enhancing cooperation & regional integration of asean equity … · 2016-03-29 · the larger...

TRANSCRIPT

Enhancing Cooperation & Regional Integration

of ASEAN Equity Markets

Jaseem AhmedDirector,

Governance, Finance and Trade DivisionSoutheast Asia DepartmentAsian Development Bank

9th OECD-ADBI after the financial crisis: Prospects towards the future

Tokyo27 February 2008

2

Background Document

I. Overview: ASEAN Equity Markets

II. Initiatives for ASEAN Financial Integration

III. ADB‘s Technical Assistance: Progress to Date &

Next Steps

3

Overview: ASEAN Equity Markets

4

1. Issuers Equity and debt securities

2. Reputational intermediaries Accounting firms, investment banks, law firms and stock exchanges

Investment funds, pension funds, financial press

3. Self-regulatory organizations Professional federations

Standard setters

Exchanges

4. Government institutions Securities Commission

Courts

5. Laws Securities laws

Company laws

Bankruptcy laws

Components of Securities Market Regulation

5

Asset Distribution in Southeast Asia

(percent of GDP)

With the exception of Hong Kong, Singapore and Malaysia, all of which have large equity markets as a percentage of GDP, banks tend to dominate financial intermediation in East Asia.

Banks Assets Equity Market Capitalization

Bonds Outstanding

Economy 1997 2004 2005 1997 2004 2005 1997 2004 2005

PRC

Hong Kong,

China

Indonesia

Republic of

Korea

Malaysia

Philippines

Singapore

Thailand

124.6

205.1

31.1

37.9

100.9

56.1

122.0

79.7

176.4

337.5

14.6

130.1

169.0

66.5

176.8

129.2

163.1

444.6

49.8

93.5

159.4

63.2

185.4

103.6

11.2

234.5

12.2

8.1

93.2

37.7

110.8

15.1

23.1

519.5

28.8

57.1

153.3

33.0

202.3

71.4

17.8

593.6

28.9

91.2

138.0

40.4

220.4

70.1

12.9

26.0

1.9

25.2

57.0

22.4

24.7

7.1

24.9

46.3

22.6

83.3

90.0

28.4

73.1

41.1

24.4

46.6

19.6

76.2

88.0

36.7

68.2

40.8

PRC = People‟s Republic of China.

Sources: International Monetary Fund, International Financial Statistics; Bank for International Settlements; Asian Development Bank, Asian Bonds

Online; and Ghosh, Swati R. 2006. East Asian Finance: The Road to Robust Markets. Washington, DC: World Bank.

6

Different Stages of Development

Among Southeast Asian countries, big differences exist in terms of market cap, velocity & risk premiums.

World Federation of Exchanges (as of Nov. 2007)

•IMF 2006/ World Federation of Exchanges

Source: NYU Stern School, Goldman Sachs, Bursa Malaysia

Market Cap (USD billion)

Velocity (%)

Market Depth* Mkt Cap/GDP

Equity Risks Premiums

Malaysia 308 58 156 7.0

Singapore 531 78 291 5.5

Philippines 96 33 58 10.2

Indonesia 204 66 38 10.2

Thailand 193 69 68 6.5

7

Market Capitalization

While Singapore and Malaysia have relatively deep capital markets, Thailand, Indonesia, and the Philippines lag behind.

* Source: McKinsey, IMF, World Federation of Exchanges

* Source:ADB, World Bank Financial Structure Dataset

Mkt Cap/GDP (%)

58

291

156

68

38

903

167

94

34

106

160

57

146

- 200 400 600 800 1,000

Philippines

Singapore

Malay s ia

Thailand

Indones ia

Hong Kong

Taiwan

Korea

China

Japan

UK

Germany

US

2006

* Singapore includes substantial foreign market cap of ‘23%,

while Hong Kong has about 45%

8

Listed Companies & New Listing

Nu mbe r o f Li s te d Compan ie s

0

500

1,000

1,500

2,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Malaysia Indonesia Korea Philippine

China (Shanghai) Singapore Thailand

* Source: McKinsey, World Federation of Exchanges

The larger global exchanges are pulling away in listing volumes, with more than ten times the volume of Southeast Asia.

* Source: World Federation of Exchanges

9

Value of Share Trading

Value of share trading in each country of the region is less than US$500 billions.

Value of Share Trading (USD billions)

0

5 0 0

1, 0 0 0

1, 5 0 0

2 , 0 0 0

2 , 5 0 0

3 , 0 0 0

3 , 5 0 0

4 , 0 0 0

4 , 5 0 0

19 9 8 19 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7

M a l a y si a I ndone si a Kor e a P hi l i ppi ne Chi na ( S ha ngha i ) S i nga por e Tha i l a nd

* Source: World Federation of Exchanges

10

Turnover Ratio

No regional exchange has turnover ratio of over 100%, and only Thailand has a ratio of over 50%.

• This places Southeast Asia far behind the developed markets and North Asian exchanges.

* Source: ADB, World Bank Financial Structure Dataset

11

Transaction Costs

As a result of small markets with low velocity, trading costs in Southeast Asian markets are significantly higher than in many other regions.

Market impact costs, while higher than in larger markets, have been heading in the right direction recently.

* Source: McKinsey, Elkins McSherry Survey * Source: McKinsey, Elkins McSherry Survey

* Market impact cost is the difference between the transaction price and what the market price would have been in the absence

of the transaction.

12

Composition of Equity Markets in ASEAN

2005/06 (in %)

Source: ADB. Figures in parentheses refer to year 2001.

Retail Institutional OtherTotal

ResidentNon-

Resident

Singapore n/a n/a n/a 56 44 (36)

Malaysia 19 - 64 83 17 (17)

Philippines n/a n/a n/a 69 31

Indonesia 4 5 17 26 74 (56)

Thailand 62 10 n/a 72 28 (30)

China 6 9 36 51 49

Japan 20 27 29 76 24

Korea 18 11 31 60 40

Composition of equity markets also shows different landscape among Southeast Asian countries.• Non-Resident composition: Indonesia 74% vs. Malaysia 17%.

13

Performance of Stock Market Indices

Indonesia has been outstanding and the other Southeast Asian countries have also showed good performance.

* Source: World Federation of Exchanges (1998 = 100)

Broad Market Indices

0

10 0

2 0 0

3 0 0

4 0 0

5 0 0

6 0 0

7 0 0

8 0 0

19 9 8 19 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7

M a l a y si a ( KL Composi t e ) I ndone si a ( J S X Composi t e ) Kor e a ( KOS P I )

P hi l i ppi ne ( P S E Composi t e ) Chi na ( S ha ngha i , S S E Composi t e ) S i nga por e ( a l l S i ng Equi t i e s)

Tha i l a nd ( S ET) J a pa n( Tok y o, TOP I X)

14

Exchanges have merged and consolidated their operations.

• To improve efficiency, in addition, most exchanges vertically integrated clearing, settlement and depository operations (Malaysia, Singapore, Philippines and Thailand).

Country Exchanges

Singapore• One exchange (SGX), Merger of Stock Exchanges of Singapore & Singapore

Monetary Exchange (derivatives). Central depository is also a division.

Malaysia• Three Exchanges - Securities Exchange (Bursa Malaysia), Derivatives

Exchange and the Offshore Exchange (Labuan Int‘l Financial Exchange)

Thailand

• SET is the main exchange. The SET also operates wholly owned subsidiaries to trade corporate & government bonds under the name of Bonds Exchange (BEX) & Thailand Futures Exchange (TFEX) that trades SET 50 futures contracts.

Philippines• The PSE, Inc. is the only market for equity securities in the Philippines.

• Bonds are also traded at the PSE, and at the recently established Philippine Dealing and Exchange Corporation (PDex)

Indonesia • One exchange (consolidated in Dec. 2007)

Market Infrastructure: Exchanges

15

Status of Demutualization

• Exchanges in the region continue to

face increased competition from

other exchanges and trading

platforms.

