fbombay stock exchange brokers' forum (bbf) orum | mumbai … ma… · investors and...

TRANSCRIPT

`15/-|MARCH 2020 VOLUME: 8 • ISSUE NO. 12 •|BOMBAY STOCK EXCHANGE BROKERS' FORUM (BBF) MUMBAI, INDIA

FORUM VIEWSWe pray for China's victory against novel coronavirus epidemic

One World One BBF

48

R.N.I. No. MAHENG/2012/47145Postal Registration No. MCS/153/2019-21 • MR/Tech/WPP-355/South/2019-21

st rd thPublished on 1 (Day) of every month • Posted at Patrika Channel Sorting Office, Mumbai - 400001 • Posting date: 3 & 4 of every month

2

UTTAM BAGRI HEMANT MAJETHIA HARIN MEHTA RAJIV CHOKSEYChairman | BBF Vice Chairman | BBF Secretary | BBF Jt. Treasurer | BBF

BCB BrokeragePvt. Ltd.

VenturaSecurities Ltd.

M/S. V. C.Mehta

KRChoksey Shares& Securities Pvt. Ltd.

EXECUTIVE COMMITTEE

GOVERNING BOARD MEMBERS

Anjana Vijay Shah Anup Gupta Cyrus Khambata Hemant Desai Jay Toshniwal Kamlesh JhaveriV.P.L. Shah Share &Securities Pvt. Ltd.

Sykes & RayEquities India Ltd.

PaytmMoney Ltd.

Concept SecuritiesPvt. Ltd.

Toshniwal EquityServices Ltd.

JhaveriSecurities Ltd.

Ketan Marwadi Madhavi Vora Naresh Rana Neeraj Choksi Nirav Gandhi Nithin KamathMarwadi Shares& Finance Ltd.

ULJK SecuritiesPvt. Ltd.

Vishwas FincapServices Pvt. Ltd.

NJ IndiaInvest Pvt. Ltd.

JM FinancialServices Ltd.

ZerodhaSecurities Pvt. Ltd.

Paresh Shah Parth Nyati Pradeep Gupta S. P. Toshniwal Sandeep Nayak Santanu SyamPCS

Securities Ltd.Swastika

Investmart Ltd.Anand Rathi Share

& Stock Brokers Ltd.ProStocks Centrum

Broking Ltd.Angel

Broking Ltd.

Sunil Sarda Vineet Bhatnagar Vivek GuptaSystematix Shares& Stocks India Ltd.

Phillip Capital(India) Pvt. Ltd.

GEPL CapitalPvt. Ltd.

3 FORUM VIEWS - MARCH 2020

BOMBAY STOCK EXCHANGE BROKERS’ FORUM (BBF)GOVERNING BOARD 2019 - 20

KUSHAL A. SHAHJt. Secretary | BBF

RatnakarSecurities Pvt. Ltd.

LALIT MUNDRATreasurer | BBF

Suresh RathiSecurities Pvt. Ltd.

5

Philosophy & Self-Management:A life of purpose40

CEO & COO DESK06

4 FORUM VIEWS - MARCH 2020

Disclaimer: This magazine is meant for information purposes only and does not constitute any opinion or guidelines or recommendation on any course of action to be followed by the reader(s). It is not intended to be used as trading or investment advice by anybody and should not in any way be treated as a recommendation. The information contained in this magazine does not constitute or form part of and should not be construed as, any offer for purchase or sale of any product or service. While the information in the magazine has been compiled from sources believed to be reliable and in good faith, readers may note that the contents thereof including text, graphics, links or other items are provided without warranties of any kind. BSE Brokers' Forum expressly disclaims any warranty as to the accuracy, correctness, reliability, timeliness, merchantability or fitness for any particular purpose, of this magazine. BSE Brokers' Forum shall also not be liable for any damage or loss of any kind, howsoever caused as a result (direct or indirect) of the use of the information or data contained in this magazine. Any alteration, transmission, photocopied distribution in part or in whole or reproduction of any form of this magazine or any part thereof without prior consent of BSE Brokers' Forum is prohibited.

Printed, Published and Edited by Dr. VISPI RUSI BHATHENA, PhD (h.c.)& Dr. V. ADITYA SRINIVAS on behalf of BSE BROKERS' FORUM,

printed at KSHITIJ PRINTERS, 49, Parsi Panchayat Road,Ashok Ind. Estate, 1st, Floor, Andheri (East) Mumbai - 400 069.

and published from BSE BROKERS' FORUM, 808 A,P. J. TOWERS, DALAL STREET, FORT, MUMBAI - 400 001.

Editor: Dr. V. ADITYA SRINIVASDesign by: Harshad Gajera | Photographer: Sanjeev Dubey

BBF Steering CommitteeUttam Bagri (Chairman)

Hemant Majethia (Vice-Chairman)Harin Mehta (Secretary)Lalit Mundra (Treasurer)

Kushal A. Shah (Jt. Secretary)Rajiv Choksey (Jt. Treasurer)

Compliance Calendar March 202024

MAY 2019 CONTEMarch 2020 CONTENTS

Follow us on: @bbfindia /bsebrokersforum/brokersforumofindia /bsebrokers’forum

Write to us:We would be happy to hear from you! Do send in your suggestions, feedback and comments via email to

[email protected] | Visit us: www.brokersforumofindia.com

Present challenges in the domesticand international context16

20 Asia-Pacific Marketsmonthly highlights and insights

12 your questions answered:Financial Planning(National Pension System (NPS))

Circulars 28

Wellness Q&A:Water works41

Healing Institute:Detox in 10 days43

Sabka vishwas (Legacy DisputeResolution) Scheme, 201932

Digital payment systems in india:opportunities and challenges35

Regulatory Pulse 26

Budget 2020: Incentives andconcessions to internationalFinancial services centre (ifsc)

34

Seminars & Events conducted by BBF for theprogress of stakeholders of Capital MarketsJanuary - February 2020

42

The effects of dispersion in carbonintensity scores on carbon-efficientportfolio construction

18

14 your questions answered:Is registration underMSME advantageous?

Digital lendingan emerging trend38

08nd

2 Global Connects:India Investment OpportunityJapan 2020

6 FORUM VIEWS - MARCH 2020

ceo & coo message

WelcomeDr. Vispi RusiBhathena,PhD (h.c.)

to magazine.Forum Views

Indian markets witness roller coaster ride on the budget day and post trading days with the markets crashing by 1000 points on the budget day and then recovering within next two trading sessions. The budget was the key driver for the volatility of the markets. The various provisions of the budget especially related to the income tax slab rates gives the taxpayers options to invest in Section 80C and continue with the old rates. If they forego 80C investment, then go with the new slab rates. This created some panic among the financial stocks since their business may take marginal hit. The budget gave lots of fund allocation to various sector and aims to increase ease of doing business.

Dr. Aditya Srinivas

BBF - Social Responsibility Initiatives | Blood Donation

Camp at S.R. Luthra Institute of Management | Surat,

Gujarat

China has reduced travel and has shut its public places. This slows down the China GDP and thus in turn the world economy, as China accounts for 9.3 %

The world economy has also taken hit due to the coronavirus threat which has originated from China and has spread to around 23 countries in the world. The world economy is likely to witness slowdown as

contribution in the world GDP.

RBI as expected kept the Repo rate unchanged at 5.15% in fact, the RBI monetary policy focussed on giving push to Auto sector, Commercial Real Estate and MSME sector by allowing

banks to lend them without counting that amount in CRR (Cash Reserve Ratio). The retail inflation has reached to 7.35% which is way above the RBI target inflation base of 4% (+-2%). This leaves little room for the RBI to reduce the interest rates in a already slowing economy.

The key question in the economy is witnessing lack of demand which is attributed to various factors like less job creation, corporate job losses which has put pressure on the demand side as people are not confident to take housing loan, car loans etc. The percentage of Indian paying taxes are around 4% which creates imbalance when it comes to contribution in the economic growth via taxes being paid.

On the BBF front:

BBF Seminars and Events

TopicDate

Seminar on Portfolio Management /Investment Advisors - Recent RegulatoryDevelopments / ChallengesSeminar on Opportunities at IndiaInternational Exchange

20 Jan

18 Feb

Blood Donation Camp at S.R. Luthra Institute of Management | Surat, Gujarat (January 18, 2020)

Bombay Stock Exchange Brokers'Forum (BBF) | Industry Partner

Post-Event Coverage

7

nd2 GLOBAL CONNECTS

JAPAN 2020

BOMBAY STOCK EXCHANGE BROKERS' FORUM (BBF)

In support with Tokyo, Japan

India Investment Opportunity

20th - 21st January, 2020

8

BOMBAY STOCK EXCHANGE BROKERS' FORUM (BBF)GLOBAL CONNECTS

SUMMARY

Summary of 2nd Global Connects Japan 2020India Investment Opportunity

The Bombay Stock Exchange Brokers Forum (BBF) successfully hosted the 2nd BBF Global Connects India Investment Opportunity at Tokyo, Japan in January 2020. This was in continuation with the positive response received post the BBF Global Connects - South Korea and Japan in Jan - Feb 2019.

The Embassy of India, Japan and Japan Securities Dealers Association (JSDA), the Self Regulatory Organization (SRO) of securities firms in Japan, acted as local support partners for the event. Invest India, National Investment Facilitation Agency, Government of India, acted as the India support partner.

The program was conducted on 20th and 21st of January 2020 at the Vivekanand Culture Centre Auditorium, Embassy of India, Tokyo, Japan. Day 1 (20-Jan) was the public seminar followed by Day 2 (21-Jan) of one to one meeting(s).

