exploration production refining … is now poised to overtake germany as the largest automotive...

TRANSCRIPT

SIBIR ENERGY PLCANNUAL REPORT & ACCOUNTSFOR THE YEAR ENDED 31DECEMBER 2007

EXPLORATIONPRODUCTION REFINING MARKETING

SIBIR ENERGY PLC

104946 Sibir07_covers_AW 27/6/08 10:33 am Page 1

SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

DRILLING RIGS AT THE SALYM OIL FIELDS IN WESTERN SIBERIA

RUSSIAN AND INTERNATIONAL

104946 Sibir07_covers_AW 27/6/08 10:34 am Page 2

BUSINESS IN HARMONY2007 HighlightsReport of the Chairman and Chief ExecutiveOperations ReviewFinancial ReviewBoard of DirectorsThe Workings of the Board and its CommitteesRemuneration ReportDirectors’ ReportStatement of Directors’ Responsibilities for the GroupIndependent Auditors’ Report for the Group

126

20283032343738

Consolidated Group Income StatementConsolidated Group Balance SheetStatement of Changes in Shareholders’ EquityConsolidated Group Cash Flow StatementNotes to the Consolidated Financial StatementsStatement of Directors’ Responsibilities for the CompanyIndependent Auditors’ Report for the CompanyCompany Balance SheetNotes to the Company Financial StatementsCorporate Directory

394041424389909192

102

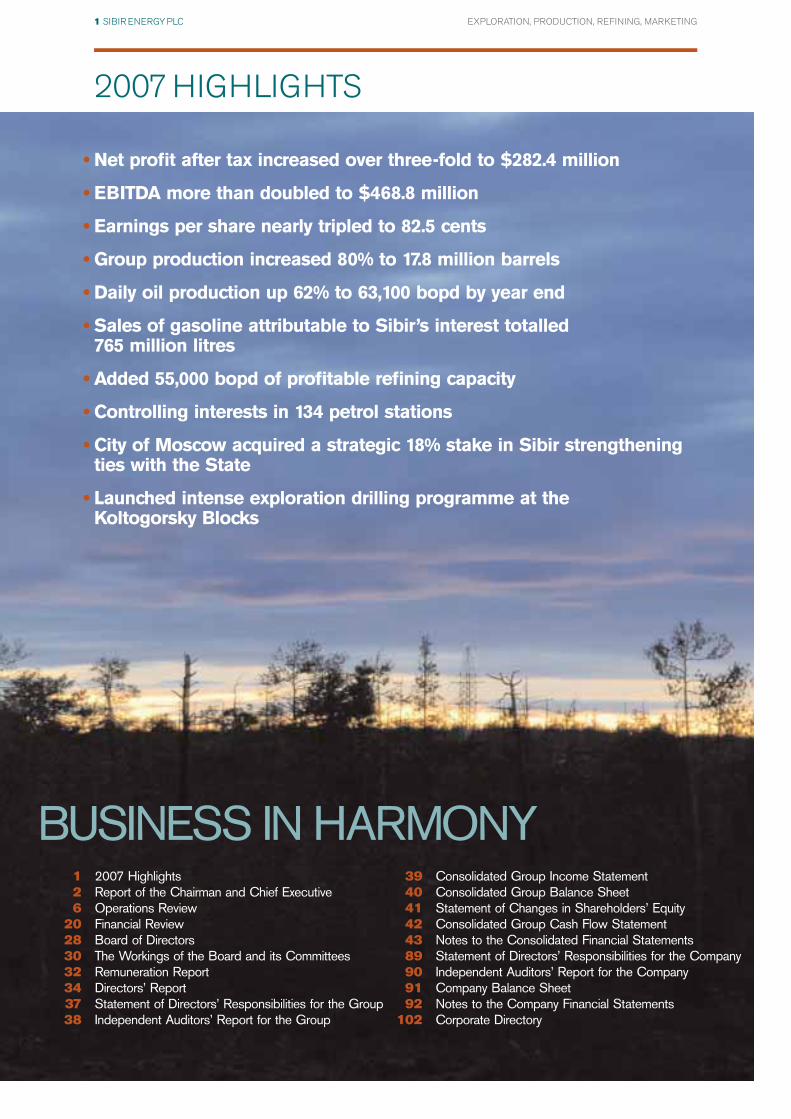

1 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

2007 HIGHLIGHTS

• Net profit after tax increased over three-fold to $282.4 million

• EBITDA more than doubled to $468.8 million

• Earnings per share nearly tripled to 82.5 cents

• Group production increased 80% to 17.8 million barrels

• Daily oil production up 62% to 63,100 bopd by year end

• Sales of gasoline attributable to Sibir’s interest totalled 765 million litres

• Added 55,000 bopd of profitable refining capacity

• Controlling interests in 134 petrol stations

• City of Moscow acquired a strategic 18% stake in Sibir strengthening ties with the State

• Launched intense exploration drilling programme at the Koltogorsky Blocks

2 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

REPORT OF THE CHAIRMAN AND CHIEF EXECUTIVE

GETTING THEFUNDAMENTALSRIGHT

The importance of this development was two fold:

First, we aligned the interests of the Russian Federation and the

other shareholders in Sibir through shared ownership of Sibir,

an essential move in a world where resource nationalism has

gained momentum.

Second, we increased the extent to which our vertically integrated

company participates in the full value chain of the sector – from well

head to gasoline pump. With 100,000 barrels a day of refining

capacity at Moscow Refinery, Sibir now holds an enviable position in

the fastest growing and most dynamic fuels markets in Europe. The

City of Moscow and the Moscow Region has a combined population

of 17 million, making it the largest metropolitan area on the continent

of Europe. Russia is now poised to overtake Germany as the largest

automotive market in Europe, something that looked a remote

possibility only a handful of years ago.

One challenge remained, namely that strained relations with fellow

shareholders at Moscow Refinery created some anxiety in the

financial markets as to our ability to maintain our position there.

We expressed our aspirations and confidence that we would find

a way to operate the Refinery without shareholder controversy. We

confidently predict that we are days away from announcing that the

security of our position at the Moscow Refinery will be well and

truly established in an equitable and evergreen fashion. Together

with Gazprom Neft, the oil subsidiary of state owned Gazprom, the

world’s largest gas company, we will agree to operate the Refinery

on a parity basis and through an independent management team of

industry experts. Any agreement entered into will have a binding

mechanism, independent of shareholders, to deal with deadlock

issues should they arise.

Partnering with majors has been a hallmark of Sibir and being

able to add Gazprom Neft to the list of our existing partners – Shell,

TNK-BP and the City of Moscow – is a formidable achievement for

your company.

We believe the positive spirit and the professionalism of the

negotiations with Gazprom Neft and recent announcements by

the Russian government about reductions in Mineral Extraction

Taxes for oil production, the lowering of export duties on certain

refined products, coupled with the overall growth rate of the Russian

economy have confirmed our optimism in Russia’s long-term

prospects and the opportunities that they provide for Sibir’s continued

development.

In our view, the investment environment in Russia for Sibir has never

been more stable or predictable. One of the fundamentals by now

must be clear to all. The Russian government wants to see Russian

control over its natural resources through state owned companies or

Russian owned entities. Sibir anticipated these developments many

years ago and has intentionally pursued a strategy of majority

Russian ownership. In 2007 we have strengthened our position in

this regard by bringing in an important arm of the Russian State,

namely the City of Moscow, as a strategic shareholder bringing the

total number of Sibir shares in Russian hands to 67% on a fully

diluted basis. As our growth over the years has shown, this is a

strategy which has worked and we believe it will continue so to do.

With the development of Salym in full swing, and as a sign of our

confidence, we embarked upon our quest for replacement reserves.

In March 2007 we acquired our first exploration asset – the eight

Koltogorsky Exploration blocks – and launched an intensive

exploration drilling programme to be completed by the end of 2008,

3 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

In September 2007 when we last reported to you we wrote about the importanceof the City of Moscow becoming a strategic shareholder in Sibir as a result ofSibir acquiring 100% of Moscow Oil and Gas Company (“MOGC”). The predictedbenefits from this development have continued to accrue as the Sibir shareincreased 37% in value from £5.11p on the day before the announcement of the deal to over £7 as we go to press.

CHAIRMAN MR. WILLIAM GUINNESS CHIEF EXECUTIVE MR. HENRY CAMERON

weather permitting. To date, 3 of the 8 wells have been drilled and

we are encouraged that the wells drilled so far have encountered

hydrocarbon-bearing sands.

When we completed the MOGC deal, we agreed with the City of

Moscow that we would undertake, on a best endeavours basis, to

seek admission of Sibir’s shares to the Official List of the London

Stock Exchange. We are taking all necessary steps to complete this

move by the end of 2008. However, there are certain opportunities

that your company is pursuing that may delay this move to the first

half of 2009. In either case, the move to the Official List is a top

priority of your management and will be completed in the earliest

timeframe possible.

We declared our maiden dividend in August last year and re-stated

our commitment to pursue a robust and regular dividend policy.

To achieve this, we are engaged in a restructuring of the Group

designed to facilitate this policy. Further announcements can be

expected after publication of our half year interim report in

September.

Production Performance

Upstream production in 2007 rose 80% to a record high of

17.8 million barrels with 15.3 million barrels contributed by SPD and

2.5 million barrels coming from Magma’s upstream unit. The Group’s

total daily production rate closed the year at 63,100 barrels of oil per

day (bopd), an increase of over 60% compared to year-end 2006

production of 38,900 bopd.

