fast fourier transform for discrete asian options european finance management association lugano...

TRANSCRIPT

Fast Fourier Transform for Discrete Asian Options

European Finance Management Association

Lugano June 2001

Eric Ben-Hamou

June 2001 Lugano 2001 Conference Slide N°2

Outline

• Motivations

• Description of the methods

• Log-Normal density

• Non-Log-Normal density

• Conclusion

June 2001 Lugano 2001 Conference Slide N°3

Motivations

• When pricing a derivative, one should keep in mind:

• Within a model, the quality of the approximation.

• model risk, reflected by the uncertainty on the model parameters

• objectivity of the model

• So need to examine the risk of a certain derivative, here Asian option.

June 2001 Lugano 2001 Conference Slide N°4

Asian option’s characteristics• academic case is geometric Brownian motion

continuous time average: no easy-closed forms (Geman Yor 93 Madan Yor 96)

• discrete averaging (see Vorst 92 Turnbull and Wakeman 91 Levy 92 Jacques 96 Bouazi et al. 98 Milevsky Posner 97 Zhang 98 Andreasen 98)

• empirical literature suggests fat-tailed distribution (Mandelbrot 63 Fama 65) and smile literature (Kon 84 Jorion 88 Bates 96 Dupire 94 Derman et al 94 see Dumas et al. 95) stochastic volatility (Hull and White 87 Heston 93)

June 2001 Lugano 2001 Conference Slide N°5

Asian option risk

• Main risks:• jump of delta risk, or reset risk at each fixing (Vorst 92

Turnbull and Wakeman 91 Levy 92…)• distribution risk underlying the jump of delta at each

fixing dates…• other issues like modeling of discrete dividends

(Benhamou Duguet 2000)

• Good method:• tackles discret averaging• non lognormal densities

June 2001 Lugano 2001 Conference Slide N°6

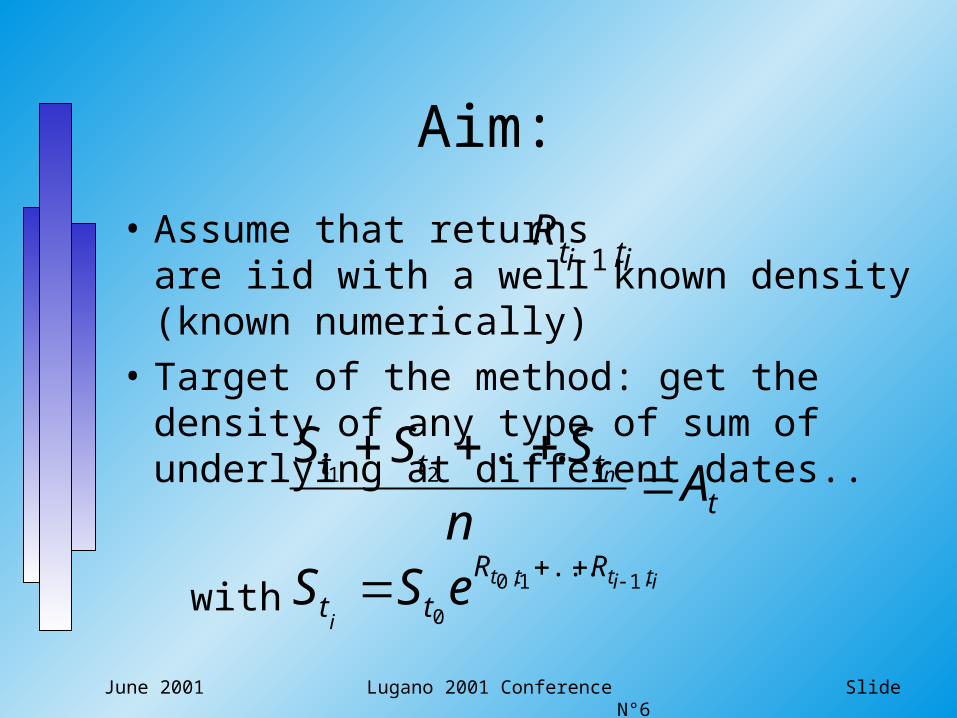

Aim:

• Assume that returns are iid with a well known density (known numerically)

• Target of the method: get the density of any type of sum of underlying at different dates..

with

tttt A

n

SSSn

...21

itittt

i

RR

tt eSS ,11,0

0

...

ititR

,1

June 2001 Lugano 2001 Conference Slide N°7

• Standard hypotheses:… complete markets and no arbitrage.

