energy tidbits - saf group · 1. saudi aramco’s announces intention to ipo, hopefully marketing...

TRANSCRIPT

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

Energy Tidbits

Dan Tsubouchi

Principal, Chief Market Strategist

Aaron Bunting

Principal, COO, CFO

Ryan Dunfield

Principal, CEO [email protected]

Alan Cooper

Vice President

Ryan Haughn

Principal, Energy

Hope Aramco IPO Marketing Gives Insight Into Abqaiq Repairs,

OPEC+ Cuts, Permian Oil Growth Views And Houthis Risk

Welcome to new Energy Tidbits memo readers. We are continuing to add new readers to our Energy Tidbits

memo and energy blogs. The focus and concept for the memo was set in 1999 with input from PMs, who were

looking for research (both positive and negative items) that helped them shape their investment thesis to the energy

space, and not focusing on day to day trading. Our priority was and still is to not just report on events, but interpret

and point out implications therefrom. The best example is our review of investor days, conferences and earnings calls

focusing on sector developments that are relevant to the sector and not just a specific company results/guidance.

Our target is to write on 48 to 50 weekends per year and to send out by noon mountain time.

This week’s memo highlights:

1. Saudi Aramco’s announces intention to IPO, hopefully marketing provides insights into Saudi view on Permian

growth potential, Abqaiq repair (diffs), Houthis and OPEC+ extension potential. (Click Here)

2. Continuing to see oil industry and analysts lower US oil growth expectations for 2020. (Click Here)

3. Denmark signs off, subject to 30 day comment period, on Gazprom’s 5.3 bcf/d pipeline to Germany. (Click Here)

4. Bloomberg “berth” data shows China LNG imports down YoY in Oct. (Click Here)

5. BP expects it to be tough for US LNG projects to run at capacity in 2020/2021. (Click Here)

6. Please follow us on Twitter at [LINK] for breaking news that ultimately ends up in the weekly Energy Tidbits memo

that doesn’t get posted until Sunday noon MT.

7. For new readers to our Energy Tidbits and our blogs, you will need to sign up at our blog sign up to receive future

Energy Tidbits memos. The sign up is available at [LINK].

Produced by: Dan Tsubouchi

Nov 3, 2019

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

2

Energy Tidbits

Table of Contents Natural Gas – Natural gas injection of 89 bcf, storage now +559 bcf YoY surplus ..................................................5

Figure 1: US Natural Gas Storage ....................................................................................................................5

Natural Gas – US gas production in August +8.5 bcf/d YoY ....................................................................................5

Figure 2: US Dry Natural Gas Production ........................................................................................................5

Natural Gas – US August LNG exports +1.5 bcf/d YoY, ..........................................................................................5

Figure 3: US LNG Exports (bcf/d) .....................................................................................................................6

Figure 4: Natural Gas Flows To Sabine Pass LNG ..........................................................................................6

Natural Gas – US August pipeline exports to Mexico +0.4 bcf/d YoY ......................................................................6

Figure 5: US Pipeline Exports To Mexico (bcf/d)..............................................................................................6

Figure 6: Mexico Gas Pipelines Map ........................................................................................................................7

Natural Gas – Mexico’s natural gas production finally breaks above 5 bcf/d in Sept ..............................................7

Figure 7: Mexico Natural Gas Production (bcf/d) .............................................................................................7

Natural Gas – Looks like a warm start to winter in Japan ........................................................................................7

Figure 8: Japan Winter Temperature Forecast For Nov Thru Jan ...................................................................8

Natural Gas – China “berth” data shows LNG import data in Oct down 17.4% YoY ...............................................8

Figure 9: China LNG imports ............................................................................................................................8

Natural Gas – Baker Hughes LNG supply needs to be >15% more than demand ..................................................8

Figure 10: Excess Supply Capacity Is Needed To Support LNG Contract Volumes .......................................9

Natural Gas – Gazprom’s 8.9 bcf/d of new export pipeline to start up soon ............................................................9

Denmark signs off on 5.3 bcf/d Nord Stream 2 to Germany ......................................................................... 10

Figure 11: Nord Stream and Nord Stream 2 Gas Pipelines .......................................................................... 10

3.6 bcf/d Power of Siberia pipeline to China now filled up natural gas ......................................................... 10

Figure 12: Gazprom’s 3.6 bcf/d Power of Siberia Natural Gas Pipeline To China ........................................ 11

Natural Gas – BP says be tough to find customers for all US LNG in 2020/2021 ................................................ 11

Natural Gas – Will Shell’s cash shortfall cause a delay in LNG Canada Phase 2? .............................................. 11

Figure 13: Canadian LNG, Potential For Multi Year Runway If Continuous Construction Cycle .................. 12

Natural Gas – Cheniere sees better LNG markets in 2021 ................................................................................... 13

Oil – US oil rigs down 5 to 691 oil rigs ................................................................................................................... 13

Figure 14: Baker Hughes Total US Oil Rigs .................................................................................................. 14

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

3

Energy Tidbits

Oil – Total Cdn rigs -5 to 142 total rigs .................................................................................................................. 14

Figure 15: Baker Hughes Total Canadian Oil Rigs ....................................................................................... 14

Oil – US oil production unchanged at 12.6 mmb/d, matching the all time high ..................................................... 14

Figure 16: Weekly US Oil Production ............................................................................................................ 15

Figure 17: US Weekly Oil Production ............................................................................................................ 15

Figure 18: YoY Change in US Weekly Oil Production ................................................................................... 16

Oil – EIA Form 914, US Aug oil production up vs July, rebound after Hurricane Barry ........................................ 16

Figure 19: EIA Form 914 US Oil Production .................................................................................................. 16

Figure 20: EIA Form 914 US Oil Production vs Weekly Estimates ............................................................... 16

Oil – Permian base oil decline rates around 40% ................................................................................................. 17

Concho’s Permian base oil declines in low 40’s but to 30’s at yr end 2020 .................................................. 17

Matador says they have a 38% to 40% base Permian oil decline rate ......................................................... 17

Figure 21: Increasing Permian Decline Rates ............................................................................................... 18

Oil – More pointing to lower US oil growth in 2020 ............................................................................................... 18

BoA/Merrill expect to lower their +800,000 b/d US oil growth in 2020 .......................................................... 19

Chevron and Exxon buck the trend, both delivering on Permian growth plans ............................................. 19

Liberty Oilfield says “we may see US oil production plateau in early 2020” .................................................. 19

US Silica Q3 – Taking out capacity, points to lesser US oil growth potential ................................................ 19

Oil – Trans Mountain and contractors have hired 2,200 people ........................................................................... 20

Oil – Reports Keystone shut in for another week or so ......................................................................................... 20

Oil – Alberta provides curtailment relief for crude by rail volumes ........................................................................ 20

Figure 22: WCS-WTI Differential ................................................................................................................... 21

Oil – Oil input into refineries up 133,000 b/d to 15.998 mmb/d ............................................................................. 21

Figure 23: US Refinery Crude Oil Inputs (thousand b/d) ............................................................................... 21

Oil – US “NET” oil imports up 1.196 mmb/d to 3.370 mmb/d ................................................................................ 21

Figure 24: US Weekly Preliminary Oil Imports By Major Countries .............................................................. 22

