export strategy manufacture of pulp, paper,...

TRANSCRIPT

This project is co-financed by the European fund for Regional Development through Operational programme “Development of the competitiveness of the Bulgarian economy” 2007 - 2013

Export Strategy

for sector

“MANUFACTURE OF

PULP, PAPER, BOARD,

AND ARTICLES”

Bulgarian Small and Medium Enterprises

Promotion Agency

2012

Operational programme “Development of the

Competitiveness of the Bulgarian Economy” 2007-2013, Priority

axis 4.2. “Strengtening the International market positions of

Bulgarian economy” Project № BG161РО003 – 4.2.01-0001

“Promotion of the Internationalization of the Bulgarian

Enterprises”

Page 2 of 130

This document was developed under project № BG161РО003 – 4.2.01-0001

“PROMOTION OF THE INTERNATIONALIZATION OF THE BULGARIAN

ENTERPRISES”.

Beneficiary: Executive agency for promotion of small and medium

enterprises.

This document was developed with the financial support of Operational

programme “ Development of the competitiveness of the Bulgarian economy”

2007 - 2013 co-financed by the European fund for Regional Development. The

overall responsibility of the document’s content lies with the Executive agency

for promotion of small and medium enterprises and under no circumstances it

can be accepted that this document reflects the official statement of the European

Union and the Contracting authority.

Page 3 of 130

CONTENTS:

INTRODUCTION .......................................................................................................................9

APPROACH FOR COMPOSING THE EXPORT STRATEGY OF THE SMALL AND

MEDIUM ENTERPRISES IN THE SECTOR „MANUFACTURE OF PULP, PAPER,

BOARD, AND ARTICLES” ....................................................................................................11

MAIN CONCLUSIONS OF THE ANALYSIS OF THE CURRENT SITUATION ..........18

MACROECONOMIC CHARACTERISTICS OF THE PRIORITY BULGARIAN

EXPORT MARKETS. BILATERAL TRADE RELATIONS ..............................................68

SWOT AND PESTEL ANALYSES – SECTOR “MANUFACTURE OF PULP, PAPER,

BOARD AND ARTICLES ” ....................................................................................................89

STRATEGIC GOALS FOR STIMULATION OF THE EXPORT BY SMALL AND

MEDIUM ENTERPRISES FROM THE „MANUFACTURE OF PULP, PAPER,

BOARD, AND ARTICLES” SECTOR ...................................................................................96

STRATEGY FOR STIMULATION OF THE EXPORT OF SMEs FROM THE SECTOR

...................................................................................................................................................100

ACTION PLAN – SECTOR „MANUFACTURE OF PULP, PAPER, BOARD, AND

ARTICLES” ............................................................................................................................103

SYSTEM FOR MONITORING AND CONTROL ..............................................................115

SOURCES ................................................................................................................................129

Page 4 of 130

List of tables:

Table 1 SMEs in the economic activity during 2009 (based on CEA-2008) /according to

data of NSI/ .................................................................................................................................20

Table 2 SMEs in the economic activity during 2010 (based on CEA-2008) /according to

data of NSI / ................................................................................................................................20

Table 3 Regional distribution of the enterprises and employees in the “ Manufacture of

pulp, paper, board and articles” sector in 2009 ...........................................................................21

Table 4 Value of the Bulgarian export of “Paper, board and articles of paper and board”

under the nomenclature of CEA /2000 – 2011/ (according to data of NSI) ................................23

Table 5 Value of the export of SMEs from the sector /2007 – 2011/ (according to data of

NSI) .............................................................................................................................................25

Table 6Value of the sector export of Bulgaria, according to the Combined Nomenclature

/2007 – 2011/ (according to data of NSI) ....................................................................................25

Table 7 Comparative analysis of the Bulgarian export from the activity /2005 - 2009/ .......26

Table 8 Consumption of paper and board by countries and by years during the period 1990 -

2010 (kg/person) .........................................................................................................................29

Table 9 Leading partners in the export by commodity groups in the “ Manufacture of pulp,

paper, board and articles” sector for the period 2000-2010 (million EUR) ................................46

Table 10 Characterization and structure of the division........................................................49

Table 11 Analysis for 2005. ..................................................................................................61

Table 12 Analysis for 2006 ...................................................................................................61

Table 13 Analysis for 2007 ...................................................................................................61

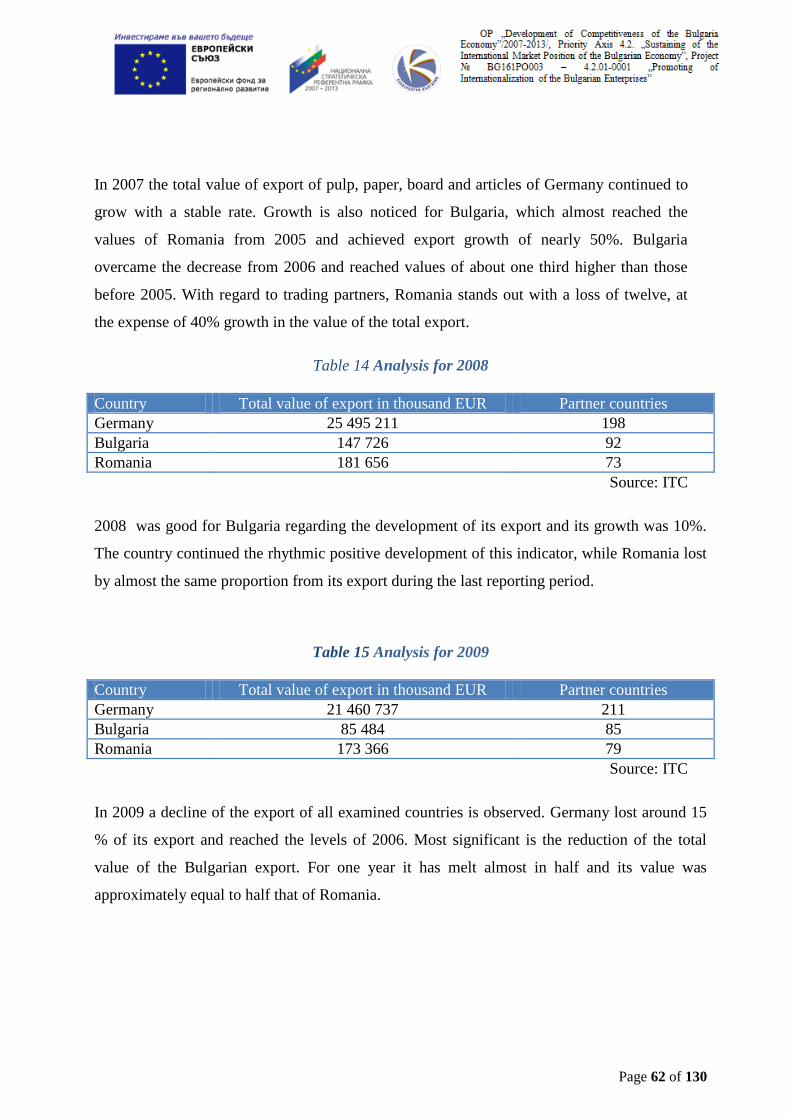

Table 14 Analysis for 2008 ...................................................................................................62

Table 15 Analysis for 2009 ...................................................................................................62

Table 16 Leading partners in the export of Bulgaria in the “ Manufacture of pulp, paper,

board and articles” sector for the period 2000 - 2010 (million EUR) .........................................67

Table 17 Main economic indicators for Germany and bilateral trade relations with Bulgaria

.....................................................................................................................................................68

Table 18 Main economic indicators for France and bilateral trade relations with Bulgaria .70

Table 19 Main economic indicators for Italy and bilateral trade relations with Bulgaria ....71

Page 5 of 130

Table 20 Main economic indicators for Romania and bilateral trade relations with Bulgaria

.....................................................................................................................................................74

Table 21 Main economic indicators for Greece and bilateral trade relations with Bulgaria.76

Table 22 Main economic indicators for Turkey and bilateral trade relations with Bulgaria 79

Table 23 Main economic indicators for Serbia and bilateral trade relations with Bulgaria ..79

Table 24 Main economic indicators for Macedonia and bilateral trade relations with

Bulgaria .......................................................................................................................................81

Table 25 Main economic indicators for Russia and bilateral trade relations with Bulgaria .82

Table 26 SWOT and LOED analyses .................................................................................90

Table 27 PESTEL-analysis ...................................................................................................92

