enterprise and cooperative development department at yahoo:

TRANSCRIPT

ENTERPRISE AND COOPERATIVE DEVELOPMENT DEPARTMENT

— Social Finance Unit —

Stock-taking Excercise -

United Kingdom

Paper prepared for the International Seminar in

Birmingham, June 2-3, 1998

“Enterprise creation by the unemployed: the role of

microfinance in industrialized countries” -

An ILO Action Programme

International Labour Office Geneva

Table of Contents

1. Micro Finance in the UK 2

1.1. Introduction and purpose 2a. ILO concept of micro

finance 2b. Methodology 3

2. What exists? Overview of programmes using a micro finance component and addressed at the unemployed for the purposes of self-employment 4

2.1. Central Government and European Union 4

a. New Deal 4b. Prince’s Youth Business

Trust (PYBT) 5c. Employment Zones

(Business Enterprise) 5d.Training and Enterprise

Councils TEC’s, Local Enterprise Companies (LEC’s), Local Enterprise Agencies (LEA’s) and Business Links 5

e. Small Firms Loan Guarantee Scheme 6

f. Taxation and Benefits 6

2.2. Local Government 6

2.3. Mainstream bank and financial service provision 7

2.4. Major Business Loan Funds 8

2.5. Micro finance, mentoring and guarantee schemes 8

2.6. Scotland 9a. The Local Economic

Company (“LEC”) Network 9b. Enterprise Trusts 9

2.7. Northern Ireland 10

3. What do we know about the quality of these programmes? (Annotated bibliography) 12

3.1. Keywords and sources12

3.2. Approaches 13

a. Micro-business 13b. Business and economics 14

c. Employment, regional development and public policy 14

4. Gaps in current research 154.1. Current research 154.2. On-going research 16

5. Opportunities to progress research17

5.1. Sustainability of the Activities Financed 175.2. Sustainability of the financial intermediary 175.3. Comparative Performance of Public and Private Sector 175.4. General 18

6. Annexes 19

I. Literature Search 19II. Micro finance Organisations 39

III. Bibliographies of some research undertaken 42

IV. Private / Public Sector Small Business/Micro credit Funds 43

V. Public Sector/Private Sector in England and Wales (1997) 44

VI. Scotland Individual Small business/micro finance funds 74

We wish to acknowledge the research undertaken by Anne Michelle Ketteridge and Developing Strathclyde Limited on the situation in Scotland which forms part of this report, for the assistance of Colin Stutt Consulting for information on Northern Ireland, and the assistance of DHP Enterprise Limited for information about training for self-employment. We would also like to thank the members of the advisory committee to this International Labour Organisation project who kindly responded to our enquiries.

This stocktaking exercise was undertaken by Leo Haidar, Julia Pellow and Malcolm Lynch of Malcolm Lynch Solicitors.

1. Micro finance in the UK

1.1. Introduction and purpose

Prior to commissioning research on the development of micro finance and employment creation in the UK, the International Labour Office has requested this preliminary research to bring into focus the areas of most concern for further research.

a. ILO concept of micro

finance

As this exercise is predominantly the cataloguing of a literature search, it is important to clarify the terms of reference.

c“Micro-credit” and “Micro

finance” means: (1) a business loan of less than 10,000 ECU; (2) made to a person or a group of persons to undertake or finance a business or community enterprise start-up; (3) in the first year; together with (4) financial support for the training of the unemployed for self-employment so as to enable them to more effectively use micro finance and/or (5) mentoring schemes for the new entrepreneur.

ementoring” means: a

formalised framework of supportive contact for the new entrepreneur, including an assigned business adviser making regular contact with the entrepreneur, a guarantee community, and a regular post enterprise training contact relationship

Accordingly, micro finance, which has not been the subject of much dedicated research in the UK, crosses over predominantly into small business finance, training of the unemployed in self-employment and self-employment research in the UK.

Elements required from micro finance include some of the following:

up to 10,000 ECU (£7,100);

lending decisions based on a business plan, rather than personal credit history, and not dependent on equity or other finance already in place;

(near) not above business loan APR;

low administrative costs;

some initial training on running a business;

some provision of continuing business advice support (not necessarily by lender); and

collateral not essential

sometimes interlocking with benefit payments.

Micro finance is concerned equally with (1) appropriate provision of loan finance to reasonably sustainable business proposals and (2) employment creation.

b. Methodology

The methodology used for this stocktaking exercise may be summarised as follows:

Correspondence with members of the panel

Correspondence with known research individuals and institutions

Internet search

„ British Library and other on-line catalogue searches

Physical review of some available literature by researchers

Interviews (telephone and personal)

The environment for micro finance organisations

2. What exists? Overview of programmes using a micro finance component and addressed at the unemployed for the purposes of self-employment

2.1. Central Government and

European Union

The Central Government has provided funds to support unemployed people to develop businesses under a variety of schemes for nearly two decades.

Current Sources of finance include:

The Department for Education and Employment (DfEE) - Work Based Training for Adult unemployed (ages 25-64) which includes self-employment as part of a training option, and is available as a scheme nation wide (and still known as Training for Work in Scotland ), but in England and Wales only 12 Training and Enterprise Council’s (“TECs”) have entered into agreements with the DfEE to operate the scheme;

The Department of the Environment, Transport and the Regions(DETR)

- the Single Regeneration Budget (SRB) is a competitive policy programme aimed at certain geographical areas which sometimes includes measures of support for self-employment, available only to winning areas in England and Wales through local authority partnerships; and

the European Regional Development Fund (ERDF) is a regional policy, a programme focusing

on the most deprived geographic areas and principally delivered through local authorities.

Previous schemes included:

Training for Work (TfW) in England and Wales which includes Enterprise Rehearsal - a self-employment option;

The Business Start up Scheme, commenced in 1991, was folded into SRBs in England and Wales in 1994, but remains in Scotland and Wales; and

Enterprise Allowance Scheme (EAS) run by the Employment Service (ES) up until 1991.

Current and new arrangements which provide self-employment options are:

One of the key elements of the current UK government’s “welfare to work policy” is the recently launched New Deal, commencing in practice from June 1998. This policy will include a self-employment option for 18-24 year old people. Essentially, it offers micro-entrepreneurs a one-off payment (grant) of £400 while they can continue to draw social security benefits. Income from the business goes into an escrow account until the client stops claiming benefit. The scheme will be managed and co-ordinated by the Employment Service and is something of a hybrid of previous enterprise rehearsal schemes.

b. Prince’s Youth Business Trust (PYBT)

PYBT (see annex) has

become something of a national scheme for entrepreneurship. It operates throughout England, Wales and Northern Ireland, and has a separate sister charity in Scotland, The Prince’s Scottish Youth Business Trust. Unless otherwise described, we shall use the term PYBT to include all its operations throughout the United Kingdom. PYBT particularly seeks to work with the severely disadvantaged unemployed (18-29 year olds). It receives its funding from several sources, including some core direct government funding to support successful start-up entrepreneurs who are still in business 15 months after commencing trading.

This is a new idea with prototype zones operating in Glasgow, South Teeside, Liverpool & Sefton, NW Wales and Plymouth. A major expansion is planned for next year. Certain specific areas of the country are designated as employment zones, which have local partnerships to deliver locally devised programmes for the unemployed. They have additional funds and new flexibilities. They are also intended to test innovative ideas, such as relationships between benefits and self-employment.

“Business Enterprise” is one of the elements which is required to be delivered within each zone. In the short term, it is likely that Business Enterprise will build on Business Rehearsal under Work Based Training for Adults. It is a self-employment option for people over 25 years who have been unemployed for more than a year.

TECS are responsible for Business Links and generally co-ordinate local self-employment strategies. They may also provide

independent funding for self-employment initiatives through support for independent start up funds. The nature of Government Funding has generally seen a drift on the part of TECs to existing, rather than new start businesses.

Business Links are meant to provide a one stop shop of advice for business people, including the would-be entrepreneur. Some operate their own in-house screening programmes for would-be entrepreneurs and work with other public and private sector providers in the area of self-employment.

The various agencies referred to above act as gatekeepers to the Government funds for training for self-employment. The training is provided by training providers and indirectly through Business Link advisers.

