employment contracts chapter 2. employer-employee relationship is a worker an employee or an...

TRANSCRIPT

EMPLOYMENT CONTRACTSChapter 2

EMPLOYER-EMPLOYEE RELATIONSHIP

EMPLOYER-EMPLOYEE RELATIONSHIP

Is a worker an employee or an independent contractor?

Is a worker an employee or an independent contractor?

The answer is based on the Law of Agency

The answer is based on the Law of Agency

Principle/agent

Employer/employee

Master/servant

Principle/agent

Employer/employee

Master/servant

Employer/independent contractor

Employer/independent contractor

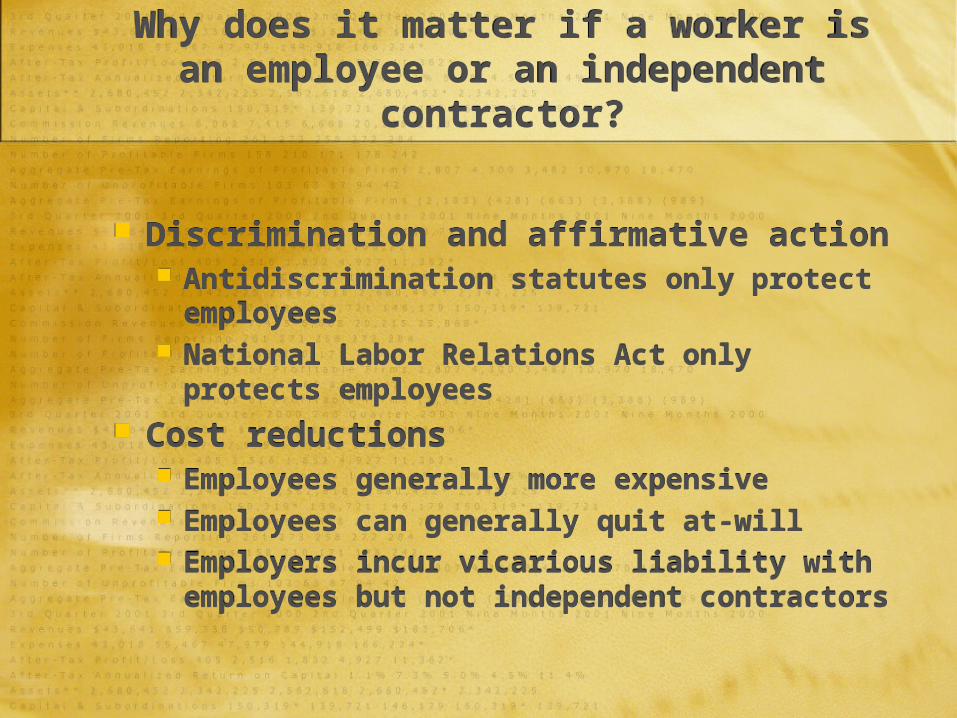

Why does it matter if a worker is an employee or an independent contractor?

Why does it matter if a worker is an employee or an independent contractor?

Why does it matter if a worker is an employee or an independent contractor?

Independent contractor – a person who contracts with a principal to perform a task according to her or his own methods, and who is not under the principal’s control regarding the details of the work

Distinction between independent contractors and employees significant for taxes, benefits, cost reduction plans and discrimination claims

Independent contractor – a person who contracts with a principal to perform a task according to her or his own methods, and who is not under the principal’s control regarding the details of the work

Distinction between independent contractors and employees significant for taxes, benefits, cost reduction plans and discrimination claims

Why does it matter if a worker is an employee or an independent contractor?

Why does it matter if a worker is an employee or an independent contractor?

Employer payroll deductions Employer responsible for FICA, RRTA, FUTA

and IRS withholdings for employees Independent contractors pay these taxes

themselves

Benefits Employee benefits protected Independent contractor provides his or her

own benefits

Employer payroll deductions Employer responsible for FICA, RRTA, FUTA

and IRS withholdings for employees Independent contractors pay these taxes

themselves

Benefits Employee benefits protected Independent contractor provides his or her

own benefits

Why does it matter if a worker is an employee or an independent contractor?

Why does it matter if a worker is an employee or an independent contractor?

