esop case study -ppt

DESCRIPTION

all esopTRANSCRIPT

CASE STUDY ON EMPLOYEE STOCK OPTION PLAN

GROUP No. 4

Ridhi Sood Rajkamal Shah

Unnati Shah Haresh Swaminathan

Overview of Case

LM UK PLC

(HOLDING COMPANY)

LML INDIA LIMITED

WOS - INDIA (LML FASTENERS

LIMITED)

WOS - SOUTH AFRICA

Questions Involved

Wide coverage of employees

To reward performing employees and motivate them to do better

Plan to cover employees of both WOS and Holding Company of LML

Plan to be operational for 10 years

Vesting of options to commence within 6 months of the announcement of the plan, and vesting to take place on the last day of each half year i.e. on 31st March and 30th

September every year

Vesting of options to be completed in 3 years

Discount offered on the price of options to be reasonably encouraging to employees and also optimize the employee compensation expenses

Is it possible for LML to issue ESOP to the employees of LM UK, its Holding Company within the same plan as per the applicable SEBI Guidelines

Types of Stock Based Compensation Plans

Employee Stock Based Compensation Plan

Employee Stock Option Plan (ESOP)

ESOP is an option, a right, a choice given to employees to buy the shares of the company

at a future date at a pre determined price

Stock Index Plans

Restricted Stock Units (RSU)

An employee receives stock which is settled in shares; the right to receive

the shares may be subject to performance. Generally, the strike

price is the face value of shares.

Phantom Stocks

Employee receives phantom stock which is settled in cash for an amount equal to the value of defined number

of shares. Methodology adopted is that of ESOP except that settlement is

in cash.

Stock Appreciation Rights (SAR)

An employee receives shares or cash equal to the increase in the value of

the specified number of shares over a specified period of time.

Employee Share Purchase Scheme (ESPS)

ESPS is an offer given to employees to buy the shares of the company immediately at a pre

determined price, with a lock-in period for sale

What are ESOPs

A right, a choice, but not an obligation

Each option converts into one or more Equity Shares

To buy shares of the Company at a Future Date

At a price fixed today – “Exercise Price”

THE RATIONALE

Market pays, Not the Company from its Cash kitty

Attract and retain talent at start up / high growth stage

Sense of ownership, particularly at a senior level

Links personal wealth creation to the organization’s value creation

Methods to issue ESOP

Direct Route

• Shares will be directly allotted to the employees of the Company

Trust Route

• A Trust is created for allotment of shares to employees

• Company issues shares to the Trust and the Trust further issues shares to the employees

