executive summary...i executive summary a. introduction the technical education and skills...

TRANSCRIPT

i

EXECUTIVE SUMMARY

A. INTRODUCTION

The Technical Education and Skills Development Authority (TESDA) was

created on August 26, 1994 by virtue of Republic Act (RA) No. 7796 otherwise known as the TESDA Act of 1994. The Act integrated the functions of the defunct agencies such as the National Manpower and Youth Council (NMYC), the Bureau of Technical and Vocational Education (BTVE), and the Apprenticeship Program of the Bureau of Local Employment (BLE) of the Department of Labor and Employment. The TESDA is mandated to become the country’s lead institution in molding a workforce that can meet the challenges of trade liberalization and global competition. It was created to mobilize the full participation of the industry, labor, technical and vocational institutions, local government and the civil society for skilled manpower development programs.

The Agency’s mission is to provide direction, policies, programs and standards

towards quality technical education and skills development, while its corporate vision is to be the leading partner in the development of the Filipino Work Force with world class competence and positive work values.

In view of the need to provide equitable access and provision of Technical Education and Skills Development (TESD) programs to the growing Technical Vocational Education and Training (TVET) clients, TESDA continues to undertake direct training provisions. There are four training modalities: a) School-based, b) Center-based, c) Enterprise - based and (d) Community-based. These are being done with TESDA’s infrastructure in place, namely: 57 TESDA administered schools, 60 training centers, enterprise-based training through Dual Training System (DTS)/apprenticeship and community-based training in convergence with the Local Government Units (LGUs).

TESDA SUPPORTS TRAINING PROVISION

TESDA Education Skills Development (TESD) creates opportunities for people to be responsible and become productive citizens. The need to provide and make accessible relevant TESD compels TESDA to undertake direct training activities at the same time support training activities undertaken by other key players in the TESD sector.

TESDA Technology Institutions (TTIs) are composed of 125 schools, regional, provincial and specialized training centers nationwide which undertake direct training activities for TESDA. The absence of an institution in the area which can provide people equitable access to TESD necessitates TESDA to undertake direct training activities. These TTIs also serve as venues to test new training schemes and are used as laboratories for new technology.

ii

Among the TESDA’s specialized training centers are the following:

a) TESDA Women’s Center (TWC)seeks to advance the economic status of women through training, entrepreneurship development, gender sensitive policies, programs and projects and research and advocacy. It was established through a grant from the Government of Japan.

b) Language Skills Institute (LSI ) serves as TESDA’s facility for language programs specifically for workers intending to work abroad. The LSI conducts training on workplace communication on the language of the country of the worker’s destination. There are 35 LSI nationwide offering different language courses which include English, Korean, Mandarin, Japanese and Spanish.

c) Korea-Philippines IT Training Centers(KPITTCs) are grant-assisted

projects from the Government of the Republic of Korea. These KPITTCs are located at the Polytechnic University in Novaliches, Quezon City and at the Regional Skills Development Centers in Guiguinto, Bulacan and Tibungco, Davao City..

The TESDA has three functions namely: a) to engage in various training cum-production, all income derived from these activities shall be deposited in the Sariling Sikap account; b) to develop the capability of LGUs to assume ultimately the responsibility for effectively providing community-based technical education and skills development opportunities; and c) to manage/administer the TESDA Development Fund (TDF). The income from TDF shall be utilized exclusively in awarding of grants and providing assistance to training institutions, industries, local government units and implement training and training –related activities. TDF is also authorized under RA No. 7796. The TESDA-Main has three books of accounts consisting of the General Fund, Fund 101, Trust Fund (101) and Sariling Sikap (161).

B. ORGANIZATIONAL SET-UP

The programs and projects of the TESDA are implemented through TESDA –

Main and the 216 operating units listed in the following table.

TESDA Operating Units No. Regional Offices (ROs) 16 Provincial Offices (POs) 74 District Offices (DOs) 6 Regional Training Centers (RTCs) 16 Provincial Training Centers (PTCs) 47 Technical Vocational Schools (TVSs) 57 Total 216

iii

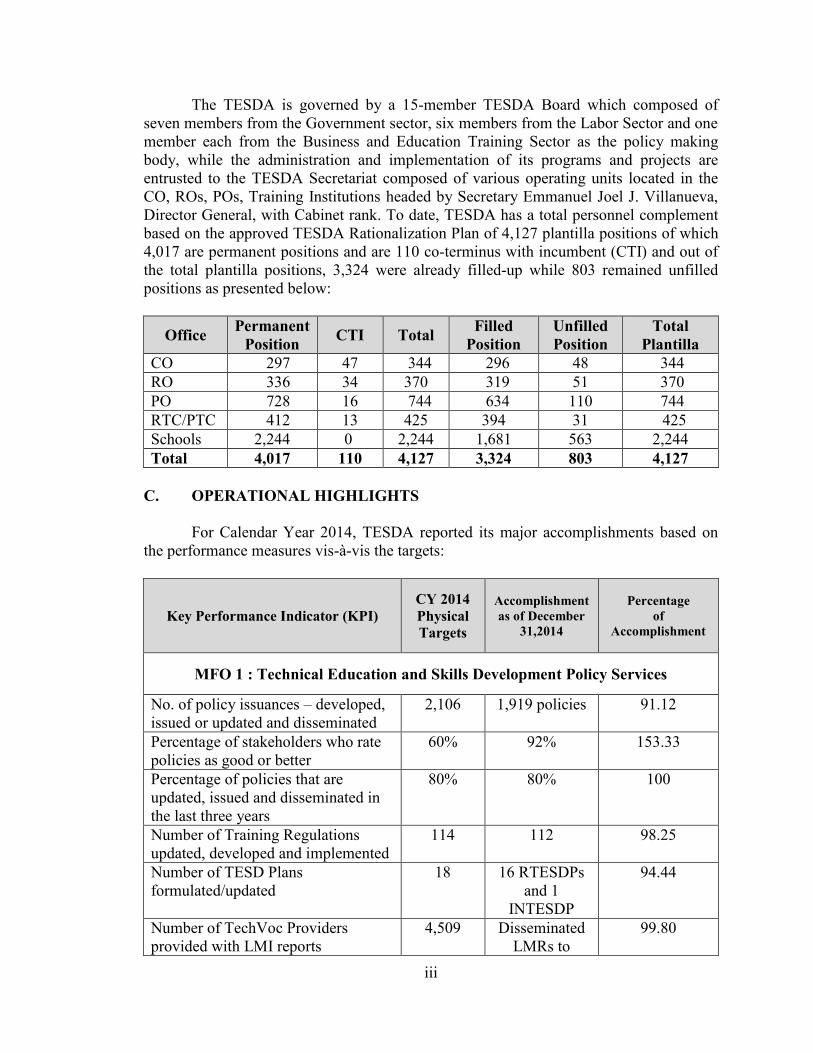

The TESDA is governed by a 15-member TESDA Board which composed of seven members from the Government sector, six members from the Labor Sector and one member each from the Business and Education Training Sector as the policy making body, while the administration and implementation of its programs and projects are entrusted to the TESDA Secretariat composed of various operating units located in the CO, ROs, POs, Training Institutions headed by Secretary Emmanuel Joel J. Villanueva, Director General, with Cabinet rank. To date, TESDA has a total personnel complement based on the approved TESDA Rationalization Plan of 4,127 plantilla positions of which 4,017 are permanent positions and are 110 co-terminus with incumbent (CTI) and out of the total plantilla positions, 3,324 were already filled-up while 803 remained unfilled positions as presented below:

Office Permanent Position CTI Total Filled

Position Unfilled Position

Total Plantilla

CO 297 47 344 296 48 344 RO 336 34 370 319 51 370 PO 728 16 744 634 110 744 RTC/PTC 412 13 425 394 31 425 Schools 2,244 0 2,244 1,681 563 2,244 Total 4,017 110 4,127 3,324 803 4,127

C. OPERATIONAL HIGHLIGHTS For Calendar Year 2014, TESDA reported its major accomplishments based on the performance measures vis-à-vis the targets:

Key Performance Indicator (KPI) CY 2014 Physical Targets

Accomplishment as of December

31,2014

Percentage of

Accomplishment

MFO 1 : Technical Education and Skills Development Policy Services

No. of policy issuances – developed, issued or updated and disseminated

2,106 1,919 policies 91.12

Percentage of stakeholders who rate policies as good or better

60% 92% 153.33

Percentage of policies that are updated, issued and disseminated in the last three years

80% 80% 100

Number of Training Regulations updated, developed and implemented

114 112 98.25

Number of TESD Plans formulated/updated

18 16 RTESDPs and 1

INTESDP

94.44

Number of TechVoc Providers provided with LMI reports

4,509 Disseminated LMRs to

99.80

iv

Key Performance Indicator (KPI) CY 2014 Physical Targets

Accomplishment as of December

31,2014

Percentage of

Accomplishment

Regions/POs/ TVIs-4,500

PQF-Registry of Qualifications per Sector

4 Sectors (Dentistry, Engineering, Maritime, Tourism

4 Qualifications

Register developed (Dentistry, Tourism,

Engineering, Maritime)

100.00

MFO 2 : Technical Education and Skills Development Services

Number of trainees 161,600 257,621 159.42 Average Training Hours Per Trainee 100 hrs. 356 hours

average training hours per trainee

356

Number of Graduates employed six months after completion of the training

79,000 70,366 89.07

Percentage of training applications acted upon within two weeks

80% 87.87% (1,087 out of 1,237 sample applications acted upon within two (2) weeks

109.84

Percentage of graduates certified within 5 days after graduation

84% 82% 97.62

Percentage of training programs that are delivered within one month of the original plan

80% 51.98% 64.98

Number of TWSP subsidized enrollees

163,300 203,706 124.74

Number of TWSP subsidized graduates

146,970 181,717 123.64

Number of STEP trainees/enrollees 74,947 48,599 64.84 Number of PESFA trainees 26,600 28,019 105.33 Number of BUB or GPB trainees 38,529 34,565 89.71 Number trainees for Skills and Livelihood Training Program for

24,535 27,721 112.99

v

Key Performance Indicator (KPI) CY 2014 Physical Targets

Accomplishment as of December

31,2014

Percentage of

Accomplishment

Yolanda Affected Areas Number of trainees for Institution-based Training Program

1,111,293 1,028,005 92.51

Number of trainees for Enterprise-based Training Program

95,098 69,138 72.70

Number of additional courses on ICT enabled Systems-TESDA Online Program

8 14 175.00

Number of registered users on ICT enabled Systems-TESDA Online Program

213,882 353,824 165.43

MFO 3: Technical Education and Skills Development Regulation Services

Number of Private TechVoc schools accredited (new programs registered)

6,500 5,670 87.23

Percentage of accredited Private TechVoc schools with accreditation condition breaches detected in the last three years

10 8 breaches (out of the 13,807

programs audited in 2011-2013

80.00

Percentage of applications for program registration of Private TechVoc schools acted upon within one week of submission

80.00 91.30 114.13

Number of TechVoc schools registered programs audited

9,989 (8,630

adjusted target)

7,838 90.82

Number of skilled workers assessed for certification

1,120,924 1,187,469 105.94

Number of persons certified 940,964 1,064,157 113.09 Percentage of accredited workers in employment three months after accreditation

61.00 70.00 114.75

Percentage of skilled workers issued with certification within seven days after application

80.00 81.00 101.25

These strategies and programs are depicted in the SEEK-FIND-TRAIN-

CERTIFY and EMPLOY framework which also account for the Major Final Output (MFO) approved for TESDA by the Department of Budget and Management (DBM).