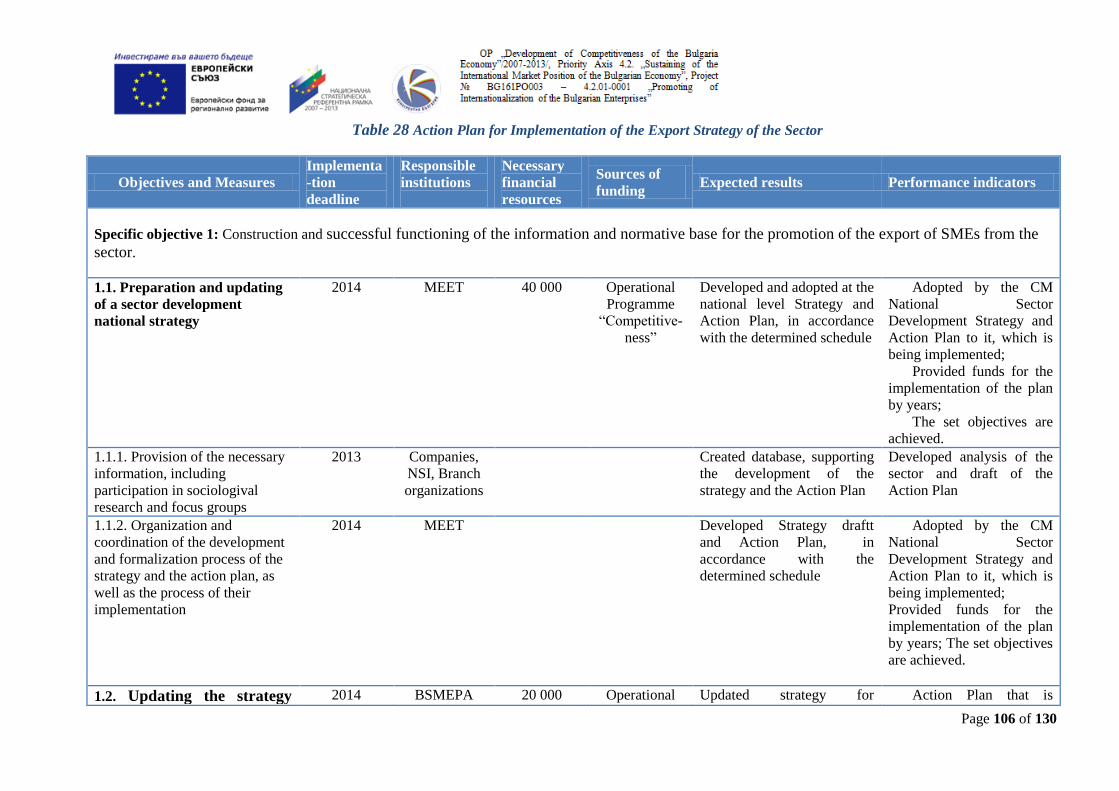

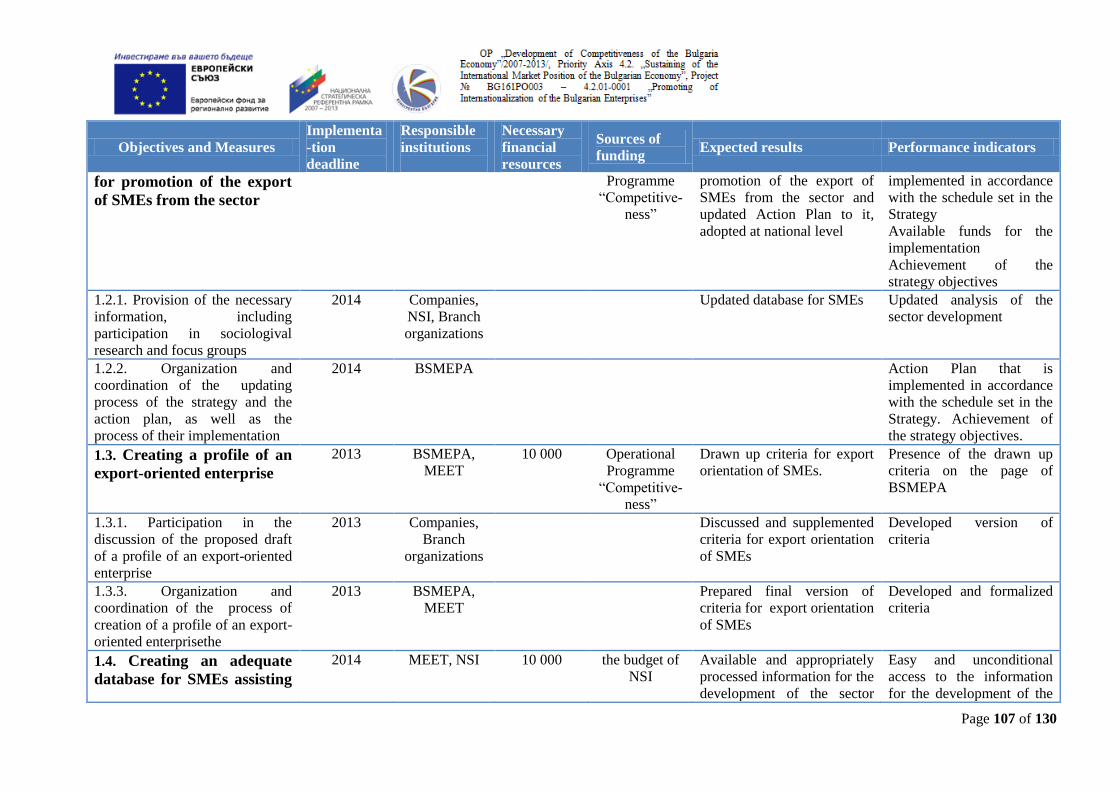

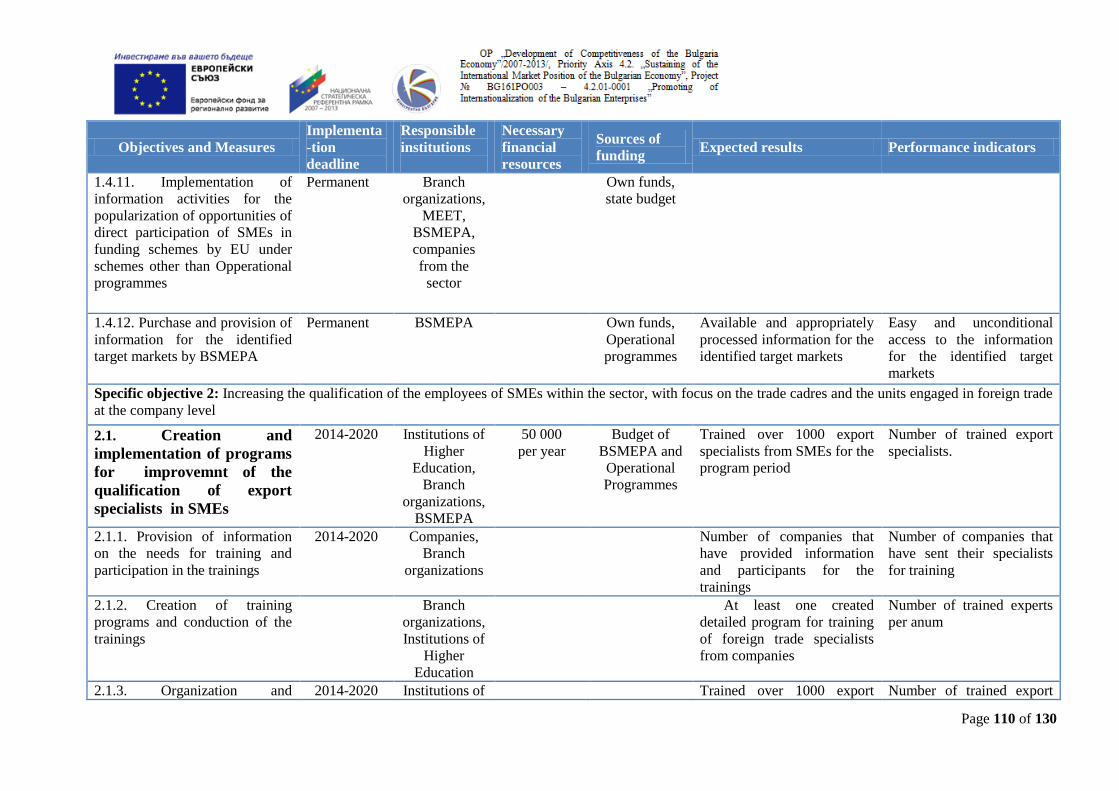

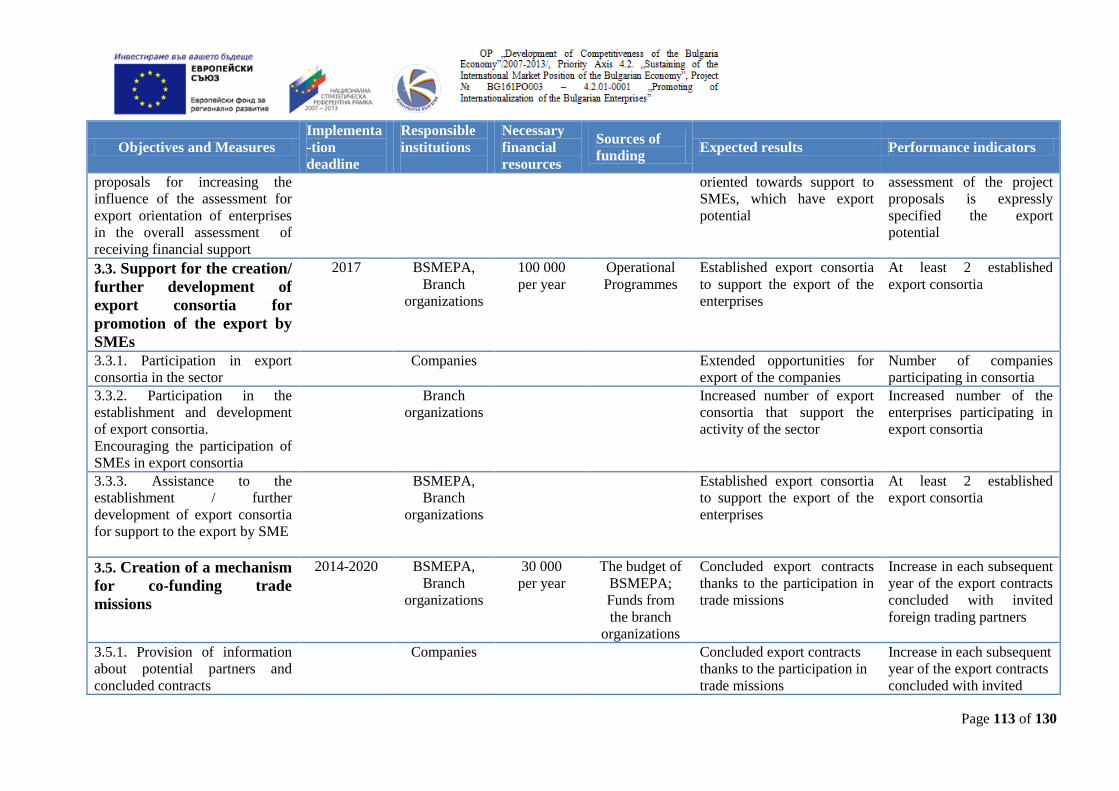

Table 28 Action Plan for Implementation of the Export Strategy of the Sector .................106

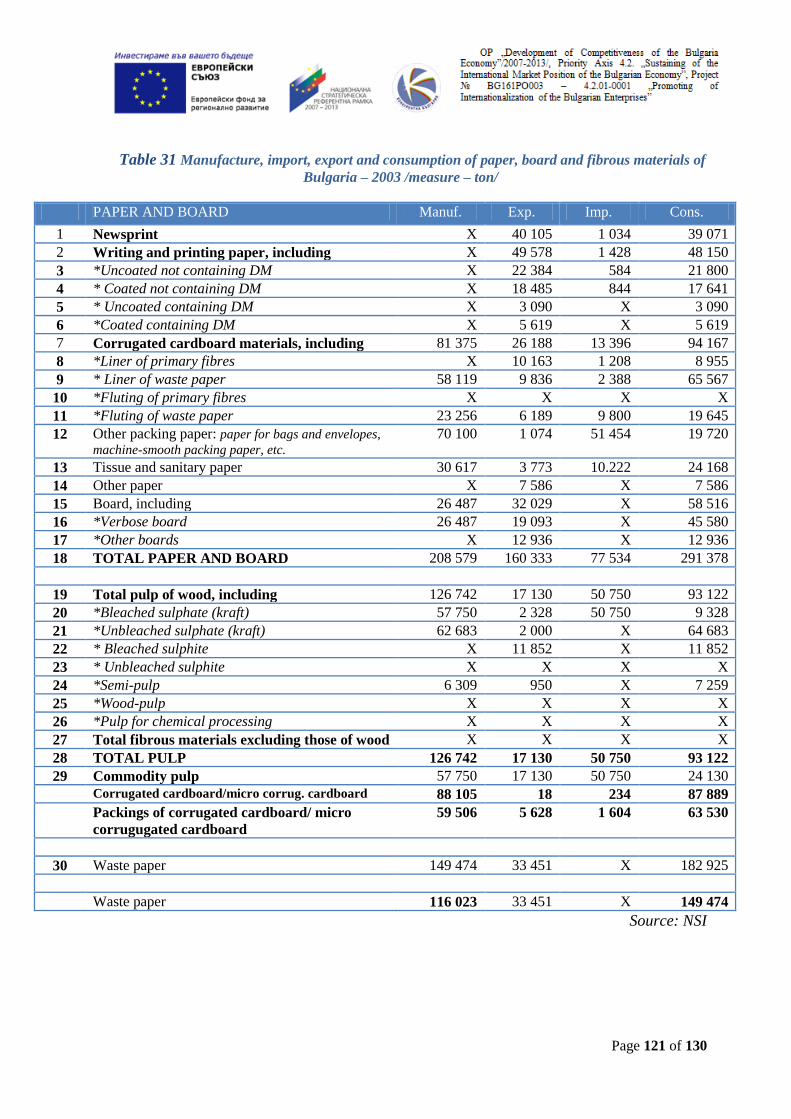

Table 29 Manufacture, import, export and consumption of paper, board and fibrous

materials of Bulgaria – 2001 /measure – ton/ ...........................................................................119

Table 30 Manufacture, import, export and consumption of paper, board and fibrous

materials of Bulgaria – 2002 /measure – ton/ ...........................................................................120

Table 31 Manufacture, import, export and consumption of paper, board and fibrous

materials of Bulgaria – 2003 /measure – ton/ ...........................................................................121

Table 32 Manufacture, import, export and consumption of paper, board and fibrous

materials of Bulgaria – 2004 /measure – ton/ ...........................................................................122

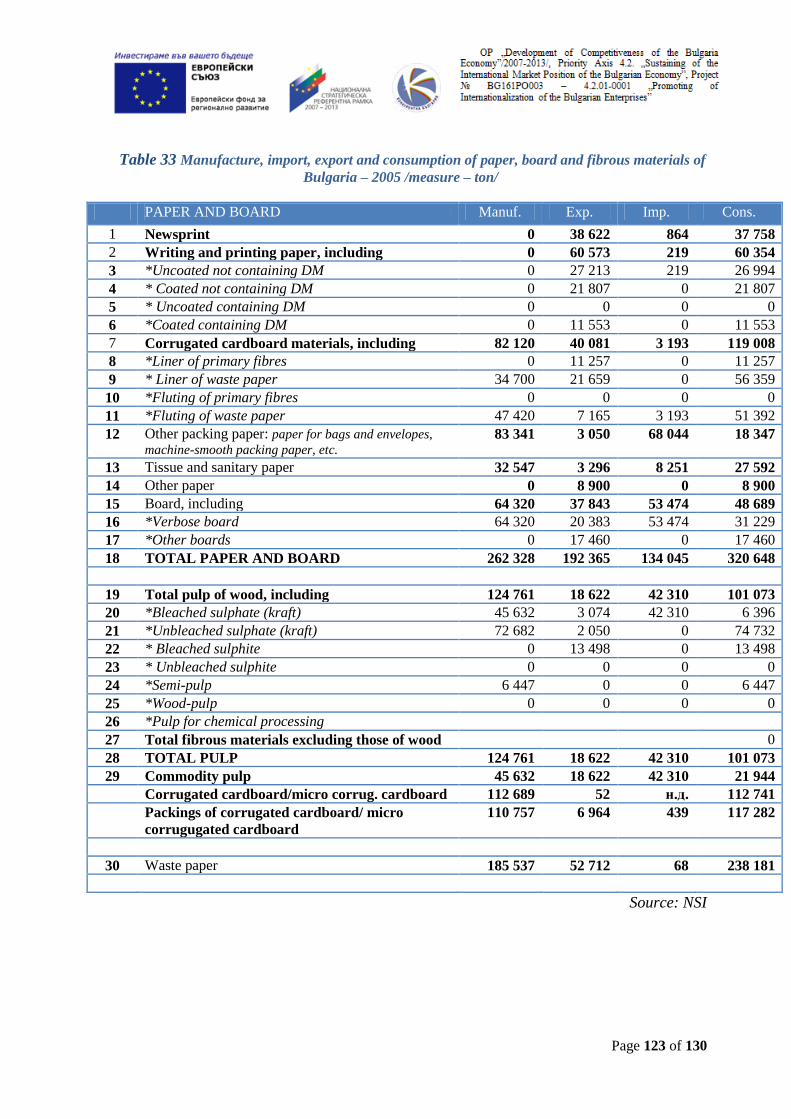

Table 33 Manufacture, import, export and consumption of paper, board and fibrous

materials of Bulgaria – 2005 /measure – ton/ ...........................................................................123

