exhibit 1 credit opinion fy2013-2018 leverage and … · 2018-01-25 · financial year ending 31...

TRANSCRIPT

CORPORATES

CREDIT OPINION20 October 2017

Update

RATINGS

Lanxess AGDomicile Koeln, Germany

Long Term Rating Baa3

Type LT Issuer Rating - FgnCurr

Outlook Stable

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Francois Lauras 44-20-7772-5397VP-Sr Credit [email protected]

Anke Richter 44-20-7772-1433Associate [email protected]

Lanxess AGUpdate to Discussion of Key Credit Factors

SummaryThe Baa3 rating reflects our expectation that the €2.4 billion acquisition of Chemtura willhelp further improve the group’s underlying operating profitability and cash flow generation,which already benefited from material cost savings achieved in the past three years through acomprehensive restructuring programme. Following the establishment of the 50-50 Arlanxeojoint venture with Saudi Aramco, which helped reduce Lanxess’s exposure to volatile syntheticrubber markets, the Chemtura acquisition will expand its specialty chemicals portfolio andshould enhance the resilience and quality of its earnings. Near-term, the deal, which waspredominantly funded with cash and senior debt, leads to a marked increase in leverage.According to our estimate based on the proportionate accounting of Arlanxeo, net debt toEBITDA will be around 3.3x and retained cash flow (RCF) to net debt in the low twenties at year-end 2017. However, Lanxess’s future results will benefit from the incremental profit contributionfrom Chemtura, augmented by merger synergies. We therefore expect Lanxess to generatesubstantial free cash flow from 2018 onwards, which should enable it to reduce total debt toEBITDA below 3x and rebuild headroom to potentially pursue external growth opportunities,as it seeks to further expand and strengthen its business portfolio.

Exhibit 1

FY2013-2018 Leverage and coverage metrics

0%

10%

20%

30%

40%

50%

0x

1x

2x

3x

4x

5x

6x

2013 2014 2015 2016 2016 PC* 2017F* 2018F*

Total Debt/EBITDA Net Debt/EBITDA RCF/Total Debt RCF/Net Debt

* Moody's estimate based on proportional consolidation of ArlanxeoSource: Moody's Investors Service; company's filings

MOODY'S INVESTORS SERVICE CORPORATES

Credit Strengths

» Savings from ongoing restructuring programme and Chemtura merger synergies to underpin future operating profitability

» Portfolio realignment including Chemtura acquisition to enhance business risk profile and future quality of earnings and cash flow

» Positive free cash flow after capex and dividend (FCF) to help reduce leverage post Chemtura acquisition and regain headroomwithin current rating category

» Management’s strong track-record at executing restructuring and conservative financial policies

Credit Challenges

» Exposure to oversupplied synthetic rubber market, albeit reduced following the formation of the Arlanxeo 50:50 joint venture withSaudi Aramco

» Operating margins remain at low end of investment grade-rated chemical peer group despite steady improvement of the past threeyears

» Risks associated with integration of Chemtura acquisition and delivery of merger synergies

» Increased financial leverage post Chemtura acquisition exacerbated by transaction related and synergy implementation costsweighing on EBITDA generation

Rating OutlookThe stable outlook reflects our expectation that the successful integration of Chemtura will allow Lanxess to consolidate its financialmetrics during 2018 and regain headroom within the current rating category for further potential external growth activity.