• To raise needed capital to enable

them to modernize their operations

and operate more efficiently, most

regional exchanges have converted

from a not-for profit membership

owned entity into a for profit

corporation (demutualized) or are in

the process of demutualizing.

Country Status of Demutualization

Singapore• Demutualized (Dec, 1999)

• Listed (Nov, 2000)

Malaysia• Demutualized (April, 2004)

• Listed (March, 2005)

Thailand • Not Demutualized

Philippines• Demutualized (Aug, 2001)

• Listed (2003)

Indonesia

• Capital Market Master plan envisages demutualization after the merger of Jakarta and Surabaya stock exchanges in December 2007.

Exchange has been demutualized and listed in Singapore, Malaysia, and Philippines.

16

CountryRules &

RegulationsEnforcement Political/reg

environmentAdoption of iGAAP

Institutional Mechanisms

and CG culture

Country score –

highest to lowest

Hong Kong 60 56 73 83 61 67

Singapore 70 50 65 88 53 65

Korea 45 39 48 68 43 49

Malaysia 44 35 56 78 33 49

Thailand 58 36 31 70 39 47

PRC 43 33 52 73 25 45

Philippines 39 19 38 75 36 41

Indonesia 39 22 35 65 25 37

Legal & Regulatory Framework

* Source: CLSA “CG Watch 2007

Lack of adequate disclosure/transparency and poor corporate governance

in the Philippines & Indonesia undermines investor confidence.(%)

17

Compliance with IOSCO Principles

Country Compliance

Singapore• FSAP Assessment (2002-2003), most principles are fully and broadly implemented• Further Strengthening valuation methods & disclosure practices of CIs was recommended

Malaysia• Self Assessment (2006), most principles fully and broadly implemented • Further alignment of Malaysian Accounting Standards with International standards was mentioned

Thailand

• Assisted Self-Assessment (2004) in preparation for FSAP. Most principles fully & broadly implemented

• Strengthening was recommended in the legal provisions & procedural arrangements for the following areas: information sharing, investigation powers, appointment of administrators to take control over market intermediaries when warranted, and access to collateral & clearing funds of clearing house in case of member default

Philippines

• FSAP assessment (2002), and its assisted self-assessment update • Majority of the principles are fully or broadly implemented, with several principles only partially

implemented • Strengthening of laws, regulations, and practices in the following areas was recommended:

regulation of investment advisors, full implementations of exchange governance arrangements, segregation of client assets, standards for NAV calculations & CIS disclosures, oversight of SROs, and regulators access to market surveillance system, etc

Indonesia

• Assisted self assessment (2005) • Several principals are only partially implemented strengthening recommended in: transparency of

regulators approach, independence of regulator, information sharing/cooperation arrangements. Procedures to deal with failures of intermediaries, and supervision & governance of mutual funds

18

Southeast Asian securities markets have established securities market regulators, although a few markets have integrated all financial regulators to reflect the integrated nature of their markets (Singapore, Korea).

• In Hong Kong & Singapore, securities regulators are independent, provided with adequate funding, are able to attract competent staff and are provided with sufficient powers to effectively regulate the market.

Where stock exchanges have self listed, regulators have assumed primary oversight over the listing and trading of exchange shares.

• In some jurisdictions, self listed exchanges are no longer primary market regulators. For example, The Hong Kong Stock Exchange is no longer an SRO – the Government regulator has primary oversight of the market.

Transformation of Regulators

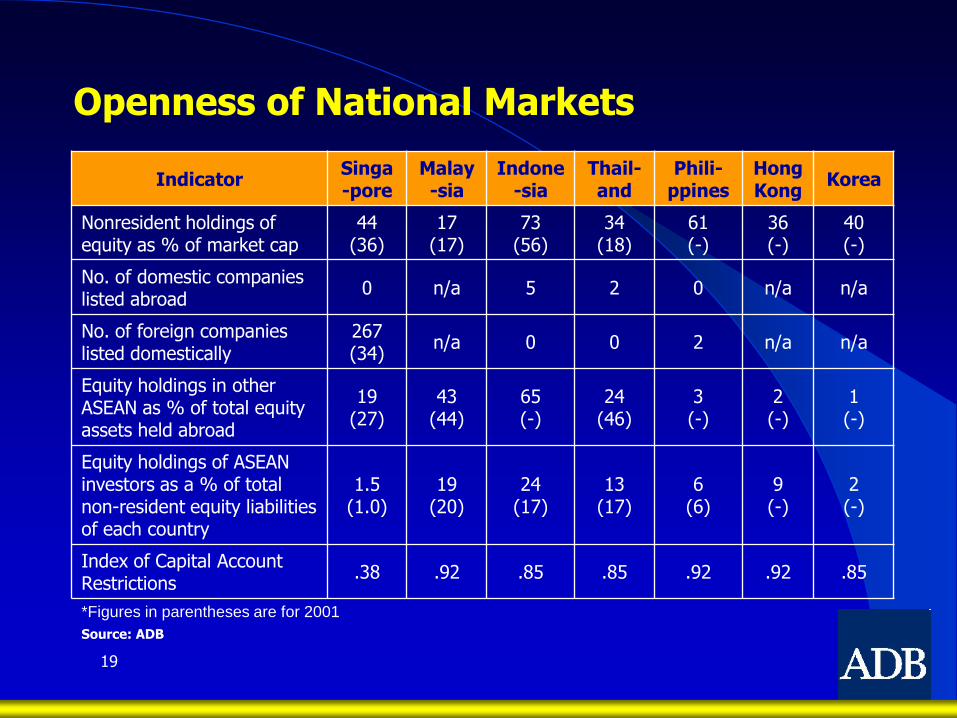

19

Source: ADB

IndicatorSinga -pore

Malay-sia

Indone-sia

Thail-and

Phili-ppines

Hong Kong

Korea

Nonresident holdings of equity as % of market cap

44(36)

17(17)

73(56)

34(18)

61(-)

36(-)

40(-)

No. of domestic companies listed abroad

0 n/a 5 2 0 n/a n/a

No. of foreign companies listed domestically

267(34)

n/a 0 0 2 n/a n/a

Equity holdings in other ASEAN as % of total equity assets held abroad

19(27)

43(44)

65(-)

24(46)

3(-)

2(-)

1(-)

Equity holdings of ASEAN investors as a % of total non-resident equity liabilities of each country

1.5(1.0)

19(20)

24(17)

13(17)

6(6)

9(-)

2(-)

Index of Capital Account Restrictions

.38 .92 .85 .85 .92 .92 .85

Openness of National Markets

*Figures in parentheses are for 2001

20

In Sum: ASEAN Equity Markets

• While ASEAN capital markets have made significant

progress in recent years, much more remains to be done.

• Many countries still have fairly shallow capital markets,

reducing their flexibility with capital allocation & resilience.

• These countries exchanges tend to be sub-scale, with low

turnover, liquidity & high transaction costs.

• In addition, levels of development and openness are

different Among them.

21

II. Initiatives for ASEAN Financial Integration

22

ASEAN Financial Integration Initiative (1)

The multitude of ASEAN level initiatives underway to foster ASEAN Regional Financial Integration are as follows:

• ASEAN leaders at their Summit in Cebu in 2006 decided to accelerate

regional integration by bringing forward to 2015 (from 2020), the target

date for the realization of the ASEAN Community, consisting of (as

envisioned in Bali Concord 2003) the ASEAN Economic Community;

ASEAN Security Community; and ASEAN Socio-cultural Community.

• Under the ASEAN Economic Community (AEC), the target for regional

economic integration has been defined mainly as free flow of goods,

services, investment, skilled labor, and freer flow of capital — commonly

referred to as ―a single market and production base‖.

23

ASEAN Financial Integration Initiative (2)

Work toward these targets has been going on since 2003 through the ASEAN Free Trade Agreement (AFTA); ASEAN Framework Agreement on Services (AFAS); and ASEAN Investment Area (AIA).