Discrimination and affirmative action Antidiscrimination statutes only protect

employees National Labor Relations Act only protects

employees

Cost reductions Employees generally more expensive Employees can generally quit at-will Employers incur vicarious liability with

employees but not independent contractors

Discrimination and affirmative action Antidiscrimination statutes only protect

employees National Labor Relations Act only protects

employees

Cost reductions Employees generally more expensive Employees can generally quit at-will Employers incur vicarious liability with

employees but not independent contractors

Result of failure to appropriately categorize workers

Result of failure to appropriately categorize workers

IRS assesses harsh penalties for failure to pay FICA and FUTA

Employer may be liable under National Labor Relations Act

Employer may be liable under Fair Labor Standards Act

Employer may be liable for unpaid benefits

IRS assesses harsh penalties for failure to pay FICA and FUTA

Employer may be liable under National Labor Relations Act

Employer may be liable under Fair Labor Standards Act

Employer may be liable for unpaid benefits

ALSO, Employers may be vicariously liable for the actions of employees based on

one of several theories:

ALSO, Employers may be vicariously liable for the actions of employees based on

one of several theories:

1. negligent entrustment

2. failure to properly supervise

3. respondeat superior

1. negligent entrustment

2. failure to properly supervise

3. respondeat superior

An employee’s conduct is within the scope of his/her employment if it meets

each of the following four tests:

An employee’s conduct is within the scope of his/her employment if it meets

each of the following four tests:

1. It was of the kind that the employee was employed to perform.

2. It occurred substantially within the authorized time period.

3. It occurred substantially within the location authorized by the employer.

4. It was motivated at least in part by the purpose of serving the employer.

1. It was of the kind that the employee was employed to perform.

2. It occurred substantially within the authorized time period.

3. It occurred substantially within the location authorized by the employer.

4. It was motivated at least in part by the purpose of serving the employer.

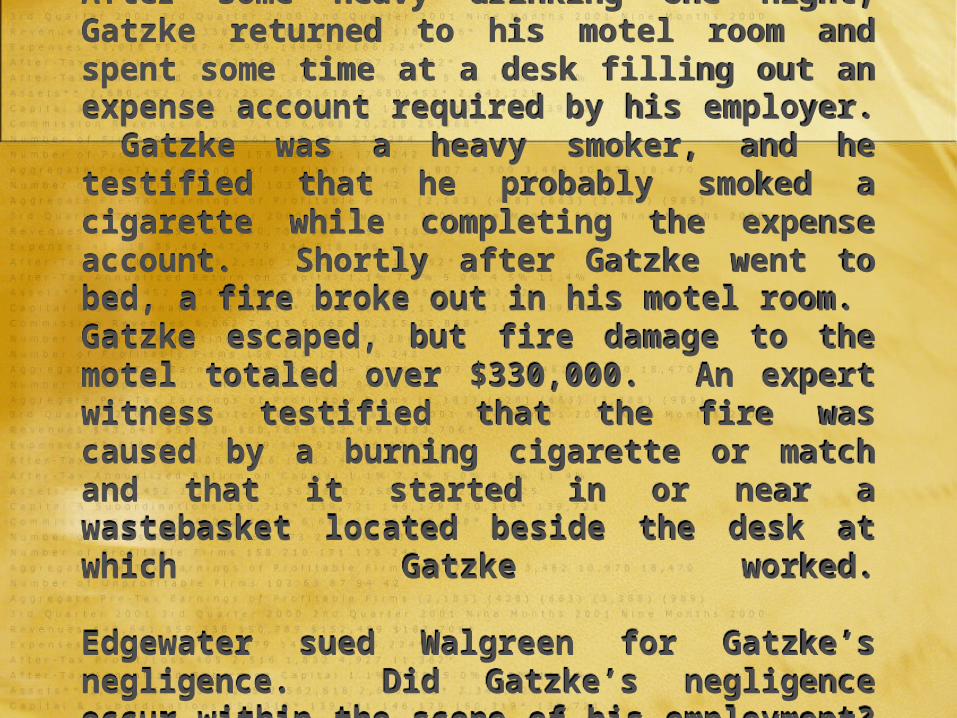

EDGEWATER MOTELS, INC. V. GATZKE

Gatzke, a district manager for the Walgreen Company, spent several weeks in Duluth, Minnesota, supervising the opening of a new Walgreen restaurant there. He remained at the restaurant approximately 17 hours a day, and he was on call 24 hours a day to handle problems arising in other Walgreen restaurants in the district. While in Duluth, he lived at the Edgewater Motel at Walgreen’s expense.

