federal and state healthcare reform: the potential financial impact on employers and employees

DESCRIPTION

Federal and State Healthcare Reform: The Potential Financial Impact on Employers and Employees. Tom Rugg, MBA Hickok and Boardman Group Benefits [email protected]. Judicial Update – Moving on. The Affordable Care Act (ACA) and the Supreme Court. - PowerPoint PPT PresentationTRANSCRIPT

Federal and State Healthcare Reform: The Potential Financial Impact on Employers and Employees

Tom Rugg, MBAHickok and Boardman Group [email protected]

2

Judicial Update – Moving on...

3

The Affordable Care Act (ACA) and the Supreme Court

The Court’s decision wasn’t much of a surprise, but the reason behind it

sure was

The Court concluded the individual mandate was not constitutional under the Commerce Clause, but could be justified within Congressional power to levy taxes

The decision did finally clear the way for the federal government and

employers to push forward with full-speed ACA implementation

But………hesitations on implementation lingered until……….

4

November Elections – Changes Coming? Not Likely

5

The Post-Election Scenario:

Obama’s re-election puts to rest any thoughts of repealing the ACA

The US House:

Republicans maintain a 233-193 edge

The votes do not exist to override a presidential veto

The US Senate:

Democrats maintain a 55-45 edge

60 votes are needed to stop a Senate filibuster

Expect only potential minor tweaks to the ACA over the next two years

6

Federal Reform – Where are we at?

7

The ACA in 2013: Getting Ready for Main Event

The year will focus on final preparations for the new state health insurance Exchanges, which must be ready for enrollment in the fall of 2013. The year’s key provisions are:

Flexible Spending Account limits

Expanded authority to bundle payments

Increase Medicare Part A tax on wages by 0.9 percent

Here come the fees……..CERF’s up!

8

The ACA in 2013: Flexible Spending Account Limits

Annual employee contributions to FSA’s capped at $2,500

Like HSA contributions, amount will be indexed to the CPI starting in 2014

No limit on employer contributions

Beware! Contribution limit applies on a calendar year basis – potential issues for non-calendar year FSA’s

9

The ACA in 2013: Medicare Part A Tax

The ACA taxes single individuals with yearly

income greater than $200,000 from self-

employment or wages by 0.9 percent.

For married couples, an income of $250,000 for those filing jointly or $125,000 for a married person filing separately would also be taxed.

An additional tax of 3.8% applies to net investment income or an adjusted gross

income that exceeds $200,000, whichever is less.

For married couples, either the net investment income or an adjusted gross income that exceeds $250,000 for those filing jointly or $125,000 for a married person filing separately would also be taxed.

10

The ACA in 2013: Comparative Effectiveness Research Fee... now affectionately

known as The Patient-Centered Outcomes Research Fee

Revenue from this fee will fund research to determine the effectiveness of various forms of medical change.

Annual fee on both fully insured (fee built into rates) and self-insured (self reported on Excise Tax Form 720) health plan

Applies to plan years beginning after 10/1/2011 and continues through 2019

First payments are due on July 31, 2013 ~Self-funding reminder~!!!!!!

Initial annual fee is $1 per plan participant, including dependents

Increases to $2 in 2012 and indexed for inflation for future years

11

The ACA in 2013: Comparative Effectiveness Research Fee... now affectionately

known as The Patient-Centered Outcomes Research Fee

Fee will apply to the following: Medical plans (fully insured and self-insured)

Stand alone behavioral health plans

Medicare supplements plans

Health Reimbursement Arrangements (HRA’s)

The fee does not apply to: Health Savings Accounts (HSA’s)

Stand alone dental and vision plans

Employee Assistance Plans (EAP’s)

Medicare Parts A through D

12

The ACA in 2013: Comparative Effectiveness Research Fee... now affectionately

known as The Patient-Centered Outcomes Research Fee

Uh-oh, special rules for account-based plans

Flexible Spending Arrangements (FSAs) are exempt from the fees (unless FSA is only benefit option offered)

HRAs will generally be subject to the fees

If a plan consists of insured coverage (such as an insured medical benefit) plus an HRA, both the plan sponsor of the HRA and the issuer of the medical benefit will pay the fees, even if the lives covered under both are the same

Plan sponsors that provide self-insured health coverage and a self-insured HRA would pay the fee once for each individual enrolled in the plan. The self-insured coverage is not counted separately from the HRA.