The Indian delegation comprised of the marquee names from the Indian Capital Market Industry represented by India International Exchange (IFSC) Limited (INDIA INX), SBI Mutual Fund, Stockholding Corporation of India Limited, Motilal Oswal Financial Services Limited, SMC Global Securities Limited, Invest India and office bearers of BBF.

We had the honour of presence of the Indian capital market regulator, Securities and Exchange Board of India (SEBI) represented by Shri Achal Singh, General Manager, Foreign Portfolio Investors (FPI) & Custodians.

HIGHLIGHTS• The conference was attended by more than 70 participants comprising of banks, sell side and buy side representatives, institutional

investors and securities companies from across Japan covering discussion on India's economic outlook from international perspective, structural changes, and the opportunities presented in Indian markets.

• The galaxy of speakers at the program included H.E. Hon. Shri Sanjay Kumar Verma, Ambassador of India to Japan and representatives from Securities and Exchange Board of India, Financial Services Agency - Japan, Ministry of Finance - Japan, Tokyo Stock Exchange, Daiwa Securities - Japan along with many experts on Indian Markets.

KEY TAKEAWAYS• There is tremendous interest in Investing in India, reinforced by the turnout at the event.• Capital gains tax for foreign investors is acting as a big hurdle for fund accounting. For the same reason, Japanese firms are preferring

investing through SGX, Singapore.• The option of coming in the International Financial Services Centre (IFSC) at Gujarat International Finance Tec-City (GIFT) City along with

option of segregated nominee account structure was very much appreciated. • There seemed to be a lack of awareness on Voluntary Retention Route introduced by Reserve Bank of India last year for foreign investors.• There is a proposal for engagement between exchanges of both jurisdictions to promote listing of ETF’s through India-Japan ETF

Connectivity.• Japanese firm(s) have shown interests towards issuance of Samurai Bonds for Indian corporates.

Going AheadBBF proposes to issue literature from time to time on operational aspects of investing in India in local languages.

We shall continue our endeavors to improve awareness of Investment Opportunities in India in general and Indian Capital Markets in particular across the globe. We are committed to make this an annual event and the 3rd Global Connects Japan is proposed tentatively in Feb 2021.

9

Day 1 - Monday, 20 January 2020

Day 2 - Tuesday, 21 January 2020

Timings Particulars

10:00 - 2.00 pm One-on-one Meetings

(by appointment)

Entities/ Persons Venue

Indian Delegation Indian Embassy

Timings Particulars Entities/ Persons Venue

Meeting Rooms at

Indian Embassy

VCC Auditorium,

Embassy of India,

Tokyo

Indian Embassy

09:30 - 11:30 am

01:00 - 1:30 pm

01:30 - 01:40 pm

01:40 - 01:45 pm

01:45 - 2:00 pm

02:00 - 3:10 pm

03:10 - 3:20 pm

03:20 - 4:30 pm

04:30 - 5:40 pm

05:40 - 5:50 pm

06:00 pm onwards

One-on-one Meetings

(by appointment)

Registrations & Welcome

Welcome Remarks

Opening Remarks

Presentation

Panel Discussion 1

Economy and Markets

Session chair - Navneet Munot

Chief Investment Officer

SBI Mutual Fund

Networking Break

Panel Discussion 2

Investment Opportunities in India

Session chair - V Bala

MD & CEO, India International

Exchange (IFSC) Limited (India INX)

Panel Discussion 3

Facilitation and Regulation

Session chair - Hideaki Imamura |

Director, Research Division,

International Bureau,

Ministry of Finance, Japan

Closing Remarks

Networking Dinner

Indian Delegation

-

Uttam Bagri | Chairman, BBF

Mario Takeno | Vice-Chairman, JSDA

Sanjay Kumar Verma | Ambassador,

Embassy of India, Tokyo

Achal Singh | General Manager,

Securities and Exchange Board of India

V Bala | MD & CEO, India International

Exchange (IFSC) Limited (India INX)

Dr. Satya Pal Kumar | First Secretary

(Trade) Embassy of India, Tokyo

Vineet Potnis | Head Business

Development - Custody, StockHolding

Navneet Munot | CIO, SBI Mutual Fund

Ion Mizuno | Director, Head of APAC &

South Asia, International Debt Origination

Daiwa Securities Co. Ltd.

Prerna Soni | Sr. AVP, Invest India

So Hirai | Deputy Director,

International Affairs Office, Financial

Services Agency (FSA)

Achal Singh | General Manager,

Securities and Exchange Board of India

Ryo Takagi | Head-Global Strategy

Hemant Majethia | Vice Chairman, BBF

Japan Exchange Group, INC

R Anand | Vice President, StockHolding

Mona Khandhar | Minister (Economic

& Commerce), Embassy of India, Tokyo

BOMBAY STOCK EXCHANGE BROKERS' FORUM (BBF)GLOBAL CONNECTS

PROGRAM FLOW

Program Flow

10

BOMBAY STOCK EXCHANGE BROKERS' FORUM (BBF)GLOBAL CONNECTS

GLIMPSES

Glimpses of India Investment Opportunity

2nd Global Connects Japan 2020

Interaction of Indian Delegation with Mona Khandhar | Minister (Economic & Commerce),Embassy of India, Tokyo and Bhagirathi Behera | First Secretary (Eco), Embassy of India, Tokyo

H.E. Shri Sanjay Kumar Verma,Ambassador, Embassy of India,Tokyo delivering Opening Remarks

Shri Achal Singh, General Manager,Securities and Exchange Board ofIndia during key note presentation

Panel - 1 Economy and Markets Panel 2 - Investment Opportunities in India

Panel 3 - Facilitation and Regulation

11

12 FORUM VIEWS - MARCH 2020

AYUSH AGGARWALCIO (Chief Investment Officer)SMC Private Wealth

Among all the retirement investment options like EPF,

PPF, NPS or Mutual Fund; NPS is the only option which provides

a disciplined and long term investment approach as other retirement investment options

can be 100% withdrawn before the retirement age.

FINANCIAL PLANNING (NATIONAL PENSION SYSTEM (NPS))

5. What are the investment choices available to NPS account holder?The NPS offers two approaches to invest subscriber’s money. Subscriber has a liberty to select any of the two below mentioned approach:

• Active choice - Individual Funds • Auto Choice – Life Cycle Fund

In Active Choice, subscriber has an option to actively decide as to how his NPS pension wealth is to be diversified among Equities, Government securities, Fixed Income securities other than Government securities and Alternative Investment Schemes including instrument like CMBS, MBS, REITS, AIFs, InvIts etc. However the maximum allocation to equities and alternatives are 75% & 5% respectively.

While in Auto Choice, according to the age of the subscriber a predefined portfolio has been constructed by the PFRDA. Below mentioned three life cycle funds are available under this Auto Choice:

Number (PRAN) is issued by Government of India to each subscriber.

There are two types of account NPS offers i.e. Tier I & Tier II, Tier I account is a default account with the objective for retirement saving. However, the Tier II account is a voluntary savings account and one cannot open Tier II without opening Tier I account.

4. How many types of NPS accounts PFRDA offers?

Particulars

Status

Withdrawals

Tax exemption

Minimum NPS contribution

Maximum NPS contribution

NPS Tier-IAccountDefault

Not permitted

Up to Rs 2 lakh p.a.

(Under 80C and 80CCD)

Rs 500 or Rs 1,000 p.a.

No limit

NPS Tier-IIAccountVoluntary

Permitted

None

Rs 250

No limit

1. What is National Pension System (NPS)?National Pension System (NPS) is a pension cum investment scheme launched by Government of India to provide old age security to Citizens of India. PFRDA launched National Pension Scheme “NPS” in the year 2004. Initially NPS was introduced to new government employees (except armed forces), whereas from 2009 it was opened for all Indian citizen to get benefits on voluntary basis.

2. How NPS works?

3. Who can subscribe to NPS?

In NPS, the contributions of the subscribers are pooled into pension funds which are invested by the PFRDA regulated professional fund managers as per the guidelines issued by the PFRDA. Professional fund managers invest in the diversified portfolios which are mix of Equities, Government securities, Fixed Income securities other than Government securities and Alternative Investment Schemes including instrument like CMBS, MBS, REITS, AIFs, InvIts etc. LIC, SBI, UTI, HDFC, ICICI Kotak, Reliance and Aditya Birla are some of the PFRDA regulated professional fund managers for NPS.

Any citizen whether a resident or NRI within the age group of 18 to 65 years can open a NPS account. NPS account is opened for the Subscriber and unique Permanent Retirement Account

13 FORUM VIEWS - MARCH 2020

Ayush Aggarwal is the CIO (Chief Investment Officer) at SMC Private Wealth and a Director at SMC Group. His opinions are carried out by prominent business channels like CNBC Awaaz. His articles have also been published by reputed groups like economictimes.com. He is also known for his knack of identifying high potential as well as fundamentally strong companies. HNI clients at SMC have gained significantly from the practical and far sighted approach of Ayush.

He is an avid reader and his love for reading keeps him abreast with latest happenings in financial sector. A graduate from the prestigious Delhi University, He is also an MBA from S.P. Jain Institute of Management and Research, Mumbai.