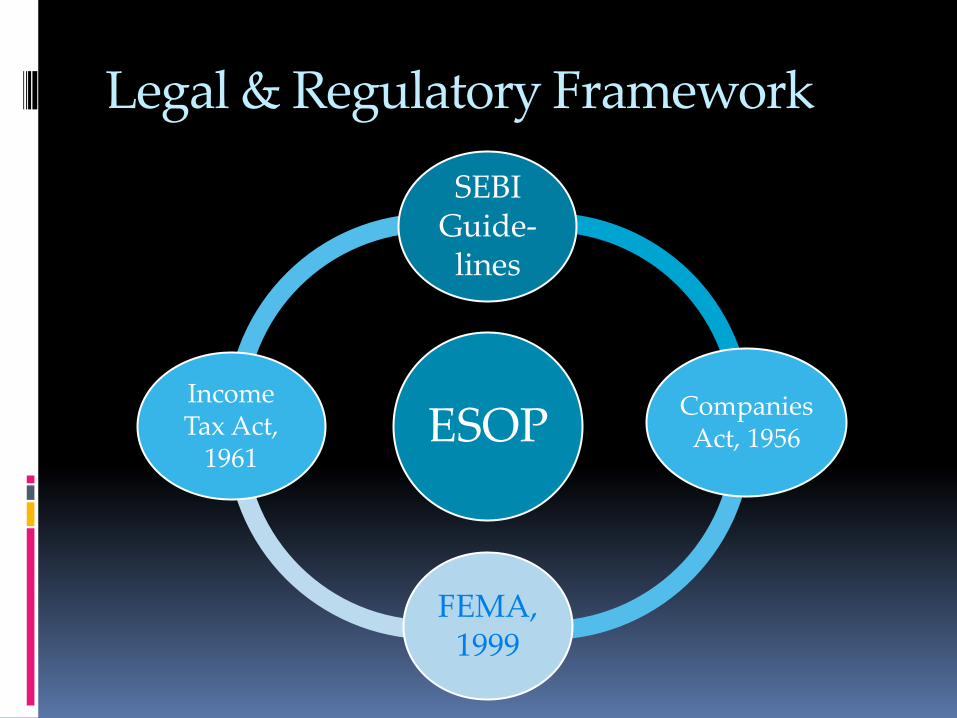

Legal & Regulatory Framework

ESOP

SEBI Guide-

lines

Companies Act, 1956

FEMA, 1999

Income Tax Act,

1961

Companies Act, 1956 Issue of Stock Options requires approval of shareholders by way of a Special Resolution under Section 81 (1a)

Conduct Board Meeting to Constitute Compensation Committee

Compensation Committee will draft ESOP as per law

Board Meeting for approval of draft ESOP

General Meeting Notice to Shareholders

Inform Stock Exchange (SE) about ESOP

Send Notice to SE as per Listing Agreement

Send General Meeting Notice

Approve ESOP by Special Resolution of Shareholders

Provide SE with a copy of proceedings of General

Meeting

File requisite forms along with Special Resolution with ROC

Companies Act, 1956 Shareholders' Special resolution for approval of the Scheme –

prior to grant

Separate resolutions in case of grant of options to – Employees of holding or subsidiary company

Identified employees, during one year, equal to or exceeding 1% of the issued capital at the time of grant of option

The explanatory statement to the Notice and resolution contains details of: Total number of options to be granted

Classes of employees entitled to participate

Requirements of vesting and period of vesting

Maximum period during which the options would be vested

Exercise price or pricing formula

Exercise period and process of exercise

Determining the eligibility of the employees

Maximum number of options to be issued per employee and in aggregate

A statement that the company would conform with accounting policies

Method to value the options –Fair Value/Intrinsic Value

Statement -To disclose in the directors report the Compensation cost impact

SEBI Guidelines "employee" means

a permanent employee of the company working in India or out of India; or

a director of the company, whether a whole time director or not; or an employee as defined in sub-clauses (a) or (b) of a subsidiary, in

India or out of India, or of a holding company of the company.

“Exercise Period” is the time period after vesting within which the employee should exercise his right to apply for shares against the option vested in him in pursuance of the Employee Stock Option Plan.

“Grant” means issue of option to employees under ESOP

“Vesting” means the process by which the employee is given the right to apply for shares of the company against the option granted to him in pursuance of ESOP.

“Vesting Period” is the period between the grant date and the date on which all the specified vesting conditions of an employee share-based payment plan are to be satisfied.

