equity house fmcg sector local research house...

TRANSCRIPT

Asiamoney’s

2013

Best Domestic

Equity House

Spotlight

2 October 2015

Disclosure: Bahana Securities does and seeks to do business with companies covered in its research reports. Investors should consider this report as only a single factor

in making their investment decision.

Please see the important disclaimer information on the back of this report

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

Tiphone Mobile Indonesia Sector: Telecommunication (Overweight)

BUY (Unchanged)

Rating momentum*:

Leonardo Henry Gavaza, CFA E-mail: [email protected] Phone: +6221 250 5081 ext. 3608

Price:IDR715–TP:IDR1,180 (From IDR1,060)

TP/consensus: 104%; TP momentum*: JCI:4,207

Reseller galore

Market share gain on extensive presence and excellent performance

Tiphone Mobile Indonesia (TELE), Telkomsel’s largest voucher distributor with

a 13% market share, is set to experience substantial revenue growth in the

next few years following its Simpatindo acquisition (Telkomsel’s voucher

distributor; 8% market share), in our view. Helped by TELE’s extensive

presence across the archipelago, with 180k active resellers and 27 clusters

that have continued to perform in the top tier among the 220 Telkomsel

clusters, TELE has been named the best Telkomsel distributor for 10 years in a

row. As Telkomsel has lowered the number of its clusters to 130 (3Q15), we

expect TELE to gain a larger area. As Telkomsel ranks its distributors regularly,

TELE, as of June this year, had managed to assume 2 additional clusters in

the Sumatera region from another voucher distributor whose performance

disappointed. Hence, we expect TELE’s voucher distribution market share to

improve from 18% in 1H15 to 20% in 2015F and 30% in 2017F.

Improving revenue sustainability through channel expansion

Telkomsel has three distribution channels: conventional, through resellers;

modern, through mini markets and super markets; and machine-to-machine

(M2M), through ATMs and Internet banking. TELE already has a strong presence

in the conventional and modern channels. In 2015, TELE is expanding into M2M

distribution, having recently signed an agreement with several private banks to

channel its voucher business using several banking platforms. This operation is

expected to start in 2H15, with annual sales guidance of around IDR3tn (15% of

TELE’s total annual voucher sales). Despite lower margins from the modern and

M2M channels, we expect these distribution network to help TELE diversify its

revenue stream and improve revenue sustainability ahead.

Handset bundling to provide growth

Following the acquisition of a 25% stake in TELE by PINS, a subsidiary of

Telekomunikasi Indonesia (TLKM IJ-IDR2,620, BUY-TP: IDR3,675), we expect

greater synergies from the handset bundling program as Telkomsel plans to

increase the total number of its smartphone users. Furthermore, TELE

distributes several popular handset brands such as Samsung, Blackberry, LG

and HTC, as well as its own brand, Tiphone. We estimate that strong growth in

3G handsets would result in 2015 handset distribution revenue of IDR6.4tn,

+18% y-y, before rising to IDR7tn in 2016, +10% y-y.

Sustained growth on defensive nature; BUY on higher IDR1,180 TP

In line with our OVERWEIGHT rating on the telco sector, we expect sentiment

on TELE to remain positive at this stage of the market cycle, supported by its

defensive nature. We see TELE entering a new growth phase on expansion of

its voucher and handset businesses. Overall, we expect TELE’s 2015F net profit

to reach IDR382bn, up 25% y-y, before rising 25% y-y to IDR479bn in 2016F.

Based on our DCF methodology (WACC: 10%), we assign a 12-month target

price of IDR1,180 (IDR1,060 previously) in line with our 4-9% upgrade in

2015F-16F net profit estimates. With 65% upside potential and 11%

underperformance in the past 3 months (exhibit 4), we reaffirm our BUY rating

on TELE. Risks: lower-than-expected revenue growth and operating margins.

Exhibit 1. Company information

Market cap (IDRbn/USDmn) : 5,091/347.6

3M avg.daily t.o.(IDRbn/USDmn) : 2.4/0.2

Bloomberg code : TELE IJ Source: Bloomberg

Exhibit 2. Shareholder information

Tiphone Mobile Group (%) : 77

Est. free float (%)

: 23 Source: Bloomberg

Exhibit 3. Key forecasts and valuations

Per 31 Dec 2014 2015F 2016F 2017F

Revenues (IDRb) 14,590 19,465 25,223 31,960

EBITDA (IDRb) 528 582 710 902

EBIT (IDRb) 507 602 732 926

Net profit (IDRb) 305 382 479 632

EPS (IDR) 43.3 54.3 68.1 89.8

EPS growth (%) 3.4 25.4 25.4 31.8

EV/EBITDA (x) 11.6 10.9 9.0 7.1

P/E (x) 16.5 13.2 10.5 8.0

FCFPS (IDR) (137) (14) (2) 17

FCF yield (%) (19.1) (2.0) (0.2) 2.3

BVPS (IDR) 355 399 454 527

P/BV (x) 2.0 1.8 1.6 1.4

DPS (IDR) 10 14 17 22

Div. yield (%) 1.4 1.9 2.4 3.1

ROAA (%) 7.2 7.3 8.2 9.7

ROAE (%) 15.7 14.4 16.0 18.3

EBIT margin (%) 3.5 3.1 2.9 2.9

Net gearing (%) 48.1 45.9 43.5 35.9

Source: Company, Bloomberg, Bahana estimates

Note: Pricing as of close on 02 October 2015; n.m. = not meaningful

Exhibit 4. Relative share price performance

Source: Bloomberg, Bahana

(3.4)

(5.1)

(11.4)

(2.6)

(1.1)

(6.6)

(12)

(10)

(8)

(6)

(4)

(2)

0

(12)

(10)

(8)

(6)

(4)

(2)

0

ytd 1M 3M 6M 9M 12M

(%) (%)

