encouraging inclusive growth through … · • national strategic policy aims for the government...

TRANSCRIPT

Ferry Irawan

Directorate of Regional Economic

and Real Sector Development

ENCOURAGING INCLUSIVE GROWTH

THROUGH INNOVATIVE

INFRASTRUCTURE FINANCING FOR

REGIONAL DEVELOPMENT

NATIONAL AND REGIONAL ECONOMIC UPDATE,

2nd Quarter of 2018

Executive Summary

2nd Quarter-2018 Economic Update

Economic Diversification Through Downstream Process of Agricultural/Plantation and Tourism Sector in North Sumatera

Analysis of Agricultural Sector Development inSouth Sulawesi

Policy Direction

OUTLINE

2

Executive Summary

3

• Amidst the heightened global economic uncertainty, Indonesia’s economic growth

in 2nd quarter of 2018, has increased to approximately 5,27% (y-o-y). From

expenditure side, economic activity showed increase in most of sectors except

Gross Fixed Capital Formation (PMTB) caused by the completion of most of the

infrastructure projects.

• One of Indonesia’s economic growth challenges is how to improve the growth and

to reduce inequality (within and between regions).

• By sector, the contribution of agriculture and industrial sectors need to be

optimized. Meanwhile spatially, Java Island remains as the main contributor of

national economic growth.

• Quantitatively, Bappenas Inclusive Economic Index indicated that economic

development at provincial level are very diverse, and mostly are below the national

level.

• National Strategic Policy aims for the Government Policy Packages (Paket

Kebijakan) such as infrastructure development, strengthening the competitiveness,

strengthening the economic zone, tourism zone development in all of Indonesia

regions with supported by economic equality policy.

• In order to boost economic inclusive growth, National Policy needs to be synergizedwith the program innovations and the financial sources of regional government.

4

5

Economic Update

Second Quarter-2018

5.148.71

5.26 5.87 7.7

15.17

55.43

1.21

8.5

31.15

20.35 20.87

Householdconsumption

Non profit institutionserving household

Governmentexpenditure

Gross fixed capitalformation

Export Import

Growth Share

Economic Growth 2nd Quarter - 2108

5.54 5.59 5.52 5.58

5.124.94 4.93

5.05

4.82 4.74 4.77

5.17

4.92

5.185.01 4.94 5.01 5.01 5.06

5.195.06

5.27

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2013 2014 2015 2016 2017 2018

5.075.034.885.015.56 5.17

GDP based on Expenditure 2nd Quarter-2018 (%yoy)

Source : BPS (2018) 6

Amidst the heightened global economic uncertainty, the

growth of Indonesian economy increased approximately 5,27% (yoy) for Q2 2018

• Expenditure side of 2nd quarter of 2018 IndonesianEconomy was driven by the growth of HouseholdConsumption, Government Expenditure and Export.

• Household and government consumptions growth hasincreased, affected by holiday allowance (THR) andgovernment expenditure such as international sport eventpreparation (Asian Games 2018) and social assistancespending.

• The growth of export sector is positive, but lower thanimport. The increase in export occurred in Java andSumatera area due to higher CPO Price. However, the rawmaterial import also increased in order to supportmanufacture industry and infrastructure project.

• Investment performance slowed down because of:

• The completion of ongoing infrastructure projectswithout additional new projects on the pipeline

• Momentum of rising commodity price utilized bycorporation to invest in 2017 and part of 2018

12.80

13.00

13.20

13.40

13.60

13.80

0.00

1.00

2.00

3.00

4.00

5.00

2011 2012 2013 2014 2015 2016 2017 2018TW 2

Growth (C to C, %) Share (%)

Agriculture, Forestry, Fishery

18.00

19.00

20.00

21.00

22.00

0.00

2.00

4.00

6.00

8.00

2011 2012 2013 2014 2015 2016 2017 2018TW 2

Growth (C to C, %) Share (%)

Manufacture

0.95

1.00

1.05

1.10

1.15

1.20

1.25

0.00

2.00

4.00

6.00

8.00

10.00

12.00

2011 2012 2013 2014 2015 2016 2017 2018TW 2

Growth (C to C, %) Share (%)

Gas and Electricity

Construction

8.00

8.50

9.00

9.50

10.00

10.50

0.00

2.00

4.00

6.00

8.00

10.00

2011 2012 2013 2014 2015 2016 2017 2018TW 2

Growth (C to C, %) Share (%)

Source : BPS (2018)

12.60

12.80

13.00

13.20

13.40

13.60

13.80

0.00

2.00

4.00

6.00

8.00

10.00

12.00

2011 2012 2013 2014 2015 2016 2017 2018TW 2

Growth (C to C, %) Share (%)

Wholesale and Retail Trade

2.60

2.70

2.80

2.90

3.00

3.10

0.00

2.00

4.00

6.00

8.00

2011 2012 2013 2014 2015 2016 2017 2018TW 2

Growth (C to C, %) Share (%)

Food Beverage and Accommodation

The growth of accommodation, food and beverage and trade sectors in the 2nd quarter of 2018 has increased

along with holiday season (school and Eid holiday)• Meanwhile, the growth of manufacturing industries had not increase significantly

• Agriculture sector performance indicating improvement since lower commodity price era in 2014. In addition, the growth in the second quarter was resulted by harvest timethat shifted earlier and also favorable weather.

• The rising domestic demand boosted the acceleration in business activities, while, manufacturing industries and construction sector distribution had not showedimprovement yet /declined because of commodity price recovery and reducing working day during religious holiday (lebaran).

7

Inter-regional Development Discrepancy and Inequality of Income Distribution… poor population in rural area are about 13.20% while 7.02% in urban area

• Poverty in urban and rural area had different characteristics, however with different poverty

line between urban and rural area, there were more poor population in the rural area.

• Comparing inter-regional data, we found inequality of social development between west

and east area. The poverty in east area of Indonesia was higher than west area, especially

in rural area such as Bali-Nusra and Maluku-Papua.

• Gini Ratio has been increasing from 0.376 in 2007 to 0.389 in 2018.

