exploiting the electromagnetic spectrum: findings and analysis · sir anthony cleaver, chairman,...

TRANSCRIPT

FORESIGHT

Exploiting the electromagnetic spectrum:Findings and analysis

OFFICE OF SCIENCE AND TECHNOLOGY

The DTI drives our ambition of ‘prosperity for all’ by working to create the best environment for business success in the UK. Wehelp people and companies becomemore productive by promotingenterprise, innovation and creativity.

We champion UK business at homeand abroad. We invest heavily inworld-class science and technology.We protect the rights of working people and consumers. And westand up for fair and open markets inthe UK, Europe and the world.

Contents

Introduction 1

Switching to light: 5

all-optical data handling

Manufacturing with light: 11

photonics at the molecular level

Inside the wavelength: 19

electromagnetics in the near field

Picturing people: 29

non-intrusive imaging

1

Project process

The scoping phase of the project, whichculminated in the selection of the four topics,was based around two workshops. The firstworkshop brought together a small group ofscientists from business and academia, andfocused on the science push. It identified around20 areas of exciting research with applicationpotential. These ranged across the wholespectrum and included technologies for: moreefficient use of the radio frequency spectrum inmobile communications; increased datacommunications capacity; better and lessintrusive sensing and imaging; and manipulatingmolecules and materials on very small scales.

The second workshop brought together a muchlarger group of business and user representativesand focused on the market pulls for thetechnologies identified by the first workshop. Thisresulted in a shortlist of nine topics where therewas felt to be both a clear market demand, andhence exploitation opportunity, and a strong UKresearch base from which to start. Four of thesewere selected against the following criteria:

• far out and innovative: major economicactivity 10–20 years hence; currently

unanswered science problems; potential forstep-change in technology

• economic significance: potential globalmarket size; UK market size

• UK ability to exploit: UK share of market; UKexport value; skills base; UK science base

• balanced topic portfolio: science-versusapplication-driven; cross-disciplinary; spreadacross spectrum; stakeholder support.

The four selected topics were:

• Switching to light: all-optical data handling

• Manufacturing with light: photonics at the

molecular level

• Inside the wavelength: electromagnetics in

the near field

• Picturing people: non-intrusive imaging

For each of these topic areas, expert actiongroups were convened to identify the technicalchallenges and business opportunities, anddevelop plans for action. Members were drawnfrom business, academia, user communities,government and other agencies. As part of thisprocess, state of the science reviews for eachtopic were commissioned from a member of theaction group, and endorsed by the rest of the

Introduction

The Foresight project on ‘Exploiting the electromagneticspectrum’ (EEMS) set out to provide a vision for the futureexploitation of the electromagnetic spectrum to ensureincreased UK innovation in selected areas. The project aimswere to identify key areas of long-term opportunity acrossthe spectrum, assess these against UK capabilities and agreea plan of action to help the UK exploit these areas. Theproject focused on four topic areas, selected through arigorous scoping process involving the academic, business,and user communities, along with representatives from othergovernment departments and funding bodies.

Findings and analysis

2

group. The reviews look at new technologicaladvances, assess their likely impacts over thenext 10–20 years and consider the UK’s relativestrengths in these areas. They are available onthe CD-ROM that accompanies the ForesightEEMS launch pack and on the project websiteat: http://www.foresight.gov.uk/emspec.html.Short and accessible overviews of the state ofthe science reviews are also available, in hardcopy and on the website.

The reviews informed the first action groupworkshops, which focused on potentialapplications and their underpinning technologies.The groups developed detailed 'technologytimelines', mapping out the intermediate stepsneeded to deliver a few exemplar applications.Streamlined versions of the key timelines areincluded in this report. Non-EEMS technologieswere sometimes highlighted in this process –for example, software for data analysis(particularly images), and advanced materialsdevelopment. In some cases, non-technologicalissues were also highlighted as key barriers toexploiting or creating markets.

Two pieces of economic work fed into a secondset of action group workshops, which focused onselecting the most promising markets andapplications for the UK to exploit, and identifyingactions to help the UK realise these opportunities.

We commissioned Professor Andrew Stark,Professor Dean Paxon, Professor David Newtonand Dr Martin Widdicks from ManchesterBusiness School to develop an easy-to-useevaluation tool to help assess potentialinvestments in research and development (R&D).This tool draws on existing real options analysis,which has come to the fore in recent years as ameans of capturing the value of the flexibilityembedded in long-term, multi-stage, R&D projectsin the presence of inevitable uncertainty. Based onwell-developed techniques used in financialmarkets to value the right, but not the obligation,to buy an asset in the future, real options analysisis gaining in acceptance as an important tool inassessing R&D proposals. The tool provides aframework to ensure that key milestones are setfor decisions on further investments and helpsmake clearer what the risks and uncertainties are.

It helps identify the scale of the upside – thepotential returns in the unlikely (but possible) eventthat success exceeds expectations. In a portfolio ofinvestments, it is these few big wins that providethe overall return. The tool allows users toexperiment in an iterative way with differentparameter values and proposal structures, andprovides analysis of the sensitivity of the value toinput parameter changes. Spin-off benefits can befactored in, if they can be quantified.

We also commissioned a market researchcompany (FreshMinds) to assess the possiblemarket sizes for the applications identified by theaction groups as offering the greatest potential.Estimating market value was particularlychallenging in some instances as there is noexisting market, and the project’s 10–20-yeartimescale is beyond that of much market data.Care should thus be exercised in any use of themarket estimates in this report.

At the second set of workshops, the actiongroups reviewed the market data and drew on itto develop their own estimates for the marketsize, the fraction capturable by the UK and theinvestment costs needed to get to market. Inmaking these estimates (best guess plus 20%upper and lower bounds), the groups consideredcompetition from other countries and othertechnologies in meeting the demand.

These figures helped inform the selection of afew key opportunities from the manypossibilities originally identified.

This document presents the main findings of theaction groups for the four selected topics.

We were greatly helped throughout the projectby Professor Will Stewart, former Chief Scientistat Marconi and the project’s expert advisor, andby Dr Rob Phaal of the Institute forManufacturing, Cambridge University, indeveloping the structure of the workshops.

The project’s sponsoring Minister, StephenTimms MP, DTI Minister for Energy, e-Commerce and Postal Services, convened astakeholder group to oversee the work of theproject. The group is actively involved in carryingforward action as a result of the project.

3

Introduction

Stakeholder group members

Dr David Clark, Director of Research andInnovation, Engineering and Physical ScienceResearch Council (EPSRC), replaced by

Professor Randal Richards, Director of Research and Innovation, EPSRC

Professor Trevor Clarkson, formerly Head of Engineering and Research,Radiocommunications Agency, now head ofExternal Research Management, Ofcom

Sir Anthony Cleaver, Chairman, MedicalResearch Council (MRC)

Anthony Dunnett, formerly Chief Executive,South-East England Development Agency(SEEDA), replaced by Professor Ed Metcalfe,Head, Science Technology Entrepreneurship andManagement, Learning and Skills, SEEDA

Martin Earwicker, Chief Executive, Defence,Science and Technology Laboratory (DSTL)

Dr Peter Greenaway, Assistant Director ofResearch and Development, Department of Health

Dr Hermann Hauser, Director, Amadeus Capital Partners Ltd

Professor Richard Holdaway, Director of SpaceScience and Technology, Council for the CentralLaboratory of the Research Council (CCLRC)Rutherford Appleton Laboratory

David Hughes, DTI Director General InnovationGroup, project director

Peter Ingram, formerly Chief Technical Officer BT Retail, now Chief Technical Officer Ofcom,replaced by

Professor William Webb, Head of Research andDevelopment, Ofcom

Dr Andrew Rickman, Chief Executive, Bookham Technology plc

Professor Michael Walker, Group Research andDevelopment Director, Vodafone Group

Professor Colin Webb, Founder, Oxford Lasers Ltd

5

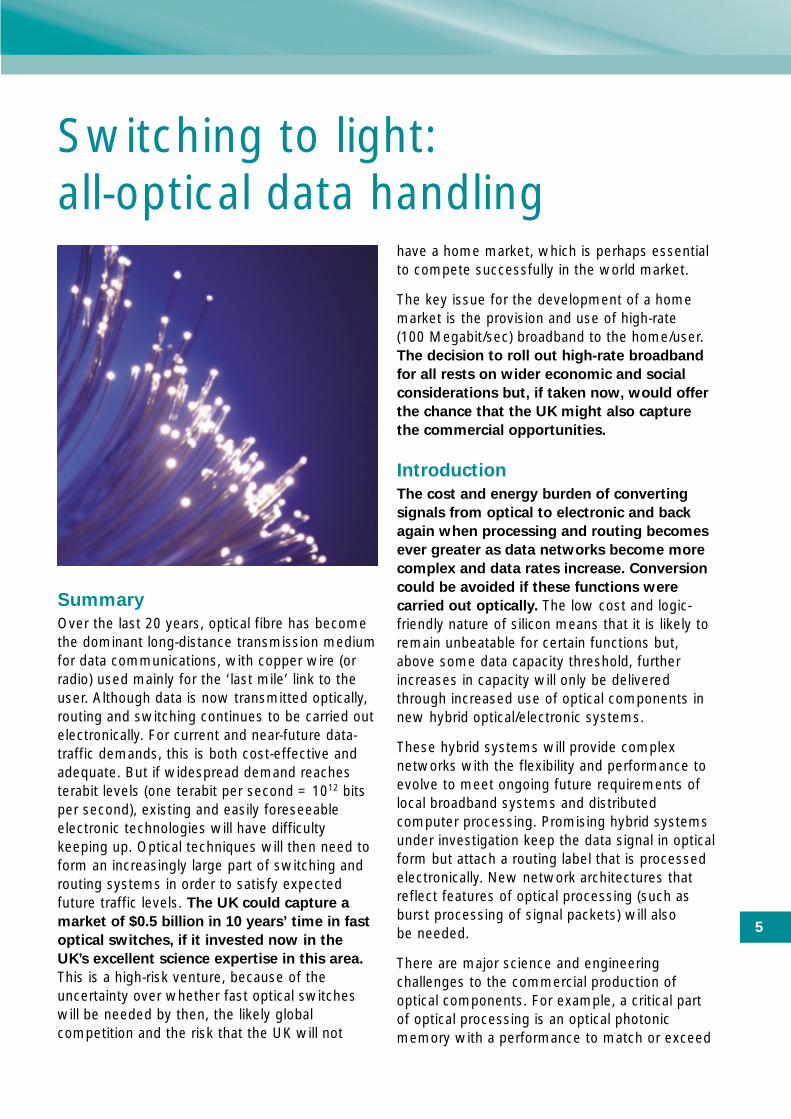

Switching to light: all-optical data handling

Summary

Over the last 20 years, optical fibre has becomethe dominant long-distance transmission mediumfor data communications, with copper wire (orradio) used mainly for the ‘last mile’ link to theuser. Although data is now transmitted optically,routing and switching continues to be carried outelectronically. For current and near-future data-traffic demands, this is both cost-effective andadequate. But if widespread demand reachesterabit levels (one terabit per second = 1012 bitsper second), existing and easily foreseeableelectronic technologies will have difficultykeeping up. Optical techniques will then need toform an increasingly large part of switching androuting systems in order to satisfy expectedfuture traffic levels. The UK could capture a

market of $0.5 billion in 10 years’ time in fast

optical switches, if it invested now in the

UK’s excellent science expertise in this area.

