essentials of the - lsuc · 2 1:45 p.m. – 2:05 p.m. the top 5 tax issues for private companies...

TRANSCRIPT

*CLE17-0090801-A-PUB*

chair

Rory Cattanach Wildeboer Dellelce LLP

September 25, 2017

ESSENTIALS OF THE Privately Held Company 2017

Prac�ce Gems

DISCLAIMER: This work appears as part of The Law Society of Upper Canada’s initiatives in Continuing Professional Development (CPD). It provides information and various opinions to help legal professionals maintain and enhance their competence. It does not, however, represent or embody any official position of, or statement by, the Society, except where specifically indicated; nor does it attempt to set forth definitive practice standards or to provide legal advice. Precedents and other material contained herein should be used prudently, as nothing in the work relieves readers of their responsibility to assess the material in light of their own professional experience. No warranty is made with regards to this work. The Society can accept no responsibility for any errors or omissions, and expressly disclaims any such responsibility.

© 2017 All Rights Reserved

This compilation of collective works is copyrighted by The Law Society of Upper Canada. The individual documents remain the property of the original authors or their assignees.

The Law Society of Upper Canada 130 Queen Street West, Toronto, ON M5H 2N6Phone: 416-947-3315 or 1-800-668-7380 Ext. 3315Fax: 416-947-3991 E-mail: [email protected] www.lsuc.on.ca

Library and Archives Canada Cataloguing in Publication

Practice Gems: Essentials of the Privately Held Company 2017

ISBN 978-1-77094-010-0 (Hardcopy)ISBN 978-1-77094-011-7 (PDF)

1

Final June 27, 2017

Chair: Rory Cattanach, Wildeboer Dellelce LLP

September 25, 2017 1:00 p.m. to 4:00 p.m.

Total CPD Hours = 2 h 30 m Substantive + 30 m Professionalism

The Law Society of Upper Canada Donald Lamont Learning Centre

130 Queen Street West Toronto, ON

SKU CLE17-00908

Agenda 1:00 p.m. – 1:05 p.m. Welcome and Opening Remarks Rory Cattanach, Wildeboer Dellelce LLP

1:05 p.m. – 1:25 p.m. Share Structures and Capitalization

David Dunlop, McMillan LLP

1:25 p.m. – 1:45 p.m. Directors’ and Officers’ Liability: Organizing for the Best

Results

Simon Bieber, Wardle Daley Bernstein Bieber LLP

PRACTICE GEMS: ESSENTIALS OF THE

PRIVATELY HELD COMPANY 2017

2

1:45 p.m. – 2:05 p.m. The Top 5 Tax Issues for Private Companies before and after Incorporation

James Fraser, Fraser Tax Law Professional Corporation

2:05 p.m. – 2:20 p.m. Corporate Property Ownership and Ontario’s New

Record-Keeping Requirements

Arielle Kieran, Dentons Canada LLP 2:20 p.m. – 2:25 p.m. Question and Answer Session 2:25 p.m. – 2:40 p.m. Networking Break 2:40 p.m. – 3:10 p.m. Professionalism Issues When Advising the Privately Held

Company (30 m )

Rory Cattanach, Wildeboer Dellelce LLP (Moderator) Panelists: Emily Fan, Lerners LLP Vaughn MacLellan, DLA Piper (Canada) LLP

3:10 p.m. – 3:30 p.m. Exiting the Private Corporation or Ousting a Shareholder Without Losing Your Shirt

Diane Brooks, Blaney McMurtry LLP 3:30 p.m. – 3:50 p.m. Succession Planning for Private Companies: Planning for Change

Maxwell Spearn, Miller Thomson LLP

3

3:50 p.m. – 4:00 p.m. Question and Answer Session 4:00 p.m. Program Ends

September 25, 2017

SKU CLE17-00908

Table of Contents

TAB 1 Corporate Property Ownership and Ontario’s New Record-Keeping Requirements…………………………………………………………………….1 – 1 to 1 – 5

Corporate Property and Ownership and Ontario’s New Record-Keeping Requirements ……………………………………………………...……………1 – 1 to 1 –3

Record of Ownership – Single Property……………..……………….1 – 4 to 1 – 4

Record of Ownership Interests……………………………………………1 – 5 to 1 – 5

Arielle Kieran, Dentons Canada LLP

TAB 2 Exiting the Private Corporation or Ousting a Shareholder without Losing your Shirt – A Case Study……………………………………………….2 – 1 to – 2 – 13

Diane Brooks, Blaney McMurtry LLP

PRACTICE GEMS: ESSENTIALS OF THE

PRIVATELY HELD COMPANY 2017

TAB 1

Corporate Property Ownership and Ontario’s New

Record-Keeping Requirements

Arielle Kieran, Dentons Canada LLP

September 25, 2017

Practice Gems: Essentials of the

Privately Held Company 2017

Corporate Property Ownership and Ontario’s New Record-Keeping Requirements If your clients own, lease, or otherwise deal with real property in Ontario, you should consider the

effect of reporting requirements that came into force on December 10, 2016. The recently enacted