The Loan Guarantee Scheme was introduced by the Government in 1981. The basis for the introduction was the perceived finance gap for some small firms which found it difficult to obtain loan finance from commercial lenders. It is administered on a UK-wide basis by the Department of Trade and Industry in London. The Scheme is targeted at:

- businesses employing fewer than 200 people, and- engaged in wholesaling or manufacturing, construction, most non-financial services and most agricultural activities.

Accordingly, it is not particularly geared towards micro finance and the average loan guaranteed is well above the 10,000 ECU figure. There is a range of ineligible business activities, including retail businesses, real estate dealings, garages, betting and gambling, and certain forms of animal husbandry and

forestry.

No security is required for a loan. The DTI will guarantee up to 70% of a loan of up to £100,000 to a new business or up to 85% of a loan of up to £250,000 to an existing business. The scheme is administered by the commercial banks and a small number of specialist lenders.

It has undertaken some pilot targets for micro finance support.

The UK tax regime is generally taken as favourable for small business and self-employment while the benefits regime is generally seen as inflexible in moving from unemployment to self-employment. It is permissible to trade for up to 16 hours a week and claim benefits provided that all earnings are declared and benefits reduced accordingly. Schemes such as the New Deal permit the unemployed to remain on benefits for a period of time whilst they run their business. Income generated by the business is held in an escrow account and only used for business purposes until the scheme finishes.

Local Authorities have been supportive of micro credit and small business funds for many years. Some local authorities have managed their own small business and micro credit funds, whilst others have engaged in partnerships with the private and voluntary sectors. However, there is not universal support for these funds and some local authority involvement is now limited to the funding it receives from the SRB or the European Regional Development Fund.

In the annex, we catalogue a survey undertaken of local authorities in England and Wales (excluding metropolitan areas), showing that while many local authorities have small business incorporating micro

finance schemes, many are also considering their introduction.

In Scotland and Northern Ireland, a similar picture emerges of many small funds supported by local authorities. Some of the funds are inactive or find it too costly to process loans, whilst others do not provide mentoring to assist entrepreneurs. Most of the funds are not specifically directed towards micro credit, but include it within the framework of the fund. No uniform criteria appear in respect to interest rates charged, term of loans, collateral required, type of business or entrepreneur supported.

The turn over rate of the funds (opening and closure) suggests that the long term financial sustainability of the fund is not considered.

The average small business bank loan in the UK is in the region of £7,000. However, the loans on offer from the mainstream banks are often different from micro finance for the following reasons:

made (mostly) on the basis of credit history of persons and individuals;

made on a 50/50 basis regarding capital or finance already in place;

collateral required, particularly towards £7,000; and

no post-loan mentoring.

Some business advisors perceive an inappropriate degree of formality in bank lending decisions in the majority of cases. Whereas, perhaps 10 years ago, bank managers exercised their discretion towards customers in whom or in whose business proposition they had confidence, now specific criteria must

be met regarding gearing and length of establishment. Some of these criteria are contained in a business proposal credit scoring analysis. The experience of banks in this field is perhaps not as extensive as with personal finance credit scoring, and there may be elements of the credit scoring techniques which will improve over time. This issue is also clouded however, because bank managers still have the ability to exercise the same discretion, but may be less willing and not incentivised to do so, (particularly where there decisions are gaged against credit scoring techniques) . It appears the difference in approach by banks is not as significant as that by individual branch managers, especially if there is a pre-existing relationship. (Source: Interviews conducted by MLS)

The Bank of England’s surveys of small business finance indicate that the clearing banks remain the largest finance source for small firms, particularly when leasing, factoring and other forms of finance by clearing bank subsidiaries are taken into account. However, it appears that High Street banks are currently lending significantly less to small business compared with a few years ago. The consistency of lending decisions fluctuates with the business cycle, but according to British Bankers Association (BBA) data, there has been a significant decline:

Table 1 : Major British Banks Assistance to Small Businesses

(a) borrowing on overdraft (£bn) / (b)

total lending (£bn)1990 1991 1992 1993

(a) 27.12 27.37 19.44 16.63

(b) 45.30 46.70 39.54 38.25

Source BBA 1997

The data does not indicate what is happening in the areas of bill factoring, and leasing, which appears to be growing in the UK as businesses have a finance package tied to a particular asset. The other interesting point to note is the decline in the use of the overdraft facility and the increase in the use of the term loan. The Bank of England does not believe that there will be an increase in term loans beyond the current 63% of lending.

Mainstream banks are also actively engaged in public private partnerships with local authorities, TECs, LECs, and LEAs to create the small firm funds referred to above. Public money has the catalytic effect of stimulating the mainstream to become active in this area of business lending. Kingston University has undertaken two surveys of availability which, as with the local authority funds, indicate a turnover of funds in this sector and insufficient attention paid to the financial sustainability of the fund.

2.

Alongside the local authority loan funds and public private sector loan funds, exists a handful of major company or major industry loan funds. Some of these were initially established to assist redundant employees of the industry, for example, the British Coal Enterprise Fund, whilst others have been set up as part of their community programme initiatives for certain geographical areas, such as the BP Enterprise Fund. They are not strictly micro credit funds and demonstrate similarities to public private sector loan funds.

2.

There are a very limited number of proper micro finance funds that fit within the definition of the ILO Study. These include the national funds of PYBT and Industrial Common Ownership Finance (ICOF), and the Birmingham based Aston Reinvestment Trust, all of which are detailed below. Credit unions are also involved in micro finance provision. There are in the region of 650 credit unions in the United Kingdom. However, they do not provide universal coverage nor, with a few exceptions, do they specialise in micro finance. However, their mode of operation includes an element of a guarantee community. In addition to these funds, experiments are occurring with Mutual Guarantee Societies since 1996 and more recently with business credit unions, the first, in Wales, having been launched in May 1998. Consideration of other micro finance funds is taking place in several other locations in the UK including Norwich, for women, Tower Hamlets, for the Asian community, and Northern Ireland.

Micro finance for community enterprise is supported by ICOF Community Capital, Charities Aid Foundation (CAF) and Local

Investment Fund (LIF) and an initiative is being examined in Northern Ireland.

Micro enterprise training for the unemployed to become entrepreneurs is undertaken by a number of training providers including DHP Enterprise Limited and PYBT, who have both undertaken research into the survival of their client businesses, and who have sought to analyse the amount of displacement or deadweight arising from their programmes.

2.6. Scotland

22 Local Enterprise Companies in Scotland come under two umbrella organisations - Scottish Enterprise, covering 13 LECs, and Highlands and Islands Enterprise, covering 10 LECs (Moray, Badenoch and Strathspey Enterprise is funded by both organisations) - both of whom in turn are responsible to the Scottish Office. Under these umbrella agencies, each LEC is responsible for enterprise activity in its own region, having a broader economic development remit than the counterpart TECs in England and Wales, and is assigned powers to make the LEC flexible so as to respond to local needs and budgets when deciding what projects and schemes to pursue in each area.

Since the publication of Scottish Enterprise’s ‘Improving the Business Birth Rate: A Strategy for Scotland’ in 1993, assistance (including financial) to individuals wishing to set up a business has been a main feature of the activity of the LECs in Scotland. However, only projects costing over £250,000 would require approval from the umbrella organisations, with the result that micro finance schemes in particular vary greatly from region to region and with only limited exchange of knowledge of what is happening in

other areas. Evaluation of projects under £250,000 is also undertaken at the regional LEC level. However, Scottish Enterprise recently (June 1997) commissioned a market evaluation of the Business Start Up Scheme across the Scottish Enterprise network, which includes a review of evaluation reports from each LEC and a survey of assisted Start ups.

Enterprise Trusts and Local Economic Development Companies may be confused with the LECs but are completely separate organisations, often the product of a private and public partnership, and set up as private companies limited by guarantee with the objective of helping small businesses start and grow. Confusion arises as the Enterprise Trusts are invariably supported in part by the LECs, as well as the local authorities and a number of private sources. Enterprise Trusts administer the services and funds (particularly the microfunds) of the LECs. There are approximately 30 Trusts in existence in Scotland, a figure sharply reduced from the number in existence in the 1980s, giving less than complete coverage of the geographic area of Scotland - there is just one Enterprise Trust to cover the Highland Council area (Highland Opportunity Ltd) and none in some of the other areas. There is a concentration of Trusts in the areas of high population (such as Glasgow and Edinburgh) which reflects the growth of Enterprise Trusts in response to local demand.