Source: BPS 8

0.401

0.324

0.389

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Indonesian Gini Ratio by Residence

Urban Rural Ur and Rural

8.656.82

4.335.83

9.18

5.037.02

11.6612.81

7.6

13.68

17.77

29.15

13.2

Sumatera Java Borneo Sulawesi Bali-Nusra Maluku-Papua Indonesia

Percentage of poor population by Island

Urban Rural

6.5

5

5.9

7

5.9

4

5.9

3

5.9

0

5.8

5

5.7

7

5.6

5

5.6

1

5.5

7

5.5

3

5.4

7

5.4

6

5.4

2

5.4

1

5.4

0

5.3

9

5.3

7

5.3

3

5.2

6

5.2

1

5.2

0

5.1

9

5.1

7

5.1

5

5.1

2

5.1

1

5.0

3

5.0

0

4.9

7

4.9

5

4.9

1

4.8

8

4.6

4

3.7

0

DK

I Jak

arta

Jaw

a Te

nga

h

DI Y

ogy

akar

ta

Bal

i

Jaw

a B

arat

Kep

ula

uan

Ria

u

Jaw

a Ti

mu

r

Sula

wes

i Uta

ra

Sum

ate

ra U

tara

Kep

ula

uan

Ban

gka…

Kal

iman

tan

Sel

atan

Ind

on

esia

Sula

wes

i Sel

atan

Sum

ate

ra B

arat

Sum

ate

ra S

elat

an

Kal

iman

tan

Tim

ur

Lam

pu

ng

Ban

ten

Kal

iman

tan

Te

nga

h

Ria

u

Kal

iman

tan

Uta

ra

Ben

gku

lu

Go

ron

talo

Sula

wes

i Ten

ggar

a

Sula

wes

i Ten

gah

Ace

h

Jam

bi

Nu

sa T

engg

ara

Bar

at

Sula

wes

i Bar

at

Kal

iman

tan

Bar

at

Mal

uku

Uta

ra

Mal

uku

Pap

ua

Bar

at

Nu

sa T

engg

gara

Tim

ur

Pap

ua

• Notes: values 1-3 are “unsatisfied” categories values 4-7 are “satisfied” categories and values 8-10 are “very satisfied”

categories. Calculation of the Inclusive Economic Development Index based on economic growth, income distribution and

poverty reduction and expansion of access and opportunity

Source: Bappenas (2018)

National Inclusive Economic Index is 5.47• Some provinces had Inclusive economic development index below the national level

• Since the number of poverty is still high it creates the low rate of Inclusive economics index.

9

Economic Diversification

through Downstream

Processing of Agriculture/

Plantation and Tourism

Sectors in North Sumatera

10

Description2017 2018 Share

Q1 Q2 Total Q1 Q2

Household Consumption 5.63 5.51 5.12 4.98 6.64 53.93

Non Profit Institution Serving Household 3.96 3.70 3.26 7.06 11.10 0.96

Government Expenditure 4.63 4.54 5.77 6.26 5.25 7.46

Gross Fixed Capital Formation 4.02 4.73 5.91 6.96 7.37 31.06

Export 1.32 -2.74 6.34 -0.08 5.38 35.51

Import 2.01 -4.92 6.65 0.88 9.95 30.59

Intraregional Net Export -135.53 -41.23 -81.72 -197.29 -52.38 0.00

GRDP 4.53 5.14 5.12 4.73 5.30 100.00

North Sumatera Economic Growth in 2nd quarter – 2018 is 5,30% (yoy), higher than previous quarter in 2017… The growth in second quarter of 2018 is driven by consumption and export performance improvement

• Non profit institution serving household grows 11,10%, increased significantlycompared to previous quarter inline with gubernatorial election in NorthSumatera.

• Export performance grows 5,38% (yoy), improved compared to the first quarterdue to the increase in chemical products (HS 38) commodity exports.

• In addition, there are market diversification of CPO commodity export (HS 15), andit can prop the sharp decline of CPO export after protectionism policy from tradingpartner like India.

• The unstable condition of world CPO Price could potentially become an obstaclefor export performance in second quarter -2018.

• Need to focus on the high rate of import especially for fuel oil. The import growthof North Sumatera could be higher than National level.

Source : BPS

GRDP based on Expenditure 2nd Quarter - 2018 (%yoy)

11

5.30

2014 2015 2016 2017 TW I-2018 TW II-2018

North Sumatera and National Economic Growth, % (yoy)

Indonesia North Sumatera

-30 -20 -10 0 10 20 30 40 50

Coffee, tea, mate and spices (09)

Organic chemicals (29)

Chemical products (38)

Rubber and articles thereof (40)

Animal or vegetables fats and oils and theircleavage products (15)

Main export commodity of North Sumatera (Jan-June 2018)

Share Growth

Description2017 2018

ShareQ1 Q2 Total Q1 Q2

Agriculture, Forestry, and Fishery 2.22 3.97 5.31 3.25 5.02 20.82

Manufacture 3.34 4.11 2.31 2.52 3.50 20.18

Construction 5.21 5.88 6.79 6.87 5.95 13.64

Wholesale and Retail Trade 7.16 6.44 5.87 5.66 6.02 18.43

Transportation and Warehousing 7.79 7.78 7.35 7.48 6.78 5.06

Gross Domestic Product 4.53 5.14 5.12 4.73 5.30 100.00

• The ongoing harvest of the food crops and horticulture sub-sectors and theend of the oil palm track season are the driving factors for improving theperformance of the agricultural sector.

• The annual plantation sub-sector has shared 45% for agricultural sector. Themain commodity in this subsector is oil palm.

• Several risk factors that need to be anticipated related to oil palm, i.e.: tariffbarriers in major export countries, non-tariff barriers such asenvironmental, health and social issues.

• It is necessary to measure the impact of these risks and its mitigation,especially the diversification of other sectors as well as tourism.

North Sumatera

Riau

South Sumatera

26%

16%

9%

On the production side, economic growth is driven by agriculture, forestry and fishery sectors’ improvement… these sectors grow 5,02% (yoy) boosted especially by increasing oil palm production

Source : Agriculture Ministry

Spread of Palm Oil Production 2017

GRDP based on Business Activity in 2nd Quarter-2018 (%yoy)

Source : BPS

12

0

1

2

3

4

5

6

7

2016 2017* 2018**

Mill

ion

s

Palm Oil Production based on Business Status (Ton)

Smallholder plantations State owned companies private companies

North Sumatera’s investment realization in 2nd quarter of 2018 declined by 22.76% and is lower compared to the previous quarter at the same time.

• In general, the realization of North Sumatra investment was thesecond largest after South Sumatra during the 2nd quarter of 2018 inthe Sumatera Island.

• However, investment growth in North Sumatra in Q2 2018 decreasedby 2.92% (qtq) compared to the previous quarter and fell to 22.76%compared to the same quarter in the previous year (yoy).

• The decline was driven by a decrease in the role of FDI in theinvestment of food, electricity, gas, and water. Foreign investmentgrowth contribution dominated the total investment in North Sumatra

• During the first semester of 2018 it was recorded the composition ofdomestic investment dominated by the food industry, while for foreigninvestment in the electricity, gas, water and mining sectors.

