emerging markets: a case study on foreign market entry in bangladesh420681/fulltext… · ·...

TRANSCRIPT

Emerging Markets: A Case Study on Foreign Market Entry in Bangladesh

Authors: Md. Ashiqur Rahman,

Marketing, Master Programme Feleke Desta Tantu Marketing, Master Programme

Tutor: Prof. Mosad Zineldin

Subject: Master Thesis, 4FE020

Level and semester: Master, Spring 2011

Acknowledgement

This thesis is the final step of the Master Programme in Marketing at Linneaus University,

Växjö, Sweden. It has been conducted in Spring 2011.

During the journey of writing this thesis we have obtained a lot of new knowledge and

experience about the subject under investigation as well as the process of putting together a

scientific study. We would herein like to express our gratitude to all the people who has

contributed to the successful finishing of this project. Our special thanks go to:

• our tutor, Prof. Mosad Zineldin, who has given us feedback and encouraged our work;

• our programme coordinator, Dr. Sarah Philipson, who has guided us through the

process;

• the people, who carried out the physical interviews in Bangladesh;

• the 150 retailers, who participated in the study and gave us valuable information

without which this study would not have been possible;

• our opponent group and persons who have assisted with support and made

recommendations for improvements.

We hope you enjoy reading!

Växjö, May 29th 2011

___________________ _____________________

Md. Ashiqur Rahman Feleke Desta Tantu

850124-T312 850127-9593

[email protected] [email protected]

2

3

Abstract

Title: Emerging Markets – A Case Study in Foreign Market Entry to Bangladesh

Keywords: emerging market, entry strategy, market entry, factors behind entry choice, entry

mode, entry node, entry timing

Background: Internationalism and international marketing are hot topics among the strategy

discussions of the companies and as a result companies continuously look for new, unreached

sales potential to their products and services as well as better use of their resources.

Purpose: To find the most efficient international market entry strategy for companies moving

from developed/transition economy to an emerging market.

Theoretical framework: The base for the start of internationalisation process is company’s

inner motives and resources. Motives and resources combined with the cultural distance,

competition and general external environment of host country form potential company-

specific risks for the entry to foreign market. Potential customers in combination with

company resources shows how big is the match between market demand and what company

can offer and therefore determines the potential reward. Risks and reward are both input to the

decision making process where the potential benefits and drawbacks are analysed against each

other. The output of this decision making is the entry strategy.

Methodology: Internet was mainly used to collect secondary data about company resources,

cultural distance and external environment. Interviews with 150 retailers in Bangladesh were

conducted to collect primary data about the competition and consumer behaviours in the

hosiery market of Bangladesh. Then comparative analysis was made based on the model

developed by the authors to reach to the decision.

Conclusion: The most effective entry strategy for the entry to emerging markets is indirect

exporting through an agent in case there is high location risk, moderately high competition

risk, medium country risk and moderately low demand risk, the company has no surplus

finances for big investments and no prior experience in doing business in an emerging market.

