epic research special stock market report 11th aug 2016

TRANSCRIPT

DAILY REPORT 11

th AUGUST 2016

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance Germany's top share index hit a new high for 2016 on Tues-day as European shares advanced for a fifth straight ses-sion, boosted by new highs on Wall Street and strong re-sults from companies like Munich Re. Germany's DAX closed up 2.5 percent, having hit 10,701.33, its highest level since the last trading day of 2015. The index is up 16 per-cent from its June low and 23 percent from a trough hit in February, meaning in technical terms it is in "bull market" territory. The STOXX Europe 600 was up 0.9 percent, in positive territory for a fifth straight session. It is just 0.4 percent away from regaining all of its losses made after Britain voted to leave the European Union on June 23. Ap-petite for equities was also buoyed as the S&P 500 and Nasdaq both hit fresh record highs on Wall Street. Asia markets opened lower on Thursday, following US losses, with sentiment likely driven by Wednesday's oil price falls and in anticipation of another data deluge from China on Friday. In Australia, the benchmark ASX 200 was down 0.74 percent in early trade, with the financials, en-ergy and materials sub-indexes down between 0.6 and 1.13 percent. Major banking stocks sold off, with shares of Com-monwealth Bank of Australia down some 2.2 percent. New Zealand's NZX 50 was near flat at 7,342.43. In South Korea, the Kospi traded 0.27 percent lower. Japanese markets were closed for the Mountain Day public holiday. US stocks closed lower, with the benchmark S&P 500 dropping 6 points as energy - the biggest laggard - dropped 1.4%. Previous day Roundup Profit booking continued for the second consecutive ses-sion Wednesday as the equity benchmarks posted a biggest one-day loss in percentage terms since June 24. The 30-share BSE Sensex lost 310.28 points or 1.10 percent at 27774.88 and the 50-share NSE Nifty plunged 102.95 points or 1.19 percent to 8575.30. The broader markets also caught in bear grip. The BSE Midcap and Smallcap indices were down more than a percent as about 1893 shares de-clined against 840 advancing shares on the exchange. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [down 191.18 pts], Capital Goods [down 172.39 pts], PSU [down 102.60 pts], FMCG [down 89.08 Pts], Realty [down 21.27 pts], Power [down 32.33 pts], Auto [down 418.32 pts], Healthcare [down 275.03 pts], IT [down 20.32 pts], Metals [down 48.56 Pts], TECK [down 17.09 pts], Oil& Gas [down 236.78 pts].

World Indices

Index Value % Change

DJI 18463.00 +0.06

S&P500 2173.50 +0.03

NASDAQ 5204.59 -0.40

FTSE100 6810.00 -0.04

NIKKEI 16650.00 -0.72

HANG SENG 22493.63 +0.03

Top Gainers

Company CMP Change % Chg

ADANIPORTS 257.60 17.85 7.45

BANKBARODA 160.05 1.60 1.01

TCS 2676.00 25.80 0.97

HCLTECH 817.95 7.10 0.88

ZEEL 515.90 3.60 0.70

Top Losers

Company CMP Change % Chg

GRASIM 4809.00 -377.35 -7.28

ACC 1612.00 -68.70 -4.39

IDEA 93.00 -4.15 -4.27

AMBUJACEM 259.5 -11.00 -4.07

LUPIN 1543.60 -63.65 -3.69

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

ADHUNIKIND 177.00 0.65 0.37

ADVENZYMES 1459.0 -12.20 -0.83

AGRITECH 34.90 1.65 4.96

AIAENG 1103.00 36.40 3.41

ALBERTDAVD 333.00 2.95 0.89

APCOTEXIND 413.50 -4.55 -1.09

APTECHT 92.70 -0.50 -0.54

Indian Indices

Company CMP Change % Chg

NIFTY 8575.30 -102.95 -1.19

SENSEX 27774.88 -310.28 -1.10

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

BIRLACOT 0.05 0.05 100.00

BROADCAST 3.10 0.00 0.00

BSLIMITED 7.80 -.30 -3.70

DAILY REPORT 11

th AUGUST 2016

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH]

SYNDICATE BANK [CASH]

On the daily chart of SYNDICATE BANK has shown down-side move yesterday session and has given breakout to near support level of 72 and closed near support only, thus stock is expected to give further downside move be-low this level. So we advise you to sell below 71 for the targets of 69.50-68.50 with stop loss above 72.50.