13

The ACA in 2013: Comparative Effectiveness Research Fee... now affectionately

known as The Patient-Centered Outcomes Research Fee

14

The ACA in 2014: The Crescendo

Most of the key changes that are expected to get health insurance to millions of uninsured Americans, improve care, and reduce costs begin in 2014. The year’s key provisions are:

Individual insurance mandateEmployer insurance mandateEssential health benefitsExcise taxesNo pre-existing conditions for all agesClinical trialsAnnual dollar limits on essential health benefitsEligibility provisionsGuarantee issueExchanges go into effectAuto enrollmentPremium tax credits

15

Under the ACA, all people must have minimum essential coverage beginning January 1, 2014

“Minimal essential coverage” is:

Government sponsored plan

Employer sponsored plan

Individual plan

If a person cannot keep minimum essential coverage, the Internal Revenue Service will collect a tax penalty from him or her. The annual tax penalty is described as the greater of:

2014: $95 per uninsured adult in the household (capped at $285 per household) or one percent of the household income over the filing threshold

2015: $325 per uninsured adult in the household (capped at $975 per household) or two percent of the household income over the filing threshold

2016: $695 per uninsured adult in the household (capped at $2,085 per household) or 2.5 percent of the household income over the filing threshold

The ACA in 2014: Individual Insurance Mandate

16

Furthermore……..

For dependent children under the age of 18, the penalty is half the individual amount

The flat dollar penalty is capped at 300% of the flat dollar amount

Family of three (two parents and one child) without insurance in 2014 would pay $95+$95+$47.50=$237.50

Family of five (two parents and three children) would pay $95+$95+$47.50+$47.50+$47.50=$285 and not the math equivalent of $332.50 because the 300% cap would apply

Percentage of taxable income calculation is the amount of household’s income that is in excess of the tax filing threshold (personal exemption plus the standard deduction, which is assumed to be $10,000 in 2014)

An individual with an income of $50,000 - $10,000 assumed threshold in 2014 x 1% = $400, which is greater than the $95 flat dollar amount

In general, the penalty is capped at an amount equal to the national average cost of a bronze level plan offered in the Exchange

If incurred, the penalty will be paid as a federal tax liability on income tax returns. Those that fail to pay the tax will not be subject to criminal penalties, liens or levies

The ACA in 2014: Individual Insurance Mandate

17

The ACA in 2014: Employer Insurance Mandate

Beginning January 1, 2014, employers must offer health insurance that employees can afford. The ACA also says that the plan offered must give employees a certain amount of value in that the plan must pay 60 percent of the cost of health services. If an employer does not meet these criteria, they will be assessed a tax.

According to Health and Human Services, a plan:

Provides minimum value if it pays at least 60 percent of the cost of services

Is affordable if a full-time employee does not have to pay more than 9.5 percent of household income for the premium

There are no tax penalties for employers with less than 50 full-time employees, or the equivalent.

18

The ACA in 2014: Employer Insurance Mandate

How do I know if I’m a “large” employer with greater than 50 employees? Calculation is based on full-time-equivalents Part-time employees are calculated by taking the aggregate number of

hours worked in a month divided by 120

A “large” employer must offer minimum value and affordable coverage to all full-time employees working 30 hours or more a week or pay a penalty

Employers would also be taxed if one or more employees can get federal premium assistance to buy health insurance through an exchange

An employers first 30 employees are exempt from the tax

19

20

21

The ACA in 2014: Health Insurance Industry Fee

Beginning in 2014, the ACA will tax health insurance companies based on their market share. The rate of this new excise tax rises each year between 2014 and 2018, and then increases at the rate of inflation.

