eversheds’ trade finance and sanctions seminar - 26th november, dubai

TRANSCRIPT

Trade finance and sanctions

An update on key

developing issues

26 November 2014 – Dubai

Trade finance and sanctions

An update on key

developing issues

26 November 2014 – Dubai

King Tak Fung – PartnerMichael Yau – Partner

26 November 2014

International trade finance workshop

Introductions

• Exchange Name Cards

• Introduce yourself to your colleagues

• Summarise what your group wants to achieve today

Background & key focus

TOPICS

W: W: W:W: W: H:

A. Warehouse Financing

B. PRC Law on L/C Fraud & Injunctions

C. Governing Law

D. Classic Injunction Case - SPC

E. Bank Guarantee Case

Topics to discuss

Warehouse financing

WarehouseReceipts to Financing Banks

WarehouseReceipts to Collateral Managers

WarehouseOperator

WarehouseReceipts to Financing

Banks

WarehouseReceipts to Financing

Banks

WarehouseReceipts to Collateral Managers

WarehouseReceipts to Collateral Managers

CMA

Pledge Agreement

(Borrower)

(CollateralManager) Goods

(Lending Bank)

Import Agent(Applicant)

Sellers(Beneficiaries)

L/C IssuingBank

2. LC Application.

3. NegotiationContract

4. ReimbursementContract

UltimateBuyer

1. Agency Contract.Collateral

Manager’s W. R. to overseas

co. for L/C negotiation

Forged BL based on genuine

information

NegotiatingBank

Letter of credit fraud

Forged or fraudulent doc.

created or presented by

bene.w.o. notice??

Carrier

No shipment(bad faith) orgoods no value!

Bene. & appli. or 3rdparty collaborate topresent fraudulent doc.w.o. genuine transaction.

Other L/C Fraud

Fraud Exception (Art. 8)

Art. 8 + Irreparable

Damage

Confirming bank honoured its

payment undertaking in

good faith

Pyt already made by

nominated party in good

faith

$Doc. Negotiated

in good faith

Stop Payment Orders – Exception (Art 9 & 10)

Issuing Bank

Discounting Bank

Sinotani v. ABC

Please

discount.

Sent to

ABC

1. We acceptthe doc.

& will pay onmaturity.

2. Discounted

•Governing law - available with ABC by acceptance?

•May ABC refuse payment?

• Agritrade v ICBC Case – available by negotiation in HK

•Marconi v Pan Indonesia Bank – available by negotiation in England but no negotiation

Pass to CM and then to supplier

(4) Pre doc & got acceptance Nego

Bank

(3) Negotiation

(4) Release doc

PRC Injunction – L/C Autonomy

(2) Usance L/C

L/C issuing bank in China

Supplier

(1) Import Agt

PRC Import Agent

Buyer

Subjective or Objective Test?

Intent to defraud

Burden of Proof

I am totally convinced.

Negligence=

Bad faith

Good or bad faith?

Import Agent(Applicant)

Seller(Beneficiary)

L/C IssuingBank

3. LC App.

6. Nego. C.5. Adv. C.

AdvisingBank

NegotiatingBank

UltimateBuyer

1. Agency C.

SWIFT

Independence principle

Silent confirmation

Import Agent(Applicant)

Seller(Beneficiaries)

L/C IssuingBank

3. LC App.

6. Nego. C.5. Adv. C.

Advising Bank

NegotiatingBank

UltimateBuyer

1. Agency C.

7. Reim C

Foreign companiesset up

Import Agent(Applicant)

Seller(Beneficiaries)

L/C IssuingBank

3. LC App.

6. Nego. C.

NegotiatingBank

UltimateBuyer

1. Agency C.

7. Reim C

What did the bank staff do and get?

Ultimate Buyer

Applicant(unconnected)

Beneficiaries

L/C IssuingBank

LC App. Fin. C.

NominatedBank

Reim. C.

Adv. C.

Advising Bank

Guarantor

Warrants checking

Documentationchallenges

Mitigation

Barclays Bank (England)

English Suppliers

(3) Guarantee

1st demand & w.o. proof or

condition

L/CUnconfirmed & conditional

(1)Sales Contract

(Libyan jurisdiction)

Independence of Bank Guarantee

Buyers (Libya)

(2) Counter-Guarantee Umma Bank (Libya)

•Edward Owen Engineering Ltd. v. Barclays Bank International Limited

1. Fraud? 2. Even if fraud – injunction against Umma?

3. Is no remedy against the buyers in Libya a valid ground for injunction?

4. Precautionary measures for the suppliers

How is your performance?

