electronic trading report - marketaxess trading report march 2012 ... steve murray editor tom lamont...

TRANSCRIPT

SPXpmSM OPTIONS GIVE YOU MORE OPTIONS. GET ELECTRONIC ACCESS TO THE S&P 500® PLUS P.M. SETTLEMENT AND CASH SETTLEMENT.

Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of Characteristics and Risks of Standardized Options. Copies

are available from your broker, by calling 1-888-OPTIONS, or from The Options Clearing Corporation at www.theocc.com. C2 and SPXpm are service marks of C2 Options Exchange, Incorporated (C2). S&P® and S&P 500® are trademarks of Standard & Poor’s Financial Services, LLC and have been licensed for use by C2. SPXpm is not sponsored, endorsed, sold or promoted by Standard & Poor’s, and Standard & Poor’s makes no representation regarding the advisability of investing in SPXpm. Copyright © 2012 C2 Options Exchange, Incorporated. All rights reserved.

www.CBOE.com/SPXpm

CBOE13c1-Options_InsitutionalInvest-FRAC6-m.indd 1 3/1/12 11:16 AM

Electronic TradingReport

March2012

CorporateAd-FTSE-GMTrading.indd 2 06/03/12 17:44

TABLE OF CONTENTS

©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997. 3

ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

EDITORIAL

Steve MurrayEditor

Tom LamontGeneral Editor

Peter ThompsonExecutive Editor

Robert McGlincheyManaging Editor [London]

(44-20) 7303-1789

Daniel O’LearySenior Reporter &

Hong Kong Bureau Chief(852) 2912-8056

Mike KentzSenior Reporter [New York]

(212) 224-3273

Kevin DuganReporter [New York]

(212) 224-3279

Beth ShahAssociate Reporter

[London](44-20) 7303-1798

PRODUCTION

Dany PeñaDirector

ADVERTISING

Patricia BertucciAssociate Publisher

(212) 224-3890

Adrienne BillsAssociate Publisher

(212) 224-3214

PUBLISHING

Allison AdamsGroup Publisher

Gauri GoyalBusiness Director(212) 224-3504

Anna LeeMarketing Director(212) 224-3175

Laura PagliaroMarketing Manager(212) 224-3896

Vincent YesenoskyHead Of US Fulfillment(212) 224-3057

David SilvaSenior Fulfillment Manager(212) 224-3573

REPRINTS

Dewey PalmieriReprint & Permission Manager [New York] (212) 224-3675

CORPORATE

Jane WilkinsonChief Executive Officer

Steve KurtzChief Operating Officer

Customer ServicePo Box 5016, Brentwood, TN 37024-5016.

Tel: 1-800-715-9195. Fax: 1-615-377-0525

UK: 44 20 7779 8704

Hong Kong: 852 2842 8011

E-Mail: customerservice@ iiintelligence.com

Institutional Investor Hotline(212) 224-3570 and (1-800) 437-9997 or [email protected]

A Publication of Institutional Investor, Inc.

© Copyright 2012. Institutional Investor, Inc. All rights reserved.

Copyright notice. No part of this publication may be copied, photocopied or duplicated in any form or by any means without Institutional Investor’s prior written consent. Copying of this publication is in violation of the Federal Copyright Law (17 USC 101 et seq.). Violators may be subject to criminal penalties as well as liability for substantial monetary damages, including statutory damages up to $100,000 per infringement, costs and attorney’s fees.

The information contained herein is accurate to the best of the publisher’s knowledge; however, the publisher can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

From the editors of:

Derivatives Intelligence

DEAR READER,

Electronic trading and its growth potential are nothing new. But there is the real sense in the derivatives market that we’re reaching a tipping point after which the traditional bespoke, phone-based service will become rarer and rarer. Advances in trading technology and basic speed, the downward pressure on fees and the inexorable drive by regulators to make derivatives trading more open and centralized are all driving the phenomenon.

With that in mind, the Derivatives Week/Derivatives Intelligence’s special supplement you have in your hands on electronic trading is aimed at delving deeper into all the key facets of the movement. Our Hong Kong, London and New York reporting team has taken the pulse from top traders on issues such as high-frequency trading, scoped the sellsides’ push on platforms and bottom lined regulatory developments in the U.S. under the Dodd-Frank Act and in Europe via its directives. We’ve also included detailed Q&A’s with key industry players.

We hope you value and enjoy the supplement.

If you have any feedback, don’t hesitate to drop me a line.

Robert McGlinchey, Managing [email protected]

FIX Implementation Takes Center StageRob McGlinchey, DI

The Financial Information eXchange Protocol is set to play a key role in fixed income trading. The industry is just trying figure out how exactly.

Lack Of Clarity On Pre-Trade Transparency VexesMike Kentz, DI

A number of thorny U.S. regulatory issues are outstanding with regards to swap execution facilities. Some see the market as being held back as a result.

Asia Embraces Electronic InnovationDan O’Leary, DI

Sellsiders and investors have been driving rapid Asia market penetration. Costs are falling for users as a result and firms are looking for twists to stay ahead of the competition.

U.S. Firms Bulk Up, Focus On NichesKevin Dugan, DI

The U.S. appears poised for a spurt of platforms. There has been a somewhat targeted approach so far, but that may be about to change.

Potting The Path To Real Time TCARob McGlinchey, DI

Transaction cost analysis is seen as ripe for a move into real time. That’s going to cut trading costs and alter strategies.

Platforms Expand As Regs Draw NearerBeth Shah, DI

Some players have been taking the plunge and forming multi-dealer platforms ahead of regulations being set. There are still challenges for them.

Futures On The RiseMatt Simon, TABB Group

The futures market is recording swelling volumes. Electronic trading is among the factors behind the prediction it is going to eat even more into OTC.