Factors that Could Lead to an Upgrade

» the successful integration of Chemtura in parallel with the completion of ongoing restructuring programmes resulting in somematerial improvement in Lanxess’s business risk profile and operating profitability evidenced by its EBITDA margin rising sustainablyinto the mid-teens together with

» permanent strengthening in financial metrics including RCF to total debt in the mid-20s (based on the proportionate consolidationof Arlanxeo)

Factors that Could Lead to a Downgrade

» failure to sustain the ongoing recovery in operating profitability and/or another large debt funded acquisition leading to

» some permanent deterioration in financial metrics (leaving aside further potential near-term volatility in pension adjustment),including total debt to EBITDA rising towards 4x and retained cash flow (RCF) to net debt falling below 20% based on theproportionate consolidation of Arlanxeo

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 20 October 2017 Lanxess AG: Update to Discussion of Key Credit Factors

MOODY'S INVESTORS SERVICE CORPORATES

Key Indicators

Exhibit 2

12/31/2016 PC* 12/31/2016 FC 12/31/2015 12/31/2014 12/31/2013 12/31/2012

Revenues (USD Billion) $7.3 $8.5 $8.8 $10.6 $11.0 $11.7

PP&E (net) (USD Billion) $2.3 $4.0 $4.0 $4.4 $4.5 $4.4

EBITDA Margin % 13.3% 12.7% 10.5% 8.5% 8.3% 13.2%

ROA - EBIT / Average Assets 5.0% 5.2% 4.4% 3.2% 2.4% 10.6%

Debt / EBITDA 4.2x 4.0x 3.2x 4.3x 4.8x 2.8x

EBITDA / Interest Expense 7.9x 8.2x 7.0x 5.2x 4.2x 7.5x

Retained Cash Flow / Debt 15.9% 16.8% 21.1% 15.1% 12.5% 25.7%

Retained Cash Flow / Net Debt 47.7% 46.5% 25.6% 18.4% 15.0% 33.5%

*Moody's estimate as of 12/31/2016 based on proportional consolidation of ArlanxeoAll ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations.Source: Moody's Financial Metrics™

ProfileHeadquartered in Cologne, Germany, Lanxess AG is a leading European chemical company with reported sales of €7.7 billion andreported EBITDA of €945 million for the financial year ended 31 December 2016 (€7.9 billion and €833 million, respectively, for thefinancial year ending 31 December 2015). It has a current equity market capitalisation of approximately €6.1 billion.

Exhibit 3

Pro-forma New Lanxess 2016 EBITDA preExhibit 4

End market exposure for New Lanxess with 50% Arlanxeo vs. NewLanxess without Arlanxeo

Advanced IntermediatesEBITDA €326 mn EBITDA margin 19%

Specialty AdditivesEBITDA €151 mn EBITDA margin 18%

Performance ChemicalsEBITDA €223 mnEBITDA margin 17%

Engineering MaterialsEBITDA €159 mnEBITDA margin 15%

ArlanxeoEBITDA €373 mnEBITDA margin 14%

26%

18%

13%

30%

12%

Source: Moody's Investors Service; company's filings

~15% ~10%

~10%~10%

~15% ~20%

~10% ~15%

~15%

~20%

~20%

~20%

~15%~5%

New Lanxess with 50%Arlanxeo

New Lanxess without Arlanxeo

Tire

Automotive

Chemicals

Consumer Goods

Agro

Construction

Others

Source: Moody's Investors Service; company's filings

Following recent Chemtura acquisition, starting from Q2 2017 Lanxess has reorganized its reporting structure into five businesssegments:

» Advanced Intermediates – comprises businesses in the field of basic and fine chemicals. The segment includes Saltigo and a portfolioof Advanced Industrial Intermediates, into which Chemtura’s organometallics business was integrated.

» Specialty Additives - a newly created business segment, which pools all units that manufacture additives. In particular, it coversAdditives (i.e. lubricant additives, plastic additives and phosphorous flame retardants, and bromine solutions), Rhein Chemie (i.e.colorant and rubber additives).

» Performance Chemicals – combines application-focused specialty chemicals used in such areas as disinfection, protection andpreservation of wood, construction materials, coatings etc. It comprises of Inorganic Pigments, Leather Chemicals, MaterialProtection Products and Liquid Purification Technologies business units.

