elliott perspectives on hyundai motor group’s … · why are we here? 4 • in reality,the...

TRANSCRIPT

1

Elliott perspectives on Hyundai Motor Group’s Restructuring Plan

Important Information

2

This Presentation (i) is from and is published by Elliott Associates, L.P. (“EALP”) and Potter Capital LLC (“Potter”), both of which are Elliott affiliates; and (ii) supplements the letter and presentation from EALPand Potter to the directors of Hyundai Mobis Co., Ltd., Hyundai Motor Company, and Kia Motors Corporation, dated 23 April 2018 (the “Letter”). Capitalized terms used in this Presentation shall unlessotherwise defined bear the meanings ascribed to them in the Letter. Many of the statements in this Presentation as well as in the Letter are the opinions and/or beliefs of EALP and/or Potter, which are basedon their own analysis of publicly available information. Any statement or opinion expressed or implied in this Presentation and the Letter is provided in good faith but only on the basis that no investmentdecision(s) will be made based on, or other reliance will be placed on, any of the contents herein by others.

EALP, Potter, Elliott and/or any of their respective affiliates (i) may at any time in the future, without notice to any person (other than as required under, or in compliance with, applicable laws and regulations),increase or reduce their holdings of any Hyundai group entity’s shares or other equity or debt securities (including such securities and derivative products directly and/or indirectly related to such securitiesincluding, for example, KOSPI 200 Index) and/or may at any time have long, short, neutral or no economic or other exposure in respect of any Hyundai group entity’s shares or other equity or debt securities;and/or (ii) may now have and/or at any time in the future, without notice to any person (other than as required under, or in compliance with, applicable laws and regulations), establish, increase and/or decreaselong or short positions in respect of or related to any Hyundai group entity’s shares or other equity or debt securities (including such securities and derivative products directly and/or indirectly related to suchsecurities including, for example, KOSPI 200 Index), in each case irrespective of whether or not all or any of the Accelerate Hyundai Proposals or the HMG Restructuring Plan are or are expected to beimplemented.

This Presentation is published solely for informational purposes and is not, and may not be construed as, investment, financial, legal, tax or other advice.

This Presentation has been compiled based on publicly available information, which has not been separately verified by EALP, Potter or Elliott or any of their respective affiliates, and does not:

(i) purport to be complete or comprehensive; or

(ii) constitute an agreement, offer, a solicitation of an offer, or any advice or recommendation to enter into or conclude any transaction or take or refrain from taking any other course of action(whether on the terms shown herein or otherwise).

The market data contained in or utilized for the purposes of preparing this Presentation is (unless otherwise specified) as at the end of trading hours on 10 May 2018. Changes may have occurred or may occurwith respect to such market data and neither EALP, Potter nor Elliott or any of their respective affiliates is under any obligation to provide any updated or additional information or to correct any inaccuracies inthis Presentation.

This Presentation contains “forward-looking statements.” Specific forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts and include, withoutlimitation, words such as “may,” “can,” “will,” “expects,” “believes,” “anticipates,” “plans,” “estimates,” “projects,” “targets,” “forecasts,” “seeks,” “could,” “would” or the negative of such terms or other variations onsuch terms or comparable terminology. Similarly, statements that describe any objectives, plans or goals of EALP and/or Potter are forward-looking. Any forward-looking statements are based on the currentintent, belief, expectations, estimates and projections of EALP and/or Potter. These statements are not guarantees of future performance and involve risks, uncertainties, assumptions and other factors that aredifficult to predict and that could cause actual results to differ materially. Accordingly, you should not rely upon forward-looking statements as a prediction of actual results, and actual results may vary materiallyfrom what is expressed in or indicated by the forward-looking statements.

No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement orsummary of the securities, markets or developments referred to herein. I t should not be regarded by recipients as a substitute for the exercise of their own judgment. You should obtain your own professionaladvice and conduct your own independent evaluation with respect to the subject matter herein. The information contained herein has been made available on the basis that the recipient is a person into whosepossession such information may be lawfully delivered in accordance with the laws of the jurisdiction in which the recipient is located.

Each of EALP, Potter, Elliott and their respective affiliates expressly disclaims any responsibility or liability for any loss howsoever arising from any use of or reliance on this Presentation or the Letter or theircontents as a whole or in part by any person, or otherwise howsoever arising in connection with this Presentation or the Letter.

Why are we here?

3

• Elliott is a significant shareholder in Hyundai Mobis Co., Ltd. (“Mobis”), Hyundai Motor Company (“HMC”) and Kia Motors Corporation (“Kia”),collectively the Hyundai Motor Group (“HMG”), holding over 1.5% common shares in each of the companies

• HMG announced a plan for business restructuring after market close on 28 March 2018 which involves Mobis spinning off its domestic module andafter-sales servicebusinessesand merging the spun-off businesses with Glovis (“HMGRestructuring Plan” or the “Plan”)

• Mobis has communicated in its materials that this restructuring is needed to (i) sever existing circular shareholdings, and (ii) eliminate potential risksarising from existing affiliate transactions1

• However, the spin-off merger by itself does nothing to resolve the existing circular shareholding

• Post spin-off merger, a share swap between the principal shareholders’ stake in Glovis and Kia’s stake in Mobis is required to sever the maincircular shareholding. However, thePlan is devoid ofa transparent process to realize fair value for Kia’s stake in Mobis

• The Plan to merge Mobis’s spun-off business with Glovis is not supported by sound business rationale and the valuation of Mobis’s spun-offbusiness is based on a questionable set of assumptions that results in its significant undervaluation

Notes: 1. Page 3 of Spin-off Merger IR Material published on 28th March 2018.

