february 25 th 2013. agenda aims of partnering trusted partner concept accounts and services...

TRANSCRIPT

February 25th 2013

AgendaAims of PartneringTrusted Partner conceptAccounts and servicesDelivery / kiosk networkBHSF – working in partnership

UK personal banking 9m adults without fit for purpose banking solutionPrepaid card market at c£650mHome credit & mail order £3bnArrears on utilities, rents and mortgages are

common

Poverty premium of £1k per annum

High cost, highly promoted and easy access payday lending sector now worth est £2bn

Potential

DWP feasibility report 2012 - “credit unions appear to be the only other realistic option”

Between 25% and 50% of the populations of the USA, Canada, & Australia are credit union members

Citysave aim for 5% of Birmingham market in 5 years

Aims of Partnering

Birmingham 187 identified communitiesDiverse & busyCitysave needs to reach into communities Need to find ways to overcome barriers to

opening accounts including language, literacy, confidence, trust

Need to find ways to scale efficiently Need to deliver a wider range of products to

a wider range of membership Those most at risk of paying poverty

premium are least likely to engage

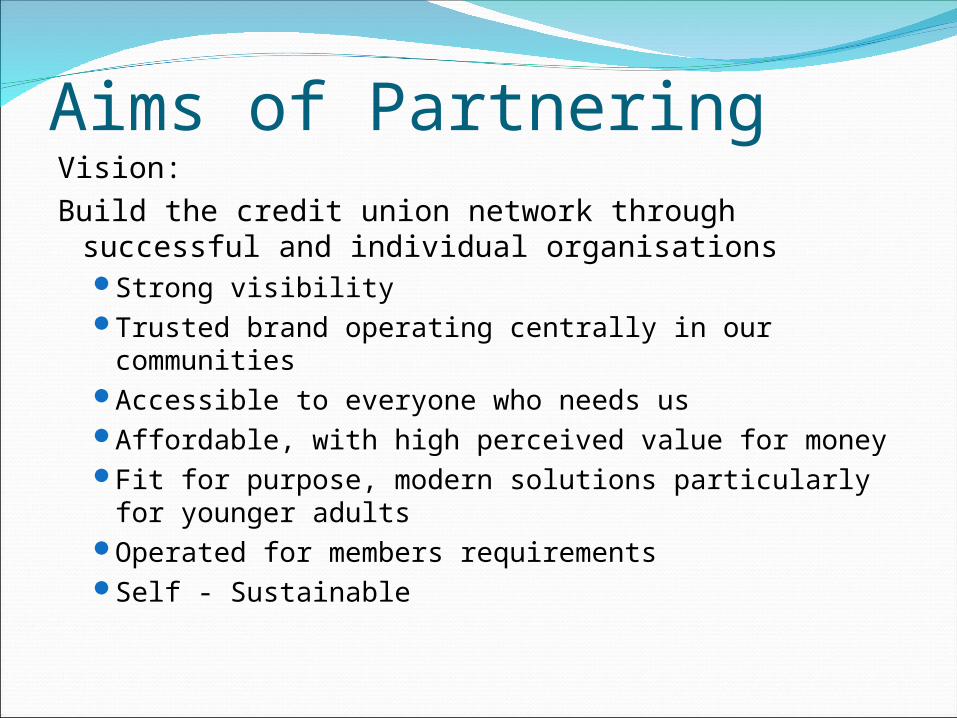

Aims of PartneringVision: Build the credit union network through successful

and individual organisations Strong visibilityTrusted brand operating centrally in our

communitiesAccessible to everyone who needs usAffordable, with high perceived value for moneyFit for purpose, modern solutions particularly for

younger adultsOperated for members requirementsSelf - Sustainable

For our membersBetter money managementBetter payment solutionsRemoval of poverty premiumBranded and trusted long term financial

alternative Good access to community based financial

institutionsLess reliance on lending & Saving ethic Access to affordable lendingAccess to first time buyer mortgages – shared

