enhancing a sustainable future! -...

TRANSCRIPT

Corporate Presentation – June 2011

Enhancing a Sustainable Future!

Safe Harbour

Certain statements in this presentation concerning our future growth prospects are forward

looking statements, which involve a number of risks, and uncertainties that could cause

actual results to differ materially from those in such forward-looking statements. The risks

and uncertainties relating to these statements include, but are not limited to, risks and

uncertainties regarding fluctuations in earnings, our ability to manage growth, intense

competition in our industry of operations including those factors which may affect our cost

advantage, wage increases, our ability to attract and retain highly skilled professionals,

cost overruns on contracts, client concentration, our ability to manage our international

operations, our ability to successfully complete and integrate potential acquisitions,

liability for damages on our contracts, the success of the companies in which Deepak Nitrite

has made strategic investments, withdrawal of governmental fiscal incentives, political

instability, legal restrictions on raising capital or acquiring companies outside India, and

unauthorized use of our intellectual property and general economic conditions affecting

our industry. Deepak Nitrite Ltd. may, from time to time, make additional written and oral

forward-looking statements, including our reports to shareholders. The company does not

undertake to update any forward-looking statement that may be made from time to time

by or on behalf of the company.

CONTENTS

1 About DNL

4

3

2 Market Environment

Differentiators & Drivers

Financials

5 Growth Plans

Deepak Nitrite Limited - A Leading Chemical Company

Deepak Nitrite : Snapshot

Deepak Nitrite : About Us

• Established in 1970s by Mr. C. K. Mehta.

• Started out with manufacturing of Sodium Nitrite / Sodium Nitrate and

has evolved to create leadership position in several products

• Is a preferred supplier to some of the leading global chemical companies

and has cultivated business relationships over 5-10 years.

• Multiple products, multiple facilities and multiple customers have enabled

it to create a de-risked business model

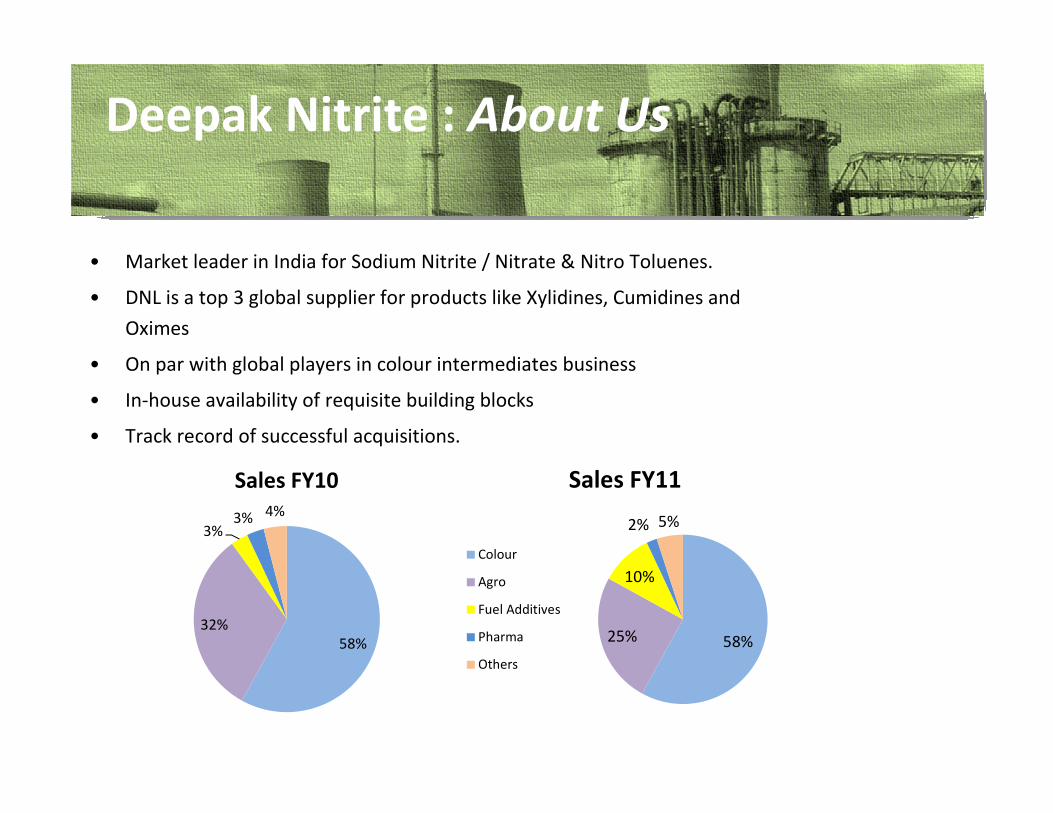

Deepak Nitrite : About Us

• Market leader in India for Sodium Nitrite / Nitrate & Nitro Toluenes.

• DNL is a top 3 global supplier for products like Xylidines, Cumidines and

Oximes

• On par with global players in colour intermediates business

• In-house availability of requisite building blocks

• Track record of successful acquisitions.

