eyes wide open - the importance of a smooth transition to a new eu deal

TRANSCRIPT

1

‘EYES WIDE OPEN’ THE IMPORTANCE OF A SMOOTH TRANSITION TO A NEW EU DEAL

London School of Economics Public Lecture

CBI Director General – Carolyn Fairbairn

Thursday 6 July 2017

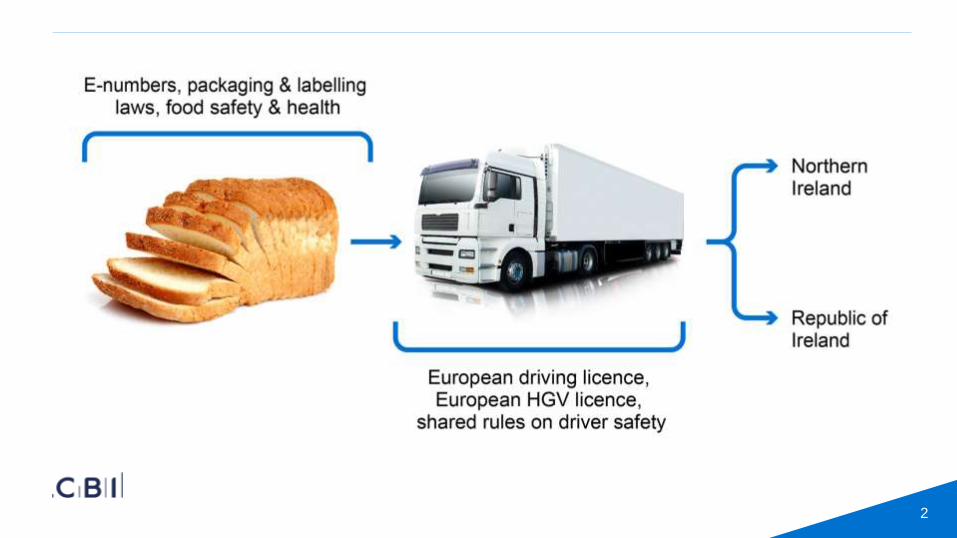

2

3

4

5

THE EU IS THE WORLD’S DEEPEST PREFERENTIAL

TRADE AGREEMENT

Source: “Trading off a ’soft’ and ‘hard’ Brexit”, Mulabdic, Osnago & Ruta; CEPR/World Bank 2017.