After some heavy drinking one night, Gatzke returned to his motel room and spent some time at a desk filling out an expense account required by his employer. Gatzke was a heavy smoker, and he testified that he probably smoked a cigarette while completing the expense account. Shortly after Gatzke went to bed, a fire broke out in his motel room. Gatzke escaped, but fire damage to the motel totaled over $330,000. An expert witness testified that the fire was caused by a burning cigarette or match and that it started in or near a wastebasket located beside the desk at which Gatzke worked. Edgewater sued Walgreen for Gatzke’s negligence. Did Gatzke’s negligence occur within the scope of his employment?

After some heavy drinking one night, Gatzke returned to his motel room and spent some time at a desk filling out an expense account required by his employer. Gatzke was a heavy smoker, and he testified that he probably smoked a cigarette while completing the expense account. Shortly after Gatzke went to bed, a fire broke out in his motel room. Gatzke escaped, but fire damage to the motel totaled over $330,000. An expert witness testified that the fire was caused by a burning cigarette or match and that it started in or near a wastebasket located beside the desk at which Gatzke worked. Edgewater sued Walgreen for Gatzke’s negligence. Did Gatzke’s negligence occur within the scope of his employment?

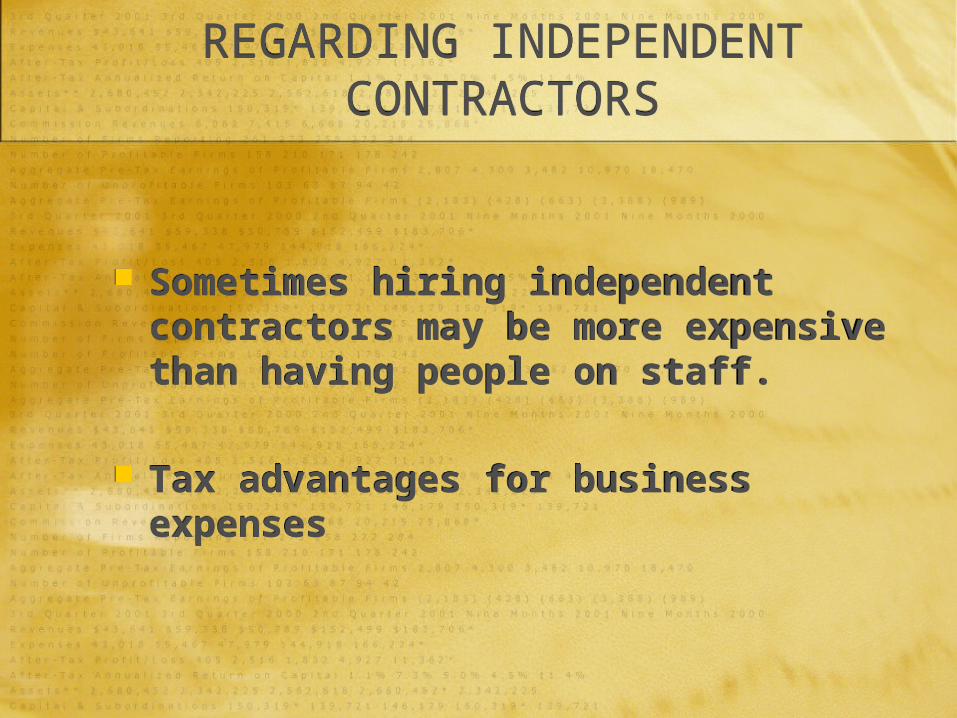

REGARDING INDEPENDENT CONTRACTORS

REGARDING INDEPENDENT CONTRACTORS

Sometimes hiring independent contractors may be more expensive than having people on staff.

Tax advantages for business expenses

Sometimes hiring independent contractors may be more expensive than having people on staff.