58%

32%

3%3% 4%

Sales FY10

58%25%

10%

2% 5%

Sales FY11

Colour

Agro

Fuel Additives

Pharma

Others

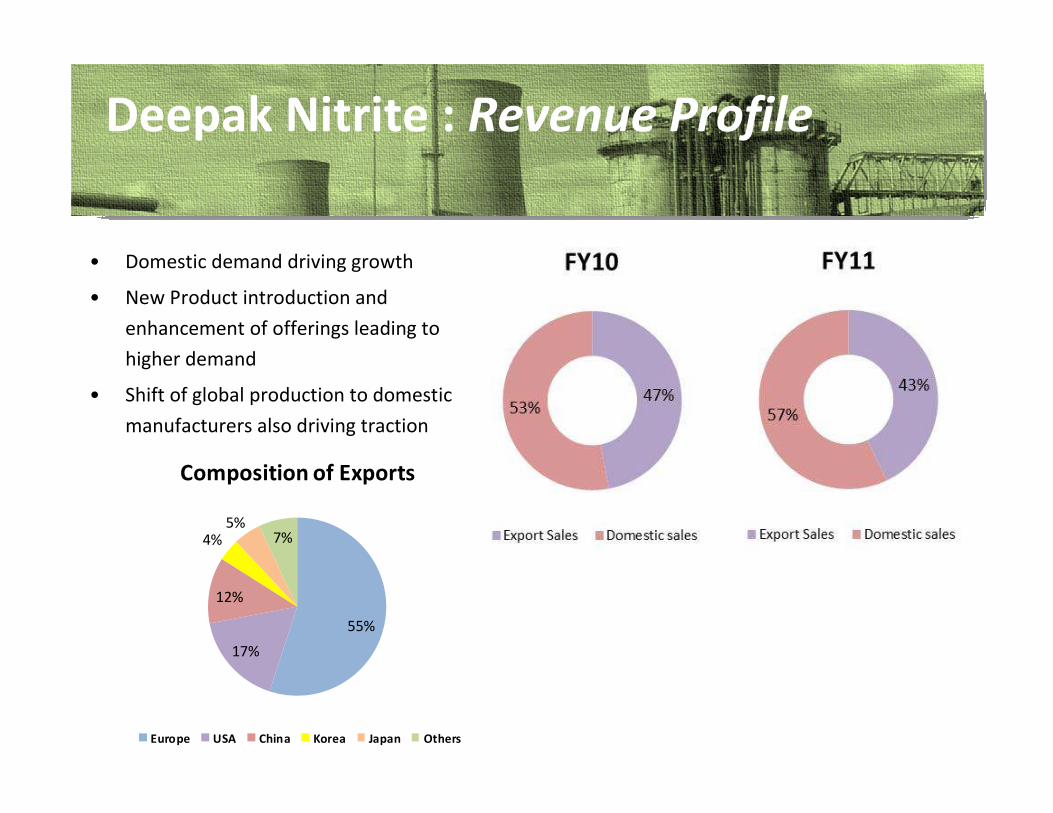

Deepak Nitrite : Revenue Profile

• Domestic demand driving growth

• New Product introduction and

enhancement of offerings leading to

higher demand

• Shift of global production to domestic

manufacturers also driving traction

55%

17%

12%

4%5%

7%

Composition of Exports

Europe USA China Korea Japan Others

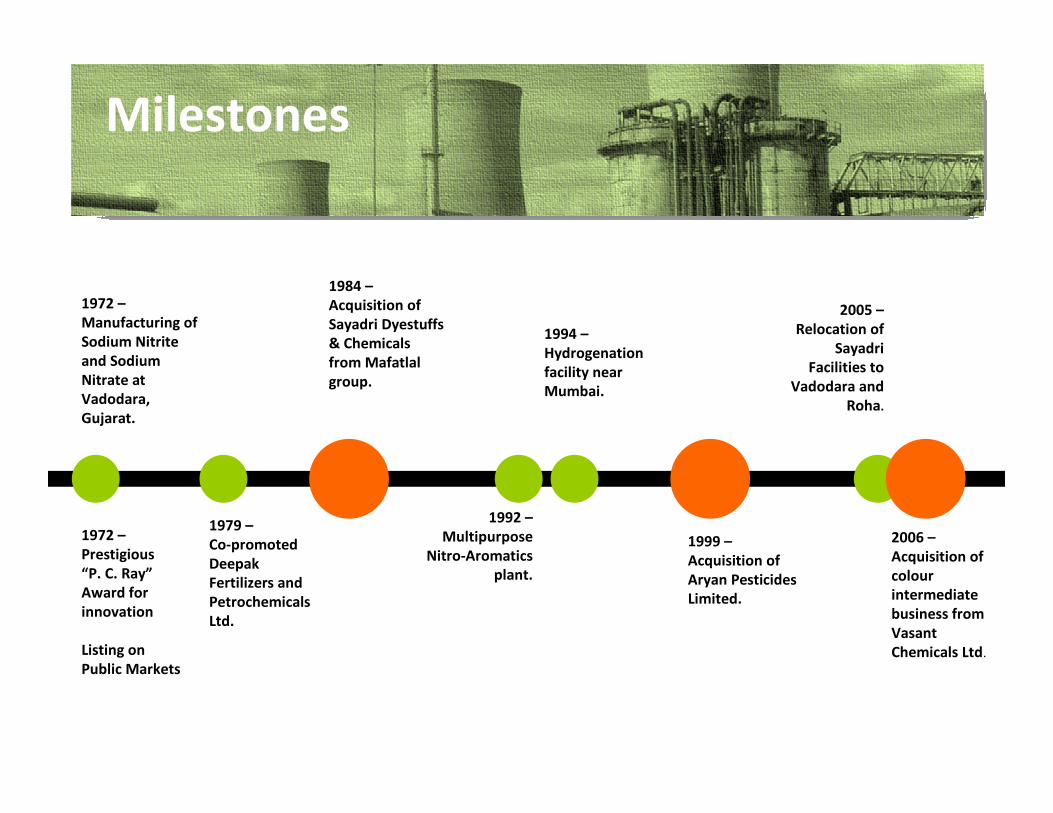

Milestones

1972 –

Manufacturing of

Sodium Nitrite

and Sodium

Nitrate at

Vadodara,

Gujarat.

1979 –

Co-promoted

Deepak

Fertilizers and

Petrochemicals

Ltd.

1984 –

Acquisition of

Sayadri Dyestuffs

& Chemicals

from Mafatlal

group.

1992 –

Multipurpose

Nitro-Aromatics

plant.

1994 –

Hydrogenation

facility near

Mumbai.

1999 –

Acquisition of

Aryan Pesticides

Limited.

2005 –

Relocation of

Sayadri

Facilities to

Vadodara and

Roha.

2006 –

Acquisition of

colour

intermediate

business from

Vasant

Chemicals Ltd.

1972 –

Prestigious

“P. C. Ray”

Award for

innovation

Listing on

Public Markets

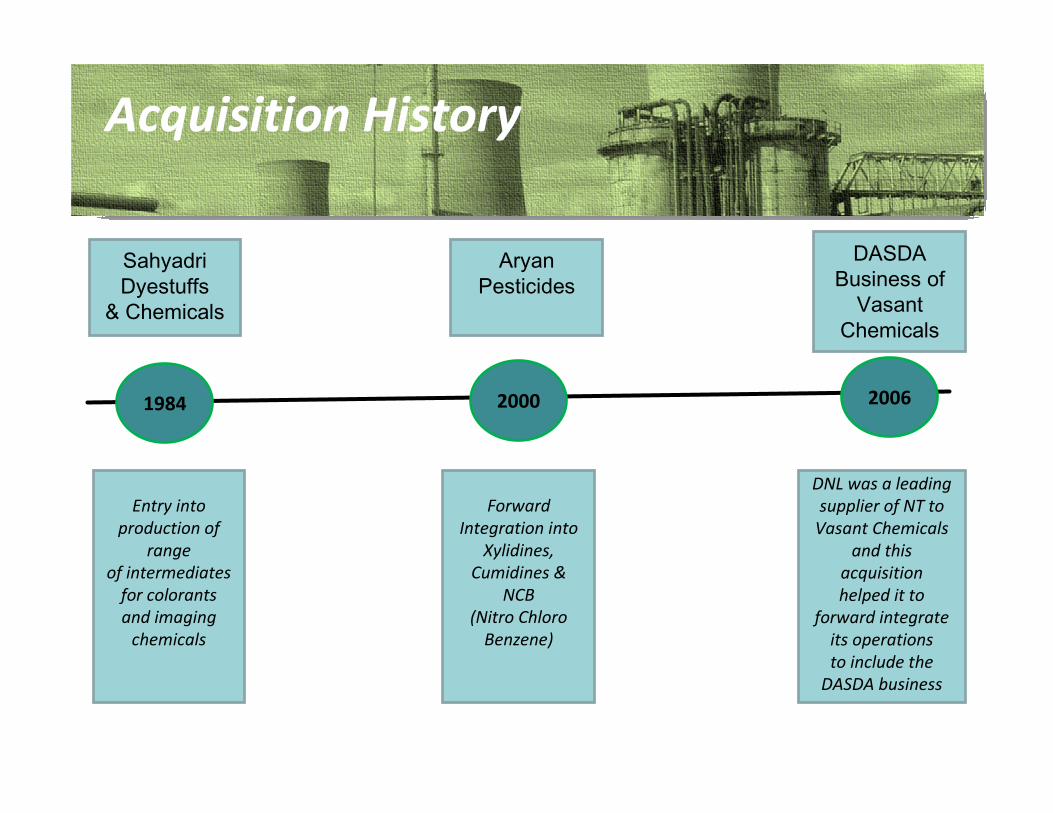

Acquisition History

1984 2000 2006

SahyadriDyestuffs

& Chemicals

Aryan Pesticides

DASDA Business of

VasantChemicals

Entry into

production of

range

of intermediates

for colorants

and imaging

chemicals

Forward

Integration into

Xylidines,

Cumidines &

NCB

(Nitro Chloro

Benzene)