Forfeited Corporate Property Act, 2015 (“FCPA”), which amends the Business Corporations Act (Ontario)

(“OBCA”) and the Corporations Act (Ontario), requires corporations to maintain a register of their

“ownership interests in land” in Ontario. The requirement is set out in an amendment to Section 140.1 of

the OBCA as follows:

Register of interests in land in Ontario 140.1 (1) A corporation shall prepare and maintain at its registered office a register of its ownership interests in land in Ontario. Same (2) The register shall,

(a) identify each property; and

(b) show the date the corporation acquired the property and, if applicable, the date the corporation disposed of it.

Supporting documents (3) The corporation shall cause to be kept with the register a copy of any deeds, transfers or similar documents that contain any of the following with respect to each property listed in the register:

1. The municipal address, if any.

2. The registry or land titles division and the property identifier number.

3. The legal description.

4. The assessment roll number, if any.

The Purpose of this Legislation is to Prevent and Manage Escheats

When a corporation that dissolves does not dispose of its property, that property is forfeited to

and vests in the Crown.1 This process is referred to as an “escheat”. Escheats can be problematic for the

Crown, particularly if the land is environmentally contaminated or subject to tax and utility arrears. In order

to manage the issues that tend to arise when corporate real property escheats, several statutes have

been introduced and amended to place additional obligations on corporate owners. For example, the

1 Business Corporations Act (Ontario), R.S.O. 1990, c. B.16 at s. 244(1).

1 - 1

FCPA introduces personal liability for directors and officers of dissolved corporations where the province

incurs costs associated with environmental remediation required to render forfeited property saleable.2

When the FCPA amendments were introduced as part of the Budget Measures Act, 2015, the

Minister of Finance stated that they would “improve the management of corporate land forfeited to the

province”.3 On the same day, the Ministry of Finance published a press release4 that identified the

following five objectives of the FCPA:

Mitigate risks to Ontario taxpayers that may arise when corporate property forfeits to and

becomes Crown property when a company is dissolved;

Reduce the number of corporate properties that forfeit to the Crown;

Increase corporate accountability for costs associated with forfeited corporate property;

Increase transparency and certainty in the management and disposition of forfeited corporate

property; and

Return forfeited property to productive use as quickly and efficiently as possible.

The Language Used to Create These Obligations is Ambiguous, but the Ministry has confirmed

that only Fee Simple Interests are captured

Now that corporations are required to keep a register of their ownership interests in land, we need

to understand what qualifies as an “ownership interest in land”. The term is not defined in the FCPA or the

OBCA. As many practitioners noted when the legislation was first published, an “ownership interest” could

ostensibly include a leasehold interest, an easement, a mortgage interest, a beneficial interest, or a

statutory right.

On April 3, 2017, Brenda Linington and Marta Zoladek of the Ministry of the Attorney General,

Civil Law Division gave a presentation titled “Top 10 Things Real Estate Practitioners Need to Know

2 Forfeited Corporate Property Act, 2015, SO 2015 C.38, Sched 7 at sections 30-31. For more information, see http://www.dentons.com/en/insights/articles/2016/december/5/corporate-dissolution-will-not-protect-former-directors-and-officers-from-environmental-liabilities

3 See http://www.ontla.on.ca/web/house-proceedings/house_detail.do?Date=2015-11-18&Parl=41&Sess=1&locale =en#para683 4 See https://news.ontario.ca/mof/en/2015/11/amendments-and-proposals-in-the-budget-measures-act-2015.html

1 - 2

about the Forfeited Corporate Property Act, 2015” as part of the 14th Annual Real Estate Law Summit. In

that presentation, Linington and Zoladek clarified that the requirement applies to “fee simple or co-

ownership interests only” and accordingly confirmed that leases, easements, mortgage interests, and

other ownership interests are not captured by the legislation.

Practical Advice for Real Estate, Leasing and Corporate Lawyers

Corporations that are incorporated on or after December 10, 2016 must comply with the

requirements in Section 140.1 immediately, and corporations incorporated before that date have until

December 18, 2018 to comply. Lawyers should reach out to all corporate clients and notify them of the

new corporate record keeping requirements as soon as possible. Many corporations are likely to require

assistance with creating their registers. Lawyers may need to complete Teraview name searches as well

as subsearches of adjacent and subject land, and may assist in obtaining roll numbers.

Lawyers should also be mindful of the fact that this register must be kept at the corporation’s

registered address in Ontario. While many of our clients have traditionally preferred to use our law firm’s

address when first incorporating, we would now suggest that law firms avoid this practice so that they are

not obligated to maintain the ownership register at their offices. During the transition period, lawyers

should review all current and historical corporate client files to determine whether the law firm’s address

has been used as the corporation’s registered address, and contact clients to update this information

wherever possible.