Tax advantages for business expenses

How do you tell if a worker is an employee?A Variety of Criteria

How do you tell if a worker is an employee?A Variety of Criteria

The Economic Realities Test Used in FLSA cases regarding

overtime, wage cases The Common Law Test

Used by some courts The Hybrid Test

Used by some courts The Right to Control Test

Used in IRS cases regarding withholding, payment of taxes

The Economic Realities Test Used in FLSA cases regarding

overtime, wage cases The Common Law Test

Used by some courts The Hybrid Test

Used by some courts The Right to Control Test

Used in IRS cases regarding withholding, payment of taxes

How do you determine if a worker is an employee?

How do you determine if a worker is an employee?

Common-law agency test Who has the right to control the

manner in which the work is performed?

IRS test 20 factors to determine whether

someone is an employee or an independent contractor

Derived from results of court judgments

Common-law agency test Who has the right to control the

manner in which the work is performed?

IRS test 20 factors to determine whether

someone is an employee or an independent contractor

Derived from results of court judgments

IRS 20 FACTOR ANALYSISIRS 20 FACTOR ANALYSIS

1. Instructions

2. Training

3. Integration

4. Services rendered personally.

5. Hiring, supervising, and paying

assistants.

6. Continuing relationships

7. Set hours of work

1. Instructions

2. Training

3. Integration

4. Services rendered personally.

5. Hiring, supervising, and paying

assistants.