DNL was a leading

supplier of NT to

Vasant Chemicals

and this

acquisition

helped it to

forward integrate

its operations

to include the

DASDA business

Fuel Additives

Petrol Blending

Diesel Blending

Aviation Turbine Fuel

Sodium Nitrite

Dyes/PigmentsPharma interm. Food coloursElectroplating Speciality chemicalsColourants

Nitro Chloro Benzene

Pharmaceuticals

Dyes

Rubber Chem.

Agrochemicals

Pigments

DASDA

Paper

Textiles

Detergents

Oximes

Agrochemicals

Nitro Tolunes

Colourants

Speciality chem

Rubber chemicals

Pharmaceuticals

Explosives

Dyes

Specialty chem.

DASDA

Agrochemicals

Specialty

Colourants

Products & Application

Cumidines

Agrochemicals

Xylidines

Pigment

Fuel Additive

Agro chemicals

Pharma interm.

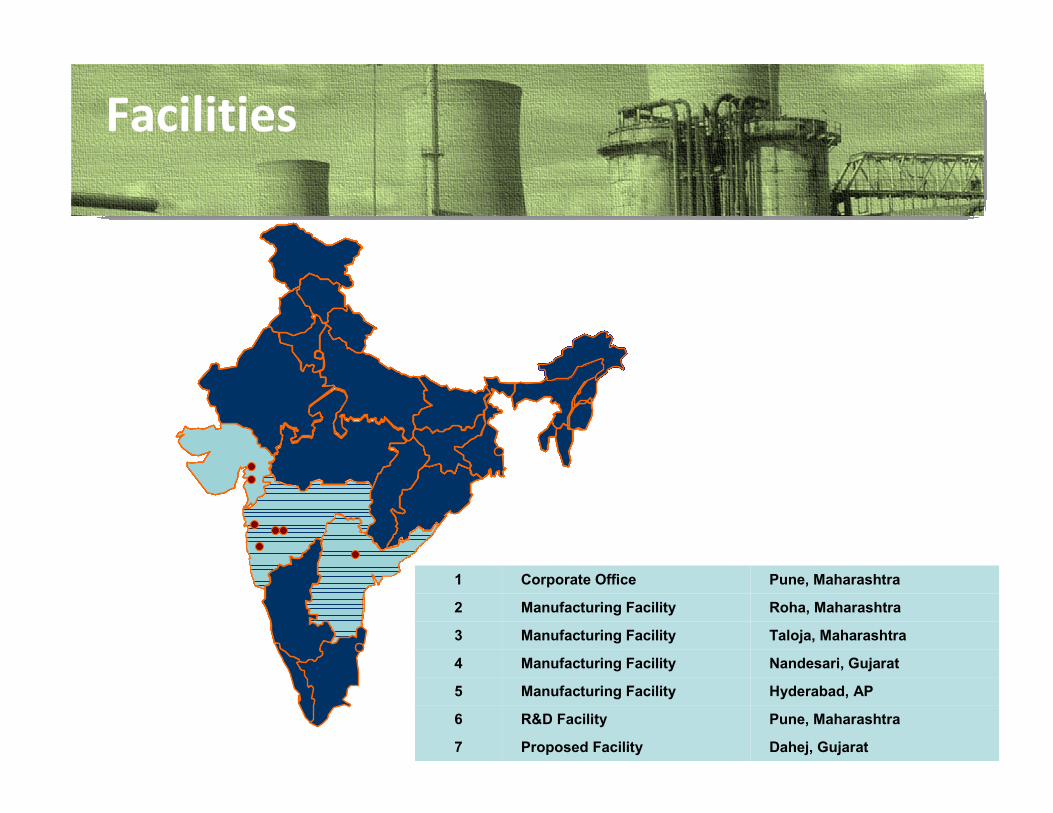

Facilities

1 Corporate Office Pune, Maharashtra

2 Manufacturing Facility Roha, Maharashtra

3 Manufacturing Facility Taloja, Maharashtra

4 Manufacturing Facility Nandesari, Gujarat

5 Manufacturing Facility Hyderabad, AP

6 R&D Facility Pune, Maharashtra

7 Proposed Facility Dahej, Gujarat

((((

Key Customers

Customer Relationships

• Deepak Nitrite has a diversified customer base consisting of some of the largest

chemical companies in the world, including Sygenta Global, Bayer Crop Science, BASF,

Kemira, Lanxess, Clariant, Isochem, Lonza, IOC, Reliance, Essar and Sudarshan

Chemicals.

• 43% of the company’s FY11 turnover was through exports

• Long standing relationships - have been supplying products for periods ranging from 5

to 10 years with several customers

• DNL has gone beyond the customer-vendor relationship and has entered into long-

term partnership arrangements with many of its customers

• Diversified customer base exposes company to different industries, economic cycles

and currencies thereby providing a natural hedge

• DNL has identified R&D as a key differentiator

and significant value creator

• Spends almost 1% of annual revenues on R&D

• Dedicated R&D facility in Pune which is Recognized by Dept. of Science and

Technology, Government of India

• R&D Headcount of over 90 personnel – Experienced & highly skilled technical

manpower including 5 Ph. D’s

• State of the Art Pilot Facility as a catalyst between R&D trials and commercial