Fraud Detector

For more information or advice please contact:

King Tak FungPartner+852 2186 [email protected]

Michael YauPartner+852 2186 3237 [email protected]

Zia Ullah – PartnerJames Robinson – Partner

26 November 2014

Financial sanctions workshop

UK sanctions

Sources Targets Impact Obligations Penalties

UNSCR EU regs UK regs CTA 2008 TAFA 2010

Individuals- assets- travel

Entities- assets

Sectors- oil and gas- precious metals

Governments

UK citizens UK

incorporated bodies

Extraterritorial effect

Freeze funds No economic

resources (directly/indirectly)

No circumvention

Individual: - imprisonment and/or unlimited fine)

Corporate entity:- unlimited fine

The UK sanctions regulators

• Foreign and Commonwealth OfficeFCO

• Her Majesty’s TreasuryHMT

• Department for Business Innovation and SkillsBIS

• Her Majesty’s Revenue and CustomsHMRC

• Financial Conduct AuthorityFCA

The UK sanctions regulators

• policyFCO

• financial sanctions (consolidated list)/breaches/licencesHMT

• trade sanctions/licencesBIS

• trade breachesHMRC

• regulated persons/SYSCFCA

• individuals and entities subject to asset freeze

Consolidated

• financial institutions subject to restrictionsUkraine Investment ban

• not in useConfidential

• individuals and entities with Iranian linksBIS Iran

• organisations banned in the UKUKHO proscribed terror

organisations

The UK sanctions regulators

Current UK regime list

Afghanistan

Al-Qaida & Taliban

Belarus

Democratic Republic of

Congo

Egypt

Eritrea

Federal Republic of

Yugoslavia & Serbia

Iran

Iraq

Ivory Coast

Lebanon and Syria

Liberia

Libya

North Korea (Democratic

People’s Republic of

Korea)

Republic of Guinea

Republic of Guinea-Bissau

Somalia

SudanSyria

Terrorism and terrorist financing

Tunisia

Ukraine

Zimbabwe

US sanctions

Sources Targets Impact Obligations Penalties

UNSCR IEEPA CFR Executive

Orders TWEA CISADA NDAA ITRSHA

Jurisdictions Individuals

- assets- travel

Entities- assets

Sectors- oil and gas- precious metals

Governments

USA citizens US

incorporated bodies

USDtransactions

Extraterritorial effect

Freeze/Block Report Notify

transgressions Information

requests NB “owned or

controlled (50% aggregate rule)”

Individual: - Imprisonmentand/or $250 fine (or x2 gain)

Corporate entity:- $1m fine(or x2 gain)

• US Department of StateState Department

• US Treasury’s Office of Foreign Assets Control

OFAC

• Bureaus of Industry and SecurityBIS

• US Department of JusticeDOJ

Federal Reserve • The Federal Reserve System

DANY• District Attorney of New York/New York

Department of Financial ServicesDANY/DFS

The US sanctions regulators

• policyState Department

• financial sanctions (SDN list)/civil breaches/ licences

OFAC

• trade sanctions/licencesBIS

• criminal breachesDOJ

Federal Reserve • regulated FI

DANY • bank licensingDANY/DFS

The US sanctions regulators

• individuals and entities subject to blockingSpecially Designated Nationals

• financial institutions subject to restrictionsPart 561

• individuals subject to rejection of businessForeign Sanctions Evaders

• individuals and entities subject to product restriction

Sectoral Sanctions

Section 311 Patriot Act • entities/jurisdictions of money laundering concern

DANY • de-barred/unverified/denied personsBIS lists

The US sanctions lists

Are there any exemptions?

