february 2017 company presentation - think up lks · 2 disclaimer • this document has been...

TRANSCRIPT

1

February 2017 Company Presentation

2

D ISCLAIMER

• This document has been prepared by CIE Automotive, S.A. ("CIE Automotive"), and is for information purposes only. No reliance may or should be placed for any purposes whatsoever on the information contained in this document or on its completeness, accuracy or fairness. This document and the information contained herein are strictly confidential and are being shown to you solely for your information. The information may not be copied, distributed, reproduced or passed on, directly or indirectly, in whole or in part, or disclosed by any recipient, to any other person (whether within or outside such person's organisation or firm) or published in whole or in part, for any purpose or under any circumstances.

• This document is an advertisement and not a prospectus for the purposes of applicable measures implementing EU Directive 2003/71/EC (such Directive, together with any applicable implementing measures in the relevant home Member State under such Directive, the "Prospectus Directive") and as such does not constitute or form part of any offer to sell or issue or invitation to purchase or subscribe for, or any solicitation of any offer to purchase or subscribe for, any securities of CIE Automotive or any of its affiliates or subsidiaries, nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied on in connection with, any contract or investment decision. Investors should not subscribe for or purchase any securities referred to in this advertisement except on the basis of the information contained in any prospectus eventually published in accordance with the Prospectus Directive. The information and opinions contained in this document are provided as at the date of the document and are subject to change.

• This document is not an offer of securities for sale in the United States, Australia, Canada or Japan. The information contained herein does not constitute an offer of securities for sale in the United States, Australia, Canada or Japan. Securities may not be offered or sold in the United States unless they are registered or are exempt from registration. No money, securities or other consideration is being solicited and, if sent in response to the information contained herein, will not be accepted. Copies of this document are not being, and should not be, distributed or sent into the United States. This document does not constitute an offer of securities to the public in the United Kingdom or in any other jurisdiction. The distribution of this document in other jurisdictions may also be restricted by law and persons into whose possession this document comes should inform themselves about and observe any such restrictions.

• Certain financial and statistical information contained in this document is subject to rounding adjustments. Accordingly, any discrepancies between the totals and the sums of the amounts listed are due to rounding. Certain management financial measures included in this document have not been subject to a financial audit.

• The information and opinions contained in this document are provided as at the date of the document and are subject to verification, completion and change without notice. Neither CIE Automotive nor any of its parent or subsidiary undertakings, or the subsidiary undertakings of any such parent undertakings, or any of such person's respective directors, officers, employees, agents, affiliates or advisers, undertakes any obligation to amend, correct or update this document or to provide the recipient with access to any additional information that may arise in connection with it.

3

TABLE OF CONTENTS

1. What is CIE Automotive? 2. Automotive Project

3. Smart Innovation Project

7. CIE in Stock Exchange 6. Strategic Commitment: What is next?

4. Corporate Social Responsibility 5. Update on Results 30th Sept. 2016

4

1.0 What is CIE Automotive?

5

DEVELOPING TWO PROJECTS

UNIQUE business model developed SUCCESFULLY since 1996, with a solid TRACK RECORD and an IRR over 20%

Facing DIGITALIZATION in

productive activities, by applying knowledge and innovation to

achieve EFFICIENCY

Automotive components

Smart Innovation

6

WHAT IS C IE AUTOMOTIVE?

Integration, sum and management of processes in a sustainable, profitable and efficient way:

Automotive project carried forward in the context of the necessary consolidation of the TIER2 atomized sector.

Dominion project developed to challenge the status quo by applying Smart Innovation.

Succesful M&A track record: almost 70 M&A transactions since 1996, with 20.000 people integrated in Europe, Nafta, South America and Asia.

Strict acquisition discipline, requiring minimum ROI.

Mkt Cap: > 2,300M€

Employees ≈ 25,000

Sales 2015: 2,632 M€

EBITDA (*) 2015:

366 M€

(*) EBITDA: Net Operating Income + Depreciation.

7

CIE CULTURE: W H A T M A K E S T H E S E P R O J E C T S U N I Q U E ?

Commercial diversification as a defense tool

Diversity, a flexibility instrument

Investment discipline and return exigence

Decentralized management, for value generation

Our Business Model:

Multilocation, our own answer

8

AN INTEGRATION AND SUM STORY. . .

9

WEST EUROPE

AFRICA

USA • Plastic • Dominion MEXICO R&D • Aluminum • Forging • Stamping & Tube Forming • Machining • Plastic • Roof Systems • Dominion

NAFTA

. . .WITH GLOBAL FOOTPRINT…

SPAIN Headquarters R&D • Aluminum • Forging • Stamping & Tube Forming • Machining • Plastic • Roof Systems • Bionor • Dominion

ITALY • Machining • Dominion PORTUGAL R&D • Plastic • Dominion UK • Forging • Dominion

FRANCE R&D • Machining • Roof Systems • Dominion GERMANY R&D • Forging • Dominion DENMARK •Dominion

CZECH REP. • Stamping & Tube Forming • Machining • Plastic • Cold Forming LITHUANIA • Forging

RUSSIA • Aluminum & Machining

ROMANIA • Aluminum • Roof Systems SLOVAKIA • Machining • Dominion POLAND • Dominion

CENTRAL & EAST EUROPE

BRAZIL R&D • Forging • Stamping & Tube Forming • Machining • Aluminium • Plastic • Casting • Dominion

SOUTH AMERICA

PERU • Dominion

ARGENTINA • Dominion

CHILE • Dominion

COLOMBIA •Dominion

HONDURAS •Dominion ECUADOR •Dominion

GUATEMALA •Bionor

MOROCCO • Plastic PANAMA

• Dominion SOUTH AFRICA • Dominion

ASIA & OCEANIA

CHINA • Forging • Stamping & Tube Forming • Machining • Plastic • Roof Systems INDIA R&D • Forging • Stamping • Machining • Casting • Composites • Dominion

AUSTRALIA • Dominion

BAHRAIN • Dominion

INDONESIA • Dominion

PHILIPPINES • Dominion

OMAN • Dominion

QATAR • Dominion

SAUDI ARABIA • Dominion

UNITED ARAB EMIRATES • Dominion

VIETNAM • Dominion

10

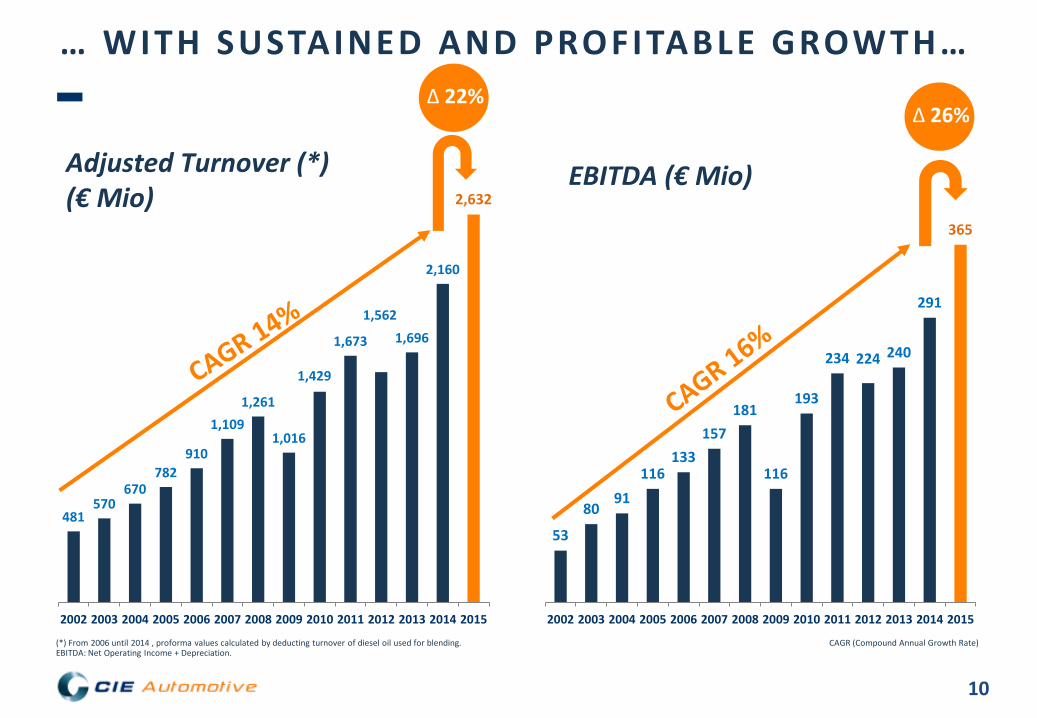

53

80 91

116 133

157 181

116

193

234 224 240

291

365

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

481 570

670 782

910

1,109 1,261

1,016

1,429

1,673

1,562 1,696

2,160

2,632

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

(*) From 2006 until 2014 , proforma values calculated by deducting turnover of diesel oil used for blending. CAGR (Compound Annual Growth Rate) EBITDA: Net Operating Income + Depreciation.