Table of content Acknowledgement 2

Abstract 3

Table of content 4

1. Introduction 6

1.1. Background 6

1.2. Problem discussion 7

1.3. Purpose 9

1.4. Delimitation and scope 10

2. Theoretical review 11

2.1. Market entry strategy 11

2.2. Market entry modes 12

2.2.1. Exporting 13

2.2.2. Licensing 15

2.2.3. Management contracting 15

2.2.4. Joint venture FDI 16

2.2.5. Acquisition FDI 17

2.2.6. Greenfield FDI 18

2.2.7. Use of different entry modes 19

2.3. Factors influencing the decision of entry mode 20

2.3.1. Company motives for entry to foreign market 21

2.3.2. Company’s internal resources 23

2.3.3. Cultural distance 24

2.3.4. Risks related entry to foreign market 25

2.3.5. Industry situation / competition in the host market 28

2.3.6. External environment 31

2.3.7. Additional aspects for the entry to emerging markets 32

2.4. Entry nodes 34

2.5. Entry timing 35

2.6. State-of-the-art 36

2.7. Research questions 38

4

3. Methodology 39

3.1. Research approach 39

3.2. Data collection 40

3.3. Sampling 41

3.4. Interview methods 42

3.5. Operationalisation 43

3.6. Validity 45

3.7. Reliability 46

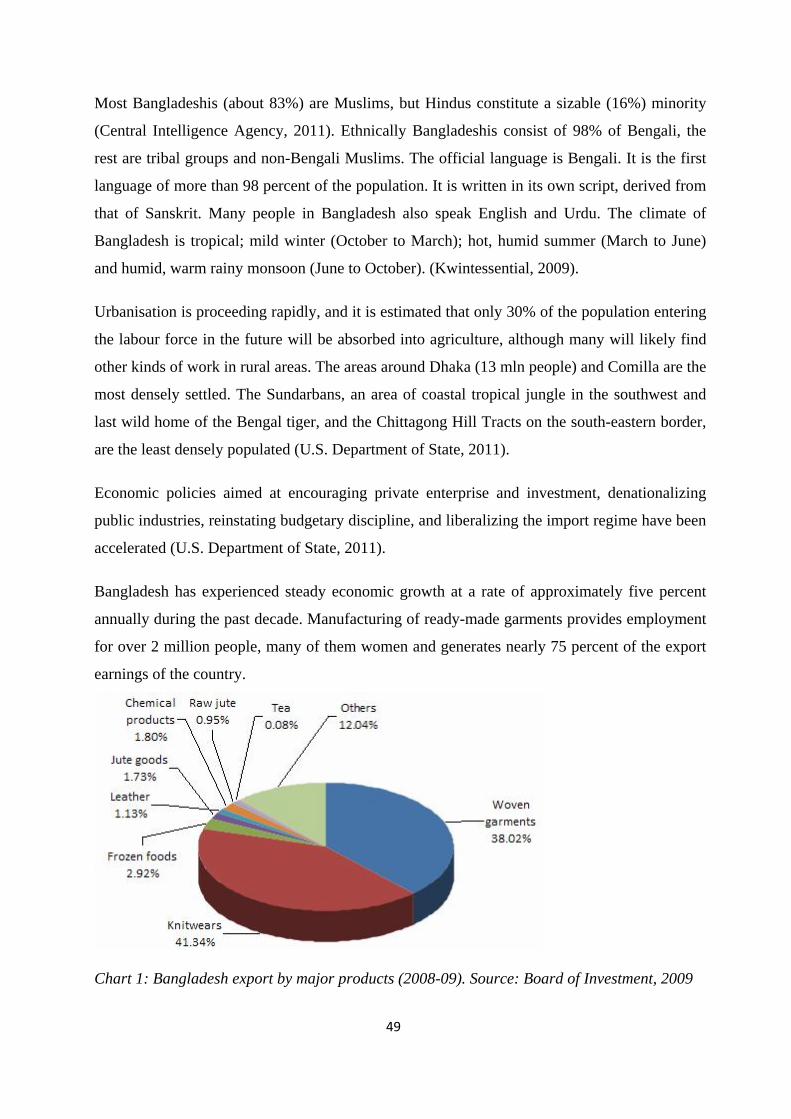

4. Empirical study 47

4.1. Company background 47

4.2. Product overview 47

4.3. The host country overview 48

4.3. The home country overview 50

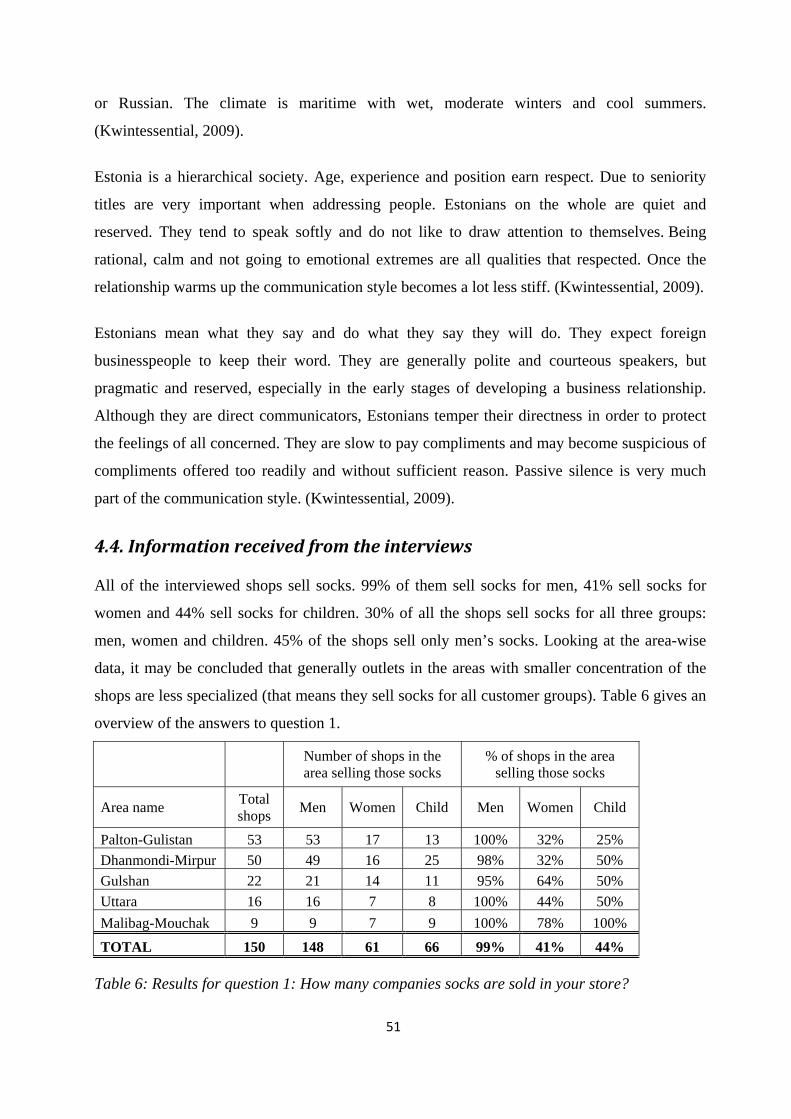

4.4. Information received from the interviews 51

5. Analysis 64

5.1. Company motives and resources 64

5.2. Cultural distance 66

5.3. Competition 67

5.4. Potential customers 70

5.5. External environment 71

5.6. Entry strategy 72

6. Conclusions 78

7. Recommendations for further research 79

References 80

Literature and articles 80

Internet 84

Appendix 1 – Interview questionnaire 85

Appendix 2 – Additional results from the survey 90

5

1. Introduction

In order to get an overview about the subject studied in the present thesis, an introductory

background on the issue is provided describing the relevance of the topic. Subsequently, a

problem discussion is elaborated and the overall purpose of the study stated. The chapter ends

with the limitation of the subject.

1.1. Background

Today’s companies, whether they are small, medium-sized or multinational, are striving to

make their products and services more global than ever. The internationalisation of firms is

occurring at an ever increasing pace. In the past 20 years, firms have changed their orientation

from domestic to international; they have shifted from multi-domestic marketing to global

marketing (Malhotra et al., 2003:1).

Internationalisation is the process of adapting exchange transaction modality to international

markets (Malhotra et al., 2003:1). Amdam adds that internationalisation is also a process

increasing commitment to foreign operations and to foreign markets in which they are already

operating (Amdam, 2009:446). According to Albaum & Duerr a firm becomes increasingly

internationalised as it becomes more involved in and committed to serving markets outside of

its home country (2008:13). They define international marketing as the marketing of goods,

services, and information across political boundaries, which could include anything from

exporting one product to one other country in response to an order, to a major effort to market a

number of products to many countries (Albaum & Duerr, 2008:14).

Different authors emphasize on the variety of reasons why companies expand to foreign

markets. Thomson et al (2005:174) mention four major motivations of the companies for going

abroad: 1) gain access to new customers for realizing the potential of increased revenues,

profits and long-term growth; 2) achieve lower costs and enhance the firm’s competitiveness as

often domestic sales volume is not large enough to fully capture manufacturing economies of

scale or learning curve effects; 3) capitalize on its core competencies; 4) spread business risk

across a wider market base so that the economic turbulences do not put the existence of the

company at risk. Couturier & Sola (2010:45) add that companies wish to acquire resources that

are more efficient than those obtainable in the home market of the firm (e.g. labour and natural

resources).

6

Album & Duerr (2008:2) bring out some more reasons derived from the developments of the

markets and global environment. They believe that the importance of international marketing is

continuously growing due to: 1) research & development costs, which for many products

cannot be recovered unless they are sold internationally; 2) increasing demand from consumers

for alternative product/service selection; 3) countries’ desire to enjoy higher per-capita GDP

growth rates and lower unemployment rates.

The major external changes that force the rapid growth of international business are

technological advances and greatly reduced costs in communications, the development of

sophisticated and diverse software to support a wide variety of business functions, the further

development of logistics and supply chain management, increasing rates of entrepreneurial

innovation and technological change, changes in the location of some major economic

activities, continuing lowering of barriers to trade and investment through multilateral

agreements and increasing regional integration, the internationalisation of capital markets, an

increase in all types of strategic alliances and the excess capacity existing in a wide range of

industries in many countries (Albaum & Duerr, 2008:2).

According to Couturier & Sola (2010) both niche players and mainstream corporations must

develop globally in order to sustain. Similar idea is expressed by Albaum and Duerr (2008),

who state that most companies are now selling to, buying from, competing against, and/or

working with enterprises in other nations. They further argue that from consumers’ perspective,

international sales and marketing provides an increasing range and selection of goods and

services with lower price and better quality as well as economic health and growth for nations

(Albaum & Duerr, 2008:2).

We can sum up that we live in a global world, where customers expect the high variety of

products/services to choose from and the market competition is continuously increasing due to

endless environmental, social and technological advancements. These trends seem to be getting

stronger, which keeps the internationalism and international marketing the hot topics among the

strategy discussions of the companies. As a result companies continuously look for new,

unreached sales potential to their products/services as well as better use of their resources.

1.2. Problem discussion

When a company goes international, there are three questions that need to be answered: a)

Who are we? b) Where do we want to go? c) How will we go there? (Thomson et al, 2005:3).

7

Who are we gives the idea of company’s core competencies and values. Where do we want to

go shows the (expansion) direction and ambitions, specifically the foreign markets where

company wants to establish itself. How will we go there identifies the strategies and ways of

entry. There are different options for entry ranging from licensing and franchising, through

exporting (directly or through independent channels), to foreign direct investment (FDI) (joint

ventures, acquisitions, mergers, and wholly owned new ventures) (Anderson & Gatignon 1986;

Domke-Damonte 2000 in Rasheed 2005:42). However, additionally the company when going

international must also see whether the market where they want to go have the potential to

receive their product.

Over the past two decades, globalization has profoundly affected the economies of both

developed and developing countries. By increasing the flow of trade and foreign direct

investment, trade liberalization policies have transformed and modernized the economies of

emerging markets (Javalgi et al., 2010:209). Emerging economic regions have been playing a

critical role in global economies. Since their market liberalization and privatization policies

were formally set forth, these areas have attracted many foreign investors (United Nations

Conference on Trade and Development [UNCTAD], 1997 in Isobe et al., 2000:468).

Despite the complexity and instability faced, emerging markets have become increasingly

attractive for doing business, inter alia due to the fact that growth rates in forthcoming years

will be significantly higher than in mature markets (Cavusgil et al, 2002). According to Jansson

(2007) the rapid growth of emerging country markets and their integration into the world

economy creates double effects of strong global pull from growing demand and push from

growing competition. Therefore, it may be concluded that it is or will be vital for companies

operating in developed countries, to give more business attention to expand their market to

developing countries.

Competition comes about because business firms, in their search for a niche in the economic

world, try to make the most of their uniqueness. The result, hopefully, is the establishment of

differential advantage that can give the firm an edge over what others in the field are offering.

It is this unending search for differential advantage that keeps competition dynamic (Albaum &

Duerr, 2008:158). In addition Hoecklin (1995) in Albaum & Duerr (2008) argues that

understanding and managing cultural differences can lead to innovative business practices and

sustainable sources of competitive advantage.

8

According to Jasimuddin (1995) the study of host cultures is of primary importance to those in

international business because cultural differences exert a pervasive influence on all business

transactions. Cultural factors will continue to be important considerations for managers

operating in foreign, and initially strange, environment is a competitive setting (Jasimuddin,

1995:62).

Specialized marketing knowledge or access to information can distinguish an exporting firm

from its competitors. A good and perhaps unique product, a strong sales force, an efficient

marketing infrastructure, and good service technical support system, for example, may act as

incentives for exporting because a company has built up competitive marketing advantages

(Albaum & Duerr, 2008:79).

When establishing business in an emerging market, understanding the external business

environment is not the only critical component. The attractiveness of the targeted market

segment in terms of profitability prospects is a major parameter for deciding on whether to

enter the market. Analyzing and being aware of the forces driving competition in the targeted

emerging market is a critical factor, since they provide opportunities and threats for growth and

determine the attractiveness of the targeted market segment (Thompson & Martin, 2005).