3 20 October 2017 Lanxess AG: Update to Discussion of Key Credit Factors

MOODY'S INVESTORS SERVICE CORPORATES

» Engineering Materials – a newly formed integrated engineering plastics business, which includes High Performance Materials andUrethane Systems units.

» Arlanxeo - comprised of Tire & Specialty Rubbers and High Performance Elastomers business units, that manufacture syntheticrubbers used in automotive engineering, tires and construction industries. It is a 50/50 joint venture with Saudi Aramco, which iscurrently controlled and fully consolidated by Lanxess under IFRS.

Detailed Rating ConsiderationsCOMPREHENSIVE RESTRUCTURING FOLLOWED BY CHEMTURA ACQUISITION ENHANCE LANXESS’S BUSINESS RISK PROFILE

In response to the challenging operating environment faced in particular by its synthetic rubber business, Lanxess initiated, in May 2014,the three-phase “Let’s LANXESS again” realignment and efficiency programme. Phases 1 and 2 were focused on creating a more efficientorganisation while enhancing the operational competitiveness of the group by rationalising its global asset base. Phase 1 was completedby year-end 2015 and the annual savings of €150 million targeted by management were realised in full in 2015, i.e. a year earlier thanoriginally expected. Phase 2 should generate further benefits of €150 million p.a., with a run rate of €50 million already achieved by year-end 2016 and the full run rate expected to be reached by 2019.

Phase 3 had for main objective to improve the balance and competitiveness of the group’s business portfolio. In particular, Lanxess wasanxious to improve raw materials and market access for its rubber business by forming some partnerships and/or marketing alliances.This led to the establishment of the Arlanxeo 50:50 joint venture with Saudi Arabia's national oil company, Saudi Aramco (unrated), towhich the synthetic rubber business was transferred in April 2016.

This enabled Lanxess to reduce its exposure to the global synthetic rubber market that has been recently affected by significantovercapacities. Arlanxeo should also have significant operational benefits and, in particular, address the lack of backward integration thatwas a constraint on the business’s performance in the past. As contracts with current suppliers run out over the next few years, Arlanxeowill gradually be able to source feedstock from Saudi Aramco on competitive terms. This access to key raw materials will improve thecost position of the joint venture and the predictability of its cash flow, which has historically been affected by the volatility of feedstockcosts, such as butadiene.

In September 2016, Lanxess announced a further major step in the repositioning of its portfolio with the acquisition of US based specialtychemical company, Chemtura Corporation for an enterprise value of around €2.4 billion (including net financial liabilities and pensionobligations), which was equivalent to 9.4x 2016 EBITDA. Completed in April 2017, the transaction falls in line with Lanxess’s strategy toexpand its specialty chemicals portfolio and enhance the resilience and quality of its earnings.

Chemtura, which historically generated relatively stable EBITDA margins averaging around 15% (on a Moody’s adjusted basis) in theperiod 2011-2016, significantly expands the footprint of Lanxess’s growing and profitable additives business.

This acquisition also boosts Lanxess’s presence in North America and Asia. It adds to its portfolio of industrial lubricant additives and flameretardants, creating the second and third largest player globally in those segments respectively. The combined business enjoys strongbackward integration, with long-term secured access to its bromine feedstock needs, and complementary product portfolios giving riseto cross selling opportunities.

As a result, the above initiatives have shifted the focus of Lanxess’s core portfolio towards businesses that are characterised by a lessconcentrated and volatile feedstock base than the rubber business, a higher degree of vertical integration, strong technological capabilities,leading market positions, a more diversified end-market exposure and lower capital intensity.

