explore psab’s exposure draft on asset retirement...

TRANSCRIPT

Explore PSAB’s Exposure Draft

on Asset Retirement Obligations

April 6, 2017

2

Webinar Overview

• Intended outcomes and expected effects

• Exposure Draft proposals

• Implications of withdrawing Section PS

3270

• Boundaries: Asset Retirement Obligations

vs. Contaminated Sites

• Next steps

3

Intended Outcomes

• Faithful representation

• Consistent accounting

• Comprehensive reporting

• Enhanced comparability

4

Expected Effects

• Review agreements, contracts, legislation,

etc.

• Determine whether there are unrecorded

liabilities

• Estimate future cash flows and other

inputs in the measurement of the liability

• Review current accounting for asset

retirement obligations

5

Project Scope

5

A legal obligation associated with the retirement of a

tangible capital asset

Asset retirement

obligation

Scope considerations

• controlled by the public sector

• In productive use, or not longer in

productive use

• Includes leased tangible capital

assets

Which tangible capital assets? Scope includes

• Solid waste landfill closure and post

closure liabilities (PS 3270)

• Asbestos

• Routine replacement

• Contaminated sites (PS 3260)

• Improper use

• Unexpected events

• Alternative use

• Waste and by-products

Scope excludes

6

Project Scope

Limit scope to legal obligations (exclude constructive and equitable obligations)

CONSIDERATIONS:

• Consistency within PSA Handbook

• Professional judgement

• Examples of asset retirement obligations

• Development of useful guidance and its effect

7

Project Scope

• Asset retirement obligations related to

controlled tangible capital assets:

− in productive use

−no longer in productive use New!

• Includes landfill-related asset

retirement obligations (PS 3270) New!

8

Recognition of Liability

8

An asset

retirement

obligation is

recognized

when:

There is a legal obligation to incur retirement costs;

The past transaction giving rise to the liability has

occurred;

It is expected that future economic benefits will be

given up; and

A reasonable estimate of the amount can be made.

9

Recognition of Liability

9

An asset

retirement

obligation is

recognized when:

There is a legal obligation to incur retirement costs;

The past transaction giving rise to the liability has occurred;

It is expected that future economic benefits will be given up;

and

A reasonable estimate of the amount can be made.

A legal obligation can result from:

Agreements or contracts

Legislation of another

government

A government’s own legislation

Promissory estoppel

10

Recognition of Liability

10

A liability can be incurred due to:

The acquisition, construction or development of a tangible capital asset

Normal use of a tangible capital asset

An asset

retirement

obligation is

recognized when:

There is a legal obligation to incur retirement costs;

The past transaction giving rise to the liability has occurred;

It is expected that future economic benefits will be given up;

and

A reasonable estimate of the amount can be made.

11

Recognition of Liability

11

An asset retirement

obligation is

recognized when:

There is a legal obligation to incur retirement costs;

The past transaction giving rise to the liability has occurred;

It is expected that future economic benefits will be given up; and

A reasonable estimate of the amount can be made.

Example

A public sector entity acquires a building that contains asbestos. Regulations

require the entity to handle and dispose of it in a prescribed manner when

the building undergoes renovations or is demolished.

Does a legal obligation exist?

What is the obligating event?

12

Recognition of Liability

12

Example

A public sector entity opens a landfill site. Regulations require that the final

cover and vegetation be put in place irrespective of the landfill site use.

Does a legal obligation exist?

What is the obligating event?

An asset retirement

obligation is

recognized when:

There is a legal obligation to incur retirement costs;

The past transaction giving rise to the liability has occurred;

It is expected that future economic benefits will be given up; and

A reasonable estimate of the amount can be made.

13

Recognition of Liability

13

Example

A public sector entity operates an energy-from-waste facility. As the bricks in

the furnace become contaminated, the entity has a legal obligation to remove

and dispose of them in a prescribed manner.

Does a legal obligation exist?

What is the obligating event?

An asset retirement

obligation is

recognized when:

There is a legal obligation to incur retirement costs;

The past transaction giving rise to the liability has occurred;

It is expected that future economic benefits will be given up; and

A reasonable estimate of the amount can be made.

14

Recognition and Allocation of Asset Retirement Costs

In productive

use

No longer in

productive use

Allocate to expense in a

rational and systematic

manner (component OR

network level)

CAPITALIZE EXPENSE

15

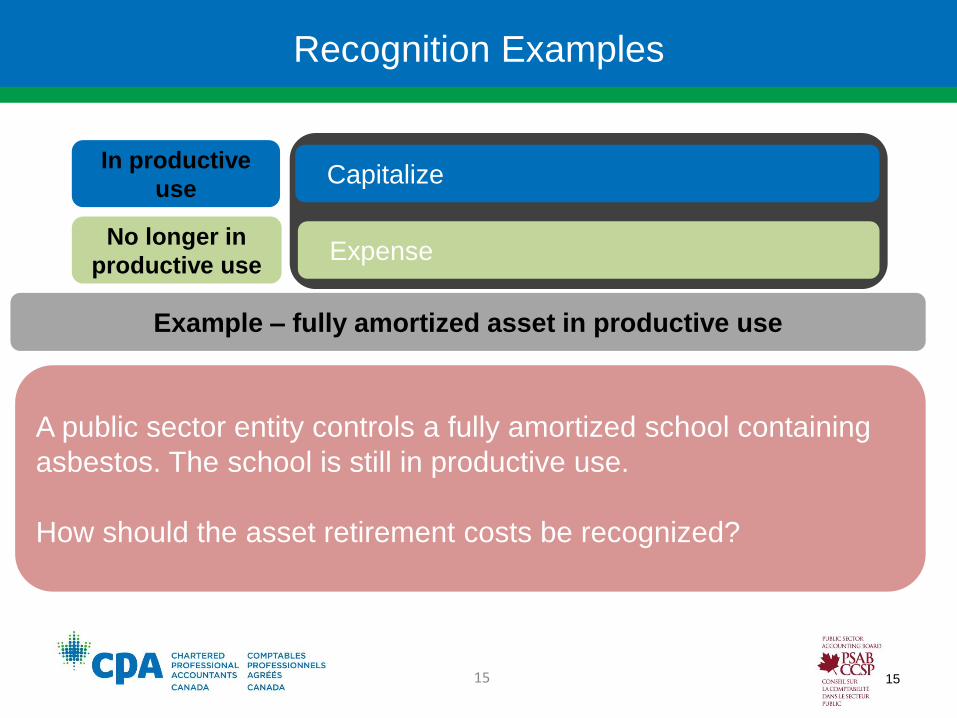

Recognition Examples

15

Capitalize

Expense

In productive

use

No longer in

productive use

Example – fully amortized asset in productive use

A public sector entity controls a fully amortized school containing

asbestos. The school is still in productive use.

How should the asset retirement costs be recognized?

16

Recognition Examples

16

Capitalize

Expense

In productive

use

No longer in

productive use

Example – no longer in productive use

A new legislation was created after the water treatment facility has

been removed from service. The new legislation now requires its

disposal in a prescribed manner and specific post-retirement

activities.

How should the asset retirement costs be recognized?

17

Recognition Examples

17

Capitalize

Expense

In productive

use

No longer in

productive use

Example – allocation of asset retirement costs

A public sector entity operates a transformer station (network) to be

retired after a 50-year period for which its power transformers

(component) need to be retired every 25 years.

Over what period should the asset retirement obligation associated with

the transformers be amortized?

18

Measurement

• Best estimate of the amount required to

retire a tangible capital asset

• A present value technique is often the best

available method

• No prescriptive guidance on appropriate

measurement techniques and discount

rate

19

Subsequent Measurement

Adjust the Tangible

Capital Asset

Expense

• Timing

• Amount

• Discount rate

• Passage of time

(accretion)

• If related asset is

no longer in

productive use

20

Recoveries

• A recovery should not be netted against the liability

• Follow:

– ASSETS, Section PS 3210 -> recognize; or

– CONTINGENT ASSETS, Section PS 3320 -> disclose.

• Consistency with PSA Handbook:

– CONTINGENT LIABILITIES, Section PS 3300 -> may be different

circumstances

– LIABILITY FOR CONTAMINATED SITES, Section PS 3260 -> proposed

consequential amendment

– FINANCIAL INSTRUMENTS, Section PS 3450 -> consistent with

proposals

21

Disclosure

Key elements:

• Description of the liability and associated

tangible capital asset

• Basis for the estimate of the liability

• Reconciliation of the changes in carrying

amount during the period

• How funding and assurance provisions are met

• Estimated recoveries

22

Implications of Withdrawing Section PS 3270

1. Asset retirement obligation standard is

more principles based

2. Transition

3. Different accounting treatment

23

Asset Retirement Obligation vs. Section PS 3270

ARO Section PS 3270

Liability Recognized as incurred

– earlier recognition

Recognized

incrementally as landfill

used – later recognition

Total liability Generally the same

Assets ARO is capitalized N/A

Net debt Both methods impact net debt

ARO = earlier increase in Net Debt

Total expenses Generally the same

Annual expenses Differences in annual expenses are due to

differences in methodology used

23

24

Asset Retirement Obligation vs. Section PS 3260

ARO Contaminated Sites

Cause for the retirement or remediation obligation

• Acquisition, construction,

development, normal use

• Not necessarily associated

with contamination

• Unexpected event,

improper use

• Contamination needs to

exist

Type of obligation

• Legal (related to TCA of the entity) • All liabilities (direct responsibility

and assumed)

Extent of contamination

• Does not need to exceed

the environmental standard

• Must exceed the

environmental standard

24

25

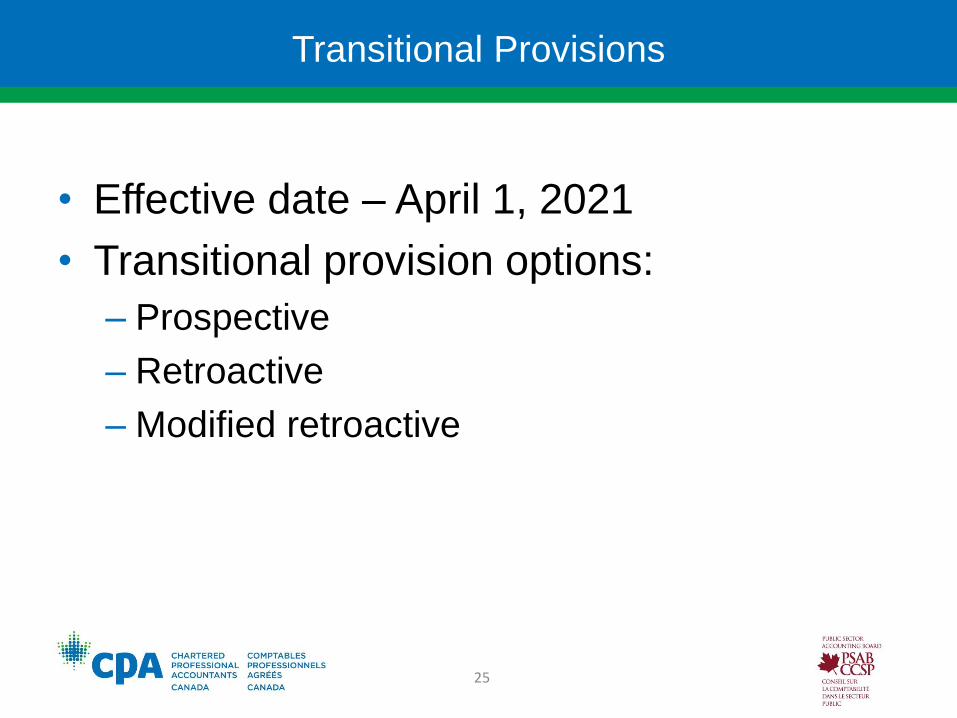

Transitional Provisions

• Effective date – April 1, 2021

• Transitional provision options:

– Prospective

– Retroactive

– Modified retroactive

26

Get Involved and Stay Informed

• Read the Exposure Draft

www.frascanada.ca

• Provide your comments by June 15, 2017

• Stay informed

– subscribe to emails http://www.frascanada.ca/subscribe

– Asset Retirement Obligations project page http://www.frascanada.ca/standards-for-public-sector-entities/projects/active/item56216.aspx