export september 2017 vol 15 no 9...

TRANSCRIPT

&i m p o r te x p o r tSOUTHERN AFRICA

September 2017 Vol 15 No 9

A recent article in the Huffington post caught my eye, and after so many months of nothing but pessimistic outlooks, it was refreshing to read something positive for a change.

The article focused on the significant growth recently recorded in the export of edible fruits, beverages, spirits and vegetables.

While in 2015 and 2016, we were all beset with news of one of the worst droughts in recent memory wreaking havoc in South Africa and its surrounding countries, the South African agricultural sector actually recorded a trade balance of USD 2.3 billion in 2016.

This, in spite of the devastating drought that seemed to dominate every headline.

While it has to be noted that these products are mainly grown in the Western Cape, which was not quite as hard hit by the drought as the rest of the country, it is still impressive that the total agricultural export value reached USD 8.6 billion – up six percent from 2015.

The drought also forced South Africa to dramatically increase imports of mainly maize (2.2 million tonnes in the 2016/2017 financial year, and wheat (2.1 million tonnes).

The article also highlighted another of my pet topics; intra-African trade, noting that the largest market for South Africa’s agricultural exports, remained – you guessed it – Africa, accounting for 44% of total agricultural exports. The EU was next in line, accounting for 26% of South Africa’s agricultural export, followed by Asia with 22%, the Americas (5%) and the rest of the world (3%).

The article goes on to give some interesting detail, showing how, despite the drought, South Africa managed to come out on top, and I quote:

•After falling by 18 percent year-on-year in 2015, South Africa's agricultural exports to Africa recovered by 4 percent in 2016 –- reaching USD3.8 billion. This uptick was driven by sugar and sugar confectionery, milling products, as well as exports of edible vegetables and certain roots and tubers.

•Moreover, South Africa's agricultural exports to Asia increased by 13 percent, from USD1.66 billion in 2015 to USD1.87 billion in 2016. Driving the country's exports to Asia was an uptick in edible fruits, wool, beverages, nuts and meat exports, amongst other products.

•South Africa's agricultural exports to the European Union firmed by 5 percent, from USD2.1 billion in 2015 to USD2.2 billion in 2016. This was supported by an uptick in exports of edible fruits, beverages and spirits, wool and meat, amongst other products.

•Lastly, South Africa's agricultural exports to the Americas increased by 5 percent in 2016, reaching USD429 million. Whilst there is a number of products driving this increase, the key ones were beverages and spirits, as well as edible fruits. – end quote.

This bit of good news is expected to continue making an impact on the economy, as the article further points out, saying that the country’s agricultural trade balance is likely to remain positive in 2017, due to significant recovery in agricultural production experienced thus far.

Johan Meyer, Editor

Agri-exports to the rescue

1 export & import SA // SEPTEMBER 2017

publisher:

Ken Nortje, [email protected]

editor:

Johan Meyer, [email protected]

Sales manager:

Sophia Nel, [email protected]

Advertising:

Danelle Aitken, [email protected]

production:

Johan Malherbe, A J van Rensburg

Layout: Patrick Letsoela

Dispatch: Willie Molefe

Circulation/Subscriptions:

Marius Nel

Subscription rates:

Local R340,00 Africa R370,00 Overseas R2 050,00

published: Monthly

Address:

Malnor (Pty) Limited

10 Judges Avenue, Cresta, 2194

Private Bag X20, Auckland Park, 2006

Tel: 011 726 3081

Fax: 011 726 3017

e-mail: [email protected]

www.malnormags.co.za

www.exportsa.co.za

BEE compliant

Export & Import Southern Africa is now available

online Visit www.exportsa.co.za

1

2 export & import SA // SEPTEMBER 20172

contentsOfficially endorsed by Wesgro and

the Exporters Clubs of South Africa – Eastern Cape and

Western Cape

September 2017 // Volume 15 Number 9

Special Focus

Nigeria and South Africa: Out of recession, not yet out of trouble .............................................................. 6

Recession exit inspires confidence, but no call for call for celebration ........................................................ 8

Investment funds: The South African headquarter company regime hurdle ............................................... 10

DHL Express unveils its first green facility in SSA ........................................................................................... 12

Central & Eastern European Insolvencies overview ....................................................................................... 13

Supply Chain

African SMEs to grow faster through supply chain management ................................................................. 16

China Homelife and China Machinex prove huge success ............................................................................ 18

Cold Chain

Next-generation cold-chain monitoring solution from ORBCOMM ............................................................ 20

rail Freight IHHA2017 emphasises need for coordinated African research and development ..................................... 26

ports & ShippingPort of Saldanha’s new LPG terminal launched .............................................................................................. 29 Africa’s transport leaders drive free trade agenda ......................................................................................... 30

Durban Container Terminal optimises operations ......................................................................................... 32

regulars

Credit Guarantee Country ProfileSwaziland ............................................................................................................................................................ 22 Thailand .............................................................................................................................................................. 24

12 2218 24

4 export & import SA // SEPTEMBER 2017

Cover Focus

A full week of activities at KZN Export Week

KZN Export Week is an annual programme of Trade Invest KZN (TIKZN) developed to recognise, promote and assist with growing KwaZulu-Natal's export businesses and industries.

Through a comprehensive programme of activities, it will provide professional development and information on growth sectors and market opportunities to KwaZulu-Natal's new and existing exporters and internationally focused businesses.

Export Week will highlight the significance of exporting to the KwaZulu-Natal economy and will aim to celebrate the success of KwaZulu-Natal exporters. Export Week KZN will be filled with information and networking session of interest for emerging exporters, existing exporters, and seasoned exporters.

•Meet trade partners and associations who can help you to reach new markets

•Network and build new relationships with fellow attendees from across the continent

•Hear some of the top business minds share their tips and stories on how to build a global business

This yeArs’progrAmme is scheduled As follows

why KZN, TiKZN? TIKZN was established to promote the province of KwaZulu-Natal as

an investment destination and to facilitate trade by assisting local companies to access international markets. The organisation identifies, develops and packages investment opportunities in KwaZulu-Natal; provides a professional service to all clientele; brands and markets KwaZulu-Natal as an investment destination; retains and expands trade and export activities and links opportunities to the developmental needs of the KwaZulu- Natal community.

foreign direct investment

Investment in KwaZulu-Natal continues to emerge as a major contributor to South Africa’s growing economy and its favourable business environment has made the province a sound investment destination for investors from around the world.

export promotion from KwaZulu-Natal

TIKZN services extend to guiding companies through customs processes and assisting in registering KZN export companies as importers and exporters with SARS. The agency puts companies in touch with clearing and forwarding agents, freight forwarders, shipping agents financial institutions – in fact, any export intermediary service provider that may be useful in reaching global markets. TIKZN staff is familiar with the Department of Trade and Industry’s (DTI’s ) Export Market and Investment Assistance (EMIA) scheme, and is resourceful in the provision of information on industry-specific assistance.

other services include:

export training

Trade & Investment KwaZulu-Natal regularly conducts export training by making use of private sector service providers to offer tailor-made training courses to existing and aspirant local exporters. These capacity-building programmes consist of the following:

•Focussed Training Sessions (Trade related)

•Mentorship Programmes with a Dutch-based service provider.

•Lead generation services.

•Provision of potential foreign importers of various goods.

•The provision of Market Intelligence

•Export awareness sessions, where exporters are taken through the more basic aspects of the export cycle.

lead generation

Linking KwaZulu-Natal companies with potential buyers, and assistance with information on possible distributors that KwaZulu-Natal companies can use for their products to enter a specific market.

export advisory services

On-the-ground support and advisory services for existing and emerging KwaZulu-Natal exporters with the following:

•Introductionstogovernmentandprivatesectorcontacts

monday

16 october

• Export Week Keynote and Summit: Day 1

• Export Climate Statistics

• The impact of Junk Status on Trade and Investments

• Maximising African Content in African Projects

• Trade legislation and Compliance

• PUM

• Expo build

• Networking reception on the expo floor

Tuesday

17 october

• Summit: Day 2

• Kzn Halal Hub and Export Growth Opportunity

• Maputo Land Corridor as it Relates to Exports

• SAAMD Export Council

• Richards Bay IDZ

• Expo

• Co-located events: African Ports and Rail Evolutions

wednesday

18 october

• Seminar: Export Essentials

• Expo

• Co-located events: African Ports and Rail Evolutions

Thursday

19 october

• Master class (invited only)

• Exporter of the Year Award

friday

20 october

• Annual KZN Export Golf Challenge

Cover Focus

5 export & import SA // SEPTEMBER 2017

•Tariffimplicationsforcertainproducts

•Tradeagreementcompliancerequirements

•Adviceonthesuitabilityofproductsandservices

•Assistancewithidentifyingpotentialbusinesspartnersandcustomers

•Assistancewiththeidentificationofdomesticsuppliersofproducts and services

export incentives

Assistance with the accessing DTI export incentives. These incentives resort under Export Marketing and Investment

Assistance (EMIA) and are further sub-divided into Primary Export

Market Research (PEMR) and Trade Show assistance. PEMR was

designed for companies wanting to engage in primary market

research in a foreign market, and refunds exporters for exploratory

foreign trips into markets that they are not currently exporting to.