Market entry in developing countries will most likely mean being exposed to unfamiliar

environments. The general business conditions might be very different from the home market

and constitute higher levels of trade barriers and socio-cultural distance may be difficult to deal

with (Petter, 2009:3). If a company lacks experiential knowledge in a volatile and unstable

foreign market, accurate market segment evaluation is a challenging process. Nevertheless,

being aware of the attractiveness of the targeted segment in an emerging market is a

precondition for deciding on whether to enter the foreign market (Pehrsson, 2002).

It can be understood, the topic of internationalisation is broad and could take hundreds of pages

of discussion. Therefore the authors of this thesis have limited their area of interest to the entry

strategies of emerging markets.

1.3. Purpose

The purpose of this thesis is to find the most efficient international market entry strategy for

companies moving from developed/transition economy to an emerging market.

9

1.4. Delimitation and scope

Due to limited time and financial resources the authors limited the scope of the research as

follows:

⇒ Thesis focuses on the appropriate entry mode selection only; full scale analysis of (long-

term) internationalisation process is not done.

⇒ The emphasis is on the entry to emerging market, both in the theoretical chapter as well as

in the rest of the paper.

⇒ The development stage of home country market and its implications to the foreign market

entry are not discussed. Therefore, in the context of this thesis, it is not considered relevant

whether the home country market is developed or in transition phase.

⇒ The theory part of this study is based on the literature that was available to the authors

within the limited time. The authors acknowledge that this may be only the fraction of the

literature that has been produced on the topic. Therefore the approach and framework

developed in this thesis by no means claims to be unique in the field.

⇒ The empirical part of this thesis is based on the case, where the company is an Estonian

hosiery company and targeted market is Bangladesh. For simplification of the text and

relying on the fact that Estonia as part of European Union and Euro zone, Estonia is

referred to as developed market. The authors are aware that in the literature, Estonia is

often said to be a transition economy.

⇒ The data collection for empirical part was done being physically in Estonia. This has effects

on the amount and possibly the depth of information.

⇒ Finally, there was 8 weeks time to for writing this thesis (starting from preparation to

finalising). The limited duration set tight deadlines to the work which has negative

influence on the depth of the study.

The theoretical part of the paper gives the overview of different aspects of the entry strategy

(e.g. entry modes, nodes, timing) and the variety of considerations that influence the choice of

the entry mode. In this part the dimensions of company, market and external environment as

well as risks are covered. Wherever possible, the distinctions specifically applicable for

emerging markets are discussed. The empirical part draws the overview of the case market and

company based on the primary and secondary data collected. Finally the analysis of the

empirical data is made based on the information provided in the theoretical chapter and the

most suitable entry strategy for the companies’ entry to emerging markets is proposed.

10

2. Theoretical review In this part of the paper, the authors present theories about the practices of market entry

strategy, market entry modes, internationalisation to an emerging market, risks associated with

new market entry, timing of entry and finally, the research questions that we came up with

based on the discussed theories.

2.1. Market entry strategy

As different authors tend to define the internationalisation, marketing strategy and foreign

market entry strategy slightly differently, it is relevant to specify the terms for the context of

this paper. For the overall approach, the authors are using the definitions from Jansson

(2007:135), who distinguishes two major strategic issues in the international business

marketing: 1) the entry strategy and 2) the internationalisation strategy.

Jansson (2007:135) sees the entry strategy as how firms get access to new customers in new

geographic markets by marketing their products there, for example how the business marketing

is initiated and built up in order to establish a strategic position in the local industry and how

business marketing is done to maintain such a position. The internationalisation strategy for

Jansson is how business marketing is increasingly globalised by the expansion of firm to

growing number of countries (Jansson, 2007:135). Therefore we can conclude that

internationalisation is a long term process and observes the development of the company in an

international business context whereas entry strategy is the first stage or step in entering a new

market. For the context of this paper, only the entry strategy (also referred to as market entry

strategy) is further relevant.

According to Jansson (2007:151-152) market entry strategy consists of four factors: entry mode

(determines whether company shall export, establish a company of its own or cooperate

through a joint venture), entry node (determines how shall company plug into the local

network), entry process (determines how company shall build relationships in the local market)

and entry role (determines what commercial role the company shall perform in the local

network - seller, buyer and/or manufacturer). Janssons view is quite well aligned with the

views of Albaum & Duerr (2008:275), who state that a market entry strategy consists of an

entry mode and a marketing plan and it determines the degree of a company’s control and its

commitment in the target market. Some identify another aspect – entry timing, which can be

crucial while entering to emerging markets (Pan & Chi 1999 in Johanson & Tellis 2008).

11

Scholars have extensively analysed some aspects of entry strategies, especially ownership and

control (Agarwal & Ramaswani 1992; Anderson & Gatignon 1986; Hill et al. 1990 in Meyer &

Nguyen, 2005:63), which are related to entry mode. Over the last decade a considerable

attention has also been placed on the nature of business relationships, strategic alliances and

networks (Zineldin 2007:366) and analyzing company performance within different entry

modes (Zineldin 2007, Zineldin & Dodourava 2005). More recent studies have indicated that

internationalisation strategies are associated with information asymmetries and substantial

risks, especially when firms invest in emerging markets with relatively less developed legal and

business environments (Filatotchev et al. 2007:558).

The variety of theories has evolved trying to explain the motives and justification for the choice

of entry strategy, mostly for entry modes. The most widespread out of those theories is

transaction cost theory (Brouthers & Brouthers 2003; Hennart 1991; Zhao et al. 2004 in

Brouthers et al. 2008:936). Quite well known are also theories of international product life

cycle, market imperfections, resource advantage, strategic behaviour, eclectic,

internationalisation, real option and network theories (Malhotra et al 2003:8). Some of those

theories focus on the external environment as the main deciding factor for the entry strategy,

some focus on the internal resources, management views and risk tolerance of the companies,

some put the main attention towards the market aspects. No specific model has been taken as

the basis of this thesis; however, the authors have tried to capture the aspects from all of those

theories that are most relevant for making the entry strategy choice for an emerging market.

2.2. Market entry modes

The firm’s performance in the host country to a great extent depends on its mode of market

entry. The choice of market entry mode selected by a firm is one of the most crucial decisions a

firm can undertake when it decides to internationalise (Choo & Mazzarol 2001:291). Choice of

entry automatically constrains the firm’s marketing and production strategy (Johanson & Tellis

2008:2).

Root (1987) in Rasheed (2005:42) defines an entry mode as an institutional arrangement that

makes possible the entry of firm’s products, technology, human skills, management or other

resources in to a foreign country. Later on Gatingnon & Anderson (1988) in Sharma &

Erramilli (2004) refer to an entry mode as a governance structure that allows a firm to exercise

control over its foreign operations.

12

As said before, the transaction cost economics is the primary theory to explain the choice of

entry modes. Based on the concepts of bounded rationality and opportunism, transaction cost

economics focuses on minimizing the costs created by uncertainties associated with protecting

proprietary assets, investing in different markets, and monitoring partner behaviour (Hennart,

1988; Williamson, 1985 in Broutherset al., 2008:936). Erramilli et al (2002:225) add that a firm

should choose an entry mode that can best transfer its re-sources or capabilities from the home

country operations to the host country operations without eroding their value. According to

Bhaumik & Gelb (2005:10), the choice of the entry mode would also depend on the rate of

growth of the local industry. If an industry is fast growing, and therefore fast changing, it may

be essential for companies to quickly have a stake in it, so as not to lose its first-mover

advantage to other multinational companies or local firms.

There are number of international market entry modes available for companies who wish to

enter in to a new market. Entry modes vary in the degree of control the firm has over invested

tangible and intangible resources, the transaction costs associated with that resource

commitment (Anderson & Gatignon 1986; Domke-Damonte 2000 in Rasheed 2005:42),

enforceability of legal rights and ease of knowledge transfer (Hennart, 1988, 1989; Williamson,

1991 in Broutherset al., 2008:937). Dunning proposed a comprehensive framework which

stipulates that market entry modes are determined by three factors: ownership advantages of a

firm, location advantages of a market and internalization advantages of integrating transactions

within the firm (Dunning in Ohlin, 1977; Dunning, 1980 in Couturier & Sola, 2010:47).

The entry modes can be non-equity based or equity based (foreign direct investments). The

most common market entry modes described by the majority of the authors are exporting

(indirect or direct), licensing, management contracting, joint venture, acquisition, Greenfield.