vi

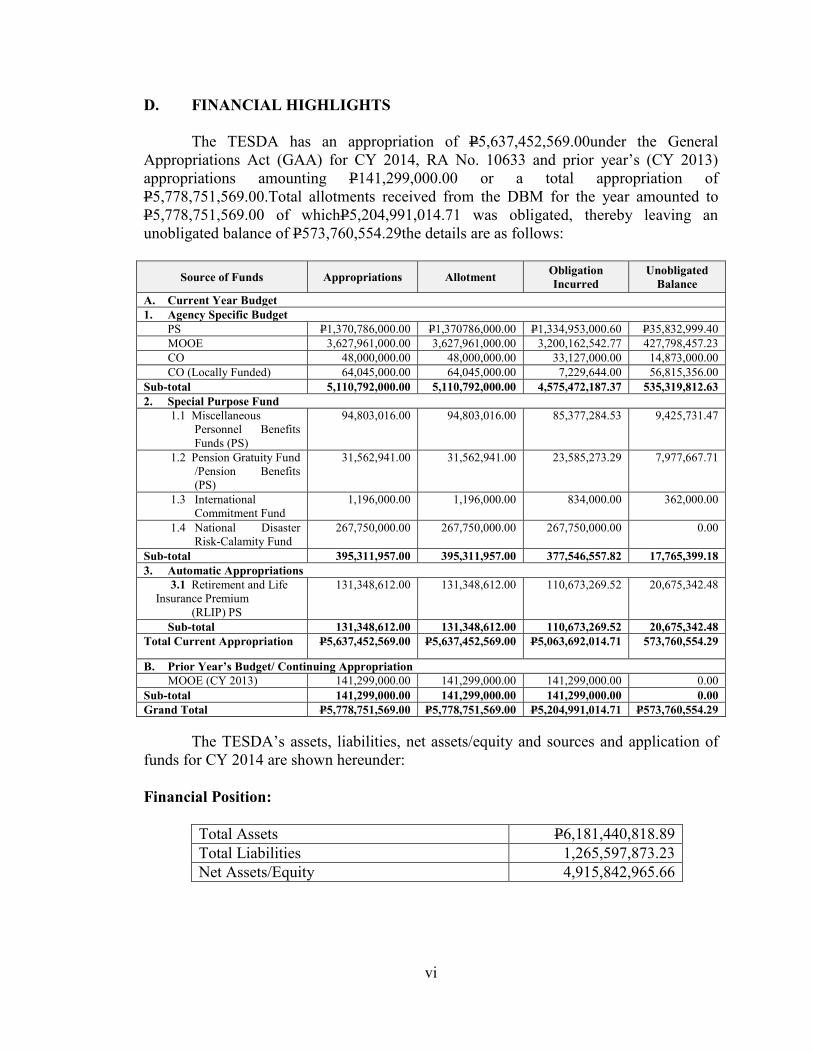

D. FINANCIAL HIGHLIGHTS

The TESDA has an appropriation of P5,637,452,569.00under the General Appropriations Act (GAA) for CY 2014, RA No. 10633 and prior year’s (CY 2013) appropriations amounting P141,299,000.00 or a total appropriation of P5,778,751,569.00.Total allotments received from the DBM for the year amounted to P5,778,751,569.00 of whichP5,204,991,014.71 was obligated, thereby leaving an unobligated balance of P573,760,554.29the details are as follows:

Source of Funds Appropriations Allotment Obligation Incurred

Unobligated Balance

A. Current Year Budget 1. Agency Specific Budget PS P1,370,786,000.00 P1,370786,000.00 P1,334,953,000.60 P35,832,999.40 MOOE 3,627,961,000.00 3,627,961,000.00 3,200,162,542.77 427,798,457.23 CO 48,000,000.00 48,000,000.00 33,127,000.00 14,873,000.00 CO (Locally Funded) 64,045,000.00 64,045,000.00 7,229,644.00 56,815,356.00 Sub-total 5,110,792,000.00 5,110,792,000.00 4,575,472,187.37 535,319,812.63 2. Special Purpose Fund

1.1 Miscellaneous Personnel Benefits Funds (PS)

94,803,016.00 94,803,016.00 85,377,284.53 9,425,731.47

1.2 Pension Gratuity Fund /Pension Benefits (PS)

31,562,941.00 31,562,941.00 23,585,273.29 7,977,667.71

1.3 International Commitment Fund

1,196,000.00 1,196,000.00 834,000.00 362,000.00

1.4 National Disaster Risk-Calamity Fund

267,750,000.00 267,750,000.00 267,750,000.00 0.00

Sub-total 395,311,957.00 395,311,957.00 377,546,557.82 17,765,399.18 3. Automatic Appropriations

3.1 Retirement and Life Insurance Premium (RLIP) PS

131,348,612.00 131,348,612.00 110,673,269.52 20,675,342.48

Sub-total 131,348,612.00 131,348,612.00 110,673,269.52 20,675,342.48 Total Current Appropriation P5,637,452,569.00 P5,637,452,569.00 P5,063,692,014.71 573,760,554.29

B. Prior Year’s Budget/ Continuing Appropriation MOOE (CY 2013) 141,299,000.00 141,299,000.00 141,299,000.00 0.00 Sub-total 141,299,000.00 141,299,000.00 141,299,000.00 0.00 Grand Total P5,778,751,569.00 P5,778,751,569.00 P5,204,991,014.71 P573,760,554.29 The TESDA’s assets, liabilities, net assets/equity and sources and application of funds for CY 2014 are shown hereunder: Financial Position:

Total Assets P6,181,440,818.89 Total Liabilities 1,265,597,873.23 Net Assets/Equity 4,915,842,965.66

vii

Sources of Funds and Application of Funds:

Sources of Funds: Service and Business Income P636,761,777.43 Shares, Grants and Donations 22,316,726.69 Gains 116,439.65 Total Revenue 659,194,943.77 Application of Funds: Personnel Services P1,596,107,657.52 Maintenance and Other Operating Expenses 3,357,493,214.67 Financial Expenses 265,606.04 Direct Costs 3,035,968.72 Non-Cash Expenses 292,029,164.58 Total Expenses 5,248,931,611.53 Surplus (Deficit) from Current Operations (4,589,736,667.76) Net Financial Assistance/Subsidy 4,813,826,118.05 Gains 111,294,467.99 Losses (1,317,112.42) Surplus for the period P334,066,805.86

E. SCOPE OF AUDIT

The audit covered the review of the accounts and operations of the TESDA for the

period 01 January to 31 December 2014. It was aimed in determining whether the financial statements present fairly the financial position and results of operations of the TESDA for the year then ended, and at determining the extent of compliance with existing laws, rules and regulations.

F. AUDITOR’S REPORT IN THE FINANCIAL STATEMENTS

The Auditor rendered a qualified opinion on the fairness of presentation of the financial statements of the TESDA for the year ended December 31, 2014 due to exceptions as stated in the Independent Auditor’s Report and as discussed in Part II of this Consolidated Annual Audit Report.

G. SUMMARY OF SIGNIFICANT AUDIT OF OBSERVATIONS AND

RECOMMENDATIONS

The following are the significant audit observations and the corresponding recommendations:

1) Out of the total amount of P1.022 billion appropriated in calendar year (CY 2014) for the implementation of Special Training for Employment Program (STEP), P824,170,534.00 was allotted,broken into P480,587,111.00 for

viii

training program expenses for targeted scholars of 79,825 amounting to P480,587,111.00 and for procurement of tool kits in the amount P343,583,423.00 which was fully obligated/utilized, while the allotment for training program expenses, only P252,053,377.04 or 52.45 percent was obligated leaving unobligated amount of, P228,533,733.96 indicative of an unattained target corresponding to scholarship slots of 37,281 or 46.70 percent of the total slots identified and funded as of year-end, with the National Capital Region (NCR) registering zero utilized slot; followed by Region IV-A, ARMM and Region X with 84.55, 80.25 and 69.05 percent unutilized slots, respectively, unfavorably affecting the expected output/outcome of the program to provide training opportunities for the beneficiaries in the barangays/communities to make them employable and productive. The balance of appropriation amounting to P197,829,466.00 was not allotted as of December 31, 2014 and will be utilized in CY 2015, although agencies are expected to obligate allotment releases within the year as stipulated in Section 4.5 NBC No. 551 dated January 2, 2014 on the subject “Guidelines on the Release of Funds for CY 2014. (Observation No. 1)

We recommended that Management/Focal Persons:

ensure optimum utilization of fund for the training needs/activities/requirements of the Special Training for Employment Program for the benefit of scholars identified in the approved STEP Form 1;

re-evaluate/re-assess and ensure that the number of STEP scholarship slots identified in the approved STEP form 1/QM is accurate, truthful and correctly stated since STEP Form 1 is the basis of the amount of allotment to be released for training of scholars; and

expedite procurement action and to speed up delivery of toolkits to

Regional Offices, Provincial Offices and District Offices in order that distribution to intended beneficiaries after graduation is made on time.