MACRO NEWS

Results: MRF, REC, Aditya Birla Nuvo, Grasim, Page In-dustries, Bank Of Baroda, IRB Infrastructure, Dhanlaxmi Bank, Godrej Industries, Granules India, Balrampur Chini, Aditya Birla Nuvo, Godrej Industries, Kesoram Industries, VIP Industries, PTC India, GE Shipping, Gujarat Pipavav Port, ICRA, IPCA Lab, JK Lakshmi Cement, Speciality Res-taurants, Coffee Day, PTC India, Amrutanjan Health, All-sec Tech, ABGShipyard, Arman Financial Serv, Ashapura Intimates Fashion, Asian Granito India, Asian Hotels, Bafna Pharma, Blue Blends, Butterfly Gandhimathi Appli-ances, FACT, Himadri Chemicals, Honda Siel Power, Ind-Swift Lab, ITI, Jindal Stainless Ltd, JMC Projects, Jyothy Lab, Kirloskar Ind, Krbl Ltd, Lt Foods, Mawana Sugars, Mm Forgings, JK Lakshmi Cement, Mukta Arts, Prime Focus, PunjabChemicals, Sanghvi Movers, SaurashtraCe-ment, STC, Stovec Ind, Sunil Health, Talwalkars Better, Tide Water Oil, Time Techno, Trent

Indian CPI inflation seen picking up in July on higher food prices

India, US push for $30mn energy storage research initia-tive

108 mobile towers found exceeding radiation limits Food ministry recommends stock limits on sugar mills,

suspending futures Car sales rise nearly 10% in July; passenger vehicles up

17% Aditya Birla Group plans to hive off financial services

arm from AB Nuvo Motherson Sumi Q1 profit, revenue up over 15%; debt

jumps 8%

STOCK RECOMMENDATIONS [FUTURE]

1. AUROPHARMA [FUTURE]

Last trading session AUROPHARMA Future show under pres-sure during the day. And closed with bearish candlestick on daily chart, while before last session stock made a low of 747.60 and respect major support level and closed near this level, So if the stock break support level, we may see sharp fall in this stock, we advise you to sell below 745 for the tar-get of 738-725 with stop loss of 757.

2.INFY [FUTURE]

Last trading session INFY future show positive strength in IT sector and close near major resistance with bullish candle-stick on daily chart. Stock open on flattish note but take a good recovery from lower level and closed near day high and since last session it rose with rising OI in long side . We may see sharp rise for that it will be good to buy above 1094 for the target of 1099-1110 with SL of 1080.

DAILY REPORT 11

th AUGUST 2016

YOUR MINTVISORY Call us at +91-731-6642300

FUTURES & OPTIONS

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,700 46.25 3,09,639 52,48,950

NIFTY CE 8,800 22.00 2,44,620 64,07,025

BANKNIFTY CE 19,000 1.65 1,65,177 8,33,920

LUPIN CE 1,700 8.70 4,700 8,37,900

M&M CE 1,500 15.00 4,235 6,25,500

ICICIBANK CE 250 2.40 4,172 91,90,000

ICICBANK CE 260 1.15 3,788 82,35,500

ADANIPORTS CE 260 8.50 3,496 8,57,500

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 8,600 95.05 2,68,240 40,95,300

NIFTY PE 8,500 56.40 2,00,846 54,66,900

BANKNIFTY PE 18,600 45.00 1,37,815 3,14,800

LUPIN PE 1,600 70.50 3,164 3,10,500

LUPIN PE 1,500 20.35 2,556 1,80,900

LUPIN PE 1,550 41.25 2,449 1,79,100

M&M PE 1,400 10.70 2,427 2,80,000

SBIN PE 230 6.60 1,662 22,83,000

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 32438 2178.52 30759 2085.89 342469 22434.01 92.62

