equity reports for the week (07th mar -11th mar - 2011)

TRANSCRIPT

8/7/2019 Equity Reports for the Week (07th Mar -11th Mar - 2011)

http://slidepdf.com/reader/full/equity-reports-for-the-week-07th-mar-11th-mar-2011 1/6

Global Research Limited

EEKLY REPORT

1 | JANUARY 2011 | www.capitalvia.com

World stocks and the US dollar fell on Friday as oil prices rose on escalating violence in Libya, overshadowing a US jobs r eport that showed the economic

recovery shifting up a gear.

For the week, the Dow was up 0.3%, while the S&P and Nasdaq were up 0.1% each. The S&P 500 is up 26% since the s tart of September when the recent rally

began.

US crude oil prices jumped to their highest since September 2008, and Brent crude rose above USD 116 a barrel as Libyan security forces clashed with rebels

near the major oil terminal of Ras Lanuf.

The Labor Department reported hiring by US employers in February hit the highest level since last May as unemployment dipped to 8.9%, an almost two-year

low.

US MARKET

Indices posts best weekly gain since November: The 30-share BSE index snapped a four-session winning streak and closed 0.02 per cent, or 3.31 points, lower at18,486.45 points, after rising as much as 1.3 per cent earlier.

The markets have been trading in a steady manner this afternoon and look set to sign off the last day of the week on a positive note as the unmoved triggered byMonday's Budget is showing no signs of hitting a roadblock, at least as yet. The Sensex is quoting at 18,564, higher by 75 points and the Nifty is at 5559, up 22points. The midcap and small cap indices are flat at 6604 and 8024 respectively.

Auto stocks have extended recent gains on the back of higher sales in February and the government's move to keep the excise duties on automobiles unchangedin the Budget, contrary to market expectations of a 2% hike.

Auto stocks have extended recent gains on the back of higher sales in February and the government's move to keep the excise duties on automobiles unchangedin the Budget, contrary to market expectations of a 2% hike.

WEEK WRAP

Asian markets were trading higher. China's Shanghai Composite added 0.21% or 6.15 points a t 2,909.13.

Asian stocks were poised for their best weekly gains in three months as market players hunted for bargains while the euro perked up after the European CentralBank signalled a rate hike as early as next month.

South Korea's KOSPI, which plumbed a three-month low on Wednesday, was among the best performers in the region, advancing 2.2% on the day.

ASIAN & EMERGING MARKET

India's fruits, veggies production estimated to rise this yr: India's production of vegetables and fruits is estimated to increase by nearly 6% and 5% respectively

in the current year as compared to previous year, Parliament was informed today. Production of vegetables during 2010-11 is estimated to be 141.3 tons against

133.5 tons in 2009-10, Minister of State for Agriculture Arun Yadav said in a written reply in Lok Sabha.

Debt market sees trade of Rs 1,638 cr at NSE: The Wholesale Debt Market (WDM) segment of the National Stock Exchange (NSE) today witnessed a totalturnover of Rs 1,638.08 crore in 73 trades.

Top securities (non-repo) traded at the WDM were, the 8.08% government securities maturing in 2022, which traded at Rs 345 crore at weighted yield of

8.07%..

MICRO ECONOMIC FRONT

th Mar - 11th Mar 2011

STOCKSSTOCKSSTOCKS

CAPITALVIA GLOBAL RESEARCH LIMITED

STRON G RALLY POST BUDGE T TAKES INDICE S HIGHER

8/7/2019 Equity Reports for the Week (07th Mar -11th Mar - 2011)

http://slidepdf.com/reader/full/equity-reports-for-the-week-07th-mar-11th-mar-2011 2/61 | DECEMBER 2010 | www.capitalvia.com