tele IJ relative to JCI

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 2

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 3

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

TABLE OF CONTENTS

INVESTMENT THESIS ………………………………………………………………………………………………………………………………………………………

FINANCIAL OUTLOOK ………………………………………………………………………………………………………………………………………………………

INVESTMENT RISKS ……………………………………………………………………………………………………………

MANAGEMENT PROFILE ………………………………………………………………………………………………………………

INDUSTRY ANALYSIS ……………………………………………………………………………………………………………………………

VALUATION …………………………………………………………………………………………………………………………

RECOMMENDATION ……………………………………………………………………………………………………………

P&L, BALANCE SHEET, RATIO ……………………………………………………………………………………………

5

9

10

12

14

16

17

18

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 4

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 5

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

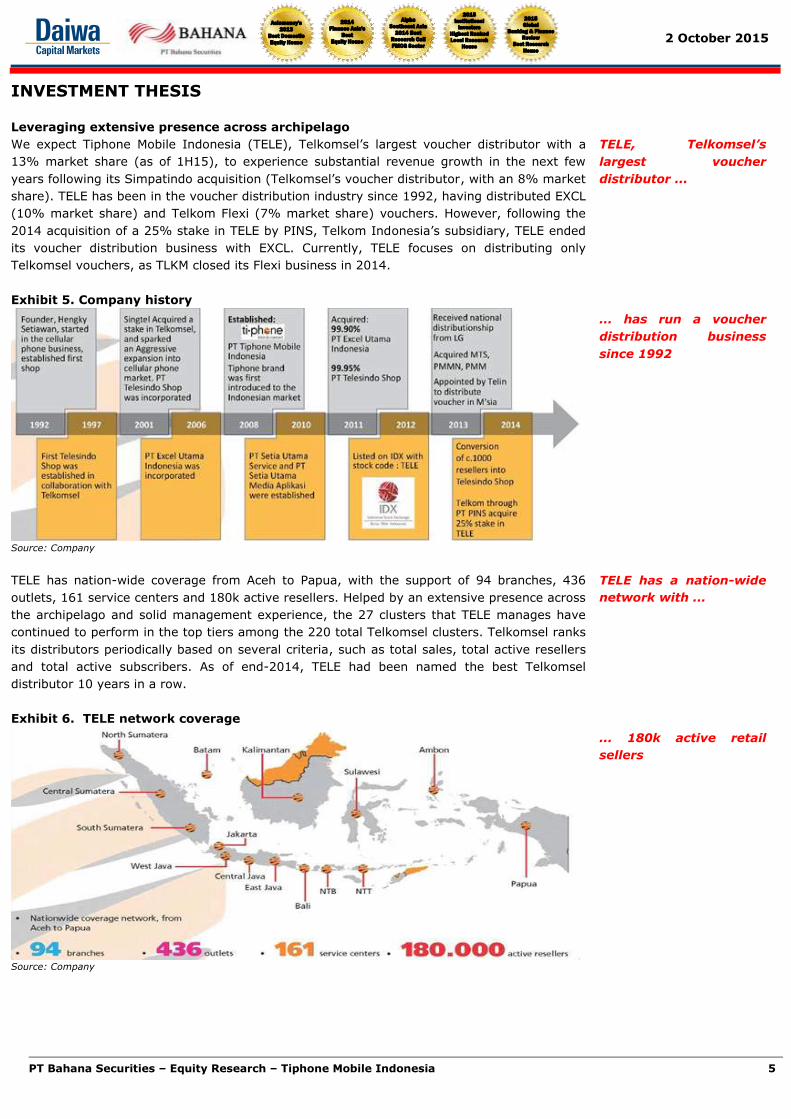

INVESTMENT THESIS Leveraging extensive presence across archipelago

We expect Tiphone Mobile Indonesia (TELE), Telkomsel’s largest voucher distributor with a

13% market share (as of 1H15), to experience substantial revenue growth in the next few

years following its Simpatindo acquisition (Telkomsel’s voucher distributor, with an 8% market

share). TELE has been in the voucher distribution industry since 1992, having distributed EXCL

(10% market share) and Telkom Flexi (7% market share) vouchers. However, following the

2014 acquisition of a 25% stake in TELE by PINS, Telkom Indonesia’s subsidiary, TELE ended

its voucher distribution business with EXCL. Currently, TELE focuses on distributing only

Telkomsel vouchers, as TLKM closed its Flexi business in 2014.

Exhibit 5. Company history

Source: Company

TELE has nation-wide coverage from Aceh to Papua, with the support of 94 branches, 436

outlets, 161 service centers and 180k active resellers. Helped by an extensive presence across

the archipelago and solid management experience, the 27 clusters that TELE manages have

continued to perform in the top tiers among the 220 total Telkomsel clusters. Telkomsel ranks

its distributors periodically based on several criteria, such as total sales, total active resellers

and total active subscribers. As of end-2014, TELE had been named the best Telkomsel

distributor 10 years in a row.

Exhibit 6. TELE network coverage

Source: Company

TELE, Telkomsel’s

largest voucher

distributor ...

... has run a voucher

distribution business

since 1992

TELE has a nation-wide

network with ...

... 180k active retail

sellers

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 6

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

In line with Telkomsel’s move to improve efficiency, the company plans to lower the number of

clusters to 130 in 4Q15. As Telkomsel would use its historical distribution ranking system to

appoint voucher distributors to its new clusters, we expect TELE to gain a larger area.

Furthermore, TELE just assumed 2 more clusters in the Sumatera region from another voucher

distributor that booked disappointing performance in June. Overall, we expect TELE’s

Telkomsel’s voucher distribution market share to improve from 18% in 1H15 to 20% in 2015F

and continue to rise to 30% in 2017F.

Exhibit 7. TELE voucher revenue, 2013-17F

Source: Company, Bahana Estimates

We expect TELE’s

voucher distribution

market share to reach

30% in 2017F ...

... with revenue of

IDR23.5tn in 2017F

8,1168,799

12,631

17,607

23,460

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

2013 2014 2015F 2016F 2017F

(IDRbn)

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 7

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

Improving revenue sustainability through channel expansion

Telkomsel has three distribution channels: conventional, through resellers; modern, through

mini markets and super market; and machine-to-machine (M2M) through ATMs and Internet

banking. Currently, TELE has a strong presence in the conventional market, as a main distributor

in 27 clusters out of Telkomsel’s total of 220 clusters. TELE’s areas are located throughout the

country, from Medan (North Sumatra) and Ketapang (West Kalimantan) to Jayapura (Papua). In

the modern channel, TELE has around an 80% share, as it sells vouchers through several strong

modern markets, including Indomaret, Alfamart, Carrefour, Superindo, Foodhall and several

others.

Exhibit 8. TELE modern channel partners

Source: Bahana

In 2015, TELE is expanding into M2M distribution as it recently signed an agreement with several

private banks to channel its voucher business using several banking platforms. This operation is

expected to start in 2H15, with annual sales guidance of around IDR3tn (30% of TELE’s total

annual voucher sales). Despite lower margins from the modern and M2M channels, we expect

this growth to provide revenue diversification for TELE, improving its revenue sustainability.

Exhibit 9. TELE M2M partners

Source: Company

TELE has a strong

presence in the

conventional channel

through its resellers,

and in the modern

channel through...

... Indomaret, Alfamaret

and Carrefour, among

others

In 2015, TELE is

expanding into the M2M

segment, through

agreements with...

