eurocypria the chartered airline of cyprus challenges eleftherios ioannou executive chairman

TRANSCRIPT

Eurocypria

The Chartered Airline of Cyprus • Challenges

Eleftherios Ioannou

Executive Chairman

Global Tourism has shown robust growth over time, despite a number of negative

external shocks

• Challenges

438

534

684 686 706 694

764804

853904 922

0

100

200

300

400

500

600

700

800

900

1,000

1990 1995 2000 2001 2002 2003 2004 2005 2006 2007 2008

Glo

bal

Inte

rnat

ion

al T

ou

rist

Arr

ival

s, M

illio

ns

CAGR 1990-20084.2%

International Tourist Arrivals (millions), 1990-2008

Sep 11SARS, 2nd Gulf War

Financial crisis

Source: World Tourism Organisation &

Europe is the largest tourism region in the world with 53% of total arrivals in 2008, but it

is growing more slowly than other regions

266315

396 393 404 407 424 442 459 480 489.4

439

540

922898

687 686 706 694764

806842

0

100

200

300

400

500

600

700

800

900

1000

1990 1995 2000 2001 2002 2003 2004 2005 2006 2007 2008

Inte

rnat

ion

al T

ou

rist

Arr

ival

s, M

illio

ns

Europe

World

CAGR 1990-20084.3%

CAGR 1990-20083.5%

European Tourist Arrivals (millions), 1990-2008

Source: World Tourism Organisation &

International Tourist Arrivals to Europe by Sub-regions, (millions), 1990 – 2008

32 40 46 46 50 53 55 56 57

109 112140 136 139 143 150 155 153

3260

70 79 86 88 91 93 100

94

103

141 147150 158

165 176 180

0

50

100

150

200

250

300

350

400

450

500

1990 1995 2000 2003 2004 2005 2006 2007 2008

Inte

rnat

ion

al T

ou

rist

Arr

ival

s, M

illio

ns

Southern/MediterraneanEurope

Central/ EasternEurope

Western Europe

Northern Europe

Within Europe, the Southern/Mediterranean region attracts the most tourist arrivals, and

also, along with CE Europe, shows the fastest growth

Source: World Tourism Organisation &

Spain34.6%

Italy30.8%

Greece10.1%

Portugal9.4%

Other1.2%

Croatia1.5%

Malta1.1%

Cyprus2.1%Israel

2.2%Turkey

7.0%

Spain34.0%

Italy29.3%

Greece9.3%

Portugal8.6%

Israel1.7%

Malta0.9%

Slovenia0.8%

Croatia4.1%

Turkey6.8%

Andorra2.1%

Cyprus1.9%

Other0.5%

1990

2000

2005

Total: 103 million

Total: 141 million

Total: 150 million

Source: UNWTO &

Croatia and Turkey have grown share

Traditionally, the Western Mediterranean has been the main destination of European leisure travel; there

