ernst & young's 2012 attractiveness survey€¦ · · 2015-07-23representative panel of...

TRANSCRIPT

Growing Beyond

Staying ahead of the gameErnst & Young's 2012 attractiveness survey

UK

Ernst & Young’s 2012 UK attractiveness survey is based on an original two step methodology that reflects first, the UK’s real attractiveness for foreign direct investors, based on Ernst & Young’s European Investment Monitor (EIM) and second, the “perceived” attractiveness of the UK for a representative panel of 500 international decision-makers.

For further information, please visit: http://www.ey.com/attractiveness

1Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

Staying ahead of the game Ernst & Young's 2012 attractiveness survey

United Kingdom

Contents

Executive summary 4

UK's challenge to staying ahead 6

The regional picture — FDI across UK regions 16

The perception of UK in 2012 20

Conclusion 32

Appendices 33

Growing your business cross border 33

Methodology 34

British Design 36

6

16

20

2 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

Foreword

3Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

Lord Green Minister of State for Trade and Investment UK Trade & Investment

I am delighted that Ernst & Young has found that, once again, the UK remains the lead destination in Europe for foreign direct investment (FDI) in 2011. With world markets affected by ongoing economic uncertainty, the sustained impact of FDI on the UK has been transformational, helping to create a globally attractive and truly international economy.

While the UK continues to attract the greatest number of investment projects in Europe, there is no room for complacency. We recognise that our market share of overall European FDI has declined. Certainly, competition within Europe and high-growth markets elsewhere in the world has never been more intense and there is always more we can do to strengthen and enhance the UK offer to overseas enterprises.

Continual improvement of the UK’s regulatory and business environment is critical, as is an ongoing commitment to make all areas of the UK attractive investment destinations, which is why, along with Ministerial colleagues, we are listening to investors’ and exporters’ views and we are acting on what we hear.

The survey results on international investors’ perceptions of the UK provide valuable pointers, by highlighting specific areas where the Government might most usefully focus its efforts. In particular, these include driving innovation, education and skills; providing more support for small and medium enterprises; and attracting foreign investors with policies, legislation and incentives.

Some of these changes are already taking place, through the many positive steps the Government is making to attract foreign investors. In this year’s Budget, for example, the Government underlined its commitment to delivering greater certainty in the UK’s tax regime, and cut the 50p top rate of income tax to 45p. Corporation tax will be further reduced to 22 per cent by 2014, which will be supported by the introduction of a new patent box in 2013 with a reduced corporate tax rate of 10 per cent.

Policy changes such as these will foster the UK’s competitiveness - and there are many promising signs in this area. The UK’s balance of trade is benefiting from increasingly strong exports of cars to China, Russia and the US, helping the UK to reach a position where car exports exceed imports. And earlier this year saw a series of very positive announcements, with Vauxhall confirming that its new Astra will be manufactured at Ellesmere Port and Tata would be further investing in Jaguar Land Rover.

One of the most exciting opportunities on the horizon is of course, the London 2012 Olympic and Paralympic Games, and we intend to make the most of this once in a lifetime opportunity to showcase the best of Britain both during the Games and afterwards through the legacy. To do this, we as a nation must continue to invest and support our key industries and areas of competitive advantage that drive our export growth and attract inward investment. Through these efforts, we can ensure that the UK maintains its lead as the European investment destination of choice for many years to come.

Foreword

4 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

Executive summary

Key highlights

• The UK maintained its lead in attracting European FDI in 2011. But this position is under threat, with Germany’s share of FDI rising for the fifth year in a row to reach 15%, just 2% behind the UK.

• Germany also secured a higher share of manufacturing investment projects than the UK for the first time, and attracted twice as many FDI projects as the UK from China.

• The US remains the largest investor into the UK in 2011, followed by Germany, India, France and China. Germany has a much more balanced portfolio of investments across both developed and emerging markets.

• FDI trends reflect general economic variations: investors into the UK see the level of demand within the UK as a critical criterion for decisions, while Germany’s success with Chinese FDI in part reflects wider trade patterns between the two countries.

• Business services, software, and machinery and equipment are the biggest sectors driving investment into the UK, while financial services is slowing down.

• The top three attributes that make the UK attractive to overseas investors are: quality of life, culture and language; the stable political environment; and technology and infrastructure.

• Most foreign investors expect the UK’s attractiveness as a location for FDI to improve further over the next three years.

• Financial services, energy and utilities and manufacturing were identified by investors as growth sectors for the UK going forward.

• To remain a major destination for investment, overseas companies say the UK should play to its strengths in research and development (R&D), innovation and financial services.

• A more strategic approach to FDI that places inward investment within the overall economic context is required if the UK is to retain its lead in an increasingly competitive global market for FDI.

Executive summaryIn 2011, the UK narrowly retained its long-held position as Europe’s leading destination for foreign direct investment (FDI) projects, despite suffering a 7% decline in projects while the total number of projects in Europe grew by 4%. For the sixth year in a row Germany increased its share of European FDI projects. As a result, Germany’s share rose to 15%, putting it in second place only 2% behind the UK. If current trends continue, Germany will overtake the UK as Europe’s leading FDI destination within the next two or three years.

When we dig into the drivers of the UK’s relative performance, it is clear that the UK is successful in – but heavily dependent on – attracting projects from the US, and is also traditionally strong in sectors such as financial services, a sector for which FDI is currently in decline. In contrast, Germany has projects from a broader spread of countries and sectors, being the leading destination for France, Switzerland, Sweden the Netherlands and Italy.

Germany is also stronger in attracting investments from the BRIC countries (Brazil, Russia, India and China), winning twice as many projects as the UK from China in 2011. Germany’s powerful performance in 2011 saw it overtake the UK in projects from Japan, and secure a higher share of manufacturing projects than the UK for the first time since records began in 1997.

In terms of the industries in which the UK is winning FDI, the leading sectors in 2011 were business services, software, and machinery and equipment – with financial services FDI slowing down, albeit not as quickly as in the rest of Europe. While the UK’s share of financial services FDI projects is holding firm, the general decline in investments in this sector is a worrying development for the UK. On a more positive note, the UK maintained and actually increased its lead in job creation from FDI in 2011, with Scotland performing especially strongly. Here too there are concerns, however, as the UK is less well positioned in the automotive, machinery and transport sectors, which are the major sources of new jobs in Europe from FDI.

In addition to the statistics on FDI, this report examines the changes in investor perceptions that drive FDI location decisions. The 500 decision-makers we interviewed in overseas-based companies said the most attractive aspects of the UK from an FDI perspective are its quality of life, culture and language; stable political environment; and technology and infrastructure. Most respondents expected the UK’s attractiveness as a location for FDI to improve further over the next three years, and some 86% were “definitely” or “fairly” confident that the UK would be able to overcome its current economic challenges. This latter point is vital, as — according to the survey responses — the level of demand within the UK is the most important driver of FDI decisions, and the ability to use the UK as an export base is the second most important.

5Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

Mark GregoryPartner Chief Economist Ernst & Young UK

Francis SmallPartner UKI Markets Leader International Clients Ernst & Young UK

These findings suggest FDI will reinforce the UK’s economic growth, but will not drive it. The economy has to be performing well at home and abroad for the UK to remain attractive to investors. There were some interesting contrasts with the responses on Germany’s attractiveness. While the UK’s main attractions were seen as its quality of life and political stability, Germany’s key strengths were its transport infrastructure and logistics, and its telecommunications infrastructure. These differences may indicate the source of Germany’s competitive advantage with certain countries and sectors.

Very few respondents (12%) used UK Trade & Investment (UKTI) to support their FDI activities. We have no comparative data with other countries, but this appears to be a key area for further research to assess whether more can be done to attract and support potential investors.

In our view…

The UK’s continued position at the top of the European FDI rankings both for projects and employment is good news, and underlines the country’s resilience and sustained attractiveness to companies from all over the world. However, we believe that the decline in both the UK’s number of projects and its relative market share ring alarm-bells that should not be ignored.

The UK’s long-standing leadership in European FDI is a direct result of two key factors: its position as the investment location of choice for US companies, and its strength in several key sectors, including the seemingly-declining financial services industry. The UK performs less well in winning projects from the stronger European economies, and is now lagging behind Germany in winning projects from both China and Japan.

Given these circumstances, the UK must adopt a more strategic approach to FDI that places inward investment within the overall economic context. Both the survey responses and the FDI data make it clear that strong domestic demand, good export links and investment in human and physical capital are key drivers of success in attracting FDI. The FDI portfolio in terms of sectors and geographies requires careful attention, and the UK needs to keep existing FDI sources and investors happy while also seeking out new markets and opportunities. Otherwise the UK risks losing its prized leadership in European FDI.

Picking winners may not be seen as the job of government. However, if the UK is performing well in a sector in terms of exports, or if it is not yet performing well but an opportunity has been clearly identified, then attracting FDI to support the

development of capability to boost the UK’s offer would seem to be a sensible and effective way of using the UK’s resources. For example, the UK’s recent success in the automotive sector might create the opportunity to attract more investment and talent, and boost the overall competitive position of the sector in the UK.