INDEX OPTIONS 690767 47499.63 694947 47861.73 1008606 65463.87 -362.10

STOCK FUTURES 89409 5995.58 99422 6571.75 886043 56990.50 -576.17

STOCK OPTIONS 72192 4863.80 72542 4883.60 86679 5668.48 -19.80

TOTAL -865.44

STOCKS IN NEWS SRF to invest Rs 345 cr for business expansion Ashoka Buildcon wins Rs 1,600 crore road project GE, L&T partner to manufacture subsea equipment Ashoka Buildcon wins Rs 1,600 crore road project in

Punjab from NHAI Tata Chemicals sells urea business to Yara Fertilisers City Union Bank Q1 profit rises 11% to Rs 124 crore Coal India anticipates higher sales as imported coal

and pet coke prices rise Reliance Jio hits back, accuses older telcos AirIndia inks pact with Spicejet for MRO facility M&M Q1 profit rises on higher SUV, truck sales Travelyaari raises $7 mn from GVFL, BCCL NIFTY FUTURE

NIFTY in yesterday trading session was bearish whole day. It lost around 135 points and closed with a bearish candlestick again with a good amount of volumes. RSI is also showing weakness. So we advise you to sell nifty from around 8630-8600 for the targets of 8550 and 8490 with strict stop loss of 8730