are however some signs that other countries are increasing their share

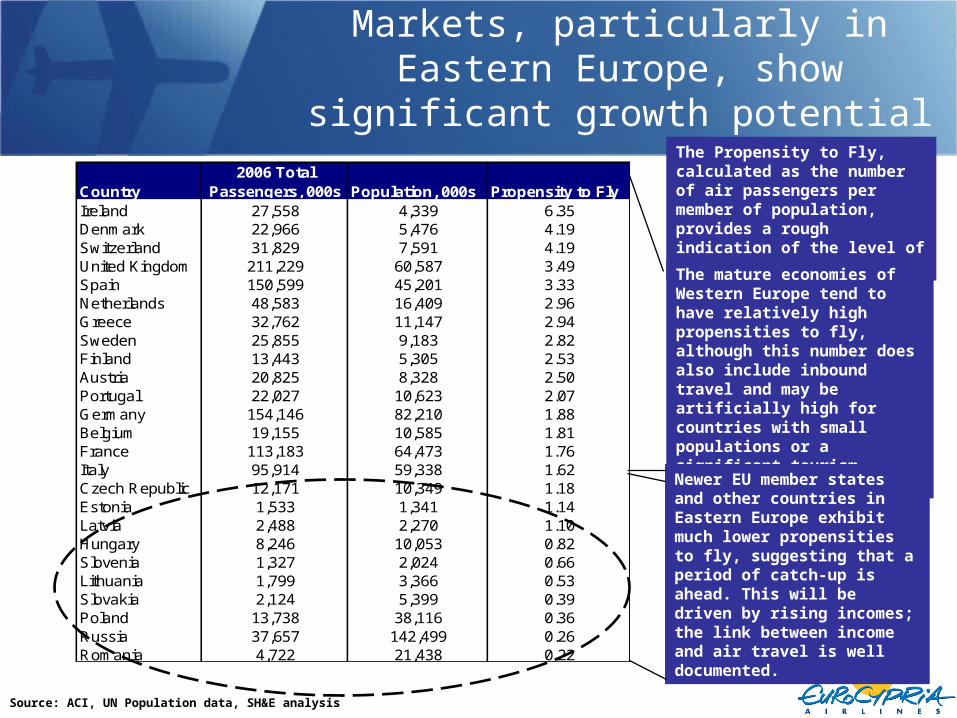

Markets, particularly in Eastern Europe, show significant growth potential

Country2006 Total

Passengers, 000s Population, 000s Propensity to FlyIreland 27,558 4,339 6.35Denmark 22,966 5,476 4.19Switzerland 31,829 7,591 4.19United Kingdom 211,229 60,587 3.49Spain 150,599 45,201 3.33Netherlands 48,583 16,409 2.96Greece 32,762 11,147 2.94Sweden 25,855 9,183 2.82Finland 13,443 5,305 2.53Austria 20,825 8,328 2.50Portugal 22,027 10,623 2.07Germany 154,146 82,210 1.88Belgium 19,155 10,585 1.81France 113,183 64,473 1.76Italy 95,914 59,338 1.62Czech Republic 12,171 10,349 1.18Estonia 1,533 1,341 1.14Latvia 2,488 2,270 1.10Hungary 8,246 10,053 0.82Slovenia 1,327 2,024 0.66Lithuania 1,799 3,366 0.53Slovakia 2,124 5,399 0.39Poland 13,738 38,116 0.36Russia 37,657 142,499 0.26Romania 4,722 21,438 0.22

The Propensity to Fly, calculated as the number of air passengers per member of population, provides a rough indication of the level of maturity

The mature economies of Western Europe tend to have relatively high propensities to fly, although this number does also include inbound travel and may be artificially high for countries with small populations or a significant tourism market

Newer EU member states and other countries in Eastern Europe exhibit much lower propensities to fly, suggesting that a period of catch-up is ahead. This will be driven by rising incomes; the link between income and air travel is well documented.

Source: ACI, UN Population data, SH&E analysis

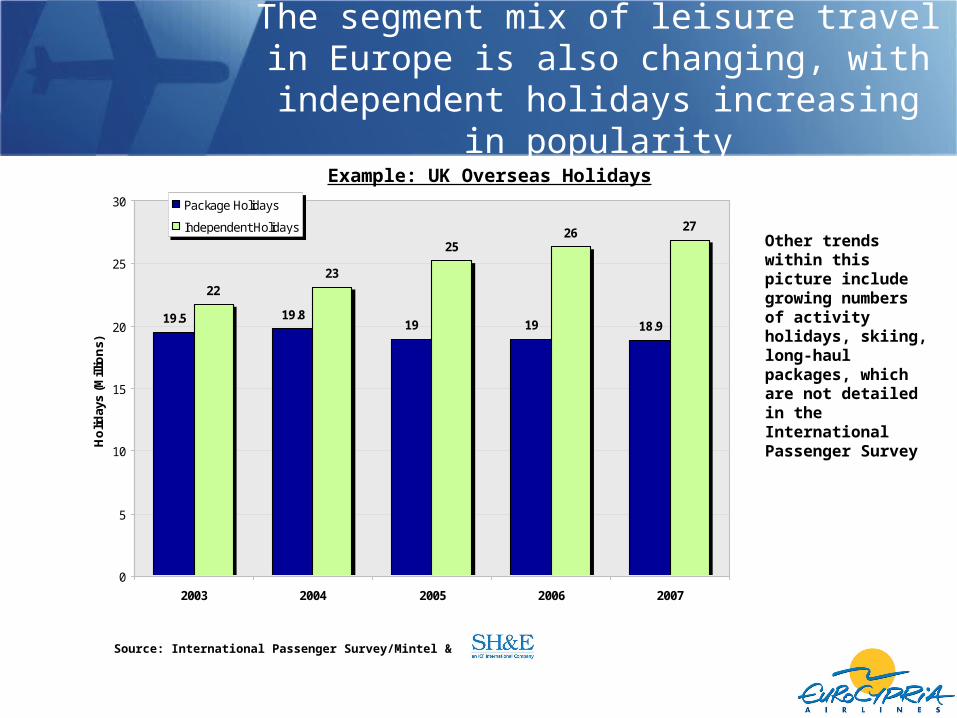

The segment mix of leisure travel in Europe is also changing, with independent holidays

increasing in popularity

19.5 19.819 19 18.9

2223

2526 27

0

5

10

15

20

25

30

2003 2004 2005 2006 2007

Ho

liday

s (M

illio

ns)