Investment NPS ELSS PPF FD

Lock-in period

Risk Profile

Expected Returns

Charges

Asset AllocationMixTaxation atMaturityPrematureWithdrawal

TillretirementRelativelyLowAs perMarketLow

Yes

LumpsumTaxfreeYes

3 years

High

As perMarketRelativelyHighNo

LTCG@10%No

15 years

Risk-free

Fixed

N.A

No

Taxfree

Yes

5 Years

Risk-free

Fixed

N.A

No

Taxable

Yes

Vesting Age < 60 years Vesting Age = 60 years

• Up to 20% of Corpus can be withdrawn in lump sum

• Balance amount to be invested in Annuity

• If the Corpus is <= 1 lakh, entire amount can be withdrawn in lump sum

• Up to 60% of Corpus can be withdrawn in lump sum

• Balance amount to be invested in Annuity

• If the Corpus is <= 2 lakh, entire amount can be withdrawn in lump sum

7. Are there any income tax benefits while contributing to NPS?

8. Can onepartially withdraw from NPS in between?

Yes, another benefit for opting NPS is taxation; it allows investors to avail tax benefit of INR 50000 under section 80 CCD (1B) which is over and above INR 1.5 Lakh under section 80 C. Apart from 80 CCD (IB) benefit, in case of salaried investor, contribution by the employer to the extent of 10% of the salary (Basic and Dearness Allowance) is also exempt from taxable income of the employee under section 80CCD (2) of Income Tax Act, 1961.

Yes, upto 25% of the contribution made by the subscriber as on date of application of withdrawal can be withdrawn.It is allowed after 3 years from the date of opening of NPS account. Please note that there are only three partial withdrawals allowed during the tenure and that too for specific purposes like Higher Education, Child’s marriage, buying home or treatment of Critical illnesses etc.

10. What would be the tax treatment at the time of withdrawal?

11 Why NPS is important?

Redemption of 60% accumulated corpus in the Tier I account of NPS is fully tax-free, however the annuity received from rest 40% amount of investment in annuity plan would be taxable as per income slab of the investors. Taxable annuity is the only drawback of this product.

All the investment and redemption tax benefits are available only in Tier I account and Tier II account is treated as income.

Retirement planning is one of the most important parts of financial plan. A well structure retirement plan ensures that a person proudly lives self dependent without compromising on their standard of living during advancing years. With the given understanding, government of India established Pension Fund Regulatory and Development Authority “PFRDA” to develop and regulate pension sector. NPS is so flexible and offers a range of investment options and choice of Pension Funds (PFs) for planning the growth of the investments in a reasonable manner and monitor the growth of the pension corpus. Subscribers can switch over from one investment option to another or from one fund manager to another.

An investor can consider NPS as one of the best options available in the market for retirement planning as it provides additional tax benefit, low cost, simple, portable and well regulated. Apart from this, it also gives a mix of asset allocation choice according to the risk profile of the investor. There is no doubt that the NPS has a capability to generate better returns as compared to any other retirement investment options in the long term. NPS is transparent and cost effective wherein the subscriber would be able to know the value of the investment on day to day basis. The ultra low-cost structure of the scheme makes it an ideal vehicle for long-term savings.

• LC75 - Aggressive Life Cycle Fund: In this Life Cycle Fund, the exposure in Equity Investments starts with 75% till age 35 and gradually reduces as per the age of the subscriber.

• LC50- Moderate Life Cycle Fund: In this Life Cycle Fund, the exposure in Equity Investments starts with 50% till age 35 and gradually reduces as per the age of the subscriber.

• LC25 - Conservative life cycle fund: In this Life Cycle Fund, the exposure in Equity Investments starts with 25% till age 35 and gradually reduces as per the age of the subscriber.

The default auto choice if the subscriber is not choosing any of the above option is Moderate life Cycle Fund.

Among all the retirement investment options like EPF, PPF, NPS or Mutual Fund; NPS is the only option which provides a disciplined and long term investment approach as other retirement investment options can be 100% withdrawn before the retirement age. However in case of NPS only an investor can withdraw 60% of the accumulated corpus in Tier I account of NPS after attaining 60 years of age and rest 40% of the corpus should be utilise to buy an annuity plan.

6. How one can compare NPS with other Investment Options?

9. When one can exit from NPS?Subscriber can exit from the Scheme after 10 years of account opening or attainment of 60 years of age whichever comes first.

15 FORUM VIEWS - MARCH 2020

7. Exclusive purchases and sheltering from competition:

8. Market assistance from the government and Export Promotion:

As part of the MSME Market Development Assistance scheme, the Central Government follows a Price and Purchase Preference policy under which more than 358 items are listed for exclusive purchases by Central Government from medium, micro and small units only.

The Government of India organizes several exchange programs, craft fairs, exhibitions, and trade-related events internationally. Being categorized as a micro, small or medium enterprise gives access to all of these platforms for international cooperation on trade-related aspects with different countries and fosters new business connections. The government also incentivizes export of goods and services by MSMEs by way of subsidies, tax exemption, and technical support.

avail 50% subsidy for patent registration by making application to respective ministry.

Enterprises that have MSME Registration are eligible for Industrial Promotion Subsidy as may be prescribed by the government in this behalf. Enterprises that have MSME Registration Certificate can avail Concession on electricity bill by making application to electricity department along with MSME Registration Certificate. Since MSMEs is a sector generating employment and giving entrepreneurial ventures a boost, the government also identifies training sectors for MSME and gives capital grants for improvisation of the infrastructure and support for entrepreneurial development.

Enterprises that have MSME Registration Certificate can claim reimbursement of ISO & HACCP Certification expenses by making application to respective authority.

In order to enhance the cost-effectiveness and promote clean energy use in manufacturing, the government reimburses project costs towards these goals for MSME sector units and also expenditure incurred for implementation of clean technology, preparation of audit report and subsidies for licensing products according to national and international standards.

4. Concession in Electricity Bills, Eligible for Industrial Promotion subsidy and Other Capital Grants

5. Reimbursement of ISO Certification charges

6. Technology and quality upgradation support to MSMEs:

Sejal Shah, Advocate• Working as an Advocate in the field of Taxation - Direct & Indirect.

Specialisation in GST. Handling Tax Litigation upto High Court.• Currently working independently after experience at Ramesh M Shah & Co,

Chartered Accountants after completing LL.B. from Government Law College.

• After Completing B. Ed. & M.B.A. a brief stint as an Educationist with Aditya Birla World Academy, Mumbai

• Member of various sub-committees of The Goods and Services Tax Practitioners’ Association of Maharashtra (GSTPAM) and Social commitment- Honorary Secretary at Jain Advocates Federation (JAF).

• Contributor to Beginners’ Book on GST Law to be Published by GSTPAM.• Athlete participating in various marathon runs all across the Country.

14 FORUM VIEWS - MARCH 2020

IS REGISTRATION UNDER MSME ADVANTAGEOUS?

The Union Government of India has provided many

benefits for small scale units or medium small and micro

enterprises (MSME). In order to be eligible to get these

benefits, any entity should register itself as MSME/SSI

enterprise under MSMED Act. Following is a list of such

advantages of obtaining SSI/MSME registration in India.

The Ministry of Micro, Small and Medium Enterprises

gives protection to MSME Registered Business against

delay in payments from Buyers and right of interest on

delayed payment through conciliation and arbitration and

settlement of dispute be done in minimum time. If any

micro or small enterprise that has MSME registration,

supplies any goods or services, then the buyer is required

to make payment on or before the date agreed upon

between the buyer and the micro or small enterprise. In

case there is no payment date on the agreement, then the

buyer is required to make payment within fifteen days of

acceptance of goods or services. Further, in any case, a

payment due to a micro or small enterprise cannot

exceed forty-five days from the day of acceptance or the

day of deemed acceptance. In case of failure by the buyer

to make payment on time, the buyer is required to pay

compound interest with monthly interest rests to the

supplier on that amount from the agreed date of payment

or fifteen days of acceptance of goods or service. The

penal interest chargeable for delayed payment to a

MSME enterprise is three times of the bank rate notified

by the Reserve Bank of India.

1. Protection against delayed payments

SEJAL SHAHTax & Legal ConsultantsSejal M. Shah & Associates

Advocate

Enterprises that have MSME Registration Certificate can avail

50% subsidy for patent registration by making

application to respective ministry.

Top 8 Advantages of MSMEregistration for your Business

2. Credit linked Guarantee Scheme / Collateral Free loans from banks:The Credit Guarantee Fund Scheme for Micro and Small Enterprises (CGS) was launched by the GOI to make available collateral-free credit to the micro and small enterprise sector. Both the existing and the new enterprises are eligible to be covered under the scheme. The Ministry of Micro, Small and Medium Enterprises, Government of India and Small Industries Development Bank of India (SIDBI), established a Trust named Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) to implement the

Credit Guarantee Fund Scheme for Micro and Small

Enterprises. Enterprises that have MSME Registration

can avail benefit of 1% exemption on interest rate on OD

as mentioned in the scheme (this is bank dependent).

Enterprises that have MSME Registration Certificate can

3. Subsidy on Patentregistration as high as 50%

17 FORUM VIEWS - MARCH 2020

INSIGHTS - ECONBUZZINSIGHTS - ECONBUZZ

c o n s e q u e n c e s o f e c o n o m i c decoupling.”

The gap between awareness on one hand and action on the other is not surprising given the fact that it takes time to switch from one paradigm the currently predominant old resource intensive and less inclusive one. (although in some instances it has been largely exclusive) to the emerging more sustainable and inclusive paradigm of economic progress. In almost every nation the imperative of sustainability has begun to and would exert an increasingly significant influence on policy making and competitiveness. It is thus the ability and expediency of countries to make the adjustments to transition to the emerging paradigm of sustainable development that will clinch the `development destiny’ of nations.