In the downstream sector the Moscow Refinery processed 72.9

million barrels of crude in 2007. Sibir’s share of barrels refined

averaged 58,630 bopd, as our tolling quota increased from 45,000

bopd to 100,000 bopd following the completion of the MOGC

acquisition. Sibir’s portfolio of three retail fuel networks in Moscow and

the Moscow Region sold over 1.5 billion litres of gasoline and diesel.

Approximately 765 million litres of this is attributable to Sibir’s interest.

Financial Performance

Sibir presents its 2007 accounts in US dollars as Sibir’s primary

commercial activities, the sale of oil and oil products, are dollar

denominated. This will minimise the effect of currency fluctuations of

the US dollar versus the British pound and thus more accurately

reflect the true operating performance of our business.

This is the first time that we present our accounts in accordance with

International Financial Reporting Standards (IFRS) in compliance with

London Stock Exchange regulations.

2007 was the year when Sibir’s long held aspirations were realised

in hard production and financial numbers. These include record

results in profits and cash flow created by robust production growth

at Salym, strong downstream trading margins from both our refining

and retail operations, and rising crude prices. In addition, our refining

operations at Moscow Refinery increased in volume in the fourth

quarter of 2007 following our MOGC acquisition. This breakthrough

performance is the harvest of many years of investment and industry

and, as we complete 10 years of a Chairman and Chief Executive

team innings, you can well imagine our pleasure in reporting to you.

4 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

REPORT OF THE CHAIRMAN AND CHIEF EXECUTIVE (CONTINUED)

COMCOR ROAD AT SALYM IN WESTERN SIBERIAPIPELINE CONSTRUCTION WORK AT SALYM OIL FIELDS

Earnings contributions from our upstream operations at Magma and

Salym grew over 255% to $249.6 million bolstered by growing

production, strong oil prices and the realisation of income which

had been deferred for accounting reasons. Downstream oil products

trading, retail and refining operations contributed an additional

$148.5 million, a 84% increase over 2006 as we took full advantage

of our increased quota at the Moscow Refinery and enjoyed strong

wholesale and retail refined products margins.

In September, we advised that after years of containing general and

administrative costs, we expected them to increase. We draw your

attention to the Financial Review where you will find an analysis of

these costs. You will appreciate our growth comes at a cost but

we have embarked upon a course of pruning and expect to make

reductions through economies of scale in the second half of 2008.

The net results of these significant developments is that EBITDA more

than doubled to $468.8 million and Net Profit after Tax grew 217% to

$282.4 million compared to $89.0 million in net profit in 2006.

Earnings per Share increased by 169% to 82.5 cents compared to

30.6 cents in 2006.

Legacy Issue

Over time we have had to crave your indulgence in terms of the time

it was taking to pursue restitution of our losses following the dilution

of our interest in Sibneft Yugra. This matter is now being pursued by

a Provisional Liquidator of Yugraneft (the subsidiary of Sibir which

held the Sibneft Yugra interest) appointed by the High Court in

England. Preliminary pleadings essentially on issues of whether the

English Courts have jurisdiction over the defenders and the efficacy

of the appointment of the Provisional Liquidator, are to be heard over

the two weeks beginning 7 July, 2008. We shall report the outcome

of these preliminary issues as and when they are reported by the

Provisional Liquidator.

Looking Forward

In September 2007 we wrote in general terms of ambitious plans to

double the size of the company in 18 months. In the same general

way we are pleased to report that these plans to materially increase

the size of your company remain on track save only that if the plan

does materialise, it is likely to be sooner than later and well within

the earlier 18 month forecast.

None of Sibir’s recent achievements or future plans would be

possible without the extraordinary and ordinary contribution of the

people who show up to work every day to make Sibir’s business a

success. A number of them are being groomed to carry on the work

of the last 10 years, thereby ensuring seamless succession. Sibir is a

young company, an energetic company and its people enthusiastically

embrace the opportunities around them in the new Russia. They are

a good sign that Sibir’s best days are still ahead.

5 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

DOWNSTREAM OIL PRODUCTS TRADING,RETAIL AND REFINING OPERATIONSCONTRIBUTED $136.2 MILLION TOPROFITABILITY, A THREE-FOLD INCREASEOVER 2006

ZITA TEDEEVA, ATTORNEY IN SIBIR’S MOSCOW OFFICE MAINTENANCE WORK UNDER WAY AT MOSCOW REFINERY

6 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

OPERATIONS REVIEW

UPSTREAM:• SALYM DAILY PRODUCTION UP 77%TO 113,000 BOPD

• 45 MW GAS POWER PLANTCOMMISSIONED

• THREE EXPLORATION WELLSDRILLED AT KOLTOGORSKY BLOCKS

DOWNSTREAM:• MOGC ACQUISITION A LANDMARKEVENT IN THE HISTORY OF SIBIR

• MOSCOW REFINERY PROCESSED 72.9 MILLION BARRELS

• RETAIL SALES VOLUMES EXCEED 750 MILLION LITRES

CENTRAL PROCESSING FACILITIES AT SALYM OIL FIELDS IN WESTERN SIBERIA

7 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

STRONGPRODUCTIONGROWTH

The Group’s daily production, at year end, grew 62% to 63,143

barrels of oil per day (bopd) up from 38,901 bopd at the close of

2006 due to continued strong production growth at Salym.

SPD and Magma made significant investments to increase utilisation

of gas associated with oil production which would otherwise be

flared wastefully. A 45MW Power Generation Plant was constructed

at Salym and is now fully operational, providing 65% of the field’s

long-term electricity needs. In 2007 a wet gas pipe line for sale of

gas to Sibur/Gazprom will allow for cessation of associated gas

flaring at Yuzhnoye and Orekhovskoye fields and will be completed

by the end of 2008.

In the spring of 2007 Sibir took its first major steps into exploration

with the acquisition of eight exploration licences, known collectively

as the Koltogorsky blocks, in the Khanty-Mansiysk District of

Western Siberia. By the end of 2007 the first of eight exploration

wells had already been drilled and six exploration rigs had been

contracted to carry out an aggressive exploration drilling program in

2008. The Koltogorsky project is now one of the leading exploration

programmes in the region. With its proximity to the Yuzhnoye and

Orekhovskoye fields, the exploration program is operated by Magma,

resulting in many economies of scale.

Capital and Exploration Expense

The Group’s upstream capital expenditure for 2007 totalled $191.7

million of which $172.4 million was attributable to Sibir’s share of

capex in the Salym fields and $19.3 million was invested at Magma’s

Yuzhnoye and Orekhovskoye fields. Exploration expenditure in 2007

for the Koltogorsky blocks totalled $9.8 million.

The Group’s upstream capital expenditure in 2008 is expected to

total $164.5 million, with $128.7 million attributable to Sibir’s share

8 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

UPSTREAM OPERATIONS REVIEWSibir enjoyed excellent performance across its entire upstream asset portfolioas Group production rose 80% to 17.8 million barrels. Of the total, 15.3 millionbarrels was produced by Salym Petroleum Development (SPD), Sibir’s 50:50joint venture with Shell which operates the Salym oil fields in the KhantyMansiysk District of Western Siberia, and the remainder was produced bySibir’s subsidiary, Magma, which operates the Yuzhnoye and Orekhovskoyefields in the same region. Total Group production is expected to reach 25 million barrels in 2008.

OPERATIONS REVIEW (CONTINUED)

WIM VAN BEERS, SENIOR WELL ENGINEER AT SALYM PETROLEUM DEVELOPMENT

of capex in the Salym fields and $35.8 million attributed to the

Yuzhnoye ($9.6 million) and Orekhovskoye ($26.2 million) oil fields.

2008 exploration expenditure for the Koltogorsky blocks is expected

to total $69.8 million, while SPD’s exploration at Salym attributable to

Sibir is $7.5 million. Sibir share of abandonment expenditures in the

Salym fields will be $2.2 million.

Operating Environment

Operations at all operating units were significantly hampered by

remarkably mild and short winters, resulting in record high flood-

waters in the swamp-like fields of western Siberia in 2007 and

2008. Changes in the Federal permitting process for construction

and development likewise led to delays in the development of the

Orekhovskoye oil field. The experience of the past several years

suggests these mild weather conditions could become a permanent

feature of the operating environment in Western Siberia and future

operations plans will have to take this into account.

Despite these climatic and administrative challenges, Sibir’s

upstream team delivered impressive production results and laid the

groundwork for continued growth in the future as the following

detailed report shows.

Magma Oil Company

Magma (95% Sibir owned) is the operator of the Koltogorsky

Exploration Blocks on behalf of the wholly owned Sibir subsidiary

licencee and is also the licence holder and operator of the Yuzhnoye

and Orekhovskoye oil fields in Khanty-Mansiysk District of West

Siberia. Magma’s operations in 2007 focused primarily on

development of the Orekhovskoye field and the exploration of the

Koltogorsky resource.

Koltogorsky Exploration Blocks

The Koltogorsky exploration blocks cover 2,100 square kilometres

and are located some 200 kilometres northeast of Nizhnevartovsk,

Magma’s operation base. The licence area comprises a syncline

structure and is surrounded by developed oil fields including the giant

Samotlor oil field some 70 kilometres to the west. In accordance with

Russian GKZ categorisation the Blocks are estimated to contain a

total of 970 million barrels of Russian category C3 oil resources.

These estimates are based on the interpretation of 2,574 kilometres

of 2D seismic profiles. In total, some 34 structures thought to bear

hydrocarbons have been identified by the seismic profile

interpretations.

The Blocks feature excellent available infrastructure including a

Transneft oil pipe line, a Sibur wet gas pipe line, as well as paved

roads and power lines passing through the licence area. This

should limit eventual capex outlays and lead to earlier production

should the exploration program be successful and move to the

development stage.