This is a high-risk venture, because of theuncertainty over whether fast optical switcheswill be needed by then, the likely globalcompetition and the risk that the UK will not

have a home market, which is perhaps essentialto compete successfully in the world market.

The key issue for the development of a homemarket is the provision and use of high-rate (100 Megabit/sec) broadband to the home/user. The decision to roll out high-rate broadband

for all rests on wider economic and social

considerations but, if taken now, would offer

the chance that the UK might also capture

the commercial opportunities.

Introduction

The cost and energy burden of converting

signals from optical to electronic and back

again when processing and routing becomes

ever greater as data networks become more

complex and data rates increase. Conversion

could be avoided if these functions were

carried out optically. The low cost and logic-friendly nature of silicon means that it is likely toremain unbeatable for certain functions but,above some data capacity threshold, furtherincreases in capacity will only be deliveredthrough increased use of optical components innew hybrid optical/electronic systems.

These hybrid systems will provide complexnetworks with the flexibility and performance toevolve to meet ongoing future requirements oflocal broadband systems and distributedcomputer processing. Promising hybrid systemsunder investigation keep the data signal in opticalform but attach a routing label that is processedelectronically. New network architectures thatreflect features of optical processing (such asburst processing of signal packets) will also be needed.

There are major science and engineeringchallenges to the commercial production ofoptical components. For example, a critical partof optical processing is an optical photonicmemory with a performance to match or exceed

6

that of the ubiquitous electronic RAM (randomaccess memory). At present there is no methodof storing and reading out data optically althougha variety of methods are under investigation.

Other techniques that could enable fast opticalswitching, including nonlinear optics and fasttuneable lasers, are also advancing rapidly.Photonic bandgap structures which cancompress light into very small spaces, makingdevices much more efficient (and potentiallylower cost), appear particularly promising.

Key drivers

For there to be a market for fast optical

switches, the action group agreed that

demand for data transmission rates would

need to reach terabit level in the network.

Such demand would be generated by a‘knowledge economy’ where value is placed onfast access to increasing amounts of globallyaccessible information. If the future is movingtowards a world of remote working – andplaying – in the widest sense of connecting in adata-rich way with experts or databases at adistance, the capability of existing technologiesto deliver the necessary information to the rightplace in an acceptable time will be put underincreasing strain.

New data is currently being generated at a rateof 2 exabytes (2 million terabytes) per year (250 megabytes for every person on earth).Companies rely ever more heavily oncomputerised records, and legal obligations tokeep data are growing. Increasing personal useof information technology is likely to lead to agrowth in demand for consumer data backupfacilities. Stored information is useless withoutrapid access for all who need it.

In addition to the corporate knowledge economy,there are other data-transmission-intensivemarkets, particularly ones such as video andtelepresence involving images, which might drivenetwork demand to terabit levels. These include:multimedia consumer gaming and video-on-demand; remote management of disasters byexperts; comprehensive security systems; andfully integrated electronic patient records.

It is difficult to estimate how fast demand isgrowing, and thus when it might reach terabitlevel, but most estimates are in line with therecent comments of Eric Mentzer, Intel’s Vice-President and Chief Technology Officer:

‘[Broadband and new multimedia

applications] are going to continue to

drive bandwidth on the optical

backbone… The net result of all this is

incredible growth in the Internet. What

is our network going to need to scale

to? It will be about a thousand times. If

it keeps up with this, which we think it

will, we'll need a network that can carry

a thousand times as much traffic ten

years from now.1’

Current capacity to broadband-equipped homesin the UK is ~1 Mb/sec (one megabit is 106 bits).A thousandfold increase takes this to 1 Gb/sec(one gigabit = 109 bits), which corresponds todata rates of hundreds of terabits in the networkbackbone. A more cautious estimate of 100 Mb/sec to the home in ten years would still imply the need for fast optical switching.

Although global markets for fast optical

switching technology could exist without

there being a UK home market, a home

market is probably essential if the UK is to

build an industry in this area. Growth indemand in the UK is presently hampered by alack of broadband capacity, and without access,demand cannot grow. This barrier is principallyeconomic: the cost of providing fibre to thehome to around 95% of the population isestimated at £10–20 billion. The current open-access-to-infrastructure regulatory framework inthe UK reduces the incentive for individualcompanies to invest in infrastructure. Whilstconsumers may be prepared to pay forinfrastructure if there are ‘must have’applications they desire, this is unlikely to createnetwork-wide demand fast, and is alsosomething of a chicken and egg situation. Aworkable business model to support investmentis needed. Japan is currently rolling out a 100 Mb/sec subscription service, but costs percapita would be much higher in the UK (due tolower population densities and underground

1 Eric Mentzer, Optical Fiber Conference 2003

7

Switching to light: all-optical data handling

Table 1. Market estimates for fast optical switches

Investment costs – three R&D phases plus one-off pre-production costs

installation of fibres – the Japanese are installingthem above ground).

The group’s assessment was that a public policyinitiative would probably be required to bringhigh-rate broadband to the home. This could takethe form of regulatory changes to allowbusinesses to keep control of their owninvestment in infrastructure, or to makeinstallation compulsory in new buildings. Whilst

wider social and economic considerations are

likely to be the primary motivation for a high-

rate broadband initiative, a clear and early

decision would allow the possibility that the

UK might also benefit commercially as well.

Markets and applications

Delivering terabit-level data rates will require fastoptical switching and routing systems. Ratherthan replacing existing electronics systems withall-optical ones, the new systems are likely to behybrid, with optics fulfilling the requirementsthat electronics will not be able to meet. Themain application areas identified for the use ofoptical technologies within the network were:

• storage area networks

• GRID equipment

• computer interconnects.

These would provide the network infrastructurefor high-capacity connections to storage, and fastretrieval and processing of data in distributeddatabases. Off-site data storing needs to be easy

for the user, fast and secure, and allow for largespikes in demand (such as end-of-the-day backingup). To be most efficient, the network needs tobe dynamic, user-defined/controlled and fullyintegrated. Rather than the route a signal takesbeing assigned by the network operator, the routewould be decided by the user. There are manyissues of data privacy, legal and industrystandards, copyright and protocols to be defined.Industry standards, which could have importantknock-on effects, are likely to be determined bythe main players. To have a say in establishingstandards the UK needs to be part of this newindustry. It is likely that new business models forselling services will evolve to reflect the featuresthat the customer regards as most valuable.

The action group’s ‘best guess’ estimate for thevalue of the global market for fast opticalswitches in 8–10 years’ time was $16 billion.They thought that the UK could capture a shareworth $0.5 billion (see Table 1). An investment ofaround $15 million is required for the initial 5-yearresearch phase, which would result in a packagedprototype switch with a demonstrated route toscaling the port count (with passive assembly).The milestones for the short second and thirdphases would be, respectively: developing arepeatable process for fab/packaging large portcount switches with initial reliability testing; andfully qualifying this process, adding electricalinterfaces, automated assembly and customersampling. The total time to market was estimatedat 8.5 years.

Phase 1 Phase 2 Phase 3 Pre- Total Value of World UK shareInitial (duration) (duration) production investment UK share marketinvestment (duration) cost (total of market(duration) duration)

Best guess $15 million $20 million $30 million $150 million $215 million $0.5 billion $16 billion 3%of UK (5 years) (1 year) (1 year) (1.5 years) (8.5 years)market size

Optimistic $32 billion $160 billion 20%market size(20% likelihood)

8

The group’s optimistic estimate (20% chance) ofthe value to the UK was $32 billion. The verylarge spread in value reflects the highly uncertainnature of this investment, which would involvesetting up new robotised production methodsand competing against the US and others whoare already investing heavily in the basictechnologies. The UK is, however, well placed interms of photonic and system expertise, andmany of the underlying technologies will havespin-off applications to provide revenue streamalong the way. The high degree of uncertainty,

together with the small initial investment

costs make this an attractive option since the

cost of ‘staying in the game’ is low compared

to the potential returns, and the major

investment costs are those of pre-production,

which may be deferred until later.

On a longer timescale (beyond 15 years), thegroup considered that niche applications takingadvantage of specific optical properties mightemerge outside the communications sector. Forexample, optical pattern recognition techniquesfor reading data labels could find wider use inpattern matching. In the even longer term, thegroup noted that storage, rather than access,may become the bottleneck, although solutionsto this are unlikely to be optical.

Technologies

At the heart of the anticipated optical

hybrid network would be fast (below

10 nanoseconds) optical switches, initially in

100 x 100 port count arrays. In these switches,light would act directly and efficiently on otheroptical signals, routing them without the needfor an electronic intermediary. To do so requiresvarious combinations of:

• wavelength-agile components, using cheaptuneable lasers so that signals can beswitched by changing their wavelength

• hybrid integrated, scaleable component arraysfor space switching

• optical buffer memory to store signals for bit-level switching, likely to involve using photonicbandgap structures in the future

• multi-wavelength optical regenerationcomponents to restore degraded signalstrengths

• scaleable Optical-Electronic-Optical (OEO)edge routers to handle the interface betweenoptical and electronic processing.

