fcpa risk management - wild apricot · baker hughes fcpa due diligence ... baker hughes fcpa due...

TRANSCRIPT

FCPA Risk Managementfor

Customs Brokerage in Context of Freight Forwarding

1

Greater Houston Business Ethics RoundtableHouston, TexasSeptember 20, 2012

Ronald T. SponbergSenior Counsel, Corporate Compliance

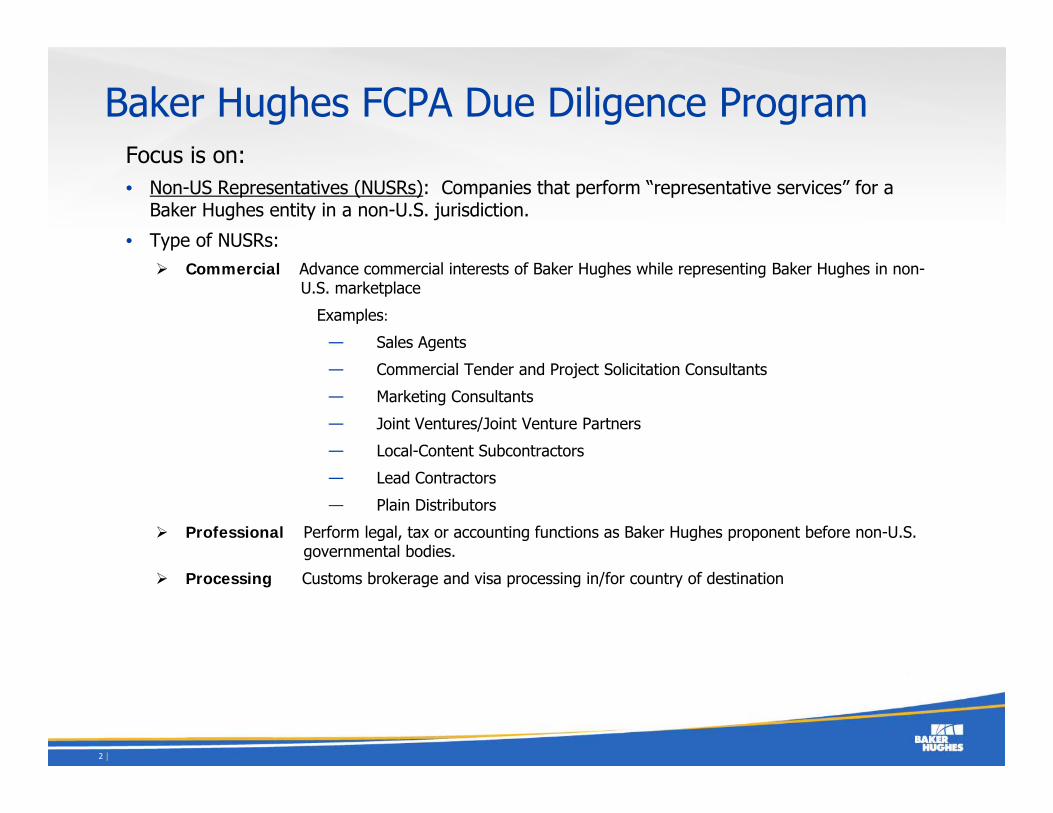

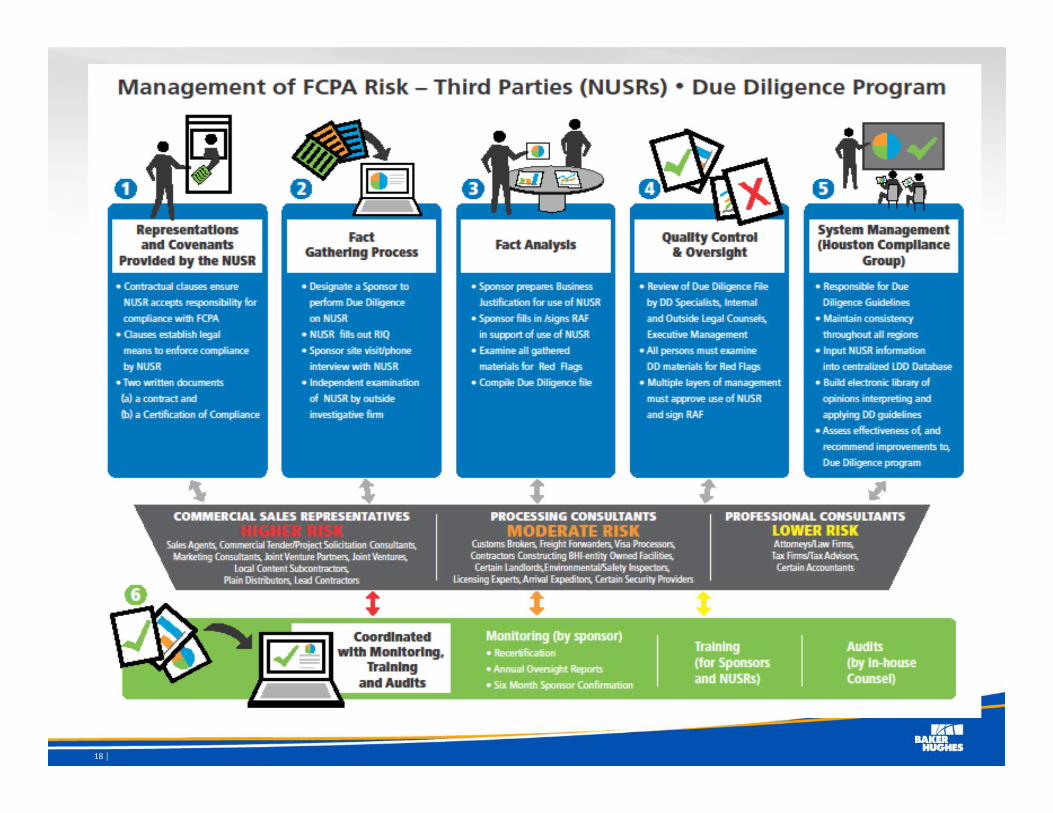

Baker Hughes FCPA Due Diligence ProgramFocus is on:• Non-US Representatives (NUSRs): Companies that perform “representative services” for a

Baker Hughes entity in a non-U.S. jurisdiction.