The Koltogorsky exploration licences require Sibir to drill and test

eight wells (one per block) and acquire an additional 180 kilometres

of 2D seismic profiles by the end of February, 2009. Should the

exploration program be successful, Sibir will apply for an extension

9 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

VYACHESLAV BARANOV, GEOLOGIST AT SALYM PETROLEUM

DEVELOPMENT

WORK PROCEEDS ON SALYM DRILLING RIG

THE KOLTOGORSKY EXPLORATION BLOCKSFEATURE EXCELLENT AVAILABLEINFRASTRUCTURE INCLUDING A TRANSNEFTOIL PIPE LINE, A WET GAS PIPE LINE, PAVED ROADS AND POWER LINES

and conversion of the licences to 20/25 years exploration, appraisal

and development licences. To meet the tight timeline of the licence

requirements, Magma has engaged three drilling contractors, each

providing two rigs, as well as several construction and testing

services contractors.

The first well (141P) was spudded in Q4 2007 and reached total

depth of 3,200 metres on Christmas Eve. After acquisition of a

vertical seismic profile the rig was disassembled and remobilised to

drill the second exploration well.

Koltogorsky Exploration Blocks 2008 Preview

By the end of the 2007-2008 winter season Magma had completed

71 kilometres of permanent and winter roads, prepared 7 well pads

and mobilised five exploration rigs. The second exploration well (111P)

was spudded in early April 2008 and reached total depth of 3,500

metres by late May. A third well (121P) was spudded at the end of

April, and fourth well (151P) is expected to spud in July. Two additional

wells (71P and 101P) are scheduled for September and the last two

(81P and 91P) in December. Sibir is encouraged by the initial results

from the first three wells as drilling cores and well logs show

hydrocarbon saturations in Middle and Upper Jurassic sandstones.

Yuzhnoye Oil Field

The Yuzhnoye oil field lies 60 kilometres to the southwest of

Magma’s operations base in Nizhnevartovsk. In 2007 Yuzhnoye

celebrated the 15th anniversary of the start of production during

which time it has produced over 24.5 million barrels of oil.

In 2007 Magma completed design documents and land surveys for

construction of a 27 kilometre wet gas pipeline from the Yuzhnoye

Central Processing Facility (CPF) to a tie-in point for deliveries to

Gazprom affiliate Sibur. Currently under construction, the pipeline will

allow Magma to sell its associated wet gas, thus eliminating flaring in

compliance with its licence obligations.

In 2007 three wells totalling 8,451 linear metres were drilled, ten

wells were completed or recompleted, fifty-seven well workovers

were carried and eighty-five well service jobs performed including

nine hydraulic fracturing treatments. A new modelling and design

plan (Technological Schema) for the Yuzhnoye field was submitted to

the authorities for approval.

Yuzhnoye 2008 Preview

Activities at Yuzhnoye in 2008 are focused on completion of the wet

gas pipeline to eliminate flaring. On the basis of results of recent

development drilling (2004 to 2007) a revised Technological Schema

will be approved in course of 2008 and is expected to include

further development drilling in the southern area of Yuzhnoye.

Orekhovskoye Oil Field

The Orekhovskoye field is a greenfield property which lies 22

kilometres to the northwest of the Yuzhnoye oil field. Sibir acquired

the licence for Orekhovskoye as part of its purchase of Magma in

1997, but development was delayed because the economics of the

project were thought to be unattractive in the lower oil price

environment that prevailed at the time. Taking into consideration the

10 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

OPERATIONS REVIEW (CONTINUED)

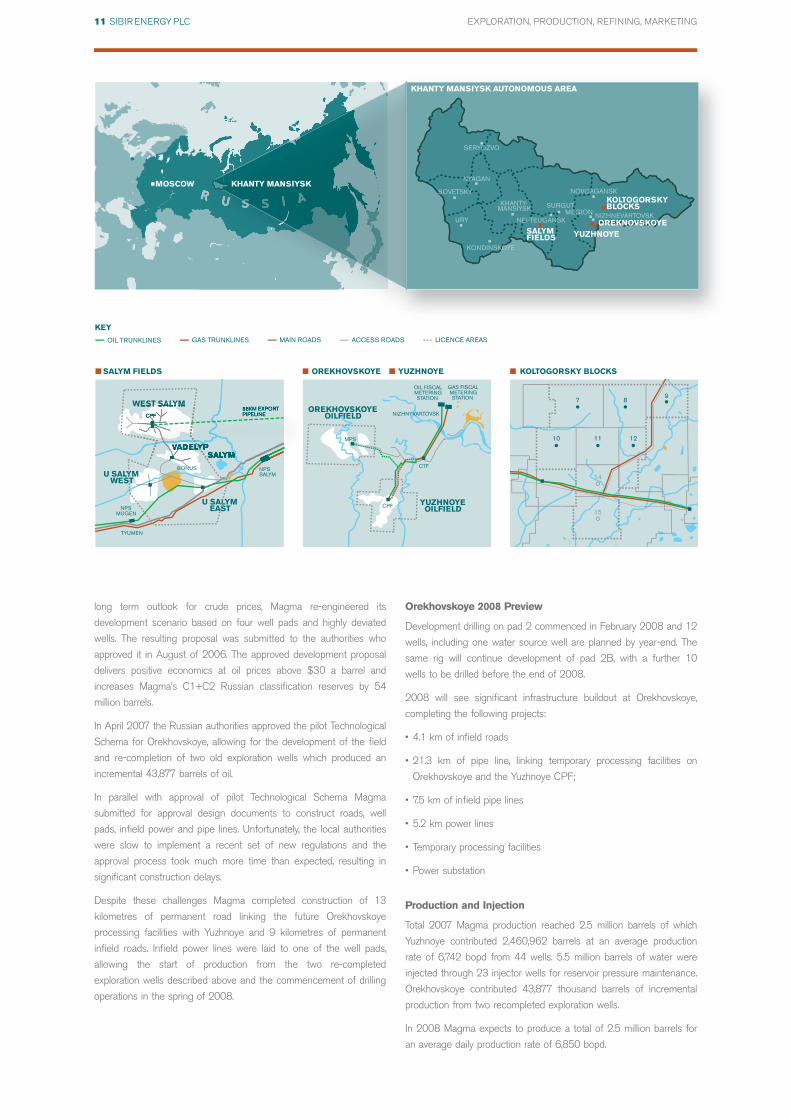

SALYM CENTRAL PROCESSING FACILITIES AT NIGHT

MOSCOW

KOLTOGORSKYBLOCKS

SALYMFIELDS

KHANTY MANSIYSK AUTONOMOUS AREA

KHANTY MANSIYSK

OREKNOVSKOYEYUZHNOYE

SOVETSKY

URY

KONDINSKOYE

KHANTY-MANSIYSK SURGUT

NEFTEUGANSK

NOVOAGANSK

MEGION NIZHNEVARTOVSK

NYAGAN

SERYOZVO

KOLTOGORSKY BLOCKS

WEST SALYM

U SALYMWEST

U SALYMEAST

SALYM

BONUS NPSSALYM

88KM EXPORT PIPELINECPF

NPSMUGEN

TYUMEN

VADELYP

SALYM FIELDS

MPS

CPF

CTF

OIL FISCALMETERINGSTATION

GAS FISCALMETERINGSTATION

OREKHOVSKOYEOILFIELD

YUZHNOYEOILFIELD

NIZHNYVARTOVSK

7 89

1211

14

15

10

OREKHOVSKOYE YUZHNOYE

OIL TRUNKLINES

KEY

GAS TRUNKLINES MAIN ROADS ACCESS ROADS LICENCE AREAS

long term outlook for crude prices, Magma re-engineered its

development scenario based on four well pads and highly deviated

wells. The resulting proposal was submitted to the authorities who

approved it in August of 2006. The approved development proposal

delivers positive economics at oil prices above $30 a barrel and

increases Magma’s C1+C2 Russian classification reserves by 54

million barrels.

In April 2007 the Russian authorities approved the pilot Technological

Schema for Orekhovskoye, allowing for the development of the field

and re-completion of two old exploration wells which produced an

incremental 43,877 barrels of oil.

In parallel with approval of pilot Technological Schema Magma

submitted for approval design documents to construct roads, well

pads, infield power and pipe lines. Unfortunately, the local authorities

were slow to implement a recent set of new regulations and the

approval process took much more time than expected, resulting in

significant construction delays.

Despite these challenges Magma completed construction of 13

kilometres of permanent road linking the future Orekhovskoye

processing facilities with Yuzhnoye and 9 kilometres of permanent

infield roads. Infield power lines were laid to one of the well pads,

allowing the start of production from the two re-completed

exploration wells described above and the commencement of drilling

operations in the spring of 2008.

Orekhovskoye 2008 Preview

Development drilling on pad 2 commenced in February 2008 and 12

wells, including one water source well are planned by year-end. The

same rig will continue development of pad 2B, with a further 10

wells to be drilled before the end of 2008.

2008 will see significant infrastructure buildout at Orekhovskoye,

completing the following projects:

• 4.1 km of infield roads

• 21.3 km of pipe line, linking temporary processing facilities on

Orekhovskoye and the Yuzhnoye CPF;

• 7.5 km of infield pipe lines

• 5.2 km power lines

• Temporary processing facilities

• Power substation

Production and Injection

Total 2007 Magma production reached 2.5 million barrels of which

Yuzhnoye contributed 2,460,962 barrels at an average production

rate of 6,742 bopd from 44 wells. 5.5 million barrels of water were

injected through 23 injector wells for reservoir pressure maintenance.