HMC

Mobis

Kia

Glovis Hyundai Steel

HMC

Mobis(post spin-off)

Kia

Glovis(post merger) Hyundai Steel

Why are we here?

4

• In reality, the HMG’s Restructuring Plan has many of the characteristics of a similar transaction that Elliott voiced significant concerns about threeyears ago: the merger between Samsung C&T and Cheil Industries

• As was the case with Samsung C&T’s management, HMG management has failed to act in the best interest of the companies and their respectiveshareholders with this Plan. The HMG Restructuring Plan continues the Group’s poor track record of deals, which have been value dilutive for theshareholders (e.g. KEPCO land purchase, and acquisitions of Hyundai E&C and Green CrossLife)

• With the support of many domestic and international shareholders, Elliott unveiled its Accelerate Hyundai Proposals on 23 April 2018 to makerecommendations on how the HMG Restructuring Plan could be improved by adopting a holding company structure

− A holding company structure is more tax efficient and sustainable in the long run. Elliott agrees that the leasing business is integral to HMG’sauto business and supports a restructuring that will enable the Group to retain control of the leasing business that is legal and within the confinesof current regulations

− Elliott also believes a holding company structure can be achieved via a further demerger of the financial subsidiaries. Hyundai Capital does nothave to be a subsidiary of HMC and Kia for it to support the Group’s auto business

• Elliott also proposed actionable targets for balance sheet optimization, improved shareholders returns, and board structures and articleamendments that would ensure best-in-classcorporate governance for the Group

• Since then, HMG has announced token measures on share buybacks and cancellation of some existing treasury shares. While Elliott believes thisis a positive development, more significant measures are needed to address the long-unresolved issues at the Group that have led to significantvaluation discounts and underperformance at each Mobis, HMC and Kia

• Elliott supports a fair restructuring of HMG that treats all shareholders equally, and the current HMG Restructuring Plan is neither fair norcomprehensive enough to receive its support

Notes: 1. Page 3 of Spin-off Merger IR Material published on 28 March 2018.

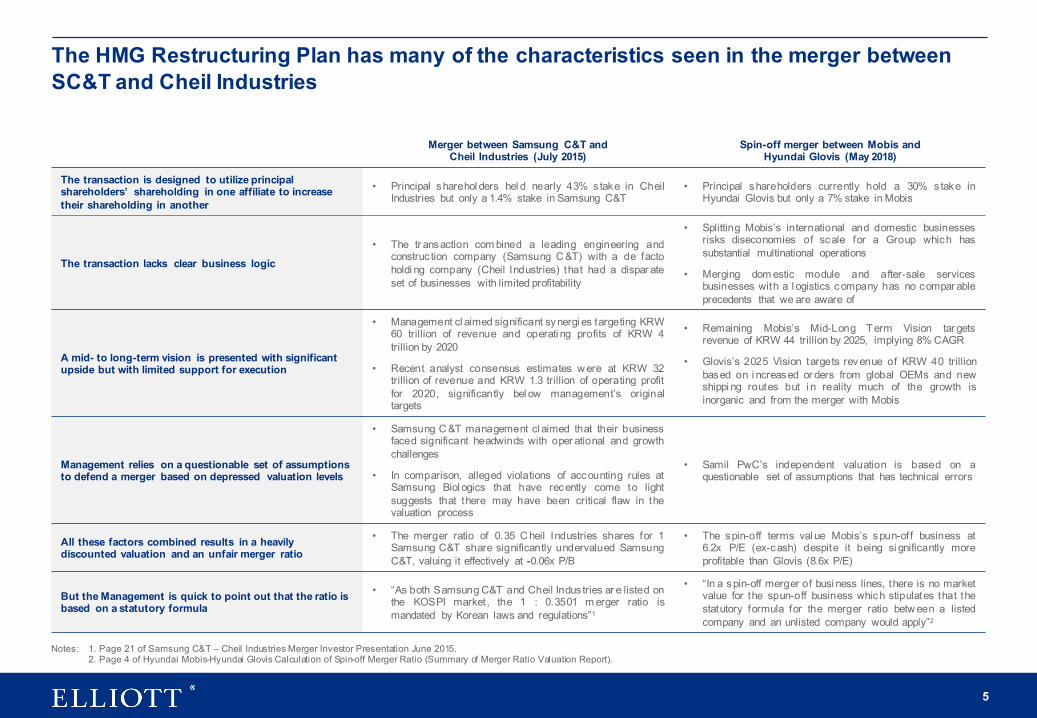

The HMG Restructuring Plan has many of the characteristics seen in the merger between SC&T and Cheil Industries

5

Notes: 1. Page 21 of Samsung C&T – Cheil Industries Merger Investor Presentation June 2015.2. Page 4 of Hyundai Mobis-Hyundai Glovis Calculation of Spin-off Merger Ratio (Summary of Merger Ratio Valuation Report).

