ey - all tied up working capital management 2015

TRANSCRIPT

All tied upWorking capital managementreport 2015

ForewordAll tied up 2015 is the eighth annual publication in a series of working capital (WC) management reports based on EY research, reviewing the WC performance of the world’s largest companies.

The survey focuses on the top 2,000 companies in the US and Europe, examining their WC performance at a company, regional, industry and country level. It also provides insights into the WC performance of another 2,000 companies in seven other regions and countries. In addition, this report sets out the

of small- and medium-sized enterprises (SMEs) with that of large companies.

Contents

04

Executive summary 05

US and Europe 06

Other regions and countries 11

SMEs and large companies 16

How EY can help 18

Methodology 19

Glossary 20

Contacts 21

All tied up. Working capital management report 2015 3

Key

Change in C2C

WC gap performance

Cash opportunity

29% SMEs’ C2C premium over large companies’

US$1.3t excess WC for leading US and European companies.

US-3% outside US and Europe -2% -2%Europe

2014 vs. 2013

2014

2014

Prime WC drivers

2014 vs. 2013

Oil price US$ Cost of capital

All tied up. Working capital management report 20154

Executive summary

Compared with 2013, our analysis of the WC performance of leading companies in the US and Europe in 2014 reveals an improvement in both regions. For US, C2C1 decreased by 3% from its 2013 level, while Europe shows a reduction of 2%.

However, closer analysis reveals a more complex picture. WC management still receives far greater attention than in the past, as companies continue to take rigorous steps to drive cash and cost out of WC. But as carrying WC became much less costly during the year following the decrease in the cost of capital, some companies may have chosen to trade off WC improvements against sales growth, margin

their suppliers and customers. In addition, factors — such as the sharp fall in the oil price and the relative strength of the US dollar against all major currencies at the end

WC performance in both the US and Europe. By way of illustration, if the oil and gas industry is excluded from our analysis, C2C decreased by 4% in the US and increased by 1% in Europe.

Companies outside the US and Europe also fared better in 2014, with overall C2C dropping by a further 2% — this

metals and mining industries were included or excluded. Six out of seven regions and countries analyzed reported an improvement in WC performance.

Interestingly SMEs fared worse in 2014 than larger companies in the US, reversing a large part of the previous gains observed in previous years.

continue to have huge opportunities to improve in many areas of WC. A high-level comparative analysis indicates that the leading 2,000 US and European companies may have as much as US$1.3 trillion in excess WC, over and above the level they require to operate their

combined sales. In other words, for every US$1 billion in sales, the opportunity for WC improvement is, on average,

relatively simpler steps, such as improving billing and cash collections or extending supplier payment terms, most companies seeking further gains will need to embrace more substantial and sustainable changes in the way they do business and manage their WC.

To achieve this, the changes required will include:

• Ensuring that WC remains a strategic focus throughout the year, with the whole business engaged and incentivized to drive improvement

•to change, with lean and agile manufacturing and supply chain solutions deployed for different products or market segments, as well as through cross-functional cooperation and effective collaboration between participants in the extended enterprise

• Ensuring that supply chains are resilient, through robust risk management policies, alternative sourcing, and enhanced visibility across the end-to-end supply chain

• Ensuring that strong discipline in terms and transactions, internal controls over cash and WC, and appropriate performance measures are in place

• Ensuring that the complex and evolving trade-offs between cash, costs, delivery levels and the risks that each company must take are clearly understood and properly managed

In the short term, we expect WC results to show even wider divergence between businesses in each region and country,

responses to rapidly evolving economic, monetary and

¹C2C: cash-to-cash

All tied up. Working capital management report 2015 5

US and Europe

WC performance improvement in the US and Europe

For the US companies analyzed, C2C1 decreased by 3% from its 2013 level, while Europe shows a reduction of 2%. By way of comparison, C2C was up 1% in the US and

For the US, each WC component contributed to the improvement in overall WC performance in 2014, with DSO and DIO down 2% and 1%, respectively, and DPO up 1%. Europe’s better results came from a higher DPO (up 3%), partially offset by an increase in DIO and DSO (both up 1%).

For each region, a number of factors, some of them

WC trends. They include:

Contrasting economic conditions: For both the US and Europe, WC results for 2014 have continued to be affected by the impact of contrasting economic conditions during the year. Compared with 2013, overall sales growth for leading companies in the US was up 4%, while remaining negative in Europe (down 1%).

