erp 1.0 is over what's next ?

DESCRIPTION

Ctof 21st jan issue 2010TRANSCRIPT

NEXT?WHAT’SERP 1.0 IS OVER

The Advent ofAndroidsPAGE 15

BEST OF BREED

Stay Hungry,Stay

Foolish PAGE 04

I BELIEVE

NEXT? NEXT?WHAT’SERP 1.0IS OVER

The Advent of Advent of AdventAndroidsPAGE 15

BEST OF BREED

StayHungry,StayFoolishStayFoolishStayHungry,Foolish

Hungry,PAGE 04

I BELIEVE

ER

P 1.0 IS

OV

ER

. WH

AT

'S N

EX

T? | T

HE

AD

VE

NT

OF

AN

DR

OID

S | M

AK

ING

GA

ME

TH

EO

RY

WO

RK

FO

R M

AN

AG

ER

SVolum

e 05 | Issue 11

January | 21 | 2010 | Rs.50Volume 05 | Issue 11

A 9.9 Media Publication

Drive a Hard Bargain PAGE 12

A QUESTION OF ANSWERS

IT MAY BE TOO EARLY TO WRITE OFF ERP, BUT THE BUSINESS SOFTWARE HAS STARTED SHOWING WORRISOME SIGNSOF FATIGUE | PAGE 18

S P I N E

Technology for Growth and Governance

CT

O

FO

RU

M

EDITORIALRAHUL NEEL MANI | [email protected]

1thectoforum.com 21 JANUARY 2010CTO FORUM

The Ultimate Cloud War. In the

battle for supremacy in the cloud, it's the user who wins

Several interesting develop-ments made the headlines

of business and technology portals this month. But one that caught my attention was the $250 million Microsoft-HP deal unveiled recently. In a nutshell, the deal is simply a joint go-to-market effort. Yet it got noticed by experts and analysts alike. Speculations abound on the rea-sons for the deal. Some say it’s a public cloud play. Others feel it is a private cloud foray. Still others interpret it as an indirect

new alliance could serve as an effective response to a similar tie-up between Cisco, VMware and EMC on private clouds announced in November 2009.

Now, it will be interesting to see how HP, which already has a similar relationship with VMware, does the balancing act. A few HP blogs claim that Microsoft is ‘a’ preferred provider of virtualisation solutions for HP and not ‘the’ only provider.

Smart Bundles — which are the combinations of HP hardware, Microsoft and HP infrastructure software, and different MS-HP apps build on top of SQL and Exchange Servers — will be available to small/mid-size businesses and partners who want to offer them as a cloud service. Although there has been no written commitment, there is

attempt to lock customers into buying integrated hardware/software/services stacks that the two companies are calling ‘Smart Bundles’.

But, I can't help but inter-pret it as an open war for the supremacy in the cloud. Here’s why. In case you didn’t notice, the deal was announced a day after Microsoft’s arch rival (in the virtualisation space) VMware announced its take-over of Zimbra, the messaging vendor from Yahoo. Also, this

speculation that at some point Microsoft and HP can also offer BI, online-transaction-processing and messaging apps in the Azure (Microsoft’s cloud operating system).

This will give Microsoft a strong foothold in the virtualisation, management and data centre spaces, where VMware is also aiming for supremacy. Clearly, battlelines are getting drawn in the cloud! But for customers, it’s a win-win – they will now have a choice between Microsoft and VMware.

EDITORS PICK26

Making Game Theory Work for ManagersA new model generates answers representing the best compromise between risks and opportunities in all likely futures.

2 21 JANUARY 2010 thectoforum.comCTOFORUM

18

JANUARY10VO

LUM

N 0

5 |

ISS

UE

11

CTOFORUM

CO

VE

R D

ESI

GN

: B

INES

H S

REE

DH

AR

AN

COVER STORY

18 | ERP 1.0 is Over : What’s Next? It may be too early to write off ERP, but the business software has started showing worrisome signs of fatigue

COPYRIGHT, All rights reserved: Reproduction in whole or in part without written permission from Nine Dot Nine Interactive Pvt Ltd. is prohibited. Printed and published by Kanak Ghosh for Nine Dot Nine Interactive Pvt Ltd, C/o K.P.T House, Plot Printed at Silverpoint Press Pvt. Ltd. TTC Ind. Area, Plot No. A-403, MIDC Mahape, Navi Mumbai 400709

COLUMN04 | I BELIEVE:STAY HUNGRY, STAY FOOLISH A CIO who strives to do something different that the world will sit up and notice.BY- G N NAGARAJ

52 | VIEW POINT: THE PROBLEM WITH RE-LATIONSHIPS Social CRM may be a great concept, but it is tough to bring customer and company together. BY- DYLAN PERSAUD

FEATURES15 | BEST OF BREED: THE ADVENT OF ANDROIDS BlackBerry changed mobile technol-ogy. The next wave will be led by Apple's iPhone and Google's Android

CO NTE NT S THECTOFORUM.COMJANUARYJANUARY

CO NTE NT S THECTOFORUM.COM THECTOFORUM.COMJANUARY10V

OLU

MN

05

| I

SSU

E 11

JANUARYJANUARYTHE ADVENTOF ERP 2.0Page 20

BREATHING LIFE INTO THE

OLD WARHORSEPage 23

S P ARYAVice-President IT, Amtek Group.

SURYA BHARDWAJ Vice President, India

Applications, Oracle India

3thectoforum.com 21 JANUARY 2010CTO FORUM

JANUARY10

A QUESTION OF ANSWERS

12 | “Drive a Hard Bargain”“Solid state drives (SSDs) will complement the traditional hard disk drives (HDDs)," Teh Ban Seng, VP & MD, APJ, Seagate

VOLUME 05 | ISSUE 11 | 21 JANUARY 2010

Managing Director: Dr Pramath Raj SinhaPrinter & Publisher: Kanak Ghosh

Publishing Director: Anuradha Das Mathur

EDITORIALEditor: Rahul Neel Mani

Resident Editor (West & South): Ashwani MishraSr. Assistant Editor: Gyana Ranjan Swain

Consulting Editor: Shubhendu ParthPrincipal Correspondent: Vinita Gupta

Sr. Correspondent: Jatinder SinghCorrespondent: Sana Khan

DESIGNSr. Creative Director: Jayan K Narayanan

Art Director: Binesh Sreedharan Associate Art Director: Anil VK

Manager Design: Chander Shekhar Sr. Visualisers: PC Anoop, Santosh Kushwaha

Sr. Designers: Prasanth TR & Anil T Photographer: Jiten Gandhi

ADVISORY PANELAjay Kumar Dhir, CIO, JSL Limired

Anil Garg, CIO, DaburDavid Briskman, CIO, Ranbaxy

Mani Mulki, VP-IS, Godrej IndustriesManish Gupta, Director, Enterprise Solutions AMEA, PepsiCo

India Foods & Beverages, PepsiCoRaghu Raman, CEO, National Intelligence Grid, Govt. of India

S R Mallela, Former CTO, AFLSantrupt Misra, Director, Aditya Birla Group

Sushil Prakash, Country Head, Emerging Technology-Business Innovation Group, Tata TeleServices

Vijay Sethi, VP-IS, Hero Honda Vishal Salvi, CSO, HDFC Bank

Deepak B Phatak, Subharao M Nilekani Chair Professor and Head, KReSIT, IIT - Bombay

Vijay Mehra, Executive VP, Global Head-Industry Verticals, Patni

SALES & MARKETINGVP Sales & Marketing: Naveen Chand SinghNational Manager Online Sales: Nitin Walia

National Manager-Events and Special Projects: Mahantesh Godi (09880436623)Product Manager – Rachit Kinger

Asst. Brand Manager: Arpita GanguliCo-ordinator-MIS & Scheduling: Aatish Mohite

Bangalore & Chennai: Vinodh K (09740714817)Delhi: Pranav Saran (09312685289)

Kolkata: Jayanta Bhattacharya (09331829284)Mumbai: Sachin Mhashilkar (09920348755)

PRODUCTION & LOGISTICSSr. GM. Operations: Shivshankar M Hiremath

Production Executive: Vilas MhatreLogistics: MP Singh, Mohd. Ansari,

Shashi Shekhar Singh

OFFICE ADDRESSNine Dot Nine Interactive Pvt Ltd

C/o K.P.T House,Plot 41/13, Sector-30,Vashi, Navi Mumbai-400703 India

Printed and published by Kanak Ghosh forNine Dot Nine Interactive Pvt Ltd

C/o K.P.T House, Plot 41/13, Sector-30,Vashi, Navi Mumbai-400703 India

Editor: Anuradha Das MathurC/o K.P.T House, Plot 41/13, Sector-30,

Vashi, Navi Mumbai-400703 India

Printed at Silverpoint Press Pvt. Ltd.D 107,TTC Industrial Area,

Nerul.Navi Mumbai 400 706

www.thectoforum.com

26 | NEXT HORI-ZONS: MAKING GAME THEORY WORK FOR MAN-AGERS A new model generates answers repre-senting the best compro-mise between risks and opportunities

REGULARS

01 | EDITORIAL08 | ENTERPRISE

ROUNDUP48 | BOOK

REVIEW

advertisers’ index

IBM REVERSE GATEFOLD

VERIZON IFC

TATA INDICOM 05

APC 07

MEGANET 33

TATA COMMUNICATION IBC

CISCO BC

This index is provided as an additional service.The publisher does not assume

any liabilities for errors or omissions.

