english course for rural region development yunnan agricultural university zhao junquan phd

TRANSCRIPT

English Course for rural region development

Yunnan Agricultural university

Zhao Junquan PhD

Unit1 Agricultural Economics

Agricultural economics may be defined as applied social science dealing. With how humans choose to use technical knowledge and scarce productive resources such as land, labor, capital, and management to produce food and fiber and to distribute it for consumption to various members of society over time.

Like economics, agricultural economics seeks to discover cause-effect relationships. It uses the scientific method and economic theory to find answers to problems in agriculture and agribusiness.The following rapid growth in the ranks of professional agricultural economists, and the ever-increasing public use of their special talents, bear testimony to the foresight of those early pioneering theorists. Most beginning students probably have only a vague concept of

agricultural economics.

For the student, it is a blend of many subject areas. An agricultural economics curriculum ordinarily includes classes in technical agriculture, science, statistics, mathematics, business, general economics, and other social sciences. Students taking a curriculum in agricultural economics may major in such areas as farm management, production economics, agricultural marketing, agricultural policy, finance, economic development, natural resources, and community development or public affairs.

Unit2 The Farm and Food System

Agriculture is an integral part of the general economic system. We subdivide our national economy so that the fundamental structure can be seen. Producing firms and consumers are the central economic units in the system.

Many people are concerned about corporate activity in agriculture because of the economic consequences that could occur with concentrated resource control.

As a result, some states have attempted to limit the growth of corporation farming. Laws passed in several states prohibit corporate farming. Statutes restricting corporate farming have been enacted in several other states. Some states have laws requiring corporations to report the land that they own in the state. More than one-half of the states also have laws restricting ownership of real property by aliens, with a great deal of variation in the restraints provided by these laws as they are applied to alien ownership of property. Many producers are concerned about farming

corporations because they think corporations are more efficient and that their size gives them market advantages, which may put the family-farm operators at a competitive disadvantage. Farmers believe capital markets, volume buying of production inputs, and volumes selling of output afford advantages to corporate farms that are not available to them. However, most studies show that moderate-sized family farms are as efficient as most corporate farms. With this situation plus the generally low returns to agricultural investments, one would expect

very little growth in corporate agriculture.

Unit3 Consumer Behavior and Demand

This chapter concentrates only on households, or consumers, and the behavior of people in meeting their desire for goods and services. It is in the observed market behavior of people that the concept of demand rests. While demand will be specifically discussed later in the chapter, suffice it to say at this point that demand means the quantities of a product bought at alternative prices holding everything else constant.

When consumer behavior is studied, certain characteristics can be noted. One feature is that consumers spend everything they earn on goods and services, including savings. Another is that consumers never seem to get enough of most things. We can infer from this characteristic of consumer behavior that human wants are insatiable and that more is preferred to less.One of the reasons consumers do not buy infinite quantities of everything is that they have a limited amount of money income. In economics, we assume that consumers,

with a given money income, will purchase clothing, housing, food, haircuts, and all the other things that they want in amounts that will maximize utility or satisfaction for them. The utility of a product or service is derived from the inherent characteristics or qualities that cause them to be desired. These may be objective or subjective qualities. But it is unlikely that two individuals would attain the same utility or satisfaction from the consumption of the

same amount of a product.

Unit4 Value Relationship

We then are directed to comparing the values of products with the values of inputs used Lip in their production. As a first step, a couple of assumptions will be useful and even a bit realistic: (1) There are so many firms producing this product that the actions of any one firm will have no influence whatsoever on either input or product prices; and

(2) that the market does not differentiate one firm's product from that of another, that is, the firms produce a homogeneous product. Thus if a corn producer were to shut down completely or, alternatively, to produce the last possible extra bushel of corn, the market price of corn would not be affected. And provided that the corn meets certain quality standards, one producer's corn will not be discriminated against or offered a premium over that of other firms producing corn.Our assumption about unchanging prices

"vas valid

regarding individual firth decisions, but that doesn't mean that we are unable to cope with changing resource and product prices, or that we even expect them to remain unchanged. Change is a fact of life, in markets as in anything else. Changing economic conditions, in total market supply and demand cause frequent price adjustments in both resource and product markets. So our optimum is correct, not for all time, but only until another price change occurs, then an adjustment in X, use must again be made to find a new optimum.

Unit5 Producer Decision Making

In the previous chapter, we discussed the simplest production functions, specifically: (1) a single, composite, variable input function with nothing fixed, and its constant returns; and (2) a single-variable input function with other resources held constant. This functional relationship between a variable factor and its product is sometimes referred to as the factor-product relationship.

Agricultural production decisions are seldom so simple that the operator can choose a single crop or single livestock enterprise as the firm's only product. Crop farms typically produce two or more different types of grain crops; stock ranches frequently produce both livestock and grain or forage crops, or even two or more types of livestock. The relationship between enterprises is referred to as the product-product relationship. These two general problem areas-factor factor

and product-product-and the economic criteria for making these choices, are dealt with in turn in this chapter.An enterprise is a specific crop or type of livestock from which products are obtained, for example, cotton, wheat, beef cattle, hogs, or onions. In which to use the variable resources.

Physical relationships and economic factors cause producers to choose one particular set of resources and not some other combination with which to produce their products. Basic in this choice is the interaction between inputs and their effect on the productivity of the employed resources as the input mix is changed.

Unit6 Financial Picture of Agriculture

This chapter discusses the financial position of agriculture, sources of farm credit, the banking system, and how to compute simple interest rates. The vitality of agriculture depends on managers who understand finance and can apply it to the farm and ranch business. A balance sheet gives you some idea of the present financial position of an individual or business.