US EuropeDSO -2% +1%DIO -1% +1%DPO +1% +3%C2C -3% -2%

Table 1. Change in WC metrics by region, 2014 vs 2013

statementsNote: DSO (days sales outstanding), DIO (days inventory outstanding), DPO (days payable outstanding) and C2C (cash-to-cash), with metrics calculated on a sales-weighted basis

A review of WC performance among the largest companies in the US and Europe reveals an improvement in both regions.

Impact of oil prices: The sharp fall in the oil price in the

WC performance in 2014. If the oil and gas industry is excluded from our calculations (the sector accounting for 11% of total sales in the US and 15% in Europe), C2C decreased by 4% in the US and increased by 1% in Europe from its 2013 level.

Exchange rates movement: Movements in US dollar exchange rates also played some part in driving last year’s WC performance. For companies reporting in US dollars, the relative strength of the US dollar against all major currencies at the end of 2014, compared with its average during the year was a positive contributory factor to WC performance. In contrast, for those reporting in euros, the weakness of that currency against the US dollar had a negative impact on WC performance.

Continued attention to WC management: Many companies in the US and Europe have continued taking steps to drive cash and cost out of WC, in an effort to grow their returns on capital and increase cash returns to shareholders. In some cases, these activities have been prompted by increased pressure from shareholders, including some activists.

Initiatives have focused on streamlining manufacturing and supply chains, collaborating more closely with customers and suppliers, managing payment terms for customers more effectively and improving billing and cash collections. In addition, extending supplier payment terms and driving

along with simplifying functions and processes, have made a contribution to better management of WC.

All tied up. Working capital management report 20156

Company performance reviewA majority of US companies reported improvements in WC performance, compared with less than half of those in Europe.

In the US, 55% of the companies included in our research reported an improvement in WC performance in 2014, compared with 2013. A high proportion of companies reported stronger inventory and receivables performance

better in payables performance. Half of the US companies that showed an improvement in WC performance in 2013 compared with 2012 achieved further progress in 2014.

In Europe, 58% of companies reported a deterioration in WC performance in 2014 compared with 2013. Only 33% and 38% of companies posted better results in receivables and inventory, respectively in 2014. These more than offset the number of those showing stronger payables performance (almost two-thirds). Just over 40% of the companies in Europe that showed an improvement in WC performance in 2013, compared with 2012, achieved further progress in 2014.

Changes in trade-offs between cash, costs, delivery levels and risks: As carrying WC became much less costly during the year following the decrease in the cost of capital, a number of companies in the US and Europe may have also chosen in 2014 to trade off WC improvements against sales growth, margin expansion or increased provision of

Competing WC strategies: With many industries trading with each other, change in WC performance is also

WC strategies. As one company is trying to collect its receivables, its customers are trying to stretch out their payment terms. As one tries to push back supplies, its suppliers are trying to sell and ship more products as fast as possible.

The results for 2014 bring the total reduction in C2C achieved since 2002 to 16% for the US and 21% for Europe. Each of the WC components contributed to this improved performance. In the US, DSO and DIO fell by 9% and 2%, respectively, while DPO rose by 6%. In Europe, DSO and DIO dropped by 11% and 3%, respectively, while DPO

Table 2. WC performance for the US and Europe, 2002-2014

statements

Table 3. Proportion of companies showing improved C2C performance, 2014 vs. 2013

statements

55%

US

42%

Europe

2013 2014

All tied up. Working capital management report 2015

Industry performance reviewIn 2014, there were wide variations in the level and direction of changes in C2C between various industries

contrasting economic growth patterns and movements in commodity prices and exchange rates during the year.

in C2C (down 24% for US and down 28% for European producers), largely as a result of the collapse in the oil price

For the pharmaceutical industry, 2014 was a year of accelerated improvement in WC performance from 2013. Its C2C fell by 4%, driven primarily by further progress in the management of payables, with DPO rising by as much as 15%. Performance in receivables was also improved (DSO down 2%). In contrast, there was a further deterioration in inventory performance, with DIO up 4%.

For automotive suppliers, change in year-on-year C2C was limited, with a decrease of 1% for the companies based in the US and an increase of 1% for those in Europe. However, a closer analysis reveals sharply diverging results by WC

For food producers, and in contrast with the year before, reported WC performance was mixed. Companies based in the US reported a further reduction in C2C (down 2%), while those in Europe saw an increase of 4%.

