establishment of cement plant and its potential in balochistan

TRANSCRIPT

1

Establishment of Cement Plant

and its Potential in Balochistan

2

Table of Contents

1. PAKISTAN CEMENT INDUSTRY OVERVIEW ___________________________________ 3

2. STATEMENT OF INSTALLED PRODUCTION CAPACITY _________________________ 5

3. TYPES OF cement PRODUCED IN PAKISTAN ____________________________________ 6

4. CEMENT PRODUCTION PROCESS _____________________________________________ 7

5. CEMENT PRODUCTION PROCESS TYPES ______________________________________ 8

6. PAKISTAN CEMENT INDUSTRY STRUCTURE _________________________________ 10

7. PAKISTAN CEMENT INDUSTRY PROJECTION _________________________________ 11

8. SETTING UP CEMENT PLANT IN BALOCHISTAN ______________________________ 13

9. RAW MATERIAL USED IN CEMENT PRODUCTION: ____________________________ 14

10. PROCEDURE FOR SETTING UP A CEMENT PLANT ___________________________ 14

11. MAJOR STAGES INVOLVED IN SETTING UP AN INTEGRATED CEMENT PLANT 15

12. PRE-PROJECT STAGE _____________________________________________________ 16

13. PROJECT EXECUTION STAGE _____________________________________________ 19

14. PROJECT IMPLEMENTATION: _____________________________________________ 19

15. PROCUREMENT OF MAIN EQUIPMENT AND SERVICES:______________________ 20

16. DETAILED ENGINEERING: ________________________________________________ 20

17. KEY FACTORS IN SETTING UP OF A CEMENT PLANT ________________________ 21

18. RULES AND REGULARITIES BY GOVERNMENT OF BALOCHISTAN ___________ 22

3

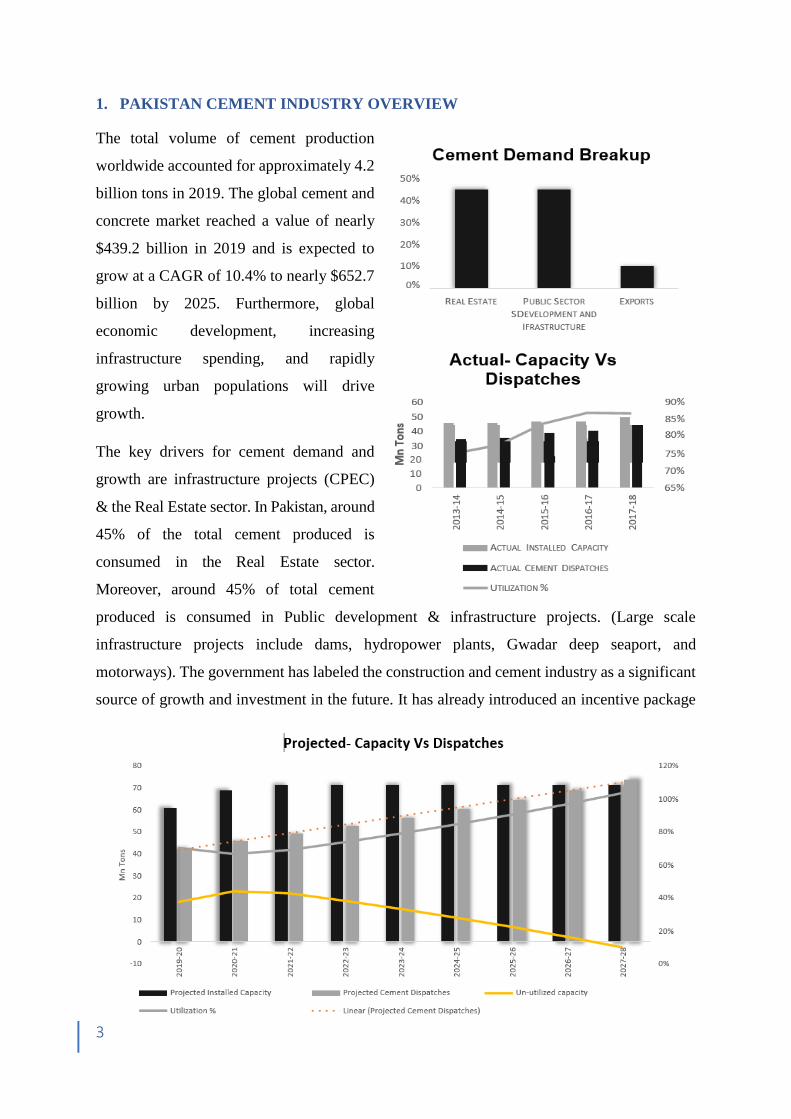

1. PAKISTAN CEMENT INDUSTRY OVERVIEW

The total volume of cement production

worldwide accounted for approximately 4.2

billion tons in 2019. The global cement and

concrete market reached a value of nearly

$439.2 billion in 2019 and is expected to

grow at a CAGR of 10.4% to nearly $652.7

billion by 2025. Furthermore, global

economic development, increasing

infrastructure spending, and rapidly

growing urban populations will drive

growth.

The key drivers for cement demand and

growth are infrastructure projects (CPEC)

& the Real Estate sector. In Pakistan, around

45% of the total cement produced is

consumed in the Real Estate sector.

Moreover, around 45% of total cement

produced is consumed in Public development & infrastructure projects. (Large scale

infrastructure projects include dams, hydropower plants, Gwadar deep seaport, and

motorways). The government has labeled the construction and cement industry as a significant

source of growth and investment in the future. It has already introduced an incentive package

4

for the construction industry in April 2020, anticipating to help increase local cement

consumption. The package includes an amnesty scheme, tax exemptions, and a PKR30bn

(US$182.2m) subsidy. Furthermore, the construction sector was given industry status in

Pakistan.

The acceleration in construction sector activity and the government's infrastructure and housing