These components will need to be power-efficient, scaleable and low cost. Theirdevelopment will depend on more genericintegrated photonic platform technologies,dense integrated optics and materials with veryhigh nonlinearities. Cheap compact tuneableshort pulse lasers are also essential.

Other important issues include developingfuture-proofed (dynamically reconfigurable)network architectures to play to the strengths ofthe new switching technologies.

In addition to the unanswered basic researchquestions, there are significant new production-advancement requirements, including:

• high-yield reliability monitored fab/automatedproduction of switch arrays

• uncooled optoelectronic components, withthermal management of the arrays

• development of a cost-effective hybridintegration platform for photonics andelectronics

• protocols and standards (quality control).

9

Switching to light: all-optical data handling

NO

W5

ye

ars

10

ye

ars

15

ye

ars

TechnologiesApplicationsDrivers

OR

wir

eles

s/R

F

Dev

elo

pm

ent o

f exi

stin

g

(tel

eco

m) t

ech

no

log

ies:

Ho

me

ente

rtai

nm

ent

gam

ing

/vid

eo T

VG

row

th in

'kn

ow

led

ge

eco

no

my'

,co

mm

erci

al d

ata

sto

rag

e an

d a

cces

sD

isas

ter

man

agem

ent

Op

tica

l pat

tern

mat

chin

g

~10

p s

ecs

Wav

elen

gth

cir

cuit

switc

hes

Op

tical

bu

rst s

witc

hes

Low

-co

st O

EO

All-

op

tical

net

wo

rk

man

agem

ent

Mes

h c

on

nec

tivity

@ 2

0 T

b/s

ec/n

od

e20

0 n

od

es

Op

tical

net

wo

rks

(sec

on

d g

ener

atio

n)

Wav

elen

gth

co

nve

rsio

n

for

op

tical

cir

cuit

switc

hin

gO

ptic

al a

mp

lifie

rs

Inn

ova

tive

use

of

exis

ting

infr

astr

uct

ure

–c

able

/du

ct

Op

tical

net

wo

rks

(fir

st g

ener

atio

n)

Op

tical re

gen

era

tio

n

- M

ult

i w

avele

ng

th

- S

cale

ab

le

New

(n

on

-tele

co

m)

tech

no

log

ies f

or

>40 G

b/s

ec b

ackp

lan

e

Op

tical

bu

ffer

m

emo

ry

Ag

gre

gat

ion

(n

on

-tel

eco

m)

Wild

card

tech

no

log

ies

to r

edu

ce

cost

of f

ibre

to th

e h

om

e

3D o

ptic

al d

evis

es

Ag

ile c

om

po

nen

ts

Data

co

mp

ressio

n

New

app

licat

ion

s

Sec

uri

ty –

pri

vate

net

wo

rks?

Ch

eap

saf

e lo

w p

ow

er

Tele

pre

sen

ce

Fast

scale

ab

le

op

tical sw

itch

<10 n

an

osecs

Po

rt c

ou

nt

100 x

100

Need

to

sta

rt o

n f

ast

op

tical sw

itch

so

on

1 M

b/s

ec1

Gb

/sec

Gro

win

g r

esid

enti

al b

road

ban

d c

apac

ity

2.3

Gb

/sec

100

Gb

/sec

40 G

b/s

ec

Gro

win

g n

etw

ork

cap

acit

y

1 T

b/s

ec

Op

tical

qu

ality

of

serv

ice

mo

nito

rin

gLe

gac

y in

teg

ratio

n

Use

ph

oto

nic

b

and

gap

?

Ch

eap

tun

eab

le

lase

rsH

igh

ly n

on

linea

r m

ater

ials

Fib

res

to a

llh

om

es/o

ffic

es. C

ost

£10–

20 b

illio

n to

last

3 k

mO

EO

ed

ge

rou

ter

• S

cale

abili

ty t

o 2

00 T

b/s

ec•

100-

no

de

net

wo

rk (

or,

5,00

0 n

od

es (

as U

K

to

day

) +

4 T

b/s

ec r

ou

ters

)

WD

M•

Tun

eab

le s

ou

rces

• S

witc

hes

– M

EM

S

Free

-sp

ace

op

tics

Twis

ted

pai

r 2

Mb

/sec

(DS

L)C

o-a

x to

10

Mb

/sec

Fib

re to

the

curb

/bas

est

atio

n c

ost

<£1

0 b

illio

n

Au

tom

ated

as

sem

bly

etc

ST

OR

AG

E A

RE

A N

ET

WO

RK

SG

RID

NE

TW

OR

KIN

G

CO

MP

UT

ER

INT

ER

CO

NN

EC

TS

•1,0

00 p

roce

ssin

g n

od

es, 4

0 –

100x

ed

ge

den

sity

Key

net

wo

rk s

ervi

ces

Reg

ula

tory

issu

es,

pro

toco

ls, l

egal

an

d

net

wo

rk s

tan

dar

ds

Un

iver

sal s

ervi

ceE

qu

alit

y o

f ac

cess

Dat

a p

riva

cy

US

Do

E

fun

din

g p

rog

ram

me

Figure 1. All-optical data handling: technology timeline for fast optical switches (key steps shown in orange)

10

The way forward

If demand for network data transfer rates

were to reach terabit levels, it would exceed

the capabilities of existing switching and

routing technology. The UK is well placed to

develop fast optical switching technologies to

meet this need. The UK might capture a shareof the global market of between $0.5 billion and$32 billion. There are a number of issues to beconsidered:

• the uncertainty as to whether or when fastoptical switches will be needed

• the risk that the UK will not have a homemarket, which is perhaps essential to competesuccessfully in the world market

• the likely global competition.

The key steps to help the UK maintain its

lead in the science in this area and keep open

the option for further investment at a later

stage to capture a share of the market,

should the demand arise, are:

• a co-ordinated and visionary strategy by

the photonics community

• an initial investment of around $20 million in

R&D, to support existing UK centres of

research excellence in integrated photonics

technology. Research should be industry-led

to leverage this investment effectively

• a commitment to high-bandwidth

broadband rollout.

Since many of the underpinning technologies(for example, cheap tuneable lasers and cost-effective hybrid integration platforms) will haveextensive use in other applications and markets,activity should probably form part of a nationalphotonics roadmap providing a strategy forphotonics both in and outside of thecommunications sector (that is, combining withthe ‘Manufacturing with light: photonics at themolecular level’ topic recommendations).

This opportunity, among others, will be

considered by the DTI Electronics team’s

newly formed Photonics Strategy Group,

which will identify opportunities and

challenges for the UK over the next 5–10

years and develop an action plan to exploit

the sector. The team is also working to bring

together key players to start a national

Photonics network along the lines of the

successful Fuel Cells initiative.

Photonics has also been identified as a

potential priority area for a Call in 2004/05

under the new DTI Technology Strategy.

Acknowledgements

We would like to thank all members of theaction group who gave so generously of theirtime and expertise.

Ron Ballingall, DSTL

Dr Peter Batchelor, DTI

Professor Polina Bayvel, University College London

Dr Andy Carter, Bookham Technology plc

Dr Russell Davey, BT

Dr Michael Dueser, University College London

Steve Ferguson, Marconi

Dr Patrick Gill, National Physical Laboratory (NPL)

Professor Michael O’Mahoney, University ofEssex

Vince Osgood, EPSRC

Professor David Payne, Southampton University

Dr Alistair Poustie, Centre for IntegratedPhotonics

Ian Williams, DTI

State of the science review authors: ProfessorPolina Bayvel, Dr Michael Dueser and ProfessorJohn Midwinter, University College London.

11

Manufacturing with light:photonics at the molecular level

Summary

Lasers have long been used for precisionmachining but as control becomes ever finer andfaster, light now offers the ability to manipulatematter on a molecular scale.

Laser micromachining in three dimensions

offers many manufacturing opportunities,such as the fabrication of microstructuredmaterials for next-generation solar cells, smartfibres, photonic crystals and photonic lab-on-a-chip devices.

The UK could capture a $5 billion market in

integrated lab-on-a-chip systems, as a

platform technology for a number of

multi-diagnostic applications, including

diabetes treatment, health monitoring,

drug targeting and cancer detection. In thelonger term, this could lead to therapeuticapplications, though these require an order ofmagnitude more investment in regulatory trials.Extrapolating the historical market growth rateand current size, this lab-on-a-chip market couldbe $100 billion by 2012. Capturing a niche of

even 5% of this is a significant opportunity thatthe UK is in a strong research position toaddress. These applications tend to have high

capital costs of setting up production, but

the potentially huge markets mean that the

relatively low initial research investment

costs are an attractive, if risky, proposition.

Introduction

More and more new developments in

microelectronics, integration and micro- and

nano-technologies require three-dimensional

structures, often made from materials that

are difficult to work with. Laser machining isadaptable to a wide range of materials and issurprisingly gentle (able to cut soft and biological materials without damage) so will play an important part in the production of these microstructures.

Large-scale precision machining did not formpart of the scope of this topic, and the actiongroup identified two broad areas for the focus oftheir work.

Micro and nano fabrication techniques nowbeing demonstrated in research laboratoriescould, if commercialised, produce the kinds ofmultiple-material microstructures needed for awide range of applications including next-generation solar cells, smart fabric, intelligentfibres (sensors) and photonic crystals. Aparticularly promising application is thefabrication of an advanced lab-on-a-chip (LoC).

Integrated photonic LoC will, in addition tobeing fabricated using photonic and lasertechnologies, also rely on them for its functionalcapabilities. Current LoC devices are mainlypassive microarrays of up to tens of thousandsof test sites at which are located specificmolecules or chemicals that test for a particularfunction. DNA chips, in which the testmolecules identify particular genetic sequences,

12

are the most common, but protein arrays arealso an important market.