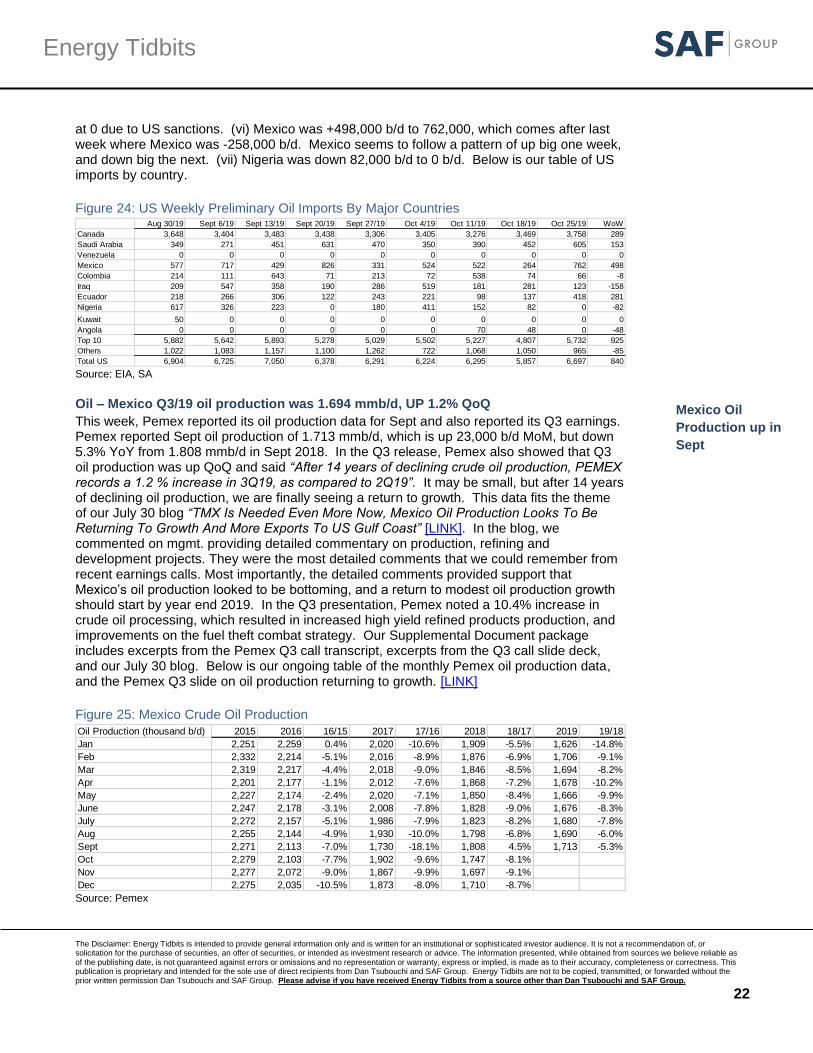

Oil – Mexico Q3/19 oil production was 1.694 mmb/d, UP 1.2% QoQ ................................................................... 22

Figure 25: Mexico Crude Oil Production ........................................................................................................ 22

Figure 26: Mexico Oil Production – From Pemex Q3 Presentation............................................................... 23

Oil – Mexico Sept oil exports were 995,000 b/d .................................................................................................... 23

Figure 27: Mexico Crude Oil Exports ............................................................................................................. 23

Oil – Johan Sverdrup loadings to already hit ~400,000 b/d in Dec ...................................................................... 23

Oil – Russia at 11.229 mmb/d in Oct, still slightly above OPEC+ quota ............................................................... 24

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

4

Energy Tidbits

Oil – Reuters OPEC for Oct production: +693,000 b/d to 29.593 mmb/d ............................................................. 24

Figure 28: Reuters Survey of Oct 2019 production ....................................................................................... 24

Oil – Bloomberg OPEC survey for Sept, Saudi down 1.47 mmb/d ave over month ............................................. 24

Figure 29: Bloomberg Survey of Sept 2019 production ................................................................................ 25

Oil – Saudi Aramco announces intention to proceed with IPO.............................................................................. 25

IPO likely to give indications on OPEC+ cuts, Houthis/Iran, diffs, etc ........................................................... 25

Also if Saudi agrees with Falih view on lower than expected Permian growth ............................................. 26

Oil – Saudi to cut govt spending, the biggest (least painful) cut would be Houthis war ........................................ 26

Don’t forget Saudi has reportedly been talking to the Houthis ...................................................................... 27

Oil – Saudi helps build the case that peak oil demand hits sooner than expected ............................................... 27

Makes us wonder about nuclear power, especially mini nukes..................................................................... 27

Figure 30: Saudi Arabia Primary Energy Consumption By Fuel ................................................................... 28

Oil – Khamenei reminds to negotiations with US .................................................................................................. 28

Oil – Sounds like lingering concerns for a Druzhba pipeline quality problem ....................................................... 28

Oil – HSFO demand likely higher with IMO 2020 non compliance ....................................................................... 28

Oil and Natural Gas – sector/play/market insights from Q3 calls .......................................................................... 29

BP – priority is Eagle Ford over the Permian ................................................................................................ 29

Concho – Reaffirmed the move to wider well spacing .................................................................................. 29

GATX – Analyst raises risk that Union Pacific may ban retrofit DOT-117R cars .......................................... 30

Liberty Oilfield – Drilling slowdown in Q4; smoother industry drilling in 2020 ............................................... 30

Nabors – Customers stretching out bill payment ................................................................................................... 31

Oil & Natural Gas – Encana’s new branding announcement ................................................................................ 31

Energy Tidbits – Now on Twitter ............................................................................................................................ 32

Energy Tidbits – Sign up on our email distribution for tidbits and blogs ................................................................ 32

LinkedIn – Look for quick energy items from me on LinkedIn ............................................................................... 32

Misc Facts and Figures.......................................................................................................................................... 32

Iran’s taking 52 US hostages was 40 years ago tomorrow ........................................................................... 32

30 year anniversary of the falling of the Berlin wall ....................................................................................... 33

Early retirement may speed up cognitive decline .......................................................................................... 33

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

5

Energy Tidbits

Natural Gas – Natural gas injection of 89 bcf, storage now +559 bcf YoY surplus

The EIA reported an 89 bcf natural gas injection, which was in line with expectations of a 85 bcf injection to bring storage to 3.695 as of Oct 25. This is a widening of the YoY surplus to 559 bcf vs 519 bcf surplus last week and storage is now 52 bcf above vs the 5 yr average. The continued expectation is for the YoY storage surplus to keep widening from higher YoY production which is holding HH prices around $2.25-$2.50. There is only 1 week to get to Nov 1, the official start of the winter heating season and it looks like storage should reach the estimate of +580 bcf YoY. Below is the EIA’s storage table from its Weekly Natural Gas Storage Report. [LINK] Figure 1: US Natural Gas Storage

Source: EIA

Natural Gas – US gas production in August +8.5 bcf/d YoY

The EIA released its Natural Gas Monthly, which includes its estimates for “actuals” for August gas production. The big negative to natural gas has been higher YoY natural gas supply, and this continues to be the case in August. August YoY increase of +8.5 bcf/d is higher than the July YoY increase of 7.9 bcf/d, but down significantly from the ~10.0 bcf/d YoY increases we saw at the beginning of 2019. They are still huge YoY, but just less. The EIA estimates US natural gas dry production in August at 93.7 bcf/d, +8.5 bcf/d YoY. Higher YoY natural gas production is the primary factor keeping HH gas prices low. Our Supplementary Documents package includes excerpts from the EIA Natural Gas Monthly. [LINK] Figure 2: US Dry Natural Gas Production