In 2014, the fee raises $8 billion and increases on a fixed dollar schedule through 2018

2015: $11.3 billion

2016: $11.9 billion

2017: $12.6 billion

2018: $14.3 billion. Beyond 2018, the total annual fee amount will increase in direct proportion to the growth in health insurance premiums

Applies only to fully insured plans, but does include dental and vision benefits

Fee is NOT tax deductible, which significantly increases the cost impact which is expected to be in the range of 2 to 2.5% of premium in 2014, increases to 3% to 4% in future years

Also……..pharmaceutical companies will be taxed on market share, which is expected to yield $2.5 billion annually while certain medical devices will be taxed at 2.3%.

22

The ACA in 2014: Reinsurance Assessment

Beginning in 2014, the ACA will assess both fully insured and self-insured medical plans to reimburse companies that insure high-cost individuals within the individual insurance market.

Assessment works on a fixed dollar schedule and applies to medical plans only

In 2014, the total assessed amount is $12 billion, or roughly $75 per member per year

2015: $8 billion, roughly $50 per member per year

2016: $5 billion, roughly $30 per member per year

This assessment is tax-deductible

23

The ACA in 2014:Health Insurance Exchanges

All states are required to have Exchanges functioning by January 1, 2014 and ready for open enrollment by October 2013.

Exchanges will offer standardized health plans in an effort to make health insurance more accessible and easier to purchase for small businesses and individuals.

Individuals purchasing coverage through an exchange may be eligible for federal premium assistance under certain circumstances

Exchanges will allow individual and small business to purchase health plans at five benefit levels: Platinum (90% AV)

Gold (80% AV)

Silver (70% AV)

Bronze (60% AV)

Catastrophic (below 60% AV, only can be purchased by young adults)

24

The ACA in 2014:Health Insurance Exchanges

Exchanges will vary from state to state, but they all must conform to requirements determined by the Department of Health and Human Services.

Any plan offered by an insurer through an Exchange must be a Qualified Health Plan

Who might use the exchanges? Who is eligible for a subsidy?

25

The ACA in 2014: Premium Tax Credits

The ACA provides that, beginning in 2014, individuals will be eligible for refundable premium tax credits if they: Are not eligible for health insurance coverage through an employer or through

a government program;

Have modified adjusted gross household incomes (MAGI) between 100 percent and 400 percent of the federal poverty level;

Are citizens of or lawfully present in the United States and not incarcerated (other than pending final disposition of charges);

The tax credits will be paid on a monthly basis directly to the qualified health plan (QHP) that an individual enrolls in through the exchange. Individual must be enrolled in at least a “silver” tiered plan, to receive subsidies

26

The ACA in 2014: Premium Tax Credits

Who’s eligible?????? The individual must be an “applicable taxpayer” (i.e., file a tax return and not

be claimed as a dependent on someone else’s return)

The applicable taxpayer’s family, which is also covered by the tax credit, includes all persons for whom the taxpayer claims a dependent tax deduction

Income based ranging from 100-400% of the Federal Poverty Level (FPL)

Income below 100% FPL trigger Medicaid eligibility Starting in 2014, Medicaid eligibility expands to 133% of FPL

• In 2014 dollars, 133% of FPL = $15,000 of annual income for individuals; 400% of FPL = $46,000 for individual

• For a family of four, 133% of FPL = $32,000; 400% of FPL = $93,700

27

The ACA in 2018 & 2020:What’s Left?!?!?!

For 2018…….

A 40% tax on excessive benefits begins. Also known as the Cadillac tax

Limits benefits to $10,200 for single person plans and $27,500 for family plans in 2018. Excess is what is taxed.

For 2020…….

The “Donut Hole” in the Medicare Part D prescription drug benefit is phased out. Enrollees will pay a standard 25% coinsurance on drug costs until they reach the threshold for catastrophic coverage

28

Vermont – It’s All About the Exchange

29

Vermont-Specific Changes Implemented in 2012

Key ACA Changes Related to Insurance Markets

Definition of a “small group” for purposes of the Vermont Health Benefit Exchange

To remain at the current community-rated level of 50 eligible employees for 2014 and 2015

An employer that had no more than 50 employees on at least 50% of its working days

Does not include a part-time employee working fewer than 30 hours per week

Per the ACA, small group definition changes to 100 eligible employees in 2016

Preemption of Vermont’s association market rating rules

Say good-bye to VACE, BRS, VHSG, and AIVIS

We’re sticking around!