An integrated photonic LoC would actively sortmolecules or particles using arrays of lasers(‘optical tweezers’) to push different moleculesin different directions as they flow through the‘optical lattice’ created by the laser beams.Preliminary experiments have shownpossibilities here and exciting newdevelopments in lasers and photonics offer theprospect of integrating many other specificfunctions on a single chip to offer multi-diagnostic capability in the future.

Key drivers

The market drivers for specific applications oflaser/photonic micromachining are diverse. Withincreasing pressure on global energy resources,improved energy efficiency (particularly, thoughnot exclusively, for portable devices) is set tobecome an ever more important considerationacross the board. Cost reduction andminiaturisation/portability are common drivers inmanufacturing, which are bolstered by trendstowards increasing personalisation of servicedelivery. They can also drive the opening up ofnew markets and ‘throw-away’ applications.Demand for environmental monitoring is rising:comprehensive surveillance of pollution ornatural resources requires small cheap low-maintenance sensors.

The overarching long-term driver for LoC

applications is healthcare and the rising

expectations of ageing but affluent societies

prepared to pay for the best available care.

Fast, efficient multi-diagnostic tests are an

essential part of evidence-based diagnostics.

They improve prevention, detection andtreatment of disease, and the matching oftreatments to the specific needs of individualpatients.

In recent years, it has become increasingly clearthat genetics affects not only predisposition todisease but also the efficacy of currentgeneration drugs. As Dr Allen Roses ofGlaxoSmithKline recently acknowledged, asmany as 90% of prescription drugs work in only

30–50% of the population. Despite thesignificant ethical issues surrounding genetictesting, the benefits in terms of preventativeand prescriptive treatments are likely to prevailand lead in the long term to the individualtailoring of drugs. This science ofpharmacogenomics offers the prospect of farbetter-targeted and efficient prescribing,screening patients both for the most appropriatedrug and for those likely to cause them adversereaction. Greater prescribing efficiency alsopromises large potential savings on drugspending, although whether this would lead toany reduction in overall spend is unclear (thesavings may simply be used to make moreexpensive drugs available to more people). Indue course this could lead to highly personalised‘chip therapy’, but because of the considerableregulatory hurdles faced by new therapeutics,the action group felt that over the next 10–20years the driver for LoC in healthcare would bediagnostic rather than therapeutic.

In the shorter term, and covering the periodwhere any new healthcare diagnostic would berequired to undergo trials, photonic LoCtechnology offers the prospect of meetingdemand for more efficient development of newpharmaceutical drugs (where the discovery cyclecurrently takes 10–15 years). It is also likely toprovide better research tools across a range ofbiosciences, including exciting areas of researchsuch as genomics and proteomics.

The growing demands for many types ofenvironmental monitoring – pollution, foodtoxins, chemical hazards – may provide a marketfor chemical use of LoC technology. There are,however, many competing technologies in thesesectors, so chemical uses are unlikely to be themain drivers for development (at present,virtually all uses of LoC are biological, so muchso that the term ‘biochip’ is used almostsynonymously).

Markets and applications

Micro and nano fabrication

Micro and nano scale fabrication methods willhave a wide range of applications. The action

13

Manufacturing with light: photonics at the molecular level

group considered in detail the market for three-

dimensional microstructured materials fornext-generation solar cells, low-intelligencemicrofibres for distributed sensing (of theenvironment, fire, biohazards), fabrics and paintsfor camouflage. The photovoltaic solar cellmarket is currently dominated by Japan, whoaccount for 70% of the manufacturing capacityin a market with significant overcapacity atpresent, although this is likely to change as useof fossil fuels becomes more expensive.

The group estimated that the UK might

capture 20% ($2 billion) of a market worth

$10 billion in 12 years’ time, for a total

investment of $580 million. They estimatedthat there was a 20% chance of the marketbeing $30 billion and the UK capturing 25% of it.The goals of the three phases of research weredefined as: (1) a scaleable manufacturingtechnology for making smart fabric and solarcells from a single material; (2) the same outputbut made from a number of materials bondedtogether (junctions between different materialsis a particular issue); (3) development ofpackaging, integration and prototyping. Thephased stages of the investment costs makethis a reasonably appealing proposal.

The group also considered the smaller marketfor the fabrication of application-specific

polymers produced in a minifab foundry, andthe litho tooling market – making themanufacturing tools rather than the end, userdevices. At present the principal known

application for these tools is display screenmanufacture. The key research phases hereinvolve developing reconfigurable masks usingspatial light modulators, and developing newresist materials in three dimensions, to achieveetching of giga-pixel resolution, but the highinvestment costs make this less suitable for UK exploitation.

Integrated photonic LoC

The short-term market for photonic LoC will bein research and development laboratories,enabling high-throughput precision-controlledsynthesis of chemicals and biochemicals forbiological purposes, and sorting and selection ofparticles and molecules. This market is a high-end, high-cost, low-volume one, in contrast tothe slightly longer-term healthcare diagnosticmarket, where the cost of a test will need to becomparable with the cost of a prescription. Key

target applications for diagnosis include

diabetes, drug targeting, cancer detection

and health monitoring (both of potentially

threatening conditions such as heart

problems and of ‘wellness’ functioning in

performance sports). Early applications wouldbe single diagnosis, with multi-diagnosticfunctionality and improvements in devicemobility following at a later stage.

The action group drew on the data supplied byFreshMinds and their own knowledge of thecurrent prescription market (there are currently10 billion prescriptions annually worldwide at acost of $1–50) to estimate the size of the

Table 2. Market estimates for three-dimensional microstructured materials

Investment costs – three R&D phases plus one-off pre-production costs

Phase 1 Phase 2 Phase 3 Pre- Total Value of World UK shareInitial (duration) (duration) production investment UK share marketinvestment (duration) cost (total of market(duration) duration)

Best guess $100 million $80 million $200 million $200 million $580 million $2 billion $10 billion 20%of UK (4 years) (3 years) (3 years) (2 years) (12 years)market size

Optimistic $7.5 billion $30 billion 25%market size(20% likelihood)

14

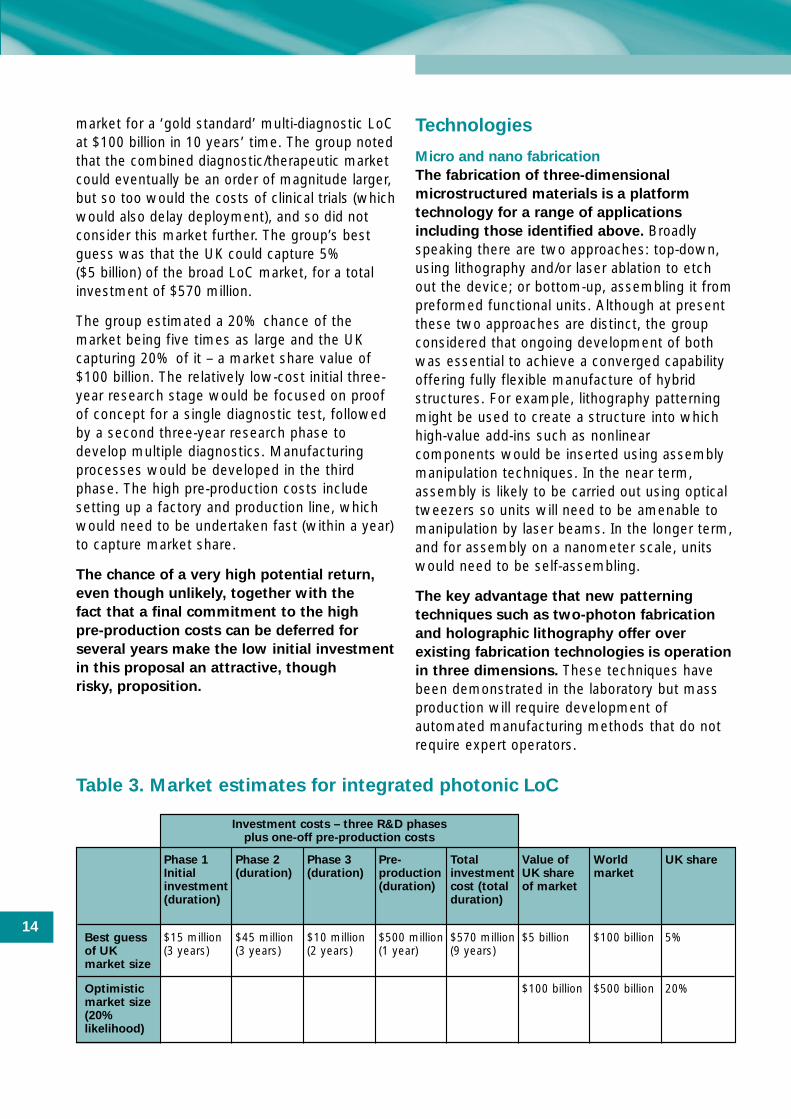

Table 3. Market estimates for integrated photonic LoC

Investment costs – three R&D phases plus one-off pre-production costs

Phase 1 Phase 2 Phase 3 Pre- Total Value of World UK shareInitial (duration) (duration) production investment UK share marketinvestment (duration) cost (total of market(duration) duration)

Best guess $15 million $45 million $10 million $500 million $570 million $5 billion $100 billion 5%of UK (3 years) (3 years) (2 years) (1 year) (9 years)market size

Optimistic $100 billion $500 billion 20%market size(20% likelihood)

market for a ‘gold standard’ multi-diagnostic LoCat $100 billion in 10 years’ time. The group notedthat the combined diagnostic/therapeutic marketcould eventually be an order of magnitude larger,but so too would the costs of clinical trials (whichwould also delay deployment), and so did notconsider this market further. The group’s bestguess was that the UK could capture 5% ($5 billion) of the broad LoC market, for a totalinvestment of $570 million.

The group estimated a 20% chance of themarket being five times as large and the UKcapturing 20% of it – a market share value of$100 billion. The relatively low-cost initial three-year research stage would be focused on proofof concept for a single diagnostic test, followedby a second three-year research phase todevelop multiple diagnostics. Manufacturingprocesses would be developed in the thirdphase. The high pre-production costs includesetting up a factory and production line, whichwould need to be undertaken fast (within a year)to capture market share.

