fdc bi-monthly economic and business update. october 26, 2016

TRANSCRIPT

The Theoretical Difference between a Re-

cession and Stagflation: Global Case Stud-

ies

In times of economic distress, it is possible for economic agents

(Consumers, firms, government, and policymakers) to get misled

with contradicting and inadequate analysis of the Nigeria’s econ-

omy. In order not to fall prey to all kinds of economic jargon, we

must be clear in describing the present state. Nigeria is experienc-

ing one of the worst economic growth contractions since the ‘80s.

It is also plagued by other structural and transient issues such as

increasing consumer prices, fiscal and external imbalances, low oil

production levels, a dysfunctional foreign exchange (forex) mar-

ket and so on. It is easy to morph the economy’s situation into a

theoretical narrative that is not necessarily representative of the

Nigerian case. This article aims to address the gaps in the theo-

retical explanations of the economic situation in Nigeria using

global case studies.

Stagflation or Recession

Stagflation

A stagflation is an economic situation where consumer prices are

high, economic growth is slowing and unemployment maintains a

steady upward trajectory. Ian Macleod first explicitly mentioned

FINANCIAL DERIVATIVES COMPANY LIMITED

Bi-monthly Economic

& Business Update

Volume 6, Issue 74

October 26, 2016

INSIDE THIS ISSUE:

The Theoretical Difference between a Recession and

Stagflation: Global Case Stud-

ies

1

Electricity and the Economy 10

Global Perspective – Culled from the Economist

16

Macroeconomics Indicators 20

Stock Market Update 25

Corporate Focus Equity Report: Unilever Nige-

ria Plc.

30

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

the concept in his assessment of the UK economy.1 Strong

growth and stable prices characterized post-war Britain. High in-

flation in the 1960s through the 1970s plagued the UK economy.

This era was known as the great inflation. The inflation rate in

that period went as high as 25% (1979). It was attributed to the

oil price shocks of the 70s where the price of oil spiked four times,

making net importers of oil highly susceptible to economic dis-

tress.

A state of stagnation is one where there is a persistent period of

slowing growth often followed by high unemployment. Slowing

growth does not mean negative growth. Negative growth best de-

scribes a recession, where a country experiences at least two con-

secutive periods of negative growth.

There are two main views that attempt to describe stagflation in a

country. The UK and other net-importers of oil in the 70s saw

stagflation come about as a result of a reduction in production ca-

pacity attributed to a negative supply shock. Prices in the econ-

omy increased because negative supply shock caused a slowdown

in output due to higher production costs. Hence, output could not

compensate demand.

The second channel where stagflation occurs is via macroeco-

nomic policy gaps. Policy in all facets of the economy is not in

sync. The government of a country might be engaging in policies

that clamp down on growth spikes to target a fairly normal busi-

ness cycle. However, the central bank might also simultaneously

free up money supply in the economy through monetary policy.

This frees up funds for goods that are unavailable.

Global Cases Studies

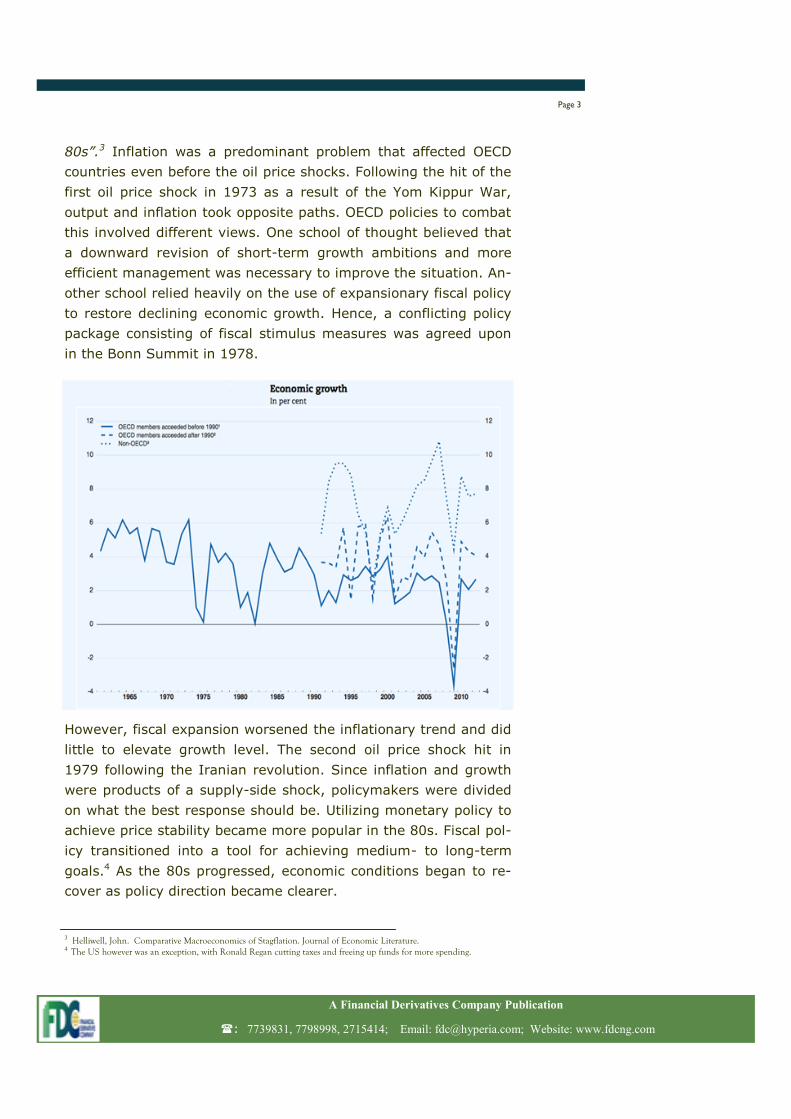

Stagflation in OECD – 70s and 80s2

The oil price shocks of the 70s created a wave of slowing growth

and rising consumer prices, which according to John F. Helliwell

was the “hallmark of OECD economic performance in the 70s and

Page 2

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

1 Gregory Mankiw (2008). Principles of macroeconomics. Pp. 464. 2 Source: OECD at 50, evolving paradigms in economic policy making. OECD Economic Outlook, No. 50 (OECD, 1991). https://www.oecd.org/eco/outlook/48010330.pdf

80s”.3 Inflation was a predominant problem that affected OECD

countries even before the oil price shocks. Following the hit of the

first oil price shock in 1973 as a result of the Yom Kippur War,

output and inflation took opposite paths. OECD policies to combat

this involved different views. One school of thought believed that

a downward revision of short-term growth ambitions and more

efficient management was necessary to improve the situation. An-

other school relied heavily on the use of expansionary fiscal policy

to restore declining economic growth. Hence, a conflicting policy

package consisting of fiscal stimulus measures was agreed upon

in the Bonn Summit in 1978.

However, fiscal expansion worsened the inflationary trend and did

little to elevate growth level. The second oil price shock hit in

1979 following the Iranian revolution. Since inflation and growth

were products of a supply-side shock, policymakers were divided

on what the best response should be. Utilizing monetary policy to

achieve price stability became more popular in the 80s. Fiscal pol-

icy transitioned into a tool for achieving medium- to long-term

goals.4 As the 80s progressed, economic conditions began to re-

cover as policy direction became clearer.

