fam law assoc pres

TRANSCRIPT

Budget 2011

www.hannanfinancial.ie

George Hannan t/a Hannan Financial is regulated by the Central Bank of Ireland

and Pensions Issues

1

George Hannan BComm QFA

Equipped to deliver the service:

General Pensions

Business

Family Pension Assets

Testimonials

UK CII IFA since 2001

QFA bridge since 2006

HF Authorised & PI late 2009

LIA, PIBA, ongoing CPD

Tech, marketing, managerial: c.20yrs

Commercial & Technical qualifications

Exising clients

Life Office Specialists

Rel. Literature in public domain

Law Society guides

Expert publications (ie G Shannon & Pensions Board)

Based on work already done

2

• Finance Bill 2011 - pension & PAO issues

3

• Non-member options re PAO’s

• PAO’s, effect of changed member circumstances

• DB schemes – some issues

• role of specialist pensions input

We’ll look at:

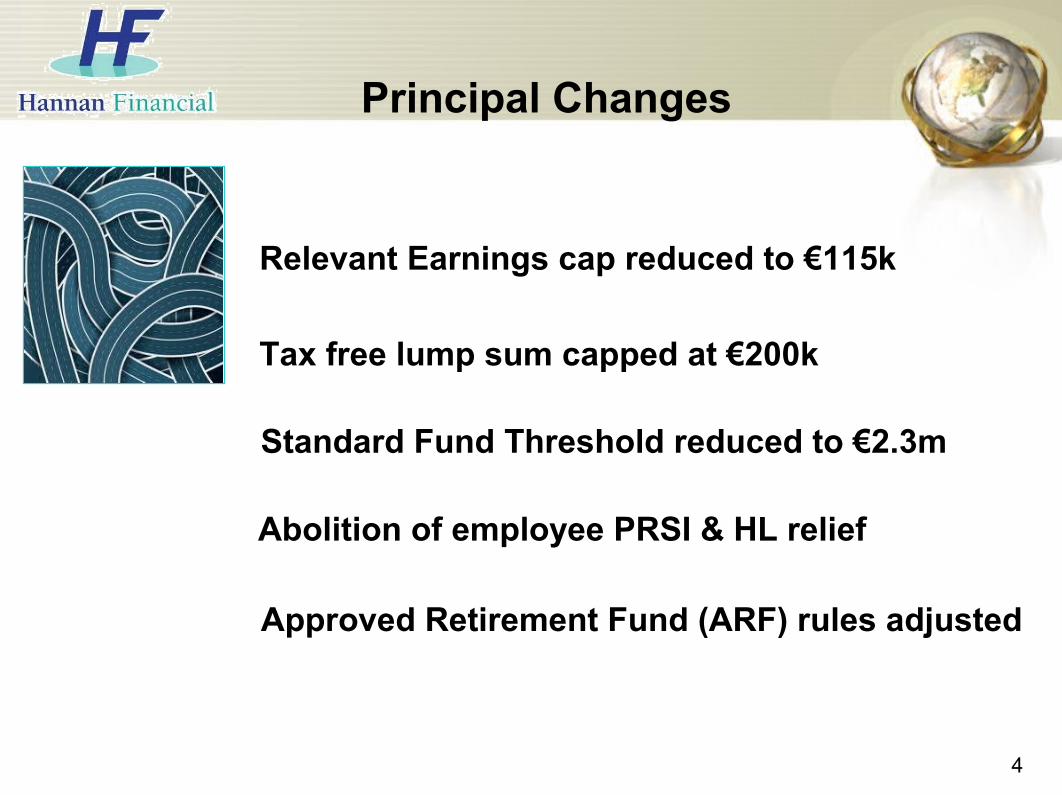

Principal Changes

Relevant Earnings cap reduced to €115k

Tax free lump sum capped at €200k

Standard Fund Threshold reduced to €2.3m

Abolition of employee PRSI & HL relief

Approved Retirement Fund (ARF) rules adjusted

4

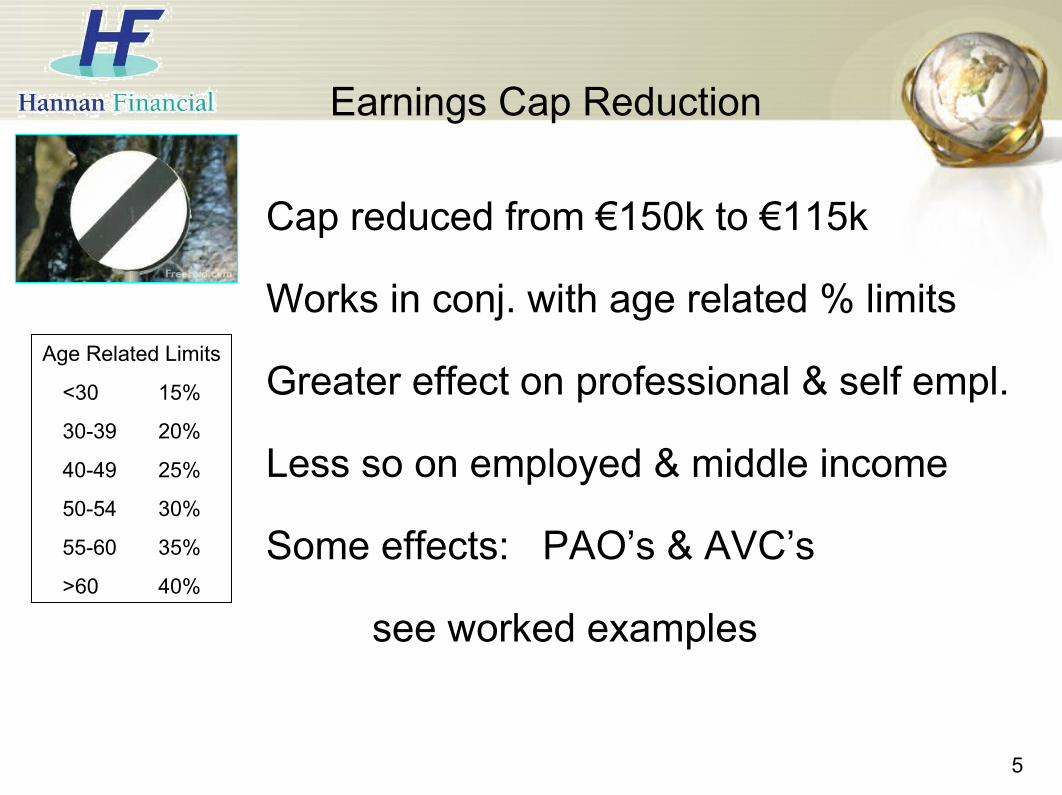

Earnings Cap Reduction

Cap reduced from €150k to €115k

Works in conj. with age related % limits

Greater effect on professional & self empl.