In the next article for Econ Buzz I will talk about what I term as the Empowerment paradigm which basically describes the context within which sustainability considerations would be addressed. Evidently at this point for most nations much more needs to be done to put into place a

The influx of new technology that w o u l d h a v e g a m e c h a n g i n g implications for numerous sectors, the productivity slowdown that has impacted most nations-developed and developing and the slowdown in trade are some of the factors which constitute the configuration of change that has begun the transition to a new paradigm. At the recent World Economic Forum in Davos the increasing cognizance and apprehension about various aspects of economic sustainability was manifest as was the fact that even as the exigencies staring at us in the fact remain largely addressed. The WEF Global Risks report 2020 explains, "Powerful economic, demographic and technological forces are shaping a new balance of power. The result is an unsettled geopolitical landscape - one in which states are increasingly viewing opportunities and challenges through unilateral lenses. What were once givens regarding alliance structures and multilateral systems nolonger hold as states question the value of long-standing frameworks, adopt more nationalist postures in pursuit of individual agendas and weigh the potential geopolitical

context that would embody the enabling factors for trajectorythat would lead to sustainable development. In various articles for Econ Buzz even as I have enumerated certain aspects of sustainability such as the environment it is evident that despite the rising costs of pursuing a path that is becoming costly, obsolete and unviable.

Piya Mahtaney completed her second Master’s in Development Economics from Leicester University in England she embarked on a career in journalism with the Times of India. She was an assistant editor in Metropolis on Saturday, subsequent to which she joined as senior feature writer in Economic Times. As an economist that reported, analyzed and wrote on a wide range of socio-economic issues, writing a book about economic development and the emerging trends of globalisation seemed almost inevitable

The books that she has authored are as follows:• India China and Globalization (2nd ed), Palgrave

Macmillan (England), December 2014• Globalization and Sustainable Economic

Development, Palgrave Macmillan (U.S), August 1st 2013

• Institute of South East Asian Studies (Singapore) published an edition (August 2010) of my book India China and Globalisation.

• The first edition of India China and Globalisation was published by Palgrave Macmillan (England, 2007)

• Globalisation Con Game or Reality was published by Alchemy Publishers, India (2004) 2004.

• The first book titled Economic Con Game, Development fact or Fiction was published by Pelanduk Publications (Malaysia) in 2002.

A worrying aspect of the sluggish growth trend is that even if the

recovery in emerging and

developing economy growth takes place as expected, per

capita growth will remain below

long-term averages and will advance at a pace too slow to meet

poverty eradication goals.

PRESENT CHALLENGES IN THE DOMESTIC AND INTERNATIONAL CONTEXT

By Professor Piya MahtaneyEconomist / Author

16 FORUM VIEWS - MARCH 2020

INSIGHTS - ECOINSIGHTS - ECONBUZZ

observations about the fact that the budget lacked the measures that would spur a quick revival of growth.

tax rates, initiatives directed at expanding the bond market are some of the measures that would have a significant impact on kick-starting the investment cycle. Furthermore the present budget needs to be viewed in conjunction with the measures that were announced over the preceding six months Admittedly the revival of economic growth would be catalysed by expedient implementation of policy measures and it is this that needs to be emphasized. If budget announcements had lent more clarity to measures that would expand employment creation and increase the productivity of farming along with an enumeration of immediate priorities that would kick start the investment cycle this would certainly have been useful. Plausibly the specifics would become more evident over the ensuing period.

Country contexts differ however the common thread is the deficiency of investment across most developing and less developed nations according to the Global economic prospects report, "A worrying aspect of the sluggish growth trend is that even if the recovery in emerging and developing economy growth takes place as expected, per capita growth will remain below long-term averages and will advance at a pace too slow to meet poverty eradication goals. Income growth would in fact be slowest in Sub-Saharan Africa - the region where 56 percent of the world’s poor live.’’ In so far as addressing present and ensuing challenges the crux lies not merely in increasing economic growth rates but ensuring that per capita income rises at a rate that will step up poverty reduction which is one of most crucial imperatives going forward.

Notably the declining growth of the Indian economy is largely the result of fall in investment that is not recent but one that is rooted in structural factors that have manifested at least over the last decade and a half. and this in turn has led to a downturn in investment. Had the Finance Minister pursued the route of short termism it is very likely that she would have countered criticism about being short sighted. The emphasis on rural development, the infrastructure pipeline, the incorporation of a tax charter that would decriminalize taxation related offences, earlier reductions in corporate

The main objective of this article is to elucidate present challenges in the domestic and international context. I proceed to begin the discussion with a reference to the recently announced budget. The immediate reaction of many commentators and experts to this budget was that it fell short of providing the much needed impetus or stimulus to an economy that finds itself in the throes of a slowdown. A convenient reason for criticism (not without its political undertones) however it does reflect that important lessons from the past have been overlooked in so far as the costs of providing stimulus to an economy without due consideration to its fundamentals. The most illustrative instance of this is the Global Financial Crisis of 2008 which was the culmination of a credit binge that was based on a laxity of macro prudence and regulatory weakness that occurred in a backdrop of increasing polarization and a corrosion of infrastructural amenities. By a differing extent and across various contexts the underlying causes of the recession and slowdown in other developed nations were quite similar and it certainly heralded the end of quick fix short term stimulus measure and would leave in its trail volatility and prolonged slowdown which has taken almost a decade to reverse and the costs of which continue to be borne by the weaker and poorer segments of society. Clearly if this is case with developed nations, the adverse implications of what I term as` bubble growth’ (having also unravelled itself in some developing nations) is obvious. Taking thus a broader and I daresay more incisive perspective of the underpinnings of growth is entailed before drawing half baked

Akash Jain is part of the Global Research &Design group at S&P Dow Jones Indices, which is responsible for conceptualizing and developing new investable index-based products across different asset classes. He represents S&P Dow Jones Indices at media engagements, conferences, and other client events.

He is an integral part of Asia Index Private Limited, which is a partnership between S&P Dow Jones Indices and BSE Limited (formerly Bombay Stock Exchange).

He joined S&P Dow Jones Indices in 2016.He has been in the financial markets for more than six years, including at Deutsche, Credit Suisse, and Edelweiss, with experience in both the buyside and the sellside. He has worked extensively in researching, back-testing,and trading portfolios across different asset classes.

He attained his Bachelor of Technology (B.Tech) degree from Indian Institute of Technology (IIT Bombay) and holds a Masters of Business Administration (MBA) from Saïd Business School (University of Oxford).

19 FORUM VIEWS - MARCH 2020

INSIGHTSINSIGHTS

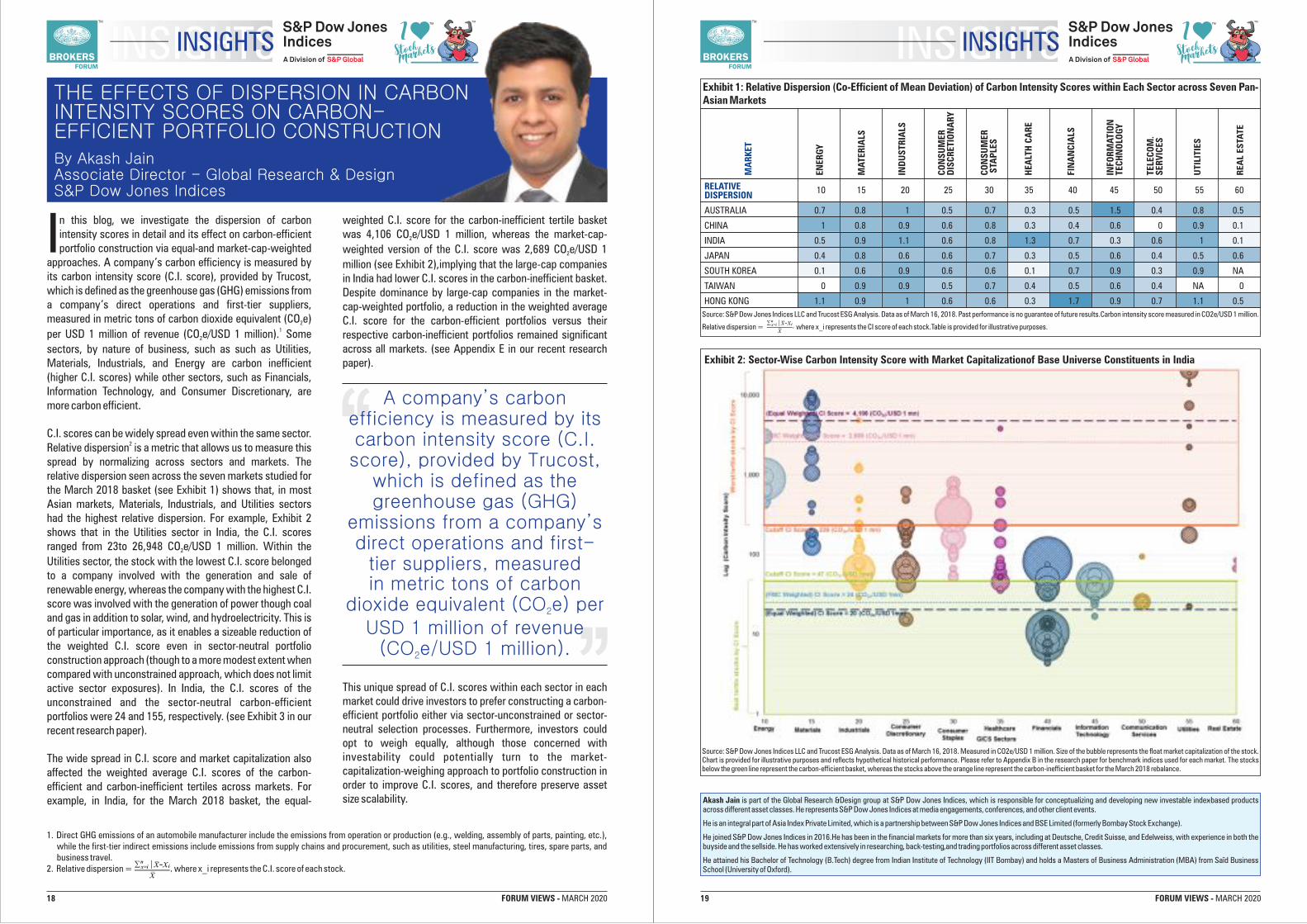

Exhibit 1: Relative Dispersion (Co-Efficient of Mean Deviation) of Carbon Intensity Scores within Each Sector across Seven Pan-Asian Markets

Source: S&P Dow Jones Indices LLC and Trucost ESG Analysis. Data as of March 16, 2018. Past performance is no guarantee of future results.Carbon intensity score measured in CO2e/USD 1 million.