In addition in 2003, a Roadmap for Financial and Monetary Integration of ASEAN (RIA-Fin) was adopted by the ASEAN Finance Ministers and the ASEAN leaders to promote free flow of financial services. Some of the main action areas that were triggered are:

• Financial Services Liberalization through successive rounds of negotiations based on a transparent positive list approach. One round of negotiations was concluded in 2004, and the second round is underway;

• Capital Markets Development Program (e.g. Asian Bond Market Initiative);

• Capital Account Liberalization; and

• Currency Cooperation

24

III. ADB’s Technical Assistance (TA)

Progress to Date & Next Steps

25

TA: Objective & Methodology

Objective: The ADB TA on Enhancing Cooperation Among Southeast Asian Equity Markets was undertaken in 2007 to develop an actionable strategy for Southeast Asian equity markets -- ASEAN equity markets in particular —to work together towards greater cross border cooperation.

Methodology: ADB in collaboration with key stakeholders in the ASEAN region has held a series of workshops in 2007 under the TA aimed at supporting reforms at the country level to enhance cross border collaboration among equity markets in the region.

• The TA prepared country stocktaking studies and reviewed the readiness of each market for enhanced cooperation and options and stepping stones that can serve as a catalyst for moving forward.

• As part of a collaborative and consultative process, three workshops were held to identify issues and build consensus on how to address these among all the major stakeholders which have an interest in or would be affected by integration of equity markets in the Southeast Asian region.

26

TA: Summary of Workshops

Workshop Host Outcomes

1st

Workshop

29~30

March 2007

(Kuala

Lumpur)

Securities

Commission

Malaysia

• Brought together the capital market regulators, stock exchange

officials, fund managers, national and international capital market

experts as well as the ASEAN Secretariat to review recent and

evolving developments in national, regional and international

capital markets

• Identified the barriers to regional cooperation among equity

markets in the ASEAN region.

2nd

Workshop

26~27 July

2007

(Bangkok)

Thai Securities

& Exchange

Commission &

Stock

Exchange of

Thailand

• Focused on the constraints to regional integration of equity

markets, in particular exchange controls & capital account

restrictions and considered some global models for exchange

market alliances.

• The Workshop was notable for bringing together senior officials

from central banks, ministries of finance, regulators & market

participants.

3rd

Workshop

29 October

2007

(Manila)

Philippine DOF,

Bangko Sentral

ng Pilipinas,

Philippines

SEC & PSE

• Served as a high-level forum for ADB to present to the Ministries

of Finance, central banks, securities commissions, stock

exchanges and the ASEAN Secretariat an overall strategic

review of the project findings and its recommendations for equity

market integration in ASEAN.

• A strategic Framework paper was endorsed by participants.

27

TA: Strategic Framework for Integration

1. Refine domestic capital market development plans from a regional integration perspective.

2. Establish a coordinating mechanism for ASEAN financial and monetary integration process.

3. Sequence the liberalization of capital account and portfolio restrictions.

4. Implement a mutual recognition framework while continuing to strengthen and harmonize legal and regulatory framework in line with global standards.

5. Strengthen and coordinate exchange governance arrangements, the SRO functions, the listing rules and corporate governance framework.

6. Agree on and work toward an exchange alliance framework.

7. Promote new products, including ASEAN ―star‖ companies and new intermediaries to foster regional integration.

The Strategic Framework consists of seven recommendations designed to promote enabling conditions, overcome constraints, and build a mutual recognition and exchange alliance framework.

28

Key Aspects of The Strategic

Framework

29

Need for a Comprehensive & Coordinated Strategy or Strategic Framework for

Regional Cooperation

• To build consensus on the modalities, benefits and costs of regional integration of securities markets generally, and equity markets in particular

• To overcome constraints to regional integration, including capital account restrictions, and the absence of a level playing

• To build a mutual recognition regime that can support exchange market alliances in the region and foster common standards

30

National Strategies for Capital Market Development – Linked to Regional Cooperation

• Complete demutualization and improvements in infrastructure.

• Strengthen investor protection and enhance regulatory surveillance of market practices.

• Adopt common international standards such as IOSCO.

• Promote cross border regulatory cooperation and judicious use of mutual recognition in finance and business.

• Further liberalization of capital controls and exchange restrictions.

• Further strengthening of prudential safeguards and risk management capabilities to help manage volatility and compete effectively

31

Rationalizing the Process –A Regional Cooperation & Integration Council

• Act as a sounding board and feedback mechanism to identify, analyze, and propose priority actions on key issues in implementing regional integration of financial markets in ASEAN.

• Help advise the ASEAN Finance Ministers and ASEAN Capital Market Forum to set priorities for the various ASEAN Working groups and Taskforces, propose additional taskforces and working groups as needed.

• Help to review the findings of these bodies, highlight the policy implications of the findings to Ministers of Finance and central banks.

• Help monitor implementation of regional integration initiatives and the actual progress in achieving integration in various markets.

• Help harness the support of APRC, IOSCO, and other regional and global bodies to facilitate regional financial integration.

32

The Exchange Alliance Framework

33

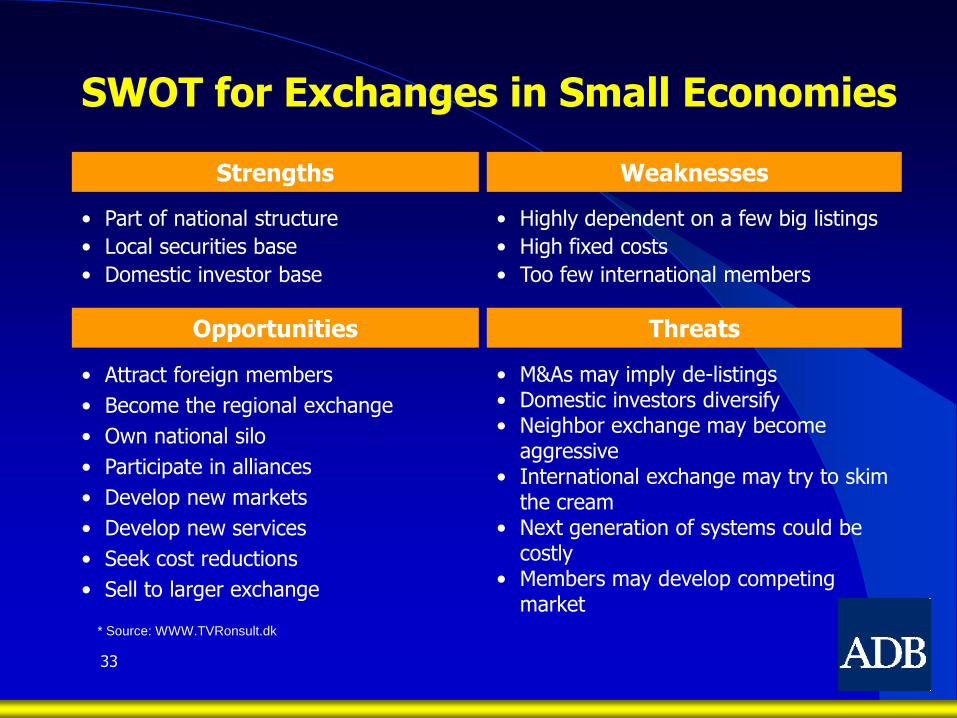

SWOT for Exchanges in Small Economies

• Part of national structure

• Local securities base

• Domestic investor base

Strengths Weaknesses

• Highly dependent on a few big listings

• High fixed costs

• Too few international members

• Attract foreign members

• Become the regional exchange

• Own national silo

• Participate in alliances

• Develop new markets

• Develop new services

• Seek cost reductions

• Sell to larger exchange

Opportunities Threats

• M&As may imply de-listings• Domestic investors diversify• Neighbor exchange may become

aggressive• International exchange may try to skim

the cream• Next generation of systems could be

costly• Members may develop competing

market* Source: WWW.TVRonsult.dk

34

Equity Markets – Lessons from Europe

• Radical transformation in equity market trading in Europe as a result of competition and technology developments

• Automated trading and convergence to common trading model with central limit order book trading for most liquid stocks

• Demutualization and emergence of for-profit exchanges: increased ability to raise capital for investments in automation, freed opportunities for consolidations and acquisitions, strengthened exchange networks, created economies of scale by sharing costs

• Exchange strategy has shifted to acquire critical mass before their competitors,

• Successful model – exchanges have independent identity, are members of ―regulated markets‖ that have mutual recognition and harmonized aspects, ―single passport‖ or single point of access for investors and intermediaries, achieve consolidation through holding company and/or shared trading structure.