Refunds are mainly for travel and accommodation expenses. Trade

show assistance on the other hand is sub-divided into National

Pavilion assistance and individual trade show assistance where,

once again, travel and accommodation expenses, by means of the

payment of a daily allowance, are refunded.

contact details:

durban office:

Physical address:

Trade & Investment House,

1 Arundel Close, Kingsmead Office

Park, Durban, 4001

Postal address:

Trade & Investment KwaZulu-Natal

PO Box 4245

Durban

4000

Tel: +27 031 3689600

Fax: +27 031 368 5888

Email: [email protected]

Website: http://www.tikzn.co.za

gauteng office:

Physical address:

Financial Place, 99 George

Storrar Avenue, Groenkloof, Pretoria,

0181

Postal address:

TIKZN Gauteng Office

Financial Place

99 George Storrar Avenue

Groenkloof

0181

Tel: +27 (0) 12 346 4386

Fax: +27 (0) 12 501178

6

Special Focus

Asexpected,quarterlynationalaccounts data published by national statistical agencies in Nigeria and South Africa indicated

that both countries have emerged from recession.

In Q2 2017, Nigeria GDP grew by a dismal 0.6% year-on-year, after five consecutive quartersofcontraction.Overtheperiodfrom March to June, South Africa grew at anannualrateof2.5%quarter-on-quarter.

Nevertheless, positive figures are mainly a result of Nigeria and South Africa bouncing back from very poor performance.

Exposed to internal and external headwinds, Nigeria and South Africa’s economic woes are not over; the recovery is still fragile.

Both in Nigeria and South Africa, agriculture is the main positive contribution to GDP growth in Q2 2017. After an El Niño-induced drought afflicted South Africa in 2016, agriculture, boosted

by better rainfalls, recorded a 13% y-o-y growth.

This figure is in line with the latest forecast from the Crop Estimates Committee, which indicates a possible 108.8% increase in maize output, the main crop, for the 2017 season.

An increase in crop output is also the main reason for the solid performance of the Nigerian primary sector.

Nigeria and South Africa also rebounded thanks to improved performance in the extractive industries. The latter were in the doldrums in 2016 because of low commodity prices.

Terrorism in the Niger Delta targeting production facilities created disruptions in Nigerian oil supply.

Hence, a rebound in oil output after six consecutivequartersofcontractioninoilGDP supported an exit from recession.

In South Africa, the mining sector - struggling with low profitability for years - benefited from higher commodity prices in order to step up output and confirmed the recovery initiated in Q1 2017.

In South Africa, the return to positive territory is also attributable to wholesale and retail activities resilience. Statistics South Africa estimates that household final expenditure contributed 2.8 percentage points to Q2 2017 GDP.

Easing inflationary pressure supported the recovery in trade activities, which recovered to 0.6% after it contracted by 5.9% in Q1.

Similarly, most sectors, except for construction(-0.5%q-o-q)andgovernmentservices(-0.6%q-o-q),benefitedfromapositive base effect after bleak performance recorded in Q1 2017.

Improved headline growth in Nigeria is also a result of particularly poor performance recorded in the reference period, namely Q2 2016.

Nigeria and South Africa: Out of recession, not yet out of trouble

export & import SA // SEPTEMBER 2017

By Coface, the international trade credit insurance company

7

risks

Widely anticipated, the return to growth in Q2 2017 of sub-Saharan Africa’s two biggest economies could prove short-lived.

Data reveal that growth is still heavily reliant on sectors vulnerable to external headwinds, namely agriculture and extractive industries:

•Agriculture output remains exposed to climatic variations, which could accelerate with global warming.

•The recovery in commodities prices is fragile. In particular, fading demand for metals and crude oil from China could hamper the recovery.

•Still exposed to supply disruptions, Nigeria is unlikely to gain much from its oil sector as they agreed to cap production as part of the OPEC effort to address the oil market imbalances. Hence, Nigeria is unlikely to obtain further upside from its main export.

In addition to external headwinds, domestic challenges remain:

•On a medical leave most of the year, Muhammadu Buhari’s ability to govern remainsinquestion,asthecountrycritically needs to diversify an economy overly dependent on oil revenues.

Increased dollar inflows and a new foreign exchange window for investors and exporters eased the pressure on the Nigerian naira. Nevertheless, multiple exchange rates continue to deter investment. Still under tight liquidityconditions,thegovernment’sreluctance to let the naira float is still an obstacle to regain investors’ confidence.

•In spite of the rebound in Q2 2017, prospects for the South African economy are still bleak. A high cost base and uncertainty surrounding the introduction of a new mining charter could weigh on a mining sector, which has been crucial in the rainbow nation’s return to positive growth.

Weak real wage growth and consumer confidence data indicate that the resilience of consumer spending, another driver of the recovery, could prove short-lived.

Plus, political turmoil could still weigh on an already low business confidence with a nail-biting ANC conference in December 2017, where Jacob Zuma’s success or is to be decided.

In addition, whoever succeeds Zuma will have to find solutions to reignite growth in order to rein in a record 27.7% unemployment rate, while curbing a rising public debt burden.

export & import SA // SEPTEMBER 2017

8

Recession exit inspires confidence, but no call for call for celebration

Special Focus

export & import SA // SEPTEMBER 2017

News that South Africa’s economy grew by 2.5 % in the secondquarterof2017wasmost certainly well received

and beat economist expectations.

The market expected growth of 2.3 percent while some meaningful analysts had the GDP growth forecast set at no more than 1.4 percent.

While this could be the first meaningful sign that SA’s economy is on the mend after spending some time in the doldrums, for many SA citizens there seems, as yet, little to celebrate.

Political uncertainty, high unemployment and junk status still remain on the agenda as inhibitors to our growth; while for those in the construction industry there is no good news as this sector continued to contract – albeit at a slower pace.

Trade Credit – the type of credit which companies grant to other companies – is a leading indicator of how the economy is performing in “real” terms.

The logic is that when the economy is performing well, companies are more likely to grant credit facilities to each other and vice versa.

We continue to see a decline in the approval ratio of trade credit transactions across almost the entire spectrum of the economy.

As a comparative - over the period March to August 2016 – we saw an outright decline ratio of 12.86%. This compares to a decline ratio of 16.5% for the same period in 2017.

Trade Credit encompasses short-term credit transactions (usually not outstanding for more than 60 days)

and constitutes literally billions of Rands worth of finance which companies grant to each other.

Almost every business in our economy finances their clients in this way. The need for trade credit also competes with other forms of credit – such as banking credit, and where banks slow their lending practices, companies have a greater demand to source credit from their suppliers.

Our experience at present is that companies are very nervous to extend facilities, and that this is a summary of their view on all the present risks that pervade in the market.

Large corporate failures such as Stuttafords (which was started in the 1850’s) do nothing to bolster this

9

Special Focus

export & import SA // SEPTEMBER 2017

confidence, but the number of business failures is not their only concern.

With high inflation and interest rates, the effect of late payments from customers could be disastrous to the profitability of an enterprise, especially in a struggling economywhereprofitmarginsarealreadysqueezed.

To understand the impact of this – a credit transaction of R 100 000 that remains unpaid for 12 months will cost the credit grantor approximately R 16 000 by adding the cost of inflation (6%) to the cost of lending (10%).

We are also seeing a rise in the number of businesses that are turning to alternative forms of financing to fund late payments from their clients – such as invoice discounting. Sadly this is potentially only a short-term fix, as financiers charge high rates for such loans – again impacting on a company’s profitability.

Particularly concerning is the effect of declining trade credit on small businesses. Where larger enterprises may have the depth in their balance sheet to withstand the effect of late or non-payment, small businesses are most vulnerable to even one bad debt or late payment.

These have a knock-on effect – if you cannot collect money from your debtors on time, you can’t pay your creditors, so you have to fund the difference through loans or extensions, all of which negatively affect cash flow; profitability; employment and ultimately economic expansion.

It will be some time before the economy can be declared “out of the woods”, but that the latest GDP numbers are at least a green shoot. If we are able to follow this through with political certainty; interest rate reductions; and fixed investment from the private sector, the latest GDP numbers could be the sign that we’re on the right path.

10

Investment funds: The South African headquarter company regime hurdle

With the increasing appetite for investments into African jurisdictions, the South African private

equitylandscapeneedstoadaptinorder to attract direct foreign investment and to facilitate the seamless investment and divestment in and from these jurisdictions.

The choice of vehicle for a private equityfundisdrivenessentiallybytwofactors – limited liability for investors and tax efficiency.