• Type of NUSRs:Commercial Advance commercial interests of Baker Hughes while representing Baker Hughes in non-

U.S. marketplace

Examples:

— Sales Agents

— Commercial Tender and Project Solicitation Consultants

— Marketing Consultants

— Joint Ventures/Joint Venture Partners

— Local-Content Subcontractors

— Lead Contractors

— Plain Distributors

Professional Perform legal, tax or accounting functions as Baker Hughes proponent before non-U.S. governmental bodies.

Processing Customs brokerage and visa processing in/for country of destination

2

Baker Hughes FCPA Due Diligence Program

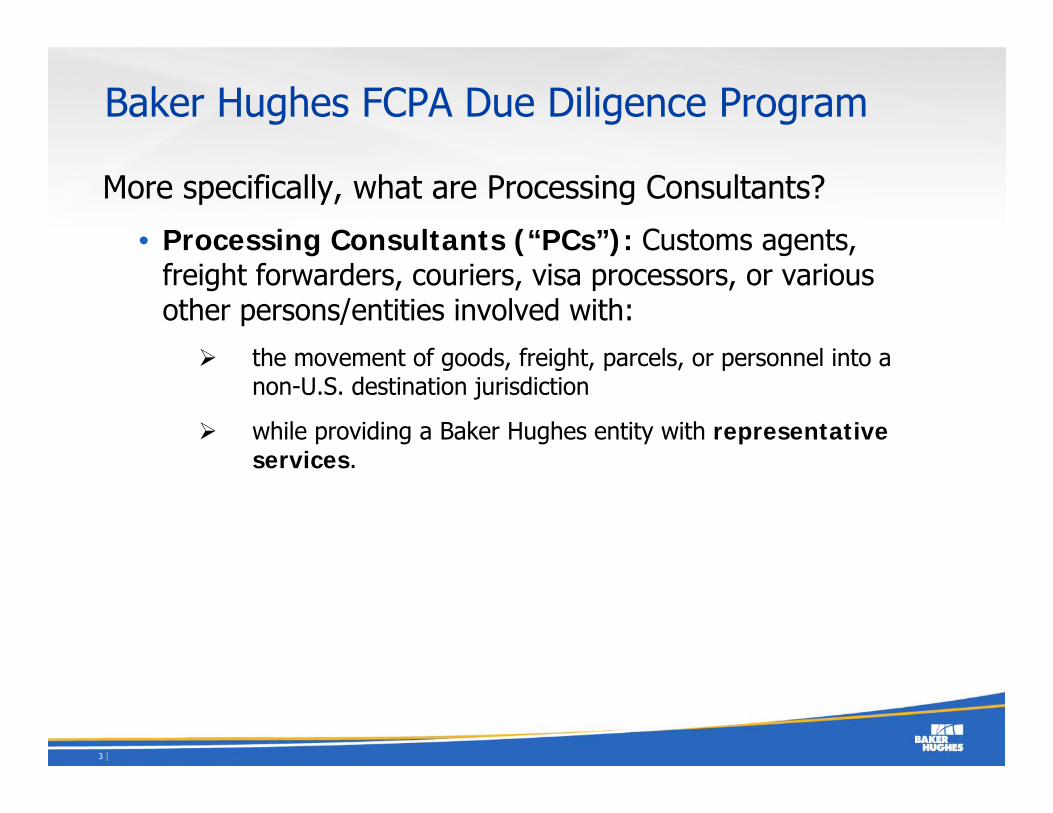

More specifically, what are Processing Consultants?

• Processing Consultants (“PCs”): Customs agents, freight forwarders, couriers, visa processors, or various other persons/entities involved with:

the movement of goods, freight, parcels, or personnel into a non-U.S. destination jurisdiction

while providing a Baker Hughes entity with representative services.