Merger between Samsung C&T and Cheil Industries (July 2015)

Spin-off merger between Mobis and Hyundai Glovis (May 2018)

The transaction is designed to utilize principal shareholders’ shareholding in one affiliate to increase their shareholding in another

• Principal sharehol ders hel d nearly 43% stake in CheilIndustries but only a 1.4% stake in Samsung C&T

• Principal shareholders currently hold a 30% stake inHyundai Glovis but only a 7% stake in Mobis

The transaction lacks clear business logic

• The tr ansaction com bined a leading engineering andconstruc tion company (Samsung C &T) with a de factoholdi ng company (Cheil Industries) that had a dispar ateset of businesses with limited profitability

• Splitting Mobis’s international and domestic businessesrisks diseconomies of scale for a Group which hassubstantial multinational operations

• Merging dom estic module and after-sale servicesbusinesses with a l ogistics company has no compar ableprecedents that we are aware of

A mid- to long-term vision is presented with significant upside but with limited support for execution

• Management cl aimed significant synergi es targeting KRW60 trillion of revenue and operati ng profits of KRW 4trillion by 2020

• Recent analyst consensus estimates w ere at KRW 32trillion of revenue and KRW 1.3 trillion of operating profitfor 2020, significantly bel ow management’s originaltargets

• Remaining Mobis’s Mid-Long Term Vision tar getsrevenue of KRW 44 trillion by 2025, implying 8% CAGR

• Glovis’s 2025 Vision targets revenue of KRW 40 trillionbased on i ncreased or ders from global OEMs and newshippi ng routes but i n reality much of the growth isinorganic and from the merger with Mobis

Management relies on a questionable set of assumptions to defend a merger based on depressed valuation levels

• Samsung C &T management cl aimed that their businessfaced significant headwinds with oper ational and growthchallenges

• In comparison, alleged violations of accounting rules atSamsung Biol ogics that have recently come to lightsuggests that there may have been critical flaw in thevaluation process

• Samil PwC’s independent valuation is based on aquestionable set of assumptions that has technical errors

All these factors combined results in a heavily discounted valuation and an unfair merger ratio

• The merger ratio of 0.35 C heil Industries shares for 1Samsung C&T share significantly undervalued SamsungC&T, valuing it effectively at -0.06x P/B

• The spin-off terms val ue Mobis’s spun-off business at6.2x P/E (ex-cash) despite it being si gnificantly moreprofitable than Glovis (8.6x P/E)

But the Management is quick to point out that the ratio is based on a statutory formula

• “As both Samsung C&T and Cheil Indus tries ar e listed onthe KOSPI market, the 1 : 0.3501 m erger ratio ismandated by Korean laws and regulations”1

• “In a spin-off merger of busi ness lines, there is no marketvalue for the spun-off business which stipulates that thestatutory formula for the merger ratio betw een a listedcompany and an unlisted company would apply”2

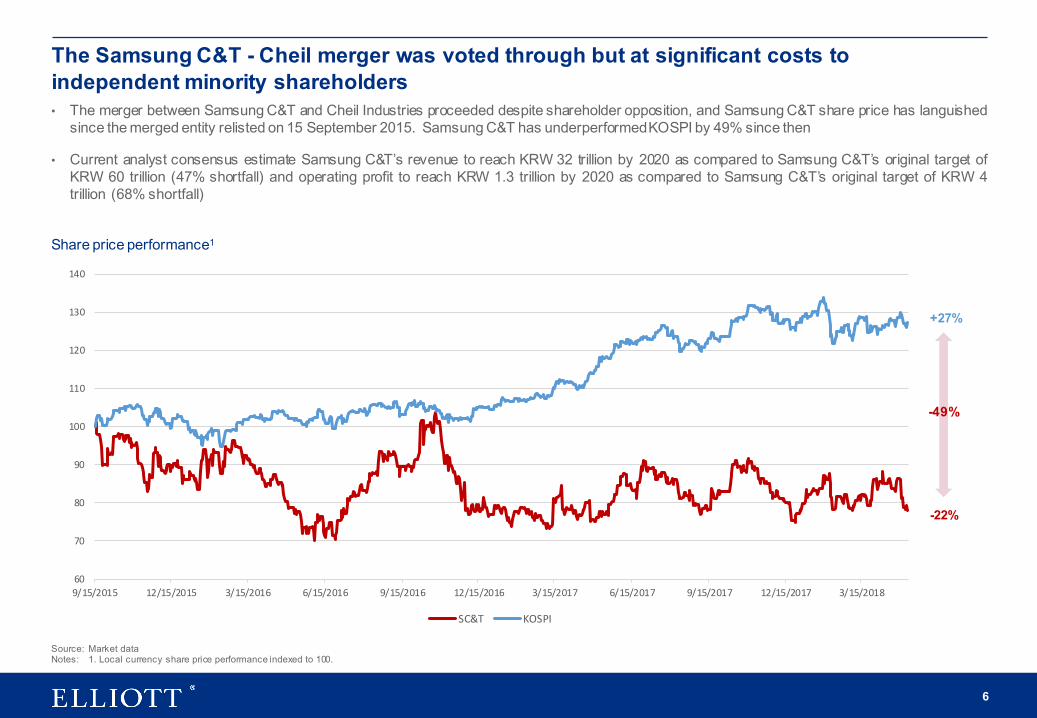

The Samsung C&T - Cheil merger was voted through but at significant costs to independent minority shareholders

6

Source: Market dataNotes: 1. Local currency share price performance indexed to 100.