The first three of them are non-equity based, the rest are different forms of foreign direct

investments – that means equity based entry modes. Following is the overview of the

mentioned entry modes with some explanation about when it may be beneficial to use one or

another.

2.2.1. Exporting

Exporting is located domestically and is controlled administratively (Anderson & Gatignon

1986 in Rasheed 2005:43). It is the easiest way to meet needs of foreign market and it has

minimal effect on the ordinary operations of the firm (Albaum & Duerr, 2008). According to

13

Rasheed (2005:41) a study results indicate that firms will have a higher rate of international

revenue growth using no-equity-based (exporting) foreign market entry modes in growing

domestic environments.

According to Albaum & Duerr (2008) as well as to Kotler & Keller (2006) exporting is

classified into two categories: a) direct exporting (every responsibility is performed by the

company itself) and indirect exporting (responsibilities are done through other intermediaries).

Huei-Ting & Eisingerich (2010) categorize firms engaged in gradual internationalisation in to

two types: regional exporter/importer and global exporter/importer. The former relates to

emerging market firms that gradually deepen their commitment and investment as they gain

more market knowledge and experience and begin by exporting to, and importing from,

geographically close markets. The latter refers to firms from emerging markets that initially

limit their investments and engagement in foreign markets but export/import on a global rather

than merely regional level (Huei-Ting & Eisingerich, 2010:116).

Advantages of export from macroeconomic point of view are that it boosts employment and

allows national economies to build up their reserves by means of foreign transactions (Reid,

1983 in Claver et al. 2007:3). Advantages of exporting mode from company perspective are

that it requires low investment, has low risk/return alternative (Agarwal & Ramaswami,

1992:3) and allows a firm to achieve competitive advantage, increase productive capacity or

improve its financial position (Reid, 1983 in Claver et al. 2007:3). It also allows the company

to maintain the complete control over production and reach customers quickly.

From negative side, even though exporting provides a firm with operational control, it lacks in

providing marketing control that may be important for market seeking firms (Agarwal &

Ramaswami, 1992:3). On top of that, research has found that exporting can have negative

effect on financial performance (Lu & Beamish (2001) in Rasheed, 2005:43). That can be

caused by high transportation costs, tariffs and quotas.

Exporting is the most appropriate choice for entry mode if there are low entry barriers, home

location has cost advantage and product customization is not crucial.

14

2.2.2. Licensing

Licensing is the provision of the companies (licensor’s) manufacturing, processing, trademark

or name, patents, etc to the licensee with payment (Albaum & Duerr, 2008). It can be the

process of transferring technology from one company to the other or from home country to the

host country (Mottner& Johnson, 2000:185). According to Claver et al. licenses and franchises

are the most important of the main contractual agreements (Claver et al. 2007:4).

Technology plays major role for firms to practice licensing. According to Ferreira and Ferreira

(2008:321) technological difference is important reason for cost differences between firms,

which may encourage them to share their technological information through licensing.

Advantages of licensing include low initial investment, avoidance of trade barriers, access to

local knowledge and easier possibility to respond to customer needs. Major drawbacks of

licensing are the lack of control over the operations and difficulty in transferring tacit

knowledge. In addition licensing has a potential of creating a competitor.

Licensing is the most appropriate when the company has well codified knowledge, there is

strong property rights regime and host country location advantage.

2.2.3. Management contracting

Management contracting exists when a local investor in a foreign market provides the capital

for an enterprise, while a company from ‘outside‘ provides the necessary know-how to manage

the company (Albaum & Duerr, 2008).

Advantages of management contracting for an outside firm is that it offers a low risk way into a

foreign market, allows a company to manage, and in many ways to control (in a functional

sense), another company without equity control or legal responsibility, quick return, establishes

clarity in administration and decision making. It provides the company with access to local

management skills and helps them avoid buying unwanted assets. On the other side, the

disadvantage of management contracting is the need for complex contract and expensive legal

document, which must differ for each case (Albaum & Duerr, 2008:383).

It has been argued that choosing the management contract is appropriate when the manager has

a reputation to protect (e.g. hotels or consulting companies) and when performance-based

contract provides no bad incentives.

15

2.2.4. Joint venture FDI

Joint venture exists when a company joins another non-national company for common interest

(Albaum & Duerr, 2008). According to Albaum & Duerr (2008) the main feature of joint

venture is that ownership and control are shared. In long run, this approach is more profitable

than any other approach. In the literature, joint venture is the topic about which different

scholars make different conclusions and recommendations.

On one hand, it is said that entry into a country in the form of a joint venture reduces the

company’s transaction cost of doing business (Bhaumik & Gelb 2005:9). In addition,

cooperative ventures have the advantage of lower capital investment risk, lower risk of return

due to faster entry and lower political risk (Contractor & Lorange 1988 in Rasheed, 2005:45).

Kim & Hwang (1992, p.35 in Brouthers & Brouters, 2003:1184) suggest that joint venture

modes of entry provides the firm with a method to decrease the exposure of fixed assets to the

potential hazards of environmental uncertainty. An agreement of joint venture is considered the

smartest move when the chosen entry market is significantly different from that of the

enterprise’s domestic culture (Hennart & Park, 1993 in Couturier & Sola, 2010:48). Because of

this, Beamish (1985, 1993) in Isobe et al (2000:469) even argues that equity joint venture has

been a dominant and often a "forced" entry mode in most emerging regions.

Several scholars (e.g. Aulakh & Kotabe, 1997; Erramilli & Rao, 1993; Gatignon & Anderson,

1988; Kim & Hwang, 1992) argue that joint ventures provide firms with greater flexibility,

which is needed when environmental uncertainty is high in order to speed up adaptation

(Brouthers & Brouters,2003:1183). On the contrary, Williamson (1991) in Brouthers &

Brouters (2003) discusses that joint venture will be used less often in high environmental

uncertainty markets because adaptations cannot be made quickly due to the need for consent

between parties.

Beamish (1985) in Mayrhofer (2004:74) identifies important differences in the characteristics

of joint ventures between developed and developing countries. The statistics provided show

that joint ventures established between firms in developed countries are equally owned more

often than joint ventures between firms in developed and developing countries. Beamish

considers that the observed differences are mainly due to the characteristics of the external

environment in developed and developing countries. Sinha (2001) goes even further claiming

that multinational companies typically use the joint ventures as vehicles toward gaining

16

knowledge about the business environment in the developing economy and once they have

absorbed this knowledge, they usually initiate their own business operations by opting out of

the joint venture (Sinha, 2001 in Bhaumik & Gelb, 2005:7).

According to the empirical study of Javorik & Saggi (2010), efficient foreign investors are less

likely to choose joint ventures and more likely to enter directly. On the other hand several

scholars (Kock & Guillen, 2001; Lane & Beamish, 1990; Osborn & Hagedoorn, 1997 in Kim et

al, 2004:15) argue that strategic alliances are an important entry mode in an emerging market.

Through alliances, western companies can share risk and resources, gain knowledge and obtain

access to markets (Kock & Guillen, 2001 in Kim et al., 2004:15).

In conclusion it may be said that joint ventures are appropriate to be used if specific conditions

apply: (1) the project depends on contributions from two or more partners; (2) the markets for

the contributions from the parents are subject to market failure, i.e. transaction costs are high;

and (3) it is not feasible to internalize the whole operation with one partner taking over the

other(s) (Buckley & Casson, 1976, 1998; Hennart,1988 in Meyer & Nguyen, 2005:74).

2.2.5. Acquisition FDI

Acquisition is defined as having a majority of interest in another company (e.g. acquisition of a

business unit) by stock purchase or exchange (Couturier & Sola 2010).

Acquisition facilitates quick entry and immediate access to local resources (Meyer & Estrin,

2001:575). Firms establishing themselves abroad for the first time often choose to do so via

acquisition. This path reduces uncertainty (Dubin 1976; Brouthers & Brouthers 2003;

Halliburton, Hünerberg & Töpfer 1993 in Couturier & Sola, 2010:47) as acquisition provides

the access to target market knowledge as well as control over foreign operations and own

technology.

From drawbacks side, acquisition may bring along the difficulty in “absorbing” acquired assets.

Also, this option is not feasible in case local market for corporate control is underdeveloped.