• Information materials

• Travel exemption

• Humanitarian donations

• Personal communications

• Journalistic activity

• Official business

• Specific/general licences

The US sanctions regime

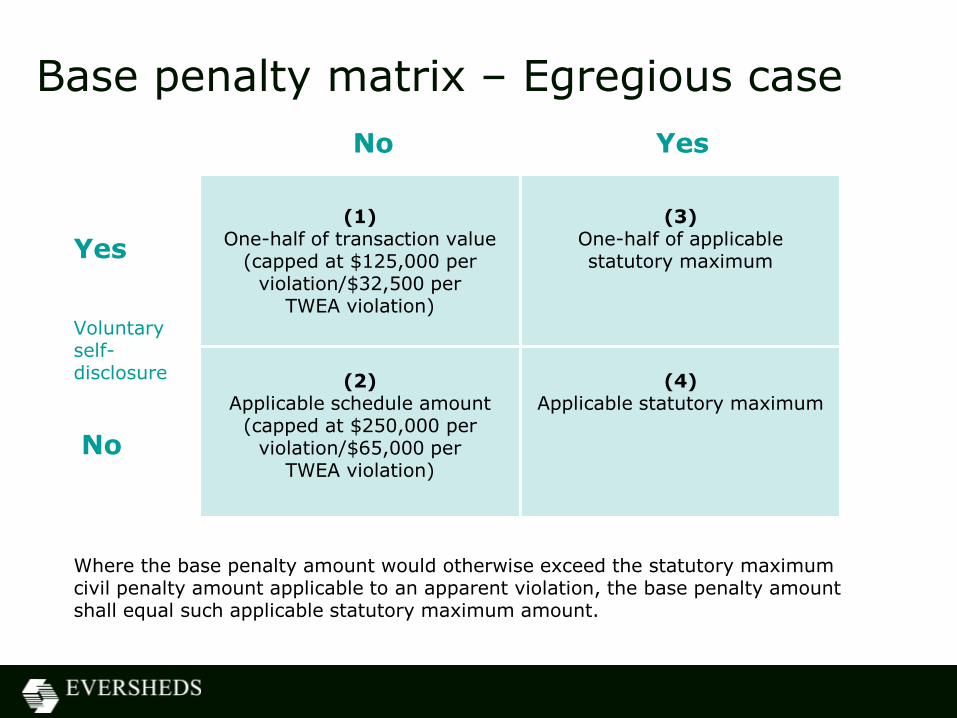

Base penalty matrix – Egregious case

No Yes

(1)One-half of transaction value

(capped at $125,000 per violation/$32,500 per

TWEA violation)

(3)One-half of applicable statutory maximum

(2)Applicable schedule amount

(capped at $250,000 per violation/$65,000 per

TWEA violation)

(4)Applicable statutory maximum

Yes

No

Voluntary self-disclosure

Where the base penalty amount would otherwise exceed the statutory maximum civil penalty amount applicable to an apparent violation, the base penalty amount shall equal such applicable statutory maximum amount.

• Hong Kong Monetary AuthorityHKMA

SFC

• Joint Financial Intelligence Unit Hong KongJFIU

• Hong Kong Department of Trade and Industry

Trade and Industry department

• Hong Kong Securities and Futures Commission

The HK sanctions regulators

HK sanctions

Sources Targets Impact Obligations Penalties

UNSCR UNATMO

(Cap 575) UNSO

(Cap 537) WMDO

(Cap 526) UNSR OFAC?

Individuals- assets

Entities- assets

HK permanent residents

HK incorporated bodies

Extraterritorial effect

Freeze funds No economic

resources (directly/indirectly)

No circumvention

Individual: - Imprisonment (14 years) and/ or unlimited fine

Corporate entity:- unlimited fine

• financial sanctions/breaches/licences (Authorised Institutions (AI))

HKMA

• financial sanctions (Listed non-AI)SFC

• reporting transactionsJFIU

• trade sanctions/licences/trade breachesTrade and Industry

department

The HK sanctions regulators

High Risk Jurisdictions

High risk jurisdictions

Financial sanctions workshop

Complying with sanctions

Zia Ullah – PartnerJames Robinson – Partner

26 November 2014

Sanctions compliance

Key compliance challenges (internal):

• Hit rates

• Identification of prohibited business/customers

• Monitoring of activity

• Escalation and exceptions

• Cost of compliance v cost of breaches

• IT tools

• Training

Key compliance challenges (external):

• Balancing conflicting regimes

• Regulatory focus

• Reputational damage

• Legislative change

• List consolidation

Regulatory expectation:

• Awareness

• Screening

• Assurance

• Training

• Benchmarking

• Engagement

Sanctions compliance

Awareness:

• Legal and Regulatory

• Senior management

• Public Policy

• Private Policy

• External stakeholders (e.g., FCA,HMT)

• Internal stakeholders, BUs

Sanctions compliance

Screening:

• List management

• Policy:– Payments/customers– Domestic/cross-border– Message types– Trade documentation– Legacy systems

• Technology

• Escalation

• False positive strategy

Sanctions compliance

Assurance:

• Testing:– People– Technology– Policy– Escalation– False positive strategy– Awareness– Systems and controls

• By whom?:– Internal/external audit

Sanctions compliance

Training:

• How:– Ftf– E-learning

• Who:– Specific roles-e.g trade finance– all/?

• What:– One size fits all?

Sanctions compliance

Benchmarking:

• Industry guidance:– JMLSG/DFSA/OFAC

• Regulatory guidance:– FCA financial crime guidance/DFSA guidance

• Peer group:– Wolfsberg

Sanctions compliance

Engagement:

• Regulatory:– HMT/AFU/UAE central bank– FCA/DFSA– BIS

• Disclosure

Sanctions compliance

• Who are you dealing with?

• Non-cooperation

• Location of interested parties

• Policy implementation versus law/regulation

• Directly versus indirectly

• Audit/termination rights

• KYB

The critical issues

Russian/Ukraine sanctions –2014 timeline

• March 5/6 – US and EU authorise sanctions (EO 13660); EU freezes assets of Ukrainian individuals

• March 20 – the Russian Foreign Ministry published a list of reciprocal sanctions against certain American citizens, which consisted of 10 names, including Speaker of the House of Representatives John Boehner, Senator John McCain, and two advisers to Barack Obama

• July 16 – US sectoral sanctions- Rosneft, Novatek, Gazprombank and Vneshekonombank

• July 31 – EU introduced a further round of (sectoral) sanctions. Sanctions included financial sector (all majority government-owned Russian banks), trade restrictions relating to the Russian energy and defence industries, and additional individuals and entities designated under the EU asset freezing provisions

• August 6 – Putin signed a decree "On the use of specific economic measures", which mandated an effective embargo for a one-year period[30] on imports of most of the agricultural products

• August 12 – US imposed sanctions on Russia's largest bank (Sberbank), a major arms maker and arctic (Rostec), deepwater and shale exploration by its biggest oil companies (Gazprom, Gazprom Neft, Lukoil, Surgutneftegas and Rosneft)

• September 12 – US and EU expands sanctions to additional people and entities, as well as providing for further sectoral sanctions

Country programmes – Russia

EU:

• Regulation 208/2014 (misappropriation and human rights):– Assets/economic resources– 6/3/14

• Regulation 269/2014 (sovereignty and territorial integrity):– Assets/economic resources– 17/3/14

Ukraine/Russia

EU and US restrictions

• EU Reg 833/2014 –money market instruments or transferable securities>90 days maturity post 1/8/14

energy

finance

export

50% extra-EU subsidiaries

• EO 13662 – debt or equity>90 days maturity post 16/7/14

energy

finance

export

General Licence No.1

• EU Reg 960/2014 – money market instruments or transferable securities>30 days maturity post 12/9/14

energy

finance

export

50% extra-EU subsidiaries

• EO 13662 – debt or equity>30/90 days maturity post 12/9/14

energy (90)

finance (30)

export (30)

General Licences Nos.1a/2

Ukraine/Russia

EU and US restrictions

Country programmes

UK:

• The Ukraine (European Union Financial Sanctions) Regulations 2014

• The Ukraine (European Union Financial Sanctions) (No.2) Regulations 2014

The Iranian regime:

Country programmes

EU:

• Regulation 267/2012 (prohibition on dealing with Iranian):– Assets/economic resources– Crude oil– Petroleum/petrochemical products– Precious metals/stones/currency notes

• Builds upon Regulation 961/2010

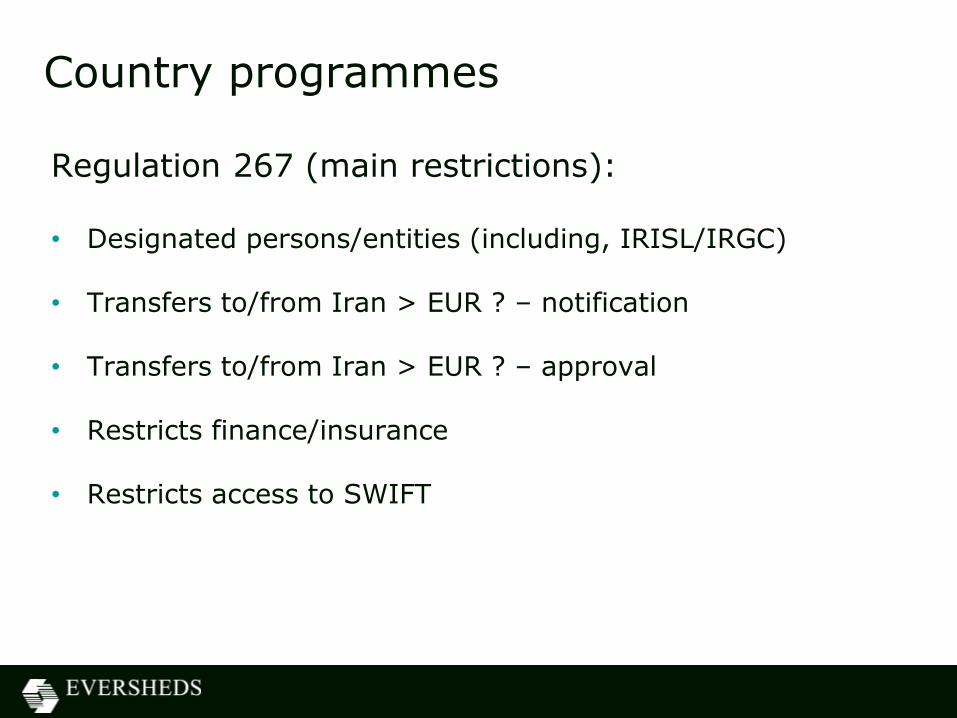

Country programmes

Regulation 267 (main restrictions):