35

Need for an ASEAN Exchange Alliance

Three plausible scenarios for Southeast Asian capital markets: (1) Dwindling relevance, (2) ―Cherry-picked‖ and absorbed in global market?, and (3) A new force in global markets.

* Source: McKinsey

36

Potential Benefits of

an ASEAN Exchange Alliance

Global presence

Shared infrastructure that reduces costs

Momentum for harmonization of governance and regulatory structures and market practices

Star companies are enabled to raise finance regionally

37

Models of Exchange Alliances

Based on general agreement on the recommendations contained in the Strategic Framework, developing a mutual recognition framework was considered the key to successful regional integration.

• Options for mutual recognition are as follows:

Ownership

Management

Membership

• All exchanges independent

• Separate, but market structureand data aligned

•All exchanges independent

Separate, but Mgm’t team for alliance with decision authority

• Membership managedindependently butstandards converge

Asian Alliance ASEAX

• Membershipmanaged independently

•All exchanges ownedby holding companies

• Single team (withrepresentation from all the exchanges)

• Single membershipacross all exchanges

AsiaNext

Infrastructure

Regulation

• Independentinfrastructure

• Independentinfrastructure butsome convergence

• Local regulation• Local regulation

• Common tradingplatform across all exchanges

• Local regulation

* Source: McKinsey

38

Proposed Exchange Alliance – ‘pipe’

Among the mutual recognition models, the easiest formulation is to construct bilateral linkages (‗pipe‘) or a purely technical IT link between exchanges to facilitate cross border trading between brokers in the home & host exchanges.

• The attractiveness of the bilateral exchange to exchange links is that they do not bypass the brokers, nor do they disrupt the current licensing, trading and clearing mechanisms in place.

• One of the main issues is how to gain support from the market players and the need for a technical study to clarify the benefits and costs of such an alliance, including related tax issues and the need to address competition risks to small brokers.

The ‗pipe‘ idea provides a framework for discussion and could be the first step toward broader collaboration as long as it does not require too extensive investments in the short term.

39

The Elements of the ‘pipe’

For a start, each exchange would allow a certain number of shares (which could be say 20 or 50 highly liquid or index stocks) to be available on an ―ASEAN Board‖.

• The ASEAN Board would comprise, say, up to 200 top ASEAN companies. The Board would be electronic, and be equivalent to the second or third board. A network can easily be established linking all the member exchanges. The Board could be made available on the internet or Reuters, preferably real-time.

Investors in country (A) would be able to route orders to buy and sell through their home brokers, who can then trade on the ASEAN Board, via placing orders to the ―host exchange‖, via clearing and settlement arrangements with a ―host broker‖.

Clearing and settlement arrangements will remain as normal, except thateach home and host broker must negotiate bilateral credit-risk management facilities to help settlement. The exchanges and clearing houses could help facilitate this electronically.

40

Options to Implement the ‘pipe’ Idea

Current state(interbroker)

Remote Trading

Membership

• No direct linkages among exchanges, clearinghouses (CLH), or CSDs• Brokers from bilateral linkages with one another direcly for trading, clearing and settlement

• No direct linkages among exchanges, CLHs, or CSDs• Foreign brokers can be members of exchange and trade directly• Brokers still need local partners to access the CLH and CSD

Interexchangetrading links

• Exchanges form trading links, allowing brokers to trade cross-borderthrough their local exchanges

• Brokers still need local partners to access the clearinghouse and CSD

CLH/CSD linkwithout

Trading link

• No direct trading linkages among exchanges• CLHs and/or CSDs have links allowing local brokers to clear and/or settle cross-border through the local CLH (eg local CLH is a member of the foreign CLH)

Trading andCLH/CSD link

• Exchanges form trading links, allowing brokers to trade cross-border• Through their local exchanges• CLHs and/or CSDs have links allowing local brokers to clear and/orsettle cross-border through the local CLH (eg local CLH is a member of the foreign CLH)

41

Further ProgressMeeting of CEOs of ASEAN Stock Exchanges

The ADB team including Andrew Sheng and Emmanuel Pitsilis from McKinsey made a presentation on the exchange alliance framework at the CEO‘s annual meeting in Bangkok on 25 November 2007.

The CEOs concluded that they wished to move forward towards implementing the concept of a virtual ASEAN Board – on a Reuters or Bloomberg platform.

• They formed a technical working group to develop a road map.

42

The ASEAN Board

Benefits

• Strengthen ASEAN capital markets‟

presence and enhance the visibility

of ASEAN as an asset class

• Attract more international funds into

ASEAN and encourage more intra-

ASEAN trading

• Allow local companies to raise

funds through regional capital

Description of ASEAN Board

• Comprise of a number of shares from

each exchange (i.e. 20 or 50 highly

liquid stocks)

• Would be electronic and equivalent to

the second or third board of each

exchange

• Show information on local currency

• Link among exchanges through a

network, which can easily be

established

• Could be made available on the

internet and data vendor (e.g.,

Reuters), preferably real-time

43

Operationalizing the Proposal

• Stands for “common customer gateway”

** Together with one trading rulebook

Trading

Clearing,settlement &

depository

Interbroker Interexchange

trading links

CCG with

assigned local

broker

(NYSE Euronext)

Remote trading

membership with

1 platform

(OMX‘s 1st step**)

CLH/CSD link

w/o trading link

Trading and

CLH/CSD link

(Euronext, OMX)

CCG with

CLH/CSD link

Localbasis

CLH/CSDlink

Source: SET

Broker-to-B Exch-to-exch CCG*Remote acc w/one platform

642

7541

44

Selection Criteria

1. Ease of accessibility

2. Ability to mitigate risks, e.g., credit risk,

Counterparty risk

Drivers Selection criteria

Objective can be

achieved

Conditions

are met

It is feasible

3. Maintain liquidity in host markets

4. Support from local brokers in both home and

Host markets

5. Ability to monitor trading volume

6. High technical practicality and regulatory support

7. Reasonable investment costs for exchanges

45

6. (page 11)

x x √ √ √ √ √

x √ √ √ √ √ √

√ √ √ √ √ √ √

√ √ x x √ x x

√ √ √ √ √ √ √

√ √ x x √ √ x

√ √ x x √ √ x

Selection criteria

1. Ease of accessibility

3. Maintain liquidity inhost markets

2. Ability to mitigate risks

4. Support from localbrokers

5. Ability to monitortrading volume

6. High technical practicality andregulatory support

7. Reasonable investmtcosts for exchanges

Inter-broker

Interex-changetradinglinks

TradingandCLH/

CSD link

CCG w/assigned

local broker

CCG w/CLH

CSD link

Remotemember-ship w/ 1platform

CLH/CLS linkw/o trad-ing link

Options

1 2 3 4 5 6 7

46

Summary

• Securities markets depend on (i) transparency and disclosure and (ii) enforcement; complex interaction between reputational intermediaries, enforcement agencies, SROs and enforcement of laws critical to market development

• Significant improvements in Southeast Asia since 1997; markets and intermediaries stronger, regulation enhanced, greater financial system stability and resilience

• But cross country differences in market development are pronounced, as are differences in linkages between regulatory stance and market development

• Equity market trading in Europe undergoing radical transformation: ASEAN exchanges need to act now to remain relevant: they need support from regulators and policymakers.

47

Questions and Comments

Thank you!