From an external viewpoint, acquisition is an attractive option when a firm wishes to enter an

oligopolistic, static or declining market. If investment cost is very high, acquisition becomes

unattractive too and no entry will be an optimal choice but in larger markets acquisition is

relatively more favourable (Muller, T., 2007:93). According to the report of Caves & Mehra

17

(1986) for entry into the US, and Zejan (1990) for Swedish multinational enterprises,

acquisition entry is favoured in rapidly growing or very slow-growing markets (Yung, 2006)

2.2.6. Greenfield FDI

Couturier & Sola (2010) define Greenfield as investment in a commercial office,

manufacturing plant, distribution facility or other physical structure in a country where no

corporate facilities previously existed. It is a direct investment normally entailing 100%

ownership and therefore full control. Greenfield uses the resources of the investor and

combines them with local assets, giving the investor more discretion over the organization of

the new venture, but generally permitting only a gradual establishment (Meyer & Nguyen,

2005:75). A Greenfield entry would be more likely if the multinational company has prior

operating experience in the host country or in similar developing countries or emerging

markets (Barbosa et al. 2004 in Bhaumik & Gelb, 2005:9). It is also more likely if the

“cultural” distance between the multinational’s home country and the host country of

operations is minor (Yip 1982 in Bhaumik & Gelb, 2005,:9)

According to Meyer & Estrin (2001:575) Greenfield project gives the investor the opportunity

to create an entirely new organization specified to its own requirements, but implies a gradual

market entry. Larger and more established multinationals are far more likely to choose a

Greenfield investment (Dubin, 1976; Brouthers & Brouthers, 2003; Halliburton et al. 1993 in

Couturier & Sola, 2010:47). Greenfield strategy is far more appealing when there is rapid

expansion in a market (Knickerbocker, 1973 in Couturier & Sola, 2010:48). The drawbacks are

that Greenfield requires knowledge of foreign management and has very high investment cost

(Muller, 2007:93), therefore it implies high risk and needs high commitment to succeed.

Greenfield strategy can be very appealing when there is lack of proper acquisition target in the

foreign marker, there is in-house foreign market expertise and embedded competitive

advantage.

18

2.2.7. Use of different entry modes

Agarwal & Ramaswami (1992) in Choo & Mazzarol (2001:293) in their examination of the

effect of interrelationships among ownership advantages, location advantages and

internalization advantages have found the following:

⇒ Larger and more multinational firms prefer sole venture (e.g. acquisition, Greenfield) and

joint venture modes to the other market entry modes in low market potential countries.

⇒ Smaller and less multinational firms prefer no entry or joint venture mode in high potential

markets to reduce costs and risks.

⇒ Firms having higher ability to develop differentiated products prefer to choose investment

modes to exporting in countries that are perceived as having high contractual risks.

⇒ Firms prefer the exporting mode in markets that have high potential but are perceived to

have high investment risk.

During the past several decades, there has been a significant change in the attitudes of many

countries toward inflows of foreign direct investment (FDI). From being viewed as exploiters,

foreign investors are now welcomed as a source of new technologies, know-how, better

management, and marketing techniques (Javorcik & Saggi, 2010:415). Developing country

governments are especially interested in the technology and know-how transfer that results

from FDI. To be able to assess the potential magnitude of such benefits, it is important to

understand preferences of different types of investors with respect to the entry mode (Javorcik

& Saggi, 2010:428). In addition to technology transfers, Konopielko in Kumar & Waheed

(2007:178) highlights the benefits of FDI for less developed countries as conferred to domestic

employment growth, formation of human capital, government revenue growth, and direct

expenditure.

By the end of the twentieth century, foreign direct investment had effectively replaced trade as

a driver of economic growth in less developed and emerging economies. In 2002, there were an

estimated 65,000 multinational corporations with about 850,000 worldwide affiliates

employing about 54 million employees, a rise of 141 percent over the 1990 employment figure

for MNCs (UNCTAD 2002). In 2004, FDI increased by 41% in developing countries and

reached an all-time high of $268 billion. Asia in particular took in nearly one in four FDI

dollars, which is quite an improvement from one in ten in 2000 (Kumar & Waheed, 2007:178).

Therefore, we can say that FDI plays as a source of financial resource for developing countries

and emerging markets.

19

From companies’ perspective acquisitions and FDIs are expensive and cumbersome; however,

the aging of the population and changes in regulations have placed many closely held

companies on the sales block, providing foreign companies access to safe vehicles for entry

and expansion (Kumar & Waheed, 2007:180). Foreign licensing is foreign located and is

controlled contractually; and FDI is foreign located and is controlled administratively.

Transaction costs theory views each choice of entry mode as an individual transaction that

involves a trade-off between control and resource commitment (Anderson & Gatignon 1986 in

Rasheed 2005:43). FDI is a more competitive way than exporting for operating in international

markets because the value of FDI was greater at later stages (Lu & Beamish ,2001 in Rasheed

2005:43).

An interesting fact is that over the last decade there has been the change in the nature of

business relationships, particularly the shift from adversarial to more strategic alliance

relationships (Zineldin & Dodourova 2005:460). This allows suggest that licensing,

management contract, joint venture and other cooperative forms of entry have become more

prevailing. Compared to go-it-alone strategies strategic alliances have a long list of motives

(Zineldin & Dodourova 2005:462): a) financial benefits related to cost reduction and profit

generation (e.g. joint investment, reduced inventory, stable supply prices), b) technological

benefits that facilitate supply process (e.g. sharing technology, joint new product development),

c) managerial benefits including interdependence, supply base reduction and loyalty, d)

strategic benefits related to competitive positioning of the supply process (e.g. future direction,

achieving core competency, stronger market base and identity). However, forming a successful

alliance is not an easy task to do as the barriers like clash of cultures, lack of coordination,

differences in operating procedures and attitudes, lack of clear goals, objectives and trust etc

must be overcome. (Zineldin & Dodourova 2005:462-463)

2.3. Factors influencing the decision of entry mode

While an industry may hold the promise of high growth, entry and expansion cannot be

successfully executed without a competitive position within the industry. Therefore entry mode

selection is very important, even critical strategic decision (Agarwal & Ramaswami 1992:2).

The list of the factors that influence the choice of entry mode is long. According to the results

of theoretical and empirical study by Yung (2006), FDI mode choice strategy is influenced by

three determinants: resources owned by the investor, resources specific to the host firm, and

20

risk derived from the international market. Zineldin & Dodourova (2005) showed in their

empirical study that the choice between strategic alliance and go-it-alone strategies depends on

the motives for entering to the foreign market. Claver et al. (2007) argue that the decision to

enter a foreign market should be based on balancing the risks and rewards derived from this

action. However, the evidence suggests that it is also determined by resource availability and

the need for control and choice of entry strategy also depends on the firm's surplus resources

(Claver et al 2007:2). Keillor et al (2001) argue that market/firm characteristics and

government policy/market imperfections have a significant relationship to entry strategy and

they are factors influencing choice of market entry mode. Kumar & Waheed (2007) concluded

in their study that strategic considerations for foreign market entry and expansion should take a

thorough account not only of the firms’ immediate operating needs but also of the competitive

environment in the dimensions of management, finance and macroeconomics.

In the following pages, the authors discuss more thoroughly the most important factors for the

choice of entry mode.

2.3.1. Company motives for entry to foreign market

As discussed already in the introductory part of this paper, there is the variety of motives for

the entry to foreign markets. Zineldin & Dodourova (2005) in their empirical study about

Swedish auto-manufacturers entry to Russia looked more into how these motives influence the

actual entry mode choice. They concluded that sharing research and development and vision,

common goals and new skills development as well as achieving stronger market position and

identity are the main motives when deciding to go for an alliance, while taking advantage of

emerging market opportunities seems to be more important to the manufacturers when

following go-it-alone strategy. The motives like increased customer service, reduced different

costs, increased market share and profits were equally important in case of alliance and go-it-

alone strategies.

They also found that a joint venture alliance may be more likely to be formed by partners that

have common goals and objectives and that joint venture alliance has a better chance to

succeed if the partners initially focus on financial objectives and at later stage on strategic and

managerial objectives.

21

Malhotra et al (2003:20) based on the analysis of various theoretical frameworks make three

conclusions related to the choice of entry based on company’s motives. These were:

⇒ The greater the significance of global synergy to the firm, the greater the probability is that

wholly owned FDI as a market entry strategy will occur at the maturity phase or early

standardization phase;

⇒ The greater the significance of global strategic motivations to the firm, the greater the

probability is that wholly owned FDI as a market entry strategy will occur at the maturity

phase or early standardization phase.

⇒ The greater the significance of global concentration to the firm, the greater the probability

is that wholly owned FDI as a market entry strategy will occur at the maturity phase or

early standardization phase.