Less so on employed & middle income

Some effects: PAO’s & AVC’s

see worked examples

5

Age Related Limits

<30 15%

30-39 20%

40-49 25%

50-54 30%

55-60 35%

>60 40%

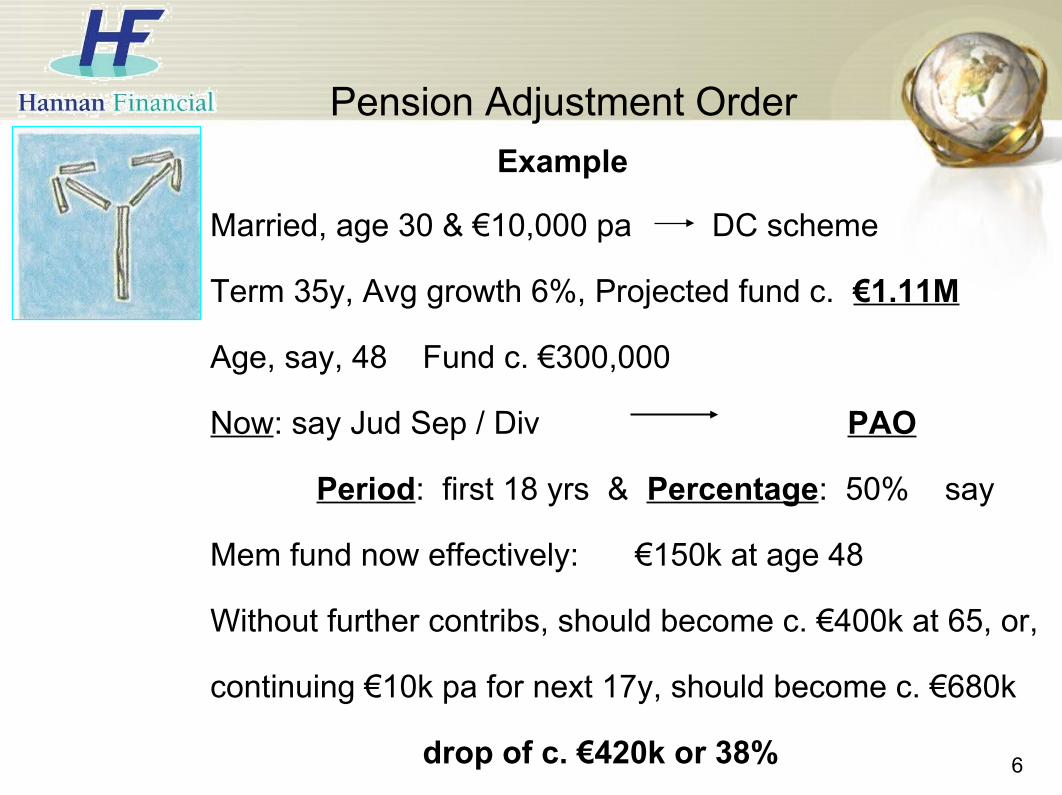

Pension Adjustment Order

Married, age 30 & €10,000 pa DC scheme

Term 35y, Avg growth 6%, Projected fund c. €1.11M

Age, say, 48 Fund c. €300,000

Now: say Jud Sep / Div PAO

Period: first 18 yrs & Percentage: 50% say

Mem fund now effectively: €150k at age 48

Without further contribs, should become c. €400k at 65, or,

continuing €10k pa for next 17y, should become c. €680k

drop of c. €420k or 38% 6

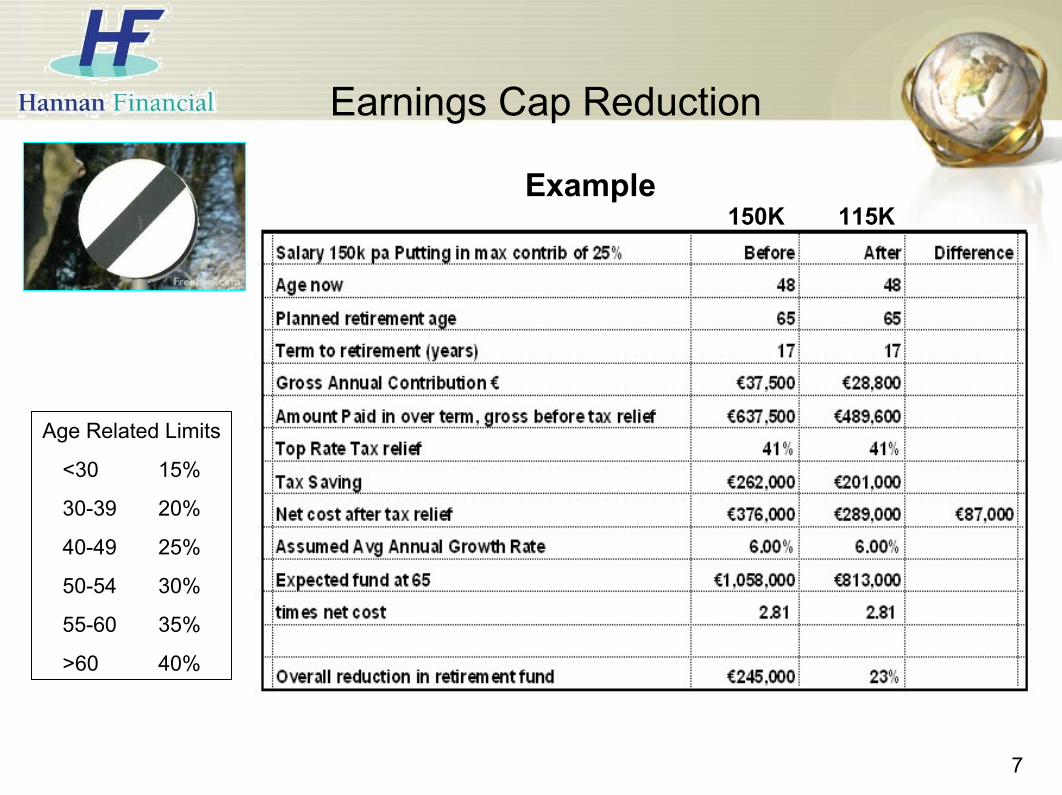

Example

Earnings Cap Reduction

7

Age Related Limits

<30 15%

30-39 20%

40-49 25%

50-54 30%

55-60 35%

>60 40%

Example150K 115K

Tax-Free Lump Sum

Capped at €200k& bal up to €575k at 20%

Potentially affects:

Employees with sal >€133k pa & 20y or more service, &

Prof / Self Emp. with fund value more than €800k

8

Note: better to take lump sum between €200k and €575k & pay 20%, than take as income due to PRSI/USC if taken as income.

