equity research reports · pdf fileof energy resources in 2015. ... umwh mkumw holdings...

TRANSCRIPT

Equity research│September 21, 2017

Asia Pacific Daily - 21 September 2017

Equity Research Reports…

▌IDEA OF THE DAY | Asia Pacific Navigating ASIA PACIFIC 2017 - China's One Belt & One Road Initiative | P2 One Belt One Road (OBOR), China's key national strategy, could be mutually beneficial for China and OBOR countries, in our view. We see infrastructure as the best angle for cooperation under the OBOR strategy. We estimate investment mobilised by OBOR to boost GDP of emerging Asia (ex-China) by 0.6% and that of ASEAN countries by 0.7% p.a. in 2017-2025F. We recommend Chinese construction companies, capital goods and commodity players, ASEAN construction companies and banks as potential key beneficiaries. ——————————————————————————————————————————————————————————————————————————————————————— ▌Economics MAL - Economic Update - Aug 2017 consumer price inflation | P3 ——————————————————————————————————————————————————————————————————————————————————————— ▌Australia TPG Telecom (REDUCE, tp:A$4.30▼) - Spending up big in the years ahead | P4 Transurban Group (HOLD, tp:A$11.68▼) - All we (might) need is just a little patience | P5 ——————————————————————————————————————————————————————————————————————————————————————— ▌China/Hong Kong Swire Properties Ltd (ADD, tp:HK$31.00) - Swire/Taikoo brand is gaining traction | P6 ——————————————————————————————————————————————————————————————————————————————————————— ▌India Financial Services - Overall (OVERWEIGHT) - Asset quality bottoming out; valuations attractive | P7 ——————————————————————————————————————————————————————————————————————————————————————— ▌Indonesia Astra International (HOLD, tp:Rp8,700.00) - Few surprises in August | P8 Property Devt & Invt (OVERWEIGHT) - Chinese developers: limited impact for now but… | P9 ——————————————————————————————————————————————————————————————————————————————————————— ▌South Korea SK Hynix (ADD, tp:W95,000.00) - Toshiba deal likely closing in favour of Hynix | P10 ——————————————————————————————————————————————————————————————————————————————————————— ▌Malaysia Berjaya Sports Toto (ADD▲, tp:RM2.85▲) - Appealing dividend yields | P11 Autos (UNDERWEIGHT) - Still in acceleration mode | P12 Strategy Note - Investor sentiment: Current vs. Jan-Feb 17 | P13 ——————————————————————————————————————————————————————————————————————————————————————— ▌Singapore Willas-Array (NR, ctp:S$0.79) - Opportunities in distribution | P14 ——————————————————————————————————————————————————————————————————————————————————————— ▌Thailand Total Access Communication (REDUCE, tp:THB53.63▲) - Misplaced optimism | P15

Showcasing CIMB Research Ideas

CHN: Navigating China: Education 19/9 Invest for a bright future

——————————————————————————————————————————————————————————————————————————————————

THB: BTS Group 18/9 Synergistic growth along MRT lines

——————————————————————————————————————————————————————————————————————————————————

IN: Strategy Note-Alpha 15/9 Metals: continued rally is contrary to history

——————————————————————————————————————————————————————————————————————————————————

HKG: Property - Overall 14/9 Navigating farmland conversion in HK

——————————————————————————————————————————————————————————————————————————————————

THB: Telco - Mobile 13/9 Rationalisation of spectrum reserve prices a catalyst

——————————————————————————————————————————————————————————————————————————————————

Regional Equity Research Contact

Michael GREENALL, CFP Regional Head of Research T: (60) 3 2261 9088 E: [email protected]

———————————————————————————————————————————————————————————————————————————————————

Show Style "View Doc Map"

CIMB Conference / Events |

SGX-CIMB Catalist Day 20 November 2017; Singapore; Singapore —————————————————————————————————————————

CIMB Korea C-Suite Double Bagger Conference 22 - 23 November 2017; Malaysia; Seoul —————————————————————————————————————————

CIMB 10th Annual Malaysia Corporate Day 04 January 2018; Malaysia; Kuala Lumpur

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Navigating Asia Pacific│Strategy│September 20, 2017

Strategy Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH. EFACustomEntityStatement|

Powered by the EFA Platform

Asia Pacific Strategy China’s Belt & Road: An Old-New Beginning ■ One Belt One Road (OBOR), China’s key national strategy, could be mutually

beneficial for China and OBOR countries, in our view. ■ We see infrastructure as the best angle for cooperation under the OBOR strategy. ■ We estimate investment mobilised by OBOR to boost GDP of emerging Asia (ex-

China) by 0.6% and that of ASEAN countries by 0.7% p.a.in 2017-2025F. ■ We recommend Chinese construction companies, capital goods and commodity

players, ASEAN construction companies and banks as key beneficiaries.

One Belt One Road - China’s key national strategy One Belt One Road (OBOR) was initiated by Chinese President Xi Jinping in 2013 and is one of China’s most important national strategies, in our view. The strategy covers c.67 countries, representing 62% of global population, 1/3 of global GDP and trade, and 75% of energy resources in 2015. These countries are important partners for China in terms of trade, investment and overseas projects. We think OBOR will be mutually beneficial for China and OBOR initiative countries and will be implemented in two “waves”. The first, Infrastructure Development, and the second, Connectivity. That said, there may also be security, political and economic risks.

Infrastructure investment – best angle of cooperation under OBOR Infrastructure is the best angle for cooperation between countries under the OBOR strategy, in our view. While the average quality of infrastructure in OBOR countries is close to the global average, there are huge gaps between the best and worst, implying great potential to address deficiency. The gap between infrastructure investment required to maintain economic growth and actual investment made over the next decade is also substantial, at c.5% of GDP for emerging Asia ex-China, based on ADB’s estimate.

OBOR to help narrow infra investment gap in emerging Asia Multilateral development banks like AIIB and ADB are important sources of infrastructure financing apart from the government and private sector. Significant progress has been made since China set up AIIB in 2015. We project the total infrastructure investment mobilised by the OBOR strategy in emerging Asia (ex-China) over 2017-2025F to be US$475bn/63bn from AIIB/ADB, which combined, will likely boost regional GDP by 0.6%.

Mutual benefits for ASEAN countries and Chinese corporates We estimate the additional infra investment in ASEAN countries to reach US$212bn over 2017 to 2025F under the OBOR strategy, accounting for 0.7% of GDP. Sector-wise, we forecast 1) additional 10% of steel exports from China; 2) 9% incremental cement capacity required; 3) 21% more new contracts in the region for Chinese construction companies and 4) 5% boost in exports for the Chinese heavy machinery industry.

We identify potential OBOR beneficiaries in the Asia-Pacific region In China, we think key direct beneficiaries of OBOR would include banks (Bank of China), railway equipment manufacturers (CRRC Corp), construction companies (CCCC, CRG, CRCC), cement (Anhui Conch), steel (Angang, Maanshan Iron & Steel), aluminum (Chalco), port operators (CM Port) and construction equipment manufacturers (Zoomlion). Potential beneficiaries from ASEAN include Singapore banks (DBS, OCBC, UOB), auto manufacturer (DRB-Hicom), construction companies from Malaysia (Gamuda, IJM), Thailand (CH. Karnchang, STECON, Italian-Thai Development, Unique Engineering) and Indonesia (Wijaya Karya).

Figure 1: Potential OBOR beneficiaries in China and ASEAN countries

SOURCES: CIMB RESEARCH

Asia Pacific

Insert

Analyst(s)

Ben BEI

T (852) 2532 1116 E [email protected]

Michael GREENALL, CFP T (60) 3 2261 9088 E [email protected] Edith QIAN T (852) 2532 1112 E [email protected]

China Indonesia

3988 HK Bank of China Banks UNTR IJ United Tractors Capital goods1766 HK CRRC Corp Capital goods WIKA IJ PT Wijaya Karya Construction1800 HK CCCC Construction Thailand

390 HK CRG Construction CK TB CH. Karnchang Contractor1186 HK CRCC Construction STEC TB STECON Contractor914 HK Anhui Conch Cement Materials ITD TB Italian-Thai Development Contractor2600 HK Chalco Materials UNIQ TB Unique Engineering Contractor144 HK China Merchants Port Transportation Singapore

347 HK Angang Steel Materials DBS SP DBS Financial 323 HK Maanshan Iron & Steel Materials OCBC SP OCBC Financial 1157 HK Zoomlion Heavy Industry Capital goods UOB SP UOB Financial Malaysia KEP SP Keppel Corporation Conglomerate GAM MK Gamuda Construction STE SP ST Engineering ConglomerateIJM MK IJM Corp Construction SCI SP Sembcorp Industries Conglomerate UMWH MK UMW Holdings Capital goods SMM SP Sembcorp Marine Offshore & marine DRB MK DRB-Hicom Auto

Beneficiaries of OBOR

2

Malaysia│September 20, 2017

Economics Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Economics Update Aug 2017 consumer price inflation ■ Headline inflation exceeded expectations in Aug, accelerating to 3.7% yoy. ■ Fuel inflation rebounded in Aug, on the back of monthly gains in retail fuel prices, a

trend that extends into Sep based on month-to-date pump prices. ■ Core inflation slipped in Aug due to dips in healthcare, recreation & culture and

miscellaneous goods and services. ■ We revise our inflation forecast upwards to 3.8% in 2017 but expect BNM to keep the

policy rate on hold at 3.00% this year.

Headline inflation ratchets up again… Higher fuel prices rekindled Malaysia’s headline inflation (+3.7% yoy in Aug vs. +3.2% yoy in Jul), outstripping gains expected by us (+3.3% yoy) and the Bloomberg consensus median forecast (+3.4% yoy). A sharp sequential jump of 0.9% mom (-0.1% mom in Jul) was the prime driver of the annual gains, rather than base effects. YTD, inflation declined to 3.9% in 8M17 (+4.0% yoy in 7M17). Core inflation nudged lower to 2.4% yoy in Aug (+2.6% yoy in Jul), due to dips in recreation & culture, healthcare and miscellaneous goods & services. … as fuel inflation bites Transport price inflation accelerated to 11.7% yoy in Aug, after dipping to 7.7% yoy in Jul. The culprit was the fuel & lubricants (F&L) index (+20.5% yoy in Aug vs. +11.8% yoy in Jul), as RON95, RON97 and diesel retail pump prices were raised by 5.2-8.3% mom in Aug. We expect fuel inflation to increase again in Sep. Month-to-date fuel prices have risen 2.1-4.0% in Sep, taking the cue from the upward trend in global oil prices. Food inflation broadly stable but expected to dip from Nov Food inflation rose slightly to 4.3% yoy in Aug (+4.2% in Jul). Food items seeing higher inflation were meat (+1.9% yoy vs. +1.3% yoy in Jul), fish & seafood (+8.1% yoy vs. +6.7% yoy in Jul), and bread & bakery products (+2.6% yoy vs. +2.3% yoy in Jul). Meanwhile, weaker inflation was observed for milk, cheese and eggs (-1.0% yoy vs -0.5% yoy in Jul), fruits (+3.2% yoy vs. +3.6% yoy in Jul), and vegetables (+2.9% yoy vs. +3.3% yoy in Jul). Inflation for food away from home fell (+4.8% yoy in Aug vs. +4.9% yoy in Jul) but price gains quickened in restaurants (+3.1% yoy vs. +2.8% yoy in Jul). Food inflation is expected to moderate sharply from Nov, as cooking oil price increases in Nov 2016 raise the year-on-year base. Rental revisions boost inflation in housing and utilities The sub-index for actual rental for housing – which has a weight of 18.1% in the consumption basket and is reflected in the CPI on a quarterly basis – grew 0.9% mom, resulting in a 3.0% yoy gain in Aug (+2.7% in Jul). This lifted inflation in housing and utilities to 2.4% yoy (+2.2% yoy in Jul). Inflation forecast raised but no OPR hike on the horizon The higher-than-expected headline print in Aug, together with further retail fuel price increases in Sep suggests that upward pressure on prices may be stronger than we initially estimated. We revise our headline inflation forecast higher to 3.8% in 2017 (vs. 3.5% previously). Despite the upward revision in inflation, we expect BNM to look through the cost-push price pressures – which should wane in 2018 – and focus on benign core inflation as an indication that slack in the economy is still present. Therefore, we keep our forecast for the Overnight Policy Rate (OPR) at 3.00% until end-2017.