• If the density of is known then simple numerical integration.

• Density of a sum of independent variables is the convolution of the individual densities

FFT O(Nlog2(N) ) typically N=2p so that p2p (like binomial tree)

KAeEP TrTQ

TA

June 2001 Lugano 2001 Conference Slide N°8

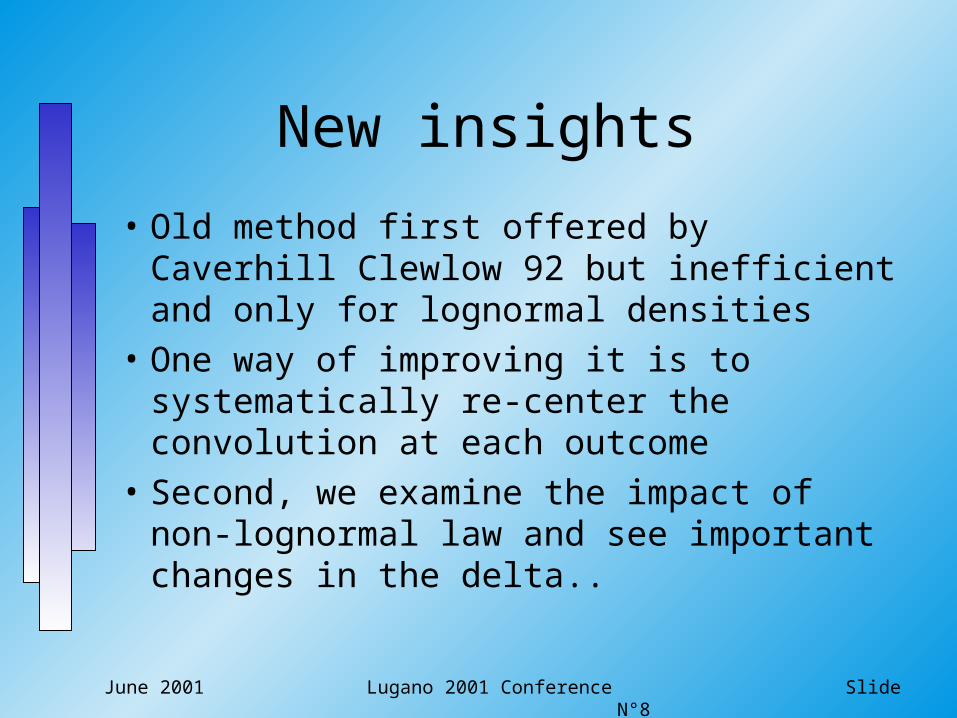

New insights

• Old method first offered by Caverhill Clewlow 92 but inefficient and only for lognormal densities

• One way of improving it is to systematically re-center the convolution at each outcome

• Second, we examine the impact of non-lognormal law and see important changes in the delta..