The stimulation of small business and entrepreneurship became a major priority for economic policy in Northern Ireland during the mid-1970’s.

A number of initiatives were

undertaken such as:

The development of a network of local enterprise agencies offering flexible business incubation space, local advice and guidance, basic business training and, in many cases, a local seed corn fund for business development;

The streamlining of Government assistance for business start up; and

The introduction of business and enterprise awareness in school and college criteria.

Subsequently, as a result of EU policies, the 26 districts in Northern Ireland were given the lead role in local economic development for their areas and under the EU Peace and Reconciliation Programme District Partnerships were formed in each local authority area to determine expenditure priorities for special EU funding packages, which in many cases, included support to small businesses.

Role of Main Players in Business Support Network at Northern Ireland Level

Organisation Main Activities

Government

Principally through the Department of Economic Development agencies of LEDU (the Local Economic Development Unit) & the Training and Enterprise Agency (T&EA) – often delivered by private sector contractors

-Financial, training, marketing, information, business process improvement and other support measures for businesses with growth potential and particularly with potential for export growth or import substitution.

-Support to local enterprise agencies and the community sector

Local Authorities Local economic development, including business start up assistance, training and mentoring, and support to local enterprise agencies and other local business support structures

Peace & Reconciliation Partnerships in each local authority area

Special programmes, particularly targeted at areas of disadvantage and disadvantaged communities

Local Enterprise Agencies Provision of flexible workspace accommodation, business support services, small business training, special ‘target’ programmes to meet local needs, seed-corn funds, and networking

Community Sector Community development and empowerment, development of local strategies, channelling funds to disadvantaged areas, networking with other providers.

There has been little general research into micro finance, as defined, in the UK. However, there is much overlapping in the general and academic literature on small business and relevant issues – such as evaluations of the government Enterprise Allowance Scheme.

For practical reasons, this stocktaking exercise on the UK in this general part will be concerned with England and Wales, making specific reference to Scotland and Northern Ireland in the annexes. Naturally much of the information relating to England and Wales also applies to Scotland and Northern Ireland in any event.

3.

In library and internet searches, the choice of keywords used is significant. The following words (including hyphenated versions) were found to produce the most appropriate results: microcredit, micro finance, microenterprise, microentrepreneur, small business finance small firm finance, employment creation, business start-up, employment rehearsal, enterprise rehearsal, self-employment.

Searches against these words produced multiple entries (sometimes into the thousands) of which self-employment produced more helpful results. The literature search incorporated into the Annex is what appeared most relevant, based on the internet search and full citations are available on the internet.

Sources consulted were:

Panel members;

The British Library at Boston Spa;

http://opac97.bl.uk (British Library - BLDSC);

Leeds University Library on-line catalogue;

Leeds Metropolitan University Library on-line catalogue;

Internet search (using Infoseek);

Previous research undertaken by Malcolm Lynch Solicitors;

SBRC, Kingston University;

ESRC centre for business research, University of Cambridge;

Professor David Storey, Warwick Business School; and

DHP Enterprise Limited.

The most relevant literature we have come across has been produced by or on behalf of micro finance providers in-house, specifically the PYBT and INAISE, the International Association of Investors in the Social Economy based in Brussels. INAISE is an association of social banks and financial intermediaries. Only this literature has examined many of the issues relating to micro finance as required by this stocktaking exercise, but even these do not go to the issue of sustainability of the financial intermediary in much depth.

DfEE (1997) Prince’s Youth Business Trust Youth Enterprise Initiative Output-related Funding Scheme report (BMRB International)

P-E International (1992) Report on PYBT

Coopers & Lybrand (1997) Evaluation of PYBT in Northern Ireland

Seddon, J Wendy (1992) The Influence of the personal characteristics of young entrepreneurs upon the success or failure of their small businesses

PYBT/EPI (1998) What works? The new deal for young people

PYBT/EPI (199_) What works? Jobs for young people

Internal research of DHP Enterprise Limited on the survival of entrepreneurs it had trained in the South Yorkshire and North Derbyshire area (unpublished 1998).

INAISE DGV Les Instruments Financiers d’Economie Sociale en Europe et la Creation d’Emplois (1997 not yet published)

While not exactly micro finance, some of the published literature we have found is prima facie very relevant, particularly:

SBRC Kingson University (1997), Indicators of success and failure in young micro firms

DfEE (1998) Review of Business Start-Up Activities under the SRB

DfEE (1998) Helping Unemployed People into Self-Employment

DfEE (1998) Self-Employment for the unemployed: the role of public policy

DSS (1997) Self-employed people: a literature review for the contributions agency

Hughes, Alan: Small firms and Employment (ESRC Cambridge)

Some of this research looks at:

For which sub-groups of the unemployed is self-employment an option

The work and incomes of self-employed people

Deadweight and displacement by self-employment programmes

Social security benefits and

self-employment

Factors affecting survival in self-employment

b. Business and economics

Some relevant literature falls into this category. The universities of Warwick, Kingston and Cambridge have respectively produced the majority of detailed work in the small business area. “Understanding the Small Business Sector” by Professor Storey is a relevant general small business text and, for example, addresses questions such as access to finance.

Generally speaking, these approaches are concerned with benchmarking what makes businesses successful and the provision of finance - adequate and appropriate finance. However, the particular issues relating to micro finance are not addressed in as far as we have observed.

The DfEE and Department of Social Security have commissioned research looking at specific issues relating to self-employment within their areas of operation. The research of the Policy Studies Institute and the Centre for Research in Social Policy is referred to above. But, for example, as a public policy issue, the DfEE is concerned with general issues rather than micro finance in terms of self-employment.

“Self-employed people: a literature review for the contributions agency”, commissioned by the DSS, was prompted by a collection of National Insurance contributions from the self-employed, and gives a general overview of the growth in self-employment.

4.1. Current Research

Micro finance or micro credit is a comparatively new term within the UK economic lexicon. It is therefore not surprising that no common thread is drawn between all of the issues involved in micro finance in the literature, but rather that there is a piecemeal approach that looks at particular issues or programmes in isolation.

“The Entrepreneurial Society” of the IPPR is the least guilty of this approach, but nevertheless does not apply a critical perspective to micro finance as a commercial proposition, assuming it is a public sector task to encourage entrepreneurship – which may be paradoxical or inappropriate when micro finance providers are aiming to become sustainable.

Some of the terminology used by the ILO is not recognised in current research. The small business literature does not deal with access to finance for people without any capital or credit history at all, rather it glosses over this start-up issue.

G overnm ent s elf - empl oymentt r ai ni ng

Self - empl oyment

Sm all bus i nes s

Regi onal as s is tance

& devel opment

Sof t- l oans

Ment or ing, bus i nessad vice and s upport

M ai ns tr eam bankbus i nes s lendi ng

St at e benefi t s

Gr ants

Mi cro fin ance i ssues

Some research on self-employment touches upon whether a grant or a loan is provided to an entrepreneur and the survival rates of people in receipt of either or both of them, including the characteristics of the entrepreneur in terms of age, gender, length unemployed, education and ethnic background, and the type of business sector in which they are established.

Self-employment is analysed from a general perspective – the most useful approaches deal with the “from unemployment to self-employment” issues but do not make explicit the financing of new business. Should a distinction be drawn between someone with a few thousand pounds redundancy money to invest in a business, who requires training to establish the business and someone who must find outside financing to actually start-up?

Entry into self-employment and length of survival are examined by research, but there may be gaps in assessing what happens to persons when they cease to trade and why they cease to trade. Ceasing to trade may have a positive outcome and not only be a negative outcome.

Micro finance straddles many areas of interest. The EU, central government and local government are all concerned with economic growth and employment. Mainstream banks want profitable small business customers and to some extent, a good reputation for small business and commitment to communities for marketing purposes. The Bank of England monitors SME financing by the banks, but not micro credit as a particular specialisation. The Bank of England has also turned its attention again to the particular problems facing the financing of businesses by ethnic minorities as have some other banks.