... several private banks,

including BCA, CIMB

Niaga and Danamon

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 8

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

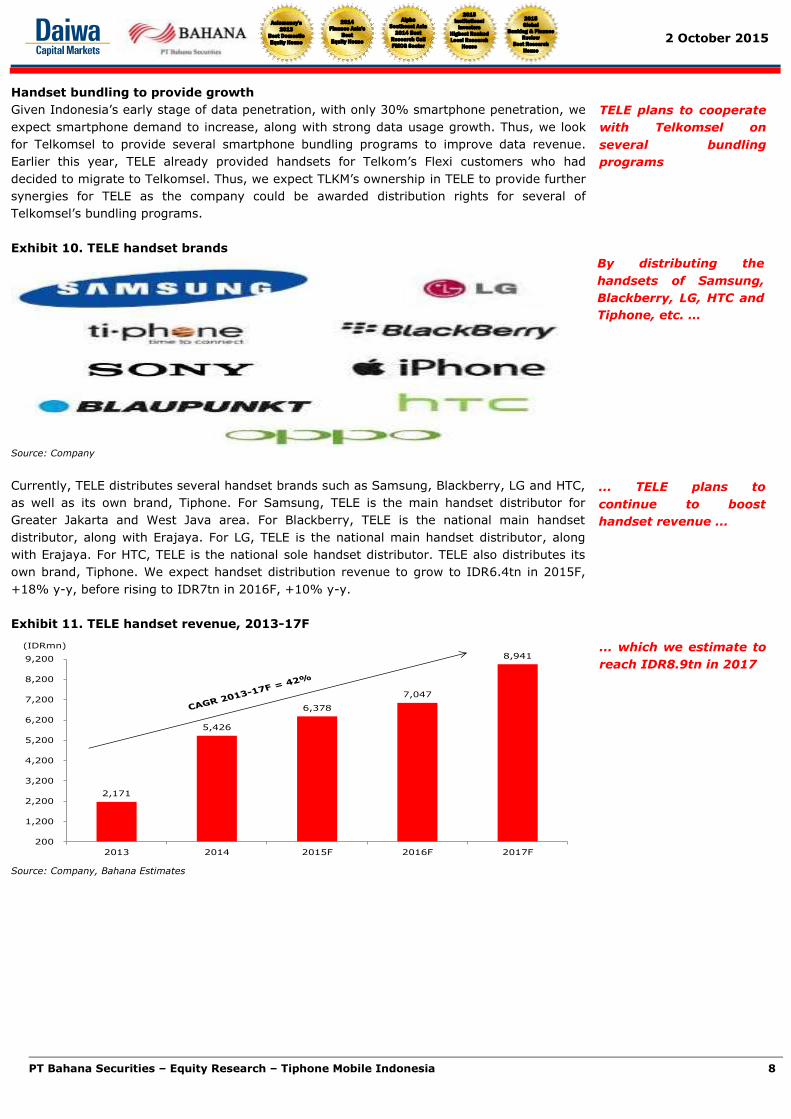

Handset bundling to provide growth

Given Indonesia’s early stage of data penetration, with only 30% smartphone penetration, we

expect smartphone demand to increase, along with strong data usage growth. Thus, we look

for Telkomsel to provide several smartphone bundling programs to improve data revenue.

Earlier this year, TELE already provided handsets for Telkom’s Flexi customers who had

decided to migrate to Telkomsel. Thus, we expect TLKM’s ownership in TELE to provide further

synergies for TELE as the company could be awarded distribution rights for several of

Telkomsel’s bundling programs.

Exhibit 10. TELE handset brands

Source: Company

Currently, TELE distributes several handset brands such as Samsung, Blackberry, LG and HTC,

as well as its own brand, Tiphone. For Samsung, TELE is the main handset distributor for

Greater Jakarta and West Java area. For Blackberry, TELE is the national main handset

distributor, along with Erajaya. For LG, TELE is the national main handset distributor, along

with Erajaya. For HTC, TELE is the national sole handset distributor. TELE also distributes its

own brand, Tiphone. We expect handset distribution revenue to grow to IDR6.4tn in 2015F,

+18% y-y, before rising to IDR7tn in 2016F, +10% y-y.

Exhibit 11. TELE handset revenue, 2013-17F

Source: Company, Bahana Estimates

TELE plans to cooperate

with Telkomsel on

several bundling

programs

By distributing the

handsets of Samsung,

Blackberry, LG, HTC and

Tiphone, etc. …

... TELE plans to

continue to boost

handset revenue ...

... which we estimate to

reach IDR8.9tn in 2017

2,171

5,426

6,378

7,047

8,941

200

1,200

2,200

3,200

4,200

5,200

6,200

7,200

8,200

9,200

2013 2014 2015F 2016F 2017F

(IDRmn)

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 9

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

FINANCIAL OUTLOOK Voucher business to support revenue growth

Supported by an improved voucher distribution market share as well as solid Telkomsel

revenue growth, we expect TELE’s voucher revenue to grow 40-44% y-y in 2015F-16F. For

the handset distribution segment, we expect more conservative revenue growth of 10-18% y-

y in 2015F-16F. Thus, we upgrade our 2015F-16F revenue expectation for TELE by 8-27% to

take into account its higher revenue from voucher business due to more clusters as well as

new deals with several private banks. All in all, we expect TELE to book 2015F revenue of

IDR19.5tn, +33% y-y, before continuing to grow 30% y-y to IDR25tn in 2016F. As most of

TELE’s distributors are small resellers selling low-nominal vouchers, TELE consistently books

lucrative vouchers margins. In 2015F-16F, we expect TELE to book gross margins of 4.97-

5.15% despite tight competition in the handset distribution business. We estimate

manageable operating expenses to translate into solid operating margins of 2.9-3.1% in

2015F-16F.

Exhibit 12. TELE earnings revisions, 2015F-17F

Source: Company, Bahana Estimates

Sustained solid net profit growth expected

As TELE is still in a significant growth phase, we expect its working capital needs to remain

above IDR250bn in both 2015F and 2016F. That said, we expect TELE to spend only around

IDR25bn each in 2015F-16F on capital expenditure, as the distribution business does not

require a huge fixed asset investment. In line with our upgrade in revenue, we also upgrade

our 2015F-16F net profit by 4-9%. Helped by solid EBIT generation, we expect TELE to record

2015F net profit of IDR382bn, +25% y-y, before continuing to grow 25% y-y to IDR479bn in

2016F.

Exhibit 13. TELE net profit, 2013-17F

Source: Company, Bahana Estimates

On the back of increased

market share in voucher

business coupled with

solid growth in

Telkomsel’s revenue...

... we upgrade 2015F-

16F net profit by 4-9%

Supported by solid EBIT

generation ...

... we expect TELE to

record 2016F net profit

of IDR479bn, +25% y-y

295 305

382

479

632

100

200

300

400

500

600

700

2013 2014 2015F 2016F 2017F

(IDRbn)

2015F 2016F 2017F 2015F 2016F 2017F 2015F 2016F 2017F

Revenue (IDRb) 18,113 19,936 - 19,465 25,223 31,960 7.5 26.5 -

EBITDA 552 639 - 582 710 902 5.3 11.2 -

EBITDA margin (%) 3.0 3.2 - 3.0 2.8 2.8

Opt profit (IDRb) 573 661 - 602 732 926 5.1 10.8 -

Opt margin (%) 3.2 3.3 - 3.1 2.9 2.9

Net profit (IDRb) 366 440 - 382 479 632 4.3 8.9 -

Net margin (%) 2.0 2.2 - 2.0 1.9 2.0

EPS (IDR) 52 63 - 54 68 90 4.3 8.9 -

Old New Change (%)

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 10

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

INVESTMENT RISKS

Dependence on retail/sales agents

As a distributor of mobile phones and pulses, the company and its subsidiaries are highly

dependent on the activities and results of the retail/sales agents in selling the company’s

products. The lower product sales of the company and its subsidiary to retail/sales agents

could materially and adversely affect the company’s financial performance, operational

activities, and prospects.

Changes in mobile phone technology

Mobile phones and other electronic devices have developed rapidly. As more advanced

technology emerges that differs from the products sold by the company and its subsidiary,

competitors’ mobile phones could materially, negatively, and directy affect the company’s

sales and result in unsold inventory.