Table 34 Manufacture, import, export and consumption of paper, board and fibrous

materials of Bulgaria – 2006 /measure – ton/ ...........................................................................124

Table 35 Manufacture, import, export and consumption of paper, board and fibrous

materials of Bulgaria – 2007 /measure – ton/ ...........................................................................125

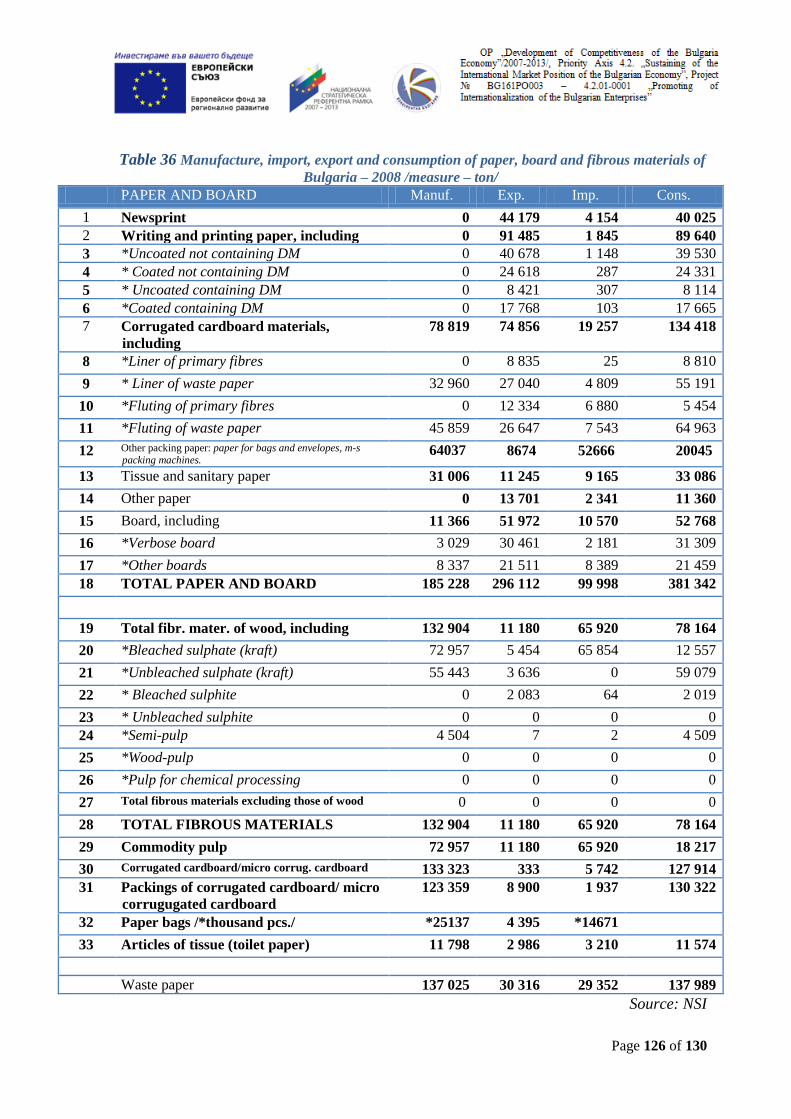

Table 36 Manufacture, import, export and consumption of paper, board and fibrous

materials of Bulgaria – 2008 /measure – ton/ ...........................................................................126

Table 37 Manufacture, import, export and consumption of paper, board and fibrous

materials of Bulgaria – 2009 /measure – ton / ..........................................................................127

Table 38 Manufacture, import, export and consumption of paper, board and fibrous

materials of Bulgaria – 2010 /measure – ton/ ...........................................................................128

Page 6 of 130

List of Graphs:

Graph 1 Export of “Paper, board and articles of paper and board”.......................................24

Graph 2 Summarized data about the export of the different products in the sector /in

thousand EUR/ ............................................................................................................................27

Graph 3 Average values of components in the formation of the final price in the sector

/2010, according to data of CEPI/ ...............................................................................................28

Graph 4 Value of Bulgarian export of paper and board (with pigmental coating) /in

thousand EUR/ ............................................................................................................................31

Graph 5 Value of Bulgarian export of writing (printing) paper / in thousand EUR/ ............32

Graph 6 Value of Bulgarian export of toilet paper, napkins, handkerchiefs /in thousand

EUR/ ............................................................................................................................................34

Graph 7 Value of Bulgarian export of cigarette paper /in thousand EUR/ ...........................36

Graph 8 Value of Bulgarian export of all types of paper labels /in thousand EUR/ .............37

Graph 9 Value of Bulgarian export of paper for household and sanitary needs /in thousand

EUR/ ............................................................................................................................................38

Graph 10 Value of Bulgarian export of packings of paper and board /in thousand EUR/ ....39

Graph 11 Value of Bulgarian export of newsprint /in thousand EUR/ .................................41

Graph 12 Value of Bulgarian export of cards and envelopes /in thousand EUR/ .................43

Graph 13 Value of Bulgarian export of micro-crepe, perforated paper, board, corrugated

cardboard /in thousand EUR/ ......................................................................................................44

Graph 14 Value of Bulgarian export in the three major areas – works of the printing

industry, pulp, paper and board /in million EUR/ .......................................................................45

Graph 15 Estimated data for export increase /2009-2013/ (in thousand EUR) .....................52

Graph 16 Main international partners of EU-27 regarding export /2007/ .............................55

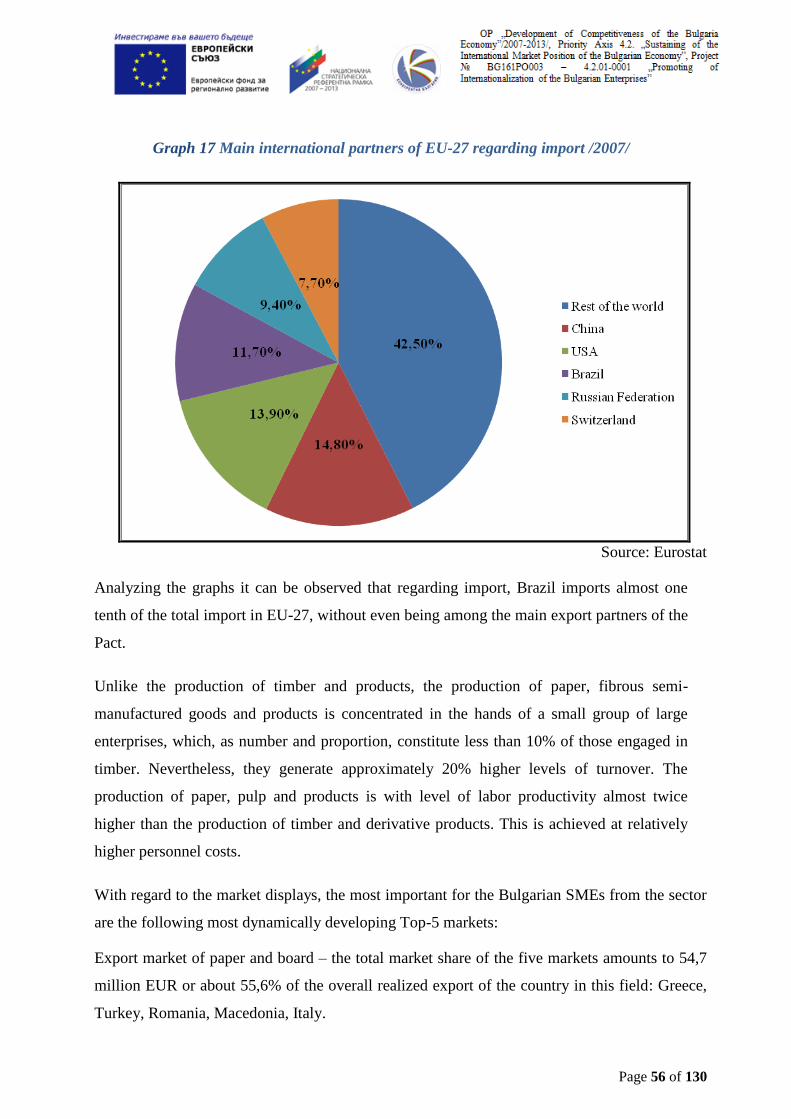

Graph 17 Main international partners of EU-27 regarding import /2007/ ............................56

Graph 18 Top-5 markets for which Bulgaria exports – paper and boards /according to data

of NSI, as at 2010/ .......................................................................................................................57

Graph 19 Top-5 markets for which Bulgaria exports – pulp /according to data of NSI, as at

2010/ ............................................................................................................................................57

Graph 20 Top-5 markets for which Bulgaria exports – works of the printing industry

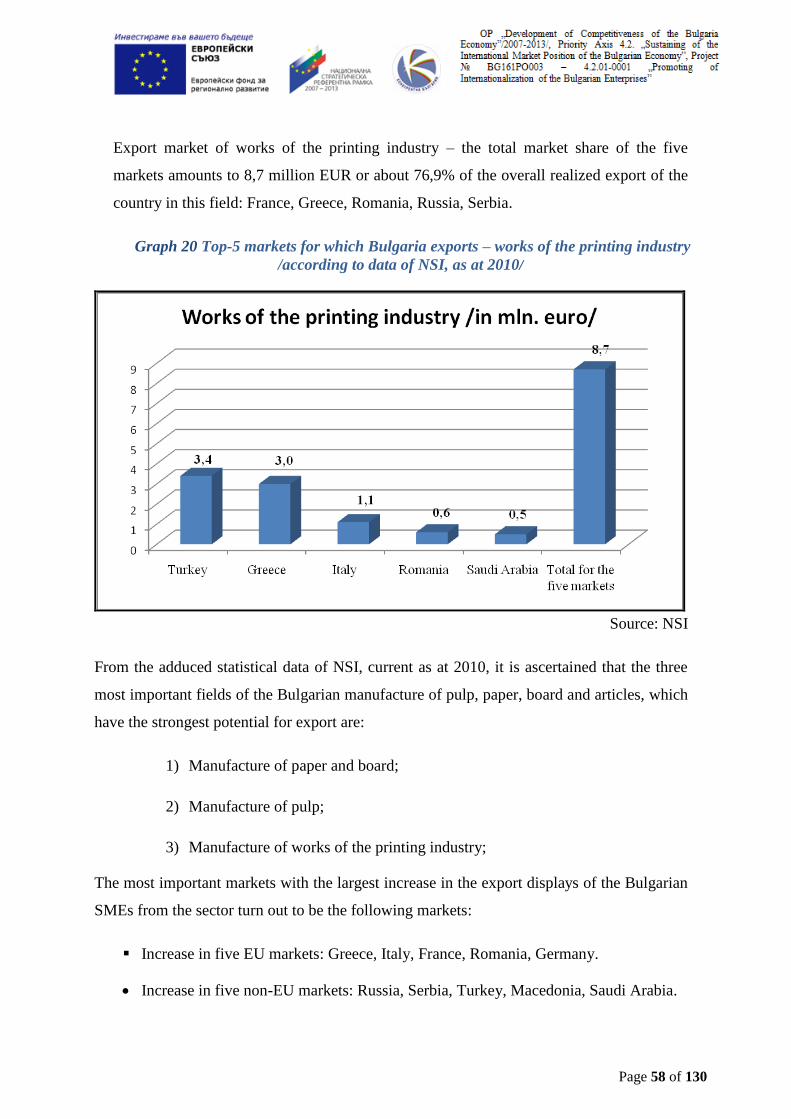

/according to data of NSI, as at 2010/ .........................................................................................58

Page 7 of 130

Graph 21 Export markets of the enterprises surveyed (in %) ...............................................59

Graph 22 Percentage distribution of the export by the number of the export markets .........59

Graph 23 Development of the export of Bulgaria and Romania /2005 - 2009/ (in thousand

EUR) ............................................................................................................................................63

Page 8 of 130

List of Abbreviations:

BSMEPA Bulgarian Small and Medium Enterprises Promotion Agency

MEET Ministry of Economy, Energy and Transport

SMEs Small and Medium Enterprises

CM Council of Ministers

ITC International Trade Center

NSI National Statistical Institute

GDP Gross Domestic Product

EC European Commission

EU European Union

EU-27 the 27 Member States of the European Union

CEA Classifier of Economic Activities

CN Combined Nomenclature

CEPI Confederation of European Pulp Industries

NACE Classification of economic activities in the European Community

Page 9 of 130

INTRODUCTION

The Export Strategy for the “Manufacture of pulp, paper, board and articles” sector was

developed under Project № BG161РО003 – 4.2.01-0001 № BG161РО003 – 4.2.01-0001

“Promotion of the internationalization of the Bulgarian enterprises”, under priority axis 4

„Strenghtening the international market positions of Bulgarian economy”, under Operational

Programme “Development of the Competitiveness of the Bulgarian Economy”, in pursuance of

Contract BG-161PO003-4.2.01-001-C00001 for direct provision of gratuitous financial help,

under which the Bulgarian Small and Medium Enterprises Promotion Agency (BSMEPA) is

an institutional beneficiary.