For chemicals and industrials, WC results diverged between both regions. Performance was positive for companies in the US, but disappointing for those in Europe.

For electric utilities, WC performance in 2014 was heavily

quarter. C2C decreased by 5% in the US and 11% in Europe.

Regional and country performance review US vs. Europe performance comparison

In contrast to the year before, the WC performance gap between the two regions widened in 2014, partly due to exchange rate movements.

A degree of caution is required when comparing WC performances in the US and Europe. Since some of the business done by North American and European companies takes place outside their home regions, their WC results

conditions in the regions where they are based.

The US continued to exhibit much lower levels of WC compared with European-based companies. Overall C2C for the US in 2014 was 1.3 days, or 3.5% below that of Europe. This was primarily due to a strong performance in inventory (minus 3.3 days, or 10%). The differential between receivables and payables cycles (DSO – DPO) across both regions was 1.8 days, with the effect of generally longer trade terms in Europe than in the US being mitigated at the net level. The wide variations in trade terms between Northern and Southern Europe should be noted, however.

2014 vs. 2013

statements

US and Europe (continued)

All tied up. Working capital management report 20158

There are many possible causes for the gap in WC performance between the US and European regions: companies in Europe tend to have more SKUs (stock keeping units) to serve different markets and customers

absence of national borders and a unique trading currency. Transport also takes longer and logistics costs are higher in Europe than in the US.

That said, our expectation is that with the trend toward globalization in sales and procurement and sharing of common leading WC practices, the WC performance gap between the US and Europe will narrow in coming years.

European country performance comparisons

Of the seven main sub-regions and countries in Europe, WC performance was better for three, worse for three

However, if the Oil and gas industry is excluded from our calculations, WC performance would have improved only for one sub-region and country, stayed the same for one

Benelux reported the biggest reduction in C2C among the main sub-regions and countries in Europe, with a drop of 16% (9% when the Oil and gas industry is excluded). Food producers and retailers reported improved results, but consumer electronics companies and telecommunications operators scored particularly poorly.

US EuropeDSO 49.4DIO 30.4DPO 31.9 45.6C2C 36.1 37.4

Table 5. WC changes by European sub-region and country, 2014 vs. 2013

statements

with C2C down 6%. However, had the oil and gas industry been excluded from our calculations, performance would have deteriorated, with C2C up 1%. Pharmaceuticals reported further progress, while aerospace and defense was again disappointing.

For Germany, WC performance was worse (C2C up 2%), adversely affected to some extent by the relative strength of the US dollar. These poor results came from an increase in both DSO and DIO (up 3% and 4%, respectively), partly

companies and telecommunications operators all reported a deterioration in WC performance. In contrast, electric utilities achieved strong progress.

For France, overall WC performance remained unchanged, but would have deteriorated (C2C up 4%) had the oil and gas industry been excluded. Industrial companies reported a deterioration in WC performance. In contrast, food producers and retailers achieved good progress.

Switzerland saw a deterioration in WC compared with 2013, with C2C up 2%. This was primarily due to a poor showing from one major food company (C2C up 12%), while results diverged between two large pharmaceutical companies.

For the Nordic and Southern European countries, WC performance continues to be heavily skewed toward the performance of certain industries. The Nordic countries reported poor results (C2C up 3%), depressed by the performance of chemical and telecommunications equipment companies. However, electric utilities put in a much better showing, while industrial and paper

Southern European countries registered a strong

and gas industry been excluded, results would have been

further their C2C, while electric and gas utilities saw a deterioration in performance.

All tied up. Working capital management report 2015 9

*WC scope = sum of tarde receivables, inventories and accounts payable

Opportunity for improvementThe wide variations that our research reveals in WC performance between companies in each regional industry

to an aggregate of up to US$1.3 trillion of cash for the leading 2,000 US and European companies.

WC cash opportunity derived for each company. This has been calculated by comparing the 2014 performance of each of its WC components with that of the average (low estimate) and the upper quartile (high estimate) achieved by its industry peer group.

Table 6. WC changes by European sub-region and country, 2014 vs. 2013

statements* Greece, Italy, Portugal and Spain** Belgium, Luxemburg and the Netherlands

On this basis, the 1,000 US companies included in this research would have in total between US$385 billion and

an amount equivalent to between 12% and 21% of their WC

and accounts payable) and between 3% and 6% of their aggregate sales.