production

• R&D efforts contributed around 18% of revenue in FY11

Research & Development

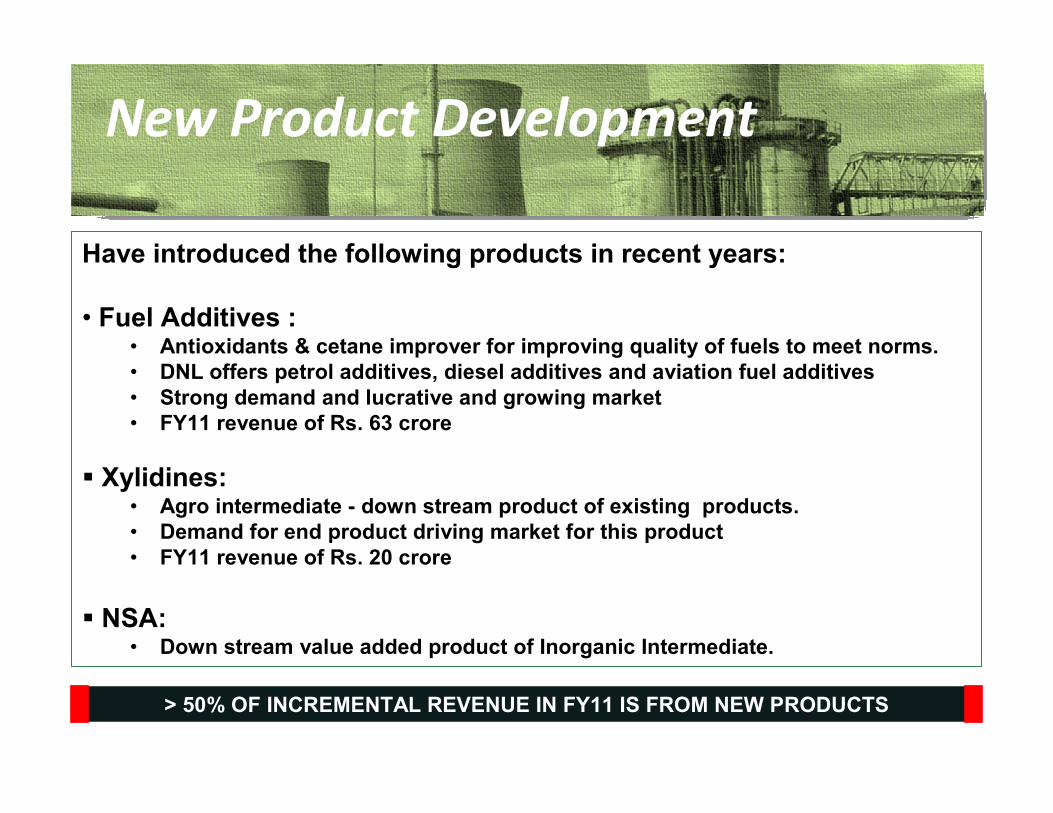

Have introduced the following products in recent years:

• Fuel Additives : • Antioxidants & cetane improver for improving quality of fuels to meet norms.

• DNL offers petrol additives, diesel additives and aviation fuel additives

• Strong demand and lucrative and growing market

• FY11 revenue of Rs. 63 crore

� Xylidines: • Agro intermediate - down stream product of existing products.

• Demand for end product driving market for this product

• FY11 revenue of Rs. 20 crore

� NSA: • Down stream value added product of Inorganic Intermediate.

New Product Development

> 50% OF INCREMENTAL REVENUE IN FY11 IS FROM NEW PRODUCTS

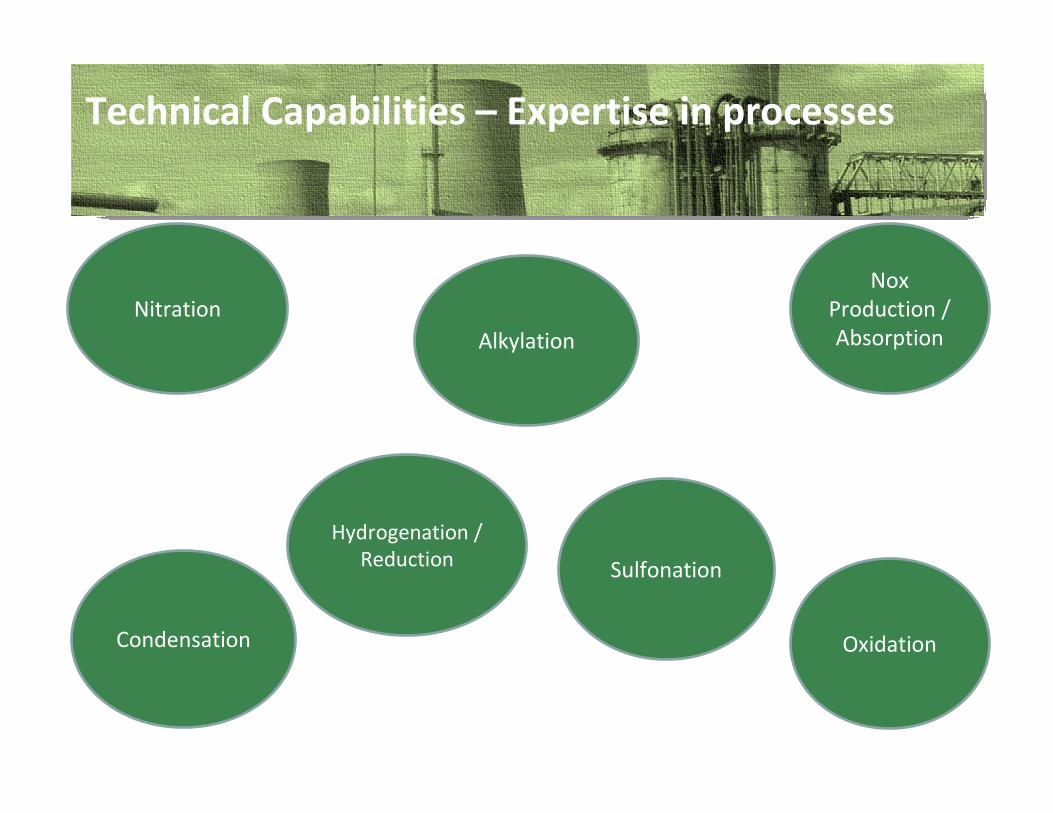

Technical Capabilities – Expertise in processes

Hydrogenation /

Reduction

Nitration

Sulfonation

Alkylation

Condensation Oxidation

Nox

Production /

Absorption

Technical Capabilities

� Able to handle complex and hazardous chemical processes with a high success ratio

� Able to optimise processes while meeting standards on product specifications, product quality and environmental norms

� Multi purpose manufacturing facilities provide flexibility to change product mix

� Focus on Technical capabilities to provide a competitive edge - R&D efforts also directed towards improvement of existing processes to enhance competence

Environmental Care

•We are committed to best practices and technologies for a cleaner, sustainable world

•We adhere to all statutory and recommended environmental norms

• R&D initiatives are supervised by Environmental scientists to ensure that all processes optimise resources and minimise impact on environment

•We have established effluent treatment plants at all of our facilities

• Compliance with environmental standards and green,sustainable business models are important parameterswhen serving global customers

