equity markets and alternative investments …...equity markets and alternative investments teaching...

TRANSCRIPT

Equity Markets and Alternative Investments Teaching Program 2017-2018 Week 10 – November 21, 2017

Private Equity and Financial Sponsors: Investment Cycle, Domestic vs International

Marco Morelli - Chief Executive Officer, Banca Monte dei Paschi di Siena SpA

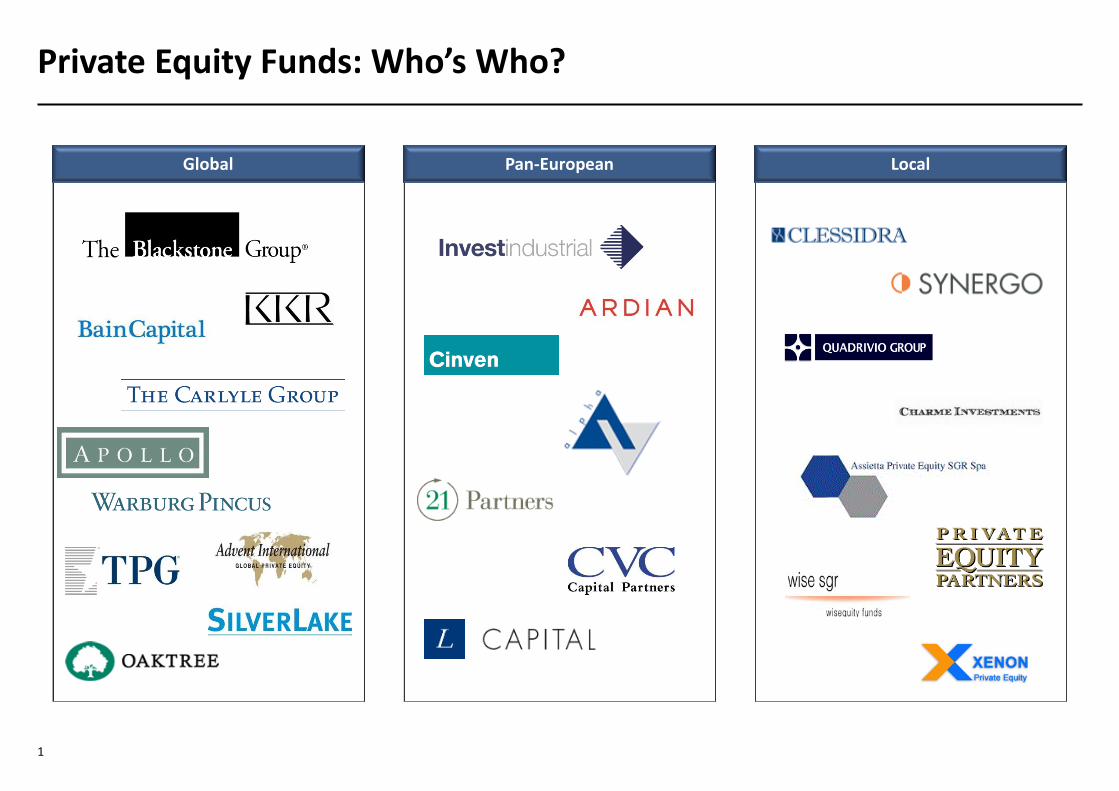

Global Global Global

1

Private Equity Funds: Who’s Who?

Pan-European Local Global

2

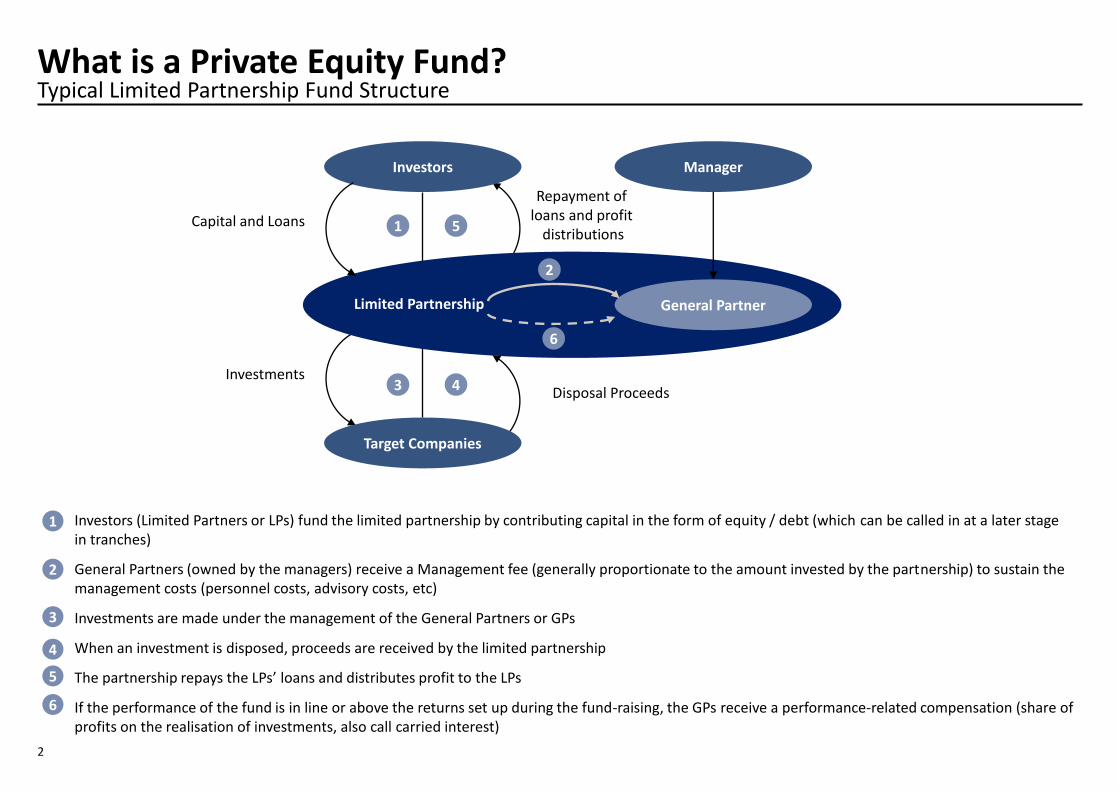

Typical Limited Partnership Fund Structure What is a Private Equity Fund?