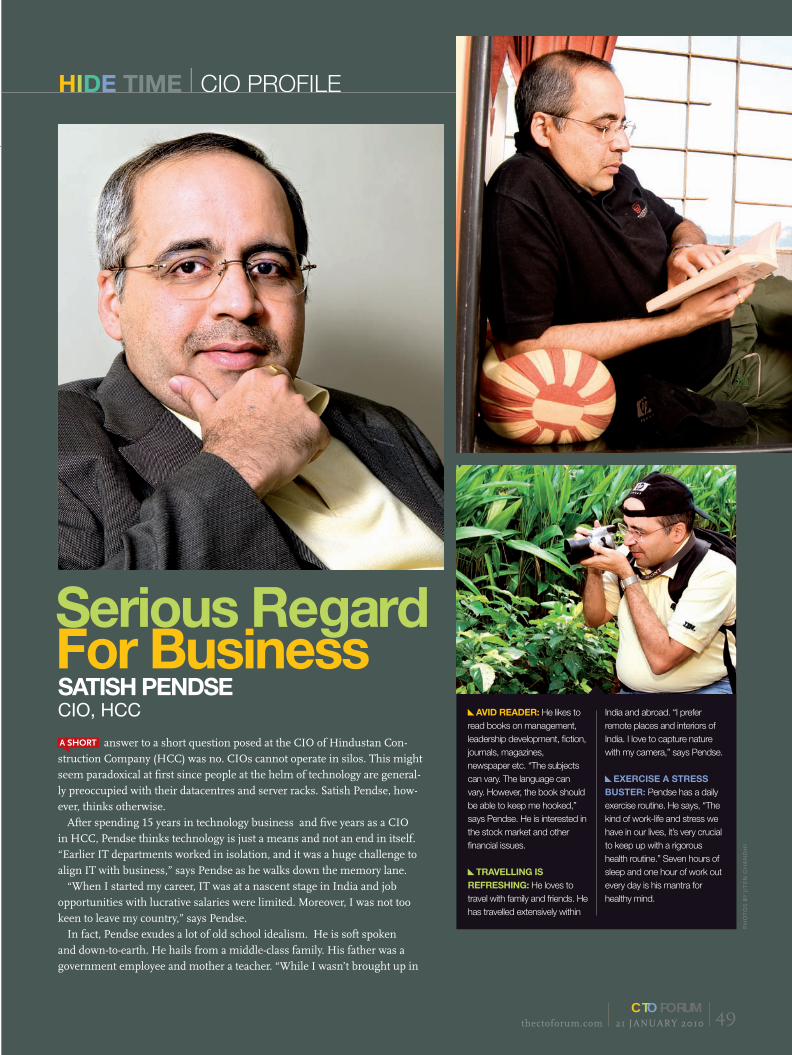

49 | HIDE TIME: SERIOUS REGARD FOR BUSINESS A CIO who believes that if the leader has trusts his team, they will surprise him by surpassing his expectations

12

26 49

I BELIEVE

4 21 JANUARY 2010 thectoforum.comCTOFORUM

CURRENTCHALLENGE

BY G N NAGARAJ | CTO, Religare EnterprisesTHE AUTHOR HAS over 18 years of experience in leading technology teams of large and

next generation financial services companies in India

DOING SOMETHING DIFFERENT THAT THE WORLD WILL SIT UP AND NOTICE

WHAT I believe in defines me. What I believe in dictates my actions and the decisions I take. I believe that Google has hit the glass ceiling in its ability to innovate in a manner that relates to the customer. I believe that Apple will belt out one wonder after another and have customers

eating out of their hands with their classy lifestyle products.

I believe that we should all go about conducting our business and managing all our relationships each day as if every day was the last day of our lives. I believe in being unrea-sonable and unstoppable in every-thing I do. I believe that when we discuss we should do so without car-rying the burden of either accepting or rejecting whatever is being said. This creates the space for listening well. Eventually we all accept or reject what is being received by our senses; such actions enable us to learn from our actions. I believe that even if there was a time machine, we should not walk back in time to correct what we notice with the advantage of hindsight, doing so eliminates all the fun and excitement that the ups and downs of life offer.

What got me here was just good enough for getting me here and will not take me further, so I need to rediscover and reinvent myself to move up. I have recently joined this highly motivated animal called Religare. I am amazed at the constant turbulence and restlessness in the organisation to do something great, something different that the world will sit up and notice. I am currently in the process of setting up an IT organisation structure for our firm without carrying the baggage of my past experience. I feel the neural energy in me keeps me on my toes as I put a structure in place, organise governance, fuel the teams with quality research and intelligence. Excited, nervous, focused and diligent is what describes my mood these days. I follow Steve Jobs’ golden rule: “Stay hungry, stay foolish.”

The views expressed here are personal

and do not represent the company.

Stay hungry, stay foolishFollowing Steve Job’s golden rule, CIOs need to be excited, focused and diligent in their day-to-day work.

LETTERS

WRITE TO US: The CTOForum values your feedback. We want to know what you think about the magazine and how

to make it a better read for you. Our endeavour continues to be work in progress and your comments will go a long way in making it the preferred publication of the CIO Community.

Send your comments, compliments, complaints or questions about the magazine to [email protected]

6 21 JANUARY 2010 thectoforum.comCTOFORUM

CTOForum LinkedIn GroupJoin more than 200 CIOs on the CTO Forum LinkedIn

group for latest news and hot enterprise technology dis-

cussions. Share your thoughts, participate in discussions

and win prizes for the most valuable contribution. You can

join The CTOForum group at:

www.linkedin.com/groups?gid=2580450

Some of the hot discussions on the group are:What are the key competencies that a CIO

should seek to acquire to become a true global

business leader?

“Understand business, finance and expenses; never talk Technology but just plain language; implement transferable skills; do it if possible, otherwise explain and convince user; cultivate

the habit of questioning; always be proactive and not provocative; accept new ideas from anyone

and evaluate with your technical knowledge”—Viswanathan Sundararaman, Vice President

(Information Technology) at Clariant Chemicals (India) Limited

Which role will die - the CIO or the CTO?

"I would say both will co-exist. This is purely based on the organisational needs and business

model. Example: If the organisation is headed towards automation and prioritise internal

needs, that might give birth to the role of a CIO if it does not exist. If the organisation is headed towards external focus and product delivery, the

CTO role will be crucial."—Raj DN, Head of Database Operations, Sify

Technologies Ltd.

CTOF Connect Govind Rammurthy, MD and CEO, eScan says banks in India need to instill confidence amongst users when it comes to online banking. He talks to Ashwani Mishra on the areas of concern in the online banking space and other emerging security threats. Excerpts from the interview. To read the full story go to:

thectoforum.com/content/stop-ignoring-basic-norms

BEYOND THE BASICSA CIO has to make an impact and deliver significant value to business.“I believe that just speaking the right language or applying known formulae is not enough to get the CIO home. As a CIO, we have to get around to some basics.” To read the full story go to:

thectoforum.com/resources/opinions

OPINION

S.R. BALA, Exec VP ITGodfrey Philips.

“Change is always for the good. The great effort done by the CTOForum team can be seen in the new look magazine. The information covered in the magazine will help the IT pro-fessionals immensely. I congratulate and wish the team all the best.”SUSHANTA KUMAR LENKA

Mitsubishi Electric Automotive India Pvt. Ltd.

USEFUL COVER STORIESThe CTOForum keeps us updated about new technology and

business processes. The topics covered under the cover story

section with quotes from CIOs and business leaders are really

very useful.

UMESH KHANDELWAL

General Manager IT, BMW India

BETTER ORGANISEDThe revamped CTOForum not only looks better organised in

terms of information positioning but also gives a better look and

feel. Content-wise the magazine has remarkably improved over

the last few months.