What the research generally

omits is discussion of the nature of the microfinance provider and how the delivery of micro finance is effected by the survival of the micro finance provider and the type of private and public sector support which it is able to obtain.

Malcolm Lynch Solicitors in their study entitled, “The Social Responsibility of Credit Institutions”, published in 1997, considered, in overview, the lack of specialisation of banks in this area; the absence of a common approach to small business and micro credit lending techniques, and the absence of the sustainability of many small business and micro credit funds. Many funds also indicated a drift towards higher amounts of lending.

Research suggests that micro finance for micro business is marginalised by existing support mechanisms of TECs and Business Links in England and Wales, and in Scotland and Northern Ireland there is anecdotal support for a similar proposition. Whilst the Government may establish national programmes which include an option for self-employment mechanisms, the delivery of this option is haphazard and lacks universality. Some business agencies may presume that savings, informal loans, grants and general resourcefulness satisfy this initial hurdle or otherwise do not give it a high priority. In rural areas of England and Wales, a specific loan scheme for rural entrepreneurs was ended in 1997 without a replacement scheme being put in its place.

4.2. On-going Research

The New Economics Foundation together with the University of Birmingham has been considering how lessons from micro credit initiatives in the United States can be applied in the UK as part of research for the Joseph Rowntree

Foundation to be completed in 1998.

Elaine Kempson, formerly of the Policy Studies Institute, has recently moved to the University of Bristol to establish a personal finance research unit. She is currently engaged in preliminary research on identifying best practice in micro credit in Europe as part of an approach to benchmark micro finance institutions for the European Union.

There is a limited amount of research that looks into whether micro finance helps the unemployed to create businesses, which suggests that certain techniques and support can produce higher survival rates than mainstream bank lending. There is also limited research on survival of these enterprises for up to a 5 year period. There is an absence of research into what is the relative importance of different techniques, for example: training before entrepreneurship as against mentoring of the entrepreneur; the significance of market or below market rates of interest; and the significance of formal guarantee mechanisms as against informal non-financial guarantors.

There is reasonably accessible information on the legal status of financial intermediaries, their funding, and their links with the public, private and voluntary sector. There is an absence of collation of this material and no research into the sustainability of the financial intermediary with the possible exception of the INAISE report, which does not consider this issue in depth.

This has implications for the public support of private and public micro finance initiatives.

The establishment of micro enterprises not only leads to sole employment, but can lead to a doubling of employment by an entrepreneur with a surviving business within a few years of establishment. The cost effectiveness of support for self-employment programmes has been established through current research, but self-employment programmes with public subsidy are not universally available.

In the UK, public programmes are supporting micro entrepreneurship, but not in a universal way. Micro finance is not seen as a specialist technique by the public or private sector and similarly receives non-universal support. Current public providers of small business finance and micro credit do not appear to learn lessons from other providers or address the issue of sustainability for the micro financial institution or for the private or public sector training providers.

There appears to be an absence of research into the comparability of funding under the Loan Guarantee Scheme for micro business where it exists, and micro finance initiatives as defined for this stock taking exercise.

Banks are involved in some micro finance initiatives, and have been for many years. Some have developed close relationships with micro finance initiatives, for example PYBT, but the commercialisation of the knowledge they have obtained into their own products or into developing their own specialisation is currently not apparent, or is not something which is on their policy agenda as an appropriate area of business development for the future.

The significance of developing or supporting national micro finance initiatives as against regional or local

ones has not been considered.

Whilst this overview has touched lightly upon geography, ethnicity and gender as ancillary sub-areas of research unemployment data can be related to ethnicity and geography, both rural and urban which may require some special attention.

Additionally, we would highlight the following supplemental areas to which consideration might be given:

Consideration of issues of best practice - benchmarking of successful micro finance lending;

Focus on meaning of success and establishment of realistic sustainability goals for micro-business, query transferability of skills learnt for failed businesses – all in context of unemployment;

Discussion of where money should come from for the finance element of micro finance;

Arguments for a special guarantee fund for micro finance ;

Assessment of the scale of the problem - how many good micro-business ideas are held back and how best to find and encourage them;

Examining the question of a “gap”, where funds ought properly to be advanced but are not currently;

Consideration of the transaction costs for a micro-credit provider and whether this should be supported through public sector support or some kind of micro finance investment scheme which engages personal or corporate funding; and

Consideration of the

destination of people whose businesses fail and whether the closure of the business had a positive outcome leading to employment, further self-employment or otherwise.

Annex I: Literature Search

§ As part of the review, some texts identified were briefly examined and a template of relevant texts completed. In addition, other texts which may have some relevance or are otherwise mentioned in the paper include those set out below.

Type of Assessment Physical review

Title The Social Responsibility of Credit Institutions in the EUUK Country Report

Date of publication 1997

Author(s) Malcolm Lynch, Leo Haidar

Addresses Malcolm Lynch Solicitors19 High Court LaneThe CallsLeeds LS2 7EU

Issues reviewedsurvival of self-employment (micro issues) Nosustainability of the intermediary Yescost effectiveness, displacement, dead-weight and other general effects (macro issues)

Yes

coverage of micro finance questions- extensive, cursory

Extensive

Type of institutions analysed? Governmental, private and not-for-profit

Type of financial services dealt with? General – credit institutions and “banking service providers”

Areas suggested for further research Consideration of United States Community Reinvestment Act approach in the UK

Method (empirical survey, if so what sample size; case studies etc.)

Survey of credit unions and local authorities

-------------------------------------------------------

Type of Assessment Physical review

Title Indicators of success and failure in young micro firms (for Solotec)

Date of publication March 1997

Author(s) SBRC, Kingston University

Addresses

Issues reviewed

survival of self-employment (micro issues)sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions- extensive, cursoryType of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

-------------------------------------------------------

Type of Assessment

Title

Date of publication

Author(s)

Addresses

Issues reviewed

survival of self-employment (micro issues)sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions

- extensive, cursoryType of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

-------------------------------------------------------

Type of Assessment

Title Start-up costs and pecuniary externalities as barriers to economic development

Date of publication (1993)

Author(s) Antonio Ciccone, Kiminori Matsuyama

Addresses National Bureau of Economic Research Working paper # 4363

Issues reviewed Cross-comparison of industrialised and developing countries and choice of technology and specialisation in production of consumer goods, discussion of incentives to start-up firms – existance of a “development trap”. Consideration of inducements for start-up firms to enter the market and circularity between degree of specialisation, market share of “intermediate” inputs and present barriers to economic development. Model proposed suggests a threshold in economic development and a development trap.

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions

- extensive, cursoryType of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

-------------------------------------------------------

Type of Assessment Physical review

Title Review of Business Start-up Activities under the Single Regeneration Budget

Date of publication (1998)

Author(s) Department for education and employment (York Consulting)

Addresses

Issues reviewed level and pattern of support for business start-up & best Practice

survival of self-employment (micro issues)sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions

- extensive, cursoryExtensive

Type of institutions analysed? SRB challenge fund funding

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

---------------------------------------------

Type of Assessment

Title

Date of publication

Author(s)

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions

- extensive, cursoryType of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

---------------------------------------------

Type of Assessment

Title

Date of publication

Author(s)