Relative dispersion = where x_i represents the CI score of each stock.Table is provided for illustrative purposes.

ENER

GY

MA

TER

IALS

IND

US

TR

IALS

CO

NS

UM

ERD

ISC

RET

ION

AR

Y

CO

NS

UM

ER S

TAP

LES

HEA

LTH

CA

RE

FIN

AN

CIA

LS

INFO

RM

AT

ION

TEC

HN

OLO

GY

TEL

ECO

M.

SER

VIC

ES

UT

ILIT

IES

RE

AL

ES

TAT

E

AUSTRALIA 0.7 0.8 1 0.5 0.7 0.3 0.5 1.5 0.4 0.8 0.5

CHINA 1 0.8 0.9 0.6 0.8 0.3 0.4 0.6 0 0.9 0.1

INDIA 0.5 0.9 1.1 0.6 0.8 1.3 0.7 0.3 0.6 1 0.1

JAPAN 0.4 0.8 0.6 0.6 0.7 0.3 0.5 0.6 0.4 0.5 0.6

SOUTH KOREA 0.1 0.6 0.9 0.6 0.6 0.1 0.7 0.9 0.3 0.9 NA

TAIWAN 0 0.9 0.9 0.5 0.7 0.4 0.5 0.6 0.4 NA 0

HONG KONG 1.1 0.9 1 0.6 0.6 0.3 1.7 0.9 0.7 1.1 0.5

nx=i x-xi

x,

10 15 20 25 30 35 40 45 50 55 60

MA

RK

ET

RELATIVEDISPERSION

Exhibit 2: Sector-Wise Carbon Intensity Score with Market Capitalizationof Base Universe Constituents in India

Source: S&P Dow Jones Indices LLC and Trucost ESG Analysis. Data as of March 16, 2018. Measured in CO2e/USD 1 million. Size of the bubble represents the float market capitalization of the stock. Chart is provided for illustrative purposes and reflects hypothetical historical performance. Please refer to Appendix B in the research paper for benchmark indices used for each market. The stocks below the green line represent the carbon-efficient basket, whereas the stocks above the orange line represent the carbon-inefficient basket for the March 2018 rebalance.

18 FORUM VIEWS - MARCH 2020

A company’s carbon efficiency is measured by its carbon intensity score (C.I. score), provided by Trucost,

which is defined as the greenhouse gas (GHG)

emissions from a company’s direct operations and first-

tier suppliers, measuredin metric tons of carbon

dioxide equivalent (CO e) per 2

USD 1 million of revenue (CO e/USD 1 million).2

THE EFFECTS OF DISPERSION IN CARBONINTENSITY SCORES ON CARBON-EFFICIENT PORTFOLIO CONSTRUCTION

By Akash JainAssociate Director - Global Research & DesignS&P Dow Jones Indices

INSIGHTSINSIGHTS

weighted C.I. score for the carbon-inefficient tertile basket was 4,106 CO e/USD 1 million, whereas the market-cap-2

weighted version of the C.I. score was 2,689 CO e/USD 1 2

million (see Exhibit 2),implying that the large-cap companies in India had lower C.I. scores in the carbon-inefficient basket. Despite dominance by large-cap companies in the market-cap-weighted portfolio, a reduction in the weighted average C.I. score for the carbon-efficient portfolios versus their respective carbon-inefficient portfolios remained significant across all markets. (see Appendix E in our recent research paper).

n this blog, we investigate the dispersion of carbon intensity scores in detail and its effect on carbon-efficient Iportfolio construction via equal-and market-cap-weighted

approaches. A company’s carbon efficiency is measured by its carbon intensity score (C.I. score), provided by Trucost, which is defined as the greenhouse gas (GHG) emissions from a company’s direct operations and first-tier suppliers, measured in metric tons of carbon dioxide equivalent (CO e) 2

1per USD 1 million of revenue (CO e/USD 1 million). Some 2

sectors, by nature of business, such as such as Utilities, Materials, Industrials, and Energy are carbon inefficient (higher C.I. scores) while other sectors, such as Financials, Information Technology, and Consumer Discretionary, are more carbon efficient.

C.I. scores can be widely spread even within the same sector. 2Relative dispersion is a metric that allows us to measure this

spread by normalizing across sectors and markets. The relative dispersion seen across the seven markets studied for the March 2018 basket (see Exhibit 1) shows that, in most Asian markets, Materials, Industrials, and Utilities sectors had the highest relative dispersion. For example, Exhibit 2 shows that in the Utilities sector in India, the C.I. scores ranged from 23to 26,948 CO e/USD 1 million. Within the 2

Utilities sector, the stock with the lowest C.I. score belonged to a company involved with the generation and sale of renewable energy, whereas the company with the highest C.I. score was involved with the generation of power though coal and gas in addition to solar, wind, and hydroelectricity. This is of particular importance, as it enables a sizeable reduction of the weighted C.I. score even in sector-neutral portfolio construction approach (though to a more modest extent when compared with unconstrained approach, which does not limit active sector exposures). In India, the C.I. scores of the unconstrained and the sector-neutral carbon-efficient portfolios were 24 and 155, respectively. (see Exhibit 3 in our recent research paper).

The wide spread in C.I. score and market capitalization also affected the weighted average C.I. scores of the carbon-efficient and carbon-inefficient tertiles across markets. For example, in India, for the March 2018 basket, the equal-

1. Direct GHG emissions of an automobile manufacturer include the emissions from operation or production (e.g., welding, assembly of parts, painting, etc.), while the first-tier indirect emissions include emissions from supply chains and procurement, such as utilities, steel manufacturing, tires, spare parts, and business travel.

2. Relative dispersion = where x_i represents the C.I. score of each stock.nx=i x-xi

x,

This unique spread of C.I. scores within each sector in each market could drive investors to prefer constructing a carbon-efficient portfolio either via sector-unconstrained or sector-neutral selection processes. Furthermore, investors could opt to weigh equally, although those concerned with investability could potentially turn to the market-capitalization-weighing approach to portfolio construction in order to improve C.I. scores, and therefore preserve asset size scalability.

Key findings:

ASIA-PACIFIC MARKETSMONTHLY HIGHLIGHTS

AND INSIGHTS

• Greater China Q4 2019 M&A Summary

• Japan Q4 2019 M&A Summary

• Australia Q4 2019 M&A Summary

• M&A Activity By Country, Sector

• Initial Public Offerings

• Private Equity Investments & Buyouts

• Venture Capital Investments

• Coronavirus In China: Early Thoughts On The Economic Impact

• Recent S&P Global Credit Ratings Actions

• Market Attributes: Index Dashboard

Contact Information: If you have any questions relating to the content featured in the publication, please contact [email protected]

Disclaimer: Copyright © 2020 by S&P Global Market Intelligence, a division of S&P Global Inc. All rights reserved.

These materials have been prepared solely for information purposes based upon information generally available to the public and from sources believed to be reliable. No content (including index data, ratings, credit-related analyses and data, research, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of S&P Global Market Intelligence or its affiliates (collectively, S&P Global). The Content shall not be used for any unlawful or unauthorized purposes. S&P Global and any third-party providers, (collectively S&P Global Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Global Parties are not responsible for any errors or omissions, regardless of the cause, for the results obtained from the use of the Content. THE CONTENT IS PROVIDED ON “AS IS” BASIS. S&P GLOBAL PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Global Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages.

S&P Global Market Intelligence’s opinions, quotes and credit-related and other analyses are statements of opinion as of the date they are expressed and not statements of fact or recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P Global Market Intelligence assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P Global Market Intelligence does not act as a fiduciary or an investment advisor except where registered as such. S&P Global keeps certain activities of its divisions separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain divisions of S&P Global may have information that is not available to other S&P Global divisions. S&P Global has established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process.

S&P Global Ratings does not contribute to or participate in the creation of credit scores generated by S&P Global Market Intelligence. Lowercase nomenclature is used to differentiate S&P Global Market Intelligence PD credit model scores from the credit ratings issued by S&P Global Ratings.

S&P Global may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P Global reserves the right to disseminate its opinions and analyses. S&P Global's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributed through other means, including via S&P Global publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees.

20 FORUM VIEWS - MARCH 2020

GLOBAL INSIGHTSGLOBAL INSIGHTS

21 FORUM VIEWS - MARCH 2020

GLOBAL INSIGHTSGLOBAL INSIGHTS

M&A ACTIVITY IN ASIA PACIFIC: SELECTED COUNTRIESIn January 2020, China saw the most number of deals and the highest deal value in APAC. In the whole region, the number of deals and the deal value went down by 8% and 30%, respectively, in 2020 YTD, compared to 2019 YTD.

Source: S&P Global Market Intelligence as of February 1, 2020. Figures are based on M&A announcement dates. Includes both closed and

pending transactions as well as those without transaction values. Charts are provided for illustrative purposes.