B. S. DALAL

Joint General Manager IT, Airports Authority of India

COVE R S TORY X X X X X X X X X X

20 07 JANUARY 2010 thectoforum.comCTOFORUM

X X X X X X X X X X COVE R S TORY

21thectoforum.com 07 JANUARY 2010CTOFORUM

What began as a small collaboration effort within

Mahindra & Mahindra has now evolved into a full-

fledged LAUNCH PAD FOR INNOVATIONS

across the group.By Ashwani Mishra

20 07 JANUARY 2010 thectoforum.comCTOFORUM 21thectoforum.com 07 JANUARY 2010

CTOFORUM

CO L L A BO R AT I O N COVE R S TORY

“The Mahindra One portal offers ease of use to employees across the enterprise and helps in sharing ideas instantly”

—Vijay Mahajan

“Unified Communications has been embraced by all M&M employees and has become a part of the group’s business culture”—Aravind Tawde

COOOOOOOOOOOOOOCOC LLOLO LLLLLLLLLLLL AAAAAAAAAAAAAAAAAALALLALLALLALAAAAAALALLLALAAAAALLLLLLLLLLLALALALLLLLLALOOLOOLOLOOOLO LLLLLLLLCCOCOOOCOC LOLOOOOOCOCOOLOOOLOOOOCCOCCCOCOCOCOCOCCOC LCOOOOCOC LLOLOOLOLOOOC

PH

OT

O B

Y J

ITE

N G

AN

DH

I

BETTER ORGANISED

21

“Unified Communications has been embraced by all M&M employees and has become a part of the group’s business culture”—Aravind Tawde

AAAAAABBBBBBABAABAABAABAABAABAABAABAAABABAABAAAAABAABAABABBABABAABAABAAABAWhat began as a small collaboration effort in M&M has

now become a launch pad for innovations

across the group| PAGE 20

A 9.9 Media Publication

AT

TH

E H

EA

RT

OF

CO

LL

AB

OR

AT

ION

| AU

TO

MA

TIO

N IM

PE

RA

TIV

E | N

OT

IGN

OR

ING

TH

E B

AS

IC N

OR

MS

Volume 05 | Issue 10

January | 07 | 2010 | Rs.50Volume 05 | Issue 10

Collaboration

AT THECollaboration

AT THEHEARTCollaboration

AT THECollaboration

AT THEHEARTHEARTHEARTOF

A QUESTION OF ANSWERSNot ignoring basic security normsPAGE 12

Adopting automationimperativePAGE 16

BEST OF BREED

Beyond the BASICSPAGE 04

I BELIEVEI BELIEVEI BELIEVE

S P I N E

Technology for Growth and Governance

CT

O

FO

RU

M

8 21 JANUARY 2010 thectoforum.comCTOFORUM

Enterprise

ROUND-UP

STORY INISDE

Peter Streips of NS Group talks about the

top concerns CISOs will face in 2010. Pg 11

was the year on year growth of PC Ship-ment in APAC region in 2009.

Juniper Research’s Top Wireless Predictions. Says best is yet to come.MOBILE DATA traffic explosion to put strain on 3G networks: Though 3G is less than ten years old, 2010 could be the year when 3G networks begin to fall over under the burden of mobile data, due largely to some 33.8m iPhones.Mobile ecosystem starts to go green: 2010 will see a surge in the deployment of high-profile “green” hand-sets, featuring recycled plastic casings, energy saving modes and preloaded “ecotainment” apps which pro-mote sustainable lifestyles. Mobile heads for the cloud: The emergence of cloud-based platforms where thin clients reside on the handset and data is processed and stored primarily in the cloud will be bolstered by the open standards BONDI OneAPI

initiative and HTML5. New category of smart books to emerge: Juniper believes that smart books will create a new category of device, falling between smart phones and netbooks.Mobile social networking to integrate with other applica-tions including m-commerce: With mobile access to the likes of Facebook, MySpace and Twitter becoming com-monplace, adding commerce capability is the next step.Smart phones to get augmented reality AR makeover: Until Q2 2009, just a single AR app – Wikitude – was available for a single handset (the G1). However, with a raft of new Android handsets fitted with the key AR-enablers – cameras, Internet, GPS, accelerometers, digi-tal compasses these launches will accelerate dramatically.

23.6%DATA BRIEFING

E N T E R PR I S E RO U N D - U P

9thectoforum.com 21 JANUARY 2010CTO FORUM

Based on IDC's research on the APAC car-rier network equipment market, there will be 30 lakh base stations and over 18 lakh cell sites by 2012 — a growth of 24.3% and 10.7% respectively from 2008-09. Half of these sites will be connected to fibre through Carrier Ethernet. Urban 3G/HSPA base stations will be linked to fibre by 2011 in most markets.

QUICK BYTE ON WIRELESS BACKHAUL

New Tablets Make a Debut. The gizmos that will make it to the news in 2010 promise amazing features.HP, DELL and Motorola – all have announced competing tablet products (more so in competition to Google) during the recently concluded CES show in the US.

Microsoft CEO Steve Ballmer in his keynote address during the CES announced a tablet PC developed by HP, which will run Windows 7. This HP tablet will see the light of the day during December 2010. The device promises to have the portability of a mobile phone, but the power of a PC.

Dell also used the CES 2010 to showcase a tablet of its own. It runs on the Android OS. The company is sceptical of a launch date and thus skipped making a commitment. Motorola – not doing so well in the mobile handset space also released a prototype tablet PC, which could be ready to launch later this year. This is also an Android-based tablet which will primarily be promoted as a media player. The prototype has a 7-inch screen, and will have up to 32GB of external memory.

THEY SAID IT

CHRISTOPHER CAPOSSELA

Ever since Google started dominating the web, there has been a great tug-of-war between the two giants, Microsoft and Google. The two companies are trying to introduce innovative, user-friendly apps for the fans of Internet but they still get time to shout at each other. Here's one instance:

“We have a ton of competitors, in many cases versions of our old stuff. Google is a company that collects data to sell ads. That doesn’t translate into a strong enterprise player.”

—Christopher

Capossela, Senior VP,

Microsoft Collaborative

& Online Applications

quoted in Forbes.

E NT E R PR I S E RO U N D - U P

10 21 JANUARY 2010 thectoforum.comCTOFORUM

Need Has Never Been Greater for Entrepreneurial CIOs: Gartner. By 2012, Companies with the top 25% earnings growth will have an entrepreneurial CIO.THE IMPACT of an entrepreneurial CIO is greatest when the need for productivity leverage is greatest, as in the current eco-nomic environment, according to Gartner, Inc. Gartner analysts said by 2012, the com-panies with the top 25 percent of earnings growth will have an entrepreneurial CIO.

Gartner maintains that the distinctive fea-ture of the entrepreneurial CIO is the pro-active willingness and courage to take the

high-level risks also undertaken by the busi-ness, to provide new or breakaway competi-tive advantages that translate directly into revenue, financial results and market share. It is this willingness to apply the highest level of creativity available within the organi-sation to do things in a fundamentally dif-ferent way that establishes new sources of shareholder value, while also setting new levels for IT productivity. It comes with the

The Annual PWC Global Security Survey 2010 says the economic downturn has shaken up the normal roster of leading drivers of information security spending.

understanding that the business may fail in the attempt, but also that it will surely fail or, at best, attain mediocre performance, if it does not act.

“One of the biggest dilemmas facing organisations as we head toward 2010 is how CEOs and CIOs can execute entrepre-neurial tasks in the current risk-averse envi-ronment,” said Jorge Lopez, vice president and distinguished analyst at Gartner. “As shareholders see the recession recede in their day-to-day actions, they will drive for revenue and earnings growth, and they will expect CEOs and CIOs to perform to height-ened expectations.”

Lopez advised organisations to check that they have the right CIO for a return to growth. He said that the right combination of vision, risk-taking and persuasiveness is needed to fill the requirements for the job.

Gartner believes that the entrepreneurial CIO is the person who, working jointly with an entrepreneurial CEO or business unit executive, marshals the resources under the command of the IT organisation, as well as creatively links to resources outside of IT to define and capture new and growing busi-ness opportunities. The primary focus of the entrepreneurial CIO is on new-business impact, and that impact is felt in three major ways by the business:

Velocity of change — the ability to influ-ence the velocity of change through the structure of the business, so that a change in strategy can be implemented at a rate that outperforms all other competitors, and, therefore, also draws revenue at an earlier time and at a rapid pace. Improve-ments in this area lead to gaining com-petitive advantage quickly in new markets with new offerings.

Strategic leverage and extension — capabili-ties that extend strategy for the enterprise to new markets, new industries and new uses, and that lead to growth in revenue against entrenched and new competition. Operational efficiencies — efficiencies that improve operations to gain breakaway competitive advantage which further increases the rate of revenue and earnings growth. Gaining an improvement that is a factor of 10 or more is key to establishing true competitive advantage in the area of operational efficiencies.

—Source: www.gartner.com

GLOBAL TRACKER

SO

UR

CE

: P

WC

AN

NU

AL

SE

CU

RIT

Y S

UR

VE

Y 2

010

levels for IT productivity. It comes with the

SO

UR

CE

: P

WC

AN

NU

AL

SE

CU

RIT

Y S

UR

VE

Y 2

010

41% 39% 38% 37%32%

Com

pany

Rep

utat

ion

Reg

ulat

ory

Com

plia

nce

Inte

rnal

Pol

icy

Com

plia

nce

Econ

omic

Dow

ntur

n

BC

/DR

Percentage of respondents who identify the following business issues as the most important

drivers of IS spending in their organisation

E N T E R PR I S E RO U N D - U P

11thectoforum.com 21 JANUARY 2010CTO FORUM

Mainframe Computing. European CIOs call mainframe a safer bet than anything else.

SECURITY BITES

What would be the top concerns

for a CISO in 2010?

This is a very important conversa-

tion for any CISO.

I am personally dealing with VP's of

Tech, IT Managers, and CSOs alike.

My job is to thoroughly understand

customer's goals and concerns as

they plan IT spending for 2010. Out-

lined below are the top 5 threats/

concerns that are on my CSO's "I

can't sleep at night" list:

Remain out of the headlines:

CISOs are most worried about

the lost laptops, encryption,

hacking, etc.