The purpose of the Export Strategy for the “Manufacture of pulp, paper, board and articles”

sector is to support the Bulgarian micro-, small and medium enterprises from the sector to

enhance their competitiveness, the degree of their internationalization and entering or

expanding the market positions of Bulgarian products and in particular those with higher added

value.

Bulgarian state, in the person of BSMEPA, MEET and other state institutions, has recognized

the sector of SMEs as particularly sensitive one and at the same time crucial for the economic

life, which should be given special attention. Diversity in the development of individual sectors

in the economy, in whose development SMEs have their place, and national priorities related to

the promotion of the export of the country, necessitate the development of export strategies for

different sectors, one of which is “Manufacture of pulp, paper, board and articles”. Focusing on

the support and giving precise references for state intervention through its institutions and

providing options for development for the other participants in the process will reinforce in a

positive aspect the planning principle in the activities of the State and will ultimately improve

Page 10 of 130

the work in the sector. As a result of the successful implementation of the Export Strategy is

expected an improvement when enetering international markets and actively expanding and

strengthening the market positions of Bulgarian small and medium enterprises realizing their

main economic activities in the “Manufacture of pulp, paper, board and articles” sector.

In the preparation of this strategy, in particular consideration was taken the document

“Methodology for strategic planning”, which has been prepared by the Council for

Administrative Reform to the Council of Ministers /CM/ of Republic of Bulgaria.

Page 11 of 130

APPROACH FOR COMPOSING THE EXPORT STRATEGY OF THE

SMALL AND MEDIUM ENTERPRISES IN THE SECTOR

„MANUFACTURE OF PULP, PAPER, BOARD, AND ARTICLES”

The Export Strategy is a strategic document that defines medium-term objectives and priorities

in export development of SMEs from the “Manufacture of pulp, paper, board and articles”

sector. It was developed on the grounds of the strategic planning approach, which has the

following advantages when skilfully used:

Creates an understanding among interested parties on trends and what the future may

bring;

Establishes a common vision and consensus among interested parties by coordinating

particular initiatives in selected targets;

Identifies undertaken or planned projects and activities;

Strengthens partnership between government, business and other parties for solving

complex problems.

When developing such strategic document it is crucial to give exact formulation of the ‘owner’

of the strategy, i.e. institution or institutions that shall be responsible for overall implementation

of the strategic document, as well as the ones for the particular steps of strategic planning.

In general steps for preparation strategic documents are as follows:

Assigning;

Preparing;

Development;

Coordination;

Adoption;

Implementation;

Valuation;

Update.

Each of these steps includes certain activities and some of them, such as assigning, preparing,

development, coordination, adoption and update later on shall be a part of the project executed

under the contract referred in the beginning. Therefore the main ‘owner’ of the Export Strategy

is the Bulgarian Small and Medium Enterprises Promotion Agency. For this reason, the goals,

measures and specific actions set in the strategic document should first assist BSMEPA to

Page 12 of 130

improve the planning and implementation of the activities related to the support of the export of

SMEs in the sector “Manufacture of pulp, paper, board and articles”. This formal logic does

not contradict to the fact that a significant number of institutions, businesses and even the

population of the country, which can be impacted through different mechanism, for example

government departments – through the forms of coordination of strategic documents of such

rank, branch organizations and business – through the provision of incentives to increase their

export potential, are recognizeded as interested parties. Crucial for SMEs from the the sector

“Manufacture of pulp, paper, board and articles” is the abilty to see a clear and predictable

policy by the state which supports export and which in a medium term will allow them to

decide whether they will take advantage of the opportunities given to them or not.

Strategic Planning Technology

The process of strategic planning includes the following steps:

Identification of interested parties;

Analysis of the environment;

SWOT analysis;

Vision;

Defining goals;

Choosing an alternative – development strategy;

Action plan;

Monitoring system.

Each of these steps is characterized by its particularities, namely:

Identification of interested parties. Interested party is any person or group that requires

attention, is able to affect a certain decision, can contribute with resources or to be affected by a

certain decision. Involving interested parties at an early stage from the preparing of the

strategic document may lead to a more expressed consensus on goals and bigger willingness for

endorsing taken decisions. Interested parties in the Export Strategy may include different

people and organizations: companies, state administration, associations of producers, individual

businesses, users of respective products, non-governmental organizations and experts.

A specificity in the preparation of strategies designed to support business is the rule that the

prepared documents should not support some businesses and discriminate against others

Therefore, as in attracting business organizations and individual branch associations has

Page 13 of 130

manifested desire for equality, in the analyses is sought an opportunity that a maximum number

of business benefit from them.

Analysis of the environment. The analysis of the environment (the SWOT analysis is

composed on the grounds of the conclusions of this analysis) enables laying down of objectives

and priorities that have to align efforts and not to be separated by time and environment.

The analyses focus on:

The current state of development of the sector in Bulgaria, trends, dynamics and

growth;

Characteristics of export-oriented SMEs, including regional distribution;

Status of the export of goods and services;

Analysis of goods and services, for which the sector has export advantages or

export potential;

Assessment of these industries that have the greatest potential for increasing the

added value in the export of goods and services in which Bulgaria has a global market

share;

Size of the international market;

Competitiveness of the export of goods and services for the existing and potential

foreign market;

Share of products originating in Bulgaria;

Share of the Bulgarian export for the product group in the total import volume on

the world market;

Leading importing countries in the relative sector;

Values and volumes of the import on specific foreign markets for a specific product

group;

Major suppliers on the relative market;

Identification of barriers to the internalization of the sector.

Based on the prepared analyses, the problems and achievements of the sector at present should

be clearly defined, but also some forecasts, opportunities and perspective for development

should be justified, such as:

Achieving significant growth of Bulgarian goods in total, as well as of those with

higher added value.

Page 14 of 130

Identification and prioritization of target markets by commodity groups.

Forecast for the development of the export and import of goods and of the trade

balance for the next five and more years.

The prepared analysis are based on existing analytical and program documents, available

statistics and information from sociological serveys conducted – interviews and focus groups.

The analysis of the environment describes existing condition of SMEs in the “Manufacture of

pulp, paper, board and articles” sector and the export process, determines reasons that cause

problems in development and outlines directions for future development.

SWOT analysis. The SWOT analysis enables identification of major internal factors

differentiated as ‘strengths and weaknesses’ and of external factors – ‘opportunities and

threats’, helps formulation of strategic goals, priorities and measures. Using SWOT keeps us

from setting unachievable tasks and priorities for export development of small and medium

enterprises in Sector “Manufacture of pulp, paper, board and articles” during the period of the

Strategy.

Using SWOT analysis to develop an Export Strategy has its own specificity, because the

‘owner’ of the strategy is BSMEPA, but the analysis is focused on the export process of SMEs

from this sector, and not on the institution itself.

PESTEL analysis. There are many factors and “variables” that affect directly or indirectly on

business environment in the country, and the overall state of the manufacturing industry. Tax

rates, changes in laws, trade barriers and administrative requirements, political and social

trends are of the type of macro factors that have noticeable effects on the operation of the

enterprises.

PESTEL analysis is focused on analyzing the factors and trends at the macro level, influencing

the development of the Bulgarian manufacturing industry, SMEs and in particular Sector

“Manufacture of pulp, paper, board and articles”.

Using this analysis will provide key conclusions for the positioning and planning the

development of SMEs in the sector.

Defining goals. Strategic planning is focused on issues of critical importance, opportunities and

problems faced by the export of small and medium enterprises in Sector ‘Manufacture of pulp,

paper, board and articles’. It helps to outline the solutions that are actually important from the

ones with temporary impact.

Page 15 of 130

Defining goals by building an hierarchical tree of goals is an operating tool that allows working

out the details from the most common general goals to the specific ones.

Defining the general strategic goal is particularly important for the future development of the

export of SMEs in Sector “Manufacture of pulp, paper, board and articles”, as it shows the

vision of institutions and business to the future. The general strategic goal seeks to answer one

fundamental question – “How do main institutions and interested parties in the process want

the export of SMEs in the sector to look in the long run?”.

Approaching the level of specific targets enables to reach the answers to the questions ‘who’,

‘what’ and ‘when’, in order to guarantee achievement of the goals identified higher in the

hierarchy.

Choosing an alternative – development strategy. Ways for goals achievement are searched for

after they are determined. Experience shows that this may be done by different ways that

represent particular alternatives for development and reaching identified goals. At this stage of

strategic planning particular alternatives shall be evaluated from different points of view and

criteria and as a result of this one alternative shall be selected and it shall become the

development strategy.

Action plan. Chosen strategy should be dressed in certain actions and measures that are

bounded by terms, persons in charge, executors and financials. The action plan and the

measures foreseen in it are turning this strategic instrument into everyday work and

implementation of policy for assisting the export of SMEs in Sector “Manufacture of pulp,

paper, board and articles”.

Monitoring system. The last phase of the strategic planning process is monitoring and

evaluation of the progress for implementation of general and specific goals set in the Export

Strategy and in the action plan. Monitoring is important, because it enables undertaking

correction actions, if the progress is unsatisfactory or if the conditions change. It is important to

make reports on the progress in achievement of general goals and before the public and

business so that they are able to evaluate the work of the respective institutions and interested

parties when realizing the strategy. We have to note that often influences may not be visible or

evident and this makes their measurability more difficult. Furthermore, impact often is an effect

with accumulation and this may complicate the analysis. This gives special weight of

monitoring that is tightly connected to all implementation steps of the Export Strategy –

preliminary (ex ante), current (parallel to the realization) and subsequent (ex post) evaluation.

Page 16 of 130

In order to exercise monitoring of the Export Strategy implementation and to evaluate

achieved results in accordance with the identified goals, it is necessary to use a few

indicators that have to be set in advance or at least early enough with respect to

implementation of the strategic document, in order data received from them to be used. In

most cases those shall be aimed values that in aggregated mode shall correspond to the goals

of the strategic document.

Monitoring provides feedback that helps to identify success or failure of planned document.

For the realization of the monitoring process, it is necessary to determine the following:

Monitoring indicators (what shall be monitored);

Frequency of monitoring and evaluation (when the respective reports shall be

prepared);

Responsibilities regarding implementation of monitoring and evaluation (who is

responsible and what for) and competencies for reaching decision for change (update

of the strategic document).

PROVISION OF INFORMATION

The following main information sources have been used when preparing the Export

Strategy:

National Statistical Institute;

Information submitted by BSMEPA;

Information from MEET;

Eurostat;

International Trade Centre;

Information published in relation with held international forums and meetings;

Official electronic information sources;

Information published by branch organizations in the sector;

Information from the Bulgarian Industrial Association and the Bulgarian

Chamber of Commerce and Industry, as well as from their regional sections;

Information from held sociological study carried out from October 31 to

November 28, 2011 within the senior management of 5 micro, 10 small and 7

Page 17 of 130

medium enterprises (total - 22 enterprises), working in the sector; and from

the focus group held.

When processing the information, it was manifested willingness for maximum objectivity of

the conclusions. In many cases the information is analyzed for the sector totally, i.e.

information that includes not only SMEs but also the large ones, based on the assumption

that where a Bulgarian enterprise has achieved success it could be expected that this will be

possible for another one as well which is from the groupof SMEs. This specificity is

expressly emphasized in the analyses.

Structure of the Export Strategy for the “Manufacture of pulp, paper, board and articles”

sector.

In determining the structure of the Export Strategy for Sector “ Manufacture of pulp, paper,

board and articles”, it was taken into account the use of the approach of strategic planning

that sets the general parameters of the strategic document. At the same time, the structure of

other institutional strategic documents was examined and the following criteria were used

for evaluation:

is there opportunity for relatively easy familiarization with the document

through understandable and logical structuring of the individual parts;

is the content presented in an attractive and easy to understand manner

accessible to non-specialists;

is thematic provision of the information possible, that is structuring the

material in a way that allows deep penetration in the problems and analyses only if desired

by the reader.

To the so chosen criteria corresponded several of the strategies examined, in

which there were two separate distinct parts, namely:

The main document where, according to the above described logic of the

technology of strategic planning, are also identified the different sections.

Appendices that contain the complete text of the prepared analyses, including

the conclusions transferred to the main material.

This approach was also chosen when structuring the Export Strategy for Sector

“Manufacture of pulp, paper, board and articles”.