3

Baker Hughes FCPA Due Diligence Program

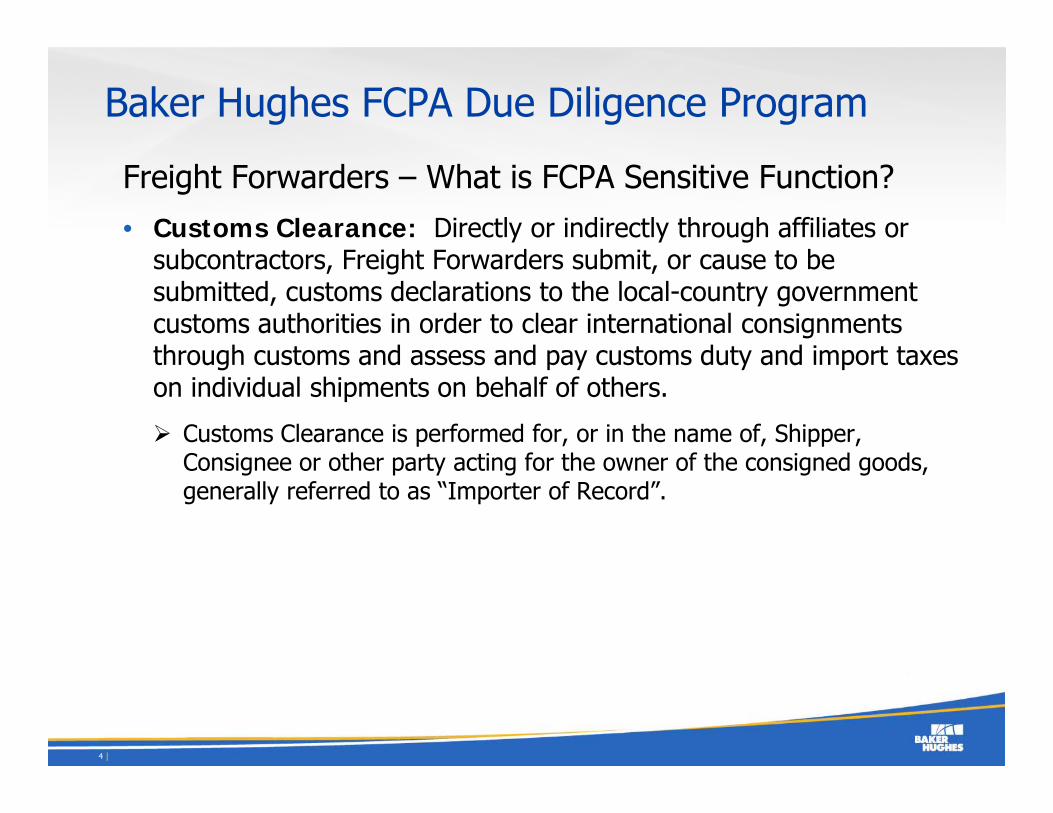

Freight Forwarders – What is FCPA Sensitive Function?• Customs Clearance: Directly or indirectly through affiliates or

subcontractors, Freight Forwarders submit, or cause to be submitted, customs declarations to the local-country government customs authorities in order to clear international consignments through customs and assess and pay customs duty and import taxes on individual shipments on behalf of others.

Customs Clearance is performed for, or in the name of, Shipper, Consignee or other party acting for the owner of the consigned goods, generally referred to as “Importer of Record”.

4

Baker Hughes FCPA Due Diligence ProgramChallenges in Managing FCPA Risk in Context of Freight Forwarding• Large number of regional or country-level Freight Forwarders

• Delivery of freight to many different and sometimes unanticipated ports of entry into destination country

Shipper may not have pre-approved customs agent in all ports.

• Customs clearance ability of Freight Forwarder may vary by type of freight.

Bulk freight

Specialized chemicals

Dangerous goods

• Prior to transportation, uncertain if customs clearance will be handled by Freight Forwarder in-house or outsourced by Freight Forwarder to a subcontractor

• When customs clearance is outsourced, no way to know in advance which local customs broker may be selected by Freight Forwarder

• Sometimes, Shipper does not know in advance if it will directly arrange for customs clearance or instruct Freight Forwarder to handle customs clearance on behalf of Shipper.

5

Baker Hughes FCPA Due Diligence Program

Fundamental Dilemma in Managing FCPA Risk in Context of Freight Forwarders Handling Customs Clearance

• Impractical to perform FCPA Due Diligence on all customs brokers utilized to clear Shipper’s (Importer of Record) goods through customs.

• Too disruptive to intervene in the selection/use of customs brokers by Freight Forwarders.

6

Baker Hughes FCPA Due Diligence Program

FCPA Risk Management Method for Freight Forwarders

• Substantially reduce number of Freight Forwarders

• In most instances, require the use of pre-selected large international Freight Forwarders

• Require pre-selected international Freight Forwarders to qualify as Global Processing Consultants

7

Baker Hughes FCPA Due Diligence Program

Qualifications for Global Freight Forwarders• Pass pre-screening for operational/compliance performance;

Logistics/Operations driven process

Financial status

Operational reputation

Experience on selected trade routes

Price competitiveness

Internal compliance program

• Sign Master Framework Agreement;

• Become certified under Baker Hughes’ Global Due Diligence Program.

8

Baker Hughes FCPA Due Diligence Program

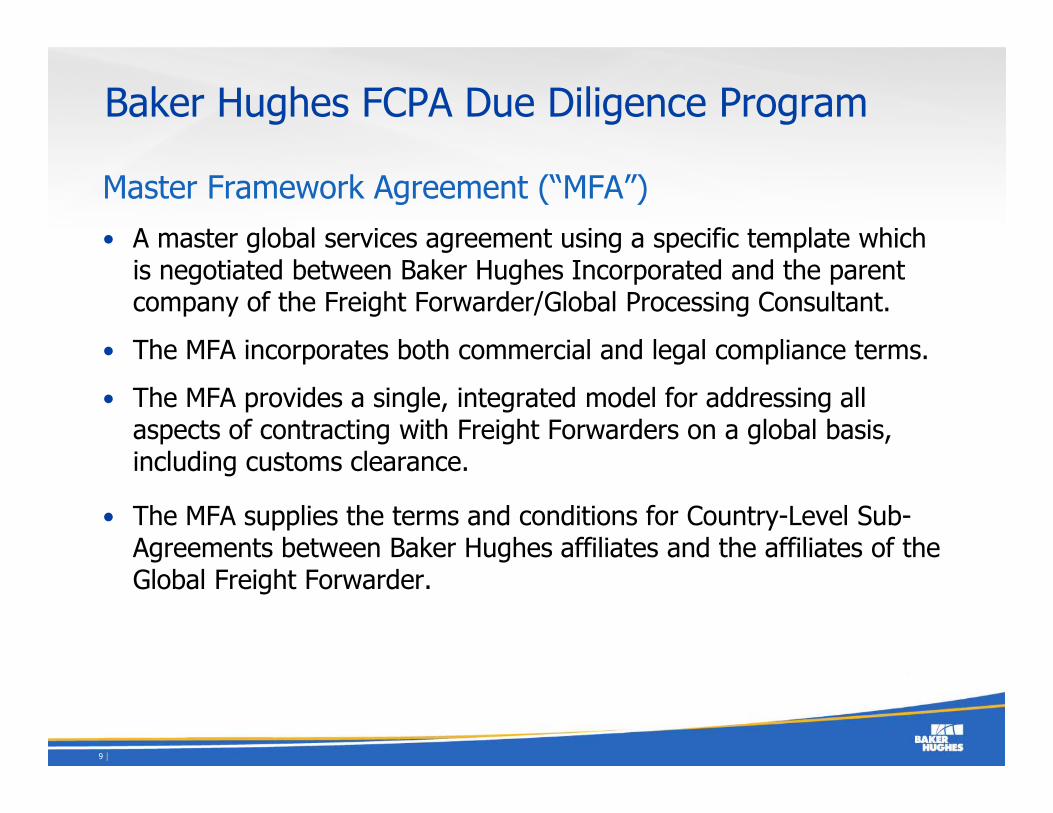

Master Framework Agreement (“MFA”)• A master global services agreement using a specific template which

is negotiated between Baker Hughes Incorporated and the parent company of the Freight Forwarder/Global Processing Consultant.