Virtualisation - making their cur-

rent infrastructure work harder for

them while spending less .

Intellectual Property - making

sure their assets stay where they

belong and out of harm.

Regulations, regulations and

more regulations: In US, we have

to — until March 1st, comply

with the CMR 201 legislation,

which deals with protecting,

both, electronic and physical

data. We make sure they are not

just compliant today, but provide

them with thorough assessing,

auditing, and reporting tools for

future regulations.

Support - Are vendors or the

suppliers better equipped to help

when the duty calls? With average

annual maintenance fees ranging

20-30%, do they have the staff

trained well to keep these costs

down or should they seek outside

help to assist?

— As told by Peter Streips, Owner

Network Security Group, USA

THE WEAKNESSES i n d i s -

tributed computing environ-

ments are contributing to

resurgence in demand for

mainframes, which many

European CIOs believe are

more secure and scalable.

An independent survey of

European CIOs by CA found

that organisations using the

mainframe as a fully connect-

ed resource within the distrib-

uted, web-enabled enterprise

experience greater benefits

than those with a disconnect-

ed, comparatively isolated

mainframe environment.

Where the mainframe is a

fully connected resource, 65%

of all respondents report it to

be an ‘incredibly secure envi-

ronment’; 63% state perfor-

mance levels are ‘excellent’;

and 52% say that ‘the system

never goes down’.

The more the mainframe is

part of an enterprise-wide

strategy, the greater the role

it plays and the greater its

level of utilisation – the aver-

age amount of business-crit-

ical data administered by the

mainframe among all ‘con-

nected’ respondents is 64%.

Some 66% agreed that main-

frame user will soon start to

suffer from a shrinking work-

force if the relevant skills are

not available. However, 52%

agreed that a web-enabled

graphic user interface (GUI)

would make the mainframe

more attractive and help to

close the skills gap.

—www.siliconrepublic.com

SUN AND FUJITSU have announced an upgrade to their SPARC Enterprise M3000 Server, loading it with new hardware for faster performance. The single-socket server will be 23 percent faster than its predecessor, with a faster processor and updated memory modules, Sun and Fujitsu said in a joint statement. The server will be powered by a quad-core SPARC64 VII processor running at a clock speed of 2.75GHz.

The rack-mount server, which was introduced in 2008, previously

ran on a SPARC64 VII processor at a clock speed of 2.52GHz. The SPARC Enterprise M3000 is a single socket, entry-level server and is part of Fujitsu and Sun's comprehensive line of servers that includes the SPARC Enter-prise M4000, M5000, M8000 and M9000 servers.

This server runs enterprise applica-tions including database, customer relationship management and enter-prise resource planning software. For high uptime, the server includes reli-ability, availability and serviceability

(RAS) also found in midrange and high-end SPARC Enterprise servers, the companies said.

The server will enable consoli-dation of multiple servers into a compact 2U chassis, that will help companies save space and realize significant savings. The server runs the Solaris 10 OS, and Ora-cle's database software has been tested to work on the system.

Oracle said it welcomes the intro-duction of the enhanced SPARC Enterprise M3000 server, which is a powerful example of the extensive collaboration between Fujitsu and Sun. “We performed extensive testing of Oracle Database 11g Release2 on Enterprise M3000 servers running Solaris 10," said Andy Mendelsohn, Senior VP of Database Server Technologies, Oracle. "Customers can be assured that the SPARC Enterprise M3000 server runs Oracle Database 11gR2 with high performance and reliabil-ity at lower cost."

"Launched just over a year ago, the Sun SPARC Enterprise M3000 server with the Solaris Operating System has been a tremendous success with our customers," said John Fowler, executive vice president, Systems Group, Sun Microsystems.

—Source: www.sun.com

Sun Micro-Fujitsu Fire Up SPARC M3000. Promise better performance and ROI.

ronment’; 63% state perfor-

graphic user interface (GUI)

be an ‘incredibly secure envi-

agreed that a web-enabled

mance levels are ‘excellent’;

would make the mainframe

and 52% say that ‘the system

more attractive and help to

never goes down’.

not available. However, 52%

close the skills gap.

FACT TICKER

ILLUSTRATION: PHOTOS.COM

A Q U E S T I O N O F AN SWE RS T E H BA N S E N G

12 21 JANUARY 2010 thectoforum.comCTOFORUM

The enterprise storage business may be heavily skewed towards traditional HDDs as opposed to solid state drives, but Teh Ban Seng, VP & Manag-ing Director, APJ Seagate believes that the initial hic-cups have been cleared, and soon will be ready to go mainstream. In an interview with Sana Khan, Seng offers an insight into the highly vol-atile storage busi-ness. Excerpts:

T E H BA N S E N G A Q U E S T I O N O F AN SWE RS

13thectoforum.com 21 JANUARY 2010CTO FORUM

TEH BAN SENG | SEAGATE

DRIVE A HARDBARGAIN

What impact will Solid State Drives (SSD) have on the

enterprise storage market? Do you think there is a possibility of SSDs replacing the traditional drives?There is definitely value and space for SSDs in the enterprise market. The superior performance of the SSDs is most visible, and the faster read rate that it offers in comparison to the traditional hard disk drive (HDD) is another great differen-tiator that goes in favour of SSDs. SSDs also consume lesser power compared to the traditional drives. However, HDDs will continue to hold the bulk of the storage market in the near future, as there are still a few more issues to be resolved before SSDs go mainstream.

What are these issues? Flash memory will not really

replace traditional memory in the next three to five years. The main

reason for this is the cost of the SSD technology. Moreover, hard drives based on DRAM technology cost much less. Another major reason is the high investment required by enterprises. We are talking about pet-abytes of data. We also need to keep in mind that storage requirements are application-specific. Also, SSD applies to Tier-Zero, and it is effective for those apps. So, it’s almost impos-sible for the flash industry to replace the hard disk drives at this point of time. I personally feel that SSDs, rather than competing, will comple-ment HDDs; they will enhance stor-age architecture.

Isn’t it high time the flash industry considered a down-

ward revision in prices?Cost is bound to come down. There is no question about that. There have been several instances of price ero-sion in the industry. Historically, the

flash memory business has been a volatile one. While price fluctuation has been a norm in the short-term, the overall trend in pricing trend has been southbound. The question is how quickly the price will erode. Whether the prices will erode by 30 or 40 percent in the next 1-2 years is anybody’s guess. Two years ago, the price erosion in flash memory market was very steep, and there was a lot of hype around SSD taking over the traditional drive market. How-ever, in the last six months, the prices have bucked the trend.

There is significant uptake of SSD in the mobile devices

industry because of lower levels of heat, lesser power consumption and steady performance. Doesn’t putting SSD in laptops make a lot of sense?I would disagree with that. There has not been any significant adop-

A Q U E S T I O N O F AN SWE RS T E H BA N S E N G

14 21 JANUARY 2010 thectoforum.comCTOFORUM

tion of SSD technology in the notebook space. In fact, the trend is downward compared to what it was two years ago. Price points are not falling in line with industry expec-tations. Also, performance has been below par. There have been a lot of issues on the quality front. When people pay a higher price, they expect a better quality product. When you add all these factors together, it deters the adoption of the SSD in the industry.

It is often perceived that data recovery is difficult

from flash-based SSD devices. Is this a deterrent which is preventing the adoption of SSDs in mobile and enterprise applications?

every year, thereby making SSDs more competitive.

What are your expectations from the newly launched

Seagate Pulsar SSD?Pulsar is the first in the range of products that we plan to launch in the flash-based SSD space. We have 30 years of experience with the enter-prise customers and our advantage lies in our understanding of the cus-tomer. There are over 90 SSD manu-facturers worldwide today, but most of them are consumer-based compa-nies that have very little or no experi-ence in the enterprise space. In our case, we have collaborated with the enterprise customers to understand what they want and designed our next generation SSD products.

Frankly, we have not faced any such objection from our customers. SSDs largely criticised for its high cost. The offerings do not justify the cost. The biggest of all issues is quality. Earlier there were significant quality issues, but that again has signifi-cantly come down.

What are the initiatives in place to increase the capac-

ity of the SSD drive? This is a question more appropri-ate for the manufacturers of flash memory. They are the ones who own the technology. These semicon-ductor players are working hard to increase the capacity. Their aim is to increase capacity and lower the cost at the same time. Their plan was to increase the capacity by 30 percent

“SSDs consume less power compared to the traditional drives. However, HDDs will continue to hold the bulk of the storage market in the near future, as there are still a few issues to be resolved before SSDs go mainstream.”

That there is

value and space

for SSDs in

enterprises.

That SSDs will

complement and

not compete with

traditional hard

drives.

That with

increase in

quality, adoption

of SSDs will

grow.

THINGS I BELIEVE IN

15thectoforum.com 21 JANUARY 2010CTO FORUM

BEST OF

BREED A Change of Spirit. Three transformational forces that can change the face of IT in your company Pg 17

FEATURE INSIDE

In April 2002, I attended the Wireless Enterprise Symposium (WES) held in Atlanta, USA to check the potential of the BlackBerry as a portable email solution for our business. Those days if you wanted to

access your corporate email on road, the only real choice was to carry a laptop, modem with access to either a VPN link or an access to the web-based Exchange 2000. The introduction of BlackBerry devices and a BlackBerry Enterprise Server that accessed corporate email changed the course of business communication.