48

The Different Layers of Securities

Market Regulation

49

Country Regulation

Indonesia

• The Issuer or the Public Company is fully responsible for the accuracy, adequacy and the truth of opinions and all information

presented in the Registration Statement submitted to Bapepam. If an item contained in a Bapepam rule or form regarding

disclosure requirements does not apply to a specific Issuer, Public Company, or Public Offering, it need not be disclosed in

the Registration Statement.

• In addition to the information and documents which must be included in the Registration Statement, the Person who submits

the registration Statement must also include other material information that is needed to ensure that investors have adequate

information regarding the financial condition and business activities of the Issuer or the Public Company and that the

disclosure is not misleading.

Malaysia

• Issuers are required to make full, timely and accurate disclosure of information to the public under the securities laws, and

guidelines issued by the SC.

• In addition, the listing requirements impose continuous disclosure obligations on listed issuers and seeks to ensure that equal

access to such information is practiced.

Philippines• Disclosure requirements are another area which was purposely strengthened under the SRC.

• The disclosure requirements in the SRC and the IRR are modeled after those in the United States.

Singapore

• Initial public offerings and continuing disclosure requirements for issuers are in place, providing timely, adequate, and

accurate disclosure of material information to investors. Prospectus disclosure requirements are state of the art.

• Issuers and their directors and underwriters are subject to criminal and civil liability if a prospectus contains false or

misleading information or if material information is not disclosed. Company law and listing rules accord fair and equitable

treatment to all shareholders. The Take-Over Code provides additional protections to all listed Singapore companies and to

unlisted public companies with 50 or more shareholders and net tangible assets of S$5 million or more. Singapore generally

follows international auditing standards.

• Quarterly financial reporting is also required for listed companies above S$75 million.

Thailand

• The SEC Act prohibits companies from offering newly issued shares and other securities for sale without prior approval from

the SEC, except for the rights offering to existing shareholders. The SEC focuses on the accuracy and sufficiency of

information disclosure in order to allow the public to make their investment decisions.

• All forms of public offering of securities must receive approvals form the SEC as well as conform to SEC prescribed disclosure

and accounting standards. The SEC also licenses and regulates all investment intermediaries as well as the SET.

1. Issuers

50

Country Regulation

Indonesia

• Among Singapore, Malaysia, Thailand and Indonesia, the later has the least number of equities and derivatives as investment

products.

• Only a Company licensed by BAPEPAM may carry on business as a Securities Company.

• Licensing requirements and procedures include such things as: requirements with respect to management, capital and

expertise; and procedures for submitting license applications

Malaysia

• All market intermediaries must be licensed by the SC in order to carry out the permitted activities under the SIA and FIA.

Minimum entry standards, which include initial capital requirements, are applied equally and consistently to applicants applying

for the same category of licenses.

• All license applicants must meet „fit and proper‟ criteria. Ethical, educational, industry knowledge, skills and experience are

assessed in approving principal officers which include directors, company secretary and key management personnel.

• The Syariah Advisory Council (SAC) advises the SC on issues relating to market compliance with Syariah principles in the

Islamic capital market.

Philippines

• The legal infrastructure for regulating market intermediaries has been enhanced in the SRC which, among other things, raises

capital requirements (initial and ongoing), provides a disciplinary bar to registration, provides for indefinite registration, and

clarifies that all regulated intermediaries must register under the new law.

• Investment Houses (Presidential Decree 129), Broker Dealers (SRC), Financing Companies (Financing Company Act of 1998)

are primary NBFIs authorized and regulated by the SEC. Among them, the Investment Houses and Broker Dealers are the

primary securities market intermediaries while the Financing Companies are essentially credit institutions without deposit taking.

Singapore

• The MAS has adopted a single modular licensing framework for securities and futures market intermediaries. The SFA

regulates intermediaries conducting regulated activities. The FAA regulates intermediaries providing financial advisory services.

The MAS has adopted a risk-based approach to supervising its licensed intermediaries. Capital requirements for licensees will

be largely based on the analysis underlying the Basel Core Principles. The new capital rule supersedes an adjusted net capital

rule and is being phased in conservatively to test the potential impact on capital.

• Holders of Capital Markets Licenses must observe customer protection procedures.

Thailand

• Domestic institutional investor base is still under developed. Except for Government Pension Fund (GPF) there is no

compulsory retirement pension scheme.

• This narrow domestic institutional investors base coupled with investment restrictions for GPF and PVD meant that their

participation in the equities market have lagged behind those of retail investors and foreign institutional investors who have

played a much more active role in the equities market.

2. Reputational Intermediaries

51

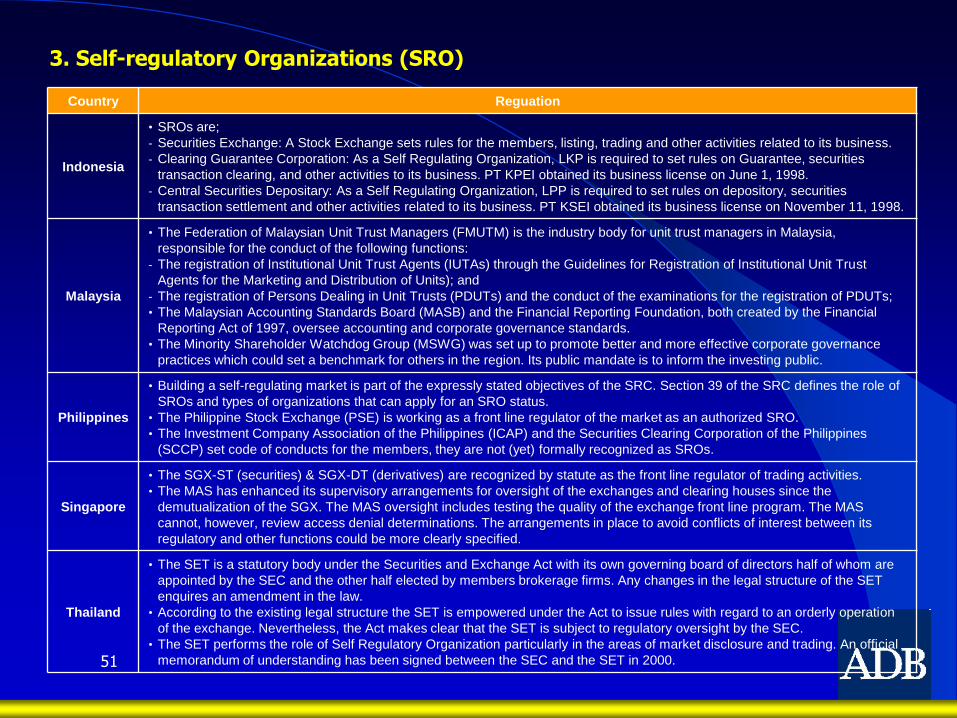

Country Reguation

Indonesia

• SROs are;

- Securities Exchange: A Stock Exchange sets rules for the members, listing, trading and other activities related to its business.

- Clearing Guarantee Corporation: As a Self Regulating Organization, LKP is required to set rules on Guarantee, securities

transaction clearing, and other activities to its business. PT KPEI obtained its business license on June 1, 1998.

- Central Securities Depositary: As a Self Regulating Organization, LPP is required to set rules on depository, securities

transaction settlement and other activities related to its business. PT KSEI obtained its business license on November 11, 1998.

Malaysia

• The Federation of Malaysian Unit Trust Managers (FMUTM) is the industry body for unit trust managers in Malaysia,

responsible for the conduct of the following functions:

- The registration of Institutional Unit Trust Agents (IUTAs) through the Guidelines for Registration of Institutional Unit Trust

Agents for the Marketing and Distribution of Units); and

- The registration of Persons Dealing in Unit Trusts (PDUTs) and the conduct of the examinations for the registration of PDUTs;

• The Malaysian Accounting Standards Board (MASB) and the Financial Reporting Foundation, both created by the Financial

Reporting Act of 1997, oversee accounting and corporate governance standards.

• The Minority Shareholder Watchdog Group (MSWG) was set up to promote better and more effective corporate governance

practices which could set a benchmark for others in the region. Its public mandate is to inform the investing public.