INDICES R2 R1 PIVOT S1 S2

NIFTY 8735.50 8655.40 8610 8529.90 8484.50

BANKNIFTY 19121.00 18884.00 18747.00 18510.00 18373.00

DAILY REPORT 11

th AUGUST 2016

YOUR MINTVISORY Call us at +91-731-6642300

COMMODITY ROUNDUP

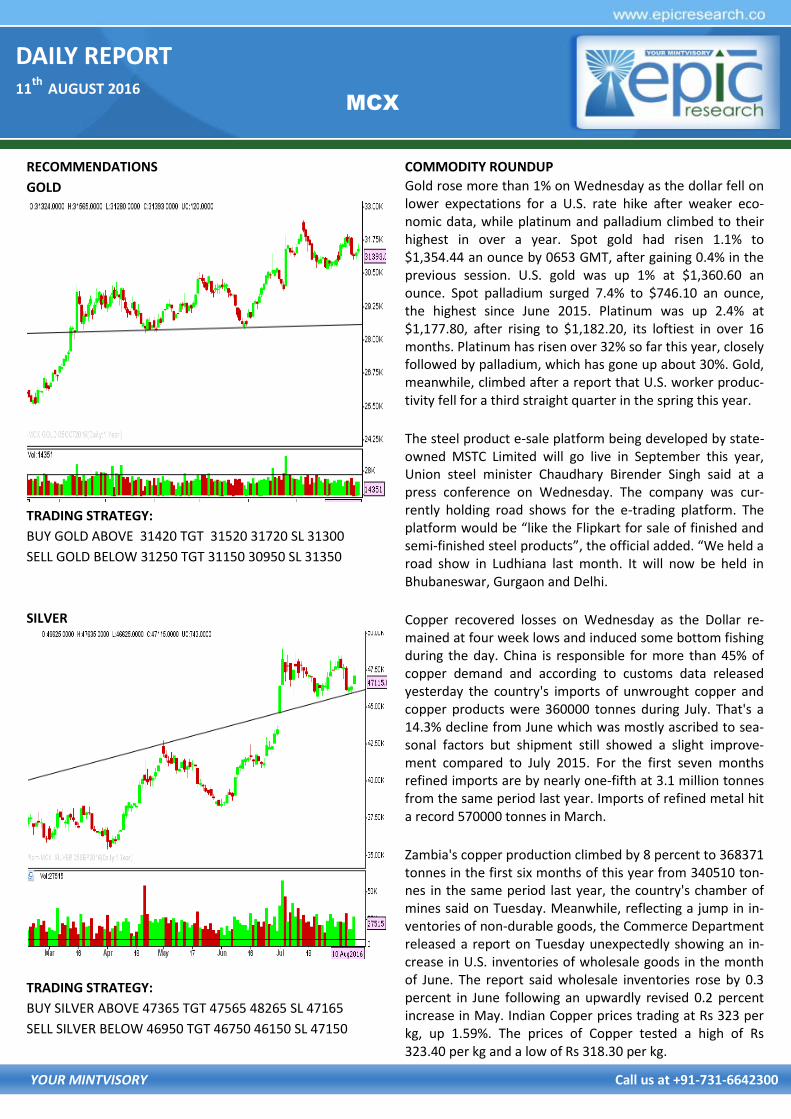

Gold rose more than 1% on Wednesday as the dollar fell on lower expectations for a U.S. rate hike after weaker eco-nomic data, while platinum and palladium climbed to their highest in over a year. Spot gold had risen 1.1% to $1,354.44 an ounce by 0653 GMT, after gaining 0.4% in the previous session. U.S. gold was up 1% at $1,360.60 an ounce. Spot palladium surged 7.4% to $746.10 an ounce, the highest since June 2015. Platinum was up 2.4% at $1,177.80, after rising to $1,182.20, its loftiest in over 16 months. Platinum has risen over 32% so far this year, closely followed by palladium, which has gone up about 30%. Gold, meanwhile, climbed after a report that U.S. worker produc-tivity fell for a third straight quarter in the spring this year.

The steel product e-sale platform being developed by state-owned MSTC Limited will go live in September this year, Union steel minister Chaudhary Birender Singh said at a press conference on Wednesday. The company was cur-rently holding road shows for the e-trading platform. The platform would be “like the Flipkart for sale of finished and semi-finished steel products”, the official added. “We held a road show in Ludhiana last month. It will now be held in Bhubaneswar, Gurgaon and Delhi.

Copper recovered losses on Wednesday as the Dollar re-mained at four week lows and induced some bottom fishing during the day. China is responsible for more than 45% of copper demand and according to customs data released yesterday the country's imports of unwrought copper and copper products were 360000 tonnes during July. That's a 14.3% decline from June which was mostly ascribed to sea-sonal factors but shipment still showed a slight improve-ment compared to July 2015. For the first seven months refined imports are by nearly one-fifth at 3.1 million tonnes from the same period last year. Imports of refined metal hit a record 570000 tonnes in March.

Zambia's copper production climbed by 8 percent to 368371 tonnes in the first six months of this year from 340510 ton-nes in the same period last year, the country's chamber of mines said on Tuesday. Meanwhile, reflecting a jump in in-ventories of non-durable goods, the Commerce Department released a report on Tuesday unexpectedly showing an in-crease in U.S. inventories of wholesale goods in the month of June. The report said wholesale inventories rose by 0.3 percent in June following an upwardly revised 0.2 percent increase in May. Indian Copper prices trading at Rs 323 per kg, up 1.59%. The prices of Copper tested a high of Rs 323.40 per kg and a low of Rs 318.30 per kg.

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD ABOVE 31420 TGT 31520 31720 SL 31300

SELL GOLD BELOW 31250 TGT 31150 30950 SL 31350

SILVER

TRADING STRATEGY:

BUY SILVER ABOVE 47365 TGT 47565 48265 SL 47165

SELL SILVER BELOW 46950 TGT 46750 46150 SL 47150

MCX

DAILY REPORT 11

th AUGUST 2016

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

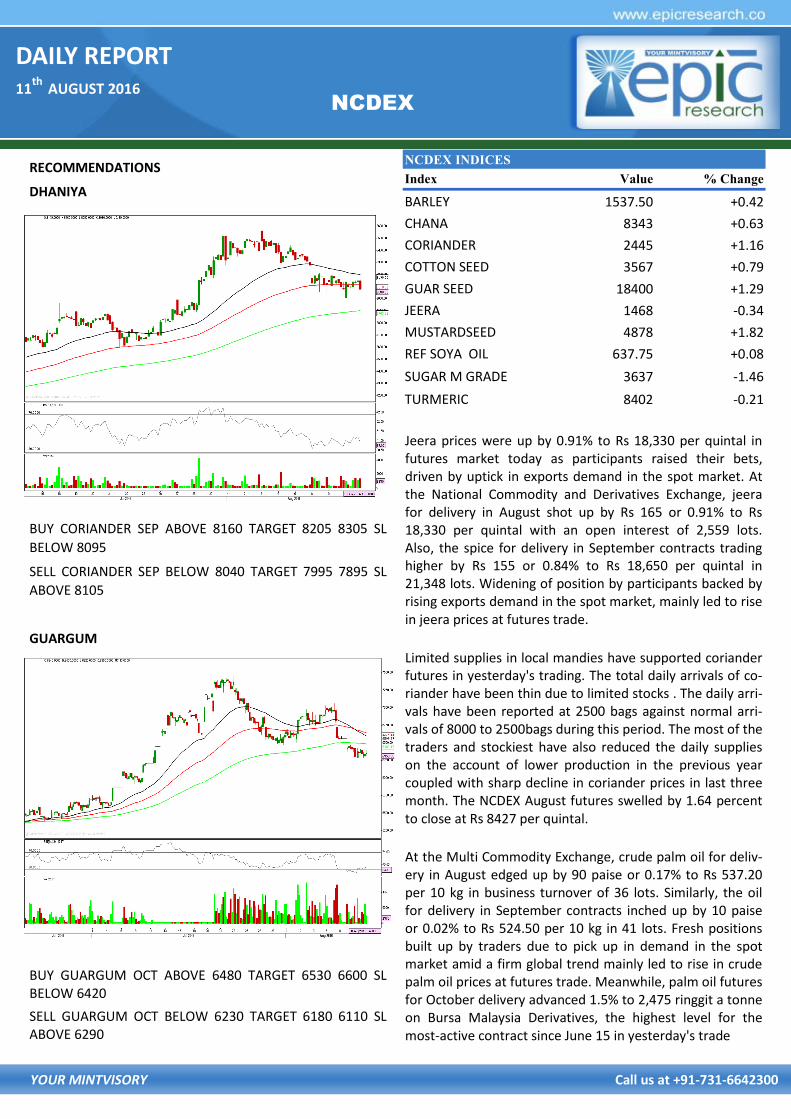

NCDEX INDICES

Index Value % Change

BARLEY 1537.50 +0.42

CHANA 8343 +0.63

CORIANDER 2445 +1.16

COTTON SEED 3567 +0.79

GUAR SEED 18400 +1.29

JEERA 1468 -0.34

MUSTARDSEED 4878 +1.82

REF SOYA OIL 637.75 +0.08

SUGAR M GRADE 3637 -1.46

TURMERIC 8402 -0.21

RECOMMENDATIONS

DHANIYA

BUY CORIANDER SEP ABOVE 8160 TARGET 8205 8305 SL

BELOW 8095

SELL CORIANDER SEP BELOW 8040 TARGET 7995 7895 SL

ABOVE 8105

GUARGUM

BUY GUARGUM OCT ABOVE 6480 TARGET 6530 6600 SL BELOW 6420

SELL GUARGUM OCT BELOW 6230 TARGET 6180 6110 SL ABOVE 6290

Jeera prices were up by 0.91% to Rs 18,330 per quintal in futures market today as participants raised their bets, driven by uptick in exports demand in the spot market. At the National Commodity and Derivatives Exchange, jeera for delivery in August shot up by Rs 165 or 0.91% to Rs 18,330 per quintal with an open interest of 2,559 lots. Also, the spice for delivery in September contracts trading higher by Rs 155 or 0.84% to Rs 18,650 per quintal in 21,348 lots. Widening of position by participants backed by rising exports demand in the spot market, mainly led to rise in jeera prices at futures trade.

Limited supplies in local mandies have supported coriander futures in yesterday's trading. The total daily arrivals of co-riander have been thin due to limited stocks . The daily arri-vals have been reported at 2500 bags against normal arri-vals of 8000 to 2500bags during this period. The most of the traders and stockiest have also reduced the daily supplies on the account of lower production in the previous year coupled with sharp decline in coriander prices in last three month. The NCDEX August futures swelled by 1.64 percent to close at Rs 8427 per quintal.