The WES 2002 event was primarily a showcase for the capabilities of Research in Motion (RIM), the company behind the BlackBerry brand. In his keynote speech Jim Balsillie, CEO of RIM, gave a fascinating insight into the fortunes and growth of the company. He also gave an indication on why the BlackBerry would soon be called "Crackberry" as he himself was addicted to checking his email all the time. In fact, a corporate IT geek sitting was toying with his BlackBerry instead of paying atten-tion to Balsillie’s address. Out of curiosity I asked him what he was doing. His response surprised me. He said, "I'm discussing the keynote with my colleague who is sitting at the back of the hall." At the time I thought this was somewhat strange and even discourteous to the keynote speaker who was actually delivering a great opening address to the WES event. Little did I know how much would the BlackBerry change our lives.

The next few days at the event were an eye-opener for me. I quickly called up my office and confirmed that the BlackBerry was a perfect alternative to the laptops. Looking back at some of the discussions in the BlackBerry development sessions, it's fascinating to see just how far mobile technology has come in the last ten years. In 2002,

The Advent of the AndroidsBlackBerry changed mobile technology; Apple’s iPhone and Google’s Android may well drive the next wave of change BY RICHARD GOUGH

16 21 JANUARY 2010 thectoforum.comCTOFORUM

B E S T O F BR E E D SM A R T PH O N E S

the BlackBerry developers did not feel the need for a colour screen. The concern then was that battery technology was incapable to support 24 hours portable email. Also, the idea of using the device to access browser-based Internet hadn’t surfaced.

However, companies like Filefish led the path by providing secure access to corporate files using BlackBerry Wireless Handhelds. "BlackBerry handhelds have become key extensions of the enterprise computing environment," said Edwin Ong, FileFish's Chief Strategy Officer, "We are excited to provide IT departments with the ability to rapidly provide secure file access to their BlackBerry users." So, BlackBerry became this trailblazer in business mobility revolu-tion. Armed with this new found knowl-edge, I headed back to my company and proposed the idea to my colleagues. Since then it has been an odyssey of sorts driven by this tiny piece of smart plastic not much larger than a paperback novel.

As we enter the next decade, portable tech-nology has become really flexible and acces-sible. An iPhone from Apple, launched in 2007, also revolutionised the mobile phone industry as much as BlackBerry changed things around the turn of new millennium. Written off by the mobile phone industry as an irreverent consumer product, Apple by the first quarter of 2009 sold 3.9million iPhones worldwide.

The popularity of the gadget among con-sumers and business alike has been driven by the compelling user experience delivered by the thoughtful touch screen interface

and a fine collection of iPhone applications available at the iTunes store. But this is a highly competitive market. While iPhone and BlackBerry gained greater market share in 2009, mobile phone major Nokia lost its market share from 45 percent in 2008 to 41 percent in 2009. It may be an indication of the times to come.

But where does Google fit in the scheme of things? Last month, it was widely reported that Google will roll out its own Smartphone. The success of Google Android smart phones in tow with HTC and Motorola has proved that it can take on

Apple and their iPhone range. If there is any doubt about the capabilities of a Google Smartphone, one needs to check the video demonstration of the Google Maps Naviga-tion system – an internet-connected GPS navigation system with voice guidance. It is available as a free service for phones with Android 2.0, but it is presently only available in the United States on the Veri-zon Droid phone.

What this service clearly demonstrates is the power of a portable Internet connected device backed by powerful cloud computing based services like Google search, maps and imaging. I already use the Google apps to call out my search needs instead of typing them. One really wonders: how long will it take before a Google powered Smartphone could read out a document from Google docs? How long will it take to dictate and record a Google document from our phone? One needs to take a look at the Dragon Dictation iPhone application from Nuance Communications to gather the experience.

Google has enterprise power and technology to drive such products, and in the next ten years, Google will become bigger than other major mobile phone companies with Apple coming a close second. Back at Atlanta in 2002, I realised what was in store for corporations. What I could not fathom was the effect of BlackBerry roll out on consumers. According to a recent Gartner report "Consumerisation Gains Momentum: The IT Civil War", customers are testing their individual purchasing power to obtain the best technology to support their virtual lifestyle.

The impact of 24/7 computing does pres-ent a challenge to IT professionals and the workforce who rely on it. It affects the fine line between personal and professional life due to the ubiquitous nature of email and access to work systems. But in a digital age, society adapts around new technology. RIM BlackBerry kicked off this revolution in the last decade; it is now up to iPhone and Android to take us forward to the next level of portable computing. And I, for one, am sure the next ten years are going to be even more exciting than the last ten!

—Richard Gough is a chartered IT Professional

and a BCS Fellow.

“Customers are testing their purchasing power to obtain the best tech-nology to support their virtual lifestyle” —Richard Gough

The Android or iPhone soft-

ware platform is more than

just a core operating system.

And really, the differences in

their core operating systems are

one of the least important fac-

tors to users. Both use a Unix-

derived kernel and operating

system environment that few

users will ever even see. Android

phones happen to use a Linux

kernel while the iPhone uses the

same Mach/BSD Unix kernel as

Apple's desktop Macs.

In the big picture, this doesn't

really matter much because nei-

ther smart phone platform pro-

vides any real access to this layer

(either to users or developers),

and neither phone platform is

designed to run desktop soft-

ware developed for Linux PCs or

Macs. Both systems are exam-

ples of well regarded technol-

ogy that is fully capable of sup-

porting the needs of the smart

phone environment above the

core OS.

The actual platform environ-

ment that matters to users on

Android and the iPhone exists

well above the core operating

system kernel. This is where

applications run, where security

is enforced, and where the busi-

ness model behind the smart

phone impacts what users can

and can't do. —Source www.

appleinsider.com

Android vs. iPhone: Under the Surface

17thectoforum.com 21 JANUARY 2010CTO FORUM

I T T R A N S F O R M AT I O N B E S T O F BR E E D

A Change of Spirit

Once in a while, I sit back and think about the real transformational

forces that will change how information technology (IT) operates. And recently I've come to a conclusion that there are three fundamental technological movements that will bring about the revolution.

1. Software virtualisationAbstracting software from the underlying CPU yields mobility, consolidation, and degrees of scalability. It also simplifies automated management and portability of workloads through virtual appliances or Amazon Virtual Machines (AMIs). Except for a few managerial kinks, this technology is already a de-facto system in IT transformation. 2. Infrastructure orchestrationAs I recently outlined, this technology is a perfect complement to software virtualisation; it essentially gives mobility to infrastructure. It allows IT operations to define I/O, storage connectivity and network-ing entirely in software, resulting in re-configurable CPUs. Egenera was a pioneer in this area, but the market now has a wider choice with the announcement of Cisco's Unified Computing solution. Unified computing or infrastructure orchestration is valuable because it enables a highly reliable, scalable and re-configurable infrastructure. It permits IT to ‘wire-once’ and then create CPU configurations (vir-tual Network Interface Cards, Host Bus Adapters, storage connec-tions etc.) using a unified or consolidated networking practise. Plus, it is a simple and efficient approach. Think of it as a provisioning hardware using software. We'll see this technology catching up. 3. Intelligent software provisioningWhile I'm not sure what this market segment may eventually be called, it represents the third critical datacentre management compo-nent. It gives software mobility and yields infrastructure flexibility.

FastScale is one company that is largely into intelligent software provisioning. Picture an intelli-gent software provisioning system that knows the minimum amount of software libraries needed to run an OS or application. As it turns out, the provisioning is usually something around 10 -15 percent of the multi-gig bag-of-bits you try to boot every time you bring up a server. And that even includes virtual machines (VMs).The result? Four really nice properties:a) Speed: Getting applications up and running faster. Not having to move as many bits over the network

to boot a given server is a real time and money saver. b) Efficient consolidation: With smaller software footprints, more VMs, appliances can fit on a given memory footprint. This means denser consolidation is frequently possible and not to mention dollar savings on those gigs of memory you have to buy when you consolidate.c) Inherent configuration management: With a database of all libraries and bits, you can always monitor configurations and verify compliance. Moreover, you can track what patches went where.d) Ability to provision into any form of container: In other words, this system can provision onto a bare-metal CPU or for that matter into an appliance like an Amazon Virtual Machine AMI if you're using a computing cloud.

This intelligent provisioning approach is also highly complemen-tary to existing compliance and configuration management products such as OpsWare (HP) or BladeLogic (BMC). SummarySo what if you have all three of these technologies? You'd have a data centre where workloads were portable and platform-independent; infrastructure was instantly re-configurable and adapted to business conditions; software could be distributed and broughtup in the order of seconds, thereby allowing adaptation to scale and business demand. Pretty sweet, eh? —Ken Oestreich is Technical VP of Product Marketing at Egenera, US.

