 This material is not for distribution to plan participants

Ethos and the Prudent Process

401k Ethos & the “Prudent” Process

Don TroneCo-Author of 401k Ethos

28 This material is not for distribution to plan participants

Ethos (ē-thäs) gr.

The link between leadership behaviors, core

values and a decision-making process

Ethos and Governance

29 This material is not for distribution to plan participants

Provides a decision-making framework which grants the capacity to manage all three facets: regulatory, governance, and stewardship. This framework is the essence of ethos.

Source: 3EthosLicensed to the Leadership Center for Investment Stewards

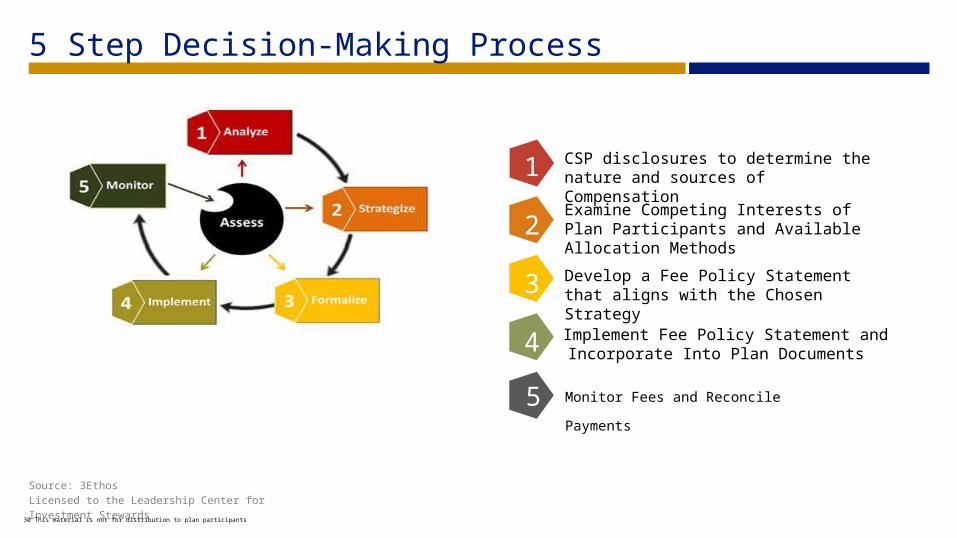

5 Step Decision-Making Process

Source: 3EthosLicensed to the Leadership Center for Investment Stewards

CSP disclosures to determine the nature and sources of Compensation

Examine Competing Interests of Plan Participants and Available Allocation Methods

Develop a Fee Policy Statement that aligns with the Chosen Strategy

Implement Fee Policy Statement and Incorporate Into Plan Documents

Monitor Fees and Reconcile Payments

1

2

3

4

30 This material is not for distribution to plan participants

5

31 This material is not for distribution to plan participants

Leadership does not come with detailed maps – only a general sense

of direction.Don Trone

Co-Author of 401k Ethos

Quotes are for information only and should not be considered an endorsement, testimonial or recommendation of any product or viewpoint.

Advisor Best Practices and Getting Started

Plan Sponsor Guide – for introducing the conversation and explaining how the FPS can help plan fiduciaries manage risk and save time

ERISA Plan Expense Worksheet – for helping plan fiduciaries evaluate plan expenses

Sample Fee Policy Statement – a framework for documenting decisions about expenses

Implementing the Fee Policy Statement – Process and Sales Ideas

Beyond Benchmarking: Advisor Best Practices & Tools

The Advisor Guide and kit materials are designed to provide a framework for Reviewing plan expenses and working with plan sponsors to develop and implement a Fee Policy Statement.

What Plan Sponsors need to access

33 This material is not for distribution to plan participants

CSP(s)

408(b)(2) Disclosures

Fiduciaries

DOL / IRS

Schedule C

Form 5500

Employees/Participants 404(a) Disclosures

Document with a Fiduciary Audit File

✓ Fee Policy

Statement

Audit Files Checklist

▪ One of the most important best practices:Prudent process and consistent documentation

▪ The fiduciary audit file is one of the most valuable tools to document prudent process.

▪ Get it right, and get it in writing.✓Plan Documents✓Gov’t / Regulatory Requirements &

Communications

✓Journals and Ledgers✓Section 404(c) Compliance

✓ERISA Fidelity Bond✓Participant Communication Documents✓Investment Policy Statement✓Third Party Service Provider Documents✓Procedures and Minutes of All Meetings

34 This material is not for distribution to plan participants

Brian P. BouchardBrian P. Bouchard, AIF ®, CRPC ®, CRPS ®

Regional Retirement Consultant

Brian Bouchard is the regional retirement consultant for the Northeast Region at Thornburg Investment Management. He has over 20 years of experience in qualified plan sales. At Thornburg, he is responsible for delivering the firm’s investment only retirement plan focused sales strategy and value-added services to plan advisor and retirement plan platform alliances.

Prior to joining Thornburg, Brian was a retirement plan consultant at Merrill Lynch in New England, and a regional retirement director for the Morgan Stanley Smith Barney Retirement Group. Brian received his BA from The Catholic University of America, and a Graduate Certificate of Special Studies in Administration and Management from the Harvard University Extension School. He is currently registered with FINRA with a Series 7 and also holds the AIF, CRPC and CRPS designations.

35 This material is not for distribution to plan participants.

www.thornburg.comBefore investing, carefully consider the Fund’s investment goals, risks, charges, and expenses. For a prospectus or summary prospectus containing this and other information, contact your financial advisor or visit thornburg.com. Read them carefully before investing.

Not FDIC Insured. May lose value. No bank guarantee.

Thornburg Funds are distributed by Thornburg Securities Corporation.

2300 North Ridgetop Road Santa Fe, New Mexico 87506

877-215-1330