6. Continuing relationships

7. Set hours of work

IRS 20 FACTOR ANALYSISIRS 20 FACTOR ANALYSIS

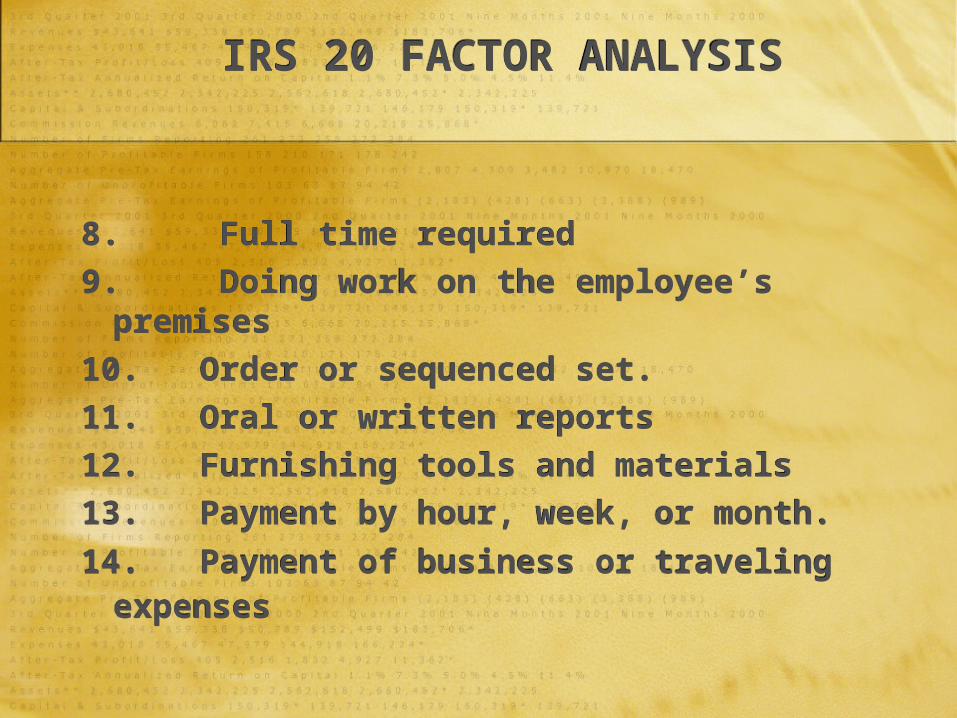

8. Full time required

9. Doing work on the employee’s premises

10. Order or sequenced set.

11. Oral or written reports

12. Furnishing tools and materials

13. Payment by hour, week, or month.

14. Payment of business or traveling expenses

8. Full time required

9. Doing work on the employee’s premises

10. Order or sequenced set.

11. Oral or written reports

12. Furnishing tools and materials

13. Payment by hour, week, or month.

14. Payment of business or traveling expenses

IRS 20 FACTOR ANALYSISIRS 20 FACTOR ANALYSIS

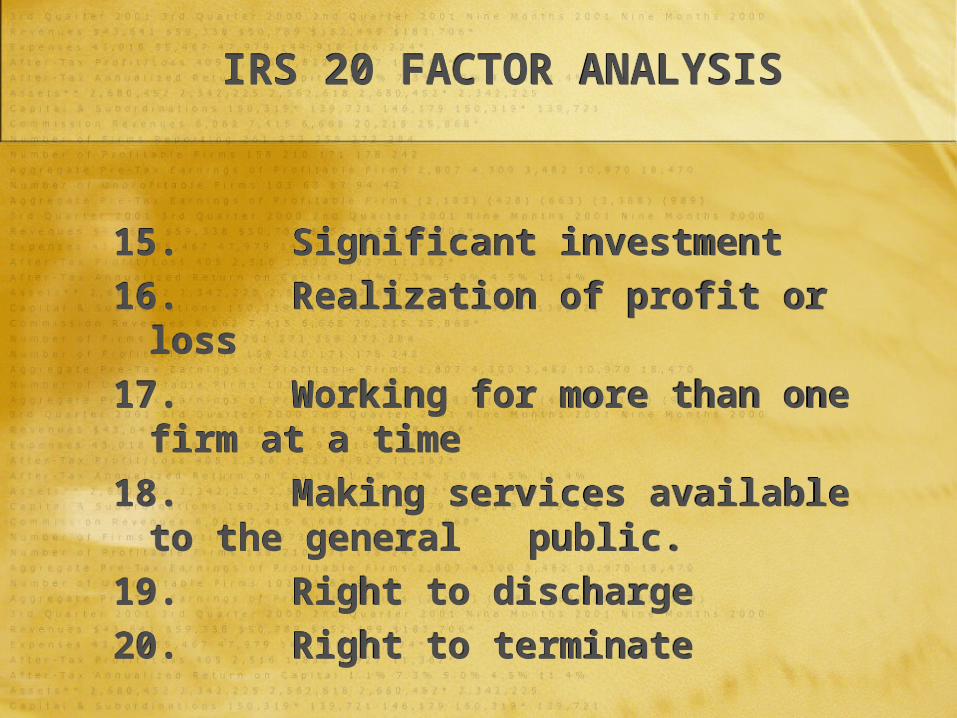

15. Significant investment

16. Realization of profit or loss

17. Working for more than one firm at a time

18. Making services available to the general public.

19. Right to discharge

20. Right to terminate

15. Significant investment

16. Realization of profit or loss

17. Working for more than one firm at a time

18. Making services available to the general public.

19. Right to discharge

20. Right to terminate

Clackamas Gastroenterology Associates v. Wells, Slide 1 of 2

Clackamas Gastroenterology Associates v. Wells, Slide 1 of 2

When addressing employee status under the ADA, the U.S. Supreme Court developed a “non-exhaustive” six-factor test to make the determination: Whether the organization can hire or fire the

individual or set the rules and regulations of the individual’s work;

Whether, and to what extent, the organization supervises the individual’s work;

When addressing employee status under the ADA, the U.S. Supreme Court developed a “non-exhaustive” six-factor test to make the determination: Whether the organization can hire or fire the

individual or set the rules and regulations of the individual’s work;

Whether, and to what extent, the organization supervises the individual’s work;