The 1,000 European companies would have in

unnecessarily tied up in WC, equivalent to between 11%

aggregate sales.

In total, the leading 2,000 US and European companies would have up to US$1.3 trillion of cash unnecessarily tied

Our “cash potential” analysis reveals that the opportunity is distributed across the various WC components, with 35% available from both receivables and payables and 30% from inventory.

treated with a degree of caution, as they are based on an external view of each company’s WC performance within its industry (based on public consolidated numbers). The top end of each range is likely to be ambitious, as it ignores differences in commercial strategies (impacting cash discounts and payment terms), customer base, supply, product mix, country sales exposure and local practices for payment terms, which can vary widely, especially across

the opportunity is calculated for each company’s WC component by comparing its performance not against the best performer, but against the top quartile of its industry peer group.

Cash opportunity

RegionValue % WC scope* % sales

Average Upper quartile Average Upper quartile Average Upper quartileEurope 11% 19% 4%United States US$385b 12% 21% 3% 6%

US and Europe (continued)

All tied up. Working capital management report 201510

Other regions and countries

Improvement in WC performance in 2014

It is worth noting that if we exclude the oil and gas and metals and mining industries (oil and gas and metal and mining which accounted for 23% of total sales in 2014) from our calculations, the year-on-year change in C2C remained the same.

Last year’s stronger WC performance was due to better results in receivables and inventories (DSO and DIO down 1% and 2%, respectively), partly offset by a weaker showing in payables (DPO down 1%). Excluding the oil and gas and metal and mining industries, year-on-year changes in C2C and for each WC metric remained the same.

excluding the oil and gas and metal and mining industries) posted an improvement in WC performance compared with 2013. Only Asia scored worse, but performance in this

and metal and mining industries. It is also worth noting that India showed better results, but this was primarily due to a strong improvement in the WC performance of its oil and gas and metal and mining industries.

there were wide variations between countries in the degree of year-on-year change in C2C.

improvement in WC performance in 2014 compared to 2013, with C2C falling by 2%.

Regions and countries

2014 Change 2014 vs. 2013

Asia 34 6%Aus/NZ 26 -4%Canada -1%CEE -9%India 45 -6%Japan 61 -2%LatAm 26 -8%Other regions 42 -2%

Regions and countries

2014 Change 2014 vs. 2013

Asia 39 0%Aus/NZ 25 -8%Canada 30 -1%CEE 38 -1%India 66 1%Japan 62 -2%LatAm 28 -3%Other regions 46 -2%

Regions and countries

2014 Change 2014 vs. 2013

China 14 54%Indonesia 64 -2%Malaysia 59 4%Singapore 62 4%South Korea 1%Taiwan 42 9%Thailand 24 14%C2C 34 6%

Table 8. Change in C2C, 2014 vs. 2013

Table 9. Change in C2C excluding the oil and gas and metal and mining industries, 2013-2014

Table 10. Change in C2C per Asian country, 2014 vs. 2013

statementsAll tied up. Working capital management report 2015 11

Regions and countries

2014 Change 2014 vs. 2013

China 6 -8%Indonesia 64 -2%Malaysia 59 4%Singapore 68 5%South Korea 58 0%Taiwan 41 10%Thailand 35 8%C2C 34 1%

2014 Change 2014 vs. 2013

Argentina 11 -44%Brazil 32Chile 34 1%Colombia 8Mexico 16 -18%C2C 26 -8%

2014 Change 2014 vs. 2013

Argentina 16 -38%Brazil 30Chile 36 3%Colombia 5 32%Mexico 20 12%C2C 28 -3%

Table 11. Change in C2C per Asian country, excluding the oil and gas and metal and mining industries, 2014 vs. 2013

Table 12. Change in C2C per LatAm country, 2014 vs. 2013

Table 13. Change in C2C per LatAm country, excluding the oil and gas and metal and mining industries, 2014 vs. 2013

A review of the WC performance of the largest companies

variations overall and for each individual metric. These variations would have been even larger had the oil and gas and metal and mining industries been excluded from our calculations.