Source: EIA

Natural Gas – US August LNG exports +1.5 bcf/d YoY,

The EIA Natural Gas Monthly also reported “actuals” for US LNG exports, which were 4.5 bc/d in August, +1.5 bcf/d YoY but -0.6 bcf/d MoM vs July. The decrease in August was expected, as trains 3 and 4 at Cheniere’s Sabine Pass were offline for a majority of Aug for

bcf/d 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Jan 56.0 60.0 65.9 65.3 67.8 72.6 73.8 71.0 77.9 88.7

Feb 57.3 58.8 65.2 65.9 67.5 73.7 74.7 71.6 79.4 89.5

March 57.3 61.5 65.1 65.4 68.2 74.1 74.0 73.3 80.2 90.0

Apr 57.6 62.3 65.4 66.0 68.6 75.0 73.8 73.4 80.4 90.5

May 58.0 62.4 65.6 66.3 69.5 74.2 73.5 73.3 81.3 90.0

June 57.2 62.1 65.4 66.3 69.8 74.3 72.5 73.8 81.8 91.0

July 58.3 62.5 65.8 67.0 70.6 74.3 73.1 74.7 83.4 91.3

Aug 58.9 63.2 65.4 67.0 71.6 74.3 72.3 74.7 85.2 93.7

Sept 59.1 63.1 66.2 67.2 71.7 75.0 71.9 75.8 86.4

Oct 60.1 65.1 66.5 67.6 72.2 74.1 71.4 76.9 87.2

Nov 60.1 65.9 66.6 68.6 73.1 74.1 72.1 79.0 88.6

Dec 61.0 65.6 65.8 66.6 74.7 74.0 71.2 79.5 88.9

Average 58.4 62.7 65.7 66.7 70.4 74.1 72.8 74.8 83.4

YoY storage at

559 bcf YoY

surplus

US Aug gas

production +8.5

bcf/d YoY

US Aug LNG

exports +1.5 bcf/d

YoY

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

6

Energy Tidbits

scheduled maintenance. Note, the EIA’s new STEO has forecast Q4 LNG exports at 5.35 bcf/d. Below is our table of EIA’s monthly LNG exports, and our graph of natural gas flows to Sabine Pass LNG, which shows the decrease in Aug.

Figure 3: US LNG Exports (bcf/d)

Source: EIA

Figure 4: Natural Gas Flows To Sabine Pass LNG

Source: EIA

Natural Gas – US August pipeline exports to Mexico +0.4 bcf/d YoY

The EIA Natural Gas Monthly also estimates gas pipeline exports to Mexico were 5.4 bcf/d in Aug, which is +0.4 bcf/d YoY vs 5.0 bcf/d in Aug 2018, and it was up marginally MoM from 5.3 bcf/d in July 2019. Gas pipeline exports to Mexico will be even higher in Sept, with the start of TC Energy’s 2.6 bcf/d Sur de Texas-Tuxpan export pipeline (running just off the east coast of Mexico), as Platts reported volumes began flowing on Sept 3 [LINK]. The Below is our table of the EIA’s monthly gas exports to Mexico.

Figure 5: US Pipeline Exports To Mexico (bcf/d)

Source: EIA

(bcf/d) 2016 2017 2018 2019

Jan 0.0 1.7 2.3 4.1

Feb 0.1 1.9 2.6 3.7

March 0.3 1.4 3.0 4.2

Apr 0.3 1.7 2.9 4.2

May 0.3 2.0 3.1 4.7

June 0.5 1.7 2.5 4.7

July 0.5 1.7 3.2 5.1

Aug 0.9 1.5 3.0 4.5

Sept 0.6 1.8 2.7

Oct 0.1 2.6 2.9

Nov 1.1 2.7 3.6

Dec 1.3 2.7 4.0

Full Year 0.5 1.9 3.0

Full Year bcf 186 708 1,084

bcf/d 2014 2015 2016 2017 2018 2019

Jan 1.7 2.2 3.2 3.9 4.4 4.9

Feb 1.8 2.3 3.4 4.1 4.5 4.8

March 1.9 2.4 3.3 4.2 4.3 4.8

Apr 1.9 2.6 3.5 3.9 4.4 4.6

May 2.0 2.8 3.7 4.2 4.4 4.9

June 2.2 3.0 3.9 4.5 4.6 5.2

July 2.2 3.3 4.0 4.4 4.9 5.3

Aug 2.1 3.3 4.3 4.4 5.0 5.4

Sept 2.2 3.3 4.1 4.2 5.0

Oct 1.9 3.2 4.2 4.3 4.9

Nov 1.9 3.0 4.0 4.5 4.7

Dec 2.1 3.2 3.7 4.4 4.5

Full Year 2.0 2.9 3.8 4.2 4.6

US Aug pipeline

exports to Mexico

+0.4 bcf/d YoY

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

7

Energy Tidbits

Figure 6: Mexico Gas Pipelines Map

Source: Platts

Natural Gas – Mexico’s natural gas production finally breaks above 5 bcf/d in Sept

One of the key Mexican energy themes continues to be their inability to grow domestic natural gas production, which means increasing natural gas imports from the US as Mexico natural gas production has been stuck below 5.0 bcf/d since Sept 2017. Although not a huge increase, Pemex reported its Sept natural gas production and Mexico natural gas production in Sept was 5.017 bcf/d and means Mexico finally broke above 5.0 bcf/d. Sept was +2.1% YoY vs Sept 2018 and +1.6% MoM from Aug 2019. Below is our ongoing table of Pemex reported monthly natural gas production. [LINK]

Figure 7: Mexico Natural Gas Production (bcf/d)

Source: Pemex

Natural Gas – Looks like a warm start to winter in Japan

The big negative to LNG prices in 2019 was the mild Asian winter led to surplus LNG cargos in peak demand season for natural gas/LNG. The surplus LNG had to find a home and ended up in Europe storage. Just like in North America, if Asian natural gas demand is weaker from a mild winter, it means that it is difficult for LNG prices to catch up over the non peak season. Last week, we saw the Japan Meteorological Agency’s updated Oct 25 forecast [LINK] for Japan winter temperatures. Unfortunately, it calls for another warmer than normal winter, and Nov thru Jan temperatures look to be well above normal. If the forecast proves accurate, it means that we wouldn’t expect to see any boost to LNG prices, at least from Japan weather. Below is the JMA temperature map for the Nov thru Jan period.