Package Holidays

Independent Holidays

Source: International Passenger Survey/Mintel &

Example: UK Overseas Holidays

Other trends within this picture include growing numbers of activity holidays, skiing, long-haul packages, which are not detailed in the International Passenger Survey

The growth in individual (seat only) travel has had a significant impact on the

traditional charter market

30 33 34 36 39 36 33 34 36 38 37 36 36 36 33 30 29

43 4348 46

51 59 6775

8189

101 107 105115

131148

162

0

50

100

150

200

1990 1992 1994 1996 1998 2000 2002 2004 2006

Pas

sen

ger

s (m

illio

ns)

Scheduled

Non-scheduled

Source: DGAC Spain &

Passengers at Spanish airports (1990-2006)• In Spain the charter

market peaked in 1994 and has declined by 25% in 12 years

• In the same period the total market has trebled, with scheduled carriers growing four fold.

• Much of the scheduled growth since 2002 has been with Low Cost Carriers

There are four main airline types competing for European leisure travellers

The boundaries between the models are however increasingly blurred, as traditional charter airlines offer scheduled ‘low-cost’ services (e.g. Monarch), low cost carriers such as Air Berlin also operate in the charter and long-haul markets, and integrated tour operators move into flight-only sales on their charter flights

Scheduled network carriers

Integrated tour operators

Independent charter carriers

Low cost carriers

Source:

Low Cost carriers have been the most significant development in the competitive

environment, increasing capacity, stimulating leisure demand, and driving down prices