• The merger between Samsung C&T and Cheil Industries proceeded despite shareholder opposition, and Samsung C&T share price has languishedsince the merged entity relisted on 15 September 2015. Samsung C&T has underperformedKOSPI by 49% since then

• Current analyst consensus estimate Samsung C&T’s revenue to reach KRW 32 trillion by 2020 as compared to Samsung C&T’s original target ofKRW 60 trillion (47% shortfall) and operating profit to reach KRW 1.3 trillion by 2020 as compared to Samsung C&T’s original target of KRW 4trillion (68% shortfall)

+27%

-22%

60

70

80

90

100

110

120

130

140

9/15/2015 12/15/2015 3/15/2016 6/15/2016 9/15/2016 12/15/2016 3/15/2017 6/15/2017 9/15/2017 12/15/2017 3/15/2018

SC&T KOSPI

Share price performance1

-49%

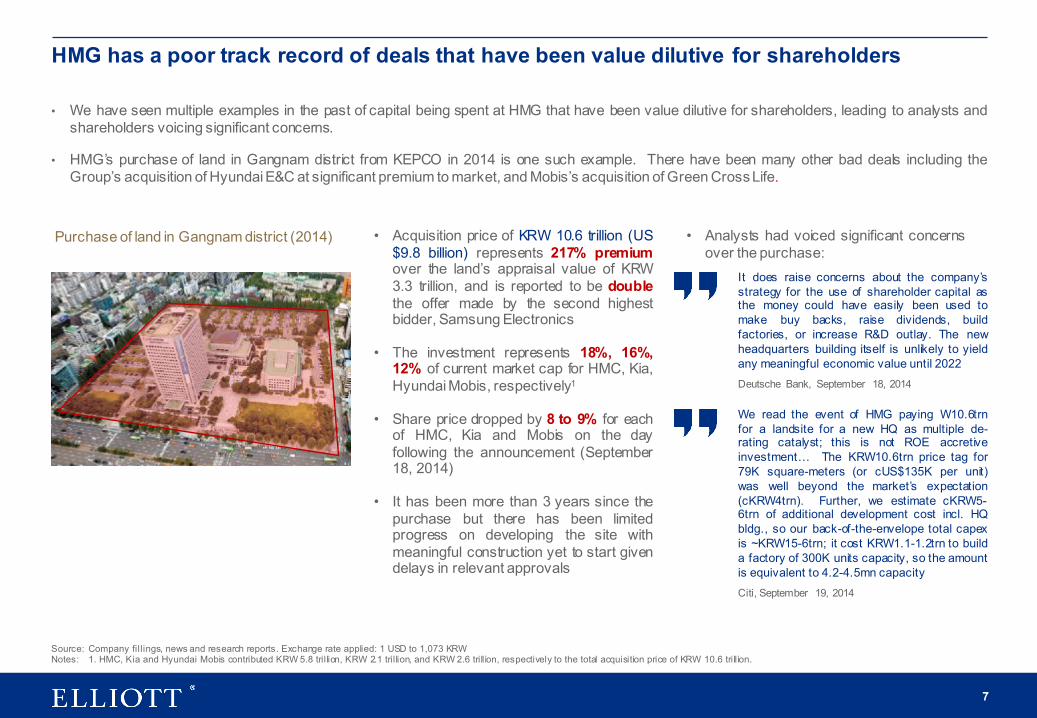

HMG has a poor track record of deals that have been value dilutive for shareholders

7

Purchase of land in Gangnam district (2014)

It does raise concerns about the company’sstrategy for the use of shareholder capital asthe money could have easily been used tomake buy backs, raise dividends, buildfactories, or increase R&D outlay. The newheadquarters building itself is unlikely to yieldany meaningful economic value until 2022Deutsche Bank, September 18, 2014

We read the event of HMG paying W10.6trnfor a landsite for a new HQ as multiple de-rating catalyst; this is not ROE accretiveinvestment… The KRW10.6trn price tag for79K square-meters (or cUS$135K per unit)was well beyond the market’s expectation(cKRW4trn). Further, we estimate cKRW5-6trn of additional development cost incl. HQbldg., so our back-of-the-envelope total capexis ~KRW15-6trn; it cost KRW1.1-1.2trn to builda factory of 300K units capacity, so the amountis equivalent to 4.2-4.5mn capacityCiti, September 19, 2014

• Acquisition price of KRW 10.6 trillion (US$9.8 billion) represents 217% premiumover the land’s appraisal value of KRW3.3 trillion, and is reported to be doublethe offer made by the second highestbidder, Samsung Electronics

• The investment represents 18%, 16%,12% of current market cap for HMC, Kia,Hyundai Mobis, respectively1

• Share price dropped by 8 to 9% for eachof HMC, Kia and Mobis on the dayfollowing the announcement (September18, 2014)

• It has been more than 3 years since thepurchase but there has been limitedprogress on developing the site withmeaningful construction yet to start givendelays in relevant approvals

• We have seen multiple examples in the past of capital being spent at HMG that have been value dilutive for shareholders, leading to analysts andshareholders voicing significant concerns.

