explosion of new mortgage regulation - reed smith

TRANSCRIPT

EXPLOSION OF NEW MORTGAGE REGULATION

Servicing Standards Rules

Mortgage Regulation Teleseminar Series

February 7, 2013

FINANCIAL SERVICES REGULATORY GROUP

Leonard A. Bernstein · [email protected]

Robert M. Jaworski · [email protected]

Travis P. Nelson · [email protected]

James C. Martin · [email protected]

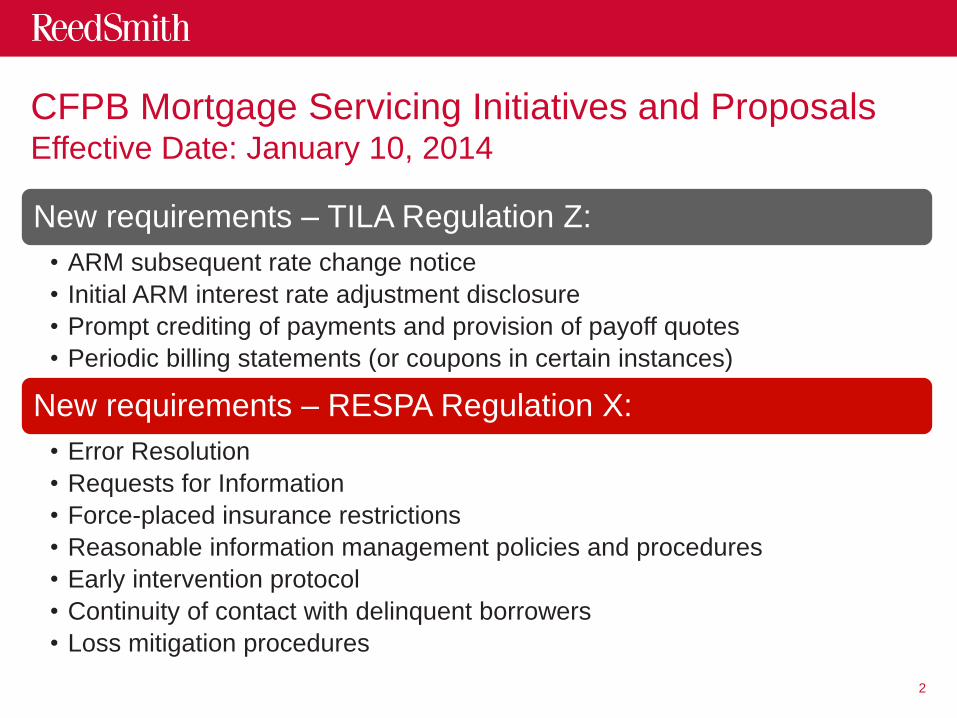

CFPB Mortgage Servicing Initiatives and Proposals Effective Date: January 10, 2014

New requirements – TILA Regulation Z:

• ARM subsequent rate change notice

• Initial ARM interest rate adjustment disclosure

• Prompt crediting of payments and provision of payoff quotes

• Periodic billing statements (or coupons in certain instances)

New requirements – RESPA Regulation X:

• Error Resolution

• Requests for Information

• Force-placed insurance restrictions

• Reasonable information management policies and procedures

• Early intervention protocol

• Continuity of contact with delinquent borrowers

• Loss mitigation procedures

2

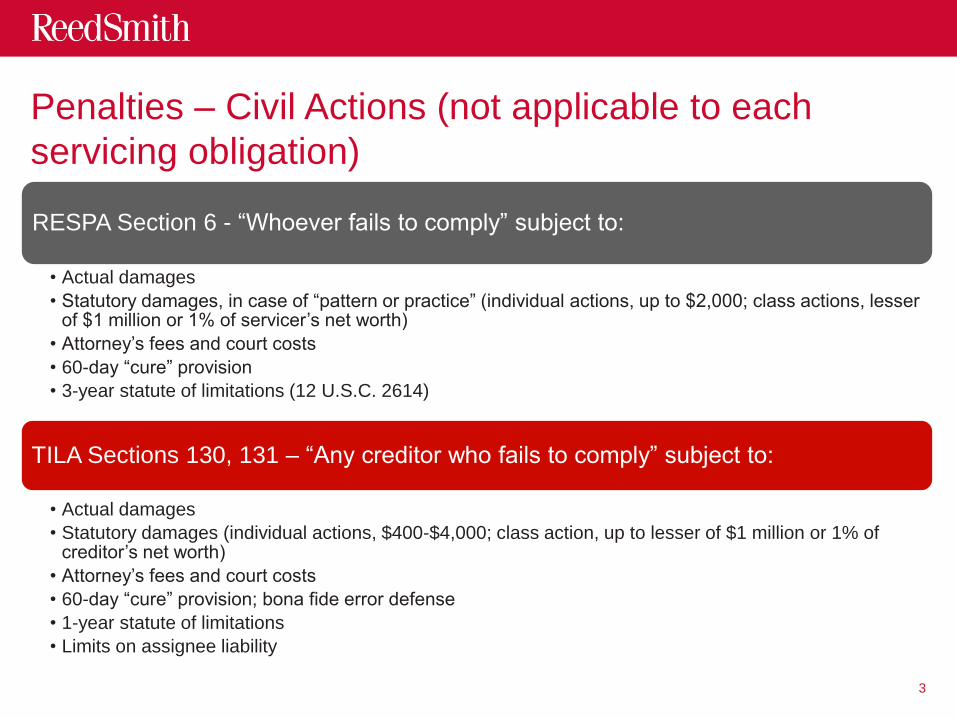

Penalties – Civil Actions (not applicable to each

servicing obligation)

RESPA Section 6 - “Whoever fails to comply” subject to:

• Actual damages

• Statutory damages, in case of “pattern or practice” (individual actions, up to $2,000; class actions, lesser of $1 million or 1% of servicer’s net worth)

• Attorney’s fees and court costs

• 60-day “cure” provision

• 3-year statute of limitations (12 U.S.C. 2614)

TILA Sections 130, 131 – “Any creditor who fails to comply” subject to:

• Actual damages

• Statutory damages (individual actions, $400-$4,000; class action, up to lesser of $1 million or 1% of creditor’s net worth)

• Attorney’s fees and court costs

• 60-day “cure” provision; bona fide error defense

• 1-year statute of limitations

• Limits on assignee liability

3

Penalties – Administrative Actions

Who has jurisdiction?