• Designated persons/entities (including, IRISL/IRGC)

• Transfers to/from Iran > EUR ? – notification

• Transfers to/from Iran > EUR ? – approval

• Restricts finance/insurance

• Restricts access to SWIFT

Country programmes

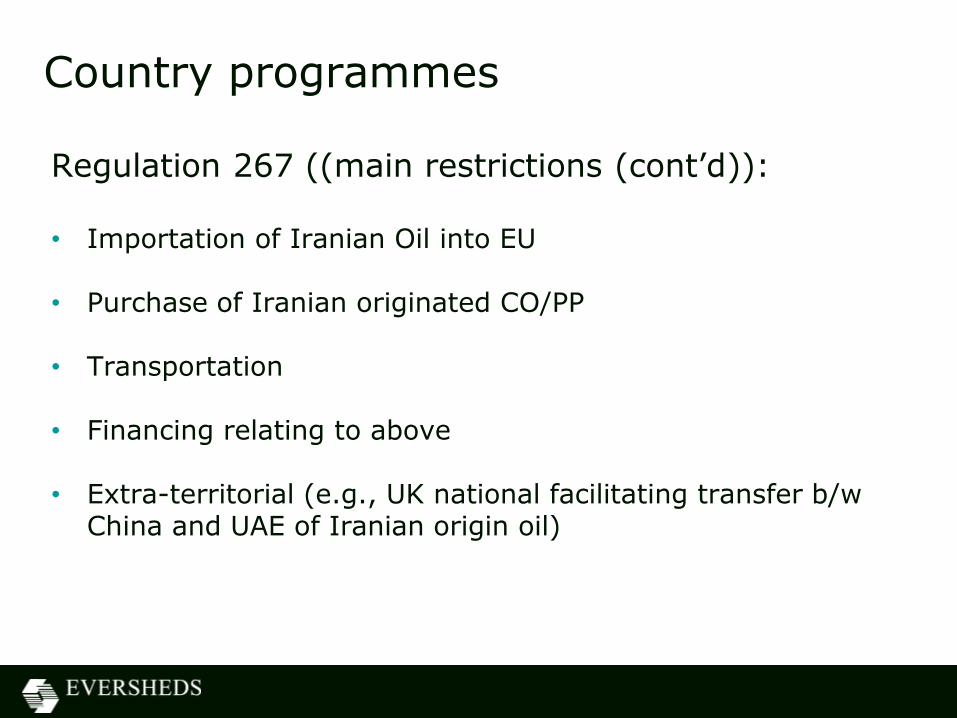

Regulation 267 ((main restrictions (cont’d)):

• Importation of Iranian Oil into EU

• Purchase of Iranian originated CO/PP

• Transportation

• Financing relating to above

• Extra-territorial (e.g., UK national facilitating transfer b/w China and UAE of Iranian origin oil)

Country programmes

Regulation 267 (other restrictions):

• Provision of loans or credit

• Buying shares

• Joint Ventures

• ‘cooperation’:– NG– LNG transmission

Country programmes

UK:

• The Iran (European Union Financial Sanctions) Regulations 2012

• Export Control (Iran Sanctions) Order 2012

• The Iran (Asset-Freezing) Regulations 2011

• The Iran (European Union Financial Sanctions) (Amendment) Regulations 2014

Country programmes

• Joint Plan of Action between the P5 +1 (E3 +3) and Iran (JPOA)

• Suspends certain US/EU sanctions until two days ago!! –news?

• Permitted?

– Petrochemical exports– Gold and precious metals– Automotive dealing– Release of frozen funds– Civil aviation licensing

The Iranian conundrum- P5+1

Financial sanctions workshop

Case studies

Zia Ullah – PartnerJames Robinson – Partner

26 November 2014

SWIFT 103 definitions

Field Tag Field Name

23B Bank Operation Code

32A Value Date/Currency/Interbank settled amount

33B Currency/Original Ordered Amount

50K Ordering Customer, Amount & Name and Address

52D Ordering Institution

53A Senders Correspondent

59 Beneficiary

70 Remittance Information

71A Details of Charges

72 Send to Receiver Information

Case study 1

• In January 2014, the Dubai Branch of your UK incorporated bank provided an RMB 1m import L/C for the benefit of its Cypriot client, a manufacturer of oil and gas valves used for shale gas projects.

• Your trade team conducted EDD on opening the facility and it transpired that the Cypriot client was beneficially owned by Rosneft bank.

• In late September 2014, a SWIFT message was received from the advising bank’s trade team: please note that the seller has advised goods linked to this facility will be sourced from Crimea….

• In November 2014, the underlying documents were received by your trade desk.