Clackamas Gastroenterology Associates v. Wells, Slide 2 of 2

Clackamas Gastroenterology Associates v. Wells, Slide 2 of 2

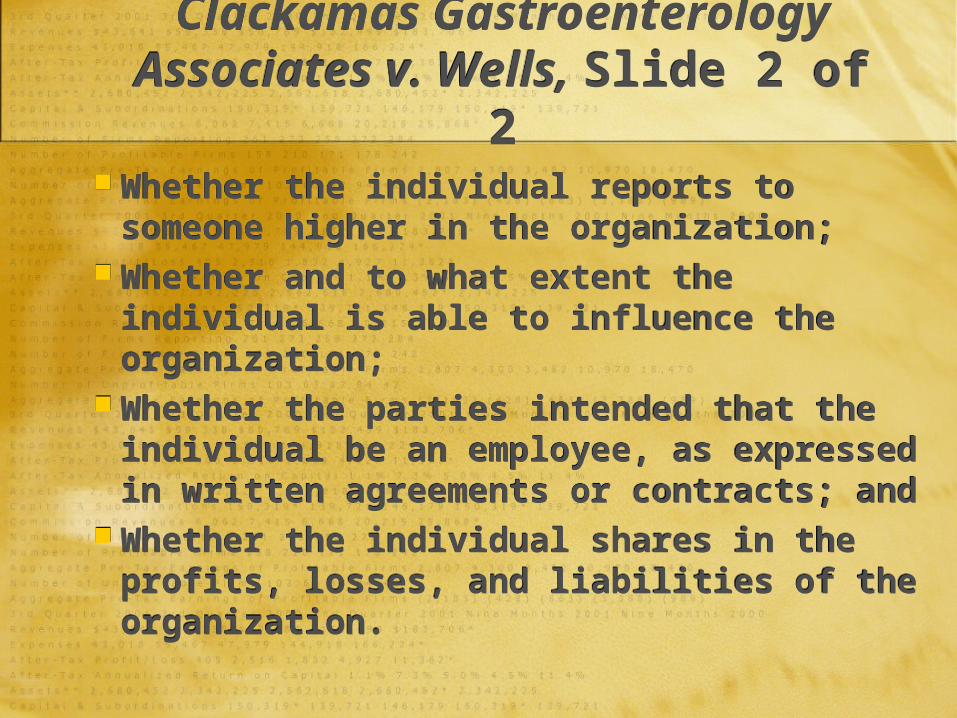

Whether the individual reports to someone higher in the organization;

Whether and to what extent the individual is able to influence the organization;

Whether the parties intended that the individual be an employee, as expressed in written agreements or contracts; and

Whether the individual shares in the profits, losses, and liabilities of the organization.

Whether the individual reports to someone higher in the organization;

Whether and to what extent the individual is able to influence the organization;

Whether the parties intended that the individual be an employee, as expressed in written agreements or contracts; and

Whether the individual shares in the profits, losses, and liabilities of the organization.

Economic Realities TestEconomic Realities Test

Factors:1) Who has the right to control how, when &

where the work is done?2) Who provides tools, materials & other

resources for the work to be done?3) What is the method of payment?4) What is the duration of the working

relationship?5) Does the work require a “special skill?”6) How integral to the business is the work

performed?7) Overall, how dependent is the hired party on

the hiring party?

Factors:1) Who has the right to control how, when &

where the work is done?2) Who provides tools, materials & other

resources for the work to be done?3) What is the method of payment?4) What is the duration of the working

relationship?5) Does the work require a “special skill?”6) How integral to the business is the work

performed?7) Overall, how dependent is the hired party on

the hiring party?