Orekhovskoye contributed 43,877 thousand barrels of incremental

production from two recompleted exploration wells.

In 2008 Magma expects to produce a total of 2.5 million barrels for

an average daily production rate of 6,850 bopd.

11 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

12 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

PUMP HOUSE AT SALYM CRUDE OIL TRANSFER FACILITY

OPERATIONS REVIEW (CONTINUED)

Capital Spending

Capital expenditure for Magma in 2007 totalled $19.3 million of

which $14.6 million was invested in Yuzhnoye projects and $4.7

million in the Orekhovskoye development.

Projected 2008 capital expenditure is $35.8 million of which

$9.6 million has been allocated to Yuzhnoye and $26.2 million to

Orekhovskoye.

Salym Petroleum Development N.V. (SPD)

SPD is Sibir’s 50/50 joint venture between its 100% owned

subsidiary Evikhon and Shell Salym Development B.V. , a member of

the Royal Dutch Shell Group. SPD operates the Salym Group of

fields (West Salym, Vadelyp and Upper Salym) in the Khanty-

Mansiysk District in West Siberia. With 1.1 billion barrels of Russian

classification C1+C2 reserves, the Salym development represents

the largest single on-shore project in Russia with foreign

participation. SPD launched production from the Salym fields in late

November of 2005 and has grown production to over 127,000 bopd

as of today.

Salym Fields

2007 was a year of spectacular production growth at Salym as the

final key infrastructure projects were commissioned and drilling

operations developed momentum. SPD’s highly efficient drilling

programme continued with four rigs operating in 2007, one heavy

duty rig was replaced with a 200-tonne mobile rig, and six service

rigs/hoists were at work on completions and work-overs. The SPD

drilling team continued to set records for drilling time, completing

wells in as few as 6.7 days. Well completion efficiency has been

improved to 4.1 days per well and well hook-up times have reached

technical limits.

Production slowdowns in the first quarter stemming from the failure

of water injection pumps were resolved, first by installation of

Russian modular water injection pumps and later, with the repair

and reinstallation of high-volume mega-pumps getting production

back on track.

SPD drilled four dedicated producing wells and one injector for the

pilot development of the Achimov reservoir. The Achimov is a tight

heterogeneous reservoir that lies beneath the main producing

reservoir and has significant volumes of oil resources in place. The

plan is to perform large volume hydraulic fracturing treatments in

2008 and produce the wells to evaluate economic potential of large

scale development of the reservoir.

SPD commenced construction of a three-turbine, 45 MW Power

Generation Plant (PGP) to utilise most of Salym’s produced

associated gas and provide a material part of the electric power

needed to run the project for decades to come. The PGP will

also allow SPD to reduce flaring in line with environmental protection

requirements while reducing exposure to anticipated increases

electricity prices resulting from the deregulation of the power

sector. The plant was fully commissioned and operational as of early

April 2008.

13 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

PRESSURE MONITORING GAUGE AT SALYM CPF

Other operational highlights at Salym included:

• Completion of the second phase of Custody Transfer Facilities

(CTF) with two 20,000m3 tanks, transfer pumps and fire pumps;

• Construction of 5 new pads with infield roads, power lines and

pipe lines

• Total of 100 new wells drilled, 78 on West Salym, 1 on Upper

Salym and 21 on Vadelyp

• 106 new wells hooked up

• 108 initial well completions

• 118 well workovers and well service jobs

• 8 hydraulic fracturing treatments

• Expansion of the operations base with two accommodation units,

office block, car wash and covered storage area

• Completion of an office block on the Salym CPF

• Construction of phase one of waste handling and processing

facilities

• Installation of modular water injection facilities on Upper Salym;

Production and Injection

Total 2007 production at Salym doubled to 30.7 million barrels

(15.3 million barrels Sibir share) up from 14.9 million barrels

(7.5 million barrels Sibir share) in 2006. The daily production rate

grew 77% from 64,000 bopd at the beginning of the year to

113,000 bopd by year end. Water injection for reservoir pressure

maintenance totalled 36.4 million barrels reaching required volumes

to balance depletion and manage reservoir pressure support.

Capital Expenditure

Sibir’s share of capital, exploration and abandonment expenses

for the period totalled $172.4 million including $87.9 million for

construction of facilities and infield infrastructure and $79.5 for

drilling and completion of the wells. $1.9 million was spent on

exploration and $3.1 million on abandonment expenditures.

Operational Highlights by Field

West Salym:

West Salym continues to be the focus of SPD’s activities as the field

contains some 70% of total Salym reserves. 2007 operational

highlights for West Salym include:

• Three well pads completed, drilling, completions and hook-ups

under way, production commenced;

• Infield infrastructure (oil and injection water pipe lines, roads and

power lines) completed for 3 pads;

• Water Injection facilities fully in place with two big flow serve

(15,000m3/day each) and back up Russian modular pumps;

• 78 wells drilled;

• 85 wells completed;

• 54 new producing wells brought on stream;

• 5 dedicated Achimov wells drilled and one hydraulically fractured;

• Construction of phase 2 Custody Transfer Facilities (CTF) at the tie

in of the export pipeline to Transneft pipeline system completed;

• Phase one of waste processing facilities completed.

Upper Salym

The Upper Salym licence area has significant potential. SPD is

continuing studies and investments to fully valuate its upside. 2007

accomplishments at Upper Salym include:

• Completion of modular pump station for water injection;

• Completion of well pad K-2;

• 1 well drilled;

• Preparation of new Technological Schema.

Vadelyp profile

Vadelyp consists of two structures, Vadelyp North and Vadelyp South.

The development of Vadelyp North commenced in 2006, and

continued during 2007. Studies and preparation of the development

of Vadelyp South took place in 2007 to be continued through 2009.

In 2007, the following progress was recorded at Vadelyp:

• new well pad built;

• 21 wells drilled;

• 23 wells completed.

Salym 2008 Preview

Continued development of the Salym fields in 2008 is expected to

bring total production of up to 45 million barrels. Daily production is

expected to reach 130,000 bopd by year-end based on currently

approved projects. SPD is preparing several incremental projects

such as hydraulic fracturing treatments, flank and in-fill drilling

which could bring 2008 year-end production to 140,000 bopd and

add incremental production in the years to come.

Development projects for 2008:

• To support steady production growth SPD plans to drill additional

water source wells to increase water injection capacity injection of

water for reservoir pressure maintenance.

• Exploration and appraisal activities at Salym will continue in 2008,

with the Achimov Pilot Development on West Salym, and the

drilling of exploration wells on Upper Salym and South Vadelyp.

SPD plans to drill two more prospects on Upper Salym (Lebed and

Glukhar) in the winter 2008/2009 and pilot development of Middle

Cretaceous BS8 reservoir on Upper Salym. This pilot, consisting of

9 wells, will be initiated in 2008 and will continue during 2009.

• The CPF on West Salym will be upgraded with two 100m3 inlet

separators, one 100m3 final stage separator and two 5,000m3

water skim tanks.

• Two new well pads will be completed, and the three pads already

completed in 2007 (21, 25 and 27) will produce first oil in 2008.

14 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

OPERATIONS REVIEW (CONTINUED)

CONTRACT DRILLING RIG OPERATOR AT THE SALYM OIL FIELDS IN WESTERN SIBERIA

.• An operations base fuel filling station, sport hall and ambulance

garage will be completed.

• Drilling with four rigs, and completions and well servicing with

6-7 rigs/hoists will continue.

• To manage remaining volumes of associated gas not utilised by the

45MW power plant, SPD has entered into an agreement with a

third party which will build and operate an LPG plant next to the

Salym CPF. The plant will take wet gas deliveries from Salym as

well as neighbouring producing properties and is expected to be

commissioned in 2010.

Group Reserves Summary

The Group’s interests in commercial reserves of oil as of 31

December 2007 are included in the unaudited table below:

RUSSIAN RESERVES CLASSIFICATION (1)

Million barrels A+B+C1 C2 Total

Magma’s Yuzhnoye and 125 11 136

Orekhovskoye Oil Fields

Salym Group of Fields 376 156 532

(50%) (2)

Total 501 167 668

1. RUSSIAN RESERVES ARE CLASSIFIED AS FOLLOWS:

A = RESERVES PROVED AND DEVELOPED IN ACCORDANCE WITH APPROVED

(BY RUSSIAN AUTHORITIES) DEVELOPMENT PLAN.

B = RESERVES PROVED AND DEVELOPED IN ACCORDANCE WITH EARLY

DEVELOPMENT PLAN.

C1 = RESERVES TESTED AND MOSTLY PROVED BUT NOT DEVELOPED.

C2 = RESERVES CONTIGUOUS TO C1 AND SUBSTANTIATED BY GEOLOGICAL

DATA AND LIE WITHIN PROBABLE, POSSIBLE AND CONTINGENT.

2. AS NOTED IN PREVIOUS REPORTS, SPD USES A RESERVES CLASSIFICATION

KNOWN AS PROVEN, EXPECTED AND SCOPE FOR RECOVERY RESERVE

ESTIMATE BASED ON THE FIELD DEVELOPMENT PLAN WHICH TOTAL 888

MILLION BARRELS (OR SIBIR SHARE – 444 MILLION BARRELS). THE

DIFFERENCE BETWEEN THE SPD ESTIMATES AND THE RUSSIAN RESERVES

NUMBERS ARE DUE PRIMARILY TO THE EXCLUSION OF THE LOWER

RESERVOIRS IN THE SPD NUMBERS.