Page 3

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

3 Helliwell, John. Comparative Macroeconomics of Stagflation. Journal of Economic Literature.

4 The US however was an exception, with Ronald Regan cutting taxes and freeing up funds for more spending.

Page 4

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

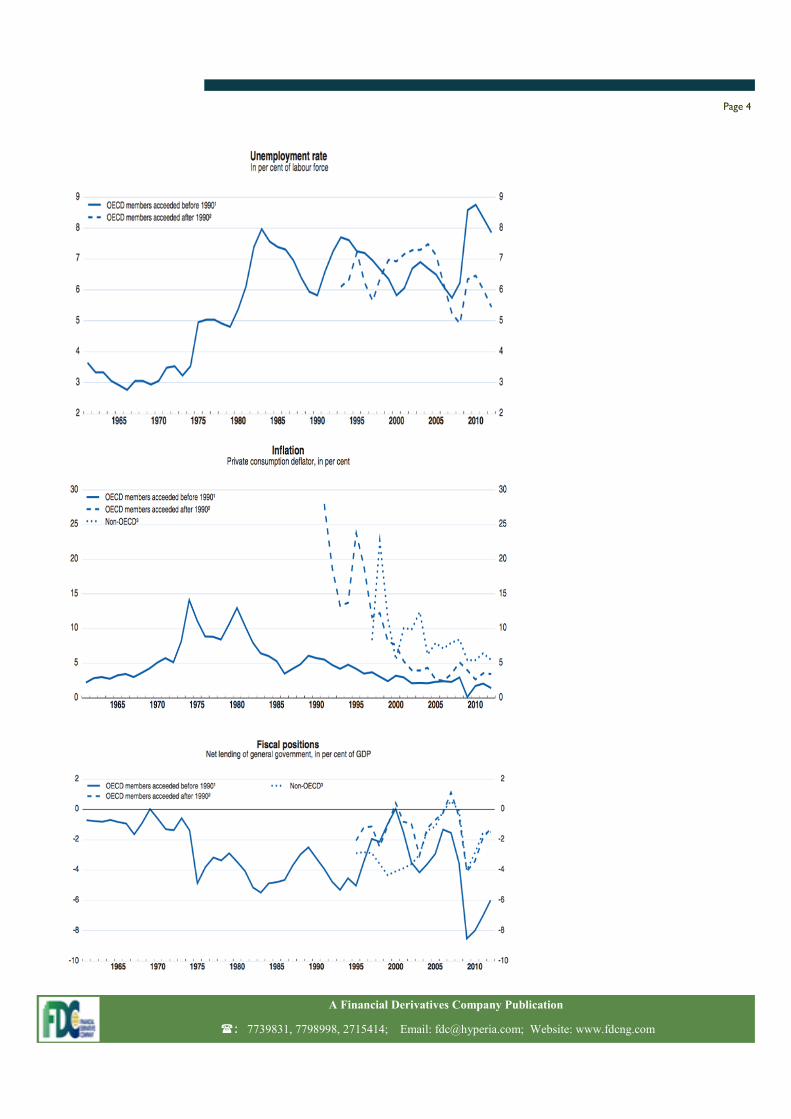

Recession

A recession can be described as two consecutive quarters of nega-

tive growth. It can also be described as a situation where a country’s

potential gross domestic product (GDP) growth outweighs its real

GDP growth for prolonged periods. In a recession, widespread con-

traction in economic activity occurs; the unemployment rate spikes

and inflation declines. This contraction in economic activity can be

attributed to events ranging from bottlenecks in the financial system

to external imbalance shocks.

History of global recessions

The United States

Since the 1980s the US has had four periods of recessions according

to the National Bureau of Economic Research.5

July 1981 – November 1982

Page 5

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

5 National Bureau of Economic Research (NBER) http://www.nber.org/cycles.html

July 1990 – March 1991

March 2001 – November 2001

December 2007 – June 2009

The recession of the 80s was part of the bigger picture of stagfla-

tion that plagued OECD countries following the aftermath of the

oil crises of the 70s and out of sync policies that further aggra-

vated the situation. The recession of the 1990s was a result of the

economic downturn that followed the stock market crash of the

late 80s.6 The Dow Jones Industrial Average fell swiftly and unex-

pectedly by 22.6%. The recession of the early 2000s is often criti-

cized as not fitting the criterion for a recession – two consecutive

quarters of negative growth. However, growth slowed as a result

of boom and bust cycles. The global economic boom of the early

to mid 90s reached the threshold for a decline and as such this

‘recession’ was predicted. The recession of the late 2000s was

caused by a combination of a financial crisis and a subprime mort-

gage crisis. The former has been considered the worst financial

crisis since the great depression of the 20s and 30s. The decline

in the value of assets and the collapse in the financial sector had

the ripple effect of causing economic shock waves to the rest of

the world. Confidence was badly bruised.

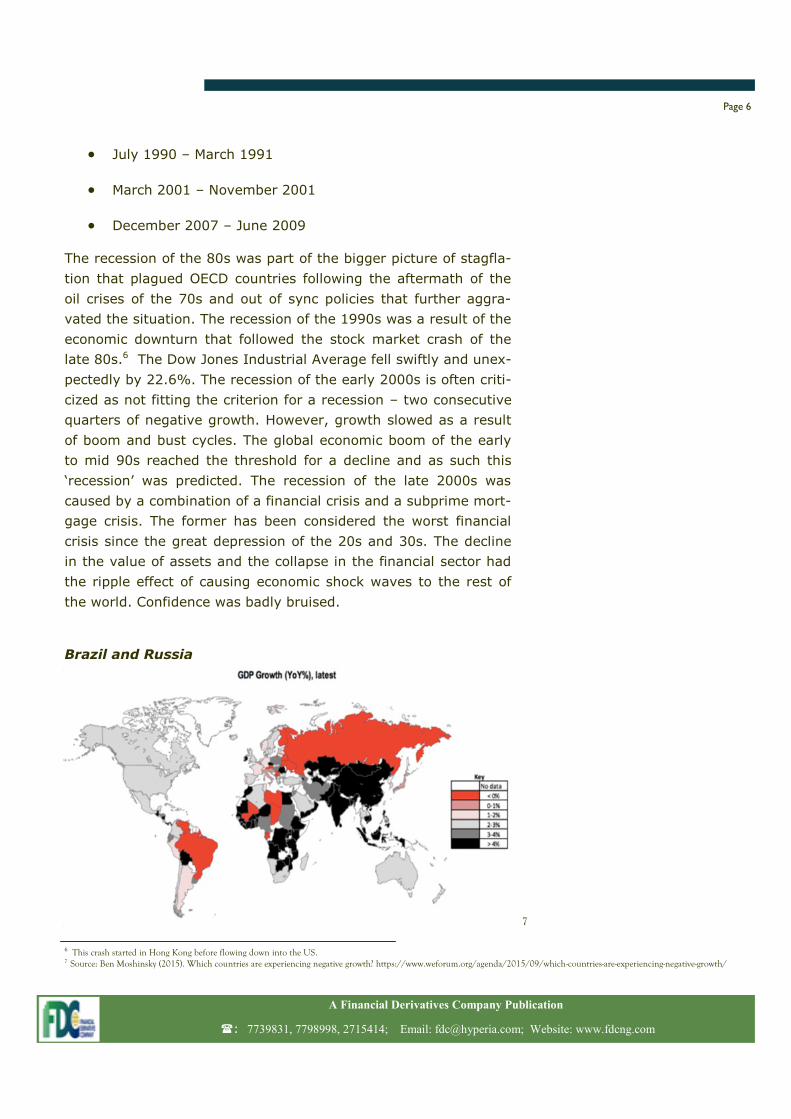

Brazil and Russia

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

6 This crash started in Hong Kong before flowing down into the US. 7 Source: Ben Moshinsky (2015). Which countries are experiencing negative growth? https://www.weforum.org/agenda/2015/09/which-countries-are-experiencing-negative-growth/

7

Page 6

Brazil and Russia are two of a few countries to be experiencing

negative growth. Brazil sank further into a recession in the sec-

ond quarter of 2016, falling to -0.6% from -0.4% in Q1 2016.

This decline is the sixth consecutive quarter of economic decline.

It is further expected that the country’s output for 2016 will main-

tain 2015’s contraction of 3.8%. This downturn is being attributed

to reduced spending power brought on through rising unemploy-

ment, weakened consumer confidence and the political woes that

plague the country. Brazil impeached President Dilma Rousseff in

August following accusations of fiscal budget manipulations. Rus-

sia has been experiencing a recession for the past 19 months. A

combination of low oil prices and economic sanctions – as a result

of its atrocities in Ukraine - has taken a toll on the country. The

economy shrunk by 0.6% in the second quarter of 2016.