LOSERSGAINERS

GAINERS

FII’S INVESTMENTSDII’S INVESTMENTS

Indices Buy Value Sell Value Net Value

Scrip Current Close Change Chg % Scrip Current Close Change Chg %

Indices Buy Value Sell Value Net Value

S&P CNX 500

CNX IT

CNX MIDCAP

CNX 100

4241.40

6688.55

7402.15

5226.55

4455.05

6918.70

7718.55

5497.15

4233.65

6628.05

7351.65

5210.95

4403.75

6810.65

7654.20

5430.55

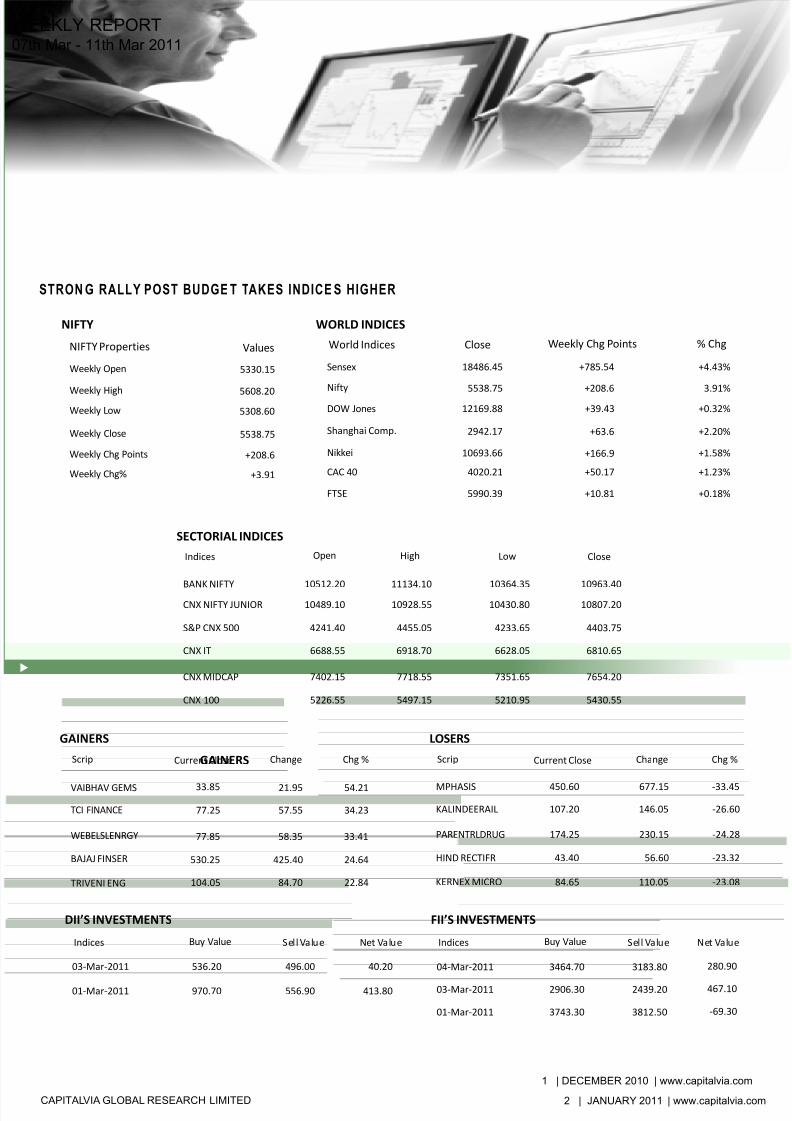

VAIBHAV GEMS

WEBELSLENRGY

33.85

77.85

TRIVENI ENG 104.05

TCI FINANCE 77.25

BAJAJ FINSER 530.25

21.95

58.35

84.70

57.55

425.40

54.21

33.41

22.84

34.23

24.64

MPHASIS

KALINDEERAIL

PARENTRLDRUG

HIND RECTIFR

KERNEX MICRO

107.20

450.60

174.25

43.40

84.65

146.05

677.15

230.15

56.60

110.05

-26.60

-33.45

-24.28

-23.32

-23.08

03-Mar-2011 536.20 496.00 40.20

01-Mar-2011 970.70 556.90 413.80

04-Mar-2011 3464.70 3183.80

03-Mar-2011 2906.30 2439.20

01-Mar-2011 3743.30 3812.50

280.90

467.10

-69.30

WORLD INDICES

CloseWorld Indices Weekly Chg Points % Chg

NIFTY

NIFTY Properties Values

Open High Low Close

SECTORIAL INDICES

Indices

Shanghai Comp.

