exercises: set b - cengage€¦ · exercises: set b financial accounting ... concept the lettered...

TRANSCRIPT

ExErcisEs: sEt B

Financial Accounting ConceptsE1B. concEpt ▶ The lettered items that follow represent a classification scheme for the concepts of financial accounting. Match each numbered term in the list with the letter of the category in which it belongs. a. Decision makers (users of accounting

information) b. Business activities or entities relevant to

accounting measurement c. Objective of accounting information d. Accounting measurement

considerations e. Accounting processing considerations f. Qualitative characteristics g. Accounting conventions h. Financial statements

1. Conservatism 2. Verifiability 3. Statement of cash flows 4. Materiality 5. Faithful representation 6. Recognition 7. Cost-benefit 8. Predictive value 9. Business transactions 10. Consistency 11. Full disclosure 12. Furnishing information that is useful

to investors and creditors 13. Specific business entities 14. Classification 15. Management 16. Neutrality 17. Internal accounting control 18. Valuation 19. Investors 20. Completeness 21. Relevance 22. Furnishing information that is useful

in assessing cash flow prospects

Accounting Concepts and ConventionsE2B. concEpt ▶ Each of the statements that follows is either a proper use of one or more concepts in accounting or a violation of the concept. State which of these selected qualitative characteristics and accounting conventions—relevance, faithful representa-tion, comparability, verifiability, timeliness, understandability, cost constraint, consis-tency, materiality, conservatism, or full disclosure relate to the statement and, if it is a violation, indicate so. 1. A series of reports that are time-consuming and expensive to prepare are presented

to the owner each month, even though they are never used. 2. A company changes its method of accounting for depreciation. 3. The company in 2 does not indicate in the financial statements that the method of

depreciation was changed; nor does it specify the effect of the change on net income. 4. A company’s new storage building, which is built next to the company’s existing

factory, is debited to the factory account, because it represents a fairly small dollar amount in relation to the factory.

5. The asset account for a pickup truck still used in the business is written down to what the truck could be sold for, even though the carrying value under conventional depreciation methods is higher.

6. A classified balance sheet is prepared so that it will be more comprehensible to read-ers of the statement.

7. A company prepares financial statements in way that corresponds to its strategic plan, allowing readers to assess its progress.

8. A company’s balance sheet shows two years of financial data.

LO 1

LO 1

Chapter Assignments 1

(Continued)

CHE-NEEDLES_FINM-12-0107-004-WEB.indd 1 14/11/12 10:10 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

2 Chapter 4: Foundations of Financial Reporting and the Classified Balance Sheet

9. A company makes every effort to include transactions in the proper accounting period so that the financial statements reflect each period properly.

10. Financial statements are prepared promptly. 11. A company’s auditors are able to reproduce reasonably well estimates made by man-

agement in the financial statements.

Classification of Accounts: Balance SheetE3B. The lettered items that follow represent a classification scheme for a balance sheet, and the numbered items in the list below are account titles. Match each account with the letter of the category in which it belongs. a. Current assets b. Investments c. Property, plant, and equipment d. Intangible assets e. Current liabilities f. Long-term liabilities g. Stockholders’ equity h. Not on balance sheet

1. Patent 2. Building Held for Sale 3. Prepaid Rent 4. Wages Payable 5. Note Payable in Five Years 6. Building Used in Operations 7. Fund Held to Pay Off Long-Term Debt 8. Inventory 9. Prepaid Insurance 10. Depreciation Expense 11. Accounts Receivable 12. Interest Expense 13. Unearned Revenue 14. Short-Term Investments 15. Accumulated Depreciation 16. Common Stock

Classified Balance Sheet PreparationE4B. The following data pertain to Mori, Inc.: Accounts Payable, $10,200; Accounts Receivable, $7,600; Accumulated Depreciation—Building, $2,800; Accumulated Depreciation—Equipment, $3,400; Bonds Payable, $12,000; Building, $14,000; Cash, $6,240; Copyright, $1,240; Equipment, $30,400; Inventory, $8,000; Investment in Corporate Securities (long-term), $4,000; Investment in Six-Month Government Secu-rities, $3,280; Common Stock, $31,000; Retained Earnings, $16,640; Land, $1,600; Prepaid Rent, $240; and Revenue Received in Advance, $560. Prepare a classified bal-ance sheet at December 31, 2014. Assume that this is Mori’s first year of operations.

Liquidity RatiosE5B. BusinEss ApplicAtion ▶ The accounts and balances that follow are from Buy-It Company’s general ledger. Compute the (1) working capital and (2) current ratio. (Round to one decimal place.)

LO 2

LO 2

LO 3

Accounts Payable $ 6,640

Accounts Receivable 4,080

Cash 600

Current Portion of Long-Term Debt 4,000

Long-Term Investments 8,320

Marketable Securities 5,040

Merchandise Inventory 10,160

Notes Payable (90 days) 6,000

Notes Payable (2 years) 16,000

Notes Receivable (90 days) 10,400

Notes Receivable (2 years) $ 8,000

Prepaid Insurance 160

Income Taxes Payable 420

Property, Plant, and Equipment 48,000

Property Taxes Payable 500

Common Stock 20,000

Retained Earnings 2,220

Salaries Payable 340

Supplies 140

Unearned Revenue 300

CHE-NEEDLES_FINM-12-0107-004-WEB.indd 2 14/11/12 10:10 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Chapter Assignments 3

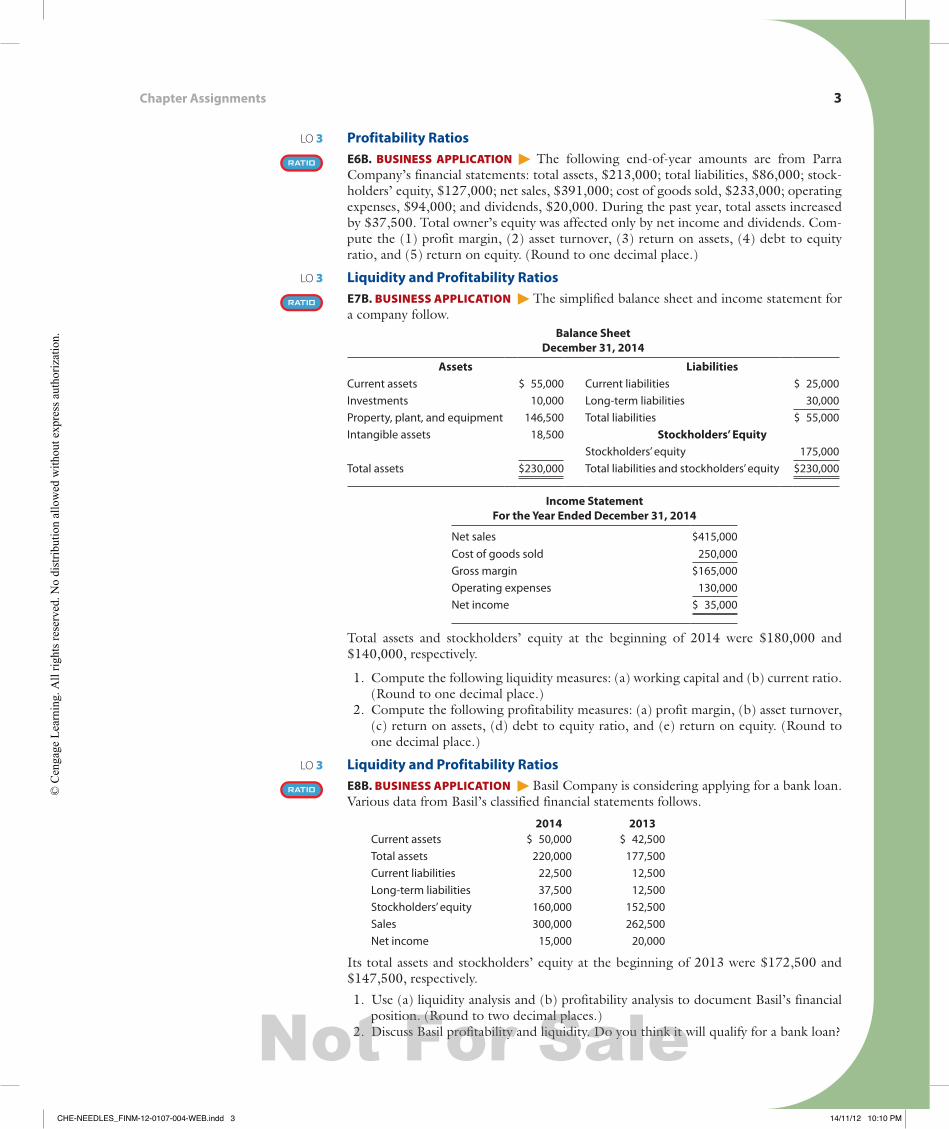

Profitability RatiosE6B. BusinEss ApplicAtion ▶ The following end-of-year amounts are from Parra Company’s financial statements: total assets, $213,000; total liabilities, $86,000; stock-holders’ equity, $127,000; net sales, $391,000; cost of goods sold, $233,000; operating expenses, $94,000; and dividends, $20,000. During the past year, total assets increased by $37,500. Total owner’s equity was affected only by net income and dividends. Com-pute the (1) profit margin, (2) asset turnover, (3) return on assets, (4) debt to equity ratio, and (5) return on equity. (Round to one decimal place.)

Liquidity and Profitability RatiosE7B. BusinEss ApplicAtion ▶ The simplified balance sheet and income statement for a company follow.

Balance Sheet December 31, 2014

Assets LiabilitiesCurrent assets $ 55,000 Current liabilities $ 25,000

Investments 10,000 Long-term liabilities 30,000

Property, plant, and equipment 146,500 Total liabilities $ 55,000

Intangible assets 18,500 Stockholders’ EquityStockholders’ equity 175,000

Total assets $230,000 Total liabilities and stockholders’ equity $230,000

Income StatementFor the Year Ended December 31, 2014

Net sales $415,000

Cost of goods sold 250,000

Gross margin $165,000

Operating expenses 130,000

Net income $ 35,000

Total assets and stockholders’ equity at the beginning of 2014 were $180,000 and $140,000, respectively.

1. Compute the following liquidity measures: (a) working capital and (b) current ratio. (Round to one decimal place.)

2. Compute the following profitability measures: (a) profit margin, (b) asset turnover, (c) return on assets, (d) debt to equity ratio, and (e) return on equity. (Round to one decimal place.)

Liquidity and Profitability RatiosE8B. BusinEss ApplicAtion ▶ Basil Company is considering applying for a bank loan. Various data from Basil’s classified financial statements follows.

2014 2013Current assets $ 50,000 $ 42,500

Total assets 220,000 177,500

Current liabilities 22,500 12,500

Long-term liabilities 37,500 12,500

Stockholders’ equity 160,000 152,500

Sales 300,000 262,500

Net income 15,000 20,000

Its total assets and stockholders’ equity at the beginning of 2013 were $172,500 and $147,500, respectively.

1. Use (a) liquidity analysis and (b) profitability analysis to document Basil’s financial position. (Round to two decimal places.)

2. Discuss Basil profitability and liquidity. Do you think it will qualify for a bank loan?

LO 3

LO 3

LO 3

CHE-NEEDLES_FINM-12-0107-004-WEB.indd 3 14/11/12 10:10 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.