employment, collective bargaining and the quality of ... cfp 101114.pdf · employment, collective...

TRANSCRIPT

Employment, collective bargaining and the quality of industrial relations in the field of fisheries and aquaculture

R E S E A R C H R E P O R T

Employment, collective bargaining and the quality of industrial relations in the field of fisheries and aquaculture

R E S E A R C H R E P O R T

With the financial support from the European Union

The sole responsibility for this publication lies with the author. The Commission is not responsible for any use that may be made of the information contained.

Grant agreement no. VS/2013/0201“The impact of the Common Fisheries Policy (CFP) reform and the contribution of collective bargaining tocreate more and better jobs toward the exit from crisis: information and training measures in Europeanfisheries and aquaculture sector for workers organizations”

Budget heading 04.03.03.02 - Information and training measures for workers' organisations

European Commission - Employment, Social Affairs and Inclusion DG

The project is supported by

EUROPEAN TRANSPORT WORKERS’ FEDERATION - ETF

FAGLIGT FAELLES FORBUND - 3F (DANIMARCA)

FÉDÉRATION GÉNÉRALE DES TRANSPORTS ET DE L’EQUIPMENT - CFDT (FRANCIA)

SYNDICAT DES MARINS PECHEURS - CFTC (FRANCIA)

FEDERACION DE SERVICIOS A LA CIUDADANIA MAR - CC.OO. (SPAGNA)

ACV TRANSCOM MARITIME (BELGIO)

INTRODUCTION 4

METHODOLOGICAL NOTE 5

PART I FISHING IN EUROPE 7

THE ECONOMIC FRAMEWORK 9The European fishing fleet 9Aquaculture 12The processing industry 15Employment 18The market 20

BARGAINING AND SECTORAL POLICIES: THE ROLE OF THE TRADE UNIONS AND MANAGEMENT REPRESENTATIVES AT EUROPEAN LEVEL 22

Collective relations at European level 22The role of the trade unions and management representatives 22Collective bargaining in Europe 24

EUROPEAN POLICIES IN THE FIELD OF FISHERIES AND AQUACULTURE 25The Common Fisheries Policy 25The impact of the CFP 26The reformed CFP 27The European Fund for Maritime Affairs and Fisheries 30

PART II COUNTRY INFO 33

BELGIUM 35Introduction 35Economic and structural characteristics 35Evaluation of the impact of the CFP 36Collective bargaining in the fishing industry 37

DENMARK 39Introduction 39Economic and structural characteristics 39Evaluation of the impact of the CFP 40Collective bargaining in the fishing industry 41

FRANCE 43Introduction 43Economic and structural characteristics 43Evaluation of the impact of the CFP 44Collective bargaining in the fishing industry 45

ITALY 47Introduction 47Economic and structural characteristics 48Evaluation of the impact of the CFP 49Collective bargaining in the fishing industry 50

THE NETHERLANDS 52Economic and structural characteristics 52Collective bargaining in the fishing industry 53

SPAIN 55Introduction 55Economic and structural characteristics 56Evaluation of the impact of the CFP 57Collective bargaining in the fishing industry 58

CONCLUSIONS 61

BIBLIOGRAPHY 63

C O N T E N T S

3

4

I N T R O D U C T I O N

In the last few years, the Italian fishing industry has undergone a period of powerful economic contraction. Those who know this industry in various roles are aware of the causes that have led to this state of affairs.From the increase in the cost of fuel, which has had a considerable impact on business costs, triggering aspiral that has negatively affected the turnover of companies and, therefore, the salaries of employees andincome of the business; to the scarcity of the catch and the inability of the same to produce an income thatwill cover costs; to issues related to the market which often has to compete with much cheaper productsimported from non-EU countries. This is a very complicated situation, and the European Commission, with the enactment of various regula-tions, has attempted to safeguard and revive the sector but without establishing a proper dialogue withthe fishermen.In addition, in some areas, the relationship with the institutions has been contentious which has resultedin difficulties in finding a common course of action to deal with the problems.It is in this scenario that trade union activity draws the strength to take action and seek solutions to revivethe sector, involving all the interested parties.On various occasions, we have had the opportunity to speak with trade unions elsewhere in Europe andnote that our problems were also theirs.Hence the idea of this project, motivated by the desire to form a relationship with others who are living inthe same conditions as we are, comparing the contractual systems, labour regulations, and the systems ofemployment and social protection, to promote an undertaking aimed at reducing the inequalities betweenmember states, improving the role of bargaining and workers’ conditions, and increasing employment.We wanted to touch the reality in which workers are employed in different countries throughout Europe,by going and hearing directly from the protagonists about the problems they face daily, to promote adebate on the prospects and challenges of the future in the fishing industry.An important exchange of information which highlighted similarities and differences which the reader willfind in this volume which provides a snapshot of the sector in Italy and in Europe.

Sara PalazzoliSegretario Nazionale FLAI CGIL

5

The aim of this work is to provide a picture of the employment situation, the status of collective bargain-ing, and the quality of industrial relations in European fisheries and aquaculture as a tool for interpretingthe sector and as a starting point for the development of initiatives and policy proposals.This is the context in which was established the project “The impact of the reform of the Common FisheriesPolicy and the contribution of collective bargaining to the creation of more and better jobs to lead to a wayout of the crisis” which this publication is part of. The first part of the book illustrates the situation of the fisheries sector in Europe (fishing, aquaculture andprocessing) and provides a picture of the role of trade unions and the functioning of collective bargainingat European level through the collection and systematisation of the most up-to-date data available in theliterature. Particularly relevant for the reconstruction are the studies by section of the Scientific, Technicaland Economic Committee for Fisheries of the European Commission, the working documents of theEuropean Commission on the impact of the CFP with a view to its reform, as well as the Eurostat, FAO andUN databases.1

The second part of this publication focuses on the six countries that were the object of the case studies:Belgium, Denmark, France, Italy, the Netherlands and Spain. The analyses were carried out with the coop-eration of the national unions as part of the project “The impact of the reform of the Common FisheriesPolicy and the contribution of collective bargaining to the creation of more and better jobs o lead to a wayout of the crisis” . The trade unions were involved in the analysis between November 2013 and June 2014 through their par-ticipation in a focus group, the compilation of questionnaires and fact sheets on collective bargaining inthe sector, as well as during the fruitful comparisons on the subject which took place in the context of train-ing meetings which took place in the major ports of the participating countries. The meetings, which were held in Thyboron, Vigo, Boulogne-sur-Mer and Ostend in May and June 2014 inthe presence of workers, employees, owners, representatives of the institutions and the trade unions werean important opportunity for comparing the different European scenarios and a step towards understand-ing the impact of the Common Fisheries Policy on local economies.

1 For references to the documents in question, see the bibliography.

M E T H O D O L O G I C A L N O T E

F I S H I N G I N E U R O P E

1

6

PART

18

The economic framework

With a value of €55 billion and 12 million tons, the European Union is the world’s largest market for fish-ery and aquaculture products. Albeit with substantial differences between countries, Europeans consumeon average 22kg of fish per year, 15% of their protein intake and these totals are expected to increase.

T H E E U R O P E A N F I S H I N G F L E E T

In 2011, small-sized boats made up almost 56% of the total fleet in terms of number of vessels, 6% in termsof gross tonnage and 25% in terms of engine power. The ocean fleet, although representing only 1% of thetotal in terms of the number of vessels, constituted 19% of gross tonnage and 7% of engine power. The indus-trial fleet, finally, accounted for 43% in terms of vessels, 75% of gross tonnage and 68% of engine power.In 2011, the European fleet landed 4,699 tons of fish, equivalent to 6.4 billion euros in volume. TheDanish fleet produced, in terms of weight, 20% of the total fish catch, followed by the UK with 17%.With regard to the value of fish landed, Italy produced 22% of the European total, followed by France(21%) and the UK (19%).As in 2010, herring was the most fished species in terms of volume, with a total of 483,000 tons caught,while mackerel reached the highest value of 390 million euros, an increase of 36% over the previous year.The first sales prices increased on average over the previous year: the first price of mackerel, in particular,increased by 20%, despite a simultaneous increase in the volume of catch of 13%, which indicates a sig-nificant increase in demand. The total income generated by the European fleet in 2011 amounted to €7.13 billion divided between €7billion from the sale of fish and €131 million in other revenue, an increase of 7.6% over the previous year.Total costs (excluding fishing rights) amounted to €6.7 billion in 2011, an increase of 7% on the previousyear, caused mainly by the costs of labour and fuel; other costs associated with production amounted to€1.02 billion, and fixed costs were approximately €1.2 billion (of which €571 million was for maintenance).In 2011, the EU fleet paid about €776 million in terms of depreciation and approximately €101 million inopportunity costs of capital.

PART

1

9

instead was the one with the highest ratio between gross value added and profit (64%), followed byDenmark (63%) and Romania (61%).As regards gross profit, the Italian fleet produced 24% of the European total, the best result in absolute terms,followed by the fleets of the United Kingdom (16%) and France (14%). In relative terms instead, the Danishfleet recorded the best performance with 34% of the ratio between GVA and gross profit, followed The UKachieved the highest net profit (38% of the EU total), followed by France (26%) and Italy (19%). The Latvianfleet got the best ratio for net income/profit (28%), followed by the Romanian (17%) and British fleets (16%).

PART

1

11

The 2011 results showed an increase in the profitability of the European fishing fleet compared to 2010.The amount of gross value added (GVA), gross profit and net profit generated by the European fishing fleetin 2011 were, respectively, €3.4 billion (+ 3.6% compared to 2010), €1.29 billion and €410 million.While 13 out of 19 states reported net profit in 2011, 6 countries – Bulgaria, Ireland, Finland, Germany,Malta and Slovenia – recorded a loss in the sector. The Spanish fleet is the one that recorded the highest gross value added in absolute terms (25% of theEuropean total), followed by the French and Italian fleets, each with 17% of the total. The Portuguese fleet

PART

110

FIGURE 2Catch per Member State (2011) (volume in tonnes live weight and percentage of total)

ES 860 030 17.59 %DK 738 846 15.11 %UK 599 523 12.26%FR 443 549 9.07 %NL 364 964 7.46%DE 224 592 4.59%PT 214 779 4.39%IT 212 730 4.35%IE 206 177 4.22%SE 179 836 3.68%PL 169 593 3.47 %LV 156 130 3.19 %LT 137 063 2.80 %FI 119 686 2.45 %EE 77 942 1.59 %HR 70 534 1.44 %EL 62 847 1.29 %BE 22 191 0.45 %BG 8 956 0.18 %HU * 6 216 0.13 %CZ * 3 990 0.08 %RO 3 254 0.07 %MT 1 920 0.04 %SK * 1 608 0.03 %CY 1 163 0.02 %SI 719 0.01 %AT* 350 0.01 %Total EU-28 4 889 188 100.00%* 2010 data. Source: European Commission, Facts and figures on the CFP (2014)

Main indicators related to fishing fleets of the member states (2011)

BEL 89 15,8 51,2 377 342 40,3 17,2 20,1 79,4 82,35 35,9 9,5 0,5 45,1

BGR 1010 5,0 33,7 3276 1668 1,1 16,1 7,6 2,7 2,70 -1,5 -3,1 -3,3 0,1

CYP n.a. n.a. n.a. n.a. n.a. n.a. n.a. 1,2 8,0 7,99 n.a. n.a. n.a. n.a.