Page 18 of 130

MAIN CONCLUSIONS OF THE ANALYSIS OF THE CURRENT

SITUATION

This section presents the conclusions from various analyses included in “Analysis of the

environment” which is a major step in the technology of strategic planning. An appendix to

this strategic document presents the complete text of the facts and analyses based on which

the conclusions are formulated. The conclusions and the analyses themselves are structured

in 5 parts, as follows:

STATE AND DEVELOPMENT OF THE SECTOR IN BULGARIA

EXPORT ORIENTATION OF THE SECTOR

GOOS WITH EXPORT ADVANTAGES AND POTENTIAL

COMPETITIVENESS OF THE EXPORT OF GOODS ON

INTERNATIONAL MARKETS

BARIERS TO THE INTERNATIONALIZATION OF SMALL AND

MEDIUM ENTERPRISES, AS WELL AS MEASURES AND

PERSPECTIVES FOR STIMULATION AND DEVELOPMENT OF

EXPORT

STATE AND DEVELOPMENT OF THE SECTOR IN BULGARIA

At this stage (2011) of the economic activity – manufacture of pulp, paper, board and

articles – at EU level exist 200,000 companies which hire approximately 1,9 million people

and the summary activity turnover is around 75 billion EUR. From the viewpoint of this

consolidated statistics on the present condition of the sector at EU-27 level, it is necessary to

Page 19 of 130

outline the place and profile of Bulgarian small and medium enterprises and their abilities to

compete on the large European market. An important aspect in the manufacture of pulp,

paper, board and articles is environment. Its conservation and preservation is the most basic

and fundamental task of any strategic plan. The environmental protection is a reinvestment.

It should primarily be pursued efficiency and effectiveness in the application of new

technologies in the sector.

The structure of operational costs in EU-27 related to the manufacture of pulp, paper, board

and articles, is to a large extent similar to that of the industrial sector.

The investments in this production have an average value of 1.4% of the industrial sector for

EU-27 and these values are highest in Finland (6.3%), Estonia (4.2%) and Latvia (4.2%).

Labor productivity in the sector, related to the production of timber and paper material is

estimated to 39.4 thousand EUR per person in 2007. This value makes it by about 10%

lower than the average for the economic sector.

The manufacture of pulp, paper, board and articles and the SMEs involved in them have a

great importance to the economy of the country, as these products are related to the way of

living and their availability, demand and the ensuring of their specificity of their purpose.

The country has a rich resource base for the manufacture of pulp, paper, board and articles.

The “Manufacture of paper, board and articles of paper and board” sector covers around

1.4% of the industrial production in the country and also creates 1.4% of the added value in

industry. The revival of the production in the sector reflected on the dynamics of the export,

which in 2010 was 1% of the total export and 2.6% of the total import of the country.

The “Manufacture of pulp, paper, board and articles” sector includes the manufacture of

paper, paper mass and recycled paper products. The grouping of these products is

characterized and grounded by the similar and common vertical production processes at the

stage of formation and generation.

For SMEs in the economic activity “Manufacture of pulp, paper, board and articles”, the

structure is significantly more simple, which allows an easier analysis. Based on

Classification of Economic Activities /CEA/ of 2008, NSI managed to collect data for 2009

and 2010 under the new methodology, which are presented in the next two tables.

Page 20 of 130

Table 1 SMEs in the economic activity during 2009 (based on CEA-2008) /according to

data of NSI/

Enterprises Turnover Added value at

factor prices

Employees

Code: Number in thousand BGN Number

17. 553 406 424 102 205 7465

17.1. 18 ** ** 443

17.2. 535 ** ** 7022 Legend:

Division-17 – Manufacture of paper, board and articles of paper and board

17.1. - Manufacture of fibrous semi-manufactured goods, paper and board

17.2. - Manufacture of articles of paper and board

** - confidential data

Table 2 SMEs in the economic activity during 2010 (based on CEA-2008) /according to

data of NSI /

Enterprises Turnover Added value at

factor prices

Employees

Code: Number in thousand BGN Number

17. 517 372 203 102 205 6 385

17.1. 15 4 122 -1 438 187

17.2. 502 368 081 77 009 6198 Legend:

Division-17 - Manufacture of paper, board and articles of paper and board

17.1. - Manufacture of fibrous semi-manufactured goods, paper and board

17.2. - Manufacture of articles of paper and board

As can be determined from the adduced tables prepared under the methodology of NSI,

some of the data for 2009 regarding the turnover and added value on factor prices are

confidential. From the disclosed data, however, it is seen that the turnover of all 553 SMEs

in this economic activity amounted to a little more than 400 million BGN and the total

number of people employed in these SMEs was 7,465. In 2010 the picture gets worse, as the

actual number of SMEs in the economic activity also decreases and the turnover of the

activity seriously decreases – to approximately 370 million BGN and the number of the

people employed also decreases – from 7,465 to 6,385.

The prospects on the data for 2011 and the next one to two years are also negative, which

means that the branch literally “collapses” and the business activity is reduced to some form

of survival. Due to the said reasons, several specific goals at different levels should be taken

into account.

Page 21 of 130

The purpose of the strategy is to create a connection, to build a bridge for the transmission of

the local company interests and their coordination with consumer countries. This is an

expression of the main and basic function of the system of the European Union, namely,

overcoming any territorial economic border and aggregation of a single market.

The positive aspect is that SMEs are more strongly represented in the manufacturing

industry than the large enterprises. The strengths of small and medium business regarding

the export of paper, board and other articles is the creation of added value. Among the

regional centers in Bulgaria with the richest timber resources are the cities: Blagoevgrad,

Burgas, Vidin, Vratsa, Gabrovo, Kyustendil, Lovech, Montana, Pazardzhik, Smolyan,

Shumen, and others. The geographical location of these cities suggests a possibility for

export both to the eastern market (Russia, China), and to the western market (Europe, USA,

Brasil).

Table 3 Regional distribution of the enterprises and employees in the “ Manufacture of

pulp, paper, board and articles” sector in 2009

Employed

in the

sector

(number)

% of those

employed in the

manufacturing

industry

% of those

employed

in the

sector

Companies

in the

sector

(number)

% of the

compa-

nies in

the sector

Northwest region 550 0,9% 5,4% 40 7,3%

North Central region 1920 2,3% 19,0% 80 14,7%

Northeast region 787 1,4% 7,8% 48 8,8%

Southeast region 466 0,6% 4,6% 44 8,1%

South Central region 3484 2,6% 34,4% 151 27,7%

Southwest region 2909 1,8% 28,8% 182 33,4%

Source: Evrostat

The level of salaries in the sector is one of the lowest. The average monthly salary is estimated

at about 460 BGN and provides employment of 9.6 thousand people (1.9% of those employed

in the manufacturing industry).

The production consists of articles of paper and board, wallpapers, stationery, etc. It is realized

by about 350 companies, more than half of which are located within the territory of the South

Central and Southwest planning regions. Among the companies engaged in the manufacture of

paper, board and articles can be distinguished: "MondiPeking Stamboliyski" EAD, "Svilosel"

EAD, "Kostenets HII" AD, "Koch and Nur Nemusmark" AD, "Vivatel" AD and others.

Unlike the production of timber, its processing into interstitial and end product is related to a

certain level of machinery and equipment. The equipment necessary for the processing of

Page 22 of 130

the raw material is not available for a big part of the small and medium enterprises and this

puts them into the position of non-competitiveness..

Main conclusions from the analysis of the situation and development of the sector:

The number of SMEs in the “Manufacture of pulp, paper, board and articles” sector

marked a decrease in 2010 by 6,51% compared to the previous 2009. In 2010 the number of

the employees in the sector also declined by 14,5% compared to 2009. A decrease was also

observed with respect to the turnover realized by SMEs from the sector as it decresed from

406 424 thousand BGN in 2009 to 372 203 thousand BGN in 2010.

From the economic activity – the manufacture of pulp, paper, board and articles, at

the EU-27 level, are formed around 75 billion EUR, while in Bulgaria, for the last fiscal year

(2010), only around 135 million EUR. The scale of market forces of Bulgarian SMEs

compared to EU-27 is only 0,19% of all competing market participants and it shows the

extremely insignificant market force of the Bulgarian small and medium enterprises in the

context of EU-27.

The regional distribution of the companies from the sector shows a significant

concentration of companies in the Southwest region and in particular in the region of Sofia.

The product assortment with which the majority of the surveyed enterprises have

proved themselves successful on the market is not very wide. Only 1/3 of the companies

have staked on the production of a richer range of goods.

A little more than half of the companies from the branch invest in development

activity (innovations) – 59,1%.

The main part of the investments is in expansion of the activity of the existing

enterprise (76,9%), followed by diversification of the production of the existing enterprise

by adding new additional products (53,8).

50,0% of the enterprises from the sector have their own trademark. Exactly the same

is the percentage of holders of international certificates.

Page 23 of 130

EXPORT ORIENTATION OF THE SECTOR

The value of Bulgarian export in the economic activity “Manufacture of pulp, paper, board

and articles” according to the latest data of the National Statistical Institute from January

2012.

Table 4 Value of the Bulgarian export of “Paper, board and articles of paper and board”

under the nomenclature of CEA /2000 – 2011/ (according to data of NSI)

Value of the exort (in BGN) Share (in %)

Year Total for products

under the Classifier

of Economic

Activities /CEA/

Value of the exort

of "Paper, board

and articles of

paper and board"

Share of "Paper, board

and articles of paper

and board" of the total

export of all products

under CEA

2000 10 274 106 727 371 715 523 3,62%

2001 11 176 068 993 456 217 411 4,08%

2002 11 857 905 747 571 303 578 4,82%

2003 13 041 906 435 670 772 499 5,14%

2004 15 617 051 924 774 824 853 4,96%

2005 18 514 553 261 805 345 179 4,35%

2006 23 493 153 075 943 278 207 4,02%

2007 26 426 895 408 1 047 300 000 3,96%

2008 29 736 375 433 267 994 380 0,90%

2009 22 881 652 090 140 826 313 0,62%

2010 30 435 009 876 314 612 346 1,03%

2011 33 952 544 356 348 948 883 1,03%

It is obvious from the table that the share of the export of paper, board and articles of paper

and board, under the nomenclature of the Classifier of Economic Activities /CEA/, adopted in

the country between 2000 and 2007, fluctuates in the range 3,5% to 5% for the different years

and the highest peak in this time series of data was 2003. The highest peak of this share for the

whole series of data from 2000 to 2011 inclusive, also turns out to be 2003. Since then until

now (2011) the share of the value of the export of paper, board and articles of paper and board

has been continuously decreasing, which is also obvious from fig. 1.

Page 24 of 130

Graph 1 Export of “Paper, board and articles of paper and board”

After the accession of the country to the EU, this share varies about 1% of the total export by

all export positions under CEA. As an absolute value, however, these are different amounts

between 270 million BGN (2008) and nearly 350 million BGN (2011).

The data show that in absolute values, the peak year for the market participants engaged in the

activity “Manufacture of pulp, paper, board and articles” was 2007, when the export amounted

to over 1 billion BGN. Subsequently, the lowest level recorded was in 2009 – around 140

million BGN, and then the growth in the following 2010 and 2011 doubled. Therefore, in the

interpretation of the export data, it is very important that both the absolute indicators and the

relative indicators of the value of the export in this direction should be studied.

In addition, it can also be enclosed updated information about what the value of the export of

SMEs form the sector is compared to all the enterprises within the sector.

Page 25 of 130

Table 5 Value of the export of SMEs from the sector /2007 – 2011/ (according to data of

NSI)

Value of the export of "Paper, board and articles of paper

and board" (in BGN)

Share (in %)

Year All Bulgarian

enterprises in the

sector

SMEs in the

sector

Share of the export of

SMEs from all

Bulgariand enterprises

in the sector

2007 1 047 300 000 not available n/a

2008 267 994 380 n/a n/a

2009 140 826 313 61 824 000 43,90%

2010 314 612 346 39 800 000 12,65%

2011 348 948 883 n/a n/a

The share of the export of SMEs from all Bulgarian enterprises in the sector amounted to

around 44% in 2009 and almost 13% in 2010.

The export of various articles: paper, board, fibrous cellulose materials and the like, is

constantly increasing and for the period 2000-2011 this export has increased almost 3 times for

the paper and board and a little over two times for the wood mass or the mass of other fibrous

cellulose materials.