Natural Gas Production bcf/d 2015 2016 16/15 2017 17/16 2018 18/17 2019 19/18

Jan 6.584 6.162 -6.4% 5.326 -13.6% 4.910 -7.8% 4.648 -5.3%

Feb 6.676 6.122 -8.3% 5.299 -13.4% 4.853 -8.4% 4.869 0.3%

Mar 6.558 6.030 -8.1% 5.383 -10.7% 4.646 -13.7% 4.857 4.5%

Apr 6.257 5.921 -5.4% 5.334 -9.9% 4.869 -8.7% 4.816 -1.1%

May 6.202 5.841 -5.8% 5.299 -9.3% 4.827 -8.9% 4.841 0.3%

June 6.390 5.881 -8.0% 5.253 -10.7% 4.840 -7.9% 4.843 0.1%

July 6.374 5.785 -9.2% 5.216 -9.8% 4.856 -6.9% 4.892 0.7%

Aug 6.366 5.686 -10.7% 5.035 -11.4% 4.898 -2.7% 4.939 0.8%

Sept 6.477 5.619 -13.2% 4.302 -23.4% 4.913 14.2% 5.017 2.1%

Oct 6.397 5.583 -12.7% 4.759 -14.8% 4.895 2.9%

Nov 6.316 5.515 -12.7% 4.803 -12.9% 4.776 -0.6%

Dec 6.236 5.380 -13.7% 4.811 -10.6% 4.881 1.5%

Mexico natural

gas production

breaks above 5

bcf/d

Warmer start t

winter in Japan

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

8

Energy Tidbits

Figure 8: Japan Winter Temperature Forecast For Nov Thru Jan

Source: Japan Meteorological Agency

Natural Gas – China “berth” data shows LNG import data in Oct down 17.4% YoY

Notwithstanding we are more bullish on others that LNG markets rebalance sooner than expected, we have been, and continue to be, negative on LNG in 2020. This was reinforced by the Bloomberg estimated China LNG important data for Oct. On Friday morning, we tweeted [LINK] “#LNG negative tone to continue unless there is very cold start to Asian and Europe winter. Bloomberg terminal just reported on “berth” data for China LNG imports in Oct would be 5.9 bcf/d, 1st YoY decrease since July 2016. <6 bcf/d for 1st time since shoulder season Apr 2016.” There was a good Bloomberg terminal story early Friday morning “China LNG Imports Slide 1st Time in 3 Years on Outage, Stocks” reporting on “berth data” for China LNG imports in Oct. This is not the official China customs data, but we have to believe the data will be pretty accurate. Its hard to think they missed a LNG tanker, and the only variance is likely to be small ie. on the load volume. Below is our running table of China LNG imports that includes the Bloomberg berth data for Oct. Our Supplemental Documents package includes the Bloomberg terminal story.

Figure 9: China LNG imports

Source: Bloomberg, LNG World News

Natural Gas – Baker Hughes LNG supply needs to be >15% more than demand

Baker Hughes held its Q3 call on Wed and reminded of a key LNG supply/demand fundamental that tends to get overlooked – LNG markets are balanced when supply exceeds

bcf/d 2016 2017 17/16 2018 18/17 2019 19/18

Jan 3.8 5.4 39.3% 8.0 50.0% 10.2 27.1%

Feb 3.1 4.1 32.3% 6.8 66.9% 7.5 9.1%

Mar 2.6 3.1 17.7% 5.0 64.5% 6.3 24.8%

Apr 3.0 3.4 14.7% 5.4 57.8% 7.3 34.0%

May 2.2 4.5 104.5% 6.4 41.9% 6.9 7.6%

June 3.5 4.9 38.2% 6.3 30.1% 7.3 14.9%

July 2.5 4.8 95.1% 6.4 33.4% 7.6 18.1%

Aug 3.5 4.9 37.4% 7.3 49.2% 8.0 10.8%

Sept 4.1 5.5 36.8% 7.0 26.3% 8.2 16.7%

Oct 2.9 5.5 93.0% 7.1 29.6% 5.9 -17.4%

Nov 4.3 6.5 52.6% 9.6 47.5% Bloomberg Oct "berth" estimate

Dec 5.8 7.8 34.5% 9.7 25.0%

LNG supply needs

to be more than

demand

China Oct LNG

imports possibly

down 17% YoY

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

9

Energy Tidbits

demand by >15%. We tweeted [LINK] “Baker Hughes Q3 call today: Need 650 mm tons #LNG nameplate capacity for demand 550 mm tons by 2030. Fits SAF why LNG markets rebalance earlier than expected, "LNG markets reach a balance when demand is within +/- 15% of LNG supply capacity”. On the Q3 call, mgmt. said “And as you look at LNG overall, over the course of the next few years that's going to be increasing project activity you've got an outlook of the demands of 550 million tons by 2030. And to put that in perspective, you're going to need to have about 650 million tons of nameplate capacity in place to actually provide that.” Ie. 650 is 18.2% more than 550, basically in line with our +/- 15%. This was a key factor in our LNG call in our SAF Group 2020 Energy Market Outlook webcast on Oct 7. In our webcast, we said the following to the below slide “We also think there is a big factor that is overlooked by markets when they look at the math to see if LNG markets are oversupplied. Its that there needs to be more LNG capacity than LNG demand. LNG suppliers have to have some excess capacity somewhere in their supply chain to meet contract volumes. It could be extra train capacity somewhere in their portfolio, or storage or some way that they felt comfortable they could deliver the LNG volumes even with normal turnarounds and maintenance. There is no firm % but we suspect with the increasing role of spot and short term contracts, its probably something like up to 15% to provide a cushion to meet deliveries. In other words, LNG markets are effectively balanced if LNG capacity is approximately 15% greater than LNG demand+’

Figure 10: Excess Supply Capacity Is Needed To Support LNG Contract Volumes

Source: SAF

Natural Gas – Gazprom’s 8.9 bcf/d of new export pipeline to start up soon

It was a good week for Gazprom on its major new natural gas export pipelines to China and Germany. And that means it’s a bad week for LNG prices in 2020 and 2021 because Gazprom’s two new pipelines (3.6 bcf/d Nord Stream 2 to Germany and 5.3 bcf/d Power of Siberia to China) are on track to start delivering natural gas in the coming months. There isn’t yet a formal timeline to how fast the volumes will ramp up in the each pipeline, but these are significant low risk pipeline additions for incremental Russia natural gas to reach the key global natural gas markets. The developments are in line with our fear for LNG prices in 2020 and 2021, which we detailed in our March 30, 2019 blog “LNG Price Pressures

Gazprom 8.9

bcfd new

pipeline capacity

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

10

Energy Tidbits

2020/2021 With Gazprom Adding ~8.9 Bcf/D Export Gas Pipeline Capacity Into Europe And China”. Our Supplemental Documents package includes the March 30 blog. [LINK]

Denmark signs off on 5.3 bcf/d Nord Stream 2 to Germany Last week’s (Oct 27, 2019) Energy Tidbits memo (and our Oct 26 tweet [LINK]) highlighted the breaking news last weekend that Denmark approved Poland’s Baltic Pipe natural gas pipeline that runs thru Danish territorial waters very close to the Nord Stream 2 route. It proved Denmark was not anti natural gas pipelines running thru its territorial waters. And we thought that meant that Denmark would sign off on Nord Stream 2 in the very near future, within the next few months. It turns out, it was only a matter of a few days for Denmark to sign off on a route. The approval is critical as it points to Nord Stream 2 moving head. There is one key caveat- the Danish approval is still subject to a 30 day period for comment. The best timing commentary was from Russian news, Vedomosti ,who noted the day comment period, the approx. 5 weeks to completed the Danish pipeline section, and the approx. 2 months for the natural gas line fill in the pipeline (see below item on line fill) and concluded the earliest possible start date is spring 2020. We agree with that timeline assuming nothing goes awry in the 30 day comment period. Our Supplemental Documents package includes a GoogleTranslate version of the Vedmosti story. [LINK]

