equity portfolio strategies - week 5. topics today - passive equity strategies - active equity...

TRANSCRIPT

Equity Portfolio Strategies

- Week 5

Topics Today

-Passive Equity Strategies-Active Equity Strategies

Generic Portfolio Management Strategies

Passive equity portfolio management– Usually tries to track an index over time– Hope to match market performance of the

selected index – Portfolio only needs to change as composition

of index changes.– Manager is judged on how well they track the

target index Active equity portfolio management

– Attempts to outperform a passive benchmark portfolio on a risk-adjusted basis

Exhibit 16.1

Passive Equity Portfolio Management Strategies

Since trying to replicate the performance of an index, process of stock selection is largely automatic. No need for analysts or other expensive research.

Costs of passive approach tiny compared to costs of active approach

Costs of active management (1 to 2 percent p.a.) make it difficult for active to beat passive on a risk-adjusted basis

Thus the main rationale for the passive approach is its substantial cost advantage over the active approach

Passive Equity Portfolio Management Strategies

Investors are unable to purchase the market index directly

Not a simple process to track a market index closely

Three basic techniques:– Full replication– Sampling– Quadratic optimization or programming

Passive Equity Portfolio Management Strategies

Full ReplicationTo ensure close tracking, all securities in the

index are purchased in proportion to their weights in the index

This leads to numerous transactions, especially as dividends have to be reinvested.

Numerous transactions leads to more transaction costs

Passive Equity Portfolio Management Strategies

SamplingFund invests in a ‘representative’ sample of the

stocks in the index in proportion to the stocks’ weights in that index

This leads to less transactions than with full replication, resulting in lower commissions

Sampling creates ‘tracking errors’ (the differences between portfolio returns and the corresponding index returns)

Tracking errors can be reduced by using a larger sample, but costs will then be larger

Passive Equity Portfolio Management Strategies

Quadratic Optimization Uses historical return data on the stocks in the

index to find a portfolio with less stocks than the index that will minimize tracking error

Suffers from the problem that the portfolio weights that minimise past tracking error may not minimise future tracking error

So there are no guarantees of close tracking with this method.

Methods of Index Portfolio Investing Index Funds

– In an indexed portfolio, the fund manager will typically attempt to replicate the composition of the particular index exactly

– The fund manager will buy the exact securities comprising the index in their exact weights

– Change those positions anytime the composition of the index itself is changed

– Low trading and management expense ratios– The advantage of index mutual funds is that

they provide an inexpensive way for investors to acquire a diversified portfolio

Methods of Index Portfolio Investing

Exchange-Traded Funds (ETF)– EFTs are depository receipts that give investors

a pro rata claim on the capital gains and cash flows of the securities that are held in deposit by a financial institution that issued the certificates

– A significant advantage of ETFs over index mutual funds is that they can be bought and sold (and short sold) like common stock

– The notable example of ETFsStandard & Poor’s 500 Depository Receipts

(SPDRs)iSharesSector ETFs

Active Equity Portfolio Management Strategies

Active managers are successful for their investors if they consistently earn a portfolio return that exceeds the return of an appropriate passive benchmark portfolio, net of transaction costs, on a risk-adjusted basis

Why?Success is not easy. Active managers have the

burden of higher costs than passive managersNeed to choose an appropriate benchmark

Fundamental Strategies

Top-Down versus Bottom-Up Approaches– Top-Down

Broad country and asset class allocationsSector allocation decisionsIndividual securities selection

Fundamental Strategies

Top-Down versus Bottom-Up Approaches– Top-Down

Broad country and asset class allocationsSector allocation decisionsIndividual securities selection

– Bottom-UpEmphasizes the selection of securities without

any initial market or sector analysisForm a portfolio of equities that can be

purchased at a substantial discount to what his or her valuation model indicates they are worth