15 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

HEAD LABORATORY TECHNICIAN, IRINA SHUVALOVA, AT MAGMA’S YUZHNOYE OIL FIELD IN WESTERN SIBERIA

The completion of the MOGC deal has also allowed for a resolution

of the long-standing conflicts between shareholders at the Moscow

Refinery, thus clearing the way for long overdue investment to make

it a world class facility. Likewise our ownership of the MTK and MNP

retail fuels networks has allowed us to start implementing an

aggressive plan to upgrade those networks to ensure a leadership

position in the marketplace.

In summary, 2007 was a watershed year for Sibir’s downstream

business and set the stage for 2008 during which the planning,

designing, securing of building permits, and the building of the

management team will allow us to start to turn our vision into

growing operations that will deliver enhanced earnings quality for

years to come.

The Moscow Market

The City of Moscow and the surrounding Moscow Region represent

one of the largest and most dynamic fuels markets in Europe. The

region has a combined population of over 17 million making it the

largest metropolitan area on the continent of Europe. With Russia’s

economic revival Moscow has become a magnet for domestic and

foreign investment, leading to increases in living standards and

consumer spending which are reflected in a 10% annual growth rate

in the number of automobiles on the road over the past three years.

Russia is now poised to overtake Germany as the largest automotive

market in Europe by the end of 2008 supporting continued strong

growth in fuels demand.

Moscow Refinery

The Moscow Refinery is a 240,000 bopd nameplate capacity facility

currently processing 200,000 bopd and supplies over 50% of

Moscow’s motor fuel requirements. Located in the southeastern

district of the city it receives crude supply via the Russian national

Transneft pipeline system whilst refined products are supplied to local

markets and export customers through pipelines, rail cars and trucks.

Over 3,200 staff are employed at the facility.

The Moscow Refinery is designed to process a high sulphur Urals

blend crude slate. The facility comprises over forty processing units

producing approximately 57% high-value light products including

16 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

OPERATIONS REVIEW (CONTINUED)

DOWNSTREAM OPERATIONS REVIEWIn the second half of 2007 Sibir successfully completed its acquisition of MOGC, materially increasing its interests in the downstream business – truly a landmark event in the history of the company.

MAINTENANCE WORKER AT MOSCOW REFINERY

gasoline (RON octane grades 80, 92 and 95), Diesel (winter and

summer) and aviation kerosene (jet fuel). The Refinery is also a

leading producer of heating oil, bitumen and LPG. A large part of the

Refinery’s output is sold into the local market, though a significant

percentage (up to 50%) of diesel is exported.

The Refinery operates as a tolling operation and does not buy crude

or sell oil products itself. Trading activities are carried out by trading

companies which supply crude to the Refinery, pay the Refinery a

per-barrel tolling fee to process the crude and then market the

refined product directly. The Refinery’s tolling fees are sufficient

to cover operating costs, regular maintenance, on-going capital

expenditure leaving profits sufficient to cover payment of dividends

on preferred shares. Thus, the full economic value of the refining

operation is reflected in the results of our trading operation.

Refining Volumes

In 2007 the Moscow Refinery processed 72.9 million barrels of

crude. Sibir’s share of total tolling capacity was 21.4 million barrels or

an average 58,630 bopd, an increase over 2006 as Sibir benefited

from increased tolling capacity after the completion of the MOGC

acquisition in September. Refinery production was temporarily

reduced by nearly 40% during the month of October due to routine

maintenance.

2008 total crude processing volumes are expected to be 71.4 million

barrels of which Sibir is expected to have tolling access to 35.7

million barrels or 97,800 bopd. Maintenance works are expected to

slow processing in April and May, resulting in lower volumes for the

first half of the year.

Future Development Plans

The Moscow Refinery has recently completed a feasibility study

which outlines several scenarios for upgrading the facility over the

next several years. The most likely option currently under study

anticipates a robust, three-stage investment program to increase light

high-value products yields to 90%, improve capacity utilisation and

produce Euro 5 specification motor fuels. Total capital expenditure for

the upgrade is expected to be in excess of $1 billion which will be

the shared responsibility of the shareholders.

Marketing and Distribution

With increasing car ownership, population and affluence, Moscow and

the Moscow region are witnessing record fuel consumption growth.

However, due to a lack of available real estate in Moscow suitable for

petrol service station construction, the market remains significantly

under supplied in terms of the number of filling stations (845 in total).

The market is thus characterised by very high and growing per-station

throughput volumes and retail fuels margins well above European

averages. This is not expected to change anytime soon.

17 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

MR. JEFF FRANKS, HEAD OF RETAIL OPERATIONS MAINTENANCE WORK UNDER WAY AT MOSCOW REFINERY

Sibir has a significant position in this exciting market with an interest

in over 185 petrol service stations in Moscow and surrounding

region. Our retail assets are held through three distinct entities:

Moscow Fuel Company: a network of 71 wholly-owned and operated

MTK-branded service stations in the city of Moscow with sales of

over 485 million litres of motor fuels in 2007. It is the largest network

of existing stations in the city. The company also has a 100%

interest in a large oil products storage and distribution terminal in the

northwest district of Moscow.

The MTK network is primarily a fuels only network which has had

minimal investment over the past 20 years. Sibir has announced a

major investment program of over $200 million over the next five

years to significantly upgrade this network to international retail

standards to include modern, multi-product fuelling facilities,

convenience retail stores, ready-to-serve food offering and automatic

carwashes where real estate dimensions permit. In 2008 the

company’s activities will focus on planning and securing the necessary

building permits to launch this ambitious development program.

Mosnefteproduct: A network of 63 NEFTO-branded service stations

51% owned by Sibir in the economically vibrant region surrounding

Moscow. This region is experiencing tremendous development and

growth as Muscovites have developed a taste for suburban living. This

is leading to increased road construction, development of housing and

consumer retail facilities and local employment. The NEFTO-branded

network is comprised of Soviet-era facilities that have suffered from

years of under-investment as reflected in its 2007 sales volumes of

65 million litres. Approximately half of the network stations are being

18 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

OPERATIONS REVIEW (CONTINUED)

PUMP ATTENDANT, MIKHAIL DUDKIN, AT MTK’S SUSHEVSKY VAL

SERVICE STATION IN MOSCOW

ABOVE TOP: MTK’S YUZHNOYE BUTOVO PETROL STATION IN MOSCOW

ABOVE: BP PETROL STATION IN MOSCOW

WITH 2007 SALESOF OVER 988MILLION LITRES,THE BP NETWORKIS THE CLEARMARKET LEADERIN MOSCOW

targeted for demolition and rebuild over the next 5 years requiring

some $75 million in capital investment. The renewed network will form

the basis for significant expansion to develop a leading position in the

Moscow region and surrounding territory.

STBP: In 2006 Sibir acquired its 25% +1 share interest in this

BP-branded service station network of 51 facilities in Moscow and

the surrounding region. Established over 10 years ago, the BP

network is a greenfield development that has been built to the

highest international retail standards. All facilities feature modern,

high-volume fuelling facilities, large convenience stores with in-

store bakeries and cafes. Automatic carwashes are available on

approximately fifty percent of locations. With 2007 sales of over 988

million litres the BP network is the clear market leader in Moscow.

Future development plans call for the network to grow to between

90 and 120 filling stations over the next 5 years.

Retail Sales Summary

2007 retail fuels sales volumes from all networks totalled 1.5 billion

litres of which 765.15 million litres are attributable to Sibir

Total Sales Sibir Net Sibirmltrs Interest % Share mltrs

MTK Network 485,000 100 485,000

Mosnefteproduct 65,000 51 33,150

STBP 988,000 25 247,000

Total 1,538,000 765,150

19 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

REFRIGERATED PRODUCTS AT MTK CONVENIENCE STORE IN MOSCOW NADEZHDA SURKOVA, EMPLOYEE AT MTK SERVICE STATION

CONVENIENCE STORE IN MOSCOW

20 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

FINANCIAL REVIEW

CRUDE STORAGE TANK AT SALYM

21 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

RECORDFINANCIALRESULTS

22 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

Key Financial Indicators2007 2006 % change

EBITDA* $468.8 $163.8 186

Net Profit $282.4 $85.4 231

Net Debt/(Net Cash) $320.4 ($12.8) n/a

Gearing % 29% n/a n/a

*EBITDA comprises the Group’s earnings before interest, tax, depreciation and amortisation andincludes a group share of EBITDA for joint ventures.

Operating Environment

The average Brent price for the year was $71.66 or 8.8% higher

than the $65.38 average for 2006.

Russian Mineral Extraction Taxes (MET) and export taxes are set

every two months based on average prices for the previous two

months. Sibir enjoyed a positive tax effect from this structure

throughout the year as lower MET and export tax calculations trailed

rising crude prices. The reverse will apply in any period if and when

the crude oil price is in decline.

General Observations on Accounts

Because Sibir’s revenues are denominated primarily in US dollars

the dollar is its functional currency and Sibir reports its results in US

dollars rather than pounds sterling as was done previously. Reporting

in US dollars eliminates the effect of fluctuations in the dollar/

sterling exchange rate and provides a more accurate picture of the

company’s financial performance.

Sibir also, for the first time, presents its full-year accounts in

accordance with International Financial Reporting Standards (IFRS).

A guide to the Group Income Statement

In our Group Income Statement, IFRS requires that in line items

“Turnover,” “Gross Profit,” and “Operating Profit,” we show only the

results of those businesses which we control, namely Magma’s

upstream and downstream operations and, from 18 September 2007,

the business of MOGC. The line item “Administrative and General

Expenses” represents expenses of those controlled businesses and

includes the general corporate expenses for the Group. The results

from SPD, Moscow Refinery and STBP are shown net of directly

related expenses including profits tax as a separate line item under

“Share of Profit from Joint Ventures and Associates.”