… WITH SUSTAINED AND PROFITABLE GROWTH…

Adjusted Turnover (*) (€ Mio)

EBITDA (€ Mio)

∆ 22% ∆ 26%

11

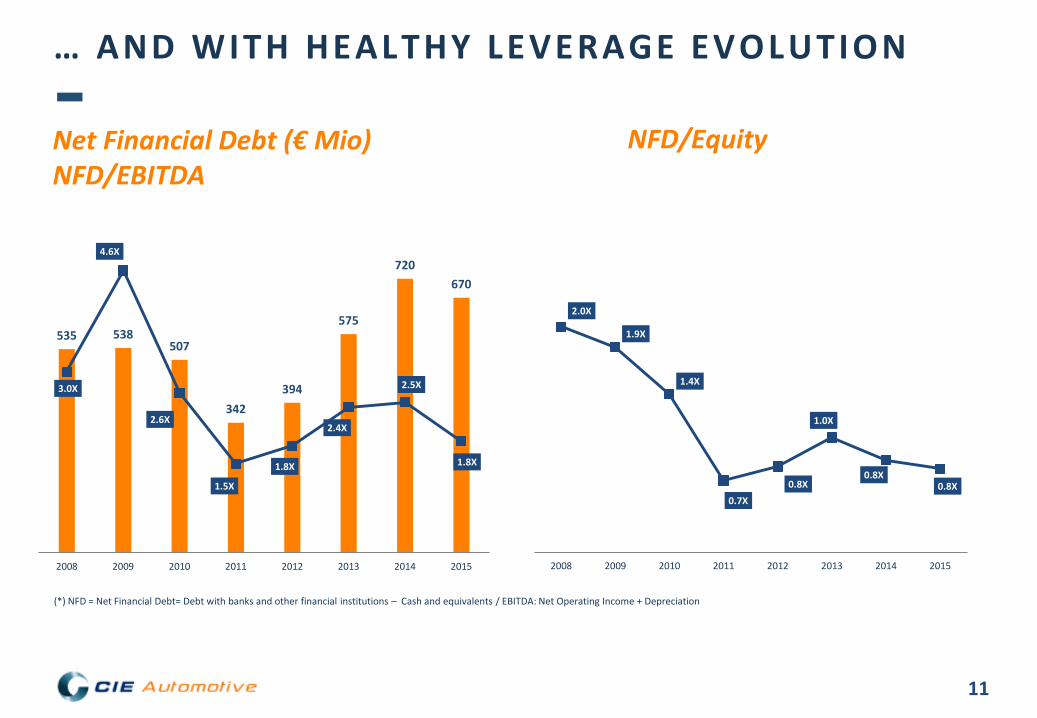

… AND WITH HEALTHY LEVERAGE EVOLUTION

(*) NFD = Net Financial Debt= Debt with banks and other financial institutions – Cash and equivalents / EBITDA: Net Operating Income + Depreciation

Net Financial Debt (€ Mio) NFD/EBITDA

NFD/Equity

535 538 507

342 394

575

720 670

3.0X

4.6X

2.6X

1.5X

1.8X

2.4X

2.5X

1.8X

2008 2009 2010 2011 2012 2013 2014 2015

2.0X

1.9X

1.4X

0.7X 0.8X

1.0X

0.8X 0.8X

2008 2009 2010 2011 2012 2013 2014 2015

12

Automotive Project 2.

0

CIE Culture

Multilocation

Multi-technological Portfolio

Investment Discipline and Return Exigence

Commercial Diversification

Decentralized Management

13

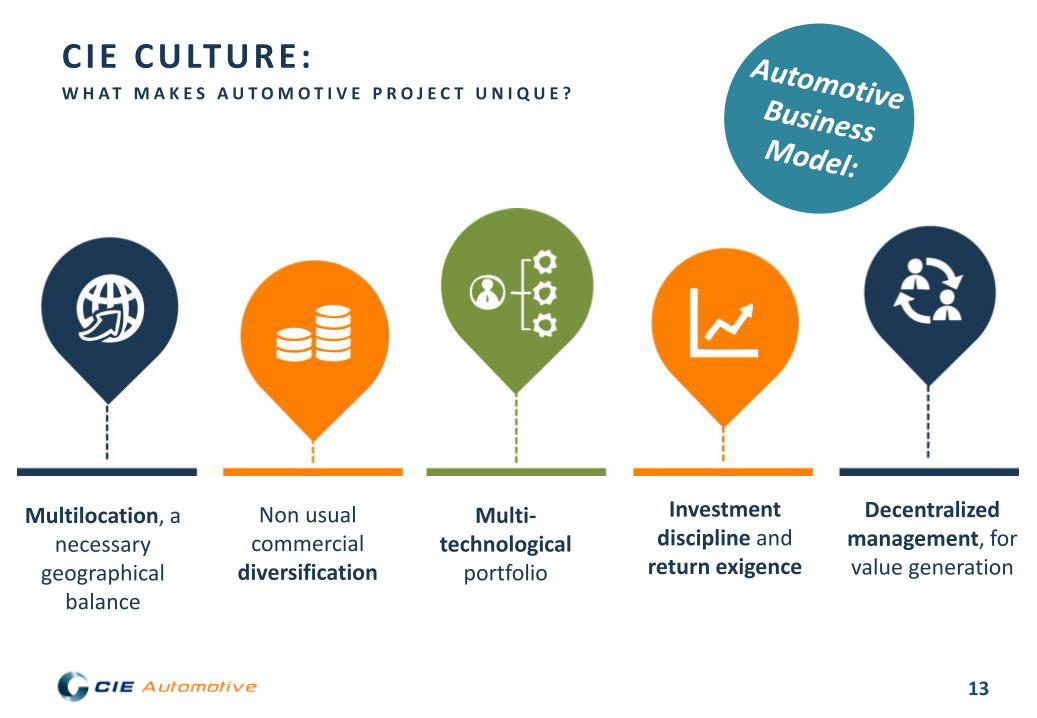

CIE CULTURE: W H A T M A K E S A U T O M O T I V E P R O J E C T U N I Q U E ?

Multilocation, a necessary

geographical balance

Non usual commercial

diversification

Multi-technological

portfolio

Decentralized management, for value generation

Investment discipline and

return exigence

14

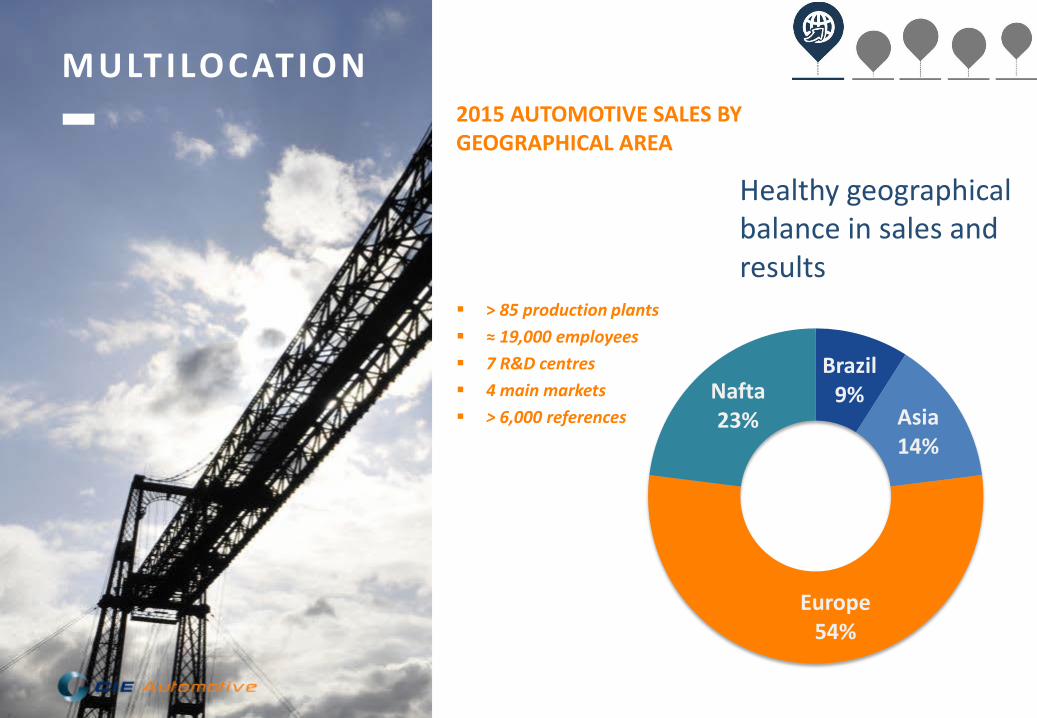

Healthy geographical balance in sales and results

2015 AUTOMOTIVE SALES BY GEOGRAPHICAL AREA

> 85 production plants ≈ 19,000 employees 7 R&D centres 4 main markets > 6,000 references

MULTILOCATION

Brazil 9%

Asia 14%

Europe 54%

Nafta 23%

15

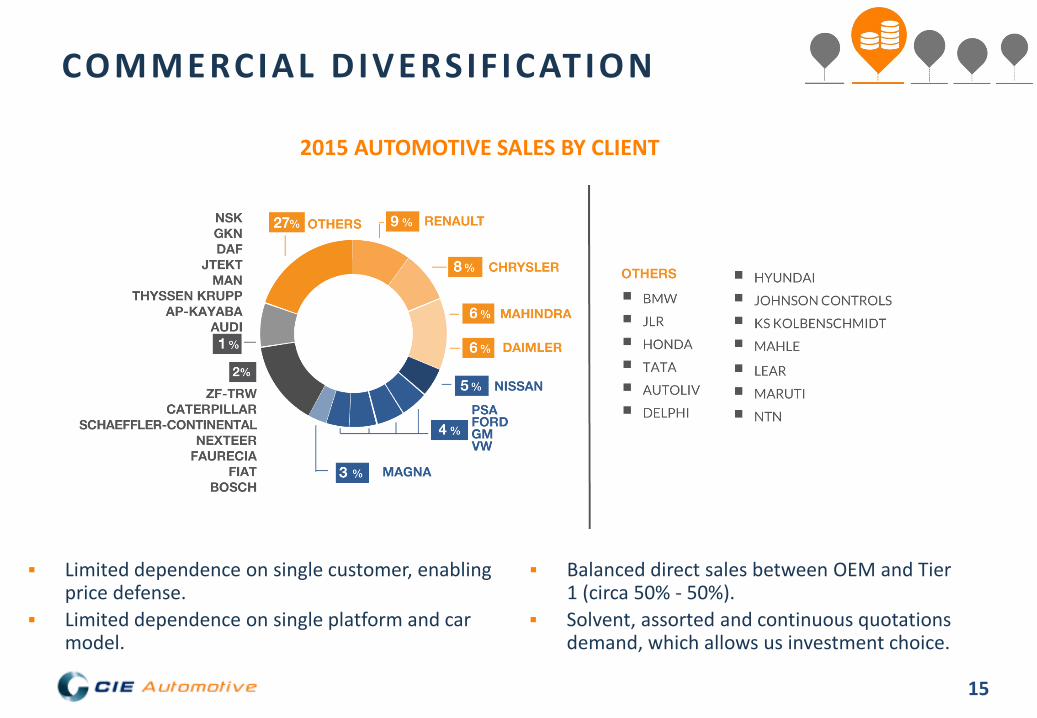

Limited dependence on single customer, enabling price defense.