Investors (Limited Partners or LPs) fund the limited partnership by contributing capital in the form of equity / debt (which can be called in at a later stage in tranches)

General Partners (owned by the managers) receive a Management fee (generally proportionate to the amount invested by the partnership) to sustain the management costs (personnel costs, advisory costs, etc)

Investments are made under the management of the General Partners or GPs

When an investment is disposed, proceeds are received by the limited partnership

The partnership repays the LPs’ loans and distributes profit to the LPs

If the performance of the fund is in line or above the returns set up during the fund-raising, the GPs receive a performance-related compensation (share of profits on the realisation of investments, also call carried interest)

1

2

3

4

5

6

General Partner

Manager Investors

Target Companies

1

Limited Partnership

5

6

3

2

Capital and Loans

Repayment of loans and profit

distributions

Investments Disposal Proceeds 4

3

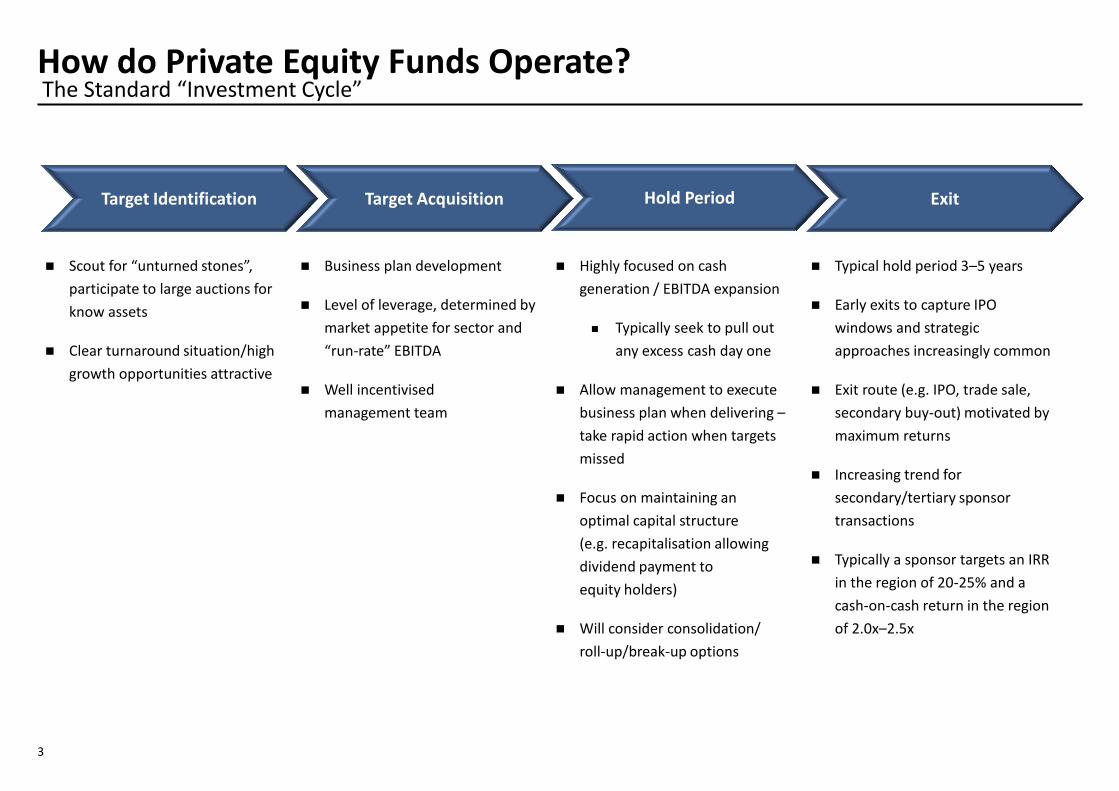

How do Private Equity Funds Operate?

Target Identification Target Acquisition Hold Period Exit

Scout for “unturned stones”,

participate to large auctions for

know assets

Clear turnaround situation/high

growth opportunities attractive

Business plan development

Level of leverage, determined by

market appetite for sector and

“run-rate” EBITDA

Well incentivised

management team

Highly focused on cash

generation / EBITDA expansion

Typically seek to pull out

any excess cash day one

Allow management to execute

business plan when delivering –

take rapid action when targets

missed

Focus on maintaining an

optimal capital structure

(e.g. recapitalisation allowing

dividend payment to

equity holders)

Will consider consolidation/

roll-up/break-up options

Typical hold period 3–5 years

Early exits to capture IPO

windows and strategic

approaches increasingly common

Exit route (e.g. IPO, trade sale,

secondary buy-out) motivated by

maximum returns

Increasing trend for

secondary/tertiary sponsor

transactions

Typically a sponsor targets an IRR

in the region of 20-25% and a

cash-on-cash return in the region

of 2.0x–2.5x

The Standard “Investment Cycle”

4

Examples of Recent Completed Exits with Italian Underlying

Target Route Sponsor Entry Exit(1) Sector

IPO +

Accelerated Placement

Jun-2011

EV: €1.2bn

Dec-2013

EV: €2.7bn Apparel

IPO+

Accelerated Placement

May-2011

EV: €1.4bn

Feb-2015

EV: €1.2bn(2) Retail

Sale to

Another Sponsor

(Apax Partners)

Jul-2007

EV: €0.4bn

Oct-2013

EV: €0.6bn Auto-Parts

____________________ (1) Valuation at first exit, in case of exits via multiple tranches (2) Value of OVS activities only, excluding separated assets (Coin, Excelsior, etc.)

Sale to

Strategic Buyer

(Volkswagen Group)

Feb-2008

EV: €0.6bn

Apr-2012

EV: €0.9bn Automotive

Sale to

Strategic Buyer

(LKQ Corporation)

Dec-2015

EV: €1.0bn Auto-Parts

Oct-2013

EV: €0.6bn

June-2008

EV: €0.9bn

May-2016

EV: €0.7bn Wellness

IPO +

Accelerated Placement

Sept-2006

EV: €0.9bn

May-2016

EV: €1.0bn Gaming

Sale to

Another Sponsor

(CVC Capital Partners)