The chance of a very high potential return,

even though unlikely, together with the

fact that a final commitment to the high

pre-production costs can be deferred for

several years make the low initial investment

in this proposal an attractive, though

risky, proposition.

Technologies

Micro and nano fabrication

The fabrication of three-dimensional

microstructured materials is a platform

technology for a range of applications

including those identified above. Broadlyspeaking there are two approaches: top-down,using lithography and/or laser ablation to etchout the device; or bottom-up, assembling it frompreformed functional units. Although at presentthese two approaches are distinct, the groupconsidered that ongoing development of bothwas essential to achieve a converged capabilityoffering fully flexible manufacture of hybridstructures. For example, lithography patterningmight be used to create a structure into whichhigh-value add-ins such as nonlinearcomponents would be inserted using assemblymanipulation techniques. In the near term,assembly is likely to be carried out using opticaltweezers so units will need to be amenable tomanipulation by laser beams. In the longer term,and for assembly on a nanometer scale, unitswould need to be self-assembling.

The key advantage that new patterning

techniques such as two-photon fabrication

and holographic lithography offer over

existing fabrication technologies is operation

in three dimensions. These techniques havebeen demonstrated in the laboratory but massproduction will require development ofautomated manufacturing methods that do notrequire expert operators.

15

Manufacturing with light: photonics at the molecular level

NO

W5

ye

ars

10

ye

ars

15

ye

ars

TechnologiesApplications

Mic

ro s

yste

ms

(op

tica

l, el

ectr

on

ic,

mic

rofl

uid

ic):

h

ybri

d s

yste

m o

n c

hip

Inte

gra

ted

o

pti

cal

circ

uit

Op

tica

l sw

itch

b

ased

on

3D

ph

oto

nic

cr

ysta

l

Low

-co

st, s

imp

le

to u

se, d

eep

U

V la

ser

sou

rces

; co

ntr

ol

Pre

fab

ricati

on

of

fun

cti

on

al b

locks

– s

elf

-assem

bly

?

Gu

ided

ass

emb

ly o

f (p

oss

ibly

sel

f-as

sem

ble

d) s

ub

un

its

Patt

ern

ab

le f

un

cti

on

al

mate

rials

Co

ntr

ol an

d

inte

gra

tio

n o

f syste

m

su

bfu

ncti

on

s f

or

hig

h v

olu

me, lo

w c

ost

Low

-in

telli

gen

ce,

low

-co

st:

• in

telli

gen

t fi

bre

s•

inte

llig

ent

pai

nts

Op

tica

l dir

ectl

y w

ritt

enm

icro

elec

tro

nic

s(p

rog

ram

mab

le)

Sta

rt

dev

elo

pm

ent

On

go

ing

dev

elo

pm

ent

FAR

FU

TU

RE

Lab

-on

-a-c

hip

:•

com

ple

x •

incl

ud

ing

val

ves

etc

• m

ult

iple

-mat

eria

ls

• 3D

arc

hit

ectu

re

All

3D in

la

bs

no

w

Pu

blic

per

cep

tio

n

of

nan

ote

ch

Op

tica

l or

chem

ical

?

Pro

cess

mo

nit

ori

ng

an

d c

on

tro

l

Sta

nd

ard

s

Hig

h-e

ffic

ien

cy

sola

r ce

lls

Inco

rpo

rati

on

of

fun

cti

on

al/

pre

fab

co

mp

on

en

ts in

to

3D

fra

mew

ork

Mic

ron

lith

og

rap

hy:

• d

eep

UV

• ~

200

nm

sca

le

• si

lico

n

Two

ph

oto

n

mic

ro fa

bri

catio

n

Rap

id

pro

toty

pin

gH

olo

gra

ph

ic

lith

og

rap

hy

New

fu

nct

ion

al

mat

eria

ls

Pat

tern

able

m

ater

ials

Two

-ph

oto

n

par

elle

lise

Mo

lecu

lar

reco

gn

itio

n

~nm

sca

le

Red

uce

co

st –

elim

inat

e n

eed

fo

r P

hD

to

op

erat

e

Mo

vin

g f

rom

vi

sib

le t

o n

ear

UV

sc

ale

(~10

0 n

m t

o 1

nm

)

Sca

le u

p t

o

larg

e vo

lum

es

at lo

w c

ost

Op

tica

l co

ntr

ol o

f ad

hes

ion

an

d

linka

ges

Par

alle

lism

of

twee

zers

– a

rray

la

sers

fo

r sp

eed

Fib

re r

esp

on

ds

to e

nvi

ron

men

t,

can

act

as

a se

nso

r o

r ac

tiva

tor

All

blo

cks

nee

d

to b

e 't

wee

zer

co

mp

atib

le'

Lase

r ab

latio

n:

• m

etal

s •

pla

stic

s•

cera

mic

s •

1 m

icro

n s

cale

Des

ign

of

fun

ctio

nal

b

lock

s an

do

vera

ll sy

stem

ar

chite

ctu

re

Man

ufa

ctu

rin

g

too

l d

evel

op

men

t

Mu

ltib

eam

para

llelise

Figure 2. Photonics at the molecular level: technology timeline for micro and nano fabrication(key steps shown in orange)

16

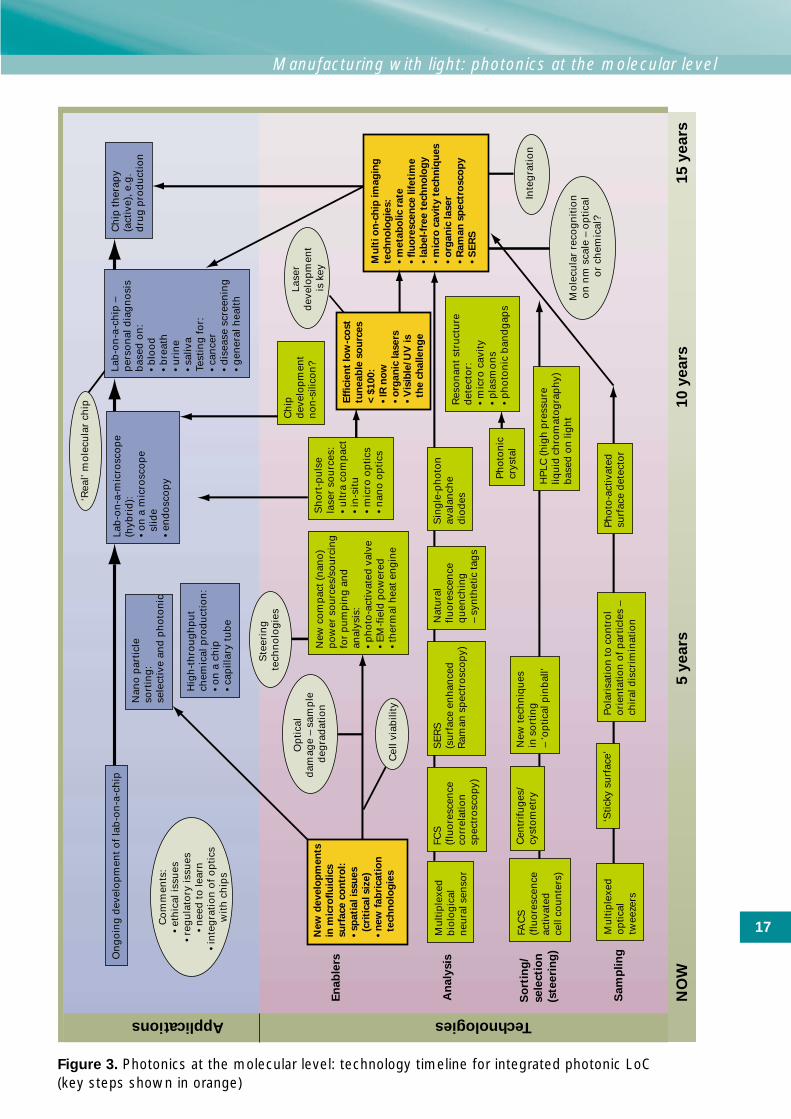

Critical issues include:

• multibeam parellisation – to deliver high-throughput speed in both patterning andassembly

• integration of functional prefabricatedcomponents into a three-dimensional structure

• patternable materials development: inparticular addressing the problem of junctionsbetween different types of base materials forstructures made of multiple materials

• high-volume, low-cost manufacturing controland integration processes.

Integrated photonic LoC

At present manipulation and selection in LoCsrelies on a limited range of physical andelectromigration effects (although the data outputis often optical). In the proposed photonic LoC thelight is used for new, more specific, diagnostics atsingle-molecule level, and for sensitive nonlineartechniques (requiring confinement of the light andvery short pulses). Light is also used for directselective manipulation using optical tweezer field-gradient effects.

Key elements of any LoC device are:

• sampling

• sorting/selection

• analysis

• ‘enabling’ functionality.

There are a number of alternative techniquesthat might deliver the first three of these. Manyinvolve near field effects, so there is someoverlap here with the ‘Inside the wavelength:electromagnetics in the near field’ topic. Adevelopment path may only need one of eachrather than all the options shown on thetechnology timeline. The critical technologies

are some of the ‘enabling’ ones:

• microfluidics: surface control, fabrication,

and spatial resolution

• laser sources: low-cost tuneable

lasers especially at visible and

ultraviolet frequencies

• detection: on-chip imaging, probably

integrating a number of modalities.

Integration of fluidics and optics into hybridchips is crucial, as is materials development. Tobe of use, test results will need interpreting:research will be needed to build up a databankof responses to enable this to be automated,especially in widespread low-end applicationssuch as health testing. The action groupenvisaged the degree of subjectiveinterpretation required falling off quite steeplywith time, with ease of use growing moreslowly (and costs falling). As with all data-intensive applications, software development forboth analysis and user interfaces is important.

Key technologies for both micro and nano

fabrication and integrated photonic LoC are

cheap compact lasers with total beam

control (shaping, pulses, tuning).