Active Equity Portfolio Management Strategies

Three basic StrategiesMarket timing – tactical asset allocation: shifting

funds into and out of stocks, bonds, and T-bills depending on broad market forecasts and estimated risk premiums

sector rotation: Shifting funds among different equity sectors and industries or among investment styles to catch hot concepts before the market does (a ‘top-down’ strategy)

Style Investing: Selecting individual stocks, based on on one or more characteristics of each company

Active Equity Portfolio Management Strategies

Two Global Strategies Identify countries with markets that appear

undervalued or overvalued and weight the portfolio accordingly (another ‘top-down’ strategy)

Manage a global portfolio from an industry perspective rather than from a country perspective

Active Equity Portfolio Management Strategies

Sector RotationTries to take advantage of the herd mentality of

many investors by exiting popular sectors and seeking to identify and invest in other sectors that might become popular next.

May base on macroeconomic trends or forecasts Difficult to do well. E.g. Tech stocks have become expensive (in P/E

terms) again, but drug stocks look cheap.e.g., housing sector vulnerable to interest rate

increases which seem more likely than not.

Style Investing

Tests of efficient market models have uncovered anomalies that suggest that the market does not behave as one market but rather is segmented (e.g. low P/B do better)

Market segments are groups of stocks with similar characteristics that tend to perform similarly

market segments can be divided into top-down (sectors and industries) and bottom-up classifications (e.g., P/E ratio)

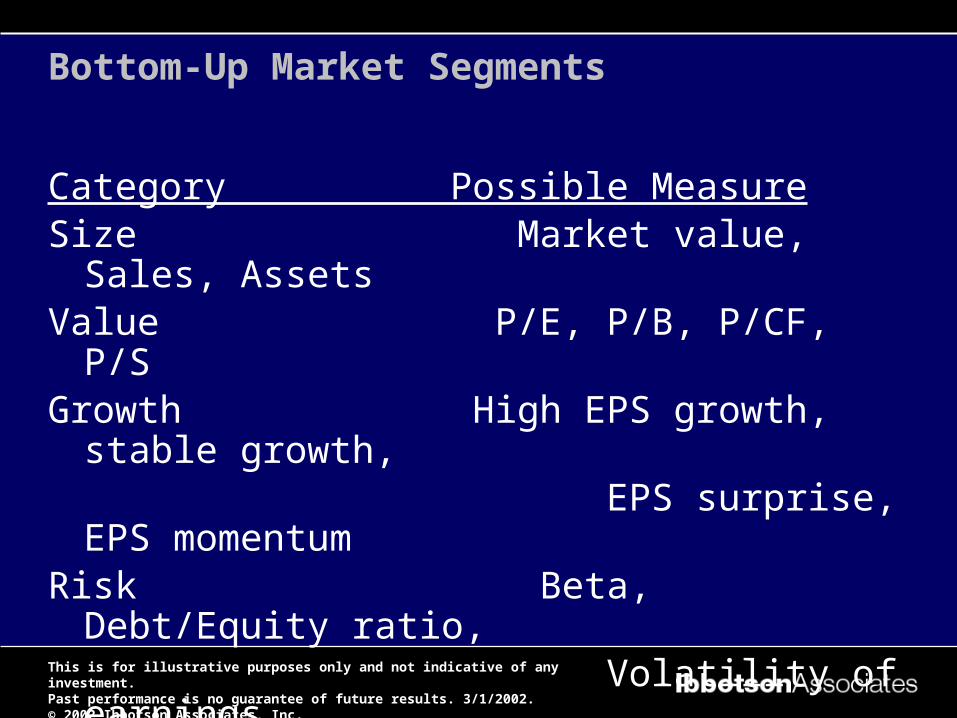

Bottom-Up Market Segments

Category Possible MeasureSize Market value, Sales, AssetsValue P/E, P/B, P/CF, P/SGrowth High EPS growth, stable growth, EPS surprise, EPS momentumRisk Beta, Debt/Equity ratio, Volatility of earnings

Hypothetical value of $1 invested at year-end 1925. Assumes reinvestment of income and no transaction costs or taxes.