June 2001 Lugano 2001 Conference Slide N°9

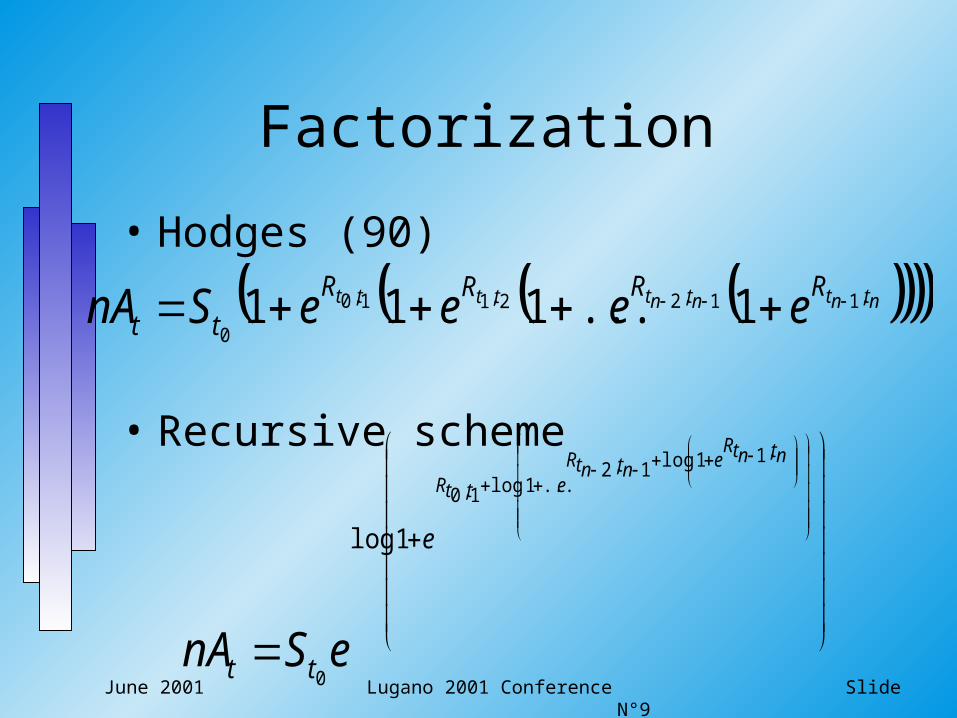

Factorization

• Hodges (90)