The way forward

The UK could reap rich rewards in the two

broad areas of:

• laser micromachining, driven by demands

for ever-smaller and cheaper devices

• integrated photonic lab-on-a-chip (LoC),

driven by demands for cheap multi-

diagnostics particularly but not solely

in healthcare.

The combined potential rewards for the UK fromthese areas could be around $7 billion. Themarket size for the integrated photonic LoC isvery uncertain, but offers a small chance of veryhigh returns. To seize these opportunities, anambitious visionary target is needed; withmarkets being so young we should not be overlyconstrained by the current industry position.

The UK has a strong science base in this area

and for a relatively small initial investment

could maintain this position and keep its

options open with respect to these markets,

both of which would require more substantial

investment at the later stages of R&D and

pre-production.

In addition to the two areas identified above,there is a wide range of potential uses of theunderpinning technologies in other applications.There are many basic science questions to

17

Manufacturing with light: photonics at the molecular level

NO

W5

ye

ars

10

ye

ars

15

ye

ars

TechnologiesApplications

On

go

ing

dev

elo

pm

ent

of

lab

-on

-a-c

hip

Ch

ip t

her

apy

(act

ive)

, e.g

.d

rug

pro

du

ctio

n

Ch

ip

dev

elo

pm

ent

no

n-s

ilico

n?

Lab

-on

-a-m

icro

sco

pe

(hyb

rid

):•

on

a m

icro

sco

pe

slid

e•

end

osc

op

y

Lab

-on

-a-c

hip

–

per

son

al d

iag

no

sis

bas

ed o

n:

• b

loo

d

• b

reat

h

• u

rin

e •

saliv

aTe

stin

g f

or:

• ca

nce

r•

dis

ease

scr

een

ing

• g

ener

al h

ealt

h

Nan

o p

arti

cle

sort

ing

:

sele

ctiv

e an

d p

ho

ton

ic

Hig

h-t

hro

ug

hp

ut

chem

ical

pro

du

ctio

n:

• o

n a

ch

ip•

cap

illar

y tu

be

Ste

erin

g

tech

no

log

ies

Lase

r d

evel

op

men

t is

key

Inte

gra

tio

n

Mu

lti o

n-c

hip

im

ag

ing

tech

no

log

ies:

• m

eta

bo

lic r

ate

• fl

uo

rescen

ce lif

eti

me

• la

bel-

free t

ech

no

log

y

• m

icro

cavit

y t

ech

niq

ues

• o

rgan

ic laser

• R

am

an

sp

ectr

osco

py

• S

ER

S

New

develo

pm

en

ts

in m

icro

flu

idic

s

su

rface c

on

tro

l:

• sp

ati

al is

su

es

(c

riti

cal siz

e)

• n

ew

fab

ricati

on

te

ch

no

log

ies

Ph

oto

nic

crys

tal

HP

LC (h

igh

pre

ssu

re

liqu

id c

hro

mat

og

rap

hy)

b

ased

on

lig

ht

New

co

mp

act (

nan

o)

po

wer

so

urc

es/s

ou

rcin

g

for

pu

mp

ing

an

d

anal

ysis

: •

ph

oto

-act

ivat

ed v

alve

• E

M-f

ield

po

wer

ed•

ther

mal

hea

t en

gin

e

Sh

ort

-pu

lse

lase

r so

urc

es:

• u

ltra

co

mp

act

• in

-sit

u

• m

icro

op

tics

•

nan

o o

pti

cs

Res

on

ant

stru

ctu

re

det

ecto

r:

• m

icro

cav

ity

• p

lasm

on

s •

ph

oto

nic

ban

dg

aps

Co

mm

ents

:•

eth

ical

issu

es•

reg

ula

tory

issu

es•

nee

d t

o le

arn

• in

teg

rati

on

of

op

tics

w

ith

ch

ips

Op

tica

l d

amag

e –

sam

ple

d

egra

dat

ion

Mo

lecu

lar

reco

gn

itio

n

on

nm

sca

le –

op

tica

l o

r ch

emic

al?

Cel

l via

bili

ty

‘Rea

l’ m

ole

cula

r ch

ip

En

ab

lers

An

aly

sis

So

rtin

g/

sele

cti

on

(ste

eri

ng

)

Sam

plin

g

Mu

ltip

lexe

d

bio

log

ical

n

eura

l sen

sor

FCS

(f

luo

resc

ence

co

rrel

atio

nsp

ectr

osc

op

y)

SE

RS

(s

urf

ace

enh

ance

dR

aman

sp

ectr

osc

op

y)

Nat

ura

lflu

ore

scen

ce

qu

ench

ing

–

syn

thet

ic ta

gs

Sin

gle

-ph

oto

n

aval

anch

e d

iod

es

FAC

S(f

luo

resc

ence

ac

tivat

ed

cell

cou

nte

rs)

Cen

trifu

ges

/cy

sto

met

ryN

ew te

chn

iqu

es

in s

ort

ing

–

‘op

tical

pin

bal

l’

Mu

ltip

lexe

d

op

tical

tw

eeze

rs

Po

lari

satio

n to

co

ntr

ol

ori

enta

tion

of p

artic

les

– ch

iral

dis

crim

inat

ion

‘Stic

ky s

urf

ace’

Ph

oto

-act

ivat

ed

surf

ace

det

ecto

r

Eff

icie

nt

low

-co

st

tun

eab

le s

ou

rces

< $

100:

• IR

no

w

• o

rgan

ic lasers

• V

isib

le/U

V is

th

e c

hallen

ge

Figure 3. Photonics at the molecular level: technology timeline for integrated photonic LoC(key steps shown in orange)

18

answer as well as the manufacturing challenges.It is important to co-ordinate a multidisciplinaryeffort: for the LoC, close involvement ofbiological and medical scientists is essential. Allthese factors indicate that support should formpart of a national photonics road map, building astrategy for photonics across all areas (that is,combining with the ‘Switching to light: all-opticaldata handling’ topic recommendations).

This opportunity, among others, will be

considered by the DTI Electronics team’s

newly formed Photonics Strategy Group,

which will identify opportunities and

challenges for the UK over the next 5–10

years and develop an action plan to exploit

the sector. The team is also working to bring

together key players to start a national

Photonics network along the lines of the

successful Fuel Cells initiative.

Photonics has also been identified as a

potential priority area for a Call in 2004/05

under the new Technology Strategy.

Acknowledgements

We would like to thank all members of theaction group who gave so generously of theirtime and expertise.

Professor Donal Bradley, Imperial College London

Nathan Davies, EPSRC

Professor Kishan Dholakia, St Andrews University

Michael Dunn, The Wellcome Trust

Professor Sir Richard Friend, Cambridge University

Dr Clive Hayter, EPSRC

David Hull, DSTL

Dr Andrew Kearsley, Oxford Lasers Ltd

Professor Thomas Krauss, St Andrews University

Dr Coulton Legge, GlaxoSmithKline

Dr Tom McLean, Avecia

David Robbins, Centre of Excellence forNanotechnology, Micro and Photonic Systems

Dr Shiv Sharma, Amersham plc

Professor Wilson Sibbett, St Andrews University

Professor Andrew Turberfield, Oxford University

State of the science review authors: ProfessorKishan Dholakia and Dr David McGloin, StAndrews University.

19

Inside the wavelength:electromagnetics in the near field

Summary

All Foresight projects seek to explore andestablish best practice for science futures work.To this end, we sought a balance betweentopics defined by application or market andthose defined by the underlying science. Thistopic is of the latter type and consequently itsapplication areas are more diverse. The nearfield is the confined non-propagating part of anelectromagnetic field (at any frequency) thatdecays away exponentially from a surface,within a distance of about a wavelength. Therecent UK-led discovery of ‘metamaterials’(composite artificial materials) will allowmanipulation and use of the near field in waysnot previously possible.

Near field technologies are critical to

developing smart antennas and integrated

radio frequency infrastructure and circuitry.

The UK has a strong industry presence in this

sector and there is already much short-termincremental development. Long-term goalsinclude wearable antennas, very accurate beamcontrol, integrated broadband antennas and lowSAR (specific absorption rate) antennas.

Metamaterials are opening up excitingpossibilities in other areas, such as sub-wavelength resolution imaging using‘superlenses’ especially in MRI (magneticresonance imaging). As yet there are no

obvious single applications that alone would

be of sufficient potential to justify focused

investment. More basic research is needed to

explore the full potential of metamaterials.

Introduction

In general, at whatever frequency in thespectrum, it is the propagating wave part of theelectromagnetic field that is exploited – whetherthat be radio waves transmitting information,visible light providing illumination or laser beamscutting materials. The full electromagnetic field,however, comprises both these travelling wavesand a non-propagating component that decaysaway very rapidly from emitting surfaces. Sinceit is negligible except within about a wavelengthof the surface, it is called the near field, althoughthe distance it extends over can be manymetres for low-frequency radio waves. Newly

discovered metamaterials offer prospects for

manipulation of the near field across a wide

range of frequencies and many diverse

applications.

Controlling the near field would enable many

advances in efficient radio communications:

reductions in interference, losses, energy

consumption and absorption of power by

human tissue. Over smaller distances, local

20

communications (for example, between smartdevices within the home) might be carriedentirely within the near field.

In addition to being highly localised and non-propagating, the near field can vary on scalesmuch smaller than the wavelength of theassociated propagating wave. If the near fieldcould be imaged, detail on sub-wavelengthscales could be resolved – detail that cannot beseen with propagating waves, whose resolutionis limited by their wavelength. Metamaterials area broad class of artificially created materials withelectromagnetic properties beyond any found innature. Some metamaterials have negativerefractive indices, which means that they bendlight in the opposite (negative) direction to thebending caused by all naturally occurringmaterials. This property opens up the possibilityof imaging the near field by creating a‘superlens’ with a negative refractive index to capture and image the information in the near field.

This could be of use in MRI where improvingresolution is currently achieved by increasing thestrength of the background magnetic field. Thisreduces the wavelength of the imaged signalbut high field magnets are expensive to makeand cumbersome to work with. As research intonegative index materials continues, there arelikely to be other potential applications for a superlens.