• Prudential bank regulators: servicing activities performed by depository institutions with $10 billion or less in assets

• CFPB: servicing activities performed by depository institutions with over $10 billion in assets, and non-bank covered entities, i.e., non-bank mortgage servicers

• Agencies can undertake lengthy investigations

• Role of state attorneys general

Available relief

• Permanent and temporary cease and desist orders

• Agencies can seek to require servicers to take a variety of remedial actions

• Fines

• Prohibition from working in the banking industry (for prudential regulators)

4

ARM Subsequent Rate Change Notice: TILA (§1026.20(c))

• Scope: Applies to creditor, assignee or servicer; does not apply to loan modification adjustment (initial); no small servicer exemption

• Scope: Principal dwelling secured loans; no preferred rate or step rate loans

• Scope: Does not apply to loans ≤ 1 year; nor to first adjustment w/in 210 days after consummation

• Eliminates existing annual rate adjustment notice (for when no payment changes within a year)

• Notice triggered when rate adjustment causes payment adjustment (and upon certain conversions)

• Civil Liability: Private right of action for actual damages; ability to collect statutory damages uncertain

5

ARM Subsequent Rate (Continued)

Change Notice: TILA (§1026.20(c))

• Timing: Deliver at least 60 but no more than

120 days before payment at a new level is due;

formerly 25 days to 120 days: increase of minimum

advance notice

• Timing: For originations prior to 1/10/15, if “look back” less then 45, 25 to

120 day delivery period permitted. Also for 60 day adjustments or more

frequent use 25/120

• Content: Table of current and new rates and payments (allocation only if

interest-only/neg am): same order and format as Appendix H-4(D)-1 and

2.

• Volume: 10% of 2012 home purchase loans are ARM’s

• Delivery: Put in the mail or otherwise deliver

6

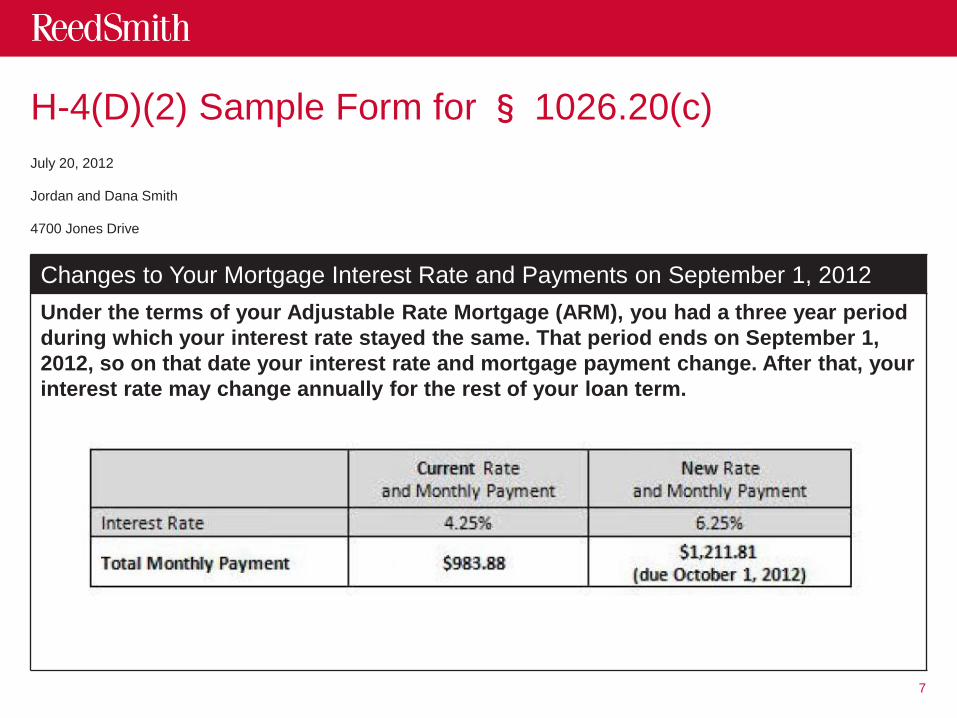

H-4(D)(2) Sample Form for § 1026.20(c)

July 20, 2012

Jordan and Dana Smith

4700 Jones Drive

Memphis, TN 38109

Springside Mortgage

1234 Main St

Memphis, TN 31801

7

Changes to Your Mortgage Interest Rate and Payments on September 1, 2012

Under the terms of your Adjustable Rate Mortgage (ARM), you had a three year period

during which your interest rate stayed the same. That period ends on September 1,

2012, so on that date your interest rate and mortgage payment change. After that, your

interest rate may change annually for the rest of your loan term.

H-4(D)(2) Sample Form for § 1026.20(c) (Continued)

8

Changes to Your Mortgage Interest Rate and Payments on September 1, 2012

Interest Rate: We calculated your interest rate by taking a published “index rate” and adding a certain number of

percentage points, called the “margin.” Under your loan agreement, your index rate is the 1-year LIBOR and your margin is

2.25%. The LIBOR index is published daily in the Wall Street Journal.

Rate Limits: Your rate cannot go higher than 11.625% over the life of the loan. Your rate can change each year by no

more than 2.00%.

New lnterest Rate and Monthly Payment: The table above shows your new interest rate and new monthly

payment. Your new payment is based on the LIBOR index, your margin, your loan balance of $189,440, and your remaining

loan term of 324 months.

Prepayment Penalty: Keep in mind that if you pay off your loan, refinance or sell your home before September 1, 2012,

you could be charged a penalty. Contact Springside Mortgage at (800) 765-4321 for more information, such as the maximum

amount of the penalty you could be charged.

Initial Rate Adjustment Notice TILA (§ 1026.20(d))

• Scope: Applies to creditor, assignee or servicer; does not apply to loan modification adjustment (initial); no small servicer exemption

• Scope: Principal dwelling secured ARM’s; reverse mortgages covered; purchase and home equity;

• Scope: Not applicable to step rate, preferred rate, shared appreciation; if ARM closes before effective date but first adjustment after, must comply

• Exempt: All ARM’s ≤ 1 year; HELOC’s

• Civil Liability: Private right of action for actual damages; ability to collect statutory damages uncertain

• Format: In writing, separate and distinct: don’t need separate envelope; can’t integrate in periodic statement

• Timing: At least 210 but not more than 240 days before first payment at new level due; if first new payment due within 210 days, disclose at consummation

9

Initial Rate Adjustment Notice (Continued)

TILA (§ 1026.20(d))

• Estimate: If new payment or rate unknown, use estimate based on index

within 15 business days of disclosure

• Content:

• Table with current and new rate and payments (allocation only if

interest-only/neg am)

• Prepayment Fee – circumstances, instructions to contact

• Index and margin; loan balance

• List of alternatives – selling, refinance, modification, forbearance

• State housing authority and list of HUD counselors

• Appendix H-4D(3) (model) & (4) (sample)