5

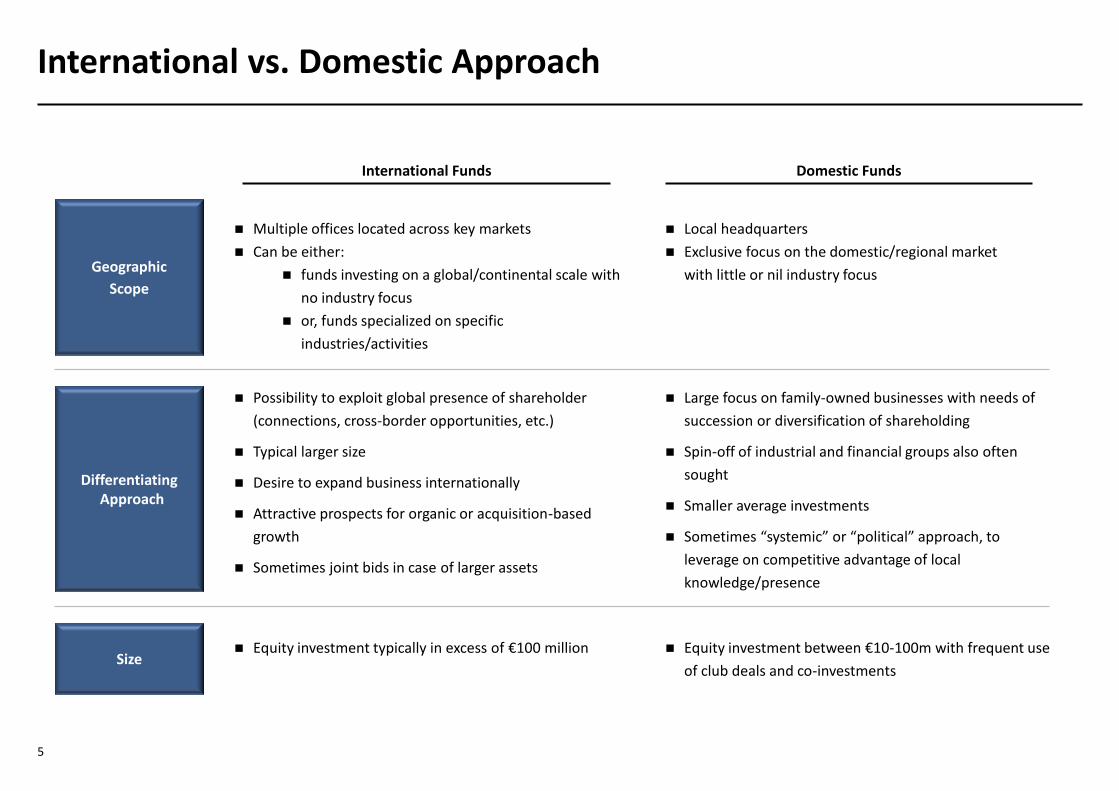

International vs. Domestic Approach

Differentiating Approach

Multiple offices located across key markets

Can be either:

funds investing on a global/continental scale with

no industry focus

or, funds specialized on specific

industries/activities

International Funds Domestic Funds

Local headquarters

Exclusive focus on the domestic/regional market

with little or nil industry focus

Equity investment typically in excess of €100 million Equity investment between €10-100m with frequent use

of club deals and co-investments

Possibility to exploit global presence of shareholder

(connections, cross-border opportunities, etc.)