Nigeria

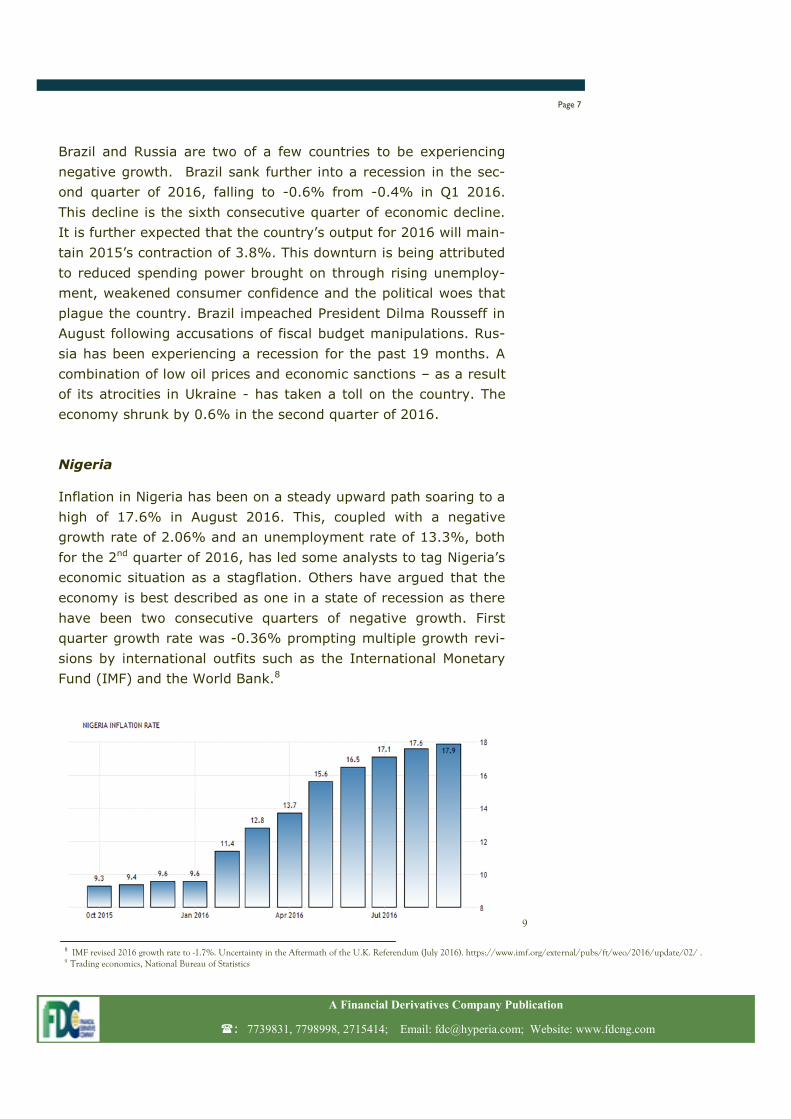

Inflation in Nigeria has been on a steady upward path soaring to a

high of 17.6% in August 2016. This, coupled with a negative

growth rate of 2.06% and an unemployment rate of 13.3%, both

for the 2nd quarter of 2016, has led some analysts to tag Nigeria’s

economic situation as a stagflation. Others have argued that the

economy is best described as one in a state of recession as there

have been two consecutive quarters of negative growth. First

quarter growth rate was -0.36% prompting multiple growth revi-

sions by international outfits such as the International Monetary

Fund (IMF) and the World Bank.8

Page 7

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

9

8 IMF revised 2016 growth rate to -1.7%. Uncertainty in the Aftermath of the U.K. Referendum (July 2016). https://www.imf.org/external/pubs/ft/weo/2016/update/02/ . 9 Trading economics, National Bureau of Statistics

An important point to note is that although inflation rate (Year-on

-Year) rate is rising, month-on-month inflation rate is declining.

The Headline rate illustrated is prone to the bias of base year ef-

fect and as such a little spike in the Consumer Price Index (CPI)

could lead to exaggerated increases in the yearly inflation rate.

The diagram below shows the slowing month-on-month inflation

rate, which is a more representative picture of prices at present.

Therefore, labeling Nigeria’s current economic situation as stag-

flation does not adequately describe its reality. So far in a bid to

curb the consequences of a ‘stagflation’, the CBN has been reluc-

tant in taking a more accommodative stance with interest rates

for fear of spurring inflationary pressures. An accommodative

stance here would require a reduction in the benchmark interest

rate to ease the cost of borrowing and generally stimulate eco-

nomic activities. However, as one who believes in markets – the

interaction of demand and supply for exchange is another solution

path that would entail the government to provide support for the

markets via limited involvement and intervention. Markets would

in turn regulate themselves and transition away from this reces-

sionary state. Whatever path policy takes, understanding the

problem is important in order not to further sink the economy into

a recession.

Page 8

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

10 FDC Think Tank, NBS

Chart 1 : Month-on-Month Inflation

10

Electricity and the Economy

Introduction

For those in developed countries it is almost impossible to imagine

life without a basic necessity such as power. During the rare occa-

sions that power supplies are temporarily cut off, cities are shut

down and activity is halted until the normality of 24/7 electricity is

restored.

But in Nigeria, this is not so. The phrase -‘Up Nepa!’ is not an un-

common one; it’s an exclamation of gratitude to the power opera-

tors for choosing to bless us with electricity. During periods of unin-

terrupted power supply, Nigerians become anxious, understanding

that this probably means that days of darkness are ahead.

In a country where there are as many generators as there are

houses and a where there is a ‘charge your phone’ booth on almost

every street, people have learned not only how to live without a

steady supply of power, but how to make a business out of it.

Power generation in Nigeria

We know that electricity generation in Nigeria is problematic, but

how do we compare to others?

Measurements and Rankings

When assessing the power sector of a country there are three sig-

nificant variables to consider.

The first is total electricity production. This measures the total out-

put from electricity plants during the period. According to the In-

ternational Energy Agency, Nigeria’s total production in 2013 was

29m megawatts hours (MwH). Compared to Nigeria’s West African

neighbors, the country appears to have outperformed. In the same

year, Senegal, Ghana and Cote d’Ivoire produced 3.7m MwH,

12.9m MwH and 7.6m MwH respectively.

Page 10

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

However, to put it in context, Nigeria’s energy production is just

about the same level as Hungary’s. This small Eastern European

country, the size of Borno state in terms of land area and half the

size of Lagos state in terms of population, produced 30m MwH in

2013.

That is why, for a deeper analysis of the power sector we need to

take into account the next variables of measurement: access to elec-

tricity and electricity consumption per capita.

These paint a clearer picture of the electricity gap as they assess

production in relation to demand. So while Hungay’s production level

is enough to supply constant electricity to all of its 9.89m popula-

tion, it is nowhere sufficient for Nigeria’s 173.6m, half of whom do

not even have access to electricity. As at 2013, only 55.6% of Nige-

rians had access to electricity.*

Electricity consumption per capita is the total electricity generation

minus losses in transmission, distribution and transformation divided

by the population. As of 2013, Nigeria’s electric power consumption

per capita was a measly 141.9 kilowatts hours (kWh), compared to

Angola at 226.8 kWh, South Africa at 4,325.5 kWh, Egypt at 1,697.5

and Ghana at 382 kWh.

In essence, it means that each year*, Nigeria generates enough

electricity for each citizen to power a light bulb for about two

months.

Sources & Structure

Prior to privatization in 2014, the Federal Government managed and

financed all the operations of the power sector. Currently, there are

six generation companies (GENCOs) which depend on two sources of

electricity: natural gas (81.6%) and hydro power (18.4%). These

privately owned GENCOs transfer all generated power to the national

grid controlled by the Transmission Company of Nigeria (TCN). Al-

though previously managed by Manitoba Hydro International, a Ca-

nadian power firm, TCN is now controlled by the Federal Govern-

ment.

Page 11

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

The TCN, in turn, transmits power to the 11 electricity distribution

companies (DISCOs). The DISCOs are responsible for distributing

electricity to households in their geopolitical jurisdictions. They

also deal directly with end-users, collecting tariffs and bill pay-

ments. Middlemen agencies are then responsible for the transfer

of profits back to the GENCOs.

Electricity & Economic growth

The importance of electricity lies in its status as a necessary inter-

mediary in the economy. It does not represent an end in itself but

it is required for the success of other initiatives or activities. These

activities can generate welfare or leisure, increase efficiency or

productivity, and generate income.

The shortage and unreliability of power and the need for Nigerians

to generate their own electricity adds unnecessary cost inefficien-

cies. Households and businesses spent N3.5 trillion to power gen-

erators. Given the increase in the price of petrol and diesel, this

figure is estimated to reach N5 trillion in 2017 - a less than ex-

pected spike given the trending switch from fuel energy to renew-

able energy (solar power, inverters etc.). With companies such as

MTN reportedly spending N8bn on power generation annually, it

shows that the present power situation has negative connotations

for business operations and profitability.

In its Ease of Doing Business Report, the World Bank* draws a

parallel between Nigeria’s frail power sector and its business envi-

ronment. Accordingly, the procedures, time and costs involved in

getting connected electricity, combined with the unreliability of

the power supply and the per unit electricity bills are factors that

contribute to making Nigeria a tough place to do business. Using

Lagos State as a proxy, it takes 184 days (6 months) on average

from the moment you submit an application for electricity connec-

tion to initial electricity flow. In the 2016 rankings, Nigeria came

182 out of 189 countries in the ‘Ease of getting electricity’ sub-

index. Furthermore, Nigeria scores 0 out of 8 on the reliability of

supply and transparency of tariff index.