• The MFA incorporates both commercial and legal compliance terms.

• The MFA provides a single, integrated model for addressing all aspects of contracting with Freight Forwarders on a global basis, including customs clearance.

• The MFA supplies the terms and conditions for Country-Level Sub-Agreements between Baker Hughes affiliates and the affiliates of the Global Freight Forwarder.

9

Baker Hughes FCPA Due Diligence Program

STRUCTURE OF MASTER FRAMEWORK AGREEMENT

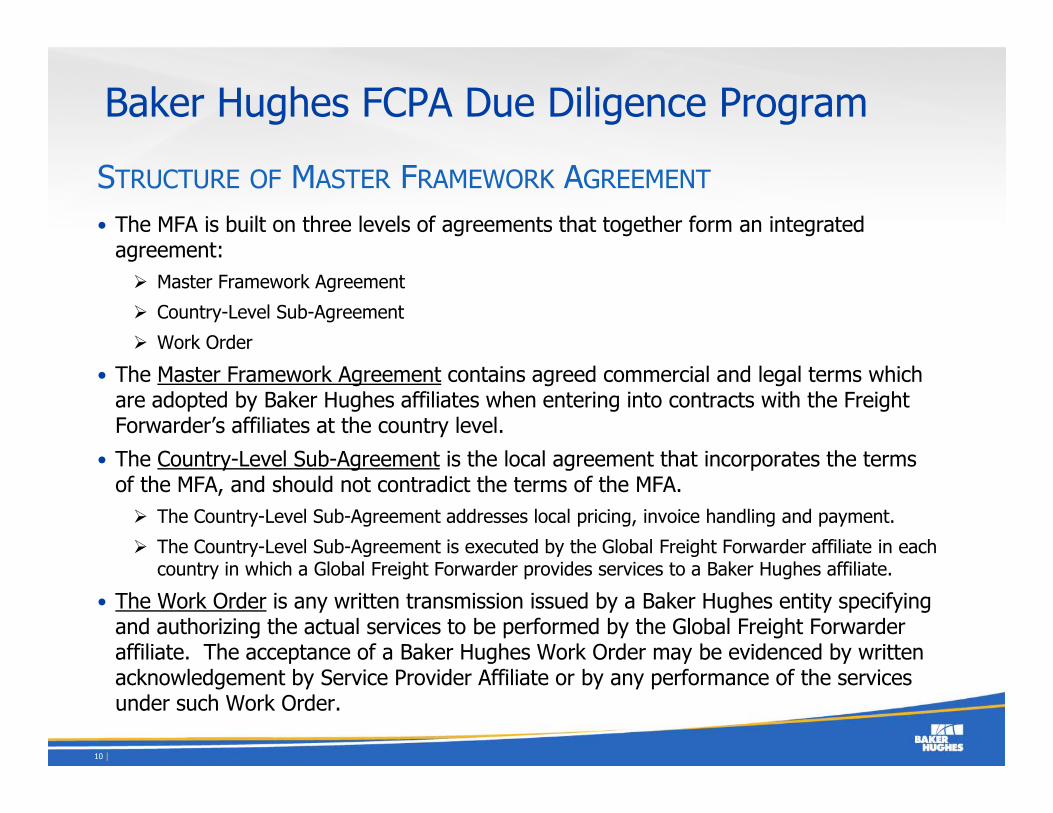

• The MFA is built on three levels of agreements that together form an integrated agreement:

Master Framework Agreement

Country-Level Sub-Agreement

Work Order

• The Master Framework Agreement contains agreed commercial and legal terms which are adopted by Baker Hughes affiliates when entering into contracts with the Freight Forwarder’s affiliates at the country level.

• The Country-Level Sub-Agreement is the local agreement that incorporates the terms of the MFA, and should not contradict the terms of the MFA.

The Country-Level Sub-Agreement addresses local pricing, invoice handling and payment.

The Country-Level Sub-Agreement is executed by the Global Freight Forwarder affiliate in each country in which a Global Freight Forwarder provides services to a Baker Hughes affiliate.

• The Work Order is any written transmission issued by a Baker Hughes entity specifying and authorizing the actual services to be performed by the Global Freight Forwarder affiliate. The acceptance of a Baker Hughes Work Order may be evidenced by written acknowledgement by Service Provider Affiliate or by any performance of the services under such Work Order.