Overseas investors provided some valuable pointers as to how the UK might achieve this. They stated that the UK should play to its strengths in financial services, research and development (R&D) and innovation to remain a major destination for FDI. And to remain attractive against global competition, they thought the UK should concentrate its efforts equally on three goals: supporting small and medium-sized enterprises (SMEs), supporting high-tech industries and innovation, and developing education and skills.

Our wider research shows that these same three priorities were highlighted by investors across Europe as a whole, but with “supporting high-tech industries and innovation” ranked first by a substantial margin. This suggests the UK is already performing relatively well in this area compared to other European countries. The wealth of talent in the UK is clearly evident. British Design 1948 — 2012: Innovation of the Modern Age, an exhibition Ernst & Young is supporting at the Victoria & Albert Museum this year, displays the history of British design and the progressive nature of Britain’s strengths in exporting innovation.

In our view, the route to improve growth for the UK lies in both encouraging businesses to export more, and also in continuing to attract FDI in an increasingly competitive global marketplace. To set out and realize this vision for the UK economy of the future, there must be several elements in place. These include an effective policy framework to support UK businesses going overseas, whether to export or establish operations in new markets; increased support for SMEs, to help them access the assistance and funding they need; and more visible Government support for foreign investors, such as efforts to raise the profile of the organizations set up to help them invest here.

A further key focus area should be employment. Job creation is central to reinvigorating the UK’s future economic growth, as the Government seeks to rebalance the economy towards high-value manufacturing and exports. With this goal in mind, the FDI figures for 2011 point to a twin-track approach for the UK: first, targeting high-FDI, high-employment sectors with promotional campaigns and investment incentives; and second, actively seeking out opportunities in new and emerging markets. Success on both counts will help to sustain the UK’s lead in European FDI into the future.

6

UK's challenge to staying ahead

7Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

UK retains lead in European FDI projects — but market share declines

In 2011, the UK retained its long-standing position at the top of the European FDI rankings, despite suffering a 7% decline in the number of inward investment projects, from 728 in 2010 to 679 in 2011. The UK’s sustained lead has seen it chosen as the location for approximately one in five of all investment announcements across Europe since 2004. This report looks at the UK's FDI performance in 2011, and then at Ernst & Young's research into foreign investors' perceptions of the UK.

Graph 1

Total annual FDI projects in the UK over the past ten years

Proj

ects

0

100

200

300

400

500

600

700

800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: Ernst & Young's European Investment Monitor 2012.

This decline in UK FDI projects in 2011 took place against the background of a 4% increase in total projects across Europe, which rose to 3,906, the highest number recorded to date. Indeed, ever-increasing FDI appears to be an ongoing corporate trend, with project numbers in Europe only falling once in the past decade, during the economic shock of 2009. However, while overall FDI in Europe continues to increase year on year, the growth in investment into the UK appears to have stalled somewhat, with no significant growth in UK project numbers since 2006 . The level of FDI projects secured in 2011 represented the UK’s joint lowest performance in the past six years, level with 2009.

Germany has almost closed the gap

On a European level, the UK, Germany, France and Spain remained Europe’s four largest recipients of FDI projects in 2011, with the UK staying in first position as the most popular destination — a lead it has held throughout the past decade. However, the combination of the rise in overall European FDI projects and the decline in the UK number saw the UK’s share of total Europe projects fall from 19% in 2010 to 17% in 2011.

In contrast, projects in Germany rose by 7%, taking its share of the total number of European FDI projects to 15%. This was only 2% behind the UK, and saw Germany take second place from France, whose number of projects also declined. Germany’s strong performance in 2011 was further underlined by the fact that it secured a higher share of manufacturing investment projects than the UK for the first time. Like Germany, fourth-placed Spain saw a rise in overall FDI projects in 2011, taking its European share to 7%.

Graph 2

European FDI market share of the top four recipients

0

5

10

15

20

25

2011201020092008200720062005200420032002

Perc

enta

ge o

f pro

ject

s

United Kingdom GermanyFrance Spain

Source: Ernst & Young's European Investment Monitor 2012.

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011UK 369 453 563 559 685 713 686 678 728 679France 254 313 490 538 565 541 522 529 562 540Germany 153 110 163 182 286 305 390 418 560 597Spain 122 119 121 147 212 256 211 173 169 273Grand total for Europe 1901 1933 2910 3065 3531 3712 3720 3303 3757 3906

Source: Ernst & Young's European Investment Monitor 2012.

Figure 1

Total annual FDI projects secured by Europe's four largest recipients over the past ten years

UK's challenge to staying ahead

8 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

UK's challenge to staying ahead

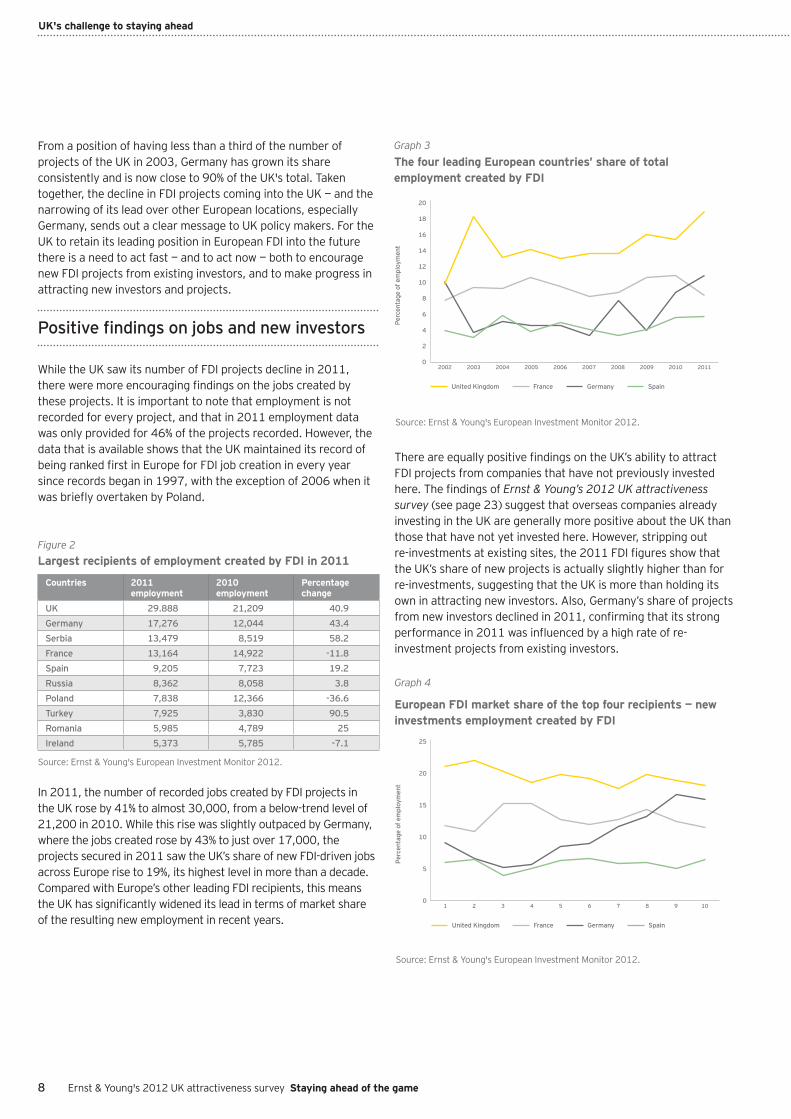

From a position of having less than a third of the number of projects of the UK in 2003, Germany has grown its share consistently and is now close to 90% of the UK's total. Taken together, the decline in FDI projects coming into the UK — and the narrowing of its lead over other European locations, especially Germany, sends out a clear message to UK policy makers. For the UK to retain its leading position in European FDI into the future there is a need to act fast — and to act now — both to encourage new FDI projects from existing investors, and to make progress in attracting new investors and projects.

Positive findings on jobs and new investors

While the UK saw its number of FDI projects decline in 2011, there were more encouraging findings on the jobs created by these projects. It is important to note that employment is not recorded for every project, and that in 2011 employment data was only provided for 46% of the projects recorded. However, the data that is available shows that the UK maintained its record of being ranked first in Europe for FDI job creation in every year since records began in 1997, with the exception of 2006 when it was briefly overtaken by Poland.

Countries 2011 employment

2010 employment

Percentage change

UK 29.888 21,209 40.9Germany 17,276 12,044 43.4Serbia 13,479 8,519 58.2France 13,164 14,922 -11.8Spain 9,205 7,723 19.2Russia 8,362 8,058 3.8Poland 7,838 12,366 -36.6Turkey 7,925 3,830 90.5Romania 5,985 4,789 25Ireland 5,373 5,785 -7.1

Source: Ernst & Young's European Investment Monitor 2012.

Figure 2Largest recipients of employment created by FDI in 2011

In 2011, the number of recorded jobs created by FDI projects in the UK rose by 41% to almost 30,000, from a below-trend level of 21,200 in 2010. While this rise was slightly outpaced by Germany, where the jobs created rose by 43% to just over 17,000, the projects secured in 2011 saw the UK’s share of new FDI-driven jobs across Europe rise to 19%, its highest level in more than a decade. Compared with Europe’s other leading FDI recipients, this means the UK has significantly widened its lead in terms of market share of the resulting new employment in recent years.

Graph 3The four leading European countries’ share of total employment created by FDI

0

2

4

6

8

10

12

14

16

18

20

2011201020092008200720062005200420032002

United Kingdom GermanyFrance SpainPe

rcen

tage

of e

mpl

oym

ent

Source: Ernst & Young's European Investment Monitor 2012.

There are equally positive findings on the UK’s ability to attract FDI projects from companies that have not previously invested here. The findings of Ernst & Young’s 2012 UK attractiveness survey (see page 23) suggest that overseas companies already investing in the UK are generally more positive about the UK than those that have not yet invested here. However, stripping out re-investments at existing sites, the 2011 FDI figures show that the UK’s share of new projects is actually slightly higher than for re-investments, suggesting that the UK is more than holding its own in attracting new investors. Also, Germany’s share of projects from new investors declined in 2011, confirming that its strong performance in 2011 was influenced by a high rate of re-investment projects from existing investors.

Graph 4

European FDI market share of the top four recipients — new investments employment created by FDI

0

5

10

15

20

25

10987654321

United Kingdom GermanyFrance Spain

Perc

enta

ge o

f em

ploy

men

t

Source: Ernst & Young's European Investment Monitor 2012.

9Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

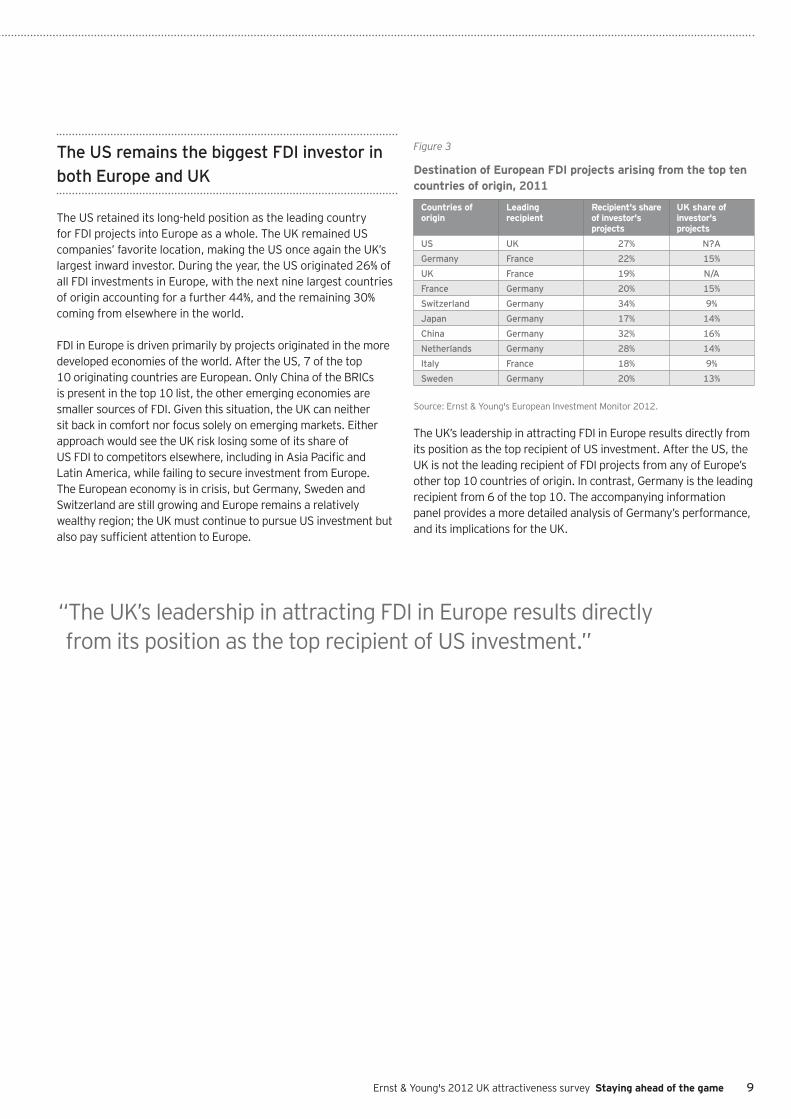

The US remains the biggest FDI investor in both Europe and UK

The US retained its long-held position as the leading country for FDI projects into Europe as a whole. The UK remained US companies’ favorite location, making the US once again the UK’s largest inward investor. During the year, the US originated 26% of all FDI investments in Europe, with the next nine largest countries of origin accounting for a further 44%, and the remaining 30% coming from elsewhere in the world.

FDI in Europe is driven primarily by projects originated in the more developed economies of the world. After the US, 7 of the top 10 originating countries are European. Only China of the BRICs is present in the top 10 list, the other emerging economies are smaller sources of FDI. Given this situation, the UK can neither sit back in comfort nor focus solely on emerging markets. Either approach would see the UK risk losing some of its share of US FDI to competitors elsewhere, including in Asia Pacific and Latin America, while failing to secure investment from Europe. The European economy is in crisis, but Germany, Sweden and Switzerland are still growing and Europe remains a relatively wealthy region; the UK must continue to pursue US investment but also pay sufficient attention to Europe.

Countries of origin

Leading recipient

Recipient's share of investor's projects

UK share of investor's projects

US UK 27% N?AGermany France 22% 15%UK France 19% N/AFrance Germany 20% 15%Switzerland Germany 34% 9%Japan Germany 17% 14%China Germany 32% 16%Netherlands Germany 28% 14%Italy France 18% 9%Sweden Germany 20% 13%

Figure 3

Destination of European FDI projects arising from the top ten countries of origin, 2011

Source: Ernst & Young's European Investment Monitor 2012.

The UK’s leadership in attracting FDI in Europe results directly from its position as the top recipient of US investment. After the US, the UK is not the leading recipient of FDI projects from any of Europe’s other top 10 countries of origin. In contrast, Germany is the leading recipient from 6 of the top 10. The accompanying information panel provides a more detailed analysis of Germany’s performance, and its implications for the UK.

“The UK’s leadership in attracting FDI in Europe results directly from its position as the top recipient of US investment.”

10 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

UK's challenge to staying ahead

Germany’s rise sounds a warning-bell for the UK

While the UK is still the leader in European FDI, the 2011 figures underline the growing competitive challenge from second-placed Germany. As we noted earlier, projects in Germany rose by 7% in 2011, while those in the UK fell by the same percentage. As a result, Germany’s share of European FDI projects rose to 15%, narrowly behind the UK’s 17%.

If these trends continue, Germany will overtake the UK as Europe’s leading FDI destination within the next two or three years. A closer look at the figures confirms that Germany’s rising performance is broadly based across several industries and countries. Like the UK, Germany has the US as its main source of projects, and business services as its main sector. But Germany is performing better in securing projects in the largest sectors from the largest country of origin — while remaining strong in gaining FDI from European neighbors.

These trends have seen Germany’s share of European FDI edge up for most of the past decade, while the UK’s share has been flat or declining. In 2011, Germany overtook the UK in manufacturing investment projects (see chart below), and closed the gap in service sector market share. It also overtook the UK for the first time in projects from Japan, and attracted twice as many Chinese projects as the UK.

The findings of Ernst & Young’s 2012 European attractiveness survey cast an interesting light on these trends. The study shows that foreign investors regarded Germany as having similar attractive attributes to the UK, including strong infrastructure, workforce skills and social and political stability, and also similar areas to improve, such as training in new technologies. However, when asked which European locations will be most attractive over the next three years, 56% cited Germany, with only a quarter naming France or the UK. The respondents also ranked Germany as Europe’s biggest FDI player in world terms, naming China (25%) and the United States (19%) as Germany’s main competitors for FDI, with only 10% and 9% respectively citing France and the UK as major competitors to Germany.

So, why are foreign investors shifting towards Germany? Part of the answer lies in many years of economic and social reform, which have boosted the competitiveness and

resilience of the German economy, and made its labor market more flexible. These gains are now being acknowledged outside of Germany. Our 2012 findings show significant year-on-year rises in Germany’s attractiveness on criteria including stability and transparency, internal market, and labor costs. Germany’s strength in manufacturing and industry is underlined by the three sectors cited as its top three drivers of growth: transportation and automotive, ICT/IT, and energy and utilities. Tellingly, Germany’s unique selling point (USP) is regarded as being research and innovation.

Taken together with the FDI trends, these findings sound a warning-bell for the UK. In recent years, Germany has returned to a regional approach, under which its länder compete for FDI projects. In contrast, the UK has closed the Regional Development Agencies (RDAs) in the English regions and Wales — a change that has seen the dominance of London and the South East increase, and Scotland (which still has Scottish Enterprise) lead the way in terms of jobs. Currently, Germany is gaining market share by focusing rigorously on FDI, playing to its strengths, and leveraging the scale of its national economy. If the UK is to retain its prized lead in European FDI, it needs to regain the initiative by actively seeking out new approaches and global markets.

Percentage share of European FDI projects in manufacturing — UK versus Germany

0

5

10

15

20

25

30

2011201020092008200720062005200420031997 1998 1999 2000 2001 2002

Perc

enta

ge o

f pro

ject

s

United Kingdom Germany

Source: Ernst & Young's European Investment Monitor 2012.

11Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

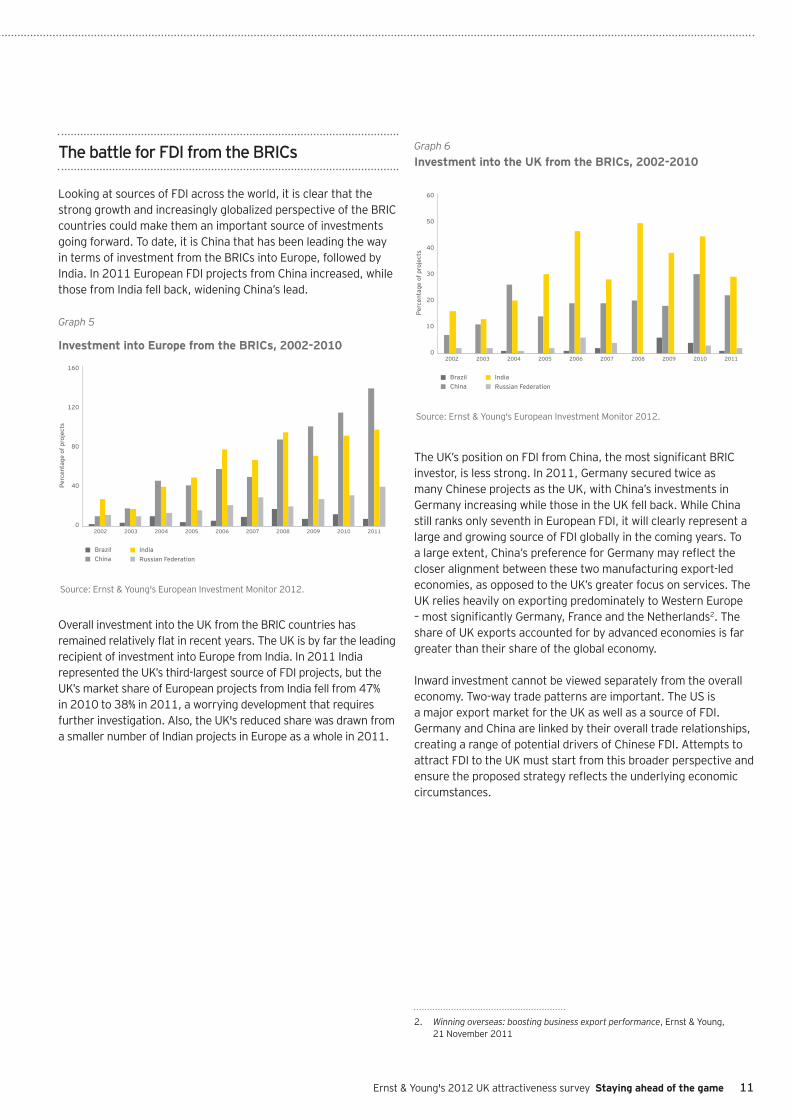

The battle for FDI from the BRICs

Looking at sources of FDI across the world, it is clear that the strong growth and increasingly globalized perspective of the BRIC countries could make them an important source of investments going forward. To date, it is China that has been leading the way in terms of investment from the BRICs into Europe, followed by India. In 2011 European FDI projects from China increased, while those from India fell back, widening China’s lead.

Graph 5

Investment into Europe from the BRICs, 2002-2010

0

40

80

120

160

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

BrazilChina

IndiaRussian Federation

Perc

enta

ge o

f pro

ject

s

Source: Ernst & Young's European Investment Monitor 2012.

Overall investment into the UK from the BRIC countries has remained relatively flat in recent years. The UK is by far the leading recipient of investment into Europe from India. In 2011 India represented the UK’s third-largest source of FDI projects, but the UK’s market share of European projects from India fell from 47% in 2010 to 38% in 2011, a worrying development that requires further investigation. Also, the UK's reduced share was drawn from a smaller number of Indian projects in Europe as a whole in 2011.

Graph 6 Investment into the UK from the BRICs, 2002-2010

0

10

20

30

40

50

60

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

BrazilChina

IndiaRussian Federation

Perc

enta

ge o

f pro

ject

sSource: Ernst & Young's European Investment Monitor 2012.

The UK’s position on FDI from China, the most significant BRIC investor, is less strong. In 2011, Germany secured twice as many Chinese projects as the UK, with China’s investments in Germany increasing while those in the UK fell back. While China still ranks only seventh in European FDI, it will clearly represent a large and growing source of FDI globally in the coming years. To a large extent, China’s preference for Germany may reflect the closer alignment between these two manufacturing export-led economies, as opposed to the UK’s greater focus on services. The UK relies heavily on exporting predominately to Western Europe – most significantly Germany, France and the Netherlands2. The share of UK exports accounted for by advanced economies is far greater than their share of the global economy.

Inward investment cannot be viewed separately from the overall economy. Two-way trade patterns are important. The US is a major export market for the UK as well as a source of FDI. Germany and China are linked by their overall trade relationships, creating a range of potential drivers of Chinese FDI. Attempts to attract FDI to the UK must start from this broader perspective and ensure the proposed strategy reflects the underlying economic circumstances.

2. Winning overseas: boosting business export performance, Ernst & Young, 21 November 2011

12 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

UK's challenge to staying ahead

Graph 7

Origin of investment projects into the UK, 2011

US

Germany

India

France

Japan

Netherlands

China

Canada

Other

Spain

Australia

21

21

19

19

18

22

60

282

2928

160

Source: Ernst & Young's European Investment Monitor 2012

Looking more broadly across the UK’s sources of FDI in 2011, the US accounted for 42% of all projects, with the next nine most important countries of origin contributing a further 35%. The Commonwealth countries of Canada, Australia and India retained their places in the UK’s top 10 origins of FDI in 2011, but did not feature in the top 10 for Europe as a whole. Japan also remained in the top 10 investors in the UK, despite a 15% decline in the UK’s market share of Japanese investment projects into Europe.

Financial services FDI is slowing down

Across Europe as a whole, historically, the leading FDI sectors of business services and software increased their share of all FDI projects in 2011, and together accounted for more than a quarter of the total. The 666 projects recorded by business services investors in 2011 represented the biggest total ever for this sector. Software projects remained below their peak of 2007, but the 436 projects recorded was a 32% increase from the low point in 2009. The UK was the leading recipient for projects in these top two sectors, and also in financial services, which ranked ninth across Europe as a whole but with its lowest number of projects for six years.

Sectors Leading recipient

Market share of the recipient

UK market share (if not leading recipient)

Business Services UK 24% N/aSoftware UK 34% N/aMachinery and Equipment Germany 21% 14%

Automotive Components Germany 15% 8%

Other Transport Services Germany 16% 4%

Food France 17% 17%Electronics Germany 18% 11%Electrical Germany 29% 11%Financial Intermediation UK 23% N/aChemicals France 17% 6%

Figure 4Ten most important sectors for European FDI, with leading recipient and market shares

Source: Ernst & Young's European Investment Monitor 2012.

The UK’s leading position in business services and software make it more reliant on FDI in these sectors than Europe as a whole. In 2011, business services continued to top the list of industries generating UK projects, despite a decline in this sector’s project numbers in the UK that ran counter to the growth recorded at a European level. Financial services investments into the UK — a traditional area of strength — fell by 15% from 2010, but this was a slower decline than recorded across Europe as a whole, meaning the UK’s market share rose slightly. The UK also increased its market share of scientific instruments and electrical FDI projects, but lost share in machinery and equipment and electronics investments.

“Financial services investments into the UK — a traditional area of strength — fell by 15% from 2010, but this was a slower decline than recorded across Europe as a whole, meaning the UK’s market share rose slightly.”

13Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

Figure 5Ten most important sectors in generating investment into the UK, 2011

Sectors 2011 projects Percentage share of 2011 projects

Percentage change on 2010

Business Services 160 23.6 -1.2

Software 147 21.6 19.5Machinery and Equipment 39 5.7 -17

Financial Intermediation 34 5 -15

Food 29 4.3 20.8Scientific Instruments 19 2.8 11.8

Electronics 18 2.7 -48.6Publishing 18 2.7 0Electrical 17 2.5 21.4Automotive Components 16 2.4 23.1

Source: Ernst & Young's European Investment Monitor 2012.

While the UK’s share of financial services FDI projects is holding firm, the general decline in projects in this sector is a worrying development. The findings of Ernst & Young's 2012 UK attractiveness survey show that overseas companies regard the UK’s position as a financial services centre as its main engine of economic growth in the coming years (see page 25). With financial services FDI currently in what may be a sustained downturn, and new investment from fast-growing markets such as China proving difficult to attract, the UK faces a pressing need to explore and open up new and additional sources of FDI.

Viewpoint

Chris Price Partner Financial Services Ernst & Young UK

The financial services industry is deleveraging fast, particularly in Europe. As it does so, the effect that regulatory change (both in terms of solvency and liquidity requirements) is having on available credit capacity is exponential rather than incremental. Against this background, the decline in financial services investment is no surprise, and it is encouraging that the UK's comparative share of such investment as is still taking place has remained solid.

The UK's position as an EU but non Eurozone member has undoubtedly contributed to this solidity. There are, however, clouds brewing on the (near) horizon. The UK's mature retail financial sector does not look attractive to foreign investment, given the opportunities in some of the less mature or emerging markets and the increasingly thin margins in that sector in the UK. But wholesale banking, capital markets and asset management in the UK do remain attractive for the long term.

However, the UK’s commitment — described in our last report — to having the most competitive tax system in the G20, and a regulatory system not materially more punitive than the other main financial centres, now looks at real risk. Although there have been some positive developments on the tax side, the UK Bank Levy — a tax on the balance sheets of banks which seems to go up in rate as balance sheets contract — is a material and largely unrivalled cost. At the same time, UK regulatory developments seem to indicate a policy change away from “not materially more punitive” towards “demonstrably more secure, regardless of cost”. The UK Government and regulators need to ensure that concerns over retail banking security — which are largely a feature of western economies — do not inhibit the wider role of UK financial services in financing and facilitating the ongoing development of global trade.

Graph 8

UK Financial Services FDI projects 1997-2011

0

30

20

10

40

50

70

60

0

10

20

30

50

40

20021997 1998 1999 2000 2001 2003 2004 2005 2006 2007 2008 2009 2010 2011

Total FS projects UK FS Share

UK

FS

proj

ects

UK

Sha

re o

f FS

proj

ects

Source: Ernst & Young's European Investment Monitor 2012.

14 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

UK's challenge to staying ahead

“The UK has a significant installed base in all of Europe’s top three job-generating sectors, and could look to boost employment by encouraging these sectors to keep building on this solid platform with new and follow-on investments.”

Top UK job creators: retail, automotive assembly and business services

In terms of employment creation through FDI projects, the industry sectors that generated the most jobs in the UK in 2011 were led by retail, closely followed by automotive assembly and business services. Significantly, while automotive assembly did not rank in the UK’s top 10 sectors in 2011 in terms of number of projects, it came second in job creation. Similarly, automotive components ranked only 10th on projects but 6th on jobs, and “other transport equipment” ranked 5th on jobs but did not make the top 10 in projects.

Figure 6

Top ten sectors generating the largest number of jobs in the UK 2011

Sectors 2011 employmentRetail 3,350Automotive Assembly 3,208Business Services 3,082Food 2,771Other Transport Equipment 2,123Automotive Components 1,802Financial Intermediation 1,765Software 1,634Machinery and Equipment 1,463Air Transport 1,193

Source: Ernst & Young's European Investment Monitor 2012.

Given the importance of job creation to the UK’s economic growth, and the stated aim of rebalancing the economy towards high-value manufacturing and exports, these findings suggest that the UK Government should target these sectors.

In assessing how these initiatives might be targeted most effectively, it is useful to look at the UK’s positioning in the sectors whose FDI is delivering the highest numbers of jobs at a European level. The top three job creators from FDI across Europe are automotive components, machinery and equipment, and automotive assembly, with retail — the UK’s top jobs creator in 2011 — lagging behind in fourth place. The UK has a significant installed base in all of Europe’s top three job-generating sectors, and could look to boost employment by encouraging these sectors to keep building on this solid platform with new and follow-on investments.

Figure 7Top ten sectors generating the largest number of jobs into across Europe 2011

Sectors 2011 employmentAutomotive Components 24,966Machinery and Equipment 13,247Automotive Assembly 12,824Retail 9,468Business Services 8,835Other Transport Equipment 8,607Food 7,999Electronics 7,615Software 7,258Clothing 6,463

Source: Ernst & Young's European Investment Monitor 2012.

15Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

16 Teesside Power Station rendered by Heatherwick studio © Heatherwick studio

The regional picture — FDI across UK regions

17Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

London and the South East of England increase their lead

In the current debate about revitalizing the UK’s growth and rebalancing the economy, a key focus is around sustaining the flexibility to attract investment in different industries across the UK regions. Historically, London and the South East of England represent the main regional focus for FDI, not just in the UK but also for Europe as a whole. Since 2004, London and the South East have secured more FDI projects than the rest of England put together, and London has received more FDI projects than any other city in Europe.

The historical concentration of activity within London and the South East intensified in 2011. Against the backdrop of an overall fall in the number of UK projects, London and the South East secured increased projects — in the case of the South East, more than twice as many as in 2010 — while every other UK region experienced a decline. As a result, London and the South East together accounted for more than 60% of UK projects in 2011 for the first time, with London alone accounting for almost 50%.

Figure 8

Regional destination of FDI projects in the UK in 2011, with percentage rises/falls

Region Project Share of UK FDI project

Change on 2011

London 327 48.2 13.1South East England 83 12.2 102.4

Scotland 51 7.5 -26.1North West England 39 5.7 -39.1

West Midlands 38 5.6 -24East England 26 3.8 -3.7South West England 25 3.7 -37.5

North East England 24 3.5 -31.4

East Midlands 20 2.9 -51.2Yorkshire 20 2.9 -33.3Northern Ireland 17 2.5 -26.1Wales 9 1.3 -52.6

Source: Ernst & Young's European Investment Monitor 2012.

Foreign investors’ continuing preference for locating projects in London and South East England was underlined by the findings of Ernst & Young’s 2012 UK attractiveness survey, with London emerging as the clear number one choice followed by the South East (see page 26). However, respondents already established in the UK were more positive than current non-investors about locating projects in other regions.

Looking across the UK as a whole, Wales saw the biggest decline in FDI projects in 2011, with its share of overall UK projects falling to 1.3%, compared to 9% in its most successful year in 2003. The Welsh Development Agency was abolished in 2006, and there has been an ongoing debate since then about the effectiveness of the Welsh economy in attracting FDI. A further worrying sign in 2011 was that all the English regions outside London and the South East saw double-digit declines in investment projects. While there is no clear-cut cause-and-effect relationship, it may be worth noting that the closure of English RDAs was announced in 2010 and they were largely disbanded in 2011, albeit with formal closure in March 2012. It remains to be seen how this affects the UK’s ability to reinvigorate FDI at a regional level.

Graph 9

Market share of UK FDI projects 1997 — 2011 — London, South of East England, Scotland and Wales

0

10

20

30

40

50

60

2011201020092008200720062005200420031997 1998 1999 2000 2001 2002

Perc

enta

ge m

arke

t sha

re

London ScotlandSE England Wales

Source: Ernst & Young's European Investment Monitor 2012.

However, the number of projects only tells part of the story on regional FDI — and the statistics on FDI employment creation paint quite a different picture. While Scotland saw its number of projects fall by 26% in 2011, it was the UK’s leading location for FDI job creation, as it was in 2010. Once again, this strong performance may reflect the committed approach of Scottish Development International over many years.

The regional picture — FDI across UK regions

18 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

The regional picture — FDI across UK regions

Figure 9UK regions securing the highest level of employment from FDI projects in 2011

Region Jobs createdScotland 5,926East Midlands 3,819North West 3,715London 3,711North East 3,019West Midlands 2,919South East England 1,706Northern Ireland 1,339East of England 1,090Wales 1,090South West 1,009Yorkshire 545

Source: Ernst & Young's European Investment Monitor 2012.

Looking at employment created elsewhere in the UK, London came fourth behind the East Midlands and North West, underlining that the high numbers of projects going into London — which are dominated by business services, software and financial services investments, primarily from the US — tend to generate fewer jobs on average than the more manufacturing-focused projects located elsewhere.

“While Scotland saw its number of projects fall by 26% in 2011, it was the UK’s leading location for FDI job creation, as it was in 2010.”