Page 12

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

This means that if Nigeria is to realize the dream of becoming the

number 1 FDI destination in the world, with a booming economy

and tourism, then something needs to be done about power- and

fast! Constant and reliable electricity will cut business costs; this

will translate into increased efficiency, productivity, output, job

creation and economic activity.

Challenges

The challenges the power sector faces are deep-rooted and multi-

faceted.

At the generation level, GENCOs continue to produce at sub-

optimal levels; yet, even if they did not, their total installed ca-

pacity would still be unable to meet electricity demands. Outdated

technology, poor maintenance, low investments etc. are some

reasons for this. The GENCOs that use natural gas are also af-

fected by pipeline vandalism and exchange rate illiquidity, both of

which lead to gas shortages and shortfall in generation.

At the transmission level, the national grid’s carrying power is too

modest, such that even if GENCOS were to generate more, the

grid would not be able to handle it. In addition to this, great

amounts of electricity are lost in transmission. Although TNC

claims an average transmission loss of about 8.5%, the loss is

estimated to be much greater due to deteriorating infrastructure.

Furthermore, the DISCOs battle with customers who do not pay

their bills- the biggest culprit being the Nigerian government. As

at Q1’2016, the government had about $300m in unpaid electric-

ity bills*. While it is easier for DISCO agents to threaten the aver-

age citizen with notices and written warnings, it more difficult to

do so with national departments such as the army barracks.

Operators also complain that the current tariff levels are not suffi-

cient to break even. The Nigerian Electricity Regulation Commis-

sion had been ordered to reverse its 45% hike in tariffs by the

Federal High Court in Lagos. Backed by the Ministry of Power, the

NERC is seeking appeal at the Supreme Court.

It is no surprise that these energy industry players have huge

debt burdens. As at March 2016, GENCOs had outstanding loans

Page 13

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

of N367 in total. TCN and DISCOs have a joint debt of N162bn.

This increases the profitability risk of the sector and discourages

further private investments.

The way forward

The major problem of the power sector is one of funds and infra-

structure, which can only be tackled with investments into pro-

curement, maintenance and operation. The government has initi-

ated a N213bn Nigerian Electricity Market Stabilization Facility

(NEMSF), out of which a total of N55.4bn has been disbursed so

far. Additionally, according to a Memorandum of Understanding

with Chinese firms, about $50m would be invested into gas infra-

structure, pipelines, power etc. If implemented efficiently and

completely, this brings large promise to the power sector.

However, there are still some risks that need to be curbed to im-

prove the attractiveness of the sector and draw more inflows in

the long run. These involve certainty and predictability of policies

and regulations as well as returns and profit. A profitable market

with an equilibrium price and a favorable policy environment will

attract investment flows.

Thus, the problem must also be approached from the bottom up

i.e. from the consumers to the GENCOs. This includes tackling is-

sues of appropriate pricing and overdue payments.

Conclusion

Nigeria’s vision 2020 is to produce 35,000 MW, the estimated

amount needed to meet consumption needs*. While this originally

seemed far-fetched when the goal was set in 2010, it is all the

more implausible now, as 4 years to the deadline the country still

produces 4,000 MW. However, if these issues are addressed the

nation would be one step closer to the ideal of 24/7 electricity.

Page 14

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

Global Perspective – Culled from the Econo-

mist

Into the light

How governments can nudge informal businesses

to leave the grey economy

The spread of mobile technology helps

Sweatshops in the back rooms of Indian family houses; Mexican

families paying their servants cash; Nigerian teenagers hawking

DVDs in the street: all are in the “informal economy”, buying and

selling beyond the ambit of the state. Toiling in the shadows like

this is a vast enterprise. Excluding farm work, two-thirds of jobs

in poor countries are informal.

Some of this is welcome, even admirable. Predatory governments

leave businesses with little choice but to elude their clutches. In

parts of Russia the only profitable way to run a firm is to hide the

profits from bribe-hungry bureaucrats. In even more repressive

countries, informality may be the only way for people to survive.

When famine struck North Korea in the 1990s, millions broke the

law by selling smuggled food.

Page 16

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

But slogging away in the grey economy is not always noble. Some

people work informally because they can get away with it; others

because it is all they know. Either way, informality hurts workers

and their fellow citizens. Fortunately, smart policies and the

spread of mobile technology can, together, help bring them out of

the shadows.

For almost any business, operating informally has its upsides.

Hiding revenues, or paying staff in cash, is an easy way of cutting

a tax bill. Avoiding regulations lets people pocket more profit. And

yet what makes sense today can be an act of self-harm tomorrow.

Informal firms have weak property rights. This makes it tough to

secure finance, so they struggle to become more productive.

Rarely do they grow.

The drawbacks are widely spread. Informal firms tend to pay

measly wages and offer few or no employee benefits. They also

deprive the state of income and sales taxes. So governments tax

other sorts of economic activity instead, causing harmful distor-

tions, for example by raising income taxes on workers in the

mainstream economy. It is no coincidence that Greece, which by

one calculation has an informal economy about as big as its for-

mal one, has such poor public finances.

Beware of the dark

The problem is that once an informal economy has formed, it is

hard to tackle. No company wants to be the first to go clean, lest

they lose out to other firms in the same industry. The idea of pay-

ing extra tax appeals to no one.

How can governments shift their economies out of this bad equi-

librium? One option is to crush the informal sector. Italy’s Guardia

di Finanza is part of the country’s armed forces. (Pasta-scoffers be

warned: tourists without a proper receipt for their meal can be

fined.) Another common strategy is to set up hotlines, where nosy

neighbours can report suspected misdeeds.

Such punitive measures are occasionally successful. But to spur a

large-scale move out of informality, firms need to see the benefits

of changing their ways. That means governments doing what it

Page 17

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

takes to make the formal economy more appealing and easier to

enter.

Grand reforms, such as creating an effective tax system, are im-

portant. But there are also easy wheezes that will nudge citizens

to behave better. Consider one: receipt lotteries. These put pres-

sure on businesses to register revenues by encouraging shoppers

to ask for proof of purchase. Every month or so, the holder of a

lucky receipt number wins a chunk of cash. Since São Paulo intro-

duced its lottery in 2007, more businesses have registered with

the city, and the tax take has swelled. Efforts to show citizens

that public money is wisely spent may also improve “tax mo-

rale”—the sense that paying taxes is a duty.

As technology improves, nudging will become easier, because the

benefits of the formal economy should become more apparent.

Around 80% of adults worldwide will have a smartphone by 2020.

That means more transactions will be recorded digitally. Informal

entrepreneurs will find it harder to do business in cash alone. At

the same time, they will find it easier to apply for credit, bringing

them into the formal economy. Tax authorities can also use digital

platforms to monitor economic activity. Some European countries

are already offering free record-keeping software to companies in

an effort to entice cash-only businesses into the formal sector.

Informality is a wise last resort for many of the world’s poorest.

But for others, life in the shadows is a needless waste. Policies

that draw them into the light need not be complicated or expen-

sive, but they can do a lot of good

Page 18

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

Macroeconomics Indicators

Money Market

The money markets opened with a liquidity position of N23.21bn

long for the month of October compared to N118.7bn in Septem-

ber. The opening position averaged N5.69bn from the 4th to the

21st of October, 48.5% higher than the N11.05bn short position

for the corresponding period in September. On the 21st of October

the markets closed at N10.49bn long compared to N54.8bn long

on September 21st. The money market remained relatively illiquid

with interest rates shooting up to record highs of 150% p.a. dur-

ing the review period. This was due to forex funding for the CBN’s

2-month forward contract.