PROBLEMPROBLEM

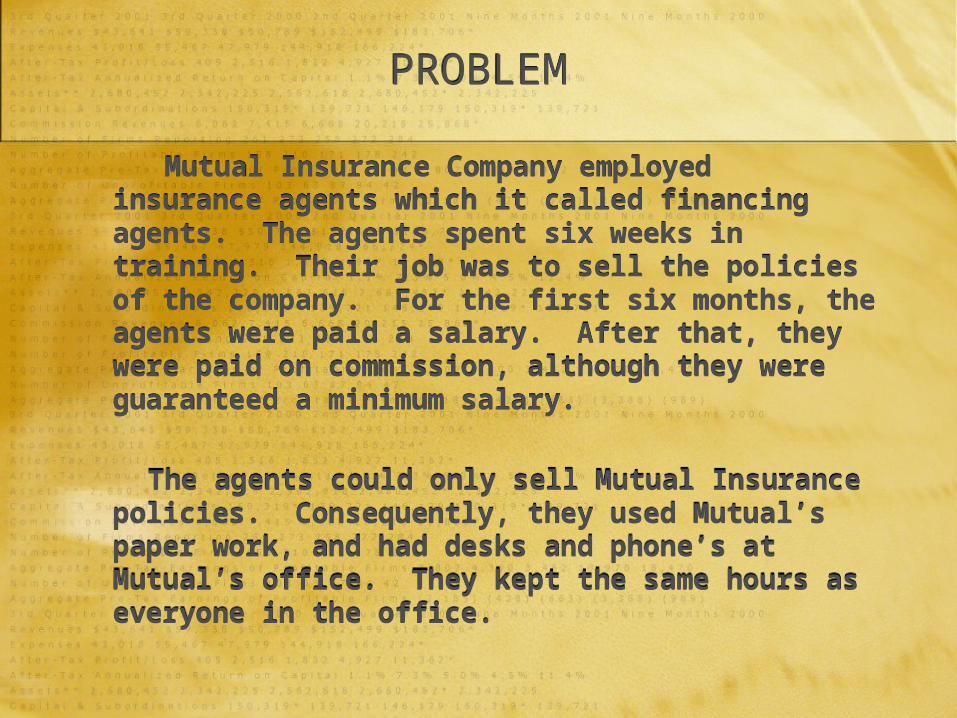

Mutual Insurance Company employed insurance agents which it called financing agents. The agents spent six weeks in training. Their job was to sell the policies of the company. For the first six months, the agents were paid a salary. After that, they were paid on commission, although they were guaranteed a minimum salary.

The agents could only sell Mutual Insurance policies. Consequently, they used Mutual’s paper work, and had desks and phone’s at Mutual’s office. They kept the same hours as everyone in the office.

Mutual Insurance Company employed insurance agents which it called financing agents. The agents spent six weeks in training. Their job was to sell the policies of the company. For the first six months, the agents were paid a salary. After that, they were paid on commission, although they were guaranteed a minimum salary.

The agents could only sell Mutual Insurance policies. Consequently, they used Mutual’s paper work, and had desks and phone’s at Mutual’s office. They kept the same hours as everyone in the office.

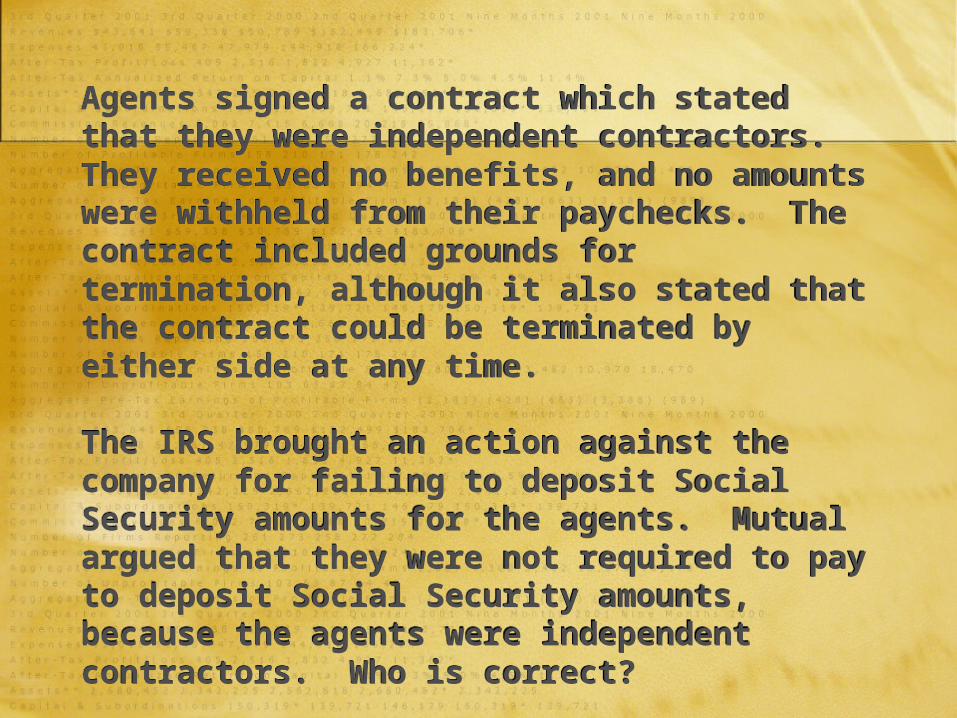

Agents signed a contract which stated that they were independent contractors. They received no benefits, and no amounts were withheld from their paychecks. The contract included grounds for termination, although it also stated that the contract could be terminated by either side at any time. The IRS brought an action against the company for failing to deposit Social Security amounts for the agents. Mutual argued that they were not required to pay to deposit Social Security amounts, because the agents were independent contractors. Who is correct?

Agents signed a contract which stated that they were independent contractors. They received no benefits, and no amounts were withheld from their paychecks. The contract included grounds for termination, although it also stated that the contract could be terminated by either side at any time. The IRS brought an action against the company for failing to deposit Social Security amounts for the agents. Mutual argued that they were not required to pay to deposit Social Security amounts, because the agents were independent contractors. Who is correct?