Potential PAO issues:

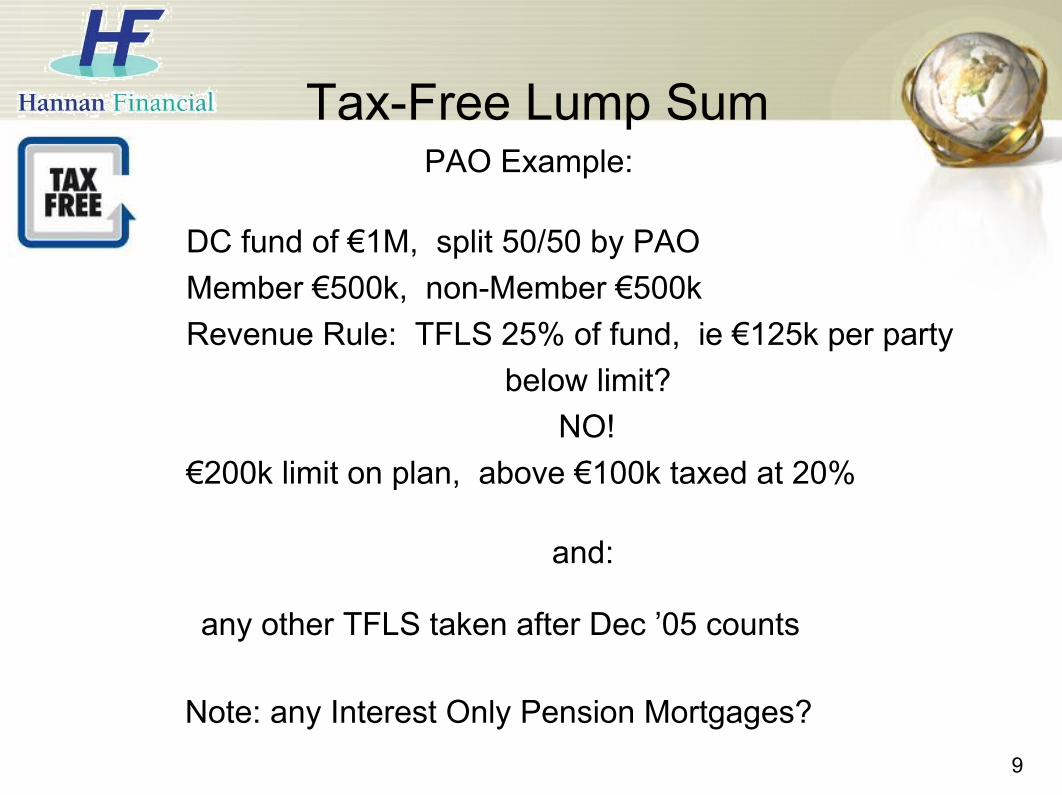

Tax-Free Lump Sum

DC fund of €1M, split 50/50 by PAOMember €500k, non-Member €500kRevenue Rule: TFLS 25% of fund, ie €125k per party

below limit? NO!

€200k limit on plan, above €100k taxed at 20%

9

PAO Example:

and:

any other TFLS taken after Dec ’05 counts

Note: any Interest Only Pension Mortgages?