10

Baker Hughes FCPA Due Diligence Program

KEY CONCEPT OF MFA

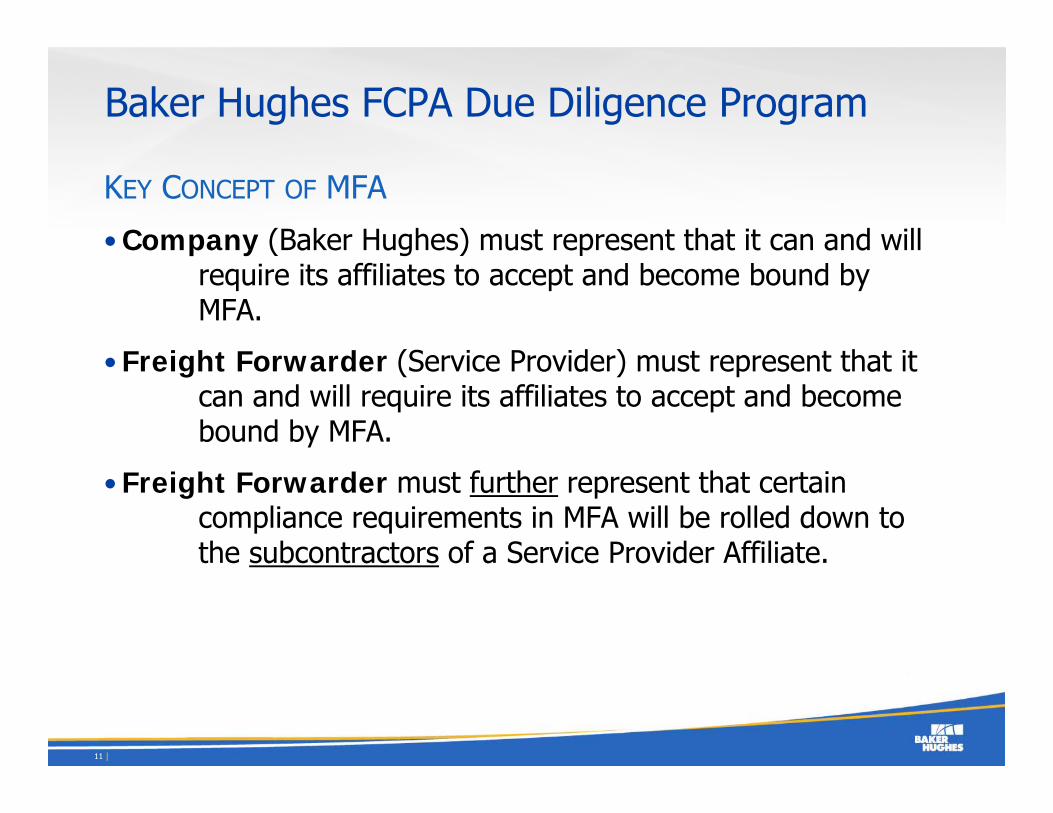

• Company (Baker Hughes) must represent that it can and will require its affiliates to accept and become bound by MFA.

• Freight Forwarder (Service Provider) must represent that it can and will require its affiliates to accept and become bound by MFA.

• Freight Forwarder must further represent that certain compliance requirements in MFA will be rolled down to the subcontractors of a Service Provider Affiliate.

11

Baker Hughes FCPA Due Diligence Program

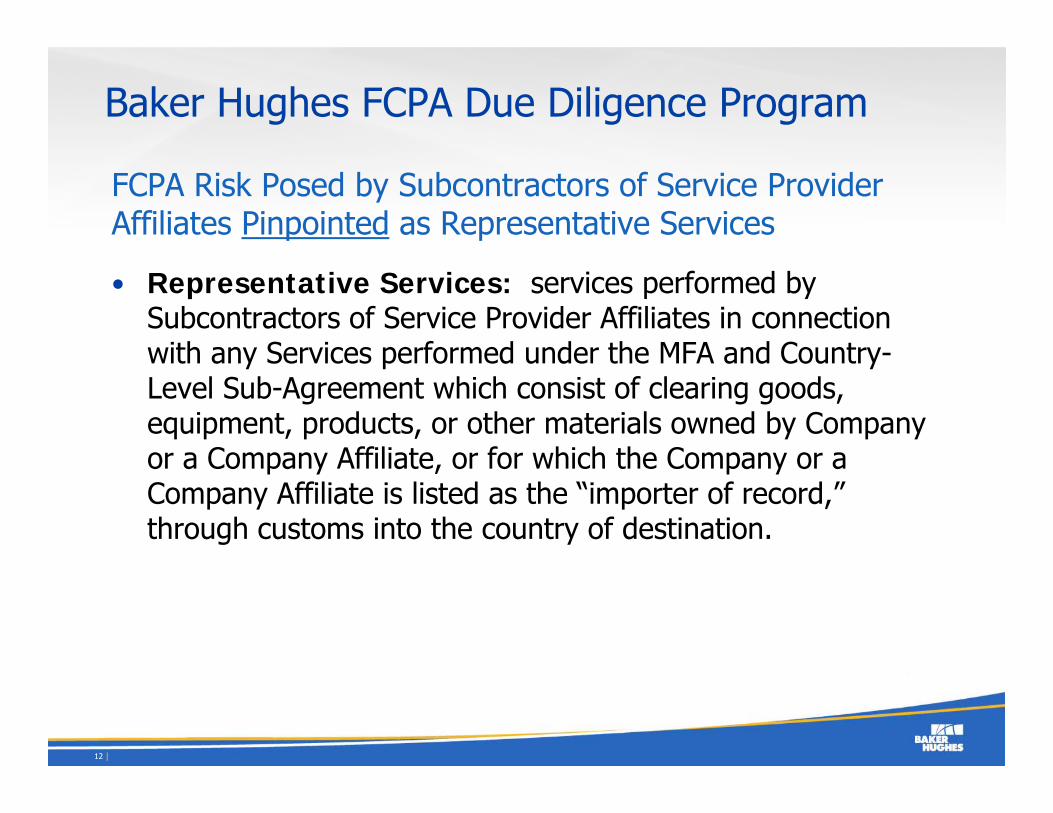

FCPA Risk Posed by Subcontractors of Service Provider Affiliates Pinpointed as Representative Services

• Representative Services: services performed by Subcontractors of Service Provider Affiliates in connection with any Services performed under the MFA and Country-Level Sub-Agreement which consist of clearing goods, equipment, products, or other materials owned by Company or a Company Affiliate, or for which the Company or a Company Affiliate is listed as the “importer of record,” through customs into the country of destination.