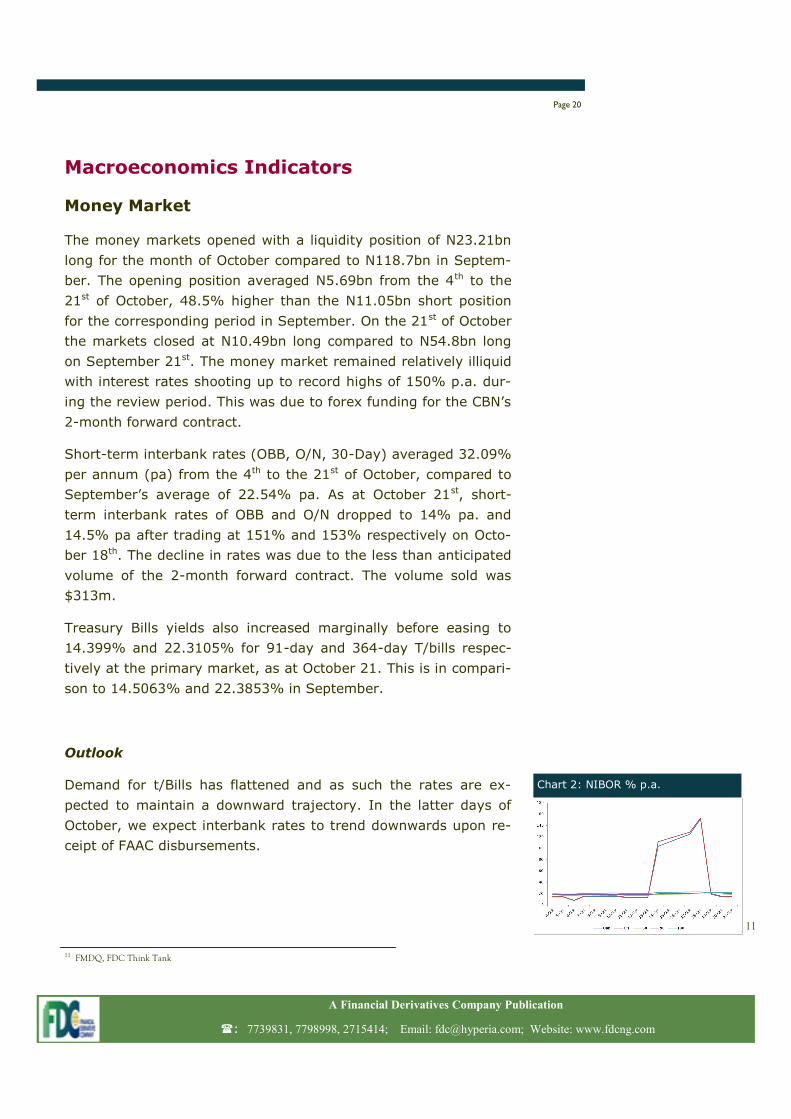

Short-term interbank rates (OBB, O/N, 30-Day) averaged 32.09%

per annum (pa) from the 4th to the 21st of October, compared to

September’s average of 22.54% pa. As at October 21st, short-

term interbank rates of OBB and O/N dropped to 14% pa. and

14.5% pa after trading at 151% and 153% respectively on Octo-

ber 18th. The decline in rates was due to the less than anticipated

volume of the 2-month forward contract. The volume sold was

$313m.

Treasury Bills yields also increased marginally before easing to

14.399% and 22.3105% for 91-day and 364-day T/bills respec-

tively at the primary market, as at October 21. This is in compari-

son to 14.5063% and 22.3853% in September.

Outlook

Demand for t/Bills has flattened and as such the rates are ex-

pected to maintain a downward trajectory. In the latter days of

October, we expect interbank rates to trend downwards upon re-

ceipt of FAAC disbursements.

Page 20

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

11 FMDQ, FDC Think Tank

Chart 2: NIBOR % p.a.

11

Oil Market

Oil Prices

Brent crude prices averaged $51.9pb between the 1st to the 21st

of October. This is a 9.86% increase from September’s average

of $47.24pb. Prices reached a peak of $53.14pb on the 10th of Oc-

tober, but have continued on a downward path. Nonetheless,

prices are manifesting the market’s sentiment towards the final-

ization of the agreed production cut by OPEC member countries

on November 30th. From a reduction of Chinese production by

9.8% to a reduction in US oil production by 5.2m barrels to

468.7m, the market is relatively bullish. However, new develop-

ments have risen in the Iraqi camp. The second largest oil pro-

ducer, after Saudi Arabia, has expressed its reservation about

production cuts and is unwilling to partake of the meeting’s pro-

ceedings.

Outlook

Although most OPEC members are united in their bid to restore

prices to former highs, Iraqi resistance towards production cut

could put this goal in jeopardy. Also, the US is not involved in

these meetings. The influx of US oil in the market is what trig-

gered the oil price shock in 2014. Therefore an intended output

cut without the contribution of the US may do little to prop up

prices.

Oil Production

Production levels recovered marginally in the month of Septem-

ber, mainly due to the ceasefire agreement between the govern-

ment and the Niger Delta avengers. Production levels increased

by 95,000 bpd to 1.524 mbpd. This is 30.72% of the 2016 budget

benchmark.

Page 21

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

Chart 3: Oil Price ($/b)

12

12 Bloomberg, FDC Think Tank 13 Source: OPEC

Chart 4: Oil Production (mbpd)

13

Outlook

The outlook on Nigeria’s production level is subject to further at-

tacks by the militants. If the cease fire is temporary, this could

result in further decline in output below 1.5mbpd.

Forex Market

Exchange Rate

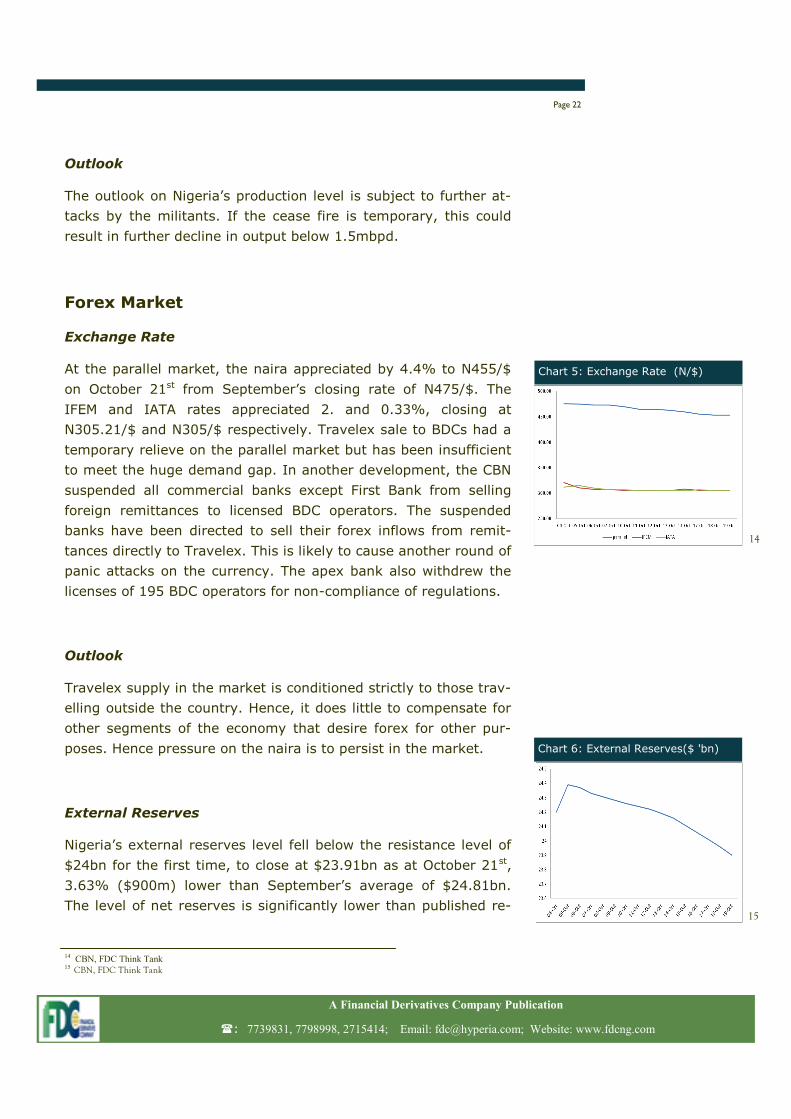

At the parallel market, the naira appreciated by 4.4% to N455/$

on October 21st from September’s closing rate of N475/$. The

IFEM and IATA rates appreciated 2. and 0.33%, closing at

N305.21/$ and N305/$ respectively. Travelex sale to BDCs had a

temporary relieve on the parallel market but has been insufficient

to meet the huge demand gap. In another development, the CBN

suspended all commercial banks except First Bank from selling

foreign remittances to licensed BDC operators. The suspended

banks have been directed to sell their forex inflows from remit-

tances directly to Travelex. This is likely to cause another round of

panic attacks on the currency. The apex bank also withdrew the

licenses of 195 BDC operators for non-compliance of regulations.

Outlook

Travelex supply in the market is conditioned strictly to those trav-

elling outside the country. Hence, it does little to compensate for

other segments of the economy that desire forex for other pur-

poses. Hence pressure on the naira is to persist in the market.