10

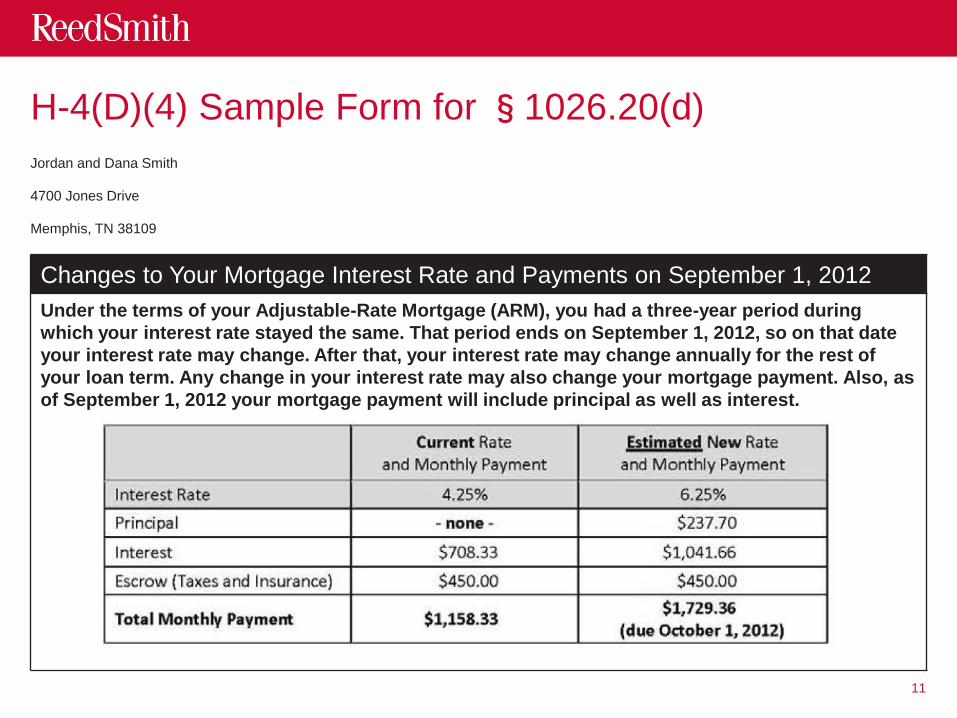

H-4(D)(4) Sample Form for §1026.20(d)

Jordan and Dana Smith

4700 Jones Drive

Memphis, TN 38109

Springside Mortgage

1234 Main St

Memphis, TN 31801

11

Changes to Your Mortgage Interest Rate and Payments on September 1, 2012

Under the terms of your Adjustable-Rate Mortgage (ARM), you had a three-year period during

which your interest rate stayed the same. That period ends on September 1, 2012, so on that date

your interest rate may change. After that, your interest rate may change annually for the rest of

your loan term. Any change in your interest rate may also change your mortgage payment. Also, as

of September 1, 2012 your mortgage payment will include principal as well as interest.

H-4(D)(4) Sample Form for § 1026.20(d) (Continued)

12

Changes to Your Mortgage Interest Rate and Payments on September 1, 2012

Interest Rate: We calculated your interest rate by taking a published “index rate” and adding a certain number

of percentage points, called the “margin.” Under your loan agreement, your index rate is the 1-year LIBOR and

your margin is 2.25%. The LIBOR index is published daily in the Wall Street Journal.

[Rate Limit[s]: Your rate cannot go higher than 11.625% over the life of the loan. Your rate can change each

year by no more than 2.00%. We did not include an additional 1.00% interest rate increase to your new rate

because a rate limit applied. This additional increase may be applied to your interest rate when it adjusts again on

September 1, 2013.

New lnterest Rate and Monthly Payment: The table above shows our estimate of your new interest

rate and new monthly payment. These amounts are based on the LIBOR index as of now, your margin, your loan

balance of $200,000, and your remaining loan term of 324 months. However, if the LIBOR index has changed

when we calculate the exact amount of your new interest rate and payment, your new interest rate and

payment may be different from the estimate above. We will send you another notice with the exact amount

of your new interest rate and payment 2 to 4 months before the first new payment is due, if your new

payment will be different from your current payment.

H-4(D)(4) Sample Form for § 1026.20(d) (Continued)

13

Changes to Your Mortgage Interest Rate and Payments on September 1, 2012

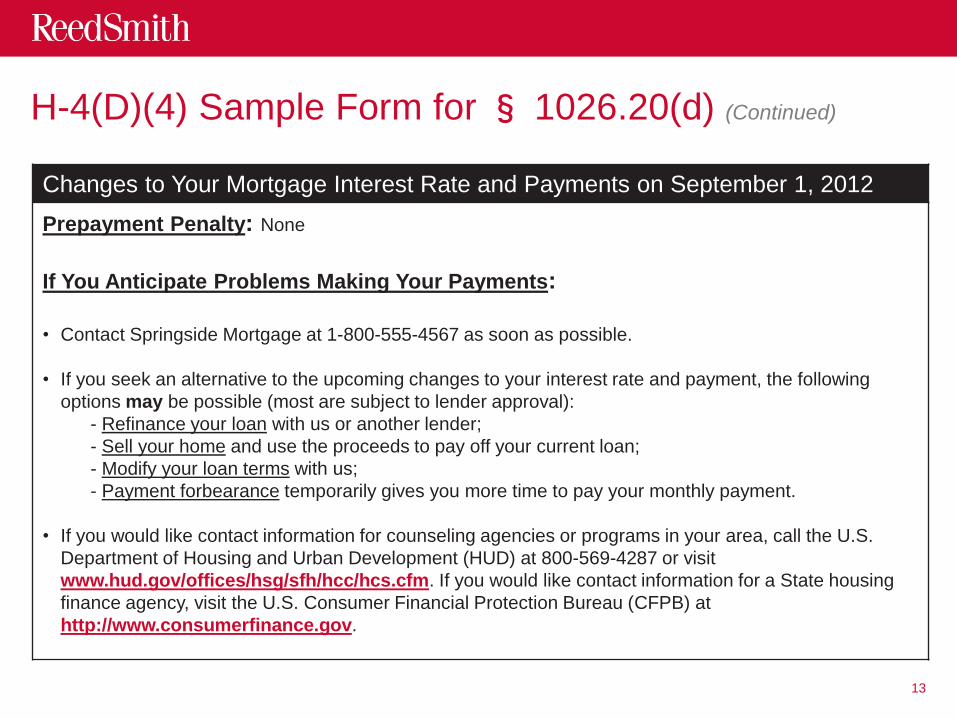

Prepayment Penalty: None

If You Anticipate Problems Making Your Payments:

• Contact Springside Mortgage at 1-800-555-4567 as soon as possible.

• If you seek an alternative to the upcoming changes to your interest rate and payment, the following

options may be possible (most are subject to lender approval):

- Refinance your loan with us or another lender;

- Sell your home and use the proceeds to pay off your current loan;

- Modify your loan terms with us;

- Payment forbearance temporarily gives you more time to pay your monthly payment.

• If you would like contact information for counseling agencies or programs in your area, call the U.S.

Department of Housing and Urban Development (HUD) at 800-569-4287 or visit

www.hud.gov/offices/hsg/sfh/hcc/hcs.cfm. If you would like contact information for a State housing

finance agency, visit the U.S. Consumer Financial Protection Bureau (CFPB) at

http://www.consumerfinance.gov.