Depth of trade agreements: number of legally enforceable provisions

6

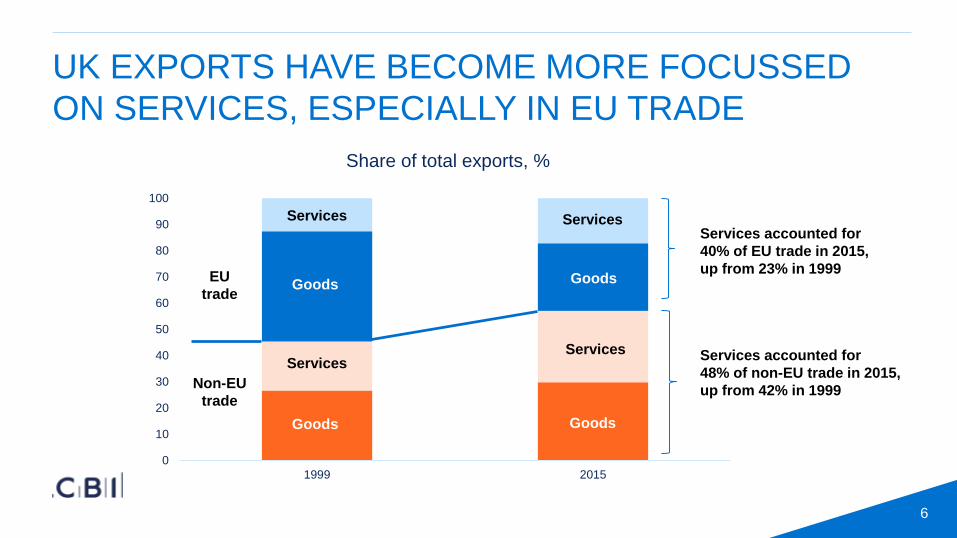

UK EXPORTS HAVE BECOME MORE FOCUSSED

ON SERVICES, ESPECIALLY IN EU TRADE

0

10

20

30

40

50

60

70

80

90

100

1999 2015

Share of total exports, %

Goods

Non-EU

trade

Services

Goods

Services

Services

Goods

Services

Goods

EU

trade

Services accounted for

40% of EU trade in 2015,

up from 23% in 1999

Services accounted for

48% of non-EU trade in 2015,

up from 42% in 1999

7

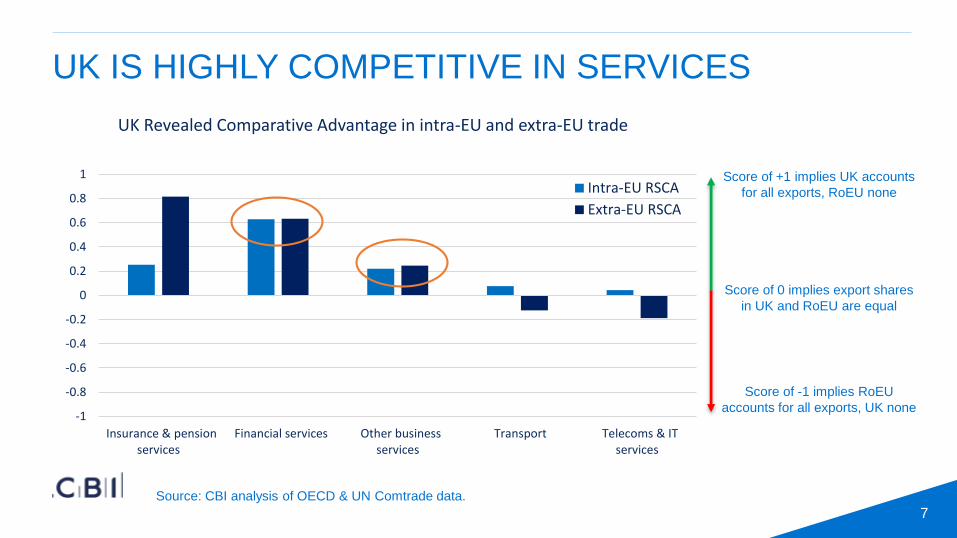

UK IS HIGHLY COMPETITIVE IN SERVICES

Source: CBI analysis of OECD & UN Comtrade data.

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Insurance & pensionservices

Financial services Other businessservices

Transport Telecoms & ITservices

UK Revealed Comparative Advantage in intra-EU and extra-EU trade

Intra-EU RSCA

Extra-EU RSCA

Score of +1 implies UK accounts

for all exports, RoEU none

Score of -1 implies RoEU

accounts for all exports, UK none

Score of 0 implies export shares

in UK and RoEU are equal

8

SOME SECTORS COULD SEE A SIGNIFICANT RISE

IN EXPORT TARIFF COSTS

Source: CBI, Heteronomics; HMRC; OECD.

[CELLRANGE] [CELLRANGE] [CELLRANGE] [CELLRANGE] [CELLRANGE]

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Motor vehicles Agriculture Textiles, clothing & footwear Food, drink & tobacco Chemicals (excl. pharma)

Additional tariff costs depending on UK content in exports

Average MFN tariff across all sectors is 4.3% (average MFN tariff per sector below)

Billions (£)

9

WEAKER POUND IMPROVED COMPETITIVENESS

Source: CBI, Industrial Trends Survey.

-40

-30

-20

-10

0

10

20

30

40

2004 2006 2008 2010 2012 2014 2016

ITS: Has your competitiveness improved or worsened on three months ago?

EU (lhs) Non-EU (lhs) Long-run average

% balance

10

NON-TARIFF BARRIERS BY INDUSTRY

Sources: CBI; World Bank.

138133 132

118

102

85 8276

6052 51

4136

22 22 20 20

9

0

20

40

60

80

100

120

140

160

Non-tariff barriers by sectorChemicals

(ex pharma)

AgricultureMachinery

Aerospace

& defence

11

[CELLRANGE] 222 [CELLRANGE] 26

[CELLRANGE] 62 [CELLRANGE] 310

[CELLRANGE] 100

[CELLRANGE] 100 [CELLRANGE] 510

0

100

200

300

400

500

600

EU EFTA FTA/CustomsUnion

Total FTA &Single Market

US Non-US Total

£bn

44%

5%12%

61%

20%

19%100%

UK GOODS & SERVICES EXPORT BY MARKET TYPE

Sources: Making Brexit Work for British Business, Peter Sands et al.

12

[CELLRANGE]

[CELLRANGE]

[CELLRANGE]

[CELLRANGE]

[CELLRANGE]

[CELLRANGE]

[CELLRANGE]

[CELLRANGE]

[CELLRANGE]

0.0 50.0 100.0 150.0 200.0 250.0 300.0 350.0

Brazil

Russia

Japan

India

China

Rest of Asia

Africa and Middle East

US

EU

Forecasts for UK goods exports over the next 10 years ($, billions)

2016 2026

IN 10 YEARS’ TIME, THE EU WILL STILL BE OUR

BIGGEST EXPORT MARKET FOR GOODS

Source: Oxford Economics.