• HMG’s purchase of land in Gangnam district from KEPCO in 2014 is one such example. There have been many other bad deals including theGroup’s acquisition of Hyundai E&C at significant premium to market, and Mobis’s acquisition of Green CrossLife.

• Analysts had voiced significant concernsover the purchase:

Source: Company fillings, news and research reports. Exchange rate applied: 1 USD to 1,073 KRWNotes: 1. HMC, Kia and Hyundai Mobis contributed KRW 5.8 trillion, KRW 2.1 trillion, and KRW 2.6 trillion, respectively to the total acquisition price of KRW 10.6 trillion.

Shortcomings of the HMG Restructuring Plan

8

The proposed spin-off merger lacks clear business logic

9

1. After the spin-off, the remaining Mobis will own the core parts business, overseas module manufacturing and overseas after-sales servicesbusinesses as well as investments in affiliates (HMC, Hyundai E&C, etc.)

2. Meanwhile, the spun-off Mobis that is to be merged with Glovis will own the domestic module and domestic after-sales services businesses andKRW 2.5 trillion of cash and equivalents

• We are not convinced by the business rationale provided to support separating the module manufacturing and after-sales services businessesfrom the international subsidiaries in the same business lines

• The segregation of the domestic operations from international operations for these two businesses creates a risk of weakening their competitivepositioning and resulting diseconomies of scale

• No business rationale was provided for KRW 2.5 trillion of cash and equivalents assumed to be in the spun-off entity to be merged with Glovis.Splitting cash and equivalent based on asset split (excluding investment securities) is not a business rationale

3. As Mobis’s shareholder, we find splitting the highly profitable and cash generative after-sales services business and merging with a logisticscompany (Glovis) not convincing

• We found no comparable precedents for an after-sale service business combining with a logistics company; nor has HMG provided any casestudy to persuade us otherwise

• Mobis has yet to present any quantifiable synergies for combining Glovis and Mobis’s module manufacturing and after-salesservicesbusinesses

The mid- to long-term vision for remaining Mobis is at best unconvincing

10

• Mobis announced its mid- to long-term vision for the remaining Mobis on 26 April 2018, in which the Management provided the market with veryambitious revenue growth targets with limited specifics on execution

• Management guided for remaining Mobis’s overall revenue to rise from KRW 25 trillion in 2018 to KRW 44 trillion by 2025 (implied CAGR of 8%)through organic growth

• However, given HMG’s own growth outlook and Mobis’s progress on its expansion to non-captive customers so far, much more details areneeded for shareholders to assess the feasibility of such growth targets

• The Company has also failed to explain why the spin-off merger is necessary for Mobis to achieve these targets in its mid- to long-term vision

• Analysts consensusestimate standalone Mobis’s revenue to reach KRW 41 trillion by 2020, representing 3 year CAGR of 5%

• Management has failed to make a convincing case on why spinning out a highly cash generative domestic after-sales services business(together with KRW 2.5 trillion of cash) is necessary for them to achieve expansion in Mobis’s core partsand future tech businesses

• Meanwhile, Glovis’s 2025 vision after merging with Mobis is to reach revenue targets of KRW 40 trillion by 2025, effectively relying on theacquisition of the spun-off business to fuel growth

• Analysts consensusestimate standalone Glovis’s revenue to reach KRW 18.5 trillion by 2020, representing 3 year CAGR of 4%