DOW Jones

18486.45

5538.75

2942.17

12169.88

5990.39

10693.66

4020.21

Sensex

Nifty

FTSE

Nikkei

CAC 40

+785.54

+208.6

+63.6

+39.43

+10.81

+166.9

+50.17

+4.43%

3.91%

+2.20%

+0.32%

+0.18%

+1.58%

+1.23%

Weekly Open

Weekly HighWeekly Low

Weekly Close

Weekly Chg Points

Weekly Chg%

5330.15

5608.205308.60

5538.75

+208.6

+3.91

BANK NIFTY

CNX NIFTY JUNIOR 10489.10

10512.20

10928.55

11134.10

10430.80

10364.35

10807.20

10963.40

2 | JANUARY 2011 | www.capitalvia.com

EEKLY REPORTth Mar - 11th Mar 2011

CAPITALVIA GLOBAL RESEARCH LIMITED

STRON G RALLY POST BUDGE T TAKES INDICE S HIGHER

8/7/2019 Equity Reports for the Week (07th Mar -11th Mar - 2011)

http://slidepdf.com/reader/full/equity-reports-for-the-week-07th-mar-11th-mar-2011 3/6

WEEK AHEAD SPOT NIFTY

Bank Nifty Futures shut stop at 10967.15, up 19.85 points or 0.18 %.It is looking bullish in the coming trading session if it

manages to trade above the resistance level of 11184 else below 10780 it might be in a bearish trend.

Figure: Bank Nifty Weekly

WEEK AHEAD BANK NIFTY

Support 1

Support 2

Resistance 1

Resistance 2

10780

10520

11184

11325

TECHNICALS

ValuesProperties

The Nifty Benchmark ended at 5547.54 up 3.05 points or 0.06 %.It is looking bullish in the coming trading session if it

manages to trade above the resistance level of 5622 above this level it would be in a bullish trend else below 5375 it might

face more selling pressure.

Figure: 1 Nifty Weekly

TECHNICALS

ValuesPropertiesSupport 1

Support 2

Resistance 1

Resistance 2

5475

5475

5622

5715

3 | JANUARY 2011 | www.capitalvia.com

EEKLY REPORTth Mar - 11th Mar 2011

CAPITALVIA GLOBAL RESEARCH LIMITED

STRON G RALLY POST BUDGE T TAKES INDICE S HIGHER

8/7/2019 Equity Reports for the Week (07th Mar -11th Mar - 2011)

http://slidepdf.com/reader/full/equity-reports-for-the-week-07th-mar-11th-mar-2011 4/6