Changes in consumer preferences

The increasing variety of brands and mobile phone features may influence a company’s

consumer preferences to move to another brand if the company does not actively renew their

products. These risks could materially and negatively affect the company’s financial

performance, operational activities, and prospects.

Changes in government regulations

The telecommunications sector is heavily regulated. Currently, the company’s main activities

in the trade of telecommunications equipment relates to mobile phones. If there is a change in

government regulations related to mobile phones, it could materially and adversely affect the

company’s financial performance, operational activities, and prospects.

Competition in mobile phone sales

Business competition in mobile phone sales is high. Various brands of mobile phones already

are sold freely, including cellular phones owned by the company. The increasing number of

brands offered freely could affect the company’s market share. These risks could materially

and negatively affect the company’s financial performance, operational activities, and

prospects.

Fluctuations in foreign exchange rates

The company faces the risk of fluctuations in foreign exchange rates as the company has a

USD47mn loan in a foreign currency to conduct its business activities. In addition, The

weakening of the rupiah could have a negatively material impact on the company’s business

activities, financial condition, and results of company’s operations.

Seasonal consumer purchasing patterns

The demand for mobile phones is seasonal, and is typically higher around holidays and feast

days, when new technologies are introduced by manufacturers as well as competitors,

depending on economic conditions, and the availability of products is at reasonable prices.

Seasonal buying patterns could materially and adversely affect the company’s cash flow.

Highly dependent on

retail/sales agents

Changes in mobile

technology are dynamic

Increases in brands and

mobile phone features

could affect consumer

preferences

Changes in government

telecommunications

regulations could affect

operational activities

Market share could be

affected by the

increasing number of

competitors in mobile

phone sales

The risk of fluctuations

in foreign exchange

rates may affect

revenue

Seasonal consumer

buying patterns …

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 11

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

Inability to launch innovations of products and services

One of the factors that may affect sales is the company’s ability to develop and launch new

products and services in accordance with prevailing trends. If the company is unable to

provide such products, it could lose market share and competitiveness, adversely affecting

growth, revenue and prospects.

Decrease in product quality

The company does not produce its own cell phone, so there is the possibility of a decline in

product quality. This could cause a decline in market share and competitiveness, which could

materially and adversely affect the company’s financial performance, operational activities,

and prospects.

Changes in management and key employees

Currently, the company’s performance is influenced by the performance by management and

the employees. Changes in management and key employees could materially and negatively

affect the company’s financial performance, operational activities, and prospects.

.. affect ability to launch

product and service

innovations, affecting

sales

A decrease in product

quality could cause a

decline in market share

Changes in management

and key employees

could affect

performance

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 12

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

MANAGEMENT PROFILE

Name and current position Previous position

Work experience in

industry

(years)

Board of Commissioners

1. Hengky Setiawan

(President Commissioner)

Director of PT Telesindo Shop

Director of PT Setia Utama Investama

Director of PT Setia Utama Towerindo

Director of PT Akses Makmur Bersama

20

2. Ferry Setiawan

(Commissioner)

Director of PT Setia Utama Media Aplikasi

Director of PT Esa Utama Inti Persada

Director of PT Pulsa Inti Nasional

Director of PT Excel Utama Indonesia

13

3. Mustapa Wangsaatmadja

(Commissioner)

President Director of PT PINS Indonesia

Commissioner of PT Admedika

Head of Department of Tech Recitation –

MASTEL

VP Innovation Strategy & Synergy of

Telekomunikasi Indonesia (Persero)

25

4. Lukman Hadikusumo

(Independent Commissioner)

Financial Consultant of PT Global Teleshop

President Director of PT Perkasa Finance

President Director of Bank Bumiputera

Money market group Head of Citibank

10

5. Achmad Herlanto Anggono

(Independent Commissioner) Audit Commitee and Risk Management of Bank

ANZ

Audit Commitee and Risk Management of PT

Energi Mega Persada Tbk

Compliance Director and Risk Management of

Bank Maybank Indocorp

Expert Group on Financial Operations

Management SBM ITB

-

Total working experience (years) 79

Average working experience (years) 14 Source: Company

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 13

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

Name and current position Previous position

Work experience in

industry

(years)

Board of Directors

1. Tan Lie Pin

(President Director)

Vice President Director of TELE

Vice Director Business Development of PT

Telesindo Shop

Country Manager (Koordinator Wilayah) of PT

Telechoice Indonesia

Sales Director of PT Teletama Artha Mandiri

18

2. Rukmono Cahyadi

(Business Development

Director)

GM Sales Regional Sales Central Java and

Yogyakarta of PT Telkomsel

GM Product Pricing of PT Telkomsel

GM Device Management of PT Telkomsel

GM Sales North Sumatera Region of PT

Telkomsel

24

3. Andry Ryanto

(Marketing Director)

General Manager of PT Telesindo Shop

Balikpapan

Branch Manager of PT Telesindo Shop Bandung

Sales Manager of PT Cahaya Hyundai

Coordinator Sales of PT Auto Cipta Karya Isuzu

13

4. Meiyati Jawidjaja

(Finance Director/

Independent Director)

GM Finance & Accounting PT Telesindo Shop

Audit Manager of PT Paragon

Head of Internal Audit of PT Primaswadana

Perkasa

Finance Manager of PT Rasa Indoselera

8

Total working experience (years) 63

Average working experience (years) 16

Source: Company

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 14

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

INDUSTRY ANALYSIS

Data migration period to benefit smartphone sellers

Over the past few years, the telecom industry has been experiencing a move from its legacy

business, which consists of voice and SMS, to digital business. This move has accelerated over

the past two years, as sector data usage has increased 8 times from 1Q13 to 4Q14 (exhibit

12). Given Indonesia’s early stage of data penetration, with only 50% data users and 30%

smartphone penetration, we believe data segment revenue should continue to boost the

sector’s long-term revenue growth. Thus, we think low smartphone penetration brings huge

opportunities for smartphone sellers such as TELE to benefit from the expected growth in

smartphone demand.

Exhibit 14. Sector data usage, 2Q13-2Q15

Source: Company

Telkomsel continues to dominate

In the past few quarters, ISAT has gained subscribers and revenue market share from EXCL,

as ISAT has a more robust network following its modernization phase, while EXCL is focusing

on its new value strategy. However, with a total subscriber base of 141mn (as of 3M15),

representing a 55% market share among the big 3, Telkomsel has maintained its dominance

in the telecom sector. Furthermore, Telkomsel has maintained its price leadership, as shown

by its high ARPU of IDR39k, much higher than those of ISAT and EXCL of around IDR29k.

Exihibit 15. Big 3 subscribers, 2Q13-2Q15

Source: Company

Expected increase in

smartphone penetration

rate ...

... should support data

usage to continue its

strong growth phase

Telkomsel continues to

be the dominant player

...

... with the total number

of subscribers reaching

141mn and a 55%

market share among the

big 3

0

20

40

60

80

100

120

140

0

10

20

30

40

50

60

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

EXCL ISAT TLKM (RHS)

(Petabytes) (Petabytes)

120.0

125.0

130.0

135.0

140.0

145.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

EXCL ISAT TLKM (RHS)

(mn subs) (mn subs)

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 15

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

Telkomsel’s strong revenue growth to support voucher business

Supported by strong data usage growth, Telkomsel booked a strong revenue CAGR of 11% in

2011-14. As of 3M15, Telkomsel’s revenue grew 12% y-y, with data usage growth of 110% y-

y. We expect this trend to continue as smartphone penetration is still low and expected long-

term GDP growth still looks attractive at 5% y-y in 2015F-17F, as 50% of the country’s

population is around 10-34 years old (young, productive and high-consuming age group).