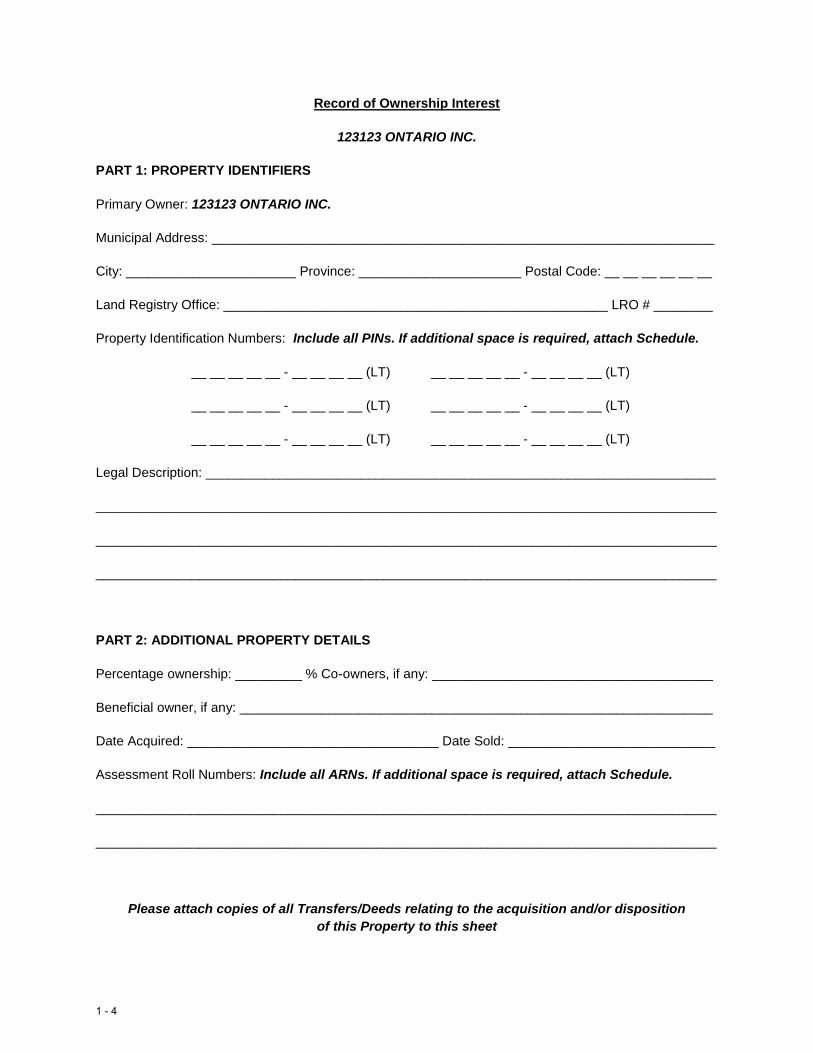

Sample Registers of Ownership Interests

To assist with the creation of registers for your clients, we have included two sample registers

with this package. The first will accommodate details regarding a single property, and is likely to be

preferred by smaller corporations with limited real estate holdings. It can be printed multiple times and

completed with respect to each property. The second, which consists of a larger ownership chart, is likely

to be more useful to clients with extensive holdings.

1 - 3

Record of Ownership Interest

123123 ONTARIO INC.

PART 1: PROPERTY IDENTIFIERS

Primary Owner: 123123 ONTARIO INC.

Municipal Address: ____________________________________________________________________

City: _______________________ Province: ______________________ Postal Code: __ __ __ __ __ __

Land Registry Office: ____________________________________________________ LRO # ________

Property Identification Numbers: Include all PINs. If additional space is required, attach Schedule.

__ __ __ __ __ - __ __ __ __ (LT) __ __ __ __ __ - __ __ __ __ (LT)

__ __ __ __ __ - __ __ __ __ (LT) __ __ __ __ __ - __ __ __ __ (LT)

__ __ __ __ __ - __ __ __ __ (LT) __ __ __ __ __ - __ __ __ __ (LT)

Legal Description: _____________________________________________________________________

____________________________________________________________________________________

____________________________________________________________________________________

____________________________________________________________________________________

PART 2: ADDITIONAL PROPERTY DETAILS

Percentage ownership: _________ % Co-owners, if any: ______________________________________

Beneficial owner, if any: ________________________________________________________________

Date Acquired: __________________________________ Date Sold: ____________________________

Assessment Roll Numbers: Include all ARNs. If additional space is required, attach Schedule.

____________________________________________________________________________________

____________________________________________________________________________________

Please attach copies of all Transfers/Deeds relating to the acquisition and/or disposition

of this Property to this sheet

1 - 4

Record of Ownership Interests

123123 ONTARIO INC.

Municipal

Address

Property

Identification

Number(s)

Land

Registry

Office

Percentage

Ownership

Date

Acquired

Date Sold Legal Description Assessment Roll

Number(s)

Transfer/

Deed

Located

at Tab

123 Main Street

Toronto, Ontario

A1A 1A1

12345-0001(LT)

12345-0002(LT)

Toronto (#80) 100% June 1, 1990 N/A – Currently

owned by 123123

Ontario Inc.