ZRH

ZTHXRY

VIE

ZAD VAR

WAWTXL

VCETSF

TRF

TRD

TJM

VKO

SZG

SXF

ZAG

TLL

SVX

SVQVLC

SVG

SUF

STR

STN

ZAZ

WRO

VST

VLLVBS

TUF

TRSTRN

TOS

TMP

TLN

SZZ

SPU SOF

SOB

SNN

SMI

SKG

SJJSKP

SDRSCQ

SCN

SAW

RZE

RTM

ROVRNS

SOU

RMIRJK

RIX

RHO

RLG

REU

REG

RDZ PUYPUF

PSRPSA

TPS

PRN

PRG

POZ

PMO

VRN

PMI

PMF

PIS

PIK

PGF PEG

PEE

PAD

OVD

OSR

OSL

VNOPLQ

ORY

TLS

ORK

OPOOMO

OLB

NYO

NUE

VOL

NTE

NQY

NOC NCL

NCE

NAP

MXPOTP

MUC

PVK

MST

MRSMPL

MMX

MMK

MLA

MJV MJT

MANNWI

MAHMAD

SBZLYS

LTN

TATLRH

LPL

LNZLJU

LIS

LINLIG

LHRLGW

VGO

LEJ

LEI

LED

LDY

LCJ

LCG

LBCLBA

KZN

KVA

KUN

KUF

KTWKSC

KRS

KRN

LLA

KRKLIL

KLU

KKN

KIR

KGS

KGD

JTRJMK

JERSEN

IST

USQ

IOM

INV

INN

IBZ

HHN

HER

HEL

VAA

RVNOUL

KUO

HAU

HAMHAJ

GWT

GVALUG

LTT

KBP

GSE

GRZ

THF

GRX

GRO

MME

GPA

GOT

GOAGNB

GLA

GIB

GDN

TKU

GCI

FRL

FRA

FNI

FMO

FLR

FKBFDH

FCO

PNL

FAO

EXT

EVE

ESB

ERF

EMA

EIN

EGC

EDO

EDI

EBA

DUS

VXO

KEF

DUB

DTM DRSDNR

DME

DLM

DBV

CWLCVT

CTA

CRL

CPH

CNDCLJ

CKZCIA

CHQ

CGN

OSI

CLY

CFU

CEK

CDG

CCF

CAG

BZR

BZG

BVA

BUD TGMBTSBSL

BRUBRS

BRQ

BRI

BRE

BOO

BOJ

BOH

BODBNXBLQ

BLLBLK

BJV

BIQBIO

BIA

BHX

DNDBHD

BGY

BGO

BFS

BES

BEG

BDU

BDSBCN

BCM

CUF BBU

AYT

AVN

ATH

ARW

ARN

UMEOSD

AOK

AOI

AOC

ANG

AMS

ALF

ALC

AJAAHO

AGP

AER

ADB

ABZ

AARAAL

RKV

LCA

European LCC Routes, August 2008

AAR

STN

ABZ

LTN

AGP

AMSCGN DRSDUS

FAO

FMO

LEI

LPLMAN

NUE

PADRTM TXL

XRYAHO

ALC

BCN

CTA

DUB

GVA

HER

NAP

NCE

ORK

PMI

PSA

RHO

SVQ

AOI

ARNHEL

JYV

MHQ

OUL

PORTKUTMP

ATH AYT

BRU

BFSSNN

BGO

BGY

FCO

BHXIOM

BIOBIQ BLQ

BOHBRE

SXFBRS

CPH

LHR

LINBUD

SJJ

BVA

PIK

CCF

CDG

CFU

ERFLEJ

ZTH

IBZ

KGS

MAH SKGCIA

GOT

CRLCWL

JERDNR

EDI

FRA

GLAGWY

KIR LBA

LCYLGW

MAD

MME

MUC

MXP

NCL

ZRHEBUFNI

GIB

GOA

HAJHAM

OSL

HHN

INV

SOU

IST

KIDLBC

LDY

LIS

LYS

MMXNOC

SMI

NYO

RNS

VAA

PGF

SCNSTRPRG

RKV

RMIZAG

SUF

TRF

TRN TSFVBSVCE

LCA

European LCC Routes, August 2000

327 Routes

750,000 Weekly Departing seats

2,542 Routes

5,412,000 Weekly Departing seats

Source: OAG Schedules, SH&E Analysis

In Eastern/Southern Europe, LCCs are less well established, but

competition is increasing

These carriers typically serve significant migrant worker and VFR segments, particularly between the home market and the UK.

Country of origin

LCCs Fleet size

Poland Central Wings 11

Czech Republic

Smart Wings 2

Slovakia SkyEurope 15

Austria InterSky 4

Hungary WizzAir 16

Romania Blue Air 6

Bulgaria WizzAir Bulgaria 1

LCC Operators and Fleet size, August 2008

Bankrupt

Closed down

Source:

In Cyprus, non-scheduled services still account for 46% of passengers; this is an increase on

last year, when the proportion was 42%

Passengers at Cyprus airports, 2007

Paphos is the smaller of Cyprus’s

two commercial airports and in 2007 served around 1.7

million terminal passengers, of

whom around 75% were travelling on

non-scheduled services

Larnaca is Cyprus’s main airport, with around 5.3 million terminal passengers in 2007. Of these, around 35% were carried on non-scheduled services.

Source:

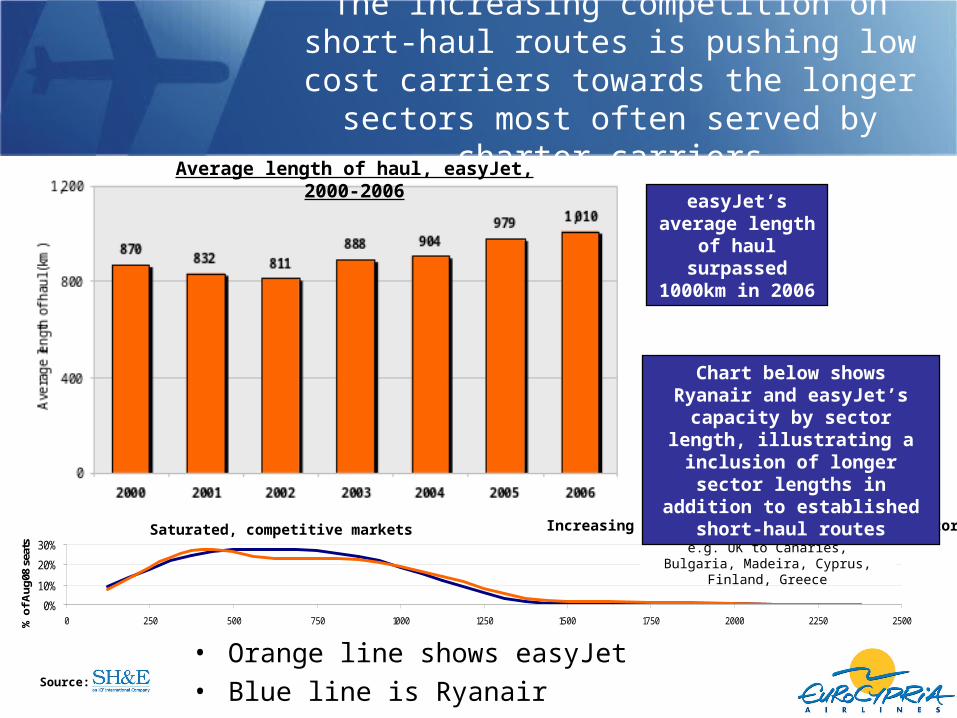

The increasing competition on short-haul routes is pushing low cost carriers towards the longer sectors most often served by charter carriers