12

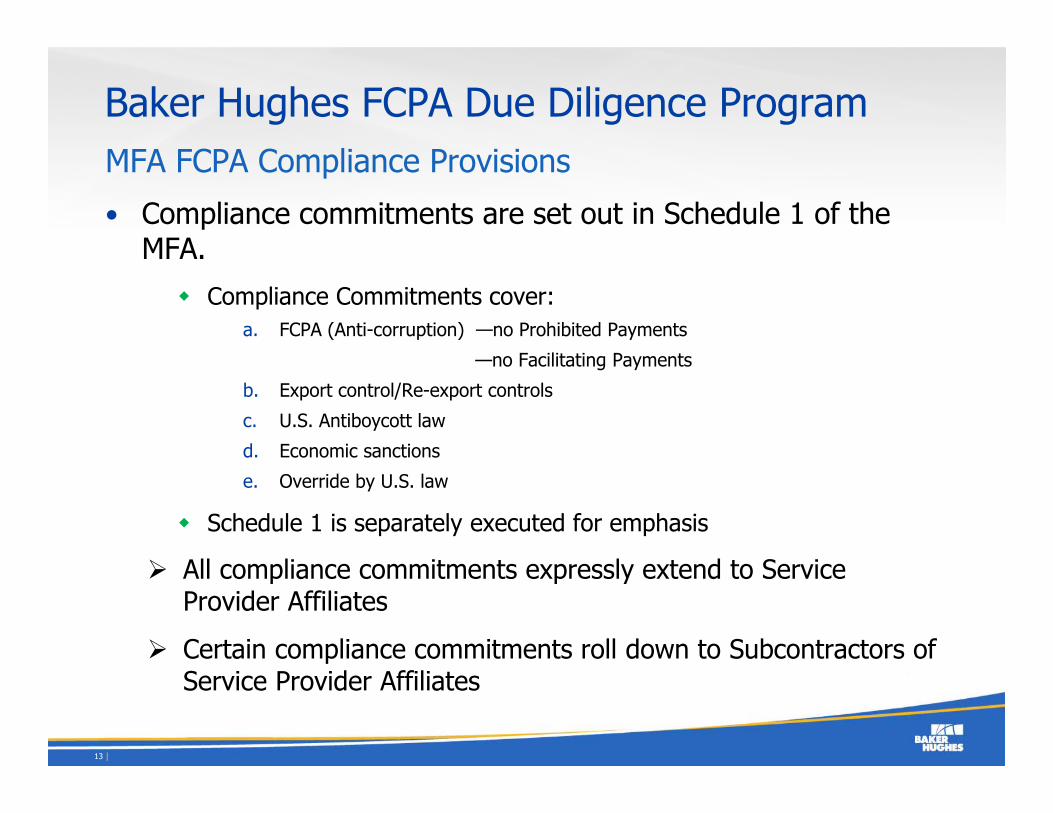

Baker Hughes FCPA Due Diligence ProgramMFA FCPA Compliance Provisions

• Compliance commitments are set out in Schedule 1 of the MFA.

Compliance Commitments cover:a. FCPA (Anti-corruption) —no Prohibited Payments

—no Facilitating Payments

b. Export control/Re-export controls

c. U.S. Antiboycott law

d. Economic sanctions

e. Override by U.S. law

Schedule 1 is separately executed for emphasis

All compliance commitments expressly extend to Service Provider Affiliates

Certain compliance commitments roll down to Subcontractors of Service Provider Affiliates

13

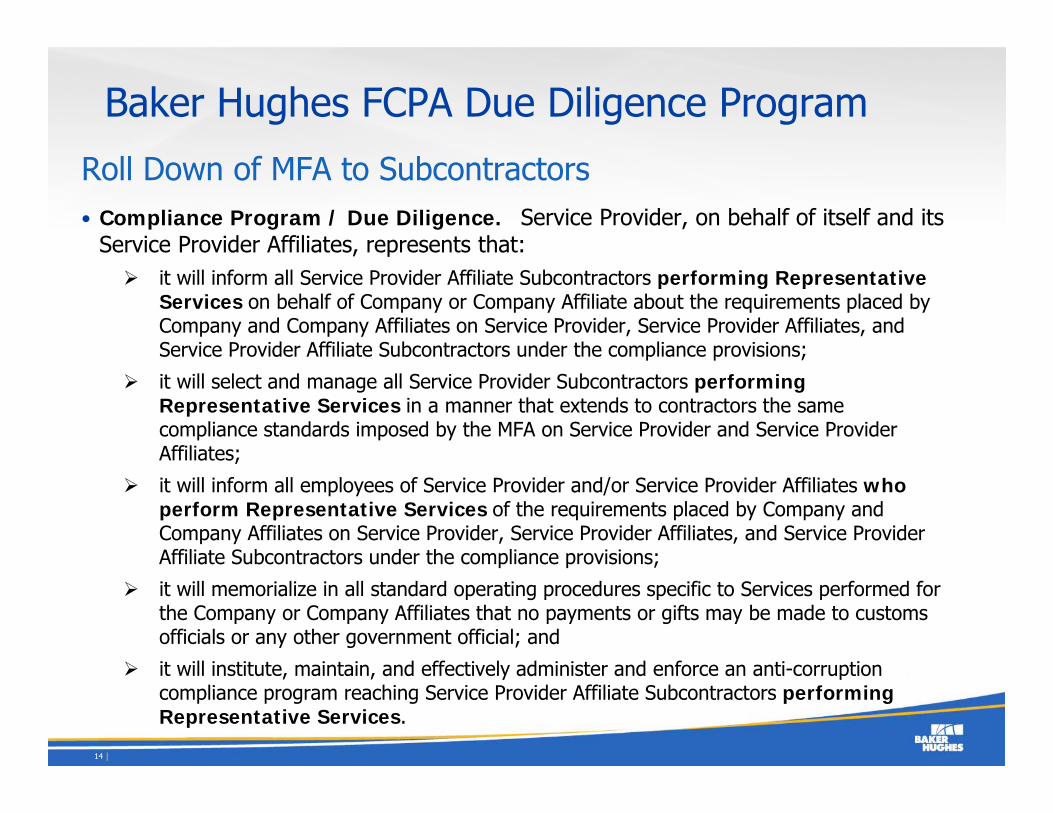

Baker Hughes FCPA Due Diligence Program

Roll Down of MFA to Subcontractors• Compliance Program / Due Diligence. Service Provider, on behalf of itself and its