Source : BKPM (2018)

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

I II III IV I II III IV I II III IV I II

2015 2016 2017 2018

Bill

ion

s ID

R

Domestic Investment Update in North Sumatera

-

100

200

300

400

500

600

700

I II III IV I II III IV I II III IV I II

2015 2016 2017 2018

Mill

ion

s U

$

Foreign Investment Update in North Sumatera

13

Rubber industries 8%

Pulp and paper industries

7%

Basic chemical, chemical and

pharmaceutical industries

8%

Basic Metal, Metal Goods, Machinery

and Electronics Industries

6%

food industries44%

Constructions9%

Domestic Invesment (Jan-June 2018)

Mining33%

Food crops and plantations

15%Food Industries

6%

Electricity, Gas and Water34%

Foreign Invesment (Jan-June 2018)

14

5.61 5.47

DK

I Jak

arta

Jaw

a Te

nga

h

DI Y

ogy

akar

ta

Bal

i

Jaw

a B

arat

Kep

ula

uan

Ria

u

Jaw

a Ti

mu

r

Sula

wes

i Uta

ra

Sum

ater

a U

tara

Kep

ula

uan

Ban

gka…

Kal

iman

tan

Sel

atan

Ind

on

esia

Sula

wes

i Sel

atan

Sum

ater

a B

arat

Sum

ater

a Se

lata

n

Kal

iman

tan

Tim

ur

Lam

pu

ng

Ban

ten

Kal

iman

tan

Ten

gah

Ria

u

Kal

iman

tan

Uta

ra

Ben

gku

lu

Go

ron

talo

Sula

wes

i Te

ngg

ara

Sula

wes

i Te

nga

h

Ace

h

Jam

bi

Nu

sa T

en

ggar

a…

Sula

wes

i Bar

at

Kal

iman

tan

Bar

at

Mal

uku

Uta

ra

Mal

uku

Pap

ua

Bar

at

Nu

sa T

en

ggga

ra…

Pap

ua

North Sumatera’s Inclusive Economic Development Index was 5.61, higher than National which was 5,47… North Sumatera index for 1st pillar was lower than Indonesia level.

• Notes: values 1-3 are “unsatisfied” categories values 4-7 are “satisfied” categories and values 8-10 are “very satisfied” categories. Calculation of the

Inclusive Economic Development Index based on economic growth, income distribution and poverty reduction and expansion of access and opportunity

Source : Bappenas (2018)

5.17

5.12

Indonesia North Sumatera

1st Pillar : Economic Growth

6.64

6.96

Indonesia North Sumatera

2nd Pillar: Income Equality and Poverty Reduction

5.05

5.42

Indonesia North Sumatera

3rd Pillar: Improving Access and Opportunity

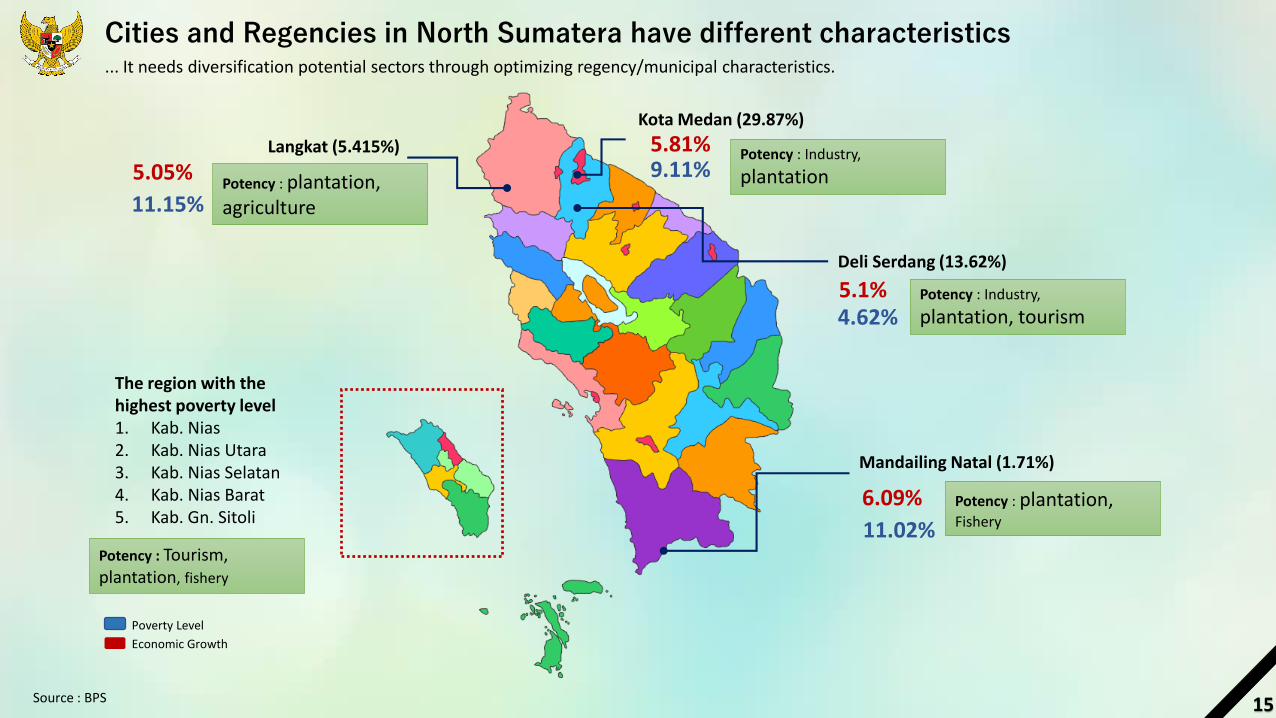

Kota Medan (29.87%)

Deli Serdang (13.62%)

Langkat (5.415%)

Mandailing Natal (1.71%)

6.09%

5.81%

5.1%

5.05%

The region with the highest poverty level1. Kab. Nias2. Kab. Nias Utara3. Kab. Nias Selatan4. Kab. Nias Barat5. Kab. Gn. Sitoli

9.11%

4.62%

11.15%

11.02%

Cities and Regencies in North Sumatera have different characteristics... It needs diversification potential sectors through optimizing regency/municipal characteristics.

Economic Growth

Poverty Level

Source : BPS

Potency : Industry,

plantation

Potency : Tourism, plantation, fishery

Potency : Industry,

plantation, tourism

Potency : plantation, agriculture

Potency : plantation, Fishery

15

Notes :

• Quadrant 1 : Commodities that include in the superior category are the commodity that have both of backward and forward linkage value more than 1.