1925-2001

$10

EndingWealth

3.1%

AverageReturnInflation

Small versus Large Stocks

$.10

$1

$10

$100

$1,000

$10,000

$17 3.8%

Treasury Bills

$51 5.3%

Government Bonds

$7,860 12.5%Small Company Stocks

10.7%Large Company Stocks $2,279

1925 1935 1945 1955 1965 1975 1985 2001

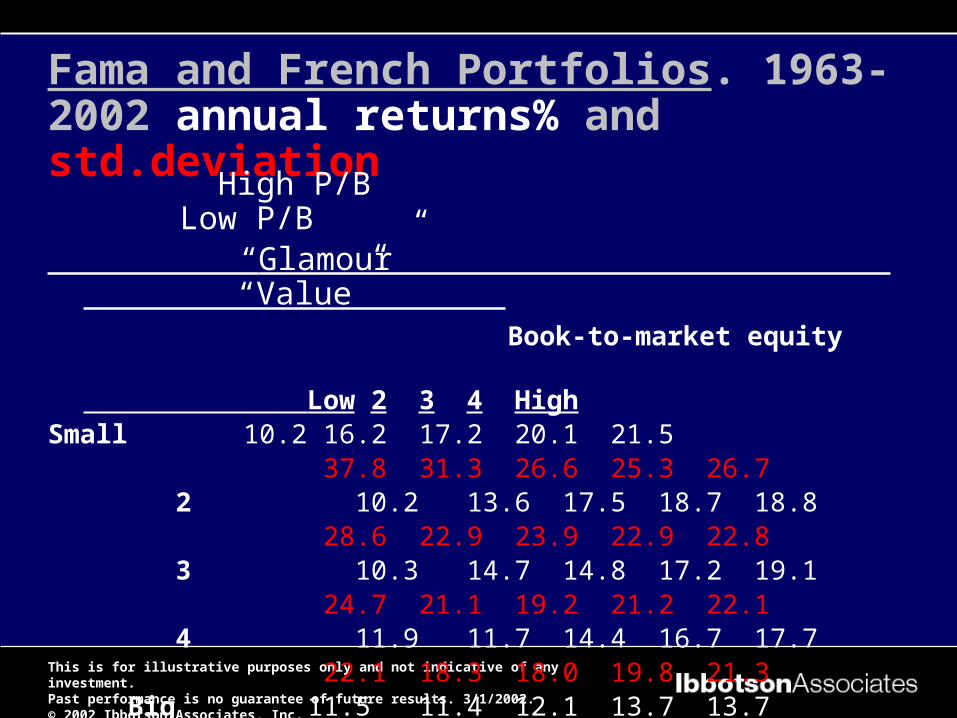

Fama and French Portfolios. 1963-2002 annual returns% and std.deviation

High P/B Low P/B “Glamour” “Value” Book-to-market equity

Low 2 3 4 HighSmall 10.2 16.2 17.2 20.1 21.5

37.8 31.3 26.6 25.3 26.7 2 10.2 13.6 17.5 18.7 18.8

28.6 22.9 23.9 22.9 22.8 3 10.3 14.7 14.8 17.2 19.1

24.7 21.1 19.2 21.2 22.1 4 11.9 11.7 14.4 16.7 17.7

22.1 18.3 18.0 19.8 21.3 Big 11.5 11.4 12.1 13.7 13.7

19.7 16.9 15.8 16.8 19.0

Style Investing

Construct a portfolio that invests in one of these market segments

e.g. Small-cap stocks, low-P/E stocks, etc…Value stocks (those that appear to be under-

priced according to various measures)– e.g. Low Price/Book value or Price/Earnings

ratiosGrowth stocks (above-average earnings per

share increases)– High P/E, possibly a price momentum strategy

Growth Stocks

Growth stocks are stocks of companies that have historically been able to grow their businesses faster than the average company and are expected to continue that growth. Growth is measured by observing the growth of company earnings, sales, or other factors.