At metal surfaces and for frequencies in theoptical range the near field interacts with theconductance electrons in the metal to form a‘surface plasmon’. In metal foils patterned withholes, surface plasmons can cause radiation of amuch longer wavelength than the dimensions ofthe holes to be transmitted through them,something that at first glance seemscounterintuitive. Surface plasmons can containlocalised regions of very high field density,offering prospects that include: holding(bio)molecules in position for individual testing;on-chip communications; and powering nonlinearoptical effects (such as are needed inapplications like fast optical switches).

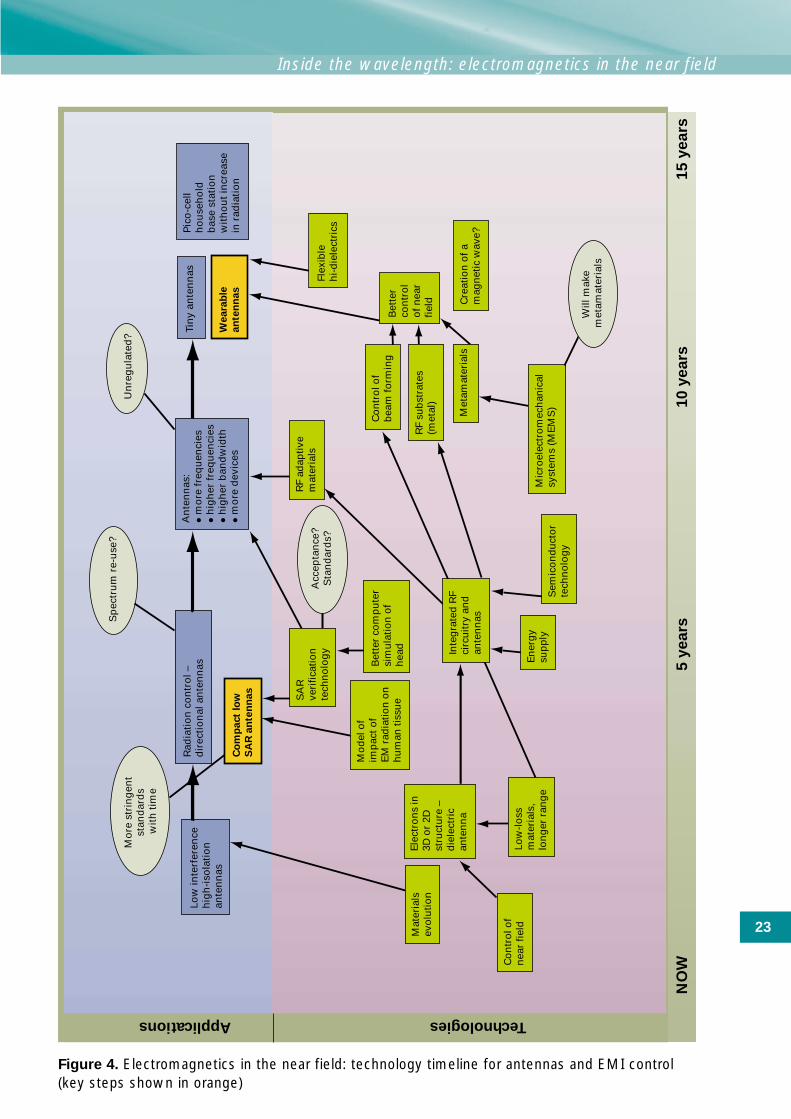

The action group considered three areas of

potential application of near field effects:antennas and electromagnetic interference

(EMI) control; MRI near field imaging; and

local near field communications and optical

bio-sensing.

Antennas and electromagneticinterference control

Key drivers

As described under ‘Switching to light: all-opticaldata handling’, global data transmissiondemands are growing and, whilst rates ofgrowth may fluctuate, the trend is likely tocontinue upwards. This is a key driver for bothfixed-line and mobile communications systems.Wireless traffic is growing and in the future maywell include increasing amounts of inter-devicecommunication between ever more intelligentdevices, such as smart home appliances, carnavigation systems and trackers for radiofrequency identity (RFID) tagged objects.Demand for more bandwidth will increase

pressure for more efficient use of the radio

frequency (RF) spectrum, for example,

through better beam control or by using

confined near field communications.

Consumer expectations create strong drivers forreducing the cost, size and weight of devices. Atpresent health concerns over SAR are not amajor driver – consumers show no preferencefor low-SAR models when buying phones – soproducers have little motivation to develop low-SAR devices. Were public opinion or regulationsto change, health concerns could rapidly becomeimportant. This possibility cannot be ruled out,especially as the network becomes morepervasive, and would be a major driver for verylow-SAR equipment.

Markets and applications

The antenna market is very cost-driven and theprice attrition that has seen unit costs formobile-handset antennas drop from $1 fouryears ago to $0.30 today is likely to continue.There is a wide range of product improvementsthat could be delivered if the market wasprepared to pay for them. The group considered

21

Inside the wavelength: electromagnetics in the near field

the markets for some examples. The UK has astrong presence in these markets (principallythrough Filtronic, along with smaller companiesincluding Antenova and Sarantel).

Most promising of these is base station RF

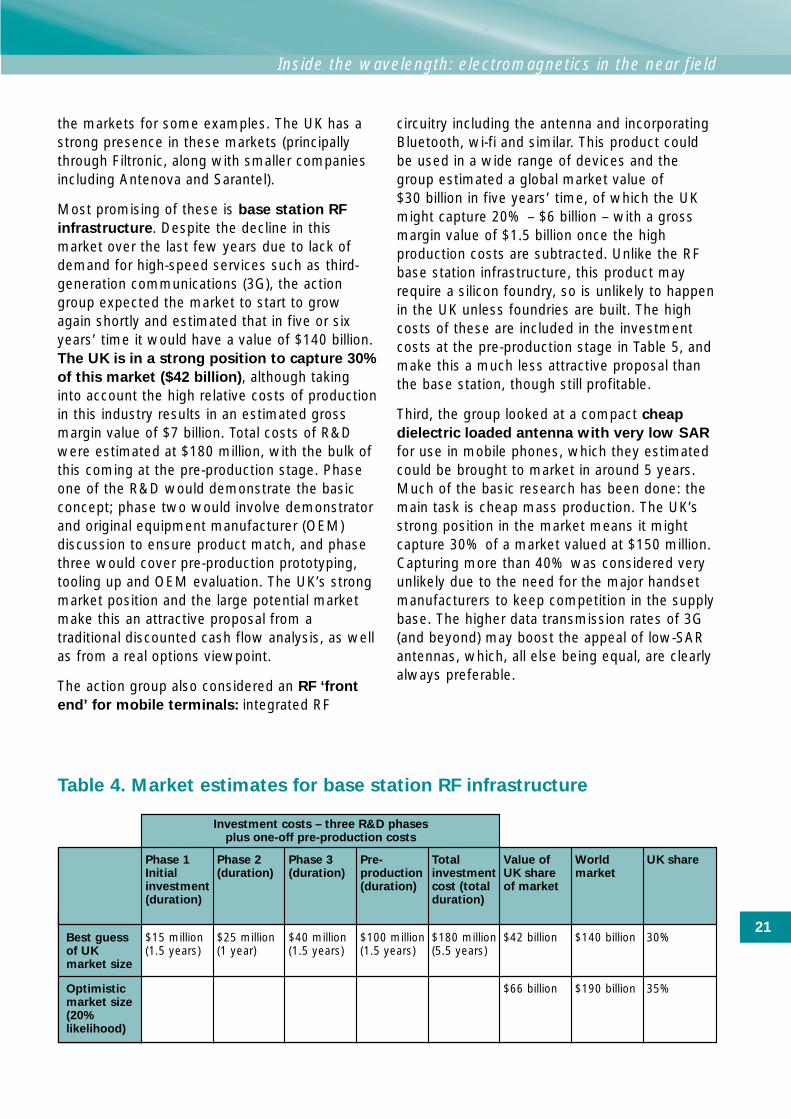

infrastructure. Despite the decline in thismarket over the last few years due to lack ofdemand for high-speed services such as third-generation communications (3G), the actiongroup expected the market to start to growagain shortly and estimated that in five or sixyears’ time it would have a value of $140 billion.The UK is in a strong position to capture 30%

of this market ($42 billion), although takinginto account the high relative costs of productionin this industry results in an estimated grossmargin value of $7 billion. Total costs of R&Dwere estimated at $180 million, with the bulk ofthis coming at the pre-production stage. Phaseone of the R&D would demonstrate the basicconcept; phase two would involve demonstratorand original equipment manufacturer (OEM)discussion to ensure product match, and phasethree would cover pre-production prototyping,tooling up and OEM evaluation. The UK’s strongmarket position and the large potential marketmake this an attractive proposal from atraditional discounted cash flow analysis, as wellas from a real options viewpoint.