A balance sheet gives you some idea of the present financial position of an individual or business. It is the result of all past transactions. A balance sheet is divided into assets, liabilities, and net worth.Most farm credit has been used to finance farm expansion and higher production cost items such as farm machinery and motor vehicles.

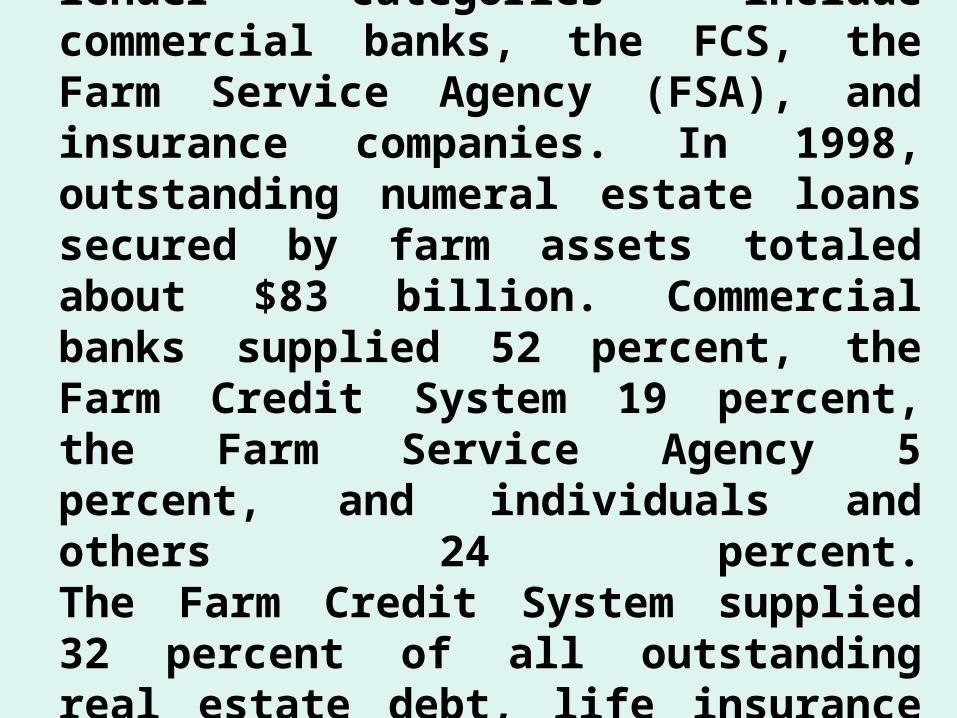

The four major institutional farm lender categories include commercial banks, the FCS, the Farm Service Agency (FSA), and insurance companies. In 1998, outstanding numeral estate loans secured by farm assets totaled about $83 billion. Commercial banks supplied 52 percent, the Farm Credit System 19 percent, the Farm Service Agency 5 percent, and individuals and others 24 percent.The Farm Credit System supplied 32 percent of all outstanding real estate debt,

life insurance companies 11 percent,

commercial banks 31 percent, the Farm Service Agency 5 percent, and individuals 21 percent. Historically, individuals have been the major source of funds for land transfers. The Farm Credit System is the largest lender involved in the land mortgage field. The total real estate debt outstanding as of December 31, 1998, was $87.6 billion.

Unit7 Farmers Home Administration

• The Farmers Home Administration primarily provided two types of loans. One was a guaranteed loan handled by a private lender. Farmers Home Administration guaranteed to limit the loss on the loan to a specified percentage. The second type was a direct loan by the Farmers Home Administration. Loan funds were obtained from insured notes backed by the government.

It is the result of all past transactions. A balance sheet is divided into assets, liabilities, and net worth. Most farm credit has been used to finance farm expansion and higher production cost items such as farm machinery and motor vehicles. The four major institutional farm lender categories include commercial banks, the FCS, the Farm Service Agency (FSA), and insurance companies. In 1998, outstanding numeral estate loans secured by farm assets totaled about $83 billion.

Commercial banks supplied 52 percent, the Farm Credit System 19 percent, the Farm Service Agency 5 percent, and individuals and others 24 percent.The Farm Credit System supplied 32 percent of all outstanding real estate debt, life insurance companies 11 percent, commercial banks 31 percent, the Farm Service Agency 5 percent, and individuals 21 percent. Historically, individuals have been the major source of funds for land transfers.

The Farm Credit System is the largest lender involved in the land mortgage field. The total real estate debt outstanding as of December 31, 1998, was $87.6 billion.

Unit 8 The Banking System• Agriculture and agricultural financial insti

tutions do not operate in isolation from conditions in other sectors of the economy. The agricultural sector must compete for available funds with public and private borrowers from all segments of the economy. While both monetary and fiscal policies influence the availability of loanable funds to agriculture, monetary policy is of greater concern here.

Fiscal policy is the government policy regarding expenditures and taxation. Thus, the government can increase expenditures of such agencies as the Farm Service Agency and increase loanable funds, or restrict credit by cutting budgets. Also, of course, tax levels influence the amount of money available to producers to invest in their operations. Fiscal policy changes affect the flow of funds to financial instituti

ons and therefore affect loanable funds.

These changes also influence business activity and savings. A tax decrease tends to stimulate incomes, employment, and savings; a tax increase will have an opposite impact on the economic system.The ability of banks to create or destroy money as they perform their usual business has a great deal to do with the performance of the economy.Given their potential impact throughout the system, the activities of the banking industry must be coordinated so as to inhibit wide swings in prices and employment levels.