Figure 1: CPI and components (% yoy)

SOURCES: CIMB, COMPANY REPORTS

Malaysia

CPI and PPI

Transport inflation vs. retail fuel prices

Insert

Economist(s)

Michelle CHIA

T (60) 3 2261 9097 E [email protected] LIM Yee Ping T (60) 3 2261 9083 E [email protected]

-20

-15

-10

-5

0

5

10

15

20

0

1

2

3

4

5

6

Jan-14 Jan-15 Jan-16 Jan-17

%yoy%yoy

Core CPIHeadline inflationPPI for local production (RHS)

-40

-20

0

20

40

60

80

Jan-14 Jan-15 Jan-16 Jan-17

%yoy

RON95 RON97

Diesel Transport CPI

Weights May-17 Jun-17 Jul-17 Aug-17 8M17

CPI 100.0 3.9 3.6 3.2 3.7 3.9Food and non-alcoholic beverages 30.2 4.4 4.3 4.2 4.3 4.2Alcoholic beverages and tobacco 2.9 0.2 0.1 0.1 0.1 0.1Clothing and footwear 3.3 -0.2 -0.4 -0.4 -0.3 -0.3Utilities 23.8 2.2 2.2 2.2 2.4 2.2Furnishing, household eqp. and maintenance 3.8 2.1 2.1 2.6 2.7 2.0Health 1.7 2.9 2.6 2.9 2.7 2.6Transport 13.7 13.1 10.5 7.7 11.7 13.5Communication 5.2 -0.3 -0.3 -0.3 -0.3 -0.3Recreation and culture 4.9 2.9 3.0 2.6 0.4 2.7Education 1.1 1.7 1.7 1.6 1.6 1.7Restaurants and hotels 2.9 2.3 2.5 2.6 2.8 2.4Misc. goods and services 6.5 1.3 1.2 1.1 0.9 1.3

Core CPI 73.2 2.6 2.5 2.6 2.4 2.5Services 50.5 2.9 3.0 3.0 2.6 2.8

3

Telco - Integrated│Australia│Equity research│September 19, 2017

IMPORTANT DISCLOSURES REGARDING COMPANIES THAT ARE THE SUBJECT OF THIS REPORT AND AN EXPLANATION OF RECOMMENDATIONS CAN BE FOUND AT THE END OF THIS DOCUMENT. MORGANS FINANCIAL LIMITED (ABN 49 010 669 726) AFSL 235410 - A PARTICIPANT OF ASX GROUP

Powered by EFA

TPG Telecom

Spending up big in the years ahead

TPM’s FY17 underlying EBITDA slightly beat guidance but the key bit of new news ■was a substantially lower final dividend (2cps which was down 73% yoy).

TPM has flagged a move to more aggressive accounting treatment in capitalising ■planned mobile expenses. This increases our reported EPS but has no material impact on our free cash flow forecasts or valuation.

We expect TPM’s capital spend to be double its operating cashflow in FY18 and ■substantially higher in the next few years as they build out their mobile businesses in AU and SG in an attempt to combat earnings pressure from the NBN.

Changing accounting treatment, declining EBITDA, negative free cashflow, rising ■debt and competitive intensity, see us to retain our Reduce recommendation.

Result snapshot Reported EBITDA of A$890.8m was up 5% yoy and 1% ahead of our forecast. Reported EPS was also 1% ahead of our forecast, but the final dividend of 2cps (vs 7.5cps the pcp) was well below. Stronger operating cashflow and lower capex resulted in net debt of A$859m which was lower than we had forecast. TPM reported free cashflow of A$119.4m for FY17 which was slightly less than the A$124.5m it received on divesting non-core VOC shares. Without this divestment, gearing would have increased in FY17. This, combined with TPM’s substantial upcoming capex requirements, likely explains the reduction in the final dividend. TPM expanded its debt facility headroom to A$2,385m, in anticipation of financing its substantial planned mobile network build.

Noteworthy items Corporate reported 1.8% revenue growth and 4.2% EBITDA growth from FY16 to FY17. This was below our expectations and shows limited traction with regard to accelerating TPM’s push into corporate to offset looming NBN margin pressure. Consumer performed better than we had expected with 4.8% revenue and 10.5% EBITDA growth from FY16 to FY17. Subscriber growth continues to slow at +25k in 2H17 (+43k in 1H17). Despite launching an aggressive mobile offering in March 2017, currently as a Vodafone reseller, mobile subscribers declined yoy and hoh, albeit with a 2H17 improvement from TPM.

Outlook and forecast changes FY18 guidance is for underlying EBITDA to decline 2-4% to A$800-815m which we think is a solid outcome considering the substantial NBN margin pressures looming. We estimate TPM will spend A$1.2bn on capex in FY18 (including A$595m of Australian mobile spectrum payments which were excluded from TPM’s FY18 capex guidance). Net debt will track substantially higher from here. We have technically upgraded our FY18 EPS by 10% but this is a function of TPM’s new - and in our view more aggressive - accounting treatment which initially capitalises a large portion of its billion dollar mobile spend. The most important free cash flow item is largely unchanged as is our valuation.

Investment view – Reduce retained We retain our Reduce recommendation and our price target decreases immaterially from A$4.39 to A$4.30 as we roll forward our valuation. In our view, the key upside and downside risk from TPM relates to its ability to deliver free cash flow and service its substantially increasing debt levels. TPM’s substantial capex program sees net debt increase, on our forecasts, towards 2.7x EBITDA in FY19 which is at the upper end of our comfort zone. Increasing competition, increasing debt levels and declining EBITDA due to NBN margin pressure see us retain our Reduce recommendation.

SOURCE: MORGANS, COMPANY REPORTS

▎Australia

REDUCE (no change) Current price: A$5.49 Target price: A$4.30 Previous target: A$4.39 Up/downside: -21.8% Reuters: TPM.AX Bloomberg: TPM AU Market cap: US$4,054m A$5,077m Average daily turnover: US$9.89m A$13.24m Current shares o/s 926.2m Free float: 39.8%

Key changes in this note

FY18 EBITDA down by 2%. FY18 EPS up 10% (due to a change to more

aggressive accounting treatment). FY18 DPS down by 72%.

Price performance 1M 3M 12M

Absolute (%) -2.7 -0.2 -53.5 Relative (%) -2.1 1.4 -61.4 Nick Harris

T +61 7 3334 4557 E [email protected] James BARKER

T (61) 7 3334 4893 E [email protected]

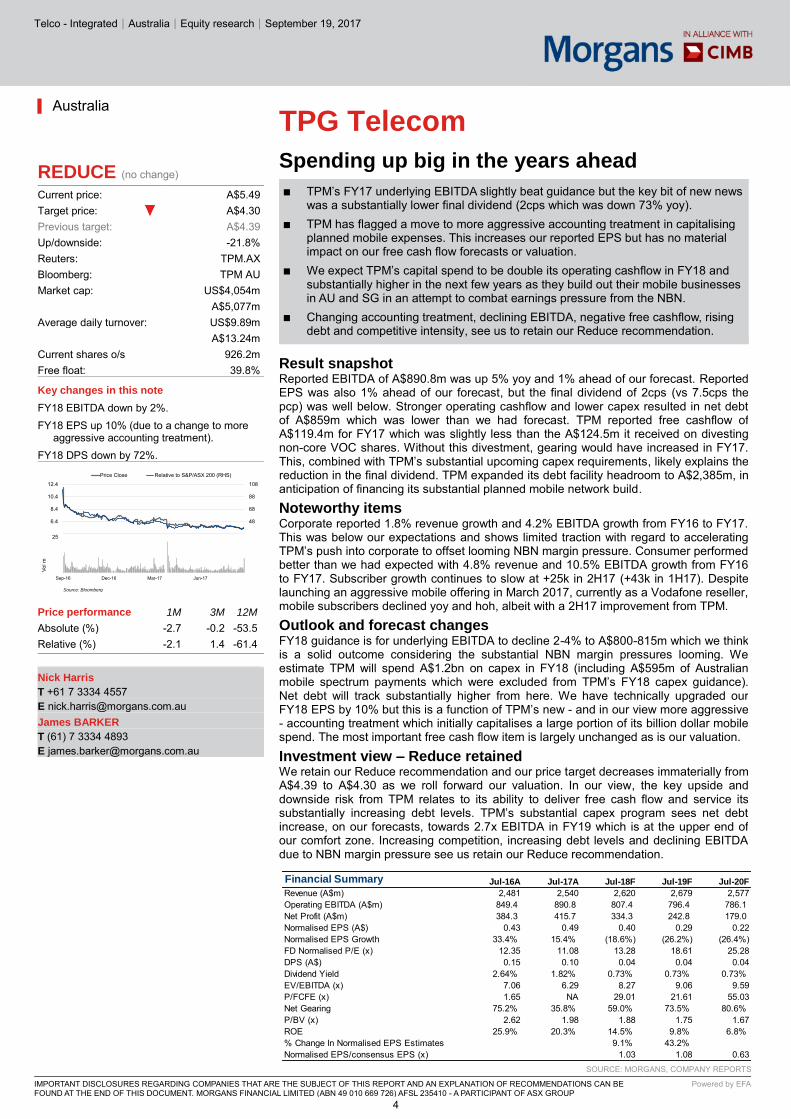

Financial Summary Jul-16A Jul-17A Jul-18F Jul-19F Jul-20F

Revenue (A$m) 2,481 2,540 2,620 2,679 2,577Operating EBITDA (A$m) 849.4 890.8 807.4 796.4 786.1Net Profit (A$m) 384.3 415.7 334.3 242.8 179.0Normalised EPS (A$) 0.43 0.49 0.40 0.29 0.22Normalised EPS Growth 33.4% 15.4% (18.6%) (26.2%) (26.4%)FD Normalised P/E (x) 12.35 11.08 13.28 18.61 25.28DPS (A$) 0.15 0.10 0.04 0.04 0.04Dividend Yield 2.64% 1.82% 0.73% 0.73% 0.73%EV/EBITDA (x) 7.06 6.29 8.27 9.06 9.59P/FCFE (x) 1.65 NA 29.01 21.61 55.03Net Gearing 75.2% 35.8% 59.0% 73.5% 80.6%P/BV (x) 2.62 1.98 1.88 1.75 1.67ROE 25.9% 20.3% 14.5% 9.8% 6.8%% Change In Normalised EPS Estimates 9.1% 43.2%Normalised EPS/consensus EPS (x) 1.03 1.08 0.63

28

48

68

88

108

4.4

6.4

8.4

10.4

12.4

Price Close Relative to S&P/ASX 200 (RHS)

Source: Bloomberg

510152025

Sep-16 Dec-16 Mar-17 Jun-17

Vol m

4

Toll Roads│Australia│Equity research│September 20, 2017

IMPORTANT DISCLOSURES REGARDING COMPANIES THAT ARE THE SUBJECT OF THIS REPORT AND AN EXPLANATION OF RECOMMENDATIONS CAN BE FOUND AT THE END OF THIS DOCUMENT. MORGANS FINANCIAL LIMITED (ABN 49 010 669 726) AFSL 235410 - A PARTICIPANT OF ASX GROUP

Powered by EFA

Transurban Group

All we (might) need is just a little patience

The CFO’s presentation to the Morgans’ network highlighted the key value drivers. ■ We are seeking a more attractive entry point into this high quality stock. This may ■

arise if TCL raises capital as expected or if there is an uptick in government bond rates.

Adjustments to forecasts for development capex, reduced DRP take-up being ■replaced with an assumed $740m capital raising, and factoring in the 395 Express Lanes have reduced our 12 month target price 9 cps to $11.68ps. HOLD retained.

Recapping CFO’s post-result briefing to the Morgans’ network CFO Adam Watson’s presentation highlighted the robust traffic and CPI/CPI+ toll growth across TCL’s four road networks, which contributed to margin expansion and double digit earnings growth in FY17. Looking forward, TCL expects its existing asset portfolio to generally deliver 5-8% pa earnings growth, which can be boosted into high single/low double digit growth as development projects ramp up. Note long-term incentives reward management for up to 10% compound annual growth in Free CF per share. Over coming years, growth of the Express Lanes (USA), the Legacy Way ramp-up and TQ integration in Brisbane, and completion of the City-Tulla Widening in Melbourne (due late 2017/early 2018) will contribute to growth, partly offset by commencement of TIFIA (USA) interest payments. FY18 DPS guidance is 56 cps, implying +8.7% growth which is slower than the double digit annual growth seen across FY14-17.

Capital deployment and funding TCL’s focus continues to be on the customer, technology, and its development pipeline. TCL estimates capital contributions to its development projects across FY18-22 will be ~$5.7bn (we estimate this includes ~$3.7bn for the West Gate Tunnel Project (WGTP) in Melbourne due for commercial close by end-2017). In addition to this development pipeline, TCL has indicated interest in the NSW Government’s 51% sell-down of WestConnex (WCX), with TCL in a strong bidding position given the synergies it may be able to generate between WCX and its existing assets in Sydney. TCL says its balance sheet remains robust, with a focus on risk management and funding the development pipeline. The CFO indicated TCL may raise equity via an entitlement offer to support the funding of the WGTP potentially around commercial close. We suspect the marked reduction in DRP take-up for the 2H17 distribution (3.8% vs ~18% average take-up over the last three years) would contribute to this thinking. A further capital raising is likely if TCL is successful with its WCX bid.

Forecast and valuation changes We have back-solved into TCL’s estimated development spend per road. This results in modelled WGTP spend being higher and more front-loaded than we had previously assumed. We assume the reduction in DRP proceeds is offset by a $740m capital raising when commercial completion of the WGTP occurs. We have also built the 395 Express Lanes into our model, noting detailed traffic and financial forecasts by TCL for the combined 95/395 Express Lanes are available in the public domain. The net impact of these changes is a 0-4% decline in forecast Free CF per share across FY18-21 and 1-3% decline in forecast DPS (with DPS coverage <100% across FY18-20). Our target price, which is predicated on an equity DCF using an 8% pa target equity return, reduces 9 cps.

SOURCE: MORGANS, COMPANY REPORTS

▎Australia

HOLD (no change) Current price: A$11.99 Target price: A$11.68 Previous target: A$11.77 Up/downside: -2.6% Reuters: TCL.AX Bloomberg: TCL AU Market cap: US$19,732m A$24,640m Average daily turnover: US$45.33m A$57.93m Current shares o/s 2,055m Free float: 100.0%

Price performance 1M 3M 12M

Absolute (%) 0.8 -7.1 11.2 Relative (%) 1.4 -5.5 3.3 Nathan LEAD

T (61) 7 3334 4548 E [email protected]

Financial Summary Jun-16A Jun-17A Jun-18E Jun-19E Jun-20E Jun-21E

Distribution (A$ cps) 45.5 51.5 56.0 60.0 64.0 68.1 - growth 14% 13% 9% 7% 7% 6%

- yield on share price 3.8% 4.3% 4.7% 5.0% 5.3% 5.7%

Prop. Toll revenue (A$m) 1,931 2,142 2,321 2,470 2,652 2,841 - growth 18% 11% 8% 6% 7% 7%

Prop. EBITDA (A$m) 1,480 1,629 1,791 1,947 2,092 2,244 - growth 15% 10% 10% 9% 7% 7%

Free CF ex one-offs (A$m) 926 1,046 1,142 1,224 1,333 1,442Free CF ex one-offs (A$ ps) 46.9 51.1 53.9 57.8 62.9 68.1 - growth 17% 9% 5% 7% 9% 8%

Prop. net debt (A$bn) 12.2 13.3 14.2 15.8 17.2 18.0 FFO:debt (BBB+: 8-12%) 7.9% 8.6% 9.3% 9.0% 9.0% 9.2%

85.0

92.5

100.0

107.5

115.0

9.20

10.20

11.20

12.20

13.20

Price Close Relative to S&P/ASX 200 (RHS)

Source: Bloomberg

10203040

Sep-16 Dec-16 Mar-17 Jun-17

Vol m

5

Property Investment│Hong Kong

Company Flash Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

Swire Properties Ltd Swire/Taikoo brand is gaining traction ■ HKRI Taikoo Hui is Swire Prop’s first property in Shanghai. It comprises the largest

mall in Nanjing West Road, 1.8msf offices and three hotels/serviced apartments. ■ After a decade of development, Swire/Taikoo brand is recognised by customers, local

developers and governments, which might present more investment opportunities. ■ Strong HK office performance and China retail sales support share price.

Swire Prop opens its first property in Shanghai ● We attended Swire Prop’s reverse roadshow in Shanghai to visit its newly-opened

HKRI Taikoo Hui and get the latest business updates. Senior management including the chief executive, finance director as well as directors for retail, office and China business, attended the briefing sessions.

HKRI Taikoo Hui - the largest mall in Nanjing West Road ● HKRI Taikoo Hui is Swire Prop’s 5th mixed-use complex opened in China. It comprises

the largest mall in Nanjing West Road (1.1msf), two office towers (1.8msf), three hotels/serviced apartments (414 rooms).

● The mall’s soft opening was in May 17 at 93% occupancy. Management expects key shoppers to be the 250k white collars working in nearby offices (70% ladies), the 300k residents in the vicinity, as well as guests in the hotel and residents in the serviced apartments. Unit rent on the first and second floors reached over Rmb1,000 psm/mth.

● The mall will introduce at least eight brands that are new to Shanghai and 14 brands that are new to China. It has the largest City Super in China and the first Starbucks Roastery outside Seattle which will create a unique shopping experience, in our view.

● The office towers are 74-80% committed and 50-60% tenants have moved in. Unit rent is c.Rmb350 psm/mth. Key tenants include law firms, private equity, retailers etc.

Swire/Taikoo brand recognised by mainlanders ● Since its first mall opened in 2008, Swire Prop has established the Swire/Taikoo brand

in China over the last decade. We believe that its unique offering and positioning is recognised by customers, local developers and governments. Management said various local developers and governments are approaching it but it is highly selective on downtown/prime locations in top tier cities.

● Swire Prop will have its sixth project in Qiantan, Shanghai, in cooperation with Lujiazui (600633 SH). The project will be completed by end-2019. The project is connected by three metro lines and will offer 2.3msf total GFA. We think Swire Prop can partner with local government or developers in getting into projects in core locations.

HK office - benefited from decentralisation and infrastructure ● Management expects Pacific Place office to be supported by strong mainlander

demand and no supply in Central, while its Quarry Bay portfolio will benefit from decentralisation. A game changer for Quarry Bay will be the Central-Wanchai Bypass (expected completion: end-2018) which will shorten the commute time to Central.

● Pre-leasing in One Taikoo Place should reach one-third by end-2017, according to management. As Swire Prop improves connectivity and people-friendliness in Taikoo Place, more law firms and top-tier financial institutions would be willing to relocate there. Management expects it to transform into HK’s Canary Wharf in the mid-term.

Reiterate Add ● Maintain Add. Our TP of HK$31 is based on 30% discount to NAV. Catalysts include

pre-leasing progress in One Taikoo Place and decent retail sales growth in China malls in 3Q17. Key risks: slowdown in HK/China economies, increasing supply in Kowloon East might weigh on Quarry Bay’s rents.

Figure 1: Swire Prop has 6 mixed-use projects in China

SOURCES: CIMB, COMPANY REPORTS

Hong Kong

September 20, 2017 - 2:54 PM

ADD (no change) Consensus ratings*: Buy 11 Hold 4 Sell 1

Current price: HK$26.20 Target price: HK$31.00 Previous target: HK$31.00

Up/downside: 18.3% CIMB / Consensus: 4.1%

Reuters: 1972.HK Bloomberg: 1972 HK Market cap: US$19,640m HK$153,270m Average daily turnover: US$6.36m HK$49.71m Current shares o/s 5,850m Free float: 18.0% *Source: Bloomberg Key financial forecasts

Source: Bloomberg Price performance 1M 3M 12M

Absolute (%) -2.6 2.3 12.7 Relative (%) -6.3 -5.9 -6.4

Major shareholders % held Swire Pacific 82.0 Insert

Analyst(s)

Siu Fung LUNG, CFA

T (852) 2539 1327 E [email protected] Raymond CHENG, CFA T (852) 2539 1324 E [email protected]

Dec-17F Dec-18F Dec-19F

Net Profit (HK$m) 7,936 8,292 8,415Normalised EPS (HK$) 1.36 1.42 1.44Normalised EPS Growth 19.7% 4.5% 1.5%FD Normalised P/E (x) 19.31 18.49 18.21Recurring ROE 3.49% 3.59% 3.59%P/BV (x) 0.67 0.66 0.65DPS (HK$) 0.75 0.77 0.80Dividend Yield 2.86% 2.94% 3.05%

92.0

97.0

102.0

107.0

112.0

20.0

22.0

24.0

26.0

28.0Price Close Relative to HSI (RHS)

5

10

Sep-16 Dec-16 Mar-17 Jun-17

Vol m

6

Financial Services│India│September 20, 2017

Sector Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Financial Services - Overall Asset quality bottoming out; valuations attractive ■ Corporate slippages are on a declining trend, in line with our thesis that a large part

of the stress has been recognised by the banks. ■ The resolution of the large stressed assets referred to NCLT could be a key sector

catalyst in the next 6-12 months. ■ Incremental NPL provisions for top 50 accounts of private lenders likely to be

manageable but PSU banks may be negatively affected given their weak profitability. ■ We believe the risk-reward is favourable for corporate lenders given attractive

valuations and improving ROEs. Maintain sector Overweight.

Corporate slippages have been trending down Corporate slippages are on a declining trend, as seen in the latest quarterly results (1QFY18). A large part of corporate slippages in 1QFY18 came from one chunky account in the electronics sector. Delinquencies were largely from agri loans due to farm loan waivers and retail/SME segment which was affected by demonetisation. Given that the bulk of the stress has been recognised by the banks we expect overall corporate delinquencies to start declining from the current levels.

Resolution of stressed loans referred to NCLT is key The resolution of stressed loans referred to National Company Law Tribunal (NCLT) could be a key catalyst in the next 6-12 months. Though banks have to make incremental provisions of up to 50% on these loans, mandated by RBI, this should improve overall coverage and strengthen balance sheets. We do not expect material incremental provisions on these loans for private banks, though the profitability of PSU banks could be dampened. Any positive resolution of stressed loans could re-rate corporate lenders.

Historical evidence of asset quality recovery across cycles Our analysis suggests that almost 35% of delinquencies were recovered or upgraded in the last 17 years. We estimate actual write-offs comprised 27% of bad loans in the last 17 years. Adjusted write-offs (after recoveries from the written-off accounts in the subsequent periods) only comprised 22% of bad loans in the past 17 years, based on our estimates. We expect overall credit costs to peak in FY18F as asset quality issues ease. We expect credit costs to normalise in FY19F onwards.

Margins negatively affected by downward re-pricing of loans Retail banks’ margins has remained stable in last 1-2 quarters (HDFCB witnessed 10bp margin uptick in 1QFY18), while corporate lenders’ margins were negative affected by the repricing of loans from base rate to MCLR. We were surprised by the pace at which corporate lenders’ margins were affected. Margins may face pressure in next 1-2 quarters but this could be partially cushioned by lower interest reversals on NPLs and improved funding profiles. We think margins will stabilise in 3Q-4QFY18F and improve thereafter.

Maintain sector Overweight We believe asset quality pressure for banks will ease going forward and the risk-reward should be favourable for corporate lenders as a large part of the stress has been recognised by banks. We expect corporate lenders to trade at a premium to their past five-year average multiples. We stay sector Overweight. Our top picks are ICICI, AXIS and SBI. Key risks include- Delayed resolutions on stressed assets than expected and weak loan growth thereby impacting profitability.

Figure 1: Sector valuation

SOURCES: CIMB RESEARCH, COMPANY

India

Overweight (no change)

Highlighted companies

Axis Bank ADD, TP Rs645.0, Rs520.8 close

Asset quality pressure likely to persist through FY18F, but PCR of ~64% offers comfort. Operating profit could bounce back in FY18F. In our view, a strong retail franchise and robust CASA accruals are likely to continue. ICICI Bank ADD, TP Rs345.0, Rs294.7 close

ICICI Bank is likely to deliver a strong 19% earnings CAGR (over FY18-20F). Key potential catalyst is the resolution of some of the chunky assets. CASA franchise remains strong and Tier 1 cap is at a comfortable level.

State Bank of India ADD, TP Rs330.0, Rs267.8 close

We like SBI for its strong capital position, liabilities franchise and peaking delinquencies. Margins are likely to remain resilient. It is a key beneficiary of the uptick in the economy, in our view.

Summary valuation metrics

Analyst(s)

Siddharth TELI

T (91) 22 4880 5158 E [email protected] Dhiren SHAH T (91) 22 4880 5170 E [email protected]

P/E (x) Dec-17F Dec-18F Dec-19F

Axis Bank 20.41 13.13 10.60 ICICI Bank 16.03 13.84 12.02 State Bank of India 24.10 15.74 11.52

P/BV (x) Dec-17F Dec-18F Dec-19F

Axis Bank 2.09 1.85 1.61 ICICI Bank 1.73 1.61 1.46 State Bank of India 0.97 0.93 0.88

Dividend Yield Dec-17F Dec-18F Dec-19F

Axis Bank 1.10% 1.15% 1.15%ICICI Bank 1.23% 1.61% 1.69%State Bank of India 1.59% 2.05% 2.12%

FY18F FY19F FY18F FY19F FY18F FY19FPublic Banks

BANK OF BARODA ADD 145 190 31% 11.1 8.4 0.8 0.8 7.9% 9.6%SBI ADD 268 330 23% 20.3 14.8 0.9 0.9 4.8% 6.2%Private Banks

AXIS ADD 521 645 24% 18.1 12.1 2.0 1.8 11.8% 15.9%HDFC BANK ADD 1,850 1,900 3% 25.5 20.8 4.5 3.9 19.3% 20.2%ICICI ADD 295 345 17% 16.4 13.4 1.7 1.6 11.1% 12.4%INDUSIND ADD 1,746 1,715 -2% 28.2 22.0 4.5 3.8 17.0% 18.7%YES ADD 1,867 1,925 3% 19.6 15.6 3.3 2.8 18.4% 19.8%NBFCs

SHTF ADD 1,069 1,280 20% 13.3 10.7 1.9 1.6 15.1% 16.4%LIC HF HOLD 650 695 7% 14.7 12.4 2.6 2.2 18.7% 19.1%

P/BV (x) ROEsReco Price (Rs.)

Target price (Rs.)

Upside/ Downside

P/E (x)

7

Autos│Indonesia

Company Flash Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

Astra International Few surprises in August ■ ASII’s wholesale 4W volumes slowed down in Aug, though 8M17 was still in line with

our expectation. ■ We are positive on its resilient 4W market share in Aug 17, but this could come at the

expense of margin given the company’s aggressive price discounting. ■ 2W sales volume continued to see positive momentum, offering a glimmer of hope of

a recovery in consumer spending in the lower-middle segment.

4W – slowing down, as expected ● Gaikindo released automotive monthly sales data today. National 4W sales volume

rose 13% mom/0.2% yoy in Aug 17; 8M17 volume picked up to 716,461 units, +3.7% yoy.

● ASII’s 4W sales volume rose at a slower rate at 9% mom/-8.4% yoy in Aug 17; 8M17 volume rose 8.5% yoy. ASII’s market share fell to 54% in Aug 17, though it maintained market share at 55.7% in 8M17.

● On a three-month moving average, ASII’s Aug 17 volume slowed further (+1.7% mom/-4.8% yoy), in contrast to competitors’ positive volume momentum (-0.1% mom/+4.6% yoy).

● Overall, the market trend in Aug was in-line with our expectation, as we had expected a slowdown in ASII’s sales due to the launch of Mitsubishi’s low-MPV Xpander model. 8M17 volume and market share were slightly ahead of our forecast (and formed 68% of our full-year forecast) which we think could be driven by ASII’s aggressive price discounting (potentially at the expense of 3Q17 margin).

2W – recovery on track ● National 2W sales volume rose 3.1% mom/5.2% yoy in Aug 17; 8M17 volume was

3,793,645 units, -21.7% yoy. ● ASII (Honda) 2W sales volume led the market growth at 3.8% mom/7.7% yoy in Aug

17; 8M17 volume was +2.8% yoy. ASII maintained market share at 75% in Aug 17 as well as in 8M17.

● Honda’s 8M17 volume was in line with our expectation.

Maintain a Hold rating ● Maintain Hold on ASII, with an SOP-based target price of Rp8,700. The stock now

trades at 15x forward P/E (in line with its historical five-year mean). Key downside risks are loss of market share following the launch of rivals’ models in Aug and lower margins for its dealership business given higher-than-expected discounts. An upside risk is better auto demand.

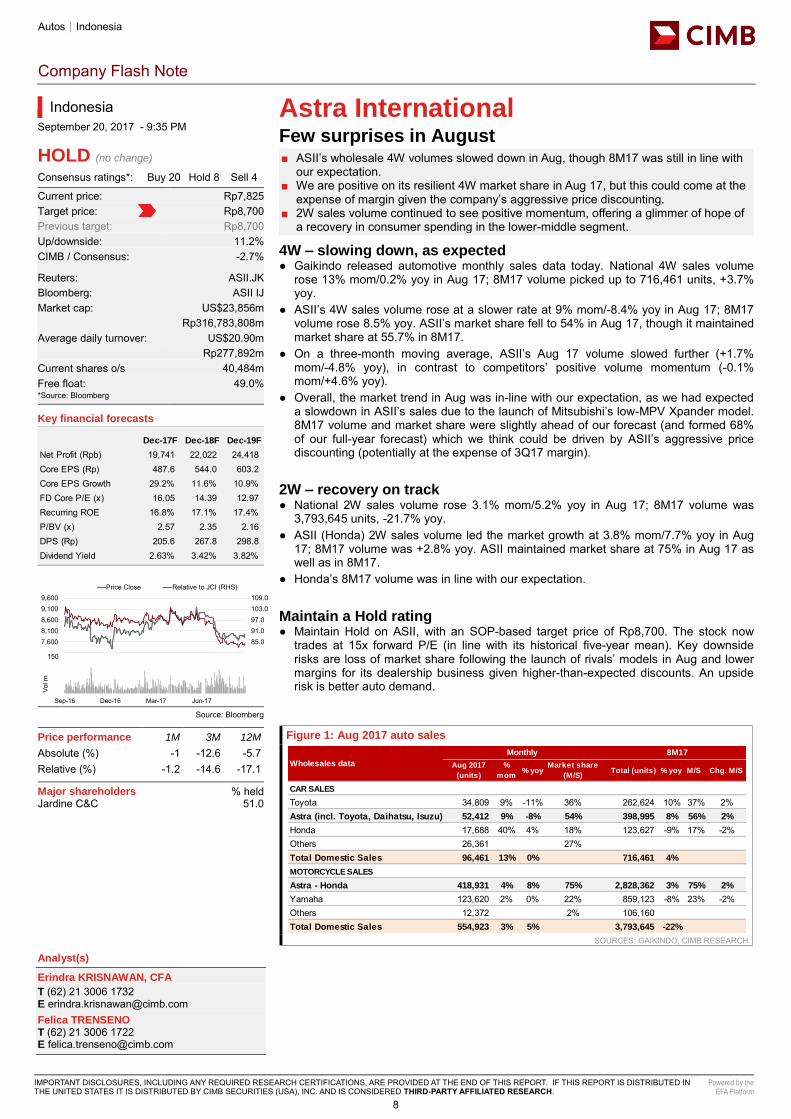

Figure 1: Aug 2017 auto sales

SOURCES: GAIKINDO, CIMB RESEARCH

Aug 2017

(units)

%

mom% yoy

Market share

(M/S)Total (units) % yoy M/S Chg. M/S

CAR SALES

Toyota 34,809 9% -11% 36% 262,624 10% 37% 2%Astra (incl. Toyota, Daihatsu, Isuzu) 52,412 9% -8% 54% 398,995 8% 56% 2%

Honda 17,688 40% 4% 18% 123,627 -9% 17% -2%Others 26,361 27%Total Domestic Sales 96,461 13% 0% 716,461 4%

MOTORCYCLE SALES

Astra - Honda 418,931 4% 8% 75% 2,828,362 3% 75% 2%

Yamaha 123,620 2% 0% 22% 859,123 -8% 23% -2%Others 12,372 2% 106,160 Total Domestic Sales 554,923 3% 5% 3,793,645 -22%

Monthly 8M17

Wholesales data

Indonesia

September 20, 2017 - 9:35 PM

HOLD (no change) Consensus ratings*: Buy 20 Hold 8 Sell 4

Current price: Rp7,825 Target price: Rp8,700 Previous target: Rp8,700

Up/downside: 11.2% CIMB / Consensus: -2.7%

Reuters: ASII.JK Bloomberg: ASII IJ Market cap: US$23,856m Rp316,783,808m Average daily turnover: US$20.90m Rp277,892m Current shares o/s 40,484m Free float: 49.0% *Source: Bloomberg Key financial forecasts

Source: Bloomberg Price performance 1M 3M 12M

Absolute (%) -1 -12.6 -5.7 Relative (%) -1.2 -14.6 -17.1

Major shareholders % held Jardine C&C 51.0 Insert

Analyst(s)

Erindra KRISNAWAN, CFA

T (62) 21 3006 1732 E [email protected] Felica TRENSENO T (62) 21 3006 1722 E [email protected]

Dec-17F Dec-18F Dec-19F

Net Profit (Rpb) 19,741 22,022 24,418Core EPS (Rp) 487.6 544.0 603.2Core EPS Growth 29.2% 11.6% 10.9%FD Core P/E (x) 16.05 14.39 12.97Recurring ROE 16.8% 17.1% 17.4%P/BV (x) 2.57 2.35 2.16DPS (Rp) 205.6 267.8 298.8Dividend Yield 2.63% 3.42% 3.82%

79.085.091.097.0103.0109.0

7,1007,6008,1008,6009,1009,600

Price Close Relative to JCI (RHS)

50

100

150

Sep-16 Dec-16 Mar-17 Jun-17

Vol m

8

Property│Indonesia│September 20, 2017

Sector Note │ Alpha series

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Property Devt & Invt Chinese developers: limited impact for now but remains a potential threat ■ Since mid-2016, Chinese developers have launched five new property projects (ex-

industrial), mainly for the mid and mid-low segment, in Greater Jakarta. ■ Based on our checks, we estimate that the five projects have garnered total presales

of Rp2.4tr, selling c.3,200 units (implying average price of below Rp1bn/unit). ■ We think the impact of Chinese developers is more area-specific. ASRI, SMRA and

BSDE will be more affected due to their proximity and similar product offerings. ■ The pace of Chinese developers’ sales is not a concern now amid slower demand but

could be a threat once they have longer track record in Indonesia. ■ Stay sector Overweight. BSDE, CTRA and JRPT are our top picks.

Chinese developers entering the residential property market Our channel checks suggest Chinese developers have launched five residential property projects in Greater Jakarta since mid-2016 (excluding Meikarta). Four of the five projects are high-rise apartments, with the exception of CFLD’s Lavon Swan City in Cikupa, Tangerang. Most of the projects are in the western part of Greater Jakarta, i.e. in Tangerang and Serpong, except for Jakarta Living Star in East Jakarta.

Decent take-up of initial launches amid attractive pricing The products cater for the mid- to mid-low segment, with most of them priced at c.Rp1bn and below. Hence, take-up rates (55-80%) have been quite good due to the affordable pricing. Based on our checks, Daan Mogot City has launched four apartment towers (one tower was sold to Chinese companies), while each of the other three high-rise projects have sold 450-550 units each. About 780 units of Lavon Swan City’s c.1,400 units launched from three clusters have been sold.

Relatively slow traction despite its ambitious targets Despite Chinese developers’ ambitious targets, we estimate that the total presales garnered by the five projects only amounted to Rp2.4tr (c.3,200 units). In relative terms, the total units sold formed less than 2% of the total apartment supply in Jakarta (Colliers expects 250k units by 2020) while Rp2.4tr forms only c.18% of large listed developers’ annual residential presales in Greater Jakarta (Rp13tr in FY16). As such, we think that Chinese developers’ sales traction has yet to present a threat to existing developers.

Limited impact on existing developers for now We think the Chinese developers’ impact will be more area-specific. Their limited track record in Indonesia also hinders them. Consequently, developers such as ASRI and SMRA may be more affected due to their close proximity to the Chinese projects (i.e. Kingland Avenue in Serpong, Lavon and Lumina near Pasar Kemis). Nonetheless, successful delivery in 2019-20F by the Chinese developers may boost their sales traction, which could pose a larger threat to big developers, in our view.

Maintain sector Overweight Stay sector Overweight. We believe that the emergence of Chinese developers does not pose an immediate threat to big developers’ presales. The sector has underperformed the JCI by 7% YTD and is currently trading at a 59% discount to NAV, steeper than its 10-year average of 43%. Our sector top picks are BSDE, CTRA and JRPT due to their better presales and earnings visibility. Key risks are poor take-up of subsequent launches and worsening sentiment due to political developments or aggressive tax collection.

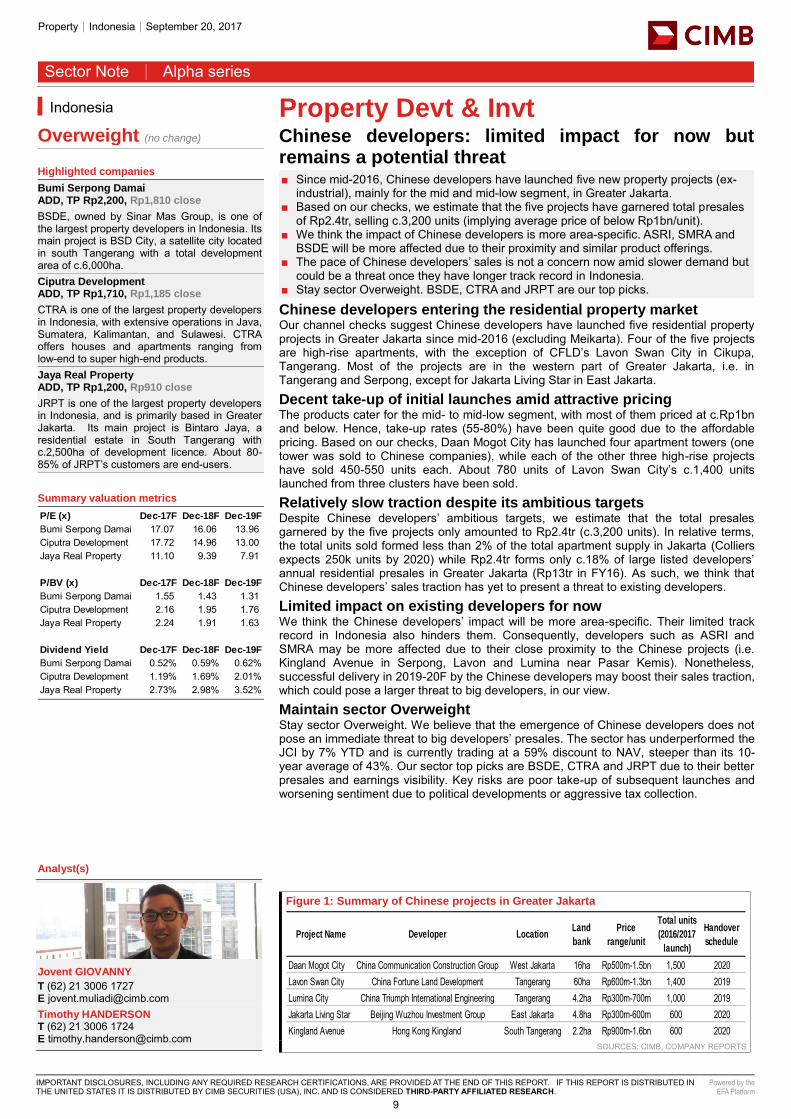

Figure 1: Summary of Chinese projects in Greater Jakarta

SOURCES: CIMB, COMPANY REPORTS

Indonesia

Overweight (no change)

Highlighted companies

Bumi Serpong Damai ADD, TP Rp2,200, Rp1,810 close

BSDE, owned by Sinar Mas Group, is one of the largest property developers in Indonesia. Its main project is BSD City, a satellite city located in south Tangerang with a total development area of c.6,000ha. Ciputra Development ADD, TP Rp1,710, Rp1,185 close

CTRA is one of the largest property developers in Indonesia, with extensive operations in Java, Sumatera, Kalimantan, and Sulawesi. CTRA offers houses and apartments ranging from low-end to super high-end products. Jaya Real Property ADD, TP Rp1,200, Rp910 close

JRPT is one of the largest property developers in Indonesia, and is primarily based in Greater Jakarta. Its main project is Bintaro Jaya, a residential estate in South Tangerang with c.2,500ha of development licence. About 80-85% of JRPT’s customers are end-users. Summary valuation metrics

Insert

Analyst(s)

Jovent GIOVANNY

T (62) 21 3006 1727 E [email protected] Timothy HANDERSON T (62) 21 3006 1724 E [email protected]

P/E (x) Dec-17F Dec-18F Dec-19F

Bumi Serpong Damai 17.07 16.06 13.96 Ciputra Development 17.72 14.96 13.00 Jaya Real Property 11.10 9.39 7.91

P/BV (x) Dec-17F Dec-18F Dec-19F

Bumi Serpong Damai 1.55 1.43 1.31 Ciputra Development 2.16 1.95 1.76 Jaya Real Property 2.24 1.91 1.63

Dividend Yield Dec-17F Dec-18F Dec-19F

Bumi Serpong Damai 0.52% 0.59% 0.62%Ciputra Development 1.19% 1.69% 2.01%Jaya Real Property 2.73% 2.98% 3.52%

Project Name Developer LocationLand

bank

Price

range/unit

Total units

(2016/2017

launch)

Handover

schedule

Daan Mogot City China Communication Construction Group West Jakarta 16ha Rp500m-1.5bn 1,500 2020Lavon Swan City China Fortune Land Development Tangerang 60ha Rp600m-1.3bn 1,400 2019Lumina City China Triumph International Engineering Tangerang 4.2ha Rp300m-700m 1,000 2019Jakarta Living Star Beijing Wuzhou Investment Group East Jakarta 4.8ha Rp300m-600m 600 2020Kingland Avenue Hong Kong Kingland South Tangerang 2.2ha Rp900m-1.6bn 600 2020

9

Semiconductor│South Korea

Company Flash Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

SK Hynix Toshiba deal likely closing in favour of Hynix ■ Bloomberg reported that Toshiba’s board agreed to sell its NAND flash business to a

tri-nation consortium headed by Bain Capital. ■ With limited control (max 15% stake within the Bain consortium), near-term benefit for

Hynix should be limited. ■ We, however, believe technology collaboration and better coordination of capacity

expansion for Toshiba and Hynix could become feasible with the deal.