EFFICIENCY SAVINGS AND CHEMTURA SYNERGIES TO UNDERPIN FUTURE OPERATING PROFITABILITY

In 2014-15, the recovery in Lanxess’s operating profitability had been constrained by cumulated cash restructuring charges of around€260 million (2014: €164 million/ 2015: €96 million) incurred in connection with Phase 1 and 2 of the restructuring. By contrast, 2016results benefited from lower cash restructuring expenses reduced to €50 million while efficiency savings reached an annual run rate of€190 million by year-end against €150 million in December 2015. Also, the Performance Chemicals and High Performance Materialsbusinesses posted strong growth in underlying results, largely driven by higher volumes combined with the €200 million acquisition of the

4 20 October 2017 Lanxess AG: Update to Discussion of Key Credit Factors

MOODY'S INVESTORS SERVICE CORPORATES

Chemours Clean and Disinfect business for the former and favourable sales mix effects for the latter. This helped offset ongoing pressurein synthetic rubber resulting from overcapacity new synthetic rubber capacities are brought on stream.

In 2016, Lanxess’s EBITDA (as adjusted by Moody’s) increased by 18% to €980 million. Based on the proportionate consolidation ofArlanxeo, which, in our view, better reflects Lanxess’s reduced economic exposure to the rubber business following the inception of theJV, the group’s EBITDA margin rose by 280 basis points (bp) to 13.3% year-on-year. This compares with a smaller gain of 220bp to 12.7%using the full consolidation method applied under IFRS.

In the first half of 2017, the group reported a 25% increase in EBITDA pre exceptionals to €695 million (including the full consolidationof Arlanxeo), which was driven by higher sales volumes (+5.9%) as well as first time contributions from Chemtura consolidated from 21April and the Clean and Disinfect specialties business acquired in August 2016. This helped offset raw material cost inflation that wereonly partially mitigated by price increases, and softer conditions in the agrochemical sector. In this context, we view Lanxess’s full year2017 guidance of EBITDA pre exceptionals ranging between €1,225 – €1,300 million as achievable.

Exhibit 5

FY2013-2018 EBITDA and EBITDA margin

8.3% 8.5%

10.5%

13.3%12.0% 13.9%

0%

3%

6%

9%

12%

15%

0

250

500

750

1,000

1,250

2013 2014 2015 2016 PC* 2017F* 2018F*

€m

illio

n

EBITDA EBITDA margin

* Moody's estimate based on proportional consolidation of ArlanxeoSource: Moody's Investors Service; company's filings

However, we expect that the increase in Moody’s adjusted EBITDA will be constrained by restructuring costs of €60 million related tothe centralisation of Lanxess’s chromium value chain, implementation costs of €50 million for the Chemtura synergies and a €60 millioninventory step-up (all classified as exceptionals by Lanxess). Based on the proportionate consolidation of Arlanxeo, we estimate thatMoody’s adjusted EBITDA will be close to €970 million (v. our estimates of €887 million in 2016).

Looking ahead, Lanxess’s future operating profitability will be boosted by a full-year contribution from Chemtura, which generatedMoody's adjusted EBITDA of €255 million on sales of around €1.5 billion in 2016, equivalent to an EBITDA margin of approximately 17.1%.In addition, Lanxess is confident to extract cost synergies of around €100 million from the integration of Chemtura for a one-time cost of€140 million. These should be achieved in full by 2020, with €25 million in 2017 and a further €25 million in 2018. Synergies should arisefrom reductions in corporate/regional costs (circ. €30 million), marketing and sales (circ. €20 million) as well as production platforms andprocurement optimisation. For instance, in early October, Lanxess announced the closure of the Ankerweg site in the Netherlands, witha view to consolidating all its production of base oils for industrial lubricants at its Elmira site in Canada.

GROWING CASH FLOW TO HELP REBUILD HEADROOM FOR FURTHER POTENTIAL EXTERNAL GROWTH OPERATIONS

In May 2014, Lanxess successfully executed a €433 million capital increase, which helped offset the cumulative cash deficit reported inthe period 2010-13, as a result of heightened capital investments. In addition, despite restructuring cash outlays of around €190 million,the group generated FCF of €150 million in 2014-15, as it cut back on capex and achieved a substantial reduction in working capital. Thisenabled it to lower net debt (as adjusted by Moody’s) by around €560 million over the two-year period.