Key Threshold (No. of Deals)

0 - 8

>8 - 48

>48 - 97

>97 - 145

>145 - 194

>194 - 242

No. of Deals and Value YTD Activity (20’ vs. 19’)

No. of Deals and Value by Country/Region (Jan’20)Country No. of Deals Value of Deals ($USDmm)

ChinaJapanAustraliaIndiaVietnamSouth KoreaSingaporeHong KongMalaysiaThailandPhilippinesIndonesiaNew ZealandTaiwan

242127818050443429231410883

13,852.509,804.602,656.901,380.90

153.81,360.908,753.701,325.50

156.31,196.50

352.9117.1128.7

0

20 YTD 19 YTD YoY Growth 20 YTD 19 YTD YoY Growth

Jan 1, 2020 -Jan 31, 2020

Jan 1, 2019 -Jan 31, 2019

YoY ComparisonThrough

Jan 31, 2020

Jan 1, 2020 -Jan 31, 2020

Jan 1, 2019 -Jan 31, 2019

YoY ComparisonThrough

Jan 31, 2020

No. of deals Value of Deals ($USDmm)

China -17% -43%Japan 124 2% 4,705 108%Australia 81 70 16% 2,657 3,525 -25%India 80 85 -6% 1,381 3,678 -62%Vietnam 50 31 61% 154 137 12%South Korea 44 61 -28% 1,361 7,298 -81%Singapore 34 39 -13% 7,198 22%Hong Kong 29 29 0% 1,326 5,735 -77%Malaysia 23 32 -28% 156 278 -44%Thailand 14 21 -33% 1,196 802 49%Philippines 10 2 353 - NAIndonesia 8 11 -27% 117 847 -86%New Zealand 8 10 -20% 129 10Taiwan 3 7 -57% - 207 -100%Total 753 815 -8% 41,240 58,763 -30%

242 293 13,852 24,344127 9,805

8,754

400%

1191%

INITIAL PUBLIC OFFERINGS BY COUNTRY

Source: S&P Global Market Intelligence as of February 1, 2020. Figures are based on public offerings offer date. Includes all closed transactions.

Tables are provided for illustrative purposes.

Key Threshold (No. of IPOs)

0

>0 - 8

>8 - 15

>15 - 23

>23 - 30

>30 - 38

China led the table with 38 IPOs and US$7,934.8mm raised in January 2020. Australia observed the highest YoY growth in both the number and the value of IPOs.

No. of IPOs and Value by Country/Region (Jan’20)Country No. of Deals Value of Deals ($USDmm)

ChinaIndonesiaHong KongAustraliaIndiaMalaysiaSingaporeSouth KoreaNew ZealandThailandVietnamJapanPhilippinesTaiwan

388544432111000

7,934.8071.894.221.23.632.635.117.98.67.52.6000

No. of IPOs and Value YTD Activity (20’ vs. 19’)

20 YTD 19 YTD YoY Growth 20 YTD 19 YTD YoY Growth

Jan 1, 2020 -Jan 31, 2020

Jan 1, 2019 -Jan 31, 2019

YoY ComparisonThrough

Jan 31, 2020

Jan 1, 2020 -Jan 31, 2020

Jan 1, 2019 -Jan 31, 2019

YoY ComparisonThrough

Jan 31, 2020

No. of deals Value of IPOs ($USDmm)

China 384%Indonesia 8 5 72 78 -8%Hong Kong 5 3 94 56 70%Australia 4 1 21 0India 4 5 -20% 4 19 -81%Malaysia 4 3 33 18 82%Singapore 3 2 35 26 37%South Korea 2 3 -33% 18 48 -63%New Zealand 1 - NA 9 - NAThailand 1 2 -50% 7 151 -95%Vietnam 1 3 -67% 3 14 -82%Japan - - NA - - NAPhilippines - - NA - - NATaiwan - 1 -100% - 19 -100%Total 71 50 42% 8,230 2,068 298%

38 22 73% 7,935 1,64060%67%

300% 4441%

33%50%

Key Threshold (No. of Deals)

0

>0 - 10

>10 - 20

>20 - 29

>29 - 39

>39 - 49

Source: S&P Global Market Intelligence as of February 1, 2020. Figures are based on M&A announcement dates. Includes both closed and pending

transactions as well as those without transaction values. Tables are provided for illustrative purposes.

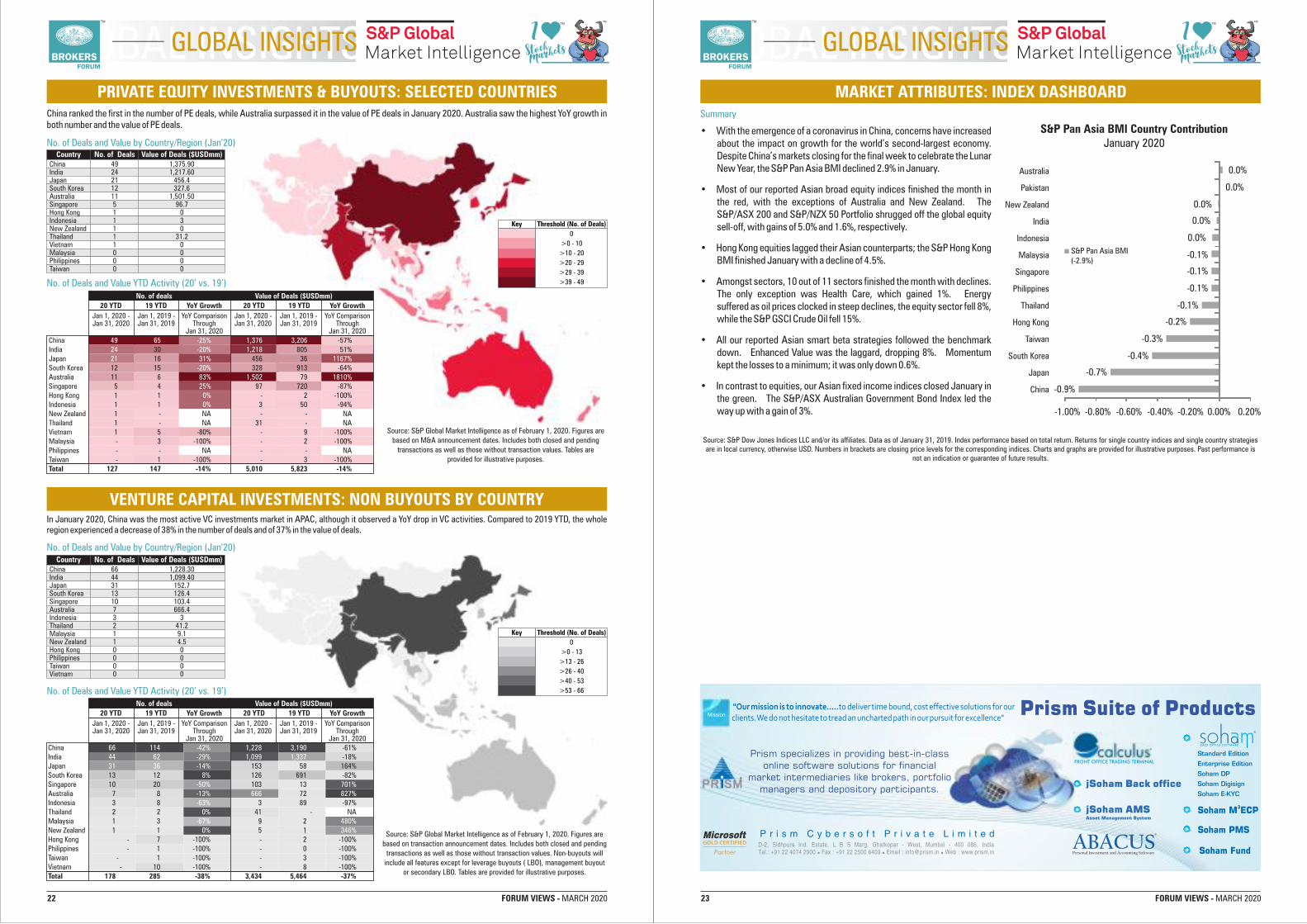

China ranked the first in the number of PE deals, while Australia surpassed it in the value of PE deals in January 2020. Australia saw the highest YoY growth in both number and the value of PE deals.

No. of Deals and Value by Country/Region (Jan’20)Country No. of Deals Value of Deals ($USDmm)

ChinaIndiaJapanSouth KoreaAustraliaSingaporeHong KongIndonesiaNew ZealandThailandVietnamMalaysiaPhilippinesTaiwan

4924211211511111000

1,375.901,217.60

456.4327.6

1,501.5096.7

030

31.20000

No. of Deals and Value YTD Activity (20’ vs. 19’)

PRIVATE EQUITY INVESTMENTS & BUYOUTS: SELECTED COUNTRIES

20 YTD 19 YTD YoY Growth 20 YTD 19 YTD YoY Growth

Jan 1, 2020 -Jan 31, 2020

Jan 1, 2019 -Jan 31, 2019

YoY ComparisonThrough

Jan 31, 2020

Jan 1, 2020 -Jan 31, 2020

Jan 1, 2019 -Jan 31, 2019

YoY ComparisonThrough

Jan 31, 2020

No. of deals Value of Deals ($USDmm)

22 FORUM VIEWS - MARCH 2020

GLOBAL INSIGHTSGLOBAL INSIGHTS

VENTURE CAPITAL INVESTMENTS: NON BUYOUTS BY COUNTRYIn January 2020, China was the most active VC investments market in APAC, although it observed a YoY drop in VC activities. Compared to 2019 YTD, the whole region experienced a decrease of 38% in the number of deals and of 37% in the value of deals.