Because growth companies are expected to grow faster than average, investors are willing to pay more for the stock of these companies than for value stocks relative to current earnings. These companies often pay little or no dividend because they are using most of their available cash to re-invest in the business to help it continue to grow.

Value Stocks

Value stocks are stocks of companies that have had historically slower growth of earnings or sales, or have recently experienced trouble of some kind causing a fall in stock price.

Many investors consider value companies to include turnaround opportunities, where a change in management, business strategy, or other factors could increase prospects and earnings for the company.

Value Stocks 2

Because current prospects for value stocks are not as robust as for growth stocks, value stocks sell for lower multiples of price-to-book and price-to-earnings.

Since growth prospects for value stocks are judged by the market to be relatively modest, the dividend yield is typically higher, which helps to attract and retain investors.

What Are Growth and Value Stocks?

Growth Stocks High growth rate of earnings,

sales Usually have high price-to-book,

price-to-earnings ratios Paying lower or no dividends

Risks Future growth does not occur as

expected Price-to-book, price-to-earnings

ratios decline unexpectedly

Value Stocks Slower growth of earnings and

sales Low price-to-book, price-to-

earnings ratios Higher dividend yields Turnaround opportunities

Risks Evaluation of stock as good

value is misread Difficult to stick to value policy

when prices are beaten down

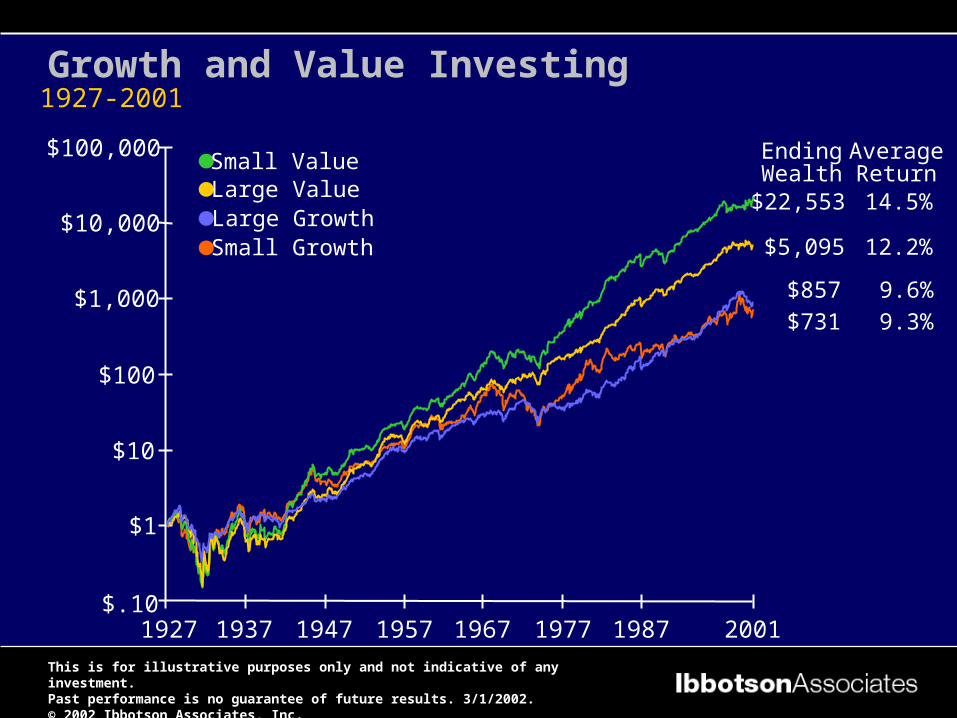

1927-2001Growth and Value Investing

1927 1937 1947 1957 1967 1977 1987 2001

$857

EndingWealth

$5,095

9.6%

AverageReturn

12.2%Large GrowthLarge Value

$.10

$1

$10

$100

$1,000

$10,000

$100,000

$731 9.3%

Small Growth

Small Value

$22,553 14.5%

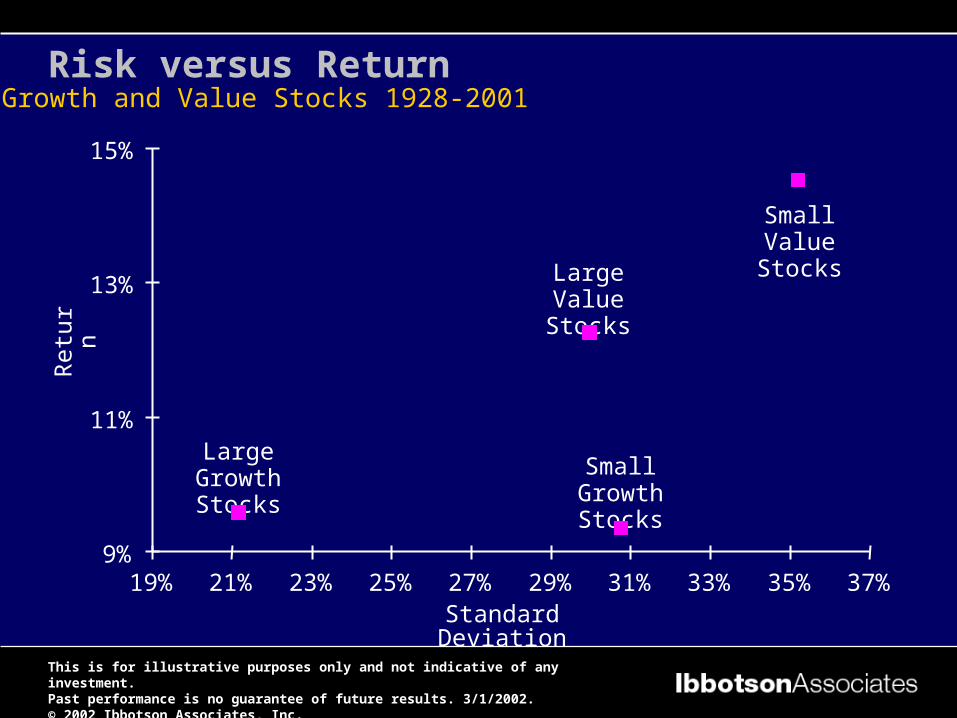

Growth and Value Stocks 1928-2001

Standard Deviation

Risk versus Return

9%

11%

13%

15%

Ret

urn

Large Value Stocks

Small Growth Stocks

Small Value Stocks

Large Growth Stocks