Three transformational forces that can change the face of IT in your company BY KEN OESTREICH

18 21 JANUARY 2010 thectoforum.comCTOFORUM

COVE R S TORY E R P 2 . 0

WHAT’SBy Ashwani Mishra & Gyana Ranjan Swain

ERP 1.0 IS OVER

Like any other technology, enterprise resource planning (ERP) is being cannibalised by newer technologies. While the Software-as-a-Service (SaaS) model, cloud computing and ERP based on virtual systems are the future, the economic chaos and business uncertainty of the past two ye ars have made CIOs think again and re-examine the investments made into the systems. CIOs today are caught up with

questions they had ignored earlier: What's the cost of deploying and maintaining an ERP? Is there a measurable return on investment (RoI)? Are ERP systems delivering their expected impact?Any investment requires measurable

returns, but ERP grabs special attention because of the amount of money and organisational bandwidth it consumes.

THE ARRIVALOF ERP 2.0The original version of ERP makes way for the newer edition of the business software – one that fits all sizes.Turn to Page 20

S P ARYAVice-President IT, Amtek Group.

E R P 2 . 0 COVE R S TORY

19thectoforum.com 21 JANUARY 2010CTO FORUM

It may be too early to write off ERP, but the business software has started showing worrisome signs of fatigue

So if the changes in delivery models turn towards ERP 2.0, the concerns of the CIOs

and thus the changes in how vendors approach the sales of this mammoth

software also indicate a tilt towards the new era of how enterprises will com-

pute and work. Debates like whether there should

be a ‘single-instance’ ERP across the enterprise or it should be specific to

locations and geographies need a prom-inent mention; whether there should

be changes in licensing models or not; will the vendors stop defaulting on both post-implementation and maintenance

contracts are some of the questions which need a serious relook.

BREATHING LIFE INTO THE OLD

WARHORSEERP needs to embrace newer

technologies to retain its old gloryTurn to Page 23

SURYA BHARDWAJ Vice President,

India Applications, Oracle India

NEXT

20 21 JANUARY 2010 thectoforum.comCTOFORUM

COVE R S TORY E R P 2 . 0

Anxiety and fatigue mar an otherwise cheerful Sudhir Pal [SP] Arya, VP-IT of the Delhi-based Amtek Group. Amidst finalising an ERP for

his group, Arya feels challenged at many fronts. “I have been in and out of nerve-racking, inconclusive meetings with the stakeholders in the company. Despite the best brains at work, it is taking a lot of time to decide which way to go,” says Arya with a grim face. Unlike the popular instances of ERP deployment, Amtek is contemplating a radically different approach. The company may decide to go in for a third-party man-aged ERP with overall control in their hands so that they can focus on keeping IT aligned with the core business values.

This is the challenge facing many compa-nies today primarily due to the reduction in IT budgets and a conscious desire to extract maximum return on investment (RoI). Ground realities have significantly changed and in the last 12-18 months the ERP, in its original form, has taken a backseat.

Yet another case is that of the interna-tional airline British Airways (BA). The loss-making airline has cautiously delayed its global ERP rollout. The deployment was delayed despite BA completing the procure-ment for the new ERP and was just a week away from selecting the vendor in late 2008. This was projected as one of the biggest ERP deployments in the Europe.“When we looked at this (ERP) initiative, we

The original version of ERP will make way for the newer editions of the business software – one that fits all sizes. BY ASHWANI MISHRA

ERP 2.0THE ARRIVAL OF

realised that it would cost us a huge amount of money. There was absolutely no doubt in my mind that we had to postpone this deployment. It was a long-term investment that would not pay us back immediately,” says Paul Coby, CIO, British Airways.

ERP investments involve huge budgets. According to analyst reports, the total cost of an average SAP deployment can go as high as $ 16.8 million. Oracle charges $12.6 million. Microsoft is less costlier at $2.6 million. The second rung of ERP providers such as Baan and Infor charge around $3.5 million.

And if such spending guaranteed that businesses would increase their efficiency and reduce costs, at least the CIOs of large enterprises would have gone ahead with the deployments despite the recession. What-ever fresh ERP deployments happened in the last 18 months were in the small and medium enterprises.

REALITY CHECKOne positive outcome during the economic turmoil is that businesses of all sizes, across all industries and geographies took the time to conduct a meticulous re-examination of their ERP investment and strategies.

According to a Forrester report in November 2009, the frustration over maintenance fees and upgrade costs for ERP and emphasis on business intelli-gence (BI) and CRM applications notwith-

standing, an ERP suite is still considered the "backbone" of an enterprise. The soft-ware supports core functions of a com-pany such as operations, sales and distri-bution, besides sustaining administrative functions of finance and procurement.

But all this comes at a price which most of the times appear prohibitive for any user company. In any given board meeting, CIOs are asked to justify the cost of these huge investments and have to show the real ROI before implementing these applications.

“We examined our past IT investments in ERP in the last few years to explore our cost management options in the long run. The good news is that our ERP system sustained itself and the strategy stood reinforced,” says Arun Gupta, Group CIO, K Raheja Corp.

The industry at large has started revisiting their ERP spend after a recent study tolled the death knell of the enterprise software. According to US-based Panorama Consulting Group, 65 percent of ERP projects went over budget. 93 percent took longer than expected time. Implementation cost in most cases exceeded the original estimate by 50 percent.

“Any ERP implementation should be viewed as a strategic initiative and not an operational one. The foremost thing required for its success is a strong manage-ment buy-in,” says Hilal Khan, Head Corpo-rate Strategic Information Systems, Honda Motor India Pvt. Ltd.

Khan adds that ERP is not about deploy-ing a technology, but it is about managing people, conflict, expectation and change. “If one can manage all the four factors effec-tively, one can do wonders with the ERP and justify the investment,” he adds.

For many large enterprises that had implemented ERP a few years ago, the focus was to capture and manage end-to-end busi-ness transactions in an integrated manner. Today, the CIOs feel that it is important for them to stop focusing merely on transac-tions. They say it is high time they focused on how these transactions can be effectively used. Organisations need to start with the implementation of an ERP and gradually move towards data warehousing and BI.

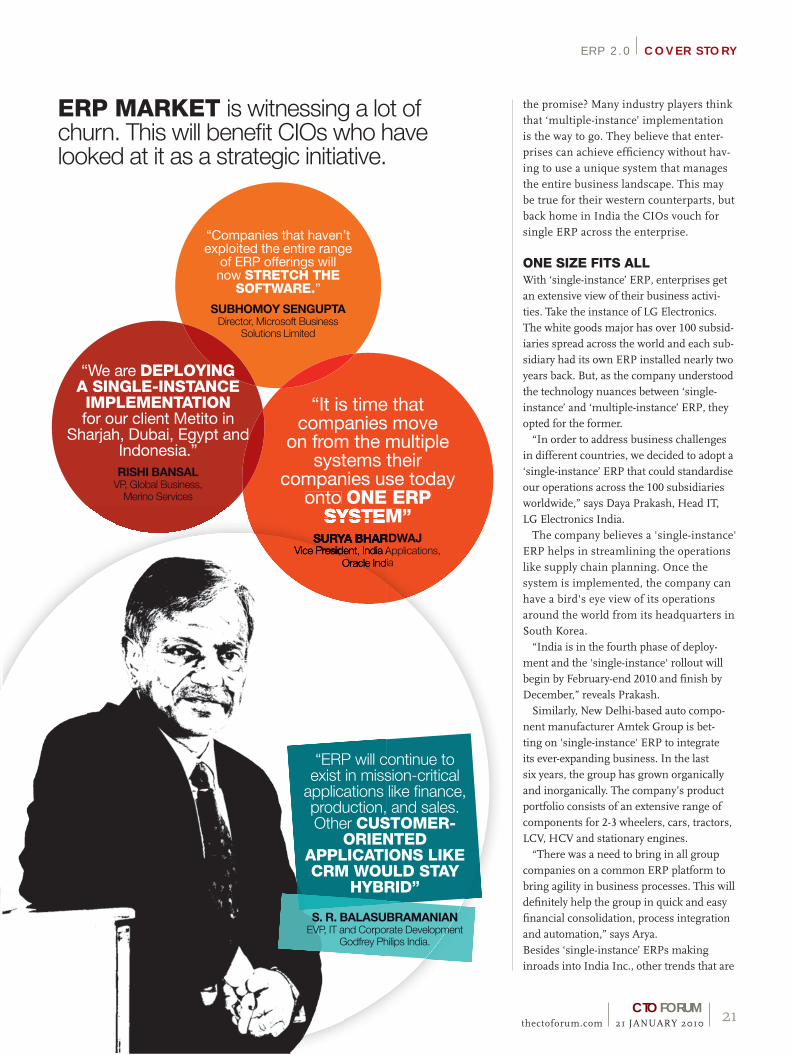

But in an IT environment where multiple systems have to be networked together, can a ‘single-instance’ ERP hold

21thectoforum.com 21 JANUARY 2010CTO FORUM

E R P 2 . 0 COVE R S TORY

the promise? Many industry players think that ‘multiple-instance’ implementation is the way to go. They believe that enter-prises can achieve efficiency without hav-ing to use a unique system that manages the entire business landscape. This may be true for their western counterparts, but back home in India the CIOs vouch for single ERP across the enterprise.