Addresses

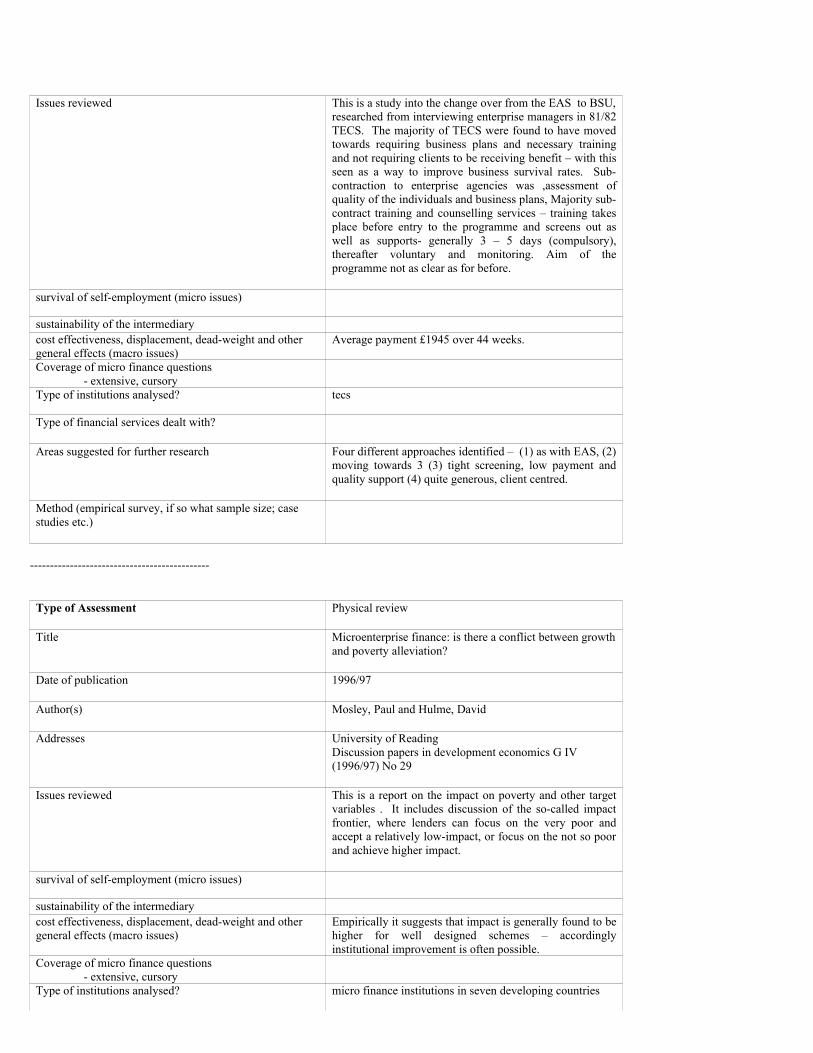

Issues reviewed This is a study into the change over from the EAS to BSU, researched from interviewing enterprise managers in 81/82 TECS. The majority of TECS were found to have moved towards requiring business plans and necessary training and not requiring clients to be receiving benefit – with this seen as a way to improve business survival rates. Sub-contraction to enterprise agencies was ,assessment of quality of the individuals and business plans, Majority sub-contract training and counselling services – training takes place before entry to the programme and screens out as well as supports- generally 3 – 5 days (compulsory), thereafter voluntary and monitoring. Aim of the programme not as clear as for before.

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)

Average payment £1945 over 44 weeks.

Coverage of micro finance questions- extensive, cursory

Type of institutions analysed? tecs

Type of financial services dealt with?

Areas suggested for further research Four different approaches identified – (1) as with EAS, (2) moving towards 3 (3) tight screening, low payment and quality support (4) quite generous, client centred.

Method (empirical survey, if so what sample size; case studies etc.)

---------------------------------------------

Type of Assessment Physical review

Title Microenterprise finance: is there a conflict between growth and poverty alleviation?

Date of publication 1996/97

Author(s) Mosley, Paul and Hulme, David

Addresses University of ReadingDiscussion papers in development economics G IV (1996/97) No 29

Issues reviewed This is a report on the impact on poverty and other target variables . It includes discussion of the so-called impact frontier, where lenders can focus on the very poor and accept a relatively low-impact, or focus on the not so poor and achieve higher impact.

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)

Empirically it suggests that impact is generally found to be higher for well designed schemes – accordingly institutional improvement is often possible.

Coverage of micro finance questions- extensive, cursory

Type of institutions analysed? micro finance institutions in seven developing countries

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

----------------------------------------------

Type of Assessment

Title

Date of publication

Author(s)

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions

- extensive, cursoryType of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

------------------------------------------

Type of Assessment

Title

Date of publication

Author(s)

Addresses

Issues reviewed Academic journal (US with some UK input) looking at access to loans by small business and securitisation in a public policy context, querying whether banking relationships constrain small bsuiness performance, bank financing of UK small business (Keasey) etcetera.

survival of self-employment (micro issues)sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions

- extensive, cursoryType of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

-----------------------------------------

Type of Assessment Physical review

Title Are Small Firms the answer to unemployment?

Date of publication 1987

Author(s) Storey, D.J. and Johnson, S.

Addresses Employment Institute

Issues reviewed Examination of UK government policy towards small firms, connection with increased start-up rates during recession and regional profile of developments. Proposes that no standard small firms policy is possible, advocating removal of public assistance and focussing on quality and likelihood of growth.

survival of self-employment (micro issues)sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions

- extensive, cursoryType of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

------------------------------------------

Type of Assessment Physical Review

Title

Date of publication

Author(s)

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediary

cost effectiveness, displacement, dead-weight and other general effects (macro issues)

coverage of micro finance questions- extensive, cursory

type of institutions analysed?

type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

------------------------------------------

Type of Assessment

Title

Date of publication

Author(s)

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)

Coverage of micro finance questions- extensive, cursory

Extensive coverage of micro finance in the USA and in developing countries. Does not cover the UK.

Type of institutions analysed? Micro finance organisations

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

------------------------------------------

Type of Assessment Physical Review

Title Barriers to business start up: A study of the flow into and out of self-employment

Date of publication 1989

Author(s) Julie Bevan Research surveys of Great Britain LtdSocial Science Branch Department of Employment

Addresses

Issues reviewed Surveys the factors which influence individuals to become self employed, and ascertains the relative importance and perceived constraints. There is a section on finance, but it does not refer to micro finance, nor does it distinguish the size of business.

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)

Coverage of micro finance questions- extensive, cursory

Type of institutions analysed?

Type of financial services dealt with? Bank lending and other forms of enterprise support grants to see how access to credit affects a persons decision to become self employed.

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

-----------------------------------------

Type of Assessment Physical review

Title Small firms in regional economic development

Date of publication 1985

Author(s) D. J. Storey 1985

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediary

cost effectiveness, displacement, dead-weight and other general effects (macro issues)

coverage of micro finance questions- extensive, cursory

type of institutions analysed?

type of financial services dealt with?

Areas suggested for further research

-----------------------------------------

Type of Assessment

Title

Date of publication

Author(s)

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)

Coverage of micro finance questions- extensive, cursory

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

Survey of small business in North and East Cornwall employing less than 10 employees.

-----------------------------------------

Type of Assessment Physical Review

Title From unemployment to self-employment

Date of publication 1996

Author(s) A Bryson and M White

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)

Estimates how advantageous self-employment is as a route out of long term unemployment in terms of time taken to enter a job, job stability earnings and subsequent unemployment avoidance.

Coverage of micro finance questions- extensive, cursory

Type of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research How the long term unemployed can be encouraged to become self employed.

Method (empirical survey, if so what sample size; case studies etc.)

Empirical surveys.

-----------------------------------------

Type of Assessment Physical review

Title Self-employment enterprise and social inclusion

Date of publication 1997

Author(s) National Economic and social forum

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediary

cost effectiveness, displacement, dead-weight and other general effects (macro issues)

Coverage of micro finance questions- extensive, cursory

Type of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

-----------------------------------------

Type of Assessment

Title

Date of publication

Author(s)

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions

- extensive, cursoryType of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

---------------------------------------------

Type of Assessment

Title

Date of publication

Author(s)

Addresses

Issues reviewed evaluation of performance against objectives

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)

yes

Coverage of micro finance questions- extensive, cursory

estensive

Type of institutions analysed? PYBT

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

survey of award recipients during three time periods

---------------------------------------------

Type of Assessment Physical review

Title Report on the Prince’s Youth Business Trust iin Northern Ireland

Date of publication 1997

Author(s) Coopers & Lybrand

Addresses

Issues reviewed evaluation of performance against objectives and LEDU activities

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)

yes

Coverage of micro finance questions- extensive, cursory

Extensive

Type of institutions analysed? PYBT

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

PYBT & LEDU client database

--------------------------------------------

Type of Assessment Physical review

Title

Date of publication

Author(s)

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions

- extensive, cursoryType of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

--------------------------------------------

Type of Assessment

Title

Date of publication

Author(s)

Addresses

Issues reviewed

survival of self-employment (micro issues)

sustainability of the intermediarycost effectiveness, displacement, dead-weight and other general effects (macro issues)Coverage of micro finance questions

- extensive, cursoryType of institutions analysed?