initiatives have seen cement consumption increasing by 17.6 percent in 2019 to reach 39.7Mt,

whereas, 8 million tons of cement was exported to Afghanistan and Central Asian countries.

Pakistan has a well-developed cement

industry with abundant raw material

available in the country. The country

ranks amongst the top 5 exporters and is

the 15th largest cement producer in the

World. Currently, there are 25 cement

production plants operational in Pakistan

with an annual production capacity of

69.2 million tons. Only two out of 25

cement plants are operational in

Balochistan.

1. DG Cement (DGKC) is the

largest cement producer in

Pakistan, and is operational in the

Hub Lasbela district of

Balochistan, with the capacity of

9000 tons/day clinker based on

the latest dry process technology.

2. Attock Cement Pakistan Limited,

branded as Falcon Cement, has a cement production plant in Hub as well, Lasbela

district of Balochistan with the capacity of 1.2 million tons per annum.

Cement producers dispatched 47.8Mt of cement in the 2020 fiscal year out of which 39.95

million tons were locally dispatched whereas 7.85 million tons were exported mainly to

Afghanistan and gulf countries.

(Dispatches M. Tons) Percentage

Year Local Exports Total Local Exports

2013 23.95 8.57 32.52 74% 26%

2014 25.06 8.37 33.43 75% 25%

2015 26.15 8.14 34.29 76% 24%

2016 28.21 7.2 35.41 80% 20%

2017 23.94 4.41 28.35 84% 16%

2018 33.5 6.5 40 84% 16%

2019 39.95 7.85 47.8 84% 16%

0

10

20

30

40

50

60

2013 2014 2015 2016 2017 2018 2019

Dispatches in Million Tons

Local Exports Total

5

2. STATEMENT OF INSTALLED PRODUCTION CAPACITY

6

3. TYPES OF cement PRODUCED IN PAKISTAN

The types of special cement now being produced can be roughly classified into the following

six categories according to the special purpose for which these have been designed. These are

classified as:

1. Rapid hardening cement.

2. Cement resistant to chemical attack of certain soil and aggregates.

3. Low heat of hydration cement.

4. Better protecting cement for steel reinforcement.

5. Better workability and whether resisting cement.

6. Decorative cement and other special cement.

7

4. CEMENT PRODUCTION PROCESS

8

5. CEMENT PRODUCTION PROCESS TYPES

5.1. WET CEMENT PRODUCTION PROCESS

The wet process method is grinding the raw materials into slurry after mixing with water and

then feeding them into the wet process kiln for drying and calcination and finally forming

clinker. The slurry’s water content is usually 32%-40%. The advantage of Wet process method

is that its good fluidity of raw materials produces high-quality clinker. But it requires more heat

consumption, so it is environmental-unfriendly.

9

5.2. DRY CEMENT PRODUCTION PROCESS

The dry process method is the manufacturing of raw materials into powder, whose water

content is generally less than 1%. The dry process can `reduce heat loss needed by heating and

autoclaving water. But the dry process has its flaw; that is the bad fluidity of materials grain in

a kiln. It will cause an uneven mix.