Company Name

52 Week High

% From High

Symbol

Change

Volume

Day High

EPS

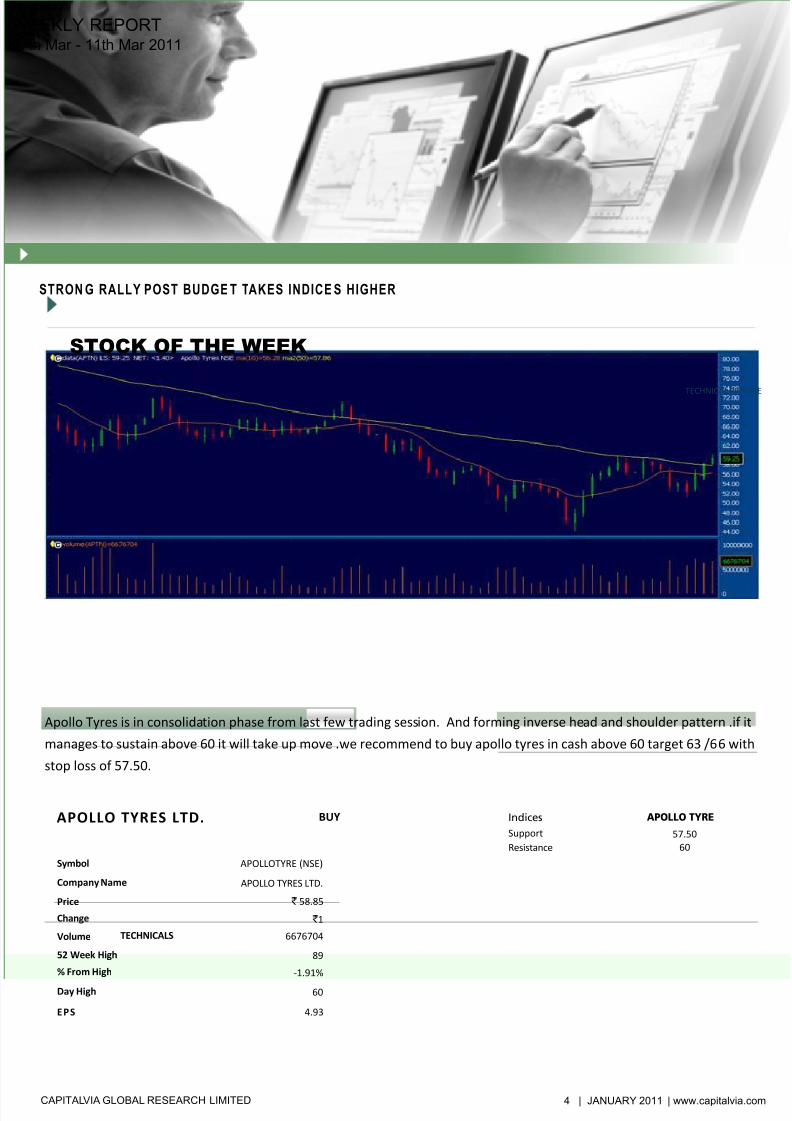

APOLLO TYRES LTD.

89

-1.91%

APOLLOTYRE (NSE)

` 1

6676704

60

4.93

` 58.85Price

Apollo Tyres is in consolidation phase from last few trading session. And forming inverse head and shoulder pattern .if it

manages to sustain above 60 it will take up move .we recommend to buy apollo tyres in cash above 60 target 63 /66 with

stop loss of 57.50.

TECHNICALS

SupportResistance

57.5060

APOLLO TYREIndices

TECHNICAL PICTURE

BUY

4 | JANUARY 2011 | www.capitalvia.com

EEKLY REPORTth Mar - 11th Mar 2011

CAPITALVIA GLOBAL RESEARCH LIMITED

STOCK OF THE WEEK

STRON G RALLY POST BUDGE T TAKES INDICE S HIGHER

APOLLO TYRES LTD.

8/7/2019 Equity Reports for the Week (07th Mar -11th Mar - 2011)

http://slidepdf.com/reader/full/equity-reports-for-the-week-07th-mar-11th-mar-2011 5/6

8/7/2019 Equity Reports for the Week (07th Mar -11th Mar - 2011)

http://slidepdf.com/reader/full/equity-reports-for-the-week-07th-mar-11th-mar-2011 6/6

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any responsibility (or

liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most.

Sincere efforts have been made to present the right investment perspective. The information contained herein is

based on analysis and up on sources that we consider reliable. This material is

for personal information and based upon it & take no responsibility

The stock price projections shown are not necessarily indicative of future price performance. The information herein, together with all estimates and

forecasts, can change without notice.

Analyst or any person related to CapitalVia might be holding positions in the stocks recommended.

It is understood that anyone who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for

which either the site or its owners or anyone can be held responsible for.

Any surfing and reading of the information is the acceptance of this disclaimer.

All Rights Reserved.

Investment in Stocks has its own risks.

We, however, do not vouch for the accuracy or the completeness thereof.

we are not responsible for any loss incurred whatsoever for any financial profits or

loss which may arise from the recommendations above.

CapitalVia does not purport to be an invitation or an offer to buy or sell any financial instrument.

Our Clients (Paid Or Unpaid), Any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Provided by

us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

D I S C L A I M E R

Contact Number:Hotline: +91-91790-02828Landline: +91-731-668000Fax: +91-731-4238027

No. 99, 1st Floor, Surya ComplexR. V. Road, BasavangudiOpposite Lalbagh West GateBangalore - 560004

Corporate Office Address:

India:CapitalVia Global Research LimitedNo. 506 West, Corporate House169, R. N. T. Marg, Near D. A. V. V.Indore - 452001

Singapore:CapitalVia Global Research Pvt. Ltd.Block 2 Balestier Road#04-665 Balestier HillShopping CentreSingapore - 320002

C O N T A C T U S

EEKLY REPORTth Mar - 11th Mar 2011