Analysis by Business Segment

While the results presented in this manner ensure we comply with

IFRS, an analysis of the same numbers by business segment

provides, in our view, a more helpful explanation to you as

shareholders of the Company’s performance.

FINANCIAL REVIEW

In 2007 Sibir’s integrated operations produced record financial results driven by production growth at Salym, higher crude oil prices combined with increasedrefined products volumes and refined product and retail margins downstream.

SALYM DRILLING RIG AT NIGHT

The segment analysis below breaks out contributions to profitability

from the key business segments in upstream and downstream

sectors. Administrative expenses of Magma and MOGC are similarly

broken out from the corporate expenses in the IFRS accounts and

allocated to the relevant segment to provide a clear picture of

segment profitability.

Profit contribution by segment

2007 2006 %$000 $000 Change

Upstream

Salym 219,109 49,774 340

Yuzhnoye and Orekhovskoye 30,500 20,537 49

Total Upstream Contribution 249,609 70,311 255

Downstream

Products trading, refining and retail 127,482 80,797 58

Share of Net Profit from BP retail 21,049 -

Total Downstream Results 148,531 80,797 84

Corporate expenses (31,753) (22,843) 39

Finance Costs (22,715) (16,290) 39

Tax (61,245) (23,005) 166

Net profit 282,427 88,970 217

Upstream

Total Sibir Group crude oil production in 2007 rose 80% to 17.8

million barrels of which 15.3 million barrels came from Sibir’s share

of growing production from SPD and the remainder from the Magma

production unit. Sibir’s 50% share of Salym production increased

33% in the second half of 2007 to 8.77 million barrels from 6.57

million barrels in the first half while Magma production held steady.

Salym

Salym’s contribution to profitability in 2007 increased 340% to

$219.1 million and is made up of three components: $90.3 million,

which represents Sibir’s 50% share of SPD’s net income after tax;

$77.7 million of interest income before tax earned by Sibir on its

outstanding loans to the SPD joint venture (these loans totalled

$598.4 million at year-end); and $51.1 million before-tax gain on the

recognition of a free carry from Shell now realised in 2007.

Production at Salym in 2007 doubled to 30.7 million barrels (15.3

million barrels Sibir share) up from 14.9 million barrels (7.5 million

Sibir share) in 2006. SPD turnover in 2007 increased to $1,330.5

million and gross profit, after depletion, grew to $408.6 million from

$165.7 million. Operating Profit rose to $320.9 million from $93.3

million in 2006.

Per barrel production expenses at SPD decreased by 45% to

$4.06/barrel compared to $7.78/barrel in 2006 due to a doubling of

production and the achievement of economies of scale associated

with such a large production ramp-up.

23 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

IRINA KOLTSOVA AND KSENIA KOSHELEVA OF SIBIR’S MAGMA

TRADING GROUP

SALYM DRILLING RIGS WORK AROUND THE CLOCK

Yuzhnoye and Orekhovskoye as operated by Magma

Magma’s upstream production unit, comprising the Yuzhnoye and

Orekhovskoye fields, contributed $30.5 million before tax, an

increase of 50% from $20.5 million in 2006.

Of Magma’s total 2.5 million barrels of production, approximately

43% was exported and the balance delivered for processing at

the Moscow Refinery. Magma’s trading unit (part of the downstream

segment) also purchases Sibir’s share of the 29% of Salym

production sold domestically for processing at the Moscow Refinery.

Transfer pricing for crude processed at the Moscow Refinery is

calculated on an arm’s length basis.

Production expenses at Magma increased 15% in 2007 due to a

$1.7/barrel increase in MET and an increase in operating expense

from an average of $3.16/barrel in 2006 to $4.38/barrel in 2007.

The increase operating expenses resulted from cost inflation of

oil treatment charges, wages, oil field services, electric power and

appreciation of the rouble against the dollar.

Downstream

Downstream contributions to profitability in 2007 grew 84% to

$148.5 million. Contributions to earnings from oil products trading

and crude processing represent $127.5 million, a 58% increase over

2006 and were due to strong product margins and an increase in

our processing quota from 45,000 bopd to 100,000 bopd (average

58,630 bopd for the year) following the completion of the MOGC

deal. Sibir’s share of earnings from the Moscow Refinery was modest

because the Refinery runs as a tolling operation and the bulk of the

profits being captured in the trading business. The contribution from

MOGC to operating profit amounted to a loss of $8.5 million for the

period following completion of the MOGC deal and includes $19.2

million in corporate expenses and $7.8 million of depreciation. This

level of expense in MOGC is clearly excessive and a restructuring

plan will eliminate such losses in the future.

For the first time, Sibir consolidates earnings from its 25% share of the

BP retail joint venture, consolidating $21.0 million in net income after

tax from this outstanding retail network of only 51 stations. These

stations sold together 988 million litres for the year making average

per-station throughput volumes amongst the highest in the world.

Corporate Expenses

As advised in September corporate expenses (which in this business

segment analysis, exclude expenses of MOGC and Magma)

increased 39% from $22.8 million to $31.8 million due to increases

in banking and consulting fees paid in association with the MOGC

acquisition, legal fees incurred in pursuing legacy issues of the

Sibneft-Yugra dilution and increases in salaries and bonuses for key

personnel.

Administrative Expenses in the IFRS income statement amount to

$73.2 million. For the segment analysis referred to above, those were

broken out in the following manner: $35.8 million are attributable

directly to Sibir Group overheads and administrative expenses; $3.5

was allocated to Magma’s Upstream Production units (at Yuzhnoye

24 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

FINANCIAL REVIEW (CONTINUED)

GAS SEPARATION UNIT AT SALYM CPF

and Orekhovskoye), $6.9 million was allocated to Magma’s products

trading unit; and $27 million (including depreciation) was attributable

to overheads at MOGC.

Finance Costs

Net Interest expense of $22.7 million was up 39% in 2007 from

$16.3 million in 2006. Of the total, $17.6 million was related to

interest receivable from bank deposits, loans to MOGC and Central

Fuel Company. The balance was made up of $38.9 million of interest

payable on bank loans used to finance the MOGC and Koltogorsky

acquisitions as well as lines of credit drawn to finance expanded

domestic crude oil purchases due to Magma’s increased processing

quota at the Moscow Refinery and increases in domestic crude prices.

Taxation

The 2007 taxation charge of $61.2 million, predominantly comprises

profits tax payable by our Russian operating subsidiaries, Magma and

MOGC, of $41.0 million (2006: $22.3 million) and $2.9 million

respectively, and $17.8 million payable by Evikhon on the non

recurring carry item of $51.1 million realised during 2007.

Net Profit and Earnings per share (EPS)

Group Net Profit after interest and taxation was $282.4 million in

2007 compared net profit of $89.0 million in 2006, a 217% increase

and an improvement in financial performance of $193.4 million.

Earnings per share (EPS) increased by 169% to 82.50 cents in

2007 from 30.65 cents in 2006.

Balance Sheet

As at 31 December 2007, the Group’s net assets have increased by

$1,082 million to $2,124 million reflecting the acquisition of MOGC

group of companies on 18 September 2007.

Net debt for the Group grew to $320.4 million at the end of 2007

from a net cash position of $12.8 million in 2006 reflecting

increased borrowings to finance the cash portion of the MOGC

share acquisition and expanded use of trade finance to support

increased trading activity arising from the doubling of Magma’s

processing quota at the Moscow Refinery. Despite this increase in

borrowings, the company’s ability to service its debt is extremely solid,

as evidenced by the Group’s 2007 EBITDA of $468.8 million being

greater than the Group’s net debt of $320.4 million.

The Group’s net current assets for 2007 increased $60.5 million to

$291.0 million compared to $230.5 million as at 31 December

2006 due predominantly to increases in the Group’s cash balances.

Total non-current liabilities increased to $492.0 million from $109.7

million as at 31 December 2006 as a result of increased borrowings

used to finance the Group’s acquisitions of MOGC and the

Koltogorsky exploration blocks and expanded cash requirements for

crude purchases arising from the increase in the tolling quota at the

Moscow Refinery. The increase in non-current liabilities also resulted

from deferred tax and other tax provisions included within MOGC

group prior to its acquisition by Sibir.

25 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

DRILLING RIG ROTARY TABLE AT THE YUZHNOYE OIL FIELD WELL WORKOVER UNDER WAY AT THE YUZHNOYE OIL FIELD

26 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

Total assets less current liabilities as at 31 December 2007

was $2,615.8 million compared with $1,151.3 million as of

31 December 2006.

Total shareholder’s equity as at 31 December 2007 was $2,123.9

million compared to $1,041.6 million as at 31 December 2006.

Cash Flow

Cash flow from operating activities:

In 2007, the Group recorded a net cash inflow from operating

activities of $73.8 million compared to a net cash outflow of $61.5

million in 2006. This is a reflection of the increased profitability of

the Group, coupled with a significant improvement in the Group’s

working capital position.

Cash flow from investing activities:

The Group financed capital expenditure of $13.5 million at Magma,

acquired the Koltogorsky Exploration Blocks for $50.0 million,

incurred subsequent exploration expenditure of $4.4 million, lent

$31.0 million to SPD as payment of cash calls in the early part of

2007 and received loan repayments from SPD in the later part of

2007 in the amount of $76.0 million. The Group also received loan

repayments from other entities in the amount of $43.2 million,

received dividends from STBP in the amount of $16.1 million and

spent $293.9 million in connection with the cash component of the

MOGC transaction (net of cash acquired).