Figure 11: Nord Stream and Nord Stream 2 Gas Pipelines

Source: Gazprom

3.6 bcf/d Power of Siberia pipeline to China now filled up natural gas Gazprom issued a short release on Tues “Power of Siberia pipeline filled up with gas” [LINK] indicating it had completed feeding natural gas in to the 3.6 bcf/d export pipeline to China. Gazprom said “gas from the Chayandinskoye field in Yakutia has reached the near-border gas metering station in the proximity of Blagoveshchensk. Power of Siberia's linear part is thus ready for the commencement of Russian pipeline gas supplies to China. The next step is to feed gas into the transborder crossing under the Amur River.” The Amur River is at the China crossing point noted on the below map. This means that Gazprom is ready to ship natural gas to China ahead of its planned Dec 1 start date. Its not clear what the expected throughput will be in the early months of the pipeline. But Power of Siberia is a key reason why we expect LNG markets to be weak in 2020 as this is a reason why

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

11

Energy Tidbits

China’s LNG imports could show only marginal growth in 2020. Please refer to our March 30, 2019 blog “

Figure 12: Gazprom’s 3.6 bcf/d Power of Siberia Natural Gas Pipeline To China

Source: Gazprom

Natural Gas – BP says be tough to find customers for all US LNG in 2020/2021

On Tues, we tweeted [LINK] on BP Q3 call that day and their global LNG outlook that points to pressure points on HH prices in 2020 and 2021. BP went thru their global LNG/natural gas outlook of oversupply in 2020 and 2021 that noted many of our LNG market themes – Europe storage full (didn’t say because of it started with a warm Asian winter), Russia gas pipeline risk, LNG cargoes needing to find a home, but low Europe gas prices means math doesn’t work for US LNG even though US source gas is low priced. As a result, US LNG facilities may not be able to find markets for all volumes in 2020/2021. Mgmt said “We've now creates the series of export terminals and more there is still no question that United States gas is the lowest cost of production in the world. It's going to be hard for you to find a market anytime soon in the next two years, probably and you probably looking at the back end of 2021 before you start see this massive supply overhang clear out and then [ph]we of LNG projects coming on stream in Australia, Middle East and around the globe, which is simply going to exacerbate the situation”. This is the argument we have been making that Europe storage is the dumping ground for LNG cargos especially in non peak season. If Europe storage is full, LNG cargos are slowing moving looking for a home or in floating storage or export facilities work at less than capacity. If US LNG can’t export at full capacity, then the US natural gas goes into storage unless the wells get shut in. This is where there is added risk to HH gas prices as most assume that US LNG projects ship at capacity adjusted for turnarounds. We say that the gas gets produced and sent into storage because a good portion of it is associated natural gas from Permian and Eagle Ford. And that natural gas doesn’t get shut in unless you shut in the oil well especially as the associated gas is still not the significant part of the well economics. Our Supplemental Documents package includes excerpts from the BP Q3 call transcript.

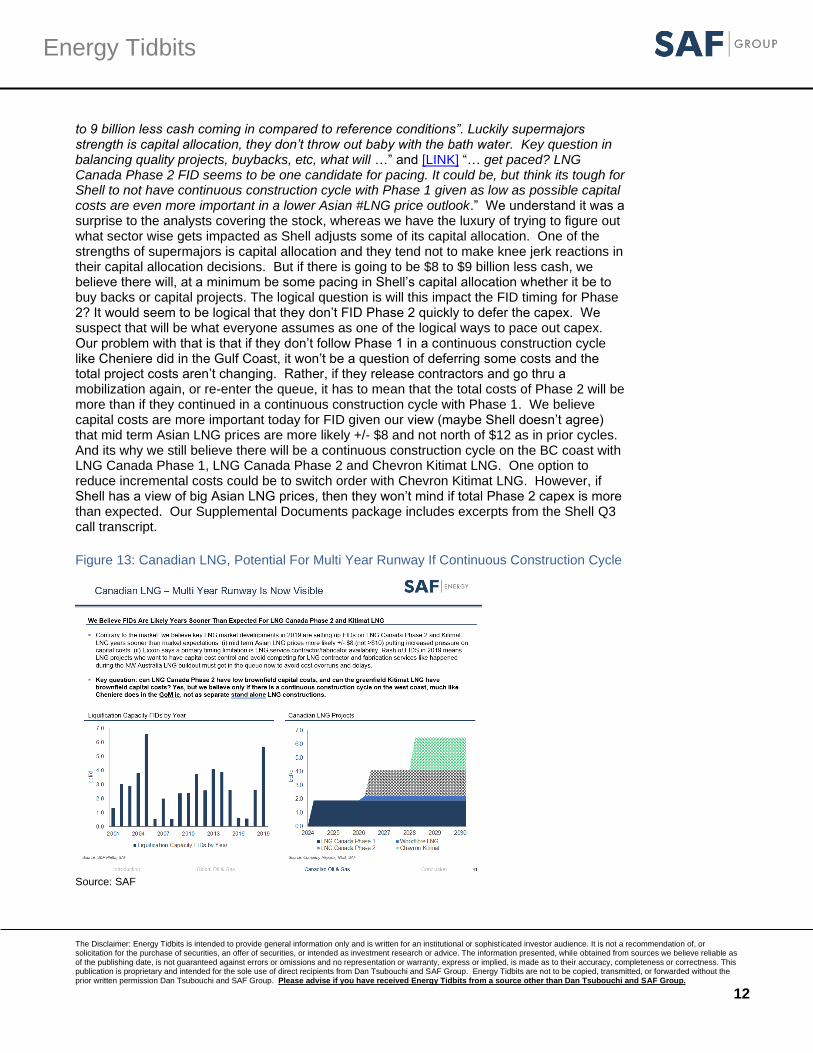

Natural Gas – Will Shell’s cash shortfall cause a delay in LNG Canada Phase 2?

Shell’s shares were down >3% following its Q3 release on Thurs morning. The headlines were similar to the FT “Shell warns economic weakness could hit investor payouts”. This was the big issue on the call for analysts. On Thurs we tweeted [LINK] “ Shell CEO on Q3 call “$8

BP sees

oversupplied

LNG market in

2020 and 2021

Risk for LNG

Canada Phase 2

delays?

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

12

Energy Tidbits

to 9 billion less cash coming in compared to reference conditions”. Luckily supermajors strength is capital allocation, they don’t throw out baby with the bath water. Key question in balancing quality projects, buybacks, etc, what will …” and [LINK] “… get paced? LNG Canada Phase 2 FID seems to be one candidate for pacing. It could be, but think its tough for Shell to not have continuous construction cycle with Phase 1 given as low as possible capital costs are even more important in a lower Asian #LNG price outlook.” We understand it was a surprise to the analysts covering the stock, whereas we have the luxury of trying to figure out what sector wise gets impacted as Shell adjusts some of its capital allocation. One of the strengths of supermajors is capital allocation and they tend not to make knee jerk reactions in their capital allocation decisions. But if there is going to be $8 to $9 billion less cash, we believe there will, at a minimum be some pacing in Shell’s capital allocation whether it be to buy backs or capital projects. The logical question is will this impact the FID timing for Phase 2? It would seem to be logical that they don’t FID Phase 2 quickly to defer the capex. We suspect that will be what everyone assumes as one of the logical ways to pace out capex. Our problem with that is that if they don’t follow Phase 1 in a continuous construction cycle like Cheniere did in the Gulf Coast, it won’t be a question of deferring some costs and the total project costs aren’t changing. Rather, if they release contractors and go thru a mobilization again, or re-enter the queue, it has to mean that the total costs of Phase 2 will be more than if they continued in a continuous construction cycle with Phase 1. We believe capital costs are more important today for FID given our view (maybe Shell doesn’t agree) that mid term Asian LNG prices are more likely +/- $8 and not north of $12 as in prior cycles. And its why we still believe there will be a continuous construction cycle on the BC coast with LNG Canada Phase 1, LNG Canada Phase 2 and Chevron Kitimat LNG. One option to reduce incremental costs could be to switch order with Chevron Kitimat LNG. However, if Shell has a view of big Asian LNG prices, then they won’t mind if total Phase 2 capex is more than expected. Our Supplemental Documents package includes excerpts from the Shell Q3 call transcript.