External Reserves

Nigeria’s external reserves level fell below the resistance level of

$24bn for the first time, to close at $23.91bn as at October 21st,

3.63% ($900m) lower than September’s average of $24.81bn.

The level of net reserves is significantly lower than published re-

Page 22

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

Chart 5: Exchange Rate (N/$)

14

Chart 6: External Reserves($ 'bn)

15

14 CBN, FDC Think Tank 15 CBN, FDC Think Tank

ports. Year to date, the gross reserves level has declined by

17.5% ($5.08bn). The external reserves level is 30.72% below

2015’s peak of $34.51bn and 21.58% lower than 2015’s average

of $30.89bn.

Outlook

The International Monetary Fund (IMF) expects Nigeria’s external

reserves level to decline to $19bn-$21.5bn by the end of

2016. The outstanding obligations are in excess of $4bn. If there

is no improvement in oil production and dollar inflows, we expect

to see a further depletion in the reserves level.

Page 23

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

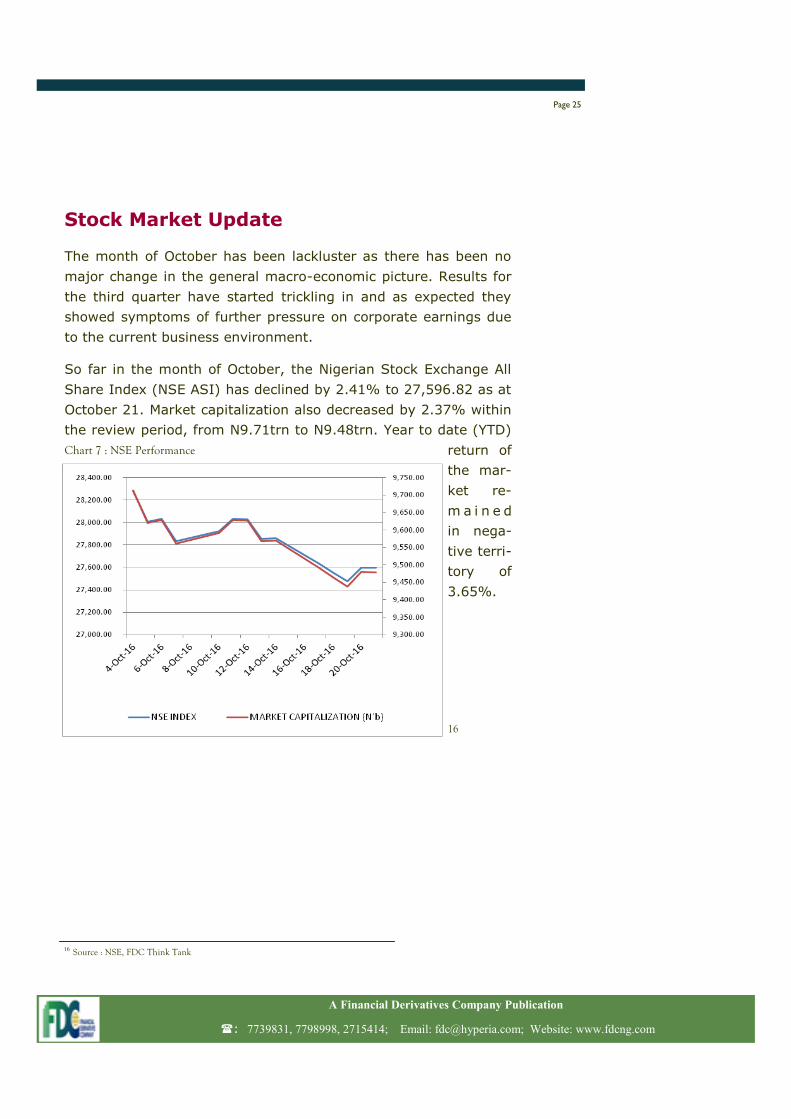

Stock Market Update

The month of October has been lackluster as there has been no

major change in the general macro-economic picture. Results for

the third quarter have started trickling in and as expected they

showed symptoms of further pressure on corporate earnings due

to the current business environment.

So far in the month of October, the Nigerian Stock Exchange All

Share Index (NSE ASI) has declined by 2.41% to 27,596.82 as at

October 21. Market capitalization also decreased by 2.37% within

the review period, from N9.71trn to N9.48trn. Year to date (YTD)

return of

the mar-

ket re-

m a i n e d

in nega-

tive terri-

tory of

3.65%.

Page 25

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

16 Source : NSE, FDC Think Tank

Chart 7 : NSE Performance

16

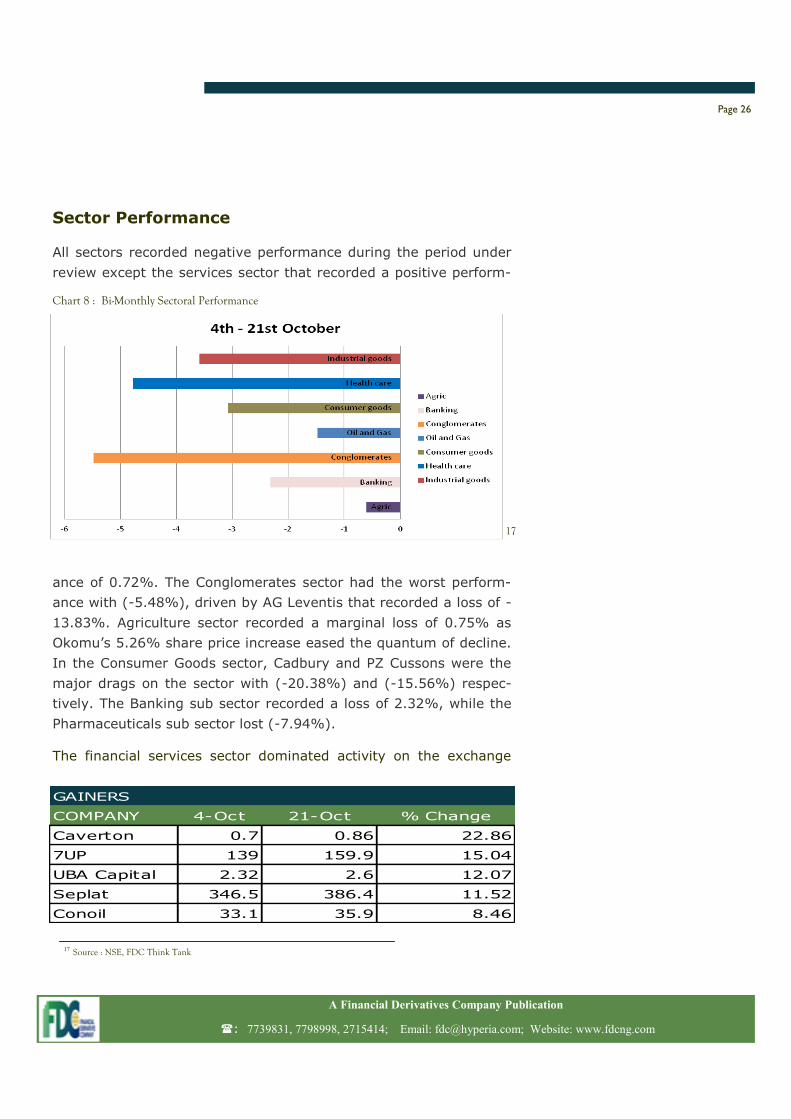

Sector Performance

All sectors recorded negative performance during the period under

review except the services sector that recorded a positive perform-

ance of 0.72%. The Conglomerates sector had the worst perform-

ance with (-5.48%), driven by AG Leventis that recorded a loss of -

13.83%. Agriculture sector recorded a marginal loss of 0.75% as

Okomu’s 5.26% share price increase eased the quantum of decline.

In the Consumer Goods sector, Cadbury and PZ Cussons were the

major drags on the sector with (-20.38%) and (-15.56%) respec-

tively. The Banking sub sector recorded a loss of 2.32%, while the

Pharmaceuticals sub sector lost (-7.94%).

The financial services sector dominated activity on the exchange

Page 26

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

Chart 8 : Bi-Monthly Sectoral Performance

17

COMPANY 4-Oct 21-Oct % Change

Caverton 0.7 0.86 22.86

7UP 139 159.9 15.04

UBA Capital 2.32 2.6 12.07

Seplat 346.5 386.4 11.52

Conoil 33.1 35.9 8.46

GAINERS

17 Source : NSE, FDC Think Tank

during the period under review accounting for 54.77% of the total

value traded. The oil and gas sector constituted 18.27% while Con-

sumer goods, industrial goods and conglomerates sectors ac-

counted for 16.17%, 6.96% and 1.39% respectively. Total value of

stocks traded within the period was 23.26bn while market breadth

was 0.32x as 60 stocks declined against 19 stocks that advanced.