Figure 10

Top three sectors generating employment in the UK regions in 2011

Regions Total Employment

Leading sector Secondary placed sector Third placed sector

Employment Employment Employment

East Midlands 3,819 Auto Assembly 1,700 Retail 850 Transport Equipment 800East England 1,090 Food 700 Pharmaceuticals 130 Logistics 150Wales 1,090 Air Transport 770 Business Services 100 Financial Services 100Northern Ireland 1,339 Other Transport 800 Business Services 242 Auto Component 130North West England 3,715 Financial Services 1009 Logistics 850 Business Services 618North East England 3,019 Metals 1000 Auto Component 500 Financial Services 456Scotland 5,926 Logistics 2,050 Business Services 670 Food 640South East England 1,706 Electronics 650 Logistics 300 Oil and Gas 180South West England 1,009 Auto Assembly 500 Other Transport 200 Plastic and Rubber 125London 3,711 Business Services 1,294 Software 811 Construction 486West Midlands 2,919 Auto Assembly 1,000 Auto Component 830 Food 750Yorkshire 545 Food 321 Plastic and Rubber 71 Auto Component 70

Source: Ernst & Young's European Investment Monitor 2012.

19Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

The perception of UK in 2012

20

The perception of UK in 2012

21Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

As this report has shown, the European Investment Monitor (EIM) for 2011 confirms that the UK has retained its ranking as the top destination for FDI into Europe. However, for the UK to sustain this position into the future, it will need to understand which of its attributes positively attract overseas-based companies to come and invest here — and which attributes are most likely to make business decision-makers look elsewhere.

To help build this understanding, interviews were carried out with over 500 international companies on their UK investments and economic experiences to date, their perceptions of the UK as an investment environment, and their expectations for the future.

UK’s main attractions to foreign investors

The six aspects of the UK that foreign-based companies considered most attractive from an investment location perspective were: the quality of life, cultural aspects and language (with 88% rating this as very attractive or fairly attractive); the stable political environment (86%); technology and telecommunications infrastructure (85%); the stable social climate (83%); education in trade and academic disciplines (80%); and entrepreneurial culture and entrepreneurship (76%).

Five of these attributes were also ranked in the UK’s top six most attractive attributes in 2011, with the new entrant being education in trade and academic disciplines, which moved up to fifth. However, perhaps more significant is the fact that, on each of the top four factors, existing investors were significantly more positive about the UK’s attractiveness than those companies not yet active here. This is a recurring theme of the research findings.

On the 16 criteria rated by the interviewees in the survey, the UK was rated as “very attractive” or “attractive” by the majority of respondents in all but two cases. The two where the UK was rated negatively were labor costs (with only 48% saying this was very attractive or fairly attractive), and the cost and availability of real estate (40%). Corporate taxation was also seen as a relatively unattractive factor (53%). Again, existing investors were more positive on all these factors, although even they regarded real estate cost and availability as a negative, with only 45% of foreign companies with a presence here rating this factor as attractive in the UK.

It is interesting that the findings this year showed the UK’s quality of life and political stability rising in importance to top the rankings, perhaps in response to the widespread geopolitical shocks and global security concerns of the past year. Yet the UK’s attractiveness on some measures has slipped back slightly, with technology and telecommunications infrastructure rated as attractive by 89% last year against 85% this time, and the proportion of 81% that rated the UK as being attractive in 2011 in terms of access to skilled labor falling to 75% in 2012.

Comparing the UK findings with those from Germany, investors rated Germany’s top strength as its infrastructure, transport and logistics, followed by its telecommunications infrastructure, and then workforce skills. Germany’s stable political environment ranked only fifth.

22 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

The perception of UK in 2012

Very attractive Fairly attractive Little attractive Not at all attractive Can’t say

Education in trade and academic

Access to skilled labor

Transport and logistics infrastructure

Quality of life, diversity, cultureand language

Stable political, environment

Technology, telecommunicationsinfrastructure

Stable social climate

Entrepreneurial culture,entrepreneurship

41% 39% 12% 2% 6%

33% 42% 10% 4% 11%

31% 42% 16% 4% 7%

48% 40% 6% 3% 3%

47% 39% 6% 4% 4%

46% 39% 8% 3% 4%

41% 42% 10% 3% 4%

31% 45% 12% 4% 8%

Graph 10

The attractiveness of different aspects of the UK for existing and new investors

Very attractive Fairly attractive Little attractive Not at all attractive Can’t say

Supportive policy environment thatencourages sustainability investments

UK’s domestic market

Transparent legal and regulatory environment

Access to capital funding, credit

Labor costs

Cost and availability of real estate

Flexibility of labor legislation

Corporate taxation

19% 38% 18% 5% 20%

11% 37% 25% 13% 14%

12% 28% 29% 16% 15%

32% 40% 12% 4% 12%

22% 45% 19% 7% 7%

20% 44% 12% 4% 20%

19% 39% 16% 6% 20%

15% 38% 15% 6% 26%

Source: Ernst & Young's 2012 UK Attractiveness Survey.

“Of all 500 respondents, some 86% said they were definitely or fairly confident that the UK would be able to overcome the current economic challenges.”

23Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

Investors’ confidence in the UK remains strong

The global financial turmoil and the strains of domestic fiscal rebalancing are creating clear challenges for the UK economy. Yet, despite this challenging background, the business leaders interviewed were very confident in the UK’s ability to overcome the current crisis. Significantly, this confidence was almost as high among prospective foreign direct investors as existing ones.

Of all 500 respondents, some 86% said they were definitely or fairly confident that the UK would be able to overcome the current economic challenges, including 40% who were definite on this. These proportions that were among the highest in any European country, and compared to an average of 81% who were definitely or fairly confident in Europe as a whole. Among existing UK investors the confidence level in the UK rose to 89%, with 44% being definite about its ability to overcome the crisis.

40%

46%

9%2% 3% Yes, definitely

Can't say

No, definitely not

No, fairly not

Yes, fairly

Graph 11

Level of confidence in the UK’s ability to overcome its economic challenges

Source: Ernst & Young's 2012 UK Attractiveness Survey.

Less positively, 11% of respondents overall said they were not confident in the UK’s ability to recover, a figure that rose to 16% among companies not established in the UK. However, the fact that these two figures are relatively close to each other confirms that confidence among non-investors is not far behind that among companies already here.

The findings also show that confidence in the UK’s economic resilience is running ahead of confidence in most of Europe as a whole, with only 80% of non-European companies surveyed saying they are confident in Europe’s ability to engineer a recovery, including 31% who were definite about it. This may suggest that the UK’s position outside the euro is seen as insulating it from the debt crisis within the Eurozone. However, perhaps unsurprisingly, overseas investors were more confident about Germany than in the UK, with 91% saying they believed Germany would overcome the current challenges, including 54% who were definite on this point.

The UK’s attractiveness continues to grow in strength

So, in the face of challenging economic conditions globally and domestically, the UK’s attractiveness to foreign investors has remained robust. This positive picture is further brightened by the fact that almost 6 out of 10 — some 59% — of the decision makers interviewed anticipated a further improvement in the UK’s attractiveness over the next three years. This was one of the highest ratings in Europe, and represented a significant increase from 47% in the 2011 study. Among existing investors the proportion expecting an improvement was even higher, at 64%.

9%

50%

32%

7% 2% Significantly improve

Significantly decrease

Can't say

slightly decrease

Stay the same

Slightly improve

Graph 12

Expectations of how the UK’s attractiveness will evolve over the next three years

Source: Ernst & Young's 2012 UK Attractiveness Survey.

Interestingly, investors based in Asia were especially confident that the UK’s attractiveness would rise further, with 70% of them expecting this to happen. Conversely, the overall proportion of 7% anticipating a deterioration in the UK’s attractiveness rose to 11% among investors based in Western Europe.

Looking back over the studies since 2004 of investors’ expectations around the UK’s future attractiveness for inward investment, there is a clear rising trend. Eight years ago, the proportion expecting a slight or significant improvement in the UK’s attractiveness over the following three years was 33%. Today, despite the clear impact of economic uncertainty since 2010 on the proportion anticipating a significant improvement, the total figure expecting positive change is 59% — the highest since these surveys began. So, through recent economic cycles, the overall trend is steadily growing confidence among inward investors that the UK will create an increasingly conducive environment for doing business.

24 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

The perception of UK in 2012

Graph 13

Expectations of how the UK’s attractiveness will evolve, 2004-2012

44%

25%

15%

8%

4%

32%

24%

7%

2%0%

32%

9%

7%

50%

201120102004

Significantly improve Slightly improve

Significantly decrease Stay the same

slightly decrease

Total improve 33% 56% 47% 59%Total Decrease 19% 9% 9% 7%Stay the same 44% 32% 37% 32%

2012

2%

40%

37%

7%

Source: Ernst & Young's 2012 UK Attractiveness Survey.

A look at the 2012 findings on this question elsewhere in Europe reveals a relatively positive picture for the UK. Exactly 50% of foreign companies expected Germany to become more attractive for FDI over the next three years, compared to the UK’s 59%. And across Europe as a whole, the figure expecting an improvement was only 38%.