At the Multi Commodity Exchange, crude palm oil for deliv-ery in August edged up by 90 paise or 0.17% to Rs 537.20 per 10 kg in business turnover of 36 lots. Similarly, the oil for delivery in September contracts inched up by 10 paise or 0.02% to Rs 524.50 per 10 kg in 41 lots. Fresh positions built up by traders due to pick up in demand in the spot market amid a firm global trend mainly led to rise in crude palm oil prices at futures trade. Meanwhile, palm oil futures for October delivery advanced 1.5% to 2,475 ringgit a tonne on Bursa Malaysia Derivatives, the highest level for the most-active contract since June 15 in yesterday's trade

DAILY REPORT 11

th AUGUST 2016

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 66.744 Yen-100 65.840

Euro 74.379 GBP 87.041

CURRENCY

USD/INR

BUY USD/INR AUG ABOVE 66.98 TARGET 67.11 67.26 SL

BELOW 66.78

SELL USD/INR AUG BELOW 66.85 TARGET 66.72 66.57 SL

ABOVE 67.05

EUR/INR

BUY EUR/INR AUG ABOVE 74.86 TARGET 75.01 75.21 SL BE-

LOW 74.66

SELL EUR/INR AUG BELOW 74.8 TARGET 74.65 74.45 SL

ABOVE 75

CURRENCY MARKET UPDATES:

Indian rupee closed nearly 13 paise higher at higher at 66.72 against dollar on Wednesday on account of fresh selling of American currency by exports and banks. The sell-off in Indian equity market did not put any pressure on rupee. TheBSE Sensex closed 310 points down at 27774, while Nifty 50 index settled 102.95 points down at 8,575. Anindya Banerjee, currency analyst, Kotak Securities said, “Broad based weakness in US dollar against majors as well as EM currencies supported rupee on Wednesday. Local bonds continue to catch bids, with 10 year trading at 7.08 per cent, at multi-year lows. Volatility in USDINR has fallen to levels from where sharp increase in volatility have oc-curred in the past.” During the day, Indian currency touched a high of 66.66 and low of 66.78. On Tuesday, ru-pee closed marginally higher at 66.84 against previous close of 66.85 on account of selling of dollar by banks and exports.

Weak US data pulled the US dollar lower and supported Gold in turn. Gold rose from a one week low on bargain buying and a recovery in global crude oil prices. The metal had witnessed a sharp drop after excellent US nonfarm payrolls data on Friday, easing from its three week highs. The metal currently trades at $1360 per ounce, up 1% on the day. An increase in speculative longs is likely to keep losses curbed for the shiny metal. MCX Gold futures trade at Rs 31497 per 10 grams, up 0.72% on the day after hit-ting a high of Rs 31550 per 10 grams.

Meanwhile, the US dollar has been witnessing tepid moves this week after failing to hold under 1.1000 levels against the Euro. The greenback has dropped to 1.1200 levels right now. Dollar eased yesterday after the US Labour Depart-ment reported an unexpected decline in US labour produc-tivity in the second quarter. The report showed that pro-ductivity fell by 0.5% in the second quarter after falling by 0.6% in the first quarter. The unexpected drop in produc-tivity, a measure of output per hour, came as hours worked jumped by 1.8% in the second quarter after surg-ing up by 1.4% in the first quarter.