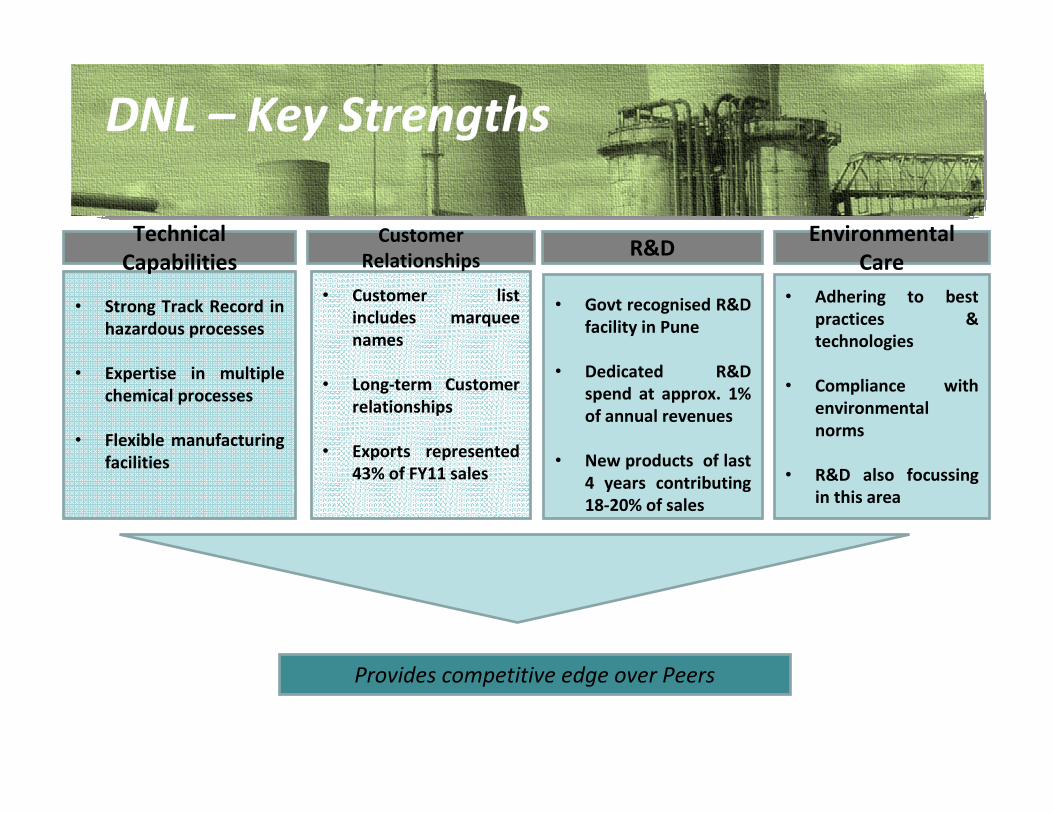

DNL – Key Strengths

• Strong Track Record in

hazardous processes

• Expertise in multiple

chemical processes

• Flexible manufacturing

facilities

• Customer list

includes marquee

names

• Long-term Customer

relationships

• Exports represented

43% of FY11 sales

• Govt recognised R&D

facility in Pune

• Dedicated R&D

spend at approx. 1%

of annual revenues

• New products of last

4 years contributing

18-20% of sales

• Adhering to best

practices &

technologies

• Compliance with

environmental

norms

• R&D also focussing

in this area

Technical

Capabilities

Customer

RelationshipsR&D

Environmental

Care

Provides competitive edge over Peers

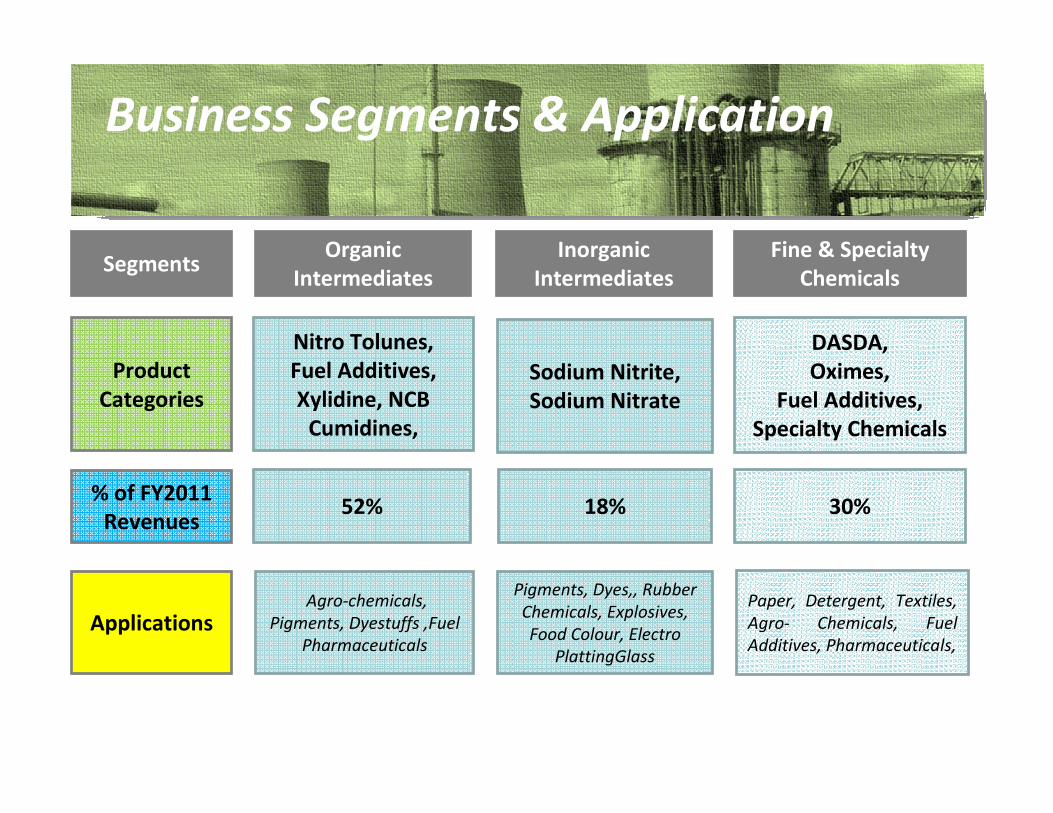

Business Segments & Application

Agro-chemicals,

Pigments, Dyestuffs ,Fuel

Pharmaceuticals

SegmentsOrganic

Intermediates

Inorganic

Intermediates

Fine & Specialty

Chemicals

Pigments, Dyes,, Rubber

Chemicals, Explosives,

Food Colour, Electro

PlattingGlass

Paper, Detergent, Textiles,

Agro- Chemicals, Fuel

Additives, Pharmaceuticals,

Applications

% of FY2011

Revenues 52% 18% 30%

Product

Categories

Nitro Tolunes,

Fuel Additives,

Xylidine, NCB

Cumidines,

Sodium Nitrite,

Sodium Nitrate

DASDA,

Oximes,

Fuel Additives,

Specialty Chemicals

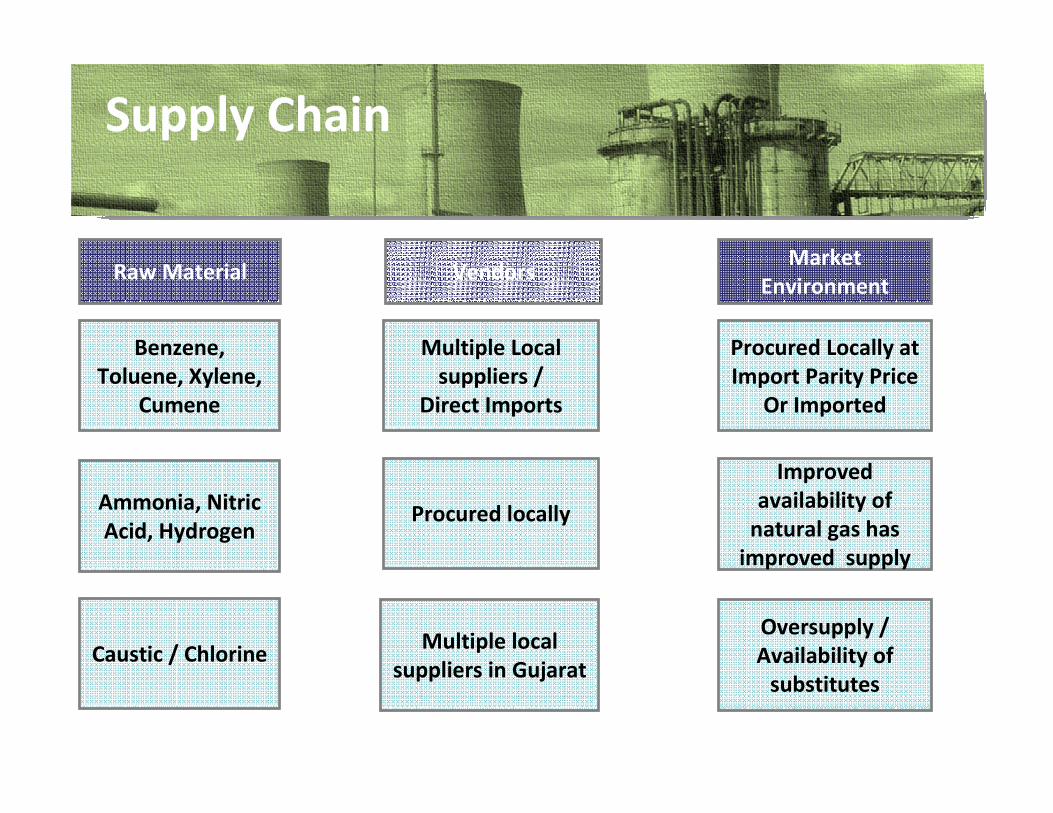

Supply Chain

Raw Material VendorsMarket

Environment

Benzene,

Toluene, Xylene,

Cumene

Ammonia, Nitric

Acid, Hydrogen

Caustic / ChlorineMultiple local

suppliers in Gujarat

Procured locally

Multiple Local

suppliers /

Direct Imports

Procured Locally at

Import Parity Price

Or Imported

Improved

availability of

natural gas has

improved supply

Oversupply /

Availability of

substitutes

Market Environment