0%

10%

20%

30%

0 250 500 750 1000 1250 1500 1750 2000 2250 2500% o

f Aug

08 s

eats

Saturated, competitive markets

Increasing network development on longer sectors

e.g. UK to Canaries, Bulgaria, Madeira, Cyprus, Finland, Greece

easyJet’s average length of haul

surpassed 1000km in 2006

Average length of haul, easyJet, 2000-2006

Chart below shows Ryanair and easyJet’s capacity by sector length, illustrating a inclusion of longer sector

lengths in addition to established short-haul routes

Saturated, competitive markets

• Orange line shows easyJet• Blue line is Ryanair Source:

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009

Charter LCC Traditional

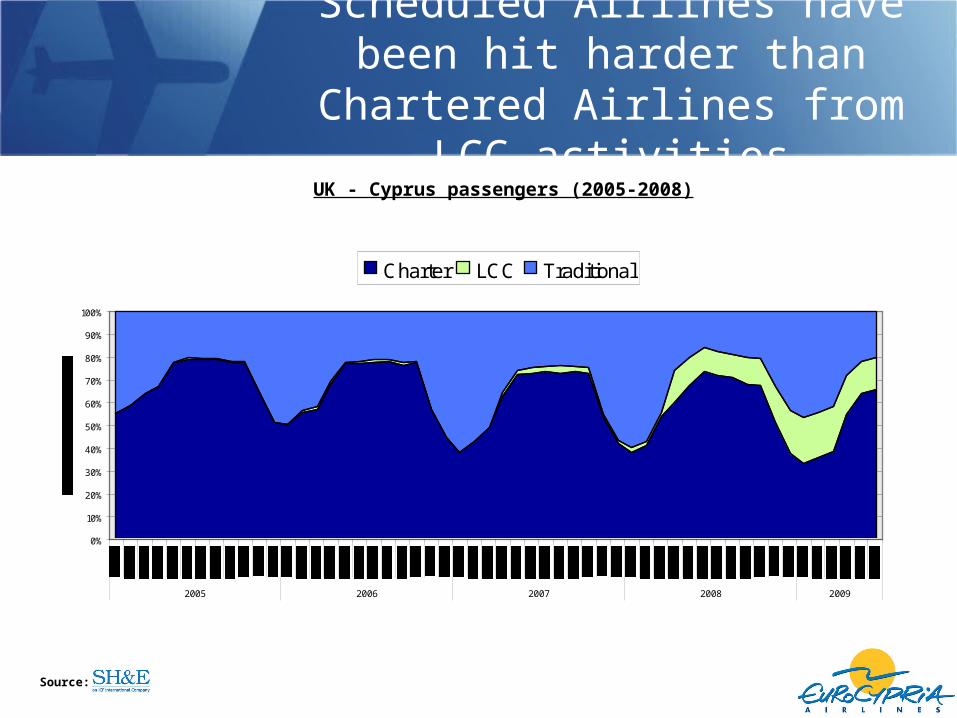

UK - Cyprus passengers (2005-2008)

Scheduled Airlines have been hit harder than Chartered Airlines from

LCC activities

Source:

While Cyprus is currently beyond the reach of most Western European LCCs, some from the

UK and from Eastern Europe have already started service

• Blue Air flies twice a week between Bucharest and Larnaca

• Flyglobespan operates scheduled services once a week between Aberdeen and Paphos, once a week between Edinburgh and Paphos, and twice a week between Glasgow and Paphos

• easyJet, having taken over GB airways and its existing routes, operates twice a day between London Gatwick and Paphos, and once a day between Manchester and Paphos

• Jet2.com flies twice a week between Leeds Bradford and Paphos

• Before their demise, SkyEurope used to fly five times a week between Vienna and Larnaca

LCA

LGW

MANDUB

NUEFRA

MUC

WAWPOZ

PRG

BUDVIE

ZRH

KBP

SVO

OTP

SOF

OSL ARN

ATH

FCO

LED

Overview of LCC services to Cyprus

1000km3000km 2000km4000km

Recently easyJet and Jet2 have announced scheduled services from the UKSource:

Eurocypria with 6 aircraft flies to 74 destinations and carries 850.000 passengers covering 25.040 Flight Hours

In this very competitive air transport world, the challenge for Eurocypria is to:

• Keep costs low, as low as LCC• Find partners, niche routes, products and services

that will add value to tourists to Cyprus.

Challenge