Case study questions

1. What are the key issues for you as issuing bank?

2. Does the fact that the deal is in RMB matter?

3. What difference would it make to the deal if the L/C was denominated in:

– USD

– Euro

4. Can you make any payments as issuing bank?

5. Why/why not?

6. If your client informed you that the products were to be used for Russian government projects, would that change matters?

Case study 2• A USD payment is being made from a

German manufacturer inbound to your customer, a Dubai based industrials group. The payment references Myanmar in Field 70 of the payment message.

• The Relationship Manager is contacted by the compliance team investigating the payment and advises that the payment is in relation to the manufacture of anti-mine equipment supplied to a company 52% owned by the Myanmar Ministry of defence.

• Upon instruction from the compliance team, the Relationship Manager questions the customer about the existence of an OFAC licence, to which the customer states that as a Dubai firm, they are not subject to US sanctions and are not required to be licensed for the activity undertaken.

20:YT16560567400845

:23B:CRED

:32A:080613USD6757,35

:33B:USD67570,35

:50K:/GDR76300040099900016016

15459

EUROPEAN METAL

COMPANY

123 Volks Strasse

Berlin

:52A:HSBCGDR

:53A:HSBCUS3NXXX

:54A:BCDUS53XXX

:59:/UAE19ABCC200000XXXXXXX

Dubai industrials

PO BOX 245

UAE

:70:MYANMAR MOD

107a 15728 UWR 9541

245462

:71A:SHA

-5:{CHK:A70C2FE9CC5B}{PFX:}}

1. What are the key issues for you?

2. Why is an OFAC licence necessary?

3. Does the fact that the deal is in USD matter?

4. What difference would it make to the deal if the paymentwas sent from the Thai MOD?

5. What difference would it make to the deal if the paymentwas sent from an entity owned 49% by an OFAC SDN?

6. What if the payment came from an entity whosemanagement and oversight was controlled by a party thatonly owned 22% of the shares and was located in the EU?

Case study questions

Financial sanctions workshop

A company perspective

Zia Ullah – PartnerJames Robinson – Partner

26 November 2014

• Same fundamental rules

• Reputation

• Do you need a licence for product / service?

• Can you be paid?

• Who is exporter / Who responsible licensing?

• Whole supply chain

– Directly or indirectly

– Back-to-Back

– Sale for stock?

• Warranties

• Termination rights – force majeure enough?

The critical issues

Common mistakes – products

• More than one regime applies

• Missing continued impact

– US consequences from lawful Iran trading

– USA re-export and deemed export

• Technology

• Warranties, controls, liability and termination need to join up

• Internal process and records

• Every step covered e.g.Exports within EU for export out of EU

Common mistakes – funding

• Unexpected elements giving jurisdiction

– Nationality / Green card

– Use of currency or banking system

– Knowledge in indirect payments

– Military items - broking

Tools

• Electronic training

• Systems design

• Audit

• Privacy

• Voluntary disclosure

For more information or advice please contact:

Zia UllahPartner+44 161 831 8454 [email protected]

James RobinsonPartner+44 207 919 0978

Looking to the future

Ben Moylan – Partner

Clint Dempsey – Principal Associate

26 November 2014

Middle East perspective

Looking to the future

Overview

• Very liquid market, flight to safety into certain countries within

the region means financial institutions are sat on large cash

deposits. Competitive market is driving prices down

• Diverse sectors driving growth: real estate, tourism,

transportation, oil and gas, infrastructure and consumer

• Mena-China trade has increased 50-fold in the past 20 years to nearly US$300 billion

• EU-GCC total trade in goods in 2013 amounted to around €152 billion (significant increase from €100,6 billion in 2010)

• The EU is negotiating a free trade agreement with the six countries of the Gulf Cooperation Council

Overview

• Significant developments in the Middle East

– Qatar 2022 World Cup

– Dubai Expo 2020

– Renewable Energy developments

– Suez Canal Expansion

– The Kingdom Tower in Jeddah

• Trade finance will continue to grow across the Middle East

• Gateway between North, South, East and West

Growth areas

• Two key areas for growth in trade finance:

– Bank Payment Obligations (BPO)

– Islamic Trade Finance

Growth areas

• BPO

– Innovative bank assisted trade instrument

– Irrevocable undertaking given by one bank to another

bank that payment will be made on a specified date

after successful electronic matching of data

– April 2013 ICC Banking Commission approved the

URBPO, contractual rules to govern BPO

– BPO relies on electronic matching, not paper based,

using global standard ISO 20022 messages

Growth areas

• BPO

• Advantages

– BPO guarantees exchange of goods for payment based

on electronic presentation of compliant data

– Slow start, but increasing in popularity. 40 corporates

across the globe are using BPO (BP, 7-Eleven, PTT

Polymer)