Toshiba’s flip flopping likely coming to an end ● According to Bloomberg and local Japanese press reports, the 7-month-long bidding

process to sell Toshiba’s NAND flash business unit is likely coming to an end soon, with Toshiba’s board agreeing to the proposal of Bain consortium today.

● The auction has long been fairly unpredictable with Toshiba continuously changing its stance over three main bidder groups (Bain Capital, Western Digital, and Hon Hai).

No details of Bain’s proposal available yet ● With no official disclosure or comment available from Toshiba and final stock purchase

agreement (SPA) yet to come, Bain consortium’s proposal details remain unknown, except for the funding.

● According to Bloomberg, Bain, Toshiba, SK Hynix and Hoya will pay about JPY960bn for common and convertible stock, while Apple, Dell, Kingston Technology, and Seagate will inject JPY440bn for convertible and non-convertible preferred stock.

● The special purpose entity for the acquisition will be called ‘Pangea’ and will receive about JPY600bn in loans. The participation of state-backed investors from Japan (the Innovation Network Corp of Japan and the Development Bank of Japan) for the Bain consortium remains unclear.

Limited near-term impact for Hynix ● We find today’s news as positive for the investment sentiment on Hynix, with higher

possibility of Hynix’s participation in Toshiba’s chip business purchase. While the acquisition by the Western Digital camp could be largely neutral to Hynix, Hon Hai’s win could have been the worst case for Hynix and the NAND industry.

● We, however, see limited benefit for Hynix in the near-term from the potential Toshiba acquisition, as Hynix would be just one of many stakeholders of the Bain Consortium.

● Potential financial burden for Hynix from the deal would be negligible, considering our estimates for Hynix’s net cash level (W2.8tr at end-FY17F) and free cash flow (W4.1tr and W7.2tr in FY17F and FY18F respectively).

Major NAND customers’ participation bodes well for NAND demand ● We believe the deal participation of major NAND customers, including Apple and Dell,

should suggest continuously tight supply of NAND in the foreseeable future. ● Our checks suggest these major NAND customers have been keen to work out a long-

term volume supply contract with the likes of Samsung Electronics but do not appear to feel safe about the supply conditions for the next year.

● We envision potential technology collaboration and better coordination of capacity expansion for Toshiba and Hynix should become more feasible if the deal goes through as reported.

Stronger for memory cycle ahead; Add maintained ● We expect memory upcycle to persist well into next year, with Hynix being one of the

major beneficiaries. We maintain Add and our target price, which is based on 1.6x FY18F P/BV (historical 10-year average). Key risk to our Add call is Hynix’s execution on new memory processes (1xnm for DRAM and 72-layer 3D NAND).

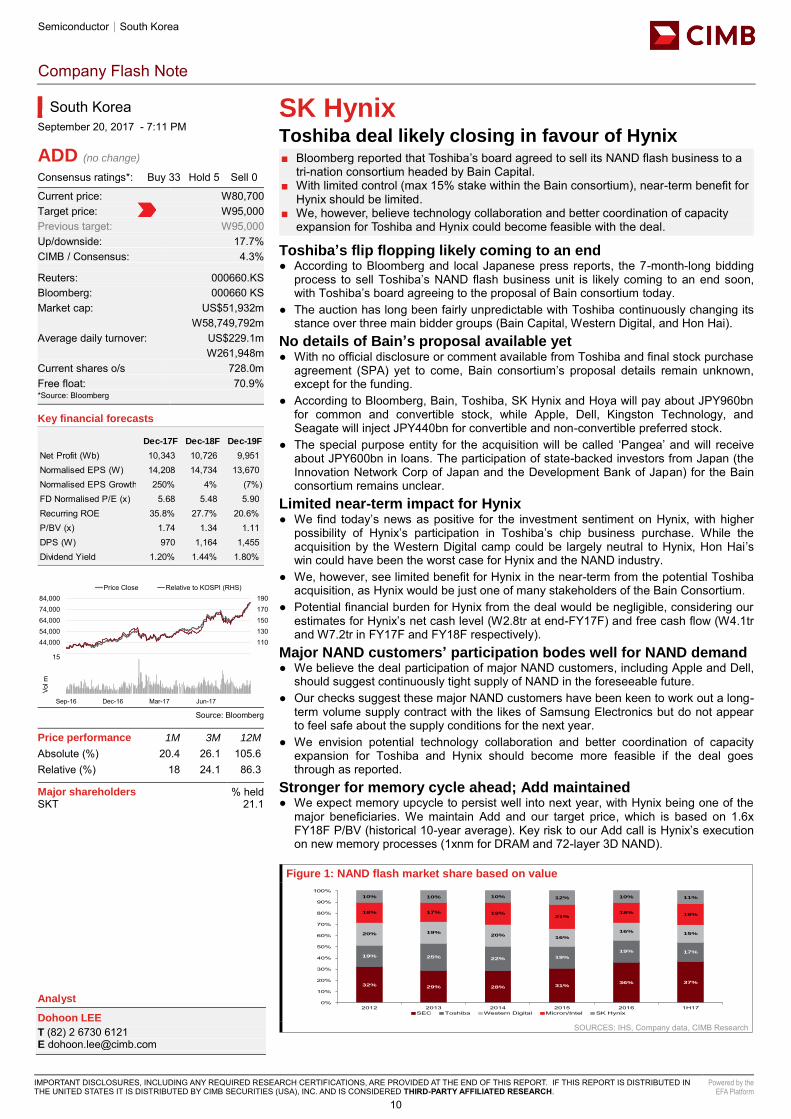

Figure 1: NAND flash market share based on value

SOURCES: IHS, Company data, CIMB Research

32% 29% 28% 31%36% 37%

19% 25% 22% 19%

19% 17%

20% 19%20%

16%

16%15%

18% 17% 19%21%

18% 19%

10% 10% 10% 12% 10% 11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016 1H17SEC Toshiba Western Digital Micron/Intel SK Hynix

South Korea

September 20, 2017 - 7:11 PM

ADD (no change) Consensus ratings*: Buy 33 Hold 5 Sell 0

Current price: W80,700 Target price: W95,000 Previous target: W95,000

Up/downside: 17.7% CIMB / Consensus: 4.3%

Reuters: 000660.KS Bloomberg: 000660 KS Market cap: US$51,932m W58,749,792m Average daily turnover: US$229.1m W261,948m Current shares o/s 728.0m Free float: 70.9% *Source: Bloomberg Key financial forecasts

Source: Bloomberg Price performance 1M 3M 12M

Absolute (%) 20.4 26.1 105.6 Relative (%) 18 24.1 86.3

Major shareholders % held SKT 21.1 Insert

Analyst

Dohoon LEE

T (82) 2 6730 6121 E [email protected]

Dec-17F Dec-18F Dec-19F

Net Profit (Wb) 10,343 10,726 9,951Normalised EPS (W) 14,208 14,734 13,670Normalised EPS Growth 250% 4% (7%)FD Normalised P/E (x) 5.68 5.48 5.90Recurring ROE 35.8% 27.7% 20.6%P/BV (x) 1.74 1.34 1.11DPS (W) 970 1,164 1,455Dividend Yield 1.20% 1.44% 1.80%

90110130150170190

34,00044,00054,00064,00074,00084,000

Price Close Relative to KOSPI (RHS)

5

10

15

Sep-16 Dec-16 Mar-17 Jun-17

Vol m

10

Gaming│Malaysia│September 20, 2017

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

Berjaya Sports Toto Appealing dividend yields ■ Berjaya Sports Toto (BST) reported 1QFY4/18 core net profit of RM68.7m; broadly in

line at 24% of our and 27% of the market’s full-year expectations. ■ The group declared 1Q18 DPS of 4 sen (vs. 1Q17 DPS: 4 sen). ■ 1Q18 sales and earnings growth yoy was fuelled by H.R. Owen due to higher vehicle

sales from new product launches as well as a lower prize payout ratio from STM. ■ We tweak up our FY18-20F EPS by 3.5-3.7% for housekeeping purposes and lower

our pay-out ratio assumption. ■ We upgrade our call to an Add in view of the share price retracement and we think

that its FY18-20F estimated yields of 6.4-6.7% should keep the stock attractive.

1QFY18 EPS broadly in line BST reported 1QFY4/18 turnover of RM1.5bn (+2.5% yoy) while core net earnings (after stripping out forex gain and reversal of inventories) increased 1.5% yoy to RM68.7m. This was broadly in line at 24% of our and 27% of the market’s full-year estimates.

4 sen DPS declared, within expectations The group also declared 1QFY18 DPS of 4 sen (vs. 1Q17 DPS: 4 sen), which represents a payout ratio of 78%. This was in line with our full-year DPS estimate of 14.8 sen (based on an 80% payout ratio assumption).

1QFY18 pre-tax profit helped by a better showing from H.R. Owen Overall, 1QFY18 yoy revenue growth was mainly fuelled by the higher contribution from H.R. Owen (a luxury car distributor and 72%-owned subsidiary of BST’s Philippine subsidiary). The improved earnings from H.R. Owen (+124% yoy) and Sports Toto Malaysia helped to offset the weaker contribution stemming from its Philippine Gaming Management Corporation (PGMC), which saw a 25.2% yoy decline in pre-tax profit on the back of lower lease rental income and higher operating expenses.

Gaming business better due to lower prize payout ratio STM, the group’s principal number forecast operator (NFO) operations, experienced declining revenue growth whereby sales declined by 2.3% yoy but pre-tax profit grew by 2.3% yoy. STM’s profitability was helped by a lower prize payout during the quarter. We estimate that 1Q18’s prize payout ratio was at 71.7% compared to 1Q17’s payout ratio of 73% (-1.3% pts yoy).

Upgrade to Add; dividend yields are attractive at 6.4-6.7% We tweak up our FY18-20F EPS by 3.5-3.7% for housekeeping purposes following the release of the group’s annual report and we impute a lower pay-out ratio assumption. However, we are upgrading our call to an Add from Hold as valuations are now attractive following the 22% share price retracement over the last 6 months and we think that estimated dividend yields of 6.4-6.7% should keep the stock attractive at these levels. Our DDM-based target price is lifted slightly to RM2.85.