In 2016, Lanxess’s financial position was further strengthened by the receipt of €1.2 billion in cash from Saudi Aramco in exchange for a50% stake in the Arlanxeo joint venture. This resulted in substantial deleveraging. Based on the proportionate accounting of Arlanxeo, we

5 20 October 2017 Lanxess AG: Update to Discussion of Key Credit Factors

MOODY'S INVESTORS SERVICE CORPORATES

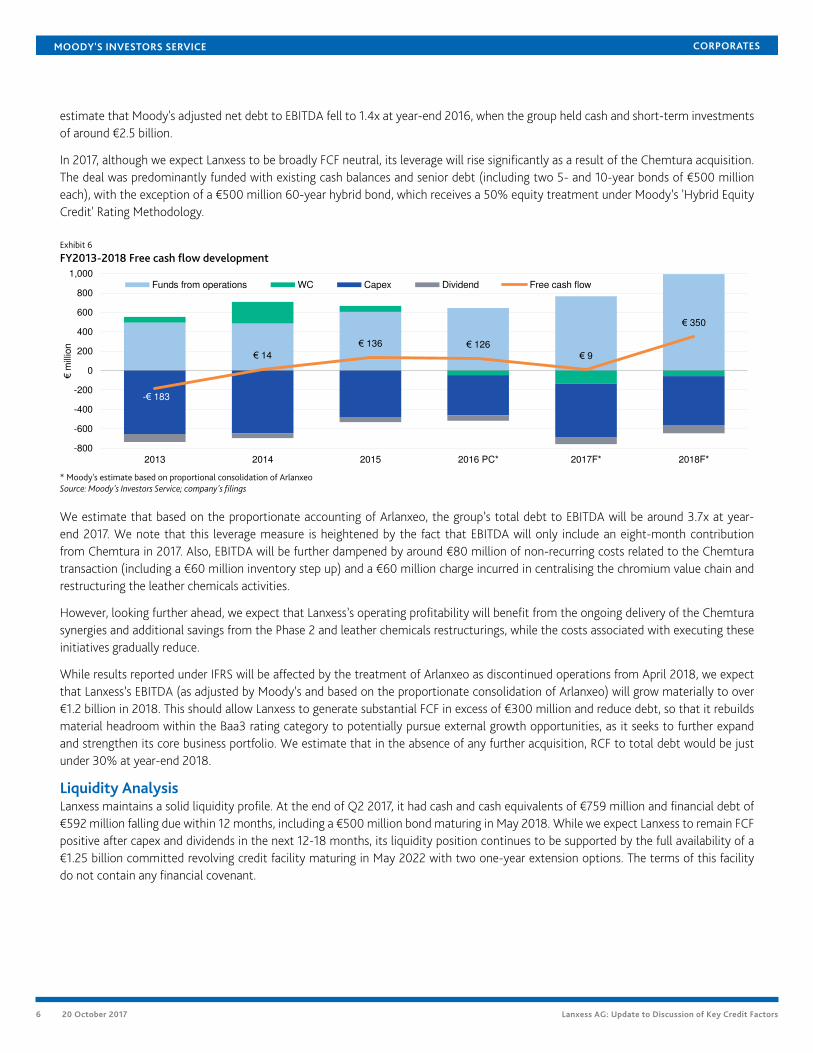

estimate that Moody's adjusted net debt to EBITDA fell to 1.4x at year-end 2016, when the group held cash and short-term investmentsof around €2.5 billion.

In 2017, although we expect Lanxess to be broadly FCF neutral, its leverage will rise significantly as a result of the Chemtura acquisition.The deal was predominantly funded with existing cash balances and senior debt (including two 5- and 10-year bonds of €500 millioneach), with the exception of a €500 million 60-year hybrid bond, which receives a 50% equity treatment under Moody’s 'Hybrid EquityCredit' Rating Methodology.