2) Procurement of toolkits was delayed although the beginning of FY 2014

GAA, budgets of departments/agencies are considered as allotments for the purpose that implementation of program/projects can proceed earlier. Procurement of toolkits with an Approved Budget for the Contract (ABC) of P346,072,305.62 was awarded to ACMI Systems Philippines, Inc. in the amount P343,583,423.00 where Notice to Proceed was issued to ACMI on October 31, 2014 and actual delivery commenced mostly in January 2015, consequently, resulting to late/non-delivery/distribution of toolkits to implementers as of December 31, 2014, which also delayed the benefits of

ix

the 26,594 graduates the chance to learn and earn a living or be productive after graduation.(Observation No. 2)

We recommended that Management:

expedite procurement action and speed up delivery of toolkits to ROs,

POs, and DOs; follow the timetable in the delivery of tool kits to coincide with the

graduation of trainees in order that benefits/purpose from the use of tool kits would be derived by the trainees/beneficiaries after completion of the training program;

strictly observe/follow deadlines/target dates necessary to attain the

prompt implementation of the program;

facilitate the conduct of inspection in the region and to immediately transfer the toolkits to Provincial Offices/District Offices to be released to the scholars without delay after graduation; and

speed up procurement action/processfor succeeding/similar programs.

3) Out of the total appropriations for CY 2014 of P1.404 billion for the implementation of Training for Work Scholarship Program (TWSP) , the amount of P1,397,529,600.00 was allotted for the current year for targeted scholarship slots numbering 207,340 per Qualification Maps (the basis of allotment). Obligations totaling P1,361,348,150.00 was incurred leaving an unutilized balance of P36,181,450.00 as of December 31, 2014 reflective of unutilized training slots reflective of 4,280 unutilized training slots, hence the purpose/objective to support rapid, inclusive and sustained economic growth through course offerings and realization of expected benefits for poverty reduction and empowerment of the poor and vulnerable were not completely achieved. (Observation No. 3)

We recommended that Management:

a. carefully review the implementing guidelines of TWSP; make a well

planned and coordinated effort to engage implementers and stakeholders in coming up with doable, efficient and effective strategies to fully attain the objectives of the program;

b. meticulously evaluate/analyze Qualification Maps submitted before

they are finally approved in order that the number of scholarship slots identified therein are correspondingly funded since QMs are the basis of allotment allocation of respective regions; and

x

c. strengthen project implementation to maximize fund utilization.

4) The balance of cash transferred to respective TESDA Regional Offices during the year to finance the implementation of TWSP maintained under Local Currency Current Account (LCCA) amounting to P25,931,150.00 representing unutilized slots, drop-outs, not assessed and payables to TVIs/Assessment Centers was not yet remitted to the National Treasury contrary to Executive Order (EO) No. 431 dated May 30, 2005 and Permanent Committee Joint Circular (PCJC) No. 4-2012 dated September 11, 2012. (Observation No. 4)

We recommended the Management Office to:

immediately remit to the NT the amount of P25,931,150.00 current

account balance without specific authority/legal basis; and thereafter to remit all cash balances in excess of the cash allocations received pertaining to but not limited to the cost of unutilized slots, dropped-outs, trainees that will not undergo assessment; and

observe sound cash management system and strictly observe rules and regulations pertaining thereto.

5) In NCR-Caloocan, Malabon, Navotas, Valenzuela (CAMANAVA),

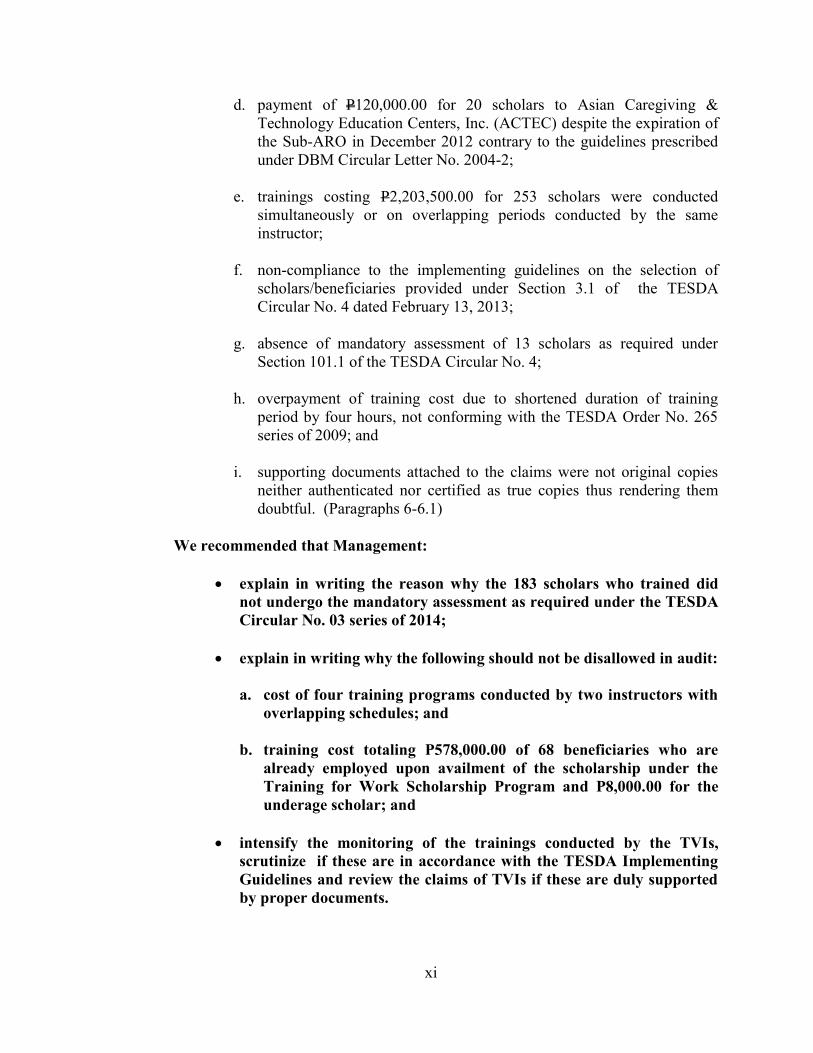

trainings conducted by a Technical Vocational Institute (TVI) under the Regular Training for Work Scholarship Program (TWSP) totaling P5,876,700.00 revealed non-compliance with The TESDA Implementing Guidelines for 2014 TWSP and due to inadequate monitoring by the Focal Person and Financial Analyst, the competency of the graduates and employment opportunities were difficult todetermine. Also, skills gained from the training were not optimized as well as the filling up of skill gap and job requirement of priority industries were not met, such that:(Observation No. 5)

a. out of the 630 scholars trained by the TVI, 183 did not undergo the

mandatory assessment contrary to Section 10.2 of the TESDA Circular No. 3 series of 2014 dated January 29, 2014 and the Affidavit of Undertaking of the TVI;

b. doubtful validity of four training programs conducted by two

instructors with overlapping schedules; and

c. sixty-eight scholars were not qualified as beneficiaries of TWSP due to employment upon availment of the scholarship program while one was underage upon graduation, thus access to TWSP for those poor residents and incidence of poverty are high was not assured;

xi

d. payment of P120,000.00 for 20 scholars to Asian Caregiving & Technology Education Centers, Inc. (ACTEC) despite the expiration of the Sub-ARO in December 2012 contrary to the guidelines prescribed under DBM Circular Letter No. 2004-2;

e. trainings costing P2,203,500.00 for 253 scholars were conducted

simultaneously or on overlapping periods conducted by the same instructor;

f. non-compliance to the implementing guidelines on the selection of

scholars/beneficiaries provided under Section 3.1 of the TESDA Circular No. 4 dated February 13, 2013;

g. absence of mandatory assessment of 13 scholars as required under

Section 101.1 of the TESDA Circular No. 4;

h. overpayment of training cost due to shortened duration of training period by four hours, not conforming with the TESDA Order No. 265 series of 2009; and

i. supporting documents attached to the claims were not original copies

neither authenticated nor certified as true copies thus rendering them doubtful. (Paragraphs 6-6.1)