Whilst the legal status of companies is well established and the limited liability position of shareholders clear, companies are inefficient for tax purposes as they are separate taxpayers in their own right.

For this reason, South African private equityfundsusuallytaketheformofen commandite partnerships (partnerships).

Partnerships for South African tax purposes are fiscally transparent, which means that any income flowing through the partnership retains its character and is taxed in the partners' hands.

As a partnership is not a separate entity and not a taxpayer in its own right, the double taxation agreements (DTA) between each partner's home jurisdiction and the jurisdiction where the investments are located may provide for reduced withholding taxes.

Should there be no DTA (as is the case between some African and European jurisdictions) withholding

taxes will be levied at their full statutory rates on that partner, making that investment less attractive and as a result deter the Investors.

To mitigate this inefficiency, partnerships utilise a dual fund structure that provides a second mirrored partnership that is established outside of South Africa, with the same intention, investment strategy and structure as its South African counterpart (the Foreign Partnership).

These foreign partnerships are ordinarily established in Mauritius, Guernsey, or Jersey and are usually the sole shareholder in an investment holding company that is able to access DTA networks to mitigate the inefficiencies alluded to above.

A disadvantage of the structure is that it is costly and administratively burdensome. Given that South Africa has an extensive DTA network, South Africa is ideally placed to facilitate investments outside the common monetary area (the CMA) countries (especially those in Africa).

However, South African legislation currently lacks a suitable investment holding vehicle regime for a partnership's foreign Investors to invest through.

The south African headquarter companyIn order to encourage foreign investors to invest into South Africa and to mirror the advantages offered to foreign partnerships, the South African Revenue Service (SARS) established a

special dispensation under section 9i of the Income Tax Act, 58 of 1962, where an investment holding company meets the following criteria:•Each shareholder must hold at least

10%oftheequitysharesandvotingrights in the SA investment holding company;

•At the financial year end, at least 80% of the cost of the total assets must either be (i) an interest in equitysharesinqualifyingforeigncompanies; (ii) loans to foreign companies; or (iii) certain intellectual property licensed by the companytoqualifyingforeigncompanies; and

•Where the company's gross income for the year exceeds R5 million, at least half of that income must be comprised of either (i) rentals, dividends, interest or service fees paidbyaqualifyingforeigncompany;or (ii) proceeds from the disposal of foreignqualifyingsharesorintellectual property.

Special Focus

By Robert Newham an Associate and Kyle Beilings, a Senior Associate at Webber Wentzel

export & import SA // SEPTEMBER 2017

Kyle Beilings

Special Focus

Meeting the criteria above will ensure that the investment holding vehicle will be classified as a section 9i "HeadquarterCompany"(HQ)andprovide the following benefits:•The HQ shareholders will be exempt

from South African withholding tax on dividends, interest and royalties;

•The HQ will be exempt from South African capital gains tax on the disposalofequitysharesinforeigncompanies, provided that the HQ held at least 10% of such shares and voting rights in the foreign company disposed of;

•South African transfer pricing rules do not apply regarding back-to-back loans from the HQ to its foreign subsidiaries; and

•The HQ can elect its functional currency and therefore not incur income tax fluctuations on foreign currency.

The South African Reserve Bank requirestheinvestmentholdingvehicle to meet the following requirementsinordertoaccesstheHQ exchange control benefits:•Each shareholder in the HQ needs

toholdatleast10%oftheequityshares and voting rights in the company;

•No more than 20% of the HQ's shares may be held directly or indirectly by South African residents;

•At the end of each financial year, 80% or more of the assets of the company must consist of foreign assets (excluding cash, cash equivalentsanddebtwithatermofless than 1 year, which are not taken into account).

Should the investment holding vehicle meetthesethreerequirements, then the investment holding vehicle will be treated as a non-resident for exchange control purposes, be able to obtain, and advance offshore loan funding without exchange control approval, as well as be allowed to elect its functional currency.

At face value the HQ regime seems to be an attractive proposition, however, it has one major pitfall in the context ofprivateequity.Withoutevenlookingto the limited partners, a partnership's general partner will never hold at least

a 10% of the interests in the Partnership and therefore the underlying HQ.

Under the current regime, fund managers are therefore limited to using the "dual fund" model in order to attract offshore capital.

The benefits which the HQ regime is positioned to attract, such as increasing foreign direct investment into South Africa, improving the balance of payments, job creation, and creating a wealth of technical expertise within South Africa are therefore frustrated.

Amendments neededSection 9i of the Income Tax Act, in our view, needs to be expanded to allow privateequityfundsasso-called permissible shareholders, thereby enabling the partnership to meet the HQ definition. This would encourage investors to use South Africa as a preferred African investment destination.

The need for a "dual fund" model would become redundant, thereby bringing all capital directly into

South Africa for purposes of investing across the continent.

Ultimately, it would attract more foreign investors into South African partnerships, as they would be able to invest through a "one-stop-shop" which would cover both CMA and non-CMA investments and allow for South Africa to become a true investment gateway to Africa.

By implementing these amendments, there would be no adverse consequencestotheSouthAfricanfiscus.

Not having the burden of a foreign partnership will result in an increase in direct foreign investments, South Africa becoming more competitive as an investment gateway jurisdiction, retention of key skilled employees in South Africa and all forms of administrative and office support being rendered in South Africa - thus significantly contributing to multiple sectors of the South African economy and general consumer spend.

11 export & import SA // SEPTEMBER 2017

Robert Newham

12

Special Focus

The facility, located in Bryanston, Johannesburg, has a state-of-the-art 10 000-litre rainwater harvesting system and rooftop

solar energy generation plant, which significantly lower the building’s carbon footprint and reduces energy consumption by 55%.

The reduced energy consumption is partly due to a 34kW solar photovoltaic system that reduces the demand for grid power by at least 25%.

The facility also uses highly efficient LED light bulbs in place of conventional ones. This lighting technology, coupled with sensors designed to automatically turn off lights installed in highly-used office areas, contributes to energy savings of up to 35%. A majority of the lighting used in the warehouse is being switched off by a timer when dusk sets in.

The facility’s energy consumption and solar energy production is monitored and reported in real time.

Anthony Beckley, Vice President, Operations, DHL Express Sub-Saharan Africa, says, “The ‘greening’ of the building is in line with Deutsche Post DHL Group (DPDHL)’s goal to reduce all logistics-related emissions to net zero

by the year 2050. The measures we put in place in the facility have reduced the building’s overall energy consumption by 55%.”

“Even though the Bryanston project is still in its infancy, early results based on performance indicate that despite the cost of electricity and water increasing, the estimated payback period for the building’s upgrades is currently around three years, down from an initial estimate of 4.5 years,” Beckley adds. .

The energy savings of the facility will be tracked for the next three months, after which DHL Express will begin the roll-out of green upgrades to additional sites

across Sub-Saharan Africa, including the rest of South Africa, Nigeria, Ghana and Mozambique.

“The last and critical outcome we hope to achieve out of this ‘greening’ of facilities is to educate the employees on the importance of working together to attain our collective zero emissions goal. We are in the process of pushing through green policies, geared at saving resources and reducing carbon emissions, which will help shape a company culture. This is the first step in building greener, more efficient supply chains throughout our African operations.

DHL Express unveils its first green facility in SSA

export & import SA // SEPTEMBER 2017

13export & import SA // SEPTEMBER 2017

2016 showed a continued decline of 6% in the number of company insolvencies in the Central and Eastern

European region, following a fall of 14% in 2015.

In all, over the course of last year, six entities per 1 000 became insolvent. This improvement was in line with the favourable macroeconomic environment, largely due to the positive situation on the labour market, with lower unemployment rates and rising wages. Despite this, insolvencies are still above the pre-crisis levels of 2008 in most countries.

Romania and Slovakia were the only two countries to record lower levels of company insolvencies than before 2008.

The dynamics vary widely among the 14 CEE countries covered in this analysis. Eight countries recorded a decline in insolvencies in 2016. Bulgaria experienced the strongest fall of 35.6% and hardly any insolvencies in the pharmaceutical, IT or education sectors.

On the other hand, insolvencies in Hungary more than doubled compared to the previous year and in Lithuania they grew +35.2%. In Hungary’s case, the rise was mainly due to a higher number of ex officio company cancellations (which were barely present in the 2015 statistics).

Lithuania’s statistics were impacted by the State Tax Inspectorate and Social Fund’s process of “cleaning” the market of companies which had in reality been insolvent for some time.

Poland recorded a slight increase of 2.6% in proceedings as its insolvency statistics were affected by legal changes implemented last year to cover insolvencies and the restructuring of companies faced with payment problems.

construction fared worst among the poor sectorsA sectoral split shows that while some sectors enjoyed improvements last year, others experienced challengeswithliquidity.Thisvariedbetween countries, although there were some common trends throughout the region.