When we look at the choice of international entry mode of firms from the perspectives of

transaction cost economics and real option theory, transaction cost economics focuses only on

cost minimization and does not consider opportunity costs associated with timing of entry,

omitting the impact of competitors action, fails to acknowledge the potential for future growth

generated by making investments when uncertainty is high (Leiblein 2003; Li 2007; Sanchez

2003; Zajacand Olsen, 1993 in Brouthers et al. 2008:936). On the other hand, real option

theory tries to address the short comings of transaction cost economics by focusing on cost

minimization and value creation as well as on the opportunity costs (the uncertainties)

associated with not making an investment (Buckley & Tse 1996; Buckley et al. 2002; Dixit &

Pindyck 1994; Kogut 1991 in Brouthers et al. 2008:.937).

In the existing literature, the entry mode decisions are often isolated from the sequence of

decisions. Entry mode decisions analysed in the context of transaction cost theory (Sarkar &

Cavusgil 1996; Rindfleisch & Heide 1997; Meyer 2001; Nakos & Brouthers 2002; Herrmann

& Datta 2002; Meyer 2004 and Zhao & Decker 2006) suggest that multinational enterprises

select entry mode through the minimization of the transaction costs associated with each form

of entry. North notes that firms try to minimize total cost, not just transaction costs (North

1987, 1990, North & Wallis 1994) in the choice of entry modes. While Kos (2010) believes

that cost minimization is critical in entry mode selection but it does not fully explain entry

mode choice (Kos, 2010:320).

22

2.3.2. Company’s internal resources

Choice of entry mode is affected by firms’ resources (Jansson & Sandberg 2008:67). As

compared to small firms, large firms tend to have greater levels of economic and managerial

resources for investments in the host market of entry. This view is supported by the transaction

cost view, which concludes that high control in entry strategies entails high resource

commitment. Wholly owned subsidiaries and joint ventures are high-cost entry modes because

of the level of resource commitment needed to set up operations (Pan & Chi 1999 in Johanson

& Tellis, 2008:2).

Each company is unique and this uniqueness stems from the resources it possesses, their

compability with one another and/or the way they are deployed (Sharma & Erramilli 2004:7).

Examples of such resources include all assets and capabilities, such as distinctive

competencies, technology, corporate culture, customer loyalty, brand name, machinery,

processes and procedures, market orientation and relational and intellectual assets (Hunt &

Morgan 1995, Reed & DeFillippi 1990, Srivastava, Shervani & Fahey 1998 in Sharma,

Erramilli 2004:7). The value of the a resource is defined in terms of its contribution to firm’s

competitive advantage (Madhok 1997 in Sharma & Erramilli 2004:9). The greater this

contribution, the greater the value.

When firm enters a foreign market, it typically relies on its existing resources to compete in

that market because it is generally more effective and/or efficient to transfer them to the foreign

market than develop new ones from scratch (Hu 1995, Madhok 1997, Kogut & Zander 1993 in

Sharma & Erramilli 2004:9). The challenge for entry modes is to transfer the firm’s resources

from the home country to the host country without affecting their ability to generate the desired

competitive advantage (Sharma & Erramilli 2004:9). If the key advantages are easily

transferable, the firm is able to choose the foreign production mode; if essential advantages are

difficult or costly to transfer, the firm will be confined to the exporting mode (Hu, 1995 in

Sharma & Erramilli 2004:10). Similar idea is expressed by Malhotra et al (2003), who propose

that the more tacit or higher the value of firm-specific know-how, the greater the probability is

that wholly owned FDI as a market entry strategy will occur during the new product or

maturity phase.

23

The following table summarizes the resource based view to the choice of entry mode:

PRODUCTION ACTIVITIES MARKETING ACTIVITIES

Firms likelihood of establishing comparative advantage in the host country

Firms ability to transfer advantage generating resources to host country partners

Firms likelihood of establishing competitive advantage in the host country

Firms ability to transfer advantage generating resources to host country partners

Favored entry mode (by the resource based framework)

Low N/A Low N/A Do not enter; Indirect exporting

Low N/A High High Direct exporting via host country intermediation

Low N/A High Low Direct exporting via company owned channels

High High High High Contractual mode (Licensing, franchising)

High High High Low Production Joint Venture

High Low High High Marketing Joint Venture

High Low High Low Wholly Owned Subsidiary

Table 1: Entry mode choices according to resource based view (Sharma&Erramilli 2004:11)

2.3.3. Cultural distance

Culture is usually defined as shared values and meanings of the members of a society. It affects

not only the underlying behaviour of customers in a market but also the execution and

implementation of marketing and management strategies. Thus, cultural distance has a direct

impact on the effectiveness of the entry (Kogut & Singh 1988 in Johanson & Tellis, 2008:4).

According to Choo & Mazzarol (2001) cultural differences are one of the most influential

factors of SME’s entry choice.

When a firm invests in foreign markets, it must face both national and corporate culture,

whether it invests through other organizations or not (Barkema et al., 1996 in Yung, 2006:205).

Hence, cultural differences between home and host market may affect how a firm operates in

the international market (Hofstede, 1980 in Yung, 2006:205). Such cultural differences may be

one of the most important decision-making determinants for the firm's foreign entry mode

24

choice (Barkema et al.; Kogut & Singh, 1988 in Yung, 2006:205).

Cultural distances between the home and the host country has different impacts on different

entry mode types. For example, high post-acquisition costs from international acquisition result

not only from different national cultures between home and host market but also from the

interactions between two organizational cultures (Kogut & Singh, 1988 in Yung, 2006: 205).

Thus the acquired firm is often troubled by "double-layered acculturation" problems resulting

from cultural distance between the acquirer and the acquired firm (Barkema et al., 1996 in

Yung, 2006:205). Hence, in order to reduce the risks of cultural distance between home and

host market, the investor is more likely to enter through Greenfield (Barkema & Vermeulen,

1998; Caves & Mehra, 1986; Kogut & Singh; Wu. 1990 in Yung, 2006:205). Kogut & Singh

(1988) in Muller (2007:94) found that with greater cultural distance Greenfield investment or

joint ventures are more likely than acquisition.

2.3.4. Risks related entry to foreign market

Generally speaking, a company opting to internationalise can select a market entry mode

ranging from very little risk and low capital expenditure (e.g. exporting) to relatively high risk

and high capital investment (e.g. manufacturing abroad) (Johanson & Vahlne 1977; Norvell,

Andrus & Gogumalla 1995). Meanwhile, two firms may perceive the same risk in a country but

choose different strategies because of each firm’s different tolerances of risk (Shama 1995 in

Choo & Mazzarol, 2001:298).

During the process of moving from home country to foreign market, firms face different types

of risks/barriers and each type of risks/barriers should be managed carefully. Malhotra et al.

(2003) discusses market variables during the entrance of an emerging market from country,

location, demand, and competition risks perspective:

Country risk refers primarily to the stability of the political, social, and economic conditions.

Firms tend to avoid or to limit their resource commitment in areas of high country risk.

Exporting and contractual agreements offer low resource commitment options in markets that

have high country risk. However, contractual agreements are increasingly used in countries

marked by high risk of intellectual property violation (as part of country-risk analysis) in which

the legislation and enforcement standards are weak (Kotabe, Sahay & Aulukh 1996 in Malhotra

et al, 2003:16).

25

Location risk is the perceived difference between home and host environments in terms of

culture, business, and economic practices. (Malhotra et al, 2003:18).

Demand risk is the risk taken by the firm because demand for its products or services may fail

to reach the desired level. When demand uncertainty is high or the expected demand is low,

firms favour entry modes that involve low resource commitment, e.g. exporting. Interesting is

that although contractual agreements such as franchising are a low-resource-commitment

option, studies indicate that a high demand potential is the key to their success (Alon & McKee

1999; Contractor & Kundu 1998 in Malhotra et al, 2003:18).

Competitive risk is the number and size of competitors and the aggressiveness of their

marketing efforts (Malhotra et al, 2003:19). When the intensity and competitive differential is

high, firms tend to avoid internalization. Exporting may be firms' preferred option. Strategic

alliances offer a promising alternative to exporting as they enhance knowledge and build

competitiveness (Madhok 1997, Sengupta & Perry 1997, Das & Teng 2000 in Malhotra et al,

2003:19).