Prompt Crediting of Payments TILA (§ 1026.36(c))

• Scope: Principal dwelling loans; no small servicer exemption

• Civil Liability: Private right of action for actual damages; ability to collect statutory damages uncertain

• Credit date of receipt for “periodic payments”.

• Partial payments:

• Disclose amount in suspense account on periodic statement

• Promptly apply to overdue payments when periodic payment has accumulated.

• Non conforming payments – if specify in writing payment requirements, but accept nonconforming payment, credit 5 days after receipt.

• No pyramiding of late charges

14

Payoff Statement Request TILA (§ 1026.36(c))

• Scope: Dwelling secured; no small servicer exemption

• Civil Liability: Private right of action for actual damages; ability to collect statutory damages uncertain

• Within “reasonable time,” but not greater than 7 business days, servicer must respond to written request.

• Request may be made by a representative including attorney or creditor.

• Can set up reasonable requirements like mailing address, e-mail – if violate, longer time OK.

• Must be accurate when issued.

15

Periodic Statements TILA (§ 1026.41)

• TILA - Section 128(f)

• Scope: Closed end dwelling-secured consumer transaction, includes 2nd homes

• Scope: Creditor, assignee, or servicer (unless sold)

• Civil Liability: Private right of action for actual damages; ability to collect statutory damages uncertain

• Exempt: Small Servicers: (1) 5000 or fewer loans serviced; and (2) servicer or affiliate is creditor or assignee

• Timing: “Reasonably prompt” time (w/in 4 days) after payment due date or end of “courtesy period”

• Format: Writing, clear and conspicuous, form can keep; electronic ok

• “Close Proximity”: Boxed off or spaced apart

16

Periodic Statements (Continued)

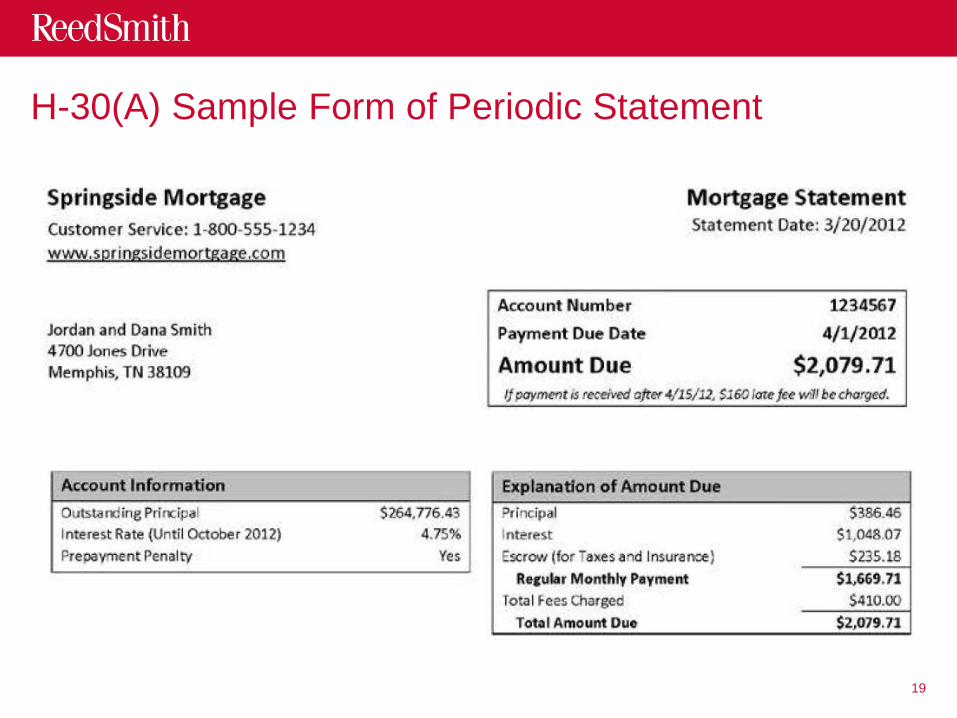

• Sample and Contents: App. H-30 “proper use” deemed “compliance”

• Top Box: Amount due (prominent); due date; late fee and date imposed

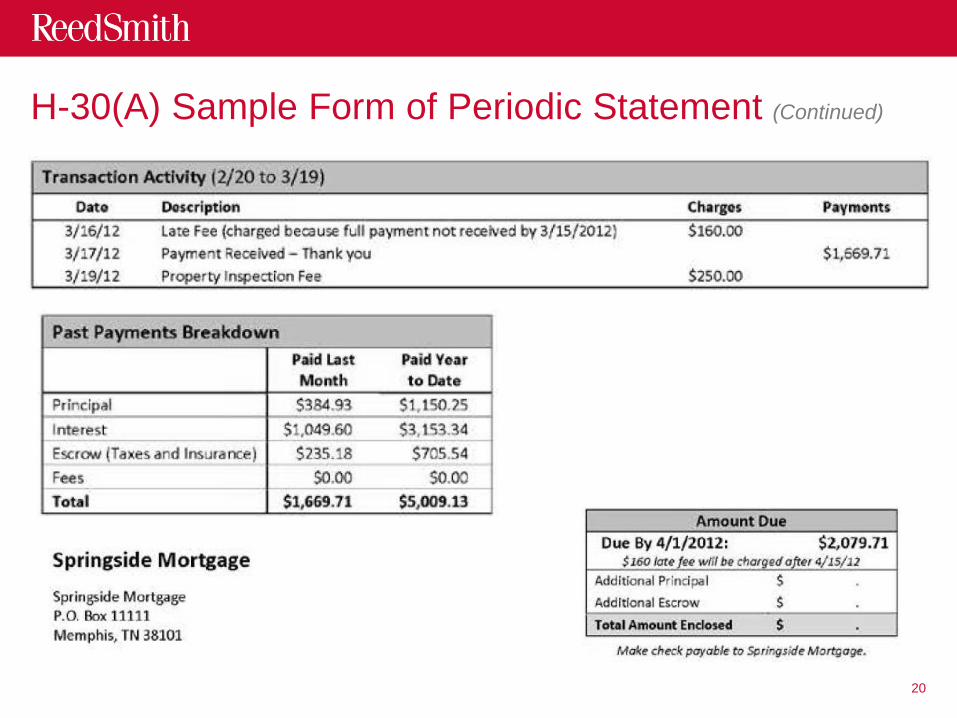

• First Page: Monthly payment amount & breakdown, sum of fees, past due payment

• First Page: Past payment breakdown: since last statement and YTD

• Transaction activity since last statement

• Partial payment: What is needed to apply funds (first or separate page)

• First Page: Contact information: Toll free phone # and if applicable, email

• Account Information: Balance, rate, change date, prepayment fee, counselor website

• Delinquency Info: If 45 days, date of delinquency, statement re risks, 6 mo. account history, loan modification options, foreclosure filing, total payment due, housing counseling (first or separate page)

17

Periodic Statements (Continued)

• Coupon Book Exception: Periodic billing statement does not apply to fixed

rate loan with coupon book, provided:

• “Top box” info printed on each coupon (due date, late fee, amount due

(bold))

• Elsewhere in the coupon book include: balance (at beginning of

coupon book period), rate, change date, prepayment fee, counseling

info, contact info

• Other periodic statement info made available upon request by phone,

writing or electronically

• Delinquency info: Given in writing w/in 45 days

18

H-30(A) Sample Form of Periodic Statement

19

H-30(A) Sample Form of Periodic Statement (Continued)

20

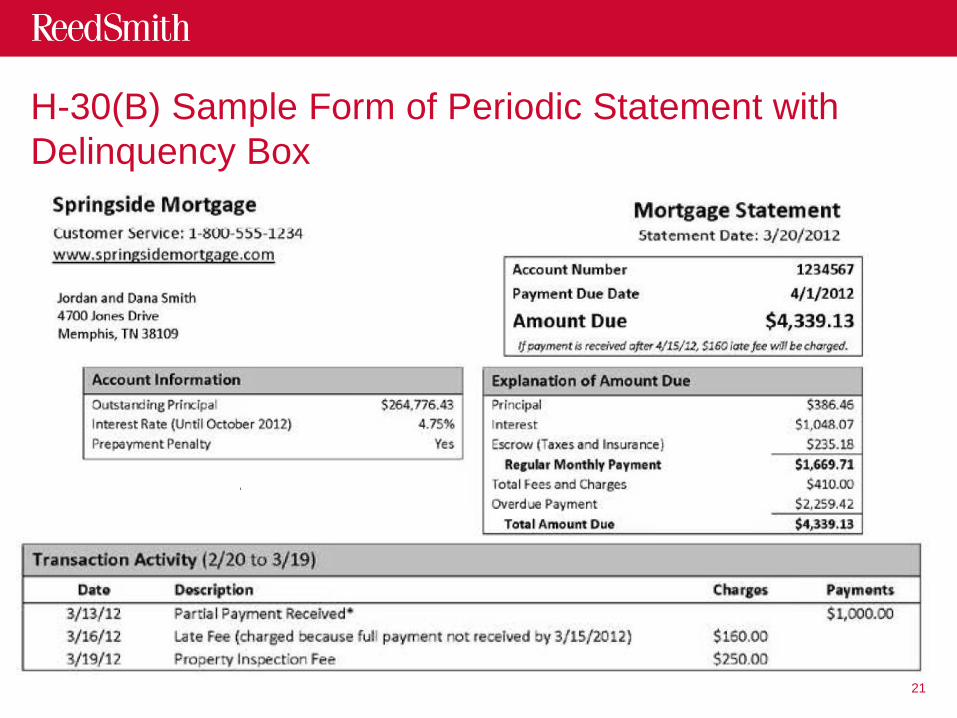

H-30(B) Sample Form of Periodic Statement with

Delinquency Box

21

H-30(B) Sample Form of Periodic Statement with

Delinquency Box (Continued)

22

Error Resolution Procedures RESPA (§1024.35)

• Scope: Small servicers (≤ 5000 loans) covered

• Civil Liability: RESPA Section 6 liability applies

• Notice of Error: Written notice from borrower, including:

• Name Account info Nature of error

• Qualified Written Request: Considered “notice of error”

• “Error” – 11 categories:

• payments – failure to accept, apply or credit

• escrow – failure to pay taxes/premiums timely

• fees – impose w/o basis

• servicing – failure to provide payoff or loss mit options; failure to transfer servicing info; foreclosure during loss mit; other

• Can establish contact info for Notice of Error by providing written notice; also keep listed on website

23

Error Resolution Procedures (Continued)

RESPA

• Written acknowledgment of receipt – 5 days

(not Sat or Sun)

• 30 days to correct or investigate and provide written response; if no error

found, give statement of reasons and phone # to request docs

• If failure to give accurate payoff: 7 days not 30

• If foreclosure filing error: earlier of foreclosure or 30 days

• Extend response 15 days if notify borrower and give reasons

• Except for payoff or foreclosure errors

• Must provide copies of documentation relied on within 15 days of

borrowers request, except “confidential proprietary or privileged info”

• Early correction alternative – correct w/in 5 days and notify

24

Error Resolution Procedures (Continued)

RESPA

• No compliance necessary if:

• Duplicative notice of error – unless new and material info

• Notice is “overbroad” or “unduly burdensome”

• Untimely – 1 year after transfer or payoff

• Notify borrower of such determination in writing no later than 5 days

• No adverse credit report furnishing for 60 days

• No impact on exercise of loan remedies

• Can’t charge fee for responding

25

Requests for Information: RESPA (§1024.36)

• Scope: Small servicers (≤ 5000 loans) covered

• Civil Liability: RESPA Section 6 liability applies

• Request for Info: Written notice from borrower, including:

• Name Account info Info requested

• Qualified Written Request: Considered “request for information”

• Can establish contact info for Request for Information by providing written notice; also keep listed on website; if provided, same address for error resolution info

• Written acknowledgment of receipt – 5 days (not Sat or Sun)

• 30 days to provide requested info and phone # for further help, or conduct reasonable search and give written notice that info not available and phone # for further help

• 10 days after request for identity of owner or assignee

26

Requests for Information: (Continued)

RESPA (§1024.36)

• Early response alternative – give info w/in 5 days

and notify

• No compliance if servicer “reasonably determines”

• Duplicative request for info

• Confidential/proprietary/corporate info cannot be released

• Irrelevant – not directly related to borrower’s account

• Notice is “overbroad” or “unduly burdensome”

• Untimely – 1 year after transfer or payoff

• Notify borrower of such determination in writing no later than 5 days

• No impact on exercise of loan remedies or furnishing adverse info

27

Force–Placed Insurance: RESPA (§1024.37)

• Scope: Small servicers (≤ 5000 loans) COVERED

• Civil Liability: RESPA Section 6 liability applies

• Definition: Hazard insurance obtained by servicer on behalf of owner/assignee

• Does not include flood insurance

• Does not include servicer’s renewal of borrower’s existing policy

• Rule: No charge for force-placed insurance absent “reasonable basis to believe” borrower failed to maintain required coverage and compliance with notice requirements

• First Notice: At least 45 days before fee assessed (Form MS-3A)

• Content: List of required items (nothing else) - including

• request for evidence of coverage

• how to provide evidence of coverage

• “may cost significantly more”/”may not provide as much coverage”