• Industries related their development: restaurants, food and beverage industry, and construction.

• Quadrant 2 : Commodities that include in this potential category are the commodities that havebackward linkage more than 1 and forward linkage less than 1.

• This quadrant is potential input supply for the other sectors, i.e. food oil industry and rubber industry.

• Quadrant 3: Commoditites that include in this potential category are the commodities that have backward linkage less than 1 and forward linkage more than 1.

• This quadrant is output market that potential for the other sectors, i.e. CPO, trade and air transport.

The sectors that need to be continuously developed i.e. CPO and its downstream industries: food & beverage and cosmetic industries… to maintain the continuity of high growth level, North Sumatra also needs diversification, some sectors that could be developed are sectors related to Tourism such as the restaurant, accommodation and food and beverage sectors.

Restoran

Konstruksi

Ind. makananKelapa Sawit

Ind. Minyak Makan

Ind. Kimia dan kosmetik

POTENTIAL COMMODITY (3)

LEADING COMMODITY (1)

POTENTIAL COMMODITY (2)

Source : IO Table –BPS, Kompas R&D (treated, 2008)

Restaurant

Construction

Food Industry

Food Oil Industry

Chemical and Cosmetic Industry

Palm Oil

Trade

16

Ranking SectorBackward

linkageForward linkage

Multiplier

Output Income Employment

1 Rice, Grains and Flour industry 2.03 1.42 2.03 6.59 37.03

2 Food oil industry 1.91 1.23 1.91 3.26 12.85

3 Beef production, vegetables and Fruits Industry 1.88 1.41 1.88 4.25 17.97

4 Other Food Industry 1.85 1.58 1.85 2.20 5.50

5 Apparel Industry 1.85 1.13 1.85 2.20 3.03

6 Rubber and Rubber Goods Industry 1.82 1.43 1.82 4.40 21.20

7 Food from flour, sugar, chocolate and processing Industry 1.82 1.76 1.82 1.95 4.64

8 Leather tanning, footwear and leather goods industry 1.81 1.01 1.81 2.55 4.88

9 Spinning, weaving and knitting Industry 1.81 1.92 1.81 2.07 2.79

10 Oil and Gas Industry 1.79 1.26 1.79 2.28 2.70

13 Restaurant 1.73 2.43 1.73 1.67 1.70

17 Residential buildings and non-residential buildings 1.69 2.08 1.69 1.56 2.08

38 Hospitality 1.44 1.13 1.44 1.33 1.23

45 Palm oil 1.33 1.56 1.33 1.30 1.08

Output, income and employment multiplier for leading and potential

sectors

• Sectors related to CPO and its derivatives have an output multiplier of 1.62, better than the overall sector average1.47.

• Meanwhile, sectors related to the tourism industry have a multiplier output reaching 1.67, higher than the average of all sectors and the average CPO and its derivatives.

• Government policy to make Lake Toba as a tourism destination is the right thing to create new sources of economic growth.

17

Analysis of Agricultural

Sector Development in

South Sulawesi

18

➢ Despite decreasing in growth in the second quarter of 2018 (qtq), the growth of South Sulawesi is always above the nationallevel (except for exports).

➢ From Expenditure side, economic growth in the 2nd quarter of 2018 is 7.38% (y-on-y), affected by positive growth in almostall expenditure components.

➢ The highest growth was achieved by the component of Non Profit Institution Consumption Expenditures Serving Households(LNPRT) by 21.7%; followed by Government Consumption at 6.8% and Gross Fixed Capital Formation (PMTB) at 6.32%.

➢ The high growth of LNPRT impact by regional head elections (pilkada) which encouraged the rapid increase in LNPRTspending.

Sumber : BPS (2018)

South Sulawesi’s Economic Growth is above the National Growth in the second

quarter of 2018Economic Growth in South Sulawesi Economic Growth based on Expenditure Side in South Sulawesi

19

6.77

7.41

7.38

5.065.27

4.5

5

5.5

6

6.5

7

7.5

8

8.5

I II III IV I II III IV I II

2016 2017 2018

per

cen

t (%

)

South Sulawesi Indonesia

0

10

20

30

40

50

60

70

HouseholdConsumption

Non profitinstitution

servinghousehold

governmentexpenditure

Gross fuxedcapital

formation

Export Import

TrilionRupiah

TWII-2017 TWI-2018 TWII-2018

The Economy of South Sulawesi is diversified but Agriculture

remain the leading sector

Source : BPS (2018)

➢ Agriculture still the main sector of South Sulawesi, this can be seen from the highest economic growth and the sector contribution whosevalue is above 22% of economy structure in South Sulawesi.

➢ The second largest sub-sector comes from trade, the growth in this sector is due to the strategic nature of South Sulawesi as a goodsdistribution channel, especially this province is the gateway of East Indonesia.

➢ Overall, the economy of South Sulawesi is diversified where other sectors such as the manufacturing industries, Construction andServices are starting to show significant contribution.

Sector based on year 2010 2016 2017 Q1 - 2018 Q2 - 2018

Agriculture, Forestry and Fishery 7,86 5,34 14,43 10,77

Mining and Excavation 1,22 4,52 -3,57 6,01

Manufacturing Industry 8,23 5,03 -6,12 -2,72

Electricity supply, Gas 11,52 6,1 -7,1 6,32

Water supply 5,44 7,89 2,76 4,84

Construction 6,75 8,66 -4,43 4,1

Large and wholesale trade 9,87 10,74 -2,37 10,5

Transportation and Warehousing 7,75 8,37 -1,31 6,62

Food and Beverage Accommodiation 8,47 11,66 0,16 5,71

Information and Communication 8,13 10,52 0,64 2,3

Financial Service 13,63 4,39 0,13 3,71

Real Estate 6,37 4,48 0,29 1,07

Firm service 7,88 8,44 0,43 2,52

Mandatory Government, Defense and Social Administration -0,22 5,2 -1,58 8,8

Education Service 6,86 9,72 0,16 5,18

Health and Social Activities Service 8,45 8,8 -2,21 3,86

Others Service 9,81 9,58 0,04 5,59

Sectoral Economic Growth in South Sulawesi

20

23.27 22.89 23.78

13.39 13.94 14.67

13.97 13.71 12.344.44 4.34 4.45.04 5.19 5.06

12.51 12.74 12.64.63 4.76 4.684.26 4.18 4.24

18.5 18.23 18.23

0%

20%

40%

60%

80%

100%

2016 2017 Tw II -2018

Sectoral Contribution in South Sulawesi

Agriculture Trade

Manufacturung industries Mandatory Government

Education services Construction

Information and communication Transportation and warehousing

Others

Number of Poor People in South Sulawesi : Downward Trend and Below the National Average