Service Provider Affiliates, represents that: it will inform all Service Provider Affiliate Subcontractors performing Representative Services on behalf of Company or Company Affiliate about the requirements placed by Company and Company Affiliates on Service Provider, Service Provider Affiliates, and Service Provider Affiliate Subcontractors under the compliance provisions;

it will select and manage all Service Provider Subcontractors performing Representative Services in a manner that extends to contractors the same compliance standards imposed by the MFA on Service Provider and Service Provider Affiliates;

it will inform all employees of Service Provider and/or Service Provider Affiliates who perform Representative Services of the requirements placed by Company and Company Affiliates on Service Provider, Service Provider Affiliates, and Service Provider Affiliate Subcontractors under the compliance provisions;

it will memorialize in all standard operating procedures specific to Services performed for the Company or Company Affiliates that no payments or gifts may be made to customs officials or any other government official; and

it will institute, maintain, and effectively administer and enforce an anti-corruption compliance program reaching Service Provider Affiliate Subcontractors performing Representative Services.

14

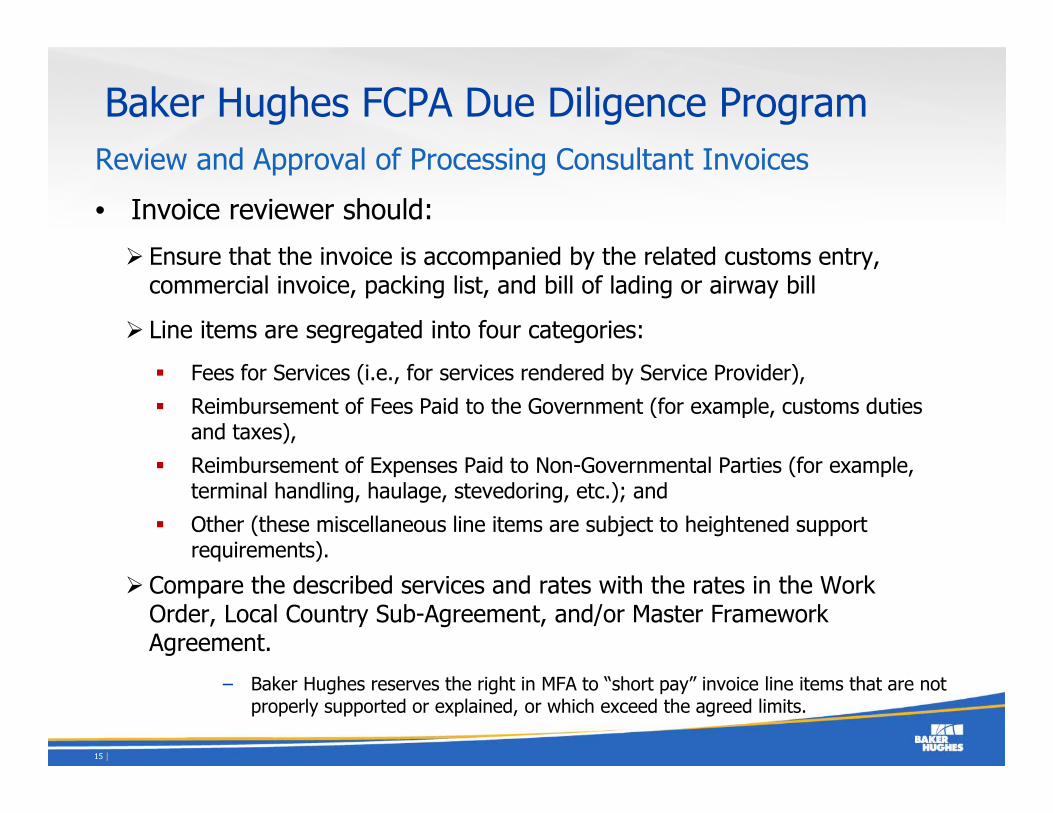

Baker Hughes FCPA Due Diligence ProgramReview and Approval of Processing Consultant Invoices

• Invoice reviewer should:

Ensure that the invoice is accompanied by the related customs entry, commercial invoice, packing list, and bill of lading or airway bill

Line items are segregated into four categories:

Fees for Services (i.e., for services rendered by Service Provider),

Reimbursement of Fees Paid to the Government (for example, customs duties and taxes),

Reimbursement of Expenses Paid to Non-Governmental Parties (for example, terminal handling, haulage, stevedoring, etc.); and

Other (these miscellaneous line items are subject to heightened support requirements).

Compare the described services and rates with the rates in the Work Order, Local Country Sub-Agreement, and/or Master Framework Agreement.

− Baker Hughes reserves the right in MFA to “short pay” invoice line items that are not properly supported or explained, or which exceed the agreed limits.