Furthermore, around 98% of total Telkomsel subscribers are pre-paid customers who use

vouchers to top up their balances. Thus, we expect Telkomsel to see strong revenue growth to

improve voucher demand.

Exhibit 16. Telkomsel revenue, 2012-2015F & 6M14-6M15

Source: Company

Telkomsel has three main voucher distribution channels

Telkomsel has three distribution channels – conventional, modern and M2M. In the conventional

segment, Telkomsel divides Indonesia into 220 clusters, and appoints one voucher distributor for

every cluster. The voucher distributor then uses a huge number of resellers to sell vouchers to

customers. In the modern market segment, the vouchers are sold through modern channels

such as minimarkets, super markets and department stores. In the M2M segment, vouchers are

sold through banking channels such as ATMs, Internet banking and mobile banking.

In terms of margins, distributors in the conventional segment usually see higher margins than

distributors in the modern and M2M channels, as low-nominal-value vouchers are usually more

popular in the conventional segment while high-nominal-value vouchers usually are more

popular in the modern and M2M segments. In the voucher distribution industry, the lower the

nominal value, the higher the margin.

Exhibit 17. Telkomsel voucher distribution channels

Source: Company

With 98% Telkomsel’s

subscribers still using

top-ups, we expect

voucher demand to

continue to see solid

growth ...

... in line with

Telkomsel’s strong

revenue growth

3 distribution channels

Conventional segment

margins are typically

higher than those of

other segments

Distribution channels

77,143

82,967

89,696

98,258

50,000

60,000

70,000

80,000

90,000

100,000

2012 2013 2014 2015F

(IDRbn)

43,542

48,840

40,500

42,000

43,500

45,000

46,500

48,000

49,500

6M14 6M15

(IDRbn)

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 16

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

VALUATION

Looks attractively valued, with solid growth prospects

In terms of valuation, regional peers are trading at a 2016F PE of 9.7x with expected EPS

growth of 20% y-y. Despite trading above the regional average at a 2016F PE of 10.5x (8%

premium to regional peers), TELE still looks attractive on expected strong growth, as its 2016F

EPS growth of 25% y-y is much higher than the peer expectation of 20% y-y. Compare to its

regional peers, TELE also has stronger 2016F ROE of 16.0% (regional peers average: 9.6%).

Thus, at this stage of the market cycle, we believe that TELE is attractively valued given its

sustained solid growth ahead as well as attractive ROE.

Exhibit 18. Telco retail companies: regional valuation, 2016F

M a rk e t C a p 2 0 16 F 2 0 16 F 2 0 16 F 2 0 16 F 2 0 16 F 2 0 16 F

C o m pa ny ( U S D bn)

IN D O N E S IA 0 .5 9 .3 2 2 .0 8 .2 1.3 0 .4 14 .3

Erajaya Swasem bada 0.1 5.6 11.2 5.5 0.5 0.5 8.9

T ipho ne M o bile Indo nes ia 0.3 10.5 25.4 9.0 1.6 0.4 16.0

A S IA 7 .5 9 .7 2 0 .3 9 .0 1.0 0 .4 9 .3

Synnex Techno lo gy 1.6 9.1 11.6 15.5 1.1 0.8 12.7

D igital C hina 1.0 16.0 na 14.8 1.0 na 6.8

R edingto n India 0.7 10.1 35.5 7.6 1.6 0.3 16.8

Ingram M ic ro 4.2 8.3 26.1 5.3 0.8 0.3 7.4

G lo ba l we igh t e d a v e ra ge 8 .0 9 .7 2 0 .4 8 .9 1.0 0 .4 9 .6

P E R ( x) E P S gwt . ( %) E V / E B IT D A ( x) P B V ( x) P E G ( x) R O E ( x)

Source: Bloomberg, *Bahana estimates for Indonesia companies

TELE trades at a

premium to...

... regional telco retail

peers, which trade at a

2016F PE of 9.7x with

expected EPS growth of

20% y-y

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 17

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

RECOMMENDATION

BUY with TP of IDR1,180

In line with our OVERWEIGHT rating in the telco sector, we expect sentiment on TELE,

supported by its defensive nature, to remain positive at this stage of the market cycle. We

believe that TLKM’s 25% ownership in TELE will benefit TELE in the longer term as we expect

significant synergies. We believe TELE is entering a new growth phase as it grows its voucher

and handset businesses. Based on our DCF methodology (WACC: 10%), we assign a 12-

month target price of IDR1,180 (IDR1,060 previously) in line with our 4-9% upgrade in

2015F-16F net profit estimates. At our target price, TELE trades at 2016 PE of 17.5x, which is

justified in our view as we now see TELE as a both a telco and a consumer play, given its

massive distribution outlets of 180k accross Indonesia. With 65% upside potential and 11%

underperformance in the past 3 months (exhibit 4), we reaffirm our BUY rating on TELE.

TELE is a BUY

2 October 2015

PT Bahana Securities – Equity Research – Tiphone Mobile Indonesia 18

2014

Finance Asia's

Best

Equity House

Alpha

Southeast Asia

2014 Best

Research Call

FMCG Sector

Asiamoney's

2013

Best Domestic

Equity House

2015

Institutional

Investors

Highest Ranked

Local Research

House

2015

Global

Banking & Finance

Review

Best Research

House

P&L, BALANCE SHEET & RATIOS

Tiphone Indonesia Year to 31 December 2013 2014 2015F 2016F 2017F PROFIT & LOSS (IDRb) Sales 10,485 14,590 19,465 25,223 31,960 Gross profit 628 819 1,003 1,252 1,582 EBITDA 452 528 582 710 902 Depreciation 15 20 20 22 24 EBIT 437 507 602 732 926 Net interest inc./(expense) (55) (121) (123) (130) (128) Forex gain/ (losses) - - - - - Other income/ (expense) 11 25 30 36 44 Pre-tax profit 393 412 509 639 842 Taxes (99) (107) (127) (160) (210) Minority interest (0) 0 0 0 0 Extraordinary gain/(losses)

Net profit 295 305 382 479 632

BALANCE SHEET (IDRb) Cash and equivalents 493 638 499 448 531 S-T investments - - - - - Trade receivables 1,301 1,642 1,854 2,193 2,557 Inventories 661 949 1,154 1,410 1,688 Fixed assets 156 145 153 153 152 Other assets 844 1,644 1,839 1,932 1,974 Total assets 3,455 5,018 5,499 6,136 6,901 Interest bearing liabilities 1,476 1,753 1,788 1,838 1,864 Trade payables 533 673 803 999 1,215 Other liabilities 59 93 100 106 117 Total liabilities 2,069 2,518 2,690 2,943 3,197 Minority interest 0 1 1 2 3 Shareholders' equity 1,387 2,499 2,809 3,193 3,705