5.2.1. DRY PROCESS CEMENT METHOD TECHNOLOGICAL PROCESS:

• Crushing and pre-homogenizing.

• Raw materials preparation.

• Raw material homogenization.

• Preheat decomposition.

(1) Material dispersion (2) Gas-solid separation (3) pre-decomposition

• Firing of cement clinker.

• Cement milling.

• Cement packaging.

5.2.2. DRY PROCESS METHOD’S ADVANTAGES INCLUDE:

• The dry process owns the perfect dust removal effect, it decreases the quantity of dust

in operation which improves the operational environment and makes environmental

protection more convenient and faster.

• The dry process has an excellent pre-warm system, which can speed up the rotation of

the kiln in operation to raise the yield.

10

• The dry process has a good stealing system. It can take full advantage of waste heat to

lower the running expenditure.

• The dry process has a great adaptation to materials. So, the device runs steadily. Cement

clinker calcinated in the kiln has better quality, which brings more economic benefits

for enterprises.

6. PAKISTAN CEMENT INDUSTRY STRUCTURE

The cement industry of the country can be divided into two separate zones: North & South

Zone. North Zone includes provinces of Punjab, Khyber Pakhtunkhwa, Azad Kashmir, Gilgit-

Baltistan, and parts of Balochistan, while South Zone includes provinces of Sindh and

Balochistan. There are 19 and 5 cement units in the North and South Region, all together. The

industries in the North Zone represent around four-fifth of the total rated capacity.

However, North and South zones have their separate demand-supply dynamics. Players

operating in the South Market have the opportunity to tap several export markets, thus

providing greater room for revenue diversification.

6.1. EXPANSION

Pakistan is amongst the three Cement Concentrations in the world where demand is expected

and has the potential to grow at its fastest. Given the favorable demand outlook and to enhance

efficiencies, four cement manufacturers (Lucky Cement, D.G. Khan Cement, Cherat Cement,

and Attock Cement) have recently added 16% additional capacity.

Company Plant

Capacity

Million MT

per year

Projected

Cost in

million

Region Completion

Year

Plant Manufacturer

DG Khan

Cement

2.68 $300 South 2018 FLSmidth (Danish

cement plant

manufacturer)