On the basis of the preceding discussion, Malhotra et al (2003) make several conclusions

(however, not empirically validated) about which types of entry modes companies would most

probably prefer for the certain product phase in case of the high level of certain risk. The

conclusions are the following:

High degree of risk Product phase The most probable entry mode

Country risk Early standardization Exporting

Country risk Late standardization Contractual Agreement

Location risk Early standardization Exporting

Location risk Late standardization Contractual Agreement or Joint venture

Demand risk Early standardization Exporting

Competition risk Early standardization Exporting

Competition risk Late standardization Strategic alliance

Table 2: compiled by the authors based on Maholtra et al (2003:19)

Root (1987) in Rasheed (2005:44) describes foreign transactional risks from the perspective

of the host country’s political and economic stability and the host country’s policies and

regulations related to transnational business activities. Risk factors related to foreign

transactions include general stability risk, ownership/control risk, operating risk, and

26

transfer risk. General stability risk refers to management’s uncertainty about the future

viability of the host country’s political system (Root 1987). Ownership/control risk is defined

as management’s uncertainty about host government actions affecting the entrant’s ownership

position. Operations risk refers to the possibility of sanctions that could constrain an

investor’s operations in the host country. Transfer risk is defined as limitations on the

entrant’s ability to transfer capital out of the host country (Root 1987 in Rasheed, 2005:44).

There are additional risks for doing business in emerging markets. These include an

inadequate marketing infrastructure, such as poorly developed distribution systems; limited

communication channels; lack of regulatory discipline and frequent changes in regulation; a

high level of product diversion; various market failures; and political and economic instability

(Arnold & Quelch 1998, Garten 1997, Khanna & Palepu 1997, 2000 in Kim et al.,2004:15).

However, according to some authors, entering to developing markets can also have some

additional benefits. For example Huei-Ting & Eisingerich (2010:116) argue that markets to

developing countries are generally less expensive and less risky to enter due to lower

competition than in markets that are already developed and geographically farther away.

Host countries with greater probability of restrictive policies impede foreign investment and

encourage non-equity modes. On the other hand, firms with a proprietary product or

technology have a greater amount of leverage in countries characterized by high investment

risk and consequently may choose higher control modes (Agarwal & Ramaswami, 1992 in

Rasheed, 2005:45).

Doing business in foreign countries is deemed to be substantially more risky than remaining in

the domestic market (Ghoshal, 1987, Vernon, 1985 in Brouthers et al 2000:183). Miller (1992)

suggests that companies should consider evaluating several dimensions of international

environmental uncertainty in an effort to allow the firm to optimize its returns for the risk

assumed (Brouthers et al 2000:183). Agarwal & Ramaswami (1992:3) state that, with respect

to international markets, a firm is expected to choose the entry mode that offers the highest

risk-adjusted return on investment (Brouthers et al, 2000:183).

Each firm needs to define its risk tolerance, which is the basis factor for the firm to make entry

mode decisions (Kos, 2010:322). When company has low risk tolerance, then in case the

excessive return is higher than risk, company chooses joint venture or strategic alliance. When

company has high risk tolerance, then in case the excessive return is higher than risk, company

27

chooses wholly owned enterprise. In both cases, when the returns are smaller than risk,

company chooses not to enter (Kos, 2010:322). The following chart illustrates the firms’ entry

mode decision based on its risk tolerance level:

Figure 1 – An explanatory model for the decision to enter emerging markets: A shareholder

perspective (Kos, 2010:323).

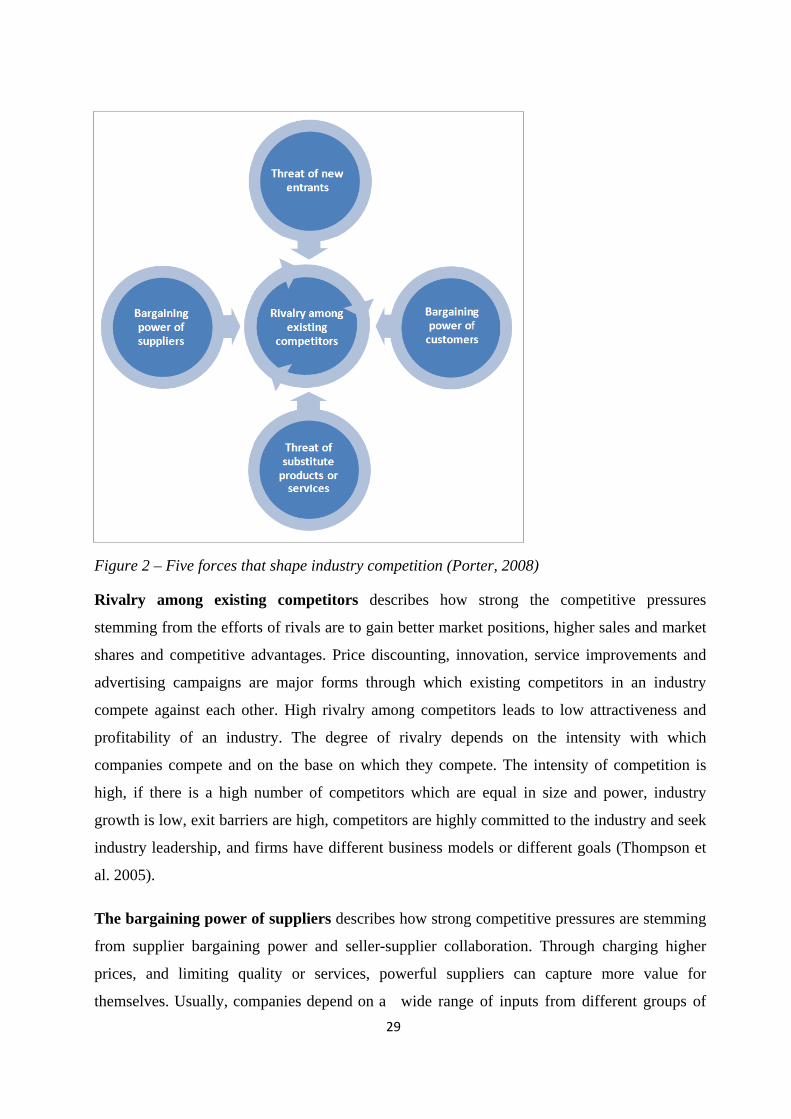

2.3.5. Industry situation / competition in the host market

Competition is often defined too narrowly, not taking into account forces except from today’s

direct competitors (Porter, 2008). In order to formulate market entry strategies, understanding

and coping with different forces influencing the level of competition is essential. Porter (2008)

argued that the profitability of an industry is determined by five forces. Except from rivalry

between existing competitors, industry attractiveness is additionally influenced by the four

following forces, illustrated in figure 3: customers and suppliers in the vertical dimension,

potential market entrants and substitute products in the horizontal dimension. Whether the

forces are intense or benign, determines the extent to which a company earns returns on

investment (Thompson et al. 2005).

28

Figure 2 – Five forces that shape industry competition (Porter, 2008)

Rivalry among existing competitors describes how strong the competitive pressures

stemming from the efforts of rivals are to gain better market positions, higher sales and market

shares and competitive advantages. Price discounting, innovation, service improvements and

advertising campaigns are major forms through which existing competitors in an industry

compete against each other. High rivalry among competitors leads to low attractiveness and

profitability of an industry. The degree of rivalry depends on the intensity with which

companies compete and on the base on which they compete. The intensity of competition is

high, if there is a high number of competitors which are equal in size and power, industry

growth is low, exit barriers are high, competitors are highly committed to the industry and seek

industry leadership, and firms have different business models or different goals (Thompson et

al. 2005).

The bargaining power of suppliers describes how strong competitive pressures are stemming

from supplier bargaining power and seller-supplier collaboration. Through charging higher

prices, and limiting quality or services, powerful suppliers can capture more value for

themselves. Usually, companies depend on a wide range of inputs from different groups of

29

suppliers. A supplier group is powerful, if it is more concentrated than the industry it sells to,

the supplier group does not depend heavily on the industry for its revenues, industry

participants face switching costs when changing suppliers, suppliers offer products which are

differentiated, there are no substitutes for what the supplier group provides, and the supplier

group can credibly threaten to integrate forward into the industry. These factors can increase

the power of supplier groups, which negatively influences the level of attractiveness and

profitability of an industry (Thompson et al. 2005).

The bargaining power of customers describes how strong the competitive pressures are from

buyer bargaining power and seller-buyer collaboration. Powerful customers can play industry

participants off against each other, at the expense of industry profitability. Powerful customers

are able to capture more value by demanding lower prices, higher quality and more services.

Customers have a high negotiating power if: there are few customers, the industry’s products

are standardized or undifferentiated, customers face switching costs in changing vendors or

customers can integrate backward into the industry. A customer is price sensitive if: the

product it purchases accounts for a significant share of its cost structure or procurement budget,

the customer earns low profits or is under pressure to lower purchasing costs (Thompson et al.