Table 6Value of the sector export of Bulgaria, according to the Combined Nomenclature

/2007 – 2011/ (according to data of NSI)

Export from Bulgaria under the Combied Nomenclature (in BGN)

Year Wood mass or mass of other fibrous

cellulose materials; paper or board

for recycling (waste and left-overs)

Paper and board; articles of pulp,

paper or board

2000 44 776 517 75 176 639

2001 35 627 856 83 609 489

2002 42 165 671 83 741 257

2003 37 079 969 130 552 885

2004 41 126 224 152 601 886

2005 33 432 076 163 695 336

2006 40 846 062 145 307 997

2007 41 372 242 191 951 493

2008 64 996 003 198 623 073

2009 11 339 917 121 542 822

2010 113 302 945 192 033 659

2011 103 752 172 239 994 284

Page 26 of 130

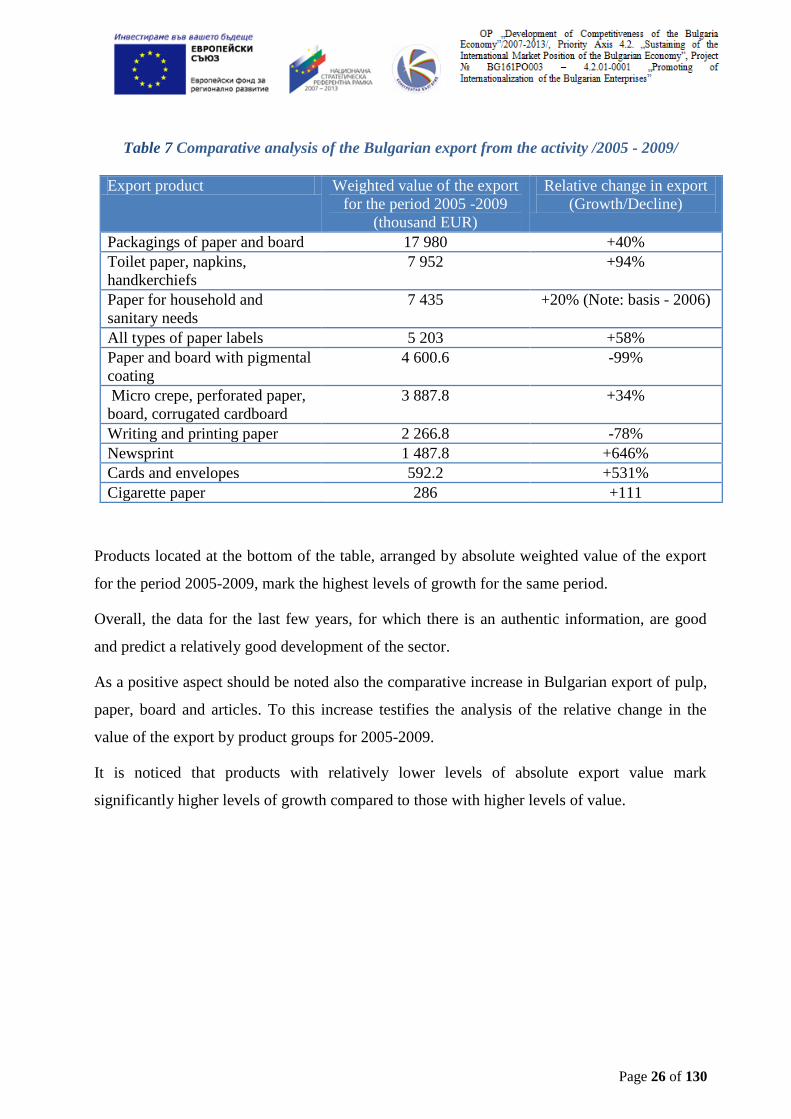

Table 7 Comparative analysis of the Bulgarian export from the activity /2005 - 2009/

Export product Weighted value of the export

for the period 2005 -2009

(thousand EUR)

Relative change in export

(Growth/Decline)

Packagings of paper and board 17 980 +40%

Toilet paper, napkins,

handkerchiefs

7 952 +94%

Paper for household and

sanitary needs

7 435 +20% (Note: basis - 2006)

All types of paper labels 5 203 +58%

Paper and board with pigmental

coating

4 600.6 -99%

Micro crepe, perforated paper,

board, corrugated cardboard

3 887.8 +34%

Writing and printing paper 2 266.8 -78%

Newsprint 1 487.8 +646%

Cards and envelopes 592.2 +531%

Cigarette paper 286 +111

Products located at the bottom of the table, arranged by absolute weighted value of the export

for the period 2005-2009, mark the highest levels of growth for the same period.

Overall, the data for the last few years, for which there is an authentic information, are good

and predict a relatively good development of the sector.

As a positive aspect should be noted also the comparative increase in Bulgarian export of pulp,

paper, board and articles. To this increase testifies the analysis of the relative change in the

value of the export by product groups for 2005-2009.

It is noticed that products with relatively lower levels of absolute export value mark

significantly higher levels of growth compared to those with higher levels of value.

Page 27 of 130

Graph 2 Summarized data about the export of the different products in the sector /in

thousand EUR/

Source: NSI

Here it should also be taken into account the chain for formation of value addition in the sector.

The formation of the final value as at 2010, according to data of CEPI is as follows– Graph 3.

Page 28 of 130

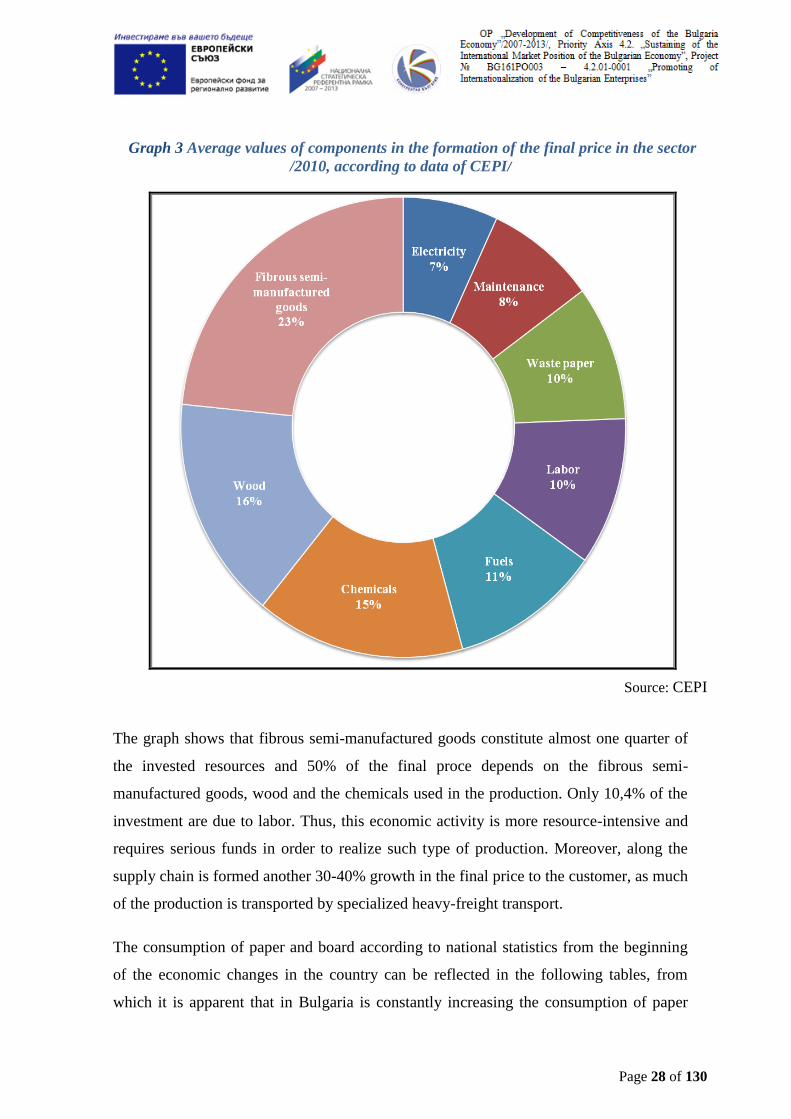

Graph 3 Average values of components in the formation of the final price in the sector

/2010, according to data of CEPI/

Source: CEPI

The graph shows that fibrous semi-manufactured goods constitute almost one quarter of

the invested resources and 50% of the final proce depends on the fibrous semi-

manufactured goods, wood and the chemicals used in the production. Only 10,4% of the

investment are due to labor. Thus, this economic activity is more resource-intensive and

requires serious funds in order to realize such type of production. Moreover, along the

supply chain is formed another 30-40% growth in the final price to the customer, as much

of the production is transported by specialized heavy-freight transport.

The consumption of paper and board according to national statistics from the beginning

of the economic changes in the country can be reflected in the following tables, from

which it is apparent that in Bulgaria is constantly increasing the consumption of paper

Page 29 of 130

and board, the lowest levels being in 2000 and 2001 and the highest level of consumption

for Bulgaria being in 2007.

Table 8 Consumption of paper and board by countries and by years during the period

1990 - 2010 (kg/person)

Country 1990 1995 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Bulgaria 28 28 17 17 27 39 41 43 45 59 52 45 49

Germany 225 194 233 225 228 225 236 233 253 256 247 221 243

Greece 61 82 114 83 111 115 104 105 109 108 112 99 93

China 13 22 28 29 33 36 42 45 50 55 59 64 69

Poland 22 40 60 64 67 73 88 89 98 109 109 108 118

Romania 22 15 19 21 23 27 27 29 32 35 31 29 31

Russia 34 13 22 38 26 31 34 36 42 47 46 42 47

USA 311 332 332 324 314 301 312 301 301 288 266 231 240

Hungary 55 50 80 70 77 88 82 88 95 97 97 85 88

Finland 279 304 211 194 333 308 285 324 330 369 342 282 281

Czech

Republic

78 67 90 96 103 114 130 133 141 159 155 133 143

Japan 228 239 250 242 241 242 247 247 247 246 242 215 220

As can be seen from the enclosed tables, ones of the world consumers of paper are Finland,

the USA, Germany and Japan with an annual consumption in 2010 of over 200 kg/perosn.

After them come the Czech Republic and Poland, closely followed by Greece and Hungary.

Bulgaria is on one of the last places according to the latest statistical data.

Anex 1 presents data on production, import, export, consumption, covering a 10-year period

of tracking the data under the nomenclature, followed by the National Statistical Institute.

From the data presented it is obvious that the sector is highly dynamic, which is also due to

the strong competition and the commitment of the sector to key participants on the

international markets. The lasting economic crisis in the country has also reflected on the

continuing stagnation in the sector, which, like almost all other sectors in the economy of the

country, was at that time forced to reduce jobs and make forced dismissals. In practice, the

unfavorable business climate in the country exacerbated seriously the inter-company

competition in the sector, as the latter is very sensitive to reduced circulations and orders.

This sector also suffers from a particular threat of the high-tech electronic media, which

create more and more users offering alternative resources of information through the

electronic media and carriers. This creates an additional reflux of customers from the sector,

Page 30 of 130

which often manifests itself as unfair competition at the national level. Moreover, due to the

specificity of the activity in this sector, companies work with relatively larger orders and the

scales of leverage between the companies are constantly growing, which creates significant

obstacles to the normal communication between the companies, institutions and end

customers.

Some of the areas performing well in the sector are the producers of packing paper,

including bag paper and machine-smooth packing papers, which are most frequently used in

stores.

Another area is the production of bleached sulphate pulp (kraft) and, to a certain extent, the

production of sanitary paper.

The long series of data for the development of the sector show that until the accession of the

country to the EU and one to two years after that the sector has developed very rapidly, but

in the last two to three years many small and medium enterprises from the sector, in practice,

are facing technical bankruptcy or irreversibility to regain the market positions of before the

crises.

The sector analysis clearly shows that the economic diagnosis of the sector indicates very

unpleasant conclusions for small and medium eneterprises, as the market here is very

parcelled out and even destroyed in certain industries, as are the cases of the production of

multilayer boards or other type of boards.

GOODS AND SERVICES WITH EXPORT POTENTIAL AND ADVANTAGES

Products with the highest potential for export in the sector:

paper for household and sanitary needs;

packings of paper and board;

newsprint;

toilet paper, napkins and handkerchiefs;

Page 31 of 130

all types of paper labels.

These goods are determined based on an analysis of two indicators – export volume and

export dynamics.

In the manufacture of paper and board coated with kaolin or other inorganic

compounds is observed a sudden decline in the export after 2005, the lowest values being in

2007. It is difficult to answer the question what are the exact reasons for the sudden decline

in the export of paper and board coated with kaolin or other inorganic compounds. They

may be related to loss of market or partners, to shrinkage of the production or ejection by the

competition.

Graph 4 Value of Bulgarian export of paper and board (with pigmental coating) /in

thousand EUR/

Source: ITC

Weighted value of the export for the period 2005-2009: 4600.6

Relative change for the period (Growth/Decline) : - 99%

Given the lowest value of 112 thousand EUR in 2007, we can assume that the export of the

product is also influenced by the global financial crisis and the values after that year mark

sustainable development. The export data for one year in themselves should not be taken as an

indicator of deterioration in the manufacture and export of a given commodity, but as a matter

of marketeering characteristics related to both internal and external environment.

Page 32 of 130

Despite the drastic decline over the period analyzed, an increase of fifteen times was observed

between 2007 and 2009, which is a clear sign that the export mechanism has started working

again.