Limited dependence on single platform and car model.

Balanced direct sales between OEM and Tier 1 (circa 50% - 50%).

Solvent, assorted and continuous quotations demand, which allows us investment choice.

COMMERCIAL DIVERSIF ICATION

2015 AUTOMOTIVE SALES BY CLIENT

16

Offering the integration of a whole range of different technologies in main Automotive geographical markets…

…Enabling the selection of the technology that fulfills better customers needs.

…Allowing CIE to focus investments on winning technology anytime.

…And at the same time projecting CIE as a Powertrain products worldwide leader.

MULTI-TECHNOLOGICAL PORTFOLIO

Process EU NAFTA Brazil India China

Forgings

Aluminum

Castings

Machining

Stampings

Plastics

Roof Systems

AUTOMOTIVE SALES BY TECHNOLOGY

TECHNOLOGY BY GEOGRAPHICAL AREA

Aluminium

HPDC 10%

Forging 26%

Stamping & Tube Forming

24%

Machining 16%

Plastic 15%

Iron Casting 4%

Roof Systems 5%

17

Strategic products with higher than market average growth and profitability, in which CIE is focusing

MULTI-TECHNOLOGICAL PORTFOLIO

FORGING PRODUCTS

Crankshaft CV- Joints Axle Shaft Axle Beam

ALUMINUM PRODUCTS

Gearbox Housing Clutch Housing Steering Housings Camshaft Cover

Brake Drum

CASTING PRODUCTS

Turbo Housing

Crankshaft Differential Housing

EPS component Flange

MACHINING PRODUCTS

Hubs, Outer Rings Differential Case

Ladder Frame

18

ROOF SYSTEM PRODUCTS

Glazing

Opening Roof Shading

MULTI- TECHNOLOGY PRODUCTS Oil Pan

Metal Forming, Aluminum, Plastic

Diesel & Gasoline Injection Rails Forging and Machining & Tube Forming

Strategic products with higher than market average growth and profitability, in which CIE is focusing

STAMPING & TUBE FORMING PRODUCTS

Body in White Brake Booster Seat Structure

PLASTIC PRODUCTS

Emblems Ashtray Arm Rest Trim Parts

MULTI -TECHNOLOGICAL PORTFOLIO

Steering Columns

19

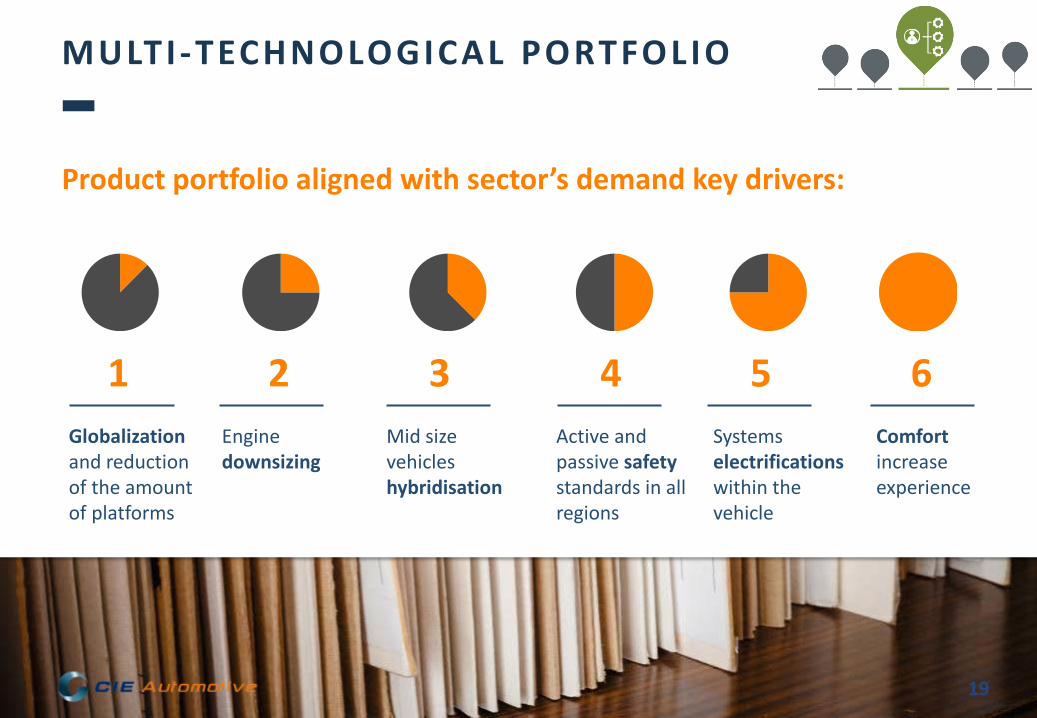

Product portfolio aligned with sector’s demand key drivers:

1 2 Globalization and reduction of the amount of platforms

Engine downsizing

3 Mid size vehicles hybridisation

4 Active and passive safety standards in all regions

5 Systems electrifications within the vehicle

6 Comfort increase experience

MULTI-TECHNOLOGICAL PORTFOLIO

20

STANDARD FLEXIBLE

MACHINERY

Valid to produce for different customers and platforms, allowing HIGH SATURATION of productive capacity. ≈4% recurrent investment level that allows maintenance and 2-3% organic growth.

STRICT INVESTMENT

DISCIPLINE

Investment analysis discipline, always requiring high returns. Capex ≥ 20% ROI. Operating Working Capital ≈0. M&A: EV/EBITDA ≤3 in 3 years.

EBITDA CONVERSION

INTO CASH

Optimization of productive capacity and investment control enables a higher than market average conversion of the EBITDA into Cash. ≈50% conversion level target.

INVESTMENT DISCIPL INE AND RETURN EXIGENCE

21

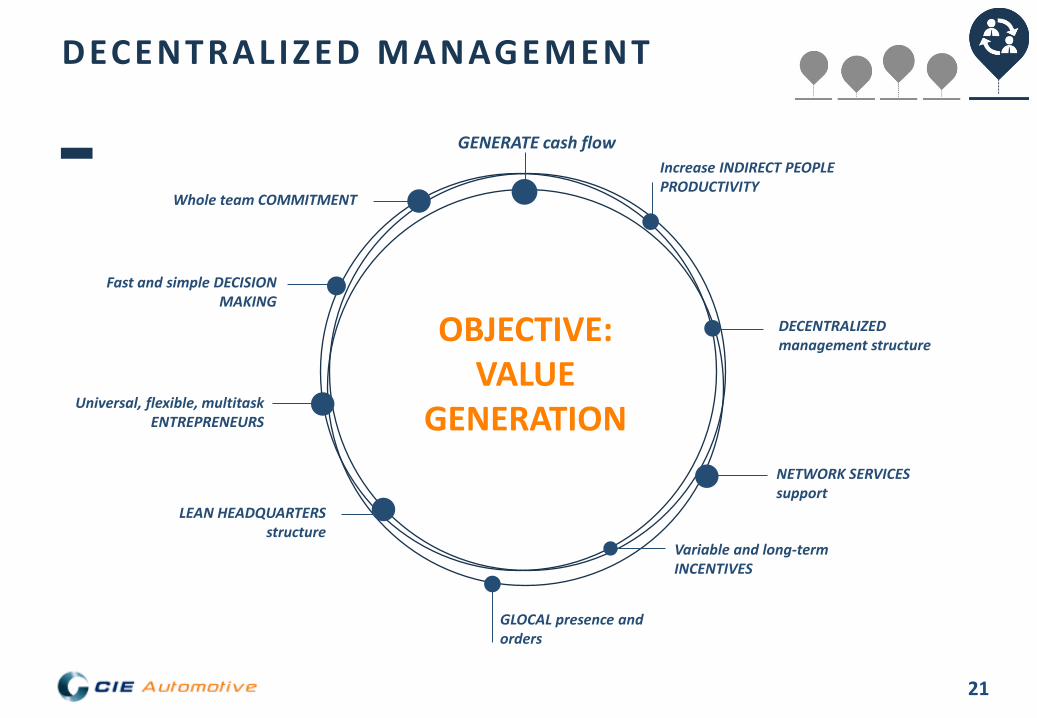

OBJECTIVE: VALUE

GENERATION

GENERATE cash flow Increase INDIRECT PEOPLE

PRODUCTIVITY

DECENTRALIZED management structure

NETWORK SERVICES support

Variable and long-term INCENTIVES

GLOCAL presence and orders

LEAN HEADQUARTERS structure

Universal, flexible, multitask ENTREPRENEURS

Fast and simple DECISION MAKING

Whole team COMMITMENT

DECENTRALIZED MANAGEMENT

22

Smart Innovation Project 3.