It is worth noting, however, that regional and country comparisons should be approached with a particular nuance in mind. Since some of the business carried out by top country-headquartered companies takes place outside

global market conditions, as well as those in the regions where they are based.Table 14. WC metrics by main region and country

Asia Aus/NZ Canada CEE India Japan LatAmDSO 41 39 39 45 44 69 35DIO 36 31 36 42 31DPO 43 43 44* 44 50 40C2C 34 32 25 37 45 61 26

DSO-DPO -2 -4 nm 1 -2 19 -5

*Includes accrued expenses

Table 15. WC metrics by main region and country, excluding the oil and gas and metal and mining industries

Asia Aus/NZ Canada CEE India Japan LatAmDSO 49 34 42 53 40DIO 38 29 30 35 51 42 33DPO 48 38 42* 50 52 52 45C2C 39 25 30 38 66 62 28

DSO-DPO 1 -4 nm 3 15 20 -5

Other regions and countries (continued)

All tied up. Working capital management report 201512

Table 16. WC metrics by Asian country

China Indonesia Malaysia Singapore South Korea Taiwan ThailandDSO 28 32 55 41 55 55 33DIO 35 62 42 33 28DPO 49 30 38 36 32 50 36C2C 14 64 59 62 57 42 24

DSO-DPO -21 2 5 23 5 -3

China Indonesia Malaysia Singapore South Korea Taiwan ThailandDSO 42 32 55 43 56 33DIO 62 42 63 33 41DPO 31 38 38 32 52 39C2C 6 64 59 68 58 41 35

DSO-DPO -30 1 5 25 4 -6

Table 18. WC metrics by LatAm country

Argentina Brazil Chile Colombia MexicoDSO 38 40 39 21 28DIO 33 38 19 23DPO 65 41 44 32 35C2C 11 32 34 8 16

DSO-DPO -1 -5 -11

Table 19. WC metrics by LatAm country, excluding the oil and gas and metal and mining industries

Argentina Brazil Chile Colombia MexicoDSO 43 43 42 21 33DIO 31 32 41 25 29DPO 59 45 48 41 43C2C 16 30 36 5 20

DSO-DPO -16 -2 -5 -20 -10

All tied up. Working capital management report 2015 13

Looking at 2014 WC performance, India, Japan and CEE exhibit the highest C2C among these regions and countries, scoring particularly poorly in receivables and inventories. In contrast, Australia/New Zealand and LatAm carry the lowest C2C, thanks to strong results in receivables and inventories.

Japan also shows the highest differential between receivables and payables cycles (DSO vs. DPO), while Asia and Australia/New Zealand exhibit the lowest.

DIO are among the lowest globally.

WC comparisons among industries across regions and countriesAn analysis of WC performance by industry across other regions and countries, and in comparison with the US and Europe, reveals substantial divergences, exacerbated by

For example, the WC performance of food producers in other regions is much weaker (with the notable exception of China and India) than in the US and Europe. As well as

with a dispersed customer base and operate comparatively

The oil and gas industry also exhibits wide variations in WC performance between the different regions and countries, partly due to differences in business models, with companies operating at various points in the value chain. For example, oil and gas companies in Japan are mostly

those involved in exploration and production.

Factors behind the WC performance variationsIndustry bias. For some regions and countries, WC results

industries. For example, the oil and gas and metal and mining industries represent as much as 44% and 42% of total sales of our sample of companies for India and CEE, respectively, but only 6% for Japan. Electric utilities and telecommunications services account for 16% of sales in Latin America, but for only 9% in Australia and New Zealand. Steel accounts for 8% and 5% of sales in India and Asia, respectively, but for only 1% in the US and 2% in Europe.

Payment practices. Payment practices vary widely across

in the length of payment delays and incidence of defaults can also be observed between regions and countries. While payment usage plays a role, these differences can also be explained by local behaviors, as well as by variations in the degree of effectiveness of credit management policies and legal enforcement procedures.

of logistics and distribution varies greatly across regions

supply chain costs, service levels and risks, as well as in WC performance.

According to the World Bank’s 2014 ranking of logistics

slowly catching up with the high-performers, but the logistics performance gap between the two groups remains wide. The US, most European countries and Japan are among the top 10 countries (out of 160), while the other Asian economies rank among the top quartile (with China being the 28th). Interestingly, India’s position in the ranking has fallen in the past two years from being the 46th in 2012 to the 54th in 2014.

Focus on cash and effectiveness of WC management processes. There are fundamental differences in the intensity of management focus on cash and the effectiveness of WC management processes among these

commercial and industrial strategies deployed (with some businesses choosing to grow sales, increase investment or enhance service rather than improve WC performance for example), as well as differences in the degree of business and process maturity among companies.