2005).

Threat of entry expresses how strong competitive pressures are associated with the entry

threat from new rivals. If new companies enter an industry, they aim to gain market shares

which puts pressure on costs, prices and the rate of investment necessary to compete in the

industry. There are seven major sources for entry barriers, which have the potential to prevent

companies from entering an industry and therefore contribute to high industry profitability:

supply-side economies of scale, demand-side benefits of scale, high switching costs of

customers, high capital requirements, incumbency advantages independent of size, unequal

access to distribution channels, and restrictive government policy. Additionally, a company’s

decision to enter or stay out of an industry is influenced by the anticipated reaction of

incumbents (Thompson et al. 2005).

The threat of substitutes describes how strong the competitive pressures are coming from the

attempts of companies outside the industry to win buyers over to their products. Substitute

products are present for any product, but they are likely to be overlooked in a competitive

analysis, since they can be very different from the industry’s product. A substitute product is

characterized by having the same or a similar function as an industry’s product by a different

30

means. The higher the threat of substitutes, the lower is the profitability of the industry. The

threat of a substitute is high if the customer’s costs of switching to the substitute are low, and if

the price performance trade-off to the industry’s product is attractive (Thompson et al. 2005).

2.3.6. External environment

Jansson (2007) argue that business environments in emerging country markets might be

different from Western markets due to differences among institutions. Large emerging markets

are regarded to be uncertain and complex. Therefore, the business environment is regarded to

be relationship-oriented and institution-building, which results in the characteristic of being a

network society. By using the institutional network approach, the description and analysis of

these uncertain and complex business environments can be enhanced. The institutional network

approach aims to reduce the risk of doing business in an emerging market by making

environmental factors more transparent and predictable before entering the foreign market

(Jansson, 2007).

According to Jansson’s (2007) basic institutions model, the company’s internal and external

environment can be divided into three layers of description for the rules prevailing for the

institutions in the respective layers, which are embedded into each other. Institutions are

characterized by predictability and standardized behaviour. Uncertainty can be reduced by

anticipating recurring behaviour. Furthermore, institutions are described to be stable which

results in established patterns of behaviour (Jansson, 2007).

The central layer contains micro institutions, e.g. the multinational company, which is

surrounded by institutions impacting on it. These institutions can be divided into two layers.

Firstly, the meso institutions level is represented by the organizational fields. Meso institutions

such as the government, the financial market, the product and service market and the labour

market have a direct impact on the multinational company but are also characterized by

influencing the societal institutions. Secondly, the societal institutions contain macro

institutions, influencing the multinational company in one direction, from the sector via the

organizational fields towards the multinational company. This layer contains the country

culture, the educational and training system, the political system, the legal system, professional

and interest associations, business moral, the religion and family/clan (Jansson, 2007).

31

The institutional network approach is visualized in figure 3 by the basic institutions model,

illustrating the constellation of the three layers and the institutions which they contain.

Religion

Family/Clan

Country Culture

Legal System

Political System

Professional and Interest Associations

Business Moral

Educational / Training System

Government

Financial Market

Product / Service Market

Labour Market

BUSINESS NETWORK

ORGANIZATIONAL FIELDS

SOCIETAL INSTITUTIONS

Figure 3 – The basics institutions model (Jansson, 2007)

2.3.7. Additional aspects for the entry to emerging markets

Emerging economic regions are generally characterized by relatively high market growth rates,

short histories of economic liberalization, and a lack of established institutional systems that

support domestic business activities (Isobe et al. 2000:471). Emerging markets exhibit high

growth potential and present a mixture of opportunities and risks for western companies

(Cavusgil 1997; Garten 1997; Kock & Guillen 2001 in Kim et al. 2004:15). Kim et al. (2004)

argue that emerging markets attract not only in cheap raw materials but also in the potential to

generate revenue and also they are not only suppliers but also buyers of goods and services.

Smallness is usually considered a disadvantage in internationalisation, as small and medium

enterprises often lack resources necessary to enter foreign markets. Compared to large

enterprises small and medium enterprises are less competitive. For instance they may not be

able to capture business opportunities due to inferior products, shortages of finance and limited

administration capacity (Jansson 2007, Mayer & Skak 2002 in Jansson & Sandberg 2008:66).

32

However, Johanson & Tellis (2008) have come up with the following findings in their study

regarding entry into an emerging market:

⇒ Smaller firms tend to be more successful than larger firms in entering emerging markets.

⇒ Entry strategies that involve high levels of control (e.g., wholly owned subsidiaries) are

more successful than those that involve low levels of control (e.g., licensing).

⇒ Earlier entrants enjoy greater success than later entrants.

Foreign investors entering emerging markets have to take strategic decisions on where and how

to set up operations (Meyer & Nguyen, 2005:63). According to the internationalisation process

theory firms tend to invest and expand in countries with a short psychic distance to the home

country (Amdam, 2009:445). The psychic distance between two countries depends on

differences in their languages, education, business practices, culture and industrial

development. The uncertainty related to foreign markets and the impact of psychic distance can

be reduced by means of interaction and integration with the market environment (Johansonet

al., 1977 in Reiljan, 2003:10).On the other hand Sim & Ali (2001) argue that firms originating

from countries at different levels of economic development seem to exhibit differences in

internationalisation (Sim & Ali, 2001:58).

Journal of accountancy (2001) has enlisted three steps a company should take before entering

the international emerging market: 1) conduct preliminary market research, 2) plan the market

entry and 3) arrange for distribution. According to Lord & Ranft (2000) in Pedersen & Petersen

(2004), the acquisition of local-market knowledge is critical for successful planning and

implementation of entry to an emerging market. Madhok (1998) in Kos (2010:321) found that

the organizational capability is a key determinant of firm boundaries of multinational

enterprises entering emerging markets.

Maximizing risk adjusted reward is the key aspect of investing in an emerging market (Ollson,

2002 in Kos, 2010:321). A major challenge for foreign investors in emerging economies is the

rapid change of institutions. In transition economies, reforms initially concern primarily formal

institutions at the central level (World Bank, 1996 in Meyer & Nguyen, 2005:69).

According to the theoretical and empirical study result, Chung & Neamish (2005:58) suggest

that foreign firms can proactively pursue opportunities in emerging economies, but with

calculated risk-taking strategies. And further, they propose that firms can take the form of joint

venture, minority joint venture or manufacturing operations in emerging economies.

33

2.4. Entry nodes

Firms entering emerging markets face several barriers according to Meyer (2001) in Jansson &

Sandberg (2008:67). These barriers include lack of information, unclear regulations and

corruption. In order to overcome those barriers, the relationships in the host country are needed

as through them the adequate information and know-how about the new external environment

is built. In terms of research in this area, scholars have found that relationships are the core of

the internationalisation process and according to network approach to internationalisation,

entries into local market networks take place through establishing relationships (Axelsson &

Johansson 1992, ford 2002, Hakansson 1982, Hakansson & Snehota 1995, Hammarkvist et al

1982, Jansson 1994, 2007, Johanson & Vahlne 2003, Majkkgard & Sharma 1998 in Jansson

& Sandberg 2008:67).

Establishment points in foreign market networks are defined as entry nodes. There are various

routes into these networks, or nodes by which a firm can enter a network. Entries through trade

either take place directly with customers or indirectly through intermediaries. Direct

relationships, dyads, can be established between buyer and seller in the respective countries.

Indirect relationships, triads, involve an outside party or other type of entry node, usually an

intermediary such as an agent, dealer or distributor (Jansson & Sandberg 2008:68).

One factor influencing the entry node is the structure of the local market network – if it has

loose or tight coupling (Jansson & Sandberg 2008:68). For instance structural changes and

economic reforms in the transitional markets can lead industrial networks to become less

tightly structured (which have happened in CEE, for example). With old regulations moved,

companies are now free to decide by themselves on new business partners and business

relationships. In transition economies, relationships tend to move from being fragmented to

being integrated relations. (Hallen & Johanson 2004 in Jansson & Sandberg 2008:68).

The empirical study conducted by Jansson & Sandberg (2008) about the internationalisation of

small and medium sized companies in the Baltic Sea region concluded that third-party

relationships (the entry node triad) are vital for SMEs. The relationship with the agent provides

the seller with the linkage to the market: to obtain information on the market and to manage the

communication with customers in the foreign language, and with parties belonging to another

business culture. The point of attention, however, is that the indirect relationships could cut-off