Exhibit 6

FY2013-2018 Free cash flow development

-€ 183

€ 14

€ 136 € 126€ 9

€ 350

-800

-600

-400

-200

0

200

400

600

800

1,000

2013 2014 2015 2016 PC* 2017F* 2018F*

€m

illio

n

Funds from operations WC Capex Dividend Free cash flow

* Moody's estimate based on proportional consolidation of ArlanxeoSource: Moody's Investors Service; company's filings

We estimate that based on the proportionate accounting of Arlanxeo, the group’s total debt to EBITDA will be around 3.7x at year-end 2017. We note that this leverage measure is heightened by the fact that EBITDA will only include an eight-month contributionfrom Chemtura in 2017. Also, EBITDA will be further dampened by around €80 million of non-recurring costs related to the Chemturatransaction (including a €60 million inventory step up) and a €60 million charge incurred in centralising the chromium value chain andrestructuring the leather chemicals activities.

However, looking further ahead, we expect that Lanxess’s operating profitability will benefit from the ongoing delivery of the Chemturasynergies and additional savings from the Phase 2 and leather chemicals restructurings, while the costs associated with executing theseinitiatives gradually reduce.

While results reported under IFRS will be affected by the treatment of Arlanxeo as discontinued operations from April 2018, we expectthat Lanxess’s EBITDA (as adjusted by Moody’s and based on the proportionate consolidation of Arlanxeo) will grow materially to over€1.2 billion in 2018. This should allow Lanxess to generate substantial FCF in excess of €300 million and reduce debt, so that it rebuildsmaterial headroom within the Baa3 rating category to potentially pursue external growth opportunities, as it seeks to further expandand strengthen its core business portfolio. We estimate that in the absence of any further acquisition, RCF to total debt would be justunder 30% at year-end 2018.

Liquidity AnalysisLanxess maintains a solid liquidity profile. At the end of Q2 2017, it had cash and cash equivalents of €759 million and financial debt of€592 million falling due within 12 months, including a €500 million bond maturing in May 2018. While we expect Lanxess to remain FCFpositive after capex and dividends in the next 12-18 months, its liquidity position continues to be supported by the full availability of a€1.25 billion committed revolving credit facility maturing in May 2022 with two one-year extension options. The terms of this facilitydo not contain any financial covenant.

6 20 October 2017 Lanxess AG: Update to Discussion of Key Credit Factors

MOODY'S INVESTORS SERVICE CORPORATES

Rating Methodology and Scorecard Factors

The principal methodology used in rating Lanxess is Moody's Global Chemical Industry rating methodology, which can be found atthe www.moodys.com website and was updated in December 2013. Other methodologies and factors that may have been consideredin the process of rating these issuers can also be found in the Credit Policy & Methodologies directory. Moody's Global ChemicalIndustry Methodology grid indicates a Ba1 rating for the year ended December 2016 based on our estimates reflecting the proportionateconsolidation Arlanxeo. The one notch differential with the actual rating reflected the weak leverage metrics that were affected by thepre-financing of the Chemtura acquisition closed in April 2017.

For the forecast period, which reflects the Chemtura acquisition, the grid indicates a Baa2 rating. This illustrates the headroom, whichwe expect Lanxess to regain within the current rating category over the next 12-18 months, and may be used to accommodate furtherexternal growth activity.

For illustrative purposes the chart on the last page of this publication maps the company utilising the full year 2016 historical financialsas well as our projections for the next 12-18 months. Please note that both historicals and projections are based on our estimates of theproportionate consolidation of the Arlanxeo joint venture.