CASH FLOW (IDRb) EBIT 437 507 602 732 926 Depreciation 15 20 20 22 24 Working capital (731) (489) (285) (399) (450) Other operating items (848) (983) (412) (342) (359) Operating cash flow (1,128) (944) (75) 13 142 Net capital expenditure (59) (17) (23) (24) (25) Free cash flow (1,187) (961) (98) (11) 116

Equity raised/(bought) 33 807 - - - Net borrowings 1,299 277 35 50 26 Other financing (47) 22 (75) (91) (113) Net cash flow 98 145 (139) (51) 29 Cash flow at beginning 395 493 638 499 448 Cash flow at end 493 638 499 448 477

RATIOS ROAE (%) 23.6 15.7 14.4 16.0 18.3 ROAA (%) 12.3 7.2 7.3 8.2 9.7 EBITDA margin (%) 4.3 3.6 3.0 2.8 2.8 EBIT margin (%) 4.2 3.5 3.1 2.9 2.9 Net margin (%) 2.8 2.1 2.0 1.9 2.0 Payout ratio (%) - 23.4 25.0 25.0 25.0 Interest coverage (x) 7.9 4.2 4.9 5.6 7.2 Net gearing (%) 70.9 48.1 45.9 43.5 35.9 Debts to assets (%) 42.7 34.9 32.5 30.0 27.0 Debtor turnover (days) 45 41 35 32 29 Creditor turnover (days) 20 18 16 15 15 Inventory turnover (days) 15 15 16 17 18

MAJOR ASSUMPTIONS Vouchers and starter kit 8,116 8,799 12,631 17,607 23,460 Cellphones 2,171 5,426 6,378 7,047 7,788

Telkomsel market share 13% 13% 20% 25% 30%

Source: Company, Bahana estimates

2015F-16F net profit to increase by 25% y-y

Cash levels expected to remain stable at around IDR400-500bn in the next two years

Working capital needs to remain

above IDR250bn in 2015-16F

Lower margin in 2016F on higher

revenue from M2M business

Voucher market share to reach 30% in 2017F

Fakhrul Fulvian

[email protected] 3602

Melvin Mikha Reminov

[email protected] Associate

ext 3621

Research: +62 21 250 5081

Harry [email protected]

Senior Associate DirectorHead of Research

Strategy, Consumer

ext 3600direct: +62 21 250 5735

Dealing Room: +62 21 527 0808 (Foreign Institutional)

Teguh Hartanto

[email protected] Director

Deputy Head of Research

Banks, Cement, Aviationext 3610

Leonardo Henry Gavaza, [email protected]

Senior Research ManagerAuto, Heavy equipment, Telco

ext 3608

Chandra Widjanarka

[email protected] Analyst

ext 1252

+62 21 250 5508 (Domestic Institutional)

Ashish Agrawal

[email protected] President

Institutional Equity Salesext 2550 / 2553

Reynard Poernawan

[email protected] Equity Sales

ext 2528

John M. Dasaad

[email protected] Sales

ext 2549

Yohanes Adhi Handoko

[email protected], Surabaya Branch

ext 7250

Suwardi Widjaja

[email protected] Sales

ext 2548

Amelia Husada

[email protected] President

Institutional Equity Salesext 2552

Michael W Setjoadi [email protected]

Research AnalystConsumer, Healthcare, Poultry

ext 3613

Nurul Farida

[email protected] Sales

ext 2543

Adrian Mahendra Putra

[email protected] AnalystIndustrial Estate

ext 3614

Hanna Marionda

[email protected] Trader

ext 2525

Adriana Kosasih

[email protected] Executive

ext 2541

Ari Santosa

[email protected] Trader

ext 2554

Adi Saputra

[email protected] & Fixed Income Associate

ext 3693

Robin Sutanto

[email protected] Analyst

Propertyext 3620

Agustinus Reza Kirana

[email protected] Analyst

Plantations, Shipping, Transportationext 3616

Research AnalystCement, Infratructure,Toll roads

ext 3605

Muhammad Wafi

[email protected] Analyst

ext 3609

+62 31 535 2788 (Surabaya Branch)

Arandi [email protected]

Research AnalystCoal, Metals, Oil & Gas

ext 3619

Head of Equity Sales & TradingInstitutional Equity Sales

ext 2545

Made Ayu Wijayati

[email protected] Executive

ext 3607

Sanni Satrio Dwi Utomo

[email protected] Associate

ext 3611

Andre Natala Susanto

[email protected] Associate

ext 3601

Bagus Adi Yoga Prawira

[email protected] AnalystConsumer, Media

ext 3604

Zefanya Halim

[email protected] Manager

ext 3612

Novianty Permata Sari

ext 3618

Renaldy Effendy

[email protected] Associate

ext 3606

Head Office Surabaya Branch

Graha Niaga, 19th Floor Wisma BII, Ground Floor

Jl. Jend. Sudirman Kav. 58 Jl. Pemuda 60-70

Jakarta 12190 Surabaya 60271

Indonesia Indonesia

Tel. 62 21 250 5081 Tel. 62 31 535 2788

Fax. 62 21 522 6049 http://www.bahana.co.id Fax. 62 31 546 1157

Important Disclosures and Disclaimer This publication is prepared by PT.Bahana Securities and reviewed by Daiwa Securities Group Inc. and/or its affiliates, and distributed outside Indonesia by Daiwa Securities Group Inc. and/or its affiliates, except to the extent expressly provided herein. Certain copies of this publication may be distributed inside and outside of Indonesia by PT. Bahana Securities in accordance with relevant laws and regulations. This publication and the contents hereof are intended for information purposes only, and may be subject to change without further notice. Any use, disclosure, distribution, dissemination, copying, printing or reliance on this publication for any other purpose without our prior consent or approval is strictly prohibited. Any review does not constitute a full verification of the publication and merely provides a minimum check. Neither Daiwa Securities Group Inc. nor any of its respective parent, holding, subsidiaries or affiliates, nor any of its respective directors, officers, servants and employees, represent nor warrant the accuracy or completeness of the information contained herein or as to the existence of other facts which might be significant, and will not accept any responsibility or liability whatsoever for any use of or reliance upon this publication or any of the contents hereof. Neither this publication, nor any content hereof, constitute, or are to be construed as, an offer or solicitation of an offer to buy or sell any of the securities or investments mentioned herein in any country or jurisdiction nor, unless expressly provided, any recommendation or investment opinion or advice. Any view, recommendation, opinion or advice expressed in this publication constitutes the views of the analyst(s) named herein and does not necessarily reflect those of Daiwa Securities Group Inc. and/or its affiliates nor any of its respective directors, officers, servants and employees except where the publication states otherwise. This research report is not to be relied upon by any person in making any investment decision or otherwise advising with respect to, or dealing in, the securities mentioned, as it does not take into account the specific investment objectives, financial situation and particular needs of any person.

Neither Daiwa Securities Group Inc. nor any of its affiliates is licensed to undertake any business within the Republic of Indonesia. Any display of any trade name or logo of the Daiwa Securities Group Inc. on this publication shall not be deemed to be an undertaking of any business within the Republic of Indonesia.

Daiwa Securities Group Inc., its subsidiaries or affiliates, or its or their respective directors, officers and employees from time to time may have trades as principals, or have positions in, or have other interests in the securities of the company under research including market making activities, derivatives in respect of such securities or may have also performed investment banking and other services for the issuer of such securities. The following are additional disclosures.