Lucky

Cement

2.42 $200 North 2018 Chinese plant with

European lines

Attock

Cement

1.26 $130 South 2017 M/s Hefei Cement Re-

search and Design

Institute (HCRDI),

Cherat

Cement

1.3 $120 North 2017 M/s Tianjin Cement

Industry Design and

Research Institute

Company Limited

(TCDRI) – China

11

7. PAKISTAN CEMENT INDUSTRY PROJECTION

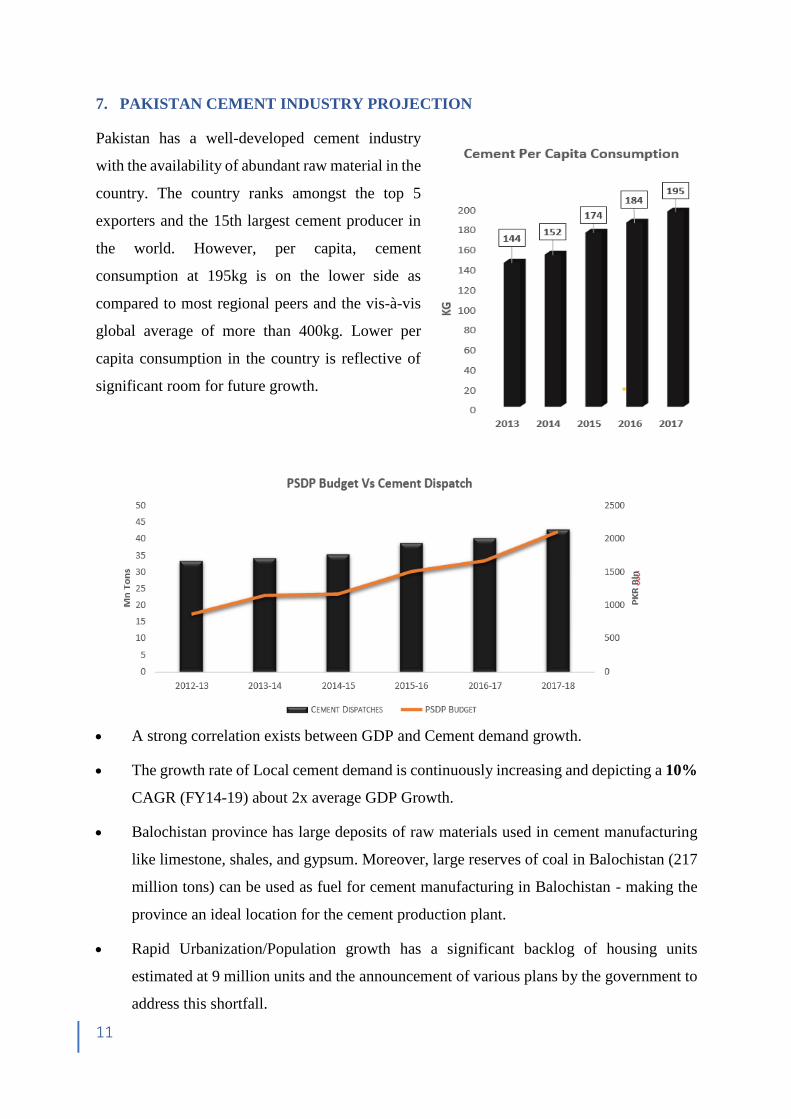

Pakistan has a well-developed cement industry

with the availability of abundant raw material in the

country. The country ranks amongst the top 5

exporters and the 15th largest cement producer in

the world. However, per capita, cement

consumption at 195kg is on the lower side as

compared to most regional peers and the vis-à-vis

global average of more than 400kg. Lower per

capita consumption in the country is reflective of

significant room for future growth.

• A strong correlation exists between GDP and Cement demand growth.

• The growth rate of Local cement demand is continuously increasing and depicting a 10%

CAGR (FY14-19) about 2x average GDP Growth.

• Balochistan province has large deposits of raw materials used in cement manufacturing

like limestone, shales, and gypsum. Moreover, large reserves of coal in Balochistan (217

million tons) can be used as fuel for cement manufacturing in Balochistan - making the

province an ideal location for the cement production plant.

• Rapid Urbanization/Population growth has a significant backlog of housing units

estimated at 9 million units and the announcement of various plans by the government to

address this shortfall.

12

• Increased spending on CPEC projects especially SEZs and Gwadar could provide upside

potential to forecasted demand.

• Increased GDP growth foreseen on account of large-scale infrastructure projects

(Hydropower, roads, etc.) and CPEC Projects i.e. Thermal (Coal) powered projects, dams.

• Balochistan being the gateway to CPEC – potential cement export to Afghanistan, Central

Asian and Gulf countries can be increased.

13

8. SETTING UP CEMENT PLANT IN BALOCHISTAN

Sustained expansion in economic activity and investment in various infrastructure projects

under PSDP and CPEC, coupled with increased demand from private housing schemes have

bolstered the construction sector during the last few years. This has had a spill over impact on

the allied segments of cement and steel as well. Rising demand and healthy margins have also

induced cement manufacturers to expand their production capacities aggressively, from 49.4

million tons to 70 million tons in the last few years.

The importance of Balochistan in cement production

1. Though raw materials (limestone, Shale, and Gypsum) are in abundance in other

provinces as well, land availability is an issue due to the high density of population and

the large number of cement plants already in operation in these areas.

2. Due to the excessive availability of raw material, Balochistan is an ideal location for

establishing cement plants especially small production plants with a capacity of up to

500 TPD at various locations.

3. A mini cement plant will target a market of an entire dissatisfied market that is too small

for a medium-size plant (intermediate cities). It can also focus on the export of cement

to Afghanistan and Gulf countries through Gwadar.

4. The whole production can be sold in the nearest market, reducing transportation costs.

5. In general, permits and licenses for a mini plant are easier to obtain than for a medium-

size plant. It is easier to find large enough mines near the plant, thus reducing the cost

of transporting raw materials.

The Government of Balochistan is encouraging and facilitating the establishment of Cement

Production Plants in the eastern part of Balochistan (Sulaiman Foldbet) such as Loralai,

Barkhan, Musa Khel, Kohlu, and Dera Bugti considering their huge deposits of cement raw

material resources like limestone, shale, and gypsum. Moreover, these areas are relatively close

to the Gwadar Seaports through CPEC routs and to Afghanistan, a major export target for the

cement industry in Pakistan.