DAILY REPORT 11

th AUGUST 2016

YOUR MINTVISORY Call us at +91-731-6642300

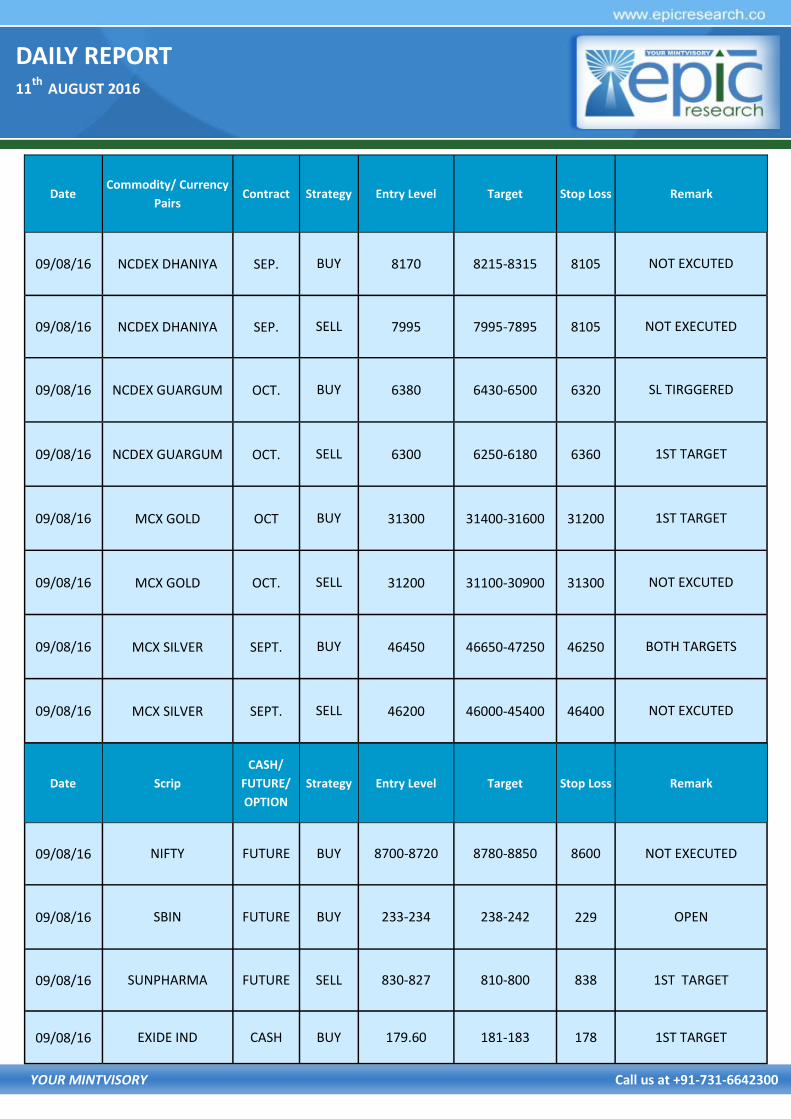

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

09/08/16 NCDEX DHANIYA SEP. BUY 8170 8215-8315 8105 NOT EXCUTED

09/08/16 NCDEX DHANIYA SEP. SELL 7995 7995-7895 8105 NOT EXECUTED

09/08/16 NCDEX GUARGUM OCT. BUY 6380 6430-6500 6320 SL TIRGGERED

09/08/16 NCDEX GUARGUM OCT. SELL 6300 6250-6180 6360 1ST TARGET

09/08/16 MCX GOLD OCT BUY 31300 31400-31600 31200 1ST TARGET

09/08/16 MCX GOLD OCT. SELL 31200 31100-30900 31300 NOT EXCUTED

09/08/16 MCX SILVER SEPT. BUY 46450 46650-47250 46250 BOTH TARGETS

09/08/16 MCX SILVER SEPT. SELL 46200 46000-45400 46400 NOT EXCUTED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