28

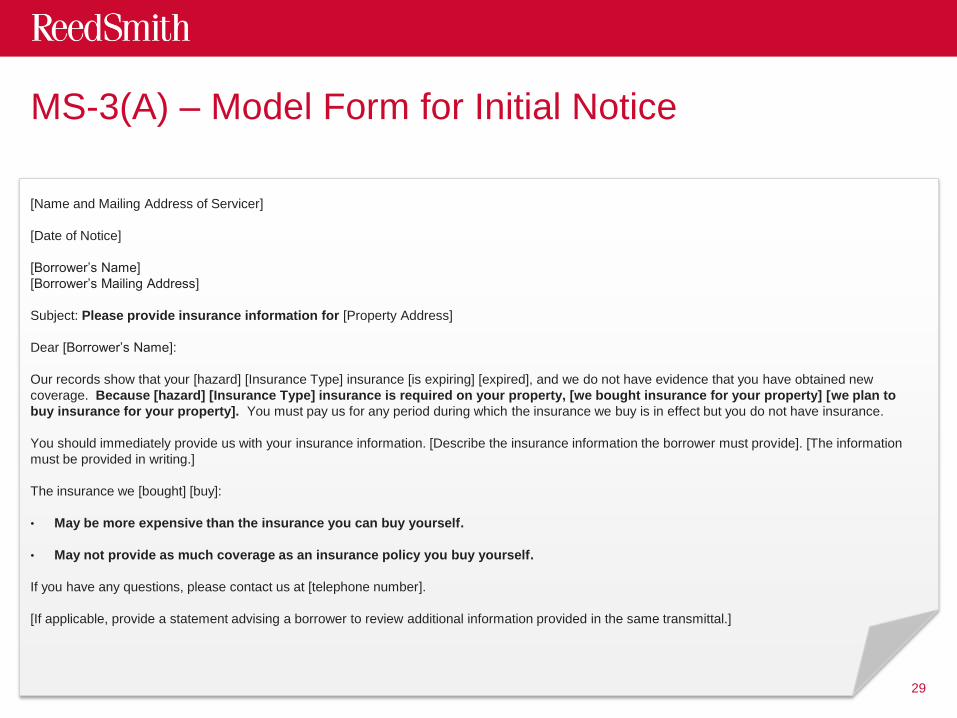

MS-3(A) – Model Form for Initial Notice

[Name and Mailing Address of Servicer]

[Date of Notice]

[Borrower’s Name]

[Borrower’s Mailing Address]

Subject: Please provide insurance information for [Property Address]

Dear [Borrower’s Name]:

Our records show that your [hazard] [Insurance Type] insurance [is expiring] [expired], and we do not have evidence that you have obtained new

coverage. Because [hazard] [Insurance Type] insurance is required on your property, [we bought insurance for your property] [we plan to

buy insurance for your property]. You must pay us for any period during which the insurance we buy is in effect but you do not have insurance.

You should immediately provide us with your insurance information. [Describe the insurance information the borrower must provide]. [The information

must be provided in writing.]

The insurance we [bought] [buy]:

• May be more expensive than the insurance you can buy yourself.

• May not provide as much coverage as an insurance policy you buy yourself.

If you have any questions, please contact us at [telephone number].

[If applicable, provide a statement advising a borrower to review additional information provided in the same transmittal.]

29

Force–Placed Insurance (Continued)

• Reminder (“Second and Final”) Notice: At least 30 days after 1st notice and 15 days before fee assessed; different content if servicer receives no insurance information (MS-3B) v. no evidence of continuous coverage (MS-3C)

• Must include cost or reasonable estimate

• Notice before renewal of force-placed policy – at least 45 days before fee assessed; before each anniversary but only once/year (MS-3D)

• Receipt of evidence of overlapping coverage – servicer must cancel force-placed policy and refund premium for overlap within 15 days

• Force-placed charges – must be “bona fide and reasonable” (except for charges subject to state insurance regulation)

• Flood insurance notices – may be sent with hazard notices (but on separate piece of paper)

30

MS-3(B) – Model Form for Reminder Notice/No Info

Received

[Name and Mailing Address of Servicer]

[Date of Notice]

[Borrower’s Name] [Borrower’s Mailing Address]

Subject: Second and final notice – please provide insurance information for [Property Address]

Dear [Borrower’s Name]:

This is your second and final notice that our records show that your [hazard] [Insurance Type] insurance [is expiring] [expired], and we do not have evidence that you have obtained new coverage. Because [hazard] [Insurance Type] insurance is required on your property, [we bought insurance for your property] [we plan to buy insurance for your property]. You must pay us for any period during which the insurance we buy is in effect but you do not have insurance.

You should immediately provide us with your insurance information. [Describe the insurance information the borrower must provide]. [The information must be provided in writing.]

The insurance we [bought] [buy]:

• [Costs $[premium charge]] [Will cost an estimated $[premium charge]] annually, which may be more expensive than insurance you can buy yourself.

• May not provide as much coverage as an insurance policy you buy yourself.

If you have any questions, please contact us at [telephone number].

[If applicable, provide a statement advising a borrower to review additional information provided in the same transmittal.]

31

MS-3(C) – Model Form for Reminder

Notice/Insufficient Info Received [Name and Mailing Address of Servicer]

[Date of Notice]

[Borrower’s Name]

[Borrower’s Mailing Address]

Subject: Second and final notice – please provide insurance information for [Property Address]

Dear [Borrower’s Name]:

We received the insurance information you provided, but we are unable to verify coverage from [Date Range].

Please provide us with insurance information for [Date Range] immediately.

We will charge you for insurance we [bought] [plan to buy] for [Date Range] unless we can verify that you have insurance coverage for [Date Range].

The insurance we [bought] [buy]:

• Costs $[premium charge]] [Will cost an estimated $[premium charge]] annually, which may be more expensive than insurance you can

buy yourself.

• May not provide as much coverage as an insurance policy you buy yourself.

If you have any questions, please contact us at [telephone number].

[If applicable, provide a statement advising a borrower to review additional information provided in the same transmittal.]

32

MS-3(C) – Model Form for Renewal/Replacement of

Force-Placed Policy [Name and Mailing Address of Servicer]

[Date of Notice]

[Borrower’s Name]

[Borrower’s Mailing Address]

Subject: Please update insurance information for [Property Address]

Dear [Borrower’s Name]:

Because we did not have evidence that you had [hazard] [Insurance Type] insurance on the property listed above, we bought insurance on your property

and added the cost to your mortgage loan account.

The policy that we bought [expired] [is scheduled to expire]. Because [hazard][Insurance Type] insurance] is required on your property, we intend

to maintain insurance on your property by renewing or replacing the insurance we bought.

The insurance we buy:

• [Costs $[premium charge]] [Will cost an estimated $[premium charge]] annually, which may be more expensive than insurance you can

buy yourself.

• May not provide as much coverage as an insurance policy you buy yourself.

If you buy [hazard] [Insurance Type] insurance, you should immediately provide us with your insurance information.

[Describe the insurance information the borrower must provide]. [The information must be provided in writing.]

If you have any questions, please contact us at [telephone number].

[If applicable, provide a statement advising a borrower to review additional information provided in the same transmittal.] 33

Information Management RESPA (§1024.38)

• Scope: Small servicers (≤ 5,000 loans) EXEMPT

• Civil Liability: No private right of action; enforced by CFPB or, for smaller banks/credit unions, OCC/FDIC/FRB/NCUA, as applicable

• Rule: Maintain policies and procedures “reasonably designed to achieve” the following objectives:

• Accessing and providing timely and accurate information, disclosures, documents; investigate and correct errors

• Properly evaluating loss mitigation applications; identify and provide accurate and timely information concerning all available options

• Overseeing service provider compliance; periodic reviews and audits

• In connection with servicing transfers – (old servicer) facilitating complete and timely information transfer; (new servicer) making sure all necessary documents are obtained

• Informing borrowers of error resolution/information request procedures

34

Information Management (Continued)

RESPA (§1024.38)

• Not one-size-fits-all: Appropriate to size, nature and scope of servicer’s

operations

• Record retention – 1 year after payoff or transfer

• Servicing File - maintain “documents and data” so that they can be

compiled into a “servicing file” within 5 days

• schedule of payments and disbursements

• mortgage/deed of trust

• notes of communications with borrowers

• data field report

• copies of all information and documents provided by borrower

35

Early Intervention RESPA (§1024.39)

• Scope: Principal residence only; small servicer (≤ 5,000) EXEMPT

• Civil Liability: RESPA Section 6 liability applies

• Live Contact – If payment is “late,” servicer must make “good faith effort”

to establish “live contact” not later than 36th day of delinquency

• Notify about loss mit options “if appropriate” and “promptly” after

establishing live contact

• “Delinquency” – Payment due date; not end of late charge grace

period

• “Live Contact” – Telephone or in person, not voicemail – may call,

email or write to arrange

36

Early Intervention (Continued)

• Written Notice:

• Not later than 45th day of borrower’s deliquency; not more than once in

180 day period

• Contents – optional model clauses (MS – 4(A), 4(B), 4(C))

• encourage borrower to contact

• mailing address and phone number

• loss mit options; can be generic list (examples if applicable –

forbearance, mods, short sale)

• Application instructions: how to obtain info

• Website for housing counselors - HUD 800 #

37

Appendix MS-4 - Model Clauses For The Written

Early Intervention Notice • Appendix MS-4 is added to part 1024 to read as follows:

Appendix MS-4 - Model Clauses For The Written Early Intervention Notice

MS-4(A)—Statement Encouraging the Borrower to Contact the Servicer and Additional Information About Loss Mitigation Options (§ 1024.39(b)(2)(i), (ii) and (iv))

Call us today to learn more about your options and instructions for how to apply. [The longer you wait, or the further you fall behind on your payments, the harder it will be to find a solution.]

[Servicer Name]

[Servicer Address]

[Servicer Telephone Number]

[For more information, visit [Servicer Website] [and][or] [Email Address]].

38

Appendix MS-4 - Model Clauses For The Written

Early Intervention Notice (Continued)

MS-4(B)—Available Loss Mitigation Options (§ 1024.39(b)(2)(iii))

[If you need help, the following options may be possible (most are subject to lender approval):]

• [Refinance your loan with us or another lender;]

• [Modify your loan terms with us;]

• [Payment forbearance temporarily gives you more time to pay your monthly payment;]

[or]

• [If you are not able to continue paying your mortgage, your best option may be to find more affordable housing. As an alternative to foreclosure, you may be able to sell your home and use the proceeds to pay off your current loan.]

MS-4(C)—Housing Counselors (§ 1024.39(b)(2)(v))

For help exploring your options, the Federal government provides contact information for housing counselors, which you can access by contacting [the Consumer Financial Protection Bureau at [Bureau Housing Counselor List Website]] [the Department of Housing and Urban Development at [HUD Housing Counselor List Website]] or by calling [HUD Housing Counselor List Telephone Number].

39

Continuity of Contact RESPA (§1024.40)

• Scope: Principal residence only; small servicer (≤ 5,000) EXEMPT

• Civil Liability: No private right of action; enforced by CFPB or, for smaller

banks/credit unions, OCC/FDIC/FRB/NCUA, as applicable

• Assign Personnel: By the time of early intervention notice but not later

than 45th day of delinquency; use single person or team

• Ensure access to assigned personnel by phone to explain loss mit

options; must respond in “timely manner”

• Personnel remains available to borrower until borrower makes 2

consecutive timely payments

40

Continuity of Contact (Continued)

• Policies & Procedures: Assigned personnel to provide:

• info about loss mit options, applications, appeal

• access to payment history, borrower’s loss mit materials

• provide notice of error and info request contact info

• circumstances in which servicer may make “referral to foreclosure”

• loss mitigation deadlines

• Delinquent: Not considered upon refinance, payoff, title transferred (deed-

in-lieu), short sale

• Borrower’s agent: Can talk with a representative and have procedures to

verify

41

Loss Mitigation Procedures RESPA (§1024.41)

• Scope – covers servicers that make loss mit available; Small servicer (≤ 5000) EXEMPT except for 2 prohibitions below; principal residence only

• Civil Liability: RESPA Section 6 liability applies

• Loss Mit Application:

• Exercise “reasonable diligence” to complete a loss mit application

• If 45 days or more before foreclosure sale, servicer receives a loss mit app, must promptly review to see if “complete,” and:

• Acknowledge receipt w/in 5 days and state if complete or not

• If incomplete, name additional documents needed and deadline for submission, which is earliest of:

• Of date submitted info becomes “stale,”

• 120th day of delinquency,

• 90 days before foreclosure sale, or

• 38 days before foreclosure sale.

42

Loss Mitigation Procedures (Continued)

• Complete Loss Mit Application: If received > 37 days before foreclosure sale, w/in 30 days of receiving complete loss mit app, must: (1) Evaluate; (2) Provide notice of determination - offer loss mit options or not.

• Denial: Notice must state specific reasons, rights to appeal, deadline.

• Incomplete Loss Mit Application: If “reasonable diligence” in obtaining information to complete, but still incomplete for “significant period of time,” servicer may in its discretion evaluate and offer a loss mit option.

• Borrower response

• Servicer can set deadline for acceptance no earlier than 14 days after notice if complete application received 90 days or more before foreclosure sale

• Servicer can set such deadline no earlier than 7 days if loss mit app received < 90 but > 37 days before sale

• Non acceptance by deadline is deemed rejection

43

Loss Mitigation Procedures: (Continued)

No Dual Tracking

• FIRST FORECLOSURE NOTICE FILING: NOT UNTIL 120 DAYS DELINQUENT

• FIRST FORECLOSURE NOTICE FILING: If borrower provides complete loss mit application during “pre-foreclosure 120”, servicer shall not make first filing unless:

• Denial notice is sent and no appeal

• Servicer denies appeal

• Borrower rejects loss mit, or

• Borrower fails to perform.

• NO MOTION FOR FORECLOSURE SALE OR JUDGMENT: If complete loss mit application submitted after first foreclosure notice, but > 37 days before sale, servicer shall not move for judgment/sale unless:

• Denial notice sent and no appeal or appeal denied,

• Borrower rejects loss mit, or

• Borrower fails to perform loss mit.

44

Loss Mitigation Procedures (Continued)

• Appeals Process: If receive complete loss mit app 90 days before sale or during the 120 day

delinquency period:

• Servicer that denies app “shall” permit appeal

• Must provide opportunity to appeal for at least 14 days after denial

• Independent evaluation – different personnel

• W/in 30 days, provide notice of decision, and if servicer offers loss mit, may require

answer no earlier than 14 days

• No further appeal permitted; no duplicate appeals

• SMALL SERVICERS: Only 2 loss mitigation prohibitions apply (No dual tracking):

• FIRST FORECLOSURE NOTICE FILING – NOT UNTIL 120 DAYS DELINQUENT

• If borrower performing under a loss mitigation agreement:

• No first foreclosure notice filing

• No Foreclosure Sale: Servicer shall not move for judgment/sale

45

Noel Canning vs. NLRB Ruling: CFPB Recess Appointment

• Three judge panel of U.S. Court of Appeals for the

D.C. Circuit found that the recess appointments of

three NLRB board members were invalid because they did not meet the

requirements of the recess appointments clause in the US constitution.

• Chief Judge David Sentelle wrote "that the President may only make

recess appointments to fill vacancies that arise during the recess.”

• CFPB director Cordray’s recess appointment made concurrently with

NLRB board members so it is vulnerable. White House says “No.”

• Legal resolution likely will make its way to Supreme Court because of

circuit conflicts and ongoing litigation involving NLRB.

46 Sources: DoJ, Lawfulness of Recess Appointments, 6 January 2012, pp1, 5 - The National Law Journal, D.C. Circuit declares NLRB recess

appointments unconstitutional, 25 January 2013

Implications of Ruling on CFPB

• Argument will be made that CFPB's authority and

rulemaking power is nullified and all actions and

rulemaking taken in the past and future are in question.

• Issue could turn on what authority and what acts are under scrutiny.

Some authority relates to transferred powers, some to new powers, some

relates to banks and non-banks, and there is an argument the Bureau

needs a director to act.

• There is litigation now involving constitutionality of Cordray’s appointment.

• Courts deciding Cordray's status might decide not to void final agency

rules because of potential disruption to important sectors of the economy,

such as mortgage lending – “De Facto Officer” theory.

47

Source: Wall Street Journal, Banks Worry CFPB May Be Weakened, 30 January 2013 - American Banker, A Texas community bank is leading

against the Consumer Financial Protection Bureau, 21 June 2012

Implications of Ruling on Supervised Entities

• Large credit card issuers have entered major settlements

• Rulemaking has effected banks and non-banks

What about companies who have been

investigated or resolved issues with

CFPB.

• Argue the CFPB has no authority to act

• Try to use ruling to delay examination or information requests

• Failing that seek a court ruling to stay further action

What about companies under examination or in

enforcement actions.

• Take a wait-and-see attitude

• Monitor trade association and political activities What about companies not under examination.

48

Some Open Issues

What role will the secretary or Treasury play in trying to buttress or defend Bureau action. Will it matter if the

secretary steps in as far as past or future action is

concerned.

Cordray’s future is in doubt by virtue of the ruling.

Cutting a deal has been suggested - giving the CFPB legal certainty

surrounding actions taken to date. Republicans have three items on the table.

Republicans have introduced bill to halt

funding from Fed until an agency director is

confirmed.

Source: American Banker, For CFPB, Parsing Which Rules Stay, and Which May Go, 28 January 2013 49

Upcoming Topics in this Four-Part Teleseminar Series

Loan Officer Compensation Rule –

February 21, 2013, Noon (EST)

Escrow Rule; HOEPA/High-Cost Mortgage Rule; ECOA Appraisal Rule; Appraisals

for High-Risk Mortgage Rule – March 7, 2013,

Noon (EST)

50

To access an audio recording and presentation slides from our previous

teleseminars, please visit the series website:

http://www.reedsmith.com/Financial-Services-Regulatory-Group-

Mortgage-Regulation-Teleseminar-Series/

Leonard A. Bernstein

• Founder and chair of the firm's Financial Services Regulatory Group

• Concentrates his practice in the representation of banks, thrifts, mortgage bankers and finance companies in providing consumer credit compliance advice on federal, Pennsylvania and New Jersey laws and regulations

• The FSR Group addresses credit card, auto finance, deposit, residential mortgage and other retail finance products

• Nationally known for expertise with federal Truth-in-Lending Act, Real Estate Settlement Procedures Act, and similar laws, and works regularly with federal and state financial services regulators

• Defends class actions and individual claims filed against financial services providers

• Elected to the American College of Consumer Financial Services Attorneys

51

215 851 8143

Philadelphia, PA

609 520 6005

Princeton, NJ

Robert M. Jaworski

• Member of the Financial Industry Group and the Financial Services

Regulatory Group

• Focuses on consumer credit compliance and other regulatory

issues of concern to banks, thrifts, mortgage bankers, secondary

mortgage lenders, finance companies and industry-related trade

associations

• A frequent speaker on compliance issues before state and national

groups, Bob has authored numerous articles on the subject

• Formerly Chief Editor of Pratt’s Mortgage Compliance Letter; Co-

Chair of the RESPA/Housing Finance Subcommittee of the ABA

Consumer Financial Services Committee; Chair, New Jersey Bar

Association Banking Law Section; and Member, Governing

Committee of the Conference on Consumer Finance Law

• Developed and taught courses on federal and state laws and

regulations affecting mortgage bankers, brokers, and servicers

52

609 520 6003

Princeton, NJ

Travis P. Nelson

• Member of the Financial Industry Group and the Financial Services

Regulatory Group

• Former Enforcement Counsel with the Office of the Comptroller of the

Currency, U.S. Treasury Department, Washington, D.C.

• Focuses his practice on financial services regulation, enforcement

defense, internal investigations, and litigation matters

• Represents clients before federal law enforcement and regulatory

agencies, including the OCC, the CFPB, and HUD, as well as various

state authorities across the country

• Adjunct faculty teaching Regulation of Financial Institutions at Villanova

University School of Law

• Co-Leader, Reed Smith Financial Institutions Enforcement &

Investigations Task Force

• Editor-in-Chief of the Reed Smith Financial Services blog –

www.financialregulatoryreport.com

• National President, Office of the Comptroller of the Currency Alumni

Association

53

609 524 2038

Princeton, NJ

212 549 0236

New York, NY

James C. Martin

• Partner in the Appellate Group

• Has focused on appellate law for more than 30 years

• Certified as a specialist in the area of Appellate Law by the State

Bar of California Board of Legal Specialization

• Fellow and Vice President of the American Academy of Appellate

Lawyers

• Member and former president of the California Academy of

Appellate Lawyers

• Founding member and former president of the Third Circuit Bar

Association

• Has handled appeals in federal and state courts across the

country and worked and consulted on hundreds of appeals,

including those involving complex litigation, products and

medical devices, financial services, intellectual properly, and

class actions

54

412 288 3546

Pittsburgh, PA

213 457 8002

Los Angeles, CA