DEU 1664 64,6 151,4 1639 1258 41,6 109,3 78,1 125,5 129,63 57,8 14,8 -6,4 97,9

DNK 2663 67,5 238,8 1460 1661 88,0 116,0 711,0 412,8 394,50 249,1 134,5 45,8 406,4

ESP 10892 414,7 936,0 36294 32194 n.a. n.a. n.a. n.a. 1982,06 839,0 180,5 18,6 516,5

EST 934 14,7 39,6 n.a. n.a. n.a. n.a. 63,3 13,8 13,78 n.a. n.a. n.a. n.a.

FIN 3365 16,7 172,8 1722 316 14,2 148,2 119,7 32,5 35,53 12,3 3,9 -0,7 69,2

FRA 6004 161,0 879,9 10713 7447 341,6 492,8 463,7 1050,7 1156,37 590,8 181,2 107,2 1300,7

GBR 6467 207,2 825,9 12405 7192 268,1 414,5 597,4 948,7 971,78 429,5 202,2 157,7 525,4

GRC n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

IRL 2162 72,2 202,4 4714 3166 63,8 49,5 199,5 200,3 246,32 111,6 45,2 -14,3 367,4

ITA 14715 185,0 1236,5 28726 20599 408,2 1748,5 212,4 1101,0 1101,03 582,9 303,2 79,6 917,9

LTU 171 46,0 54,4 768 575 26,4 10,3 114,7 65,6 46,96 12,9 7,5 4,7 53,2

LVA 319 8,5 22,3 712 378 6,5 19,6 63,1 21,8 22,62 10,7 7,4 6,2 9,7

MLT 1087 12,1 83,4 225 155 2,6 41,3 1,9 11,4 11,37 6,1 -1,5 -22,2 81,6

NLD 738 130,5 290,1 2763 1768 193,8 46,1 339,4 326,6 327,61 109,1 30,8 3,0 343,8

POL 805 38,0 88,1 2411 1576 12,7 58,2 179,9 46,0 46,41 21,5 8,8 4,8 91,0

PRT 8557 102,5 377,4 17234 17188 107,3 375,1 178,8 344,2 442,38 283,6 129,2 29,0 358,0

ROU 488 1,0 7,0 454 28 0,2 2,9 0,5 1,4 1,42 0,9 0,4 0,2 3,9

SVN 186 1,0 10,9 114,0 77,0 0,5 7,6 0,7 2,0 2,68 1,6 0,0 -0,4 4,5

SWE 1359 32,9 178,1 1679,0 974,0 40,9 83,7 173,4 116,5 130,50 59,8 32,5 0,2 164,3

Source: Scientific and Technical Committee for Fisheries (STECF), 2013

Coun

try

Num

ber

of v

esse

ls

Gro

ss T

onna

ge(1

000

GT)

Kilo

wat

ts

(100

0 kW

)

Tota

l job

s

FTEs

Ener

gy c

onsu

mpt

ion

(mill

ion

litre

s)

Day

s at

Sea

(tho

usan

d)

Wei

ght

of la

ndin

gs(t

hous

and

tonn

es)

Land

ed v

alue

(€ m

illio

n)

Inco

me

(€ m

illio

n)

GVA

(€ m

illio

n)

Gro

ss P

rofit

(€ m

illio

n)

Net

pro

fit(€

mill

ion)

Fixe

d A

sset

val

ue(€

mill

ion)

FIGURE 1

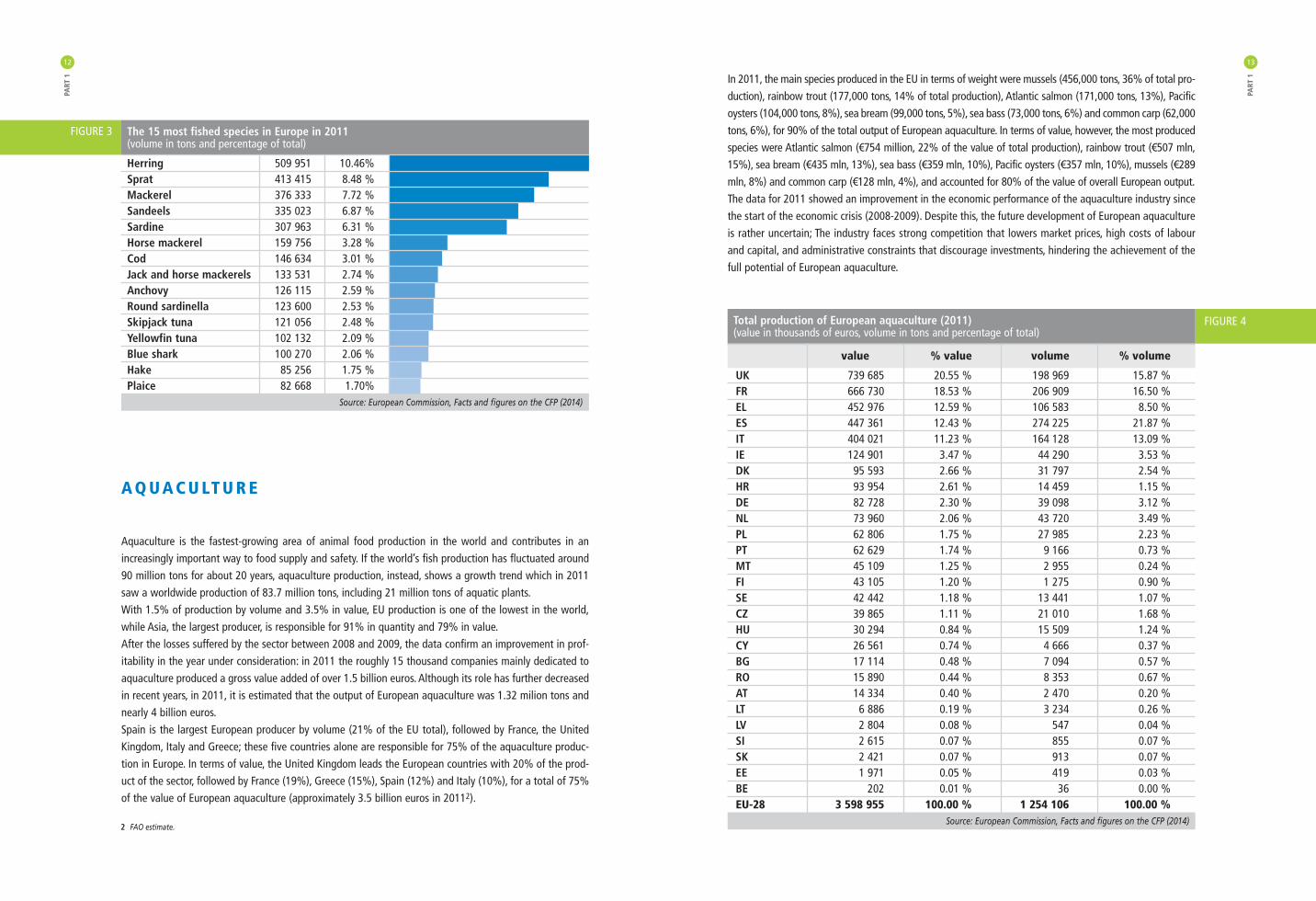

In 2011, the main species produced in the EU in terms of weight were mussels (456,000 tons, 36% of total pro-duction), rainbow trout (177,000 tons, 14% of total production), Atlantic salmon (171,000 tons, 13%), Pacificoysters (104,000 tons, 8%), sea bream (99,000 tons, 5%), sea bass (73,000 tons, 6%) and common carp (62,000tons, 6%), for 90% of the total output of European aquaculture. In terms of value, however, the most producedspecies were Atlantic salmon (€754 million, 22% of the value of total production), rainbow trout (€507 mln,15%), sea bream (€435 mln, 13%), sea bass (€359 mln, 10%), Pacific oysters (€357 mln, 10%), mussels (€289mln, 8%) and common carp (€128 mln, 4%), and accounted for 80% of the value of overall European output.The data for 2011 showed an improvement in the economic performance of the aquaculture industry sincethe start of the economic crisis (2008-2009). Despite this, the future development of European aquacultureis rather uncertain; The industry faces strong competition that lowers market prices, high costs of labourand capital, and administrative constraints that discourage investments, hindering the achievement of thefull potential of European aquaculture.

PART

1

13

A Q U A C U LT U R E

Aquaculture is the fastest-growing area of animal food production in the world and contributes in anincreasingly important way to food supply and safety. If the world’s fish production has fluctuated around90 million tons for about 20 years, aquaculture production, instead, shows a growth trend which in 2011saw a worldwide production of 83.7 million tons, including 21 million tons of aquatic plants. With 1.5% of production by volume and 3.5% in value, EU production is one of the lowest in the world,while Asia, the largest producer, is responsible for 91% in quantity and 79% in value.After the losses suffered by the sector between 2008 and 2009, the data confirm an improvement in prof-itability in the year under consideration: in 2011 the roughly 15 thousand companies mainly dedicated toaquaculture produced a gross value added of over 1.5 billion euros. Although its role has further decreasedin recent years, in 2011, it is estimated that the output of European aquaculture was 1.32 milion tons andnearly 4 billion euros.Spain is the largest European producer by volume (21% of the EU total), followed by France, the UnitedKingdom, Italy and Greece; these five countries alone are responsible for 75% of the aquaculture produc-tion in Europe. In terms of value, the United Kingdom leads the European countries with 20% of the prod-uct of the sector, followed by France (19%), Greece (15%), Spain (12%) and Italy (10%), for a total of 75%of the value of European aquaculture (approximately 3.5 billion euros in 20112).

PART

112

FIGURE 3 The 15 most fished species in Europe in 2011 (volume in tons and percentage of total)

Herring 509 951 10.46%Sprat 413 415 8.48 %Mackerel 376 333 7.72 %Sandeels 335 023 6.87 %Sardine 307 963 6.31 %Horse mackerel 159 756 3.28 %Cod 146 634 3.01 %Jack and horse mackerels 133 531 2.74 %Anchovy 126 115 2.59 %Round sardinella 123 600 2.53 %Skipjack tuna 121 056 2.48 %Yellowfin tuna 102 132 2.09 %Blue shark 100 270 2.06 %Hake 85 256 1.75 %Plaice 82 668 1.70%

Source: European Commission, Facts and figures on the CFP (2014)

2 FAO estimate.

Total production of European aquaculture (2011) (value in thousands of euros, volume in tons and percentage of total)

value % value volume % volume

UK 739 685 20.55 % 198 969 15.87 %FR 666 730 18.53 % 206 909 16.50 %EL 452 976 12.59 % 106 583 8.50 %ES 447 361 12.43 % 274 225 21.87 %IT 404 021 11.23 % 164 128 13.09 %IE 124 901 3.47 % 44 290 3.53 %DK 95 593 2.66 % 31 797 2.54 %HR 93 954 2.61 % 14 459 1.15 %DE 82 728 2.30 % 39 098 3.12 %NL 73 960 2.06 % 43 720 3.49 %PL 62 806 1.75 % 27 985 2.23 %PT 62 629 1.74 % 9 166 0.73 %MT 45 109 1.25 % 2 955 0.24 %FI 43 105 1.20 % 1 275 0.90 %SE 42 442 1.18 % 13 441 1.07 %CZ 39 865 1.11 % 21 010 1.68 %HU 30 294 0.84 % 15 509 1.24 %CY 26 561 0.74 % 4 666 0.37 %BG 17 114 0.48 % 7 094 0.57 %RO 15 890 0.44 % 8 353 0.67 %AT 14 334 0.40 % 2 470 0.20 %LT 6 886 0.19 % 3 234 0.26 % LV 2 804 0.08 % 547 0.04 %SI 2 615 0.07 % 855 0.07 %SK 2 421 0.07 % 913 0.07 %EE 1 971 0.05 % 419 0.03 %BE 202 0.01 % 36 0.00 %EU-28 3 598 955 100.00 % 1 254 106 100.00 %

Source: European Commission, Facts and figures on the CFP (2014)

FIGURE 4

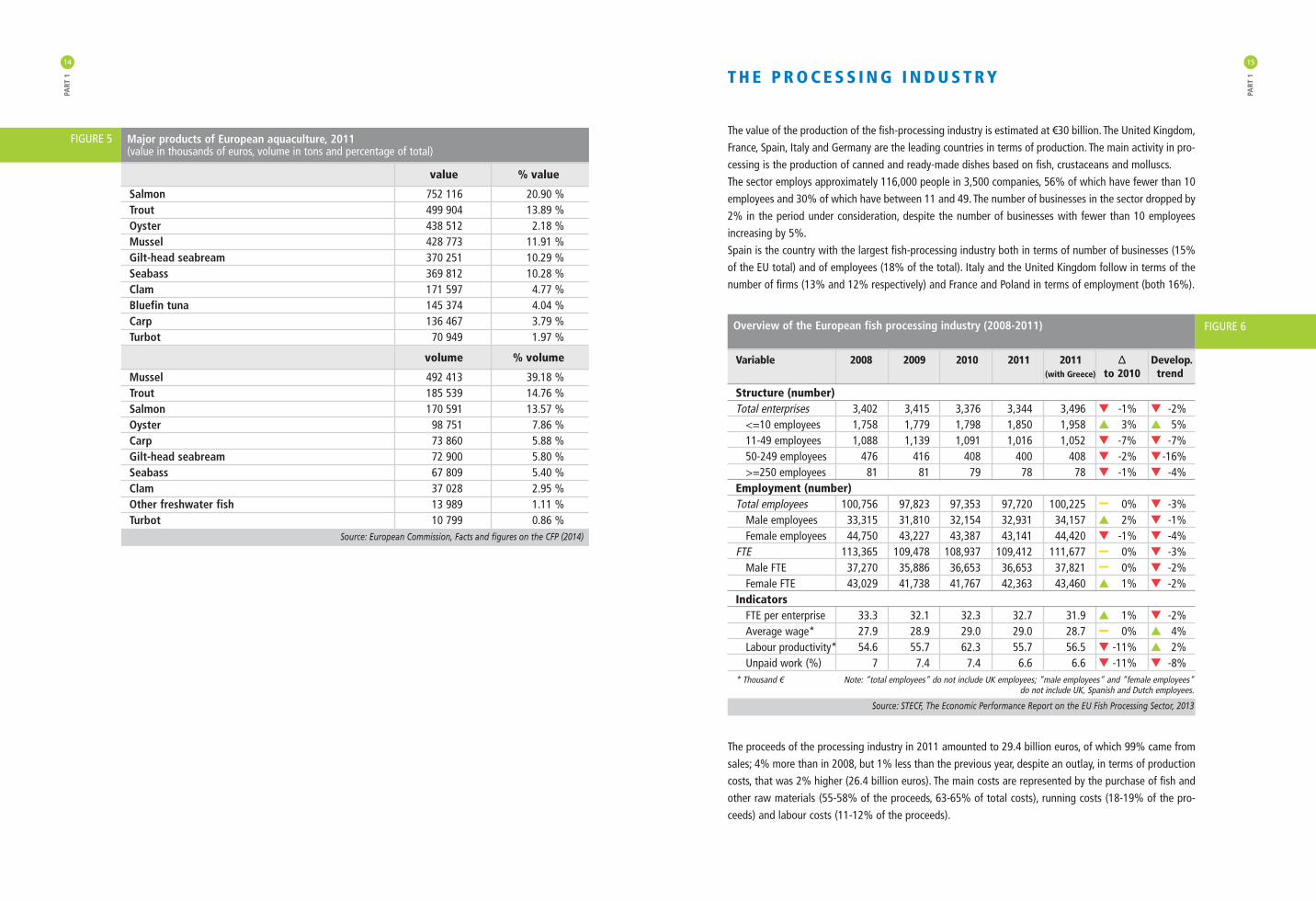

T H E P R O C E S S I N G I N D U S T R Y

The value of the production of the fish-processing industry is estimated at €30 billion. The United Kingdom,France, Spain, Italy and Germany are the leading countries in terms of production. The main activity in pro-cessing is the production of canned and ready-made dishes based on fish, crustaceans and molluscs. The sector employs approximately 116,000 people in 3,500 companies, 56% of which have fewer than 10employees and 30% of which have between 11 and 49. The number of businesses in the sector dropped by2% in the period under consideration, despite the number of businesses with fewer than 10 employeesincreasing by 5%. Spain is the country with the largest fish-processing industry both in terms of number of businesses (15%of the EU total) and of employees (18% of the total). Italy and the United Kingdom follow in terms of thenumber of firms (13% and 12% respectively) and France and Poland in terms of employment (both 16%).

The proceeds of the processing industry in 2011 amounted to 29.4 billion euros, of which 99% came fromsales; 4% more than in 2008, but 1% less than the previous year, despite an outlay, in terms of productioncosts, that was 2% higher (26.4 billion euros). The main costs are represented by the purchase of fish andother raw materials (55-58% of the proceeds, 63-65% of total costs), running costs (18-19% of the pro-ceeds) and labour costs (11-12% of the proceeds).

PART

1

15PA

RT 1

14

Major products of European aquaculture, 2011 (value in thousands of euros, volume in tons and percentage of total)

value % value

Salmon 752 116 20.90 %Trout 499 904 13.89 %Oyster 438 512 2.18 %Mussel 428 773 11.91 %Gilt-head seabream 370 251 10.29 %Seabass 369 812 10.28 %Clam 171 597 4.77 %Bluefin tuna 145 374 4.04 %Carp 136 467 3.79 %Turbot 70 949 1.97 %

volume % volume

Mussel 492 413 39.18 %Trout 185 539 14.76 %Salmon 170 591 13.57 %Oyster 98 751 7.86 %Carp 73 860 5.88 %Gilt-head seabream 72 900 5.80 %Seabass 67 809 5.40 %Clam 37 028 2.95 %Other freshwater fish 13 989 1.11 %Turbot 10 799 0.86 %

Source: European Commission, Facts and figures on the CFP (2014)

Overview of the European fish processing industry (2008-2011)

Variable 2008 2009 2010 2011 2011 Δ Develop.(with Greece) to 2010 trend

Structure (number)Total enterprises 3,402 3,415 3,376 3,344 3,496 q -1% q -2%

<=10 employees 1,758 1,779 1,798 1,850 1,958 p 3% p 5%11-49 employees 1,088 1,139 1,091 1,016 1,052 q -7% q -7%50-249 employees 476 416 408 400 408 q -2% q-16%>=250 employees 81 81 79 78 78 q -1% q -4%

Employment (number)Total employees 100,756 97,823 97,353 97,720 100,225 0% q -3%

Male employees 33,315 31,810 32,154 32,931 34,157 p 2% q -1%Female employees 44,750 43,227 43,387 43,141 44,420 q -1% q -4%

FTE 113,365 109,478 108,937 109,412 111,677 0% q -3%Male FTE 37,270 35,886 36,653 36,653 37,821 0% q -2%Female FTE 43,029 41,738 41,767 42,363 43,460 p 1% q -2%

IndicatorsFTE per enterprise 33.3 32.1 32.3 32.7 31.9 p 1% q -2%Average wage* 27.9 28.9 29.0 29.0 28.7 0% p 4%Labour productivity* 54.6 55.7 62.3 55.7 56.5 q -11% p 2%Unpaid work (%) 7 7.4 7.4 6.6 6.6 q -11% q -8%

* Thousand € Note: “total employees” do not include UK employees; “male employees” and “female employees”do not include UK, Spanish and Dutch employees.

Source: STECF, The Economic Performance Report on the EU Fish Processing Sector, 2013

FIGURE 6

FIGURE 5

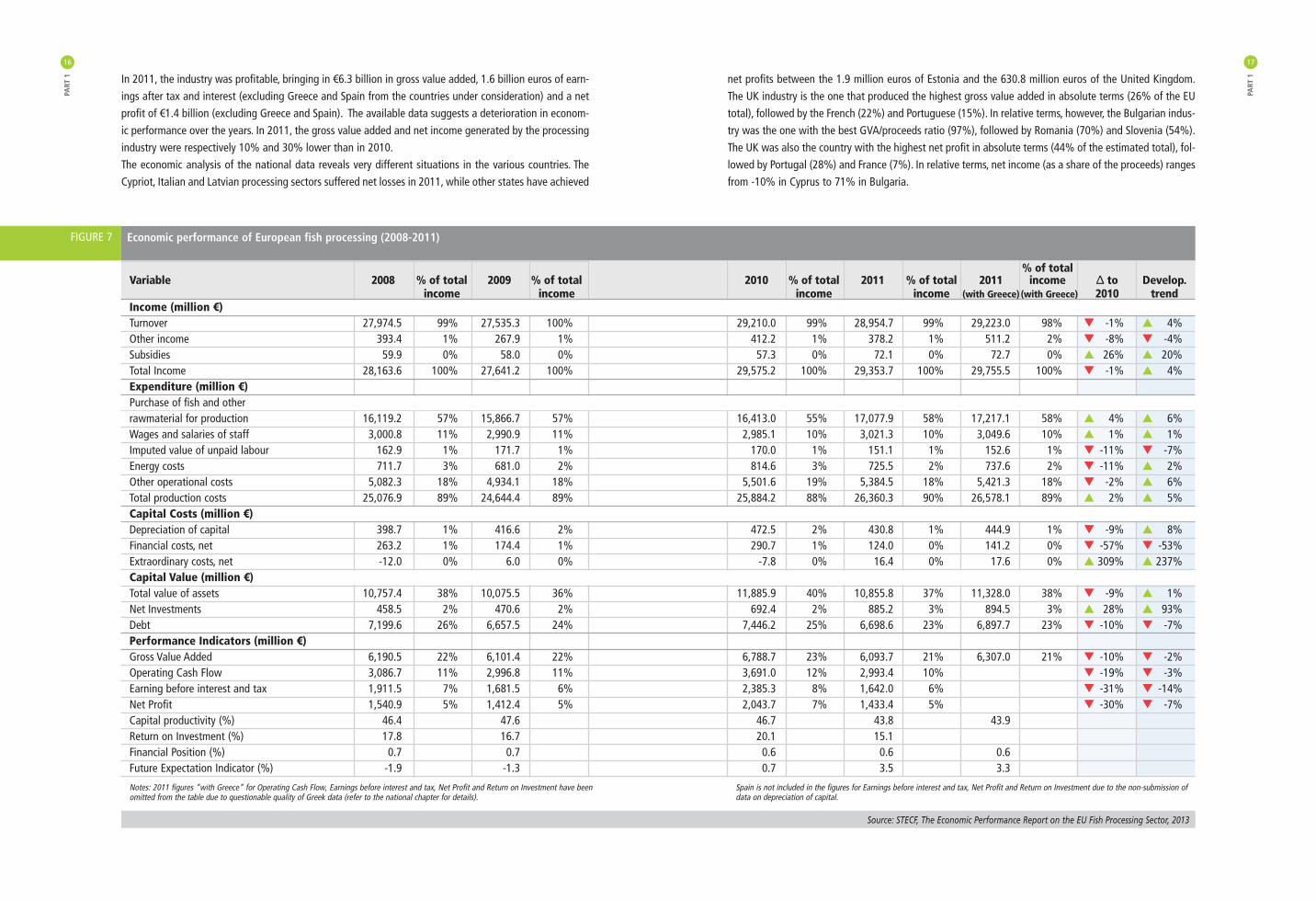

net profits between the 1.9 million euros of Estonia and the 630.8 million euros of the United Kingdom.The UK industry is the one that produced the highest gross value added in absolute terms (26% of the EUtotal), followed by the French (22%) and Portuguese (15%). In relative terms, however, the Bulgarian indus-try was the one with the best GVA/proceeds ratio (97%), followed by Romania (70%) and Slovenia (54%).The UK was also the country with the highest net profit in absolute terms (44% of the estimated total), fol-lowed by Portugal (28%) and France (7%). In relative terms, net income (as a share of the proceeds) rangesfrom -10% in Cyprus to 71% in Bulgaria.

PART

1

17

In 2011, the industry was profitable, bringing in €6.3 billion in gross value added, 1.6 billion euros of earn-ings after tax and interest (excluding Greece and Spain from the countries under consideration) and a netprofit of €1.4 billion (excluding Greece and Spain). The available data suggests a deterioration in econom-ic performance over the years. In 2011, the gross value added and net income generated by the processingindustry were respectively 10% and 30% lower than in 2010.The economic analysis of the national data reveals very different situations in the various countries. TheCypriot, Italian and Latvian processing sectors suffered net losses in 2011, while other states have achieved

PART

116

Economic performance of European fish processing (2008-2011)

% of total Variable 2008 % of total 2009 % of total 2010 % of total 2011 % of total 2011 income Δ to Develop.

income income income income (with Greece) (with Greece) 2010 trendIncome (million €)Turnover 27,974.5 99% 27,535.3 100% 29,210.0 99% 28,954.7 99% 29,223.0 98% q -1% p 4%Other income 393.4 1% 267.9 1% 412.2 1% 378.2 1% 511.2 2% q -8% q -4%Subsidies 59.9 0% 58.0 0% 57.3 0% 72.1 0% 72.7 0% p 26% p 20%Total Income 28,163.6 100% 27,641.2 100% 29,575.2 100% 29,353.7 100% 29,755.5 100% q -1% p 4%Expenditure (million €)Purchase of fish and other rawmaterial for production 16,119.2 57% 15,866.7 57% 16,413.0 55% 17,077.9 58% 17,217.1 58% p 4% p 6%Wages and salaries of staff 3,000.8 11% 2,990.9 11% 2,985.1 10% 3,021.3 10% 3,049.6 10% p 1% p 1%Imputed value of unpaid labour 162.9 1% 171.7 1% 170.0 1% 151.1 1% 152.6 1% q -11% q -7%Energy costs 711.7 3% 681.0 2% 814.6 3% 725.5 2% 737.6 2% q -11% p 2%Other operational costs 5,082.3 18% 4,934.1 18% 5,501.6 19% 5,384.5 18% 5,421.3 18% q -2% p 6%Total production costs 25,076.9 89% 24,644.4 89% 25,884.2 88% 26,360.3 90% 26,578.1 89% p 2% p 5%Capital Costs (million €)Depreciation of capital 398.7 1% 416.6 2% 472.5 2% 430.8 1% 444.9 1% q -9% p 8%Financial costs, net 263.2 1% 174.4 1% 290.7 1% 124.0 0% 141.2 0% q -57% q -53%Extraordinary costs, net -12.0 0% 6.0 0% -7.8 0% 16.4 0% 17.6 0% p 309% p 237%Capital Value (million €)Total value of assets 10,757.4 38% 10,075.5 36% 11,885.9 40% 10,855.8 37% 11,328.0 38% q -9% p 1%Net Investments 458.5 2% 470.6 2% 692.4 2% 885.2 3% 894.5 3% p 28% p 93%Debt 7,199.6 26% 6,657.5 24% 7,446.2 25% 6,698.6 23% 6,897.7 23% q -10% q -7%Performance Indicators (million €)Gross Value Added 6,190.5 22% 6,101.4 22% 6,788.7 23% 6,093.7 21% 6,307.0 21% q -10% q -2%Operating Cash Flow 3,086.7 11% 2,996.8 11% 3,691.0 12% 2,993.4 10% q -19% q -3%Earning before interest and tax 1,911.5 7% 1,681.5 6% 2,385.3 8% 1,642.0 6% q -31% q -14%Net Profit 1,540.9 5% 1,412.4 5% 2,043.7 7% 1,433.4 5% q -30% q -7%Capital productivity (%) 46.4 47.6 46.7 43.8 43.9Return on Investment (%) 17.8 16.7 20.1 15.1Financial Position (%) 0.7 0.7 0.6 0.6 0.6Future Expectation Indicator (%) -1.9 -1.3 0.7 3.5 3.3

Notes: 2011 figures “with Greece” for Operating Cash Flow, Earnings before interest and tax, Net Profit and Return on Investment have been omitted from the table due to questionable quality of Greek data (refer to the national chapter for details).

Source: STECF, The Economic Performance Report on the EU Fish Processing Sector, 2013

FIGURE 7

Spain is not included in the figures for Earnings before interest and tax, Net Profit and Return on Investment due to the non-submission ofdata on depreciation of capital.

The aquaculture sector too has a significant socio-economic impact, with a turnover of approximately €3.5billion and 85,000 employees (part-time and full-time), of whom 27% are women.The high prevalence of part-time workers in this sector should be highlighted because from the compari-son of total employment and FTE, it appears that the employees made equivalent with full-time, come to45% of the total. In the processing industry, in 2011, total employment was 100,225, with an average salary of €28,674.Leaving aside the case of Greece, between 2008 and 2011, there was a fall in employment of 3%, in par-allel with an increase of the average wage by 4%.

PART

1

19

E M P L OY M E N T

The fisheries sector plays a fundamental role in many European regions in terms of its contribution toemployment and local economic activities; in some coastal communities, more than half of jobs are relat-ed to the fisheries sector. Employment in this sector tends to be concentrated in a few countries. Spain alone is home to a quarter ofthose employed in fishing in Europe and the four countries with the highest levels of employment (Spain,Italy, Portugal and Greece) have 70% of the total. In 2011, the number of fishermen employed in the European fleet was 127,686, a decrease compared to2010 of almost 6%3. Spain confirmed its leading position in terms of employment levels (more than 32,000FTE4), followed by Italy (20,600 FTE) and Portugal (17,100 FTE). 41% of the total workforce is employed inthe small vessels fleet, 51% in the industrial fleet and 7% in the ocean fleet.In 2011, wage levels rose to an average total of €21,600: €10,700 in the small vessels, €29,000 in theindustrial and €27,000 in the ocean fleet.

PART

118

3 This does not include Cyprus, Estonia and Greece.4 Full Time Equivalents: unit of measure which, consisting of one day of full-time work, equalises total hours and allows a comparison between

employees’ activities over differing period of employment.

Dependence on Employment in the European regions of the fisheries sector (2011)

Source: European Commission, Facts and figures on the CFP (2014)

FIGURE 8

FIGURE 9Employment in the fisheries and aquaculture sector (2011) (measured in full-time equivalents)

Fisheries1

ES 32 194IT 20 599PT 16 773EL 12 169 2

UK 11 277FR 7 447IE 3 428NL 1 768BG 1 668DK 1 661PL 1 576DE 1 258SE 974CY 911 3

LT 575EE 521 3

LV 378BE 341FI 316MT 155SI 77RO 28

Source: European Commission, Facts and figures on the CFP (2014)

Aquaculture4

FR 10 658ES 6 639EL 5 559 5

UK 2 671IT 2 116PT 1 749RO 1 047IE 958FI 349DK 299CY 276BG 270SE 263MT 165

4 Data not available for AT, BE, CZ, EE, HR, HU, LT, LU, LV, NL and SK. For the following Member States data only cover marine aquaculture: DE 18, PL 49 and SI 32.

5 Total employment (full-time and part-time).

1 Data not available for AT, CZ, HR, HU, LU and SK.2 2010 data taken from the Hellenic Statistical Authority.3 2010 data.

PART

1

21

T H E M A R K E T 5

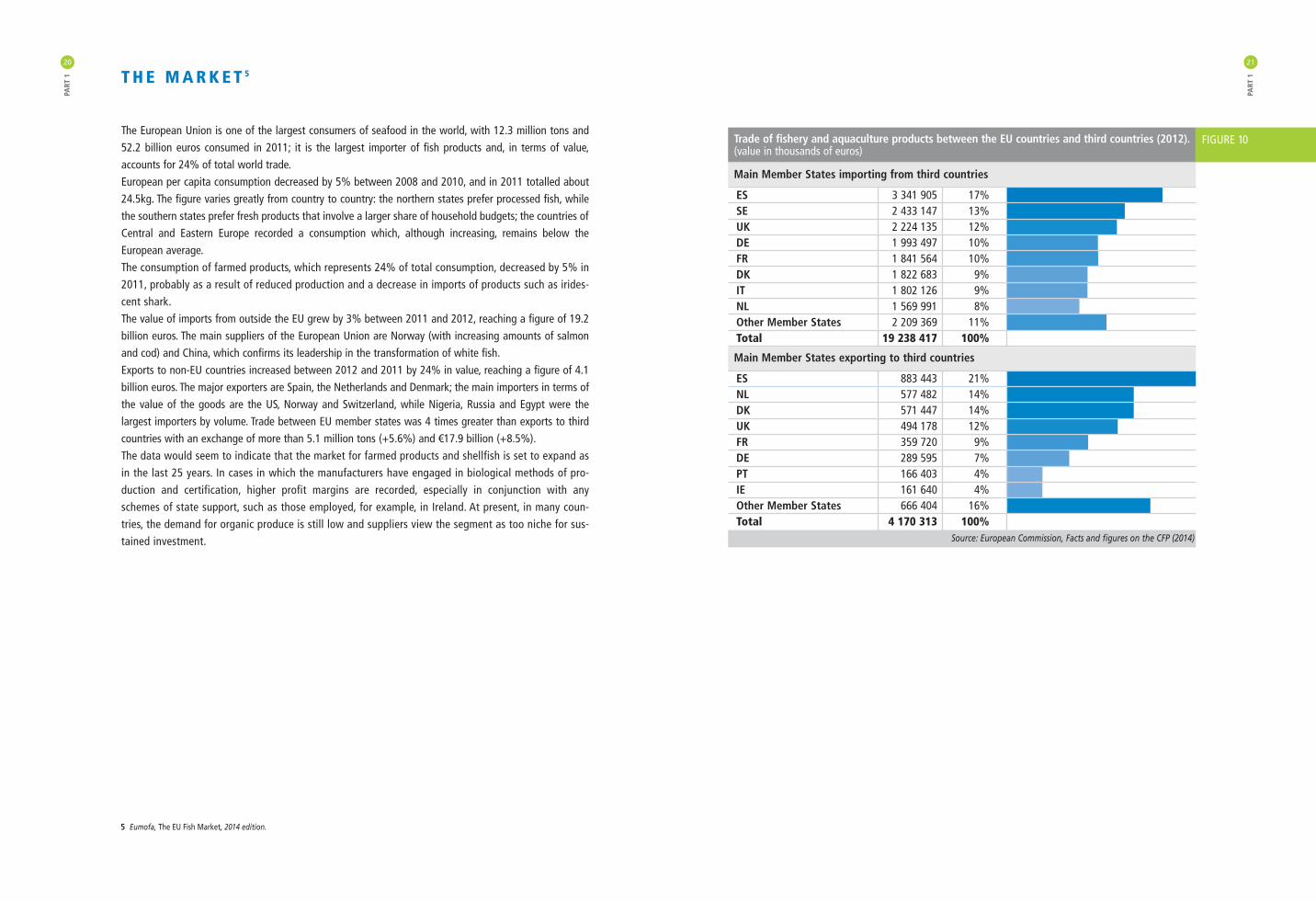

The European Union is one of the largest consumers of seafood in the world, with 12.3 million tons and52.2 billion euros consumed in 2011; it is the largest importer of fish products and, in terms of value,accounts for 24% of total world trade. European per capita consumption decreased by 5% between 2008 and 2010, and in 2011 totalled about24.5kg. The figure varies greatly from country to country: the northern states prefer processed fish, whilethe southern states prefer fresh products that involve a larger share of household budgets; the countries ofCentral and Eastern Europe recorded a consumption which, although increasing, remains below theEuropean average.The consumption of farmed products, which represents 24% of total consumption, decreased by 5% in2011, probably as a result of reduced production and a decrease in imports of products such as irides-cent shark.The value of imports from outside the EU grew by 3% between 2011 and 2012, reaching a figure of 19.2billion euros. The main suppliers of the European Union are Norway (with increasing amounts of salmonand cod) and China, which confirms its leadership in the transformation of white fish.Exports to non-EU countries increased between 2012 and 2011 by 24% in value, reaching a figure of 4.1billion euros. The major exporters are Spain, the Netherlands and Denmark; the main importers in terms ofthe value of the goods are the US, Norway and Switzerland, while Nigeria, Russia and Egypt were thelargest importers by volume. Trade between EU member states was 4 times greater than exports to thirdcountries with an exchange of more than 5.1 million tons (+5.6%) and €17.9 billion (+8.5%). The data would seem to indicate that the market for farmed products and shellfish is set to expand asin the last 25 years. In cases in which the manufacturers have engaged in biological methods of pro-duction and certification, higher profit margins are recorded, especially in conjunction with anyschemes of state support, such as those employed, for example, in Ireland. At present, in many coun-tries, the demand for organic produce is still low and suppliers view the segment as too niche for sus-tained investment.

PART

120

5 Eumofa, The EU Fish Market, 2014 edition.

Trade of fishery and aquaculture products between the EU countries and third countries (2012).(value in thousands of euros)

Main Member States importing from third countries

ES 3 341 905 17%SE 2 433 147 13%UK 2 224 135 12%DE 1 993 497 10%FR 1 841 564 10%DK 1 822 683 9%IT 1 802 126 9%NL 1 569 991 8%Other Member States 2 209 369 11%Total 19 238 417 100%

Main Member States exporting to third countries

ES 883 443 21%NL 577 482 14%DK 571 447 14%UK 494 178 12%FR 359 720 9%DE 289 595 7%PT 166 403 4%IE 161 640 4%Other Member States 666 404 16%Total 4 170 313 100%

Source: European Commission, Facts and figures on the CFP (2014)

FIGURE 10

alent to law: binding for all the employers and workers concerned and retroactive with regard to theeffects that ensure its persistence, even if the parties withdraw from the agreement (“generalised” and“binding” application of the agreement);

2. it formalises the advisory role of the trade unions and management representatives from the stage ofdrawing up Community rules by the Commission (Article 154 TFEU). Before submitting proposals in thearea of social policies, the Commission has to consult management and labour on their possible orien-tation; where action is taken by the EU, the trade unions and management representatives should exam-ine the content and submit to the Commission an opinion or a recommendation if both sides have man-aged to reach a common position;

3. it provides for the normative power of the collective agreement (in conjunction with Articles 154 and 155TFEU), which consists of the possibility for the trade unions and management representatives, in the set-ting of the second consultation on the merits of the proposal of the Commission, to claim for themselvesthe drafting of the regulations on the matter. The agreement will have to be transmuted into a norma-tive provision endorsed by the Commission (the Commission will carry out a control that takes intoaccount the representativeness of the contracting parties, their mandate and the legality of each clauseof the collective agreement in terms of European Union law, as well as the relevance of European actionon the subject and the consistency of the measures to be taken with regard to small and medium-sizedenterprises), and submitted to the European Council (becoming a directive). It is widely held that theterms of the agreement cannot be changed by the Council, but only accepted or rejected “in toto”.

The possibility of concluding collective agreements at European level raises several issues relating to theeffects, both in terms of the member states (insofar as they are required to implement them) and individ-ual employees.In any case, it is to be excluded that a European collective agreement might operate with universal regu-latory effects in different countries. The direct effect would depend, that is, on national legislations. In theItalian case, in particular, it would find a limit to its generalised efficacy simply with the collective agree-ment thanks to case law as a result of the non-application of Article 39 of the Constitution. The most critical elements of the system concern the effective representativeness and negotiating capaci-ty, in particular, the absence of an effective mandate from their members and, therefore, of the power tobind themselves contractually with the counterparties. The problem of representativeness occurs in particular whenever the parties themselves are signatories toan agreement in the sense of Article 155 TFEU. In this case, the Commission must determine whether, inlight of the content of the agreement, the trade unions and management representatives have a sufficient-ly representative status overall and, where this is lacking, will refuse to implement it.The representativeness criteria are to some extent similar to those valid for the national trade unions andmanagement representatives: the trade unions and management representatives need to be organised atEuropean level, they need to consist of organisations recognised as an integral part of the structures of thetrade unions and management of the member states, they need to have the ability to negotiate agree-ments, and they need to have adequate facilities to enable them to participate effectively in the consulta-tion process.Based on these criteria, the Commission has drawn up a list, updated regularly, of the representative organ-isations including the European Trade Union Confederation (ETUC), UNICE-BUSINESS EUROPE and CEEP. As for the fishing sector, the organisations admitted to consultation by the European Commission are theETF, Europeche and COGECA.

PART

1

23

Bargaining and sectoral policies: the role of the trade unions and management representatives at European level

C O L L E C T I V E R E L AT I O N S AT E U R O P E A N L E V E L

Collective labour relations matters are particularly resistant to the influence of European Community law,even in its mildest forms.One fundamental reason lies in the marked heterogeneity of the various European collective legal systemsregarding labour, both as regards the forms of the legal regulation of such relationships, and as regards thefactual elements of the employment relationship. It needs to be added, on the one hand, the central posi-tion they occupy in the social structure and the widespread belief that state power should refrain as muchas possible from intervening, limiting itself to establishing a framework in support of collective bargaining.It is therefore understandable that there should be a widespread distrust of any directives that seek tointervene directly on the institutions of collective relations. It is doubted that collective bargaining as such falls within the competence of the European Union, buttending in the opposite direction we have:• Article 153.3 TFEU, which refers to the “representation and collective defence of the interests of workers

and employers”• Article 28 of the Nice Charter that enshrines the right to collective bargaining.

T H E R O L E O F T H E T R A D E U N I O N S A N D M A N A G E M E N T R E P R E S E N TAT I V E S

The agreement on social policy has led to the development of the consultative function carried out by thetrade unions and management representatives and the express recognition of transnational collective bar-gaining as a source of social regulation.In particular: 1. it provides for a state to entrust to the trade unions and management representatives, at their joint

request, the task of implementing the directives in specific areas of competence, but, in this case, thestate must take the necessary measures that will enable it to guarantee at all times the results requiredby said directives (Article 153, para. 4 TFEU). A widespread practice in Belgium, but which has to meetthe requirements identified by the Court of Justice to ensure that the contract can be considered equiv-

PART

122

tive usefulness of European negotiation all prevented the development of a real practice of collectivebargaining at European level, which is mostly concentrated in a few large multinational groups. Theseagreements usually contained procedural rather than regulatory content, in that they provide proceduresfor information and consultation between the company and workers’ representatives on matters for themost part different to those relating to national bargaining such as restructuring, corporate socialresponsibility and health and safety. The Commission has proposed calling these agreements “transna-tional texts” rather than true collective agreements. They have a binding value for the business (which isthe most identifiable partner in the relationship), while not exerting any direct effect on workers as partsof the individual relationship. The recognition of EWCs has provided a useful institutional basis for thedevelopment of collective relations in a company, even if the existing powers of EWCs are limited andnot directly related to the purpose of collective bargaining. These texts, despite the weakness of collec-tive social rights, are evidence of the spirit of initiative of the parties who voluntarily and in a totallyinformal way launch forms of social dialogue outside the institutional context.

European policies in the field of fisheries and aquaculture6

T H E C O M M O N F I S H E R I E S P O L I C Y

Fisheries is characterised by what is defined as the “tragedy of common assets”, a phenomenon in whichmultiple individuals acting in their own interest and competing with others to get “their” part, tend to over-exploit a common resource. That which a fisherman catches today cannot be caught by another tomorrow.In deciding their fishing strategies, fishermen do not take into account the impact that this will have onother operators (fewer resources, damage to habitats, etc). Without proper regulation of access rights,stocks will be exploited to levels that will lead to their decline and prevent their commercial exploitation.For these reasons, regulatory intervention is required and the “no EU action” option has to be abandoned.Since 1970, there has been a shared organisation of the markets in fishery and aquaculture products,which constitutes one of the pillars of the Common Fisheries Policy. Its current legal basis is Regulation(EU) No. 1379/2013.The objectives of the CFP are set out in Article 3, letter d), Article 4 letter d), and Articles 38 and 39 of theTFEU. Article 11 of the TFEU is also applied to the Common Fisheries Policy, according to which the require-ments linked to the protection of the environment must be integrated into the definition and implementationof Union policies and activities, in particular from the point of view of promoting sustainable development.Article 39 of the TFEU defines for agricultural policy, and therefore also for the CFP, the following objectives:

PART

1

25

C O L L E C T I V E B A R G A I N I N G I N E U R O P E

Collective bargaining is the most widespread and significant form of collective activity in most EU coun-tries that deals with the regulation of working conditions. The common regulation and progressive convergence of national systems might find in European collectivebargaining a significant tool for implementation precisely because this instrument is recognised in practi-cally all the legal systems. This is even more valid if we consider that almost all the states adopt a proce-dure for allocating general effectiveness (erga omnes) to the collective agreement. However, the promotion of the bargaining method has received unequal attention and priority in EU action.Despite the legal recognition of bargaining in the Maastricht Protocol, the inclusion of the trade unions andmanagement representatives in decision-making as legislators by the Treaty of Lisbon and the recognitionas fundamental rights of collective bargaining and the use of collective action (strikes) by the Treaty of Nice,the affirmation of those rights was not followed in practice by secondary legislation (implementation).The European experience of collective bargaining may be historically outlined in three types of activity:bilateral (or trilateral) activities, social dialogue, true collective bargaining (although the formula of socialdialogue is often used in the inclusive sense).• Bilateral or trilateral activities: these are bilateral or trilateral activities, with an EU presence, between the

parties, supported by a shared interest, aimed at finding converging guidelines on defined themes. Theyare particularly widespread at the sectoral level. These activities are carried out mainly within the jointsectoral committees, later replaced by the Sectoral Social Dialogue Committees since 1998 (members areappointed by the Commission on the proposal of sectoral organisations and have advisory functions withrespect to the Council and the Commission), often accompanied by the joint committees (activated exclu-sively or primarily at the initiative of the professional organisations). Their work leads to shared opinions,guidelines, codes of conduct, proper agreements pursuant to Article 155 TFEU (which become bindingonly if implemented by a directive on the part of the Council).

• European social dialogue: (tripartite meetings launched in 1985 at Val Duchesse) forms of discussion andexchange of views between trade unions and management representatives, promoted by the EU, directedat the search for converging positions on matters of common interest. There is a large set of bilateral andtrilateral interactions between trade unions and management representatives and between them and theCommission. For many, social dialogue and collective bargaining are seen as a possible continuum, but itis important not to confuse the nature of the dialogue which tends towards the collaborative, and which,despite the importance of the dialogue, is not binding. The role of these agreements is largely to exercisea form of orientation and pressure on the European Community authorities. The meetings took place from1985 to 1990 (on the topics of education, the impact of new technologies, mobility of labour, and themeans to improve the functioning of the European labour market) and did not achieve convergences thatwere strong enough to translate into meaningful guidance, especially for the national players. In 1992, theCommittee for Interprofessional Social Dialogue was established, on the initiative of the trade unions andmanagement representatives, where relations are informal and voluntary, and it is in this area that thegreatest results were achieved in the form of framework agreements adopted by the Council .

• Collective bargaining: the lack of social players with decision-making powers at the European level; theabsence of conflict at the supranational level; business resistance to accepting an additional level of reg-ulation; the hesitation of the national unions in transferring decision-making powers to the Europeanlevel with direct results on the working conditions of their members; as well as doubts about the effec-

PART

124

6 Services of the European Commission, SEC (2011) 884 definitive, cited.

• A fourth problem is the fact that the CFP had an extremely complex legal framework, which promotesmicromanagement and prevents the achievement of environmental sustainability.

• The external dimension of the CFP too has had worse results than expected, especially in the area of envi-ronmental sustainability, but also in terms of international governance.

The reformed CFP should allow the environmental, economic and social sustainability of the activities ofexploitation of fish resources. In legal terms these goals have the same importance and none of them canbe achieved in isolation.Guaranteeing the environmental sustainability of fisheries means ensuring that fishing is carried out in sucha way as not to prejudice the future exploitation of stocks. Fishing pressure, therefore, must be such as toproduce the maximum sustainable yield (MSY), an objective that is to be achieved with the greatesturgency for the stocks being depleted and, where possible, by 2015. Achieving environmental sustainabili-ty will also comply with the obligation, laid down in the framework directive on the strategy for the marineenvironment, to achieve a good environmental status in the marine environment by 2020.In order to achieve environmental sustainability it is necessary to:• eliminate the overexploitation of resources in the short term;• reduce as much as possible overcapacity and discarding catch;• establish a decision-making system in line with long-term sustainability that is flexible and able to adapt

to local conditions;• encourage the industry to take greater responsibility for the results and to comply with the law; • improve the availability of scientific and economic data.Ensuring economic sustainability means having fleets that are profitable and cost-effective in the long run.The same applies to processing, aquaculture and related activities, called on to work within the constraintsimposed by environmental sustainability and in the context of a competitive global market and consump-tion patterns that are constantly evolving.Ensuring social sustainability means transforming fisheries and related activities into a source of interest-ing jobs that ensure a fair standard of living for those who depend on them and allow the preservation offishing communities. As well as fishing activities themselves, social sustainability in these regions shouldbe based on economic diversification in related maritime sectors.

T H E R E F O R M E D C F P

The European Council and the Parliament adopted a new Common Fisheries Policy (CFP), which has been inforce since 1 January 2014. The new CFP aims to restore stocks to sustainable levels, put an end to fishingpractices that lead to a waste of resources, and create new opportunities for jobs and growth in coastal areas.To achieve this objective, the new policy provides for the prohibition of discarding fish, the strengthening ofrights in the fisheries sector, the decentralisation of decision-making, the strengthening of the aquaculture sec-tor, support for small-scale fisheries, the improvement of scientific knowledge about the state of stocks andthe assumption of responsibility in the waters of third countries through international agreements of the EU.

PART

1

27

• to increase agricultural productivity by promoting technical progress and ensuring the rational develop-ment of agricultural production and the optimum utilisation of production factors, in particular of labour;

• to ensure a fair standard of living for the agricultural community, in particular by increasing the individ-ual earnings of persons engaged in agriculture;

• to stabilise markets;• to ensure security of supply;• to ensure that supplies reach consumers at reasonable prices.

T H E I M PA C T O F T H E C F P 7

The reform of the Common Fisheries Policy represented an excellent opportunity to analyse and possiblyrevise the objectives and market policy instruments for fishery and aquaculture products.Starting in 2008, the Commission has carried out in-depth evaluations and consultations, with the dual aimof examining the effectiveness of the current legal framework and the trends that have appeared in the lastdecade in the markets of the EU, and then obtaining the views of interested parties.The previous common fisheries policy did not allow the guaranteeing of the sustainable exploitation of liv-ing aquatic resources despite the introduction of new instruments such as long-term management plansaimed at exploiting fish stocks at sustainable levels and rebuilding overexploited stocks, and the regionaladvisory councils intended to strengthen the dialogue between the interested parties and the Commission. The problems at the root of this failure are interdependent. Excess capacity is the main factor responsiblefor the overexploitation of resources. All the same, the reduction of quotas, designed to reduce overfish-ing, has only succeeded in further increasing excess capacity. Similarly, this is at the origin of the poor eco-nomic performance of the catch sector, which, in turn, pushes operators to practise overfishing in the shortterm to make up for the loss of income. In this situation the sector is forced to solicit continuous publicsupport, so the excess capacity remains and the TACs (total allowable catches) are set at levels higherthan those recommended in the scientific advice. Given these correlations, the problems can be sum-marised as follows.• The main problem of the CFP is the lack of environmental sustainability due to overfishing, which all the

other problems stem from. Fleet overcapacity, TACs that do not comply with scientific advice and the lackof prioritisation of the objectives are the main factors responsible for the overfishing problem. To theseare added the principle of relative stability, the high level of discarded fish, poor compliance with the rulesand lack of sufficient scientific advice.

• The second problem is the lack of economic sustainability that characterises the catch sector in particu-lar. Many fleets are unprofitable and vulnerable to external pressures (e.g. high fuel prices).

• The third problem is the lack of social sustainability, primarily involving the catch sector and regionsdependent on fishing. Low wages and serious safety risks mean that this sector is not an occupation thatis in a position to attract new generations of fishermen. Employment, especially in the catch sector, hastherefore seen over the last 15 years a steady decline in many sectors that are dependent on fisheries.

PART

126

7 Services of the European Commission, Summary of the Impact Assessment accompanying the document “Proposal for a Regulation of theEuropean Parliament and of the Council on the Common Fisheries Policy”, SEC (2011) 892 definitive, Brussels, 2011.

• Decentralisation of governanceThe new CFP moves the decisions closer to the subjects for which they are intended and clarifies the rolesand obligations of each party. It will put an end to micromanagement from Brussels: European legislatorswill limit themselves to outlining the general framework, principles and basic standards, the overall objec-tives, performance indicators and timetables. Member states will cooperate on a regional level and devel-op the actual implementation measures. Once agreement has been reached by all of the member states,these recommendations will become the rules for all the fishermen involved.

• Support for small-scale fisheriesIn the European Union the small-scale fleet makes up 77% of the entire fleet by number of vessels, butonly 8% in terms of tonnage (vessel size) and 32% in terms of engine power. Its impact on resources istherefore less relevant. Small-scale coastal fishing often plays an important role in the social fabric andcultural identity of Europe’s coastal regions and therefore requires specific support. The reformed CFPextends until 2022 the right of member states to restrict fishing activities within a zone of 12 nauticalmiles from the coastline.

• Developing sustainable aquacultureCreating a better environment for aquaculture will increase the production and range of marine productsin the EU, reducing the dependence on imports of fish and encouraging growth in coastal and rural areas.By 2014, member states will have prepared national strategic plans to improve the conditions for aquacul-ture, remove administrative barriers and promote compliance with the environmental, social and econom-ic norms for the fish-farming industry. It will set up a new advisory council for aquaculture to advise onissues related to the sector. The growth of aquaculture has a clear European Union dimension: the strate-gic choices made at national level might affect the development of the sector in neighbouring countries.

• Advancing scientific knowledgeHaving reliable information and knowledge on the state of fishing and marine resources is essential tomake justifiable management decisions and to carry out an effective implementation of the reformed CFP.Member states will have to deal with the collection, processing and sharing of data on fish stocks and theimpact of fishing fleets at the level of sea basins. The policies will be adopted taking into account the bestavailable scientific advice. To coordinate this activity, national research programmes will be set up.

• New market policy - Making the industry responsible and providing better information for consumers

The new market policy is aimed at strengthening the competitiveness of the fisheries and aquaculturesectors in the EU to improve market transparency and to ensure a level playing field for all products mar-keted in the EU.The current intervention system will be modernised and simplified: producer organisations will be able tobuy fish products when prices fall below a certain level and store them to then reintroduce them on to themarket at a later stage. This system will promote market stability.Producer organisations will contribute most to the collective activities of management, monitoring andcontrol. New standards for labelling, traceability and quality will provide clearer information to consumersand help to promote sustainable fisheries. Some of the information on the label will be mandatory, somemay be provided on a voluntary basis.

PART

1

29

These are the main elements of the new policy9:

• SustainabilitySustainable fishing is fishing at a level that does not threaten the reproduction of stocks while allowingfishermen to obtain the largest catch. This level, known as “maximum sustainable yield” (MSY), is the limitwhich the catch must respect on stocks under the new CFP. This goal was set in the United NationsConvention on the Law of the Sea and was confirmed as part of the World Summit on SustainableDevelopment in 2002 as a global objective to be achieved as far as possible by 2015. In terms of the newCFP, exploitation rates will have to correspond as much as possible to MSY levels by 2015. This objectivehas be achieved for all stocks by 2020.It is estimated that if stocks were exploited on the basis of these modules their size would significantlyincrease, with obvious positive effects on catches and incomes.Sustainable fishing will help to stabilise prices in a transparent way, with clear benefits for consumers.

• Multi-year management based on the ecosystemsMulti-year management plans continue to be central to the management of our fisheries. Current plansrelating to individual stocks will be replaced by plans based on types of fishing: this will allow the inclu-sion of more fish stocks in fewer plans and to pursue the objective of sustainability more effectively. As partof these plans, the Council will establish the annual fishing opportunities. The plans might also includeother technical and conservation measures that are part of the proposed set of instruments. To rebuild a profitable fishing economy in Europe it is necessary to respect more effectively the boundariesof the marine environment. Fisheries activities in the European Union will be managed with an ecosystemapproach in accordance with the precautionary principle, in order to limit impact on the ecosystem and thusprotect marine resources.

• Prohibition of discardsIt is estimated that discards, the practice of throwing overboard fish that has been accidentally caught, con-stitutes about 23% of the total catch (and in some cases a lot more). This unacceptable practice will bephased out between 2015 and 2019, according to a precise timetable for implementation, and along withsome accompanying measures. Fishermen will be obliged to land all commercial species they catch. Theremaining catches of undersized fish cannot normally be sold for human consumption. The prohibition will allow for more reliable data on fish stocks, to provide a more effective support to man-agement and to improve the efficiency of resources. It is also an incentive for fishermen to avoid acciden-tal catches by making use of technical solutions such as the use of more selective fishing gear.Member states will have to ensure that their vessels are fitted with equipment which will document all fish-ing and processing activities, in order to monitor compliance with the obligation to land all catches.

• Management of the fishing capacity of the fleetMember states will have to ensure that the capacity of the fleet (number and size of vessels) is commen-surate with the fishing opportunities by adopting appropriate action plans for the segments where there isexcess capacity. The failure to obtain, by a member state, of the necessary reduction in capacity can resultin the suspension of EU financial support.

PART

128

9 European Commission, Questions and Answers on the reformed Common Fisheries Policy, MEMO/13/1125 10/12/2013.

PART

1

31

• International responsibilityAccording to FAO, numerous global fish stocks are fully exploited or overexploited. As the world’s largestimporter of fisheries products in value terms, the EU has to act on the international level according to thesame principles applied within the Union. Foreign fisheries policy must be an integral part of the CFP. Withinthe framework of international and regional organisations, the EU will therefore invoke the principles ofsustainability and conservation of fish stocks and marine biodiversity. It will establish alliances and initiateactions with strategic partners to combat illegal fishing and reduce overcapacity.As part of the bilateral fisheries agreement with third countries, the EU will promote sustainability, goodgovernance and the principles of democracy, human rights and the rule of law. Current arrangements willbe replaced by partnership agreements for sustainable fisheries, which will ensure that the exploitation offisheries resources occurs on the basis of sound scientific advice and involves only the surplus resourcesthat the partner country cannot or does not intend to fish. As part of the sustainable fishing agreements,the partner countries will receive compensation in exchange for access to their fishery resources, as well asfinancial support for the implementation of a sustainable fisheries policy.

T H E E U R O P E A N F U N D F O R M A R I T I M E A F FA I R S A N D F I S H E R I E S

Structural policies in the fisheries sector contribute to the achievement of the objectives of the CommonFisheries Policy (CFP), strengthening economic and social cohesion. The European Fisheries Fund (EFF), inplace since 1 January 2007, was the financial instrument of this policy. With a budget of about €4.3 billionfor the period 2007-2013, of which 75% was destined for countries with slower development, it has helpedto fund projects submitted by businesses, government agencies or representative bodiesIn 2014, the EFF was replaced by the EMFF (European Maritime and Fisheries Fund) with Regulation (EU)no. 508/2014, with a budget of about €5.8 billion for 2014-2020. Among the changes introduced, the EMFF will support the recovery of fish stocks and the phasing out ofdiscards. Priorities of the fund will also be to improve the collection of data on the sector to ensure thatdecisions are taken on the basis of statistical evidence, as well as to reduce the impact of fishing on themarine environment. The Fund will also focus on monitoring programmes to ensure compliance with the rules on responsibleand sustainable fishing, as well as the Integrated Maritime Policy by investing in the identification of thebarriers to the growth of coastal communities and emerging maritime sectors.

PART

130

Distribution of EFF funds to countries and axes (value in thousands of euros)

Axis 1 Axis 2 Axis 3 Axis 4 Axis 5 Total %per country per country

BE 14 259 800 8 502 1 900 800 26 262 0.61%BG 8 001 36 004 20 002 12 001 4 000 80 010 1.86%CZ 0 14 427 11 324 0 1 355 27 107 0.63%DK 32 980 23 289 57 991 15 960 3 456 133 675 3.11%DE 3 347 43 171 72 946 23 539 3 579 146 582 3.41%EE 15 265 24 584 21 210 19 282 4 228 84 568 1.97%IE 29 937 6 246 5 047 788 250 42 267 0.98%EL 77 272 59 690 32 320 33 300 5 250 207 832 4.83%ES 473 719 327 624 258 259 52 790 19 499 1 131 891 26.30%FR 70 728 43 109 94 574 5 454 1 784 215 650 5.01%HR 4 507 3 757 0 0 435 8 699 0.20%IT 163 905 110 778 97 181 31 275 21 204 424 343 9.86%CY 6 150 2 600 9 474 1 000 500 19 724 0.46%LV 26 197 52 320 30 300 11 238 4 961 125 016 2.91%LT 4 869 30 795 9 684 6 694 2 672 54 713 1.27%HU 0 30 209 2 519 0 2 041 34 770 0.81%MT 2 935 910 3 982 0 545 8 372 0.19%NL 16 913 7 379 16 903 4 987 2 395 48 578 1.13%AT 0 5 202 12 0 45 5 259 0.12%PL 124 184 173 757 164 537 234 910 36 705 734 093 17.06%PT 62 865 74 187 83 408 17 403 8 622 246 485 5.73%RO 6 222 123 719 29 991 53 978 16 736 230 646 5.36%SI 2 164 7 141 7 574 2 164 2 597 21 640 0.50%SK 0 11 432 896 0 684 13 012 0.30%FI 2 495 18 430 14 220 3 606 698 39 449 0.92%SE 13 111 10 933 20 133 7 755 2 733 54 665 1.27%UK 17 269 40 365 62 119 14 187 3 890 137 828 3.20%Total per axis 1 179 295 1 282 857 1 135 107 554 210 151 665 4 303 134Total in % 27.41% 29.81% 26.38% 12.88% 3.52% 100.00% 100.00%

Source: European Commission, Facts and figures on the CFP (2014)

Adaptation of the Community fishing fleet to the available resources (aid for permanent or temporary cessation, for small-scale coastal fishing, for investments on board fishing boats, etc.)

Aquaculture, inland fishing, processing and marketing of fishery and aquaculture products (measures for productiveinvestments in aquaculture, aqua-environmental measures, public health measures, etc.)