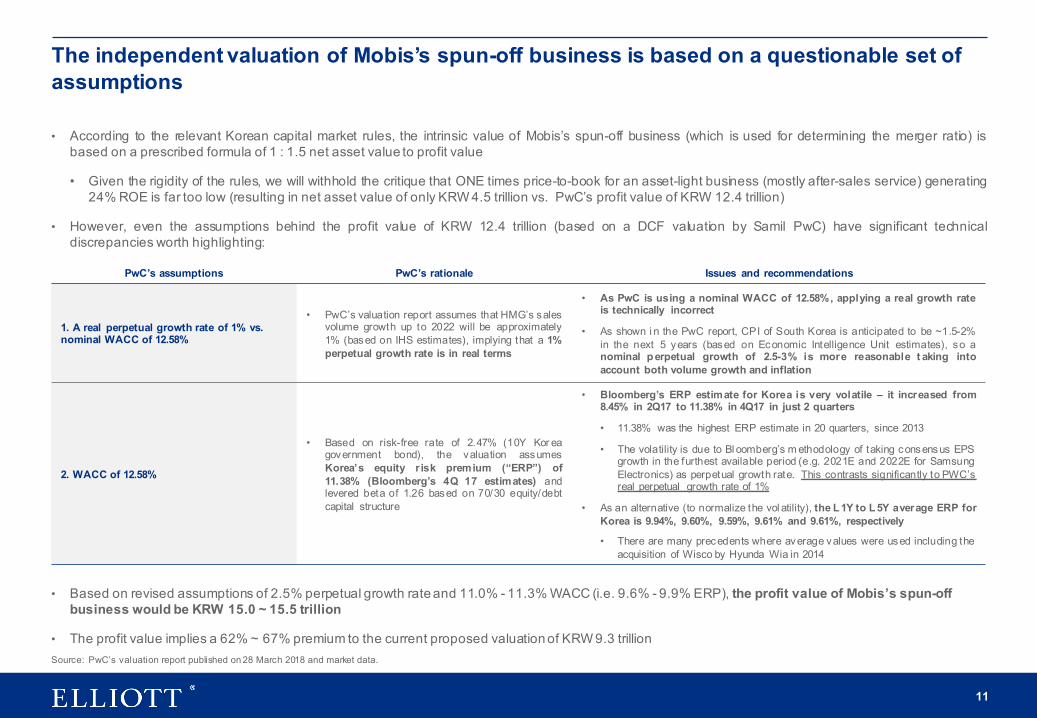

• According to the relevant Korean capital market rules, the intrinsic value of Mobis’s spun-off business (which is used for determining the merger ratio) isbased on a prescribed formula of 1 : 1.5 net asset value to profit value

• Given the rigidity of the rules, we will withhold the critique that ONE times price-to-book for an asset-light business (mostly after-sales service) generating24% ROE is far too low (resulting in net asset value of only KRW 4.5 trillion vs. PwC’s profit value of KRW 12.4 trillion)

• However, even the assumptions behind the profit value of KRW 12.4 trillion (based on a DCF valuation by Samil PwC) have significant technicaldiscrepancies worth highlighting:

• Based on revised assumptions of 2.5% perpetual growth rate and 11.0% - 11.3% WACC (i.e. 9.6% - 9.9% ERP), the profit value of Mobis’s spun-off business would be KRW 15.0 ~ 15.5 trillion

• The profit value implies a 62% ~ 67% premium to the current proposed valuation of KRW 9.3 trillion

The independent valuation of Mobis’s spun-off business is based on a questionable set of assumptions

11

Source: PwC’s valuation report published on 28 March 2018 and market data.

PwC’s assumptions PwC’s rationale Issues and recommendations

1. A real perpetual growth rate of 1% vs. nominal WACC of 12.58%

• PwC’s valuation report assumes that HMG’s salesvolume growth up to 2022 will be approximately1% (based on IHS estimates), implying that a 1%perpetual growth rate is in real terms

• As PwC is using a nominal WACC of 12.58%, applying a real growth rateis technically incorrect

• As shown i n the PwC report, CPI of South Korea is anticipated to be ~1.5-2%in the next 5 years (based on Economic Intelligence Unit estimates), so anominal perpetual growth of 2.5-3% is more reasonable t aking intoaccount both volume growth and inflation

2. WACC of 12.58%

• Based on risk-free rate of 2.47% (10Y Kor eagovernment bond), the valuation assumesKorea’s equity r isk premium (“ERP”) of11.38% (Bloomberg’s 4Q 17 estimates) andlevered beta of 1.26 based on 70/30 equity/debtcapital structure

• Bloomberg’s ERP estimate for Korea is very volatile – it increased from8.45% in 2Q17 to 11.38% in 4Q17 in just 2 quarters

• 11.38% was the highest ERP estimate in 20 quarters, since 2013

• The volatility is due to Bl oomberg’s m ethodology of taking consensus EPSgrowth in the furthest available period (e.g. 2021E and 2022E for SamsungElectronics) as perpetual growth rate. This contrasts significantly to PWC’sreal perpetual growth rate of 1%

• As an alternative (to normalize the vol atility), the L1Y to L5Y average ERP forKorea is 9.94%, 9.60%, 9.59%, 9.61% and 9.61%, respectively

• There are many precedents where average values were used including theacquisition of Wisco by Hyunda Wia in 2014

(KRWbn)Mobis

(pre spin-off)Mobis

(remaining business)Mobis

(spun-off business)Glovis

(pre-merger)Global auto parts peers’ average1

Pre-announcement market price (KRW) 261,500Merger price (KRW) 452,523 154,911Equity value (excl. treasury) 24,764

(based on market value)

15,493(market value -merger value)

9,271(based on

merger value)

5,809(based on

merger value)

Net debt / (cash) (6,030) (3,879) (2,151) 300Affiliates (30% discount)2 (6,000) (6,000) (326)Minority interests 64 64Enterprise value 12,798 5,678 7,121 5,784

Valuation metrics:FY17A financials:Revenue 35,145 26,770 14,010 16,358EBITDA 2,732 1,100 1,469 894Pre-tax profit 2,734 1,250 1,440 889Net income (assumes 24.2% tax ratefor illustration)3 2,073 948 1,092 674

% net margin 5.9% 3.5% 7.8% 4.1% 4.9%% ROE (based on 2017 net assets) 9.8% 5.7% 24.0% 16.9% 15.8%Forward financials4:Revenue 37,736 29,320 14,466 17,336EBITDA 3,309 1,789 1,520 974Net income 2,660 1,583 1,077 590% net margin 7.0% 5.4% 7.4% 3.4% 5.8%

Implied FY17 P/E 11.9x 16.4x 8.5x 8.6x 14.3xImplied forward P/E 9.3x 9.8x 8.6x 9.8x 12.5xImplied FY17 EV/EBITDA 4.7x 5.2x 4.8x 6.5x 8.0xImplied forward EV/EBITDA 3.9x 3.2x 4.7x 5.9x 6.5x