FedEx and UPSFedEx and UPS

http://www.law.com/jsp/law/LawArticleFriendly.jsp?id=900005546990

http://taxprof.typepad.com/taxprof_blog/2008/06/what-can-brown.html

http://www.law.com/jsp/law/LawArticleFriendly.jsp?id=900005546990

http://taxprof.typepad.com/taxprof_blog/2008/06/what-can-brown.html

What would you include in an independent contractor agreement?

Smart Practice – IC Agreements 1Smart Practice – IC Agreements 1

Declaring someone to be an independent contractor does not make it so.

The firm must give up the right of control over the worker.

The firm should not have ICs doing work that is central to the firm’s business or the same work as employees perform.

The firm should closely review long term IC agreements and not assign new projects without renewing agreements.

Declaring someone to be an independent contractor does not make it so.

The firm must give up the right of control over the worker.

The firm should not have ICs doing work that is central to the firm’s business or the same work as employees perform.

The firm should closely review long term IC agreements and not assign new projects without renewing agreements.

Smart Practice – IC Agreements 2Smart Practice – IC Agreements 2

A good IC Agreement should: Require that the IC supply his own

tools, materials & equipment, and pay his own assistants and business expenses.

Document the firm’s payment of a flat fee, rather than hourly or weekly payment.

Provide no benefits, not even time off. Make it clear that the IC is free to offer

his services to others.

A good IC Agreement should: Require that the IC supply his own

tools, materials & equipment, and pay his own assistants and business expenses.

Document the firm’s payment of a flat fee, rather than hourly or weekly payment.

Provide no benefits, not even time off. Make it clear that the IC is free to offer

his services to others.

Other Contingent Workers 1Other Contingent Workers 1

Temporary Workers If hired to do the same work as regular

employees or kept on for a long time, they may become employees under the common law test, entitled to the same benefits as regular employees.

Example: Microsoft’s “permatemps” Rule: Employers should not employ

temps on a long term basis, or hire them to do the work of regular employees.

Temporary Workers If hired to do the same work as regular

employees or kept on for a long time, they may become employees under the common law test, entitled to the same benefits as regular employees.

Example: Microsoft’s “permatemps” Rule: Employers should not employ

temps on a long term basis, or hire them to do the work of regular employees.

Other Contingent Workers 2Other Contingent Workers 2

Students and Interns Are Graduate and teaching assistants

who work for their universities employees or students? Generally not. But …

A graduate assistant was determined to be an employee because she received a stipend and benefits for her work, sick days and annual leave, equipment and training.

Student Athletes are not employees.

Students and Interns Are Graduate and teaching assistants

who work for their universities employees or students? Generally not. But …

A graduate assistant was determined to be an employee because she received a stipend and benefits for her work, sick days and annual leave, equipment and training.

Student Athletes are not employees.

Other Contingent Workers 3Other Contingent Workers 3

Volunteers Volunteers are generally not

employees. But auxiliary choristers who were paid a fee for singing on an on-call basis were employees.

Partners, Officers, Board Members, and Major Shareholders are generally not employees. The extent to which the individual acts

autonomously and participates in management controls.

Volunteers Volunteers are generally not

employees. But auxiliary choristers who were paid a fee for singing on an on-call basis were employees.

Partners, Officers, Board Members, and Major Shareholders are generally not employees. The extent to which the individual acts

autonomously and participates in management controls.

Other Employee Status Issues Other Employee Status Issues Undocumented Workers

The general policy of federal agencies is to enforce employment laws without inquiry into immigration status, but illegal status may affect the remedies due.

Example: The NLRB held that no back pay was due to an illegal immigrant. Instead, the NLRB issued a “cease and desist” letter to the employer, directing it to stop illegal conduct.

Consider: Will this penalty stop illegal hiring?

Undocumented Workers The general policy of federal agencies is

to enforce employment laws without inquiry into immigration status, but illegal status may affect the remedies due.

Example: The NLRB held that no back pay was due to an illegal immigrant. Instead, the NLRB issued a “cease and desist” letter to the employer, directing it to stop illegal conduct.

Consider: Will this penalty stop illegal hiring?