Figure 13: Canadian LNG, Potential For Multi Year Runway If Continuous Construction Cycle

Source: SAF

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

13

Energy Tidbits

Natural Gas – Cheniere sees better LNG markets in 2021

Cheniere held its Q3 call on Friday. (i) LNG market is “very rapidly self-correcting”. It wasn’t 100% clear from this comments and they didn’t have LNG supply/demand graph, but they seem to be saying the LNG markets get out of their oversupply situation by then end of 2020. In the Q&A, they highlighted LNG markets are “very rapidly self-correcting. They noted in the slides and comments that LNG markets are just coming thru a period of major LNG supply growth. In the Q&A, mgmt. replied “Our gas supply team takes about 5.5 Bcf of gas to our plants alone. The US is 7.5 so number one, I think we're much closer to the end of the supply of wave, obviously the question of how quickly world absorbs that is in part weather, but certainly we fully expect that the emerging markets and actually old world Europe to continue to grow and have fundamental demand growth and over to you switch off 15% of global supply is going to have quite an impact on the Henry Hub here and LNG prices globally. So we don't expect that to happen. We think it's very rapidly self-correcting and of course that the LNG world does not run off the spot spread neither physically more financially. So we think there is a good chance that we are in another nine to 12 months of a steep contango and as Michael discussed in Jack discussed earlier, we'll take advantage of that Contango and secure margins for ourselves.” (ii) We are more negative on LNG prices in 2020, but they seemed to qualify their call by adding in a bit of weather caveat. Later in the Q&A, they do a bit of a qualifier that need a decent winter, but then suggest the supply glut is gone post 2020 ie. a year or two ahead of our outlook presentation. Mgmt replied “yeah, a great question. Fair point. Right. We don't, reset to zero and have Europe able to grow from this base by another 20 million tonnes plus that's very fair point. One of the things that has played out is fewer lower volumes on pipes, as a function of North African and European supply Norway has been down pretty significantly. We need a winter cleans us out faster. We have had very robust demand growth on the Power Gen side. So that is something that is not dependent on seasonality and it's back half of 2019 weighted as everything was put in place and as Europe continues to grow that demand function. So all of those health again 2020 will be a very big supply year right, there is no question big supply year on a run rate basis and of course you get the full year effect of the 40 million tonnes coming on in 2019. So we are -- not as you can tell we're not that optimistic on 2020 hence as as Michael said, we've got more or less everything we can have put away for the way. My point is that that's beyond 2020 there really is no meaningful supply it's literally a couple of trains for a number of years with most of those being our trains. So, fairly confident that 2020 is the, transition year and 21 through 23 look much better.” (ii) One trend we have to watch (and one that is a logical negative) to the LNG supply call is the view that LNG facilities can produce above nameplate capacity. We have noted this specifically in Exxon’s Papua New Guinea, but Cheniere talks about adding capacity by debottlenecking. This makes sense, why shouldn’t LNG facilities be like refineries or other plants. The negative is that it means that we wouldn’t need some of the excess capacity that we say is needed to meet demand. IN the outlook presentation, we put that LNG markets are balanced when LNG demand is within +/- 15% of LNG supply capacity. In the Q&A, mgmt. replied “Yeah, I do think having worked closely with the operational team recently on our debottlenecking initiatives. I think the debottlenecking plan that they've put before us for some additional capital, we could achieve over 5 million tonnes. If necessary, but I think what you're hearing from Michael is we're trying to do all of the low hanging fruit first, due to the debottlenecking that gets us as much LNG as we possibly can without having to invest large quantities of capital.” Our Supplemental Documents package include excepts from the Cheniere Q3 call and Q3 call slide deck.

Oil – US oil rigs down 5 to 691 oil rigs

Baker Hughes reported its weekly rig data on Friday which was positive for WTI. US oil rigs were down again this week, with a decrease of 5 to 691 oil rigs as of Nov 1. There were no

US oil rigs

were -5 this

week

Cheniere sees

better LNG

markets in 2021

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

14

Energy Tidbits

increases this week, and decreases were in Others -2, Permian -1, Mississippian -1, and Granite Wash -1. Major US service companies have been reporting Q3 earnings over the past two weeks, and the general consensus is for drilling activity to move lower and reach a bottom in Q4, and then modestly increase in Q1 with fresh 2020 budgets. Below is our graph of total US oil rigs.

Figure 14: Baker Hughes Total US Oil Rigs

Source: Baker Hughes

Oil – Total Cdn rigs -5 to 142 total rigs

Baker Hughes reported total Cdn rigs were -5 to 142 total rigs as of Nov 1. Cdn oil rigs were down 9 to 93 Cdn oil rigs. Cdn gas rigs were up 4 to 49 gas rigs with the higher AECO spot prices. Alberta rigs were up 2, BC rigs were up 1, and Sask was down 7. Cdn rigs are now -2 compared to where they were a month ago at 144 total rigs. Despite the decrease this week, Cdn rigs are close to where they should be at this time of year – normally relatively flat going into the winter drilling season. The feedback is unchanged – producers are going to be very careful with capex spending in Q4/19 given the continued weak share prices and no real access to equity. The expectation is that we will have an earlier and extended Xmas break for drilling compared to prior years.

Figure 15: Baker Hughes Total Canadian Oil Rigs

Source: Baker Hughes

Oil – US oil production unchanged at 12.6 mmb/d, matching the all time high

EIA reported US oil production was unchanged at the all time high of 12.6 mmb/d for the Oct 25 week. Lower 48 production was also unchanged at the all time high of 12.1 mmb/d. US oil production has been unchanged for 4 weeks now, but should continue ramping up with the new Permian egress that has come onstream in H2/19, and should continue increasing in Q4 to the EIA’s forecast of 12.87 mmb/d which is 270,000 b/d above the current production level. Below we pasted an excerpt from the EIA weekly oil production data. [LINK]

US production

at 12.6 mmb/d

Total Cdn rigs -5

this week

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

15

Energy Tidbits

Figure 16: Weekly US Oil Production

Source: EIA

Figure 17: US Weekly Oil Production

Source: EIA, SAF

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

16

Energy Tidbits

Figure 18: YoY Change in US Weekly Oil Production

Source: EIA, SAF

Oil – EIA Form 914, US Aug oil production up vs July, rebound after Hurricane Barry

The EIA released its Form 914 data [LINK] on Thursday, which is the EIA’s “actuals” for Aug US oil and natural gas production. The headline was that US oil production was up 600,000 b/d in Aug vs July, but the big increase is due to a rebound in Gulf of Mexico oil production following the Hurricane Barry shut in during July. Form 914 shows Aug of 12.365 mmb/d, up 599,000 b/d vs July of 11.766 mmb/d for the US in total, but also shows GoM was +469,000 b/d to 2.006 mmb/d in Aug vs 1.537 mmb/d in July. Putting the GoM variance aside, US oil production was +305,000 b/d in Sept vs June (pre-Hurricane Barry) which represents very strong growth, considering the average 2019 MoM increases up to June was just +41,000 b/d. Below is the EIA Form 914 data for oil, and our graph of