Key risks Upside risks to our call include lower-than-expected prize payout ratios and better-than-expected dividend payout, while downside risks include further proliferation of illegal gaming operators.

SOURCE: COMPANY DATA, CIMB FORECASTS

Malaysia

ADD (previously HOLD) Consensus ratings*: Buy 6 Hold 6 Sell 1

Current price: RM2.32 Target price: RM2.85 Previous target: RM2.80

Up/downside: 22.9% CIMB / Consensus: 0.2%

Reuters: BSTB.KL Bloomberg: BST MK Market cap: US$746.3m RM3,125m Average daily turnover: US$0.76m RM3.25m Current shares o/s: 1,351m Free float: 63.3% *Source: Bloomberg Key changes in this note

FY18-20F EPS increased by 3.5-3.7%.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 1.3 -9.7 -31 Relative (%) 1.5 -9.3 -38.1

Major shareholders % held Gateway Benefit SB 23.2 Berjaya Land 13.5 Insert

Analyst(s)

Kristine WONG

T (60) 3 2261 9085 E [email protected]

Financial Summary Apr-16A Apr-17A Apr-18F Apr-19F Apr-20F

Revenue (RMm) 5,563 5,735 5,905 6,042 6,186Operating EBITDA (RMm) 522.0 419.3 468.6 479.1 487.8Net Profit (RMm) 306.2 241.3 259.5 265.9 272.6Core EPS (RM) 0.23 0.18 0.19 0.20 0.20Core EPS Growth (19.4%) (21.2%) 7.5% 2.5% 2.5%FD Core P/E (x) 10.24 12.99 12.08 11.79 11.50DPS (RM) 0.19 0.14 0.15 0.16 0.16Dividend Yield 8.19% 6.03% 6.62% 6.79% 6.96%EV/EBITDA (x) 7.25 9.34 7.84 7.56 7.30P/FCFE (x) 4.30 15.44 8.16 13.85 13.31Net Gearing 73.5% 90.8% 41.0% 35.3% 30.0%P/BV (x) 4.09 4.08 2.49 2.39 2.29ROE 42.2% 31.4% 25.6% 20.7% 20.4%% Change In Core EPS Estimates 3.72% 3.53% 3.70%CIMB/consensus EPS (x) 0.90 0.89 0.93

55.0

72.9

90.7

2.10

2.60

3.10

Price Close Relative to FBMKLCI (RHS)

20406080

Sep-16 Dec-16 Mar-17 Jun-17

Vol m

11

Automobiles and Parts│Malaysia│September 20, 2017

Sector Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Autos Still in acceleration mode ■ Aug 2017 TIV rose 6.5% mom due to sales recovery post-Hari Raya holidays and

fulfillment of back orders as the e-daftar registration system normalised. ■ 8M17 TIV grew 3.9% yoy, driven by stronger sales of passenger vehicles (+5.2%

yoy) amidst lower sales of commercial vehicles (-5.9% yoy). ■ Maintain Underweight as we think the strong sales growth is not sustainable in 2H17

due to lack of new model launches and on-going margin erosion from higher opex. ■ Bermaz is our top pick for its attractive yield and strong earnings recovery prospects.

We also like DRB-HICOM for its exposure to the Proton-Geely partnership.

Aug TIV up 6.5% mom, but fell 1% yoy Total industry volume (TIV) in Aug 17 grew 6.5% mom due to sales recovery following post-Hari Raya holidays and fulfillment of back orders as the e-daftar registration system normalised. However, Aug 17 TIV dropped 1% yoy due to a higher base in July 16 following multiple new model launches in the middle of 2016. Malaysian Automotive Association (MAA) expects sales in Sep 17 to be flat mom due to the ongoing promotional campaigns by dealers.

8M17 TIV grew 3.9% yoy, driven by stronger passenger car demand 8M17’s TIV grew 3.9% yoy to reach 384,734 units, driven by higher passenger vehicle sales of both national and foreign brands, which rose 6.4% and 3.8% yoy respectively. The growth came from various new model launches from both national and foreign brands. In addition, the stronger TIV sales were in line with the higher passenger car hire purchase loan applications and approvals in 8M17, which are up 4% and 5% YTD respectively. Overall, 8M17 TIV made up 64% of our full-year TIV forecast of 597k units.

However, total vehicle production volume in 8M17 fell by 1% yoy Despite the improving TIV sales, MAA said total vehicle production volume fell by 1% yoy to 342,958 units in 8M17. MAA attributed the production decline to the cautious stance taken by the automakers and inventory adjustments amid the soft market environment.

National brand closing the gap with foreign brands Perodua maintained its dominant position with 36% market share on the back of 3% volume growth YTD. Meanwhile, Proton’s market share improved to 13% YTD (vs. 12% in FY16), driven by multiple new model launches. Overall, the national brand continued to close the gap with 49% market share in 8M17 vs. 48% in 8M16. Meanwhile, Honda continued to dominate the foreign brands with 18% market share, driven by 27% yoy sales volume growth in 8M17 from various new model launches.

Still projecting tepid industry demand growth in 2017 We expect TIV sales growth to ease in 2H17F due to a high base in 2H16 as total 2H16 TIV grew by 11% hoh. The sector is also facing headwinds from currency volatility, which has resulted in higher import costs for CBU models and CKD kit components. We expect the market to remain competitive, with prolonged discounting as dealers continue to drive down inventory levels. Overall, we still project 3% TIV growth in 2017F.

Maintain Underweight rating with Bermaz as our top pick We maintain our Underweight call on the sector as we think the strong sales growth is not sustainable in 2H17 due to lack of new model launches and on-going margin erosion from higher opex. The sector trades at 1.1x CY18F P/BV, in line with its 3-year mean. However, disappointing earnings over the next one year could present downside risks. Key upside risks are the strengthening of RM vs. US$ and JPY and better-than-expected TIV growth. Bermaz remains our top pick due to its attractive earnings recovery outlook.

Figure 1: 8M17 TIV against historical FY15-16 (units)

SOURCES: CIMB RESEARCH, COMPANY

Malaysia

Underweight (no change)

Highlighted companies

Bermaz Auto Berhad ADD, TP RM2.30, RM2.06 close

Bermaz is our top sector pick for its attractive dividends and strong earnings recovery prospects in FY18F on the back of new model launches in Malaysia and expansion into the Philippines. A higher dividend payout and the successful listing of Bermaz Auto Philippines are potential re-rating catalysts. Tan Chong Motor Holdings REDUCE, TP RM1.55, RM1.73 close

We expect Tan Chong to stay focused on reducing its inventory levels. However, it may need to sacrifice profit margins in order to accelerate this process. It has no plans for any new model launches until 2018F, which does not augur well for sales. To recap, Nissan’s market share fell from 7.4% in 8M16 to 4.8% in 8M17.

Summary valuation metrics

Insert

Analyst(s)

Mohd Shanaz NOOR AZAM

T (60) 3 2261 9078 E [email protected]

P/E (x) Dec-17F Dec-18F Dec-19F

Bermaz Auto Berhad 16.45 12.99 11.61 Tan Chong Motor Holdings NA 152.29 16.22

P/BV (x) Dec-17F Dec-18F Dec-19F

Bermaz Auto Berhad 5.47 5.29 4.98 Tan Chong Motor Holdings 0.41 0.41 0.40

Dividend Yield Dec-17F Dec-18F Dec-19F

Bermaz Auto Berhad 6.10% 6.80% 7.51%Tan Chong Motor Holdings 0.58% 1.16% 1.73%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(unit)

TIV 2017 TIV 2016 TIV 2015

12

Malaysia│September 20, 2017

Strategy Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Malaysia Strategy Investor sentiment: Current vs. Jan-Feb 17 ■ We spent many weeks marketing our 2H economic and strategy outlook to investors. ■ Foreign investors are more positive and some have raised their position in Malaysia to

Overweight. However, foreign investors’ sentiments were not unanimous. ■ Domestic funds were less upbeat given the strong 8% YTD gain in KLCI. ■ Top questions are on (1) GDP growth numbers; (2) consumer sentiment; and (3)

timing of the 14TH general election for the country. ■ Maintain our KLCI target of 1,790 and top three picks for the market.

Foreign funds interests in Malaysia continue to improve We spent several weeks marketing our 2H17 economic and strategy outlook to 178 investors from 52 investment firms in Kuala Lumpur, Bangkok, Singapore and Hong Kong. Overall, domestic funds were less upbeat compared to the start of the year, following the strong YTD KLCI performance. However, we noted stronger foreign funds interests compared to our marketing trip in Jan-Feb 2017 due to stronger-than-expected GDP growth of 5.7% in 1H17.

Areas of macro interests have shifted to GDP growth At the start of the year, foreign investors were more interested in our forex views but that has now shifted to the sustainability of the strong 1H17 GDP growth as well as better appreciation of key drivers behind the GDP. We sensed that foreign investors are now more comfortable with the ringgit, which has appreciated 7.3% YTD to RM4.1875/US$1. In terms of investment themes, investors are most keen on our PNB transformation, tourism, GE14 and progress of the small-mid cap research schemes (MiDs) themes.

Key questions at the top of investors’ minds Top questions on strategy are: 1) potential timeline and market impact of GE14, 2) potential reasons for slower-than-expected corporate earnings growth against better-than-expected GDP growth, 3) whether the PNB transformation will unlock value for companies and 4) which companies offer the best exposure to the infrastructure and consumer stories in Malaysia. Key questions on macro were potential measures in Budget 2018, which we think is likely to maintain a prudent fiscal deficit and focus on advancing infrastructure investments, improving business conditions for SMEs, spurring productivity growth and providing fiscal support to lower income households.

Casting an eye over Malaysia’s improving fundamentals Investors broadly agreed that macro risks had subsided, following the stronger-than-expected upturn in Malaysia’s economy (1H17: +5.7% yoy; 2017F: +5.4%). Many, however, pointed out that consumer confidence, business sentiment and corporate earnings continued to lag the robust headline GDP growth numbers. A key driver of sequential gains in real GDP growth was the recovery in the upstream and downstream palm oil output after weather-related disruptions last year. Other sectors that contributed to accelerating growth in 1H17 were E&E, retail trade and finance.

Taking a breather on monetary policy As economic momentum reasserts itself in Malaysia and inflationary pressures gradually moderate, the urgency for monetary policy to pull strings from the top has reduced. Investors concurred that there was little urgency for BNM to raise or lower the Overnight Policy Rate from the current rate of 3%, at this juncture. There were also divergent views on whether the market’s more dovish view of global interest rates in the next year or the more hawkish guidance by central bankers in the US and Eurozone would prevail.

Maintain KLCI target and our top picks Investors generally concur with our view that the Malaysia market is likely to remain range-bound as the market awaits new catalysts to drive the market. We are of the view that potential catalysts for KLCI could include stronger-than-expected corporate earnings and/or strong foreign funds inflows. We maintain our end-2017 KLCI target of 1,790 points (16x P/E) and our top three picks continue to be Axiata, Tenaga and Gamuda.