Federal law allows for “grandfathered” plans to remain intact. Very few plans will have retained grandfathered status by 2014, but a majority of those will be those plans offered by school districts

30

Vermont-Specific Changes Implemented in 2012

Key ACA Changes Related to Insurance Markets

Merging of the individual and small group health markets

All small group plans MUST be sold through the Exchange

No alternative “off-exchange” market

Bronze level plans allowed for sale in the Exchange

Original plan only allowed the sale of platinum, gold, and silver plans

Creates a role for brokers to assist with enrollment through the Exchange

The intent of the Shumlin Administration remains that the Exchange will serve as the initial step towards a single payer system called Green Mountain Care

31

Vermont-Specific Changes Implemented in 2012 What needs to be decided in the next 6-8 months:

What carriers will offer plans on the Exchange

BC/BS of Vermont and MVP Healthcare

What will the plans cost

What will the plan designs look like

1 platinum plan

1 gold plan

2 silver plans

2 bronze plans

3 “Choice” plans designed by insurance carriers at each metal level

32

33

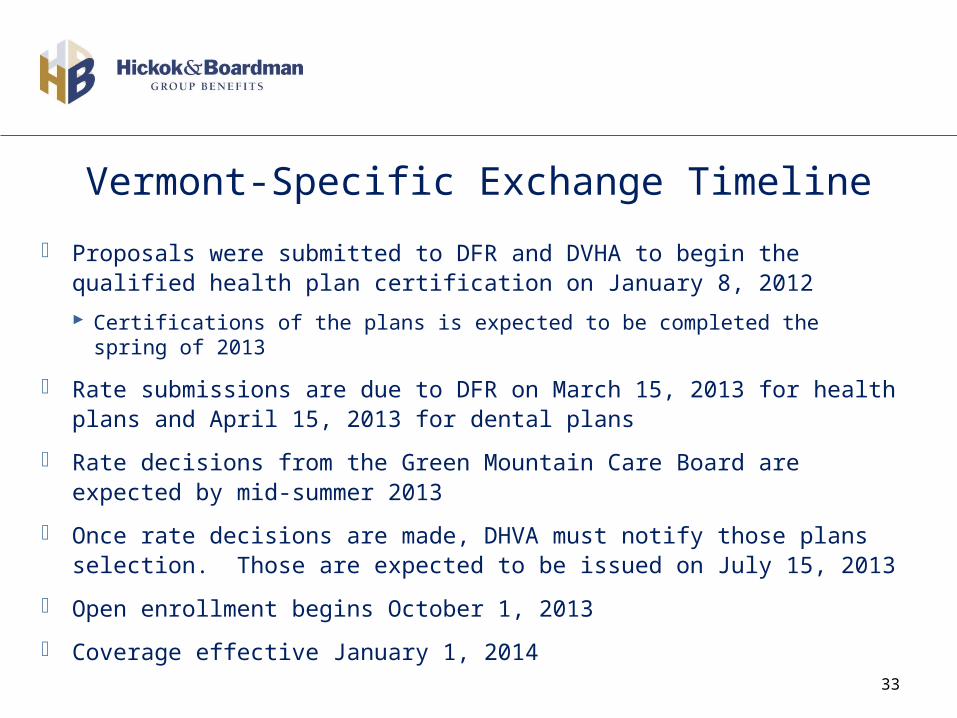

Vermont-Specific Exchange Timeline

Proposals were submitted to DFR and DVHA to begin the qualified health plan certification on January 8, 2012

Certifications of the plans is expected to be completed the spring of 2013

Rate submissions are due to DFR on March 15, 2013 for health plans and April 15, 2013 for dental plans

Rate decisions from the Green Mountain Care Board are expected by mid-summer 2013

Once rate decisions are made, DHVA must notify those plans selection. Those are expected to be issued on July 15, 2013

Open enrollment begins October 1, 2013

Coverage effective January 1, 2014

34

Vermont – Today’s Issues... The “Catamount Assessment”

With the advent of the Exchange in 2014, state-subsidized insurance programs expire

The Administration has proposed to keep the current assessment in place even though Catamount Health will be going away