The resulting valuation significantly undervalues MOBIS’s spun-off business…

12

• Although Mobis’s spun-off businessrepresents 54% of pre-tax income inFY17, the implied valuation of the spun-off business at KRW 9.3 trillion onlyrepresents 37% of the pre-announcement market value of Mobis.The Company has been unabl e toexplai n the stark difference i n theimplied FY17 P/E multi ple of 16.4x forthe rem aining Mobis as compared to8.5x of the spun-off businesses despitethe latter’s higher profitability in FY17

• While Mobis’s spun-off business (with anet margin of 7.8% and ROE of 24.0%in FY17) is m ore profitable than Gl ovis(with a net margin of 4.1% and ROE of16.9% in FY17), the proposed termsvalue M obis’s spun-off business at asimilar FY17 P/E multipl e of 8.5x (or6.2x P/E excluding cash) andEV/EBITDA m ultiple of 4.8x, ascompared to Gl ovis’s 8.6x P/E and 6.5xEV/EBITDA

• Similarly, valuation of Mobis’s spun-offbusiness is also significantly l ower thanauto parts peers’ average of P/E of12.5x and EV/EBITDA 6.5x

Source: Company fillings and IR materials, market dataNotes: 1. Global auto parts peers include Mando, Hanon, Denso, Aisin Seiki, Continental, Valeo, Brembo, Magna, Autoliv and Tenneco.

2. Based on page 5 of the FAQ materials published by Mobis on 18 April 2018.3. Excluding the impact of origination and reversal of temporary differences in tax expenses (KRW497.5 billion), the effective tax rate in 2017 was 24.0%.4. Based on cons ensus estim ates as of 28 M arch 2018 ( pre-announc ement date). Forward intra-segm ent revenue assume to be the sam e % of sales as FY17A. Forwar d net inc ome of Hy undai Mobis’s s pun- off business bas ed on company’s for ecastoperating profit after tax, while the remaining income vs. forward consensus net income is attributed to the remaining business of Hyundai Mobis.

1 23

3

1

2

3

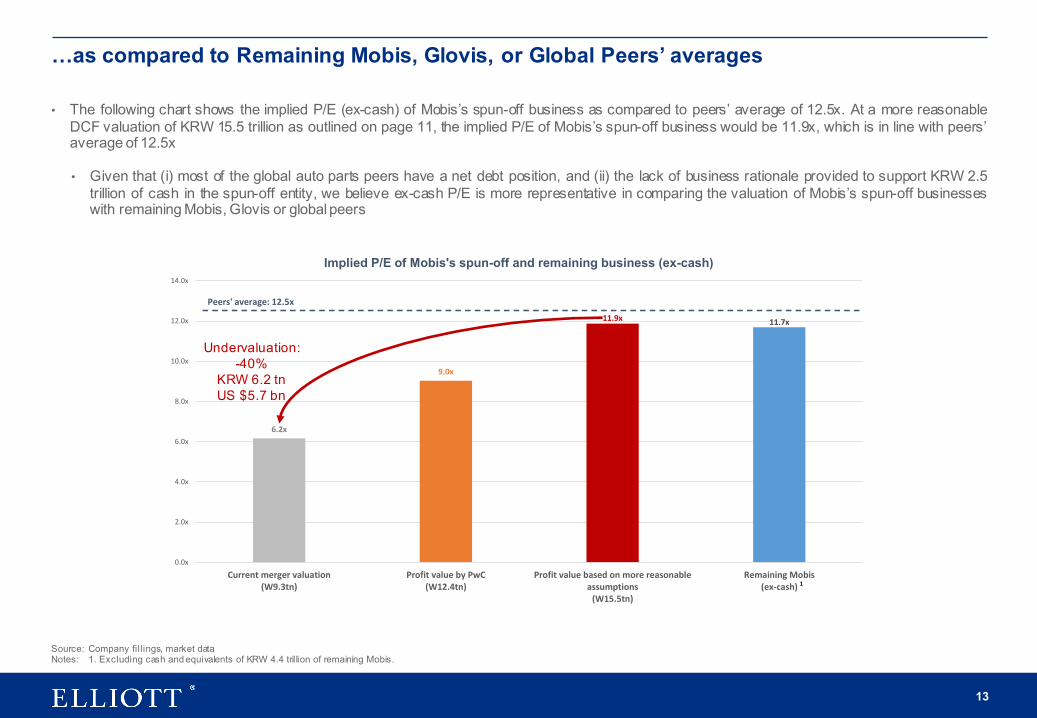

…as compared to Remaining Mobis, Glovis, or Global Peers’ averages

13

Source: Company fillings, market dataNotes: 1. Excluding cash and equivalents of KRW 4.4 trillion of remaining Mobis.