PT LT 1, CON 2 AS IN

123123 S&E PTS 4 & 5,

66R123123; SUBJECT TO

AN EASEMENT IN GROSS

OVER PT 1, 66R321321

AS IN AT123123; CITY OF

TORONTO

10.01.010.100.010

00.0000

11.01.010.100.010

00.0000

1

1 - 5

TAB 2

Exiting the Private Corporation or Ousting a Shareholder

without Losing your Shirt

Diane Brooks, Blaney McMurtry LLP

September 25, 2017

Practice Gems: Essentials of the

Privately Held Company 2017

1

Exiting the Private Corporation or Ousting a Shareholder without

Losing your Shirt

A CASE STUDY

Of

LUCY’S DIAMONDS INC.

Diane Brooks

Blaney McMurtry LLP

Prepared for Practice Gems: Essentials of the Privately Held Company 2017

September 25, 2017

2 - 1

2

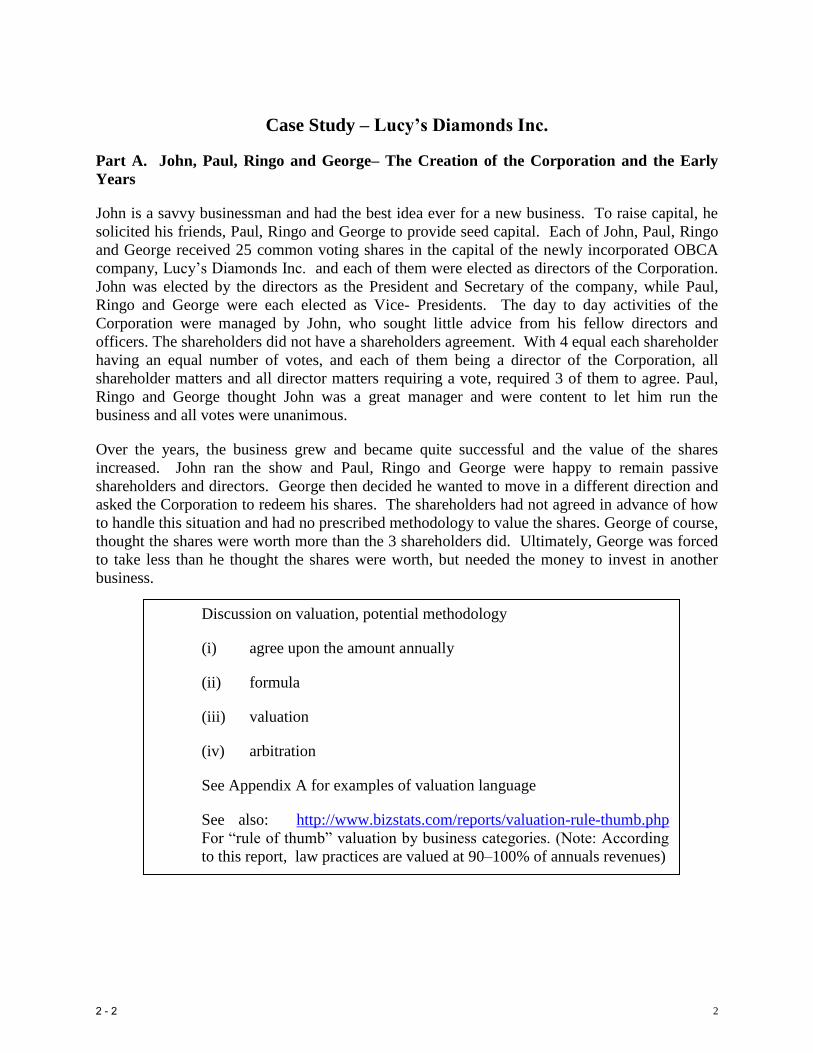

Case Study – Lucy’s Diamonds Inc.

Part A. John, Paul, Ringo and George– The Creation of the Corporation and the Early

Years

John is a savvy businessman and had the best idea ever for a new business. To raise capital, he

solicited his friends, Paul, Ringo and George to provide seed capital. Each of John, Paul, Ringo

and George received 25 common voting shares in the capital of the newly incorporated OBCA

company, Lucy’s Diamonds Inc. and each of them were elected as directors of the Corporation.

John was elected by the directors as the President and Secretary of the company, while Paul,

Ringo and George were each elected as Vice- Presidents. The day to day activities of the

Corporation were managed by John, who sought little advice from his fellow directors and

officers. The shareholders did not have a shareholders agreement. With 4 equal each shareholder

having an equal number of votes, and each of them being a director of the Corporation, all

shareholder matters and all director matters requiring a vote, required 3 of them to agree. Paul,

Ringo and George thought John was a great manager and were content to let him run the

business and all votes were unanimous.