ONE SIZE FITS ALLWith ‘single-instance’ ERP, enterprises get an extensive view of their business activi-ties. Take the instance of LG Electronics. The white goods major has over 100 subsid-iaries spread across the world and each sub-sidiary had its own ERP installed nearly two years back. But, as the company understood the technology nuances between ‘single-instance’ and ‘multiple-instance’ ERP, they opted for the former.

“In order to address business challenges in different countries, we decided to adopt a ‘single-instance’ ERP that could standardise our operations across the 100 subsidiaries worldwide,” says Daya Prakash, Head IT, LG Electronics India.

The company believes a 'single-instance' ERP helps in streamlining the operations like supply chain planning. Once the system is implemented, the company can have a bird's eye view of its operations around the world from its headquarters in South Korea.

“India is in the fourth phase of deploy-ment and the 'single-instance' rollout will begin by February-end 2010 and finish by December,” reveals Prakash.

Similarly, New Delhi-based auto compo-nent manufacturer Amtek Group is bet-ting on 'single-instance' ERP to integrate its ever-expanding business. In the last six years, the group has grown organically and inorganically. The company’s product portfolio consists of an extensive range of components for 2-3 wheelers, cars, tractors, LCV, HCV and stationary engines.

“There was a need to bring in all group companies on a common ERP platform to bring agility in business processes. This will definitely help the group in quick and easy financial consolidation, process integration and automation,” says Arya.Besides ‘single-instance’ ERPs making inroads into India Inc., other trends that are

ERP MARKET is witnessing a lot of churn. This will benefit CIOs who have looked at it as a strategic initiative.

“Companies that haven’t exploited the entire range

of ERP offerings will now STRETCH THE

SOFTWARE.”

SUBHOMOY SENGUPTADirector, Microsoft Business

Solutions Limited

RISHI BANSALVP, Global Business,

Merino Services

“It is time that companies move

on from the multiple systems their

companies use today onto ONE ERP

SYSTEM”SURYA BHARDWAJ

Vice President, India Applications, Oracle India

SYSTEMSYSTEMSURYA BHARDWAJ

Vice President, India Applications, Vice President, India Applications, Oracle IndiaOracle India

“ERP will continue to exist in mission-critical

applications like finance, production, and sales. Other CUSTOMER-

ORIENTED APPLICATIONS LIKE CRM WOULD STAY

HYBRID”

S. R. BALASUBRAMANIANEVP, IT and Corporate Development

Godfrey Philips India.

“We are DEPLOYING A SINGLE-INSTANCE IMPLEMENTATION for our client Metito in

Sharjah, Dubai, Egypt and Indonesia.”

22 21 JANUARY 2010 thectoforum.comCTOFORUM

COVE R S TORY E R P 2 . 0

fast catching up are: advances in middle-ware offerings; tools that allow integration between databases and infrastructure; and Software-as-a-Service (SaaS) applications that can be deployed wherever necessary. The industry refers to it as a hybrid model.

CHANGE IN FORMThe primary reason for the buzz around the hybrid model is that most companies are upgrading their old ERP applications. CIOs are now evaluating if they need to stick to the older version of the enterprise software or move to the newer models such as SaaS or cloud computing.

enterprise support contracts at the 2009 level of 18.36 percent. The plan to gradu-ally increase that price will resume in 2011, bringing enterprise contracts to 22 percent by 2016 instead of 2015.

However, some CIOs offer a word of caution. “We may consider ourselves smart by negotiating terms of implemen-tation and price of licenses, but they (ERP vendors) will do everything possible to hook you in. Once you fall in the trap, there is no way out,” says the CIO of a leading manufacturing company.That is one of the reasons why Arya of Amtek says that he is open for new deliv-ery models like managed services and

mentation issues related to manpower and technology,” says Khan who is determined to look at the models as they mature. "I would surely look at them as possible add-ons to the company’s existing ERP," he says.

The current downturn has also changed the rules of the game. With IT spending going down, the opportunities of revenues for ERP providers have also shrunk. In fact, many traditional vendors are now providing SaaS as a value addition to their offerings and making up for lost revenues.

MORE BANG FOR THE BUCKCIOs are negotiating tooth and nail to get a fair deal. Many enterprises objected to soft-ware maintenance fees levied on traditional on-premise applications. In fact, a leading

“ERP will continue to exist in mission-critical applications like finance, produc-tion, and sales. Other customer-oriented applications like CRM would stay hybrid,” says S R Balasubranian, Executive Vice President, IT and Corporate Development, Godfrey Phillips India.

For CIOs, it is the high licensing fees along with support and maintenance costs that make them look for greener pastures in the hybrid model. The SaaS model offers numerous cost benefits, including no up-front costs, no licensing fees and rapid deployment.“SaaS or cloud computing model has the potential, but providers need to clear imple-

ERP giant gave in to customer demands to call off their hike in enterprise support fee.

Business software leader SAP recently stepped back from its plan to move its customers to enterprise support contracts priced at 22 percent (of the sale price of the licenses) per year.

Instead, it will adopt a two-tiered system that reintroduces a standard support option set at 18 percent and a slightly higher price to the customers who want advance sup-port. SAP also froze prices for existing

SaaS with an assurance that the model will safeguard the company's investment in ERP.

There is no doubt that the ERP market is witnessing considerable amount of churn. This will certainly benefit CIOs who have looked at it as a long-term strategic initia-tive. With the economy showing signs of recovery, CIOs are hoping that their ERP strategies can pack the much needed punch in the future, and yes, without any ques-tions asked.

“ERP is not about deploying a technology, but it is about managing PEOPLE, CONFLICT, EXPECTATION AND

CHANGE”

“In order to address business challenges in different countries,

LG decided to adopt a ‘SINGLE-INSTANCE’

ERP TO STANDARDISE OPERATIONS”

“When we looked at ERP, we realised that it would cost

us a huge amount. We had to postpone this deployment as THERE WAS NO IMMEDIATE ROI”

HILAL KHANHead Corporate Strategic

Information Systems, Honda Motor India. DAYA PRAKASH

Head IT, LG India Electronics.

PAUL COBYChief Information Officer, British

Airways, India.

“ERP is not about

Airways, India.

23thectoforum.com 21 JANUARY 2010CTO FORUM

E R P 2 . 0 COVE R S TORY

When research firm Gartner introduced Enterprise Resource Planning (ERP) way back in 1990, little did

anyone know that one day it will become so ubiquitous that businesses cannot do without it. Created as an extension to Materials Requirements Planning (MRP), ERP has come a long way in the last two decades.

Though ERP applications have gained prominence across enterprises, web-enabled and open source technologies have emerged as serious challengers. Industry players say the future of ERP really lies in coalition. Gone are the days when a single technology could monopolise over the market.

End-to-end integration no longer means only integration of logistics, financial and HR processes. ERPs have come up with products in the areas of customer relationship management (CRM), supplier relationship management (SRM), product lifecycle management (PLM), manufacturing optimisation, environmental health and safety, etc. and

the trend points towards industry micro vertical specialisation. Also, it has been witnessed in the past that with the advent of service-oriented architecture (SOA), increased flexibility of interfacing has made choices more open for customers. The increased penetration of business applications in the mid-market has also helped compress the time taken for ERP implementation. And this helped mid-size customers whio cannot afford to tie up their resources in protracted implementation.

WHAT’S NEXT?The evolution of new technology is reshaping the product offerings in ERP and enriching user experience, increasing flexibility, and providing better insight. Software-as-a-Service (SaaS) is starting to gain traction as a viable deployment option in some ERP markets including India. Riding on the success

of the best-of-breed CRM and human capital management (HCM) applications, ERP application providers are creating an environment where ERP is becoming a must-have for even mid-size businesses.

Keeping the drawbacks in the earlier versions of ERP in mind, it is fair to say that model-based, configurable applications based on SOA will be the next big change for ERP applications. The key here is the shift of focus from the enterprise applications to the end-to-end

business process, and that is what will drive the market in the future.

The new business processes will be mapped against today’s ERP functionality, but will be more than just transactions – they will have rich analytics and will be supported by structured and unstructured data. Also customers will be able to exploit the applications to their maximum extent. “Companies that haven’t

The age-old mammoth application needs to embrace newer technologies to retain its old glory. BY GYANA RANJAN SWAIN

OLDWARHORSE

BREATHINGLIFE INTO THE

30%of new enterprise application license purchases (in APAC excluding Japan) will be in form of SaaS, or delivered through

the SaaS model

24 21 JANUARY 2010 thectoforum.comCTOFORUM

COVE R S TORY E R P 2 . 0

exploited the entire range of ERP offerings will now stretch the software,” says Subhomoy Sengupta, Group Director, Microsoft Business Solutions, Microsoft India.By end of 2010, experts say, buyers will be a lot savvier about SOAs, native web services, Web 2.0 technologies, business process platform and other application infrastructure products. Major application vendors are eyeing these technologies and will position their solutions as a non-disruptive technology for continued business. SOA is an area where most ERP product vendors have been investing. That is the future. The key objective of SOA is to provide the customer with logical extensions to ERP systems. Players like Infor have also been investing a lot on deploying SOA in its various business solutions.