Q&A: WMBAA’s Chris Ferreri

84

10 14

17

23

15

21

Q&A: FIA EPTA’s Remco Lenterman31CFTC Rules On Swap Entity Registration

David Felsenthal, partner, Gareth Old, partner, David Yeres, counsel, and Inna Zaychik, associate at Clifford Chance in New York map out the shape of current CFTC rulemaking.

26

4 ©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997.

MARCH 2012 | www.DeRivAtivesintelligenCe.CoM ELECTRONIC TRADING REPORT ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

(Continued on page 6)

The request-for-quote system of trading an over-the-counter derivative allows end users to customize a trade

and find out which dealer will give the best price without any other entities knowing their identity or desired trade. Most market participants consider the system vital to the health of the OTC market. Dodd-Frank’s call for pre-trade transparency and the coming creation and use of swap execution facilities is running the risk of dismantling that system.

The CFTC and the SEC have been tasked with defining swap

execution facility and how it will function. They differ widely

when it comes to the format for RFQs.

The CFTC has published a proposal which says end users

placing an RFQ will have to post each request to five different

dealers every time. The SEC has proposed RFQs will only be

required to be posted to one dealer at a time. The CFTC’s

rules will apply to index-based credit default swaps and

interest rate swaps while the SEC’s rules will apply to single-

name CDS.

Another layer to this regulatory disparity is the pace and

form with which each Commission is attacking the rules. The

CFTC has finalized over 25 rules to the SEC’s two to this point,

according to their website, with market participants largely

split between supporting the ‘Slow and steady’

SEC and the ‘Let’s get going’ CFTC.

“The Commission and staff are working hard

to adopt effective rules as quickly as possible,

with an emphasis on getting the rules right,”

said an SEC spokesman.

“The CFTC’s on a quicker track and on the

whole we think that’s a good thing,” said Jim Rucker, chief credit and risk officer at MarketAxess in New York, a planned SEF for both index and single name CDS. “There’s considerable uncertainty, [and that] makes it difficult to make business decisions to introduce the changes that we eventually will need to.”

Regardless of the time frame, large institutions like BlackRock and MetLife are crying foul, saying that the CFTC five-dealer requirement will lead to banks front-running their trades. “SEFs should be allowed to structure their RFQ platforms on whatever basis the SEF believes will serve its clients’ interests, whether one-to-one or one–to-five,” wrote Joanne Medero and Richard Prager of BlackRock in a comment letter back in June.

“The requirement that participants solicit bids and offers from at least five swap dealers would not only fail to meaningfully increase price discovery, but would likely diminish it, particularly in markets with a limited number of market makers,” wrote Todd Lurie of MetLife.

But it wouldn’t be a debate without a flip side. Dodd-Frank wasn’t written to protect the incumbency of big banks and large institutions. It was written to safeguard the market and increase competition, meaning smaller players get to see the same prices bigger players do (via a SEF).

“[A] system that permits request for quotes from only one market participant would facilitate abusive trading practices such as prearranged trading and ‘painting the screen,’” wrote James Cawley, co-founder of the Swaps and Derivatives Markets Association and head of planned SEF Javelin Capital Markets, in a comment letter. Painting the screen means posting inaccurate prices for personal gain.

With this type of pressure coming from all angles, it’s no wonder the regulators appear to be buckling under the pressure. In late February, the CFTC delayed a final vote on the definition of the term ‘swap dealer’ because the SEC wasn’t ready, according to reports. One market participant said he has had separate conversations with high-ranking officials at both Commissions where the officials blamed their counterparts for the slow pace of rule implementation.

When the regulators do get to a final vote on SEFs, which will

Jim Rucker

Lack Of Clarity On Pre-Trade Transparency Vexes

Differences in opinion between the Securities and Exchange Commission and the Commodity Futures Trading Commission regarding the nature of swap execution facilities are slowing the

pace of regulations and drawing the ire of market participants. Mike Kentz explains.

SponSored Article

Expanding Your Global Trading Reach

Jeff Ferro

Emerging and frontier markets offer compelling opportunities, but local presence

remains key to efficient trade execution.

An interview with HSBC Securities’ Jeff Ferro, Vice President, Customized Execution Services. Americas.

Q: What are the growth prospects for emerging and frontier market trading? Given the remarkable economic development in emerging and frontier markets, it is little surprise that these countries have continued to play a steadily expanding role in U.S. portfolios. Since 2001, domestic exposure in U.S. investor equity holdings has declined from 90% to 79%. During the same period, exposure to developed foreign markets has nearly doubled from 9% to 17%, and exposure to emerging and frontier markets has grown from less than 1% to just under 5%. However, even after this historic increase, the level of U.S. investor emerging and frontier market equity exposure still remains well below the MSCI All Country World Index’s 14% benchmark weight. We think this suggests incredible growth prospects in the years ahead as allocations to these countries continue to rise.

Q: What is the breadth of your global access? Our sophisticated network offers Programtrading execution in 77 countries across6 continents, Direct Market Access in43 different countries and a full suite ofglobal Algorithms that automates specific strategies for quality execution and consistency of intended results across 36 of those countries.

Q: How does HSBC help traders access these markets? As U.S. buy-side traders have become more interested and skilled with global developed and emerging markets, they have understandably wanted to take greater control of their trades in these regions. HSBC has responded by offering its trading system to support these clients with the same industry-leading technology and worldwide infrastructure used by our in-house trading desks and investment professionals. Clients also gain access to the extensive insights and consultation of our Customized Execution Services team to help navigate these markets without having to change trading style, with 24-hour support from professionals across the Americas, Europe, the Middle East and Asia.

Q: How important is strong local presence in efficient trade execution? We think it is critical and have structured our platform with major trading hubs in Hong Kong, London, New York and Dubai, each with an extensive network of corresponding on-the-ground spokes into the surrounding regions. There are three primary risks to consider in terms of execution efficiency. The first is information leakage. HSBC is one of the largest owners of local exchange memberships, which substantially reduces reliance on subcontracting trade execution, particularly compared to systems with less direct global scope. We are also one of the largest sub-custodians in terms of presence

across various international markets. Both factors provide a distinct competitive advantage in helping to maintain trading anonymity.

The second risk involves market microstructure. Exchange access rules and local execution nuances can vary greatly in each market, and it is crucial to understand if an order might interact in a way that could risk execution quality. That is why our team continuously monitors each client trade to offer an additional checkpoint as orders are executed. When it comes to emerging and frontier market trading, it isn’t just about access; it’s about providing intelligent access that applies our expertise in local country knowledge to help our clients secure the most efficient trade execution possible. The third risk entails trade consistency across countries. The true power in HSBC’s trading system is that it centralizes our expansive regional insights across developed and emerging economies into a single platform that quite literally puts the world at our clients’ fingertips. This empowers them to concentrate on strategy and performance, while we focus on quality of execution, settlement and reporting, including trade transparency, counterparty controls, best execution checks, market anomaly detection, and pre- and post-trade analytics, all backed by the significant capitalization and stability of one of the most trusted names in global banking.

Contact information:

CES Americas: Leon McIntyre, Head of CES Americas (212) 525 3334

Jeff Ferro, Algorithmic and DMA Sales (212) 525 2430

Email: [email protected]

CES Asia: Gerry Pablo, Head of CES Asia 852-2822-3821

Email: [email protected]

CES EMEA: Simon Cornwell, Head of CES EMEA 4420 7991 5616

Email: [email protected]

Global Toll Free: 855 HSBC-24-7 (855 472 2247)

6 ©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997.

MARCH 2012 | www.DeRivAtivesintelligenCe.CoM ELECTRONIC TRADING REPORT ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

(Continued from page 4)

n Dodd-Frank says that all trades “made available for trading” need to be listed on SEFs. The definition of that term has sparked debate.

n Most SEFs and inter-dealer brokers believe that if a trade is clearable then it is ultimately tradable. Dodd-Frank lays out a five-factor test for clearable trades. If a trade passes that test, SEFs should be able to list it, they say.

n “If you get the rules right on the clearing mandate, then the trading mandate should just follow. SEFs will only work if the clearing mandate doesn’t get spread too broadly. [We believe that] the mandate [for available for trading] in Dodd-Frank was not meant to be an entire other definition.”– Jim Rucker, chief credit and risk officer, MarketAxess.

n The International Swaps and Derivatives Association, representing the dealers, believes the regulators should lay out a separate test for the term. Their fear is that SEFs will list illiquid

swaps if they are given carte blanche, so to speak, and damage liquidity in those markets as a result.

n “SEFs…have an economic incentive to designate as many swaps as “available to trade” as possible, and to do so as soon as possible in order to acquire market share in trading those swaps. Accordingly, there is an inherent conflict of interest between the profit incentive of SEFs/DCMs to have as many swaps as possible required to be traded on their platforms and whether there is actual benefit to the market of requiring a swap to be traded on a SEF/DCM.” – Robert Pickel, ceo at ISDA, in conjunction with two other industry trade groups.

n The CFTC followed dealer concerns and proposed an eight-factor test.

i. Whether there are ready and willing buyers and sellers;

ii. The frequency or size of transaction on SEFs,

DCMs or bilateral transactions;

iii. The trading volume on SEFs, DCMs or of bilateral transactions;

iv. The number and types of market participants;

v. The bid/ask spread;

vi. The usual number of resting firm or indicative bids and offers; or

vii. Whether a SEF’s trading system or platform or a DCM’s trading facility will support trading in the swap;

n A compromise exists. “In our opinion, there should be a one-year transition period where SEFs provide execution on products that are already traded on electronic platforms. Then we can use the previous twelve months to create a data set to figure out if any swaps should be added or subtracted from the ‘available for trading’ definition.” - Jon Williams, head of U.S. markets at Tradeweb.

‘Available For Trading’ Calls Out For Clarity Too

be in April at the earliest, the question with respect to RFQs is what rule will both protect a customer trading illiquid swaps while also guaranteeing pre-trade price transparency and increased competition.

Javelin, for one, plans to offer anonymous RFQ and anonymous request-for-market options. Anonymous RFQ means the customer puts in a request for pricing on a customized trade but does not include its name. Anonymous request-for-market means the customer withholds both name and the direction of the trade. That means the customer asks for both sides of a particular trade, including the size, but without the name. That way, conceptually, there will be no clear opportunity for front-running and less risk of ‘painting the screen.’

Rucker at MarketAxess said his firm was “working on facilitating things to make that happen, but we’re not

ready,” adding that the firm would wait for more regulatory clarity. Tradeweb, a provider of multi-dealer credit default swap and interest rate swap execution and another planned SEF, “is not currently planning” to offer ARFQ or ARFM. The reason, they said, is that their clients have not asked for that functionality and they would wait until it became a regulatory requirement before taking such steps.

TeraExchange, which is planning to execute all CDS and

IRS, is “bypassing [the] RFQ model and rolling out a fully anonymous central limit order book” for non-block trades, said Christian Martin, ceo at the firm in Summit, N.J. Bloomberg’s AllQ platform for index-based CDS and IRS will “adapt the platform to the SEF protocols once they have been finalized.” Ben MacDonald, global head of fixed income

trading, products, and services at Bloomberg in

New York, added the firm views the five-dealer

requirement as “problematic.”

As for the SEC, whose low public profile

to this point has unnerved some market

participants, the market will wait to see if their ‘one-to-one’

SEF trading requirement changes either. Officials familiar

with the regulatory discussions said the SEC is satisfied with

its approach and that the one-to-one requirement doesn’t preclude or require the use of ARFQ or ARFM, though a spokesman declined comment.

Lost in the shuffle of all this lobbying is the concept that many OTC market participants may begin to exit the stage left to populate the futures market no matter what. SEFs, regardless of a buyer’s ability to cloak its name and trade direction in an RFQ, may struggle with the ability to confirm trades in real-time considering each customer will have the choice as to which clearinghouse they use. That concept of vertical integration is something the futures market can still boast. n

Ben MacDonald

Christian Martin

C

M

Y

CM

MY

CY

CMY

K

CDSToolbox_II_2Q12.pdf 1 3/6/2012 9:52:35 AM

8 ©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997.

MARCH 2012 | www.DeRivAtivesintelligenCe.CoM ELECTRONIC TRADING REPORT ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

The emergence of new trading venues, such as swap execution facilities and organized trading facilities,

on the back of the U.S. Dodd-Frank Wall Street Reform and Consumer Protection Act and the proposed update to the E.U. Markets in Financial Instruments Directive, have reinforced the need to promote the increased use of Financial Information eXchange Protocol, the global language used by firms to facilitate electronic trading. Already the standard language in markets such as the equity markets, the need to promote FIX for credit default swaps and interest rate swaps has grown in importance as such instruments are increasingly becoming fast tracked to electronic trading.

“SEFs are going to be a new concept as part of Dodd-Frank. Today, you have existing platforms and some support CDS and IRS,” said Lisa Taikitsadaporn, chair of the FPL Global Fixed Income Technical Subcommittee and managing partner at Brook Path Partners. “The challenges the banks are facing with these platforms is that the interfaces to these platforms are in proprietary formats. So with this initiative, the banks are encouraging the SEFs to move away from only offering proprietary formats, they are saying that they want to use FIX.”

“It’s very important we start to look at different paradigms and it has been clear that we needed to aim at a world of hyper connectivity where if you really want to communicate, that it’s not only about the broker and trader on the phone, but it is going to be increasingly about electronic systems that can talk to each other,” said Francesco Cicero, head of eTrading at GFI Group. “To talk to each other they need to talk the same language. So it goes without saying that any initiative facilitating that transition was welcomed by us.”

Some of the trading venues already operating offer FIX connectivity for IRS and CDS, however more venues are expected to emerge after MiFID II and Dodd Frank implementation. Other venues typically offer so-called proprietary application programming interfaces for sellside firms to connect to. The interfaces can typically be time

consuming to support and lead to increased costs for the sellside.

Yann L’Huillier, cio at Tradition, which already offers FIX, noted that developing proprietary protocols are a step in the wrong direction. “If everyone came up with a proprietary protocol, then it isn’t standard at all,” he said. “Today, what you have, if

you look at the financial markets as a whole, is the FIX Protocol everywhere. If you look at equity, for example, FIX is the standard. Why would we invent a different set of connectivity when people are trying to reduce the costs and issues with connectivity with FIX Protocol?”

According to market participants, by adopting FIX, new and existing venues will reduce costs for the market by minimising the costs of market entry and reducing switching costs. With the completion of the project, firms will also be

FIX Implementation Takes Center Stage

Last June, 12 investment banks, supported by FIX Protocol, came together to launch the Fixed Income Connectivity Working Group to promote the increased use of FIX

when trading fixed income products. Rob McGlinchey looks at how the project has been developing and what efforts trading venues are making to implement FIX.

FICWG ExTEnDS To CASH BonDS

The Fixed Income Connectivity Working Group is to promote standardized protocols for the electronic trading of cash bonds in 2012.

The scope of the initiative includes standardization of protocols for pricing and trading government bonds, such as U.S. Treasuries, eurozone government bonds and gilts, as well as sovereigns, corporates, high yield and emerging markets.

“This initiative will increase transparency and efficiency in fixed income OTC markets by promoting greater technical standardization and openness across the industry,” said neil Chinai, head of global rates and emerging markets technology at Barclays Capital. “Among

market participants, the initiative will provide a more cost efficient and

faster integration process, which is a key requirement in today’s rapidly

changing environment.”

Francesco Cicero

Yann L’Huillier

MARCH 2012 | www.DeRivAtivesintelligenCe.CoM ELECTRONIC TRADING REPORT

©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997. 9

ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

able to speed up their integration with SEFs and OTFs.

The FPL Global Fixed Income Technical Subcommittee, which is part of the Global Fixed Income Committee, has established best practices documents for applying FIX in CDS and IRS. “We took the base FIX standard out there and we took a look at how it can be applied to the work flows and the nuances of trading CDS and IRS, and then established the recommended ways of using the FIX messages across these products between the venues and the banks,” added Taikitsadaporn.

Trading venues are now looking at implementing FIX across CDS and IRS. Market participants note that the implementation process will take time as both the trading venue and the end client would need to introduce changes. These could also entail thorough testing and possibly operational upgrades.

GFI, for example, is working on adapting its APIs to make them compliant with best practices and then release them to clients. “It will take some time to implement all of the recommendations, but with the extra push generated by

Dodd-Frank and MiFID in Europe, at this point in time is when a lot of banks are deciding how to connect and who to connect to, so it’s all coming to fruition now,” said Cicero. “It will keep evolving as we introduce more products and sub-asset classes, but it is definitely going in the right direction.”

BGC Partners is another firm working on implementing FIX in CDS and IRS, and already offers FIX in U.S. Treasuries. The next focus, however, for the firm is working with the industry to apply FIX to fx options.

“BGC has been a strong proponent for the inclusion of fx options into the work streams for CDS and IRS being managed concurrently by the FIX Working Groups. FIX is a standard already widely in place for fx, so fx options require only slight tweaking to add the required FIX fields and to deploy them dynamically, such as trading vols instead of a price and adding deposit rates to the legs,” said Borys Harmaty, head of integration services at BGC Partners in New York. “FIX is now used much less in CDS and IRS and therefore it is much more of a community effort to agree on best practices which is well underway for the benefit of all.” n

Market participants took issue with

some of the proposed rules from the

European Commission in the updated

Markets in Financial Instruments

Directive, particularly around pre trade

transparency, at the FIX Protocol EMEA

Trading Conference in London on March

13. They said some of the proposed rules

could be detrimental to the way the

market operates.

Denzil Jenkins, head of compliance

and regulation at the London Stock

Exchange, said on the regulation panel

that the proposed requirement to inform

the European Securities and Markets

Authority in advance to utilize a waiver

was of particular concern. “When you look

at the requirement of pre-trade waivers,

it is a requirement that the use of pre-

trade transparency waivers will potentially

have to go through a process of where if

anyone in the industry wants to utilize

one of those waivers, they are going to

have to inform ESMA at least six months in

advance,” he said. “That is not going to be

beneficial to innovation.”

“One of the surprises around the draft

was that they took so long and they got

so much of it wrong,” noted Stephen

McGoldrick, co-chair of the FPL EMEA

Regulatory subcommittee and director in

market structure at Deutsche Bank. “There

is lots of good stuff, but there are some

things that display a fundamental lack of

understanding over how the market works.”

McGoldrick highlighted one example

where he took a senior policy officer

around Deutsche Bank’s trading floors to

show the differences between the equity

and fixed income markets. The realization,

from the policy officer, was that regulation

for pre-trade transparency that works in

an equity market cannot be presumed to

work in fixed income.

Separately, panelists noted they were

increasing becoming worried over the

ability of ESMA to establish policy and

technical standards for regulation due to

budgetary constraints and a lack of staff

and expertise. Concerns have increased

given the amount of projects the pan-

European regulator is dealing with to meet

G20 deadlines.

“I fear that ESMA whilst I agree there

is a lot to be applied…has not got the

staff and the resources or the insight

to legislate some of the things that

are being delegated to it. Some of the

things that have been passed to ESMA

are so fundamental that they relate to

policy, they don’t relate to technical

implementation,” said McGoldrick. “I

think the industry increasingly stands

ready to help the regulator adopt or

develop standards to implement agreed

direction. But a lot of what is coming

down to ESMA is not agreed direction; it’s

about collaboration of things such as pre-

trade transparency waivers and the rules

surrounding those. How those ESMA rules

fall out will actually define the policy.”

InDuSTRY STRIkES ouT AT uPDATED MIFID PRE-TRADE RuLES

10 ©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997.

MARCH 2012 | www.DeRivAtivesintelligenCe.CoM ELECTRONIC TRADING REPORT ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

Asia Embraces Electronic Innovation

S ingle-dealer electronic trading platforms have become

the new world order. They are tools that aim to

reduce costs and increase efficiency for clients. Platforms

offering derivatives trading have been operating in Asia

for around nine years, with Barclays Capital’s BARX,

the Royal Bank of Scotland’s Marketplace and uBS’

Equity Investor amongst the platforms currently offered

locally. During the last year, firms have been aggressively

expanding their e-trading teams and product offerings on

these platforms.

At the same time, Asian investors have been increasingly

flocking to platforms and dealers are increasingly

recognizing the growing potential and suitability for such

platforms in the region. What makes Asia so prime for the

development of electronic trading platforms is that they

give greater diversity to an investor base already at home

with a fragmented market. Jump in an airplane and fly an hour in any direction from Singapore and you can find

yourself in a completely different world with different

products and systems of law and governance.

“The fact that a client now is able to have access to

various markets and various exchanges and facilitate

both inbound and outbound business, in addition

to their domestic market, makes it even more

compelling,” says Leanna Raja, head of South Asia

sales for Barclays Capital’s BARX platform in Singapore.

“Yes, [fragmentation] is an obstacle, but it’s also an

opportunity,” she said. Some emerging markets in Asia

present a challenge, due to the lack of technological

infrastructure, “Such as a lack of Internet connectivity,”

she noted. “Yes, it does make it more difficult to get

the client base to trade electronically within their own

country. But once you overcome the connectivity issues,

we’ve seen rapid uptake from clients who have a desire to

leverage the benefits electronic trading offers them.”

According to Raja, the uptake in electronic trading has

been most pronounced in fx, while fixed-income and

commodity derivatives are also rising in popularity in the

region. “There’s definitely more and more recognition

in Asia as to what electronic trading platforms actually

bring to clients,” she said. “The drive has been from private banks and hedge funds, but we’re also seeing the client base open up to the possibilities to the benefit of electronic trading. They’re the real money and increasingly corporate accounts.”

Credit Suisse and Barclays are examples of two firms that have been expanding in the region to meet the growing

demand for electronic trading from clients while also

broadening the potential client base.

Credit Suisse launched its Asia-focused electronic trading

platform Spirit Asia in April 2010. The click-and-trade

platform was initially only available to Credit Suisse’s

internal private bank, but has since been rolled out to

over 800 private bank subscribers. Min Park and kenneth Pang championed the development of the e-trade

platform when they came over from UBS in 2009 as

co-heads of equity derivatives and convertibles for Asia.

While Spirit Asia is modeled after Credit Suisse’s European

equivalent, Spirit, the system is slightly different and uses

its own structures and IT. The platform’s product suite

covers equity-linked structured notes, such as vanilla

and variable options, plain vanilla and knockout ELNs,

Electronic trading in derivatives and structured products in Asia is well established and the region is increasingly becoming a major driver of growth.

Daniel O’Leary reports.

“By doing this, we automate so much that the issuing cost is quite minimal. Our system has one of the lowest launch

sizes on the street.”

— Min Park

MARCH 2012 | www.DeRivAtivesintelligenCe.CoM ELECTRONIC TRADING REPORT

©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997. 11

ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

accumulators and range and fixed-coupon notes.

“With this system, it basically means everything can be

much quicker. Everything will be much more efficient,”

said Patricia Lau, head of private bank sales, Hong Kong

and Singapore at Credit Suisse. “Previously, the way that

private banks get quotes is the client will call the private

banker and the private banker

will have to call their products

desk at the private bank and

then the private bank’s product

desk will have to call us. And

then we have to get back to

the private bank’s structured

products desk, which then has to

get back to the client. Normally

it goes back and forth a few

times, depending on the client’s

needs.”

The turnaround time for the

platform’s development was

swift after Park and Pang arrived, according to Lau. “We

wanted to bring in an electronic platform to improve

the experience of our private bank clients,” she said. Lau

noted electronic trading platforms empower the private

banker. “They’re able to get their own pricing quotations,

they’re able to place orders by themselves,” she noted.

“While the private banker speaks to the client over the

phone, they’re able to get different pricings and price

variations as they speak to the clients.”

Credit Suisse is planning to broaden the product suit it

makes available to investors as the market landscape

changes, with structured products such as callable

variable reverse convertibles and drifter notes expected

to be added to the platform this year. “We’ll also be

adding more underlyings and more features,” said Lau.

“These products don’t have as much volume as our other

products, but it’s important that we have a very broad

product suite. We need to cover as much as possible on

the platform, even if client demand is in small tickets. We

want to cover that.”

Barclays, like Credit Suisse, has also been developing the

capabilities of its platform. One development has been

the addition of pricing and execution capabilities for fx

and commodities to its Comet equity structured product

platform, which sits within BARX Investor Solutions.

The broadening of the client base is being driven by the

development of the platform, said Raja. “What we are

offering currently in regards to Asia is more and more

complete,” Raja noted. “In the Singapore market, for

instance, not only can clients trade [U.S. dollar/Singapore

dollar] spot, forwards and futures over the Singapore Exchange, but they can also have access to exceptional

liquidity in Singapore bonds, Singapore interest rate

swaps and Singapore credit. So the completed product is

encouraging more uptake.”

Barclays is also looking to expand its emerging markets

electronic offering after launching CNH spot, forwards

and options on the BARX platform in 2011. “I think with

fx options, we’ll continue to develop our suite of products

and functionality,” said James Cowell, head of efx trading

at Barclays Capital. “A lot of development over the last

12 months has been around Asian currency options and

emerging market options and a lot of that is driven by

Asian demand.”

If you take into consideration the challenges currently

facing market participants—higher costs from impending

regulation and increased capital requirements—the

increase in electronic platform expansions makes

economic sense. “Also, this front end automation, isn’t

just efficient execution,” Park said. “It can also generate

documents automatically and automate back office

bookings.”

The automated process means Credit Suisse is able to

handle much smaller order sizes than before. “And then

our end doesn’t have to wait to get certain minimum sizes

to launch the product. Now we can lower the minimum

price to as low as USD25,000.”

The system also lowers issuing costs. “If we don’t have the

proper size we cannot cover the cost,” Park noted. “By

doing this, we automate so much that the issuing cost is

quite minimal. Our system has one of the lowest launch

sizes on the street.”

Lau said investors have been increasingly turning to lower

order sizes as a consequence of the financial crisis. “But

they also don’t want to put all their eggs in one basket

and they want to diversify,” she added. “Without this kind

of platform, doing trades like this would never be possible

from either the investment banking side or the private

banking side. It doesn’t really make much sense for either

side of the trade to handle such small orders.” n

“We need to cover as much as possible on the platform, even if client demand is small. We want to cover that.”

— Patricia Lau

SponSored Article

The Golden Age of Cross-Asset Strategies

By Gary Stone

Relative value arbitrage (RV) exploits

the difference between two or

more securities in the same or

different markets. Investors will sell

an overvalued security (securities)

and use the proceeds to buy a

security (securities) that is perceived

as undervalued or offering better

value. The strategy is attractive in

these market conditions because it

reduces directional beta. According

to data from Hedge Fund Research,

relative value hedge fund strategies

had strong net capital inflows of

$35.8 billion in 2011. Additionally, RV

was the only hedge fund strategy

to generate positive performance,

gaining 0.51% for the year.

In two short years, the complexion

of the global markets has changed

dramatically. Globally, regulators

have approved electronic market

Since the 2008 bottom, most markets have predominantly traded in a range. A glance at the

weekly charts shows that the U.S. S&P 500 index has crossed 1,200 around 13 times, similarly

the MSCI World Index has crossed 1,200 around 10 times and the NYMEX

perpetual front contract crossed $95 approximately 19 times. With

market direction uncertain and volatility being driven by unpredictable

geopolitical shocks and other exogenous events, many investors are

finding that relative value and hedged multi-legged strategies may

deliver more alpha per unit of risk.

structures across different asset classes. In some cases, regulators have gone beyond

establishing electronic central limit order books at primary exchanges—approving

fragmented market structures where liquidity is spread across several venues that

compete with one another. The implication for RV is that electronic markets: (1)

Gary Stone

Figure 1

make possible direct access to global

multi-asset class liquidity and (2) enable

algorithms to implement complex

multi-legged strategies that

were impossible to efficiently

execute manually. In the past,

while a market maker might have

conceivably provided a price for

an N-Leg strategy, the spread

reflected the complexity of the

trade and transaction costs made

the strategy impractical.

Now, with platforms such

as Bloomberg Tradebook,

technology can connect widely

scattered markets and asset

classes; algorithms can then

manage the wide variety of multi-asset

exchange and security-specific rules, the

liquidity aggregation across lit and dark

pools, control slippage and maximize

liquidity capture while simultaneously

executing multiple securities efficiently.

Once impractical complex strategies are

now becoming viable.

The Bloomberg Professional service

and Bloomberg Tradebook together

create a logical workflow. Bloomberg

Professional advanced search and

analytic functions all help identify

investment opportunities. With

functions such as the Custom Index

Expression (CIX<GO>), investors can

create a synthetic security representing

the complex strategy. The index can be

integrated into Bloomberg’s charting

packages (G<GO>) and can utilize

advanced technical studies such as

Capital Market Research’s ATM studies

to gain a technical perspective on

the strategy (Figure 1). A Bloomberg

Tradebook pairs ticket (Figure 2) can be

launched from CIX to seamlessly move

from idea generation to execution.

Tradebook algorithms enable traders

to implement single-market and cross-

border equity pairs, option spreads,

fixed-income future curve trades,

option/equity volatility and delta

strategies, etc. Additionally, multi-leg

strategies such as commodity crush

and crack spreads, butterflies and

option/equity 90/110% risk reversals

can be modeled on the Bloomberg

Professional service and implemented

on Bloomberg Tradebook. These

algorithms can be integrated into third-

party order management and execution

management systems.

Relative value arbitrage is a strategy

that is gaining momentum. Today’s

environment combined with advances

in technology make it possible to

implement more complex strategies.

If you want to stay competitive, you

have to automate. This is especially true

when dealing with highly fragmented

markets, cross-border strategies and

across asset classes. Traders need to

have all of the information from the

strategy on the same ticket so it can be

delivered to an algorithm that efficiently

manages execution. With Bloomberg

Tradebook pairs platform, now you

have all required information in one

place. Tradebook’s algorithms can

reduce scrambling to find thin liquidity

to complete a final leg, the fretting of

losing alpha due to slippage or having

to pass on profitable opportunities

because you don’t have the bandwidth

(or systems) needed to take them.

Final result: New opportunities,

improved productivity, less hassle, less

leg risk, more alpha.

SponSored Article

Figure 2

Nothing in this document constitutes an offer or a solicitation of an offer to buy or sell a security or financial instrument or investment advice or recommendation of a security or financial instrument. Bloomberg Tradebook believes the information herein was obtained from reliable sources but does not guarantee its accuracy.

This communication is directed only to market professionals who are eligible to be customers of the relevant Bloomberg Tradebook entity. Communicated, as applicable, by Bloomberg Tradebook LLC; Bloomberg Tradebook Europe Limited, authorized and regulated by the U.K. Financial Services Authority; Bloomberg Tradebook (Bermuda) Ltd.; Bloomberg Tradebook Services LLC. Please visit http://www.bloombergtradebook.com/pdfs/disclaimer.pdf for more information and a list of Tradebook affiliates involved with Bloomberg Tradebook products in applicable jurisdictions. The BLOOMBERG PROFESSIONAL service (“BPS”) is owned and distributed by Bloomberg Finance L.P. (“BFLP”), except that Bloomberg L.P. and its subsidiaries distribute the BPS in Argentina, Bermuda, China, Japan, Korea and India. Bloomberg Tradebook is provided by Bloomberg Tradebook LLC and its affiliates and is available on the BPS. BLOOMBERG, BLOOMBERG PROFESSIONAL and BLOOMBERG TRADEBOOK are trademarks and service marks of BFLP or its subsidiaries.

14 ©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997.

MARCH 2012 | www.DeRivAtivesintelligenCe.CoM ELECTRONIC TRADING REPORT ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