Cash flow from financing activities:

The Group paid dividends in the amount of $44.2 million, drew down

trade finance and other loans in the amount of $630.2 million

and repaid borrowings and trade finance lines in the amount of

$330.8 million.

The year closed with a cash and cash equivalent balance of $293.3

million compared to $216.7 million as at 31 December 2006.

Financial Instruments

The Group’s financial instruments comprise borrowings, cash and

liquid resources, and various items, such as trade debtors, and trade

creditors which arise directly from its operations. The main purpose of

these financial instruments is to finance the Group’s operations. It is,

and has been throughout the period under review, the Group’s policy

that there be no trading in financial instruments. The main risks

arising from the Group’s financial instruments are foreign currency

risk, oil price risk, interest rate and liquidity risk (further information is

contained in note 3 to the financial statements).

The Board reviews and agrees policies for managing each of these

risks and they are summarised as follows under the following two

headings:

FINANCIAL REVIEW (CONTINUED)

GAS SEPARATOR UNITS AT SALYM CPF AT NIGHT

27 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

CONTRACT DRILLING RIG OPERATOR AT THE SALYM OIL FIELDS IN WESTERN SIBERIA

Foreign Currency Policy

Approximately 54% of Sibir’s revenue in 2007 was received in

dollars, the balance being received in Russian roubles. As some of

the development, production and taxation expenditures are in roubles,

along with some interest servicing and loan repayments, the risk from

variations in the value of the rouble is not significant.

Sibir continues to transfer funds to and from Russia without incident

or impediment.

Interest Rate and Liquidity Policy

The Group finances its operations though its own cash on hand,

project finance and trade finance.

Forward Looking Statements

This report contains certain forward looking statements that involve

substantial known and unknown risks and uncertainties, some of

which are beyond Sibir’s control, including the impact of general

economic conditions where Sibir operates, industry conditions,

changes in laws and regulations including the adoption of new

environmental laws and regulations and changes in how they are

interpreted and enforced, increased competition, the lack of

availability of qualified personnel or management, fluctuations in

foreign exchange or interest rates, stock market volatility and market

valuations of companies with respect to announced transactions and

the final valuations thereof, and obtaining required approvals of

regulatory authorities. Sibir’s actual results, performance or

achievement could differ materially from those expressed in, or

implied by, these forward looking statements and, accordingly, no

assurances can be given that any of the events anticipated by the

forward looking statements will transpire or occur, or if any of them

do so, what benefits, including the amount of proceeds, that Sibir will

derive therefrom.

Going Concern

The directors have a reasonable expectation that the Group has

adequate resources to continue its operations for the foreseeable

future. For this reason, they continue to adopt the going concern

basis in preparing the financial statements.

William L. S. Guinness Henry O CameronChairman Chief Executive Officer30 June, 2008 30 June, 2008

28 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

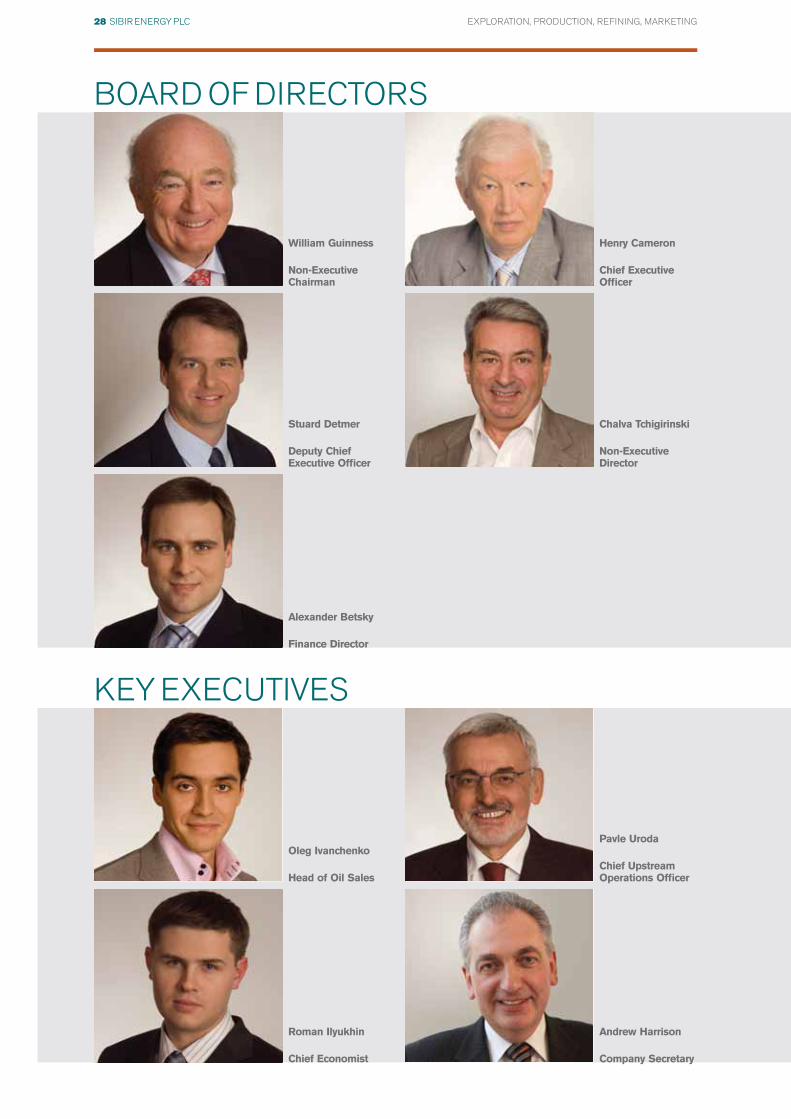

William Guinness

Non-ExecutiveChairman

Henry Cameron

Chief ExecutiveOfficer

Stuard Detmer

Deputy ChiefExecutive Officer

Chalva Tchigirinski

Non-Executive Director

BOARD OF DIRECTORS

KEY EXECUTIVES

Alexander Betsky

Finance Director

Oleg Ivanchenko

Head of Oil Sales

Roman Ilyukhin

Chief Economist

Andrew Harrison

Company Secretary

Pavle Uroda

Chief UpstreamOperations Officer

29 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

Oleg Ivanchenko, Head of Oil Sales

Mr. Ivanchenko, age 31, holds a Candidate of Economic Sciencesdegree from the Moscow Aviation Institute. Prior to joining Sibir, hewas responsible for foreign economic relations and export tradingactivities for the Moscow Refinery. Mr. Ivanchenko speaks fluentRussian and English.

Roman Ilyukhin, Chief Economist

Mr. Ilyukhin, age 30, holds a degree from the Plekhanov Academy ofEconomics and a PhD from the Russian National Academy ofEconomics. Prior to joining Sibir he was Chief Economist for EuroSovPetroleum (UK). Mr. Ilyukhin speaks fluent Russian and English.

Pavle Uroda, Chief Upstream Operations Officer

Mr. Uroda, age 59, has over 36 years’ experience in all areas ofupstream engineering and management. Prior to joining Sibir Mr. Uroda worked for the Croatian National Oil Company, INA,Baker Hughes, Marc Rich & Co, and most recently as CEO of theRussian independent company, Sintez. Mr. Uroda speaks fluentRussian, English and Croatian.

Andrew Harrison, Company Secretary

Mr. Harrison, age 50, is a chartered accountant who qualified withErnst & Young in 1983. Mr. Harrison has wide experience in all areas of financial control and company secretarial matters havingpreviously worked with Dana Petroleum and Caverdale Group plc,an engineering company.

Sibir’s Board and executive team has extensive experience both in Russia andinternationally. The core team is resident in Moscow which allows for seamlesscommunication with our business partners and Russian shareholders.

Mr. William L.S. Guinness, Non-Executive Chairman

Mr. Guinness, age 68, has been Chairman of Sibir since March1999, having previously been a Non-Executive Director of PentexEnergy plc and Pentex Oil plc. He is a director of Boston LifeSciences, Inc. and numerous private companies involved in a widerange of commercial activities.

Mr. L. Stuard Detmer, Deputy Chief Executive Officer

Mr. Detmer, age 44, has extensive experience in the oil industry,having previously worked with Mobil in the US, Latin America andRussia. He attended Leningrad State University and received aBachelor of Arts degree from Vanderbilt University as well as anMBA from the University of Virginia. Mr. Detmer speaks fluentRussian and Spanish.

Mr. Alexander Betsky, CA, Finance Director

Mr. Betsky, age 38, is a Canadian chartered accountant. Beforejoining Sibir in July 2000, he worked as a corporate financeexecutive at Dresdner Kleinwort Benson in Moscow and earlier as an investment banking associate with Bank Menatep in Moscow. Mr. Betsky also has three years of accounting and audit experiencewith Ernst & Young and Lippman Leebosh April in Canada. He holdsa Bachelor of Commerce degree and a Graduate Diploma in PublicAccounting, both from McGill University. He is also a member of the Canadian Institute of Chartered Accountants. Mr. Betsky speaksfluent Russian and French.

Mr. Henry O. Cameron, Chief Executive Officer

Mr. Cameron, age 68, is a Scottish solicitor by profession. Beforedevoting his full attention to the oil sector Mr. Cameron founded andwas senior partner of Peterkins, a large firm of solicitors in Scotland.Peterkins had clients deeply involved with the former Soviet Unionwhich enabled Mr. Cameron to acquire a rare working knowledge ofdoing business in Russia. He has had association with the oil sectorsince the earliest beginnings of the North Sea. In 1989 he assumedcontrol of the Pentex Oil group of companies, which in turn led to thecreation of Sibir Energy plc.