Typical larger size

Desire to expand business internationally

Attractive prospects for organic or acquisition-based

growth

Sometimes joint bids in case of larger assets

Large focus on family-owned businesses with needs of

succession or diversification of shareholding

Spin-off of industrial and financial groups also often

sought

Smaller average investments

Sometimes “systemic” or “political” approach, to

leverage on competitive advantage of local

knowledge/presence

Size

Geographic

Scope

€

6

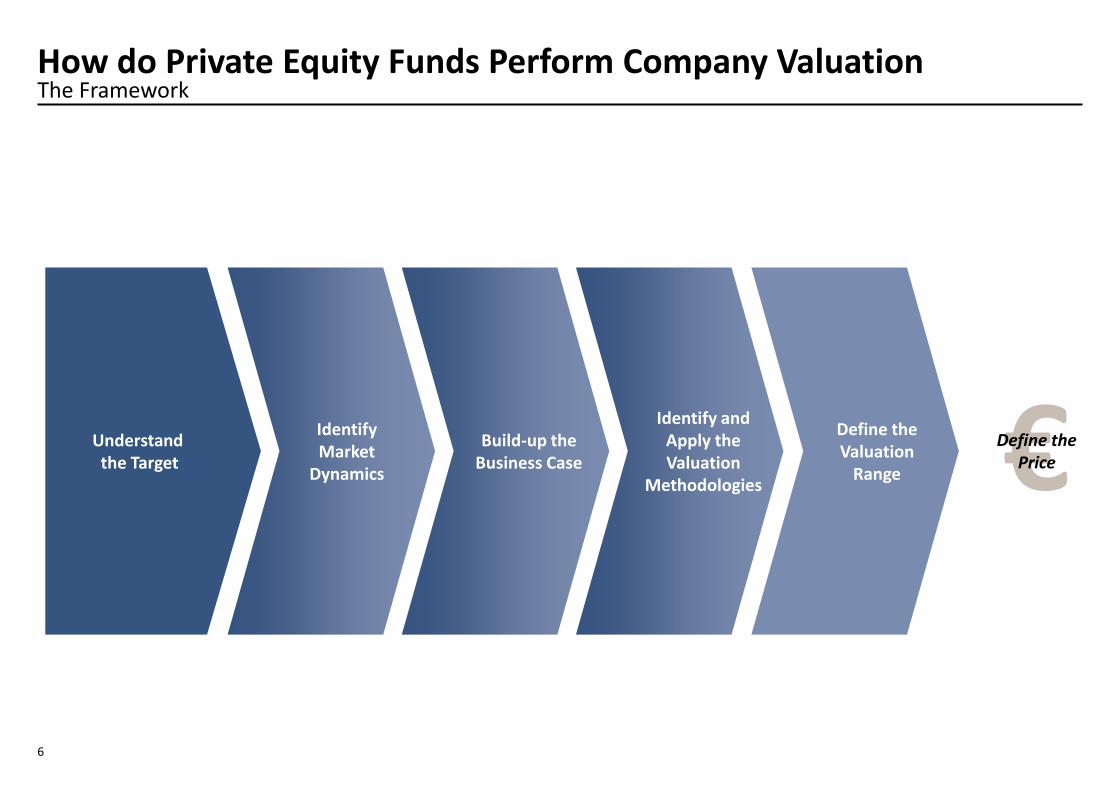

The Framework How do Private Equity Funds Perform Company Valuation

Define the Price

Identify Market

Dynamics

Build-up the Business Case

Identify and Apply the Valuation

Methodologies

Define the Valuation

Range

Understand the Target

7

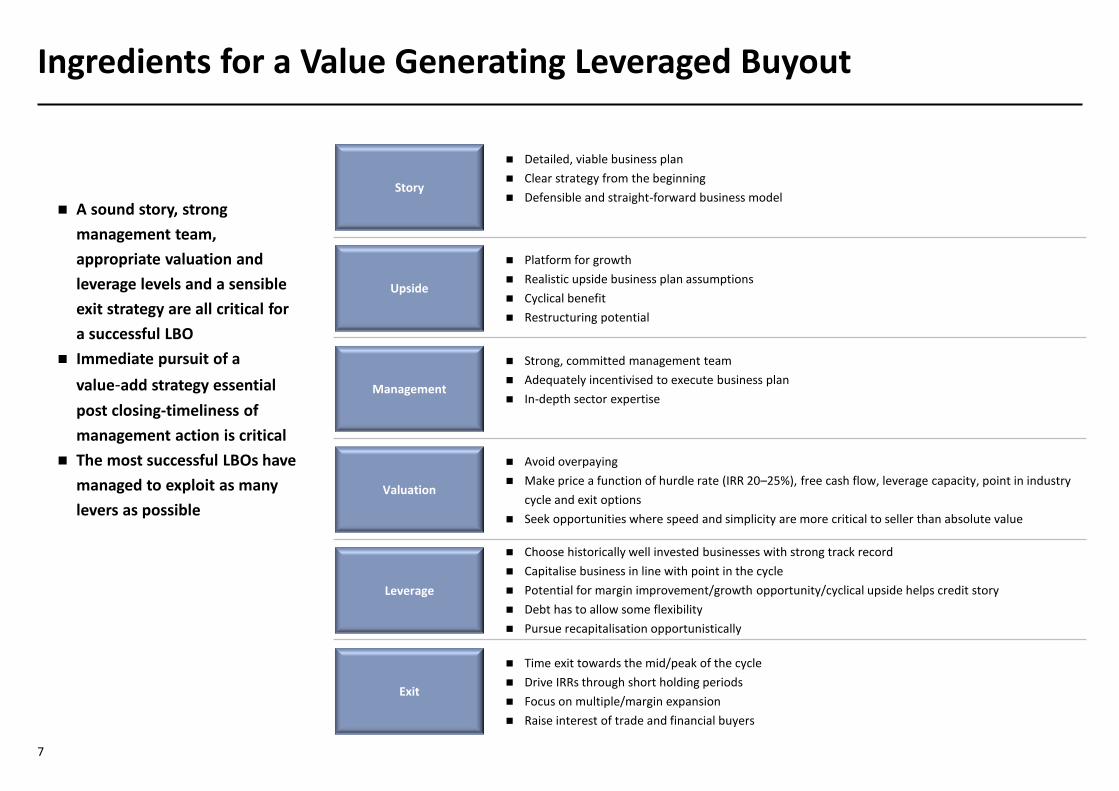

Ingredients for a Value Generating Leveraged Buyout

A sound story, strong

management team,

appropriate valuation and

leverage levels and a sensible

exit strategy are all critical for

a successful LBO

Immediate pursuit of a

value-add strategy essential

post closing-timeliness of

management action is critical

The most successful LBOs have

managed to exploit as many

levers as possible

Story

Management

Detailed, viable business plan

Clear strategy from the beginning

Defensible and straight-forward business model

Exit

Leverage

Valuation

Upside

Platform for growth

Realistic upside business plan assumptions

Cyclical benefit

Restructuring potential

Strong, committed management team

Adequately incentivised to execute business plan

In-depth sector expertise

Avoid overpaying

Make price a function of hurdle rate (IRR 20–25%), free cash flow, leverage capacity, point in industry

cycle and exit options

Seek opportunities where speed and simplicity are more critical to seller than absolute value

Choose historically well invested businesses with strong track record

Capitalise business in line with point in the cycle

Potential for margin improvement/growth opportunity/cyclical upside helps credit story

Debt has to allow some flexibility

Pursue recapitalisation opportunistically

Time exit towards the mid/peak of the cycle

Drive IRRs through short holding periods

Focus on multiple/margin expansion

Raise interest of trade and financial buyers

8

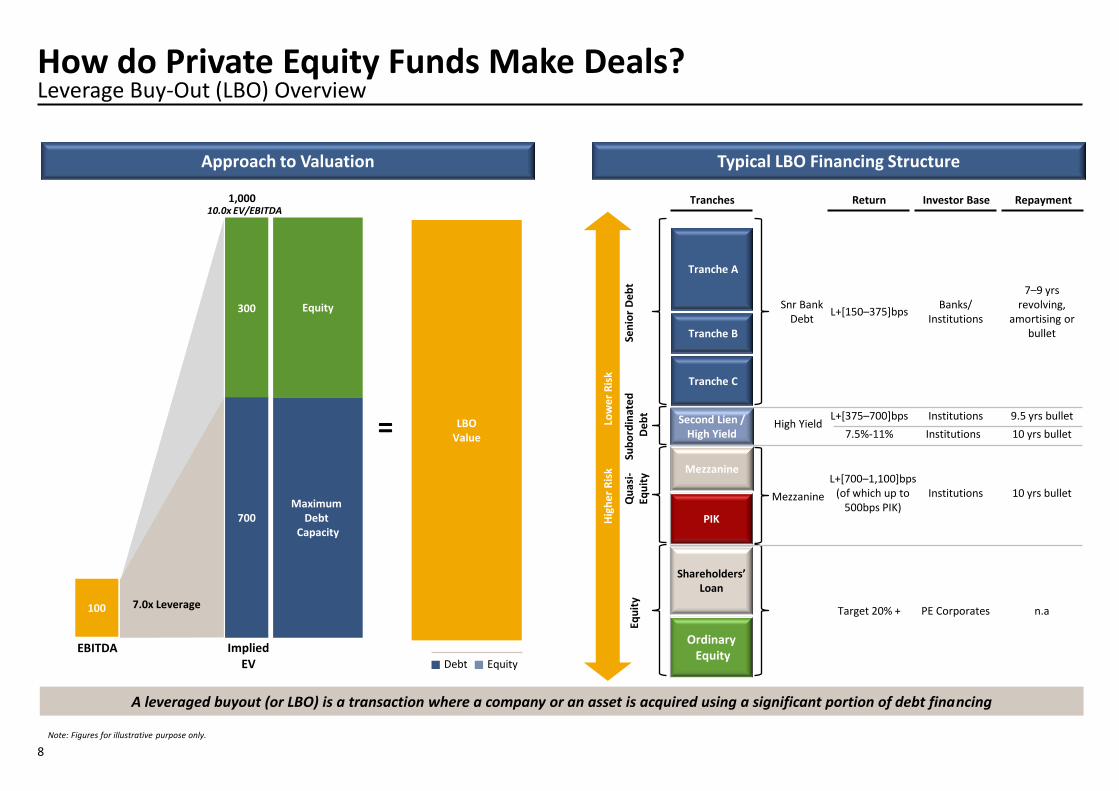

Leverage Buy-Out (LBO) Overview How do Private Equity Funds Make Deals?

Approach to Valuation Typical LBO Financing Structure

A leveraged buyout (or LBO) is a transaction where a company or an asset is acquired using a significant portion of debt financing

Note: Figures for illustrative purpose only.

Ordinary Equity

Shareholders’ Loan

PIK

Mezzanine

Second Lien / High Yield

Tranche C

Tranche B

Tranche A

Qu

asi-

Eq

uit

y Eq

uit

y

10.0x EV/EBITDA

Equity Debt

= LBO Value

7.0x Leverage

Equity 300

100

Maximum Debt

Capacity 700

1,000

Hig

he

r R

isk

Lo

we

r R

isk

Sub

ord

inat

ed

D

eb

t Se

nio

r D

eb

t

Tranches Return Investor Base Repayment

L+[150–375]bps Banks/

Institutions

7–9 yrs revolving,

amortising or bullet

Snr Bank Debt

L+[375–700]bps Institutions 9.5 yrs bullet High Yield

Mezzanine

7.5%-11% Institutions 10 yrs bullet

L+[700–1,100]bps (of which up to

500bps PIK) Institutions 10 yrs bullet

Target 20% + PE Corporates n.a

EBITDA Implied EV

9

Leverage Buy-Out (LBO) Overview (Cont’d) How do Private Equity Funds Make Deals?