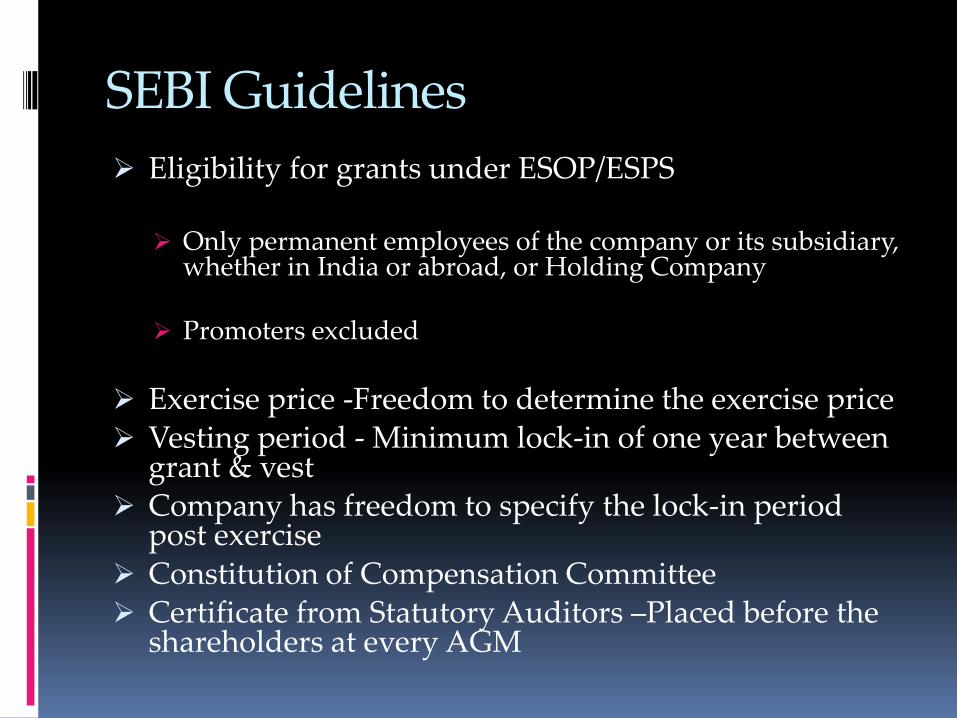

SEBI Guidelines

Eligibility for grants under ESOP/ESPS

Only permanent employees of the company or its subsidiary, whether in India or abroad, or Holding Company

Promoters excluded

Exercise price -Freedom to determine the exercise price Vesting period - Minimum lock-in of one year between

grant & vest Company has freedom to specify the lock-in period

post exercise Constitution of Compensation Committee Certificate from Statutory Auditors –Placed before the

shareholders at every AGM

SEBI Guidelines Employee eligible not to include promoters and directors holding

10% or more of outstanding share capital

Shareholder approval required

Separate resolution for grants to – Employees of holding and subsidiary companies Identified employees holding = or > 1% of issued capital

Explanatory statement to include – Price of shares and number of shares offered Eligibility of employees Total number of shares to be issued

Number of shares offered maybe different for different categories

Special resolution to conform to accounting policies

Freedom to determine the exercise price

Shares issued to be locked in for a minimum period of one year from the date of allotment

Accounting Policies & its Impact ESOPs are treated as another form of employee compensation in

financial statements

Accounting value of options = intrinsic value / fair value of options

Accounting value to be amortized over the vesting period

In case of lapse of unvested options, the accounting to be reversed

In case of lapse of vested options, the accounting to be reversed

Options granted through a Trust –Company required to account assuming the company has issued the options directly to the employees

Two broad methods in place Intrinsic Value Method

Intrinsic Value = Market Price –Exercise Price Static Value as on a particular date

Fair Value Method Amount for which the option can be exchanged between knowledgeable,

willing parties in an arms length transaction Computed using an Option-pricing model like Black Scholes, Binomial

valuation methods.

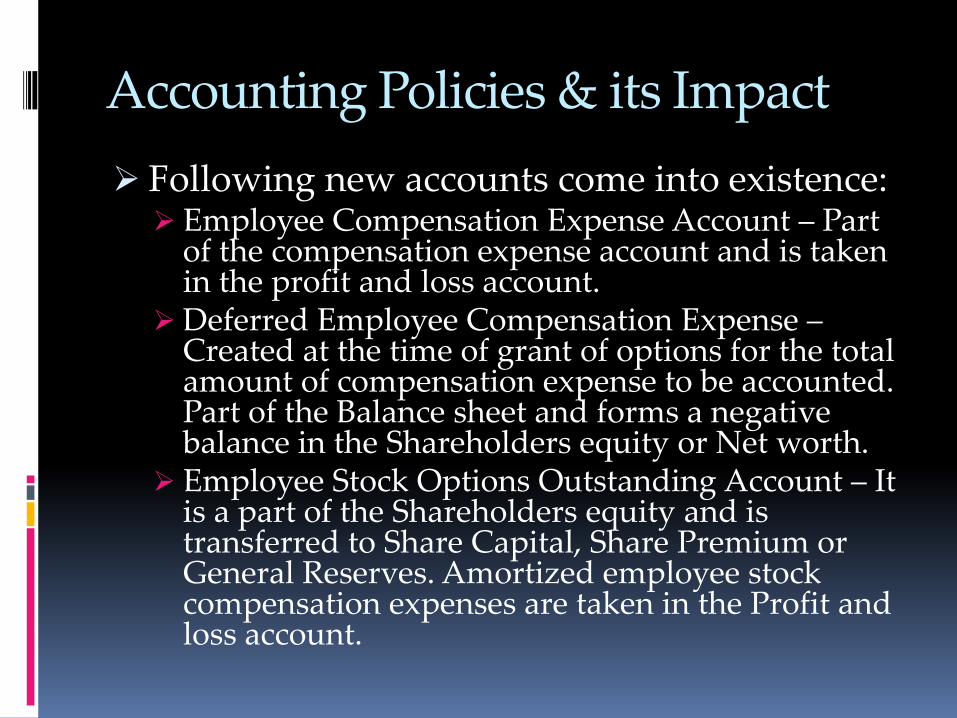

Accounting Policies & its Impact

Following new accounts come into existence: Employee Compensation Expense Account – Part

of the compensation expense account and is taken in the profit and loss account.