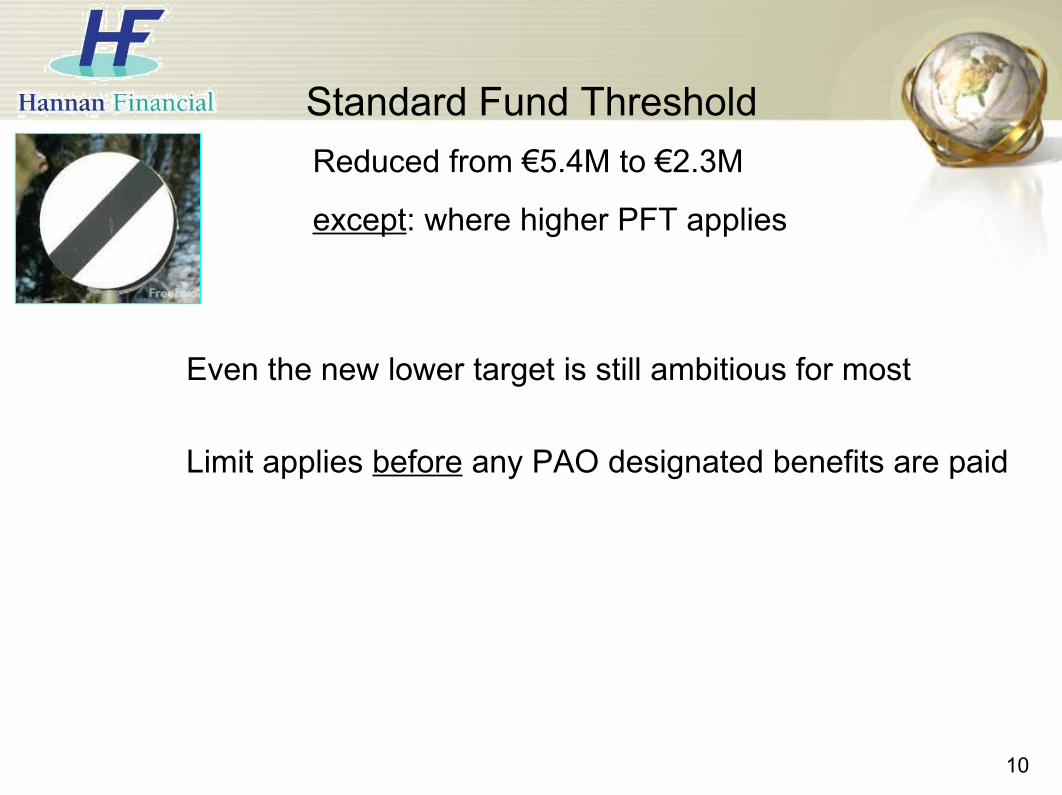

Standard Fund Threshold

Even the new lower target is still ambitious for most

Limit applies before any PAO designated benefits are paid

10

Reduced from €5.4M to €2.3M

except: where higher PFT applies

PRSI, etc

Employee: PRSI & HL relief abolished on contribs

Prof / Self Empl: never had these

11

PAO issues:

more expensive for employee member to rebuild fund

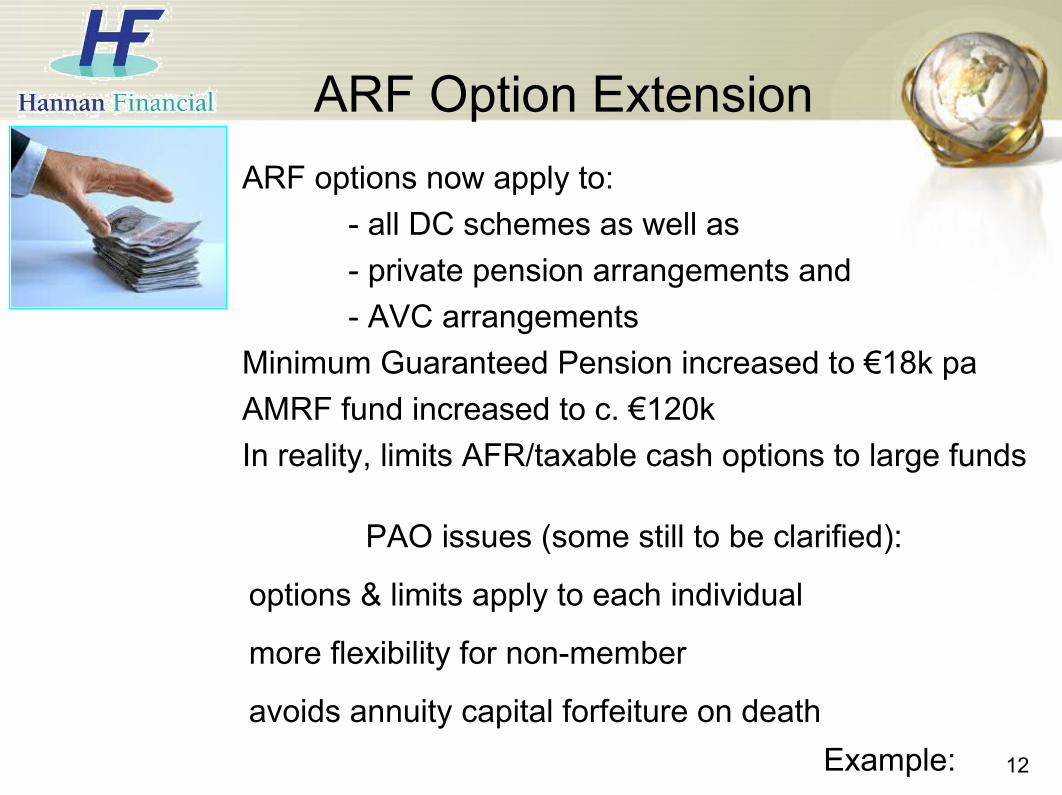

ARF Option ExtensionARF options now apply to:

- all DC schemes as well as- private pension arrangements and- AVC arrangements

Minimum Guaranteed Pension increased to €18k paAMRF fund increased to c. €120kIn reality, limits AFR/taxable cash options to large funds

12

PAO issues (some still to be clarified):

options & limits apply to each individual

more flexibility for non-member

avoids annuity capital forfeiture on deathExample:

ARF Option Example

DC fund €400k, say split 50/50 through PAOnon-member, only State pension at €12k pa

- Takes €50k tax free lump sum- Puts €120k into AMRF (converts to AFR at age 75)

draws interest / growth from AMRF as income- Puts €30k into AFR, with 5% deemed distribution- & Consider PRSA/PRB if income not needed

13

Tick 1

• Finance Bill 2011 issues

14

• Non-member options re PAO’s

• effect of changed member circumstances

• DB schemes – some issues

• role of specialist pensions input

PAO’s - Non-Member Options

Designated Retirement Benefit on DB Scheme- decision at non-member’s sole discretion

(except where member leaves scheme)- leave designated benefit combined with member benefit- create independent entitlement in member’s scheme- split entitlement out into another scheme or pension vehicle

Issues:- DB schemes no longer considered risk-free- benefits include legal trust, funding obligations, generally lower costs, etc- current transfer values heavily discounted- dependency on member decisions 15

PAO’s - Non-Member Options

Designated Retirement Benefit on DC Scheme- decision at trustees’ sole discretion- normally transfer out- into another scheme or pension vehicle

Issues:- more straightforward- investment risk choice at non-member discretion- independent of member decisions- fund & transfer value transparent

16

PAO’s - Non-Member Options

Designated Contingent Benefit (DIS), DB or DC Scheme- apply within 12 months of decree date- no variations- lapses on remarriage of non-member- lapses if member leaves scheme- lapses on member retirement

Issues:- limited benefit

17

Changed Member Circumstances

Changed Member Circumstances- DB scheme member?- early retirement with employer’s consent (or late?)- ill health early retirement- redundancy

Potential Effects on Non-Member- remove any independent benefit or transfer options- compromise actual entitlements- change time frame of entitlements

Suggested Non-Member Strategy- remain alert & informed re member & employer- consider transfer out ahead of likely pivotal events- take professional advice 18

Member – Measures to Rebuild:

Professional / Self Employed- Avail of existing limits- Incorporate where possible (consultants: special situation)

benefit from larger employer contributions

Employed- Avail of limits (AVC’s)- Key employees: special employer contributions)

18

Topical Issues – DB Schemes

19

c. 80% DBS’s closed or closing to new members (Oct ’10)

> 70% now in deficit ref min funding standard (excl. PSS)

Some Issues for DB Schemes:

funding proposals

vastly increased life expectancy

inbuilt rules, harshest being statutory escalation of benefits

affordability for employers (cost / competitiveness)

investment performance

onerous trusteeship & admin regulations

DBS Issues / Risks – PAO’s

20

Currently, Transfer Values very low

Risk: Scheme poss. unable to fulfill promises at retirement date

Risk: Possible reduction in benefits at retirement date

Risk: Change of member plans / circumstances

Funding Proposals

Remain alert & informed (re member & employer)

Pensions Specialist - Role

• Pensions – Professional Risks alleviated• Convenience of a Packaged Service:

Experienced, qualified, insured Summary Info straight into FLCB / AOM Single point of contact re pensions Regular Updates on case progress Reduced emotives

• Focus on legal outcome• Quicker case turn-around & paperwork saving• Defined fee structure

21

As Outsourced Service:

Tick 2

• Finance Bill 2011 issues

22

• Non-member options re PAO’s

• effect of changed member circumstances

• DB schemes – some issues

• role of specialist pensions input