16.2215.4

14.41 14.33 14.0113.28 13.16 12.62

11.1410.28 9.71 9.66 9.38 9.24 9.24 8.78 8.46 8.42 8.29 7.97 7.66 7.38

5.7 5.324.59

0

2

4

6

8

10

12

14

16

18

Pan

gkep

Jen

epo

nto

Tora

ja U

tara

Lutr

a

Luw

u

Sela

yar

Enre

kan

g

Tato

r

Mar

os

Bo

ne

Bar

ru

Ban

taen

g

Suls

el

Taka

lar

Sin

jai

Ko

ta P

alo

po

Pin

ran

g

Go

wa

Sop

pen

g

Bu

luku

mb

a

Luti

m

Waj

o

Ko

ta P

are

-Par

e

Sid

rap

Ko

ta M

akas

sar

➢ The percentage of poor population in South Sulawesi isstill below the National percentage.

➢ Seen from distribution, rural poverty higher than urbanareas, but with a downward trend.

➢ There are 50% of districts in South Sulawesi that have apoor population above the provincial level. But, citiessuch as Makassar and Pare-Pare which is more developedwas far below South Sulawesi.

Number of poor people in South Sulawesi

Sumber : BPS (2018) 21

149 162 162 154 146 157 149 151 154 167 168

645 702 702 652 651 707 658 646 660 659 625

10

10 10

1009

10

0909

0909

09

08

09

09

10

10

11

11

Mar 2013 Sep 2013 Mar 2014 Sep 2014 Mar 2015 Sep 2015 Mar 2016 Sep 2016 Mar 2017 Sep 2017 Mar 2018

0

100

200

300

400

500

600

700

800

900

1000

Tho

usa

nd

Peo

ple

Urban Rural percentage

9.54

10.32 10.28

9.549.39

10.12

9.409.24

9.389.48

9.06

11.3711.46

11.25

10.96

11.2211.13

10.8610.7 10.64

10.12

9.82

9.00

9.50

10.00

10.50

11.00

11.50

12.00

Mar2013

Sep2013

Mar2014

Sep2014

Mar2015

Sep2015

Mar2016

Sep2016

Mar2017

Sep2017

Mar2018

Indonesian and South Sulawesi Poverty Trends

South Sulawesi Indonesia

GRDP/capita’s Disparity between districts / cities and Gini Ratio in South Sulawesi is quite high

0.405

0.410

0.4290.425 0.424

0.426

0.4070.406

0.414

0.408

0.402

0.3970.394 0.393

0.370

0.380

0.390

0.400

0.410

0.420

0.430

0.440

0

10

20

30

40

50

60

2011 2012 2013 2014 2015 2016 2017

Gin

i In

dex

Per

sen

Inequality of Population Income and Gini Index

40% Penduduk Berpenghasilan Rendah 40% Berpenghasilan Sedang 20% Penduduk Berpenghasilan Tinggi Indeks Gini Indeks Gini Nasional

Rp- Rp10,000,000 Rp20,000,000 Rp30,000,000 Rp40,000,000 Rp50,000,000 Rp60,000,000 Rp70,000,000 Rp80,000,000 Rp90,000,000

Gowa

Jeneponto

Tana Toraja

Bulukumba

Takalar

Enrekang

Toraja Utara

Barru

Luwu Utara

Luwu

Bantaeng

Kota Palopo

Sinjai

Soppeng

Bone

Kep. Selayar

Sidrap

Kota Pare-Pare

Pinrang

Wajo

Maros

Pangkep

Luwu Timur

Kota Makassar

GRDP per capita between districs/cities in South Sulawesi

2016 2011 Averages 2016 Averages 2011

Sources : Macroeconomic Indicators and BPS (2018)

There was an incomeincreasing between2011 and 2016. Severalcities in South Sulawesi had highest income than other districts.

• Inequality of income in South Sulawesi is relatively higher thanNational level. • The growth of income

Group of 20% of thehigh incomepopulation is higherthan the other group.

22

40% Low-Income Population40% Moderate Income

Population 20% High Income Population Gini Index

Indonesia Gini Index

Sector February 2017 August 2017 Februaryy 2018

Agriculture 1.544.614 1.391.639 1.617.680

Trade 666.962 674.127 652.232

Manufacture 279.668 279.246 304.224

Adm. Government 239.782 206.819 262.878

Education Service 246.833 228.271 253.103

Construction 245.679 232.673 236.673

Others 577.869 585.888 622.506

Amount 3.801.407 3.598.663 3.949.296

Agriculture and Trade Sectors were the dominant sector to absorb Labor in South Sulawesi

➢ The agriculture still the main sector to absorb labor in South Sulawesi Province. In February 2018, agricultural sector was able toabsorb 1.62 million people, this number grew positively compared to February and August 2017.

➢ This increase was caused by the harvest in early 2018 so that the needs of worker in the harvest season had raised.

➢ Other sectors that contribute to absorb labor in South Sulawesi are Trade and followed by the Processing Industry.

Source : BPS (2018) 23

41% 39% 41%

18% 19% 17%

7% 8% 8%

6% 6% 7%

6% 6% 6%

6% 6% 6%

15% 16% 16%

0%

20%

40%

60%

80%

100%

February 2017 Agustus 2017 February 2018

Agriculture Trade Manufacturung industries

Mandatory Government Education services Construction

Others

6.5

5

5.9

7

5.9

4

5.9

3

5.9

0

5.8

5

5.7

7

5.6

5

5.6

1

5.5

7

5.5

3

5.4

7

5.4

6

5.4

2

5.4

1

5.4

0

5.3

9

5.3

7

5.3

3

5.2

6

5.2

1

5.2

0

5.1

9

5.1

7

5.1

5

5.1

2

5.1

1

5.0

3

5.0

0

4.9

7

4.9

5

4.9

1

4.8

8

4.6

4

3.7

0

DK

I Jak

arta

Jaw

a Te

nga

h

DI Y

ogy

akar

ta

Bal

i

Jaw

a B

arat

Ke

pu

lau

an R

iau

Jaw

a Ti

mu

r

Sula

wes

i Uta

ra

Sum

ater

a U

tara

Ke

pu

lau

an B

angk

a…

Kal

iman

tan

Sel

atan

Ind

on

esi

a

Sula

wes

i Sel

atan

Sum

ater

a B

arat

Sum

ater

a Se

lata

n

Kal

iman

tan

Tim

ur

Lam

pu

ng

Ban

ten

Kal

iman

tan

Ten

gah

Ria

u

Kal

iman

tan

Uta

ra

Be

ngk

ulu

Go

ron

talo

Sula

wes

i Te

ngg

ara

Sula

wes

i Te

nga

h

Ace

h

Jam

bi

Nu

sa T

engg

ara

Bar

at

Sula

wes

i Bar

at

Kal

iman

tan

Bar

at

Mal

uku

Uta

ra

Mal

uku

Pap

ua

Bar

at

Nu

sa T

engg

gara

Tim

ur

Pap

ua

• Notes: values 1-3 are “unsatisfied” categories, values 4-7 are “satisfied” categories and values 8-10 are “very satisfied” categories. Calculation of the