Deferred Employee Compensation Expense – Created at the time of grant of options for the total amount of compensation expense to be accounted. Part of the Balance sheet and forms a negative balance in the Shareholders equity or Net worth.

Employee Stock Options Outstanding Account – It is a part of the Shareholders equity and is transferred to Share Capital, Share Premium or General Reserves. Amortized employee stock compensation expenses are taken in the Profit and loss account.

Income Tax Act, 1961

According to the Finance Bill 2009, Fringe Benefit Tax on ESOPs has been abolished

ESOPs have been included in the definition of “Perquisites” under Section 17 (2)

A person holding more than 10% of the shares in a company would not be eligible to participate in employee stock option plan or scheme of the company.

Income Tax Act, 1961

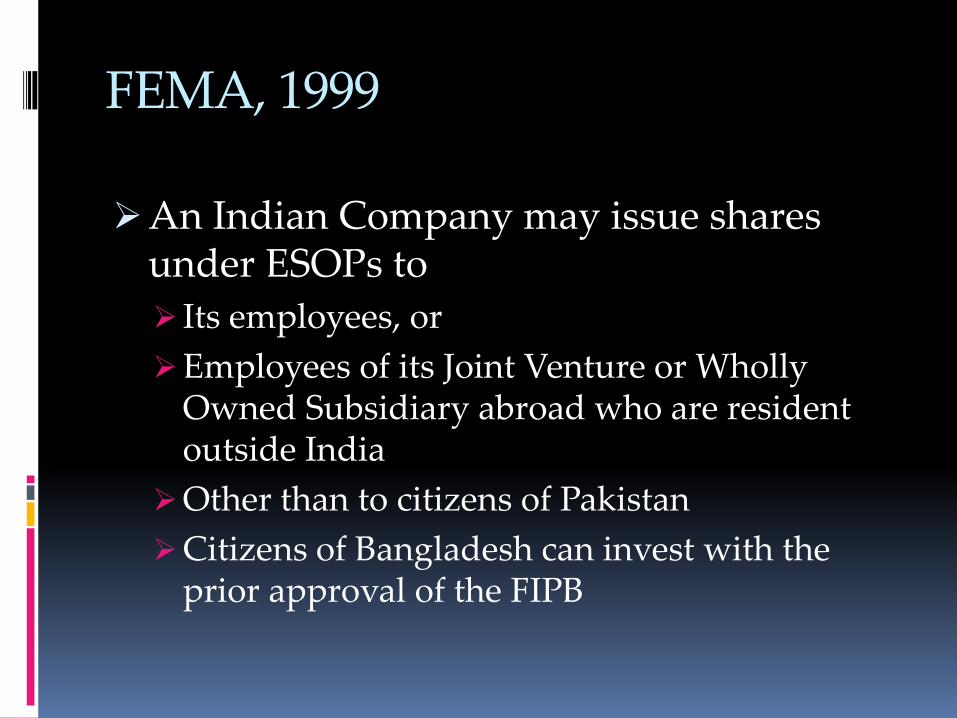

FEMA, 1999

An Indian Company may issue shares under ESOPs to

Its employees, or

Employees of its Joint Venture or Wholly Owned Subsidiary abroad who are resident outside India

Other than to citizens of Pakistan

Citizens of Bangladesh can invest with the prior approval of the FIPB

FEMA, 1999 Conditions:

Scheme must be drawn in compliance with the SEBI (Employee Stock Option Scheme and Employee Stock Purchase Scheme) Guidelines, 1999

Face value of shares to be allotted to non-resident employees should not exceed 5% of the paid up capital

The issuing company shall furnish to the Reserve Bank , within thirty days from the date of issue of shares under the scheme, a report giving the following particulars/documents, -

Names of persons to whom shares are issued under the scheme and

number of shares issued to each of them;

A certificate from the Company Secretary of the issuing company that the value of shares issued under the scheme does not exceed 5% of the paid up capital of the issuing company and that the shares are issued in compliance with the regulations issued by the SEBI in this behalf.