14

9. RAW MATERIAL USED IN CEMENT PRODUCTION:

1. Limestone: (Total annual production in Balochistan is 7 million tons)

Limestone exists in abundance in different parts of Balochistan. Quetta, Kalat, Harnai,

Sor Range, and Spintangi areas have reserves of limestone with several hundred meters

thick layers of limestone.

2. Gypsum: (Total annual production in Balochistan is 0.5 million tons)

In Balochistan Sibi, Barkan, Kohlu, and Loralai districts have huge deposits of Gypsum.

3. Shale: (Total annual production in Balochistan is 1.2 million tons)

Shale is a fine-grained sedimentary rock that is formed from the compaction of silt and

clay-size mineral particles that we commonly call "mud." Found all over Balochistan.

Additionally, Balochistan also has 217 million tons of coal reserves, which is 520 mainly used

as cement production.

10. PROCEDURE FOR SETTING UP A CEMENT PLANT

Setting up a cement plant is both time and capital-intensive; it could take anywhere between

Two to Five years from concept to commissioning and an investment of around US $ 250 - 270

million for a typical integrated plant of 3 million tpa cement capacity. The size of a cement

plant could vary from 0.2 million tpa to 5.0 million tpa. (0.2 million tpa (i.e., 500 TPD) plant

will cost about US $ 1.8 – 2 million.

A mini cement plant (between 100 and 500tpd of clinker) can be a better solution compared to

plants of medium and large size, for the following reasons:

• It does not require a large investment. In this way, small and medium entrepreneurs can

venture into the cement business.

• Mini cement plants have the same technology that medium and large size plants have.

• Their production costs compared with larger plants are relatively higher, but

competitive.

• It is possible to install a mini cement plant to attend an entire dissatisfied market that is

too small for a medium-size plant (intermediate cities).

• A mini cement plant can be installed at remote sites with non-existent or inadequate

access roads.

• The whole production can be sold in the nearest market, reducing transportation costs.

15

• In general, permits and licenses for a mini plant are easier to obtain than for a medium-

size plant. It is easier to find large enough mines near the plant, thus reducing the cost

of transporting raw materials.

Before starting to build a cement plant, it is imperative to know what the cement-making

process involves. The cement manufacturing process starts with the mining of limestone

followed by grinding it with other raw materials like clay, shale, bauxite, iron ore, etc. to

prepare a raw meal, which is heated at a sintering temperature of 1,400 to 1,500 degree Celsius

in a kiln to manufacture clinker. The clinker is then finely ground along with additives like

gypsum, fly ash, slag, etc. to produce the desired type and quality of cement. Cement is then

stored in silos from where it is dispatched to the market in 50 kg bags and/or in bulk.

11. MAJOR STAGES INVOLVED IN SETTING UP AN INTEGRATED CEMENT

PLANT ARE:

11.1. INITIATION & CONCEPTION STAGE

A. First step is to decide the kind of plant to be set up for manufacturing cement. There are four

major types of plants (units) that can be set up:

• Integrated unit (IU): This type of unit comprises an all-inclusive facility to produce

clinker from limestone, which further is ground with additives to manufacture cement.

• Grinding Unit (GU): This type of unit, as the name suggests, has the facility to only

grind clinker along with desired additives to manufacture cement. Clinker for a grinding

unit is sourced either from its parent unit or from other sources/open market. Most of

the grinding units are typically set up near a major cement consumption center to

capture the market, subject to it being in reasonable vicinity to the envisaged blending

material source(s).

• Blending unit (BU): This kind of establishment essentially blends Ordinary Portland

Cement (OPC) with fine blending material(s) to manufacture different kinds of cement.

The objective of setting up a blending unit is also to be near a major market center with

a primary function of mixing sourced OPC with a suitable blending material of

relatively high fineness (high Blaine). Thus, blended or mixed cement product requires

less specific power consumption subject to sourcing the blending materials of relatively

high fineness.

• Bulk Cement Terminal (BCT): This type of unit is primarily a separately located

storing and packing/dispatching plant of a parent cement manufacturing plant located

16

elsewhere. Cement is received in bulk essentially by sea, or rail, and stored in a set of

silos. It is typically packed and sold in 50 kg bags and can be dispatched in bulk also

depending on end-users' requirements. The primary objective of such an establishment

is to be located in close vicinity of a major cement consumption center and to cater to

its needs ensuring quicker turnaround from the time order is placed by the end-user for

delivery of cement.