Over the years, the business grew and became quite successful and the value of the shares

increased. John ran the show and Paul, Ringo and George were happy to remain passive

shareholders and directors. George then decided he wanted to move in a different direction and

asked the Corporation to redeem his shares. The shareholders had not agreed in advance of how

to handle this situation and had no prescribed methodology to value the shares. George of course,

thought the shares were worth more than the 3 shareholders did. Ultimately, George was forced

to take less than he thought the shares were worth, but needed the money to invest in another

business.

I.

Discussion on valuation, potential methodology

(i) agree upon the amount annually

(ii) formula

(iii) valuation

(iv) arbitration

See Appendix A for examples of valuation language

See also: http://www.bizstats.com/reports/valuation-rule-thumb.php

For “rule of thumb” valuation by business categories. (Note: According

to this report, law practices are valued at 90–100% of annuals revenues)

2 - 2

3

Part B. The Lender/Shareholder

With George gone, the business continued to thrive, however soon more operating capital was

required. John found an investor, Brian Epstein, who was willing to lend the Corporation

money, but for tax reasons, wanted to invest by way of equity, through his private holding

company, Epstein Ltd., instead. The Corporation issued Epstein Ltd. preferred non voting

shares, redeemable in 3 years, with monthly dividends which equivalated to an interest rate of

10%. However, as a way to protect its investment, Mazursky Ltd wanted voting shares in

addition to its preferred shares. Desperate for his investment, John caused the Corporation to

issue Mazursky Ltd 25 common shares and Epstein Ltd. elected Brian Epstein, as its nominee on

the board of directors.

Now, the Corporation was back to having 4 equal shareholders and 4 directors.

At this point, having learned their lesson after George’s departure, the shareholders entered into a

shareholders agreement providing for the following terms and conditions:

The day to day operations of the company would be overseen by the President.

The shareholders would agree annually on the share valuation based on the Corporation’s

performance for the previous year.

No shares could be redeemed or sold for a period of 2 years. After 2 years, a majority of

the shareholders could cause the Corporation to call any shareholder’s shares for 120% of

their value, or any shareholder could put their shares to the Corporation for 80% of their

value.

Shares could not be transferred without the consent of a majority of the shareholders.

Discussion on Oppression Remedy - Could George have used the oppression

remedy to challenge the valuation? \

Unlikely if the valuation method was remotely reasonable.

See Re BCE Inc., 2008 SCC 69

See also Appendix B for excerpt of the provisions of the Business

Corporations Act relating to oppression.

Who is entitled to use the oppression remedy? The Supreme Court set out a 2

step process. Has the party’s reasonable expectations been breached and if so,

does the conduct complained of amount to oppression, unfair prejudice or

unfair disregard?

2 - 3

4

John continued to operate the company on a day to day basis. The other shareholders put

minimal time into the business, but enjoyed the ownership aspects of the company. Monthly

management fees were paid to each of them for their minimal time. John took a salary and

management fees and was awarded annual bonuses. The business continued to thrive and the

shareholders voted annually on the share valuation.

Part C. Removing another Shareholder

Two years after the shareholders agreement was signed, Ringo was starting to irritate John. Paul

and Brian, who thought John could do no wrong, sided with John and they caused the company

to call Ringo’s shares. Ringo was not happy, but had no choice but to sell his shares back to the

company for 120% of their value.

Part D. Is John Misbehaving

With Ringo gone, the remaining shareholders each had 25 common shares each and Epstein Ltd.

continued to hold its preferred shares (having continued to inject capital by way of preferred

shares, on the same terms and conditions as the original, with redemption rights after 3 years and

with monthly dividends equating to 10% interest). With only 3 shareholders and directors, two

shareholders and two directors could carry any vote. Brian and John were great pals and Brian

was happy with the returns that he was making on his money.

Soon however, chinks in the armour began to show through. This was John’s big idea and he

treated the Corporation as if it were his own. While the company was making money, John took

risks without consulting his fellow shareholders or directors and made some bad investments.

Discussion – What issues arise as a result of a lender also being a shareholder?

Discussion: Could Ringo have challenged the call on his shares?

Unless Ringo can argue that (a) he had no opportunity for independent legal

advice before he signed it or (b) that in setting the annual value of the shares,

he was oppressed, there is little he can do.

2 - 4

5

Brian, worried about his investment in the Corporation began to take a more active role in the

day to day activities and asked John a lot of questions. John’s reaction was to be more secretive

and was angered by Brian questioning his management. John felt he was acting in the

Corporation’s best interests.

As Brian did more and more digging, he discovered that John was not drawing his bonus as he

felt the Corporation needed the cash flow. Instead, he was submitting his personal expenses

through the Corporation and deducting the amounts from what was owed to him.