We recommended that Management:

explain in writing the reason why the 183 scholars who trained did not undergo the mandatory assessment as required under the TESDA Circular No. 03 series of 2014;

explain in writing why the following should not be disallowed in audit: a. cost of four training programs conducted by two instructors with

overlapping schedules; and

b. training cost totaling P578,000.00 of 68 beneficiaries who are already employed upon availment of the scholarship under the Training for Work Scholarship Program and P8,000.00 for the underage scholar; and

intensify the monitoring of the trainings conducted by the TVIs,

scrutinize if these are in accordance with the TESDA Implementing Guidelines and review the claims of TVIs if these are duly supported by proper documents.

xii

strictly adhere with the provisions of DBM Circular Letter No. 2004-2; and revert all the expired funds every end of the year to the National Treasury and request from DBM to issue certification/authority to use the remaining the funds;

require the TVIs to strictly comply with the provisions set forth with regards to the proper conduct of trainings and documentary requirements in billing the District office for Training Costs or Assessment Fees;

require the TVIs to submit the lacking documents and complete the requirements pursuant to the guidelines prescribed under the above-mentioned TESDA Circulars to avoid the possible suspension or disallowance of their claims;

require the Financial Analyst to coordinate with designated focal person in undertaking the program, and careful evaluation must be conducted by both personnel to ensure that the TVI concerned will submit all the mandatory requirements within the timeline before the payment; and

CAR

6) Of the 139 selected samples of enrollees for Baguio City and Benguet, 114 enrollees could not be located and contacted due to wrong addresses and contact numbers, while of the 25 respondents, 10 respondents claimed to have never availed of any scholarship in TESDA-CAR, thereby, rendering doubt on the existence of the scholars reported to have availed of the TWSP and on the accuracy of the reported accomplishments. It also rendered difficulty in determining whether the purpose of the program was fully attained. (Observation No. 6)

We recommended that Management:

create an investigation team to probe on the authenticity and

existence of the scholars reported to have availed of the TWSP, of which majority were reported by the private training providers but their names, addresses, and contact numbers appear to be invalid/fictitious;

take appropriate actions against the erring training providers and require them to refund the amount paid pertaining to 10 respondents who claimed not to have availed of any scholarship;

update grantees records/profiles thru periodic visits to the schools to reflect correct data of grantees; and

xiii

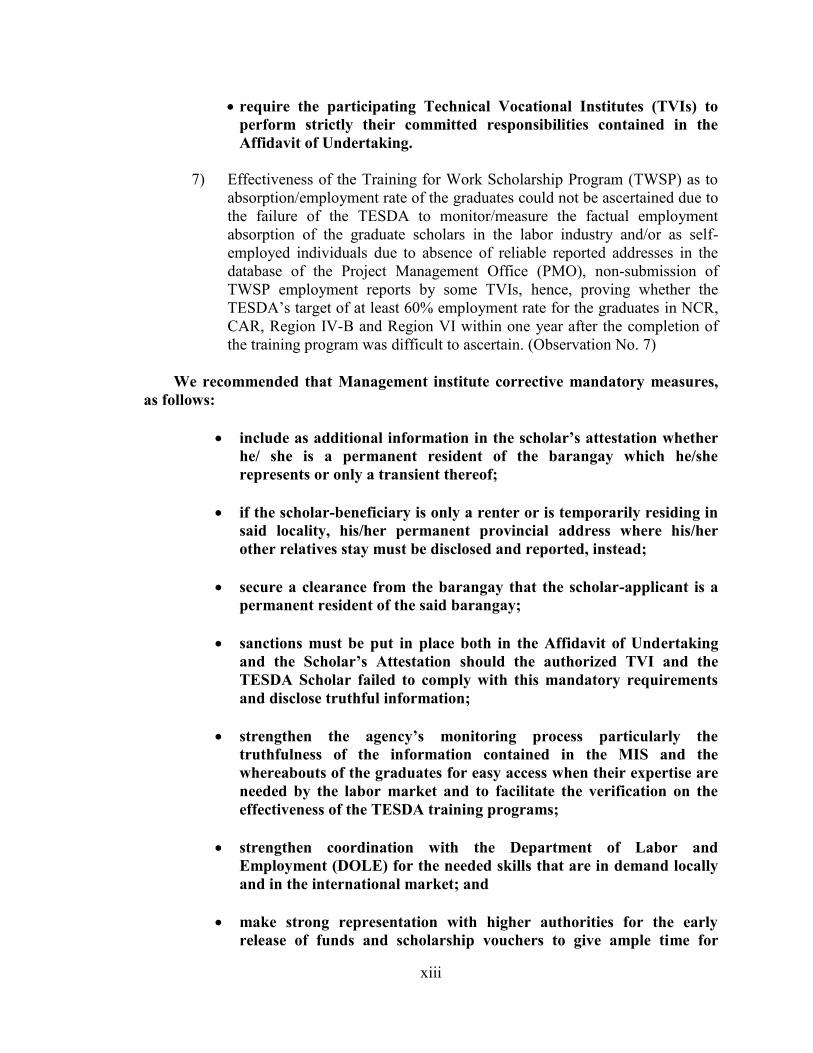

require the participating Technical Vocational Institutes (TVIs) to perform strictly their committed responsibilities contained in the Affidavit of Undertaking.