The construction sector faced the most difficult business environment. CEE economies were impacted by the switching to the new EU budget and lower investments in 2016, with a slower pace of GDP growth (down from 3.5% in 2015, to 2.9% in 2016).

In terms of construction output, most countries recorded a significant fall in activity which led to deteriorated liquidityconditionsforcompaniesinthe sector. For some countries, such as Estonia, Hungary and Russia, insolvencies of construction companies represented over 20% of total proceedings. positive trends anticipated over the upcoming yearsCoface therefore forecasts continued decreases in company insolvencies in CEE, down 3.9% in 2017 and a further 2.3% in 2018.

“The acceleration in GDP growth and the rebound in investment activity

herald more positive signals for businesses,” said Grzegorz Sielewicz, regional economist Central and Eastern Europe. “A new flow of infrastructural projects, stable contributions from household consumption and the development of foreign markets will all be economic supporters.”

The rebound in investments should be particularly beneficial for sectors such as construction, transport and the manufacturing of machinery, constructionequipmentandconstruction materials. Nevertheless, labour shortages will remain an obstacle for many expanding businesses.

Finally, businesses could experience some challenges related to developments in the global economy and political uncertainties.

The latter include the eventual negativeconsequencesofBrexitandinsecurities in Western Europe, such as the unclear election results in Italy. Political issues have also been observed in the Czech Republic, Poland and Romania.

Central & Eastern European Insolvencies overview

Special Focus

GROUP AFRICA pays close attention to the details whilst conducting your business to make sure that you are nothing but 100% satisfied with our service! Our Vision:

Our vision is to use Innovative technology with efficiency and Service Excellence we strive to become a logistics leader within the African continent.

Our Mission:

Is to implement our core values in developing good relationships in using a wide area of network clients and resources to provide cargo solutions to the corporate end user worldwide. We are committed to applying ethical business principles and practices. We aim at satisfying our clients and becoming socially responsible in engaging in community development.

Our Core Values At GROUPAFRICA we embrace core values such as:

• Accountability• Building authentic business relationships• Commitment• Communication• Honesty & integrity• Professionalism

• Quality with simplicity• Respect• Applying skills and utilizing resources.

The Expertise

Our company is a global logistics Service provider that is also registered with various networks specializing in the clearing and forwarding of Import cargo from International consignments to project shipments into Africa from the ports of South Africa, to the Exports of cargo all over the world.

Needless to say we have all the expertise that allows us to prepare and process the documentation and perform related activities pertaining to international shipments, port services and transport you can rest assured while we handle the tedious odds and ends with 100% service levels.

1) CLEARING AND FORWARDING: Our Services in this sector includes:

• Clearing and forwarding of import and export cargo from the local port to our

nominated warehouses and packing for export international.

• Booking the shipping lines and shipping of cargo to and from overseas.

• Import and export documentation services.

• Customs clearance working of EDI.• SA borders clearances and acquittal

services.• Port handling supervision and tally.• Project shipments and management.

2) TRANSPORT SERVICE’S:

We manage and run our own fleet of trucks that can carry loads from a (consolidated load) to 125 tonner abnormal load.

Our fleet

Consists of dedicated vehicles, abnormal units, flat decks, well decks, skeletal trailers, air ride units, crane truck units, hazardous packing and transport vehicles, heavy lift cranes, a 35 ton reach stacker (6m and 12m) and to our advantage we can stage your cargo free of charge.

Trucking has been the core activity of the group since its creation. Today, the group enjoys partnership co-operation with several of the main trucking companies in all of Africa. We have the following facilities, road bonds, port handling, bonded cargo storage, DDU and DDP shipments, and cross border road freight. GROUPAFRICA offers a comprehensive solution to any request of consolidated transport as well as full-contained loads, throughout Africa Tracing/tracking and reporting is available 24/7.

(T) +27 31 827 6311 (F) +27 86 697 8451 (E) [email protected] (W) www.groupafrica.org(E) [email protected] (Mobile) +27 74 038 3829

(Branch offices): TATA Chemicals building, Ground floor, 140 Johnson road, Maydon Wharf 15, Durban, 4000, South Africa

Through our vast infrastructure in Central and Southern Africa, we service all the available road freight routes, such as:

• Zimbabwe - all destinations• Zambia - all destinations• DRC - Lubumbashi, Likasi, Tenke, Kolwezi,

Kinshasa • Mozambique - all destinations • Botswana - all destinations• Lesotho - all destinations• Swaziland - all destinations• Namibia - all destinations• Angola - from Oshikango to Cabinda, Lobito

to Chitato • Tanzania – all destinations• Kenya - Nairobi, Mombasa, Kisumu, Moyale• Uganda - Kampala, Mbarara, Kabale• Rwanda - Kigali, Bakavu, Gisenyi• Burundi - Bujumbura • Congo Republic - Brazzaville• Malawi - all destinations.

16 export & import SA // SEPTEMBER 2017

African SMEs to grow faster through supply chain management

Small and medium enterprises (SMEs) have great potential for expansion in Africa, because they are agile and flexible enough to

exploit the opportunities in the continent’s growing economies.

This according to John Lucas, Country Manager of DHL Express South Africa, speaking at the China Homelife & China Machinex Fair in Johannesburg this month.

Lucas adds that SMEs however need to make supply chain management part of their business plan if they want to succeed. “According to DHL’s own research, conducted by HIS Global Insight, SMEs that engage in international markets are twice as likely to be successful than those that only operate domestically.”

Lucas states that DHL considers SMEs to be the engines for growth in Sub Saharan Africa. “The International Monetary Fund has estimated that the number of Africans joining the working age population by 2035, will exceed that of the rest of the world combined.

SMEs make up a large portion of the employment for these individuals, and indeed, around 92% of DHL’s business globally comes from the SME market.”

Finding the right partner to help build and manage a company’s supply chain is vital in an SME’s growth process, according to Lucas. He explains that SMEs have a need to achieve certain important outcomes, which is why the capacity of one’s logistics service provider matters.

“In order to succeed, an SME needs to be able to increase inventory velocity, achieve the shortest possible cycle times, continually improve their supplier performance and drive their sales and market share. Supply chain management is central to this.”

Additionally, utilising opportunities to take part in the global economy will speed up SMEs’ growth, says Lucas.

“According to the World Trade Organisation, studies on African firms show that participation of SMEs in international markets can result in higher growth and employment through economies of scale and in enhanced productivity and innovation through learning effects.” Partnering with a logistics provider experienced with the customs requirementsofvariousregionsisvital,according to Lucas.

“Exporting goods can become challenging when going through customs, and improper or incomplete documentation, restricted items or any other issues could potentially add significant delays to one’s delivery. A good logistics service provider should be able to give its clients advice on how to avoid delays with customs, as well as be able to facilitate if goods are delayed at international borders.”

With operations across 51 markets in Sub-Saharan Africa, servicing over 40,000 customers, delivery efficiency is an important factor for DHL.

“DHL considers SMEs to be the engines for growth in Sub Saharan Africa, but they need to be agile and flexible enough to adapt to changing regulatory standards anddistributionrequirementsfortheirproducts. Effective supply chain management is central to this,” Lucas concludes.

Supply Chain

John Lucas

17 17 export & import SA // SEPTEMBER 2017

18 18 export & import SA // SEPTEMBER 2017

China Homelife and China Machinex prove huge success

The reason co-located shows such as China Homelife and China Machinex allow for strategic and effective business

between buyers, traders and exhibitors, comes down to the efficient match-making services offered onsite.

This facility ensured resourceful networking and successful high level negotiation, as complimentary Mandarin translation services were offered in order to conduct proficient business deals.

More than 900 one-on-one appointments were set up in the matchmaking zone between buyers and exhibitors. What also made this year’s shows effective, was the new Online to

Offline Campaign, which launched this year and allowed exhibitors and buyers the opportunity meet online prior to conducting business face-to-face on the show floor to sign the deal.

This campaign now enables Southern African buyers to source products from participating Chinese Manufacturers and suppliers 365 days a year, on the newly developed Meorient International Exhibition sourcing portal.

VIP hosted buyer from Mauritius, Hekhmat Currimjee, who owns Currimjee Group of Companies, found the shows to be very valuable. He said, “Shows like China Homelife and China Machinex are pivotal for SADC countries and countries that form part of BRICS,

because of the trade relations and economic growth for all countries involved.

“We are always on the lookout for new products to introduce to the African market, and this exhibition has proven to be a wonderful platform for my companytosourcetopqualityandtrending products. I have been very impressed with this well-defined show, and it’s great to see how it has grown year-on-year.”

A leading Chinese exhibitor, MF Textile, forming part of China Homelife, was very happy to showcase the company’s products to the South African market for the first time. Jason Yang, General Manager of MF Textile said, “We will

Supply Chain

19 export & import SA // SEPTEMBER 2017

Supply Chain

most certainly be back at China Homelife in 2018. We have had a great show and made some important contacts on our first visit to South Africa. We look forward to continued business in this market.”