Key Threshold (No. of Deals)

0

>0 - 13

>13 - 26

>26 - 40

>40 - 53

>53 - 66

Source: S&P Global Market Intelligence as of February 1, 2020. Figures are based on transaction announcement dates. Includes both closed and pending

transactions as well as those without transaction values. Non-buyouts will include all features except for leverage buyouts ( LBO), management buyout

or secondary LBO. Tables are provided for illustrative purposes.

No. of Deals and Value by Country/Region (Jan’20)

No. of Deals and Value YTD Activity (20’ vs. 19’)

Country No. of Deals Value of Deals ($USDmm)ChinaIndiaJapanSouth KoreaSingaporeAustraliaIndonesiaThailandMalaysiaNew ZealandHong KongPhilippinesTaiwanVietnam

6644311310732110000

1,228.301,099.40

152.7126.4103.4666.4

341.29.14.50000

20 YTD 19 YTD YoY Growth 20 YTD 19 YTD YoY Growth

Jan 1, 2020 -Jan 31, 2020

Jan 1, 2019 -Jan 31, 2019

YoY ComparisonThrough

Jan 31, 2020

Jan 1, 2020 -Jan 31, 2020

Jan 1, 2019 -Jan 31, 2019

YoY ComparisonThrough

Jan 31, 2020

No. of deals Value of Deals ($USDmm)

China -57%India 30 805 51%Japan 16 456 36South Korea 12 15 328 913 -64%Australia 11 6 79Singapore 5 4 97 720 -87%Hong Kong 1 1 - 2 -100%Indonesia 1 1 3 50 -94%New Zealand 1 - NA - - NAThailand 1 - NA 31 - NAVietnam 1 5 -80% - 9 -100%Malaysia - 3 -100% - 2 -100%Philippines - - NA - - NATaiwan - 1 -100% - 3 -100%Total 127 147 -14% 5,010 5,823 -14%

49 65 -25% 1,376 3,20624 -20% 1,21821 31% 1167%

-20%83% 1,502 1810%25%0%0%

China -61%India -18%Japan 153 58 164%South Korea 13 12 126 691 -82%Singapore 10 20 103 13Australia 7 8 72Indonesia 3 8 3 89 -97%Thailand 2 2 41 - NAMalaysia 1 3 9 2New Zealand 1 1 5 1Hong Kong - 7 -100% - 2 -100%Philippines - 1 -100% - 0 -100%Taiwan - 1 -100% - 3 -100%Vietnam - 10 -100% - 8 -100%Total 178 285 -38% 3,434 5,464 -37%

66 114 -42% 1,228 3,19044 62 -29% 1,099 1,33731 36 -14%

8%-50% 701%-13% 666 827%-63%

0%-67% 480%

0% 346%

23 FORUM VIEWS - MARCH 2020

GLOBAL INSIGHTSGLOBAL INSIGHTS

MARKET ATTRIBUTES: INDEX DASHBOARD

• With the emergence of a coronavirus in China, concerns have increased about the impact on growth for the world’s second-largest economy. Despite China’s markets closing for the final week to celebrate the Lunar New Year, the S&P Pan Asia BMI declined 2.9% in January.

• Most of our reported Asian broad equity indices finished the month in the red, with the exceptions of Australia and New Zealand. The S&P/ASX 200 and S&P/NZX 50 Portfolio shrugged off the global equity sell-off, with gains of 5.0% and 1.6%, respectively.

• Hong Kong equities lagged their Asian counterparts; the S&P Hong Kong BMI finished January with a decline of 4.5%.

• Amongst sectors, 10 out of 11 sectors finished the month with declines. The only exception was Health Care, which gained 1%. Energy suffered as oil prices clocked in steep declines, the equity sector fell 8%, while the S&P GSCI Crude Oil fell 15%.

• All our reported Asian smart beta strategies followed the benchmark down. Enhanced Value was the laggard, dropping 8%. Momentum kept the losses to a minimum; it was only down 0.6%.

• In contrast to equities, our Asian fixed income indices closed January in the green. The S&P/ASX Australian Government Bond Index led the way up with a gain of 3%.

Summary

Source: S&P Dow Jones Indices LLC and/or its affiliates. Data as of January 31, 2019. Index performance based on total return. Returns for single country indices and single country strategies are in local currency, otherwise USD. Numbers in brackets are closing price levels for the corresponding indices. Charts and graphs are provided for illustrative purposes. Past performance is

not an indication or guarantee of future results.

-0.9%

-0.7%

-0.4%

-0.3%

-0.2%

-0.1%

-0.1%

-0.1%

-0.1%

0.0%

0.0%

0.0%

0.0%

0.0%

-1.00% -0.80% -0.60% -0.40% -0.20% 0.00% 0.20%

Australia

Pakistan

New Zealand

India

Indonesia

Malaysia

Singapore

Philippines

Thailand

Hong Kong

Taiwan

South Korea

Japan

China

S&P Pan Asia BMI Country ContributionJanuary 2020

S&P Pan Asia BMI(-2.9%)

25

HOW TO CHOOSESECURE WEBCASTINGSERVICES?

#ADVERTORIAL

By Siddharth BeraManaging DirectorEpitome Corporation Pvt. Ltd.

Contact us: [email protected]

Telephone: +91 98795 44338 Website: http://epitomesolutions.in

Log on www.epitomesolutions.in to know about the services they offer.

re you planning to produce a webcast? You must be aware Aof the ways you can stage

video production. You need to get the best shots of the event you are organizing and edit those to make a great video package. However, webcasting is completely different from that. You need to know how to distribute the video online. The challenge is even greater when you need to webcast live videos on the web channels. India based company Epitome Corporation Pvt Ltd offer your own secured channel or can also take the services of the secure webcasting services using which you can deliver a branded video streaming with full of security.

Why choose secure webcasting services?You may not be aware of all the technical details of webcasting a video on the Internet. That is the r e a s o n y o u s h o u l d c h o o s e webcasting service providers to take up the task for you. Webcasting services are around for a long time. There are quite a few good ones. However, you need to choose the best webcasting service provide who would provide secure webcasting services. There are certain important things that you need to consider while choosing such a service provider:

India based company Epitome Corporation Pvt Ltd

offer your own secured channel or can also take the services of the

secure webcasting services using which you can

deliver a branded video streaming with

full of security.

for a packaged solut ion for webcasting the videos of the company, you should choose hosted solutions. These service providers generally have their own cloud-based platforms. These platforms support the webcast distribution process. However, the webcasts will be managed by you by subscribing to their hosted solutions. If you produce webcasts too frequently, choosing this type of hosted services seems to be a viable solution to your video webcasting problem.

Secure webcasting will also broaden the online event experience. With the right services your events can turn into large virtual events for the target audiences to follow. The videos are often as big as online trade shows bringing a lot of details about the products and services to the potential customers. The virtual events are nowadays becoming the platform for attracting online customers and brand enthusiasts.

The foremost decision that you need to take is which of the company events you’d like to webcast. If it is a single live event about an important product launch or any special occasion in the company that you’d like the targeted audiences to know, you need to choose webcasting services. You need to measure whether this approach of webcasting will help to generate leads and revenue for the company. If it does, you should opt for live webcasting services.

If you have a certain in-house webcast expertise and yet are looking

FORUM VIEWS - MARCH 2020

Kamlesh P. Mehta B.Com. FCA, DISA (Post qualification course in information system audit from ICAI) is a practicing Chartered Accountant by profession having an experience of 24 years in the field of capital market compliance consultancy, depository services audit, management consultancy, system audit and Commodity market compliance consultancy.

He is a Proprietor of CA firm M/s. KAMLESH P. MEHTA ASSOCIATES & Partner of MEHTA SANGHVI & ASSOCIATES located at Borivali, Mumbai.

He along with his associated concerns specializes in Audit and Assurance Services of various compliance areas related to Capital Market Operations and system audits of broking industry.

He is also providing compliance calendar to BSE brokers forum and ANMI regularly and same is published in their journal. Recently he and his team had drafted compliance manual for commodity brokers published by BSE brokers forum.

He is a regular speaker of the various seminars for broking and DP compliances organized by WIRC (Western India Regional Council of ICAI) and study circle group.

COMPLIANCE REQUIREMENT FORTHE MONTH OF MARCH - 2020

Compiled by CA Kamlesh P. Mehta(B.Com, FCA, DISA)M/s. Kamlesh P. Mehta Associates

COMPLIANCE COMPLIANCE CALENDAR

24

Segment Particulars Due Date

BSE

All Equity & Commodity

Exchanges

PMS

All Stock Exchanges

All Exchanges

All Exchanges

NSE

Income Tax

Stamp Duty

Depositary

All Equity & Commodity

Exchanges

All Stock Exchanges

Income Tax

All Equity & Commodity

Exchanges

All Stock Exchanges

All Equity & Commodity

Exchanges

All Stock Exchanges

NSE

BSE

BSE- Uploading of margin funding file for the month of February 2020

Uploading of Clients’ Funds, collateral and other details lying with the member broker -

Week ended 28.02.2020

PMS- Uploading of activity report on SEBI Portal

Applicability of uploading of day-wise Holding statement in the specified standard format to exchange.-

Week ended 29.02.2020

Uploading clients’ fund balance and securities balances by the stock brokers on stock exchanges

system as per SEBI circular of Enhanced supervision.- Monthly basis.

Contingency Drill / Mock Trading Session (Subject to circular from respective exchanges)

NSE- Uploading of margin funding file for the month of February 2020

TDS Payment for the Month of February 2020 for Corporate and Individual.