Strategic objectives associated with this type of production, seeking to promote and stimulate

export, should focus on achieving rhythmicity and stability on the market. SMEs must have a

very good and accurate system for planning their production, as well as a detailed vision and

information about the outlet realization. The aim is winning positions and establishment of a

developed export market with a specific demand, given the characteristics of the product.

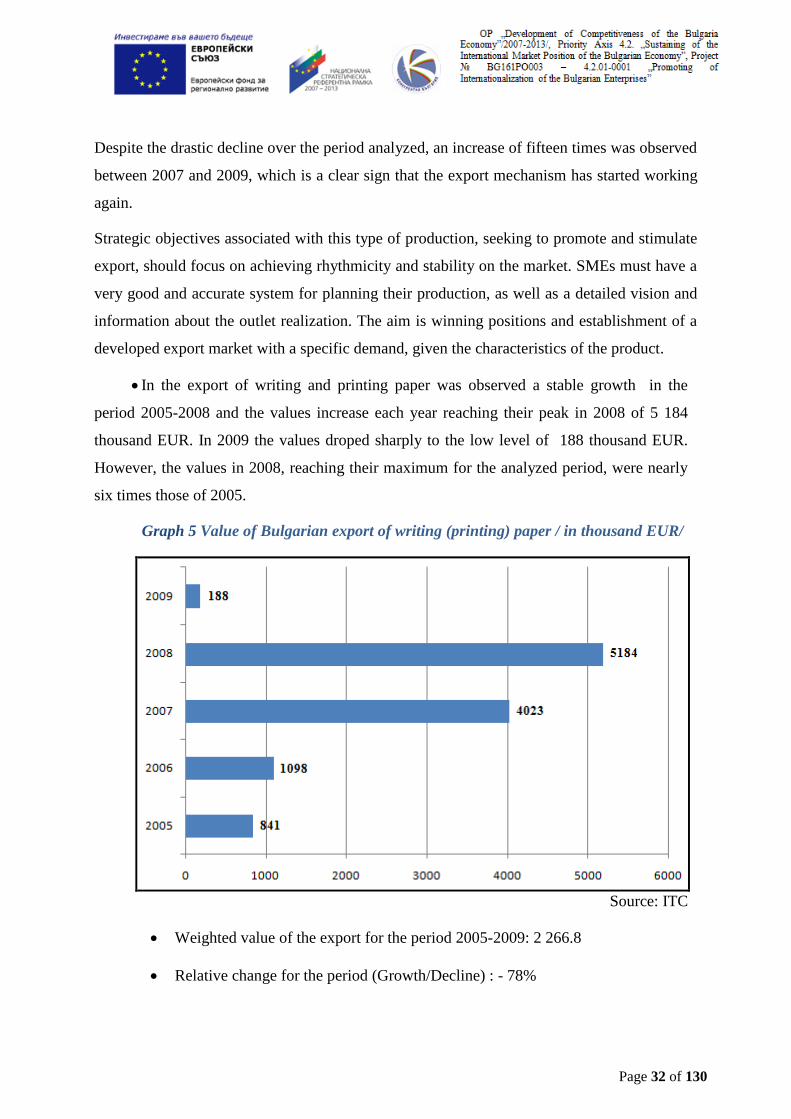

In the export of writing and printing paper was observed a stable growth in the

period 2005-2008 and the values increase each year reaching their peak in 2008 of 5 184

thousand EUR. In 2009 the values droped sharply to the low level of 188 thousand EUR.

However, the values in 2008, reaching their maximum for the analyzed period, were nearly

six times those of 2005.

Graph 5 Value of Bulgarian export of writing (printing) paper / in thousand EUR/

Source: ITC

Weighted value of the export for the period 2005-2009: 2 266.8

Relative change for the period (Growth/Decline) : - 78%

Page 33 of 130

The highest annual increase was observed between 2006 and 2007, when the export increased

almost four times. This significant growth is due to the skillful combination of numerous

factors, guaranteeing development of market positions on the international market. The quality

characterization and the level of necessity of the product make it a commodity with a low

demand flexibility, as tangible alternatives almost do not exist.

The sharp decline in 2009 can be attributed to both financial and economic instability of the

international trade markets, and the ecological trends of reducing levels of use of office paper.

In front of SMEs stands a large market with continuous and relatively constant demand. The

strategic objectives of promoting the export of this product should be based on the optimization

of the quality of both the goods itself and the service.

There is need of establishing export channels for quick access and processing the practices, as

well as a network reflecting the necessary cash. The aim is optimization and achievement of

minimum levels of information noise regarding logistics and implementation deadlines. Pricing

and value formation includes not only the product itself and its cost price, but also the ability of

the exporting company to supply as needed. To achieve this goal is necessary elasticity and

flexibility. SMEs should focus their efforts on achieving a good balance between the price level

and the superiority of the quality, since due to its specificity, the product requires a huge market

and high levels of competition. This is struggle which is won by the one who supplies

regularly, on time, the necessary quantity and offers the best conditions.

Writing and printing paper is among the most important resources for the operation of a

business and it is the necessary basis for the preparation of projects, contracts and any type of

office documentation. The Bulgarian SMEs are facing the task to develop the necessary

competitive advantages by which they could build up the necessary added value of the product

so that it can be preferred to the local alternatives. Given the similar qualitative characterization

of the product concerned, innovations regarding the structure, vision, or composition are less

likely or they hide a risk of incompatibility with the market principles. That is why SMEs

should focus on the quality of export implementation and act as local suppliers, even better.

There is need of opening and development of an optimal transport network, with the possibility

of flexibility of supplies and minimum delays. Building up this basis and the extent of its

effective realization would allow the exporting company to use the instruments of pricing as

competitive advantages.

Page 34 of 130

But to reach this stage, it is necessary to achieve scale effect or lower relative production costs

per unit of article. This model, however, is at variance with the structure of SMEs and poses

one of the major problems for the export as a whole, namely the gap between the capabilities of

the small and medium business and the strategic objectives for export development. This

strategy is yet to consider exactly the alternatives and possible solutions to this problem.

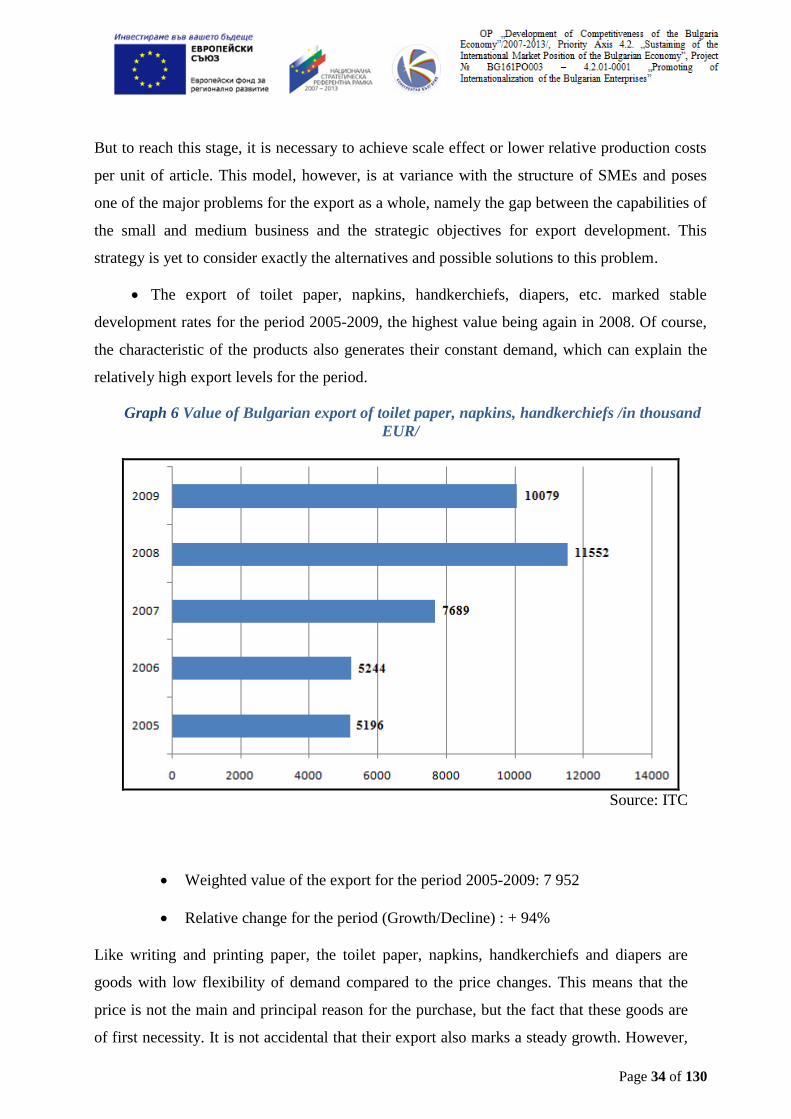

The export of toilet paper, napkins, handkerchiefs, diapers, etc. marked stable

development rates for the period 2005-2009, the highest value being again in 2008. Of course,

the characteristic of the products also generates their constant demand, which can explain the

relatively high export levels for the period.

Graph 6 Value of Bulgarian export of toilet paper, napkins, handkerchiefs /in thousand

EUR/

Source: ITC

Weighted value of the export for the period 2005-2009: 7 952

Relative change for the period (Growth/Decline) : + 94%

Like writing and printing paper, the toilet paper, napkins, handkerchiefs and diapers are

goods with low flexibility of demand compared to the price changes. This means that the

price is not the main and principal reason for the purchase, but the fact that these goods are

of first necessity. It is not accidental that their export also marks a steady growth. However,

Page 35 of 130

the goal here should be to preserve and maintain the market positions with a vision for

growth.

It is important to take into account that the market is an extremely dynamic and unstable

mechanism and good data should not be accepted as a certainty or guarantor for future

development. Efforts are needed, aimed at the continuous development of the product, the

conditions of its sale through export and development of the competitive advantages of the

company as a whole.

Toilet paper, napkins, handkerchiefs, diapers and similar products are among the most

widely known and used in everyday life products. This fact also determines high levels of

supply. The data in Graph 6 show some stable and relatively constant levels of growth in the

export of these goods, which means that the companies which produce them are well placed

and established on the foreign markets. In ordet that this realization is present, it is necessary

that be taken into consideration that the material expression of export is in money, but its

more important dimension is the client’s assessment or that moral value, which puts it as a

leader among the other alternatives offered by the local market.

The more specific a product is, the easier it can be disposed, of course, provided that the

market appropriate for it has been found. While the goods for mass consumption are an

objective-oriented marketing target for a wide range of companies, and this is a fact

increasingly heightens the competitive battle between them. Bearing that in mind, we can

conclude that the Bulgarian companies realizing export of toilet paper, napkins,

handkerchiefs, diapers and the like, are worthy of being an example for the rest of the

business and a model in which SMEs can develop their export policy.

The export of cigarette paper marked a steady growth for the period, despite its

relatively low absolute values. The specificity of this export, like the previous two, is

connected with almost zero elasticity of demand. Cigarettes and cigarette products are very

specific goods the demand of which is highly irrelevant to the level of prices. This makes

these goods and their components products with guaranteed demand and provides the small

and medium business with a good niche for development of its production potential. It

should be borne in mind that establishing onself on the market is particularly difficult and

the marketing barriers for entering are extremely high. This is related to the popularity of the

end product and its ability to generate constant demand at rising price level. In Bulgarian

Page 36 of 130

export of cigarette paper was noted a stable and gradual growth and the relative export

values decreased only in 2008, this being a single phenomenon and not a tendency.

Graph 7 Value of Bulgarian export of cigarette paper /in thousand EUR/

Source: ITC

Weighted quantity of the export for the period 2005-2009: 286

Relative change for the period (Growth/Decline) : + 111%

It is also important to note that for the considered period between 2005 and 2009, the total

volume of the export increased by double, like the export of toilet paper, handkerchiefs,

napkins and diapers. This relative index ranks the export of cigarette paper among the

leaders in the export of Bulgaria. Despite the low absolute value of the export, the growth

trend is clearly noticeable. This means that companies representing the production of

cigarette paper know how to organize their export and how to manage it. This is an

important and priceless know-how for the achievement of the strategic objectives on the

development of the export policy for the small and medium business.

The export of all types of paper and board labels marked a steady growth, despite the

relatively poor indices for 2006. They can be attributed to multiple factors, but it is more

Page 37 of 130

important not to focus on the low effectiveness in 2006, but to consider the marketeering

framework of the export for the given period more globally and generally. In the analyzed

period there was an increase of more than 50% and despite the low level in 2006, in 2007

the export increased by 10 times.

Graph 8 Value of Bulgarian export of all types of paper labels /in thousand EUR/

Source: ITC

Weighted value of the export for the period 2005-2009: 5 203

Relative change for the period (Growth/Decline) :+ 58%

These indices guarantee for a good and balanced export policy by the exporting companies

and testify to their good practices in the field of corporate planning, forecasting and goal

setting.