Mr. Chalva P. Tchigirinski, Non-Executive Director

Mr Tchigirinski, age 58, is the representative of the largest share-holder in Sibir. He is a well know Russian businessman. He built hisreputation as one of Russia’s leading real estate developers duringthe late eighties and throughout the nineties. His most recent realestate projects are world class and have extended his reputationworldwide. From June 2000 he has played a fundamental role in thecreation of Sibir as it is today. His business advice and guidance onall matters has proved extremely useful. His commitment to Sibir isunstinting and he is fully devoted to the realisation of optimum valuefor all Sibir shareholders. He speaks fluent English, Georgian and of course Russian.

The Board

At 31 December 2007 the Board comprised three executive Directors and two non-executive Directors, whose details are included on

pages 28 and 29.

The Board is responsible to the shareholders for the proper management of the Group. It meets formally four times a year, to review trading

performance, set and monitor strategy, examine acquisition and divestment possibilities, approve major capital expenditure projects, corporate

overhead costs, significant financing matters and report to shareholders. Matters reserved for the Board are communicated in advance of

formal meetings.

The following committees deal with specific aspects of the Group’s affairs:

Audit Committee

The Company currently does not have an Audit Committee, however it is the intention that this situation will not continue as and when new

non-executive Directors are appointed to the Board. The Audit Committee will then, once again, provide a forum for reporting by the Group’s

external auditors. It is the intention that these meetings will be attended, by invitation, by the Finance Director, the auditors and the CEO.

Remuneration Committee

The Remuneration Committee is responsible for recommending to the Board the remuneration of the executive Directors and the ongoing

review of the remuneration and other benefits of the executive Directors and senior executives; recommending from time to time the

introduction, variation or discontinuance of any benefits, including bonuses and share options and keeping under review the line of succession

of senior executives in the Group. The Remuneration Committee comprises all non-executive Directors.

The report on the Directors’ remuneration, which includes details of the Directors’ interests in options together with information on service

contracts, is set out on pages 32 and 33.

Relations with Shareholders

Communication with shareholders is conducted through correspondence, face to face meetings, press announcements, stock exchange

releases and Sibir’s website, www.sibirenergy.com. The Report of the Chairman and Chief Executive and the Financial Review include a

detailed summary of the business and future developments. The Board proposes to use Annual General Meetings (AGM) to communicate

with private and institutional investors, and welcomes their participation.

Internal controls

The Group has not complied with the Turnbull guidance on internal controls, and the Board believes that due to the current size of the

Company’s business it is not necessary to do so. Whilst the Company is quoted on AIM and as such is not required to comply with the

Turnbull guidance, the Directors continue to monitor and review the Group’s procedures and policies on internal control.

The Board acknowledges that it is responsible for establishing and maintaining the Group’s system of internal control, the effectiveness of

which is reviewed on a regular basis. The internal control system is designed to meet particular needs of the Group and the risks to which it is

exposed, and by its nature can provide reasonable, but not absolute, assurance against material misstatement or loss. In view of the size of the

Company, the Board does not consider that an internal audit function is required at present, however, the Board intends to keep this under

review.

The Group’s internal controls and the need for an internal audit function, are being considered in the light of the Group’s stated intention to

IPO in the second half of 2008 or the first half of 2009.

The key procedures which the Directors have established with a view to providing effective internal control are as follows:

30 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

THE WORKINGS OF THE BOARD AND ITS COMMITTEES

Management structure

The Board has overall responsibility for the Group and there is a formal schedule of matters specifically reserved for decision by the Board.

Each executive has been given responsibility for specific aspects of the Group’s affairs. The executive Directors together with the key senior

executives constitute the Executive Committee, which meets as required to discuss operational matters.

Quality and integrity of personnel

The integrity and competence of personnel is ensured through supervision and training. High quality personnel are seen as an essential part of

the control environment.

Identification of business risks

The Board is responsible for identifying the major business risks faced by the Group and for determining the appropriate course of action to

manage those risks.

Budgetary process

Each year the Board approves the annual budget. Key risk areas are identified. Performance is monitored and relevant actions taken

throughout the year through the monthly reporting to the Board of variances from the budget, updated forecasts for the year together with

information on the key risk areas.

Investment appraisal

Capital expenditure is regulated by the budgetary process and authorisation levels. For expenditure beyond specified levels, detailed written

proposals have to be submitted to the Board. Reviews are carried out after the acquisition is complete and, for some projects, during the

acquisition period, to monitor expenditure. Major overruns are investigated.

The Directors continue to monitor and review the Group’s procedures and policies on internal controls on an annual basis.

31 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

Policy

Whilst not mandatory for an AIM Company, the Directors have produced a Directors Remuneration Report. This report is not intended to

comply with the provisions of Schedule 7A to the Companies Act.

The Remuneration Committee comprises non-executive Directors only. The role of the Committee is to make recommendations to the Board

within agreed terms of reference on the Company’s framework of executive remuneration and its cost and to determine, on their behalf,

specific remuneration packages for each of the executive Directors including pension rights and any compensation payments. The Committee

also determines the overall remuneration policy for staff and reviews the recommendations of the executive Directors in respect of the annual

salary reviews of employees.

Directors remuneration packages are designed to attract, motivate and retain Directors of the quality needed and with the appropriate skills

and experience. Remuneration packages currently comprise basic salary and pension contributions. The Company has implemented a share

options scheme which it recognises as an important element of the remuneration package as employees are rewarded for their contribution to

enhancing shareholder value.

The fees of non-executive Directors are reviewed periodically to ensure that they are in line with the current practice. Changes are

recommended by the Chief Executive and approved by all executive Directors. The Company’s Articles of Association restrict non-executive

Director’s remuneration to an aggregate of $300,000 per annum or such other sum as the Company, in general meeting, shall from time to

time determine.

Annual remuneration of Executive Directors

The annual salaries and employer pension contributions contracted into by the executive Directors and the remuneration paid to the Directors

in the year ended 31 December 2007 are shown in the tables below.

Executive Director Annual Salary Pension Contributions

H O Cameron £389,000 £39,000

A Betsky £222,000 £7,000

S Detmer $600,000 $–

32 SIBIR ENERGY PLC EXPLORATION, PRODUCTION, REFINING, MARKETING

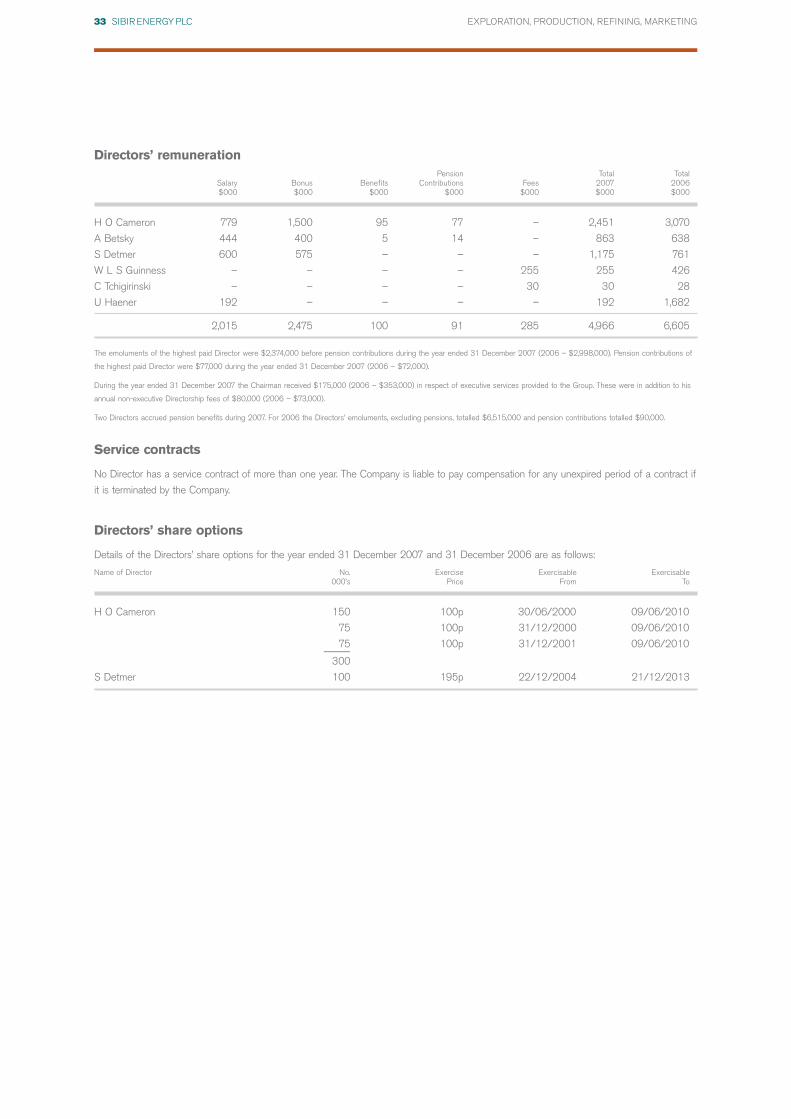

REMUNERATION REPORT

Directors’ remunerationPension Total Total

Salary Bonus Benefits Contributions Fees 2007 2006$000 $000 $000 $000 $000 $000 $000

H O Cameron 779 1,500 95 77 – 2,451 3,070

A Betsky 444 400 5 14 – 863 638

S Detmer 600 575 – – – 1,175 761

W L S Guinness – – – – 255 255 426

C Tchigirinski – – – – 30 30 28

U Haener 192 – – – – 192 1,682

2,015 2,475 100 91 285 4,966 6,605