“Over the past decade, Chinese manufacturers and suppliers have seen an increased demand from Africa when it comes to sourcing qualityproductsacrossabroadspectrum of industries,” says Binu Pillai, Chief Operating Officer of Meorient International Exhibition.

“This is evident in the shows’ growth over the past three years. We are happy that we have been able to provide a platform whereby buyers can meet with relevant suppliers all under one roof.

“We look forward to coming back next year and expanding the show to host more than 750 Chinese exhibitors, incorporating a broad range of sectors.”

Together with logistics partner, DHL, visitors were given added value when attending this year, with the constructive and informative “All you need to know about Importing” seminar programme, which assisted interested businesses and traders with valuable information on how to import products from China.

“Working with DHL, one of the world’s largest logistics companies, has proven invaluable for visitors this year. A strategic partnership of this nature helped take the buyers needs to the next level as they not only able to source topqualityChineseproducts,buttostart the importing process as well,” said Pillai.

The lucky winner of the 2017 China Homelife and China Machinex Grand Prize was VIP Buyer, Simon Modau, of Aristo Trading Group. Modau will have the opportunity to visit China Homelife in Dubai, a prize valued at R35 000.

China Homelife and China Machinex

2018 are set to take place from 26 to

28 September 2018 at the Gallagher

Convention Centre in Johannesburg.

China Homelife and China Machinex will

also be expanding into Africa in 2018,

with their African Series, introducing two

new shows in Lagos, Nigeria (5 to 7

September 2018) and Nairobi, Kenya

(5 to 7 December 2018).

20 export & import SA // SEPTEMBER 2017

Cold Chain

Next-generation cold-chain monitoring solution from ORBCOMM

Fuel and temperature management, maintenance, logistics, and regulatory compliance for refrigerated

transport assets are now a cinch thanks to a next-generation cold-chain monitoring solution from ORBCOMM.

The leading global provider of Machine-to-Machine and Internet of Things (IoT) solutions’ PT 6000 is available as a 3G or LTE cellular or dual-mode satellite-cellular version.

It forms part of ORBCOMM’s comprehensive telematics solution, which includes sensors, connectivity, and the CargoWatch application.

The compact, ruggedised PT 6000 enables complete visibility and control of cold-chain operations to help ensure the integrity of temperature-controlled cargo as it moves along the supply chain, Henry Smith, Vice President Sales – Africa at ORBCOMM explains.

ORBCOMM’s enhanced reefer management solution provides the precise temperature monitoring capabilities and records needed for compliance with the Food Safety Modernisation Act of the Food and Drug Administration (FDA) of the US.

“In refrigerated trucking, it is critical for fleet owners to be compliant with the FDA’s regulatoryrequirements.ORBCOMM’s technology provides the end-to-end visibility and control to not only meet these regulatoryrequirements,butensure the highest level of service throughout the cold chain,” says Craig Malone, Executive Vice President of Product Development at ORBCOMM.

The solution can set reefer temperature remotely, change

reefer state, initiate a defrost, and more, with two-way commands.

It can also receive real-time alarms when specific conditions are detected, such as when an active reefer is turned off, or when the cargo-area temperature deviates from the set points, or does not match values specified by the order,

an asset enters or exits a geofence, rapid fuel loss is detected, and more.

ORBCOMM’s feature-rich solution is compatible with every type of refrigerated unit for maximum utilisation and seamless installation on the wall of a refrigerated trailer or inside a reefer cabinet.

The device supports up to three temperature sensors to accommodate reefers with multiple zones, and has a rechargeable battery that reports for up to ten days on a single charge when no vehicle power is available.

In addition, the device is integrated fully with third-party dispatch and in-cab software providers, including Innovative Computing Corp., TMW Systems, McLeod Software, Add On Systems, PeopleNet, SSI, and Prophesy.

“We continue to see a migration toward IoT technology as part of our transportation customers’ core strategies to reduce costs and add efficiencies, and we are pleased to be the solution provider of choice for some of the biggest names in the industry,” Malone concludes.

Henry Smith vice president sales africa at Orbcomm

21 export & import SA // SEPTEMBER 2017

22 export & import SA // SEPTEMBER 2017

Credit Guarantee experienceCover is considered on a case-by-case basis

Recent political highlights•KingMSWATIIIIassumedthethrone

since25April1986.TheHouseofAssemblyelectionswerelastheldon24August2013witharunoffon20September2013,thenextarescheduledforSeptember2018.

•AccordingtotheIMF’svisitreporttoSwaziland,“Thegovernmenthastakenactionsonvariousfrontstosupportgrowth,tacklehighunemploymentandreducepovertyandincomeinequality.Structuralreformstoaddressthelackofskilledworkers,betteralignwageandproductivitydynamics,simplifybusinessregulationsandstrengthentheinstitutionalenvironmenthavethepotentialtosignificantlyboostinvestmentandemployment.Focusingreformeffortsinthisdirectionappearsthemostpromisingwaytodeliverstrongermoreinclusive

growth.•InJuly,TheAfricanNationalCongress

calledforSwaziland, sub-Saharan Africa'slastabsolutemonarchy,tobereferredtotheSouthernAfricanDevelopmentCommunity(SADC)forabuseofhumanrightsandsuppressionofdissentandpoliticalactivity.Swaziland’sSuppressionofTerrorismAct,whichhasbeenusedbygovernmenttobanpoliticalgroupsopposingKingMswati’srule,waslastyeardeclaredunconstitutionalbythecountry’sHighCourt.

Recent economic highlights•Colombia’seconomybenefitsfrom

AccordingtotheBMI’sview:Swaziland'srealGDPgrowthwillreturntopositiveterritoryin2017onthebackofrecoveringagricultureoutput,butthegoodnewsfortheeconomyendsthere.WeakgrowthinneighbouringSouthAfricawillweighonfiscalspendingandexportgrowthwhilehigherinflationinSwazilandthaninSouthAfricawillerodethepurchasingpoweroffiscalrevenuesandexacerbateweakSouthAfricandemandforSwaziland'sexports.Theeconomywillcontinuetofacesignificantchallengesoverthecomingquarters.ThegroupisforecastingthatrealGDPgrowthwillremainbelow1.5%inboth2017and2018.Farmingoutputfellsharplyin2016onthebackofaseveredrought,butissettoimprovein2017asrainsreturn.Productionofsugarcane,thecountry'smaincrop,fellby15%in2016butisforecastbytheUS

DepartmentofAgriculturetoriseby17%in2017.

•SwazilanddependsonSouthAfricafor60%ofitsexportsandformorethan90%ofitsimports.Subsistenceagricultureemploysapproximately70%ofthepopulation.Themanufacturingsectordiversifiedinthe1980sand1990s,butmanufacturinghasgrownlittleinthelastdecade.Sugarandsoftdrinkconcentratearethelargestforeignexchangeearners.Mininghasdeclinedinimportanceinrecentyears.Coal,gold,diamond,andquarrystoneminesaresmallscale,andtheonlyironoremineclosedin2014.

•2017IndexofEconomicFreedomreportedthatinefficientregulatoryandlegalframeworkshavedeterreddevelopmentofmoredynamicprivateinvestmentandproductioninSwaziland.Privatizationhasprogressedonlymarginally.Averagingannualgrowthofaround2%overthepastfiveyears,Swaziland’seconomicperformancehaslaggedbehindthatofothereconomiesintheregion.Thereportcontinuestostatethatbureaucraticinefficiencyandcorruptionaffectmanyaspectsoftheeconomy,discouragingmorevibrantactivity.Themostvisibleconstraintsontheemergenceofeconomicdynamismarerelatedtopoormanagementofpublicfinance,administrativecomplexities,andalackofrespectforcontracts.Courtenforcementofpropertyrightsisvulnerabletopoliticalinterference.

•TheIMFforecastedthatSwaziland’seconomywillgrowataslowerpacein

SWAZILAND

Credit Guarantee Insurance Corporation of Africa Limited

Credit Guarantee House, 31 Dover Street, Randburg, 2194, PO Box 125,

Randburg, 2125, Tel: 011 889 7000, Fax: 011 886 1027,

Email: [email protected]

Credit Guarantee country profile

23 export & import SA // SEPTEMBER 2017

Customs

Source: IMF DataMapper (http://www.imf.org/external/datamapper/index.php)

Key Indicators 2015 2016 2017 2018

GDP 1.1 -0.4 0.3 0.3

Inflation(Average consumer price) 4.9 8.0 7.6 6.2

Volume of imports of goods and services -5.5 20.9 -10.9 3.4

Volume of exports of goods and services 7.6 1.4 0.7 1.9

General government revenue (GDP%) 28.4 24.5 27.1 25.9

General government total expenditure (GDP%) 33.0 36.9 35.2 35.9

Current account balance (GDP%) 10.8 -5.2 -0.9 35.9

Latest trade developments

Economic Indicators

2017becauseofaregion-widedrought,whichislikelytohurtSwaziland’srevenuefromsugarexportsandotheragriculturalproducts;tourismandtransportsectorswillalsodecline.Overgrazing,soildepletion,drought,andfloodsarepersistentproblems.Swaziland’srevenuefromSACUreceiptsalsoareprojectedtodeclinein2017,makingitharderforthegovernmenttomaintainfiscalbalance.