Brian became more and more disenchanted with John’s management. He complained profusely

to Paul, who, knowing that Brian was the money man, was sympathetic to Brian’s concerns.

They called a shareholders’ meeting to confront John.

Brian and Paul combined now hold the majority vote as shareholders and as directors. While the

shareholders agreement prohibited them from removing John as a director (John as a shareholder

is entitled to name a nominee to the board of directors), Brian and Paul called a directors’

meeting and removed John as President of the Corporation and appointed Brian as President. As

the shareholders agreement provided that the President run the day to day business of the

Corporation, Brian was now in charge.

Discussion – Why this is inappropriate?

Discussion - Is Brian acting in the best interests of the Corporation or he is

merely protecting his investment in the Corporation to ensure that he gets paid

back what he has put into the Corporation through his preferred shares. What

are the duties of a lender who is also a shareholder and a director.

Discussion - Could John have a claim against the Corporation for

constructive dismissal?

2 - 5

6

.

Discussion - Could Brian and Paul have used the oppression remedy or the

derivative action remedy under the OBCA to challenge John’s actions, or can

John challenge Paul and Brian’s actions in removing him as President.

Oppression Remedy vs Derivative Action

(see Appendix C for excerpts of the provisions of the OBCA relating to

derivative action)

See Rea v. Wildeboer, 2015 ONCA 373, 2015 CarswellOnt 7602

The Ontario Court of Appeal has recently clarified the dividing line between

oppression remedy and derivative action remedy:

Oppression remedy is a personal remedy by a complainant against the

corporation or the board of directors;

Derivative action remedy is a remedy by a complainant on behalf of the

corporation for wrongful acts done TO the corporation itself – the conduct is

alleged to have affected the corporation and all shareholders equally.

Discussion - As lawyer to the Corporation, how does the lawyer

handle the representation of the Corporation? Who does the lawyer take

instructions from?

2 - 6

7

APPENDIX A

VALUATION METHODS

(1) “Book Value” shall be calculated as total equity, plus retained earnings, as determined in

accordance with GAAP by reference to the annual audited financial statements of the

Corporation.

(2) “Fair Market Value” means the price determined in an open and unrestricted market

between informed prudent parties, acting at arm’s length and under no compulsion to act,

expressed in terms of money; (problematic)

(3) Fair Market Value of the Shares

(a) As soon as practicable after the occurrence of a Valuation Event, the Vendor and the

Purchaser shall use all reasonable best efforts to reach agreement as to the Fair Market Value of

the Shares and upon agreement being reached, written confirmation signed by both of the

Vendor and the Purchaser shall be forwarded to the Accountants. In the event that the Vendor

and the Purchaser are unable to agree upon the Fair Market Value of the Shares within a period

of thirty (30) days from the Valuation Event, then within five (5) days after the end of such thirty

(30) day period each of the Vendor and the Purchaser shall deliver written notice (the “Best Price

Notice”) setting out their own separate determination of the Fair Market Value of the Shares.

(b) In the event that the Vendor and the Purchaser are unable to agree upon the Fair Market

Value of the Shares within the thirty (30) day period contemplated in section 12.2(a), then the

Fair Market Value of the Shares shall be determined by an independent qualified appraiser

jointly appointed by the Vendor and the Purchaser, and who shall provide to each of the Vendor,

the Purchaser and to the Accountants a written report setting forth a determination of the Fair

Market Value of the Shares within thirty (30) days of appointment.

(c) In the event that the Vendor and the Purchaser do not agree upon the Fair Market Value

of the Common Shares within the period contemplated in section 12.2(b) and cannot mutually

agree upon an independent qualified appraiser within seventy-five (75) days from the Valuation

Event, then either of the Vendor or the Purchaser shall be entitled, on written notice given to the

other, to apply to a judge of the Ontario Superior Court for selection of two (2) independent

qualified appraisers from among the names of independent qualified appraisers submitted by

each of the Vendor and the Purchaser (not to exceed three (3) names each). Each independent

qualified appraiser so selected shall deliver to each of the Vendor, the Purchaser and to the

Accountants a written report setting forth the determination of the Fair Market Value of the

Shares within thirty (30) days of being so selected, and for the purposes hereof the Fair Market

Value of the Shares shall be the simple average of the two valuations of such appraisers.

(d) If necessary, in preparing any of the valuations contemplated in this section, an

independent qualified appraiser shall be entitled to engage the services of such additional

2 - 7

8

professional valuators or appraisers as such independent qualified appraiser, in his absolute and

unfettered discretion, considers necessary or desirable to perform valuations or appraisals of one

or more of the assets of the Corporation. Each of the Shareholders and the Corporation shall in

all respects co-operate with any independent qualified appraiser in the determination of the Fair

Market Value of the Shares. In particular, each of the Parties shall make available to the

independent qualified appraiser all such documents and information with respect to the affairs of

the Corporation or its Subsidiaries as such independent qualified appraiser may reasonably

require to make his determination. If an independent qualified appraiser specifies a range of

values for the Fair Market Value of the Shares, the Fair Market Value of the Shares determined

by such independent qualified appraiser shall be the mid-point of such range.