• Recursive scheme

ntntntnttttt RRRR

tt eeeeSnA ,11,22,11,0

01...111

ntntRentntR

ettR

e

tt eSnA

,11log1,2...1log1,0

0

1log

June 2001 Lugano 2001 Conference Slide N°10

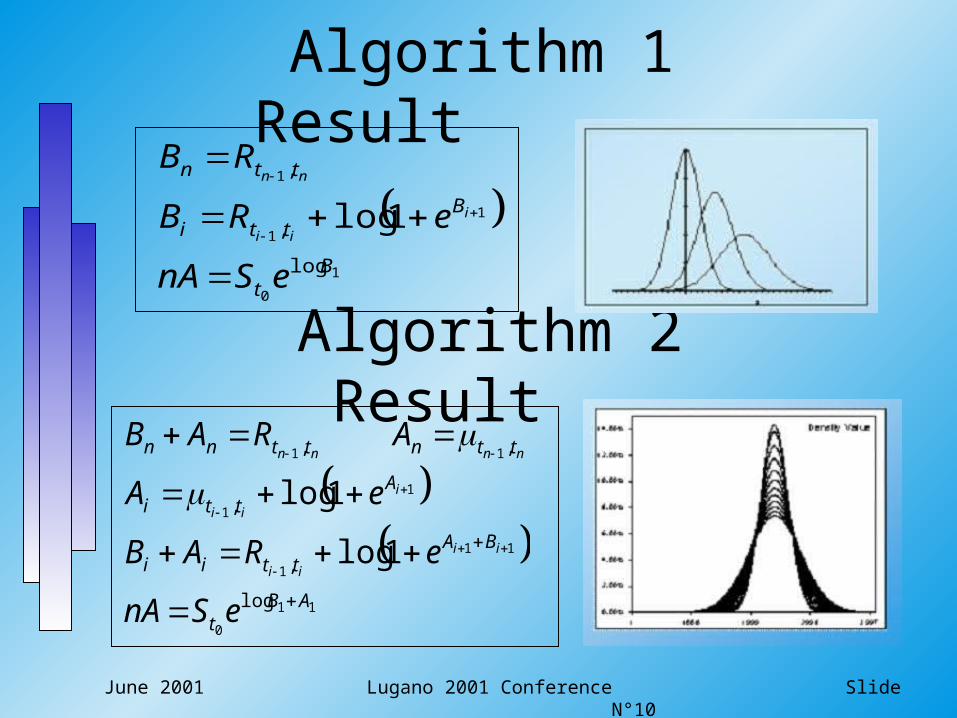

Algorithm 1 Result

1

0

1

1

1

log

,

,

1logB

t

Btti

ttn

eSnA

eRB

RB

i

ii

nn

Algorithm 2 Result

11

0

11

1

1

1

11

log

,

,

,,

1log

1log

ABt

BAttii

Atti

ttnttnn

eSnA

eRAB

eA

ARAB

ii

ii

i

ii

nnnn

June 2001 Lugano 2001 Conference Slide N°11

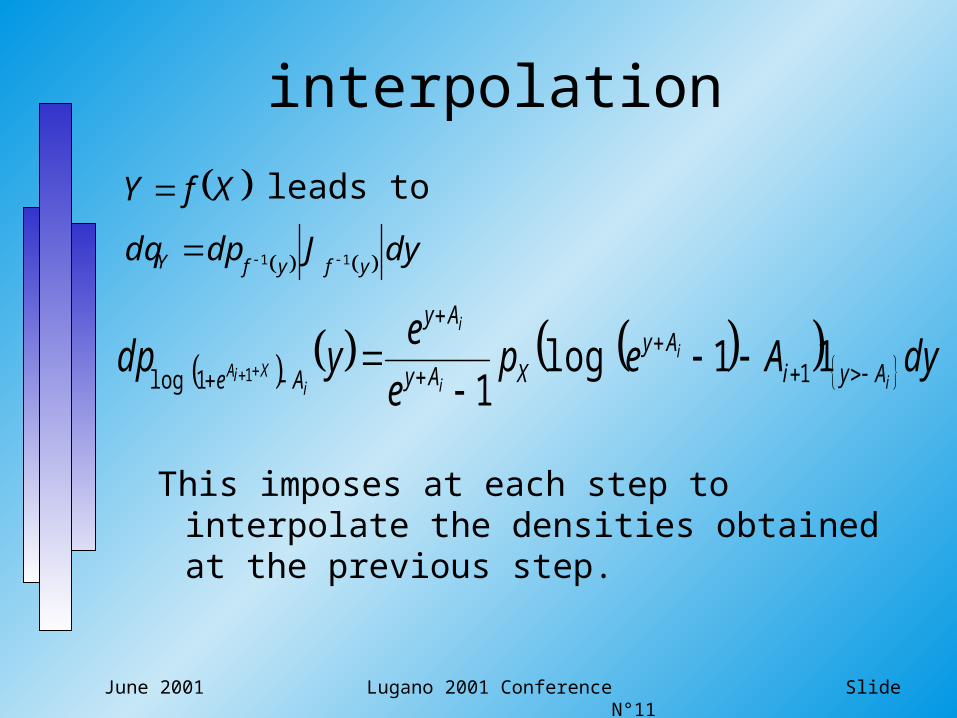

leads to

This imposes at each step to interpolate the densities obtained at the previous step.

interpolation

dyJdpdq

XfY

yfyfY 11

dyAepe

eydp

i

i

i

i

iXiA Ayi

AyXAy

Ay

Ae

11log

1 11log 1

June 2001 Lugano 2001 Conference Slide N°12

Efficiency of the algorithm

June 2001 Lugano 2001 Conference Slide N°13

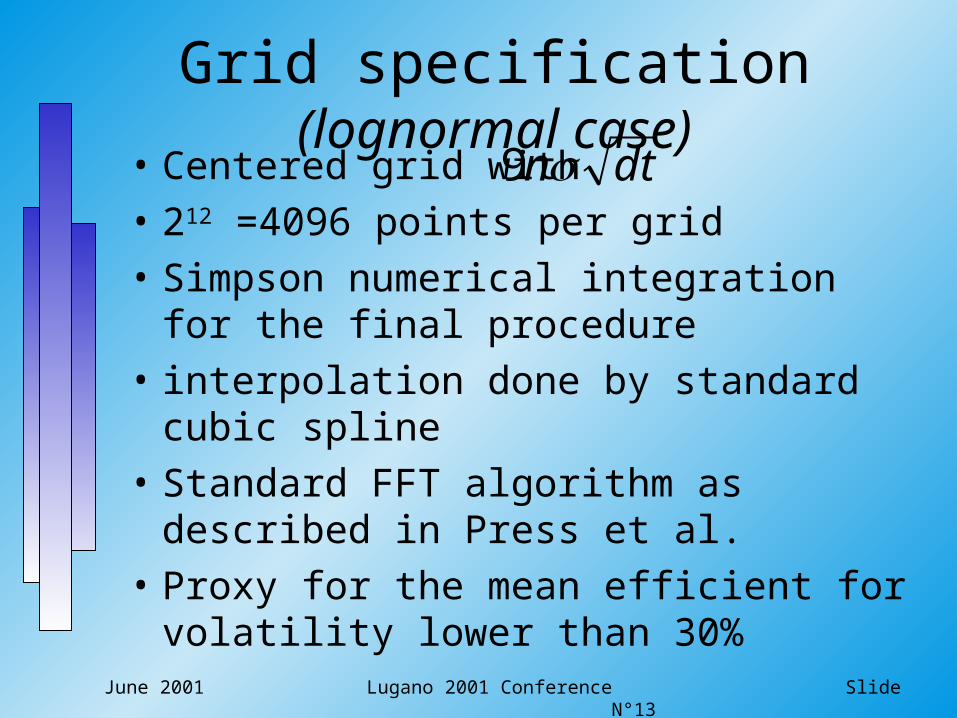

Grid specification (lognormal case)• Centered grid with

• 212 =4096 points per grid

• Simpson numerical integration for the final procedure

• interpolation done by standard cubic spline

• Standard FFT algorithm as described in Press et al.