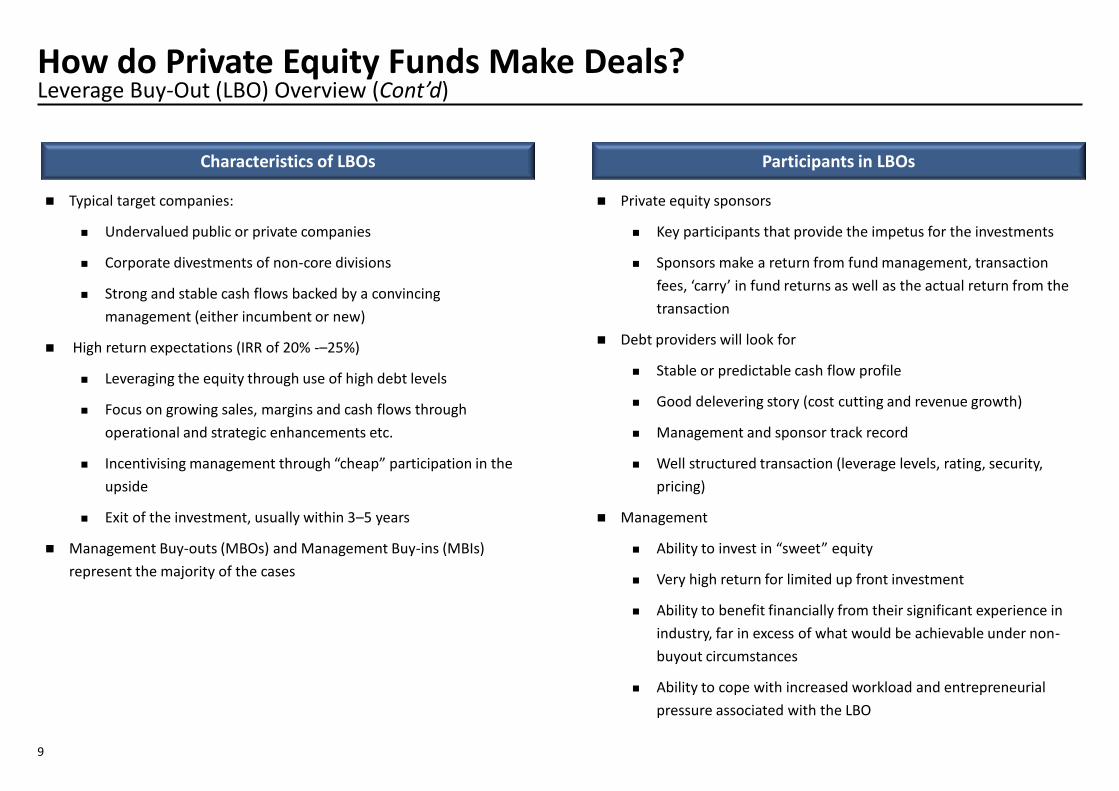

Typical target companies:

Undervalued public or private companies

Corporate divestments of non-core divisions

Strong and stable cash flows backed by a convincing

management (either incumbent or new)

High return expectations (IRR of 20% -–25%)

Leveraging the equity through use of high debt levels

Focus on growing sales, margins and cash flows through

operational and strategic enhancements etc.

Incentivising management through “cheap” participation in the

upside

Exit of the investment, usually within 3–5 years

Management Buy-outs (MBOs) and Management Buy-ins (MBIs)

represent the majority of the cases

Characteristics of LBOs Participants in LBOs

Private equity sponsors

Key participants that provide the impetus for the investments

Sponsors make a return from fund management, transaction

fees, ‘carry’ in fund returns as well as the actual return from the

transaction

Debt providers will look for

Stable or predictable cash flow profile

Good delevering story (cost cutting and revenue growth)

Management and sponsor track record

Well structured transaction (leverage levels, rating, security,

pricing)

Management

Ability to invest in “sweet” equity

Very high return for limited up front investment

Ability to benefit financially from their significant experience in

industry, far in excess of what would be achievable under non-

buyout circumstances

Ability to cope with increased workload and entrepreneurial

pressure associated with the LBO

10

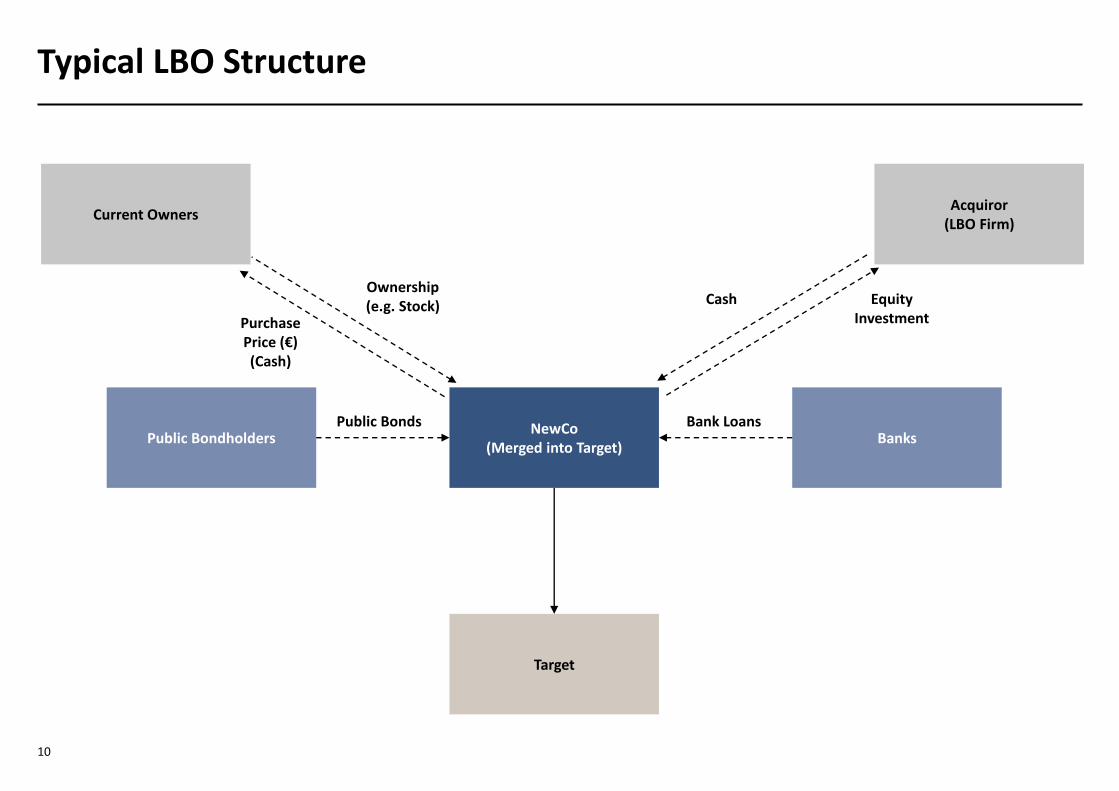

Typical LBO Structure

NewCo (Merged into Target)

Target

Public Bondholders Banks

Current Owners Acquiror

(LBO Firm)

Purchase Price (€) (Cash)

Equity Investment

Public Bonds Bank Loans

Cash Ownership (e.g. Stock)