Measures of common interest (protection and development of aquatic fauna and flora,promotional campaigns, transformation of fishingvessels for a different use, etc.)

Sustainable development of fishing areas (local projects for sustainable development, diversificationof economic activities, etc.)

Technical assistance intended to facilitate the implementation of aid from the EFF (financing thework of public services that manage the funds, etc.)A

XIS

5 A

XIS

4 A

XIS

3 A

XIS

2 A

XIS

1

FIGURE 11

C O U N T R Y I N F O

2

PART

132

PART

234

PART

2

35

10 Shipowner Marc Vieren, intervening during the meeting in Ostend, told us that there were 73 boats in 2014, 30 of which form part of the indu-strial fleet.

Belgium

I N T R O D U C T I O N (by ACV Transcom Sector Water - Algemeen Sectorverantwoordelijke)

Belgian fisheries represent only some percentages in the EU TAC. In spite of this, Belgian fishers are the

only in EU that are for 100% covered by collective bargaining agreements. There are no exceptions for any

kind of fisheries. Belgian fishermen are paid also a share, but they have a guaranteed salary based on the

number of days at sea.

The labour relations are regulated by law dating from 2003. Before this they were regulated by a law of

1926 that had the objective to regulate labour relations at the Belgian merchant fleet. 10 years ago that

situation was out of time. The most important objective of this new law has always been to develop a fair

balance between fishermen on the one hand and workers ashore on the other hand.

Because Belgian fishermen are always considered as workers, contrary to most other EU countries where

the authorities allow employers to engage fishers as self-employed or something that looks alike. This ends

in deteriorating the work and living conditions for fishers all over Europe. Fishers are subject to enormous

fluctuations in their income due to fluctuations on the oil markets, which drives fishers out of their jobs

when they have the opportunity.

The Belgian model should be considered as a model for future labour relations in the fishing sector. It has

proved to be sustainable and can guarantee not only jobs but also better working and living conditions for

fishermen.

E C O N O M I C A N D S T R U C T U R A L C H A R A C T E R I S T I C S

• Fishing In 2012, the Belgian fleet consisted of 86 vessels registered10 with a total tonnage of 15 thousand tons, a

driving force of 49 thousand kW and an average age of 25 years. There were 80 registered companies, 99%

of them with a single boat.

The size of the fleet between 2011 and 2012 decreased by 3% in terms of number of vessels and tonnage

and 4% of driving force. Compared to 2008 the number of vessels was reduced by 13%. Similarly, days at

sea decreased, 17 thousand in 2012 (-14% compared to 2008) as did fuel consumption (-13% between

2010 and 2011).

In 2011, employment in the sector was 377, corresponding to full-time units of 342 FTEs, a decrease of 18%

compared to 2008 (-10% considering only the FTEs). The average wage, in the same period, underwent an

increase of 4% which projections indicated as likely to be stable in 2012 as well.

In 2012, the Belgian fleet landed 22 thousand tons of fish (+ 9% compared to 2011) to a value of €76 mil-

lion (-4% compared to 2011). Sole was the species caught with the highest value in 2012: 29.7 million

euros, equal to 47% of the total fish catch and a sale price of 10€/kg.

C O L L E C T I V E B A R G A I N I N G I N T H E F I S H I N G I N D U S T R Y PA

RT 2

37

Prices remained stable between 2010 and 2011 for the five major species caught, but fell between 2011

and 2012 for most of the market, with the exception of shrimp that saw a 67% increase.

In 2011, the income of the Belgian fleet was 82 million euros (+4% compared to 2010), split between 72

million euros of the value of fish and 3 million euros of income not directly resulting from fishing activities.

Operating expenses in 2011 totalled 73 million euros, equal to 92% of income. The costs of labour and fuel,

the two main cost items, amounted to €26 million and €25 million respectively.

The general trend for the Belgian fleet is a deterioration in economic performance, mainly due to competi-

tion with the more efficient Dutch fleet. Despite a continued commitment to energy savings, if fish prices

do not rise, it is difficult to imagine an improvement in the profitability of the sector.

• AquacultureBelgian aquaculture, which focuses exclusively on freshwater farms, produced 49 tons in 2011, with a value

of approximately 230 thousand euros. Rainbow trout was the species bred most and constituted 73% of

the weight and 68% of the value of the total production.

• ProcessingThe processing industry is divided in two main branches. On the one hand the fish auctions and the depend-

ing activities as there are soring, packing and delivery to the wholesalers off the fresh fish markets.

On the other hand the food processing industry. This industry is changing rapidly a basic industry into a pro-

duction line of the retail markets, either fresh, frozen and instant meals.

This sector employs the majority in the fishing sector and easily rises above 5000 FTE due to large impor-

tation of fish products.

E VA L U AT I O N O F T H E I M PA C T O F T H E C F P

Currently, the main problem for Belgian fishermen, according to Michel Claes (Secretary of ACV Transcom)11,

is the ban on the discarding of fish waste in the sea. European standards today require that waste is brought

back to land to be destroyed, but this leads to an increase of work onboard, a problem of space on the ship

and additional costs for the disposal. At this stage, it is not yet clear how these problems can be solved and

how exactly the waste should be managed.

European regulations on fishing, more generally, appear to be too restrictive and unnecessarily complicat-

ed, to the extent, in many cases, of forcing owners to make use of expensive consultants to guide them in

the interpretation of the rules before being able to make decisions regarding the company. The distance

between the measures adopted and the real needs of the sector is probably related to the fact that those

who are called on to draw up the rules at European level do not have a very thorough knowledge of the

peculiarities of the industry.

PART

236

11 Intervention during the training session held in Ostend 19-20 June 2014.

The duration of the collective labour agreement, concluded on the basis

of the type of fishing, is generally two years, but can be changed by the

government which decides on this matter.

Until 2003, the year of the contractual reform, contracts were managed

independently by the owner and his crew.

There are working relationships that can be activated for each fishing

season and fixed-term contracts. Specifically, the contract is valid for

only one trip to sea: it starts at the moment when the fisherman goes

on board and ends when he disembarks.

The minimum number of the personnel making up the crew depends on

the type of fishing, the tonnage of the ship and the duration of the trip.

With an experience of at least 100 days of work, the fisherman can get

the necessary certification to practise the profession which is issued by

a joint committee, an executive body composed of boat crews and land-

side staff, wholesalers and processors. Without this certification the role

that the employee can perform onboard is very limited. The bill under

consideration for the collective labour agreement states that without

certification there is no possibility of working.

There are national laws that relate specifically to the matter of the

health and safety of workers in fishing and the collective agreement

provides better conditions than those requirements.

There are national laws that relate to the specific training activities

aimed at workers in fishing. The collective agreement does not provide

better conditions than those requirements.

There are economic sanctions and/or disciplinary measures in the event

of wrongful conduct by workers.

There is a weekly rest day.

The maximum working time is 38 hours for both onboard crew and

landside workers. However, the time indicated by the Belgian legislation

is only theoretical, because working time is in reality linked to the pres-

ence of the fish.

Duration of contract

Working positions

Minimum crew

Professional qualifications for crew

Health and safety of workers

Training activities

Economic sanctions or disciplinary measures for employees

Contractual breaks

Hours of work

Denmark

I N T R O D U C T I O N (by 3F)

Both historically and at present Denmark has been one of the largest fishing nations in Europe. With a long

coast line and abundant natural fishing resources in the adjacent waters fishing has been a natural part of

daily life for many Danes. Fishing has been an important supply of food throughout centuries and turned

into a major industry in the last part of the twentieth century with both catching and processing activities.

Compared with many other European countries the Danish fisheries has not only been concentrating on

fishing for human consumption but also for industrial purposes by fishing after species such as sand eel

and sprat with the purpose of producing fishmeal and oil.

Danish fisheries have gone through a period of transition, when a shift in the composition of the fleet took

place. Although a sizeable portion of the fleet is still relatively old, new and large fishing vessels have been

introduced over the last 10 years. A contributing factor to this has been the introduction of ITQ`s, first in

the pelagic fisheries with the result of a concentration in ownership and access to resources.

As a consequence approximately 10 vessels fish around 90 per cent of the Danish quota for herring and

mackerel in 2014. This has led to a situation where a number of jobs in the fishing industry not only in the

seagoing sector but also in the processing industry have been vastly reduced especially to the detriment of

the fishing dependent areas.

Aquaculture was until recently dominated by traditionally small land based entities primarily producing

rainbow trout. Over the last 10 to 15 years Denmark has however seen a significant rise in the number of

sea based aquaculture plants originally also producing trout but experiments with other species such as

turbots and eel are now taking place.

Aquaculture is in other words increasing in importance both from a financial and employment perspective.

Once the fish stock has recovered, the future for Danish fisheries is bright with a high level of efficiency

and productivity provided a sustainable level of exploitation can be achieved and maintained.

E C O N O M I C A N D S T R U C T U R A L C H A R A C T E R I S T I C S

• Fishing The Danish fleet was composed, in 2011, of 2,787 registered vessels with a gross tonnage of 64,5 thou-

sand tons, a driving force of 239 thousand kW and an average age of 30 years. The downsizing of the fleet

(-1% for vessels and tonnage, -3% kW) follows the general trend of replacing older vessels with larger and

more efficient new vessels. The quota system also ensures that the more efficient businesses, perhaps

because they are equipped with new technology, acquire the quotas of the vessels which are less so.

In Denmark there is no division between artisanal and industrial fisheries but the fleet can be divided by

size as follows (for 2012):

• Under 12 meters: 2,290 vessels

• 12-16 meters: 216 vessels

• Above 16 meters: 248 vessels

PART

2

39PA

RT 2

38

Overtime work is governed by national law.

Emoluments for fishermen provide a minimum guaranteed amount of

money, which is also due in the event that nothing is caught: a sailor is

entitled to €35,000 a year, a fisherman aboard a ship of 40 meters (fish-

ing in the North Sea) is entitled to 75,000/100,000 euros, an engineer

is entitled to 80% of the latter amount.

Fishermen who cannot go to sea are entitled to compensation. During

the break between one trip and another, the worker is entitled to unem-

ployment benefit.

There is no productivity bonus.

There are no other levels of bargaining other than the national ones.

The cost of the food consumed by workers during fishing activity is the

responsibility of either the worker or the owner/entrepreneur.

The contract recognises paid holidays, assistance to family members,

parental leave and time off for studying.

For the fisheries sector, it is not expected to have private insurance for

accidents at work, but a National fund has been set up, co-funded by

the shipowners and the State. It is part of the national social security

system. PREVIS is installed to organise prevention in the fishing sector