7) Effectiveness of the Training for Work Scholarship Program (TWSP) as to

absorption/employment rate of the graduates could not be ascertained due to the failure of the TESDA to monitor/measure the factual employment absorption of the graduate scholars in the labor industry and/or as self-employed individuals due to absence of reliable reported addresses in the database of the Project Management Office (PMO), non-submission of TWSP employment reports by some TVIs, hence, proving whether the TESDA’s target of at least 60% employment rate for the graduates in NCR, CAR, Region IV-B and Region VI within one year after the completion of the training program was difficult to ascertain. (Observation No. 7)

We recommended that Management institute corrective mandatory measures,

as follows:

include as additional information in the scholar’s attestation whether he/ she is a permanent resident of the barangay which he/she represents or only a transient thereof;

if the scholar-beneficiary is only a renter or is temporarily residing in said locality, his/her permanent provincial address where his/her other relatives stay must be disclosed and reported, instead;

secure a clearance from the barangay that the scholar-applicant is a permanent resident of the said barangay;

sanctions must be put in place both in the Affidavit of Undertaking and the Scholar’s Attestation should the authorized TVI and the TESDA Scholar failed to comply with this mandatory requirements and disclose truthful information;

strengthen the agency’s monitoring process particularly the truthfulness of the information contained in the MIS and the whereabouts of the graduates for easy access when their expertise are needed by the labor market and to facilitate the verification on the effectiveness of the TESDA training programs;

strengthen coordination with the Department of Labor and Employment (DOLE) for the needed skills that are in demand locally and in the international market; and

make strong representation with higher authorities for the early release of funds and scholarship vouchers to give ample time for

xiv

implementation of planned activities and programs to fully attain the objectives of the Training for Work Scholarship Program

8) Audit of prior year’s disbursements of PDAF showed that out of the P125,952,200.00 received by the agency for training program, P92,177,215.11 was disbursed, P12,986,674.89 for unbilled trainings, P1,500,000.00 was reverted to the National Treasury (NT), the balance ofP19,288,310.00 was said to be for remittance to the NT. Audit observations revealed that there were instances of overlapping schedules of trainees/scholars, trainings conducted with more than 25 scholars per batch, higher training cost and multi-availment of training by one scholar. (Observation No. 8)

We recommended that Management:

require the concerned TVIs to refund the excess/overpaid training

costs on the following:

a) Training cost in excess of allotment in the amount of P246,500.00; and

b) overpayment of the total amount of P802,000.00 due to overcharging of cost per scholar at P5,000.00 instead of P3,000.00;

explain in writing why the following should not be disallowed in audit:

a) training programs which were billed twice by two different training providers totaling P552,000.00; double billing/payment - P203,000.00;

b) attendance of 176 scholars in different training programs but the same training dates/period amounting to P1,056,000.00;

c) attendance of 69 scholars in the same training programs but different training period amounting P414,000.00;

d) discrepancy in the training cost; overcharging of P5,000.00 instead of P3,000.00 totaling P802,000.00;

e) conduct of training programs not accredited/registered with TESDA;

f) payment of training cost of shortened duration as compared to the duration of a whole training course; and

xv

g) payment of training costs despite discrepancies in the attached supporting documents.

intensify monitoring of the trainings conducted by TVIs;

review documents and/or issue affidavit on the veracity of erasures in

the attendance sheets, dates of training period, name and signature of the instructor and other documents with discrepancies and if found not in order, to cause responsible/accountable persons to answer for any lapses committed;

refrain from using unremitted/expired NCA’s (deposited in LCCA bank accounts) to augment unobligated disbursements amounting to P1,773,000.00;

require the Financial Analysts (FAs) to strictly adhere to the completeness of the required documents before certifying the DVs; and

remit the unexpended/excess PDAF to the National Treasury and furnish a copy of the validated deposit slip for audit purposes.

9) Other deficiencies were noted in the implementation of training programs,

such as: a) excess/overpayment of training cost to Sta. Cecilia College, Inc. by P26,500.00 due to over-charge of Training Cost for P500.00/scholar for 53 scholars on Tour Guiding Services NC II; b) two batches of trainings were conducted at the same time and place by the same instructor; c) inappropriate selection of scholars/beneficiaries as stipulated under TESDA Circular No. 23, series of 2011 dated October 10, 2011; d) failure to conduct mandatory assessment of 182 scholars; e) duration/no. of hours for the training Housekeeping NC II conducted by 102 GEM Training Center, Inc. were shortened to 4 – 52 hours, but training cost paid for P210,000.00 was allotted to 436 hours, as required under TESDA Order No. 59 series of 2009; f) excess no. of scholars per approved QMs resulted to unfunded obligation for P14,000.00, prompting the District to use the unutilized/unremitted funds of other QMs; g) supporting documents attached to the claims were not original copies neither authenticated nor certified as true copy and not duly signed by authorized representative and h) inadequate documentation. (Observation No. 9)

We recommended the District Focal Person/Management:

require the TVI, Sta. Cecilia College, Inc. to refund the P26,500.00 excess payment made for 53 scholars;

xvi

strictly adhere to the Implementing Guidelines set forth in TESDA Circular No. 23, s. 2011 dated October 10, 2011 for the implementation of the training programs funded under the PDAF;

require the FA to strictly review and scrutinize the completeness of the required documents before certifying the voucher for the claim/s; and

submit immediately the lacking documents to avoid issuance of Notice of Suspension (NS).

10) Administration of priority development scholarship programs implemented

by three (3) duly accredited Technical Vocational Institutions namely Asian Spirit Career Foundation, Inc., Asiantouch International Training Institute Inc. and Phil-Best Entrepreneurs, Inc. totaling P29,874,000.00 were not properly carried out which resulted in the following deficiencies thereby the President’s commitment to improve the lives of the people through employment, reduce poverty and build national competitiveness is not completely addressed:

Unrealistic offering of similar technology skills lumped in the same or

adjacent locality proved to be an insufficient alternative solution for job opportunities which run contrary to the guidelines set under Section Nos. 2.2.2 and 2.2.3 of TESDA Circular No. 23 dated October 10, 2011;

Skills that were not suited to address the immediate needs of the targeted community produced an unstable, temporary or non-employment of the beneficiary-graduates thereby limiting their chance of a reasonable opportunity of acquiring a permanent means of income and get themselves and their families out of poverty defeating the objectives and purposes provided under Section 2.1.2 and 2.2.1 of TESDA Circular No. 23 dated October 10, 2011, respectively; and

Lack of coordination between the district and the Technical Vocational Institution and inefficient monitoring resulted to a half-baked execution of the post-training mechanisms such as career guidance, counseling and employment facilitation depriving the graduates of the badly needed support for a guaranteed job placement which also contradicts Section No. 2.1.11 and Section 3.1 of said TESDA Circular No. 23 and Section Nos. 4.2, 4.3 and 6.2, TESDA Circular No. 4 dated February 13, 2013. (Observation No. 10)

We recommended that:

the District Offices and Management and training providers must apply the cluster of competencies prescribed in the Training

xvii

Regulations in designing the programs to be offered that would guarantee the employment of the scholars after graduation;

the training programs offered must match the needs of the community to be served and the requirements of business sectors which have high employment demands; and

the Focal Staff must provide regular written feedbacks to TESDA and its partners to update them on the progress of the post-training implementation and to coordinate with the Barangay for the identification, organization and establishment of a permanent contact and business location where everybody concerned, from the Implementers thru its Focal Staff, Training Institutions, its partners and the graduates themselves could meet, work, address problems and avail of needed services.

11) Trainings and assessments totaling P49,080,443.00 were conducted and

charged from the Priority Development Assistance Fund in violation of the Supreme Court Decision No. G.R. No. 208566 dated November 19, 2013 declaring the 2013 PDAF unconstitutional. (Observation No. 11)

We recommend that Managementrequire concerned TESDA officers and

employees written justification on why conduct of training and assessment was made after the issuance of the Temporary Restraining Order and after the promulgation of the Supreme Court Decision on the unconstitutionality of PDAF and was considered illegal, and therefore payment thereof be disallowed in audit.

12) Out of 1,680,302 nationwide backlogs of school armchairs and other furniture requirement of DepEd, only 3.5 percent or 58,643 were produced by TESDA since CY 2011-2014. The slow phase of deliveries of wood from DENR as reported attributed to the non-attainment of its objective to zero out backlogs in DepEd, as well as threaten the employment opportunity of the trainees. (Observation No. 12)

We recommended that the TESDA Management require the Bayanihan

Project Coordinator:

fast track production of armchairs to address the shortage that has been the perennial problem of DepEd during opening of the school year by revisiting the terms and conditions stated in the Memorandum of Agreement (MOA) and closely coordinating with the partner agencies;

request additional funds from PAGCOR as needed;

xviii

closely coordinate with DENR to provide the pre-cut wood sizes needed in the production of armchairs;

enforce the immediate implementation of other identified sites to

accommodate trainees in other regions; and

device necessary measures geared to solve the problems encountered in the production, to attain its objective otherwise defeating the purpose to alleviate shortage of armchairs in DepEd.

13) The amount of P313,286,791,60 or 37.67 percent of the total NCA of

P831,721,823.00 released by the Department of Budget and Management (DBM) for TESDA’s operating requirements for the first and second semester was unutilized/reverted to the National Treasury although record showed that accounts payable amounting to P13,370,391.05 remained unpaid as of December 31, 2014, therefore showing non-maximization of NCA received as of yearend which also affected the disbursement performance of the agency in line with the principle/purpose of National Budget Circular (NBC) No. 550 dated October 29, 2013. (Observation No. 13)

We recommended that Management:

maximize the use of NCA received vis-à-vis monthly disbursement

program and financial plan to speed up implementation of projects and avoid lapsing of cash allocation on the last day of the 3rd month of the quarter;

prepare realistic cash program to cover payment for current year and

prior years’ requirements (accounts payables as well as not due and demandable obligations but are expected to become A/Ps during the current year); and

fast track processing of papers to facilitate payment due to creditors

for a given period.

14) The TESDA consolidated balance of Cash-Local Currency Current Account (LCCA) amounting to P1,742,985,257.59 maintained in an AGDB included cash balances out of the amount transferred by the Regional Office to Provinces/Districts in the amount of P1,554,676,200.47 or 89.20 percent of the aggregate LCCA accounts with no specific authority or legal basis thus, violates EO No. 431 dated May 30, 2005 and PC JC No. 4-2012 dated September 11, 2012 and non-remittance of this amount affected the sound cash programming of the government. (Observation No. 17)

xix

We recommended that Management:

maximize the use of the quarterly NCA cum LCCA to meet the training program’s obligations within the implementation of the period of particular program/project/activity to avoid incurring unutilized cash allocations;

remit to NT all cash balances maintained in LCCA bank accounts

without legal authority or legal basis; and

require the acting financial analyst/acting accountant of the Regional Offices to prepare and submit within the prescribed period the monthly Bank Reconciliation Statements (BRS) pursuant to Section 74 of PD 1445, COA Circular No. 96-011 and Item 2.1.4 of COA Circular No. 92-125A and to avail of the on-line facility of their government servicing bank to view and print the agency’s bank statement in order to come up with a timely report; and

15) Outstanding unliquidated cash advance still remained at P4,737,413.93 as of

year-end because of the practice of the agency in granting additional cash advances although previous cash advances were not yet liquidated. Likewise, cash advance granted to employees of TESDA-Southern Isabela College of Arts and Trades for travelling expense were inadvertently recorded as expense without liquidation. Also, in TESDA-Provincial Office of Aklan, inconsistencies where found between the liquidation of cash advances posted in the General Journal and the reported amount liquidated/reflected in the Status of Cash Advances and Liquidations which affected the reliability and accuracy of account Advances to Officers and Employees and appropriate expense accounts. (Observation No. 20)

We recommended that Management:

adopt a stricter measures to account for outstanding unliquidated

cash advance by: –

a. strictly enforcing the submission of liquidation documents as soon as the purpose of CA has been served, within the prescribed period or when a new CA is necessary, whichever period is earlier; and

b. imposing sanctions against accountable officers who continue to

neglect their obligations in accordance with the provision of COA Circular No. 97-002 dated February 10, 1997 and E.O. No. 298 dated March 23, 2004.

xx

stop the practice of recording the cash advances as expense. Prepare adjusting entries of the affected accounts, Likewise impose the regulation of no cash advance shall be allowed for employees with outstanding cash advance and shall require the immediate liquidation of the cash advance pursuant to Section 2.2.2 of COA Circular No. 96-004 dated April 19, 1996; and

ensure that liquidations posted in the General Journal are duly

supported with the corresponding Liquidation Reports for the specific month, and all Liquidation Reports during the month be duly posted on the same period.

16) The balance of Accounts receivable is understated by the amount of P26,051,553.79 due to non-recording of the accounts. Also receivables amounting to P1,699,681.01 lack billing statements and subsidiary ledgers to support the claim therefore, casting doubt on the reliability and accuracy of the accounts receivables as of year-end balance. (Observation No. 21)

We recommended that Management:

exercise diligence to classify specific accounts used in recording

transactions as prescribed in the Revised Chart of Accounts (RCAs) for National Government Agencies (NGAs) under COA Circular No. 2013-002 dated January 30, 2013;

enforce the immediate settlement of the said disallowances. If the

persons liable are no longer with the TESDA, or have been transferred to other regions or agencies, or are no longer in service, send demand letters requiring them to settle their respective disallowance to avoid unnecessary sanctions; and

prepare the JEVs to effect the necessary corrections/adjustments in

order to reflect the correct accounts and balances;

d. conduct periodic reconciliation should be made between the reciprocal accounts in order to make sure that the balances are always reconciled.