11

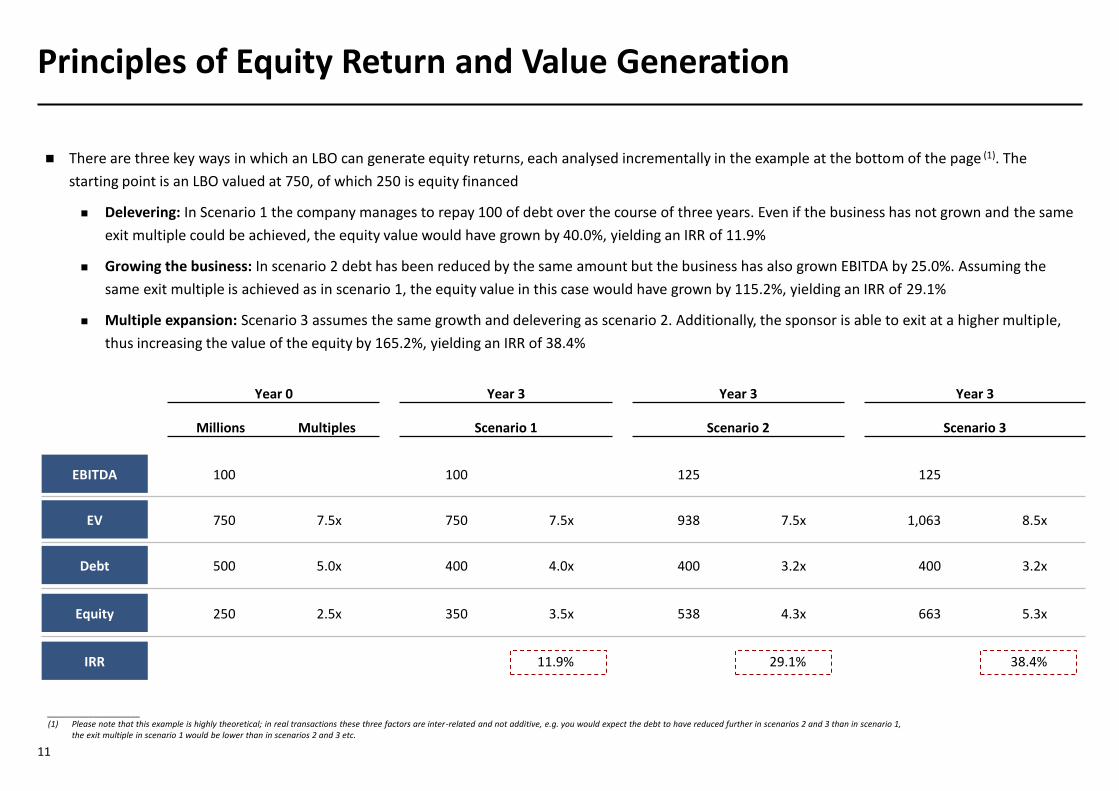

Principles of Equity Return and Value Generation

There are three key ways in which an LBO can generate equity returns, each analysed incrementally in the example at the bottom of the page (1). The

starting point is an LBO valued at 750, of which 250 is equity financed

Delevering: In Scenario 1 the company manages to repay 100 of debt over the course of three years. Even if the business has not grown and the same

exit multiple could be achieved, the equity value would have grown by 40.0%, yielding an IRR of 11.9%

Growing the business: In scenario 2 debt has been reduced by the same amount but the business has also grown EBITDA by 25.0%. Assuming the

same exit multiple is achieved as in scenario 1, the equity value in this case would have grown by 115.2%, yielding an IRR of 29.1%

Multiple expansion: Scenario 3 assumes the same growth and delevering as scenario 2. Additionally, the sponsor is able to exit at a higher multiple,

thus increasing the value of the equity by 165.2%, yielding an IRR of 38.4%

____________________ (1) Please note that this example is highly theoretical; in real transactions these three factors are inter-related and not additive, e.g. you would expect the debt to have reduced further in scenarios 2 and 3 than in scenario 1,

the exit multiple in scenario 1 would be lower than in scenarios 2 and 3 etc.

Year 0 Year 3 Year 3 Year 3

Millions Multiples Scenario 1 Scenario 2 Scenario 3

EBITDA 100 100 125 125

EV 750 7.5x 750 7.5x 938 7.5x 1,063 8.5x

Debt 500 5.0x 400 4.0x 400 3.2x 400 3.2x

Equity 250 2.5x 350 3.5x 538 4.3x 663 5.3x

IRR 11.9% 29.1% 38.4%

12

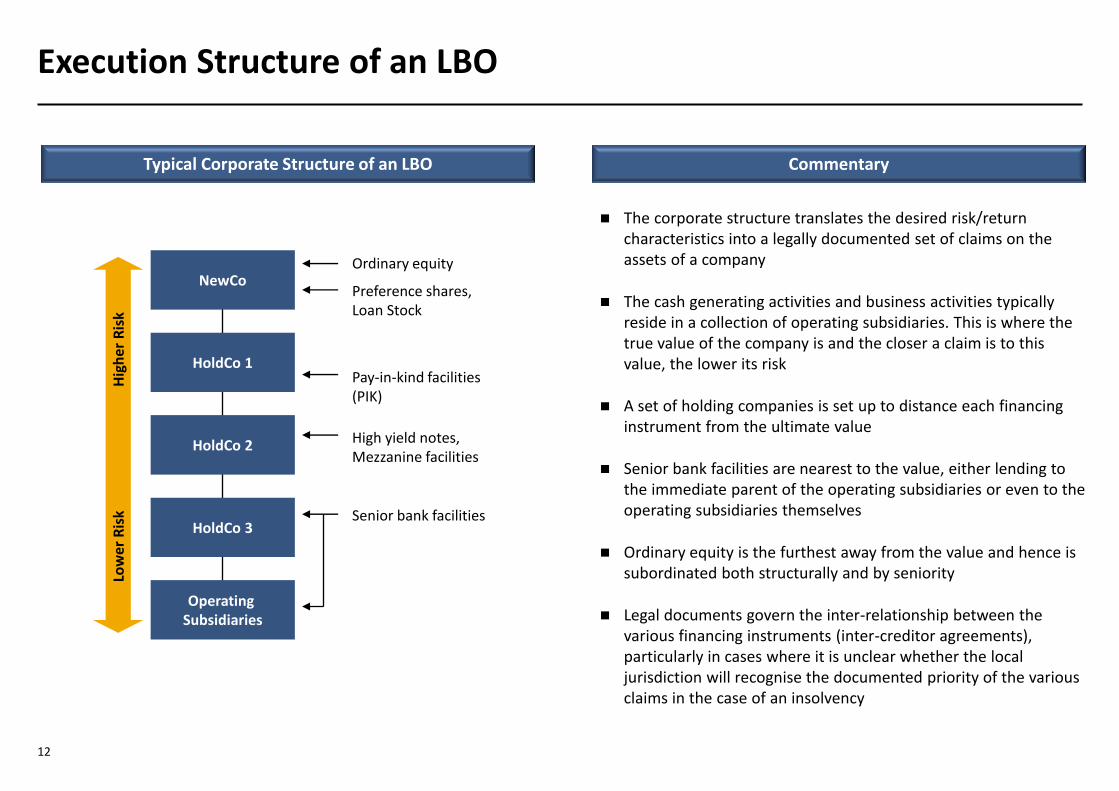

Execution Structure of an LBO

The corporate structure translates the desired risk/return characteristics into a legally documented set of claims on the assets of a company

The cash generating activities and business activities typically reside in a collection of operating subsidiaries. This is where the true value of the company is and the closer a claim is to this value, the lower its risk

A set of holding companies is set up to distance each financing instrument from the ultimate value