Investors focus primarily on manufacturing, sales and marketing, supply chain and logistics investments into the UK

As the UK’s attractiveness to foreign companies continues to rise, investments in new operations will continue to flow in. The research suggests that the richest source of these future investments will be companies already established and active here. When all respondents were asked whether their company had plans in place to establish operations in the UK during the coming year, 24% said they did. However, the proportion of existing investors planning to invest in new operations here was 34%, against just 6% of current non-investors.

24%

68%

8%Yes

Can't say

No

Graph 14Intention by current non-investors to set up in the UK in the next 12 months

Source: Ernst & Young's 2012 UK Attractiveness Survey

Graph 15

Types of investment planned in the UK in the next 12 months

0 10% 20% 30% 40% 50%

Acquisition

Joint venture

Greenfield

Outsourcing

Expansion

Can’t say

Relocation

Source: Ernst & Young's 2012 UK Attractiveness Survey.

Of the 123 overseas-based companies that said they were planning investments in the UK, over four in five were able to specify the type of activity into which they would be investing. As in last year’s survey, the top two types of investment were into manufacturing capacity (29%) and a sales and marketing office (28%). These top two investment options were then followed by supply chain, logistics (16%) and e-commerce technology (9%). While only 7% overall were planning to invest in sustainable development, low-carbon goods and services, the proportion intending to target investment into these areas was much higher among industry − automotive and energy companies, at 14%.

25Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

Graph 16Types of project planned in the UK in the next 12 months

0 10% 20% 30%

Manufacturing

Sales and marketing office

Supply chain/logistics

E-commerce technology

Back office

Training centre

Research and development

Infrastructure

Real estate development

Retail shop

Power station

Services centre

Headquarters

Can’t say

Sustainability development/low carbon goods and services

Source: Ernst & Young's 2012 UK Attractiveness Survey.

Growth opportunities in energy and utilities

Turning to the business sectors that leaders of overseas business expect to drive growth in the UK in the coming years, the clear first choice by a wide margin was financial services, with 36% citing it as the top growth driver, reflecting the UK’s established reputation as a global leader in this industry. However, the dominance of financial services in investors’ view of the UK may also be slightly worrying, given that the EIM figures referred to earlier showed a downturn in financial services FDI projects across Europe as a whole, including (albeit less severely) in the UK. Among the UK’s expected growth drivers, financial services was followed by energy and utilities with 18%. Industry − automotive and energy companies were more likely to regard energy and utilities as a major growth driver, with 25% of respondents mentioning it as one of their top two choices.

Despite the widespread view within the UK that manufacturing here is in decline, the study confirms that its importance to the UK economy is more fully appreciated by foreign investors. Some 18% of all respondents named manufacturing as one of the top three industries driving UK growth in the coming years, rising to 22% among respondents already established here. This is a positive finding for growth and employment, given the UK Government’s commitment to rebalance the economy, and the EIM findings show that manufacturing projects on average tend to produce higher numbers of jobs.

Graph 17Top sectors expected to drive UK growth in the future

0 10% 20% 30% 40%

Financial services centre

Energy utilities

Manufacturing

Telecommunications, technology

Clean technology

Pharmaceutical industry andbiotechnologies

Infrastructure, logistics anddistribution channels

Consumer goods and retail

B to B services excluding finance

Oil and gas

Transports industry and automotive

Real estate and construction

None

Can’t say

Source: Ernst & Young's 2012 UK Attractiveness Survey.

UK seen as a gateway to export to other markets help drive investment decisions

Asked to name the two most important factors when evaluating the UK as a potential investment location, the level of demand for their product in the UK was mentioned by 35% of respondents, rising to 44% among consumer goods companies. Other major considerations included the ability to use the UK as a base to export to other markets, cited by 20% of all respondents, by 31% of Asia-based companies, and 33% of interviewees in the chemical and pharmaceutical industries.

These findings underline the importance that many investors attach to the UK’s role as a gateway to other European markets. While 13% of all respondents felt unable to identify the main factors influencing decisions to invest in the UK, this proportion rose to 21% among companies not established here, again reinforcing the need for information and education.

“Some 10% of all respondents named manufacturing as the most important industry driving UK growth in the coming years, and 18% ranked it in the top two.”

26 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

The perception of UK in 2012

Graph 18Top factors influencing decisions to invest in the UK

0 10% 20% 30% 40%

The level of demand in the UK for yourproducts

The ability to use the UK as a base toexport to other markets

Economic growth prospects for the UK

The existence of clusters of expertise in theUK relevant for your business

The reciprocal trade that already existsbetween countries you operate in and the UK

History of your investment in the UK

The ability of the UK to support researchand innovation

The UK’s track record as a destination forinvestment

Can’t say

The demographics profile of the UK

Source: Ernst & Young's 2012 UK Attractiveness Survey.

A comparison between these findings and those elsewhere in Europe reveals some interesting contrasts. Across Europe as a whole, the top three factors influencing location decisions were the local domestic market (ranked first, as in the UK), then political stability and transparency, and thirdly labor costs. So it seems that the UK’s stability is taken as given, and that companies do not come here looking for cheap labor. Instead, a much bigger factor in the UK’s favour is its role as a gateway to the rest of Europe.

London still the number one location

In terms of the preferred location for investment within the UK, London emerged as the clear number one choice, with some 35% of all respondents choosing it — a figure that rose to 47% among businesses interviewed in North America. This finding reflects the EIM statistics showing that London and the South East of England increased their dominance in UK FDI projects in 2011. However, the attractiveness survey also shows that companies already established in the UK are more aware of the advantages offered by other locations in England, and are more open to making investments in those regions.

While 12% of all respondents chose the South East outside London as their preferred location, this rose to 15% among companies established here, and 18% among Western European businesses, who may be more familiar with the UK’s geography and trade routes to continental Europe. And existing investors were more likely than non-investors to pick the English West Midlands, North East, East Midlands and North West.

Overall, English regions outside London were the preferred choice for 38% of the interviewees as a whole, a figure that rose to 49% among existing investors, but fell to 17% among non-investors. And while 23% of all respondents could not name a preferred regional location in the UK, the proportion lacking the knowledge needed to do this was much higher among companies not yet established in the UK (42%), interviewees in North America (41%), and interviewees in Asia (40%). Again, there may be useful pointers here for marketing and information campaigns about the English regions to attract foreign investors.

Some significant industry biases also emerged. Industry − automotive and energy companies were especially keen on the West Midlands, the traditional heart of industries such as motor manufacturing. And interviewees in North America were more likely than companies from elsewhere to choose the North West of England, perhaps reflecting the strong historical trading and cultural links with cities such as Liverpool. Taken together, all these findings may provide some useful pointers for how the UK might reverse the declines in FDI in most English regions in 2011, as highlighted by the EIM figures.

Graph 19

Preferred regional locations for investment in the UK

0 10% 20% 30% 40%

London

South East England

West Midlands

North East England

East Midlands

North West of England

South West England

Scotland

Can’t say

Wales

Yorkshire

Northern Ireland

East of England

Source: Ernst & Young's 2012 UK Attractiveness Survey.

27Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

The top factor behind choice of region: local skills

When foreign companies are considering investing in the UK regions, the most important consideration by a wide margin is the availability and skills of the local workforce. This factor was rated as the number one criterion by 52% of all respondents. And several groups of respondents regarded skills availability as even more important: for example, this was highlighted as a top two consideration by 58% of companies based in North America, 61% of companies already established in the UK.

Other important considerations included the strength of business in the local area. This was mentioned by 35% of all respondents, and by 46% of those who chose London as their preferred location. Access to regional grants and investment incentives was cited by 31% of companies, and — not surprisingly — by a higher proportion (37%) of those preferring regional English locations outside London. Consumer companies were also especially influenced by regional grants and incentives, with 42% of them mentioning these.

While 15% of all respondents felt unable to name any criteria for assessing regional investments in the UK, this figure rose to 25% for companies interviewed in North America, 28% among companies not established in the UK, and 29% for companies interviewed in Asia.

Graph 20

Criteria for investing in regional locations in the UK

0 10% 20% 40%30% 50% 60%

Availability and skills of local workforce

Strength of business locally

Access to regional grants andincentives for investment

Support from regional economicadvisory bodies

Access to airports/access to harbours/good transport infrastructures

Centrally located/good location

Availability of business partners

Other

Can’t say

Source: Ernst & Young's 2012 UK Attractiveness Survey.