• The following chart shows the implied P/E (ex-cash) of Mobis’s spun-off business as compared to peers’ average of 12.5x. At a more reasonableDCF valuation of KRW 15.5 trillion as outlined on page 11, the implied P/E of Mobis’s spun-off business would be 11.9x, which is in line with peers’average of 12.5x

• Given that (i) most of the global auto parts peers have a net debt position, and (ii) the lack of business rationale provided to support KRW 2.5trillion of cash in the spun-off entity, we believe ex-cash P/E is more representative in comparing the valuation of Mobis’s spun-off businesseswith remaining Mobis, Glovis or global peers

6.2x

9.0x

11.9x 11.7x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

Currentmergervaluation(W9.3tn)

ProfitvaluebyPwC(W12.4tn)

Profitvaluebasedonmorereasonableassumptions(W15.5tn)

RemainingMobis(ex-cash)

Implied P/E of Mobis's spun-off and remaining business (ex-cash)

Peers'average:12.5x

1

Undervaluation:-40%

KRW 6.2 tnUS $5.7 bn

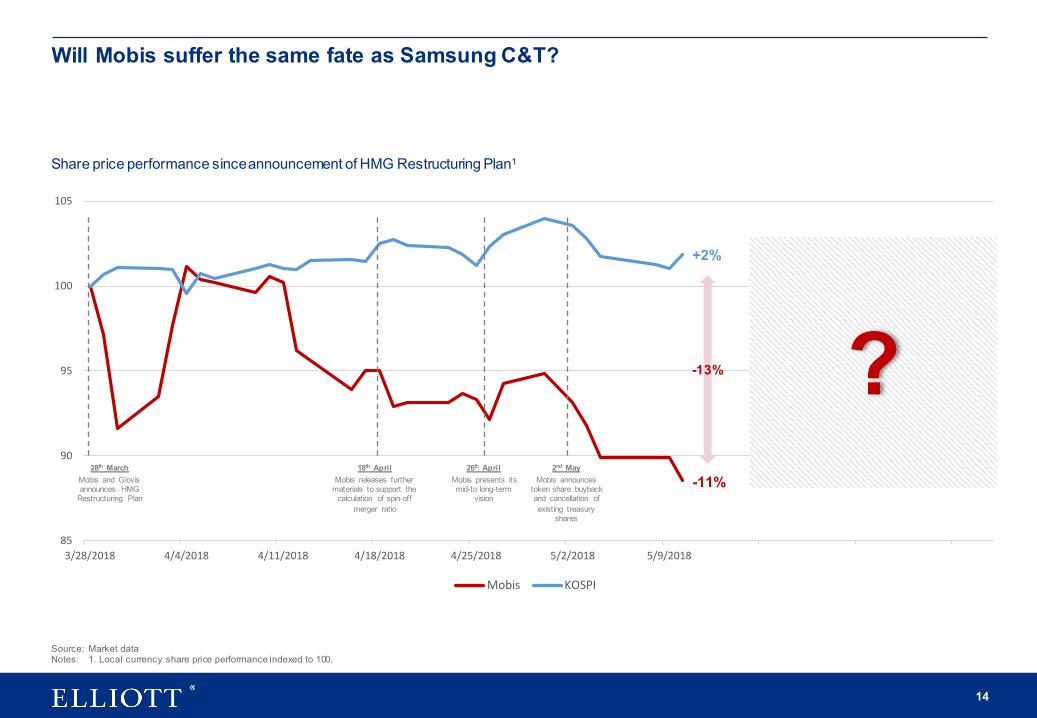

Will Mobis suffer the same fate as Samsung C&T?

14

Source: Market dataNotes: 1. Local currency share price performance indexed to 100.

85

90

95

100

105

3/28/2018 4/4/2018 4/11/2018 4/18/2018 4/25/2018 5/2/2018 5/9/2018 5/16/2018 5/23/2018 5/30/2018

Mobis KOSPI

?+2%

-11%

Share price performance since announcement of HMG Restructuring Plan1

28th MarchMobis and Glovisannounces HMG

Restructuring Plan

18th AprilMobis releases further

materials to support the calculation of spin-off

merger ratio

26th AprilMobis presents its mid-to long-term

vision

2nd MayMobis announces

token share buyback and cancellation of existing treasury

shares

-13%

Conclusion

15

• An inflexible statutory formula does not replace directors’ fiduciary duty to carefully review and assess the proposed terms andconditions of the spin-off and merger, with a view to maximizing the company’s interest and in turn shareholder value

• Elliott emphasizes again that the proposed terms of the spin-off and the merger ratio do not ascribe fair value to Mobis’s modulemanufacturing and after-sales services businesses

• The unfairness of the transaction is only one of the many factors that have weighed negatively on HMG’s share price

• Measures adopted so far by HMG in relation to shareholder buyback and cancellation of existing treasury shares are token and do not gofar enough to address the broader issues of suboptimal balance sheets, declining shareholder returns and corporate governance that isbelow global standards

• HMC’s buyback of KRW 415 billion represents only 7% of KRW 6 trillion of excess cash balance and 1% of its pre-announcement marketcap1

• Mobis’s announced buyback of KRW 187.5 billion over 3 years starting from 2019 or KRW 62.5 billon annually only represents a 2%increase in payout ratio based on consensus net income, and is only 3% of KRW 6 trillion of excess cash and 1% of pre-announcementmarket cap2

• Elliott cannot support the HMG Restructuring Plan on an as-is basis, which fails to treat all shareholders equally

• Elliott calls on the Hyundai Motor Group to revise its proposed transaction to adopt a holding company structure, and to implement a morecomprehensive set of measures that optimize balance sheets, improve shareholder returns policy to be in line with global peers, and reformits board structure and articles to reflect its status as a leading global automotive brand

Source: Company fillings, market dataNotes: 1. Market cap as of 26 April 2018.

2. Market cap as of 1 May 2018.

16