Senior bank facilities are nearest to the value, either lending to the immediate parent of the operating subsidiaries or even to the operating subsidiaries themselves

Ordinary equity is the furthest away from the value and hence is subordinated both structurally and by seniority

Legal documents govern the inter-relationship between the various financing instruments (inter-creditor agreements), particularly in cases where it is unclear whether the local jurisdiction will recognise the documented priority of the various claims in the case of an insolvency

Typical Corporate Structure of an LBO Commentary

NewCo

HoldCo 1

HoldCo 2

HoldCo 3

Operating Subsidiaries

Ordinary equity

Preference shares, Loan Stock

Pay-in-kind facilities (PIK)

High yield notes, Mezzanine facilities

Senior bank facilities

Low

er R

isk

H

igh

er R

isk

13

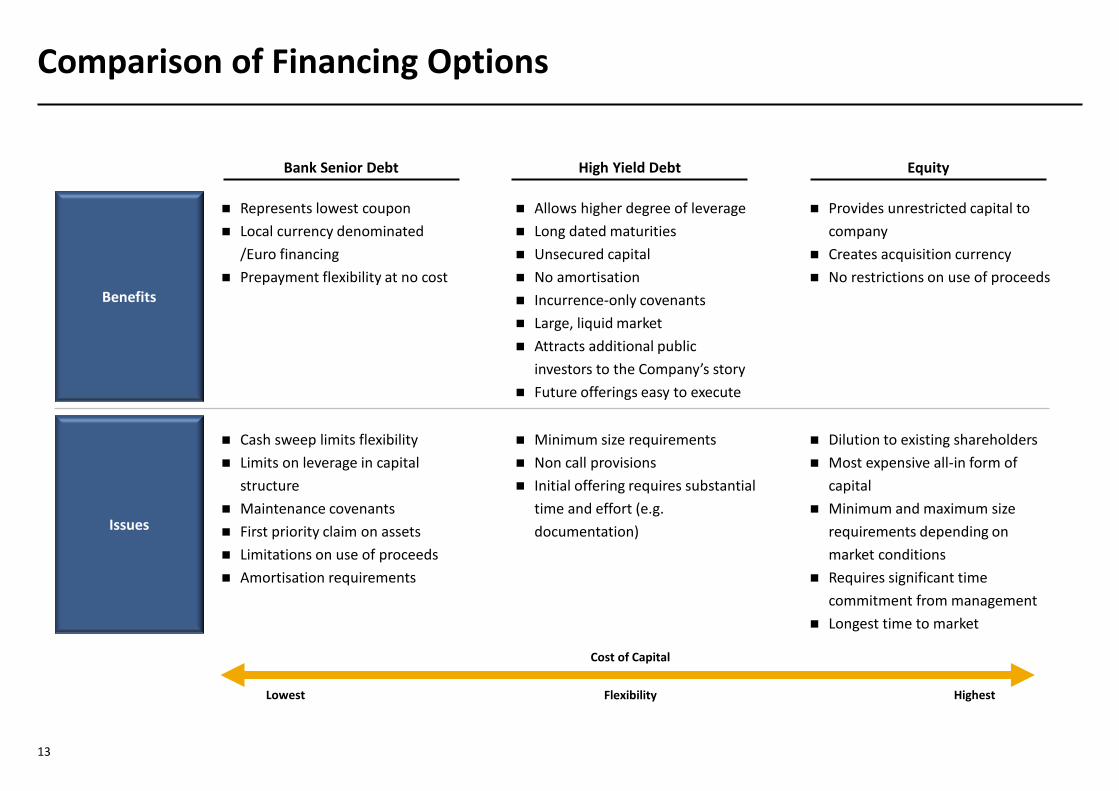

Comparison of Financing Options

Benefits

Issues

Represents lowest coupon

Local currency denominated

/Euro financing

Prepayment flexibility at no cost

Bank Senior Debt

Cash sweep limits flexibility

Limits on leverage in capital

structure

Maintenance covenants

First priority claim on assets

Limitations on use of proceeds

Amortisation requirements

High Yield Debt

Allows higher degree of leverage

Long dated maturities

Unsecured capital

No amortisation

Incurrence-only covenants

Large, liquid market

Attracts additional public

investors to the Company’s story

Future offerings easy to execute

Minimum size requirements

Non call provisions

Initial offering requires substantial

time and effort (e.g.

documentation)

Equity

Provides unrestricted capital to

company

Creates acquisition currency

No restrictions on use of proceeds

Dilution to existing shareholders

Most expensive all-in form of

capital

Minimum and maximum size

requirements depending on

market conditions

Requires significant time

commitment from management

Longest time to market

Cost of Capital

Lowest Highest Flexibility

14

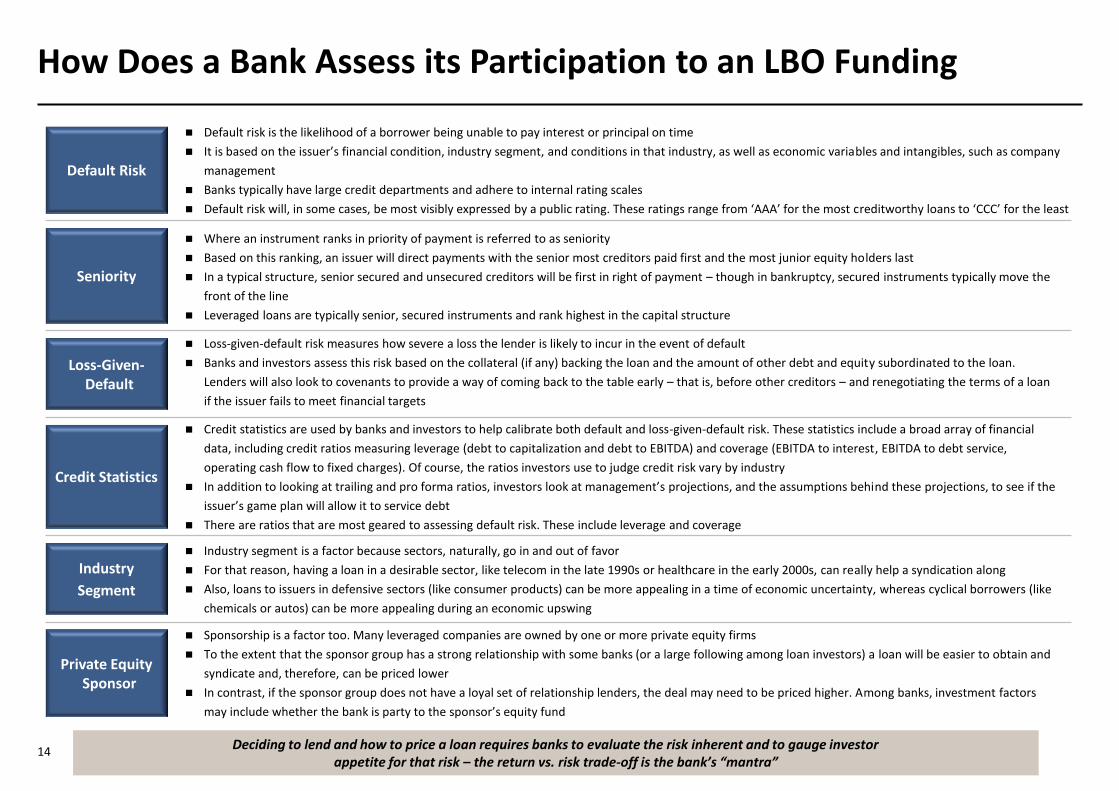

How Does a Bank Assess its Participation to an LBO Funding

Default Risk

Default risk is the likelihood of a borrower being unable to pay interest or principal on time