B. The next major step is to identify the location for setting up the cement plant. A plant location

is an irrevocable strategic decision. Parameters for determining the location principally depend

on the type of plant envisioned to be set up. Salient parameters in context being:

• IU: location of an IU is comparatively easier to decide as it ideally must be located as

close as possible to a limestone source. However, for this, a company needs to secure a

limestone mine. Acquisition of limestone deposit is a critical decision; thus, it is

important to carry out a detailed study to examine and evaluate the deposit in terms of

quality, quantity, ease of mining, etc. before investing in the mines.

• Downstream units: The decision on the location of these units depends upon several

factors including access to high consumption markets, future demand growth,

competition intensity, blending material sources and availability, prices, etc.

At the end of this stage, a broad concept of the project should be in place in terms of plant

location(s), capacity and investment requirement. This phase can span anywhere between 0.5

to 2 years depending upon when the board gives its approval to go ahead to the next phase.

12. PRE-PROJECT STAGE

The initiation/conception stage lays the foundation for the next important milestone of setting

out the action plan for the "pre-project activities". The pre-project stage is the preparatory stage

where the concept and configuration of the proposed cement plant need to be transformed to a

relatively structured form from the initial broad concept.

17

12.1. THE MAJOR MILESTONES OF THE PRE-PROJECT STAGE ARE:

Securing limestone: Limestone is the key ingredient in cement manufacturing and thus, it is

very critical to secure limestone before going ahead with setting up a cement factory.

This involves the following activities:

• If the company does not own mines, then limestone mines can be acquired either

through an auction process or through the acquisition of any existing company holding

a mining lease or by applying for a mining license in some other countries

• The acquisition of limestone has become very critical as limestone mines can now be

obtained only through mining lease auctions carried out by the Government. With this,

the process of mine leasing has become relatively challenging and cost-intensive, which

calls for assiduous planning in fulfilling cost and strategy effective bidding expertise

• Geological investigations for estimating the limestone reserves

• Mine planning

• Statutory approvals for mines

Techno-economic feasibility report (TEFR)/detailed project report (DPR): to establish the

technical feasibility and financial viability of the project. This also helps the stakeholders in

evaluating associated risks and exploring possible mitigative measures.

12.2. THE SALIENT FEATURES OF A TYPICAL TEFR/DPR ARE AS FOLLOWS:

• Input materials: Availability of limestone, correctives, additives, fuel, etc. It also

includes the availability and cost of utilities.

• Markets: Market transparency, estimation of achievable sales volume, and ex-factory

realization.

• Location and Infrastructure.

• Technology: Suitable technology, equipment sizing, and estimation of storage

capacities, broad civil design, electrical and instrumentation engineering concepts,

environmental control measures, etc.

• Human resource: Manpower count and cost

• Implementation: Implementation strategy and schedule

• Financial analysis: Investment cost, financial returns, and sensitivity analysis

• Risks and mitigation measures

18

12.3. LAND PROCUREMENT

The acquisition of land for mines and plants is a tedious and time taking process. This typically

involves the following steps:

• Identification of land for setting up the plant and ascertaining its land use pattern.

• Establishing the land use pattern and applying for a change in land use, if required.

• Acquisition and registration, and allied works about the land patches.

12.4. Regulatory and statutory clearances

Many regulatory and statutory clearances are required for setting up of a plant and start

operations, the few major ones out of many such required clearances/permissions are:

• Environment clearances for mines and plant

• Forest clearance

• Consent to establish the mines and plant (CTE)

• Consolidated approvals for sourcing utilities (power, water, etc.) and handling effluents

• Consent and/ or no objection certificate from local pollution control board(s)

• Certificate of commencement

12.5. Financial closure.

Ideally, the company should arrange for the funds before starting the project. Although some

large business houses begin the project by first putting in a portion of the equity and then

parallelly commencing the process of arranging for other types of finances.

A detailed techno-economic feasibility report is usually submitted to the financial institutions

for obtaining a loan. The project is appraised by financial institutions based on their paraments

to validate the results highlighted in the TEFR. Once the institution is satisfied with feasibility,

the loan is sanctioned for the project. The institution can either grant the loan on its own or

form a consortium of financial institutions that together finance the loan.

The aforementioned activities play an important role in determining the overall success of the

proposed cement project. Pre-project activities can span from 1 to 2 years dependent primarily

on the time taken on securing limestone mines and getting financial closure.