– Reduction in overall operational costs to banks, allows

for competitive pricing

– Safer than prepayment, buyer does not have to pay

upfront before receiving goods

– Automated data matching reduces complexity

– Cross-sale opportunities for banks e.g. financing and

working capital management systems

Growth areas

• BPO

• Potential shortfalls

– Capital cost to banks in investing in new systems,

supporting and communicating with ISO20022

compliant messages as well as Transaction Matching

Application

– Physical trade documents are required under local

legislation and to release delivery of goods from

customs

– Not defined for the purposes of Basel Capital Adequacy

Requirements, most bank’s treat BPO the same as LC

(capital conversion factor 20% sitting on balance sheet

i.e. still cheap for banks to hold these assets)

Growth areas

• Islamic Trade Finance

– Increasing popularity in the region

– Shifting preference towards Shari’ah-compliant banking

– Liquidity of Islamic banks in the region means

competitive pricing in the region

Growth areas

• Islamic Finance

• Typical structures

– Murabaha – Bank will purchase the commodities from

the supplier and then sell them to the beneficiary with a

deferred payment arrangement. The difference between

the purchase price and the sale price is the bank’s profit

– Syndicated Murabaha – Bank appointed by syndicate of

banks pursuant to Mudaraba agreement, bank (as

Mudarib) will then enter into Murabaha agreement with

customer. Profits are split between the syndicate of

banks

Growth areas

• Islamic Finance

• Typical structures

– Instalment Sale – Bank purchases the asset on

beneficiary’s behalf and immediately transfers

ownership upon delivery to the beneficiary. Beneficiary

will provide the same asset delivered to it as security.

The sale price will usually be paid in instalments.

Structure is often backed by guarantee

Growth areas

• Islamic Finance

• Typical structures

– Istisna’a – The bank agrees to buy an asset to be

delivered once construction or manufacturing of that

asset is complete. The bank pays the purchase price of

the asset in accordance with the progress of the asset's

construction or manufacture that gives the

contractor/manufacturer the liquidity it needs to

construct or manufacture the asset. Once manufacture

or construction is complete, the bank acquires the asset

that it can then sell or lease to the

contractor/manufacturer or a third party for a profit

For more information or advice please contact:

Ben MoylanPartner+97 44 49 67 39 [email protected]

Clint DempseyPrincipal Associate+97 14 38 97 01 8 [email protected]

Greg Brandman, Partner, Eversheds LLP

26 November 2014

Recent developments in the regulation of individuals in UK financial services

New senior management arrangements and

conduct rules

Greg Brandman - Partner

26 November 2014

New Senior Manager arrangements and conduct rules - overview

• “Restore trust and improve culture”

• “Individual accountability has often been unclear and confused”

• New regime for employees of UK banks, building societies, credit unions and PRA-designated investment firms

– Senior Managers regime

– Certification regime

– New Conduct Rules (PRA + FCA)

How things are changing

New Senior Managers regime

• Senior Manager Function (SMF) replaces Significant Influence Function

• 18 SMFs and some new functions

• Each SMF must have a statement of responsibilities

• Firms must maintain a Responsibilities Map that describes the firm’s management and governance arrangements

• Firms must vet Senior Managers for fitness and propriety before approval and on an annual basis

• Senior Managers must be vetted for each function they hold

• Senior Managers must provide handover notes to a successor

SMFs of particular interest

• PRA prescribed functions

– oversight of whistleblowing policy

– culture and standards and staff behaviours

• FCA prescribed functions

– Money Laundering Reporting and Compliance Oversight

– individuals with overall responsibility for certain key functions or identified risks, including:

• establishing and operating systems and controls in relation to financial crime

New Certification Regime

• Applies to functions that can cause ‘significant harm’ to a firm or its customers

• Certification is role specific and if multiple functions are performed by an individual must assess against each function

• Firms must assess and certify that individuals within the regime are fit and proper at least annually

• Consultation also includes a proposal that prospective employers seek a “regulatory reference” before hiring a senior manager or certified employee

• Regulators cannot intervene in individual certification decisions but may challenge the overall effectiveness of a firm’s process

• Senior manager must be allocated to oversee the Certification Regime

The new rules of conduct - overview

• For relevant firms, these will replace the existing APER principles and guidance

• Contained in a new code of conduct sourcebook: C-CON

• PRA and FCA will apply their own rules separately

• They will apply to:

– senior managers

– persons within the certification regime

– “all individuals within relevant firms who are in a position to have an impact on the PRA/FCA’s statutory objectives”

• APER will continue to apply to approved persons at other firms

Increased training, policing and reporting obligations for firms

• Only senior management functions will be subject to prior regulatory approval

• Relevant firms are now responsible for

– assessing the fitness and propriety of employees within the certification regime

– policing the compliance of other conduct rules staff with the conduct rules

• far wider population of staff than before

• increased training and compliance burden

• notification and reporting requirements

Scope of the conduct rules

• FCA and PRA will apply the conduct rules separately

• FCA will apply its own conduct rules “to the large majority of those working within relevant firms”