Philippines

• Building a self-regulating market is part of the expressly stated objectives of the SRC. Section 39 of the SRC defines the role of

SROs and types of organizations that can apply for an SRO status.

• The Philippine Stock Exchange (PSE) is working as a front line regulator of the market as an authorized SRO.

• The Investment Company Association of the Philippines (ICAP) and the Securities Clearing Corporation of the Philippines

(SCCP) set code of conducts for the members, they are not (yet) formally recognized as SROs.

Singapore

• The SGX-ST (securities) & SGX-DT (derivatives) are recognized by statute as the front line regulator of trading activities.

• The MAS has enhanced its supervisory arrangements for oversight of the exchanges and clearing houses since the

demutualization of the SGX. The MAS oversight includes testing the quality of the exchange front line program. The MAS

cannot, however, review access denial determinations. The arrangements in place to avoid conflicts of interest between its

regulatory and other functions could be more clearly specified.

Thailand

• The SET is a statutory body under the Securities and Exchange Act with its own governing board of directors half of whom are

appointed by the SEC and the other half elected by members brokerage firms. Any changes in the legal structure of the SET

enquires an amendment in the law.

• According to the existing legal structure the SET is empowered under the Act to issue rules with regard to an orderly operation

of the exchange. Nevertheless, the Act makes clear that the SET is subject to regulatory oversight by the SEC.

• The SET performs the role of Self Regulatory Organization particularly in the areas of market disclosure and trading. An official

memorandum of understanding has been signed between the SEC and the SET in 2000.

3. Self-regulatory Organizations (SRO)

52

Country Regulation

Indonesia• Bapepam-LK is not an independent authority but an agency within the Ministry of Finance (MoF). It is the principal regulator

and is supported by a number of selfregulatory organizations (SROs).

Malaysia

• The Securities Commission (SC) is a statutory body with investigative and enforcement powers and it reports to the Minister

of Finance. The SC is the regulatory authority for the Malaysian capital market; it also supervises the activities of market

institutions, including the exchanges and clearing houses, and regulates persons licensed under the Securities Industry Act

(SIA) and Futures Industry Act (FIA).

• Bursa Malaysia is vested with regulatory powers under the law and has a statutory responsibility to ensure a fair and orderly

market and prudent risk management. These responsibilities relate to the regulation and surveillance of securities markets.

Philippines

• The Securities Regulation Code of 2000 empowered SEC to make it a more enforcement-oriented & independent regulator.

• The supervision of the Philippine financial market is divided among different regulatory agencies. Banking supervision is the

under the responsibility of the Bangko Sentral ng Pilipinas; supervision of the insurance industry is under the Insurance

Commission; and the supervision of the securities market is under the Securities and Exchange Commission. Moreover, the

mandate and jurisdiction of these agencies are defined under different legislations.

• The “Compliance and Surveillance Group”(CSG) of the PSE carries front line responsibility for market surveillance,

compliance inspections, and investigation by PSE or SEC depending upon the type and scope of violations. SEC exercises

some oversight of PSE in order to enhance the independence and capacity to perform surveillance and compliance activities

through the CSG, the CSG was transformed into Market Regulations Division, supervised by a semi-independent, Market

Integrity Board (MIB).

Singapore

• The MAS is legally and institutionally independent of the executive and legislative branches of the government and

accountable to the public. The MAS‟ responsibilities with respect to securities regulation are clearly stated in the applicable

legislation and rules in the SFA of 2001, the FAA, the Exchanges Demutualization and Merger Act, and related regulations.

• Exercise of regulatory powers in securities is subject to the SFA. The MAS clearly has the staff, powers, expertise, and

resources to conduct effective regulation. The consultation process with the industry and the public is in place and sound.

Thailand

• Regulatory framework is quite advanced though fragmented. The Bank of Thailand is the main regulator for commercial banks

and finance companies and is in the process of implementing the BASLE II capital requirement as well as consolidated

supervision of financial institutions. The Bank also has limited jurisdiction over specialized banks and non bank activities.

• The Securities and Exchange Commission is an independent statutory body responsible for regulating all aspects of fund

raising, financial investment dealings, market activities as well as promotion of good corporate governance.

4. Government institutions

53

Country Regulation

Indonesia• The legal basis for capital market activities in Indonesia is the Capital Market Law Number 8/1995 . The

• Law governs the operations of the Capital Markets Supervisory Agency, Badan Pengawas Pasar Modal

• dan Lembaga Keuangan (Bapepam-LK).

Malaysia

• The Capital Market is governed by the following Acts of Parliament:

• Securities Industry Act 1983/ Securities Industry (Central Depositories Act) 1991/ Securities Commission Act 1993

• Companies Act 1965/ Futures Industry Act 1993/ Labuan Offshore Securities Industry Act 1995

• All market intermediaries must be licensed by the SC in order to carry out the permitted activities under the Securities Industry

Act and Futures Industry Act. Minimum entry standards, which include capital adequacy requirement, must be met.

Philippines

• BSP draws its supervisory and regulatory powers from Article XII, Section 20 of the 1987 Constitution, the New Central Bank

Act of 1993, and the General Banking Law of 2000. The mandate of the Insurance Commission is mainly based from the

Insurance Code of 1974.

• The Securities and Exchange Commission derives its authority from the Securities Regulation Code of 2000, the Investment

House Law of 1973, the Investment Company Act of 1960, and the Financing Company Act of 1998.

Singapore

• The order of precedence of the various legislative and quasi-legislative instruments applicable to the Singapore capital market

and its participants are as follows in descending order:

- The statutory Act and related regulations

- The rules contained in the Rulebook

- Directives issued pursuant to the Rulebook

- Practice Notes

- Circulars

• In the event of a conflict between any provisions in the instruments provisions contained in the higher level instruments shall

prevail.

Thailand

• To initiate a new legal framework and mark a new era for the Thai capital market, on March 16, 1992, the Securities and

Exchange Act B.E. 2535 (1992) or “the SEC Act” was promulgated and came into force on May 16, 1992 so as to reinforce the

unity, consistency, and efficiency in supervision and development of the market. The enactment of the SEC Act empowered

the Securities and Exchange Commission, Thailand to be established as an independent state agency with responsibility for

supervision and development of the capital market under the direction and guidance of the Board of the SEC.

• On July 3, 2003, the Derivatives Act B.E. 2546 (2003) was promulgated and came into force on January 6, 2004 so as to

create a legal certainty for derivative contracts, provide a regulatory framework for derivatives markets and intermediaries, and

allow the SEC to oversee the financial integrity of the market and take action to prevent adverse systemic effect.

5. Laws

54

Layer Regulation

Issuers

• The Issuer or the Public Company is fully responsible for the accuracy, adequacy and the truth of opinions and all information

presented in the Registration Statement submitted to Bapepam. If an item contained in a Bapepam rule or form regarding

disclosure requirements does not apply to a specific Issuer, Public Company, or Public Offering, it need not be disclosed in

the Registration Statement.

• In addition to the information and documents which must be included in the Registration Statement, the Person who submits

the registration Statement must also include other material information that is needed to ensure that investors have adequate

information regarding the financial condition and business activities of the Issuer or the Public Company and that the

disclosure is not misleading.

Reputational

intermediaries

• Among Singapore, Malaysia, Thailand and Indonesia, the later has the least number of equities and derivatives as investment

products.

• Only a Company licensed by BAPEPAM may carry on business as a Securities Company.

• Licensing requirements and procedures include such things as: requirements with respect to management, capital and

expertise; and procedures for submitting license applications

Self-regulatory

organizations

• SROs are;

- Securities Exchange: A Stock Exchange sets rules for the members, listing, trading and other activities related to its business.

- Clearing Guarantee Corporation: As a Self Regulating Organization, LKP is required to set rules on Guarantee, securities

transaction clearing, and other activities to its business. PT KPEI obtained its business license on June 1, 1998.