Figure 1: Malaysia Economic Outlook and Strategy marketing for 2H17

SOURCES: CIMB, COMPANY REPORTS

Malaysia

Highlighted companies

Axiata Group ADD, TP RM6.00, RM5.06 close

We expect Axiata’s core EPS to rebound by a strong 29%/50% in FY18F/19F due to a) much higher contributions from XL, 2) net profit breakeven for Airtel by end-2018, and 3) cessation in equity accounting for Idea's losses post-merger with Vodafone. Gamuda ADD, TP RM6.15, RM5.37 close

Gamuda is the frontrunner in the rail tunnelling tenders totalling RM41bn across all projects. In the short term, resolution to the sale of its 40%-owned Splash is the key event catalyst that may lead to special dividends. Tenaga Nasional ADD, TP RM15.70, RM14.56 close

Tenaga offers resilient organic earnings growth potential. It is building four new power plants in Malaysia, which should raise its generation earnings in 2017-2020F, in our view. In addition, stronger earnings driven by the new assets it acquired in the past year is another potential re-rating catalyst for the stock.

FBMKLCI performance in 2016 and 2017

Insert

Analyst(s)

Ivy NG Lee Fang, CFA

T (60) 3 2261 9073 E [email protected] Michelle CHIA T (60) 3 2261 9097 E [email protected]

1,550

1,600

1,650

1,700

1,750

1,800

1,850

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017

Cities No of investment firms Fund managers and analysts

Kuala Lumpur 23 135Bangkok 5 13Singapore 13 19Hong Kong 11 11Total 52 178

13

Technology Components│Singapore│September 20, 2017 Shariah Compliant

Eyes on the Ground

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Willas-Array Opportunities in distribution ■ WAE is an established electronic components distributor. ■ The company was listed on the SGX in 2001 and dual-listed on the Stock Exchange

of Hong Kong in 2013. ■ Management expects market conditions to be challenging in FY18F but still sees

growth opportunities in the automotive and home appliances segments. ■ We note that a single supplier accounted for 40.7% of WAE’s FY3/17 purchases. ■ WAE trades at a historical FY17 P/BV of 0.6x and FY17 dividend yield of 6.8%.

What it does WAE was established in the early 1980s and listed on the Main Board of SGX in 2001. The company also dual-listed on the Main Board of The Stock Exchange of Hong Kong in 2013. WAE is engaged in the distribution of electronic components used in industrial, audio and video, telecommunications, home appliance, lighting, electronic manufacturing services and automotive segments. The company also provides engineering solutions. Established player Backed by long-standing relationships with more than 20 internationally-reputable principal suppliers, WAE distributes over 10,000 product items to over 3,000 customers. Its main markets are China, Hong Kong and Taiwan. WAE has established a network of offices that are strategically located in Beijing, Chengdu, Chongqing, Guangzhou, Qingdao, Shanghai, Shenzhen, Xiamen and Zhongshan. It has a subsidiary in Shanghai, which serves as a logistics centre for the group in Northern China. Key business segments are telecommunications and industrials In FY17, China accounted for 98% of revenue, while Taiwan accounted for the remaining 2%. WAE’s three largest revenue contributors in FY17 were telecommunications (27%), industrials (22%) and home appliances (13%). The automotive segment registered the strongest yoy revenue growth of 32.4% in FY17 and accounted for 11% of sales in FY17 (FY16: 9%). Key risks are customer concentration and supplier risk According to management, in FY17, sales to the group’s five largest customers accounted for approximately 20.0% of total sales for the year and the single largest customer accounted for approximately 5.9% of revenue. Purchases from the group’s five largest suppliers accounted for approximately 87.7% of WAE’s total purchases for FY17 and the single largest supplier accounted for approximately 40.7%. Outlook Management expects market conditions to remain challenging in the year ahead, in line with China’s slowing economic growth. Although it admits that the electronic components industry is unlikely to experience exponential growth in the near term, management is confident that WAE’s business is viable because of the diverse usage of electronic components. Management plans to focus its resources on potential growth segments, such as automotive and home appliances. Historical valuations WAE trades at a historical FY17 P/E of 8.7x (local peers’ average: 30.2x) and P/BV of 0.6x (local peers’ average: 0.74x). Historical FY17 dividend yield was 6.8%. Net gearing at end Mar-17 was 0.95x.

SOURCE: COMPANY DATA, CIMB

Singapore

NON RATED Current price: S$0.79 Consensus Tgt Price: N/A Up/downside: N/A Reuters: WLAR.SI Bloomberg: WAE SP Market cap: US$44.73m S$60.31m Average daily turnover: US$0.01m S$0.01m Current shares o/s: 75.50m Free float: 54.9%

Source: Bloomberg Price performance 1M 3M 12M

Absolute (%) -1.3 4.6 31.7 Relative (%) -0.5 5.3 18.6

Major shareholders % held Max Power Assets Ltd 23.7 Kwok Chan Cheung 10.4 Yeoman 3-Rights Value 8.2

This Eyes On the Ground report represents a preliminary assessment of the subject company, and does not represent initiation into CIMB's coverage universe. It does not carry investment ratings and CIMB does not commit to regular updates on an ongoing basis.

Insert

Analyst(s)

William TNG, CFA

T (65) 6210 8676 E [email protected]

Financial Summary Mar-13A Mar-14A Mar-15A Mar-16A Mar-17A

(HK$, m)

Revenue 3,157.8 3,196.3 3,391.9 3,642.2 3,883.6Gross profit 305.7 327.8 309.7 319.6 316.0Gross profit margin 9.7% 10.3% 9.1% 8.8% 8.1%Pretax profit 54.4 40.2 42.4 (58.0) 46.4Net profit 41.3 25.4 30.2 (70.0) 37.0EPS (HK cts) 54.7 33.6 40.0 (92.7) 52.1EPS growth na -38.5% 18.9% na naP/E (x) 8.3 13.5 11.4 (4.9) 8.7DPS (HK cts) 30.7 34.1 31.7 0.0 31.0Dividend yield (%) 6.7% 7.5% 7.0% 0.0% 6.8%P/BV (x) 0.63 0.62 0.52 0.62 0.59ROE 7.5% 4.6% 4.6% loss 6.8%Net gearing (x) 0.37 0.61 0.62 0.66 0.95

83.0

100.5

118.0

135.5

153.0

0.500

0.600

0.700

0.800

0.900Price Close Relative to FSSTI (RHS)

100

200

300

Sep-16 Dec-16 Mar-17 Jun-17

Vol t

h

14

Telco - Mobile│Thailand│September 20, 2017 Shariah Compliant

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

Total Access Communication Misplaced optimism ■ Maintain Reduce due to possible delays in the 2.3GHz deal and spectrum auctions in

FY18. ■ We raise our TP by 8.3% to THB53.63 as we roll forward our valuation to FY18F. ■ We think investors are too optimistic on the 2.3GHz deal and better cost structure. ■ DTAC’s EV/EBITDA looks cheap in FY17F but could rise in FY19F. ■ Upside risks to our call are stronger revenue from 2.3GHz and lower network costs.

Too optimistic Our recent discussions with investors indicate that the market is overly optimistic on DTAC on many fronts, i.e. revenue market share gain from the 2.3GHz deal, not needing additional bandwidth due to the 2.3GHz deal, cost savings from the transition from concession to licence and the stock trading at a cheap FY17F EV/EBITDA. Contrary to the market, our Reduce call on DTAC hinges on 1) only marginal upside from the 2.3GHz deal, 2) DTAC’s inability to avoid a capex cycle, and 3) its FY18F EV/EBITDA rising.

2.3GHz deal We think the 2.3GHz deal between DTAC and TOT could reduce its regulatory costs during the last phase of the concession contract, which ends in Sep 18, and enhance DTAC’s ability to defend its revenue market share. We have built DTAC’s 2.3GHz deal into our forecasts from 4Q17F onwards. However, we also cannot rule out the probability of delays in the 2.3GHz deal, similar to AIS, which has been waiting for TOT to endorse the 2.1GHz deal and tower/network rental deals for nine quarters.

850MHz and 1800MHz spectrum auction in 2H18F We think DTAC can win an 850MHz licence at THB32.9bn and 1800MHz licence at THB33.7bn during the 2H18 spectrum auctions. We think the National Broadcasting and Telecommunications Commission will set the reserve prices for 850MHz and 1800MHz licences at the final prices of the 900MHz and 1800MHz licences in 2015. We believe DTAC will need both licences to maintain 1) competitiveness in bandwidth holding, 2) its coverage and indoor penetration capability, and 3) 2G services for 3m-4m customers.

Marginal savings from transition from concession to licence We expect pre-tax cost savings from the transition from concession to licence to be THB1bn in FY19F. We estimate DTAC’s FY17F concession-related costs, i.e. regulatory fees, amortisation expense on concessionary assets and other D&A expense to be THB34.7bn. After its concession ends in Sep 18, we estimate FY19F licence-related costs, i.e. regulatory fees, network rental fees and D&A expense, to be THB33.7bn (Fig 5). We expect FY19F core net profit to rise due to favourable operating leverage effect.

Cheap FY17F EV/EBITDA DTAC’s FY17F EV/EBITDA at 5.8x looks cheap compared to AIS’s 10x and True’s 9.6x. If we incorporate higher net debt from a new capex cycle for licence and network acquisitions and lower EBITDA from network rental fees, the difference in EV/EBITDA multiples between AIS and DTAC falls from 4.3x currently to only 1.7x in FY19F and between True and DTAC from 3.9x currently to zero in FY19F (Fig 7).

Maintain Reduce Maintain Reduce. Potential de-rating catalysts are 1) delay in 2.3GHz deal, and 2) delay in 850MHz and 1800MHz auctions. We maintain FY17-19F forecasts but raise our DCF-based target price by 8.3% to THB53.63 as we roll forward our cashflow projection from FY17F to FY18F (Fig 6). Upside risks to our bearish call are 1) stronger revenue growth from the 2.3GHz deal, and 2) lower network rental fees from the JV deal with CAT.

SOURCE: COMPANY DATA, CIMB FORECASTS

Thailand

REDUCE (no change) Consensus ratings*: Buy 6 Hold 7 Sell 17

Current price: THB56.75 Target price: THB53.63 Previous target: THB49.50

Up/downside: -5.5% CIMB / Consensus: 3.2%

Reuters: DTAC.BK Bloomberg: DTAC TB Market cap: US$4,063m THB134,373m Average daily turnover: US$13.54m THB454.0m Current shares o/s: 2,368m Free float: 29.4% *Source: Bloomberg Key changes in this note

No change.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 7.1 9.1 66.9 Relative (%) 0.3 3.3 54.9

Major shareholders % held Telenor Asia Pte. Ltd. 42.6 Thai Telco Holding 22.4 TOT 5.6 Insert

Analyst(s)

Pisut NGAMVIJITVONG

T (66) 2 761 9226 E [email protected]

Financial Summary Dec-15A Dec-16A Dec-17F Dec-18F Dec-19F