•Economicgrowthisprojectedtoreboundto1.7%in2017,inpartduetomodestlyimprovedregionalgrowthprospectsandrecoveryofagriculturalproductionfollowingbetterrains.Thisisexpectedtosupportmoderategainsinpovertyreduction.Overthemediumterm,amorefavorableregionaleconomicoutlookisexpectedtosustaintheexternalsector.However,accumulationofdomesticarrearstogetherwithfiscalpressuresexertedbythe2016salaryreviewwillcontinuetoposesignificantriskstomacroeconomicsustainability

•TheIMFcontinuestoreport“Swaziland’skeychallengegoingforwardistopreservemacroeconomicstabilityagainstlowSACUrevenueandsustaingrowthtomakeinroadsinreducinghighunemploymentand

incomeinequality.ThegovernmentandtheCentralBankofSwazilandhavetakensomestepstocontainthefiscaldeficitandcounterthestillhighinflation.However,heightenedfiscalandexternalvulnerabilitiescallforadditionalactions.

•Inlightofthemacroeconomicoutlook,significantfiscaladjustmentisneeded,startinginfiscal2017/18,toensuremacroeconomicstabilityanddebtsustainability.Thefinancialsectorremainssoundandtheauthoritiesaretakingstepstomonitorandmanagepossiblerisksandadvancekeyfinancialsectorreforms.

•GDPexpanded0.6%in2016fromthepreviousyear.

•Theinflationratewasrecordedat6.9%inJuneof2017.

•Swazilandranks108in2016accordingtothe2017IndexofEconomicFreedom.

•Major exports: soft drink concentrates, sugar, timber, cotton yarn, refrigerators, citrus, and canned fruit

•Major imports: motor vehicles, machinery, transport equipment, foodstuffs, petroleum products, chemicals

•Main trade partners: South Africa,

•SA exports to Swaziland totalled R11.5bn in 2011, R12.4bn in 2012, R14.6bn in 2013, R16.3bn in 2014, R15.9bn in 2015, R16.9bn in 2016 and R9.3bn in Jan-July 2017.

•SA imports from Swaziland totalled R6.8bn in 2011, R9.4bn in 2012, R11.2bn in 2013, R12.5bn 2014, R13.9bn in 2015, R15.4bn in 2016 and R8.4bn in Jan-July 2017.

Researched and compiled by Cindy Motloung, economic services – Credit Guarantee Insurance

SA EXPORTS TO SWAZILANDA (TOP 5)

2016 2017 (Jan-Juiy)

Mineral products R2953285819 Mineral products R1616505123

Chemicals R2005666619 Machinery R1012354262

Machinery R1796658419 Prepared foodstuffs R979393540

Prepared foodstuffs R1673569196 Chemicals R969392857

Vehicles aircraft & vessels R1520948765 Vehicles aircraft & vessels R742095789

Country ratingS/T business cycle indicatop

S/T political indicator

Debt recovery

3C Suggested use of a collection agent

Credit Guarantee country profile

Country rating key - political risks: 1 = low, 2 = medium, 3 = highCommercial risks: A = low, B = medium, C = high

24 export & import SA // SEPTEMBER 2017

Credit Guarantee experienceCover is considered on a case-by-case basis

Recent political highlights•ThailandistheonlySoutheastAsian

countrynevertohavebeencolonizedbyaEuropeanpower.Asaidtobebloodlessrevolutionin1932ledtotheestablishmentofaconstitutionalmonarchy.

•Theinterimmilitarygovernmentcreatedseveralinteriminstitutionstopromotereformanddraftanewconstitution,whichwaspassedinanationalreferenduminAugust2016.Electionsaretentativelysetformid-2018,lastheldon30March2014.KingPhumiphonAdunyadetpassedawayinOctober2016after70yearsonthethrone;hisonlyson,Wachiralongkon,ascendedthethroneinDecember2016.HesignedthenewconstitutioninApril2017.

•Thailandisexpectedtoholdageneralelectioninmid-OctobernextyearattheearliestorDecember2018atthelatest,accordingtoanElectionCommissionofficial.Thecountry's2017Constitutiongivescharterwritersupto240daysfromApril6thisyear,thedatethecharterwaspromulgated,towrite10organicBills-fourofwhicharerequiredtobeenactedbeforethegeneralelectioncanbeheld.Basedonthistimeframe,therewassomespeculationthattheexercisemaybecompletedbeforethe2December2017,deadline.ThefourBillsconcerntheElectionCommission,politicalparties,MPelectionsandacquisitionofsenators.

•Thailand'sSupremeCourthasissued

anarrestwarrantforformerprimeminsterofThailandYingluckShinawatraaftershefailedtoshowupincourttoheartheverdictofanegligencetrialthatislikelytofurtherpolarizethekingdom’smuch-dividedpoliticalsystem.Thehighly-anticipatedverdicthasnowbeenpostponeduntil27Septemberandifconvicted,Yingluckfacesupto10yearsinprisonandalifetimebanfrompolitics.AccordingtosourceswithinherPheuThaiparty,Yingluckhasfledabroad,reportstheBBCandReuters.Herexactwhereaboutsareunknown.

•AccordingtotheOECD’soverview,thesourcestatedthat,forThailandtobecomeamoreinclusiveandhigh-incomeeconomy,thecountryneedstogobeyondpromotingregionalintegrationandbusiness-friendlyregulatoryreform.Itneedstoinvestineducationandlife-longskillstrainingtoempoweritslabourforceandmakeitmoreproductive.

Recent economic highlights•HongKonghasafreemarket

Thailandishighlydependentoninternationaltrade,withexportsaccountingforabouttwo-thirdsofGDP.Thailand’sexportsincludeelectronics,agriculturalcommodities,automobilesandparts,andprocessedfoods.Theindustryandservicesectorsproduceabout90%ofGDP.Theagriculturalsector,comprisedmostlyofsmall-scalefarms,contributesonly10%ofGDPbutemploysaboutone-thirdofthelabourforce.Thailandhasattractedanestimated3.0-4.5millionmigrantworkers,mostlyfromneighboring

countries.•Growthhasslowedinthelastfew

years,however,duetodomesticpoliticalturmoilandsluggishglobaldemand.Nevertheless,Thailand’seconomicfundamentalsaresound,withlowinflation,lowunemployment,andreasonablepublicandexternaldebtlevels.Tourismandgovernmentspending-mostlyoninfrastructureandshort-termstimulusmeasures–havehelpedtoboosttheeconomy,andTheBankofThailandhasbeensupportive,withseveralinterestratereductions.

•ReutersinMayreportedThailand’seconomyexpandingatitsfastestquarterlypaceinfouryearsinthefirstquarterboostedbyrecoveringexports,butalsomentionedthecountry’smonetarypolicywilllikelyremainloosetocushionstill-subduedinvestmentactivity.

•Thegovernmentraiseditsexportoutlookfor2017,suggestingtherecoverywasgainingtraction,buttheeconomyfacesrisingglobaltradeprotectionismandcapitaloutflowrisksastheU.S.FederalReservepreparestohikeratesagainthisyear.

•AccordingtoanotherReuters’report,“Aglobaleconomicrecoveryhelpedliftourexportstoallkeymarkets.Shipmentsofcapitalgoodsandagriculturalproductscontinuedtogrow,”saidPimchanokVonkhorporn,anofficialatthecommerceministry.InJanuary-May,exportsrose7.2%fromayearearlier,thehighestpaceinsixyears.Shipmentsareworthabouttwo-thirdsofSoutheastAsia’ssecond-largesteconomyandarejust

THAILAND

Credit Guarantee Insurance Corporation of Africa Limited

Credit Guarantee House, 31 Dover Street, Randburg, 2194, PO Box 125,

Randburg, 2125, Tel: 011 889 7000, Fax: 011 886 1027,

Email: [email protected]

Credit Guarantee country profile

25 export & import SA // SEPTEMBER 2017

Source: IMF DataMapperSource: IMF DataMapper

Source: IMF DataMapper (http://www.imf.org/external/datamapper/index.php)

Key Indicators 2015 2016 2017 2018

GDP 2.9 3.2 3.0 3.3

Inflation -0.9 0.2 1.4 1.5

Volume of imports of goods and services 0.9 -2.5 2.7 4.3

Volume of exports of goods and services 1.8 1.1 3.1 1.8

Unemployment rate 0.9 0.8 0.7 0.7

General government revenue (% of GDP) 22.4 21.9 21.9 22.1

General government total expenditure (% of GDP) 22.2 21.5 23.5 23.9

Current account balance (% of GDP) 8.1 11.4 9.7 7.8

Latest trade developments

Economic Indicators

recoveringafteryearsofweakness.Theministryisconfidentofachievingits2017exportgrowthtargetof5%andseesastrongbahtasashort-termfactor,Pimchanoksaid.

•KrisadaChinavicharana,headoftheministry'sfiscalpolicyoffice,toldanewsconferencelateJulythattheeconomywillbedrivenbyexportsandgovernmentspending,whileprivateinvestmentintheconstructionsectorislikelytoslowdown.

•Thailand’sGDPexpanded3.7%fromayearearlierintheJunequarterof2017,comparedtoa3.3%growthinthefirstquarter2017andabovemarketexpectationsofa3.2%expansion.Thepacewasslightlyfasterthanthe1.2%forecastinaReuterspollandthe0.5%growthinthepreviousquarter,whichwasrevisedupfrom0.4%.

•Consumerpricesincreased0.3%year-on-yearinAugustof2017,followinga0.2%riseinthepreviousmonthbutbelowmarketexpectationsofa0.4%gain.

•Thailandisranked46among190economiesintheeaseofdoingbusiness,accordingtothelatestWorldBankannualratings.

•Major exports: automobiles and parts,

computer and parts, jewelry and precious stones, polymers of ethylene inprimaryforms,refinefuels,electronic integrated circuits, chemical products,rice,fishproducts,rubberproducts, sugar, cassava, poultry, machinery and parts, iron and steel and their products

•Major imports: machinery and parts, crude oil, electrical machinery and parts, chemicals, iron & steel and product, electronic integrated circuit, automobile’s parts, jewelry including silver bars and gold, computers and

parts, electrical household appliances, soybean, soybean meal, wheat, cotton, dairy products

•Main trading partners: US, China, Japan, Malaysia, Hong Kong, UAE, Australia.

•SA exports to Thailand totalled R3.4bn in 2011, R3.9bn in 2012, R4.6bn in 2013, R5.2bn in 2014, R5.5bn in 2015, R7.2bn in 2016 and R4.5bn in Jan-July 2017.

•SA imports from Thailand totalled R16.5bn in 2011, R22.1bn in 2012, R26.5bn in 2013, R25.8bn in 2014, R26.3bn in 2015, R31.8bn in 2016, R18.4bn in Jan-July 2017.

Researched and compiled by Cindy Motloung, economic services – Credit Guarantee Insurance

SA EXPORTS TO THAILAND (TOP 5)

2016 2017 (Jan-July)

Products Iron & steel R2358260488 Products Iron & steel R1984688507

Machinery R1779385750 Machinery R942735517

Wood pulp & paper R1049752369 Wood pulp & paper R621306944

Chemicals R982060129 Chemicals R463147064

Vehicles aircraft and vessels R323286482 Mineral products R155607851

Country ratingS/T business cycle

indicatopS/T political

indicatorDebt recovery

1A Suggested use of a collection agent

Credit Guarantee country profile

Countryratingkey-politicalrisks:1=low,2=medium,3=highCommercialrisks:A=low,B=medium,C=high

26 export & import SA // SEPTEMBER 2017

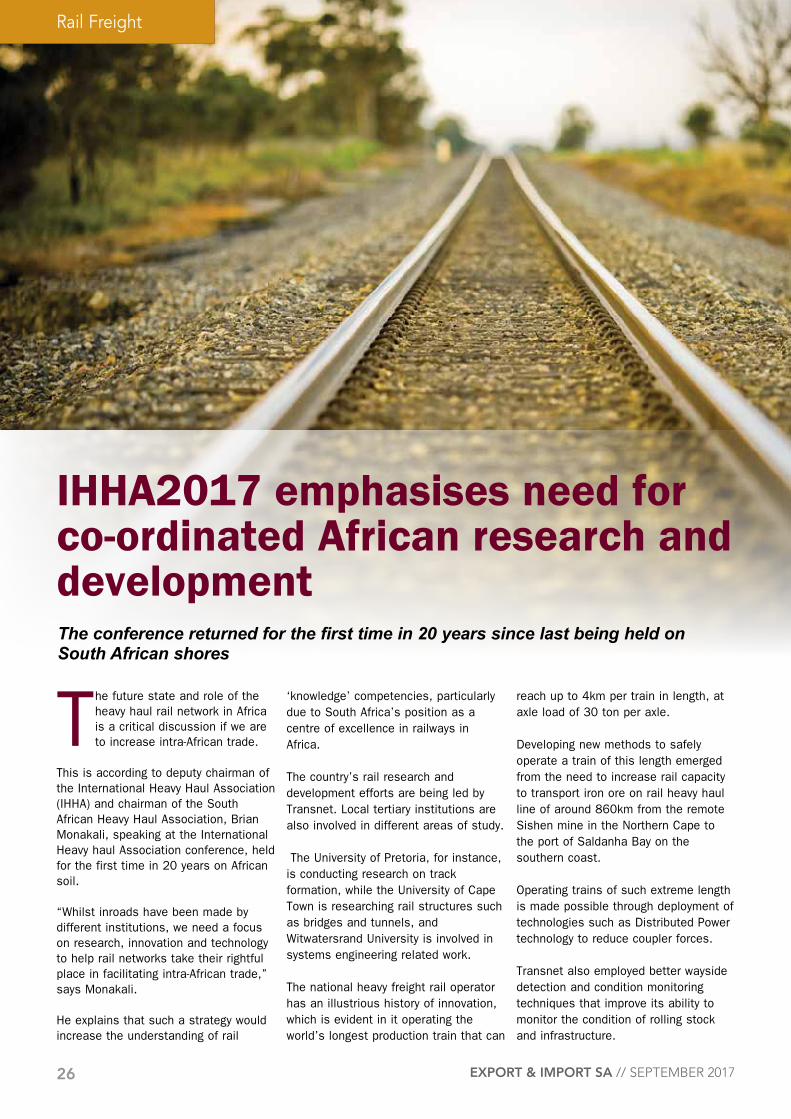

The future state and role of the heavy haul rail network in Africa is a critical discussion if we are to increase intra-African trade.

This is according to deputy chairman of the International Heavy Haul Association (IHHA) and chairman of the South African Heavy Haul Association, Brian Monakali, speaking at the International Heavy haul Association conference, held for the first time in 20 years on African soil.

“Whilst inroads have been made by different institutions, we need a focus on research, innovation and technology to help rail networks take their rightful place in facilitating intra-African trade,” says Monakali.

He explains that such a strategy would increase the understanding of rail

‘knowledge’ competencies, particularly due to South Africa’s position as a centre of excellence in railways in Africa.

The country’s rail research and development efforts are being led by Transnet. Local tertiary institutions are also involved in different areas of study.

The University of Pretoria, for instance, is conducting research on track formation, while the University of Cape Town is researching rail structures such as bridges and tunnels, and Witwatersrand University is involved in systems engineering related work.

The national heavy freight rail operator has an illustrious history of innovation, which is evident in it operating the world’s longest production train that can

reach up to 4km per train in length, at axle load of 30 ton per axle.

Developing new methods to safely operate a train of this length emerged from the need to increase rail capacity to transport iron ore on rail heavy haul line of around 860km from the remote Sishen mine in the Northern Cape to the port of Saldanha Bay on the southern coast.

Operating trains of such extreme length is made possible through deployment of technologies such as Distributed Power technology to reduce coupler forces.

Transnet also employed better wayside detection and condition monitoring techniquesthatimproveitsabilitytomonitor the condition of rolling stock and infrastructure.

Rail Freight

IHHA2017 emphasises need for co-ordinated African research and developmentThe conference returned for the first time in 20 years since last being held on South African shores

27 export & import SA // SEPTEMBER 2017

Rail Freight

Monakali says countries that have successfully harnessed the power of rail, like the United States, have demonstrated the benefits that can be derived from a co-ordinated research, development and testing ecosystem. He gives example of the Transportation Technology Center, Inc in Colorado, as well as Sweden’s Chalmers Railway Mechanics institute at Chalmers University of Technology.

He adds, however, that the outcomes from their research efforts cannot be applied universally because the characteristics of their rail infrastructure differs from South Africa and the rest of the African continent.

“This is why we’ve prioritised this topic for high level discussion at the conference as it was the ideal opportunity to firm up thinking around the issue to address our African rail research.”

He adds that the heavy haul principles of running longer trains can be used to promote rail interconnectivity between countries on the continent, and are a lower cost alternative to upgrading

rolling stock axle loads or building new heavy haul lines.

Further cost savings can be achieved through strict maintenance standards and condition monitoring systems, with Transnet, for instance, recording at least 30% improvements in reliability and reduction in asset failures.

“I believe that the best way to achieve our goals would be to create a forum and platform that manages and co-ordinates African rail technology intellectual property,” Monakali says. “Its role would be to align institutional knowledge and create uniform rail technology solutions, while identifying gaps in the African rail knowledge landscape, with Transnet, as the heavy haul operator, at the forefront.