19

13. PROJECT EXECUTION STAGE

Project execution is a crucial stage and needs to be carefully planned to avoid cost and time

overrun. Most companies set up a multi-functional team of technical professionals for project

execution. Liaison, finance, and administration functions are also important to ensure that land

acquisition, clearances, and funds availability do not create a bottleneck in project execution,

as many of these activities from the pre-project stage continue well into the project execution

stage. Project execution has two main components ' planning and monitoring, and

implementation.

Project planning and monitoring: The establishment of an efficient system for project

planning and monitoring, including exporting procedures for progress review and coordination,

is very vital for successful project execution. This can either be done by an in-house team or

can be outsourced to a project management consultant.

14. PROJECT IMPLEMENTATION:

Project implementation comprises the following steps.

14.1. Basic engineering:

This step covers the following:

• Finalization of technical concept covering basic specifications for plant and machinery

and other relevant features

• Systems engineering for utilities

• Preparation of plant layout and process flow sheet

• A decision on execution mode, viz.,

• Turnkey: One single contractor is responsible for all project activities concluding with

the handing over of the plant to the owner.

• Semi-turnkey: There are usually two agencies - supplier and contractor. The supplier is

responsible for all activities that occur offshore, i.e. outside the country/project site. The

contractor is responsible for all activities that occur onshore i.e. within the country/

project site.

• Package: The plant is split up into functional process departments and procured

accordingly. Several main suppliers are responsible for the detailed engineering,

manufacture, and supply of equipment(s).

20

• Shopping: In this case, the company/consultant formulates the basic design for the

project and assists in procuring equipment

• Most of the companies prefer package mode. Thus, this step also involves defining

packages and battery limits for each package so that there are no grey areas and no gaps

which could potentially create a bottleneck during the plant construction phase.

15. PROCUREMENT OF MAIN EQUIPMENT AND SERVICES:

This covers the following:

• Preparation and release of a tender for inviting bids

• Receipt of offers from various suppliers

• Evaluation of offers

• Technical rating of offers

• Financial negotiation

• Award and signing of the contract

16. DETAILED ENGINEERING:

This covers the following:

• Engineering of plant and integration of equipment from different suppliers

• Review of suppliers' drawings

• Procurement of other auxiliaries and services

• Civil construction: Construction of civil structures

• Mechanical erection: Setting up of plant and machinery

• Electrical erection: Setting up of power system and electrical equipment

• Mechanical completion: Completion of mechanical erection

• Electrical completion: Completion of electrical erection

• Pre-commissioning trials: Trial run(s) to ensure all equipment are operational and

identify issues/bottlenecks if any

• Commissioning: Commissioning of a plant implies that all components of the plant are

operational, and the plant as a whole is running smoothly?

• Performance guarantee (PG) tests: These tests are conducted by the equipment suppliers

to ensure/certify that the equipment is delivering the output as per the terms mentioned

in the contract

21

• Commercial production: After successful PG tests, the plant is considered ready to start

commercial production

Many companies engage a technical consultant for some or all stages of project

management/construction monitoring to ensure a smooth execution process.

17. KEY FACTORS IN SETTING UP OF A CEMENT PLANT

Some of the important factors which need to be kept in mind during setting up a cement plant

are:

• Markets: Revenue for the business comes from the market, and thus, it is important to

do thorough research in terms of market transparency to understand the market demand,

competition, prices, and prospects before venturing into this business.

• Limestone: Limestone being the key input material and fuel being important to

sustaining the energy-intensive cement manufacturing process, reliable availability of

limestone and fuel are two vital factors in smooth and cost-effective operations of a

cement plant.

• Location: The location of the plant should be selected keeping in view the availability

and price economics of input materials, access to all required infrastructure and utilities,

and proximity to high consumption cement markets.

A plant location is an irrevocable strategic decision. Parameters for determining the

location principally depend on the type of plant envisioned to be set up. Ideally, it must

be located as close as possible to a limestone source. However, for this, a company

needs to secure a limestone mine. Acquisition of limestone deposit is a critical decision;

thus, it is important to carry out a detailed study to examine and evaluate the deposit in

terms of quality, quantity, ease of mining, etc. before investing in the mines.

• Financial viability: To ensure the financial viability of the project, it is important to

simulate various downside cases and thereby know the possible impact if the cement

demands, prices, etc. do not meet future growth assumptions. This sensitivity scenario

also brings confidence that the debt component of the business can still be serviced

despite an economic slowdown and will keep the business afloat.