(e) The costs of all such appraisals shall be borne by the Party whose determination of the

Fair Market Value of the Shares as set forth in its Best Price Notice was furthest from the Fair

Market Value of the Shares, as finally determined.

(f) In completing such appraisals, all such independent qualified appraisers shall be acting as

experts and not as arbitrators and all such determinations shall be final and binding upon the

parties hereto and no appeal shall lie therefrom.

(4) CALCULATION OF VALUE PER SHARE

(a) “Fair Market Value of the Shares” means the highest cash price in terms of money which

would be obtained as at the Valuation Date if all of the Shareholders sold all of their respective

Shares in an open and unrestricted market (recognizing that the Shares may be securities of a

Corporation which cannot offer its securities to the public) without compulsion, to a willing and

knowledgeable purchaser acting at arms length and wherein determining such amount: (i) no

distinction is made between the various classes of Common Shares; (ii) no diminution or

accretion in value is attributed to any majority or minority interest; (iii) the value of any

insurance on the life of the Principals and the proceeds of such insurance shall be excluded; and

(iv) the fair market value of all intangible and unrecorded assets is included, all as determined in

accordance with generally accepted valuation principles. All other terms or phrases appearing in

title case shall have the meanings ascribed thereto respectively in the Agreement to which this

Schedule is attached and in Article 9 thereof.

(b) “Value Per Share” means the amount obtained when the Fair Market Value of the Shares

is divided by the number of Shares issued and outstanding on the Valuation Date.

2. Immediately following the occurrence of a Valuation Event, the Corporation shall

instruct the Accountants to prepare and deliver to the Vendor and Purchaser under the sale

transaction contemplated in Articles 6, 8, 9 or 10, within a period of forty-five (45) days from the

date of its appointment by the Corporation, a draft report setting forth the Accountant's estimate

as to the Fair Market Value of the Shares and the basis upon which such estimate has been

calculated (the "Accountant's Report").

2 - 8

9

3. If the estimate of the Fair Market Value of the Shares set forth in the Accountant's Report

is acceptable to the Vendor and the Purchaser and agreed to in writing within a period of thirty

(30) days following delivery of the draft Accountant's Report to the Vendor and the Purchaser,

the Accountants shall deliver the Accountant's Report in final form and it shall become the Fair

Market Value of the Shares for the purposes of this Schedule A.

4. If the statement of the Fair Market Value of the Shares set forth in the Accountant's

Report is unacceptable to the Vendor or the Purchaser, they shall negotiate expeditiously and in

good faith during such thirty (30) day period to arrive at a mutually agreeable Fair Market Value

of the Shares. If such agreement is reached the Vendor and the Purchaser shall notify the

Accountants of the amount so determined and agreed upon and such amount shall become the

Fair Market Value of the Shares for the purposes of this Schedule.

5. If the Vendor and the Purchaser are unable to agree as to the Fair Market Value of the

Shares within such thirty (30) day period, the Vendor and Purchaser shall immediately jointly

agree upon an independent, qualified business or realty valuator (the "Valuator") for a final

determination as to the Fair Market Value of the Shares. If the Vendor and the Purchaser are

unable to agree upon a Valuator within fifteen (15) days after the expiry of such thirty (30) days

period, the Valuator shall be selected by the Accountants by lot from among the names of

independent qualified business valuators submitted by each of the Vendor and the Purchaser

(not to exceed three (3) names each).

6. The Valuator so selected shall determine the Fair Market Value of the Shares as quickly

as practicable after the date of its selection. The Valuator may also have regard to any

representations which either the Vendor or the Purchaser wish to make. The Valuator shall

deliver its report concerning the Fair Market Value of the Shares to the Vendor, the Purchaser

and the Accountants (“Valuator’s Report) and such report shall be conclusive and binding on the

Vendor and the Purchaser. The Fair Market Value of the Shares so determined shall become the

Fair Market Value of the Shares for the purposes of this Schedule. In determining the Fair

Market Value of the Shares, the Valuator shall also be considered an expert and shall not be

construed as acting as an arbitrator.

7. The costs and expenses of the Accountants incurred in connection with the preparation of

the Accountant’s Report shall be paid shared equally by the Vendor and the Purchaser. The costs

and expenses of the Valuator incurred in connection with the preparation of the Valuator’s

Report shall be shared equally by the Vendor and the Purchaser, unless the Fair Market Value of

the Shares, as calculated by the Valuator, differs by less than 20% from the Fair Market Value of

the Shares as determined by the Accountants, in which case the party requesting the Valuator

shall pay the costs and expenses of the Valuator incurred in connection with the preparation of

the Valuator’s Report.