Other regions and countries (continued)

All tied up. Working capital management report 201514

Interestingly, machinery makers report high levels of WC

nature of this industry.

Steel companies in both Asia and Australia/New Zealand carry the lowest levels of C2C, while their counterparts in CEE, LatAm and Japan display much higher levels.

In the case of telecommunications services, WC performance in individual regions and countries varies

between pre-paid and post-paid on the other hand, as well as by local payment practices, payment methods and levels of capital expenditure.

Table 20. WC metrics by industry across main regions and countries

C2C Asia Aus/NZ Canada CEE India Japan LatAm US EuropeAutomotive supplies 41 nm 33 56 50 60 65 34 54Building materials 54 61 56 83 44 91 50 51Chemicals 46 65 46 85 92 6 63Electric Utilities 33 20 10 35 52 24 34Food producers 52 43 58 61 40 38 30Industrials* 61 nm nm nm 89Machinery makers 113 nm 120 nm 103 125 108 83Oil and gas 20 23 -5** 30 15 52 19 4 20Steel 64 54 124 63 83 83Telecommunications -45 41 2** 11 -34 49 2 13 -3

** Includes accrued expenses

All tied up. Working capital management report 2015 15

SMEs and large companies

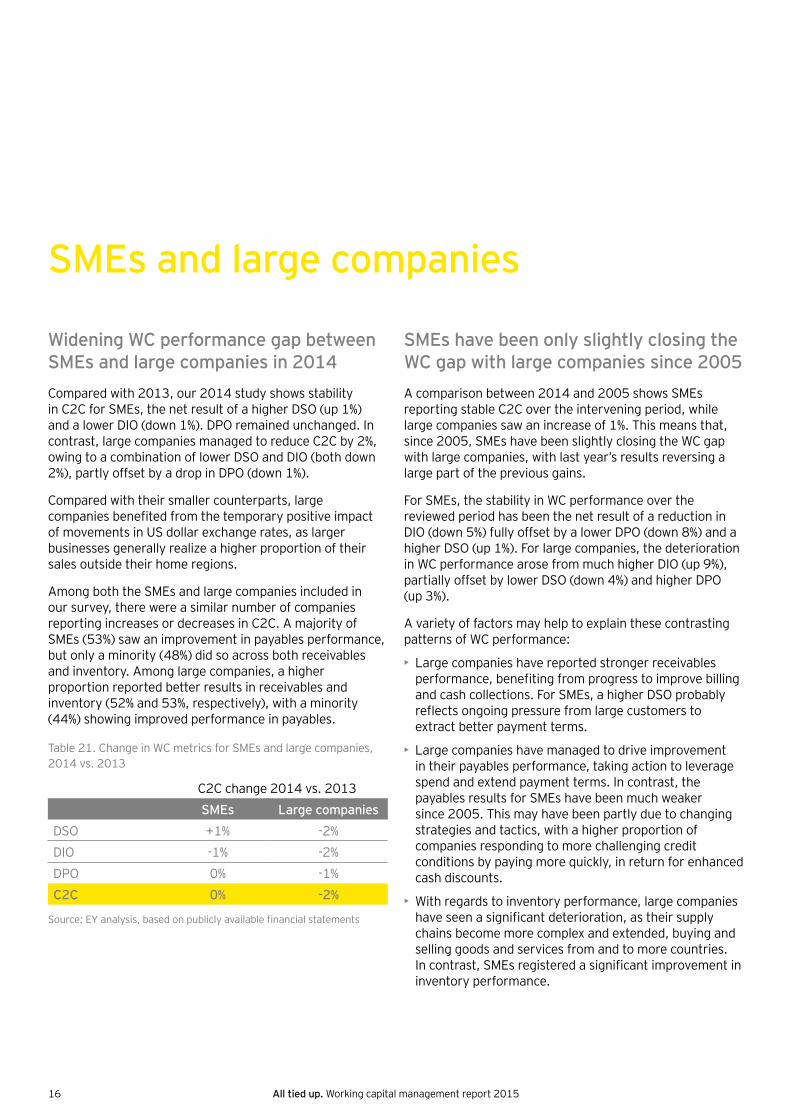

Widening WC performance gap between SMEs and large companies in 2014

SMEs have been only slightly closing the WC gap with large companies since 2005 A comparison between 2014 and 2005 shows SMEs reporting stable C2C over the intervening period, while large companies saw an increase of 1%. This means that, since 2005, SMEs have been slightly closing the WC gap with large companies, with last year’s results reversing a large part of the previous gains.