105 stocks remained unchanged during the period under review.

The best performing stocks include Caverton 22.86%, 7UP 15.04%,

UBA Capital 12.07%, Seplat 11.52% and Conoil 8.46%.

Top losers during the period were; Forte -23.27%, Lafarge -

21.51%, Cadbury -20.38%, Guinness -18.36% and E-Tranzact -

18.28%.

Corporate Disclosures

United capital ushered in the earnings season by being the first

listed company to release its third quarter results. As expected, the

results were impressive and will be used as a benchmark for its

peers in the financial services sector.

Guaranty Trust Bank (GTB) Plc published its third quarter finan-

cial results and there was a noticeable improvement in both top and

bottom line performance, compared to Q3’15. The bank recorded a

5.17% increase in interest income to N181.91bn, while fee and

commission income increased by 27.1% to N50.41bn. Net interest

income increased by 28.2% to N48.13bn, compared to N37.54bn in

Q3’15. Profit before and after tax were higher by 52.98% and

59.57% to N140.84bn and N119.93bn respectively on gains in the

top line. However, the bank reported a foreign exchange revalua-

tion gain of N93.63bn, compared to N6.77bn recorded in Q3’15.

Loan impairment charges also increased sharply to N57.08bn, from

Page 27

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

COMPANY 4-Oct 21-Oct % Change

Forte 165.9 127.3 -23.27

Lafarge 54.8 43.01 -21.51

Cadbury 16.49 13.13 -20.38

Guinness 97.99 80 -18.36

E-Tranzact 5.69 4.65 -18.28

LOSERS

N8.51bn in the corresponding period last year.

Zenith Bank Plc. released its third quarter corporate earnings

which showed improvements in both top and bottom line. Gross

earnings increased by 12.9% to N380.35bn from N336.85bn in

Q3’16. Notwithstanding, impairment charges increased by

38.53% to N21.86bn from N15.78bn in the corresponding period

in 2015. Profit before tax (PBT) increased by 16.6% to N121.28bn

while profit after tax (PAT) increased by 20.4% to N100.07bn.

Outlook

We expect the release of more third quarter results to continue to

drive the performance of the equities market in the coming week.

We therefore advise investors to be cautious in their activities on

the bourse and maintain a medium to long-term investment hori-

zon

Page 28

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

Corporate Focus

Equity Report: Unilever Nigeria Plc.

Analysts Recommendation: SELL

Recommendation Period: 365 days

Industry: Consumer Goods

Market Capitalization: N139.04bn

Current Price: N45.90

Target Price: N13.45

The FDC Think Tank places a SELL recommendation on Unilever Ni-

geria Plc following a comprehensive analysis of the company.

Recent challenging macroeconomic conditions caused a contraction

in domestic output. In July 2016, the Central Bank of Nigeria (CBN)

announced an unusual increase of 200 basis points (bps) in mone-

tary policy rate (MPR). Manufacturers face rising raw materials and

logistics costs caused by the increase in the cost of the dollar and

an upward review of the Premium Motor Spirit (PMS) price from

N86.5 to N145/ per liter. While households cut down on spending,

the consumer goods industry has proven to be resilient and regis-

tering growth.

Page 30

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

Unilever Nigeria Plc’s H1’16 revenue grew 12.4% to N32.27bn, up

from N28.72bn recorded a year earlier. While the company posted a

half year results decline of 94% in profit after tax (PAT) from

N1.46bn (2014) to N85.5m (2015), it showed remarkable improve-

ment in its H1’16 results, which reported N1.09bn in PAT. Its share

price increased by 14.8% in the ten weeks following the half year

results.

Unilever plans to further increase its investment in Nigeria by ac-

quiring farmlands to grow most of its inputs and secure the supply

of essential ingredients for the long term. This strategy increases

competitiveness by providing affordable, nutritious and sustainable

products as the economy recovers. Given these investments, Unile-

ver could remain a leading figure in the consumer goods industry.

Yet, the cumulative effects of supply shocks, in the foreign ex-

change (forex) and energy markets, pose a colossal threat to its

ability to grow revenues consistently. While the devaluation of the

naira created a 12.4% increase in revenues, the company’s inability

to pass on higher costs to consumers affects its profitability. The

company’s receivables increased by 40% (H1’16) hampering its

ability to generate cash. Unilever is currently operating on a debt

1.5 times greater than its shareholders’ equity of N8.9bn. Approxi-

mately 94% of its loans are short-term. It is unlikely that lenders

will call in the loans. Yet, the highly leveraged position remains a

cause for concern, and could possibly cartwheel into a liquidity cri-

sis.

Unilever’s share price for 2016 opened at N43.18. It has gained

6.3% year-to-date (YTD) and 7.3% in the past year. In June 2015

the company’s parent company, Unilever Overseas Holdings BV,

restated its intention to raise its stake in the Nigerian market to

75%, pending regulatory approvals. The company has a price earn-

ings multiple of 65. (Investors are willing to pay 65 times the com-

pany’s reported earnings for a share, as against an industry aver-

age of 19.)

We believe that Unilever’s stock is overvalued, and recommend a

SELL, as we do not foresee a sustainable appreciation in its share

price.

Page 31

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

Home-grown supply practices could lead to long-

term sustainability

Unilever Nigeria is a leading manufacturer of consumer goods in

Nigeria. Established in 1923, it is the oldest surviving manufactur-

ing organization in the country. The company has been quoted on

the Nigerian Stock Exchange since 1973. Its roots are in soap

manufacturing, diversifying into several successful strategic busi-

ness segments including food and drink, personal care, and home

care products.

The company is an advocate of long-term sustainable business

practices. It sources all its key ingredients locally through farmers

and suppliers where available. The company also grows some of its

Page 32

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

Business Segment Product lines

Food & Drink Blue Band, Knorr, Royco and Lipton Tea

Personal Care Vaseline, Lifebuoy, Rexona, Fair&Lovely, CloseUp and Dove

Home Care Omo Detergent and Sunlight

FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 CAGR

N'000 N'000 N'000 N'000 N'000 %

ASSETS

Non-current assets 16,019.9 21,719.4 25,352.8 27,165.1 29,164.7 16.16%

Current assets 16,260.1 14,778.3 18,401.3 18,571.2 21,007.8 6.61%

Total non-current liabilites (3,731.1) (4,121.5) (5,955.5) (6,886.6) (7,471.6) 18.96%

Total current liabilites (18,884.2) (22,332.6) (28,158.9) (31,370.8) (34,697.7) 16.43%

Net Assets 9,664.7 10,043.5 9,639.7 7,478.8 8,003.3 -4.61%

CAPITAL AND RESERVES

Share capital 1,937.4 1,937.4 1,937.4 1,937.4 1,937.4 0.00%

Retained earnings 7,727.3 8,106.2 7,702.3 5,541.4 6,065.9 -5.87%

Total Equity 9,664.7 10,043.5 9,639.7 7,478.8 8,003.3 -4.61%

COMPREHENSIVE INCOME

Revenue 54,724.7 55,547.8 60,004.1 55,754.3 59,221.7 1.99%

Profit Before Taxation 10,655.8 8,186.0 6,911.4 2,873.2 1,771.1 -36.15%

Taxation (5,250.7) (2,588.4) (2,104.5) (460.9) (578.7) -42.38%

Profit After Taxation 5,405.1 5,597.6 4,806.9 2,412.3 1,192.4 -31.47%

UNILEVER NIGERIA PLC

raw materials on agricultural lands it owns. Exposure to currency

volatility and uncertainty is reduced through a sustainable and se-

cure supply of essential ingredients. The company’s performance

over the years is in the snapshot of its financials shown below:

Macroeconomics work against Unilever’s growth

strategy

Unilever’s revenues grew approximately 8.3%, from N15.49bn in

Q1’16 to N16.78bn in Q2’16. This is an H1’16 increase of 12.4%

(YoY). Improvements in the food and drink, and home care seg-

ments propelled this growth. They increased by 22.3% to N16.86bn

and 25.2% to N7.49bn (YoY) respectively. A more efficient use of

third-party bank facilities saw finance costs drop by 55.6%. This

contributed to the N1.04bn profit reported in H1’16 in contrast to

N85.5m in H1’15.