Figure 19: EIA Form 914 US Oil Production

Source: EIA

Figure 20: EIA Form 914 US Oil Production vs Weekly Estimates

Source: EIA

U.S. Total Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2019 11,856 11,669 11,892 12,123 12,113 12,060 11,766 12,365

2018 10,018 10,281 10,504 10,510 10,460 10,649 10,891 11,361 11,498 11,631 11,999 12,038

2017 8,863 9,103 9,162 9,100 9,183 9,107 9,235 9,248 9,512 9,653 10,071 9,973

2016 9,197 9,056 9,089 8,869 8,823 8,654 8,646 8,676 8,534 8,834 8,897 8,798

2015 9,383 9,507 9,585 9,655 9,474 9,354 9,442 9,415 9,478 9,396 9,322 9,263

2014 8,072 8,152 8,291 8,522 8,644 8,747 8,846 8,914 9,078 9,256 9,317 9,561

2013 7,081 7,147 7,203 7,371 7,325 7,276 7,523 7,531 7,836 7,757 7,916 7,928

Notes: The sum of individual s tates may not equal tota l U.S. volumes due to independent rounding. A zero may indicate volume of less

than 0.5 thousand barrels per day. Previous months ' production volumes may have been revised for a l l s tates/areas .

US Aug oil

production up

post Hurricane

Barry

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

17

Energy Tidbits

Oil – Permian base oil decline rates around 40%

We continue to recommend investors look to the Q&A section of oil earnings calls for typically is the best insight and often unplanned insight. As noted below, one of our key calls from our Oct 7 webcast detailing the SAF Energy Outlook is that it was inevitable for analysts and agencies to lower their Permian oil growth forecasts for 2020, which means that US oil growth forecasts are also lowered. Our thesis is that all forecast models use the same basic inputs and that the math problem is because every input into their Permian oil growth equations are worse (lower) today than at the beginning of the year. The starting point for Permian oil growth forecasts is base decline rate. As a general rule, the US players do not disclose base decline rates, but no so this week. The challenge is that higher decline rates mean more oil production has to be added every year just to keep production flat. Our webcast slide (see below) included some excellent work from BTU on play overall base declines and it looks like the BTU estimates are being validated by the Q3 calls. BTU estimated the base Permian oil decline was in the high 30’s. Our last comment on base decline rates is that we recall how Cdn oil producers used to be hammered by investors if their oil base decline rates were over 30%. A base decline of ~40% is supportive of why we believed US oil growth rates would be lowered.

Concho’s Permian base oil declines in low 40’s but to 30’s at yr end 2020 On Wed, we tweeted [LINK] on the Concho Resources Q3 call was on Wed. Recall Concho stock was hammered after the Q2 reporting when it advised it’s downspacing wasn’t’ working and they would have to move to wider spacing. This followed the Q1 reporting that had the initial producing rates showing good rates, but markets learned the reminder that you need to get past the first 60 to 90 days to see how good the wells will be. This week, Concho’s move to a more conservative model (wider well spacing, less aggressive drilling, moving to free cash flow, etc) was leading to more predictable results going forward. In the Q3 call Q&A, mgmt. replied “Sure. Yeah, the our overall base decline is in the high 30s and oil is in the low 40s and as we move through 2020 and move into 2021, we see that oil declined moving back into the 30s.” We believe the vast majority of CEOs would say a 40% base decline is a big challenge for any oil producer to deliver sustainable, significantly oil growth. Matador says they have a 38% to 40% base Permian oil decline rate On Thurs, we tweeted [LINK] on the Matador Rsources Q3 call on Wed. Matador hasn’t had the same issues as Concho and is actually increasing intis production guidance. However, Matador also confirmed its estimate of base Permian oil decline rates as being 38% to 40%. In the Q&A, mgmt. replied ““Well, I think is we've answered that question in the past. I said, I think for 2019, the base decline was 38% to 40%, and that for the company as a whole and I would help and that would continue to shallow as we become a more mature organization, and also I do think that as we drill more of the longer laterals. I think that our observation has been that those wells tend to exhibit a bit shallower declines early. And so as a result, I'm hopeful that will also contribute to the improvement in the base decline rate going forward”

Permian base decline ~40%

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

18

Energy Tidbits

Figure 21: Increasing Permian Decline Rates

Source: SAF

Oil – More pointing to lower US oil growth in 2020

Last week’s (Oct 27, 2019) Energy Tidbits memo started to group the increasing number of of analyst forecasts and industry comments calling for, or point to, a lowering of US oil growth in 2020. This is in line with our expectations this summer, although we had expected analysts to lower the US oil growth forecasts after Labor Day and not necessarily wait until the Q3 reporting period. Soon we will not be able to say this is a lowering of US oil growth expectations because it seems like almost everyone is lowering US oil growth forecasdts. This was one of our major themes in our recent Oct 7, 2019 SAF Energy Outlook, we highlighted our view that the math says it is inevitable for agencies and analysts to lower their Permian growth forecasts and therefore their US oil growth forecasts for 2020. To be clear, we still see Permian growth, just at a lot lower rate. Anyone with a detailed model for estimating Permian oil growth has to include at least these basic inputs into their equation - Annual decline rates on the existing production base ie. how much production needs to be added to stay flat. how much capital is available, to fund drilling and completion of new wells, and for completion of the inventory of DUCs. to add production based on the well productivity rates. We think the math problem comes about because every input into this Permian oil growth equation is worse now. A big one is how capital available for producers is less. Its not just the lower well productivity rates, its all of these inputs into any model are worse so we think it is inevitable that Permian (and therefore total US) oil growth forecasts have to be lowered. And we believe a lowering of US oil growth forecast will be the key driver to a change in market sentiment to oil. Here are some of this week’s views/forecasts calling for lower US oil growth in 2020.

Baker Hughes sees decelerating growth in US oil production Baker Hughes held its Q3 call on Wednesday and noted its view on decelerating US oil production growth. Baker Hughes didn’t give a forecast for US oil growth, rather they just noted that its decelerating. In the Q3 earnings call, mgmt. said “On the supply side, we agree with the view that OPEC may have to consider additional cuts as non-OPEC non-US production at is poised for solid growth in 2020 as new