The export of all types of paper labels is another good example of not only how to lead an

useful and effective export policy, but also how business can cope with situations of decline

and low reporting indicators. All companies in the most general sense have, if not equal,

then at least similar tools for interaction and impact on the internal and external

environment. However, far from all have the potential to use it to make rational and

effective management decisions concerning the planning and organization of future events

and periods.

Page 38 of 130

The export of paper for household and sanitary needs marked relatively high levels

of export and only the data 2005 are almost zero compared with the other analyzed periods

from the interval 2005-2009. However, this export group marked high average levels of

value. The export of paper for household and sanitary needs marked its higher value in 2008,

following a growth of nearly 40% compared to the previous year. This tendency did not

established itself and in 2009 there was a decline also by about 40%.

Graph 9 Value of Bulgarian export of paper for household and sanitary needs /in

thousand EUR/

Source: ITC

Weighted value of the export for the period 2005-2009: 7 435

Relative change for the period (Note: Due to the extremely low value for 2005,

for a basis have been taken the data from 2006) (Growth/Decline): + 20%

Nevertheless, the absolute dimention of the export is significant and is among the exports

with highest value among the considered export product categories. This is explained both

by the practical and and everyday application of the goods, and by the effective export

policy of the companies. Among them those producing toilet paper, handkerchiefs, napkins

and diapers are most frequently specialized in the production of paper for household and

sanitary needs, too. A proof of this are the good indicators of growth and absolute value of

Page 39 of 130

the export. They are the basis for the further development and utilization of this export

channel.

Even if they do not have the necessary equipment for the production and processing of raw

materials for this type of production, the small and medium can act as jobbers, suppliers or

dealers. In this way they deprive themselves of the risk related to the manufacture of the

production, to the high costs of obtaining and processing the materials and thanks to their

not numerous staff they can also be competitive to the bigger enterprises which have

significantly higher cost burden. The formation of sush international mediations is among

the main export strategies available for the development of the export by SMEs.

The export of packings of paper and board is among the leaders in the export of

products of pulp, paper, board and articles, with an absolute measurement of the export

much higher than the other prouct groups.

Graph 10 Value of Bulgarian export of packings of paper and board /in thousand EUR/

Source: ITC

Weighted value of the export for the period 2005-2009:: 17 980

Relative change for the period (Growth/Decline): +40%

Page 40 of 130

Here are observed annual values, each of which exceeds significantly the limit of 10 million

EUR. It makes impression that the value of the export for each year individually exceeds

almost all of the highest levels of export of the rest of the products analyzed. With a

weighted value of the export of approximately 18 million EUR, the export of packings of

paper and board exceeds more than two times the export ranked second. These high values

can be explained by the necessity of packing of most of the products.

In today’s realities and with a pursuit of achieving a more ecological environment, nylon is

being displaced by paper globally. This global trend, no doubt, gives its impact on the

Bulgarian export, too. In large numbers nylon bags and packagings are being replaced and

displaced by ones made of paper or board, due to their properties of degradation. The idea of

environmental protection and achievement of sustainable development is among the current

issues of today and is a starting point for this strategy. This is an example of the influence of

a trend on the market development or how non-economic factors can acquire economic

impact.

Exactly because of that reason, it is necessary to build a more massive and global vision

regarding the promotion of the export of SMEs. Not the detail is important, but the final

result; the vision is important which is necessary to be built in order to create the link

between SMEs and international market.

The production of paper and board packings is yet to develop both in innovative and in

environmental aspect. SMEs and the specialists representing them should focus their

attention on the ways of achieving symbiosis between three main production factors:

effectiveness, efficiency and environmental friendliness.

This means to find a way to use a minimum amount of resource, which should be

processesed with a relatively minimum share of the costs in order to create a product leaving

a minimum mark on the environment.

The optimization of these factors is the way to achieve a better product and since the idea

should precede technology, SMEs need to develop their conceptions for the production of

ecological packings, as well as to create a system for their reproduction and recycling. In

other words, the specificity of this product requires unlimited responsibility of the producer.

This concept is the basis for building a new and better export line, in the center of which

stands the product and not the export itself. Reconsideration of this formulation will enable

Page 41 of 130

the Bulgarian small and medium business to fit in the global trading environment with

regard to the production of pulp, paper, board and articles.

When determining the amount and quantity of the export, it should also be considered the

unit value of the articles, since the price forms the value and does not give a real idea of the

scale of the export. In the export of newsprint, a standstill was observed from 2005 to 2007,

then the values increased approximately five times and continued their growth. The absolute

growth between 2005 and 2009 was almost ten times, which is a sign of conducting an

active export policy. It in itself is a mechanism which does not have sudden impact on the

marker processes. If we assume that in 2005 the companies adopted a number of measures to

increase and stimulate the export, the data for 2006 cannot give a clear idea of the degree of

fulfillment of the set criteria, as market and foreign trade processes include numerous

factors.

Graph 11 Value of Bulgarian export of newsprint /in thousand EUR/

Source: ITC

Weighted value of the export for the period 2005-2009: 1 487.8

Relative change for the period (Growth/Decline) : + 646 %

In 2007 were observed values exceeding by about 50% those of 2005 and more than twice

those of the previous 2006. This testifies to expansion of the export and we can assume that

Page 42 of 130

it the result of the anti-crisis measures of the companies. Between 2007 and 2008 the export

marked an increase by nearly five times.

The export of newsprint is largely related to finding the appropriate export partner. It is

important to take into consideration that, like for the writing and printing paper, of great

importance here is regularity of supply, as well as compliance with the agreed quantity and

quality.

The production of newspapers, like the composition of written documents, is a process of

creating additional value, in the form of information. The framework and scaffolding for this

information is the paper, which makes it an extremely important and valuable material.

To stimulate the Bulgarian export of newsprint, it is necessary to analyze the actions of the

companies in the branch in 2005, 2006 and 2007, as they give effect to the increase of the

export value in the following periods.

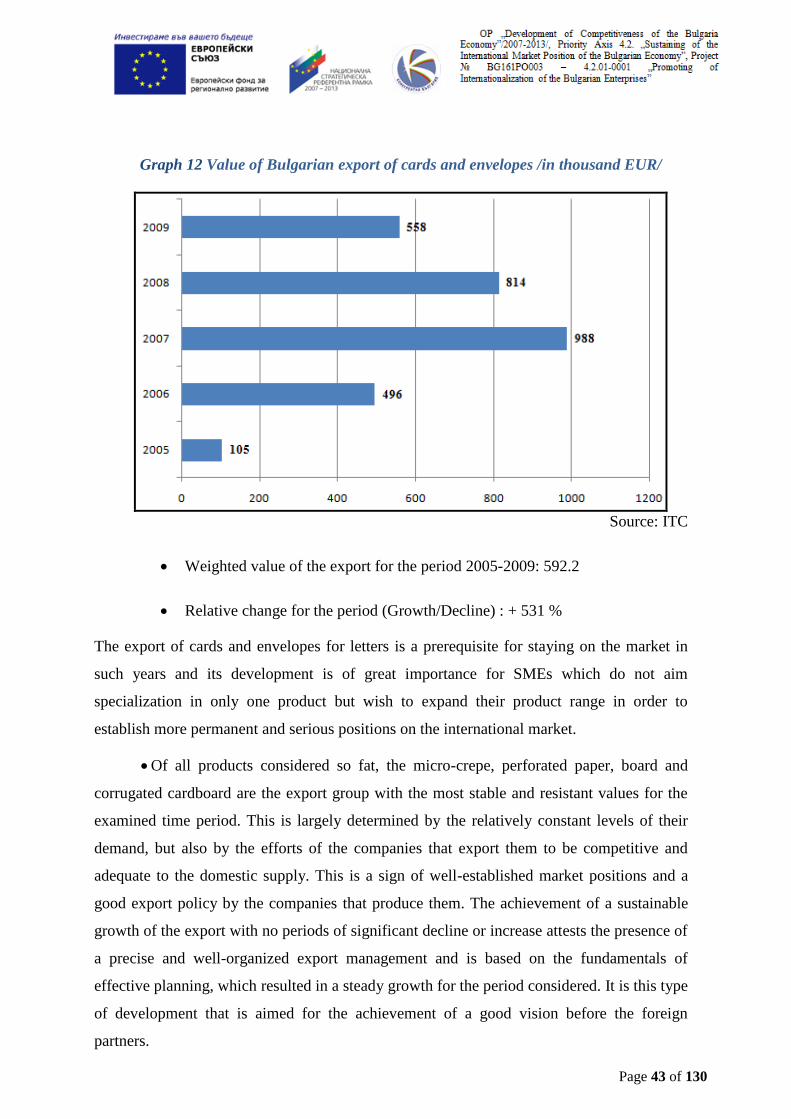

The export of cards and envelopes for letters marked an increase in a period 2005-

2007, when it reached its maximum of 988 thousand EUR and gradually declined in the

period 2007-2009. The export of cards and envelopes for letters is definitely not among the

supporting pillars of the export of pulp, paper, board and articles, but its importance

determines the width of the range of products which our country is able to offer on the

international market. This production, despite its relatively low values of export, can serve

as a counterweight to ensure profitability in case of realization of a poor annual export of

another product, as often happens according to the graphs analyzed so far.

Page 43 of 130

Graph 12 Value of Bulgarian export of cards and envelopes /in thousand EUR/

Source: ITC

Weighted value of the export for the period 2005-2009: 592.2

Relative change for the period (Growth/Decline) : + 531 %

The export of cards and envelopes for letters is a prerequisite for staying on the market in

such years and its development is of great importance for SMEs which do not aim

specialization in only one product but wish to expand their product range in order to

establish more permanent and serious positions on the international market.

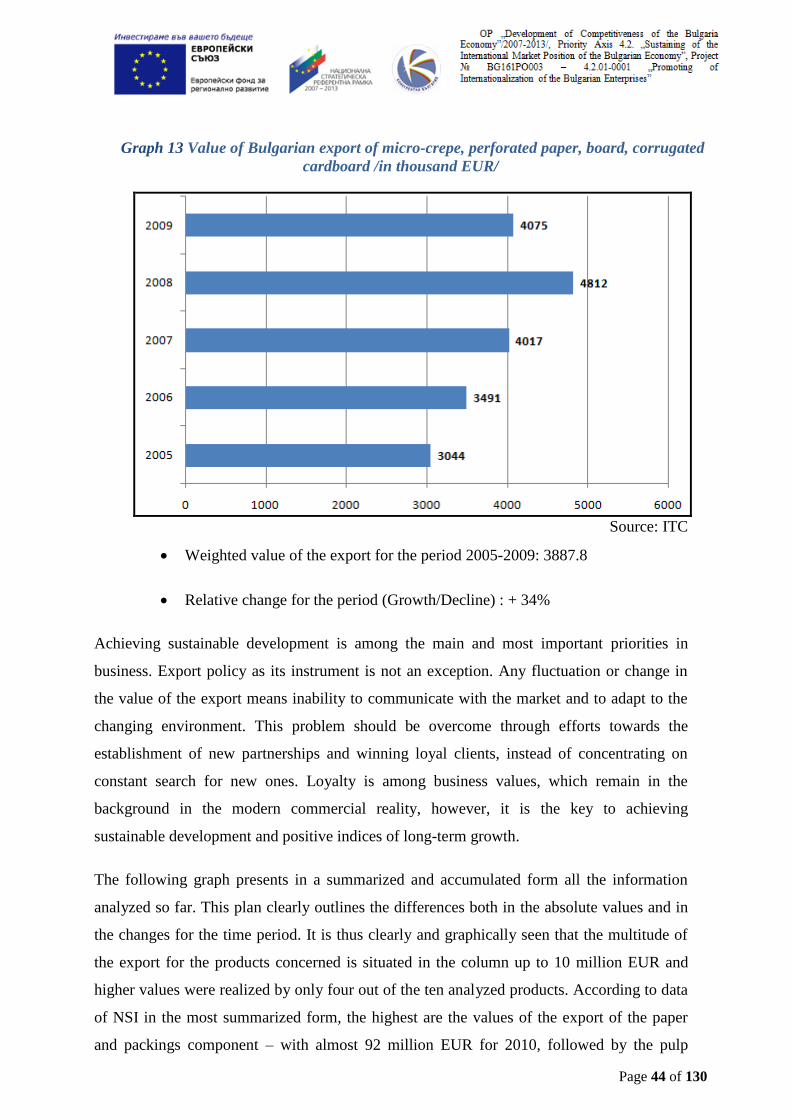

Of all products considered so fat, the micro-crepe, perforated paper, board and

corrugated cardboard are the export group with the most stable and resistant values for the

examined time period. This is largely determined by the relatively constant levels of their

demand, but also by the efforts of the companies that export them to be competitive and

adequate to the domestic supply. This is a sign of well-established market positions and a

good export policy by the companies that produce them. The achievement of a sustainable

growth of the export with no periods of significant decline or increase attests the presence of

a precise and well-organized export management and is based on the fundamentals of

effective planning, which resulted in a steady growth for the period considered. It is this type