The Fast Moving Consumer Goods (FMCG) sector remains one of

the fastest growing in the economy despite a decline in its contribu-

tion to GDP. The Nigerian consumer market, estimated at N15 tril-

lion, presents increasing opportunities. Companies, such as Unile-

ver, are at its forefront. Yet, there are several factors that can af-

fect Unilever’s future revenues and share price. The most prominent

is the domestic economy with its increased inflation, decreasing

value of the naira, depleting reserves and a fall in forex earnings

due to variances in oil production. The lower availability of dispos-

able income is also affecting sales in the FMCG sector as consumers

choose cheaper substitutes. Thus, Unilever’s performance walks a

macroeconomic tightrope with management navigating an unpre-

dictable environment.

Management

His Majesty Nnaemeka Achebe CFR, MNI, the Obi of Onitsha, who

joined Unilever in 2003, leads the board. Managing Director, Mr.

Yaw Nsarkoh has led the company since 2004. He has held many

portfolios throughout his 23-year career within Unilever.

The executive management includes knowledgeable individuals who

Page 33

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

have worked in Unilever in various capacities. Their perceived com-

mitment to expand in Nigeria earned them the support of the Nige-

rian Senate and the Ministry of Trade and Investment in a press re-

lease in January 2016. This support could enable management to

put in place their strategy to acquire farmlands in secure locations

throughout the country. If Unilever is successful in diversifying, it

could regain and perhaps exceed previous levels of success.

Bulls Say:

Prominent brand value across all its business segments

Investments in its sustainable sourcing program could reduce

costs and enhance the company’s profitability margins

Extensive distribution channels, which could be strengthened

through retail network optimization and strategic expansion

Experienced management team

Bears Say:

Intense competition in the food and drink segments of the con-

sumer goods industry

Increasing consumer resistance, due to lower disposable in-

come, could lead to slowdown in sales

Disruptions in distribution and sales channels, due to insecurity

and insurgency, to put pressure on margins

Performance also limited by higher energy costs and borrowing

costs

Emergence of cheaper substitutes as consumer demand for

economy brands rises

Risks & Outlook: Markets, recession and reduced

Page 34

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

household spending

Unilever Nigeria faces several prevailing market risks and security

challenges in the country. Market risks include currency volatility

and uncertainty in the prices of raw materials. With commodity

prices increasing, the company needs to speed up its local sourcing

program to hedge against increased costs of global goods.

Nigeria recorded a negative growth of -2.06% in Q2’16. This con-

firms the economy is in a recession. In spite of management’s abil-

ity to cope with the macroeconomic challenges it faces, the head-

winds, such as weak consumer demand could challenge the com-

pany’s performance.

Finally, the macroeconomic factors and risks may reduce Unilever’s

potential full year performance in spite of the noteworthy H1’16 re-

sults. These factors, alongside our Unilever projections for FY’16,

show that the stock is overvalued. It will likely see a drop in its

share price in the foreseeable future, thus, supporting our SELL rec-

ommendation.

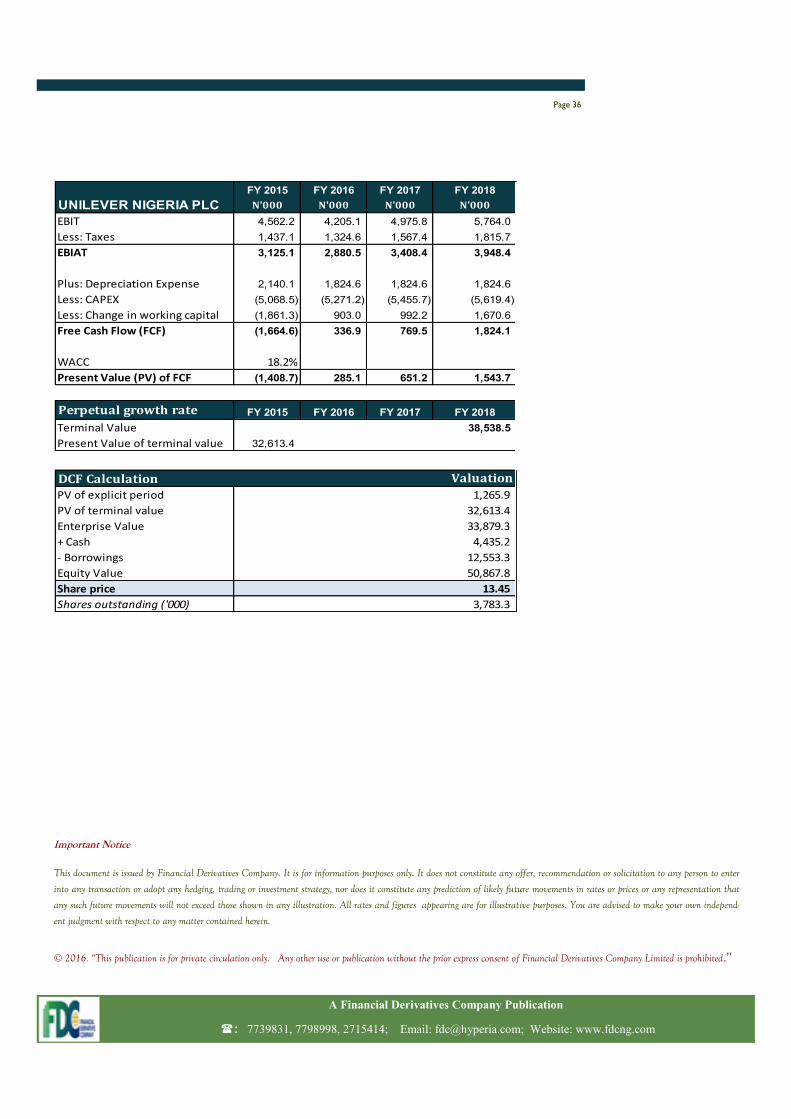

Appendix : Valuation

We derived our valuation for Unilever Nigeria Plc by using the Dis-

counted Cash Flow (DCF) methodology. Our fair value estimate for

Unilever Nigeria Plc is N13.45, which is a 70.7% downside on the

current share price as at October 21, 2016.

Unilever’s intrinsic value is derived to be N13.45 when the DCF

method is used. The discount rate or the weighted average cost of

capital (WACC) of 18.2%, is derived using a 14.99% risk free rate

(the rate for the 3 year FMDQ Bond maturing on August 2019), a

beta of 0.91, an after-tax cost of debt of 17.3%, and a market risk

premium of 5%. The long term cash flow growth rate to perpetuity

calculated is 12.8%.

Despite Unilever’s impressive H1’16 result and its expansionary

plans, we foresee a three-year revenue CAGR of 3.63%. This is off

the back of deteriorating macroeconomic conditions alongside in-

creasing consumer resistance and switch to more affordable substi-

tutes.

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

Page 35

Page 36

A Financial Derivatives Company Publication

: 7739831, 7798998, 2715414; Email: [email protected]; Website: www.fdcng.com

FY 2015 FY 2016 FY 2017 FY 2018

N'000 N'000 N'000 N'000

EBIT 4,562.2 4,205.1 4,975.8 5,764.0

Less: Taxes 1,437.1 1,324.6 1,567.4 1,815.7

EBIAT 3,125.1 2,880.5 3,408.4 3,948.4

Plus: Depreciation Expense 2,140.1 1,824.6 1,824.6 1,824.6

Less: CAPEX (5,068.5) (5,271.2) (5,455.7) (5,619.4)

Less: Change in working capital (1,861.3) 903.0 992.2 1,670.6

Free Cash Flow (FCF) (1,664.6) 336.9 769.5 1,824.1

WACC 18.2%

Present Value (PV) of FCF (1,408.7) 285.1 651.2 1,543.7

Perpetual growth rate FY 2015 FY 2016 FY 2017 FY 2018

Terminal Value 38,538.5

Present Value of terminal value 32,613.4

DCF CalculationPV of explicit period

PV of terminal value

Enterprise Value

+ Cash

- Borrowings

Equity Value

Share price

Shares outstanding ('000)

13.45

3,783.3

32,613.4

33,879.3

4,435.2

12,553.3

50,867.8

Valuation

1,265.9

UNILEVER NIGERIA PLC

Important Notice

This document is issued by Financial Derivatives Company. It is for information purposes only. It does not constitute any offer, recommendation or solicitation to any person to enter

into any transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of likely future movements in rates or prices or any representation that

any such future movements will not exceed those shown in any illustration. All rates and figures appearing are for illustrative purposes. You are advised to make your own independ-

ent judgment with respect to any matter contained herein.

© 2016. “This publication is for private circulation only. Any other use or publication without the prior express consent of Financial Derivatives Company Limited is prohibited.”