Potential employer paradox of being recommended to drop employer sponsored coverage, but being taxed if you do so

Administration claims the dollars will be used to pay for the same services next year as it does now

35

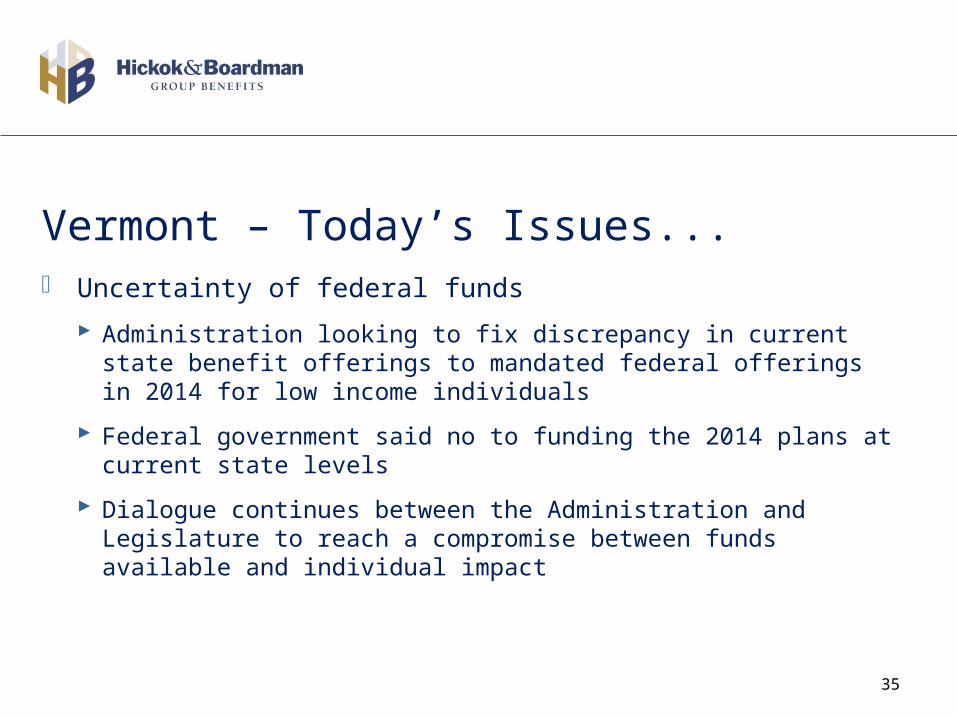

Vermont – Today’s Issues... Uncertainty of federal funds

Administration looking to fix discrepancy in current state benefit offerings to mandated federal offerings in 2014 for low income individuals

Federal government said no to funding the 2014 plans at current state levels

Dialogue continues between the Administration and Legislature to reach a compromise between funds available and individual impact

36

Nationwide Estimates of Plan Designs Meeting Selected ACA Actuarial Value Thresholds, 2014

Actuarial Research

Corporation Aon Hewitt Towers Watson

Actuarial Value

Out-of-Pocket Maximum Deductible Coinsurance Deductible Coinsurance Deductible Coinsurance

A 60% $6,350 $6,350 0% $4,350 20% $2,750 30%

B 70% $6,350 $4,200 20% $2,050 20% $1,850 20%

C 70% $4,200 $4,200 0% $2,650 20% $1,550 30%

D 70% $3,200 $3,200 0% $3,200 0% $2,050 30%

E 73% $3,200 $3,200 0% $3,200 0% $1,750 25%

G 87% $2,100 $1,050 20% $250 20% $150 20%

I 94% $2,100 $60 10% $200 5% $0 8%

37

38

Ok, now what do I do?

As an employer, do I?

Continue to provide an employer-sponsored health plan to employees No longer offer an employer-sponsored plan health plan and let employees purchase coverage through

the Exchange with premium subsidies

Part of the decision making formula will involve:

Current plan costs compared to paying a penalty for not offering coverage Making assumptions of family household income

Available subsidies Affordability

The impact:

Employers will terminate their plan offering(s) Employers will offer benefits on a defined contribution basis as opposed to a defined benefit The rest will continue offering benefits similar to the way they do now