- Central Securities Depositary: As a Self Regulating Organization, LPP is required to set rules on depository, securities

transaction settlement and other activities related to its business. PT KSEI obtained its business license on November 11,

1998.

Government

institutions

• Bapepam-LK is not an independent authority but an agency within the Ministry of Finance (MoF). It is the principal regulator

and is supported by a number of self-regulatory organizations (SROs)

Laws

• The legal basis for capital market activities in Indonesia is the Capital Market Law Number 8/1995 .

• The Law governs the operations of the Capital Markets Supervisory Agency, Badan Pengawas Pasar Modal dan Lembaga

Keuangan (Bapepam-LK).

1. Indonesia

55

Layer Regulation

Issuers

• Issuers are required to make full, timely and accurate disclosure of information to the public under the securities laws, and

guidelines issued by the Securities Commission (SC).

• In addition, the listing requirements impose continuous disclosure obligations on listed issuers and seeks to ensure that equal

access to such information is practiced.

Reputational

intermediaries

• All market intermediaries must be licensed by the SC in order to carry out the permitted activities under the SIA and FIA.

Minimum entry standards, which include initial capital requirements, are applied equally and consistently to applicants applying

for the same category of licenses.

• All license applicants must meet „fit and proper‟ criteria. Ethical, educational, industry knowledge, skills and experience are

assessed in approving principal officers which include directors, company secretary and key management personnel.

• The Syariah Advisory Council (SAC) advises the SC on issues relating to market compliance with Syariah principles in the

Islamic capital market.

Self-

regulatory

organizations

• The Federation of Malaysian Unit Trust Managers (FMUTM) is the industry body for unit trust managers in Malaysia,

responsible for the conduct of the following functions:

- The registration of Institutional Unit Trust Agents (IUTAs) through the Guidelines for Registration of Institutional Unit Trust

Agents for the Marketing and Distribution of Units); and

- The registration of Persons Dealing in Unit Trusts (PDUTs) and the conduct of the examinations for the registration of PDUTs;

• The Malaysian Accounting Standards Board (MASB) and the Financial Reporting Foundation, both created by the Financial

Reporting Act of 1997, oversee accounting and corporate governance standards.

• The Minority Shareholder Watchdog Group (MSWG) was set up to promote better and more effective corporate governance

practices which could set a benchmark for others in the region. Its public mandate is to inform the investing public.

Government

institutions

• The SC is a statutory body with investigative and enforcement powers and it reports to the Minister of Finance. The SC is the

regulatory authority for the Malaysian capital market; it also supervises the activities of market institutions, including the

exchanges and clearing houses, and regulates persons licensed under the Securities Industry Act (SIA) and Futures Industry

Act (FIA).

• Bursa Malaysia is vested with regulatory powers under the law and has a statutory responsibility to ensure a fair and orderly

market and prudent risk management. These responsibilities relate to the regulation and surveillance of securities markets.

Laws

• The Capital Market is governed by the following Acts of Parliament:

• Securities Industry Act 1983/ Securities Industry (Central Depositories Act) 1991/ Securities Commission Act 1993

• Companies Act 1965/ Futures Industry Act 1993/ Labuan Offshore Securities Industry Act 1995

• All market intermediaries must be licensed by the SC in order to carry out the permitted activities under the Securities Industry

Act and Futures Industry Act. Minimum entry standards, which include capital adequacy requirement, must be met.

2. Malaysia

56

Layer Regulation

Issuers• Disclosure requirements are another area which was purposely strengthened under the SRC.

• The disclosure requirements in the SRC and the IRR are modeled after those in the United States.

Reputational

intermediaries

• The legal infrastructure for regulating market intermediaries has been enhanced in the SRC which, among other things, raises

capital requirements (initial and ongoing), provides a disciplinary bar to registration, provides for indefinite registration, and

clarifies that all regulated intermediaries must register under the new law.

• Investment Houses (Presidential Decree 129), Broker Dealers (SRC), Financing Companies (Financing Company Act of 1998)

are primary NBFIs authorized and regulated by the SEC. Among them, the Investment Houses and Broker Dealers are the

primary securities market intermediaries while the Financing Companies are essentially credit institutions without deposit

taking.

Self-

regulatory

organizations

• Building a self-regulating market is part of the expressly stated objectives of the SRC. Section 39 of the SRC defines the role of

SROs and types of organizations that can apply for an SRO status.

• The Philippine Stock Exchange (PSE) is working as a front line regulator of the market as an authorized SRO.

• The Investment Company Association of the Philippines (ICAP) and the Securities Clearing Corporation of the Philippines

(SCCP) set code of conducts for the members, they are not (yet) formally recognized as SROs.

Government

institutions

• The Securities Regulation Code of 2000 empowered SEC to make it a more enforcement-oriented & independent regulator.

• The supervision of the Philippine financial market is divided among different regulatory agencies. Banking supervision is the

under the responsibility of the Bangko Sentral ng Pilipinas; supervision of the insurance industry is under the Insurance

Commission; and the supervision of the securities market is under the Securities and Exchange Commission. Moreover, the

mandate and jurisdiction of these agencies are defined under different legislations.

• The “Compliance and Surveillance Group”(CSG) of the PSE carries front line responsibility for market surveillance, compliance

inspections, and investigation by PSE or SEC depending upon the type and scope of violations. SEC exercises some oversight

of PSE in order to enhance the independence and capacity to perform surveillance and compliance activities through the CSG,

the CSG was transformed into Market Regulations Division, supervised by a semi-independent, Market Integrity Board (MIB).

Laws

• BSP draws its supervisory and regulatory powers from Article XII, Section 20 of the 1987 Constitution, the New Central Bank

Act of 1993, and the General Banking Law of 2000. The mandate of the Insurance Commission is mainly based from the

Insurance Code of 1974.

• The Securities and Exchange Commission derives its authority from the Securities Regulation Code of 2000, the Investment

House Law of 1973, the Investment Company Act of 1960, and the Financing Company Act of 1998.

3. Philippines

57

4. Singapore

Layer Regulation

Issuers

• Initial public offerings and continuing disclosure requirements for issuers are in place, providing timely, adequate, and accurate disclosure of

material information to investors. Prospectus disclosure requirements are state of the art.

• Issuers and their directors and underwriters are subject to criminal and civil liability if a prospectus contains false or misleading information

or if material information is not disclosed. Company law and listing rules accord fair and equitable treatment to all shareholders.

• The Take-Over Code provides additional protections to all listed Singapore companies and to unlisted public companies with 50 or more

shareholders and net tangible assets of S$5 million or more. Singapore generally follows international auditing standards.

• Quarterly financial reporting is also required for listed companies above S$75 million.

Reputational

intermediaries

• The MAS has adopted a single modular licensing framework for securities and futures market intermediaries.

• The SFA regulates intermediaries conducting regulated activities.

• The FAA regulates intermediaries providing financial advisory services.

• The MAS has adopted a risk-based approach to supervising its licensed intermediaries.

• Capital requirements for licensees will be largely based on the analysis underlying the Basel Core Principles. The new capital rule

supersedes an adjusted net capital rule and is being phased in conservatively to test the potential impact on capital.

• Holders of Capital Markets Licenses must observe customer protection procedures.

Self-regulatory

organizations

• The SGX-ST (securities) and SGX-DT (derivatives) are recognized by statute as the front line regulator of trading activities on their markets.

• MAS has enhanced its supervisory arrangements for oversight of the exchanges & clearing houses since the demutualization of the SGX.

• MAS oversight includes testing the quality of the exchange front line program. MAS cannot, however, review access denial determinations.

The arrangements in place to avoid conflicts of interest between its regulatory and other functions could be more clearly specified

Government

institutions

• The MAS is legally and institutionally independent of the executive and legislative branches of the government & accountable to the public.

• The MAS‟ responsibilities with respect to securities regulation are clearly stated in the applicable legislation and rules in the SFA of 2001,

the FAA, the Exchanges Demutualization and Merger Act, and related regulations.

• The MAS has both prudential and conduct of business responsibility for those intermediaries for which Capital Markets Services Licenses

are required. Because there are significant interrelationships between the government and statutory boards, greater disclosure of the MAS‟

operating procedures that guide implementation of policies would enhance accountability and transparency.

• Exercise of regulatory powers in securities is subject to the SFA.

• The MAS clearly has the staff, powers, expertise, and resources to conduct effective regulation. The consultation process with the industry

and the public is in place and sound.

Laws

• The order of precedence of the various legislative and quasi-legislative instruments applicable to the Singapore capital market and its

participants are as follows in descending order: 1. The statutory Act and related regulations; 2. The rules contained in the Rulebook; 3.

Directives issued pursuant to the Rulebook; 4. Practice Notes; and 5. Circulars

• In the event of a conflict between any provisions in the instruments provisions contained in the higher level instruments shall prevail.

58

Layer Regulation

Issuers

• The SEC Act prohibits companies from offering newly issued shares and other securities for sale without prior approval from

the SEC, except for the rights offering to existing shareholders. The SEC focuses on the accuracy and sufficiency of

information disclosure in order to allow the public to make their investment decisions.

• All forms of public offering of securities must receive approvals form the SEC as well as conform to SEC prescribed disclosure

and accounting standards. The SEC also licenses and regulates all investment intermediaries as well as the SET.

Reputational

intermediaries

• Domestic institutional investor base is still under developed. Except for Government Pension Fund (GPF) there is no

compulsory retirement pension scheme.

• This narrow domestic institutional investors base coupled with investment restrictions for GPF and PVD meant that their

participation in the equities market have lagged behind those of retail investors and foreign institutional investors who have

played a much more active role in the equities market.

Self-regulatory

organizations

• The SET is a statutory body under the Securities and Exchange Act with its own governing board of directors half of whom are

appointed by the SEC and the other half elected by members brokerage firms. Any changes in the legal structure of the SET

enquires an amendment in the law.

• According to the existing legal structure the SET is empowered under the Act to issue rules with regard to an orderly operation

of the exchange. Nevertheless, the Act makes clear that the SET is subject to regulatory oversight by the SEC.

• The SET performs the role of Self Regulatory Organization particularly in the areas of market disclosure and trading. An official

memorandum of understanding has been signed between the SEC and the SET in 2000.

Government

institutions

• Regulatory framework is quite advanced though fragmented. The Bank of Thailand is the main regulator for commercial banks

and finance companies and is in the process of implementing the BASLE II capital requirement as well as consolidated

supervision of financial institutions. The Bank also has limited jurisdiction over specialized banks and non bank activities.

• The Securities and Exchange Commission is an independent statutory body responsible for regulating all aspects of fund

raising, financial investment dealings, market activities as well as promotion of good corporate governance.

Laws

• To initiate a new legal framework and mark a new era for the Thai capital market, on March 16, 1992, the Securities and

Exchange Act B.E. 2535 (1992) or “the SEC Act” was promulgated and came into force on May 16, 1992 so as to reinforce the

unity, consistency, and efficiency in supervision and development of the market. The enactment of the SEC Act empowered

the Securities and Exchange Commission, Thailand to be established as an independent state agency with responsibility for

supervision and development of the capital market under the direction and guidance of the Board of the SEC.

• On July 3, 2003, the Derivatives Act B.E. 2546 (2003) was promulgated and came into force on January 6, 2004 so as to

create a legal certainty for derivative contracts, provide a regulatory framework for derivatives markets and intermediaries, and

allow the SEC to oversee the financial integrity of the market and take action to prevent adverse systemic effect.

5. Thailand

59

Markets in SE Asia – Lessons from Europe

• In Asia, progress towards international standards, IOSCO, etc. adoption of risk based supervision, demutualization of exchanges.

• Greater market depth, transactions volume and openness.• But each market is small, with limited openness to region, high

transactions cost because of sub-scale volume. The challenge is from Europe

• In Europe, demutualization is complete, for-profit exchanges have invested in automated trading and convergence to common trading model with central limit order book trading for most liquid stocks

• Lower transactions cost and ability to link trading venues• Greater competition between venues within and across borders• But also alliances and mergers which have brought significant

advantages in terms of greater access to capital raising and lower costs• Need to ensure competitive markets in trading, clearing, settlement and

deposit

60

The Way Forward

Phase 2: bilateral/multilateral linkage

• Agreed to pursue option 5 with determination of having option 6 as an end game

Phase 2: issues to be addressed

ASEAN level

• Business requirement for selecting solution provider - Tools (e.g., short selling, SBL)- Infrastructure (e.g., speed)

• Business model, including data dissemination• Revenue model, including investment costs and operating costs to conduct the

feasibility analysis• Marketing messages

Bilateral level

• Ways to deal with credit risk• Supporting rules and regulations at each exchange• Support from market participants and regulators

1 2 3 4 5 6 7

61

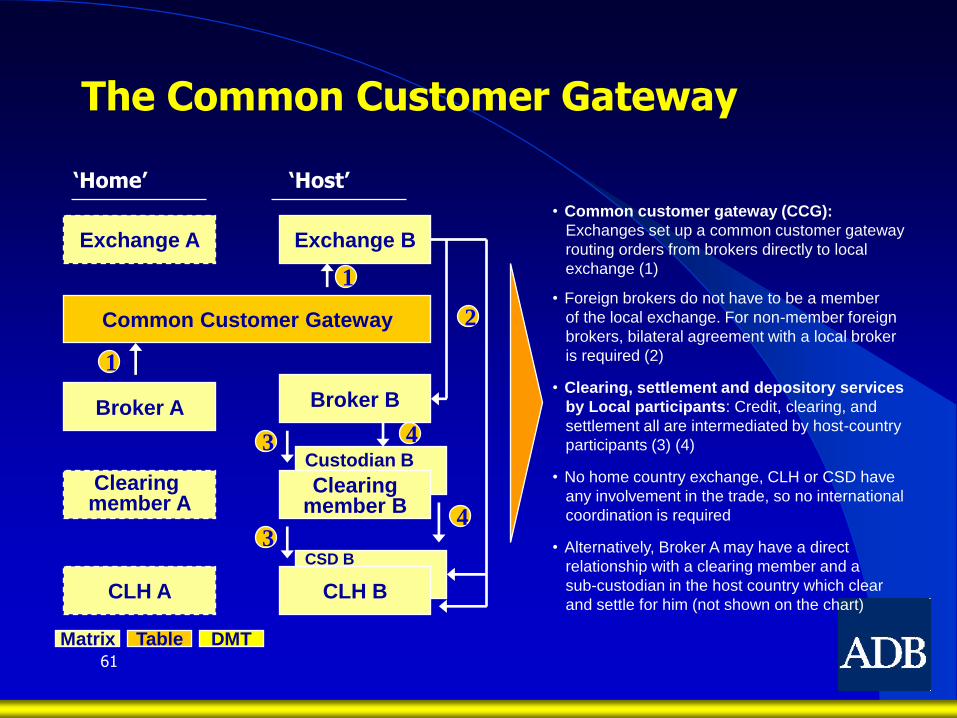

The Common Customer Gateway

• Foreign brokers do not have to be a member

of the local exchange. For non-member foreign

brokers, bilateral agreement with a local broker

is required (2)

• Clearing, settlement and depository services

by Local participants: Credit, clearing, and

settlement all are intermediated by host-country

participants (3) (4)

• No home country exchange, CLH or CSD have

any involvement in the trade, so no international

coordination is required

• Alternatively, Broker A may have a direct

relationship with a clearing member and a

sub-custodian in the host country which clear

and settle for him (not shown on the chart)

• Common customer gateway (CCG):

Exchanges set up a common customer gateway

routing orders from brokers directly to local

exchange (1)

Exchange A

Broker B

CSD B

Broker A

Clearing member A

CLH A

Exchange B

Custodian B

Common Customer Gateway

Clearingmember B

CLH B

‘Home’ ‘Host’

Matrix Table DMT

1

2

3 4

4

1

3