• Global production shifting from developed countries to developing economies

• Demand for end products growing well in regional economies

• India established as favourable and reliable supplier in view of heightened focus on environmental awareness.

• High barriers to entry are favouring established players

• DNL position strong due to • Established long-term contracts with global MNCs• Supplying large proportion of requirement in key products • Supplies are split between different customers, markets and

currencies thereby mitigating risk arising in any individual market

Inroads to China

• China is considered to be the epicentre of global manufacturing and is an extremely competitive market

• DNL has been able to leverage strengths in quality, process expertise and environmental awareness to make inroads into the Chinese market

• China enjoys a reputation of being a low cost manufacturer and DNL has been able to demonstrate its competitiveness by supplying products to the Chinese domestic market

• Exports to China in FY11 were Rs. 35 crore

Inroads to USA

• DNL has been able to make inroads into the US market

• Pursuing additional business wins as the US market is large and lucrative –offering significant growth opportunities

• DNL is already catering to India & Europe – by establishing itself in China & USA, DNL will be catering to the largest markets across the globe

• Exports to USA were Rs. 47 crore in FY11, Growth of over 50%

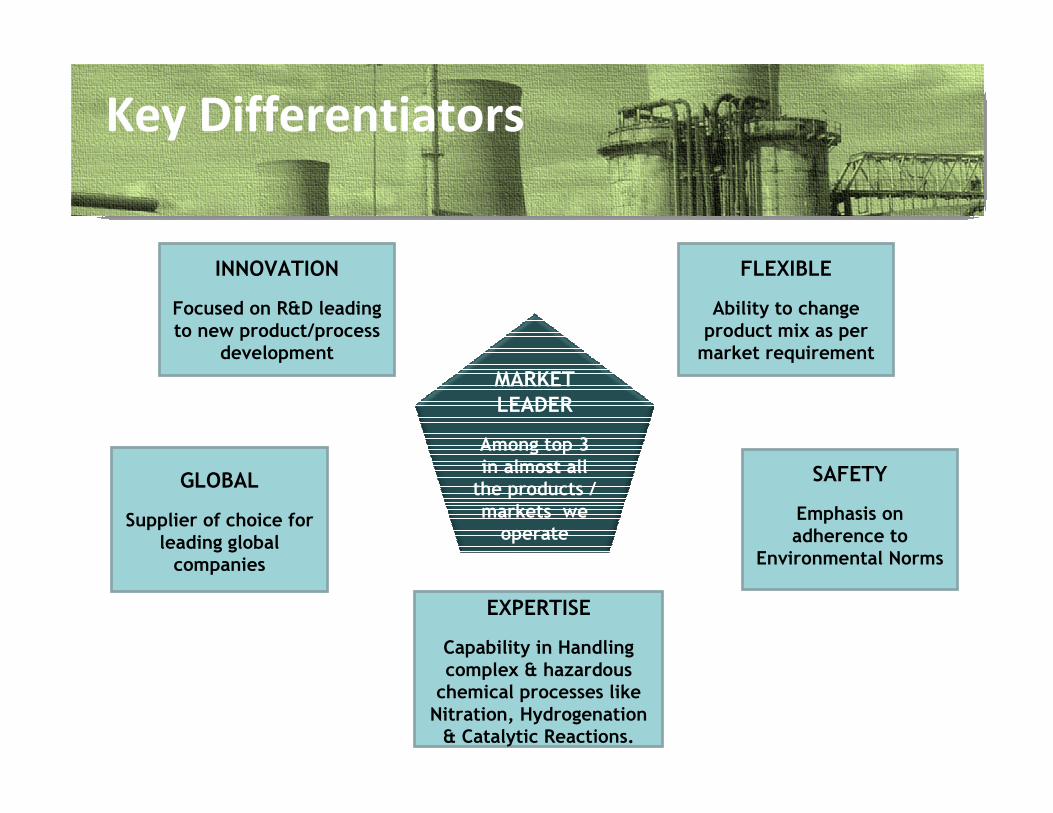

Key Differentiators

MARKET

LEADER

Among top 3

in almost all the products /

markets we operate

GLOBAL

Supplier of choice for

leading global companies

EXPERTISE

Capability in Handling

complex & hazardous chemical processes like

Nitration, Hydrogenation & Catalytic Reactions.

SAFETY

Emphasis on

adherence to

Environmental Norms

INNOVATION

Focused on R&D leading

to new product/process development

FLEXIBLE

Ability to change

product mix as per market requirement

Growth opportunities in Chinese Markets

Developing “New Process” Pipeline for established markets

Business Drivers

Reduction in Carbon emission norms

Growth in Environmental Challenging areas

Cost competitiveness causing consolidation of weaker players

in developed economies

Growth Markets shifting to Asia

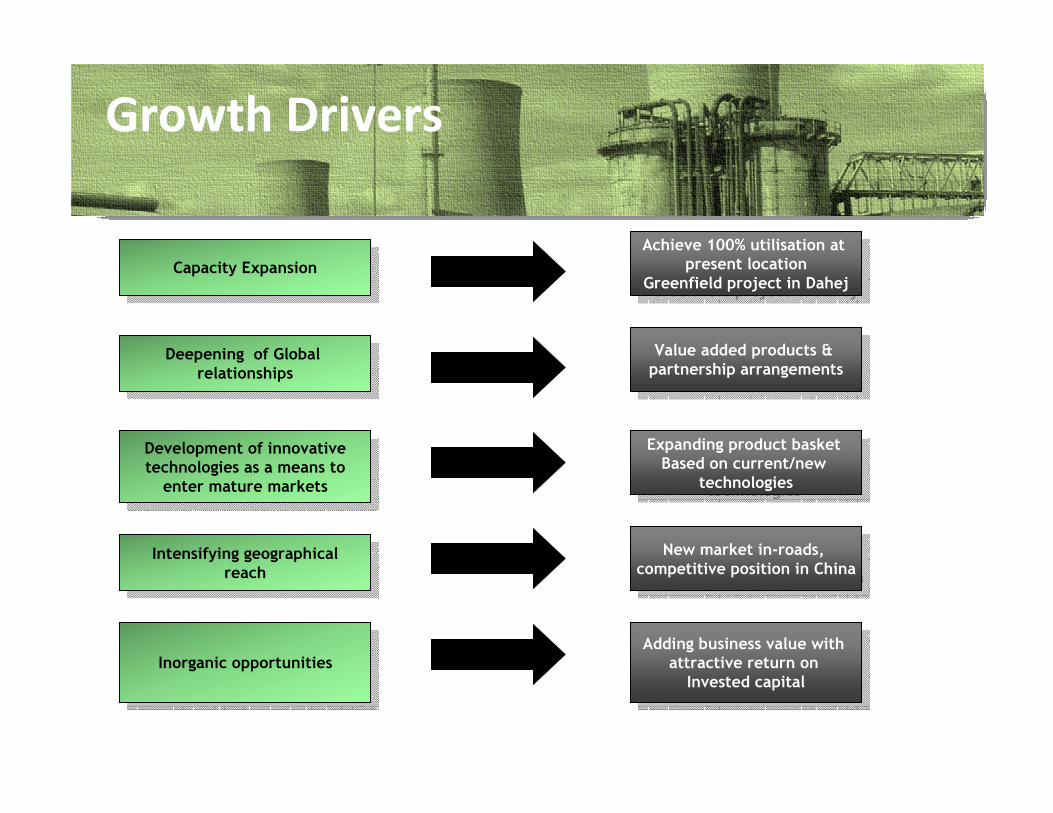

Growth Drivers

Capacity ExpansionCapacity Expansion

Achieve 100% utilisation at present location

Greenfield project in Dahej

Achieve 100% utilisation at present location

Greenfield project in Dahej

Deepening of Global

relationships

Deepening of Global

relationshipsValue added products &

partnership arrangements

Value added products &

partnership arrangements

Development of innovativetechnologies as a means to

enter mature markets

Development of innovativetechnologies as a means to

enter mature markets

Expanding product basket Based on current/new

technologies

Expanding product basket Based on current/new

technologies

Intensifying geographical

reach

Intensifying geographical

reachNew market in-roads,

competitive position in China

New market in-roads,

competitive position in China

Inorganic opportunitiesInorganic opportunities

Adding business value with attractive return on

Invested capital

Adding business value with attractive return on

Invested capital

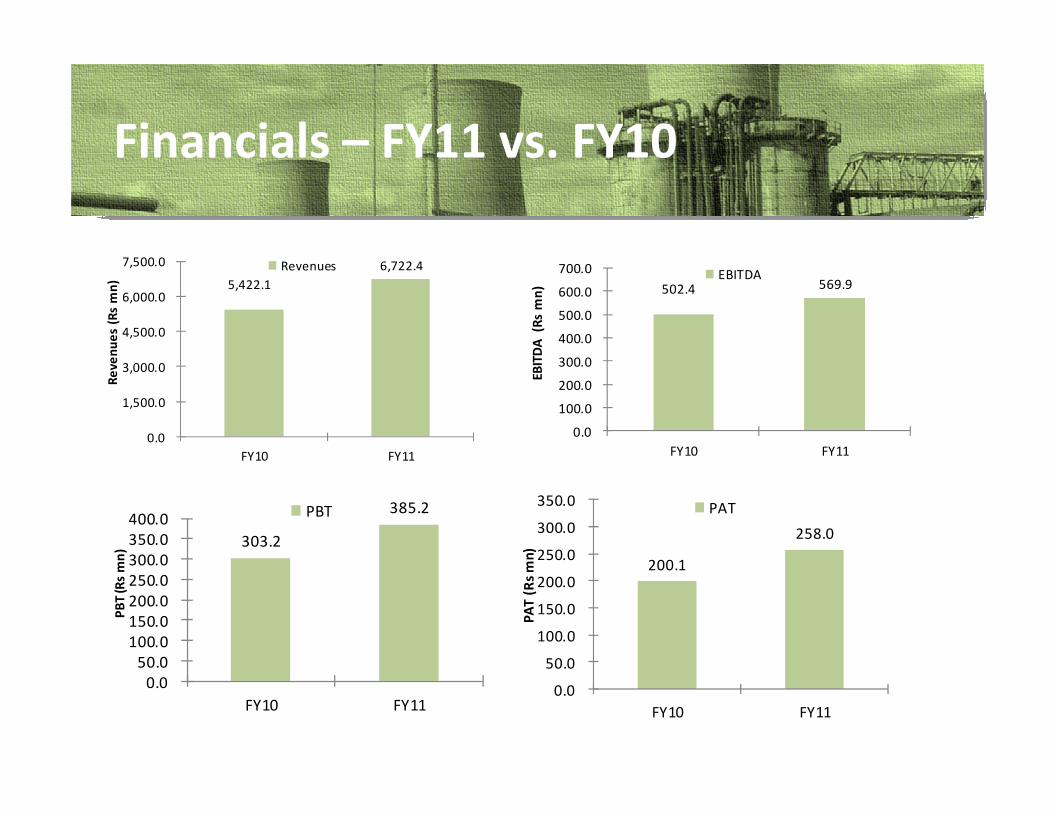

5,422.1

6,722.4

0.0

1,500.0

3,000.0

4,500.0

6,000.0

7,500.0

FY10 FY11

Re

ve

nu

es

(Rs

mn

)

Revenues

Financials – FY11 vs. FY10

502.4 569.9

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

FY10 FY11

EB

ITD

A

(Rs

mn

)

EBITDA

303.2

385.2

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

FY10 FY11

PB

T (R

s m

n)

PBT

200.1

258.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

FY10 FY11

PA

T (

Rs

mn

)

PAT

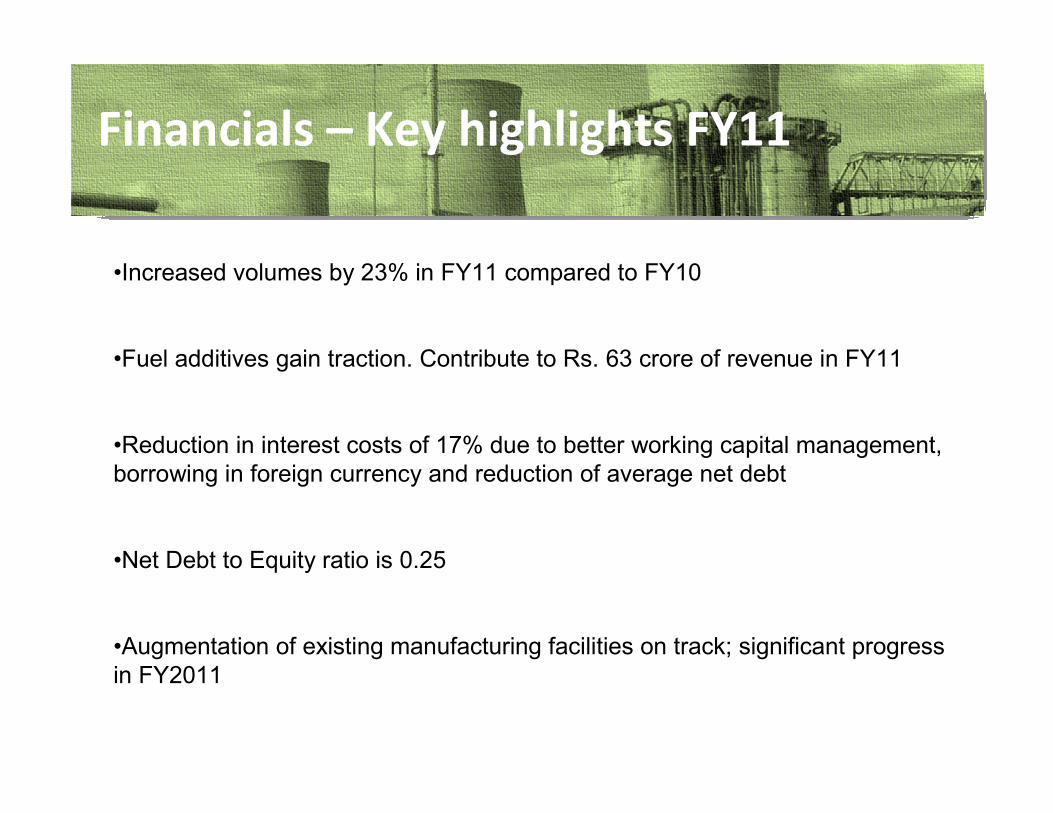

Financials – Key highlights FY11

•Increased volumes by 23% in FY11 compared to FY10

•Fuel additives gain traction. Contribute to Rs. 63 crore of revenue in FY11

•Reduction in interest costs of 17% due to better working capital management,

borrowing in foreign currency and reduction of average net debt

•Net Debt to Equity ratio is 0.25

•Augmentation of existing manufacturing facilities on track; significant progress

in FY2011

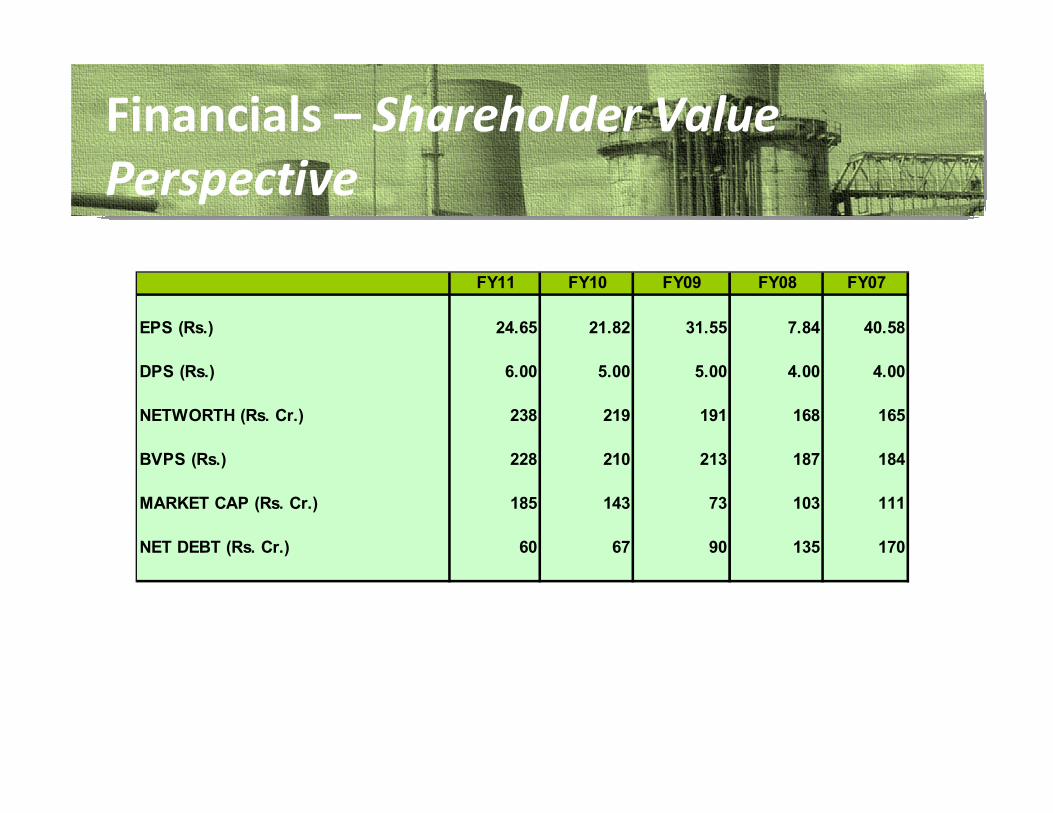

Financials – Last 5 years(INR Mn except EPS)

Financials – Shareholder Value

Perspective

FY11 FY10 FY09 FY08 FY07

EPS (Rs.) 24.65 21.82 31.55 7.84 40.58

DPS (Rs.) 6.00 5.00 5.00 4.00 4.00

NETWORTH (Rs. Cr.) 238 219 191 168 165

BVPS (Rs.) 228 210 213 187 184

MARKET CAP (Rs. Cr.) 185 143 73 103 111

NET DEBT (Rs. Cr.) 60 67 90 135 170

Deepak Nitrite : Financial Stability

• Consistent track record of paying dividends

• Strong Revenue growth – improving operating cash flows

• Reduction in interest cost by 17% in FY11 vs FY10

• Low gearing:

– Net D/E of 0.25 (March 31, 2011)

• BVPS of Rs. 228

Deepak Nitrite : Growth Plans

PRODUCT: PERFORMANCE CHEMICAL

SEGMENT: FINE & SPECIALTY CHEMICALS

CAPITAL OUTLAY: ` 150 CRORE

PROJECTED REVENUES: ` 350 – 400 CRORE AT PEAK UTILISATION

TIME FRAME FOR COMPLETION: 15 MONTHS

DAHEJ - GREENFIELD EXPANSION1

Deepak Nitrite : Growth Plans

PRODUCT: INORGANIC INTERMEDIATE

SEGMENT: INORGANIC CHEMICALS

CAPITAL OUTLAY: ` 50 CRORE

PROJECTED REVENUES: ` 120 – 140 CRORE AT PEAK UTILISATION

TIME FRAME FOR COMPLETION: 15 MONTHS

NANDESARI - BROWNFIELD EXPANSION2

Key Takeaways

• Well entrenched multi segment chemical company with

leading world players as its customers

• One of the top 3 producers of fine intermediates

• New products / markets opportunities driving growth

• Strong Financials – Low gearing & track record of dividends

Thank you

More information available online:

• Annual Reports

• Quarterly Financial Results

• 5 Years Financial Data & more

http://www.deepaknitrite.com/