Ownership of Securities

For “Ownership of Securities” information, please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Investment Banking Relationship

For “Investment Banking Relationship”, please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Japan

Daiwa Securities Co. Ltd. and Daiwa Securities Group Inc.

Daiwa Securities Co. Ltd. is a subsidiary of Daiwa Securities Group Inc.

Investment Banking Relationship

Within the preceding 12 months, The subsidiaries and/or affiliates of Daiwa Securities Group Inc. * has lead-managed public offerings and/or secondary offerings (excluding straight bonds) of the securities of the following companies: Modern Land (China) Co. Ltd (1107 HK); econtext Asia Ltd (1390 HK); Accordia Golf Trust (AGT SP); Hua Hong Semiconductor Ltd (1347 HK); GF Securities Co Ltd (1776 HK); Mirae Asset Life Insurance Co Ltd (085620 KS).

*Subsidiaries of Daiwa Securities Group Inc. for the purposes of this section shall mean any one or more of:

• Daiwa Capital Markets Hong Kong Limited (大和資本市場香港有限公司)

• Daiwa Capital Markets Singapore Limited

• Daiwa Capital Markets Australia Limited

• Daiwa Capital Markets India Private Limited

• Daiwa-Cathay Capital Markets Co., Ltd.

• Daiwa Securities Capital Markets Korea Co., Ltd

Disclosure of Interest of Bahana Securities

Investment Banking Relationship

Within the preceding 12 months, Bahana Securities has lead-managed public offerings and/or secondary offerings (excluding straight bonds) of the securities of the following companies: J Resources Asia Pasific Tbk PT (PSAB IJ); Waskita Karya Persero Tbk PT (WSKT IJ); Adhi Karya Persero Tbk PT (ADHI IJ); PP Properti Tbk PT (PPRO IJ); Merdeka Copper Gold Tbk PT (MDKA IJ); Anabatic Technologies Tbk PT (ATIC IJ).

Hong Kong

This research is distributed in Hong Kong by Daiwa Capital Markets Hong Kong Limited (大和資本市場香港有限公司) (“DHK”) which is regulated by the Hong Kong Securities and Futures Commission. Recipients of this research in Hong Kong may contact DHK in respect of any matter arising from or in connection with this research.

Relevant Relationship (DHK)

DHK may from time to time have an individual employed by or associated with it serves as an officer of any of the companies under its research coverage.

Singapore

This research is distributed in Singapore by Daiwa Capital Markets Singapore Limited and it may only be distributed in Singapore to accredited investors, expert investors and institutional investors as defined in the Financial Advisers Regulations and the Securities and Futures Act (Chapter 289), as amended from time to time. By virtue of distribution to these category of investors, Daiwa Capital Markets Singapore Limited and its representatives are not required to comply with Section 36 of the Financial Advisers Act (Chapter 110) (Section 36 relates to disclosure of Daiwa Capital Markets Singapore Limited’s interest and/or its representative’s interest in securities). Recipients of this research in Singapore may contact Daiwa Capital Markets Singapore Limited in respect of any matter arising from or in connection with the research.

Australia

This research is distributed in Australia by Daiwa Capital Markets Australia Limited and it may only be distributed in Australia to wholesale investors within the meaning of the Corporations Act. Recipients of this research in Australia may contact Daiwa Capital Markets Stockbroking Limited in respect of any matter arising from or in connection with the research.

India

This research is distributed in India to Institutional Clients only by Daiwa Capital Markets India Private Limited (Daiwa India) which is an intermediary registered with Securities & Exchange Board of India as a Stock Broker, Merchant Bank and Research Analyst. Daiwa India, its Research Analyst and their family members and its associates do not have any financial interest save as disclosed or other undisclosed material conflict of interest in the securities or derivatives of any companies under coverage. Daiwa India and its associates may have received compensation for any products other than Investment Banking (as disclosed) or brokerage services from the subject company in this report during the past 12 months. Unless otherwise stated in BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action, Daiwa India and its associates do not hold more than 1% of any companies covered in this research report.

There is no material disciplinary action against Daiwa India by any regulatory authority impacting equity research analysis activities as of the date of this report.

Taiwan

This research is distributed in Taiwan by Daiwa-Cathay Capital Markets Co., Ltd and it may only be distributed in Taiwan to institutional investors or specific investors who have signed recommendation contracts with Daiwa-Cathay Capital Markets Co., Ltd in accordance with the Operational Regulations Governing Securities Firms Recommending Trades in Securities to Customers. Recipients of this research in Taiwan may contact Daiwa-Cathay Capital Markets Co., Ltd in respect of any matter arising from or in connection with the research.

Philippines

This research is distributed in the Philippines by DBP-Daiwa Capital Markets Philippines, Inc. which is regulated by the Philippines Securities and Exchange

Commission and the Philippines Stock Exchange, Inc. Recipients of this research in the Philippines may contact DBP-Daiwa Capital Markets Philippines, Inc.

in respect of any matter arising from or in connection with the research. DBP-Daiwa Capital Markets Philippines, Inc. recommends that investors

independently assess, with a professional advisor, the specific financial risks as well as the legal, regulatory, tax, accounting, and other consequences of a proposed transaction. DBP-Daiwa Capital Markets Philippines, Inc. may have positions or may be materially interested in the securities in any of the markets

mentioned in the publication or may have performed other services for the issuers of such securities.

For relevant securities and trading rules please visit SEC and PSE link at http://www.sec.gov.ph/irr/AmendedIRRfinalversion.pdf and

http://www.pse.com.ph/ respectively.

United Kingdom

This research report is produced by Daiwa Capital Markets Europe Limited and/or its affiliates and is distributed in the European Union, Iceland, Liechtenstein, Norway and Switzerland. Daiwa Capital Markets Europe Limited is authorised and regulated by The Financial Conduct Authority (“FCA”) and is a member of the London Stock Exchange, Eurex and NYSE Liffe.

This publication is intended for investors who are not Retail Clients in the United Kingdom within the meaning of the Rules of the FCA and should not therefore be distributed to such Retail Clients in the United Kingdom. Should you enter into investment business with Daiwa Capital Markets Europe’s affiliates outside the United Kingdom, we are obliged to advise that the protection afforded by the United Kingdom regulatory system may not apply; in particular, the benefits of the Financial Services Compensation Scheme may not be available.

Daiwa Capital Markets Europe Limited has in place organisational arrangements for the prevention and avoidance of conflicts of interest. Our conflict management policy is available at http://www.uk.daiwacm.com/about-us/corporate-governance-regulatory.

Germany

This document is distributed in Germany by Daiwa Capital Markets Europe Limited, Niederlassung Frankfurt which is regulated by BaFin (Bundesanstalt fuer Finanzdienstleistungsaufsicht) for the conduct of business in Germany.