15

Baker Hughes FCPA Due Diligence Program

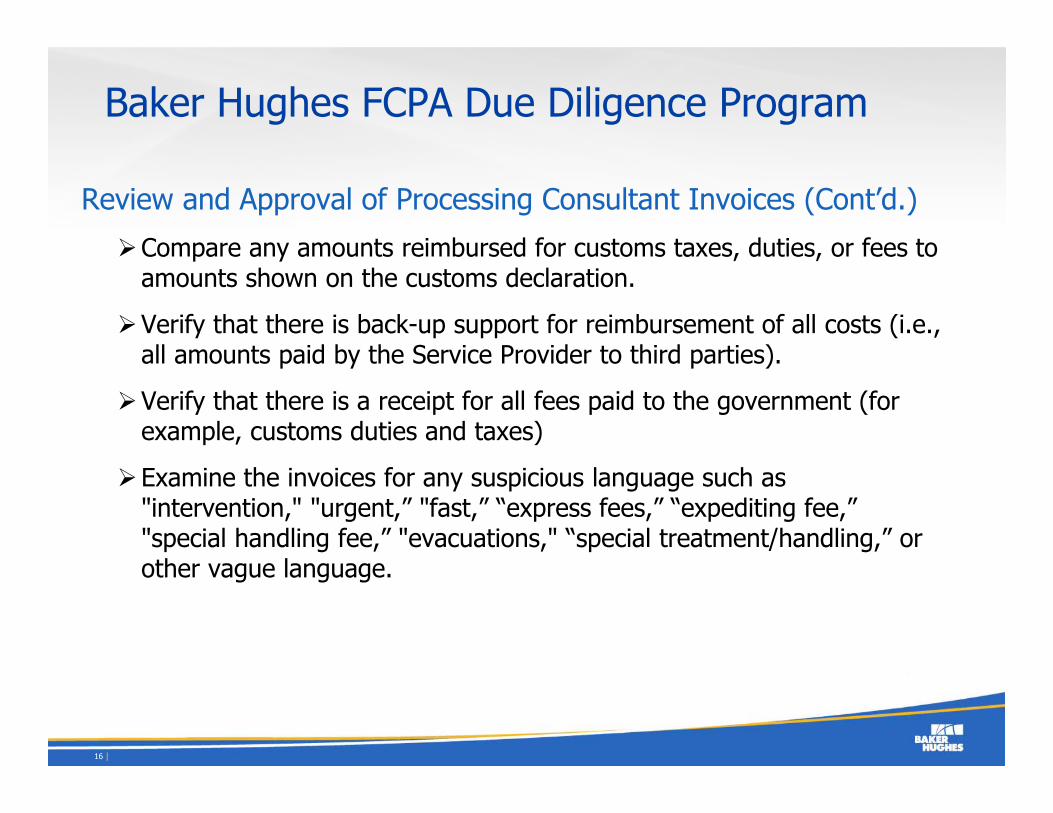

Review and Approval of Processing Consultant Invoices (Cont’d.)

Compare any amounts reimbursed for customs taxes, duties, or fees to amounts shown on the customs declaration.

Verify that there is back-up support for reimbursement of all costs (i.e., all amounts paid by the Service Provider to third parties).

Verify that there is a receipt for all fees paid to the government (for example, customs duties and taxes)

Examine the invoices for any suspicious language such as "intervention," "urgent,” "fast,” “express fees,” “expediting fee,” "special handling fee,” "evacuations," “special treatment/handling,” or other vague language.

16

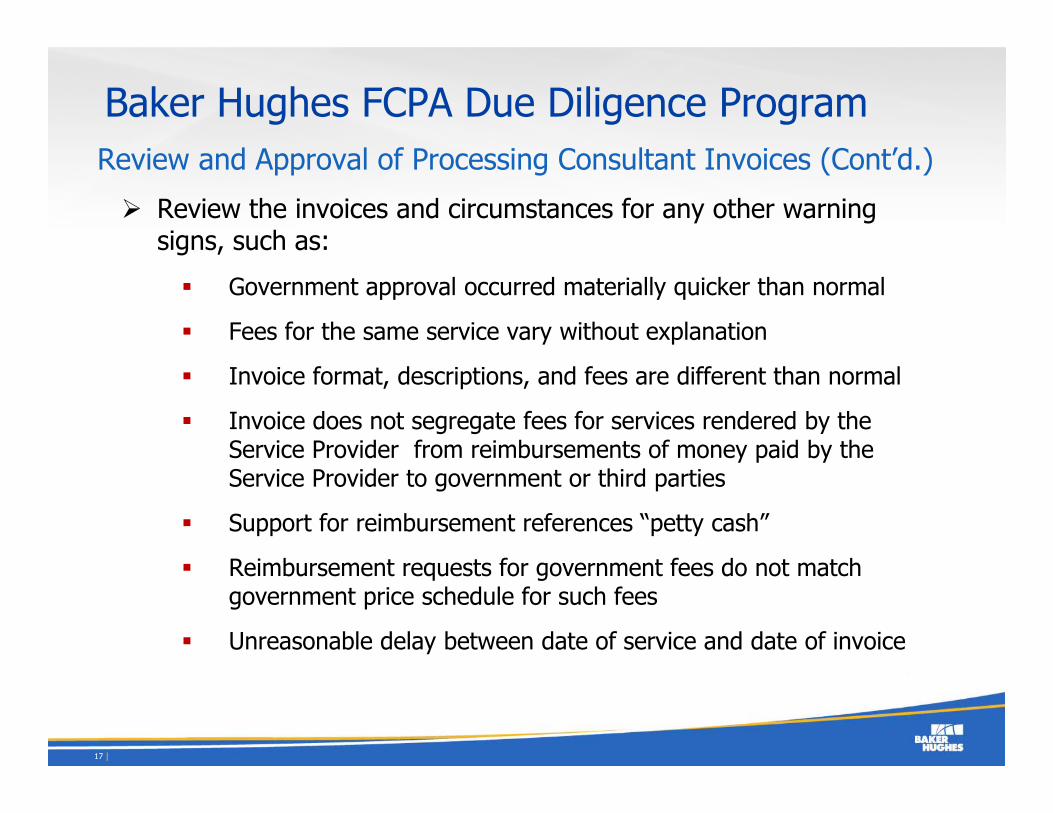

Baker Hughes FCPA Due Diligence ProgramReview and Approval of Processing Consultant Invoices (Cont’d.)

Review the invoices and circumstances for any other warning signs, such as:

Government approval occurred materially quicker than normal

Fees for the same service vary without explanation

Invoice format, descriptions, and fees are different than normal

Invoice does not segregate fees for services rendered by the Service Provider from reimbursements of money paid by the Service Provider to government or third parties

Support for reimbursement references “petty cash”

Reimbursement requests for government fees do not match government price schedule for such fees

Unreasonable delay between date of service and date of invoice

17

18