0

23

Workforce: ~25.000

Experts in process management

Facing DIGITALIZATION in productive activities by applying technology, knowledge and innovation to achieve EFFICIENCY in our clients´ processes

+

>50% Dominion Capital

Revenues(2): 2.632 M€

Ebitda(2): 366 M€

Workforce ~5,500

Revenues (1) >600 m€

Ebitda (1) >45 m€

Global >30 countries

Shared culture

Growth plan

Cash Flow Convers. >100% & above peers

(1) 2016E estimated data (2) 2015 data

24

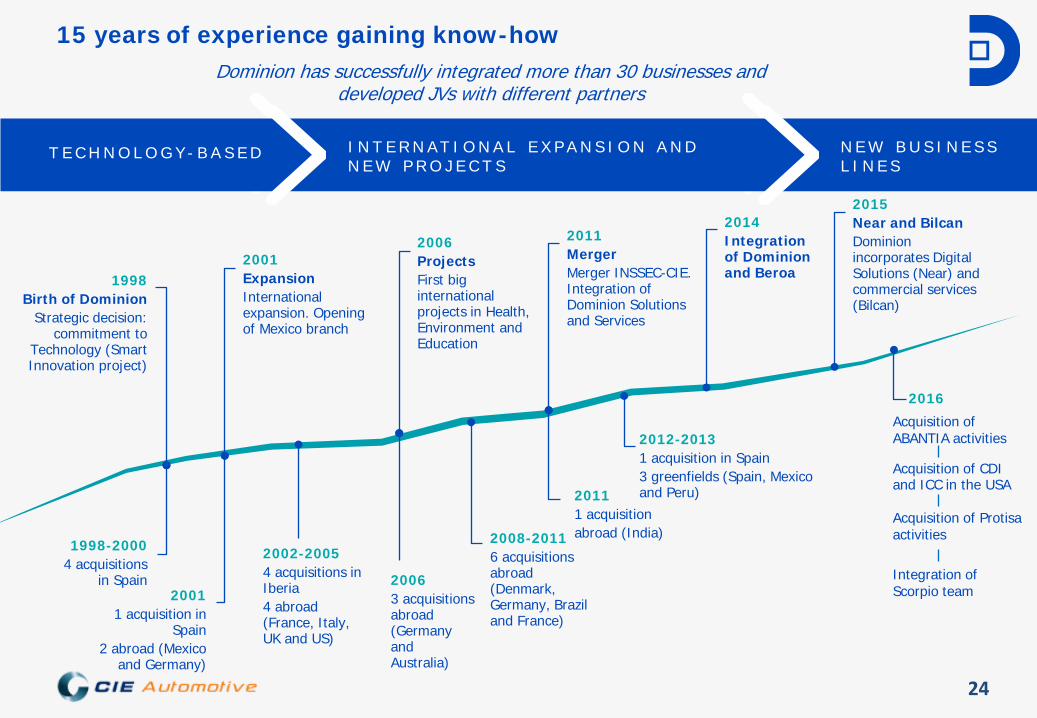

15 years of experience gaining know-how

1998 Birth of Dominion

Strategic decision: commitment to

Technology (Smart Innovation project)

2001 Expansion International expansion. Opening of Mexico branch

2006 Projects First big international projects in Health, Environment and Education

2011 Merger Merger INSSEC-CIE. Integration of Dominion Solutions and Services

2014 Integration of Dominion and Beroa

2015 Near and Bilcan Dominion incorporates Digital Solutions (Near) and commercial services (Bilcan)

1998-2000 4 acquisitions

in Spain 2001

1 acquisition in Spain

2 abroad (Mexico and Germany)

2002-2005 4 acquisitions in Iberia 4 abroad (France, Italy, UK and US)

2006 3 acquisitions abroad (Germany and Australia)

2008-2011 6 acquisitions abroad (Denmark, Germany, Brazil and France)

2011 1 acquisition abroad (India)

2012-2013 1 acquisition in Spain 3 greenfields (Spain, Mexico and Peru)

2016

Acquisition of ABANTIA activities Acquisition of CDI and ICC in the USA

Acquisition of Protisa activities

Integration of Scorpio team

T E C H N O L O G Y - B A S E D

I N T E R N A T I O N A L E X P A N S I O N A N D N E W P R O J E C T S

N E W B U S I N E S S L I N E S

Dominion has successfully integrated more than 30 businesses and developed JVs with different partners

25

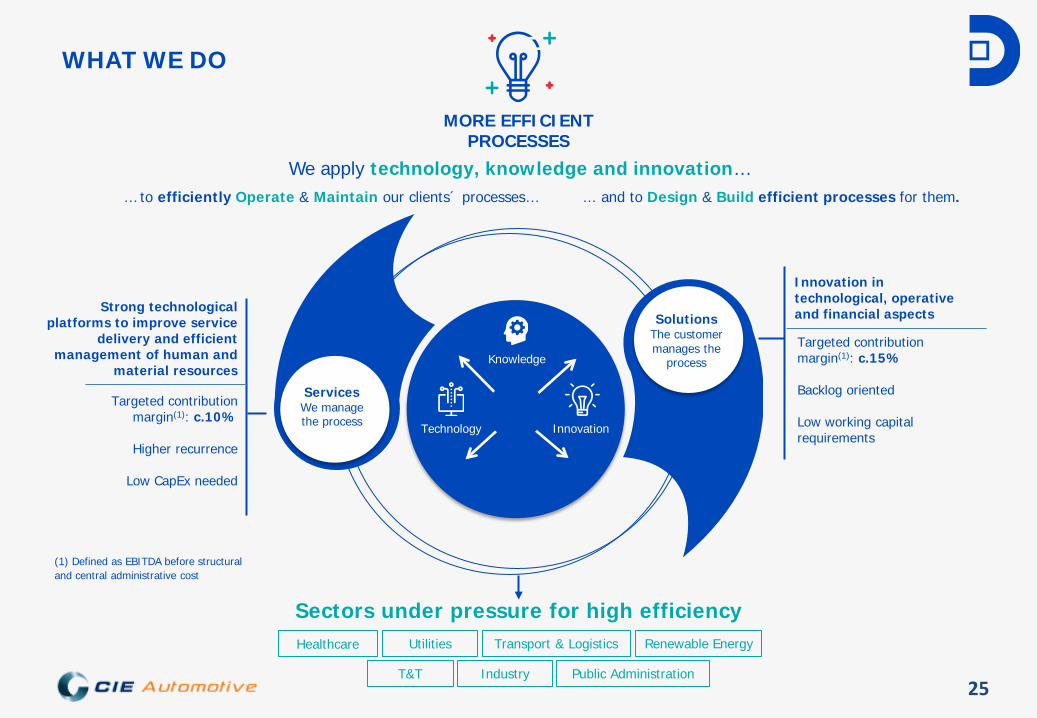

Knowledge

Technology Innovation

Services We manage the process

WHAT WE DO

MORE EFFICIENT PROCESSES

We apply technology, knowledge and innovation…

Strong technological platforms to improve service

delivery and efficient management of human and

material resources

Sectors under pressure for high efficiency

... and to Design & Build efficient processes for them.

Targeted contribution margin(1): c.10%

Higher recurrence

Low CapEx needed

T&T Industry

Healthcare Renewable Energy Transport & Logistics

Public Administration

Utilities

Solutions The customer manages the

process

Innovation in technological, operative and financial aspects

Targeted contribution margin(1): c.15%

Backlog oriented

Low working capital requirements

… to efficiently Operate & Maintain our clients´ processes…

(1) Defined as EBITDA before structural and central administrative cost

26

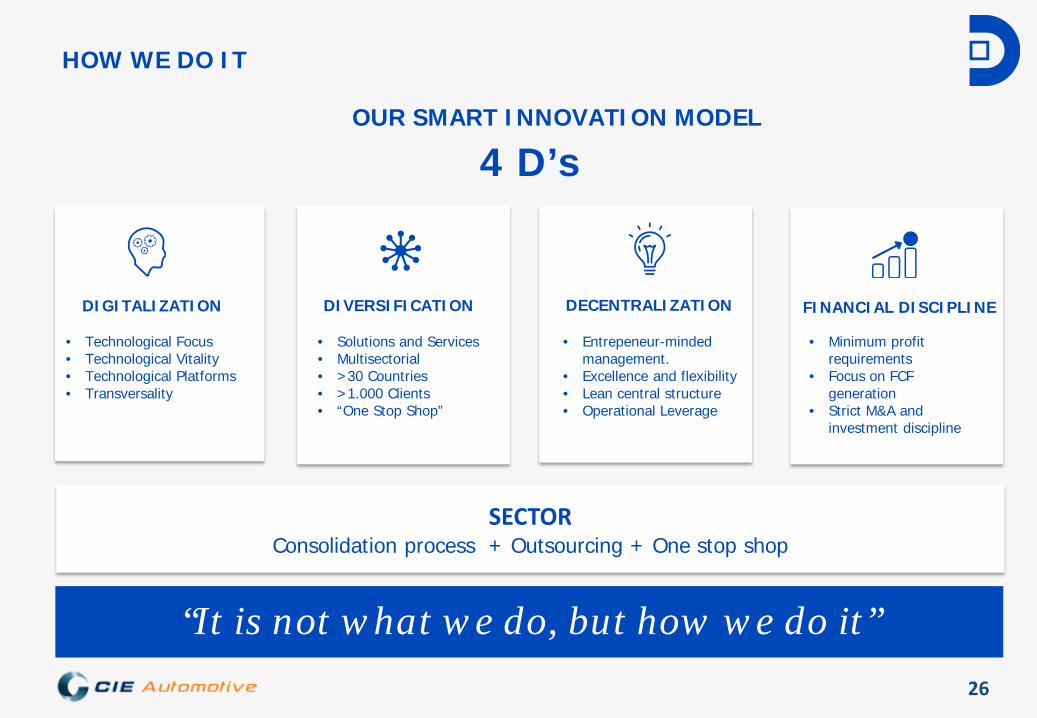

SECTOR Consolidation process + Outsourcing + One stop shop

“It is not what we do, but how we do it”

4 D’s

DIGITALIZATION

• Technological Focus • Technological Vitality • Technological Platforms • Transversality

DIVERSIFICATION

• Solutions and Services • Multisectorial • >30 Countries • >1.000 Clients • “One Stop Shop”

DECENTRALIZATION

• Entrepeneur-minded management.