At the time of conversion of options into shares the Indian company has to ensure reporting to the Regional Office concerned of the Reserve Bank in form FC-GPR, within 30 days of allotment of such shares.

LML India Limited’s ESOP As per the express definition of the term “employee”

provided under the SEBI Guidelines, 1999, LML can issue ESOPs to the employees of both its Wholly Owned Subsidiaries in India and South Africa.

The management desires the vesting to commence within 6 months from the announcement of the plan. This would be a violation of the minimum lock-in requirement period as prescribed under the SEBI Guidelines, and hence, the management is advised to commence the vesting only after completion of one year from the date of grant of options.

As regards vesting of options on the last day of each half year i.e. on the 31st March and 30th September every year, SEBI Guidelines provide freedom to the Company to take such decisions.

LML India Limited’s ESOP

Since LML desires to offer ESOPs to employees of its Wholly Owned Subsidiary in South Africa Hence, LML must comply with the FEMA requirements and furnish a report to the RBI within 30 days of issue of shares, along with the requisite certificate from Practising Company Secretary.

LML India cannot issue shares through the

medium of ESOP to the employees of its Foreign Holding Company viz. LM UK PLC since employees of Foreign Holding Companies have not been categorized as “Eligible Employees”, both under SEBI Guidelines and FEMA

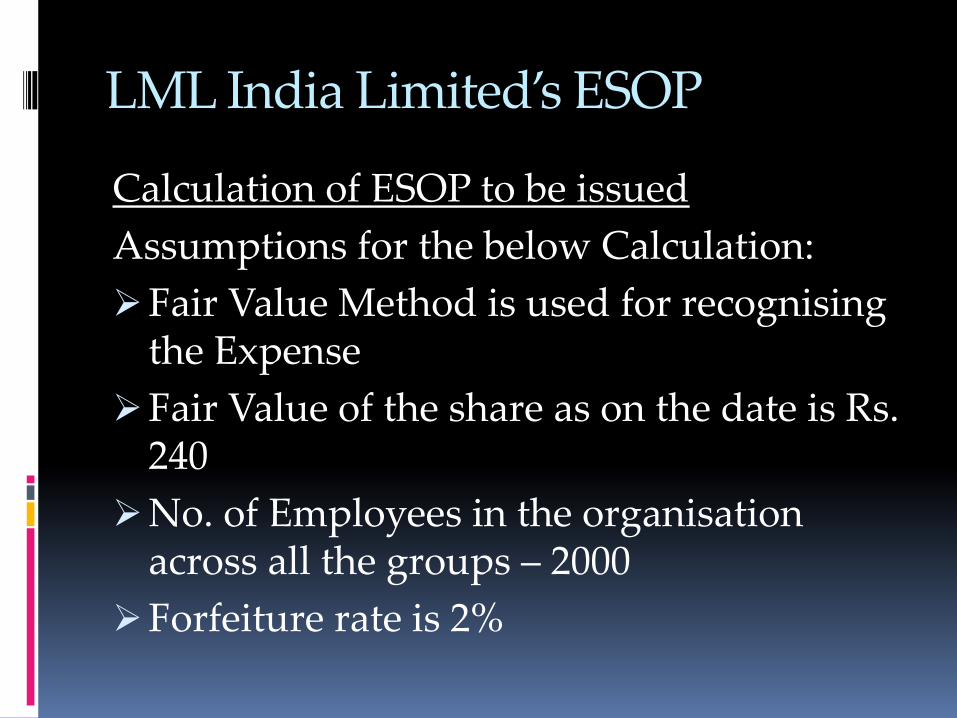

LML India Limited’s ESOP

Calculation of ESOP to be issued

Assumptions for the below Calculation:

Fair Value Method is used for recognising the Expense

Fair Value of the share as on the date is Rs. 240

No. of Employees in the organisation across all the groups – 2000

Forfeiture rate is 2%

LML India Limited’s ESOP

Particulars Amount Rs.