19% 21% 23% 25% 27% 29% 31% 33% 35% 37%

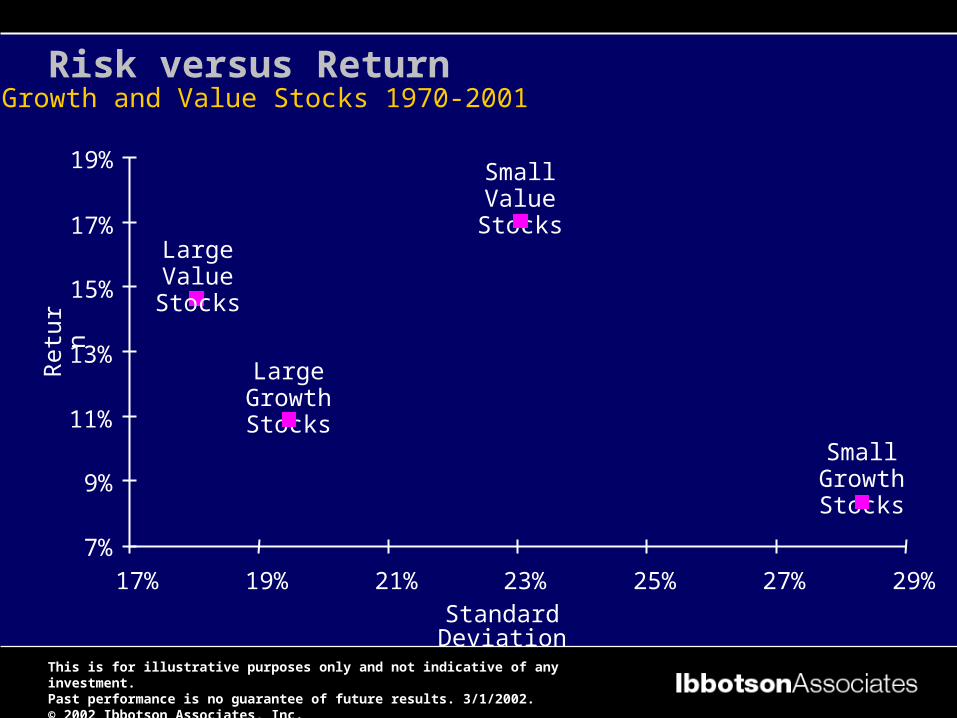

Growth and Value Stocks 1970-2001

Standard Deviation

Risk versus ReturnR

etur

n

7%

9%

15%

17%

19%

17% 19% 21% 23% 25% 27% 29%

Small Growth Stocks

Small Value Stocks

Large Growth Stocks

Large Value Stocks

11%

13%

*1920s based on the years 1928-1929. **Based on the years 2000-2001.

Compound Annual Rates of Return by DecadeGrowth and Value by Decade

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1920s* 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s**

All Growth Stocks

All Value Stocks

One-Year Growth and Value Trends 1928-2001

Based on the period 1928-2001. Data calculated using 12-month returns.

Large Growth

Ann

ual P

rem

ium

sGrowth versus Value Stocks

0%

40%

80%

120%

160%

200%

1928 1938 1948 1958 1968 1978 1988

Large Value

2001

Ann

ual P

rem

ium

s

0%

5%

10%

15%

20%

25%

30%

1930 1940 1950 1960 1970 1980 1990 2001

Three-Year Growth and Value Trends 1928-2001

Large Growth

Based on the period 1928-2001. Data calculated using 36-month returns.