• Excellence and flexibility • Lean central structure • Operational Leverage

FINANCIAL DISCIPLINE

HOW WE DO IT

OUR SMART INNOVATION MODEL

• Minimum profit requirements

• Focus on FCF generation

• Strict M&A and investment discipline

27

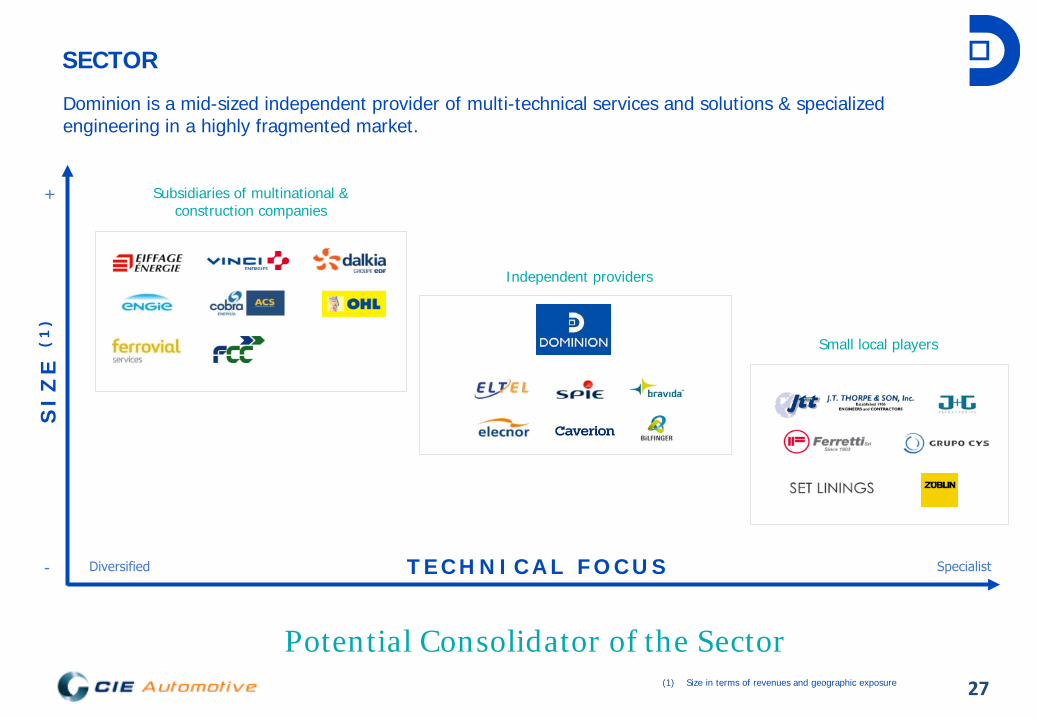

Dominion is a mid-sized independent provider of multi-technical services and solutions & specialized engineering in a highly fragmented market.

SECTOR

Subsidiaries of multinational & construction companies

Independent providers

Small local players

Potential Consolidator of the Sector

SI

ZE

T E C H N I C A L F O C U S

+

-

Small local players

SI

ZE

(1

)

(1) Size in terms of revenues and geographic exposure

28

DIGITALIZATION

Multi-source Data

Example of technology application in a Multi-Technical Service: ADSL REPAIR

Dominion´s mgmt platforms

CCC

Resources

Sensoring • Monitoring and

Digitalization • Intelligence thanks to

highly qualified technical team

Tickers / Resources allocation • Workforce (installers,

salesmen, etc.) • Tools, vehicles

• Big Data ADSL REPAIR

ORDER

TICKER

• TECHNICAL CHARACTERISTICS

• NETWORK CLIENT • END USER DETAILS • PRIORITY • NEXT ORDER

ORDER DATA

• WORKFORCE • FLEET DATA • INVENTORIES &

TOOLS

OWN RESOURCES

MULTIPURPOSE WORKFORCE SUBCONTRACTING

• TRAFFIC • WEATHER

ENVIRONMENT

CCC

Quality excellence and workplace safety

Worldwide presence

Flexibility (identical requirements applied to subcontractors)

Multifunctional teams

A trustworthy partner for its customers

Strong technological platforms to improve service delivery and efficient management of human and material resources.

29

DIVERSIFICATION

A strong portfolio diversification(1)… … in several activity fields…(1)

…with a global footprint in more than 30 countries (1)… …and a wide client base…

Multi-Technical Services 57%

Solutions & Spec.

Engineering 43%

T&T 49% Industry

45%

Renewable Energy

6% T&T (49% REVENUES 15A)

INDUSTRY (45% revenues 15A)

RENEWABLE ENERGY (6% revenues 15A)

+1,000 clients

Asia & Oceanía: 12% Europa & Africa: 61% America: 27%

(1) 2016E estimated data. Revenue split

30

FINANCIAL DISCIPLINE

Focus on FCF generation

EBITDA Conversion into Cash R&D Investment Discipline Strict M&A Discipline

Target >60% EBITDA Maintain current RONA levels M&A: Target 3y-forward looking (including synergies) EV/EBITDA <=3x

• Limited CapEx requirements and WIP strict control

• Neutral WC model

• Strict R&D analysis and return exigency

• R&D projects developed under efficiency schemes

• Cash generation as the relevant valuation criteria

• Recurrent and thorough analysis of opportunities

• Strict screening and control on the integration of knowledge and companies to our “strategic carrier model”

• Post-acquisition strategy: digitalization/restructuring/internationalization

Value creation for shareholders

31

DECENTRALIZED MANAGEMENT

+

Experienced Multidisciplinary management and more than 5,500 employees with a common efficiency culture

DIRECTORS BY BUSINESS LINES AND COUNTRIES

Entrepreneurs with global responsibility up to the contribution margin

LEAN CORPORATE SERVICES

Capacity to integrate new contribution margins with current structure

32

Corporate Social

Responsibility

4.0

33

4.1 ENVIROMENTAL AND SOCIAL GOVERNANCE

• Adherence to the United Nations Global Compact and implementation of the 10 universally

accepted principles to encourage business social responsibility in the areas of human rights, labour regulations, the environment and the struggle against corruption.

• Reasserting our commitment to provide employees a safe and healthy working environment by adopting necessary measures to prevent accidents and health hazards.

• Corporate governance driven by principles of ethics and transparency.

• In collaboration with Deloitte, developing a multi-year CSR Strategic Plan that will support our 2016-2020 Business Strategic Plan, and that will allow us to improve our Risk Management Model.

• Focusing firmly on the future and on sustainable development by integrating commitment to environmental preservation in our management model through ambitious certification standards.

34

4.2 ENVIROMENTAL AND SOCIAL GOVERNANCE A u t o m o t i v e

• Balancing industrial activity with minimum environment impact: skilled knowledge on production processes enables us consumption optimization and materials reuse.

• Our recycling activity:

Used oils collection and production of biofuel from them. Recycling processes that allow to turn shavings produced in the machining

process into new parts or scrap for re-use. The aluminium division recycled 48,089 tonnes

• The main R&D initiatives focused on projects and technologies for reducing vehicle

weight, efficient powertrains, new forms of propulsion, new manufacturing technology and industry 4.0.

• Programme – AVANZA, pursues the defined triple zero target of ‘zero defects, zero

accidents and zero contamination’ via four lines of initiative: safety, training, systematic reviews and ongoing learning.

35

Dominion’s activities are intrinsically related to environmental protection and relationship with the community through the projects it carries out for its customers:

• Deployment of meteorological networks and development of platforms aimed at

measuring weather and water/air data and coordinating civil protection efforts, particularly in developing regions frequently devastated by natural disasters (Honduras and Venezuela).

• Energy-efficiency solutions for application in its customers’ productive processes with the

aim of delivering energy savings by both reducing consumption and recovering residual heat. (Several industrial clients).

• Anti-tsunami alert systems. Arica (Chile). • Accident prevention at rail crossings and early fire detection at industrial plants based on

video content management (VCM) . • Hospital equipment projects. (Chile, Argentina and Honduras). • Radio communication system for railways. (Rancagua-Chile).

4.3 ENVIROMENTAL AND SOCIAL GOVERNANCE D o m i n i o n

36

Update on results: 30th September 2016

5.0

Group Results September 2016

Balance Sheet

37

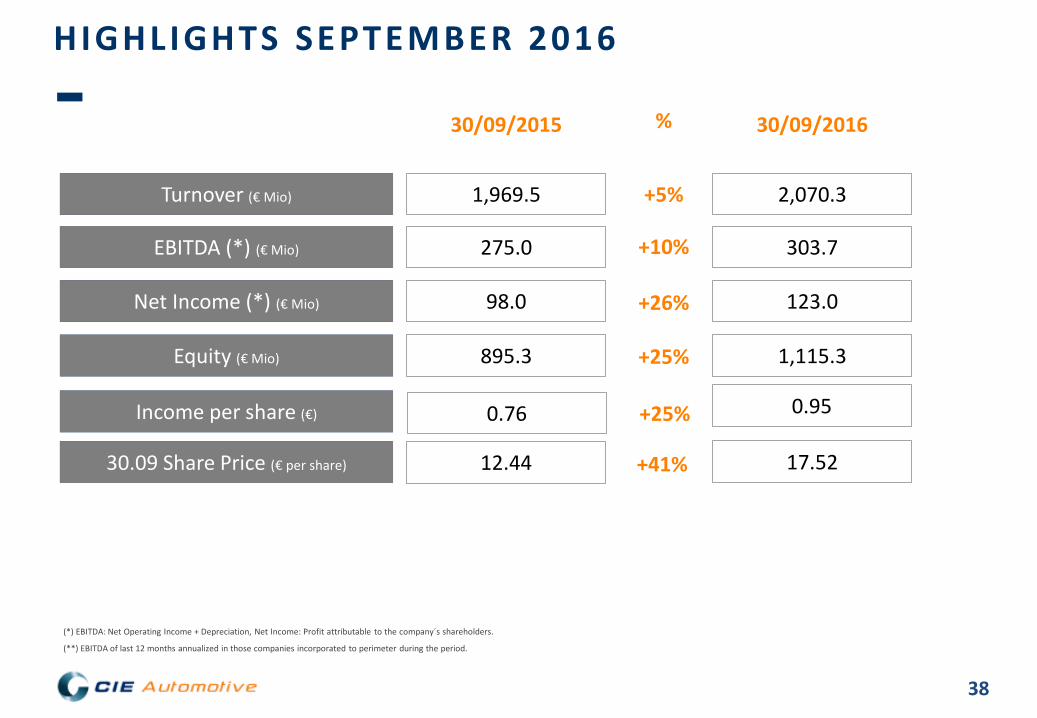

5.1 Group Results September 2016

38

Cifra de negocio (MM€)

EBITDA (*) (MM€)

30/09/2015

30/09/2016

Patrimonio Neto (MM€)

1,969.5

275.0

895.3

2,070.3

303.7

1,115.3

+5%

+10%

+26%

%

+25%

Resultado Neto (*) (MM€) 98.0 123.0

12.44

0.76 Beneficio por acción (€)

Cotización 30.06 (€/acción)

(*) EBITDA: Net Operating Income + Depreciation, Net Income: Profit attributable to the company´s shareholders.

(**) EBITDA of last 12 months annualized in those companies incorporated to perimeter during the period.

0.95

17.52 +41%

+25%

H IGHLIGHTS SEPTEMBER 2016

NFD/EBITDA (**)

Turnover (€ Mio)

EBITDA (*) (€ Mio)

Equity (€ Mio)

Net Income (*) (€ Mio)

Income per share (€)

30.09 Share Price (€ per share)

39

(*) EBITDA: Net Operating Income + Depreciation, EBIT: Net Operating Income, Net Income: Profit attributable to the company´s shareholders

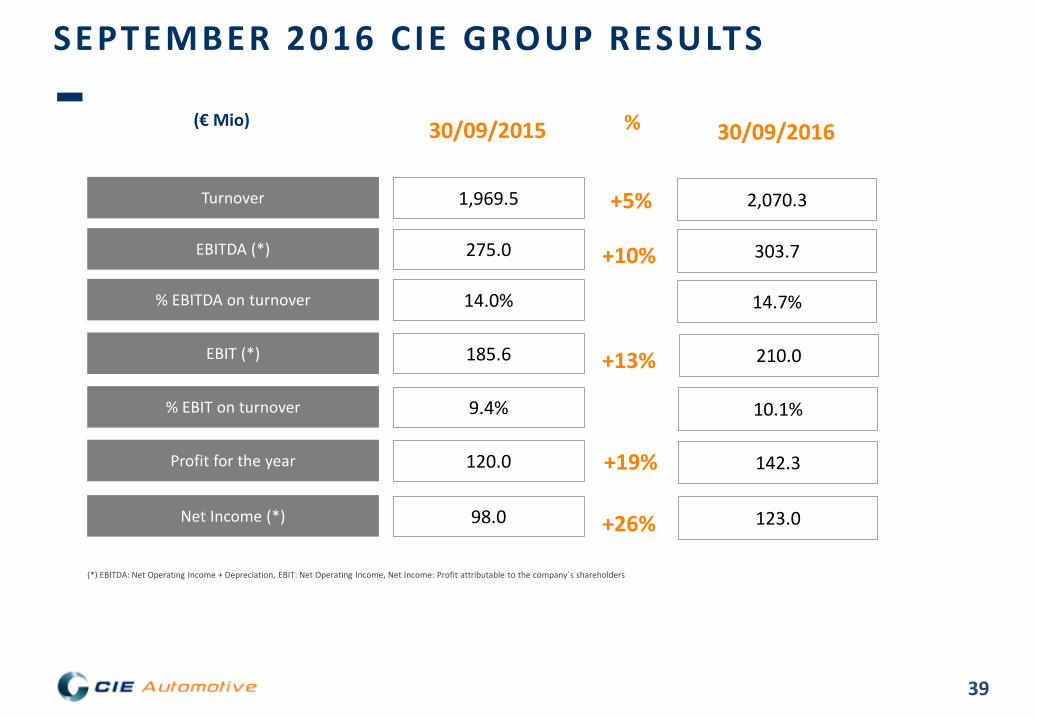

SEPTEMBER 2016 CIE GROUP RESULTS

Turnover

30/09/2015

30/09/2016

% EBITDA on turnover

EBIT (*)

Profit for the year

Net Income (*)

1,969.5

14.0%

185.6

120.0

98.0

2,070.3

14.7%

210.0

142.3

123.0

% EBIT on turnover 9.4% 10.1%

EBITDA (*) 275.0 303.7 +10%

+13%

+26%

+5%

% (€ Mio)

+19%

40

(*) EBITDA: Net Operating Income + Depreciation, EBIT: Net Operating Income, Net Income: Profit attributable to the company´s shareholders

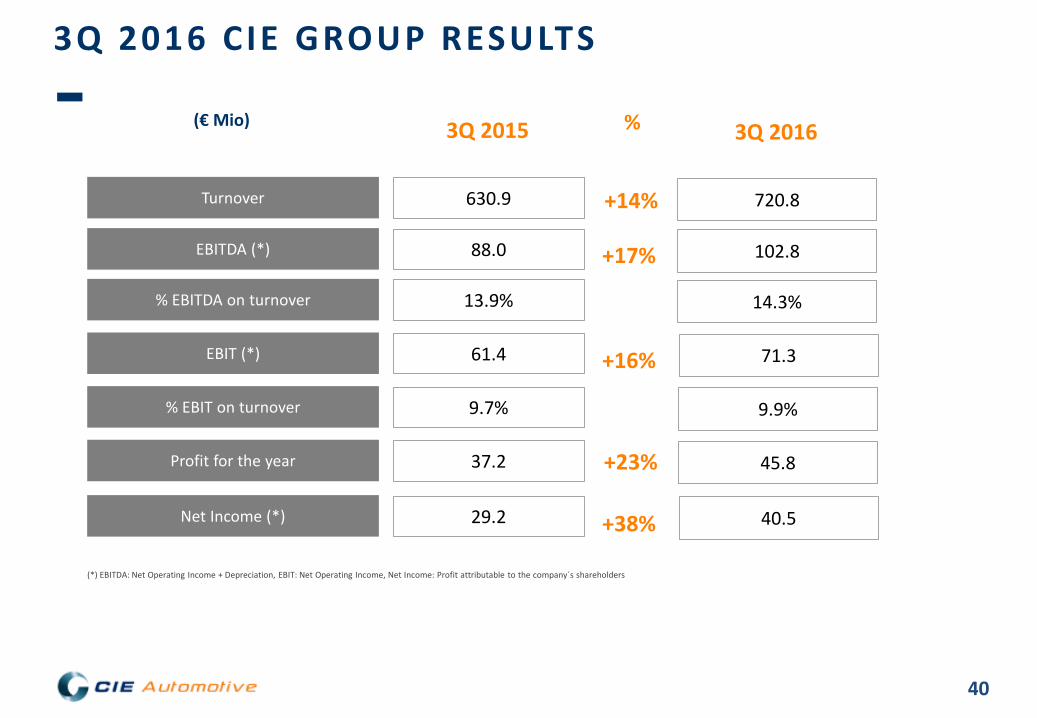

3Q 2016 CIE GROUP RESULTS

Turnover

3Q 2015

3Q 2016

% EBITDA on turnover

EBIT (*)

Profit for the year

Net Income (*)

630.9

13.9%

61.4

37.2

29.2

720.8

14.3%

71.3

45.8

40.5

% EBIT on turnover 9.7% 9.9%

EBITDA (*) 88.0 102.8 +17%

+16%

+38%

+14%

% (€ Mio)

+23%

41

QUARTERLY EVOLUTION 2013/2014/2015/2016

Net Income (€ Mio)

Growing profit quarter after quarter Very significant growth of Net Income +25% vs September 2015, as a result of continuous improvement in operations’

margins.

17 16 13 14

19 20 21 21

31

38

29 31

37

45

41

1Q 2Q 3Q 4Q

2013 2014 2015 2016

42

(*) EBITDA: Net Operating Income + Depreciation, EBIT: Net Operating Income.

SEPTEMBER 2016 AUTOMOTIVE RESULTS

Turnover

30/09/2015 30/09/2016

% EBITDA on turnover

EBIT (*)

1,595.9

167.2

1,661.8

187.6

% EBIT on turnover

EBITDA (*) 247.6 271.7 +10%

+12%

+4%

% (€ Mio)

15.5% 16.3%

10.5% 11.3%

Net growth in sales of 4% mitigated by the exchange rate effect, by the pass through of raw material prices’ -2% drop into our selling prices

Excellent performance of margins in all regions, having reached EBIT margin 11.3%

43

3Q 2016 AUTOMOTIVE RESULTS

Turnover 491.5

3Q 2015 3Q 2016 % (€ Mio)

567.2

63.0

91.2 +17%

+16%

+15%

78.0

% EBITDA on turnover

EBIT (*)

% EBIT on turnover

EBITDA (*)

54.1

(*) EBITDA: Net Operating Income + Depreciation, EBIT: Net Operating Income.

15.9% 16.1%

11.0% 11.1%

44

(*) EBITDA: Net Operating Income + Depreciation, EBIT: Net Operating Income.

SEPTEMBER 2016 DOMINION RESULTS

Turnover

30/09/2015 30/09/2016

% EBITDA on turnover

EBIT (*)

373.5

18.3

408.5

22.5

% EBIT on turnover

EBITDA (*) 27.4 32.0 +17%

+22%

+9%

% (€ Mio)

7.3% 7.8%

4.9% 5.5%

Close to double-digit organic growth affected by an effect of exchange rate of -4%. +17% and +22% increase in EBITDA and EBIT respectively, supported by operating leverage and by last integrations

'margins improvement, following Dominion´s Smart Innovation business model

45

3Q 2016 DOMINION RESULTS

Turnover 139.4

3Q 2015 3Q 2016 % (€ Mio)

153.6

8.3

11.6 +16%

+14%

+10%

10.0

% EBITDA on turnover

EBIT (*)

% EBIT on turnover

EBITDA (*)

7.3

(*) EBITDA: Net Operating Income + Depreciation, EBIT: Net Operating Income.

7.2% 7.6%

5.2% 5.4%

46

7%

18%

26% 17%

12%

20% BrazilNAFTAEuropeMahindra EuropeAsia (India/China)Dominion

Turnover

5%

30%

31%

14%

10%

10%

BrazilNAFTAEuropeMahindra EuropeAsia (India/China)Dominion

EBITDA

EBITDA: Net Operating Income + Depreciation.

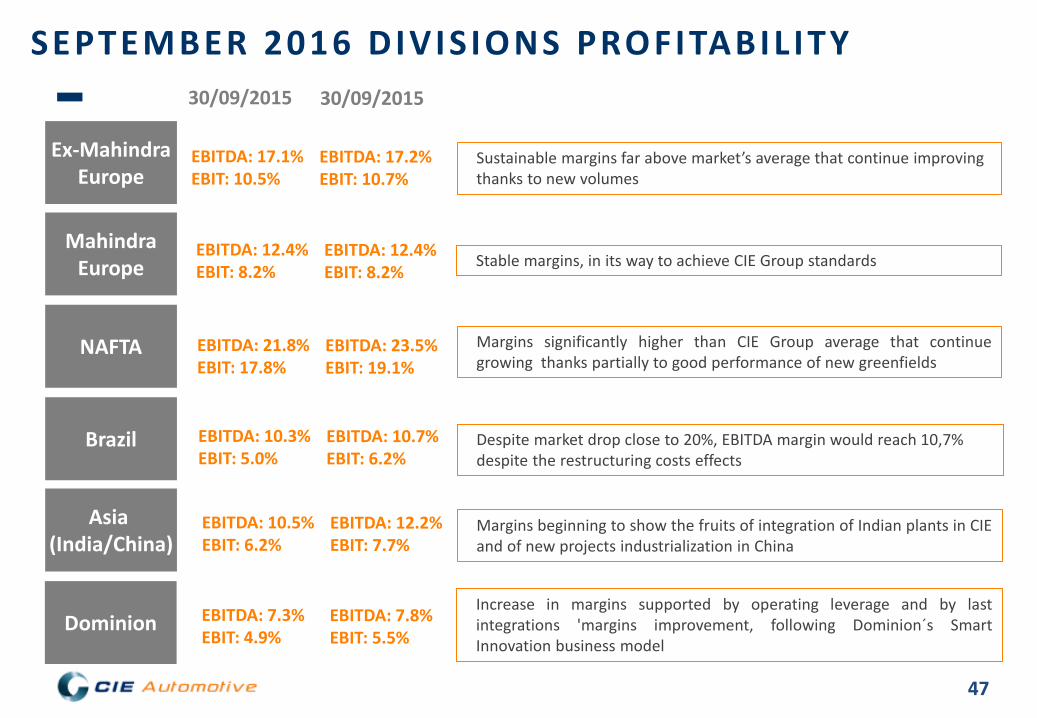

SEPTEMBER 2016 DIVIS IONS CONTRIBUTION

47

Sustainable margins far above market’s average that continue improving thanks to new volumes

EBITDA: 12.2% EBIT: 7.7%

EBITDA: 10.7% EBIT: 6.2%

EBITDA: 23.5% EBIT: 19.1%

EBITDA: 12.4% EBIT: 8.2%

EBITDA: 17.2% EBIT: 10.7%

Brazil

NAFTA

Ex-Mahindra Europe

Mahindra Europe

Asia (India/China)

Despite market drop close to 20%, EBITDA margin would reach 10,7% despite the restructuring costs effects

Margins significantly higher than CIE Group average that continue growing thanks partially to good performance of new greenfields

Stable margins, in its way to achieve CIE Group standards

Margins beginning to show the fruits of integration of Indian plants in CIE and of new projects industrialization in China

EBITDA: 17.1% EBIT: 10.5%

30/09/2015 30/09/2015

EBITDA: 12.4% EBIT: 8.2%

EBITDA: 21.8% EBIT: 17.8%

EBITDA: 10.3% EBIT: 5.0%

EBITDA: 10.5% EBIT: 6.2%

EBITDA: 7.8% EBIT: 5.5%

Dominion Increase in margins supported by operating leverage and by last integrations 'margins improvement, following Dominion´s Smart Innovation business model

EBITDA: 7.3% EBIT: 4.9%

SEPTEMBER 2016 DIVIS IONS PROFITABIL ITY

48

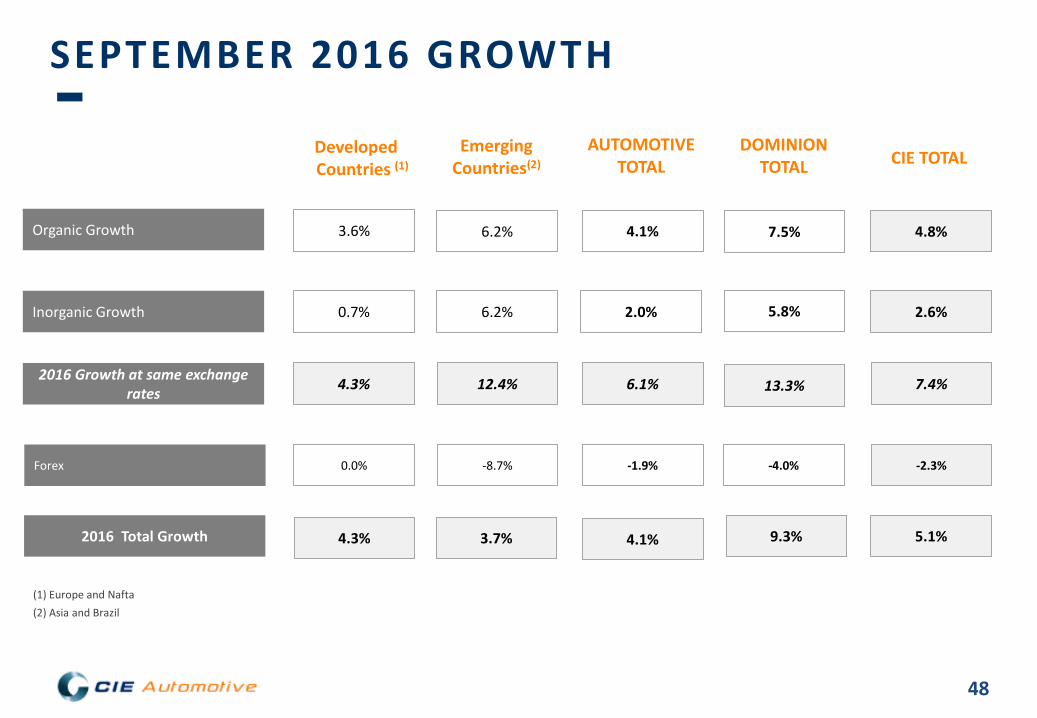

SEPTEMBER 2016 GROWTH

Inorganic Growth 0.7%

Organic Growth 3.6%

Forex 0.0%

Developed Countries (1)

6.2%

6.2%

-8.7%

Emerging Countries(2)

2.0%

4.1%

-1.9%

AUTOMOTIVE TOTAL

2016 Total Growth 4.3% 3.7% 4.1%

(1) Europe and Nafta (2) Asia and Brazil

5.8%

7.5%

-4.0%

DOMINION TOTAL

2.6%

4.8%

-2.3%

CIE TOTAL

9.3% 5.1%

2016 Growth at same exchange rates 4.3% 12.4% 6.1% 13.3% 7.4%

49

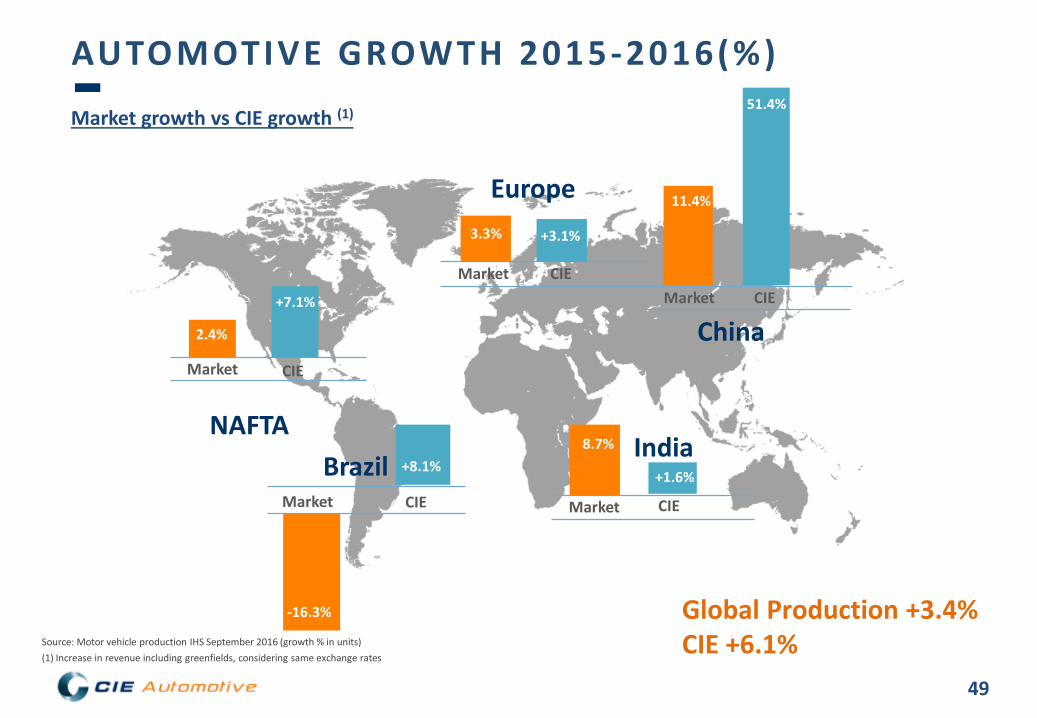

Market growth vs CIE growth (1)

NAFTA

2.4%

Market CIE

Brazil Market CIE

China Market CIE

Global Production +3.4% CIE +6.1%

-16.3%

Source: Motor vehicle production IHS September 2016 (growth % in units) (1) Increase in revenue including greenfields, considering same exchange rates

51.4%

AUTOMOTIVE GROWTH 2015-2016(%)

+7.1%

+8.1%

Europe 3.3%

Market CIE

+3.1%

India

Market CIE

+1.6%

8.7%

11.4%

50

51

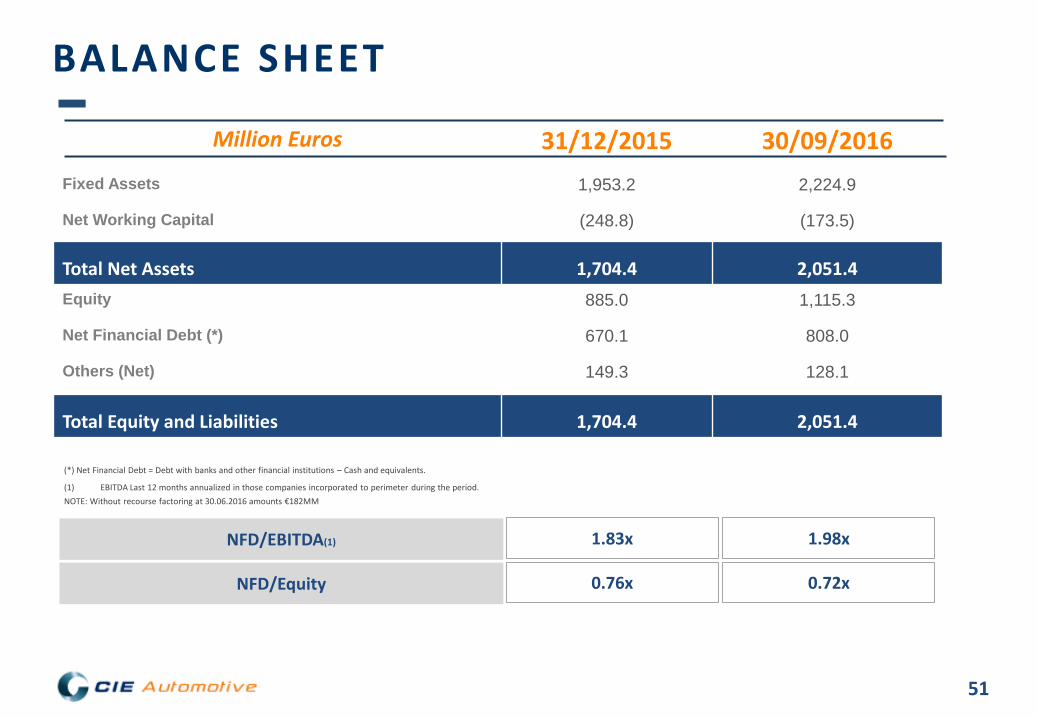

Million Euros 31/12/2015 30/09/2016 Fixed Assets 1,953.2 2,224.9

Net Working Capital (248.8) (173.5)

Total Net Assets 1,704.4 2,051.4 Equity 885.0 1,115.3

Net Financial Debt (*) 670.1 808.0

Others (Net) 149.3 128.1

Total Equity and Liabilities 1,704.4 2,051.4

BALANCE SHEET

(*) Net Financial Debt = Debt with banks and other financial institutions – Cash and equivalents.

(1) EBITDA Last 12 months annualized in those companies incorporated to perimeter during the period. NOTE: Without recourse factoring at 30.06.2016 amounts €182MM

NFD/EBITDA(1) 1.83x 1.98x

NFD/Equity 0.76x 0.72x

52

CAPEX DISCIPLINE

Maintenance investment accounts 80% of total depreciation of the Group

On the way of achieving the goal of reducing depreciation level from 5% to 4%

RONA

Continuous improvement towards the challenge of reaching 20% RONA

Investment analysis discipline, always requiring high returns

Capex ≥ 20% ROI. Net Working Capital ≈0 M&A: EV/EBITDA ≤3 in 3 years

EBITDA CONVERSION

INTO CASH

Operating Cash Flow reaching 50% of EBITDA, enabling the Group to ensure investment commitments

≈50% conversion level target EBITDA into Cash

INVESTMENT DISCIPL INE AND RETURN EXIGENCE

≈4% recurrent investment level that allows an organic growth of 2-3%

53

Strategic Commitments: What is next?

6.0

54

STRATEGIC TARGETS - ORGANIC

(1) EBIT: Net Operating Income.

(2) RONA = “Return on Net Assets”: EBIT/ Net Assets (Fixed Assets + Net Working Capital – Goodwill not associated to cash outs)

(3) Net Financial Debt= Debt with banks and other financial institutions – Cash and equivalents

55

Doubling Net Profit

56

STRATEGIC TARGETS - INORGANIC

Integrate strategical companies to consol idate CIE as one of the most important players in the world; with a very balanced account, achieving at the end of period, a NFD<2xEBITDA ratio

57

New market opportunities

STRATEGIC TARGETS - INORGANIC

700 Mio€ Automotive

addit ional sales

Aluminium

58

New market opportunities

STRATEGIC TARGETS - INORGANIC

300 Mio€ Dominion

addit ional sales

T&T

Renewable Energy Industry

59

CIE in Stock Exchange

7.0

60

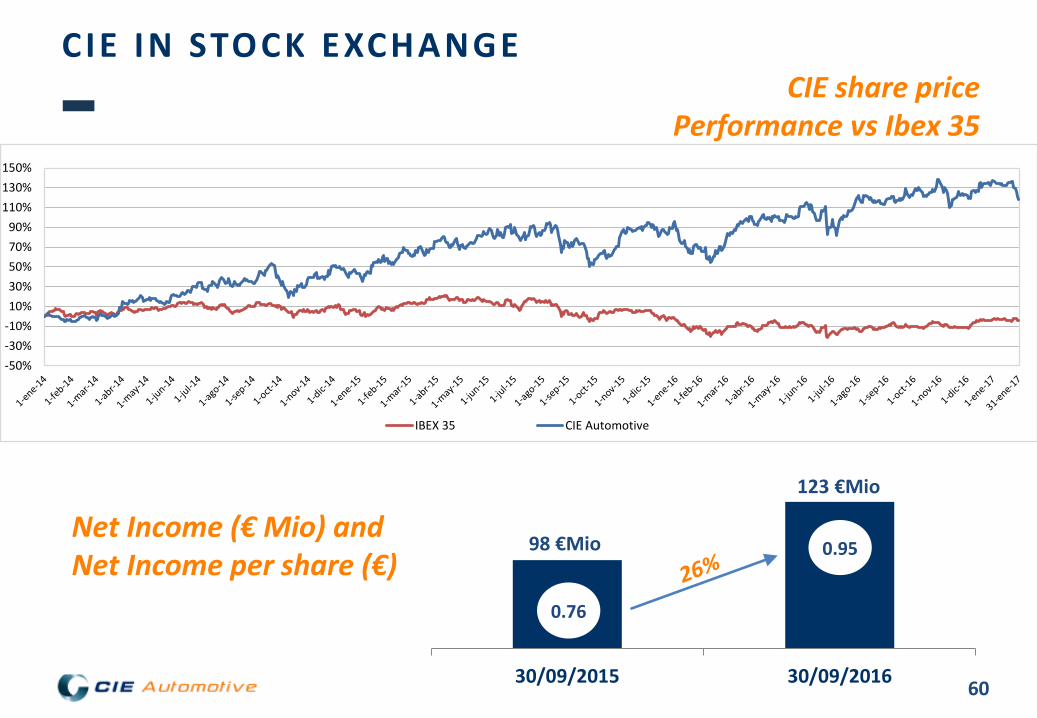

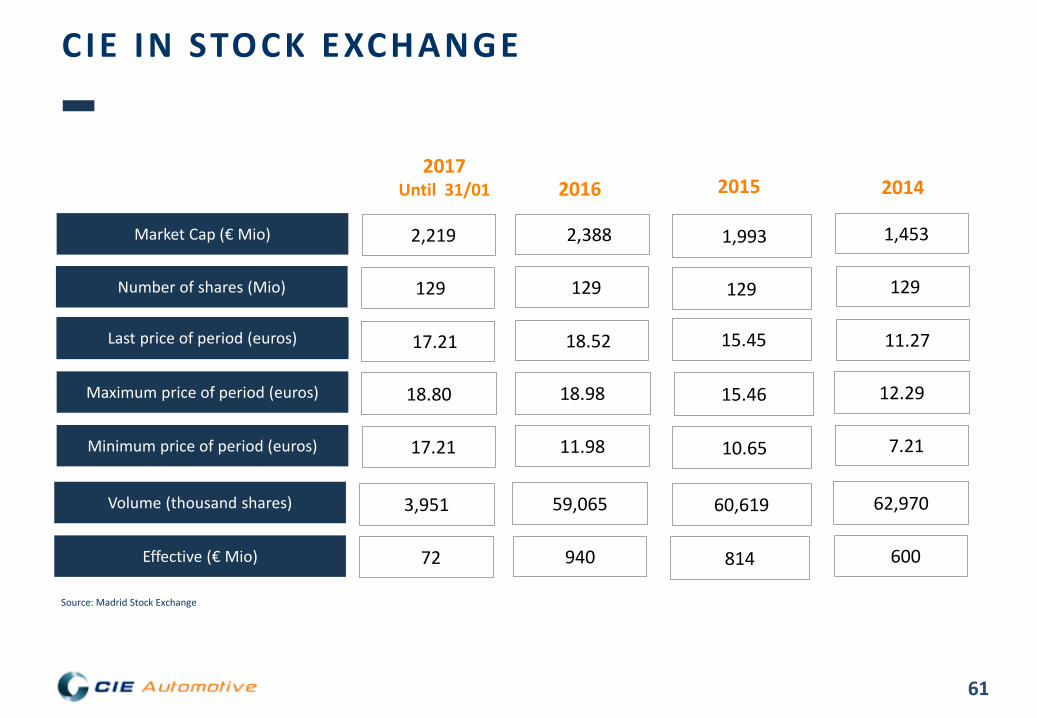

CIE

CIE IN STOCK EXCHANGE

Net Income (€ Mio) and Net Income per share (€)

CIE share price Performance vs Ibex 35

98 €Mio

123 €Mio

30/09/2015 30/09/2016

0.76

0.95

-50%-30%-10%10%30%50%70%90%

110%130%150%

IBEX 35 CIE Automotive

61

Market Cap (€ Mio)

2016

% EBITDA s/ cifra negocio ajustada

Maximum price of period (euros)

2,388 1,993

15.46

Minimum price of period (euros) 11.98 10.65

Last price of period (euros) 18.52

Number of shares (Mio) 129 129

18.98

1,453

7.21

11.27

129

12.29

Volume (thousand shares) 60,619

Effective (€ Mio) 940 814

59,065

600

62,970

2015 2014

Source: Madrid Stock Exchange

CIE IN STOCK EXCHANGE

15.45

2,219

17.21

17.21

129

18.80

72

3,951

2017 Until 31/01

62

Market Cap (€ Mio)

2016

% EBITDA s/ cifra negocio ajustada

Maximum price of period (euros)

2,388 1,993

15.46

Minimum price of period (euros) 11.98 10.65

Last price of period (euros) 18.52

Number of shares (Mio) 129 129

18.98

1,453

7.21

11.27

129

12.29

Volume (thousand shares) 60,619

Effective (€ Mio) 940 814

59,065

600

62,970

2015 2014

Source: Madrid Stock Exchange

CIE IN STOCK EXCHANGE

15.45

2,219

17.21

17.21

129

18.80

72

3,951

2017 Until 31/01

63

Thank you