Grant Date 01//09/2012

Market Value of per share as on Grant Date(Rs.) 490

No.of Employees covered 2000

No.of Options Per employee 1000

Vesting Date 01/09/2013

Exercise Date 01/09/2013

Fair value as on Grant Date per share (Rs.) 240

Size of Options (No. of shares to be issued) 2000000

LML India Limited’s ESOP

Particulars Amount Rs.

Fair Value of the option per share 240

Average Annual Forfeiture 2%

No.of shares expected to be vested

(2000 Employees x 1000 Shares x 0.98 x 0.98 x

0.98) 1882384

Value of options to be expected to be vested(Rs.) 451,772,160

Vesting Period 3 Years

Value of Option to be recognised as Expense in

the first year 150,590,720

CALCULATION

Conclusion

In conclusion it can be stated that LML India Limited can effectively combine ownership and participative employment to reward its employees and motivate them by granting ESOPs to its employees and to employees of its Wholly Owned Subsidiaries, both in India and in South Africa.

However, the employees of its Holding

Company LM UK PLC cannot derive the benefits of the ESOP, being outside the purview according to the provisions of the applicant legislations.

Study and Survey

The Survey was conducted by KPMG in India seeking inputs from multinational companies and Indian listed and unlisted companies.

The Survey was divided into fi ve sections:

A) Basic information of the company.

B) Particulars of ESOPs – General.

C) Conditions of grant.

D) Conditions of vesting.

E) Conditions of exercise.

Participation - Industry

Out of the 203 companies having an active ESOP or who were considering implementing a plan:

Approx. 40 percent (82) of respondents were from the ICE sector; and

Approx. 16 percent of respondents were each from the Financial Services and Private Equity sector (33) and the Manufacturing and Consumer Goods sector (32) respectively.

40

16

18

11

7

6 2

ICE

BFSI

Manu.& FMCG

Health & Life Science

Energy

Real Estate

Others

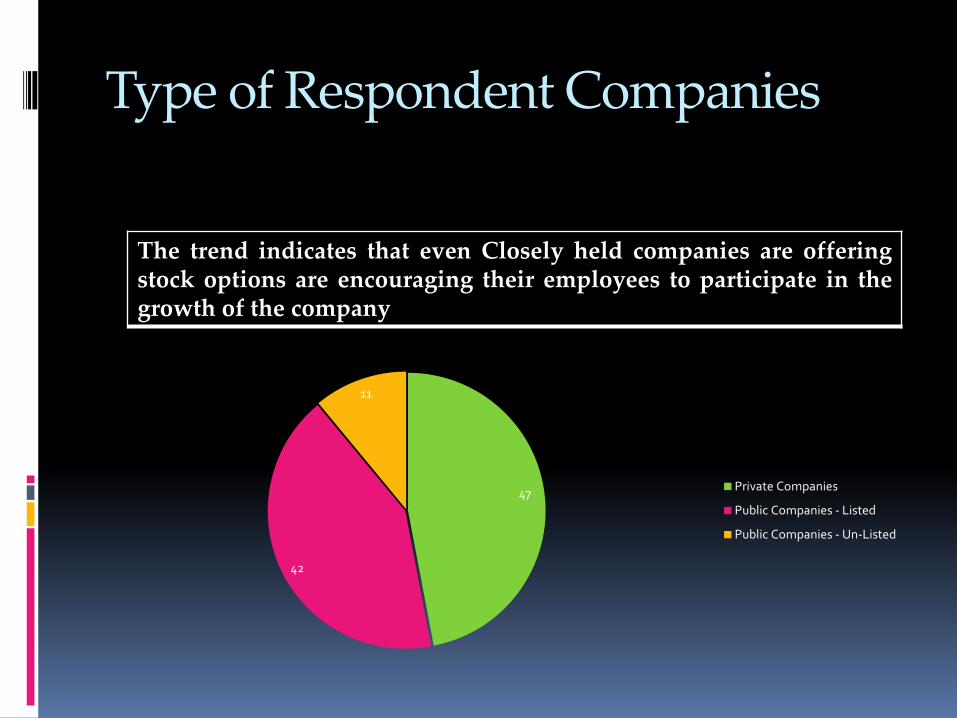

Type of Respondent Companies

The trend indicates that even Closely held companies are offering stock options are encouraging their employees to participate in the growth of the company

47

42

11

Private Companies

Public Companies - Listed

Public Companies - Un-Listed