Longer-term agenda to compete more effectively for global FDI

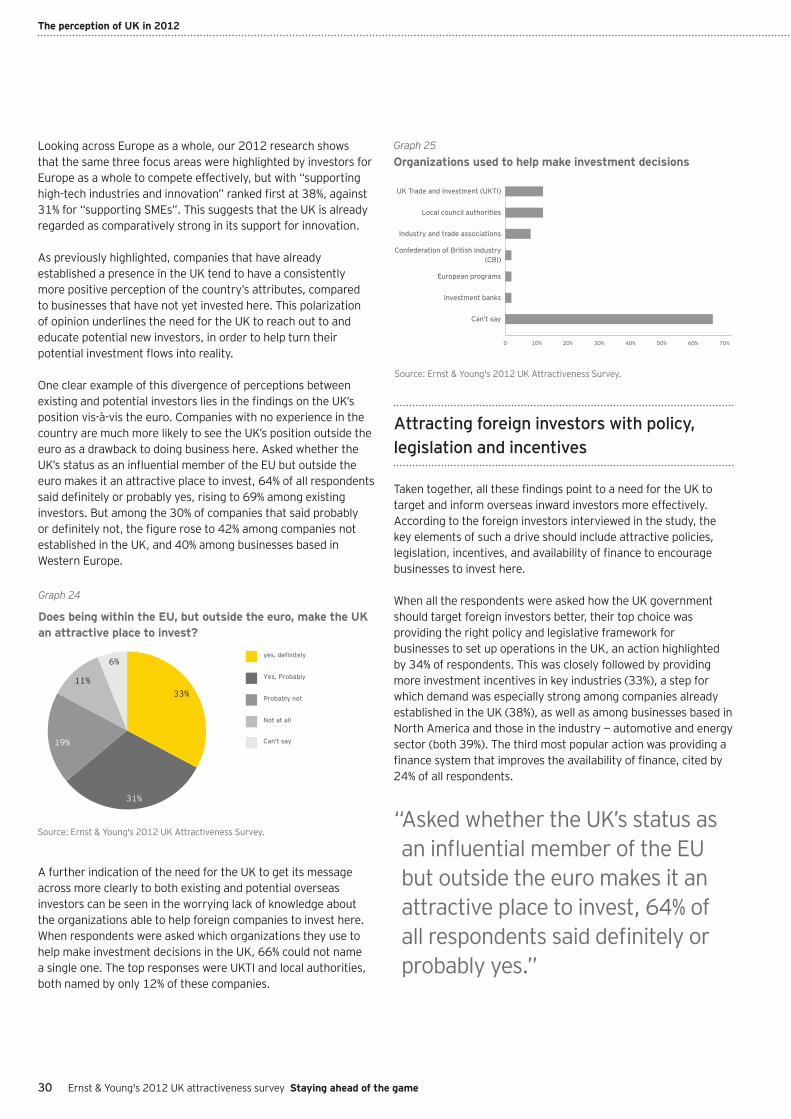

Given that the majority of direct investments into the UK in the foreseeable future are set to originate from foreign companies already established here, it is vital that the country sustains and grows its attractiveness to these businesses. However, it is equally important for the UK to tap into new sources of direct investment, by attracting more companies that to date have not had a UK presence. In many cases, the fact that new entrants will be establishing new operations means their investments will be larger than those by foreign companies already established here, whose investments may often be more incremental in nature — and therefore smaller in scale.

Asked what world-class features the UK should display in order to remain a major destination for investment, 33% of overseas companies as a whole said the UK should play to its strengths in research and development (R&D), innovation and financial services. Next came the UK’s position as a leading world-class financial services center, which was highlighted by 30% of all respondents, and by 37% of those based in Western Europe. Interestingly, in the 2011 study overseas companies ranked the UK’s “stable business environment” as the top feature it should display — perhaps reflecting the greater economic challenges faced at that time, and investors’ cautious optimism about the global outlook.

0 10% 20% 30% 40%

Leading financial service centre

Technology, telecomunications infrastructure

Predicatable business environment

Emphasis on green/sustainable business

Emphasis on social responsibility

High purchasing power

Emphasis on flexible labor laws

Research and development and innovation quality

Diversity and quality of labor force

Graph 21

Top features the UK should display to remain a major destination for FDI

Source: Ernst & Young's 2012 UK Attractiveness Survey.

Further strengths that foreign companies in the 2012 study thought the UK should focus on to attract investment included its technology and telecommunications infrastructure (highlighted by 28% of all respondents), and its predictable business environment, which was cited by 27% overall. The diversity and quality of the UK labor force was rated as a key feature for the future by 23% of all respondents, and especially by smaller businesses turning over less than €150 million, 30% of whom mentioned this factor. This suggests that smaller growing businesses are coming to the UK looking for specific technical skills.

28 Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

The perception of UK in 2012

In the research across Europe as a whole, investors agreed that R&D and innovation quality was the top feature that Europe should display to remain a major FDI destination. However, unlike in the UK, this was followed by the quality and diversity of the labor force, and the need to remain a leading financial services center — ranked second for the UK — did not even appear in the top six features that Europe as a whole should display. This contrast underlines the strength of the UK’s appeal in financial services, a position that may prove to be double-edged as financial services FDI slows down.

Innovation leadership requires a focus on education

As well as regarding innovation as key to the UK’s future attractiveness, foreign companies also saw a close correlation between the level and quality of education in the UK, and the country’s ability to be a world leader in innovation. Asked what areas the UK should reform to achieve innovation leadership, they pointed first to improving education and academic training in new technologies. This priority was highlighted by 40% overall, by 45% of existing investors, and by some 62% of respondents in the chemical and pharmaceutical industries. In our German study, improved education was also ranked first as the main focus for Germany to be an innovation leader.

As was highlighted earlier in this report, the UK’s ability to sustain and increase its economic growth in the future will depend on it remaining both a world-class exporter and also a leading investment destination. To achieve both of these goals, the country needs to enhance and grow its skills base. Whether

businesses originate from the UK or overseas, they all need access to high-quality employees with technical skills, cultural awareness and an ability to innovate.2

0 10% 20% 30% 40% 50%

Develop a culture of reaserch and innovation

Increase tax incentives for innovative companies

Develop more attractive policiesfor sustainable investment

Develop venture capital and other financial tools

Other

Improve education in trade, academic and training in new technologies

Develop enterpreneurship

Graph 22Main areas of reform to make the UK a leader in innovation

Source: Ernst & Young's 2012 UK Attractiveness Survey.

Other areas that overseas companies thought the UK should focus on to raise its game in innovation included developing a culture of research and innovation, cited by 35% of all respondents, and increasing the tax incentives for innovative companies, highlighted by 32% of all respondents, and 44% of consumer companies. While just 16% of all respondents said the UK should focus on developing venture capital and other capital tools to become a leader in innovation, the proportion advocating this type of reform was dramatically higher among high-tech and telecommunication infrastructure and equipment companies (29%), and companies based in Asia (26%).

2. Winning overseas: boosting business export performance, Ernst & Young, 21 November 2011.

Viewpoint

Managing Director, International electronics company

In my view, energy and utilities is definitely one of the sectors that will drive UK economic growth in the coming years. This is especially true of low-carbon energy projects such as smart grids.

The UK has a number of advantages as an investment location for overseas investors in the power infrastructure and technology industry. The government and private sector are driving many leading-edge initiatives to enable the low-carbon economy, and the low-carbon projects we see in the UK tend to be clearer and more focused than in most other countries. Also, the UK Energy Technologies Institute

(ETI) has close working relationships with overseas investors in the sector, and the ETI’s vision for 2020 and 2050 is very clear on both power consumption and generation.

One major opportunity for the UK is skills. The people with the right engineering capabilities and technical insights to build and manage complex low-carbon power ecosystems are in short supply not just in the UK, but all over the world. So companies, Government, universities and innovation centers in the UK should work together to create the next generation of workforce. In the long term, this new skills base will not only attract more inward investment, but will also help to boost UK exports.

29Ernst & Young's 2012 UK attractiveness survey Staying ahead of the game

Factors for remaining attractive to investors

To remain attractive in the global competition for inward investment, 29% of overseas investors believe the UK should focus on supporting SMEs, high-tech industries, innovation, and the development of education and skills. Existing investors voice an especially strong view that the UK should support SMEs and develop education and skills, with both of these factors being mentioned by 35% of those companies already established here. The top three focus areas are closely followed by lower taxation, which is highlighted by 27% of all companies, and by 34% of those based in North America.

This finding further underlines the importance of the UK Government targeting more support at SMEs as they increasingly look to enter new markets. If delivered correctly, this support would boost the UK’s growth in two ways — both by helping domestic SMEs to export more goods and services, and also by helping the foreign SME investors already present in the UK to access the right assistance and funding to grow their operations here.3

3. Winning overseas: boosting business export performance, Ernst & Young, 21 November 2011.

“The UK needs to take positive steps to attract new investors”

Viewpoint

Tony Ward, Power & Utilities sector, Ernst & Young UK

There are a number of sectors expected by respondents to drive the UK's growth, with energy and utilities second only to Financial Services. In fact, despite the recent economic downturn and slow growth, the sector has invested £8.5 billion in 2010 and £11 billion in 2011*, a reflection of its independence from the broader economic cycle. The shift to a low-carbon economy and the need to upgrade an aging infrastructure requires an even higher level of investment in the near future – around £200bn** of investment is required in the sector by 2025 if the UK is to meet its current environmental targets. Furthermore, as capital investment in the UK's energy sector has a larger indirect effect on the rest of the economy than a pound invested in most other sectors, it is clearly seen as one of the critical engines of growth.