09/08/16 NIFTY FUTURE BUY 8700-8720 8780-8850 8600 NOT EXECUTED

09/08/16 SBIN FUTURE BUY 233-234 238-242 229 OPEN

09/08/16 SUNPHARMA FUTURE SELL 830-827 810-800 838 1ST TARGET

09/08/16 EXIDE IND CASH BUY 179.60 181-183 178 1ST TARGET

DAILY REPORT 11

th AUGUST 2016

YOUR MINTVISORY Call us at +91-731-6642300

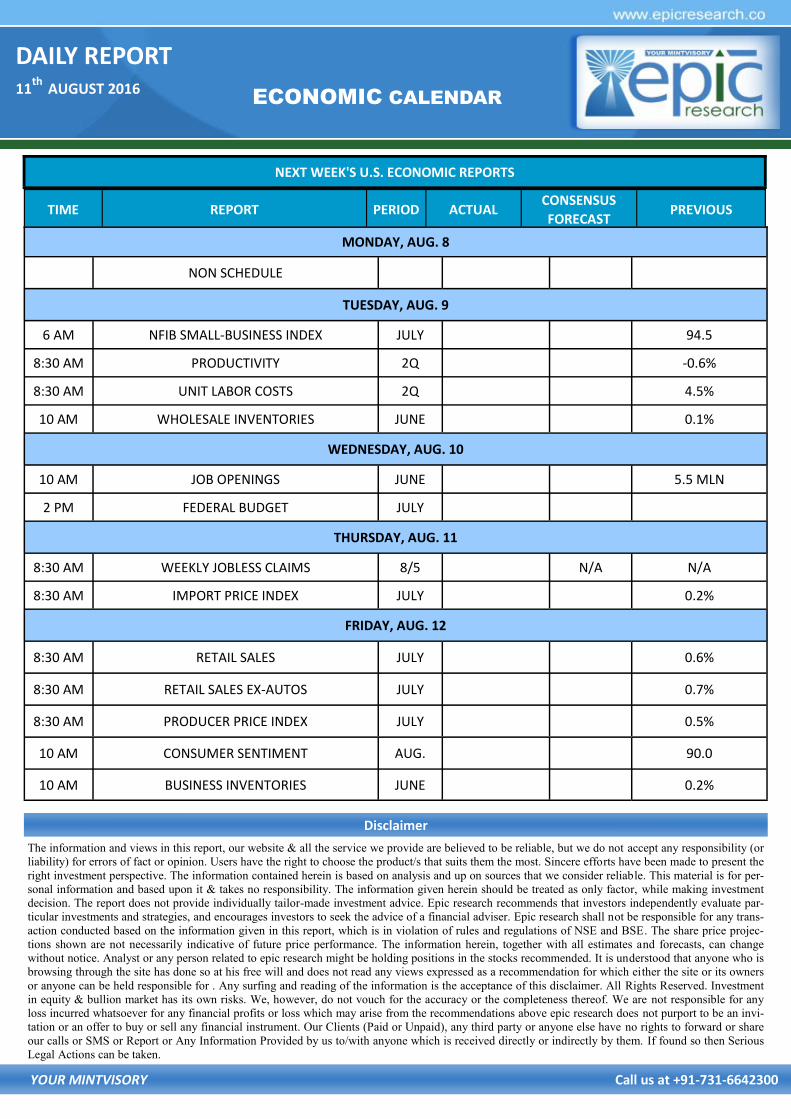

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any responsibility (or

liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere efforts have been made to present the

right investment perspective. The information contained herein is based on analysis and up on sources that we consider reliable. This material is for per-

sonal information and based upon it & takes no responsibility. The information given herein should be treated as only factor, while making investment

decision. The report does not provide individually tailor-made investment advice. Epic research recommends that investors independently evaluate par-

ticular investments and strategies, and encourages investors to seek the advice of a financial adviser. Epic research shall not be responsible for any trans-

action conducted based on the information given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projec-

tions shown are not necessarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change

without notice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone who is

browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either the site or its owners

or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this disclaimer. All Rights Reserved. Investment

in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the completeness thereof. We are not responsible for any

loss incurred whatsoever for any financial profits or loss which may arise from the recommendations above epic research does not purport to be an invi-

tation or an offer to buy or sell any financial instrument. Our Clients (Paid or Unpaid), any third party or anyone else have no rights to forward or share

our calls or SMS or Report or Any Information Provided by us to/with anyone which is received directly or indirectly by them. If found so then Serious

Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, AUG. 8

NON SCHEDULE

TUESDAY, AUG. 9

6 AM NFIB SMALL-BUSINESS INDEX JULY 94.5

8:30 AM PRODUCTIVITY 2Q -0.6%

8:30 AM UNIT LABOR COSTS 2Q 4.5%

10 AM WHOLESALE INVENTORIES JUNE 0.1%

WEDNESDAY, AUG. 10

10 AM JOB OPENINGS JUNE 5.5 MLN

2 PM FEDERAL BUDGET JULY

THURSDAY, AUG. 11

8:30 AM WEEKLY JOBLESS CLAIMS 8/5 N/A N/A

8:30 AM IMPORT PRICE INDEX JULY 0.2%

FRIDAY, AUG. 12

8:30 AM RETAIL SALES JULY 0.6%

8:30 AM RETAIL SALES EX-AUTOS JULY 0.7%

8:30 AM PRODUCER PRICE INDEX JULY 0.5%

10 AM CONSUMER SENTIMENT AUG. 90.0

10 AM BUSINESS INVENTORIES JUNE 0.2%