Type of financial services dealt with?

Areas suggested for further research

Method (empirical survey, if so what sample size; case studies etc.)

Full details of most of the texts below are available from http://opac97.bl.uk (British Library) by undertaking a title search. The nature of the searches undertaken make full references here problematic.

(1981) The Business start-up scheme

(1986) Business start-up checklist

(1987) Business start-up

(1987) The Start-up

(1989) 3i management start-up what it takes to bring into being the kind of business most likely to succeed

(1989) Barriers to business start-up A study of the flow into and out of self-employment

(1989) supporting the start-up and growth of small firms A study in West Lothian

(1989) Training for enterprise start-up – the gender dimension

(1990) Clothing business start-up project a year’s work with inner city residents in the West Midlands trying to start their own clothing businesses

(1991) An investigation into failure in start-up businesses and some suggestions on how failure rates might be reduced

(1994) Business start-up checklist

(1996) ECRH-assisted start-up in ITER

(1996) Microenterprise finance is there a conflict between growth and poverty alleviation

(1996) What makes a new business start-up successful?

(1997) Policy, prediction and growth picking start-up winners

(c1983) financing your new business

(c1989) Start-up money: Raise what you need for your small business

A start-up is born! Symposium 192nd National Meeting Abstracts

Allen, David. Enterprise allowance scheme evaluation

Arkebauer, James B (c1993) Ultrapreneuring taking a venture from start-up to harvest in three years or less

Bank of England (1997) Finance for Small Firms - a fourth report

Bates, James. The financing of small business

BBA Banks and Businesses: Working Together: A Statement of Principles March 1997, The British Bankers' Association

Berle, Gustav (c1990) Raising start-up capital for your company

Bevan, Julie (1989) barriers to business start-up: a study of the flow into and out of self-employment

Birley, Sue (1982) New enterprises A start-up case book

Birley, Sue (c1982) New enterprises A start-up case book

British Venture Capital Association (1996/7) Sources of Business Angel Capital

Collinge, Chris. (1983) Investing in the local economy: business finance and the role of local government

Creevey, Lucy E (1996) Changing women’s lives and work an analysis of the impacts of eight microenterprise projects

Department of the Environment for Northern Ireland (1998, unpublished) Micro-enterprise finance in disadvantaged areas of Belfast, A catalogue and analysis

Department of Trade and Industry Loan Guarantee Scheme

Gray, Colin (1986) Allowing for enterprise - small business research trust

Harroch, R D (1988). Start-up companies planning, financing and operating the successful business

Herbert, A and Kempson, E Credit Use and Ethnic Minorities (PSI)

Hughes A, Storey D J. Finance and the small firm

ILO Geneva, Collateral, Collateral Law and Substitutes, Poverty Orientated Banking Programme

INAISE, DGV Les Instruments Financiers d’Economie Sociale en Europe et la Creation d’Emplois

Johnson, S. and Rogaly, B. Micro finance and poverty reduction Oxfam

Journal of entrepreneurial and small business finance

Journal of Small Business FinanceKlett, Martina (August 1993 & June 1994) A Directory of Soft Loan Schemes Available for Small

Business in England Small Business Research Centre, Kingston University

Klett-Davies, Martina A directory of Soft Loan Schemes available for small businesses in England

Lambden, John. (1993) small business finance a simple approachMalcolm Lynch Solicitors (1997) Survey of Local Authorities’ Support of

Micro finance

Meager, Nigel Self-employment and Labour Market Policy in the European Community WZB Berlin

Microenterprise News

Mullineux, A. SME financing in the UK

National Westminster Bank (1992) The NatWest guide to starting and running a business

National Westminster Bank (1996) African-Caribbean businesses and their banks

National Westminster Bank (Robert Cressy & David Storey) (1995) New firms and their bank

National Westminster Bank (1997) Asian businesses and their banks

NatWest/BiTC brochure Local Investment Fund

OFT (1997) Non-Status Lending Guidelines for Lenders and Borrowers

OFT (May 1992) Credit scoring- a report by the director general of fair trading

Opportunity Trust (1995) Annual Global Summary

Otero, Maria and Rhyne, Elisabeth (eds.)(1994) The new world of microenterprise finance

Building healthy financial institutions for the poor

Prince’s Youth Business Trust 10th anniversary 1986-1996 press pack

Rhyne, Elisabeth and Rotblatt, Linda S (1994) What makes them tick? Exploring the anatomy of major microenterprise finance organisations

Rodriguez, Cheryl Rene (c1995)

Women, microenterprise and the politics of self-help

SBRC, Kingston University Enterprise support for young people: a study of the effects of business counselling on young business owners

Segal Quince Wicksteed (1988) Encouraging small business start-up and growth Creating a suppotive local environmentSmall Business Research Centre Department of Applied Economics University of Cambridge The State of British Enterprise: growth, innovation and competitive advantage in small and medium sized firms

Small Business research Centre, Kingston University (1997) Indicators of Success and failure in young micro-firms

Stearns, Katherine. (1991) Interest rates and self-sufficiency tool for microenterprise programs, financial assistance section

Storey, D J. (1983) Small firms in regional economic development

Storey, D J. (1987) Are small firms the answer to unemployment?

Storey, D J (1994)Understanding the Small Business Sector Routledge

Storey, D J. (1993) Should we abandon the support to start-up businesses

The case of Scotland’s largest ever stand-alone start-up enterprise HCI at Clydebank

The Journal of entrepreneurial and small business finance

The problems of raising start-up capital for workers’ co-operatives

LENTA (1982) sources of finance for small firms

New entrepreneurs - self-employment and small business in europe

Golzen, Godfrey Daily Telegraph guide to working for yourself

The inequlity of employment and self-employment incomes - A decomposition anaysis for the UK

Annex II: Micro finance Organisations

Fund Prince’s Youth Business Trust

Products a maximum loan of £5,000 (average £2,000) and a maximum grant of £1,500.

Comments The Prince’s Youth Business Trust is the largest national soft loan fund for micro-credit in the United Kingdom. It is a truly national fund operating in all four provinces (under slightly different arrangements) but is targeted towards young people. Over three quarters of its funds are disbursed as loans repayable over two or three years with a low interest rate. It considers itself as a lender of last resort, so it is a condition of lending that finance is not forthcoming elsewhere. All lending is unsecured.

After-care A key element of the Trust’s support is the provision to each business which receives support of an adviser who provides a few hours support every month to the business for up to three years. It is this latter support which distinguishes it from most other micro-credit providers, and which is one of the most significant reasons for the high survival rates of its clients.

Statistics On average more than 60% of its business clients survive 3 years as against 25% nationally. It assisted 3,600 people with financial support in 1996. In 1996 41% of those supported were women, 10% were from ethnic minorities, 5% were disabled and 10% young offenders

---------------------------------------------

Fund David Hall Partnership business support

Products business counselling and support – no finance

Comments Although not strictly speaking a micro finance provider, DHP is a commercial provider of business support and advice which works directly for TECS and through their high street presence, the Business Links. The organisation is perhaps best viewed as an outsourced provider of self-employment counselling.

After-care yes

Statistics

---------------------------------------------

Fund

Products

Comments

After-care

Statistics

---------------------------------------------

Fund

Products

Comments (ART) is the newest socially directed investment fund in the United Kingdom. Its principal purpose is to fill the funding gaps created by the withdrawal of banks and building societies from the Aston area of Birmingham. ART sees its role model in the South Shore Bank of Chicago. A bank, based in what became a poorer district of Chicago the ownership of which was acquired by community activists to some extent as a result of the Community Reinvestment Act of the United States. The target of the ART group’s investments are micro-businesses, housing associations and voluntary organisations. The development of ART has been assisted by several banks which have provided advice (for example Triodos Bank) and financial assistance in cash and kind. Barclays have provided a secondee as managing director. NatWest have provided a board director, as have ICOF. Unity Trust Bank, the trade union bank based in Birmingham have launched a regional investment bond with an option for investors to donate a part of the interest with the ART Group. The chairman of the ART Group is a former Bank of England Board Director.