• FCA conduct rules will cover all who are in a position to impact its statutory objectives

– all individuals approved by FCA/PRA as senior managers

– all individuals covered by FCA/PRA certification regime

– all other employees save ancillary staff specifically excluded in C-CON

• Certain conduct rules will apply to SMFs only

Staff not subject to the new conduct rules

• Those whose role would be fundamentally the same, if they did not work for a financial services firm:

– receptionists / switchboard staff

– post room / repro staff

– facilities / events management

– security / concierge staff

– cleaners and catering staff

– IT support / archive staff

Rules common to both PRA and FCA

• Tier 1 (applying to all relevant staff)

– 1. You must act with integrity

– 2. You must act with due skill, care and diligence

– 3. You must be open and cooperative with the FCA, the PRA and other regulators

Additional FCA conduct rules

• Tier 1 (applying to all relevant staff)

– 4. You must pay due regard to the interests of customers and treat them fairly

– 5. You must observe proper standards of market conduct.

Other rules common to both PRA and FCA

• Tier 2 (Senior Managers only)

– SM1: You must take reasonable steps to ensure that the business of the firm for which you are responsible is controlled effectively

– SM2: You must take reasonable steps to ensure that the business of the firm for which you are responsible complies with the relevant requirements and standards of the regulatory system

– SM3: You must take reasonable steps to ensure that any delegation of your responsibilities is to an appropriate person and that you oversee the discharge of the delegated responsibility effectively

– SM4: You must disclose appropriately any information of which the FCA or PRA would reasonably expect notice

Complying with the Tier 2 conduct rules for senior managers

• What the regulators will take into account broadly follows existing APER 5-7 guidance:

– exercised reasonable care when considering the information available

– reached a reasonable conclusion upon which to act

– scale and complexity of the firm’s business

– their role and responsibility as determined by reference to the relevant statement of responsibility

– the knowledge that they had, or should have had, of regulatory requirements

Personal Culpability

• A person will only be in breach of any of the new Conduct Rules where they are “personally culpable”. This means where:

– the person’s conduct was deliberate; or

– the person’s standard of conduct was below that which would be reasonable in all the circumstances.

Presumption of Responsibility (senior managers only)

• Concept of personal culpability may be inverted for senior managers where the firm has contravened a requirement

• Effect: reversal of the burden of proof for individual misconduct

– no longer for the FCA to show the senior manager failed to act reasonably; instead

– the senior manager must satisfy the regulator that he took reasonable steps to prevent/stop the contravention

• Criteria for taking action against a senior manager – case by case basis

• When bringing enforcement action against senior manager (whether under the presumption of responsibility or otherwise) the FCA will use the Statement of Responsibilities and the firm’s Responsibilities Map to help inform it of the scope of the Senior Manager’s duties

Implications of the new rules

• FSMA (as amended) places 3 key obligations on relevant firms with regard to the Conduct Rules

– awareness and training

– notification of breaches

– notification of disciplinary action

Notification of suspicions and formal disciplinary action

• When does the firm need to notify ?

• Firms will have to inform the regulators if:

– they suspect / are aware that a person has breached a Conduct Rule

– having previously notified a breach, they reach a subsequent or different determination

– they have issued a formal written warning to, suspended or dismissed or reduced or recovered remuneration from an employee as a result of conduct amounting to a breach of the Conduct Rules

When / whom to notify ?

• Senior Manager breaches (known or suspected)

– notify within 7 business days

• Other individuals – notify quarterly

– list of known or suspected breaches

– identities of persons to whom notifications relate

– disciplinary action taken in that quarter

• Known or suspected breaches by persons subject to the PRA’s conduct rules should be notified to PRA

Employment law concerns

• Employment rights of conduct rules staff ?

– prior to notifying, the firm must satisfy itself that it has reasonable grounds to suspect

– timing of notifications ?

– internal investigation first ?

– employee right of reply before notification ?

– incorporate rights in future employment contracts ?

– nb s398 FSMA !

Applying the new regime to UK branches of foreign banks

• FSMA gives HM Treasury powers to bring non-UK institutions (including UK branches of overseas firms) into scope by Order

• The Chancellor has announced he intends to extend the regime to all banks that operate in the UK, including the branches of foreign banks

• HMT Consultation and draft Order due later this year

Next Steps

• Consultation has closed (31 October 2014)

• Technical CP to follow

– operational and consequential aspects of the new regime

– forms

– transitional arrangements

• Policy Statement with final rules due Q1 2015

• Implementation Q3 2015-Q1 2016 for senior managers and certification regime staff

• Other conduct rules staff after that

Keep updated:

www.eversheds.com/financialinstitutions

@EvershedsFI