For SMEs, the stability in WC performance over the reviewed period has been the net result of a reduction in DIO (down 5%) fully offset by a lower DPO (down 8%) and a higher DSO (up 1%). For large companies, the deterioration in WC performance arose from much higher DIO (up 9%), partially offset by lower DSO (down 4%) and higher DPO (up 3%).

A variety of factors may help to explain these contrasting patterns of WC performance:

• Large companies have reported stronger receivables

and cash collections. For SMEs, a higher DSO probably

extract better payment terms.

• Large companies have managed to drive improvement in their payables performance, taking action to leverage spend and extend payment terms. In contrast, the payables results for SMEs have been much weaker since 2005. This may have been partly due to changing strategies and tactics, with a higher proportion of companies responding to more challenging credit conditions by paying more quickly, in return for enhanced cash discounts.

• With regards to inventory performance, large companies

chains become more complex and extended, buying and selling goods and services from and to more countries.

inventory performance.

Compared with 2013, our 2014 study shows stability in C2C for SMEs, the net result of a higher DSO (up 1%) and a lower DIO (down 1%). DPO remained unchanged. In contrast, large companies managed to reduce C2C by 2%, owing to a combination of lower DSO and DIO (both down 2%), partly offset by a drop in DPO (down 1%).

Compared with their smaller counterparts, large

of movements in US dollar exchange rates, as larger businesses generally realize a higher proportion of their sales outside their home regions.

Among both the SMEs and large companies included in our survey, there were a similar number of companies reporting increases or decreases in C2C. A majority of SMEs (53%) saw an improvement in payables performance, but only a minority (48%) did so across both receivables and inventory. Among large companies, a higher proportion reported better results in receivables and inventory (52% and 53%, respectively), with a minority (44%) showing improved performance in payables.

C2C change 2014 vs. 2013SMEs

DSO +1% -2%DIO -1% -2%DPO 0% -1%C2C 0% -2%

Table 21. Change in WC metrics for SMEs and large companies, 2014 vs. 2013

All tied up. Working capital management report 201516

Much higher current C2C for SMEs than for large companies

SMEs continue to exhibit much higher C2C than large companies. In 2014, SMEs’ C2C was 29% (equivalent to 14 days) higher than that of large companies on a sales-weighted basis.

Compared with SMEs, large companies enjoy superior

the view that scale provides greater opportunities to negotiate favorable payment terms with customers and suppliers. SMEs scored slightly better than their larger counterparts in inventory management. Several factors may explain the difference in performance. For example, SMEs may have simpler product offerings and supply chains. Large companies are also more likely than smaller companies to sell outside their home regions, potentially giving rise to longer lead times and excess safety stocks. On the other hand, lean practices and vendor-managed inventory arrangements are more widespread among large companies. Increased use of outsourcing may have also

remains unclear how much of the WC performance gap between SMEs and large companies is due to SMEs’ reluctance to engage more openly with other participants in the value chain.

Comparing the relative WC performance of large companies and SMEs in the same industry highlights that SMEs in almost two-thirds of industries have higher C2C than large companies. In 2014, the median C2C

large companies was 11 days (median being used as a more appropriate measure in this case, given the uneven distribution of companies by industry).

The most meaningful variations at a C2C level for major industries are reported in the table below. Among electrical components, clothing companies and chemical, for

SMEs in the oil equipment industry display lower C2C (-25%) than their larger peers.

Performance by company Performance by industry

% daysDSO 22% 9DIO (9%) (3)DPO (28%) (8)C2C 29% (14)

Table 22. WC metrics differential between SMEs and large companies, 2014

Table 23. C2C differential by industry between SMEs and large companies, 2014

C2C differential% days

Electrical components 69% 39Clothing and fabrics 31Chemical 35% 22Communication technology 29%Software 18% 8Semiconductors 13%

11% 8Oil equipment -25% -24

All tied up. Working capital management report 2015

How EY can helpEY’s global network of dedicated working capital professionals helps clients to identify, evaluate and prioritize actionable improvements to liberate

changes to commercial and operational policies, processes, metrics and procedure adherence

We can assist organizations in their transition to a cash-focused culture and help implement the relevant metrics. We can also identify areas for

then assist in implementing processes to improve forecasting and create the frameworks to sustain those improvements.