“I’m confident we’ll be able to walk away from this year’s conference with a framework of how that can be achieved. But we need to improve co-operation between organisations doing research and those gathering data that can help the entire industry make better-informed decisions. The railway community has to

keep pushing the envelope to improve performance and benchmarks.”

The conference, bringing over 1 000 international and local delegates, was hosted in Cape Town from 2-6 September around the theme of ‘Advancing Heavy Haul Technologies and Operations in a Changing World’.

Brian Monakali

28 export & import SA // SEPTEMBER 2017

World ACD: China engine sputtering

The stories about recent developments in air cargo run the risk of becoming somewhat monotonous: July was again a

month with double digit year-over-year (YoY) growth. As Sonny Bono wrote 50 years ago in his famous, yet rather repetitive song: "the beat goes on, yes, the beat goes on".

Indeed the beat goes on and it is not at all surprising that many within the industryarequitehappygoingalongwiththe beat. After all, with the industry now steadily picking up after a number of years in the doldrums, what is there to complain about?

Underneath the continuing worldwide trend, however, we noticed a movement worthy of mention. But first the overall picture for July.

Overall YoY volume growth was 11.8% worldwide, caused by above average growth from the origins Europe (14.2%), MESA (13.5%) and Asia Pacific (13%), and below average figures for other regions.

The southern hemisphere origins of South America and Africa did rather poorly (3.6% and 2.6% respectively).MESA (Middle East and South Asia) and Asia Pacific were the fastest growing

destination areas with growth of 14.9% and 13.3% respectively.

General cargo continued to increase faster (+12.6%) than the other product categories (+9%), with the exception of pharmaceuticals (+17.6%).In terms of yields, July saw a considerable worldwide YoY-yield increase, of +7.8% in USD.

The Asia Pacific region contributed heavily to this impressive figure by scoring an even more impressive 13.2% USD-yield increase for business originating in the area. Month-over-month (MoM), however, worldwide yields did not increase. Measured in USD they remained stable, in EUR they lost 2,3%.

Yield-wise, North America was a good destination to send goods to. Whilst incoming volume remained the same as in June, USD-yields for business to the region were slightly better MoM, but increased by 15.6% YoY.

The surprising July-developments were related to China. For the first time this year, the world's air cargo engine sputtered a bit (relatively speaking, that is). The origin China saw double-digit growth for every month so far this year,

managing an average growth of 19% thus far this year and outstripping by far every market in the rest of the world, with the exception of July, where it only managed a meager 8% growth.

Air cargo needed the compensation of high growth from places like Hong Kong, Germany, India, the United Kingdom, Singapore and the Netherlands to achieve its July-growth of 11.8% YoY. By the way, incoming traffic in China continues to boom (+21% YoY).

The China situation is also reflected in our DTK measure for July. When the %-growth in DTK's (Direct Ton Kilometers) surpasses the %-growth in volume, this means an increase in the average distance between origin and destination of shipments.

In the first half of the year, DTK-growth indeed easily outpaced volume growth, but hardly so in July (DTK +11.9% vs. volume +11.8%).

Given the mostly long distance character of air cargo ex-China, the country's relative weakness contributed to this deviation from the trend.

Air Freight

29 export & import SA // SEPTEMBER 2017

Ports & Shipping

A newopen-accessliquefiedpetroleum gas (LPG) plant has been opened at the Port of Saldanha on the West Coast of

South Africa and will aid in increasing the use of environmentally-friendly and affordable LPG in the national energy mix.

Transnet National Ports Authority (TNPA) awarded Sunrise Energy a 30-year concession – including planning and construction – in 2013 to build and operate the LPG terminal.

Sunrise Energy is a partnership between the South African private and public sectors. It is 60% owned by Mining, Oil & Gas Services (MOGS), a subsidiary of Royal Bafokeng Holdings, and 31% by the Industrial Development Corporation.

Saldanha Port Manager Vernal Jones said: “This investment of R1.09 billion will create broader LPG access in the Western Cape. The terminal will boost the capacity of existing LPG distributors as well as enable the entry of new small, medium-sized and microenterprises, who have had restricted access to the market

because of supply constraints and lack of access to enabling infrastructure.”

Jones said TNPA’s awarding of this contract to a black owned company speaks strongly to Transnet’s commitment to its Market Demand Strategy (MDS) and the vision of the South African government’s Operation Phakisa programme of creating capacity ahead of demand and unlocking South Africa’s oceans economy.

Partnerships between South Africa’s state-owned port authority and the private sector emanate from Section 56 of the National Ports Act, which mandates TNPA as landlord and ports master planner, to contract with private terminal operators to design, construct, rehabilitate, develop, finance, maintain and operate port terminals or facilities.

The facility comprises a 10.9 hectare landside terminal and waterside multi-buoy mooring connected via a three kilometer subsea and over-land pipeline. Phase 1 of the terminal entails five tanks with 5,500 tonnes of storage, allowing for a monthly capacity of 17,500 tonnes

of LPG. Construction of Phase 1 was completed on schedule and a trial shipment was handled at the terminal at the end of May 2017.

Phases 2 and 3 of the project will see modular expansion that will enable the terminal to meet regional LPG supply demands for the next 27 years.

More than 1 000 indirect jobs have been created to date through the project including 31 permanent positions.

Energy is recognised as one of the key commodities in driving economic growth in South Africa.

The Sunrise Energy Terminal is poised to become the country’s largest such facility for handling both imports and exports of LPG.

Earlier this month TNPA’s 24-year concession awarded to black-empowered Burgan Cape Terminals saw a new independent fuel storage, distribution and loading facility become fully operational at the Port of Cape Town.

Port of Saldanha’s new LPG terminal launched

30

Ports & Shipping

export & import SA // SEPTEMBER 2017

Africa’s transport leaders drive free trade agenda

National development across Africa continues to support the commitment undertaken by the 54 members of the

African Union in Addis Ababa, Ethiopia in November 2016 to create a continent-wide free trade area.

At the helm of this initiative is Africa’s transport sector, taking continuous strides to unlock cross-border opportunities for intra-African trade and development. There is a much to be gained from a free trade area for Africa, as intra-African trade is the lowest of any region in the world at a mere 10%. A properly executed free trade area couldchangethestatusquoandtransform Africa.

As projects and initiatives in support of transport infrastructure development to boost intra-African trade continue to crop up across the continent, Africa’s transport leaders take action to demonstrate their vision of modernised transport and free trade for the region.

The Federal Republic of Nigeria has most recently reaffirmed its commitment to intra-African trade and development with the confirmation of The Honourable Chibuike Rotimi Amaechi, Nigeria’s Minister of Transport, to join the strategic round table discussions that will be held during the 6th annual African Ports Evolution Forum in Durban, South Africa this October.

The Honourable Amaechi’s presence in Durban this October alongside Kenya’s Principal Secretary of Maritime and Shipping, Nancy Karigithu and South Africa’s Minister of Transport, The Honourable Joe Maswanganyi will catalyse the ensuing strategic pan-African discussions for cathartic expansion and modernisation of ports, corridors and multi-modal connectivity. The African Ports Evolution Forum, now in its 6th year, is an annual initiative

created in response to Africa’s transport infrastructure gap.

The initiative unites ports authorities, Ministries of Transport, terminal operators and rail operators to support the scale of development currently underway across the continent.

Not only will Ministries of Transport from Nigeria to Kenya to South Africa be in attendance but also myriad ports authorities from Namport to Djibouti Ports and Free Zone Authority will be there to boost intra-African collaboration and prepare for post-neo-panamaxshippingrequirementsasthe4th industrial revolution sweeps the globe and Africa’s profile as a global trade partner gains momentum.

African Ports Evolution is strategically located with the 2nd annual African Rail Evolution Forum and Trade and Investment KwaZulu-Natal’s Export Week initiative to provide comprehensive access to strategic

development for both coastal and hinterland trade.Supported by the Ports Management Association of Eastern and Southern Africa (PMAESA) and hosted by eThekwini Municipality, the forum garners support from more than 100 sponsors and exhibitors and 80 media and association partners to form one of Africa’s leading transport initiatives.

Port and corridor expansion is not only creating new business opportunities for port city development across the sub-Saharan region but also opening up new access to hinterland areas and strategic trade corridors.

“African Ports Evolution Forum unpacks best practices for sustainable port development and expansion with emphasis on the latest technologies available to drive sustainable construction, interoperability of systems, port efficiency and optimisation,” says Carly Pols, International Business Director at Hypenica.

Ports & Shipping

31 export & import SA // SEPTEMBER 2017

32 export & import SA // SEPTEMBER 2017

The erection of the first two of 23 straddle carriers commenced recently at the Transnet Port Terminals (TPT) Durban Container

Terminal (DCT) Pier 2.