Growth versus Value Stocks

Large Value

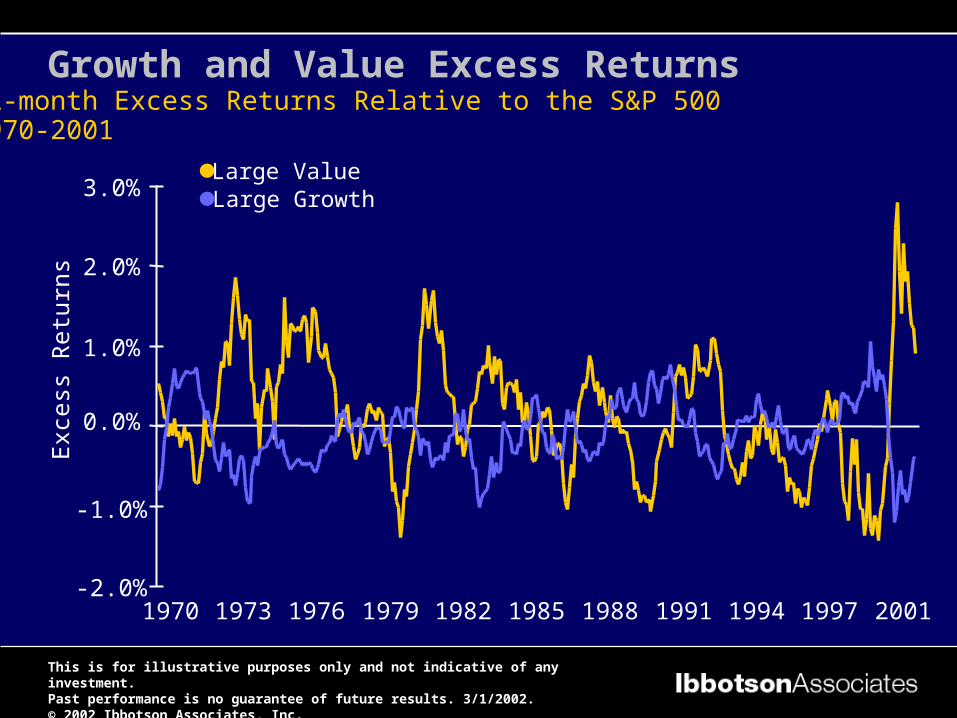

12-month Excess Returns Relative to the S&P 5001970-2001

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2001

Exc

ess

Ret

urns

Large GrowthLarge Value

Growth and Value Excess Returns

Year-end 1998–February 2001

$1,021

$1,136

$900

$1,000

$1,100

$1,200

$1,300

$1,400

Dec-98 Jun-99 Dec-99 Jun-00 Feb-01

$1,094

Diversified PortfolioLarge Value

Large Growth

Diversified portfolio represented by 50% growth stocks and 50% value stocks.

Growth and Value Diversification Benefits

Major ‘Bottom-Up’ Investment Styles

Common styles are based around size and value-growth distinctions: Large Cap-Value, Large Cap-Growth, Small Cap-Value and Small Cap-Growth

GARP (growth at a reasonable price)GARP attempts to cross the growth/value boundary by

searching for growth stocks that appear undervalued, or undervalued stocks that have unappreciated growth potential

Style-Neutral: tries to construct a portfolio with an even balance of value and growth stocks, small and large stocks

Exhibit 16.20

Other Investment Styles

Some styles based on Technical Analysis

Most common of these is Momentum Investing. Uses measures of relative strength such as relative return over the last six months. In such a case, the fund might only invest in stocks within the highest 6-month return decile, for example.

More on Value and Growth Investment Styles

Classifications such as Value = Low P/B are too simplistic and naïve

An intelligent investor will pay more (in P/B terms, for example, or P/E etc.) the better the business is. Thus there should be a trade-off between the quality of the business and its price. Value is not a one-dimensional concept

QARP

Some of the more successful investors (e.g. Warren Buffett) employ a more-sophisticated investment style that can be described as Quality at a Reasonable Price (QARP).

This name implies that the higher the quality of the business the higher the price you should be prepared to pay.

Such investors recognise that there is a tradeoff between quality and price. They usually leave themselves a margin of safety in case their analysis is wrong. (The price they are prepared to pay is always less than what they think it is worth.)

QARP

But what is the “quality of a business” ?

What are the features of a high quality business?

Buffett on Growth and Value

Most analysts feel they must choose between two approaches customarily thought to be in opposition: ‘value’ and ‘growth’. Many investment professionals see any mixing of the two as a form of intellectual cross-dressing. We view that as fuzzy thinking in which, it must be confessed, I myself engaged some years ago. In our opinion, the two approaches are joined at the hip: growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous and whose impact can be negative as well as positive.

Buffett on Growth and Value (2)

In addition, we think the very term ‘value investing’ is redundant. What is ‘investing’ if it is not the act of seeking value at least sufficient to justify the amount paid? Consciously paying more for a stock than its calculated value--in the hope that it can soon be sold for a still-higher price--should be labeled speculation which is neither illegal, immoral nor, in our view, financially fattening. Whether appropriate or not, the term ‘value investing’ is widely used. Typically it connotes the purchase of stocks having attributes such as a low ratio of price to book value, a low P/E ratio, or a high dividend yield.

Buffett on Growth and Value (3)

Unfortunately, such characteristics, even if they appear in combination, are far from determinative as to whether an investor is indeed buying something for what it is worth and is therefore truly operating on the principle of obtaining value in his investments. Correspondingly, opposite characteristics--a high P/E ratio, price to book and low dividend yield--are in no way inconsistent with a ‘value’ purchase. Similarly, business growth, per se, tells us little about value. It’s true that growth often has a positive impact on value. But such an effect is far from certain. For example investors have poured money into the domestic airline business to finance profitless growth.