After-care yes

Statistics none available

Annex III: Bibliographies of some research undertaken

In addition to the above literature sources, there are additional bibliographic references which may have some relevance. These include the bibliographies of :

tDepartment of Social Security

Literature Review andL

IPPR “The Entrepreneurial Society”

Annex IV: Private / Public Sector Small Business/Micro credit Funds

Small Business Research Centre, Kingston University

The Small Business Research Centre of Kingston University sponsored by Midland Bank plc undertook research in 1993 and 1994 to ascertain how many schemes there were and what conditions attached to the loans made by each scheme. In 1993 they found 61 soft loan schemes in England. In 1994 they found 28 new schemes to add to the list and 11 that had closed bringing the total to 82. The schemes contained within this survey are all schemes which are separate from local authorities. Some received funding from a local authority, and others were supported by commercial banks, government departments, commercial companies and charities or were established together with Training and Enterprise Councils or Business Links.

*We attach a copy of the cover of the last report undertaken. Copies are available from Kingston University.

Annex V: Public Sector/Private Sector in England and Wales (1997)

An edited extract from the Social Responsibility of Credit Institutions:

As part of a previous research project Malcolm Lynch Solicitors undertook a survey of district, county and unitary authorities in England and Wales, including the major conurbations (excepting London) to consider to what extent local authorities were still active in providing loan funds for micro business. In total 463 local authorities were contacted by way of a written questionnaire, full details of which are set out in the Appendix. 127 responses were received. The results of the survey are given in the following table:

Local authority economic development funds for small and

young business

Total number of fundsSmall firms loan funds 32Small firm grant funds 17

Sample 127 local authority EDUs Source MLS

The survey shows that one quarter of local authorities responding to our survey in England and Wales have loan funds which are available to assist micro-business with appropriate micro finance. Some of the funds placed some limitations on their target clients, so that it was restricted for example to manufacturing, or tourism. Only one preferred to concentrate on businesses which had survived the first year. There were a wide range of interest rates charged, from 0% to 3% above base lending rate, and some differing requirements in the collateral required. Many of the funds had the criterion that they would be a lender of

last resort if a loan was not available from the commercial banking sector. Some of the funds were drawing to a close because of bad debts and the exhaustion of funds from the sponsoring body. Others may have a restricted time span for similar reasons.

The overall impression given by the survey is a lack of uniformity of approach which may be because each local authority was seeking to address local circumstances which had been identified. Alternatively, it may be due to a lack of comparative experience with information about what makes revolving loan funds more viable not being shared between different local authorities.

Local authorities were not asked whether they operated grant assistance programs for micro-business but 17 (13%) volunteered that they only had grant schemes while some offered both. It is not possible to tell whether this was an under-representation of the total number of grant schemes or not. Grants can play a useful role for micro-entrepreneurs in providing the equity capital equivalent which may lever out loans and credit from the private sector. However, they may also put off the day when the micro-entrepreneur has more effectively to plan to meet the discipline of loan repayments.

Many local authorities still play an important role in providing micro finance to micro-business. Our survey found several local authorities considering whether they might become active in this area. Some were seeking to access European or central Government funds for that purpose. A few had involved commercial banks in a partnership with the local authority, or had placed the fund with an existing local or regional development fund. One authority included in the survey had

placed the fund with the Prince’s Youth Business Trust. It is likely that many local authorities would benefit from a program to share experience on the operation of their funds.

The division of economic development between local authorities, Training and Enterprise Councils and Business Links has led to calls for rationalisation of agencies delivering business support. The British Chambers of Commerce have suggested that a distinction is drawn between services to business, which should be provided by those agencies and services to the unemployed or those with a social content which should be the responsibility of other agencies. (FT15.7.1997 p9) The impact of suggestions such as these on financial support for micro-business is difficult to judge.

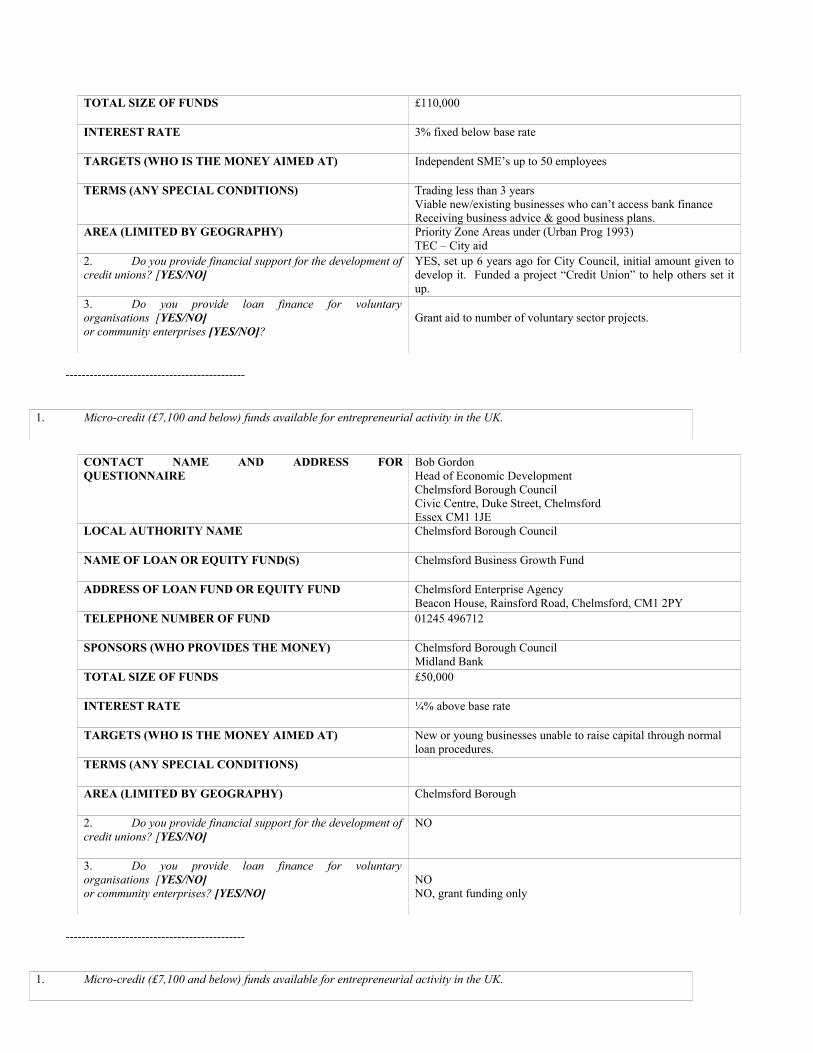

1. Micro-credit (£7,100 and below) funds available for entrepreneurial activity in the UK.

CONTACT NAME AND ADDRESS FOR QUESTIONNAIRE

LOCAL AUTHORITY NAME

NAME OF LOAN OR EQUITY FUND(S)

ADDRESS OF LOAN FUND OR EQUITY FUND

TELEPHONE NUMBER OF FUND

SPONSORS (WHO PROVIDES THE MONEY)

TOTAL SIZE OF FUNDS

INTEREST RATE

TARGETS (WHO IS THE MONEY AIMED AT)

TERMS (ANY SPECIAL CONDITIONS)

AREA (LIMITED BY GEOGRAPHY)