• Funds availability: While it is important to wisely select the location, plant technology,

suppliers, etc., it is also critical to ensure funds availability at the right time to avoid

delays and thereby cost overruns.

22

• Project management: A multi-disciplinary team, internal and/or external, is vital for

conceptualization, planning, procurement, system integration, and execution of the

project.

• Rule and regulations: It is important to identify and adhere to all applicable rules and

regulations and obtain all the regulatory and statutory clearances for establishing and

running the plant. It would also be prudent to foresee possible changes in policies that

may impact the cement business.

18. RULES AND REGULARITIES BY GOVERNMENT OF BALOCHISTAN

18.1. RULES FOR EXPLORATION LICENSE

The following documents will be required for the Exploration License application under rule

10 & 26 of Balochistan Mineral Rules, 2002.

• Five copies of the comprehensive geological description of the area of land over which

the license is sought.

• Five copies of the geological Map of the applied area (A3 size) covering all the

geological features, structure, formation, etc.

• Location of the area regarding the magisterial district; (Refer rule 18(1)(d))

• The extent of the area and the boundaries by reference to identifiable physical features

and co-ordinate reference points; (Rule 26(1)(b) and (C)).

• The potential for a nature of mineralization in the applied area (Rule 26(1)(i)).

• The program of exploration operations proposed to be carried on, the estimated

expenditure in respect thereof, and the period within which the operation will be carried

on;(Rule (1)(d)(i)).

• A report containing particulars of the state of the environment in the area to which the

application relates, including any existing damage to the environment, the anticipated

effect and likely adverse impact which the proposed exploration operations may have

on the environment; including measures for the prevention of pollution, disposal of

waste and the rehabilitation of land; (Rule 26(d)(ii)).

• Proposals for the control or elimination of any particular risks (whether health, safety,

or otherwise) involved in exploration operations proposed to be undertaken.

• Particulars of the applicant’s technical and financial resources to carry out the

exploration operations and those of any person to be engaged to provide such resources,

23

together with supporting documentary evidence and copies to relevant contractual

agreements; (Rule 18(1) (f) and 26 (1)(e)).

• A copy of the Memorandum and Articles of Association of the company and an attested

copy of the certificate of incorporation/registration of the company in Pakistan.

• Proposals in respect of the matters specified in rule 13(1)(b) to (h).

• Annual reports and audited financial statements of the company for the last three (3)

years.

• List of Directors/ Shareholders with the address.

• CV of Technical officers.

• Bank Certificate (Local Bank).

• Application fee for Exploration License Rs: 240,000/- and application form fee

Rs.6,000/- as specified in the First Schedule to the rules (Rule 10 (1) (c)).

18.2. REGULARITIES BY BALOCHISTAN INDUSTRIES AND COMMERCE

DEPARTMENT

18.2.1. PARTNERSHIP ACT, 1932

Meaning and Nature of Partnership

• Association of two or more than two persons.

• Result of agreement between two or more persons.

• The agreement must be to share the profit of the business.

• Business must be carried on by all or any of them acting for all.

• Unlimited Liability

• Restriction on transfer of Interest

• Unanimity of consent

REGISTRATION OF FIRM

Under the partnership act, all firms don't need to get themselves registered. But an unregistered

firm may suffer several disabilities.

An Application in the prescribed format (Form A) with the prescribed fee of PKR. 20,000 has

to be submitted to the registrar of the firms of the state in which the place of business of the

firm is situated.

24

The Application must contain the following particulars

• The name of the firm

• The place of the business of the firm.

• The names of any other places where the business of the firm is carried on.

• The date when each partner joined the firm

• The names in full and permanent addresses of the partners.

18.2.2. THE BALOCHISTAN BOILER AND PRESSURE VESSEL ACT, 2015

The boiler Act contains the law related to registration and inspection of the steam boiler. It

Extends to the whole of Balochistan.

REGISTRATION OF BOILER

• The owner of the Boiler shall apply to the chief inspector to have the boiler registered.

• In case of Boiler is imported a third-party inspection is required to obtain an

examination certificate confirming the integrity of the boiler.

• After receipt of the application chief inspector shall arrange a visit for the examination

of the boiler.

• The boiler is examined at maximum pressure and if the test passed registration

certificate is awarded to the owner for the period not exceeding 12 months.

• The schedule for fee inspection is provided in the next slide