equity research cardiology - baylor...

TRANSCRIPT

Equity Research

30 October 2006Americas/United States

Medical Supplies & Devices

UNDERWEIGHT

Cardiology Maturity Here to Stay

• Initiating coverage at Underweight. We are initiating coverage of the Medical Supplies & Devices—Cardiology sector with an Underweight stance. We believe that the core cardiology markets are more mature than appreciated, particularly the market for implantable cardioverter defibrillators (ICDs).

• Core markets slowing. Drug-eluting stents (DES) for angioplasty and ICDs for primary prevention of sudden cardiac death were rapidly accepted in 2003-05, and we believe incremental adoption will largely cease for stents and slow considerably for ICDs. Further, we do not see new treatment areas, such as peripheral vascular disease, atrial fibrillation, or neurostimulation driving a return to historical top-line growth of 15-20%, or even double digits, in the near term.

• ICD expectations still too high. We estimate that the number of patients accessible for primary prevention for ICDs is 15% smaller than is widely believed. Women, minorities, and patients not under the care of cardiologists are not likely to receive devices, and companies will have a difficult time accelerating referrals for treatment. We forecast 2005-10 U.S. and global market growth at 3% and 5%, respectively, compared with 6% and 8% for consensus.

• Companies face difficult marketing challenges to reinvigorate growth. Our view of the structure of the heart failure population implies that the companies will need to market to a 16-160x larger and less accessible group of physicians than they have reached before and they will need to deliver a message of insurance, not acute care, like the balance of their therapies.

• Valuation low for a reason. While the sector typically trades at a 50% premium to the P/FE of the S&P 500, it now is near historical lows at a 31% premium. Given the sector’s challenges to growth, we anticipate the sector to remain at a relatively low 25% premium for the next 6-12 months as sales and earnings expectations continue to adjust downward.

• We expect divergent share price performance within the group:

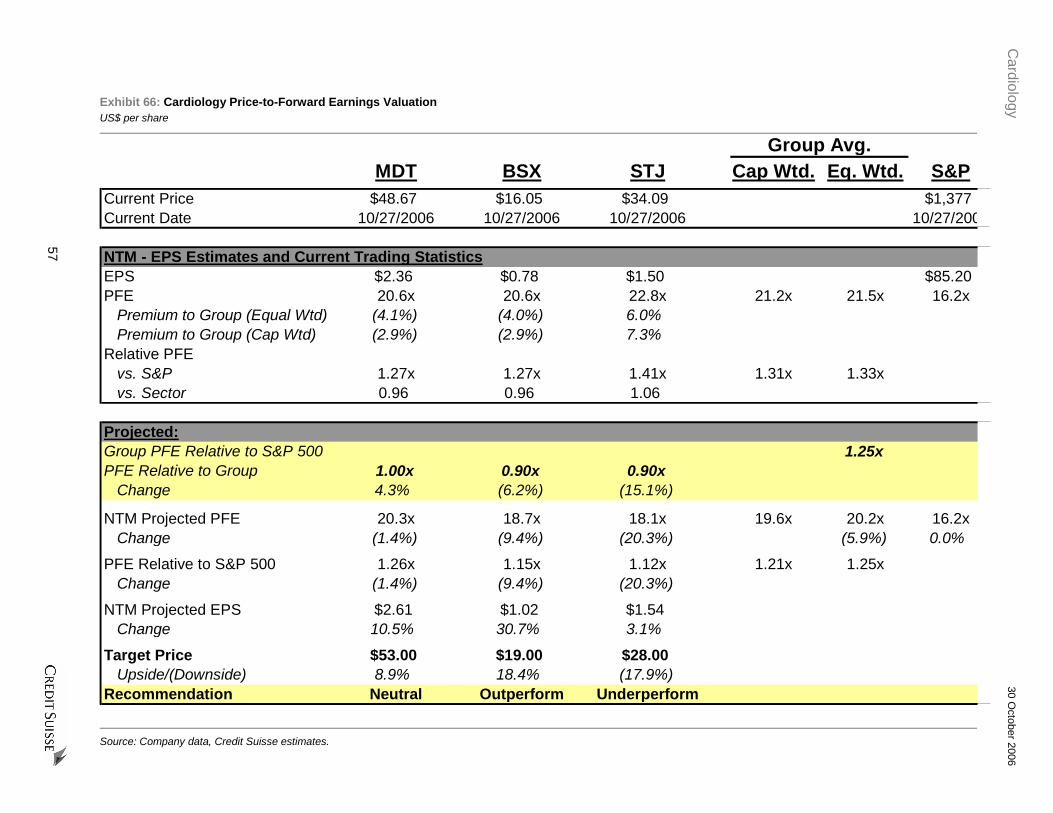

Boston Scientific—Outperform, target: $19 (19% upside). We see a favorable risk/reward trade-off, with valuation reflecting a severe scenario for Boston Scientific’s ICD business and the integration of Guidant.

St. Jude Medical—Underperform, target: $28 (18% downside). Expectations are based on overly optimistic ICD market growth and share forecasts, setting STJ up to miss 2008 consensus by 15-20%. We see the potential for an acquisition by a larger company, such as JNJ, as the only reason to own this stock, but an unlikely event.

Medtronic—Neutral, target: $53 (9% upside). While its valuation is attractive versus historical benchmarks, we see near-term volatility based on negative ICD earnings revisions and positive launches at its Spinal and Vascular businesses.

IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS AND INFORMATION ON TRADE ALERTS AND ANALYST MODEL PORTFOLIOS ARE IN THE DISCLOSURE APPENDIX. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Customers of Credit Suisse in the United States can receive independent, third party research on the company or companies covered in this report, at no cost to them, where such research is available. Customers can access this independent research at www.credit-suisse.com/ir or call 1 877 291 2683 or email [email protected] to request a copy of this research.

research team

Marshall Gordon Research Analyst 212 325 5210 [email protected]

Thijs Spoor Research Analyst 212 538 8045 [email protected]

Rodny Nacier Research Analyst 212 538 8046 [email protected]

Cardiology 30 October 2006

2

Table of Contents

Executive Summary ..........................................................................................................4 The Goldilocks Era of Cardiology Is Past......................................................................4 Growth Rates Will Not Be Robust Through 2010..........................................................5

Cardiac Rhythm Management—No Return to Robust Growth.........................................8 We Forecast 5% Annual CRM Market Growth..............................................................9 Heart Failure Epidemiology Implies Smaller Available Market .....................................9 Primary Prevention Penetration Should Peak at 65-70% ...........................................10

Total Heart Failure Patient Numbers Are Reasonable ...................................................12 Coronary Disease Survival Means More Heart Failure...............................................12 Heart Failure in the United States—5 Million Symptomatic Individuals ......................14 The Faint of Heart—1.3 Million People with Low Ejection Fraction ............................15

Fewer Heart Failure Patients Are Accessible .................................................................16 Market Estimation Approach Different, but Trying to Measure the Same Variables...16 Women Likely to Get Less Cardiac Care Than Men...................................................18 Almost Half of Heart Failure Patients Are Not Cared for by Cardiologists ..................20 African-American Patients Also Get Less Cardiac Care.............................................26

Natural Limits to the Adoption of Therapies....................................................................29 Only Two-Thirds of Heart Failure Patients Get Ejection Fraction Measurements ......29 Optimal Medical Therapy for Heart Failure Peaks at 75%..........................................30 ICD Use for Secondary Prevention Remains at 60%..................................................31

ICD Growth Will Be Harder to Drive................................................................................32 Changing Medical Biases Will Take a Long Time.......................................................32 Insurance Is More Difficult to Sell Than Treatment .....................................................32 New Patients Mean Marketing to New Physicians......................................................33

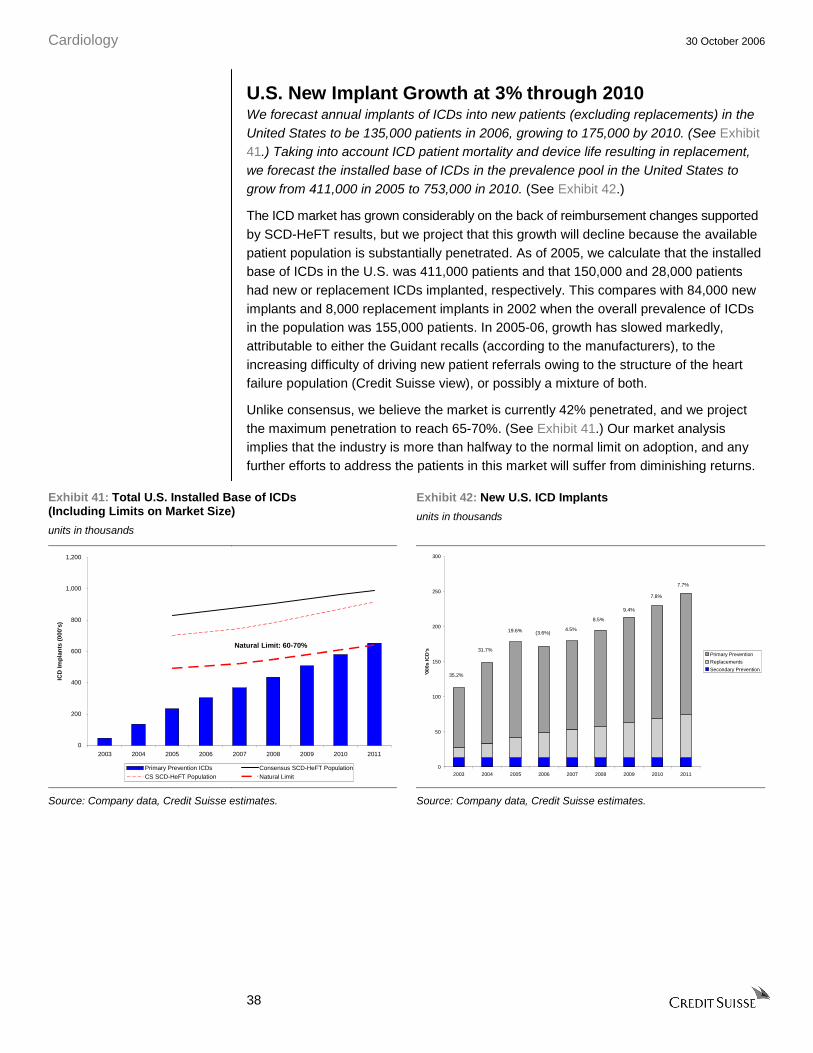

Credit Suisse Global CRM Market Forecast...................................................................36 U.S. New Implant Growth at 3% through 2010 ...........................................................38 U.S. Unit Price Erosion to Continue at 1-2%—Innovation Will Not Keep ASP Level .39 U.S. ICD Revenue to Grow at 6.6% through 2010......................................................40 U.S. Market Share Moves Slowly Back to Pre-Recall Equilibrium..............................41 RoW Market Smaller, but Growing Faster ..................................................................42

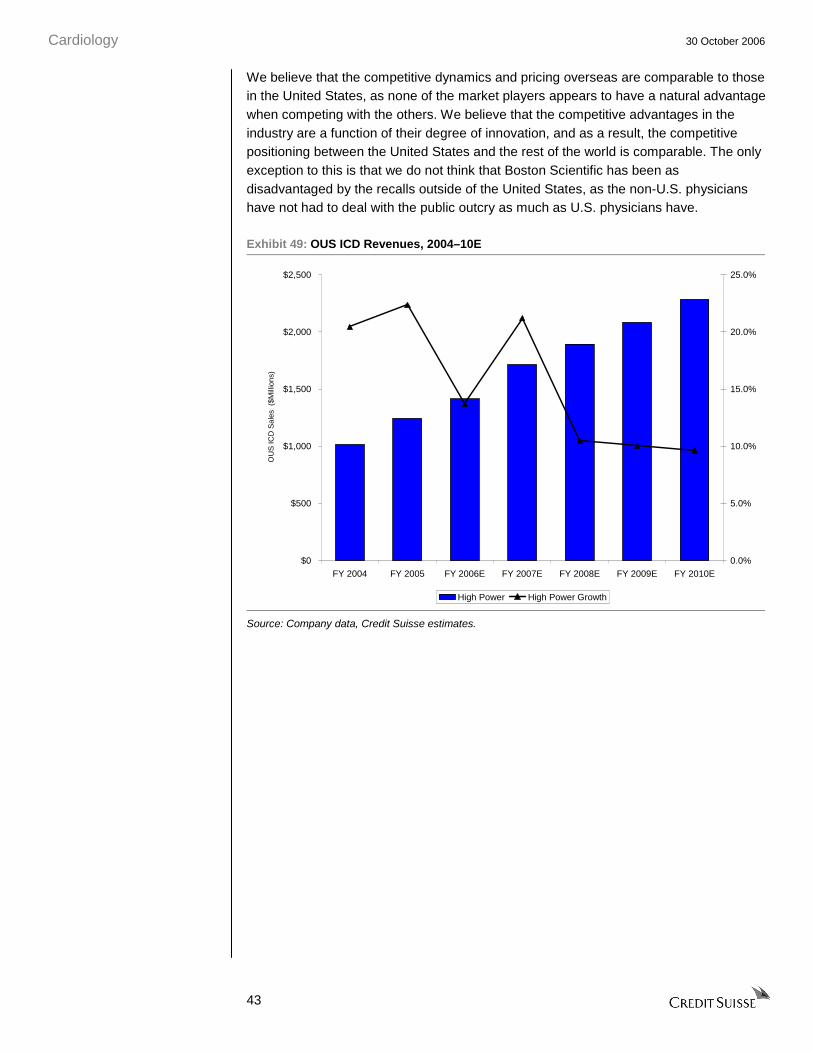

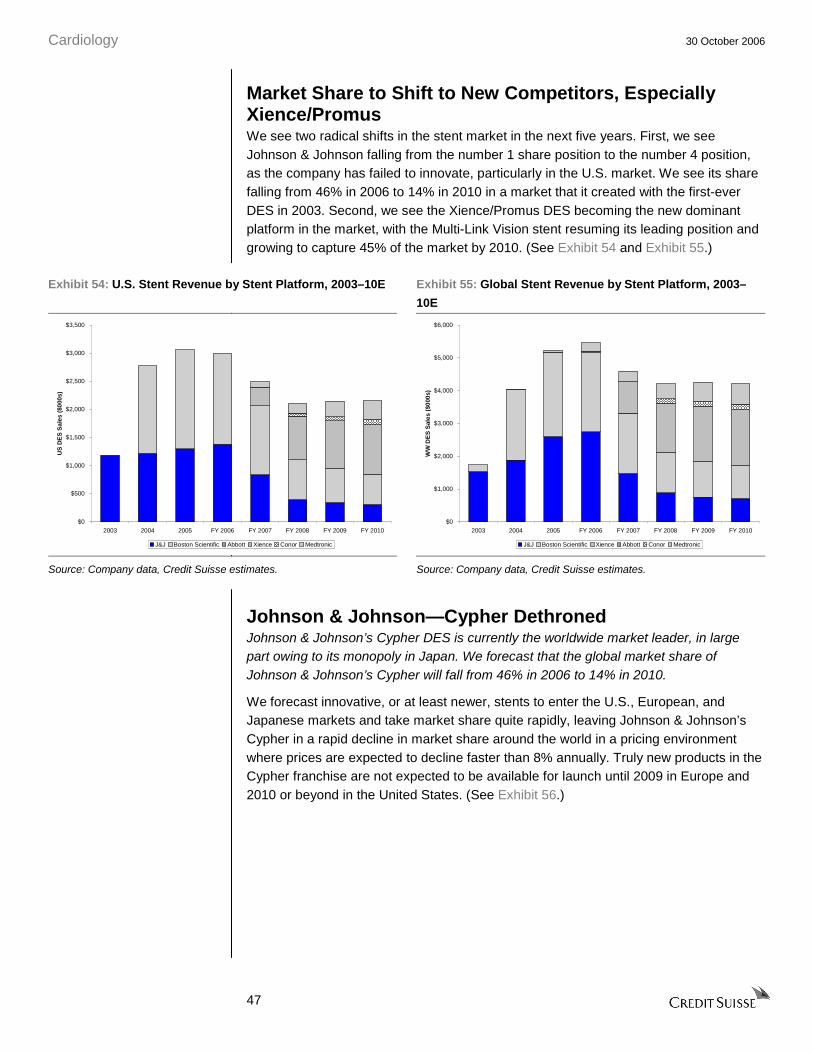

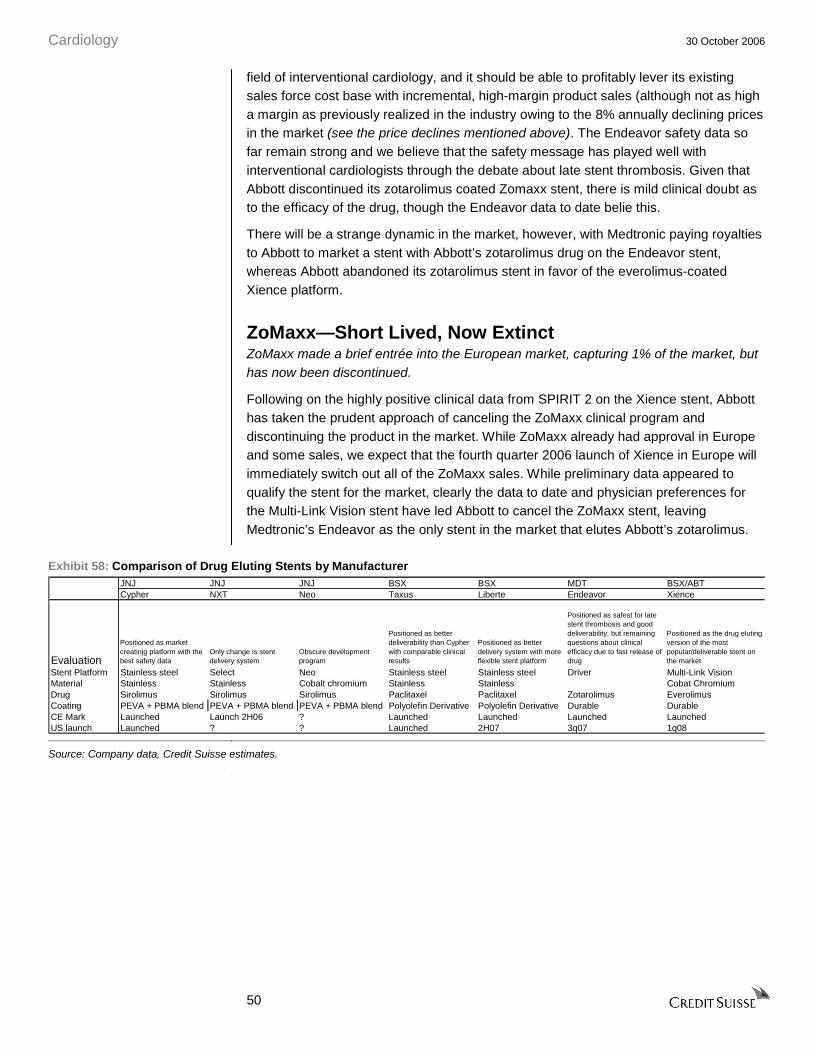

Stent Market Also at Maturity..........................................................................................44 Worldwide Unit Demand Growth Will Slow .................................................................45 Pricing Erosion Should Intensify with Competition......................................................46 Market Share to Shift to New Competitors, Especially Xience/Promus ......................47 Johnson & Johnson—Cypher Dethroned....................................................................47 Boston Scientific-Promus’es to Be a Credible Number 2............................................48 Abbott-Xience—A New Market Leader Emerging.......................................................49 Medtronic Endeavors to Do Well.................................................................................49 ZoMaxx—Short Lived, Now Extinct.............................................................................50

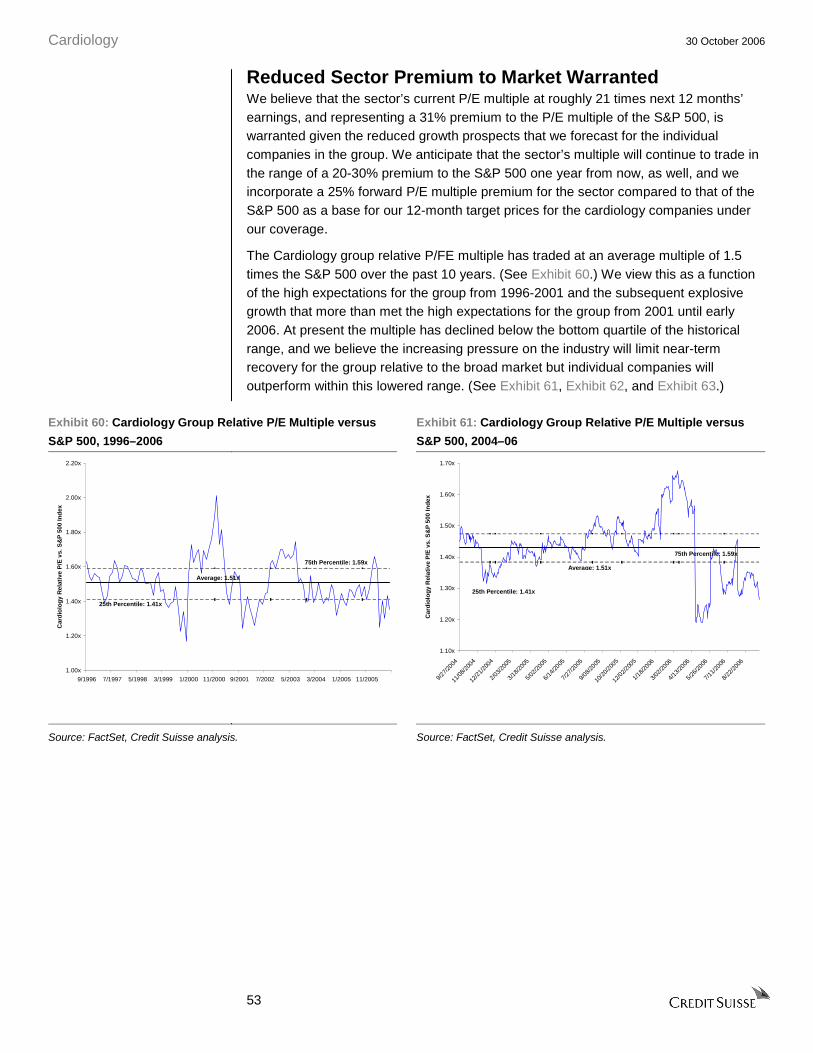

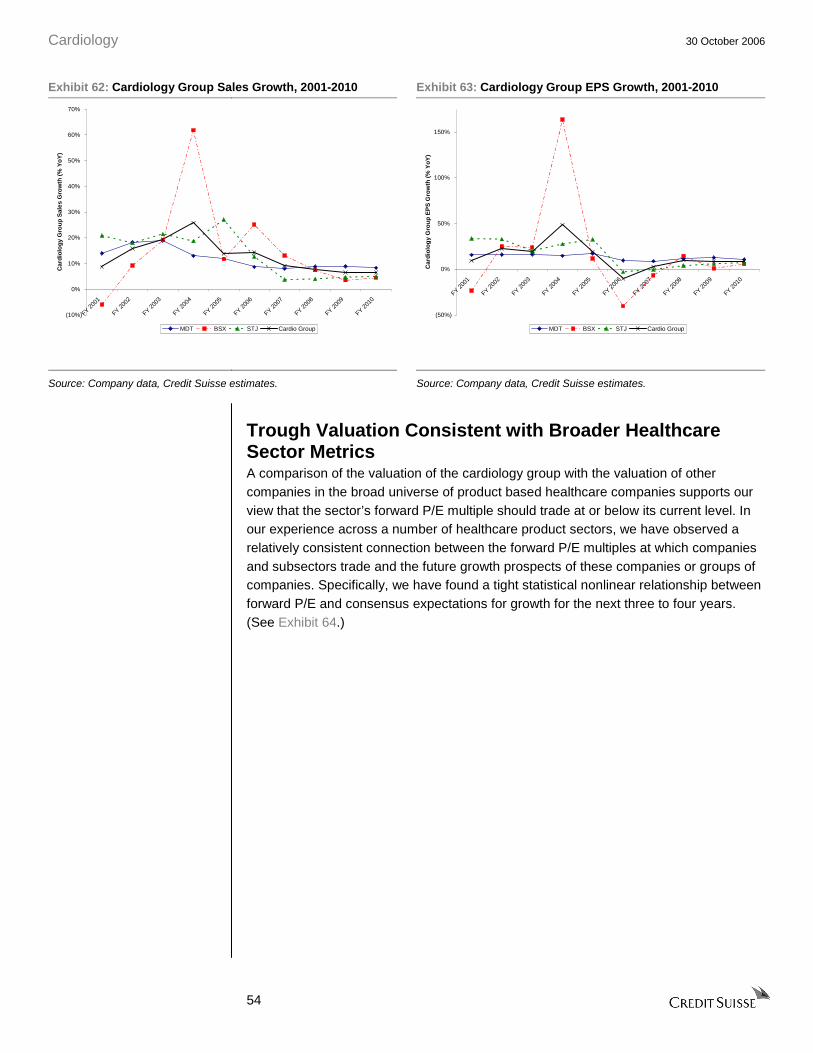

Sector Should Remain at Historical Low Valuation ........................................................52 Forward Price-to-Earnings (P/E) Valuation Methodology ...........................................52 Reduced Sector Premium to Market Warranted .........................................................53

Cardiology 30 October 2006

3

Trough Valuation Consistent with Broader Healthcare Sector Metrics .......................54 HOLT Valuation Suggests Further Downside .............................................................55

Cardiology 30 October 2006

4

Executive Summary We are initiating coverage of the Cardiology sector of Medical Supplies & Devices, which includes Medtronic, Boston Scientific and St. Jude Medical, with a sector Underweight stance. Based on our in-depth analysis of the epidemiology of heart failure and its relationship to the market for implantable cardioverter defibrillators (ICDs), we believe that the core markets for devices to treat cardiac conditions, especially ICDs, are more mature than appreciated by investors. We anticipate that there will be additional downward sales and earnings revisions. Therefore, despite the sector trading near the bottom of its historical multiple relative to the S&P 500 at only a 31% premium, we see limited stock appreciation potential and substantial continuing volatility for the group as a whole over the next 6-12 months.

We think, however, that different degrees of optimism and pessimism are reflected in the share prices of the individual companies that make up the sector. We see Boston Scientific discounting a very severe scenario, allowing us to rate it Outperform, albeit on a relative basis to its peers. St. Jude, on the other hand, reflects optimism about market size and share, unjustified in our opinion, and we rate it Underperform. Finally, Medtronic, the largest cardiology company, needs market growth to meet expectations, and we rate it Neutral, with a negative bias until expectations adjust downward.

The Goldilocks Era of Cardiology Is Past The practice of cardiology has been transformed since 2000 through the rapid adoption of new interventional medical technologies—the drug-eluting stent (DES) and the ICD. Following the launch of the Cypher DES in 2003, the interventional cardiology community worldwide quickly embraced the use of DES to enhance the outcome of balloon angioplasty and stenting, increasing the potential stent market to two to three times its original size on an absolute dollar basis. In electrophysiology, the MADIT II and, more important, the Sudden Cardiac Death in Heart Failure Trial (SCD-HeFT) paved the way for reimbursement and broad use of ICDs to prevent Sudden Cardiac Death (SCD) in patients who were at risk for such events but had not yet experienced one. Not only did these innovative technologies materially improve health outcomes, but they greatly benefited the manufacturers of these devices. From 2001-05, sales by the leading cardiology device companies—Medtronic, Boston Scientific, Guidant, St. Jude Medical, and Johnson & Johnson’s Cordis Division—doubled (see Exhibit 1), catalyzing strong outperformance of the shares of these companies. (See Exhibit 2.)

Cardiology 30 October 2006

5

Exhibit 1: Cardiology Company Revenue, 2001–10

$US in millions

Exhibit 2: Cardiology Company Stock Price Performance,

2000–06 Year to Date

$35,294

$28,023

$14,417

18%

23%

20%

12%

4%4%

5% 5% 5%

$0

$10,000

$20,000

$30,000

$40,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Co

re C

ard

iolo

gy

Ind

ust

ry S

ales

($m

m)

0%

5%

10%

15%

20%

25%

Yo

Y G

row

th R

ate (%)

Core Cardiology Industry Sales ($mm) YoY Growth Rate (%)

185

225

67

99

0

50

100

150

200

250

2000 2001 2002 2003 2004 2005 2006

Sto

ck P

rice

Per

form

ance

(I

ndex

ed 2

000=

100)

Core Cardiology - Equal Weighted S&P 500 Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Growth Rates Will Not Be Robust through 2010 We believe that the market for medical devices to treat cardiovascular disease has reached a period of maturity, more so than is reflected in today’s share prices of the core cardiology companies. For the DES market, there appears to be a broad consensus among investors around the weak prospects for the stent business. We agree with the majority view that the global market will be flat to declining and that new competitors, such as Abbott and Medtronic, will capture share and erode prices.

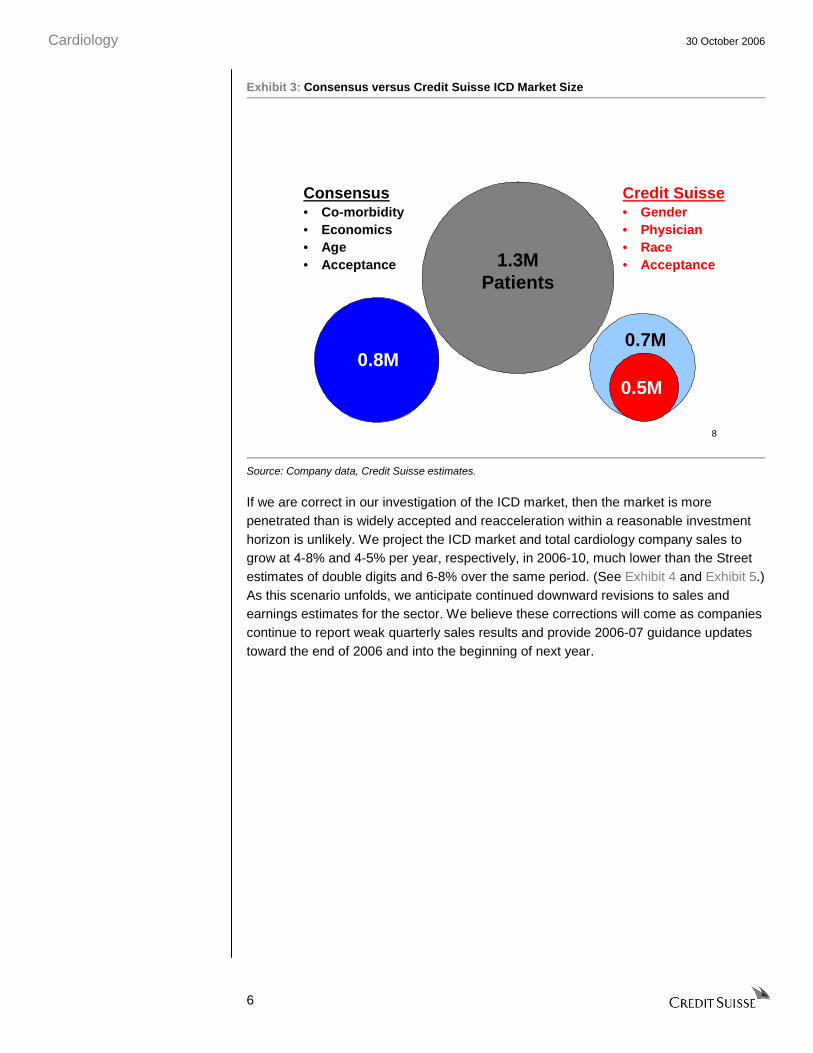

There is controversy, however, over the trajectory of the U.S. and global ICD market. The U.S. market has slowed from 15-20% growth in 2005 to 5% contraction in the most recent quarter, catalyzing 30-40% declines in the stocks in the sector thus far in 2006. Our analysis of the U.S. ICD market, which accounted for over 75% of the global market in 2005, suggests that it will not return to robust growth. Our view stands in contrast to what the companies and many investors think at the present time. We believe that the patient pool for the primary prevention of SCD is 15% smaller than previously assumed because major cardiology companies will have difficulty accessing women, minorities, and the patients under the care of noncardiologists; this group makes up a significant proportion of the pool of potential patients. (See Exhibit 3.) Further, getting device therapy to these patients requires overcoming long-standing medical practice biases and building expensive sales capabilities that the companies currently do not have.

Cardiology 30 October 2006

6

Exhibit 3: Consensus versus Credit Suisse ICD Market Size

8

1.3MPatients

0.8M

Consensus• Co-morbidity• Economics• Age• Acceptance

0.7M

0.5M

Credit Suisse• Gender• Physician• Race• Acceptance

Source: Company data, Credit Suisse estimates.

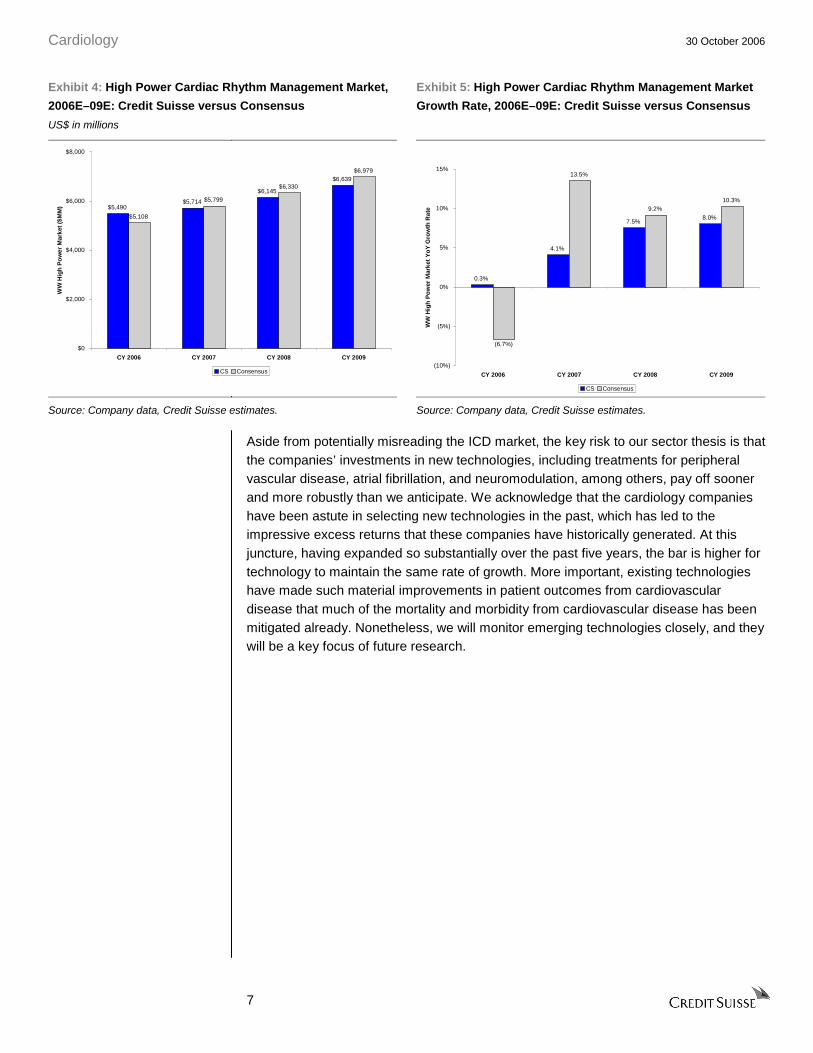

If we are correct in our investigation of the ICD market, then the market is more penetrated than is widely accepted and reacceleration within a reasonable investment horizon is unlikely. We project the ICD market and total cardiology company sales to grow at 4-8% and 4-5% per year, respectively, in 2006-10, much lower than the Street estimates of double digits and 6-8% over the same period. (See Exhibit 4 and Exhibit 5.) As this scenario unfolds, we anticipate continued downward revisions to sales and earnings estimates for the sector. We believe these corrections will come as companies continue to report weak quarterly sales results and provide 2006-07 guidance updates toward the end of 2006 and into the beginning of next year.

Cardiology 30 October 2006

7

Exhibit 4: High Power Cardiac Rhythm Management Market,

2006E–09E: Credit Suisse versus Consensus

US$ in millions

Exhibit 5: High Power Cardiac Rhythm Management Market

Growth Rate, 2006E–09E: Credit Suisse versus Consensus

$5,490$5,714

$6,145

$6,639

$5,108

$5,799

$6,330

$6,979

$0

$2,000

$4,000

$6,000

$8,000

CY 2006 CY 2007 CY 2008 CY 2009

WW

Hig

h P

ow

er M

arke

t ($

MM

)

CS Consensus

0.3%

4.1%

7.5%8.0%

13.5%

9.2%10.3%

(6.7%)

(10%)

(5%)

0%

5%

10%

15%

CY 2006 CY 2007 CY 2008 CY 2009

WW

Hig

h P

ow

er M

arke

t Y

oY

Gro

wth

Rat

e

CS Consensus

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Aside from potentially misreading the ICD market, the key risk to our sector thesis is that the companies’ investments in new technologies, including treatments for peripheral vascular disease, atrial fibrillation, and neuromodulation, among others, pay off sooner and more robustly than we anticipate. We acknowledge that the cardiology companies have been astute in selecting new technologies in the past, which has led to the impressive excess returns that these companies have historically generated. At this juncture, having expanded so substantially over the past five years, the bar is higher for technology to maintain the same rate of growth. More important, existing technologies have made such material improvements in patient outcomes from cardiovascular disease that much of the mortality and morbidity from cardiovascular disease has been mitigated already. Nonetheless, we will monitor emerging technologies closely, and they will be a key focus of future research.

Cardiology 30 October 2006

8

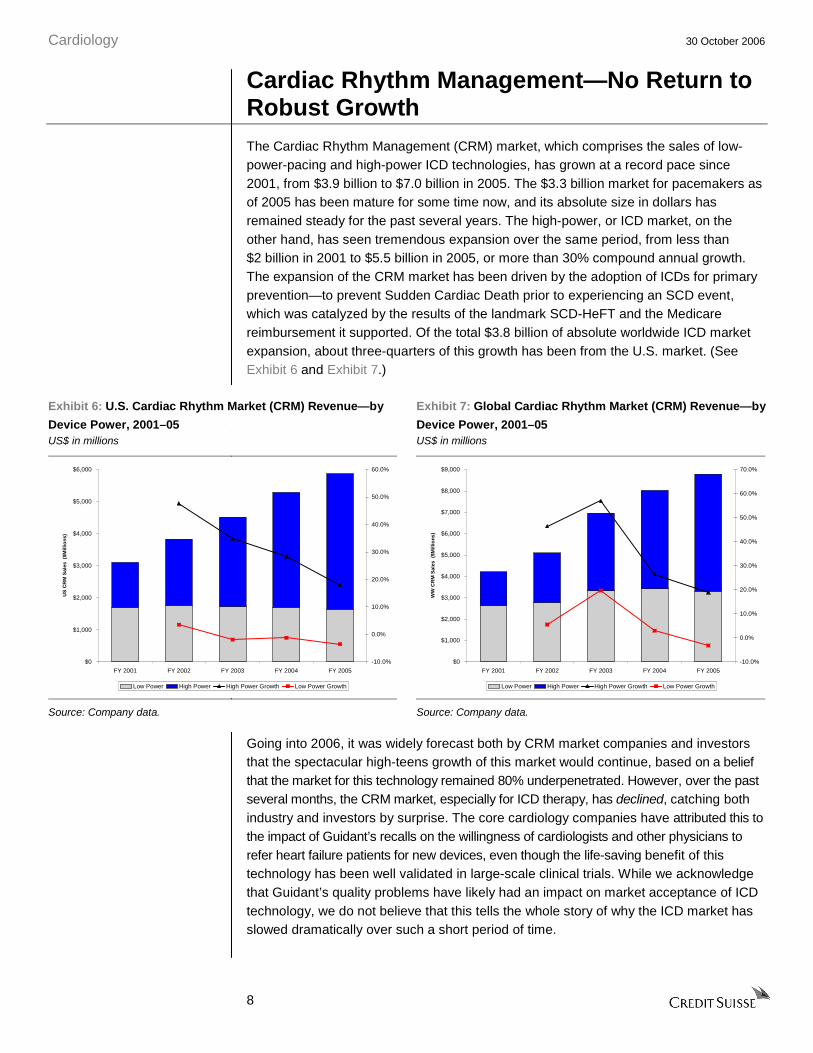

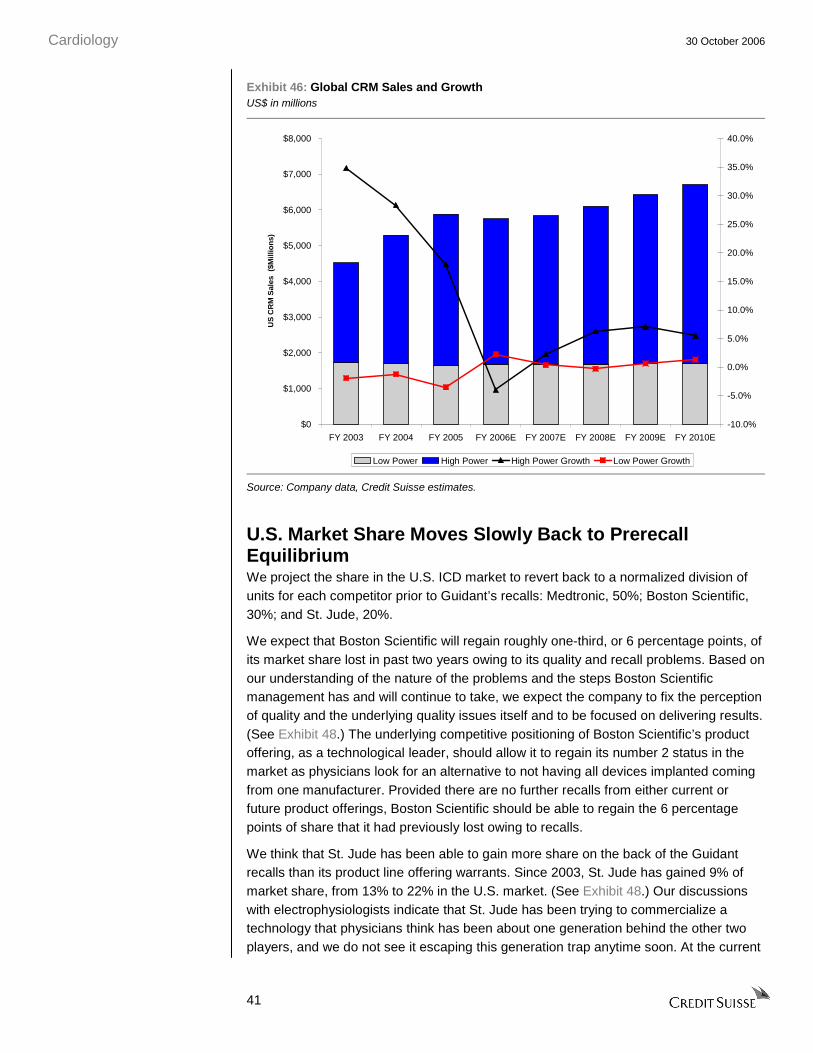

Cardiac Rhythm Management—No Return to Robust Growth The Cardiac Rhythm Management (CRM) market, which comprises the sales of low-power-pacing and high-power ICD technologies, has grown at a record pace since 2001, from $3.9 billion to $7.0 billion in 2005. The $3.3 billion market for pacemakers as of 2005 has been mature for some time now, and its absolute size in dollars has remained steady for the past several years. The high-power, or ICD market, on the other hand, has seen tremendous expansion over the same period, from less than $2 billion in 2001 to $5.5 billion in 2005, or more than 30% compound annual growth. The expansion of the CRM market has been driven by the adoption of ICDs for primary prevention—to prevent Sudden Cardiac Death prior to experiencing an SCD event, which was catalyzed by the results of the landmark SCD-HeFT and the Medicare reimbursement it supported. Of the total $3.8 billion of absolute worldwide ICD market expansion, about three-quarters of this growth has been from the U.S. market. (See Exhibit 6 and Exhibit 7.)

Exhibit 6: U.S. Cardiac Rhythm Market (CRM) Revenue—by

Device Power, 2001–05 US$ in millions

Exhibit 7: Global Cardiac Rhythm Market (CRM) Revenue—by

Device Power, 2001–05 US$ in millions

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

FY 2001 FY 2002 FY 2003 FY 2004 FY 2005

US

CR

M S

ales

($M

illio

ns)

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Low Power High Power High Power Growth Low Power Growth

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

FY 2001 FY 2002 FY 2003 FY 2004 FY 2005

WW

CR

M S

ales

($M

illio

ns)

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Low Power High Power High Power Growth Low Power Growth

Source: Company data. Source: Company data.

Going into 2006, it was widely forecast both by CRM market companies and investors that the spectacular high-teens growth of this market would continue, based on a belief that the market for this technology remained 80% underpenetrated. However, over the past several months, the CRM market, especially for ICD therapy, has declined, catching both industry and investors by surprise. The core cardiology companies have attributed this to the impact of Guidant’s recalls on the willingness of cardiologists and other physicians to refer heart failure patients for new devices, even though the life-saving benefit of this technology has been well validated in large-scale clinical trials. While we acknowledge that Guidant’s quality problems have likely had an impact on market acceptance of ICD technology, we do not believe that this tells the whole story of why the ICD market has slowed dramatically over such a short period of time.

Cardiology 30 October 2006

9

We Forecast 5% Annual CRM Market Growth We do not see the market reaccelerating back to its historical growth rate, but rather to 2-7% annually, or a compound annual growth rate of 5% through 2010, slightly above the rate of expansion of the incidence of heart failure in the population. (See Exhibit 8 and Exhibit 9.) Our market forecast is predicated on our analysis of who makes up the population of heart failure patients and which physicians provide care to these individuals. We believe that the ICD primary prevention market, which accounts for the majority of the CRM growth opportunity, is approximately 15% smaller than does consensus. We also see saturation of the market earlier than the majority of investors for two reasons: (1) We estimate that primary prevention market penetration is not 35%, but rather 42%, based on our smaller assessment of market size. (2) We forecast adoption of ICD technology reach a ceiling at 65-70% rather than the unstated assumption from the industry that 100% of eligible patients should receive a device.

Exhibit 8: U.S. Cardiac Rhythm Management Revenue, 2003–10E US$ in millions

Exhibit 9: Global Cardiac Rhythm Management Revenue, 2003–10E US$ in millions

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

FY 2003 FY 2004 FY 2005 FY 2006E FY 2007E FY 2008E FY 2009E FY 2010E

US

CR

M S

ales

($0

00s)

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Low Power High Power High Power Growth Low Power Growth

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

FY 2003 FY 2004 FY 2005 FY 2006E FY 2007E FY 2008E FY 2009E FY 2010E

WW

CR

M S

ales

($0

00s)

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Low Power High Power High Power Growth Low Power Growth

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Heart Failure Epidemiology Implies Smaller Available Market We believe that consensus assumptions about ICD primary prevention market size are overestimated, and as a result that the degree of market penetration is overestimated. Many have estimated the size of the primary prevention patient pool by examining the total population of heart failure patients and excluding people who are too sick or cannot afford a device. From a base of 1.3 million heart-failure patients with a weak heart (defined as an ejection fraction less than 35%), these reductions, 20% for comorbidity and 15% for economics, or 35% in total, imply a current pool of 850,000 patients for whom an ICD is indicated. (See Exhibit 10.) Given a base of slightly more than 400,000 implanted devices, of which 180,000 are implanted in secondary prevention patients, consensus analysis implies 35% market penetration. In our opinion, initial results from these catch-all reductions in the overall patient pool have not been well validated by independent data sources.

Cardiology 30 October 2006

10

Exhibit 10: Consensus View of Available ICD Primary

Prevention Population

patients in 000s

Exhibit 11: Credit Suisse View of Available ICD Primary

Prevention Population

patients in 000s

854

1,313

0

500

1,000

1,500

Primary PreventionPopulation

Co-morbidity Economics Total

Pri

mar

y P

reve

nti

on

Pat

ien

t P

op

ula

tio

n (

000'

s)

-35%

723

1,313

0

500

1,000

1,500

Primary PreventionPopulation

Women Treating Physician Race Total

Pri

mar

y P

reve

nti

on

Pat

ien

t P

op

ula

tion

(00

0's)

-45%

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

As an alternative to the traditional method of looking at the market, we used demographic variables and treating physicians to examine the size of the available pool of primary prevention patients. We use specific estimates from published data sources on heart failure epidemiology and treatment, as well as on invasive and pharmacologic cardiology treatments more broadly, to support our market estimates. We believe the indicated ICD primary prevention population is reduced from 1.3 million to 723,000 patients. (See Exhibit 11.) Our exclusions imply the U.S. primary prevention ICD market appears to be 42% penetrated in 2006, rather than 35% as believed by consensus.

Specifically, we believe that three variables are good proxy for the exclusions from the primary prevention pool:

• Gender. Women are 60% less likely to receive an ICD than men, and they make up 55% of the heart failure population.

• Treating physician. Patients who are not under the care of a cardiologist are 50% less likely to receive an ICD than patients who are, and 30-40% of heart failure patients never even receive a cardiology consult.

• Race. African-Americans are 30% less likely to receive an ICD than whites, and they account for 15% of the heart failure population.

Primary Prevention Penetration Should Peak at 65-70% We forecast that the adoption of ICD technology among indicated patients will reach only 65-70%, whereas consensus appears to accept that eventually all indicated patients will receive devices. The adoption of invasive medical technology, even those that are life saving, is rarely 100%. In the case of ICDs, we see three close proxies: the adoption of testing for ejection fraction; the adoption of optimal pharmaceutical therapy for heart failure; and the penetration of ICDs in the secondary prevention population. Levels of penetration for all of these similar interventions reached a plateau at around 65-70%, and we do not believe that primary prevention ICD therapy will differ materially.

Cardiology 30 October 2006

11

Our Key ICD Market Assumptions are as follows:

• Growth of incident heart disease population is 3-4%, in-line with age and population growth.

United States

• The primary prevention market is 723,000 total patients, of which 300,000, or 42%, have received devices. Our estimate of market size is 15% smaller than that of CRM consensus and the companies.

• The secondary prevention market is estimated at 300,000 total patients, of which 180,000, or 60%, receive devices. Given the number of years ICD technology has been available, the penetration in this market has reached its peak.

• Growth in patients being referred in to electrophysiologists recovers, but more in-line with the growth in the prevalence of the disease.

• Peak penetration of eligible and available patients will be 65-70%; consistent with the adoption of pharmaceuticals in heart failure patients and ICD therapy in the primary prevention cohort.

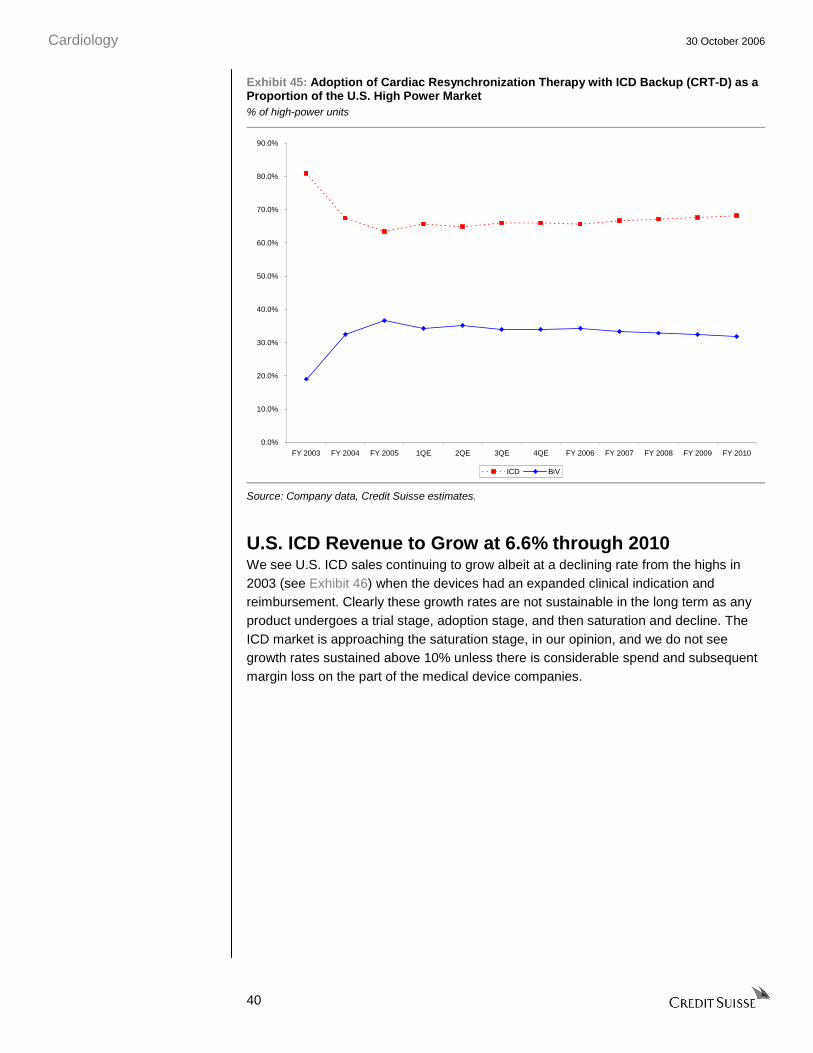

• We forecast that 60,000 CRT-D devices will be implanted in 2006, representing 34% of the secondary prevention pool. The proportion of patients receiving CRT-D devices will remain at around one-third of high-power patients.

• Pricing declines of 1-2% annually will more than offset market growth in unit demand.

Europe/RoW

• Growth in patients being referred in to electrophysiologists is steadily increasing with the change in demographics as well as a continued acceptance of the technologies as the national healthcare systems increase their willingness and correspondingly their budgets to pay for the technology.

• Prices in-line with the United States, mild decline on the same device price with some mix shift to new devices and more expensive BiV pacing to offset this.

Cardiology 30 October 2006

12

Total Heart Failure Patient Numbers Are Reasonable We agree with the market’s view of the number of total, symptomatic, and weak heart (low ejection fraction) heart failure patients. It is widely accepted, based on reports from a number of reliable medical and disease specific sources, that there are approximately 65-70 million individuals who suffer from some stage of heart failure in the United States. Further, we accept standard proportions of patients who are symptomatic and in need of appropriate medical care, largely Stage C heart failure as defined by the American Heart Association. Therefore, we believe that there are approximately 5 million individuals with symptomatic heart failure in the United States. Finally, we believe of the 5 million people with symptomatic heart failure, 1.3 million, or 26%, have weak hearts, defined as having an ejection fraction—the standard measure of cardiac output—of less than 35%. This group of individuals represents the core market for primary prevention ICD therapy as this EF threshold is one of the key qualifying criteria as defined in MADIT-2 and SCD-HeFT for suitability to receive a device and as such is part of the required patient workup to qualify for reimbursement.

Coronary Disease Survival Means More Heart Failure We forecast the growth rate of heart failure at 3%, in-line with the growth rate of ischemic heart disease. Patients with coronary artery disease (CAD) are developing congestive heart failure (CHF) as they survive the circulatory disorder, and they are now dying from complications secondary to CHF. The result of better interventions for CAD through the rapid innovations and the acceptance of balloon angioplasty and the drug eluting stent revolution mean that more and more patients are now able to survive blockages of the coronary arteries that 20 years ago would have been fatal. Heart failure patients, those who have a stretching of the cardiac muscle and a decrease in cardiac output, remain asymptomatic until the heart starts a process known as remodeling. This stretching causes scarring and trauma and is thought to lead to a degradation in the conductive pathways of the heart. Remodeling gives rise to the risk of SCD, which occurs when the electrical system of the heart shuts down, stopping it from beating. The growing epidemic in the developed world has now become the onset of heart failure as exacerbated by hypertension and prior myocardial ischemia. (See Exhibit 13.)

Cardiology 30 October 2006

13

Exhibit 12: Evolution of Heart Disease and the Corresponding Medical Devices

Congenital Heart Disease

Coronary Artery Disease CAD

Acute Myocardial Infarction AMI

Congestive Heart Failure

CHF

Sudden CardiacDeath SCD

Blood Chemistry

High Blood Pressure

Stable Angina

Stents

ICD’s

Congenital Heart Disease

Coronary Artery Disease CAD

Acute Myocardial Infarction AMI

Congestive Heart Failure

CHF

Sudden CardiacDeath SCD

Blood Chemistry

High Blood Pressure

Stable Angina

Stents

ICD’s

Source: Company data, Credit Suisse estimates.

Exhibit 13: Mortality in Cardiology

150

200

250

300

350

‘80 ‘85 ‘90 ‘95 ‘0020

30

40

50

60Deaths due to CHF

Deaths due to AMI

AMI Deaths (000) CHF Deaths (000)

150

200

250

300

350

‘80 ‘85 ‘90 ‘95 ‘0020

30

40

50

60Deaths due to CHF

Deaths due to AMI

AMI Deaths (000) CHF Deaths (000)

150

200

250

300

350

‘80 ‘85 ‘90 ‘95 ‘0020

30

40

50

60Deaths due to CHF

Deaths due to AMI

AMI Deaths (000) CHF Deaths (000)

Source: American Heart Association, Credit Suisse estimates.

Cardiology 30 October 2006

14

Heart Failure in the United States—5 Million Symptomatic Individuals Heart failure is a burgeoning global epidemic with a particularly high burden in developed nations where patients are surviving ischemic heart disease. The American Heart Association currently estimates that 46 million people have Stage A “heart failure.” These are patients who are at high risk of disease, but do not have any structural heart disease or symptoms of heart failure. These patients typically have several comorbidities such as hypertension, CAD, and diabetes, among others. Owing to the dynamic nature of the disease (see Exhibit 12), we believe that this population will continue to grow at 3%, in-line with the growth of the aging population and the number of CAD survivors becoming heart failure patients.

Exhibit 14: American Heart Association Classification

Stage A

At high risk for heart failure but

without structural heart disease or symptoms of HF

e.g. Patients with: - hypertension

- CAD

- diabetes

or

Patients

- using cardiotoxins

- with FHx CM

Structuralheart

disease

Stage B

Structural heart disease but without

symptoms of HF

e.g. Patients with: - previous MI

- LV systolic dysfunction

- asymptomatic valvular disease

Stage C

Structural heart disease with prior

or current symptoms of HF

e.g. Patients with: - known structural heart disease

- shortness of breath & fatigue, reduced exercise tolerance

Developmt

of symptoms

of HF

Stage D

Refractory HF requiring

specialised interventions

Patients who have marked symptoms at rest despite maximal medical therapy (e.g. those who are recurrently hospitalised or cannot be safely discharged from the hospital without specialised interventions)

Refractorysymptoms

of HFat rest

46M 15M 5M 25-40,000

Stage A

At high risk for heart failure but

without structural heart disease or symptoms of HF

e.g. Patients with: - hypertension

- CAD

- diabetes

or

Patients

- using cardiotoxins

- with FHx CM

Structuralheart

disease

Stage B

Structural heart disease but without

symptoms of HF

e.g. Patients with: - previous MI

- LV systolic dysfunction

- asymptomatic valvular disease

Stage C

Structural heart disease with prior

or current symptoms of HF

e.g. Patients with: - known structural heart disease

- shortness of breath & fatigue, reduced exercise tolerance

Developmt

of symptoms

of HF

Stage D

Refractory HF requiring

specialised interventions

Patients who have marked symptoms at rest despite maximal medical therapy (e.g. those who are recurrently hospitalised or cannot be safely discharged from the hospital without specialised interventions)

Refractorysymptoms

of HFat rest

46M 15M 5M 25-40,000

Source: 2004 Update, American Heart Association.

It is estimated that 5 million people in the United States have symptomatic heart failure based on the American Heart Association definition. (See Exhibit 14.) Patients with active disease, however, will present in a variety of fashions and are further classified according to various staging scales, the most widely used being the New York Heart Association (NYHA) class, which ranges from 1 (asymptomatic) to 4 (symptomatic at rest). Given the large numbers of patients involved, it is important to try and segregate the patient population further, as the treatment patterns, medical therapy, and device referral patterns all result from the initial classification of patients by the severity of their disease. Since broad stroke implantation of ICDs in this 5 million population cohort is irresponsible from the point of view of both cost effectiveness and appropriateness of treatment, landmark trials such as MADIT II and SCD-HeFT have served to limit use by identifying the patients appropriate for implantable cardioverter defibrillator therapy.

Cardiology 30 October 2006

15

The Faint of Heart—1.3 Million People with Low Ejection Fraction The 5 million Stage C heart failure patients are spread out across a clinical continuum for disease progression. One of the more prognostic techniques available to assess and stratify these patients involves the use of ejection fraction (EF) to assess the functional capacity of the heart. This clinical parameter can be assessed in a variety of ways, with the most common being via ultrasound and the more accurate being through a stress nuclear scan. The ejection fraction parameter, owing to its quantitative nature and the readily available equipment to perform the procedure, is one of the qualifying/ inclusionary criteria for patients eligible for ICD therapy. The distribution of EF scores across Stage C patients is not uniform and generally the less healthy patients on a NYHA class tend to have worse EF results. (See Exhibit 15.) We estimate the percentage breakdown in these patients according to overall assumptions of the disease burden in the published literature, and our analysis is consistent with the overall estimates of ejection fraction measurement in the CHF population discussed by the major CRM companies.

Exhibit 15: Patient Stratification by Ejection Fraction and NYHA Class

patients in 000s

C la ss I C las s 2 C la ss 3 Class4

1,5 46 1 ,8 0 3 1 ,54 6 25 8 T ota l = 5 ,15 3

0

2 0

4 0

6 0

8 0

1 00 %

E F< 35 %E F> 35 %

Source: Company data, Credit Suisse estimates.

Cardiology 30 October 2006

16

Fewer Heart Failure Patients Are Accessible At the core of our below-consensus ICD market projection is our unique look at the epidemiology of symptomatic heart failure and its treatment. Based on our review of quantitative public data, we calculate that the primary prevention ICD market is 15% smaller than is currently accepted by the industry or consensus. We arrive at our conclusion because we use alternative proxies for the exclusions from the 1.3 million symptomatic patients with weak hearts (ejection fractions below 35%). Instead of the broadly embraced 35% exclusion for patients that are too sick for or cannot afford an ICD (Exhibit 16), we examine patient gender and race and treating physician to find that 45% of patients should be excluded from the available patient pool for ICDs. (See Exhibit 17.) Therefore, we estimate that the primary prevention patient pool is approximately 720,000 patients, not the more than 850,000 estimated by the companies in the industry and The Wall Street Journal.

Exhibit 16: Consensus View of Available ICD Primary

Prevention Population

patients in 000s

Exhibit 17: Credit Suisse View of Available ICD Primary

Prevention Population

patients in 000s

854

1,313

0

500

1,000

1,500

Primary PreventionPopulation

Co-morbidity Economics Total

Pri

mar

y P

reve

nti

on

Pat

ien

t P

op

ula

tio

n (

000'

s)

-35%

723

1,313

0

500

1,000

1,500

Primary PreventionPopulation

Women Treating Physician Race Total

Pri

mar

y P

reve

nti

on

Pat

ien

t P

op

ula

tio

n (

000'

s)

-45%

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Market Estimation Approach Different, but Trying to Measure the Same Variables To evaluate the prospects for ICD sales, we are looking to quantify the group of patients for which device therapy is indicated, as well as likely to be used. As we discuss above, we accept the broader view that there are 1.3 million individuals eligible for ICDs placed for the primary prevention of SCD. We differ from consensus, however, as to how we view the exclusions for the likelihood of implantation of ICDs.

Many ICD market observers consider comorbidities, (socio)economics, age, and patient acceptance to calculate the group of patients unlikely to receive devices. However, we found a paucity of quantitative data to support the conventional wisdom that these variables excluded 35% of the total pool of eligible patients. Therefore, as an alternative, we analyzed the eligible patients along the more tangible lines of gender, race, treating physician, and geography. For these key variables, we found a substantial body of

Cardiology 30 October 2006

17

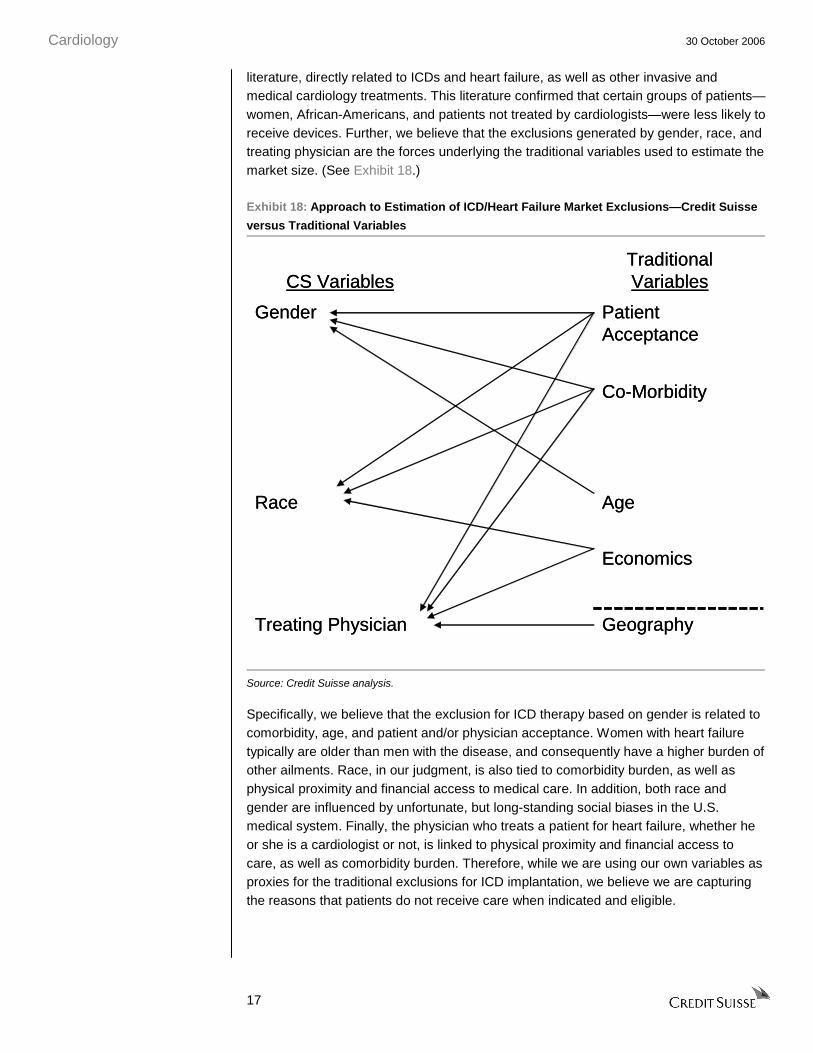

literature, directly related to ICDs and heart failure, as well as other invasive and medical cardiology treatments. This literature confirmed that certain groups of patients—women, African-Americans, and patients not treated by cardiologists—were less likely to receive devices. Further, we believe that the exclusions generated by gender, race, and treating physician are the forces underlying the traditional variables used to estimate the market size. (See Exhibit 18.)

Exhibit 18: Approach to Estimation of ICD/Heart Failure Market Exclusions—Credit Suisse

versus Traditional Variables

GeographyTreating Physician

Economics

AgeRace

Co-Morbidity

Patient Acceptance

Gender

Traditional VariablesCS Variables

GeographyTreating Physician

Economics

AgeRace

Co-Morbidity

Patient Acceptance

Gender

Traditional VariablesCS Variables

Source: Credit Suisse analysis.

Specifically, we believe that the exclusion for ICD therapy based on gender is related to comorbidity, age, and patient and/or physician acceptance. Women with heart failure typically are older than men with the disease, and consequently have a higher burden of other ailments. Race, in our judgment, is also tied to comorbidity burden, as well as physical proximity and financial access to medical care. In addition, both race and gender are influenced by unfortunate, but long-standing social biases in the U.S. medical system. Finally, the physician who treats a patient for heart failure, whether he or she is a cardiologist or not, is linked to physical proximity and financial access to care, as well as comorbidity burden. Therefore, while we are using our own variables as proxies for the traditional exclusions for ICD implantation, we believe we are capturing the reasons that patients do not receive care when indicated and eligible.

Cardiology 30 October 2006

18

Women Likely to Get Less Cardiac Care Than Men Women make up a slight majority (55%) of the patient population with symptomatic heart failure, and we estimate that, as a group, they have a 60% lower chance of receiving an ICD than comparable men. Women tend to present with heart failure later in the disease cycle (i.e., sicker) and thus their heart failure will not be the most urgent patient management need. Women, in healthcare systems around the world, also experience negative biases that affect their diagnoses and treatment patterns, and we have not seen any data that lead us to believe that this is different in the population of heart failure patients. After controlling for age, mortality and all other factors, we calculate that the exclusion for women being less likely to receive devices reduces the 1.3 million patient population eligible for ICDs by 300,000 patients.

In the healthcare system in general and in cardiology specifically, women are not managed the same way as men are. Only 20% of women consider heart disease to be their greatest health risk, yet the disease accounts for 35% of all deaths. In fact, 62% of women who die suddenly of a heart attack had no prior symptoms. It has been well documented that there are biases inherent in the healthcare system against women and how they are treated across the disease spectrum.

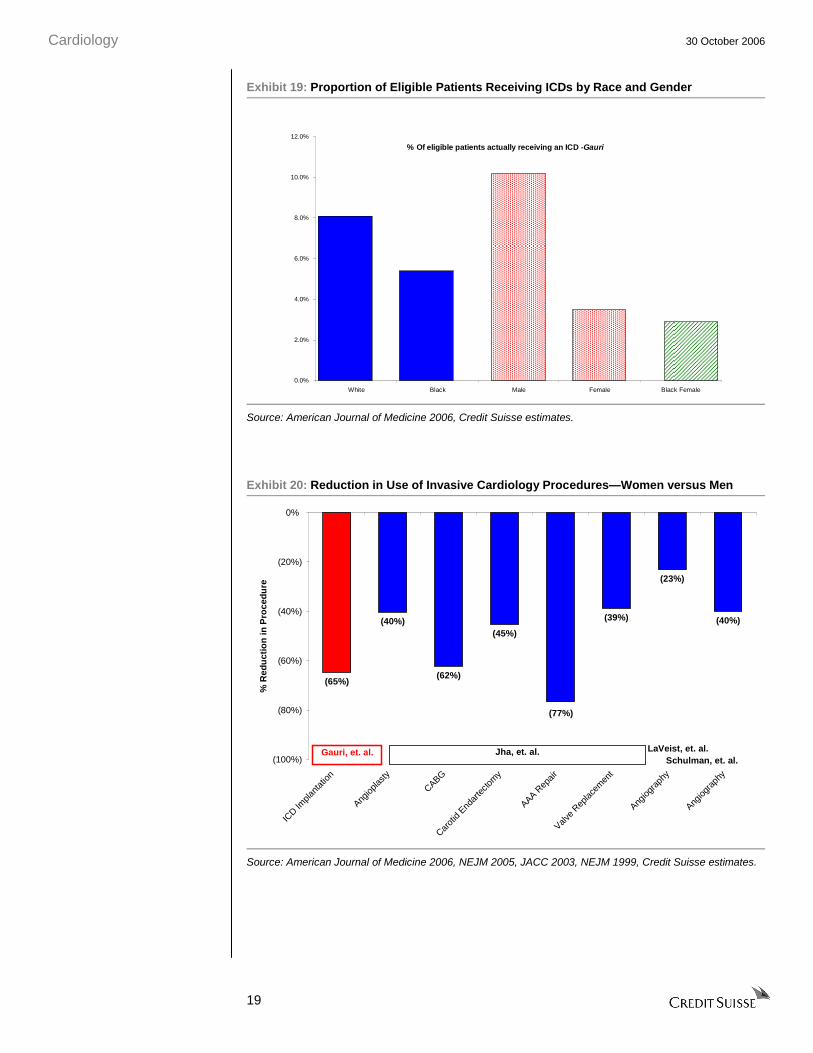

A number of large observational studies have evaluated differences in treatment patterns for common cardiac disease and procedures based on patient gender. These studies strongly suggest that, matched for other variables, women receive half to one-third of the care that men do. For ICDs, in particular, a review of CMS data (Gauri, et al., American Journal of Medicine, 2006) demonstrated that women received ICDs for the same diagnoses (ICD-9 codes) at a rate 65% less than that of men. (See Exhibit 19.) Studies of the use of other common and well-established surgical interventions for cardiac disease, such as angioplasty, coronary artery bypass graft (CABG), and valve replacement, among others, support a reduction of this magnitude in use of procedures for women as compared to men. (See Exhibit 20.)

Cardiology 30 October 2006

19

Exhibit 19: Proportion of Eligible Patients Receiving ICDs by Race and Gender

% Of eligible patients actually receiving an ICD -Gauri

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

White Black Male Female Black Female

Source: American Journal of Medicine 2006, Credit Suisse estimates.

Exhibit 20: Reduction in Use of Invasive Cardiology Procedures—Women versus Men

(65%)

(40%)

(62%)

(45%)

(39%)

(23%)

(40%)

(77%)

(100%)

(80%)

(60%)

(40%)

(20%)

0%

ICD Im

plant

ation

Angiop

lasty

CABG

Carot

id End

arte

ctom

y

AAA Rep

air

Valve

Replac

emen

t

Angiog

raph

y

Angiog

raph

y

% R

edu

ctio

n in

Pro

ced

ure

Jha, et. al.Gauri, et. al. LaVeist, et. al.Schulman, et. al.

Source: American Journal of Medicine 2006, NEJM 2005, JACC 2003, NEJM 1999, Credit Suisse estimates.

Cardiology 30 October 2006

20

In the large pools of data looking at how men and women present differently with the disease, certain factors may explain why men are treated more aggressively, as well as more often by a cardiologist. Men tend to present more frequently with ischemic conditions, which can be diagnosed on exercise or seen through related symptoms. Women, on the other hand, are more likely to present with hearts that are dilated from chronic and undertreated hypertension, which is perceived as less pressing and possibly less appropriate for preventative ICD therapy. Also, women typically present to physicians for evaluation when they are either older, later in the heart failure disease process, or both, and therefore, women tend to have greater comorbidity burdens than their male counterparts.

Finally, we acknowledge the unfortunate fact that there may be gender bias on the part of treating physicians. In one recent study (Schulman, et al., New England Journal of Medicine, 1999), male and female actors presented to physicians with identical symptoms, case histories, and risk factors, but physicians prescribed different recommendations for treatment. Women generally received less treatment, or at least less aggressive treatment, than men. To be sure, women’s hearts are different than men’s in that they are smaller, and have a more complicated vasculature, and the presentation and symptoms of cardiac disorders present differently. While the underlying social reasons that women do not receive treatment on a par with men are beyond the scope of our analysis, we believe this phenomenon has carried over to the ICD market and to the degree of acceptance of device therapy for women.

Almost Half of Heart Failure Patients Are Not Cared for by Cardiologists Not all heart failure patients receive medical attention from a cardiologist, and we believe that this affects the type of care that they ultimately receive. Heart failure is a chronic disease, and without an SCD event, the disease is characterized by a slow progression of declining cardiac function. Many heart failure patients may not perceive a need to see a cardiologist because their symptoms are being managed, rather than treating the direct failure of their heart muscle. We would contrast this to coronary artery disease, where patients present with acute symptoms that require immediate medical attention, typically from specialized interventional cardiologists.

As a result, of the 5 million individuals with symptomatic heart failure, only 20% receive the majority of their care from a cardiologist, with another 40-50% receiving a consultation from a cardiologist about their condition. Among the 1.3 million symptomatic heart failure patients with low ejection fractions, however, we estimate approximately 70% receive care from or a consultation by a cardiologist. We consider this to be one of the most significant barriers to adoption of ICDs, as the adherence to heart failure treatment guidelines, including those endorsing preventative ICD therapy based on SCD-HeFT results, are lower in the noncardiology community. Available data suggest that noncardiologists do not prescribe optimal pharmaceutical therapy and recommend fewer invasive cardiac surgical procedures. We estimate that noncardiologists are 50% less likely to recommend ICD therapy. We further calculate that the exclusion for noncardiologists being less likely to recommend device therapy reduces the 1.3 million patient population eligible for ICDs by 160,000 patients.

Cardiology 30 October 2006

21

We summarize what we estimate as the structure of the ICD eligible patient population in Exhibit 21.

Exhibit 21: Structure of the Heart Failure Market by Treating Physician

Primary CarePhysicians: 160,000Patients: 390k w/out ICD

CardiologistsPhysicians: 16,000Patients: 470k w/out ICD

Electrophysiologists(EPs)Physicians: 1,000Patients: 440k w/ICDs

Likelihood of ICD

Implantation Increases

Primary CarePhysicians: 160,000Patients: 390k w/out ICD

CardiologistsPhysicians: 16,000Patients: 470k w/out ICD

Electrophysiologists(EPs)Physicians: 1,000Patients: 440k w/ICDs

Likelihood of ICD

Implantation Increases

Source: Company data, Credit Suisse estimates.

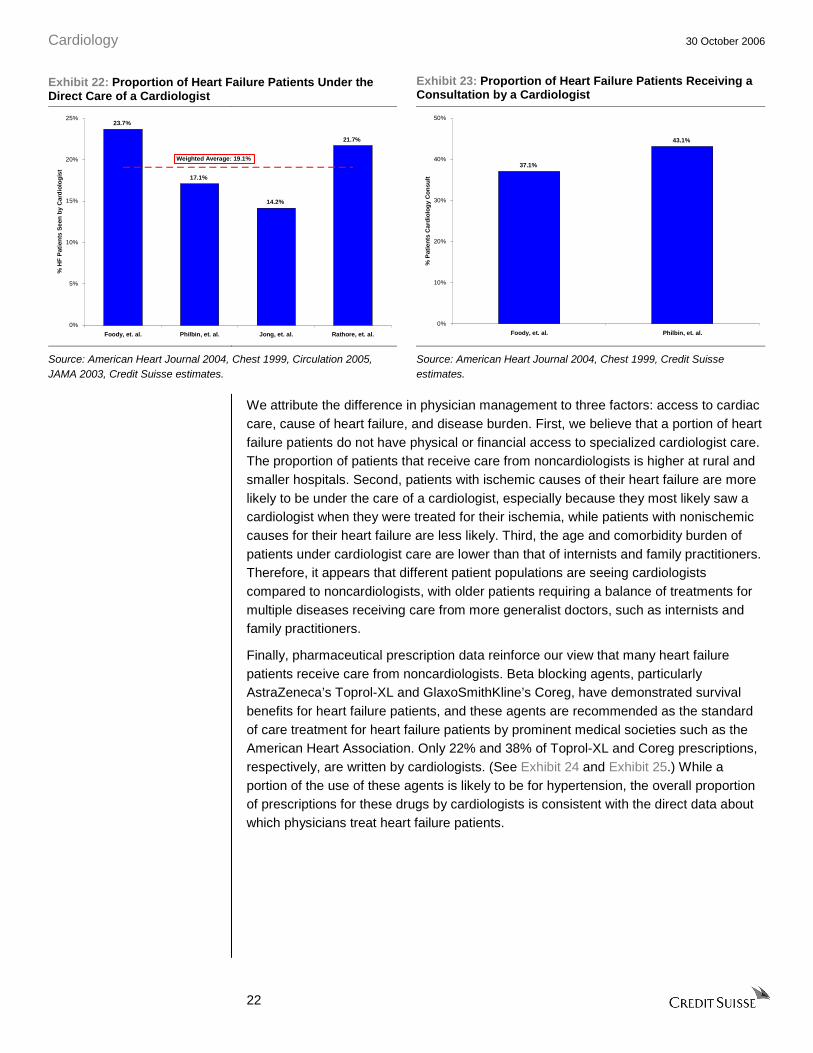

Forty Percent of Heart Failure Patients Do Not Receive Cardiologist Care Of the 5 million patients in the symptomatic heart failure prevalence pool, we estimate that only 50-60% receive any care from a cardiologist. Large-scale observational studies of patients hospitalized for heart failure, which we believe are representative of the ICD eligible population, show that 14-29% of patients, or an average of 19%, have a cardiologist as the provider of the majority of their medical treatment in the hospital. (See Exhibit 22.) Internists, primary care physicians, family practitioners, or, to a lesser extent, physicians of noncardiac specialties manage the balance of the patients. These same studies indicate that an additional 30-40% of symptomatic hospitalized heart failure patients receive a consultation from a cardiologist. (See Exhibit 23.) This leaves 40-50% of patients receiving no care from a cardiologist for their heart failure.

Cardiology 30 October 2006

22

Exhibit 22: Proportion of Heart Failure Patients Under the Direct Care of a Cardiologist

Exhibit 23: Proportion of Heart Failure Patients Receiving a Consultation by a Cardiologist

23.7%

17.1%

14.2%

21.7%

0%

5%

10%

15%

20%

25%

Foody, et. al. Philbin, et. al. Jong, et. al. Rathore, et. al.

% H

F P

atie

nts

See

n b

y C

ard

iolo

gis

t

Weighted Average: 19.1%

37.1%

43.1%

0%

10%

20%

30%

40%

50%

Foody, et. al. Philbin, et. al.

% P

atie

nts

Car

dio

log

y C

on

sult

Source: American Heart Journal 2004, Chest 1999, Circulation 2005, JAMA 2003, Credit Suisse estimates.

Source: American Heart Journal 2004, Chest 1999, Credit Suisse estimates.

We attribute the difference in physician management to three factors: access to cardiac care, cause of heart failure, and disease burden. First, we believe that a portion of heart failure patients do not have physical or financial access to specialized cardiologist care. The proportion of patients that receive care from noncardiologists is higher at rural and smaller hospitals. Second, patients with ischemic causes of their heart failure are more likely to be under the care of a cardiologist, especially because they most likely saw a cardiologist when they were treated for their ischemia, while patients with nonischemic causes for their heart failure are less likely. Third, the age and comorbidity burden of patients under cardiologist care are lower than that of internists and family practitioners. Therefore, it appears that different patient populations are seeing cardiologists compared to noncardiologists, with older patients requiring a balance of treatments for multiple diseases receiving care from more generalist doctors, such as internists and family practitioners.

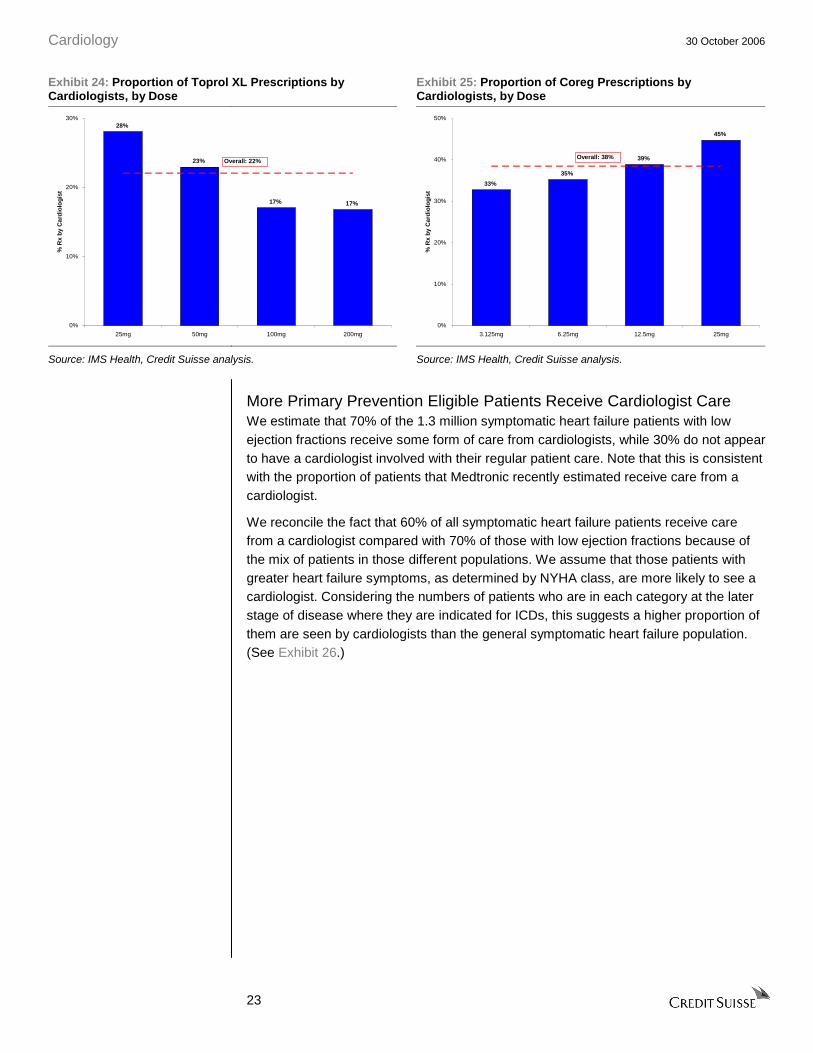

Finally, pharmaceutical prescription data reinforce our view that many heart failure patients receive care from noncardiologists. Beta blocking agents, particularly AstraZeneca’s Toprol-XL and GlaxoSmithKline’s Coreg, have demonstrated survival benefits for heart failure patients, and these agents are recommended as the standard of care treatment for heart failure patients by prominent medical societies such as the American Heart Association. Only 22% and 38% of Toprol-XL and Coreg prescriptions, respectively, are written by cardiologists. (See Exhibit 24 and Exhibit 25.) While a portion of the use of these agents is likely to be for hypertension, the overall proportion of prescriptions for these drugs by cardiologists is consistent with the direct data about which physicians treat heart failure patients.

Cardiology 30 October 2006

23

Exhibit 24: Proportion of Toprol XL Prescriptions by Cardiologists, by Dose

Exhibit 25: Proportion of Coreg Prescriptions by Cardiologists, by Dose

28%

23%

17% 17%

0%

10%

20%

30%

25mg 50mg 100mg 200mg

% R

x b

y C

ard

iolo

gis

t

Overall: 22%

33%

35%

39%

45%

0%

10%

20%

30%

40%

50%

3.125mg 6.25mg 12.5mg 25mg

% R

x b

y C

ard

iolo

gis

t

Overall: 38%

Source: IMS Health, Credit Suisse analysis. Source: IMS Health, Credit Suisse analysis.

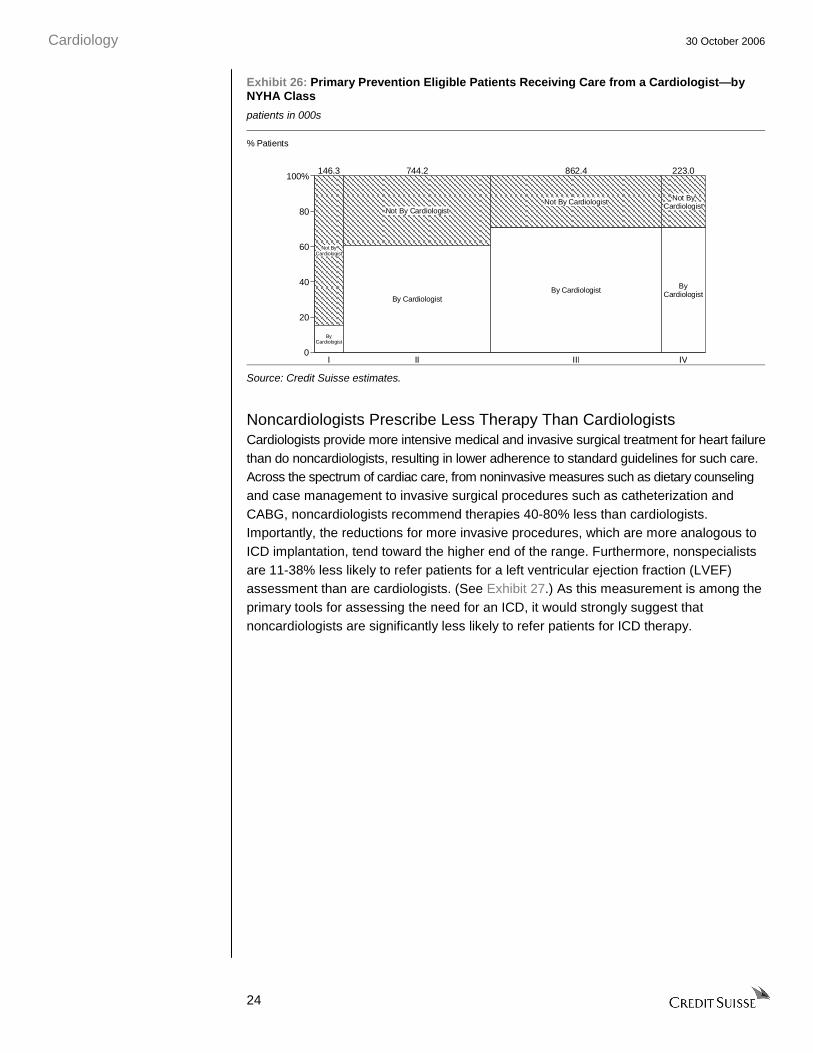

More Primary Prevention Eligible Patients Receive Cardiologist Care We estimate that 70% of the 1.3 million symptomatic heart failure patients with low ejection fractions receive some form of care from cardiologists, while 30% do not appear to have a cardiologist involved with their regular patient care. Note that this is consistent with the proportion of patients that Medtronic recently estimated receive care from a cardiologist.

We reconcile the fact that 60% of all symptomatic heart failure patients receive care from a cardiologist compared with 70% of those with low ejection fractions because of the mix of patients in those different populations. We assume that those patients with greater heart failure symptoms, as determined by NYHA class, are more likely to see a cardiologist. Considering the numbers of patients who are in each category at the later stage of disease where they are indicated for ICDs, this suggests a higher proportion of them are seen by cardiologists than the general symptomatic heart failure population. (See Exhibit 26.)

Cardiology 30 October 2006

24

Exhibit 26: Primary Prevention Eligible Patients Receiving Care from a Cardiologist—by NYHA Class

patients in 000s

Not ByCardiologist

ByCardiologist

Not By Cardiologist

By Cardiologist

Not By Cardiologist

By Cardiologist

Not ByCardiologist

ByCardiologist

I II III IV

146.3 744.2 862.4 223.0

0

20

40

60

80

100%

% Patients

Source: Credit Suisse estimates.

Noncardiologists Prescribe Less Therapy Than Cardiologists Cardiologists provide more intensive medical and invasive surgical treatment for heart failure than do noncardiologists, resulting in lower adherence to standard guidelines for such care. Across the spectrum of cardiac care, from noninvasive measures such as dietary counseling and case management to invasive surgical procedures such as catheterization and CABG, noncardiologists recommend therapies 40-80% less than cardiologists. Importantly, the reductions for more invasive procedures, which are more analogous to ICD implantation, tend toward the higher end of the range. Furthermore, nonspecialists are 11-38% less likely to refer patients for a left ventricular ejection fraction (LVEF) assessment than are cardiologists. (See Exhibit 27.) As this measurement is among the primary tools for assessing the need for an ICD, it would strongly suggest that noncardiologists are significantly less likely to refer patients for ICD therapy.

Cardiology 30 October 2006

25

Exhibit 27: Reduction in Left Ventricle Ejection Fraction (EF) Assessment—by Physician Type

Exhibit 28: Reduction in Cardiology Care Recommendations—by Physician Type

(11%)

(28%)

(37%)

(17%)

(40%)

(30%)

(20%)

(10%)

0%

Foody, et. al. Philbin, et. al. Edep, et. al.

% R

edu

ctio

n in

LV

EF

Ass

essm

ent

Internist GP/FP/Other Comb. Other

(100%)

(80%)

(60%)

(40%)

(20%)

0%

Stress

test

Cathe

teriz

ation

CHF doc

umen

ted

Echo/

vent

riculo

gram

Dietar

y con

sult

Case

man

agem

ent

Cathe

teriz

ation PCI

CABG

% R

edu

ctio

n in

Pro

ced

ure

/Use

Internist GP/FP/Other Comb. Other

Foody, et. al. Philbin, et. al. Jong, et. al.

Source: 27 American Medical Journal, 2005; Chest, 1999; JACC, 1997. Source: 28 American Medical Journal, 2005; Chest, 1999; Circulation, 2005.

Like interventional procedure care, primary care physicians and internists do not prescribe heart failure patients the standard of care medications endorsed by treatment guidelines as consistently as do cardiologists. After accounting for all other variables, noncardiologists are 10-25% less likely to prescribe Angioensin Converting Enzyme (ACE) inhibitors to symptomatic heart failure patients (see Exhibit 29), and this class of drugs has long been established as the gold standard of pharmacologic treatment for heart failure. Further, noncardiologists prescribe beta blockers 23-50% less than cardiologists. (See Exhibit 30.) As a more recently established therapy for heart failure, we believe that beta blocker prescription rates are more indicative of the difference in ICD use between cardiologists and noncardiologists, but we would argue that, given the invasive nature of ICD therapy, adoption of ICD use would be even lower among noncardiologists than drug therapy.

Exhibit 29: Reduction in Angiotensin Converting Enzyme (ACE) Inhibitor Prescription, by Physician Type

Exhibit 30: Reduction in Beta-Blocker Prescription, by Physician Type

(4%)

0%

(11%)

0%

(10%)

(25%)

(2%)

(16%)

(6%)

(30%)

(25%)

(20%)

(15%)

(10%)

(5%)

0%

5%

Foody, et. al. Philbin, et. al. Jong, et. al. Edep, et. al.

% R

edu

ctio

n in

AC

E R

x at

Dis

char

ge

Internist GP/FP/Other Comb. Other

(23%)

(27%)

(32%)

(50%)

(26%)

(38%)

(41%)

(60%)

(50%)

(40%)

(30%)

(20%)

(10%)

0%

Foody, et. al. Philbin, et. al. Jong, et. al.

% R

edu

ctio

n in

B-B

lock

er R

x at

Dis

char

ge

Internist GP/FP/Other Comb. Other

Source: 29 American Medical Journal, 2005; Chest, 1999; JACC, 1997; Circulation, 2005.

Source: 30 American Medical Journal, 2005; Chest, 1999; Circulation, 2005.

Cardiology 30 October 2006

26

We ascribe the difference in care to two factors: lower awareness of recommended therapies and different treatment goals for different patient populations. Our research, admittedly anecdotal, indicates that primary care physicians have less awareness of the results of the landmark SCD-HeFT trial and the preventative benefits of ICD therapy. Cardiologists who are not in the catchment area for an electrophysiologist appear to be aware of the guidelines, but an ICD is not likely to be in their consideration set until a patient develops electrical disturbances, rather than looking specifically at SCD risk factors, particularly low ejection fraction.

Additionally, we noticed differences between the patient populations seen by cardiologists and internists and family practitioners. With older and sicker patients, noncardiologists are probably more focused on nonheart failure symptoms and outcomes. This would lead to ICDs being considered only after the patients were considered stable with regard to their diabetes, renal disease, and hypertension.

African-American Patients Also Get Less Cardiac Care The burden of heart disease is disproportionately high among the African-American community in the United States. Heart disease is still the leading cause of death for African-Americans, and the death rate for African Americans from heart disease is 31% higher than for Caucasians. Recently published observational studies demonstrate that African-American patients are 30-40% less likely to receive ICD therapy than Caucasian patients with the same clinical presentation. (See Exhibit 31.) Public sources further show that African-Americans make up 12% of the U.S. population, and are overrepresented in the heart failure population, accounting for 15% of all patients. We determine that the exclusion for African-Americans being less likely to receive device therapy reduces the 1.3 million patient population eligible for ICDs by 50,000 patients.

We identified three independent, peer reviewed studies using observational data seeking to quantify the differences in ICD implantation rates between African-Americans and Whites. After controlling for age, geographical variables, and socioeconomic factors, these studies demonstrated that there was a 30-80% decrease in the likelihood of an African-American patient receiving an ICD relative to a comparable White patient.

Cardiology 30 October 2006

27

Exhibit 31: Reduction in ICD Use—White versus African-American Patients

(32%)

(81%)

(31%)

(42%)

(100%)

(80%)

(60%)

(40%)

(20%)

0%

Gauri, et. al. Voigt, et. al. Groeneveld, et. al. Groeneveld, et. al.

% R

edu

ctio

n in

ICD

Imp

lan

tati

on

Median: (37%)

Source: 31 Am Journal of Medicine, 2006; JACC, 2004; Circ, 2003; JACC, 2005.

Other studies show that racial differences in care are not isolated to ICD therapy, but extend across the spectrum of cardiac care. In fact, African-Americans are 30-70% less likely to receive many well-established cardiovascular interventions, including angioplasty, CABG, and valve replacement surgery. (See Exhibit 32.)

Cardiology 30 October 2006

28

Exhibit 32: Reduction in Cardiology Care Recommendations—White versus African-

American Patients

(30%)

(58%)

(67%) (68%)

(62%)

(13%)

(32%)(35%)

(62%)

(40%)

(80%)

(60%)

(40%)

(20%)

0%

Angiop

lasty

CABG

Carot

id End

arte

ctom

y

AAA Rep

air

Valve

Replac

emen

t

Angiop

lasty

CABGEith

er

Angiog

raph

y

Angiog

raph

y

% R

edu

ctio

n in

Pro

ced

ure

Jha, et. al. Peterson, et. al. LaVeist, et. al.Schulman, et. al.

Source: 32 NEJM, 2005; NEJM, 1997; JACC, 2003; NEJM, 1999.

The difference in cardiac care between African-Americans and Whites can be partially attributed to higher comorbidity burdens among the African-American population. Studies have also shown that the comorbidity burden for whites when diagnosed with heart disease is statistically significantly lower with whites than blacks. The prevalence of having any two risk factors for heart disease and stroke (high blood pressure, high cholesterol, diabetes, being a smoker, physically inactive, and obesity) was highest among African Americans (49%). It is difficult to separate out the causative versus the correlative issues in this field, as there are degrees of severity along the disease cascade for respiratory, renal, and metabolic issues, which tie in to the overall disease burden and thus may render the patients “too sick” for an ICD.

African-American patients also tend to be situated in lower-income areas with less generous insurance coverage, and they are less likely to have ischemic heart disease. As a result, African-American heart failure patients are up against intrinsic barriers in the system to get them into the cascade of appropriate evaluation to receive a device. That said, there is a decrease in the utilization of the technology in this population unexplained by the comorbidity burden, and we sadly suspect that this stems from systemic or societal issues.

Cardiology 30 October 2006

29

Natural Limits to the Adoption of Therapies We disagree with the unspoken implication of the medical device companies that, since market penetration of ICDs is only at 20-25% of the prevalence pool, the market could be 4-5 times as large as it currently is. There are normal limits to the adoption of medical technologies in indicated populations. In the case of ICDs, unlike pharmaceutical therapy, there will not be spillover from completely nonindicated patients who decide to prophylactically get an expensive, and unreimbursed, ICD. A number of independent data points suggest that the natural limit to therapy adoption is 65-70%, which we see as reasonable especially given the highly invasive nature of this therapy. To determine this level, we look to the proportions of symptomatic heart failure patients that receive ejection fraction assessments and optimal medical therapy, as well as the proportion of secondary prevention patients (the rare patient that lives through his or her first SCD event without an ICD) receiving ICD therapy.

Apart from the clinical barriers to acceptance, two other factors, which are multifactorial, influence whether or not a medical technology is adopted.

Emotional/“Fear” Factors Limiting ICD Referral

Patient refusal

• Under/nonreporting of symptoms

• Feel they are too sick

• Uncertainty of undergoing a procedure

• Uncertainty in “quality” of devices

• Not wanting ICD resuscitation

• Fear of inappropriate shocks

Physician unwilling to refer

• Feels patient won’t benefit/not sick enough

• Feels patient is too ill to receive treatment

• Not convinced of cost effectiveness of device therapy

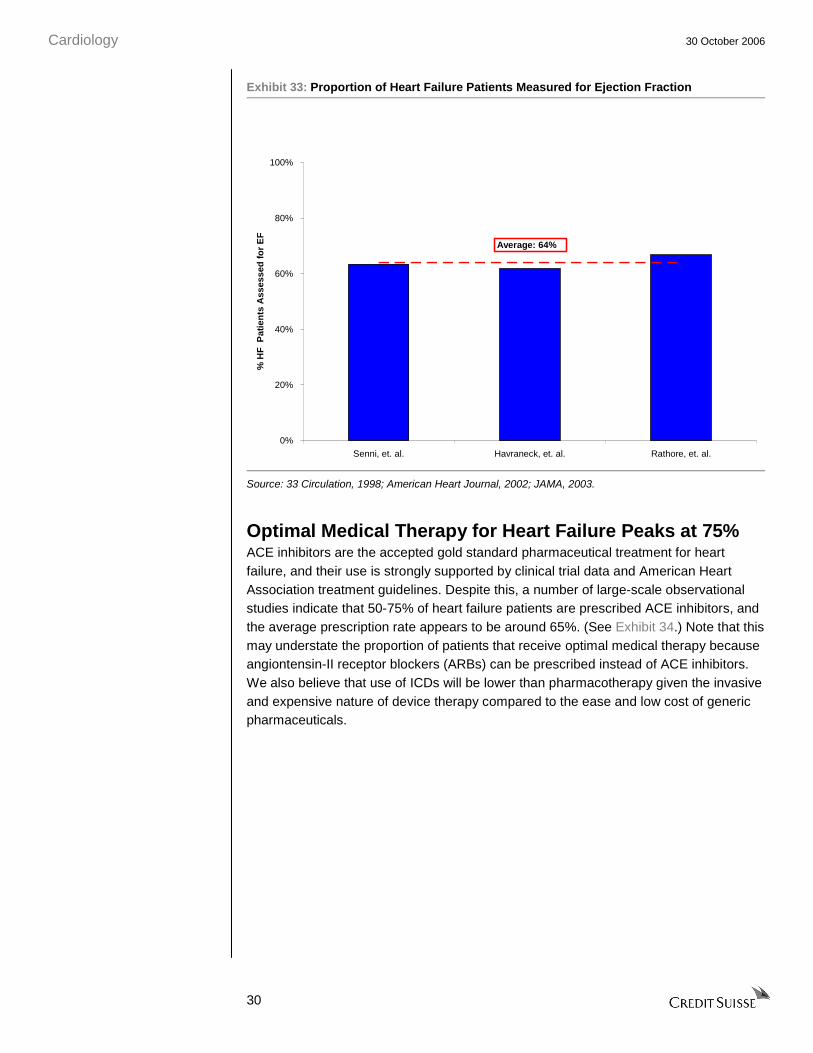

Only Two-Thirds of Heart Failure Patients Get Ejection Fraction Measurements A number of large-scale observational studies suggest that only 60-70% of symptomatic heart failure patients are referred for measurement of their ejection fraction. (See Exhibit 33.) Given the importance of ejection fraction assessment to determine ICD need, we view this data point as the most compelling information about the potential limit to adoption of ICD technology. This statistic shows not just the reduction for which patients are even being considered for heart failure management, but it excludes 30-40% of patients from being considered for ICD evaluation, as the primary decision criteria for device implantation is driven by a patient’s ejection fraction.

Cardiology 30 October 2006

30

Exhibit 33: Proportion of Heart Failure Patients Measured for Ejection Fraction

0%

20%

40%

60%

80%

100%

Senni, et. al. Havraneck, et. al. Rathore, et. al.

% H

F P

atie

nts

Ass

esse

d f

or

EF

Average: 64%

Source: 33 Circulation, 1998; American Heart Journal, 2002; JAMA, 2003.

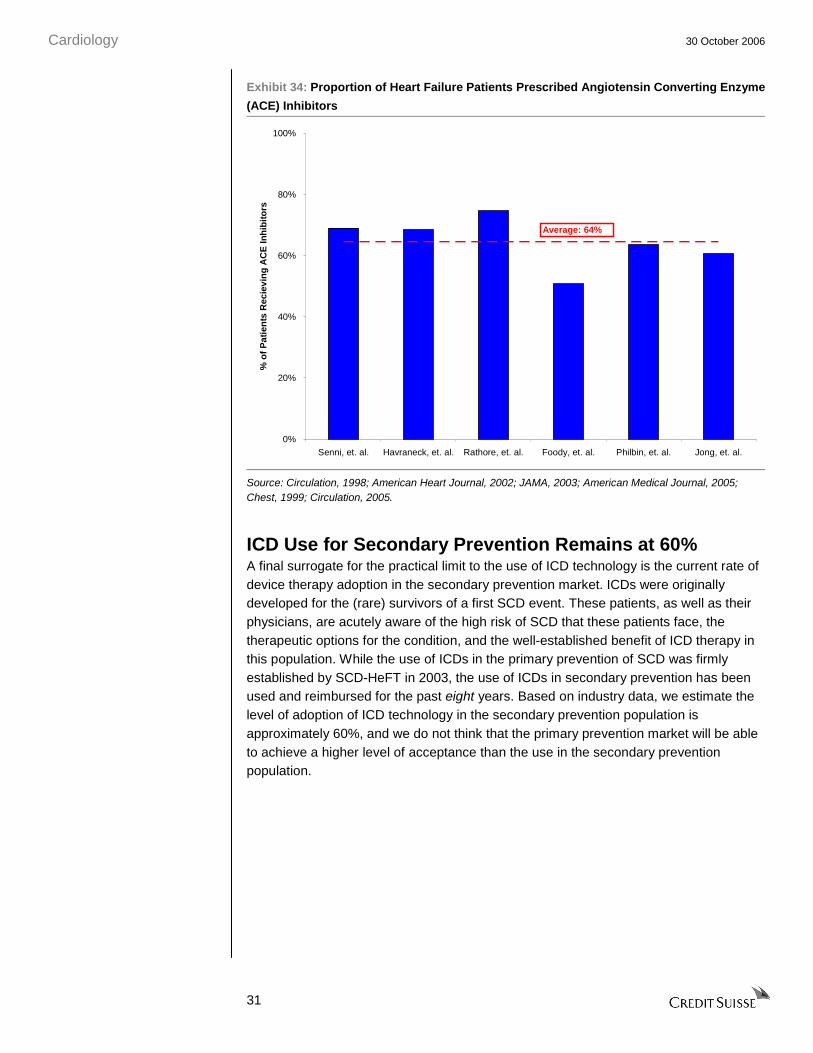

Optimal Medical Therapy for Heart Failure Peaks at 75% ACE inhibitors are the accepted gold standard pharmaceutical treatment for heart failure, and their use is strongly supported by clinical trial data and American Heart Association treatment guidelines. Despite this, a number of large-scale observational studies indicate that 50-75% of heart failure patients are prescribed ACE inhibitors, and the average prescription rate appears to be around 65%. (See Exhibit 34.) Note that this may understate the proportion of patients that receive optimal medical therapy because angiontensin-II receptor blockers (ARBs) can be prescribed instead of ACE inhibitors. We also believe that use of ICDs will be lower than pharmacotherapy given the invasive and expensive nature of device therapy compared to the ease and low cost of generic pharmaceuticals.

Cardiology 30 October 2006

31

Exhibit 34: Proportion of Heart Failure Patients Prescribed Angiotensin Converting Enzyme

(ACE) Inhibitors

0%

20%

40%

60%

80%

100%

Senni, et. al. Havraneck, et. al. Rathore, et. al. Foody, et. al. Philbin, et. al. Jong, et. al.

% o

f P

atie

nts

Rec

ievi

ng

AC

E In

hib

ito

rs

Average: 64%

Source: Circulation, 1998; American Heart Journal, 2002; JAMA, 2003; American Medical Journal, 2005; Chest, 1999; Circulation, 2005.

ICD Use for Secondary Prevention Remains at 60% A final surrogate for the practical limit to the use of ICD technology is the current rate of device therapy adoption in the secondary prevention market. ICDs were originally developed for the (rare) survivors of a first SCD event. These patients, as well as their physicians, are acutely aware of the high risk of SCD that these patients face, the therapeutic options for the condition, and the well-established benefit of ICD therapy in this population. While the use of ICDs in the primary prevention of SCD was firmly established by SCD-HeFT in 2003, the use of ICDs in secondary prevention has been used and reimbursed for the past eight years. Based on industry data, we estimate the level of adoption of ICD technology in the secondary prevention population is approximately 60%, and we do not think that the primary prevention market will be able to achieve a higher level of acceptance than the use in the secondary prevention population.

Cardiology 30 October 2006

32

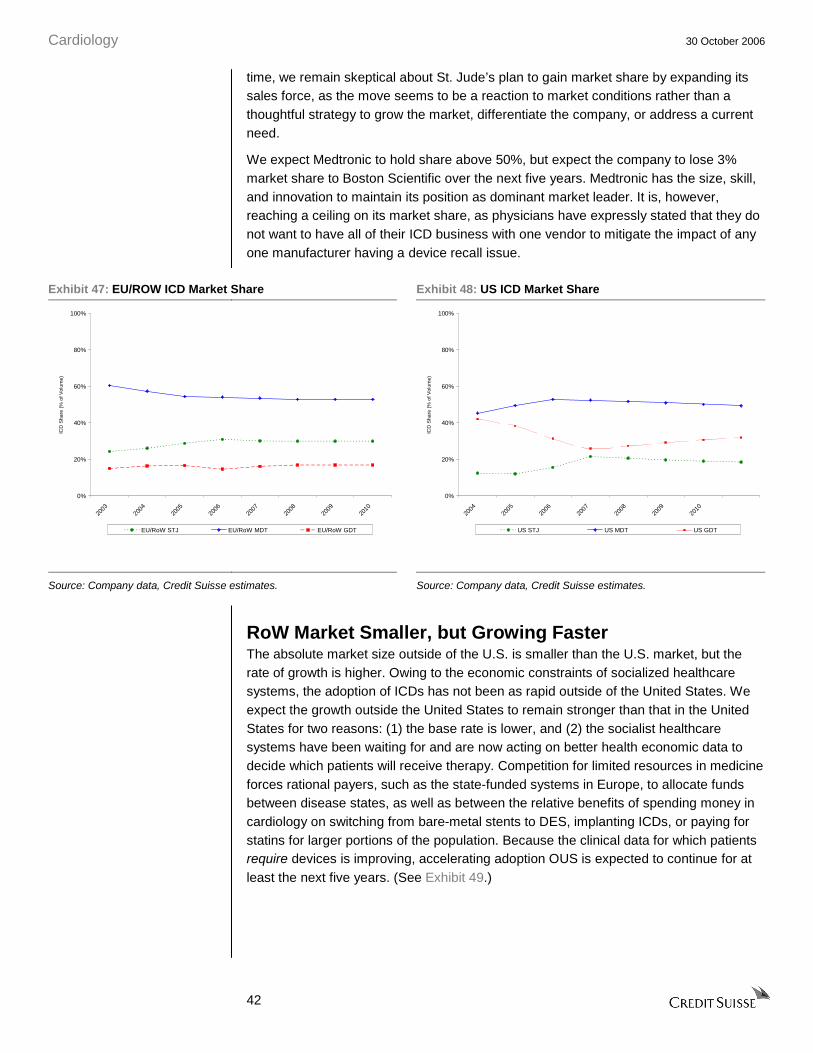

ICD Growth Will Be Harder to Drive Given our view on the structure of the market for primary prevention ICD use, we believe that it will be challenging for the existing companies to re-invigorate the growth of the market. It would appear that a significant proportion of the “low-hanging fruit” in the primary prevention population—clinically appropriate males already under the care of cardiologists—has been harvested. In fact, we estimate that the penetration rate among these individuals could be as high as 70%. To drive a sufficient number of incremental referrals to reaccelerate the ICD market, the CRM companies will need to change long-standing gender and race biases in the way medicine is practiced. The CRM companies will also need to reach far beyond their traditional specialty physician bases to a large, diverse physician audience. Finally, the companies will need to promote expensive preventative therapy, rather than the relative benefits of one device over another.

We currently see Medtronic and other companies beginning the process of reaching out to the ICD referral network. However, we believe that it will take some time for the CRM companies to recruit the marketing and sales talent that they need to establish effective programs and implement these in the marketplace. Even more important, it will take the promotional efforts a significant amount of time to affect referral patterns, especially given the deeply rooted practice patterns that the companies seek to modify.

Changing Medical Biases Will Take a Long Time Based on our review of heart failure epidemiology, we believe that a significant contributor to the slowdown in the growth of the U.S. ICD market is a lower rate of device use among women and African-Americans, compared to their male and White counterparts. While a portion of the difference in ICD use can be attributed to medical factors such as age and comorbidity burden, which would suggest that device adoption should be lower in these groups, we sadly infer that social biases may play a meaningful role, as well. If this is the case, the CRM companies will need to implement marketing programs to promote device use in these patient populations. We know that there are campaigns such as “Go Red for Women,” conducted by established medical societies such as the American Heart Association, to improve care for women with cardiac conditions, but that these efforts have made only small changes in the practice of medicine thus far. In addition, physician treatment biases are not overt, and encouraging changes among individuals must be done carefully and with nuance. Therefore, we would expect any company-driven marketing efforts, which are typically met with skepticism by physicians, will take two to three years to have an impact on device referral patterns.

Insurance Is More Difficult to Sell Than Treatment Until now, the CRM companies have largely focused their marketing and sales efforts on either promoting the benefits of specific devices to highly focused specialist physicians, such as electrophysiologists, or to selling acute treatments in other portions of their businesses, such as stents for coronary artery disease. (See Exhibit 35.) The task of marketing ICD therapy for primary prevention is a considerably different task. ICD implantation for primary prevention of SCD is a prophylactic intervention, unlike

Cardiology 30 October 2006

33

almost any other product that the CRM companies have experience marketing. In contrast to telling doctors and patients to have a procedure that will immediately alleviate symptoms or improve critical laboratory measures, ICD implantation is strictly an expensive preventative measure. In addition, ICDs have the potential for a particularly unpleasant inappropriate (shock) therapy, and its implementation is invasive. As a result, nonspecialists and patients will have a tough time trying to understand how receiving an invasive procedure, getting an implant that “may need to be recalled,” and dealing with the issues of not getting near magnetic fields, caution with electrical sources, metal detectors, etc., is an improvement on unseen and unfelt risk factors. Thus, we believe that the marketing of ICDs for primary prevention will be a challenge, even for large companies such as Medtronic.

Exhibit 35: Comparison of CRM Company Target Markets Market Disease/ Symptoms Treatment/Prophylaxis

ICDs Enlarged heart, post-MI scarring Prevention of Chance of Sudden Death

Cardiac stents Acute MI Treatment

CABG equipment Acute MI Treatment

Atrial fibrillation Fainting Treatment

Neurostimulation Parkinsons’s tremors Treatment

Severe chronic pain

Pacing Slow heartbeat Treatment

Spine Chronic debilitating pain Treatment

Source: Credit Suisse analysis.

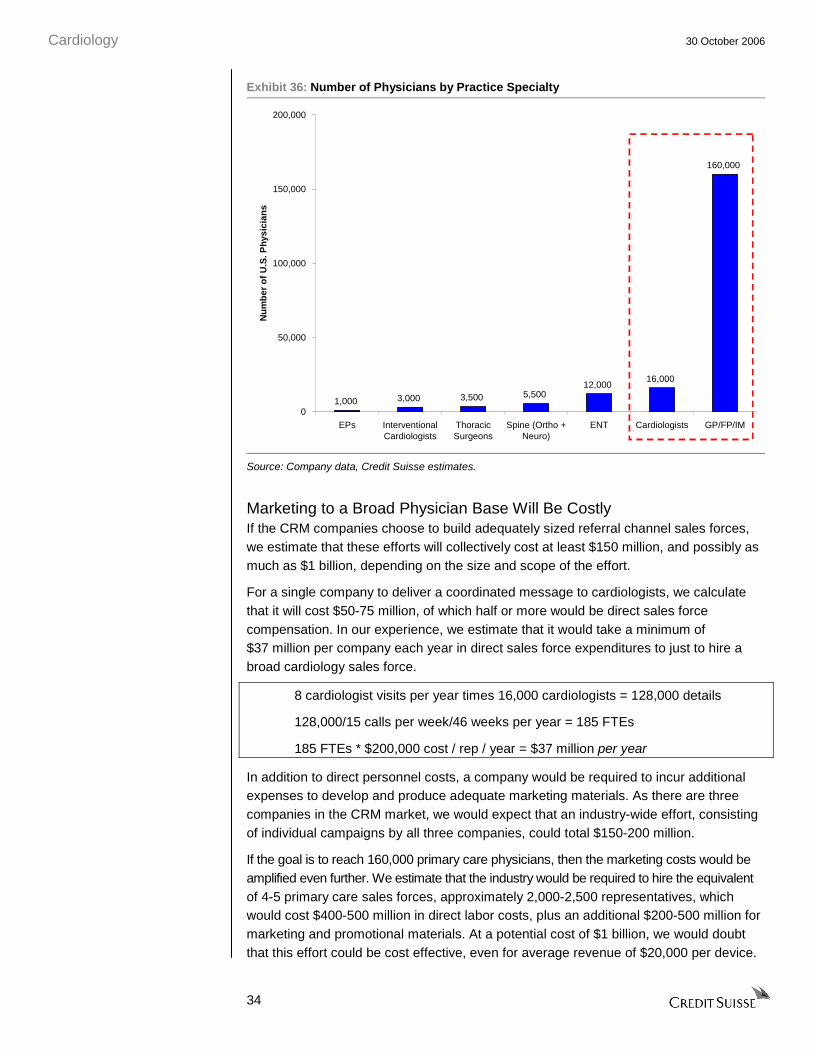

New Patients Mean Marketing to New Physicians Beyond the difficulty of delivering a new type of message to physicians, the CRM companies now need to target a much larger and unfamiliar physician base than they have ever done to re-invigorate the referral process for ICDs. To reach the majority of heart failure patient physicians, it will be essential for the device companies to market to all U.S. cardiologists and to the larger community of primary care physicians, including internists and family practitioners. We do not believe that investors or the companies appreciate the magnitude of this challenge, nor do they appreciate the level of competition for these physicians’ time. Current CRM company sales force efforts are spent on implanting electrophysiologists, or in the case of other products, groups of specialty physicians or surgeons numbering in the single-digit thousands. (See Exhibit 36.) While these energies have been useful (as evidenced by the rate of growth of sales and adoption to date), the expansion of the sales force to access the referring communities of physicians requires efforts 16-160 times that of the companies’ current efforts. Moreover, gaining access to busy cardiologists or primary care physicians, who are already inundated with practice concerns and marketing calls by pharmaceutical company representatives, will be much tougher than marketing to their core specialty physician bases.

Cardiology 30 October 2006

34

Exhibit 36: Number of Physicians by Practice Specialty

1,000 3,000 3,500 5,50012,000

16,000

160,000

0

50,000

100,000

150,000

200,000

EPs InterventionalCardiologists

ThoracicSurgeons

Spine (Ortho +Neuro)

ENT Cardiologists GP/FP/IM

Nu

mb

er o

f U

.S. P

hys

icia

ns

Source: Company data, Credit Suisse estimates.

Marketing to a Broad Physician Base Will Be Costly If the CRM companies choose to build adequately sized referral channel sales forces, we estimate that these efforts will collectively cost at least $150 million, and possibly as much as $1 billion, depending on the size and scope of the effort.

For a single company to deliver a coordinated message to cardiologists, we calculate that it will cost $50-75 million, of which half or more would be direct sales force compensation. In our experience, we estimate that it would take a minimum of $37 million per company each year in direct sales force expenditures to just to hire a broad cardiology sales force.

8 cardiologist visits per year times 16,000 cardiologists = 128,000 details

128,000/15 calls per week/46 weeks per year = 185 FTEs

185 FTEs * $200,000 cost / rep / year = $37 million per year