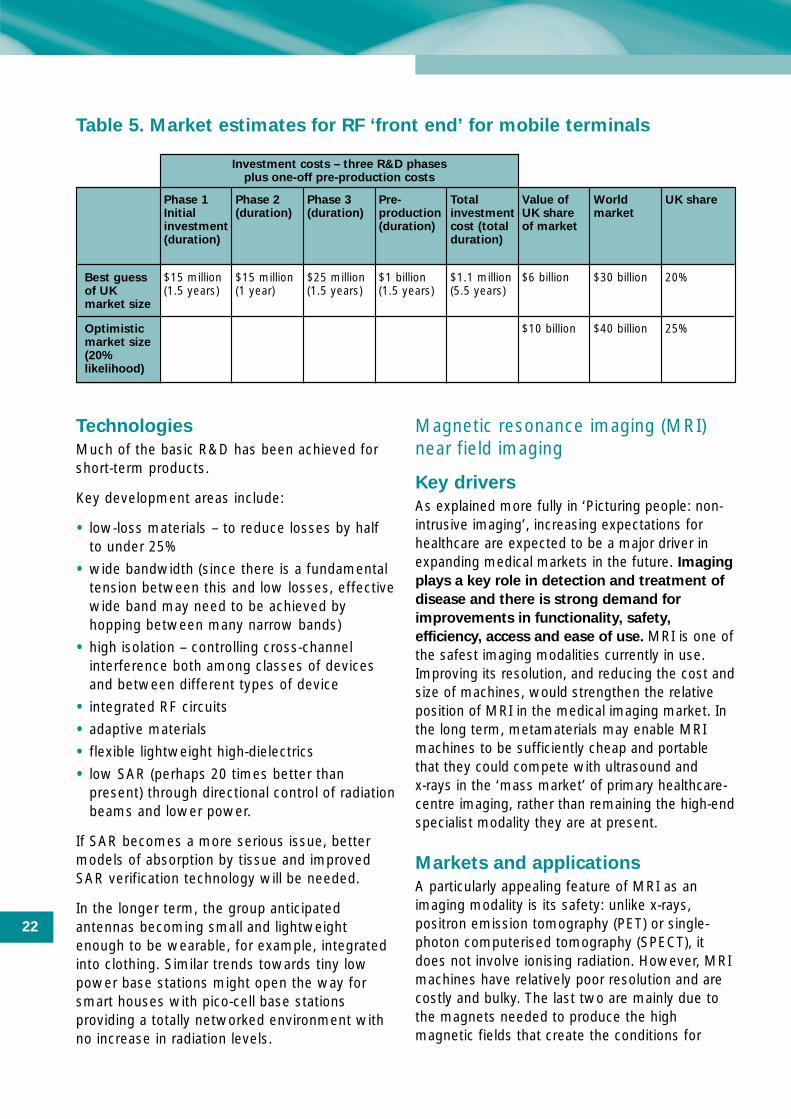

The action group also considered an RF ‘front

end’ for mobile terminals: integrated RF

circuitry including the antenna and incorporatingBluetooth, wi-fi and similar. This product couldbe used in a wide range of devices and thegroup estimated a global market value of $30 billion in five years’ time, of which the UKmight capture 20% – $6 billion – with a grossmargin value of $1.5 billion once the highproduction costs are subtracted. Unlike the RFbase station infrastructure, this product mayrequire a silicon foundry, so is unlikely to happenin the UK unless foundries are built. The highcosts of these are included in the investmentcosts at the pre-production stage in Table 5, andmake this a much less attractive proposal thanthe base station, though still profitable.

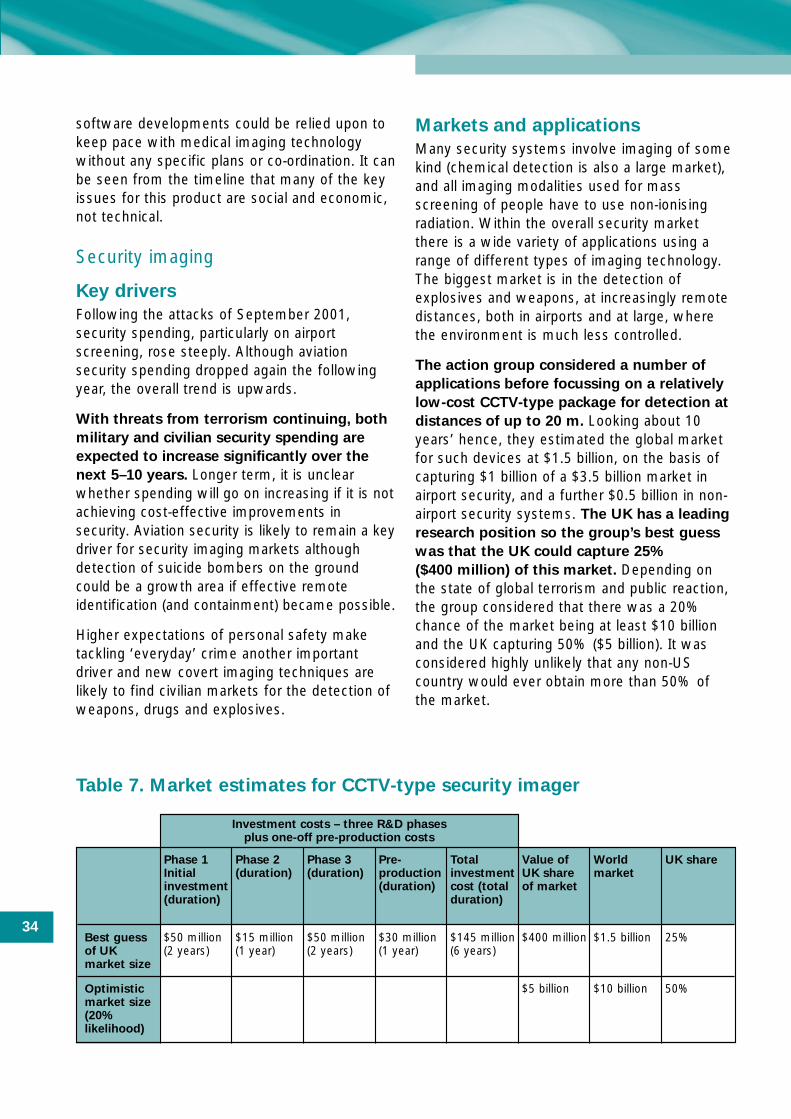

Third, the group looked at a compact cheap

dielectric loaded antenna with very low SAR

for use in mobile phones, which they estimatedcould be brought to market in around 5 years.Much of the basic research has been done: themain task is cheap mass production. The UK’sstrong position in the market means it mightcapture 30% of a market valued at $150 million.Capturing more than 40% was considered veryunlikely due to the need for the major handsetmanufacturers to keep competition in the supplybase. The higher data transmission rates of 3G(and beyond) may boost the appeal of low-SARantennas, which, all else being equal, are clearlyalways preferable.

Table 4. Market estimates for base station RF infrastructure

Investment costs – three R&D phases plus one-off pre-production costs

Phase 1 Phase 2 Phase 3 Pre- Total Value of World UK shareInitial (duration) (duration) production investment UK share marketinvestment (duration) cost (total of market(duration) duration)

Best guess $15 million $25 million $40 million $100 million $180 million $42 billion $140 billion 30%of UK (1.5 years) (1 year) (1.5 years) (1.5 years) (5.5 years)market size

Optimistic $66 billion $190 billion 35%market size(20% likelihood)

22

Technologies

Much of the basic R&D has been achieved forshort-term products.

Key development areas include:

• low-loss materials – to reduce losses by halfto under 25%

• wide bandwidth (since there is a fundamentaltension between this and low losses, effectivewide band may need to be achieved byhopping between many narrow bands)

• high isolation – controlling cross-channelinterference both among classes of devicesand between different types of device

• integrated RF circuits

• adaptive materials

• flexible lightweight high-dielectrics

• low SAR (perhaps 20 times better thanpresent) through directional control of radiationbeams and lower power.

If SAR becomes a more serious issue, bettermodels of absorption by tissue and improvedSAR verification technology will be needed.

In the longer term, the group anticipatedantennas becoming small and lightweightenough to be wearable, for example, integratedinto clothing. Similar trends towards tiny lowpower base stations might open the way forsmart houses with pico-cell base stationsproviding a totally networked environment withno increase in radiation levels.

Magnetic resonance imaging (MRI)near field imaging

Key drivers

As explained more fully in ‘Picturing people: non-intrusive imaging’, increasing expectations forhealthcare are expected to be a major driver inexpanding medical markets in the future. Imaging

plays a key role in detection and treatment of

disease and there is strong demand for

improvements in functionality, safety,

efficiency, access and ease of use. MRI is one ofthe safest imaging modalities currently in use.Improving its resolution, and reducing the cost andsize of machines, would strengthen the relativeposition of MRI in the medical imaging market. Inthe long term, metamaterials may enable MRImachines to be sufficiently cheap and portablethat they could compete with ultrasound and x-rays in the ‘mass market’ of primary healthcare-centre imaging, rather than remaining the high-endspecialist modality they are at present.

Markets and applications

A particularly appealing feature of MRI as animaging modality is its safety: unlike x-rays,positron emission tomography (PET) or single-photon computerised tomography (SPECT), itdoes not involve ionising radiation. However, MRImachines have relatively poor resolution and arecostly and bulky. The last two are mainly due tothe magnets needed to produce the highmagnetic fields that create the conditions for

Table 5. Market estimates for RF ‘front end’ for mobile terminals

Investment costs – three R&D phases plus one-off pre-production costs

Phase 1 Phase 2 Phase 3 Pre- Total Value of World UK shareInitial (duration) (duration) production investment UK share marketinvestment (duration) cost (total of market(duration) duration)

Best guess $15 million $15 million $25 million $1 billion $1.1 million $6 billion $30 billion 20%of UK (1.5 years) (1 year) (1.5 years) (1.5 years) (5.5 years)market size

Optimistic $10 billion $40 billion 25%market size(20% likelihood)

23

Inside the wavelength: electromagnetics in the near field

NO

W5

ye

ars

10

ye

ars

15

ye

ars

TechnologiesApplications

Pic

o-c

ell

ho

use

ho

ld

bas

e st

atio

n

wit

ho

ut

incr

ease

in

rad

iati

on

Inte

gra

ted

RF

circ

uitr

y an

d

ante

nn

as

Mic

roel

ectr

om

ech

anic

alsy

stem

s (M

EM

S)

Sp

ectr

um

re-

use

?

Rad

iati

on

co

ntr

ol –

d

irec

tio

nal

an

ten

nas

Tin

y an

ten

nas

Weara

ble

an

ten

nas

Low

inte

rfer

ence

hig

h-i

sola

tio

nan

ten

nas

Mat

eria

ls

evo

lutio

n

Low

-loss

m

ater

ials

,lo

ng

er r

ang

eE

ner

gy

sup

ply

Sem

ico

nd

uct

or

tech

no

log

y

Co

ntr

ol o

f n

ear

field

Co

ntr

ol o

f b

eam

form

ing

RF

adap

tive

mat

eria

ls

Met

amat

eria

lsC

reat

ion

of a

mag

net

ic w

ave?

RF

sub

stra

tes

(met

al)

Mo

del

of

imp

act o

f E

M r

adia

tion

on

h

um

an ti

ssu

e

Bet

ter

com

pu

ter

sim

ula

tion

of

hea

d