Bahrain

This research material is distributed by Daiwa Capital Markets Europe Limited, Bahrain Branch, regulated by The Central Bank of Bahrain and holds Investment Business Firm – Category 2 license and having its official place of business at the Bahrain World Trade Centre, South Tower, 7th floor, P.O. Box 30069, Manama, Kingdom of Bahrain. Tel No. +973 17534452 Fax No. +973 535113

This material is provided as a reference for making investment decisions and is not intended to be a solicitation for investment. Investment decisions should be made at your own discretion and risk. Accordingly, no representation or warranty, express or implied, is made as to and no reliance should be placed on the fairness, accuracy, completeness or correctness of the information and opinions contained in this document, Content herein is based on information available at the time the research material was prepared and may be amended or otherwise changed in the future without notice. All information is intended for the private use of the person to whom it is provided without any liability whatsoever on the part of Daiwa Capital Markets Europe Limited, Bahrain Branch, any associated company or the employees thereof. If you are in doubt about the suitability of the product or the research material itself, please consult your own financial adviser. Daiwa Capital Markets Europe Limited, Bahrain Branch retains all rights related to the content of this material, which may not be redistributed or otherwise transmitted without prior consent.

United States

This report is distributed in the U.S. by Daiwa Capital Markets America Inc. (DCMA). It may not be accurate or complete and should not be relied upon

as such. It reflects the preparer’s views at the time of its preparation, but may not reflect events occurring after its preparation; nor does it reflect

PT.Bahana Securities’ or DCMA’s views at any time. Neither PT.Bahana Securities, DCMA nor the preparer has any obligation to update this report

or to continue to prepare research on this subject. This report is not an offer to sell or the solicitation of any offer to buy securities. Unless this report

says otherwise, any recommendation it makes is risky and appropriate only for sophisticated speculative investors able to incur significant losses.

Readers should consult their financial advisors to determine whether any such recommendation is consistent with their own investment objectives,

financial situation and needs. This report does not recommend to U.S. recipients the use of any of PT.Bahana Securities’ or DCMA’s non-U.S. affiliates to effect trades in any security and is not supplied with any understanding that U.S. recipients of this report will direct commission business to

such non-U.S. entities. Unless applicable law permits otherwise, non-U.S. customers wishing to effect a transaction in any securities referenced in this

material should contact a Daiwa entity in their local jurisdiction. Most countries throughout the world have their own laws regulating the types of

securities and other investment products which may be offered to their residents, as well as a process for doing so. As a result, the securities

discussed in this report may not be eligible for sales in some jurisdictions. Customers wishing to obtain further information about this report should

contact DCMA: Daiwa Capital Markets America Inc., Financial Square, 32 Old Slip, New York, New York 10005 (Tel no. 212-612-7000).

Ownership of Securities

For “Ownership of Securities” information please visit BlueMatrix disclosure Link at https://daiwa3.bluematrix.com/sellside/Disclosures.action .

Investment Banking Relationships

For “Investment Banking Relationships” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

DCMA Market Making

For “DCMA Market Making” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Research Analyst Conflicts

For updates on “Research Analyst Conflicts” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action. The

principal research analysts who prepared this report have no financial interest in securities of the issuers covered in the report, are not (nor are any members of their household) an officer, director or advisory board member of the issuer(s) covered in the report, and are not aware of any material

relevant conflict of interest involving the analyst or DCMA, and did not receive any compensation from the issuer during the past 12 months except as

noted: no exceptions.

Research Analyst Certification

For updates on “Research Analyst Certification” and “Rating System” please visit BlueMatrix disclosure link at

https://daiwa3.bluematrix.com/sellside/Disclosures.action. The views about any and all of the subject securities and issuers expressed in this

Research Report accurately reflect the personal views of the research analyst(s) primarily responsible for this report (or the views of the firm

producing the report if no individual analysts[s] is named on the report); and no part of the compensation of such analyst(s) (or no part of the

compensation of the firm if no individual analyst[s)] is named on the report) was, is, or will be directly or indirectly related to the specific recommendations or views contained in this Research Report.

For stocks and sectors in Indonesia covered by Bahana Securities, the following rating system is in effect:

Stock ratings are based on absolute upside or downside, which is the difference between the target price and the current market price. Unless otherwise specified, these ratings are set with a 12-month horizon. It is possible that future price volatility may cause a temporary mismatch between upside/downside for a stock based on the market price and the formal rating. "Buy": the price of the security is expected to increase by 10% or more. "Hold": the price of the security is expected to range from an increase of less than 10% to a decline of less than 5%. "Reduce": the price of the security is expected to decline by 5% or more.

Sector ratings are based on fundamentals for the sector as a whole. Hence, a sector may be rated “Overweight” even though its constituent stocks are all rated “Reduce”; and a sector may be rated “Underweight” even though its constituent stocks are all rated “Buy”. “Overweight”: positive fundamentals for the sector. “Neutral”: neither positive nor negative fundamentals for the sector. “Underweight”: negative fundamentals for the sector.

Ownership of Securities For “Ownership of Securities” information, please visit BlueMatrix disclosure Link at https://daiwa3.bluematrix.com/sellside/Disclosures.action .

Investment Banking Relationships For “Investment Banking Relationship”, please visit BlueMatrix disclosure Link at https://daiwa3.bluematrix.com/sellside/Disclosures.action . Relevant Relationships (Bahana Securities) Bahana Securities may from time to time have an individual employed by or associated with it serves as an officer of any of the companies under its research coverage.

Bahana Securities market making Bahana Securities may from time to time make a market in securities covered by this research.

Additional information may be available upon request.

Japan - additional notification items pursuant to Article 37 of the Financial Instruments and Exchange Law

(This Notification is only applicable where report is distributed by Daiwa Securities Co. Ltd.)

If you decide to enter into a business arrangement with us based on the information described in materials presented along with this document, we ask you to pay close attention to the following items.

In addition to the purchase price of a financial instrument, we will collect a trading commission* for each transaction as agreed beforehand with you. Since

commissions may be included in the purchase price or may not be charged for certain transactions, we recommend that you confirm the commission for

each transaction.

In some cases, we may also charge a maximum of ¥ 2 million (including tax) per year as a standing proxy fee for our deposit of your securities, if you are

a non-resident of Japan.

For derivative and margin transactions etc., we may require collateral or margin requirements in accordance with an agreement made beforehand with

you. Ordinarily in such cases, the amount of the transaction will be in excess of the required collateral or margin requirements.

There is a risk that you will incur losses on your transactions due to changes in the market price of financial instruments based on fluctuations in interest

rates, exchange rates, stock prices, real estate prices, commodity prices, and others. In addition, depending on the content of the transaction, the loss

could exceed the amount of the collateral or margin requirements. There may be a difference between bid price etc. and ask price etc. of OTC derivatives handled by us.

Before engaging in any trading, please thoroughly confirm accounting and tax treatments regarding your trading in financial instruments with such experts

as certified public accountants.

*The amount of the trading commission cannot be stated here in advance because it will be determined between our company and you based on current

market conditions and the content of each transaction etc.

When making an actual transaction, please be sure to carefully read the materials presented to you prior to the execution of agreement, and to take responsibility for your own decisions regarding the signing of the agreement with us.

Corporate Name: Daiwa Securities Co. Ltd.

Financial instruments firm: chief of Kanto Local Finance Bureau (Kin-sho) No.108

Memberships: Japan Securities Dealers Association, Financial Futures Association of Japan

Japan Securities Investment Advisers Association

Type II Financial Instruments Firms Association