17) Transfer of funds to NGOs/POs, NGAs, LGUs and Operating Units totaling P51,965,757.03 from TESDA Regions V, VI and XIII amounting to P33,013,076.61P13,356,180.42 and P5,596,500.00, respectively which were intended for personnel Services and Maintenance and Other Operating expenses and for use of various projects such as establishment of Livelihood Resource Centers, allowances for trainees training conducted by LGUs, etc., remained unliquidated at year end. (Observation No. 23)

xxi

We recommended that Management:

issuedemand letters to NGOs/POs, NGAs, LGUs and Operating Units concerned requiring the immediate liquidation of funds to be supported with a copy of the disbursement vouchers indicating the amount released to them, require them to refund the fund transferred in case of failure to liquidate;

verify whether the NGO/POs are still existing, if no longer existing

and liquidation is impossible, initiate proper disposition of the accounts in accordance with COA Circular 97-001 (Guidelines on the Proper Disposition/Closure of Dormant Funds and/or Accounts of National Government Agencies) considering that the accounts have been non-moving for five consecutive years;

plan its strategies in monitoring the actual implementation of the

funded projects and submission of financial and accomplishment reports by the implementing agencies. The planned strategies should be executed right away in order to clear the books of the agency from balances which have been carried in the books for over ten years especially for Due from NGO/POs and Due from LGUs;

require the Local Executive Chief of LGU’s with unliquidated fund

transfers from TESDA Surigao del Norte and Surigao del Sur Provincial Offices to submit the liquidation documents, as agreed upon in the Memorandum of Agreement (MOA); and

observe strictly the provisions of COA Circular No. 94-013 dated

December 13, 2994 on the grant, utilization and liquidation of fund transfers.

18) Non-compliance with rules and regulations affected the validity, accuracy

and reliability of the inventory accounts totaling P22,067,384.68 of NCR and Regions I, III, IV-A, V, VI, XIII and X due to the absence/non-completion of inventory reports/records amounting to P19,120,085.34 direct charging to expense account of purchases of P2,947,299.34. (Observation No. 25)

We recommended that the TESDA Provincial Offices to implement the following:

require the Property/Supply Officers concerned together with the Inventory Committee to conduct physical count of inventories on a regular basis and to submit the report thereon on the required date in compliance with the foregoing regulations;

xxii

require the Accountant to record all purchases of inventory items in the respective inventory account pursuant to Section 43, Vol. I of the MNGAS;

remind both the Accounting Unit and the Supply Office to maintain

the Supplies Ledger Cards (SLCs) and the Stock Cards (SCs), respectively for each inventory stocks for check and balance and for fair presentation of the inventory account in the provincial offices’ financial statements;

prepare the Journal Entry Voucher (JEV) and effect the necessary

adjustments to reflect the correct inventory account balances for the supplies and materials in the stockroom as at year-end;

prepare and update data in Report of Supplies and Materials Issued (RSMI) and Accounting and Supply Office should regularly reconcile its records; and

cause the conduct of physical inventory semi-annually or at least once

a year pursuant to Section 46, Vol. I of the Manual on New Government Accounting System (MNGAS).

19) The validity, accuracy, and existence of the TESDA consolidated Property,

Plant and Equipment amounting to P2,860,116,964.38 as of December 31, 2014 is unreliable due to the absence of Report on the Physical Count of Property, Plant and Equipment (RPCPPE), property cards/PPE Ledger Cards totaling P438,760,820.19, reporting difference between inventory report and the books of account of P17,998,678.47 and unrecorded PPE/error in recording and inclusion of obsolete/ unserviceable property resulting to net overstatement of P13,954,197.65. (Observation No. 26)

We recommended that Management and concerned officers:

require the Inventory Committee to prepare the RPCPPE every year

to be submitted to the Accounting Office to updaterecords of property/equipment subsidiary/general ledger accounts;

require the Accountant and Property Officer to maintain an updated

property cards and equipment subsidiary ledgers, respectively;

require the Accountant to effect the necessary adjusting entries for misclassified, erroneous entries to reflect a more reliable balance of PPE accounts in the financial statements; and

require the Accountant and Property Officer to regularly monitor the

movement or increases or decreases of PPE accounts to facilitate

xxiii

reconciliation of respective records to show true balances of each PPE account in the financial statements.

20) The correctness and validity of the account Accounts Payable totaling

P969,842,572.56 as of December 31, 2014 is doubtful due to: a) net overstatement of account in NCR and Region VIII amounting to P21,810,647.10; b) in Region II liability is not supported with complete documentations in the amount of P11,900,290.00; c) non-reversion of undocumented and unclaimed payables, claims with no valid claimants and outstanding for over two (2) years or more of NCR, CAR, Region I, V, and VIII totaling P22,985,060.06; d) non-submission/preparation of Region IV of schedule of subsidiary balances amounting to P13,193,298.67. (Observation No. 27)

We recommended that Management:

avoid recording of liabilities without valid claimants;

verify and analyze long outstanding payables;

revert to the unappropriated surplus of the general fund accounts

payable balances which have been outstanding for more than two years;

direct the Financial Analyst and Budget Officer to review the legality

and validity of obligation to warrant payment, and if proven futile, effect reversion of the long outstanding accounts; and

stop obligating unutilized cash allocation, record only valid

obligations.

Further, we recommended the Regional TESDA Management to:

direct the Accountant of TESDA Benguet and Pangasinan PO to immediately revert to the unappropriated surplus of the General Fund the outstanding undocumented accounts payable;

require the Financial Analyst of Sorsogon PO to conduct an

evaluation of the payable accounts aged over one year and determine the causes of its non-payment to creditors, and effect payments for due and demandable accounts to reduce the liabilities of the Agency; and

direct the Financial Analyst of TESDA-RTC of Region VIII and Bukidnon PO Region X to prepare a Journal Entry Voucher to record

xxiv

an adjusting entry to correct accounts payable amounting to P88,123.50.

21) Various disbursements totaling P139,373,487.33 including payments of

salary, honoraria, professional/ personnel benefits monetization, overtime pay, traveling expense, rent expense, representation expenses, communication expense, various repairs and procurement not supported with adequate documentation or not included in the annual procurement plan; the disbursement vouchers of which have not been submitted for post-audit, thus casting doubts on the validity and propriety of expenditures. (Observation No. 29)

We recommend that Management:

comply with the prescribed guidelines relative to pertinent rules and

regulations on the payment of monetization, overtime pay, gasoline expenses, repairs of equipment, communication expenses, rental and procurement of goods and services;

submit documents that will support the validity and regularity of the

disbursements; and require the concerned personnel to comply with Section 100 of PD

1445 on the submission of monthly reports of the agency transactions not later that the 5th day of the following month to the office of the Auditor.

22) Amounts of Suspensions/Disallowances/Charges found in audit and still not

settled totaled P198,738,541.68 as of December 31, 2014 which is not in accord with Sections 5.4, 7.1 and 10.4 of the pertinent rules in the Rules and Regulations on Settlement of Accounts (RRSA) prescribed under COA Circular No. 2009-006 dated September 15, 2009. (Observation No. 34)

We recommended that Management:

direct concerned officers and employees and other concerned party to

settle respective suspensions, disallowances and charges in accordance within the prescribed period as required by rules and regulations in the settlement of accounts; and

henceforth require concerned officers and employees to strictly observe/follow laws, rules and regulations in order that transactions and payments made thereof are in accordance with the tenet of good governance.

xxv

H. IMPLEMENTATION OF PRIOR YEARS’ AUDIT

RECOMMENDATIONS

Out of the 100 audit recommendations embodied in the previous years’ CAAR, 25 were fully implemented, 56 were partially implemented and 19 were not implemented. Details are presented in Part III of the Report.