Exhibit 7

Rating Factors

Lanxess AG

Chemical Industry Grid [1][2]Current

as of 12/31/2016

Moody's 12-18 Month Forward View

as of 10/16/2017 [3]

Factor 1 : Scale (20%) Measure Score Measure Score

a) Revenues (USD Billion) $7.3 Baa $10 - $10.5 Baa

b) PP&E (net) (USD Billion) $2.3 Ba $3.2 - $3.5 Baa

Factor 2 : Business Profile (20%)

a) Business Profile Baa Baa Baa Baa

Factor 3 : Profitability (10%)

a) EBITDA Margin % 13.3% Ba 13.5% - 14% Ba

b) ROA - EBIT / Average Assets 5.0% Ba 8% - 8.5% Ba

Factor 4 : Leverage & Coverage (30%)

a) Debt / EBITDA 4.2x B 2.4x - 2.6x Baa

b) EBITDA / Interest Expense 7.9x Ba 9.5x - 10x Baa

c) Retained Cash Flow / Debt 15.9% Ba 26% - 29% Baa

Factor 5 : Financial Policy (20%)

a) Financial Policy Baa Baa Baa Baa

Rating:

a) Indicated Rating from Grid Ba1 Baa2

b) Actual Rating Assigned Baa3 Baa3

[1] All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations.[2] The ratios are computed on the basis of Moody's estimates reflecting the proportionate consolidation of Arlanxeo.[3] This represents Moody's forward view; not the view of the issuer; and unless noted in the text, does not incorporate significant acquisitions and divestitures.Source: Moody's Financial Metrics™

7 20 October 2017 Lanxess AG: Update to Discussion of Key Credit Factors

MOODY'S INVESTORS SERVICE CORPORATES

Appendix

Exhibit 8

Lanxess AG peer comparison

$ million 2014 2015 2016 2014 2015 2016 2014 2015 2016 2014 2015 2016

Revenue 10,637 8,773 8,519 9,527 9,648 9,008 7,908 8,530 8,337 15,626 13,414 13,171

EBITDA 905 920 1,085 2,087 2,314 2,136 950 1,149 1,256 1,565 1,708 2,247

Total Debt 3,521 2,884 4,164 8,384 7,740 7,183 2,523 3,147 3,089 6,777 4,328 3,449

Cash & Cash Equiv. 627 506 2,658 214 293 181 1,390 772 657 733 697 440

EBITDA Margin 8.5% 10% 13% 22% 24% 24% 12% 13% 15% 10% 13% 17%

ROA - EBIT / Avg. Assets 3.2% 4.4% 5.2% 11% 10% 9.2% 5.9% 7.0% 7.0% 5% 8% 11.9%

EBITDA / Int. Exp. 5.2x 7.0x 8.2x 9.2x 7.5x 6.9x 10.5x 10.5x 11.4x 7.6x 10.3x 20.4x

Debt / EBITDA 4.3x 3.2x 4.0x 4.0x 3.3x 3.4x 2.9x 2.8x 2.6x 4.8x 2.6x 1.6x

Net Debt / EBITDA 3.5x 2.6x 1.5x 3.9x 3.2x 3.3x 1.3x 2.1x 2.0x 4.2x 2.2x 1.4x

RCF / Debt 15% 21% 17% 19% 22% 25% 18% 21% 22% 16% 24% 48%

RCF / Net Debt 18% 26% 47% 20% 23% 25% 40% 28% 28% 18% 29% 56%

Baa3 Stable

Lanxess AG

Baa2 Stable

Covestro AG

Baa2 Stable

Arkema

Baa2 Stable

Eastman Chemical Co

All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations.Source: Moody's Financial Metrics™

Exhibit 9

Lanxess AG historical Moody's adjusted debt breakdown

€ million 2012 2013 2014 2015 2016

As Reported Debt 2,334 2,317 1,854 1,677 2,789

Pensions 674 565 744 702 1,129

Operating Leases 401 395 312 276 280

Hybrid Securities (250)