Inclusive Economic Development Index based on economic growth, income distribution and poverty reduction and expansion of access and opportunity

• The position of South Sulawesi is still below the National level due to the low index of economic growth pillars and pillars ofequity and poverty

alleviation.

Source : Bappenas (2018)

The Inclusive Economy Index of South Sulawesi Province is 5.46… The inclusive economic development index of South Sulawesi Province was still below the national level

24

5.17

4.88

Indonesia South Sulawesi

1st Pillar : Economic Growth

6.64

6.57

Indonesia South Sulawesi

2nd Pillar: Income Equality and Poverty Reduction

5.05

5.82

Indonesia South Sulawesi

3rd Pillar: Improving Access and Opportunity

Problems in Economic Inclusive Index in South Sulawesi

Source : Bappenas (2018)

Share of Manufacturing Sector was still low to GRDP

• No sustainable supply of raw materials

• Sociologist/culture factor: Sulawesi people as “Trader”

• Policies related to the down streaming of the agricultural sector to the manufacturehave not yet been optimal yet

High Level of Inequality

Income

➢The majority of farmers (70%) = sharecroppers, not landowners

➢The majority of fishermen= fishermen workers, not owner

➢Wage Gap between sectors

➢Change in economics structure

➢HRD disparity between income groups

Region

❖Infrastructure

❖Excellent commodities that are already saturated

❖Geographical-spatial and regional endowment factors25

Policy Direction

26

Policy Strategy

ENCOURAGING ECONOMIC GROWTH TO THE WHOLE AREA

Capacity building of human resources

through vocational education

Providing affordable business financing

opportunities through KUR

Economic Equality Policy

Industry

Basic Industry: Iron / Steel,

Petrochemical, and Basic Chemicals

SDA, Agro and Mineral Downstream

Industry

Land Chance Human Resource Capacity

TARGET :

PKE Reformation 16Infrastructure

222 National Strategic

Projects and 3 Programs*

Economic Area

12 Special Economic Zone

(SEZ)

16 industry areas

*) Program Kelistrikan dan Program Pesawat Jarak Menengah

Land Reform Policy: asset reform,

land redistribution, access reform

The success of economic growth and the improvement of people's welfare cannot be separated from government policies. Government policy

packages are in the form of infrastructure development, strengthening competitiveness, economic zones and building tourism areas in all parts of

Indonesia which supported by economic equality policies.

Increasing

investment

climate

Increasing

logistic efiency

Export stimulation

Encouraging industrial competitiveness

Tourism Promotion

Strengthening people’s purchasing power

27

Kereta Api Tebing Tinggi – Kuala Tanjung

• As a means of supporting KEK Sei Mangkei and being part of KA Trans Sumatra Network

• Total investment sebesar Rp 477 Billion

Industrial Zone of Kuala Tanjung

Kuala Tanjung International Hub Seaport• The Kuala Tanjung international hub port aims to create an

entrance for logistic flow to the western region of Indonesia

• Support the development KEK Sei Mangkei

• Total investment Rp 30 Trilion

Bendungan Lausimeme

• Total investment sebesar Rp 741 Billion

• Operation Target: 2021

KEK Sei Mangkei

• The main business is in the form of palm oil and rubber industries.

• Project impact on the economy Rp. 92,1 trillion

• Employment in 2017 : 3.672 person.

• Estimated Invesment

1. Infrastructure : Rp. 4,2 trilion

2. Business investment : Rp 123,3 trilion

• Existing investor:

1. PT. Unilever Oleochemical Indonesia (PT UOI)

2. PT. Industri Nabati Lestari

3. PT. Alternatif Protein Indonesia (on process)

Encouraging the diversification of sources of growth : Development of Infrastructure through PSN (National Strategic Project)

Source : KPPIP

• Total invesment Rp 3.5 Trilion

• Progress :

1. Land acquisition until May 2018 amounting to 61 hectares (11%)

Toll Road Project

• Medan – Binjai – Toll Road (16 km)

• Kisaran – Tebing Tinggi – Toll Road

• Medan – Kualanamu – Lubuk Pakam – Tebing Tinggi Toll Road (62 km)

• Binjai – Langsa Toll Road (110 km)

• Rantau Prapat – Kisaran Toll Road (100 km)

• Tebing Tinggi – Pematang Siantar – Prapat – Tarutung – Sibolga Toll Road (200 km)

• Dumai – Sp. Sigambal – Rantau Prapat Toll Road (175 km)

Lake Toba is one of the top 10 national destinations.

28

Types and Characteristics of Regional Infrastructure Financing Instruments

Desirability criteria

Tenor Interest Rate Currency match Risk profileComplexity and

transaction costsImplementation Amount available

APBN/APBD Not applicable Not applicable Not applicable Not applicable

Unlikely to increase

significantly in the

medium term

PT SMI Up to 25 years <10% Debt issued in IDR

Government

guarantee; Local

government debt

transfer if there is a

default

Outstanding 1,21

Trillion

Commitment 2,78

Trillion

SMI has sufficient

funds in the medium

term

Regional Bonds 10-15 years*10%

(rating AA+)Debt issued in IDR

No government

guarantee

Prov. Jateng for

issuance planned

2019-2021

Limited by investor

demand*

Regional Loans

through BPD<10 years* >12%* Debt issued in IDR

No government

guarantee;

Rp1.204 billion

Update per August

2018*

Loan ceiling size is

likely to be small

Public Private

Partnerships

(PPPs)10-30 years 16-18%*

Finance can be in

any currency

Depends on risk

allocation

Only two local

government PPPs

signed

Limited by pipeline

of suitable projects

Undesirable Very DesirableNeutral DesirableSomewhat undesirable

Source: Prospera*the data is the number of loans proposed by the Regional Government to the BPD and has been approved by the Minister of Home Affairs in 2018