THE SAAS SAGADelivering ERP on a SaaS model is a revolutionary approach in enterprise software and offers enterprises of all sizes a viable, scalable and flexible model. This is destined to provide lucrative benefits to the users of enterprise applications.

Gartner predicts that by 2010 nearly 30 percent of new license purchases (in APAC excluding Japan) will be in the form of SaaS, or will be delivered using the SaaS model. In a recent survey comprising 1,017 technology decision makers, Forrester found that the worldwide adoption of SaaS in large enterprises is now at 16 percent, up 33 percent from the previous year.

While SMEs have a viable option of monthly subscription in the SaaS model, large enterprises do not have many of such flexible alternatives. But there are players who have started plugging the gaps. Microsoft, for instance, has a different view on ERP being deployed under the SaaS platform. “The definition of SaaS has changed from Software-as-a-Service to Software-and-a-Service,” says Sengupta while adding that best end-user experience is delivered through a combination of hosted and on-premise software on a multitude of devices.

Reports from various research agencies suggest the worldwide SaaS revenue is expected to reach US$14.8 billion in 2012 and India will contribute the majority of it. The commercial advantage that SaaS

THOUGH ERP applications have gained prominence, Industry players say the future of ERP really lies in coalition

“We examined our past investments in the ERP. The

good news is that the SYSTEM SUSTAINED ITSELF AND THE STRATEGY STOOD

REINFORCED”

ARUN GUPTAGroup CIO, K Raheja

Corporation.“We will go in for a BUSINESS-CENTRIC

APPLICATION DELIVERY MODEL where we limit ourselves to focus on business objectives”

S P ARYAVice-President IT, Amtek Group.

By end of 2010,experts say, BUYERS

WILL BE A LOT SAVVIER ABOUT SOAs, NATIVE WEB SERVICES, WEB 2.0 TECHNOLOGIES,

business process platform and other application

infrastructureproducts

business process platform business process platform and other application and other application

infrastructureinfrastructureproductsproducts

“As long as there are provisions in ERP for consolidation across

different business units, 'SINGLE-INSTANCE' ADOPTION WILL BE

A REALITY”

S SUNDERARAJSenior Vice President, Indian

Operations & Business Consulting Group, Ramco

Systems

25thectoforum.com 21 JANUARY 2010CTO FORUM

E R P 2 . 0 COVE R S TORY

offers is that neither do the companies have to make upfront investments in technology nor do they have to devote time and resources on software deployment and maintenance. Although the utility of SaaS is expanding, its growth is driven by horizontal applications across a distributed virtual workforce using the latest web-enabled technologies. Moreover, SaaS can be delivered through a hybrid model. Some core functions of ERP will be on premises and non-core operations can go in the cloud depending on the maturity of a company's IT systems.

THE WEB OF CONVENIENCE Web-enabled technology gives customers an option to extend their access to multiple locations without getting worried about vendor's installation and desktop level management. Further, it offers options to build home pages, portal environments and more content rich pages to give the user consolidated information on one screen.

ERP major Infor offers MyDay a pre-defined web portal with separate home pages for various users like sales manager, account payable user, account receivable user etc. Being SOA enabled, they can be deployed on multiple Infor solutions and it helps individual users to visit their own home page and do the required work.

With the Internet changing the rules of communication, business collaboration has brought a fundamental shift in how companies define their processes.

Companies no longer look at their business with unifocal attention; trading partners and customers are very much part of the game now. As a result, they need systems that support e-business transactions, which is what web-enabled ERP fundamentally helps them with.

Web-enabled ERP solutions have moved the organisational focus from administration to self-service, self-indulgence to a collaborative approach, transactional to business intelligence. The solutions have now brought concepts such as e-commerce, web-based procurement, BI and CRM under their wings.

The focus is now on quick and simple reconfiguration of business processes, intuitive interfaces that require no training, real-time or near real-time data access,

interactive and collaborative features such as real-time chat and white boarding, real-time analysis, and open access to both internal and external users. What is also important is the ability to dynamically re-configure and re-allocate assets on the fly based on current needs.

SINGLE INSTANCE - ORDER OF THE DAYAs enterprises get acquainted with the ERP appilications, demand for 'single instance' ERP has grown. Of late, enterprises have started preferring 'single-instance' implementation over multiple-instance rollout.

“It is time that companies move on from the multiple systems they use today to a single ERP system,” says Surya Bhardwaj, Vice President, India Applications, Oracle India.

ERP is an amalgamation of three very important components; Business Management Practices, Information Technology and Specific Business Objectives. ERP consolidation offers a single data store that serves the entire company, irrespective of its size and depth of offerings.

“Having a common, global and standardised platform not only reduces the complexity of multiple systems, but also gives the required flexibility to expand into new markets,” he adds.

Rishi Bansal, the VP, Global Business of Merino Services, a global partner of ERP vendor Infor echoes similar views. “We are deploying a 'single-instance' implementation for our client Metito in Sharjah, Dubai, Egypt and Indonesia,” he says.

Though single-instance implementation is being accepted by the organisations gradually, the adoption largely depends on maturity of the organisations.

“As long as there are provisions in ERP for consolidation across different business units, 'single-instance' adoption will be a reality,” concludes S Sunderaraj, Senior Vice President, Indian Operations & Business Consulting Group, Ramco Systems.

Wireless technology has helped enterprises in

many ways. Firstly it has facil-itated the stakeholders in get-ting up-to-date information on enterprise operations as and when required through the use of modern commu-nication devices like smart phones and laptops.

Wireless ERP gives best results only if it falls in line with proper communication channels. The communica-tion channels should be improved in the organisation to make it ready for wireless ERP. The obsolete computers should be replaced with the latest smart phones. Mobile

and telecommunication facilities should also be at par with the best standards in the industry.

There are times that com-panies resort to wireless ERP without improving the communication facilities. This does not serve any purpose regardless of how much money is spent in ERP implementation. More-over, there is another major advantage in improving communication facilities. Apart from dissemination of information and improving productivity it also helps the companies to improve professional standards in

the market. This will also motivate the companies to improve other facilities that directly or indirectly contrib-ute to the working of ERP and make use of facilities like image Enabled ERP sys-tem and ERP data capture.

Wireless ERP has a huge market potential which is evident from the fact that big players like SAP and PeopleSoft have penetrated the segment. However, major concerns like privacy issues, message persistency, mul-tiple device compatibility and connection speed have to be taken care of before wireless ERP bears fruit.

WIRELESSERP

26 21 JANUARY 2010 thectoforum.comCTOFORUM

NEXTHORIZONS

In times of uncertainty, game theory should come to the forefront as a strategic tool, for it offers perspec-tives on how players might act under various circumstances, as

well as other kinds of valuable information for making decisions. Yet many managers are wary of game theory, suspecting that it’s more theoretical than practical. When they do employ this discipline, it’s often misused to provide a single, overly precise answer to complex problems.

Our work on European passenger rail deregulation and other business issues shows that game theory can provide timely guidance to managers as they tackle difficult and, sometimes, unprecedented situations. The key is to use the discipline to develop a range of outcomes based on decisions by rea-sonable actors and to present the advantages and disadvantages of each option. Our model shifts game theory from a tool that generates a specific answer to a technique for giving informed support to managerial decisions.

Several factors in today’s economic envi-ronment should propel game theory to a prominent place in corporate strategy. The global downturn and uncertain recovery, of course, have prompted radical shifts in demand, industrial capacity, and market prices. Some companies, emboldened by the crisis, have tried to steal market share. New global competitors from emerging economies, particularly China and India, are disturbing the established industrial order.

Making Game Theory Work for ManagersA new model generates answers representing the best compromise between risks and opportunities in all likely futures. BY HAGEN LINDSTÄDT AND JÜRGEN MÜLLER

Sense and Simplicity Where simplicity and technology intersect. Pg 30

Customer is Always Right 7-steps to better customer experience in 2010 Pg 31

FEATURES INSIDE

ILLU

ST

RA

TIO

N:

SA

NT

OS

H K

US

HW

AH

A

GA M E T H E O RY N E X T H OR I ZO N S

27thectoforum.com 21 JANUARY 2010CTO FORUM

They use new technologies and business models and even have novel corporate objec-tives, often with longer-term horizons for achieving success. These uncertainties can paralyze corporate decision making or, per-haps worse, compel managers to base their actions on gut feelings and little else. Game theory can revitalize and contribute clear information to decision making but only if its users choose a set of inputs detailed enough to make the exercise practical and analyze a range of probable scenarios.

Decades old and misunderstoodGame theory as a management tool has been around for more than 50 years. Today, most university business students are intro-duced to the idea through the classic “pris-oner’s dilemma.” This and similar exercises have instilled the idea that game theory generates a single solution representing the best outcome for reasonable players.

In academic settings, game theory focuses on logically deriving predictions of behav-iour that are rational for all players and seem likely to occur. It does so by seeking some form of equilibrium, or balance, based on a specific set of assumptions: the prison-ers aren’t aware of each other’s actions, can give only one answer, and so on.