• Proxy for the mean efficient for volatility lower than 30%

dtn9

June 2001 Lugano 2001 Conference Slide N°14

Non log-normal case• Smile can be seen as a proof of non log-

normal densities with fatter tails. (excess kurtosis and skewness)

• Lognormal case already requires numerical methods

• So instead use of Student distributions, Pareto, generalized Pareto, power-laws distributions.. Here took Student density

June 2001 Lugano 2001 Conference Slide N°15

• Student additional advantage to converge to normal distribution… which gives the geometric Brownian motion

• Assumptions:

follows a Student density of df

normal case

12

1

2

, 21

ii

iitt

tt

ttrRii

1

22

1

2

1

Example of Student law

1

June 2001 Lugano 2001 Conference Slide N°16

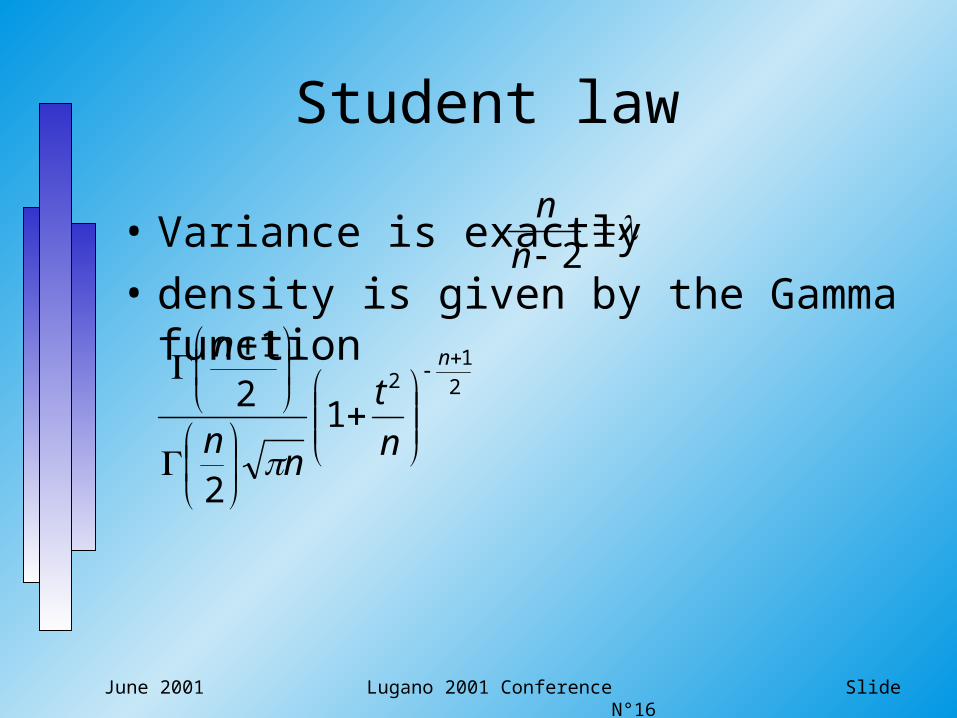

Student law

• Variance is exactly

• density is given by the Gamma function

2n

n

2

12

1

2

21

n

n

t

nn

n

June 2001 Lugano 2001 Conference Slide N°17

Non log-normal densities

June 2001 Lugano 2001 Conference Slide N°18

Delta hedging

• Strong impact on the delta whereas small impact on the price.

• Price effect offsets by the overpricing of the lognormal approximation

• This justifies the use of lognormal approximation as a way of incorporating fat tails… but wrong for the delta

June 2001 Lugano 2001 Conference Slide N°19

Results

Long maturity

before expiry

short maturity

before expiry

June 2001 Lugano 2001 Conference Slide N°20

Conclusion• Offered an efficient method for the pricing of

discrete Asian options with non lognormal laws.• Shows that fat tails impacts much more for the

Greeks than the price• future work:

• adaptation to floating strike option

• use of other fat tailed distribution

• raises the issue of deriving an efficient methodology for deriving densities from Market prices