…..Local governments need to be encouraged to develop regional infrastructure development innovations by adopting aportfolio approach

29

Transparancy and quality of financial reports

• Audit opinion for last 2 years

• Timeliness of publishing financial reports

• Public access to fiscal information(APBD, RKA and SKPD)

Budget performance

• Aggregate expenditure outturn*)

• Capital expenditure outturn*)

• Proportion of capital to totalexpenditure*)

• PAD outturn

• Proportion of PAD to totalrevenue

• SILPA balance proportion ofexpenditure

• Ratio of debt to revenue / assets

Budget processes and governance

• Implementation of Medium Term Budget Finance (MTBF) and it’s alignment with strategic plan

• Multi-year contracts expenditure as proportion of total expenditure

• Perda APBD passed on time

• Use of e-Government for PFM

Infrastucture planning andmanagement

• Economic analysis of investmentproposals

• Investment project selection

• Investment project costing

• Investment project monitoring

Innovation of Financing Sources by Enhancing Investment Opportunity and Creditworthiness, through:• Efficiency and Effectiveness of Financial Governance• Transparency and Accountability in Local Government Execution

Source: Prospera 30

Thank you

31

32

▪ Monitoring and EvaluationTo ensure the right amount, on time and on target

▪ Replicating National Program increases the participation coverage

▪ Regional Program Innovation

▪ Encouraging Synergy of National Priority

▪ Preparing Business Units to be accessible by banks

▪ Preparing Human Resources to compete and could be

more productive

▪ Preparing Regulations to improve the effectiveness of

the implementation of the Village Law (Utilization of

DD and ADD)

▪ Regional Program Innovation

▪ Encouraging Synergy of National Priority

Reducing Expense

(especially for the poor)

Increasing Income

(especially for the poor and vulnerability)

Increasing the role of local governments to reduce inequality in their respective regions

32

GOVERNMENT POLICY

The government issued var ious pol ic ies to suppor t investment c l imate and economic equal i ty

33

ONLINE SINGLE SUBMISSION (OSS)

Basic Principle

OSS is a system that integrates all business licensing services within the authorized authority (i.e

Minister/Head of Institution, Regent, or Mayor) through single electronic platform.

2

3

45

6

1

Monitoring is accompanied

and/or done by certificated

profession.

Integrated with all related

Ministries/Institutions/Governments.

Easy to access IT services for all

community/business actors.

Confidence to comply to

standard from business actors

(through commitment).

Standardized licensing

(national and/or international).

Fulfilment assurance of the Safety,

Health, and Security, and Environment

Aspect.

22

1

Government Policy : Fiscal Incentives

100% Corporate Income Tax Reduction

(Tax Holiday) for pioneer industries, with

concession period of :

500B - <1T Investment value 5 years

1T - <5T Investment value 7 years

5T - <15T Investment value 10 years

15T - <30T Investment value 15 years

≥30T Investment value 20 years

25

Reduction in final income tax rates from

1% to 0.5%

TAX HOLIDAYINCOME TAX REDUCTION

FOR MSMEs

1 2

2

36

Fiscal Incentives: New Tax Holiday Policy

Internship

Link and Match between the Education and

Business and Industry Sectors.

Competency Standard

Kelembagaan

The use of Work Competency

Standard (SKK) defined by the

Profession Certificate Institution

(LSP).

Building cooperation between

the education and business

and industry sectors.

Internship program within the

cooperation of Ministry of

Manpower and KADIN

Development of education

institution and vocation training

(BLK, SMK, and Poltek).

3.5 Years A C H I E V E M E N T

▪ 7.710 People by 2017

▪ 2.000 People (By March 2018)

568 Companies

1.537 vocational school

37.534 3-in-1 education

and training

Participants

2.770 Cooperation

AgreementP.S until the launching of the 5th vocational industry in Banten

3.5 Years A C H I E V E M E N T

2014 2015 2016 2017

421.927 Certificated

manpower by 201764

SKK

104

SKK

107

SKK

45

SKK

3.5 Years A C H I E V E M E N T

13.236 SMK 192 Politeknik

301 BLK 9.106 LPK Swasta

3.5 Years A C H I E V E M E N T

Sumber : Kementerian Tenaga Kerja dan Kementerian Perindustrian

Government Policy: Improvement of Human Resources Through

Vocational School

26

3

38

Progress Status of National Strategic Projects (PSN) and 35 GW Electricity Program

Progress of PSN and Programsper June 20181

2 projects already completed

6 projects in transaction

53 projects and 1 Airplane Industry Program in

preparation

29 projects in construction and will start operating in 2018

44 projects and 1 Electricity Program in construction and

partial operation phase

52 projects in construction and will start operating in 2019

37 projects in construction and will start operating after 2019

1%

20%

13%

23%

16%

3%

24%

223 + 3 PSN

2.614 MW are operating

17.403 MW are in construction

12.281 MW have signed PPA but have not reached financial close

1.002 MW are in planning

35GW

2.135 MW are in procurement

Progress of 35 GW Electricity Programper July 2018

3%6%

35%

49%

7%

1 Excluding the economic equality program that will be reported separately

Government Policy: Accelerate Infrastructure Development4.1

39

Government Encourages The Center Of Economic Growth Through SEZ

Investment incentives in SEZs▪ 100% foreign ownership▪ Corporate Income Tax

Holiday up to 25 years / local taxes in tourism SEZ

▪ *for activities that comply with the main focus of the zones

▪ Tax allowance up to 10 years

▪ Competitive Capital Cost ▪ Online Single Submission

and One Stop Shop for all relevant clearance

▪ 0% import duties for imported goods (negative list) entering SEZ

▪ 0% Value-Added Tax for transaction within SEZ

▪ Simplified immigration formalities

Total Output 12 SEZUSD 4,8 Billion

Expected Minimum PDB2025

USD 1.908 TrillionPer Capita US$ 6700/Capita

Expected Output (2025)USD 53 Billion

4.2

Kuala Tanjung Landak

Tanggamus Kendal

Tanah Kuning Morowali Buli, Halmahera Timur BintuniKetapang

Batulicin

Jorong

KonaweGresikTanjung Buton Wilmar Serang Bantaeng

40

Government is Developing 14 Integrated Industrial Zones Across Indonesia Such as Aluminum, Food, Manufacturer, Furniture Industry, Etc.