More calling for lower 2020 US oil growth

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

19

Energy Tidbits

offshore developments come online. In the US production growth is likely to decelerate it should remain resilient despite the expectation of E&P CapEx cuts next year when these factors together we expect an adequately supplied market and the most economic scenarios, resulting in the range bound oil price environment 2020”. BoA/Merrill expect to lower their +800,000 b/d US oil growth in 2020 On Tues, we attended an excellent presentation BoA/Merrill “Global Energy Outlook” presentation by Dr. Francisco Blanch (Head of Global Commodities and Derivatives Research). During the presentation, he said “for US supply growth, we are at 800,000 b/d for next year but maybe we are too high. we are waiting for q3 reporting for US producers to finish”. In the short q&a, I confirmed what he said that they were currently at +800,000 b/d for 2020 US oil growth, they are looking to lower the growth forecast, and that they are looking for what they see on capital allocation ie. the keeping to free cash flow models before making any adjustment. I asked on if lower well productivity was a factor in why they are expecting to lower US oil growth or just the capital allocation item. He said that they are seeing well productivity gains come down, but still are assuming 5% to 10% gains in well productivity. Ie. the reduction in growth will be driven by capital allocation. Our Supplemental Documents package includes the notes we took of the slide deck. Chevron and Exxon buck the trend, both delivering on Permian growth plans We didn’t get a chance to write up the Exxon and Chevron Q3 calls this week, but the main message from both was that they are on track with their Permian growth plans. We remind that Chevron and Exxon only make up about 15% of total Permian oil production so they can’t carry the Permian oil growth by themselves. Liberty Oilfield says “we may see US oil production plateau in early 2020” This week, we saw the most pessimistic call so far on US oil growth in 2020 from the Liberty Oilfield services Q3 call on Wed. On Wed, we tweeted [LINK] “Big plus for #Oil in 2019 if Liberty Q3 call views are right, “rate of growth in US oil production has also declined significantly. With this trend, we may see US oil production plateau in early 2020” #OOTT More in Sunday Nov 3, 2019 Energy Tidbits memo”. If this view plays out, it will more than tighten the market. This has been the most pessimistic call we have seen so far on US oil growth. In the prepared comments, mgmt. said “The US rig count has declined roughly 20% over the last year not surprisingly, the rate of growth in US oil production has also declined significantly. With this trend, we may see US oil production plateau in early 2020, which could help tighten oil markets and provide upward bias on oil prices. While timing is uncertain, we appear to be making progress towards a healthier US oil and gas industry as supply of frac fleets in Oil are both facing significant downward pressure”. US Silica Q3 – Taking out capacity, points to lesser US oil growth potential US Silica reported Q3 earnings on Thursday, and mgmt. comments supports the view of lower US growth. Similar to other service companies, they are taking out capacity, which points to the view that there is lesser oil growth potential than previously expected. Less capacity shouldn’t impact 2020 very much, but less service sector capacity means less ultimate growth potential. US Silica reduced frac sand capacity by 5 million tons, but the reduction was in the traditional Northern White mines and not the Permian. Mgmt said “We've been effectively executing all year on our playbook for capacity management, over the past few months we've taken approximately 5 million tons of Northern white and regional sand capacity

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

20

Energy Tidbits

offline through a combination of reducing hours worked for completely idling plants are also increasingly coupling sandbox our industry-leading last mile full service logistics solution with US special sand with a goal of doubling company directs and sales to the well site blender to 20% of overall sand sales”. This is what we would have expected, ie. the more likely reductions are first in Northern White as opposed to local Permian, as local Permian has lower transportation costs. Ultimately, this commentary fits our view of lower US oil production growth and is similar to other service companies reducing drilling and frack capacity, reduced capacity means lower than expected forecasts for US oil growth.

Oil – Trans Mountain and contractors have hired 2,200 people

Last week, we noted Trudeau’s clear comments that TMX is continuing, and this week brought another positive for the Trans Mountain expansion. On Monday, JWN Energy [LINK] reported that Trans Mountain and its have hired more than 2,200 people for the project. JWS quoted Trans Mountain saying “As of September 30, Trans Mountain and our contractors have hired more than 2,200 people for the Project, with a focus on Indigenous, local and regional workers … This includes heavy equipment operators, trades people, environment and safety roles, engineers and construction managers”. We see this as a big positive for the project, especially with the hiring of heavy equipment operators, trades and construction managers.

Oil – Reports Keystone shut in for another week or so

As of our news cut off of 8am MT today, Keystone has not posted an update on its Edinburgh Incident website [LINK] since Oct 31 at noon MT, which was “Our on-site team is focused on responding to the release and has begun recovering oil, using specialized equipment. The approximate size of the impacted area is 2,500 yd2 or less than half the size of a football field. We continue to inform regulatory agencies and local stakeholders of our progress. We have provided an initial estimate that 9,120 barrels of oil was released; approximately half the size of an Olympic-sized swimming pool. Our crews remain focused on oil recovery as they plan to make repairs to the pipeline. We will provide updates as they become available.” However on Friday, Bloomberg terminal reported “TC Energy’s Keystone oil pipeline is expected to be down for between 7 to 12 days from Friday, pending a full excavation of the area around the leak in North Dakota, according to people familiar with the matter. * Bulk of excavation work set to this weekend * Timeline could change depending on what is found during excavation, people say”. Keystone’s capacity is 590,000 b/d.

Oil – Alberta provides curtailment relief for crude by rail volumes

This week, the Alberta gov announced [LINK] it will allow companies to exceed oil production limits if they ship the incremental production by rail. This move was expected, and in our Sept 22, 2019 Energy Tidbits memo we said [LINK] “This move seems likely given the fact that Alberta is attempting to offload the crude by rail contracts signed by the NDP government. Our assumption is that large producers weren’t interested in taking on crude by rail contracts without the ability to ramp up production due to curtailment”. In the announcement, AB Energy Minister Savage said “The special allowance program will protect the value of our oil by ensuring that operators are only producing what they are able to move to market. Pipeline delays ultimately have constrained market access and dampened investment in our oil sector. This program will lead to more production and increased investment, benefitting industry, our province’s bottom line, and, ultimately, Alberta taxpayers”. The WCS-WTI differential is ultimately a driver for CBR volumes, and the diff was $21.50 as of Friday, which puts crude by rail in the money. Note, the special allowance

Trans Mountain

has hired 2,200

people

AB gov

provides curtail

relief for CBR

Keystone shut

in for another

week or so

The Disclaimer: Energy Tidbits is intended to provide general information only and is written for an institutional or sophisticated investor audience. It is not a recommendation of, or solicitation for the purchase of securities, an offer of securities, or intended as investment research or advice. The information presented, while obtained from sources we believe reliable as of the publishing date, is not guaranteed against errors or omissions and no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This publication is proprietary and intended for the sole use of direct recipients from Dan Tsubouchi and SAF Group. Energy Tidbits are not to be copied, transmitted, or forwarded without the prior written permission Dan Tsubouchi and SAF Group. Please advise if you have received Energy Tidbits from a source other than Dan Tsubouchi and SAF Group.

21

Energy Tidbits

takes effect in December. Below is the WCS-WTI differential graph, and our Supplemental Documents package includes the Alberta announcement.

Figure 22: WCS-WTI Differential

Source: Bloomberg

Oil – Oil input into refineries up 133,000 b/d to 15.998 mmb/d

For the Oct 25 week, EIA estimates crude oil inputs to refineries were up 133,000 b/d to 15.865 mmb/d. Overall crude inputs are now 419,000 b/d lower YoY, which is largely driven by PADD 3 refinery maintenance, along with the closure of the PES Philadelphia refinery complex (335,000 b/d) following the Q2 fire. Without the PES refinery fire, crude inputs would have been -84,000 b/d YoY which is reasonable considering the higher than usual refinery maintenance in preparation for IMO 2020. We would expect to crude inputs to rise higher as we move into year end. Refinery utilization was up 2.5% this week to 87.7%. Below is our graph of the EIA weekly crude oil input to refineries.

Figure 23: US Refinery Crude Oil Inputs (thousand b/d)

Source: EIA, SAF

Oil – US “NET” oil imports up 1.196 mmb/d to 3.370 mmb/d