It is based on the issuer’s financial condition, industry segment, and conditions in that industry, as well as economic variables and intangibles, such as company

management

Banks typically have large credit departments and adhere to internal rating scales

Default risk will, in some cases, be most visibly expressed by a public rating. These ratings range from ‘AAA’ for the most creditworthy loans to ‘CCC’ for the least

Deciding to lend and how to price a loan requires banks to evaluate the risk inherent and to gauge investor appetite for that risk – the return vs. risk trade-off is the bank’s “mantra”

Seniority

Where an instrument ranks in priority of payment is referred to as seniority

Based on this ranking, an issuer will direct payments with the senior most creditors paid first and the most junior equity holders last

In a typical structure, senior secured and unsecured creditors will be first in right of payment – though in bankruptcy, secured instruments typically move the

front of the line

Leveraged loans are typically senior, secured instruments and rank highest in the capital structure

Loss-Given-Default

Loss-given-default risk measures how severe a loss the lender is likely to incur in the event of default

Banks and investors assess this risk based on the collateral (if any) backing the loan and the amount of other debt and equity subordinated to the loan.

Lenders will also look to covenants to provide a way of coming back to the table early – that is, before other creditors – and renegotiating the terms of a loan

if the issuer fails to meet financial targets

Credit Statistics

Credit statistics are used by banks and investors to help calibrate both default and loss-given-default risk. These statistics include a broad array of financial

data, including credit ratios measuring leverage (debt to capitalization and debt to EBITDA) and coverage (EBITDA to interest, EBITDA to debt service,

operating cash flow to fixed charges). Of course, the ratios investors use to judge credit risk vary by industry

In addition to looking at trailing and pro forma ratios, investors look at management’s projections, and the assumptions behind these projections, to see if the

issuer’s game plan will allow it to service debt

There are ratios that are most geared to assessing default risk. These include leverage and coverage

Industry

Segment

Industry segment is a factor because sectors, naturally, go in and out of favor

For that reason, having a loan in a desirable sector, like telecom in the late 1990s or healthcare in the early 2000s, can really help a syndication along

Also, loans to issuers in defensive sectors (like consumer products) can be more appealing in a time of economic uncertainty, whereas cyclical borrowers (like

chemicals or autos) can be more appealing during an economic upswing

Private Equity Sponsor

Sponsorship is a factor too. Many leveraged companies are owned by one or more private equity firms

To the extent that the sponsor group has a strong relationship with some banks (or a large following among loan investors) a loan will be easier to obtain and

syndicate and, therefore, can be priced lower

In contrast, if the sponsor group does not have a loyal set of relationship lenders, the deal may need to be priced higher. Among banks, investment factors

may include whether the bank is party to the sponsor’s equity fund

15

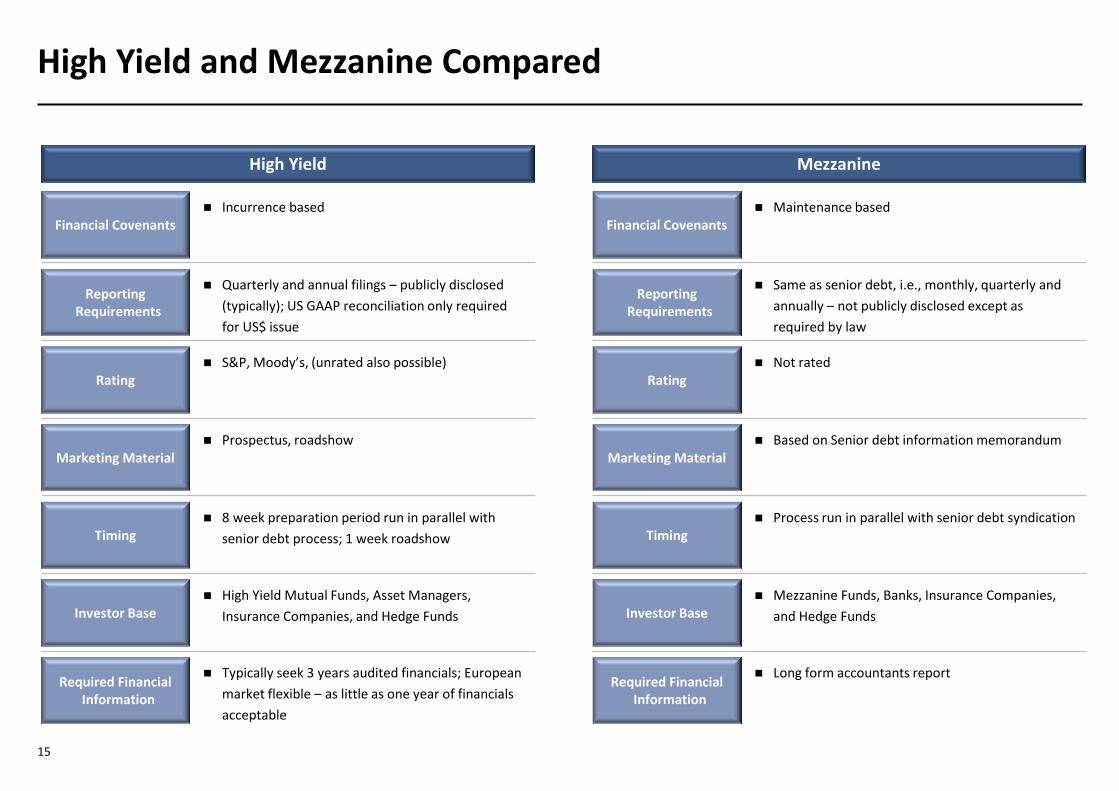

High Yield and Mezzanine Compared

High Yield Mezzanine

Financial Covenants

Rating

Incurrence based

Required Financial Information

Investor Base

Timing

Marketing Material

Reporting Requirements

Quarterly and annual filings – publicly disclosed

(typically); US GAAP reconciliation only required

for US$ issue

S&P, Moody’s, (unrated also possible)

Prospectus, roadshow

8 week preparation period run in parallel with

senior debt process; 1 week roadshow

High Yield Mutual Funds, Asset Managers,

Insurance Companies, and Hedge Funds

Typically seek 3 years audited financials; European

market flexible – as little as one year of financials

acceptable

Financial Covenants

Rating

Maintenance based

Required Financial Information

Investor Base

Timing

Marketing Material

Reporting Requirements

Same as senior debt, i.e., monthly, quarterly and

annually – not publicly disclosed except as

required by law

Not rated

Based on Senior debt information memorandum

Process run in parallel with senior debt syndication

Mezzanine Funds, Banks, Insurance Companies,

and Hedge Funds

Long form accountants report