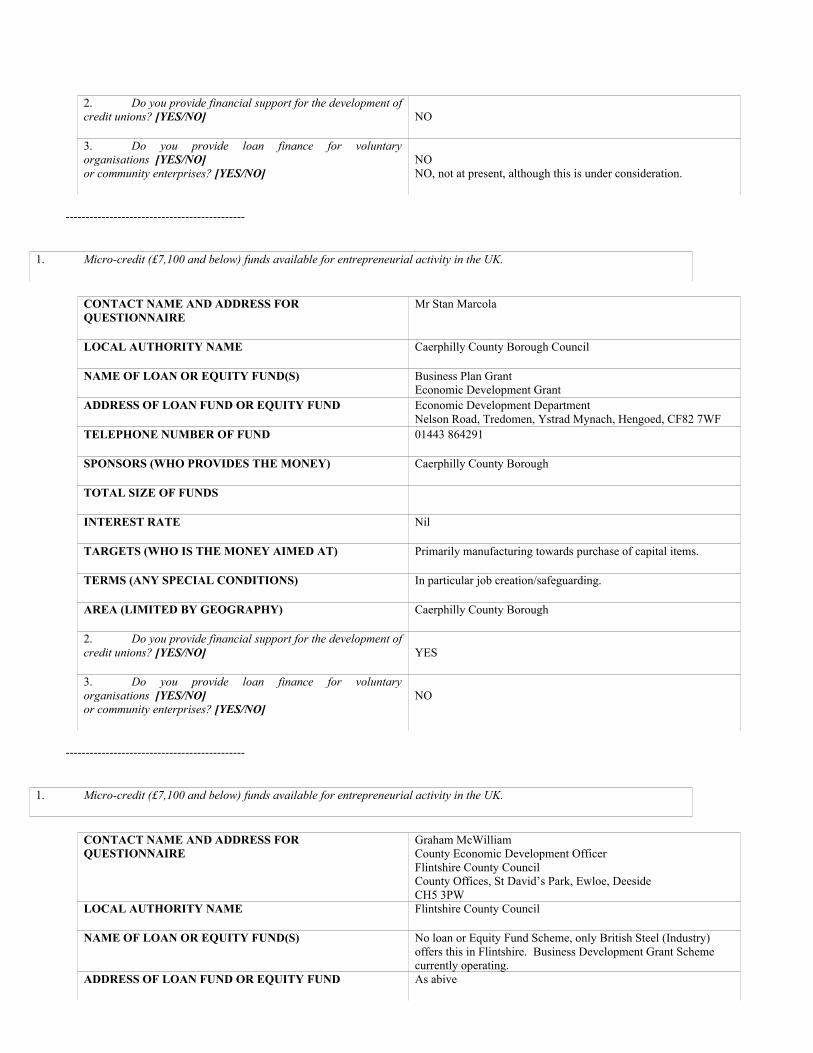

2. Do you provide financial support for the development of credit unions? [YES/NO]

3. Do you provide loan finance for voluntary organisations [YES/NO] or community enterprises? [YES/NO]

---------------------------------------------

1. Micro-credit (£7,100 and below) funds available for entrepreneurial activity in the UK.

CONTACT NAME AND ADDRESS FOR QUESTIONNAIRE

Tony CurtisCommunity Enterprise Officer

LOCAL AUTHORITY NAME Northumberland County CouncilSouthgate, MorpethNE61 2EH

NAME OF LOAN OR EQUITY FUND(S) Co-operative & Community Business Grants Fund

ADDRESS OF LOAN FUND OR EQUITY FUND As above

TELEPHONE NUMBER OF FUND 01670 533927

SPONSORS (WHO PROVIDES THE MONEY) Northumberland County Council

TOTAL SIZE OF FUNDS£20,000 Per annum Maximum feasibility grant £1,000Maximum starting grant £3,000

INTEREST RATE (grants only)

TARGETS (WHO IS THE MONEY AIMED AT) Co-ops. (workers, secondary, consumer, community enterprise) LETS, Credit Unions, Out of school clubs, etc

TERMS (ANY SPECIAL CONDITIONS) Usual return of funds if project fails or if co-op reverts to non-democratic ownership.

AREA (LIMITED BY GEOGRAPHY) Northumberland County

2. Do you provide financial support for the development of credit unions? [YES/NO]

YES

3. Do you provide loan finance for voluntary organisations [YES/NO] or community enterprises? [YES/NO}

NONO

---------------------------------------------

1. Micro-credit (£7,100 and below) funds available for entrepreneurial activity in the UK.

CONTACT NAME AND ADDRESS FOR QUESTIONNAIRE

Norman WhyteYork Business Development Centre Ltd

LOCAL AUTHORITY NAME City of York Council

NAME OF LOAN OR EQUITY FUND(S) York Business Development Fund

ADDRESS OF LOAN FUND OR EQUITY FUND 1 DavygateYork YO1 2QE

TELEPHONE NUMBER OF FUND 01904 646803

SPONSORS (WHO PROVIDES THE MONEY) City of York Council

TOTAL SIZE OF FUNDS

INTEREST RATE

TARGETS (WHO IS THE MONEY AIMED AT)

TERMS (ANY SPECIAL CONDITIONS)

AREA (LIMITED BY GEOGRAPHY)

2. Do you provide financial support for the development of credit unions? [YES/NO]

3. Do you provide loan finance for voluntary organisations [YES/NO] or community enterprises? [YES/NO]

---------------------------------------------

1. Micro-credit (£7,100 and below) funds available for entrepreneurial activity in the UK.

CONTACT NAME AND ADDRESS FOR QUESTIONNAIRE

LOCAL AUTHORITY NAME

NAME OF LOAN OR EQUITY FUND(S)

ADDRESS OF LOAN FUND OR EQUITY FUND

TELEPHONE NUMBER OF FUND

SPONSORS (WHO PROVIDES THE MONEY)

TOTAL SIZE OF FUNDS

INTEREST RATE

TARGETS (WHO IS THE MONEY AIMED AT)

TERMS (ANY SPECIAL CONDITIONS)

AREA (LIMITED BY GEOGRAPHY)

2. Do you provide financial support for the development of credit unions? [YES/NO]

3. Do you provide loan finance for voluntary organisations [YES/NO] or community enterprises? [YES/NO]

---------------------------------------------

1. Micro-credit (£7,100 and below) funds available for entrepreneurial activity in the UK.

CONTACT NAME AND ADDRESS FOR QUESTIONNAIRE

East Sussex County CouncilMrs C ParfectEconomic Development Manager

LOCAL AUTHORITY NAME Transport & environment DepartmentSouthover Road, LewesEast Sussex, BN7 1YA

NAME OF LOAN OR EQUITY FUND(S) East Sussex Small Loans Fund

ADDRESS OF LOAN FUND OR EQUITY FUND C/O Enterprise AgenciesSummerfields Business CentreBohemia Road, HastingsTN34 1UT

TELEPHONE NUMBER OF FUND 01424 433333

SPONSORS (WHO PROVIDES THE MONEY) East Sussex County Council

TOTAL SIZE OF FUNDS£36,202

INTEREST RATE Attached leaflet

TARGETS (WHO IS THE MONEY AIMED AT) As above

TERMS (ANY SPECIAL CONDITIONS) Available C/O Enterprise Agencies

AREA (LIMITED BY GEOGRAPHY) East Sussex County

2. Do you provide financial support for the development of credit unions? [YES/NO]

NO

3. Do you provide loan finance for voluntary organisations [YES/NO] or community enterprises? [YES/NO]

---------------------------------------------

1. Micro-credit (£7,100 and below) funds available for entrepreneurial activity in the UK.

CONTACT NAME AND ADDRESS FOR QUESTIONNAIRE

Michael LenihanEconomic Development Officer

LOCAL AUTHORITY NAME Rigby Borough CouncilThe Retreat, Newbond RoadRigby

NAME OF LOAN OR EQUITY FUND(S) RBC does not have a loan but Warwick County Council do – named Small Business Loan Scheme

ADDRESS OF LOAN FUND OR EQUITY FUND Warwickshire County Council, Sir Frank Whittle Business Centre, Great Central Way, Butlers Leap, Rigby, CV 21 3XH

TELEPHONE NUMBER OF FUND 01788 551500

SPONSORS (WHO PROVIDES THE MONEY) Warwickshire County Council

TOTAL SIZE OF FUNDS 150k available in 5k-7.5k

INTEREST RATE +1%

TARGETS (WHO IS THE MONEY AIMED AT) SMES

TERMS (ANY SPECIAL CONDITIONS)

AREA (LIMITED BY GEOGRAPHY)

2. Do you provide financial support for the development of credit unions? [YES/NO]

3. Do you provide loan finance for voluntary organisations [YES/NO] or community enterprises? [YES/NO]

---------------------------------------------

1. Micro-credit (£7,100 and below) funds available for entrepreneurial activity in the UK.

CONTACT NAME AND ADDRESS FOR QUESTIONNAIRE

LOCAL AUTHORITY NAME

NAME OF LOAN OR EQUITY FUND(S)

ADDRESS OF LOAN FUND OR EQUITY FUND

TELEPHONE NUMBER OF FUND