Moody's Adjusted Debt 3,409 3,277 2,910 2,655 3,948

Source: Moody's Financial Metrics™

Exhibit 10

Lanxess AG historical Moody's adjusted EBITDA breakdown

€ million 2012 2013 2014 2015 2016

As Reported EBITDA 1,169 619 619 822 932

Pensions 18 11 1 1

Operating Leases 48 61 67 65 61

Interest Expense Discounting (13) (11) (14) (15) (12)

Unusual Adjustments (44) (1)

Non-Standard Adjustments (1) (2)

Moody's Adjusted EBITDA 1,203 687 681 829 981

Source: Moody's Financial Metrics™

8 20 October 2017 Lanxess AG: Update to Discussion of Key Credit Factors

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 11

Lanxess AG historical and projected Moody's adjusted financial data

€ million 2012 2013 2014 2015 2016 FC 2016 PC* 2017F* 2018F*

INCOME STATEMENT

Revenues 9,094 8,300 8,006 7,902 7,699 6,664 8,050 8,850

EBITDA 1,203 687 681 829 981 887 967 1,232

EBIT 791 182 235 329 460 411 509 725

Interest Expense 160 165 130 118 119 113 156 125

Net Income 488 (12) 65 99 193 162 187 432

BALANCE SHEET

Cash&Cash Equivalents 797 533 518 466 2,520 2,476 425 415

Total Debt 3,409 3,277 2,910 2,655 3,948 3,711 3,609 3,199

CASH FLOW

Funds from Operations 947 494 485 606 720 644 767 995

Change in Working Capital items (201) 60 224 61 (46) (46) (136) (58)

Cash Flow from Operations 746 554 709 667 674 598 631 937

Capital Expenditures (CAPEX) (707) (654) (649) (485) (488) (417) (555) (504)

Dividends (72) (83) (46) (46) (55) (55) (67) (83)

Free Cash Flow (FCF) (33) (183) 14 136 131 126 9 350

Retained Cash Flow (RCF) 875 411 439 560 665 589 700 912

RCF / Debt 26% 13% 15% 21% 17% 16% 19% 29%

RCF / Net Debt 33% 15% 18% 26% 47% 48% 22% 33%

FCF / Debt -1.0% -5.6% 0.5% 5.1% 3.3% 3.4% 0.2% 11%

PROFITABILITY

% Change of Sales (YoY) 3.6% -8.7% -3.5% -1% -3% -16% 21% 10%

EBIT Margin % 8.7% 2.2% 2.9% 4.2% 6.0% 6.2% 6.3% 8.2%

EBITDA Margin % 13.2% 8.3% 8.5% 10.5% 12.7% 13.3% 12.0% 13.9%

INTEREST COVERAGE

EBIT / Interest Expense 4.9x 1.1x 1.8x 2.8x 3.9x 3.6x 3.3x 5.8x

EBITDA / Interest Expense 7.5x 4.2x 5.2x 7.0x 8.2x 7.9x 6.2x 9.8x

LEVERAGE

Debt / EBITDA 2.8x 4.8x 4.3x 3.2x 4.0x 4.2x 3.7x 2.6x

Net Debt / EBITDA 2.2x 4.0x 3.5x 2.6x 1.5x 1.4x 3.3x 2.3x

*Moody's estimate based on proportional consolidation of ArlanxeoAll ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations and represent Moody's forward view, not the view ofthe issuer; and unless noted in the text, does not incorporate significant acquisitions and divestitures.Source: Moody's Investors Service

Ratings

Exhibit 12Category Moody's RatingLANXESS AG

Outlook StableIssuer Rating Baa3Senior Unsecured -Dom Curr Baa3Pref. Stock -Dom Curr Ba2

Source: Moody's Investors Service

9 20 October 2017 Lanxess AG: Update to Discussion of Key Credit Factors

MOODY'S INVESTORS SERVICE CORPORATES

© 2017 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGSDO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’SOPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVEMODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’SPUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOTPROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THESUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATIONAND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FORPURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1086501

10 20 October 2017 Lanxess AG: Update to Discussion of Key Credit Factors