Payment of Stamp duty: - Security and Commodity Exchanges

Submission of Investor Grievances Report • CDSL & • NSDL

Uploading of Clients’ Funds, collateral and other details lying with the member broker -

Week ended 06.03.2020

Applicability of uploading of day-wise holding statement in the specified standard format to exchange. -

Week ended 07.03.2020

Advance payment of Income Tax

Uploading of Clients’ Funds, collateral and other details lying with the member broker -

Week ended 13.03.2020

Applicability of uploading of day-wise Holding statement in the specified standard format to exchange.-

Week ended 14.03.2020

Uploading of Clients’ Funds, collateral and other details lying with the member broker -

Week ended 20.03.2020

Applicability of uploading of day-wise Holding statement in the specified standard format to exchange.-

Week ended 21.03.2020

Discontinuation of VSAT services

No. of STR filed with FIU-IND for the month of February, 2020. (Including NIL STR)

01/03/2020 To

07/03/2020

04/03/2020

05/03/2020

05/03/2020

06/03/2020

07/03/2020

07/03/2020

07/03/2020

10/03/2020

10/03/2020

12/03/2020

13/03/2020

15/03/2020

18/03/2020

19/03/2020

25/03/2020

26/03/2020

31/03/2020

Before

31/03/2020

27 FORUM VIEWS - MARCH 2020

REGULATORY PUREGULATORY PULSE

Disclaimer :The newsletter is not in the nature of alegal opinion or advice. Copyright reserved.

Courtesy: Finsec Law Advisors A financial sector law firm which provides regulatory advice and assistance focusingon the securities, investments and banking industry. www.finseclaw.com

SEBI CIRCULAR ON ‘INC’ RATINGS AND WITHDRAWAL OF CREDIT RATINGS

cooperation by the issuer, the CRAs are required to review the instrumentsbased on ‘best available information’.

Besides the above, certain conditions for withdrawal of ratings by CRAs have also been modified. Previously, as per SEBI’s circular dated June 06, 2018, a CRA could withdraw its ratings for instruments which have been assigned multiple ratings, if i) such instruments have been rated by such CRA for a continuous period of five years or 50% of the tenure of the instrument, whichever is higher, and ii) an undertaking has been obtained from the issuer that ratingsare available on such instruments.

According to the new circular, ratings may be withdrawnfor instruments with multiple

ratings, provided theinstrumentshave been rated for three years or 50% of the tenure of the instruments, whichever is higher. Further, apart from an undertaking from the issuer, a CRA is required to obtain a no-objection certificate from 75% of the bondholders of the outstanding debt.

The above circular follows a string of measures recently imposed by SEBI to further reduce information asymmetry with regard to the financial health of listed entities. Previously, in November 2019, SEBI had mandated listed entities to make public disclosures regarding defaults in payment obligations towards loans, including revolving facilities such as cash credit, etc. which continue beyond 30 days.

On January 03, 2020, SEBI issued a circular directing credit rating agencies (CRAs) to downgrade ratings of an issuer to non-investment grade with ‘Issuer Not Cooperating’ (INC) status, if such issuer has all outstanding ratings as non-cooperative for more than six months.The circular further provides that if such non-cooperation continues for a further period of six months from the date of such downgrade, no CRA shall assign new ratingsuntil i) the issuer resumes cooperation, or ii) the ratings so assigned are withdrawn.

Under the SEBI (CRA) Regulations, 1999, issuers are required to cooperate with CRAs in order to enable them to arrive at a true and accurate rating and in case of non-

INFORMAL GUIDANCE BY SEBI ON DISCLOSURE OF ‘MATERIAL FINANCIAL RELATIONSHIP’

definition of material financial relationship included any kind of payment, such as loan or gift, not only monetary transactions but non-monetary transactions would also be covered for the purpose of disclosure of MFR. Further, it was clarified that in case a DP shares a MFR with one of his immediate relatives, the name of such relative must also be separately disclosed under category of persons with whom the DP shares a MFR.

The Applicant had also sought for clarifications regarding disclosure in certain situations. Out of these situations, SEBI clarified that the DP is required to make disclosures in the following instances: • If a DP makes payment of fees,

exceeding 25% of his annual income, on behalf of his granddaughter by directly depositing such amount in the University’s account (in case the granddaughter is a minor, the names of both the parents and the guardian must be disclosed in addition to that of the granddaughter);

• If a DP gifts a piece of land / an amount of INR 2 lakh to his / her daughter on her birthday, where the cost of such

land / the amount is more than 25% of the DP’s annual income;

• If a DP makes payment of fees, exceeding 25% of the DP’s annual income, for her niece’s higher education, where such fees will be repaid by the niece to the DP (without interest); and

• Where a DP undertakes to repay the financial obligation of a person which exceeds 25% of the DP’s annual income, where the actual payment is made over a period of two years.

Besides the above instances, SEBI clarified that no disclosures are needed where a DP’s relative sponsors a foreign trip for such DP, where the sponsorship exceeds 25% of such person’s annual income.

While the above disclosure requirements were introduced with a view to prevent insiders from funding relatives to trade on their behalf, they have fuelled concerns over breach of privacy and the extent of disclosures required. This clarificatory informal guidance will assist the DPs in making appropriate disclosures.

On January 03, 2020, SEBI issued an informal guidance to Gujarat State Petronet Limited (Applicant), inter alia clarifying when designated persons (DPs) are required to disclose details of persons with whom they share material financial relationships.

In December 2018, certain amendments were made to the SEBI (Prohibition of Insider Trading) Regulations, 2015 (PIT Regulations) which required DPs of listed entities, intermediaries and fiduciaries to annually disclose details of immediate relatives and persons with whom they share a ‘material financial relationship’ (MFR).

As per the PIT Regulations, MFR denotes transactions where a DP makes any kind of payment such as a loan or gift to any person during the preceding twelve months and such payment is equivalent to at least 25% of the DP’s annual income. However, payments based on arm’s length transactions are excluded from the ambit of MFR.

Pursuant to the queries raised by the Applicant, SEBI clarified that since the

26 FORUM VIEWS - MARCH 2020

REGULATORY PUREGULATORY PULSE

SEBI PROPOSES REVISED NORMS FOR INVESTMENT ADVISERS

will be charged by IAs for providing implementation services to advisory clients, either directly or indirectly, at the group / family level of the IAs. Further, it has been proposed that implementation services may be provided by IAs only through direct schemes / direct code in the securities market.

Ordinari ly, for recommendations involving equity or debt products, clients would require the services of a SEBI-registered stock broker. However, this proposal restricts receipt of all kinds of commissions by the IA and its related entities, including consideration in the form of a brokerage fee. Usually clients prefer a one-stop solution from wealth management groups, however, this provision would compel investors to look for separate service providers for implementation of the advice and also undergo the KYC process all over again.

Enhanced Eligibility Criteria Currently, either appropriate educational qualification or adequate professional experience is sufficient for individual IAs, principal officers and persons associated with IA, to apply for a registration as an IA. The consultation paper now proposes to mandate both educational qualification and experience before applying for registration. This will not only render a number of existing IAs (who are graduates with ample experience) unemployed, but also inhibit new aspirants and qualified persons from becoming IAs.

Increased Net Worth RequirementsFurther,SEBI has proposed to enhance the minimum net worth requirements for individual IAs from INR 1 lakh to INR 10 lakh, and for corporate IAs, from INR 25 lakh to INR 50 lakh. In our view, a minimum net worth requirement for intermediaries such as IAs, which do not have custody of clients’ funds or securities, is unwarranted. Further, mandating an individual to maintain such a high net worth is unreasonable, as it is more important for advisors to have appropriate resources at their disposal such as infrastructure, technology, human resources, etc., instead of a higher net worth.

Corporatization of IAsIt is proposed that individual IAs with more than 150 clients or assets under management (AUA) more than INR 40 crore shall compulsorily re-register themselves as a corporate adviser within six months of the trigger event. The above proposal is arbitrary and would dramatically increase the costs and burden of compliance for small players. A single or few high net-worth clients can together easily cross such a low threshold of INR 40 crore. Moreover, mandatory corporatization may put a vast majority of small-town IAs out of business.

FeesIt has been proposed that advisory fees should be based on AUA, capped at a maximum of 2.5% of the AUA. Alternatively, it is stated that a fixed fee should be charged at a maximum of Rs. 75,000/- per annum per family. In our view, while the capping should only be done on the percentage basis, additionally, SEBI may consider providing for an enabling provision for receipt of performance-linked fee from the clients.

Documentation of the terms and conditions of IA servicesUnder the present framework, execution of a written IA agreement is not mandatory. The consultation paper proposes that IAs must provide their clients a document detailing the terms and conditions of the advisory services, before any service is offered to such clients. The contents of such document have been broadly provided in the consultation paper, such as requirement of written consent from clients, description of the scope of services to be offered, inclusion of investment objective and risk factors, etc.

While the above proposal will provide a clarity on the terms of agreement however, the applicability of such provision with respect to the existing clients is unclear. Further, the requirement of a written consent should be construed in a manner to include electronic and digital confirmation, as a number of IAs provide their services in digital / electronic mode.

On January 15, 2020, SEBI issued a consultation paper ushering major reforms in the regulatory framework for investment advisers (IAs). Based on the recommendations of the working group constituted by SEBI, the consultation paper inter alia seeks to address the existing conflict of interest arising out of the dual role played by IAs providing distribution services as both agents of investors and manufacturers of financial products.

Some of the key changes proposed in the consultation paper are discussed below:

Segregation between client advisory and distribution activitiesCurrent ly, under the SEBI ( IA) Regulations, 2013, incorporated entities can provide both advisory and distribution services through separately identifiable department / division / subsidiary, and individual IAs are not permitted to provide distribution services. SEBI has now proposed that to segregate the two activities, a client can either be an advisory or a distribution client at the group / family level of the corporate / individual IA entities and a group / family can only receive consideration in the form of advisory fee or distribution commission from one client.