4.3

Realization

Rp 96,7 Trilion

0.3%KUR of Placement for Migrant Worker (TKI)

32.9% KUR RETAIL

66.8% KUR of MicroKUR Distribution Performance of 2017

Stakeholders14 Central Government2 Supervisor34 Bank (State-owned Enterprises (BUMN) & Privates)

4 Non Bank Institutions2 Cooperatives2 Deposite Insurance Agency (LPS)Entire Regional Government (Province, Municipalities)

Economic Sector

Fisheries, Hunting, Forestry, Processing Industry, Trade, Construction, and Services

Debtor

2,893,035

Rp 65,2 Trilion

Rp 31,2 Trilion

Rp 0,3 Trilion

Realization of KUR by July 2018:

65%(of target at Rp 126.9 Trilion)

NPL: 0.04%41

5 Expansion of KUR Recepient

AMENDMENT OF KUR 2018B a s e d o f P e r m e n k o N o . 11 T h n 2 0 1 7

The Business Group Becoming The

Recipient Of KUR

Special KUR Schemes (For Plantations, Livestock, And

Fishery)

Interest Rate of KUR in 2018 to be 7%

Minimum Portion of Distribution to the Production Sector

Multisectoral KUR Scheme

Payment Mechanism for Bayar Panen

(Yarnen) and Grace Period

Changing Terminology of Retail KUR to be Small KUR

Micro KUR Ceiling for Production sector is Rp 25 Million per

production cycle, while outside the maximum production sector

the ceiling accumulation is Rp100 million

Channel distribution in conjunction with other

allowed credits (KUR, KPR, KKB, SSRG)

Cost Structure of Placement Migrants

Worker’s KUR

KUR for Border Inhabitans

KUR for the KUBEoptimalization

42

To optimize the KUR program implementation and the accuracy increase of KUR distribution target, the Coordinating Ministry for Economic Affairs

designated Regulation Number 11 of 2017 regarding the KUR Implementation Guidelines. The 12 KUR policy points are valid from January 1, 2018.

In the last three years, government has taken some strategic measures to improve

financial inculsion:

FINANCIAL INCLUSION PROGRAM

Issuance of regulation related to NSFI:

1. President Regulation No 82/2016 on NSFI

2. Decree of Coordinating Ministry for Economic

Affairs No 93/2017 on Working Groups and the

Secretariat of National Council of Financial

Inclusion.

3. Coordinating Ministry for Economic Affairs

Regulation No 6/2017 on Work Mechanism and

Procedure of National Council of Financial

Inclusion.

01

Implementation of Financial Inclusion program:

1.Non-cash allowance such as Non-cash Social

Allowance, Non-cash Food Allowance, Farmer Card,

Smart Indonesia Program.

2.Credit program for people business including

People Business Credit (KUR) and Developing

Prosperous Family's Economy (Mekaar)

3.Financial services program by agent namely Digital

Financial Services and Laku Pandai where people

can open bank account through agents

02

03As the ecosystem of financial service sector has been developing in the last three years, Indonesia financial service and infrastructure sector regulator has succeeded to encourage some key aspects in

improving financial service ecosystem such as:

1. National Non-Cash Movement has promoted Less Cash Society,

2.Development of regulation which facilitate the growth of

financial technology,

3.Implementation of Palapa Ring and Base Transceiver Station

have increased the internet coverage to 55% of villages in

Indonesia

4. The launching of National Payment Gate in 4 December 2017

expands interoperability of financial service.

Acceleration of market access expansion of farmer/fisher/entrepreneur in village through food e-commerce application platform.

1. Market access expansion of farmer/fisher/entrepreneur in

village through food e-commerce application platform.

2. Beside market access, the application allows expansion of

farmer/fisher/entrepreneur’s access to financial products

especially financing and insurance.

terutama pembiayaan dan asuransi.

3.The application already can be utilized in some pilot regions before

it's national implementation date of 2019.

04

5

Indonesia encourages the use of savings accounts: 42% of savings account holders are in formal financial institutions such as banks or microfinance institutions - 10% higher than the average of developing countries.

10%higher than the average

of developing countries.

GLOBAL FINDEXINDONESIA

Digital payment activity has increased, such as in making or receiving online payment system

2014 2017

62% 71%

Referring to Global Findex 2017 survey result, Indonesia needs to add 54,388,751 adult residents who have accounts in formal financial institutions to achieve the target of 75% of financial

inclusion in 2019

To accelerate financial inclusion while achieving Indonesia finansial inclusion target in 2019, Indonesia’s National Council of Financial Inclusion has recommended strategic measures which

will be executed by seven working groups.

STRATEGY TO ACCELERATE FINANCIAL INCLUSION

1

2

34

5

6

Encourage the increasing role of cooperative in rural area to expand its service range

Use biometric data of electronic national identity card (KTP-el) for e-KYC and as obligation to open bank account

Expand financial services through synergy with Telko and non-bank institutions

Enhance electrification and internet infrastructure that support financial inclusion

Accelerate the certification of community property rights

Increase public awareness of bankaccount opening and financial literacy

The Rich and The Poor

Indonesia has experienced a considerable growth in savings account holder for

the poor between 2014 and 2017, from 22% to 37%. This growth is much higher

than other countries in East Asia and the Pacific which below 10%.

1

22% 37%

2014 2017

The Poor The Rich

57%45%

2014 2017

Rp

2

2014 2017

35% 46%

2014 2017

37% 51%

Financial Inclusion RateBased on Gender

Indonesia is one of the countries experiencing gender equality in account

ownership. The percentage of adult women holding savings account is greater

than the percentage of adult males, which is 51% and 46%. Though, men have a

higher percentage of account ownership than women globally.

2014 2017

3Financial Inclusion RateBased on Living Location

Ownership of savings account in rural areas increased

sharply. By 2014, only 28% of rural adults have savings

account in formal financial institutions. By 2017, the

percentage increases to 47%. There is a 15% increase in

ownership of saving accounts in rural areas. This increase in

ownership of savings accounts is greater than that of East

and Pacific (2%) and global (8%) countries.

29% 47%

Urban Area

51%46%

FINANCIAL INCLUSION SEGMENTATIONINDONESIA

Rural Area

Male Female

2014 2017

29% 47%

Use an account to pay bills

12%

4%

Use the internet to

pay bills

11%

Use the internet to

buy product online

Use the internet or

mobile phone to access

the account

8%

INDONESIA DIGITAL FINANCIAL DEVELOPMENT

Indonesia has made rapid progress in digital financial transactions over a period of three years.

As many as 35% of adult population has made or received payment

digitally or increased 13% compared to the results of 2014. The

amount of adult population who use digital transactions for certain

purposes include: