evonik. power to create. - platts · source: linde and encyclopaedia of hydrocarbons platts...

TRANSCRIPT

Platts 2nd Annual

Petrochemical

Conference

Stephen Bowers

BL PI Strategy 2014 – BU Workshop 10/11 April 2014 in Hünxe Page 2

Topics in the News

2

• Oil Pricing- how low and for how long will oil pricing remain

depressed

• EU growth outlook – who will benefit from low oil pricing

• Impact of potential Greek Exit from Euro (ongoing)

• China growth prospects

• Outlook for European chemical producers

Platts Petrochemical 2015

Low Oil Pricing

Winners or Losers?

Platts Petrochemical 2015 Page | 3

Winner or

Loser

Oil and Gas

Producers

Base

Chemical

Producers

Transport Manufacturing

Tourism

Services

Retail

Construction

Oil , Gas and Coal Thermal

Equivalents

Platts Petrochemical 2015 Page | 4

Relative to oil, gas and coal remain highly competitive for thermal

applications.

Oil remains the only viable option for bulk transport fuels (gasoline, jet,

diesel) and for some base chemical production – e.g. aromatics

$/MMBTU $/BOE $/MTE

Natural Gas 1-8 6-48 50-400

Crude Oil 8 50 365

Thermal Coal 2-3 13-20 66-100

Crude Oil to

Olefines

A possibility or wishful thinking?

Stephen Bowers

March 2015

BL PI Strategy 2014 – BU Workshop 10/11 April 2014 in Hünxe

Disclaimer

•This presentation contains forward-looking statements and

opinions concerning the general global economic condition and

that of the oil, gas and light olefines industry. Evonik Industries

AG does not warrant the reliability, accuracy or completeness of

any information contained in this presentation and, to the extent

permitted by the applicable law, disclaims any and all

responsibility for any loss or damage (including without limitation

consequential, indirect or economic losses and damages) arising

in any way, including by reason of negligence for errors or

omissions in this presentation.

•You should therefore seek independent verification of any

information presented herein that you intend to rely on, and

consult your professional advisors to determine the course of

action appropriate to you.

•Where possible this information has been gained from public

sources that are widely available free of charge and to the best of

our knowledge has not infringed any terms of use or copyright.

Page 6

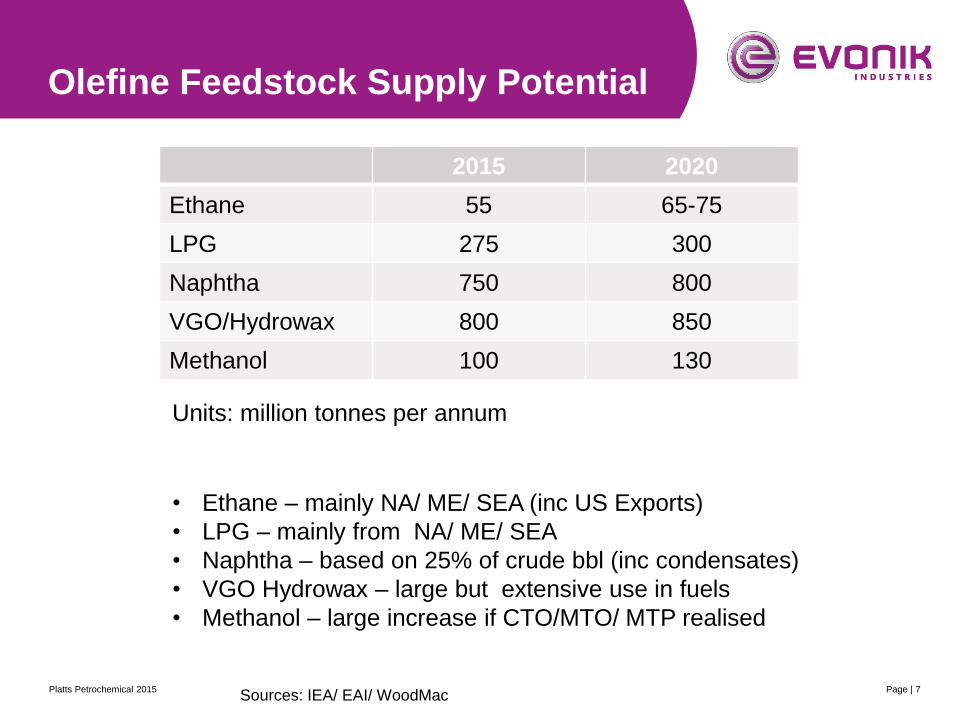

Olefine Feedstock Supply Potential

Page | 7

2015 2020

Ethane 55 65-75

LPG 275 300

Naphtha 750 800

VGO/Hydrowax 800 850

Methanol 100 130

• Ethane – mainly NA/ ME/ SEA (inc US Exports)

• LPG – mainly from NA/ ME/ SEA

• Naphtha – based on 25% of crude bbl (inc condensates)

• VGO Hydrowax – large but extensive use in fuels

• Methanol – large increase if CTO/MTO/ MTP realised

Units: million tonnes per annum

Sources: IEA/ EAI/ WoodMac Platts Petrochemical 2015

Page | 8

Why Crack Crude Oil?

Global crude oil supply (2015)

• Approx 4200 million tonnes crude oil and condensates

• Approx 450 million tonnes petroleum gases

Cracking crude oil to olefines would –

• Increase potential olefine feedstock supply

• Reduce the need for expensive refinery assets

• Reduce dependency on naphtha for ethylene production

• Provide additional co-products (butadiene and aromatics)

Downsides -

• There is no standard crude oil

• Crude oil ranges from C2 to C50+ carbon chain length

• Species composition (PONA) varies according to source

Platts Petrochemical 2015

Composition of European Crudes

Page | 9

Each crude oil is characterised by an assay

• Most important is the boiling range and distribution of components.

• Benchmark Brent contains around 26.5 Wt % light and heavy naphtha.

• Other important paramaters are the PONA, sulphur, metals and condensable carbon

Source : TOTSA

Coke Precursor !

Platts Petrochemical 2015

US Light Sweet Crudes -

comparison

Page | 10

US Tight Oil production

• Eagle Ford and Bakken

tight oil production.

• LLS and WTI crude oil

benchmarks

• LLS and WTI

referenced to Brent

• Tight oil now accounts

for about 3.5 million out

of 9 million barrels of

US oil production.

Source: Platts Platts Petrochemical 2015

Crude Supply, Gravity and Sulphur

Page | 11

Source: David Wood and Associates

Sweet Sour

Light

Heavy

Platts Petrochemical 2015

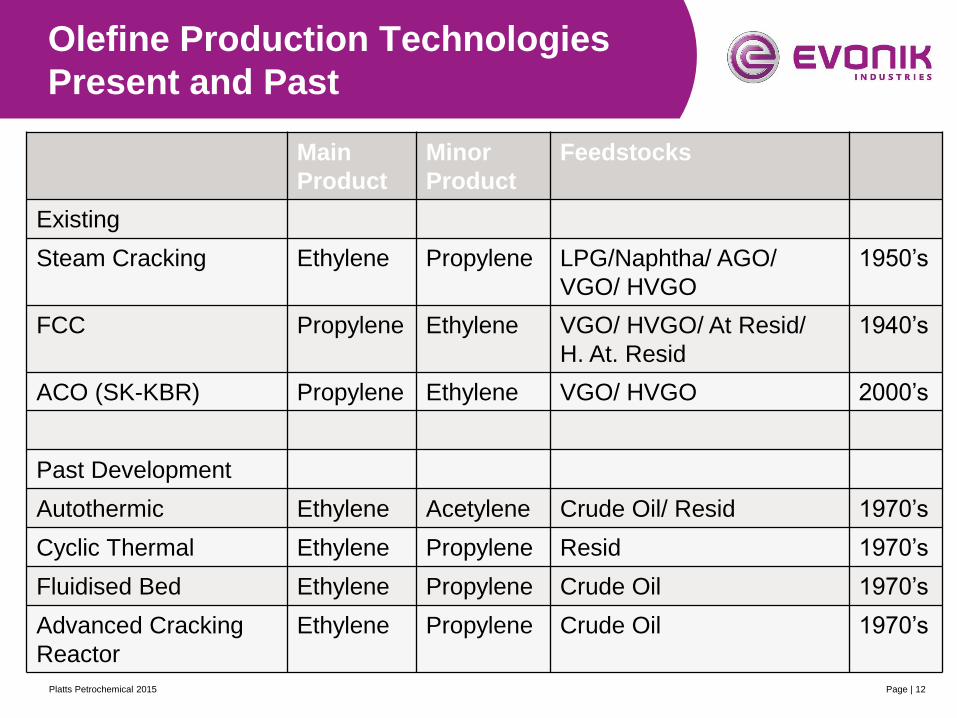

Olefine Production Technologies

Present and Past

Page | 12

Main

Product

Minor

Product

Feedstocks

Existing

Steam Cracking Ethylene Propylene LPG/Naphtha/ AGO/

VGO/ HVGO

1950’s

FCC Propylene Ethylene VGO/ HVGO/ At Resid/

H. At. Resid

1940’s

ACO (SK-KBR) Propylene Ethylene VGO/ HVGO 2000’s

Past Development

Autothermic Ethylene Acetylene Crude Oil/ Resid 1970’s

Cyclic Thermal Ethylene Propylene Resid 1970’s

Fluidised Bed Ethylene Propylene Crude Oil 1970’s

Advanced Cracking

Reactor

Ethylene Propylene Crude Oil 1970’s

Platts Petrochemical 2015

Low Severity Steam Cracking Yields

Yields in Wt % on feed flow

Page | 13

FRN AGO VGO Hydrowax

P/E (severity) 0.66 0.7 0.72 0.59

Methane/ Hydrogen 13.3 9.9 7.0 11.8

Ethylene 25.5 21.9 19.4 26.0

Propylene 17.0 15.3 13.9 15.3

Butadiene 4.5 4.9 5.0 8.0

Butenes/ Butane 7.3 6.1 7 4.2

C5’s 4.9 3.6 4.4

Benzene 4.0 4.5 4.0 5.6

C6+ 15.2 11.4 14.9 11.2

Fuel Oil 2.5 17.5 25.0 8

Others 5.8 4.8 4.8 5.5

Ethylene +

Propylene

42.5 37.2 33.3 41.3

Source: Various (Eni/ Linde/ Lummus/ Ullmans/ Evonik model) Platts Petrochemical 2015

Page | 14

Ethylene Pyrolysis Furnace

Ethylene pyrolysis furnace operating

conditions (single unit)

Source: Linde and Encyclopaedia of Hydrocarbons

Platts Petrochemical 2015

Exxon 1970’s Patent US3617493 Crude Oil Steam Cracking using flash drums

Page | 15

Pseudo Vacuum

Residue 510+ °C

Naphtha/ Kerosine

0-230°C

AGO/ VGO

230-600 °C

Flash Drum 1

Flash Drum 2

Furnace 1

Furnace 2

In 1970 Exxon filed this patent which

claimed a process for the preparation

and steam cracking of crude oil.

• The whole crude is heated in the

convection section of Furnace 1

and then flashed in Falsh Drum 1.

• The flashed vapour has a boiling

range of about 0-230°C containing

naphtha and kerosine fractions

which are cracked in Furnace 1

• The reduced crude is heated in the

convection section of Furnace 2

and then flashed in Flash Drum 2.

• The flashed vapour has a boiling

range of about 230-600 °C

containing AGO and LVGO

fractions which are cracked in

Furnace 2.

• The pseudo vacuum residue is

used as fuel oil

Actual patent drawing

Source : Patent US 3617493 Platts Petrochemical 2015

Equistar Patent US 6743961 B2 (2004)

Crude oil steam cracking using mild pre-cracking

Page | 16

Equistar 2004 patent using mild

thermal pre-cracking.

• Whole crude is first preheated

and then transferred to mild

thermal cracker.

• First zone flashes vapours to

steam cracker

• Second zone reacts liquids

with high temperature steam to

promote mild cracking.

• Packing reduces carryover of

liquid droplets

• Coke is deposited in bottom of

mild cracker.

• Periodic de-coke of mild

cracker using steam.

• Process designed to use very

light 45 API Saharan Blend

crude oil (10% vac residue)

Source: US Patent 6733961 B2 Platts Petrochemical 2015

Subsequent Variations

Page | 17

Exxon, Equistar (LBI) and Shell have all patented many variations for steam

cracking feedstocks containing residue. They include but are not limited to:

• Visbreaking the residue stream

• Hydrovisbreaking the residue stream

• Coking of the residue stream either by delayed or fluid coking

• Hydroprocessing and thermal cracking of the residue stream

• Fluid catalytic cracking of the heavy stream containing residue followed by

hydroprocessing of the light cycle oil (LCO) and subsequent steam cracking

of the HLCO.

Exxon, have by far posted the greatest number of patents, and continue to

develop new variations for cracking whole crude or residues in “conventional

steam pyrolysis” plants.

Platts Petrochemical 2015

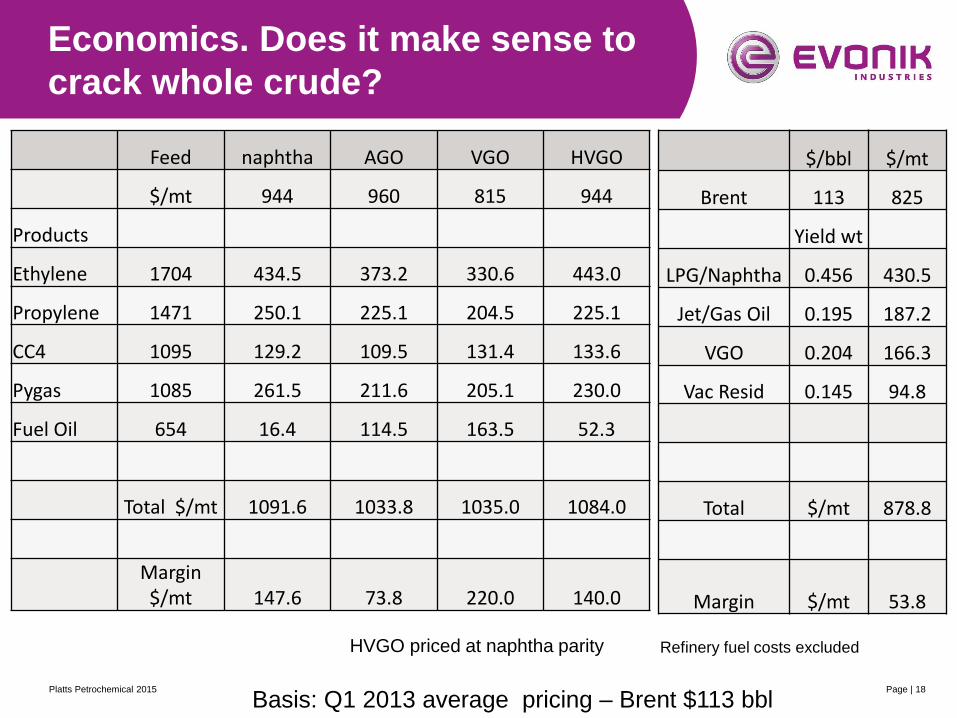

Economics. Does it make sense to

crack whole crude?

Page | 18

Feed naphtha AGO VGO HVGO

$/mt 944 960 815 944

Products

Ethylene 1704 434.5 373.2 330.6 443.0

Propylene 1471 250.1 225.1 204.5 225.1

CC4 1095 129.2 109.5 131.4 133.6

Pygas 1085 261.5 211.6 205.1 230.0

Fuel Oil 654 16.4 114.5 163.5 52.3

Total $/mt 1091.6 1033.8 1035.0 1084.0

Margin $/mt 147.6 73.8 220.0 140.0

$/bbl $/mt

Brent 113 825

Yield wt

LPG/Naphtha 0.456 430.5

Jet/Gas Oil 0.195 187.2

VGO 0.204 166.3

Vac Resid 0.145 94.8

Total $/mt 878.8

Margin $/mt 53.8

Basis: Q1 2013 average pricing – Brent $113 bbl

HVGO priced at naphtha parity Refinery fuel costs excluded

Platts Petrochemical 2015

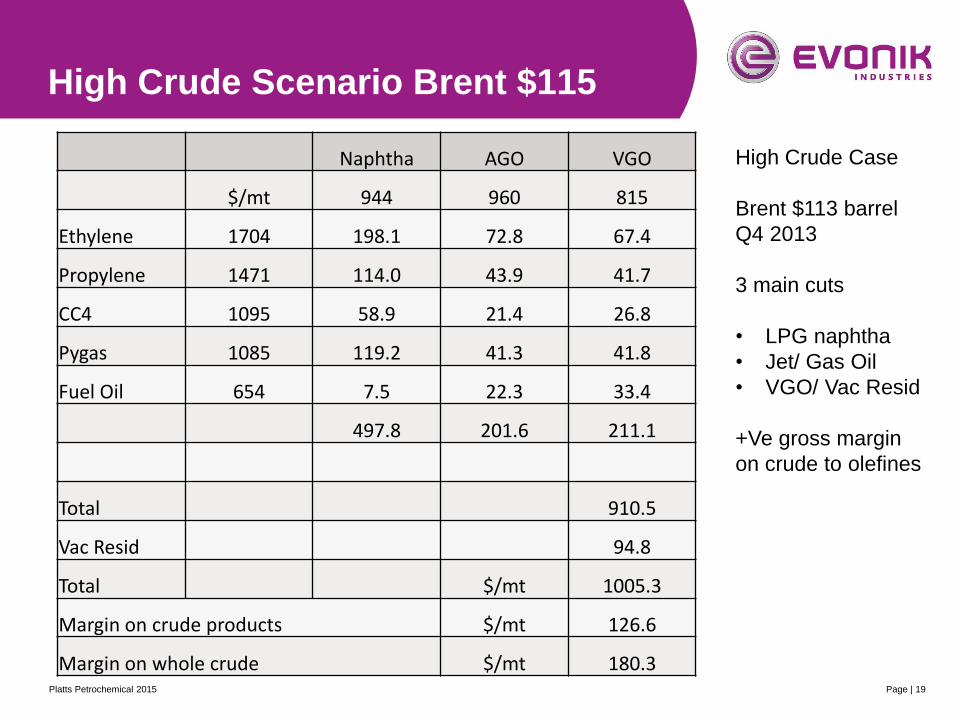

High Crude Scenario Brent $115

Page | 19

Naphtha AGO VGO

$/mt 944 960 815

Ethylene 1704 198.1 72.8 67.4

Propylene 1471 114.0 43.9 41.7

CC4 1095 58.9 21.4 26.8

Pygas 1085 119.2 41.3 41.8

Fuel Oil 654 7.5 22.3 33.4

497.8 201.6 211.1

Total 910.5

Vac Resid 94.8

Total $/mt 1005.3

Margin on crude products $/mt 126.6

Margin on whole crude $/mt 180.3

High Crude Case

Brent $113 barrel

Q4 2013

3 main cuts

• LPG naphtha

• Jet/ Gas Oil

• VGO/ Vac Resid

+Ve gross margin

on crude to olefines

Platts Petrochemical 2015

Economics. Does it make sense to

crack whole crude?

Page | 20

naphtha AGO VGO HVGO

$/mt 393 469 330 393

Ethylene 1038 264.7 227.3 201.4 269.9

Propylene 985 167.5 150.7 136.9 150.7

CC4 344 40.6 34.4 41.3 42.0

Pygas 449 108.2 87.6 84.9 95.2

Fuel Oil 238 6.0 41.7 59.5 19.0

Total 586.9 541.6 523.9 576.8

Margin 193.9 72.6 193.9 183.8

$/bbl $/mt

Brent 51.4 375

Yield wt

Naphtha 0.456 179.2

Gas Oil 0.195 91.5

VGO 0.204 67.3

Vac Resid 0.145 34.5

Total $/mt 372.5

Margin $/mt -2.7

Basis: Q1 2013 average pricing – Brent $113 bbl Platts Petrochemical 2015

HVGO priced at naphtha parity Refinery fuel costs excluded

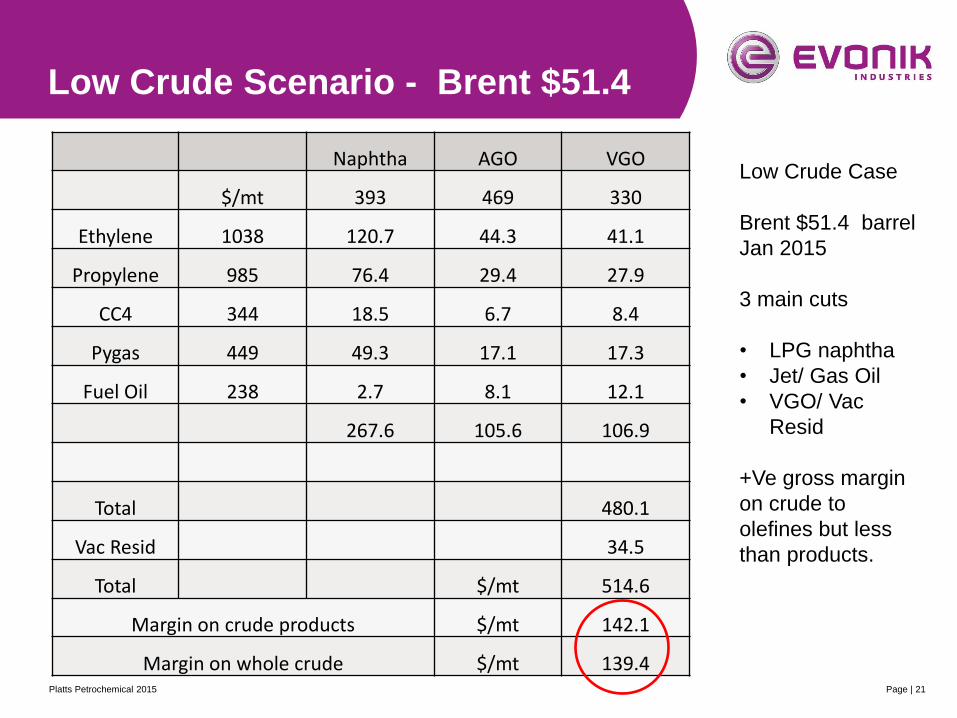

Low Crude Scenario - Brent $51.4

Page | 21

Naphtha AGO VGO

$/mt 393 469 330

Ethylene 1038 120.7 44.3 41.1

Propylene 985 76.4 29.4 27.9

CC4 344 18.5 6.7 8.4

Pygas 449 49.3 17.1 17.3

Fuel Oil 238 2.7 8.1 12.1

267.6 105.6 106.9

Total 480.1

Vac Resid 34.5

Total $/mt 514.6

Margin on crude products $/mt 142.1

Margin on whole crude $/mt 139.4

Low Crude Case

Brent $51.4 barrel

Jan 2015

3 main cuts

• LPG naphtha

• Jet/ Gas Oil

• VGO/ Vac

Resid

+Ve gross margin

on crude to

olefines but less

than products.

Platts Petrochemical 2015

Is Crude to Olefines Viable?

Page | 22

Basic Observations and Conclusions

• Crude to olefines via steam cracking is possible as long as the

residue is removed. Whole crude processing is not possible

• Light Sweet Crude is the only viable option- lighter the better

• Gas Oil fractions will crack but have higher value options elsewhere

• VGO is potentially a very attractive feedstock but Sulphur removal

would be a major issue and cost.

• Hydrotreated VGO is a very attractive option, even more so if mildly

hydrocracked, and is already practised (Shell, BP)

• Residues can be coked, deasphalted or hydrocracked.

• Many integration options exist. Platts Petrochemical 2015

Naphtha and LPG pricing 2011-2014

Platts Petrochemical 2015 Page | 23

Naphtha $/mt

Butane $/mt

Propane $/mt

Source : IHS Monthly Spot prices for WE

Page | 24

Does cracking of crude oil make sense?

• Light feeds – C2,C3 and C4 consistently offer better economics over

naphtha for ethylene production.

• Crude oil steam cracking would be typically compared to naphtha cracking

and as a result does not show a compelling economic case.

• High oil pricing suggests higher margins on crude, but is offset by the

consistently lower costs for lighter feedstocks (C2,C3,C4).

• Though many patents exist, there are no known examples of whole crude

oil cracking currently, though Exxon (Singapore) and Saudi Aramco (KSA)

claim to have flexible crackers that can process some “crude oil” (Exxon -

operational, Saudi Aramco in design stage).

• Integration with a refinery would appear to be the best option.

Platts Petrochemical 2015

Seite | 25

Petrochemical Refinery Flowsheet

with Integrated Naphtha Cracker

Page | 26

Distillation

Residue Hydrocracker

Residue FCC

Naphthas to SC

15 million tonnes crude, 1.1 million tonnes ethylene SC, 5 million tonnes RFCC 900 kt propylene Platts Petrochemical 2015

Brent Blend Assay 2011

Page | 27 Platts Petrochemical 2015