WC improvement initiatives are also typically earnings-accretive. In addition to increased levels of

productivity improvements, reduced transactional and operational costs and from lower levels of bad and doubtful debts and inventory obsolescence. Improved processes also increase the quality of services both internally and externally. Wherever you do business, our WC professionals are there to help.

All tied up. Working capital management report 201518

performance of the largest 4,000 companies (by sales) headquartered in the US (consisting of 1,000 companies), Europe (1,000) and seven other main regions and countries — Asia (600); Australia and New Zealand (100); Canada (300); Central and Eastern Europe (150); India

the WC performance of SMEs with that of large companies. Using sales as the indicator of each company’s size, SMEs

under US$1 billion, while large companies are those with sales exceeding US$1 billion. A total of 1,000 companies (all domiciled in the US for comparison purposes) were analyzed, evenly divided between the two sub-groups.

•2014 reports. Performance comparisons have been made with 2013 and with the previous eleven years in the case of the US and Europe, and eight years for SMEs and large companies.

• The review on which the report is based is segmented by region, country, industry and company. It uses metrics to provide a clear picture of overall WC management and to identify the resulting levels of cash opportunity.

• Each of the companies analyzed in this research has been allocated to an industry and to a region or country. Reported global, regional and country numbers are sales-weighted.

•auto manufacturing industry (OEMs) is also excluded due

activities.

• The performance trends at the country and industry level need to be treated with a degree of caution: the approach is based on consolidated numbers in the absence of further local details, with each company being allocated to the location of its headquarters.

• Because of differences in industry weightings and in the level of international activity within each economy, an analysis of the WC performance gap across countries in Europe would not have been useful or meaningful.

• The WC performance metrics are calculated from the

and consistent as possible, adjustments (see glossary)

of acquisitions and disposals and off-balance sheet arrangements.

Methodology

All tied up. Working capital management report 2015 19

• DSO (days sales outstanding): year-end trade receivables net of provisions, including VAT and adding back

by full-year pro forma sales and multiplied by 365 (expressed as a number of days of sales, unless stated otherwise)

• DIO (days inventory outstanding): year-end inventories net of provisions, divided by full-year pro forma sales and multiplied by 365 (expressed as a number of days of sales, unless stated otherwise)

• DPO (days payable outstanding): year-end trade payables, including VAT and adding back trade-accrued expenses, divided by full-year pro forma sales and multiplied by 365 (expressed as a number of days of sales, unless stated otherwise)

• C2C (cash-to-cash): equals DSO, plus DIO, minus DPO (expressed as a number of days of sales, unless stated otherwise)

• Pro forma sales: reported sales net of VAT and adjusted for acquisitions and disposals when this information is available

Glossary

All tied up. Working capital management report 201520

ContactsWorking Capital Services contacts

AustraliaWayne BoultonT: +61 3 9288 8016E: [email protected]

FranceArthur WastynT: +33 1 55 61 01 55E: [email protected]

FinlandGösta Holmqvist

IndiaAnkur Bhandari

IsraelNir Ben-David

Matias De San PabloT: +54 1143 181531E: [email protected]

SwedenPeter StenbrinkT: +46 8 5205 9426E: [email protected]

BeneluxDeniz Ates

Nicolas Beaumont

AsiaAlvin TanT: +65 6309 8030E: [email protected]

GermanyDirk Braun

Bernhard WendersT: +49 211 9352 13851E: [email protected]

CanadaSimon RockcliffeT: +1 416 943 3958E: [email protected]

Chris Stepanuik

UK and Ireland

Matthew Evans

USEdward Richards

Peter Kingma

Mark Tennant

Hye Yu

All tied up. Working capital management report 2015 21

All tied up. Working capital management report 201522

All tied up. Working capital management report 2015 23

EY | Assurance | Tax | Transactions | AdvisoryAbout EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and

develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of

by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s Transaction Advisory Services

position tomorrow. We work with clients to create social and economic value by helping them make better, more informed decisions about strategically managing capital and transactions in fast-changing markets. Whether you're preserving, optimizing, raising or investing capital, EY’s Transaction Advisory Services combine a unique set of skills, insight and experience to deliver focused advice. We help you drive competitive advantage and increased returns through improved decisions across all aspects of your capital agenda.

© 2015 EYGM Limited. All Rights Reserved.

EYG no. DE0621

ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for

ey.com