ownership and easy start options

Members of a modern financial co-operative

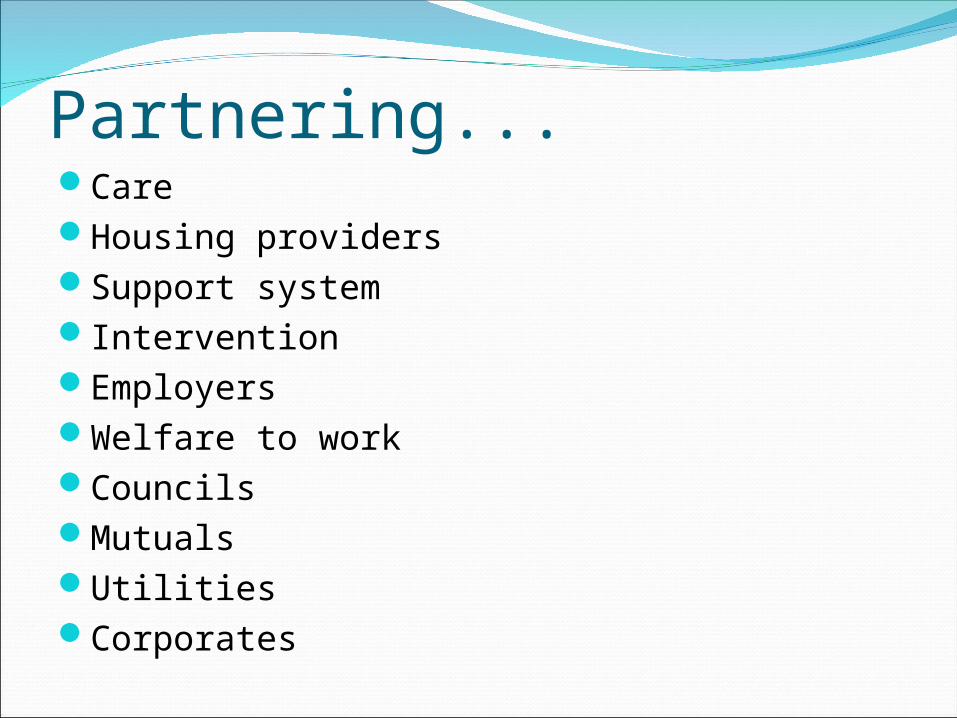

Partnering...CareHousing providersSupport systemInterventionEmployersWelfare to workCouncilsMutualsUtilities Corporates

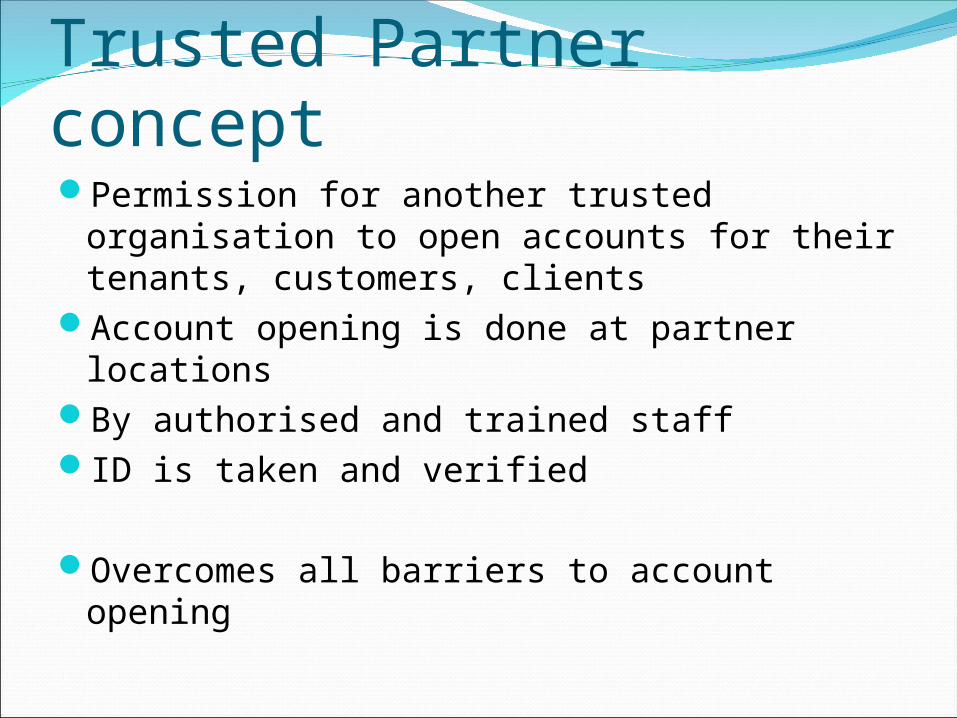

Trusted Partner conceptPermission for another trusted organisation

to open accounts for their tenants, customers, clients

Account opening is done at partner locationsBy authorised and trained staffID is taken and verified

Overcomes all barriers to account opening

Trusted Partner ProcessInitial agreement is made Due diligence Management sign offTrusted Partner Agreement is entered into Implementation plan is set Trusted partner app is downloaded onto TP

systemTraining of front line staff – AML and Data

Protection

AccessibleDuring any relevant meeting, banking checklist is

used & if alternative is required, the account is opened – total time 2 minutes

Account appears on our system within 15 minutesA call is made from service centre within 24 hours Explain our service and credit union, Confirm T&C’sSet up payments in and out if requiredSet up savings planOrder cardSend welcome packDiary for next contact

Products and services4 transactional accounts planned from AprilSavings Manager with savings plan and debit

cardRent Direct / Power Direct – single payee,

savings plan and cardBudget Account – household bills, savings

plan & cardDebt Management plan – household bills,

debt payment plan, savings plan and cardAll have sort code and account number Regular payments and direct debit capability

Low cost, high impactAccess points at partners through Kiosks

high visibilitymultiple useeasy to use

Members assistance plan – debt, legal and medical emergency advice

Proactive callsRelationship managed by service team Email statements Secure on line areaMobile appMonthly text balances

A real alternative to banking – yesA solution to use of high cost lending....Range of affordable loans

Balanced and segmented loan booksClear credit risk strategiesRelationship lending - Instant decisions,

smaller loans, and revolving facilities

Credit unions promote thrift and financial well being

Responsible lending is based upon affordability

Some solutions – insulate from financial shocks in householdSimple savings plans for all – lets remove the

societal need to have to borrow every time you have a minor emergency. Savings plans from payroll should be a right.

Refer to advice and support agencies where more appropriate

Solutions from partnering: Social landlords to provide indemnified loans

for tenants – small revolving loans where rent is being collected

Work with CDFI’sInsulate household from other financial

risks....

Brian Hall