8. Immediately after a final determination of the Fair Market Value of the Shares in

accordance with the foregoing, the Accountants shall sent to the Corporation and each of the

Vendor and the Purchaser a report setting out the Value Per Share.

2 - 9

10

APPENDIX B

OPPRESSION REMEDY

(Business Corporations Act, Ontario)

Oppression remedy

248. (1) A complainant and, in the case of an offering Corporation, the Commission may apply

to the court for an order under this section. 1994, c. 27, s. 71 (33).

Idem

(2) Where, upon an application under subsection (1), the court is satisfied that in respect of a

Corporation or any of its affiliates,

(a) any act or omission of the Corporation or any of its affiliates effects or threatens to

effect a result;

(b) the business or affairs of the Corporation or any of its affiliates are, have been or are

threatened to be carried on or conducted in a manner; or

(c) the powers of the directors of the Corporation or any of its affiliates are, have been or

are threatened to be exercised in a manner,

that is oppressive or unfairly prejudicial to or that unfairly disregards the interests of any security

holder, creditor, director or officer of the Corporation, the court may make an order to rectify the

matters complained of. R.S.O. 1990, c. B.16, s. 248 (2).

Court order

(3) In connection with an application under this section, the court may make any interim or final

order it thinks fit including, without limiting the generality of the foregoing,

(a) an order restraining the conduct complained of;

(b) an order appointing a receiver or receiver-manager;

(c) an order to regulate a Corporation’s affairs by amending the articles or by-laws or

creating or amending a unanimous shareholder agreement;

(d) an order directing an issue or exchange of securities;

(e) an order appointing directors in place of or in addition to all or any of the directors

then in office;

2 - 10

11

(f) an order directing a Corporation, subject to subsection (6), or any other person, to

purchase securities of a security holder;

(g) an order directing a Corporation, subject to subsection (6), or any other person, to pay

to a security holder any part of the money paid by the security holder for securities;

(h) an order varying or setting aside a transaction or contract to which a Corporation is a

party and compensating the Corporation or any other party to the transaction or contract;

(i) an order requiring a Corporation, within a time specified by the court, to produce to

the court or an interested person financial statements in the form required by section 154

or an accounting in such other form as the court may determine;

(j) an order compensating an aggrieved person;

(k) an order directing rectification of the registers or other records of a Corporation under

section 250;

(l) an order winding up the Corporation under section 207;

(m) an order directing an investigation under Part XIII be made; and

(n) an order requiring the trial of any issue. R.S.O. 1990, c. B.16, s. 248 (3).

2 - 11

12

APPENDIX 3

DERIVATIVE ACTION

(Business Corporations Act, Ontario)

Derivative actions

246. (1) Subject to subsection (2), a complainant may apply to the court for leave to bring

an action in the name and on behalf of a Corporation or any of its subsidiaries, or

intervene in an action to which any such body corporate is a party, for the purpose of

prosecuting, defending or discontinuing the action on behalf of the body corporate.

R.S.O. 1990, c. B.16, s. 246 (1).

Idem

(2) No action may be brought and no intervention in an action may be made under

subsection (1) unless the complainant has given fourteen days’ notice to the directors of

the Corporation or its subsidiary of the complainant’s intention to apply to the court

under subsection (1) and the court is satisfied that,

(a) the directors of the Corporation or its subsidiary will not bring, diligently

prosecute or defend or discontinue the action;

(b) the complainant is acting in good faith; and

(c) it appears to be in the interests of the Corporation or its subsidiary that the

action be brought, prosecuted, defended or discontinued. R.S.O. 1990, c. B.16, s.

246 (2).

Notice not required

(2.1) A complainant is not required to give the notice referred to in subsection (2) if all of

the directors of the Corporation or its subsidiary are defendants in the action. 2006, c. 34,

Sched. B, s. 38.

Application

(3) Where a complainant on an application made without notice can establish to the

satisfaction of the court that it is not expedient to give notice as required under subsection

(2), the court may make such interim order as it thinks fit pending the complainant giving

notice as required. R.S.O. 1990, c. B.16, s. 246 (3).

Interim order

(4) Where a complainant on an application can establish to the satisfaction of the court

that an interim order for relief should be made, the court may make such order as it thinks

fit. R.S.O. 1990, c. B.16, s. 246 (4).

2 - 12

13

Court order

247. In connection with an action brought or intervened in under section 246, the court

may at any time make any order it thinks fit including, without limiting the generality of

the foregoing,

(a) an order authorizing the complainant or any other person to control the

conduct of the action;

(b) an order giving directions for the conduct of the action;

(c) an order directing that any amount adjudged payable by a defendant in the

action shall be paid, in whole or in part, directly to former and present security

holders of the Corporation or its subsidiary instead of to the Corporation or its

subsidiary; and

(d) an order requiring the Corporation or its subsidiary to pay reasonable legal

fees and any other costs reasonably incurred by the complainant in connection

with the action. R.S.O. 1990, c. B.16, s. 247.

2 - 13