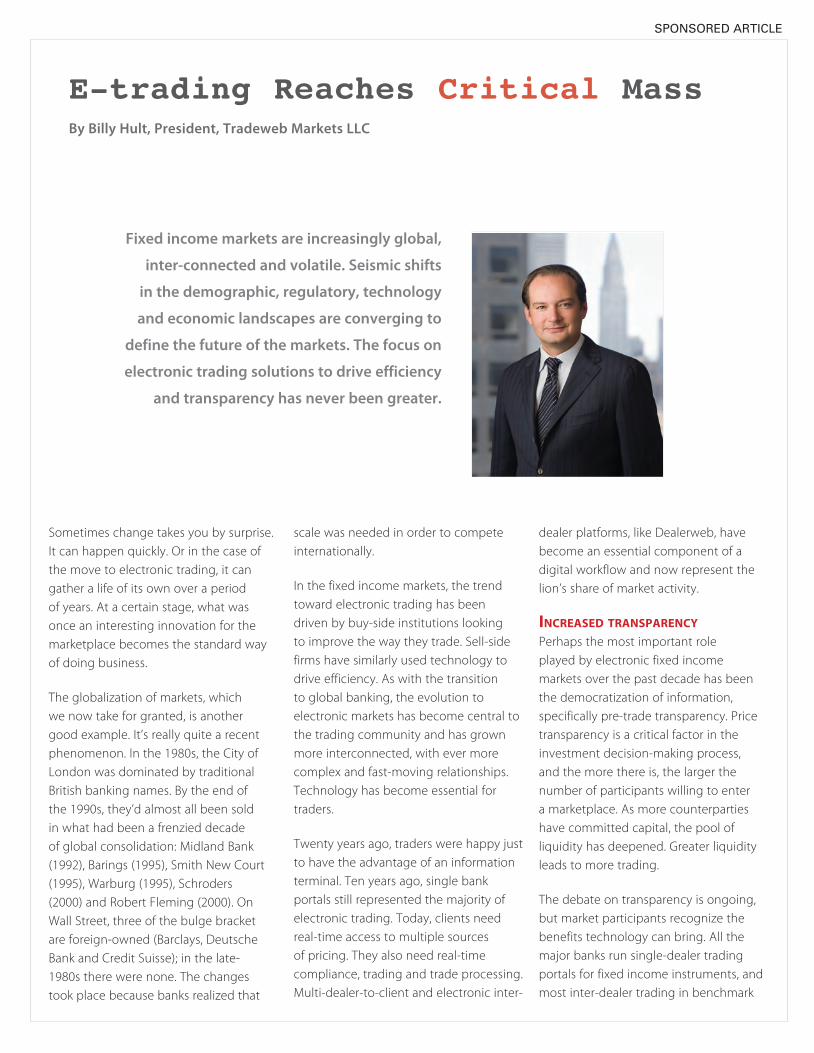

S ince the summer of 2010 when the Dodd-Frank Wall Street Reform and Consumer Protection Act was passed,

the market has seen significant developments in the way derivatives are traded, fuelled by a demand for more automation from industry participants.

The U.S. legislation mandates that all cleared swaps must trade on an exchange or a swap execution facility. Many multi-dealer electronic trading providers intend to register as SEFs when the regulation is implemented. In Europe, the E.U. has proposed the introduction of organised trading facilities, which are similar to SEFs. OTFs are defined as platforms operated by a market participant which is not a multilateral trading facility, where multiple third-party buying and selling interests in financial instruments are interacted that result in a contract. An OTF would include a broker crossing system and a derivatives trading platform.

“I think there is a move towards e-trading in markets generally. As markets become more efficient and more transparent this is a natural progression,” said Robin Poynder, head of regulation for the marketplaces group at Thomson Reuters. “Not only is there a regulatory push

but there is clearly a commercial incentive for the buy-side in terms of operational efficiencies,” said Eric kolodner, managing director at Tradeweb in London.

The volume of derivatives traded on electronic platforms has grown over the last year. ICAP, for example, has

seen record numbers in 2011 on its BrokerTec platform for repo and fixed income, while Tradeweb has seen record highs of trading volumes in interest rate swaps during last year. Multi-dealer platform providers have also had to develop their service to deal with the increase in trading volumes, and have also been expanding their asset class and instrument offering.

Tradeweb is one firm that has been developing product offerings in different asset classes and tradable instruments.

The firm recently launched fx options on its platform allowing customers to buy and sell plain vanilla options and multi-leg strategies across G10 currencies. It comes hot on the heels of three-way trade confirmation functionality on its U.S. tri-party repo trading platform.

“We have been focused on derivatives in particular, not only growing our existing products such as interest rate swaps, but expanding into other asset classes within derivatives--credit default swap indices, fx options and equity derivatives--so that is one way in which we are looking to capitalise on regulatory change in efforts to expand our business,”said Kolodner. “We have a lot of different products with different timing protocols depending on the asset class and on what is feasible and doable because as a multi-dealer platform we can only offer what dealers are actually capable of responding to,” said uwe Hillnhütter, director, interest rate swaps at Tradeweb in London.

As the proposed legislation comes into force there is going to be a requirement to centrally clear qualifying credit default swap trades. MarketAxess has been trading CDS on its electronic platforms since 2005. “We have developed a range of solutions to improve the reliable trading of CDS and the proposed legislation is tending towards encouraging, if not enforcing, the industry to trade in the same ways that we were already proposing,” said Joe Feerick, head of European product management at MarketAxess in London. “We have already built links to the main clearers that market participants will be required to clear through once the SEF rules come into practice,” he added.

MarketAxess already had its CDS products live, with 10 dealers streaming executable CDS index pricing onto its platform; however, they also intend to expand into streaming prices for single names CDS. “An area where the industry

Platforms Expand As Regs Draw Nearer

The trading of derivatives on multi-dealer platforms has grown over the last year as regulation in the U.S. and Europe will require the migration of the majority of over-the-counter swaps and derivatives to electronic trading platforms. Beth Shah examines how would-be swap execution facilities, or organised

trading facilities as they are known in Europe, are expanding, and what challenges still remain.

“Some people are creatures of habit, others have felt that they will be able to find better liquidity on the phone.”

— Joe Feerick

Robin Poynder

MARCH 2012 | www.DeRivAtivesintelligenCe.CoM ELECTRONIC TRADING REPORT

©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997. 15

ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

hasn’t developed yet electronically is single names CDS. We have developed a functionality to support streaming markets for single names and we have been offering electronic trading of single name CDS via our RFQ protocol since last year.” said Feerick.

Like CDS and fx, interest rate swaps have also seen increased volume on electronic platforms. “A lot of IRS trading is voice-broked at the moment, but it is being moved towards electronic trading in Europe and the U.S. because of regulation,” said Poynder. “IRS as we know are largely cleared in the inter-dealer space so this lends itself very naturally to that [e-trading] model,” he added.

E-trading, however, still faces tough competition from the conventional telephone: observers estimate 15% is electronic. “In IRS it is a matter of increasing volumes, numbers of dealers, and buyside clients on the platform, as well as expanding its functionality according to client needs—effectively expanding the connections between the market participants interacting on our platform,” said Kolodner.

“One of our biggest competitors is still the phone,” he added.

Some investors worry about disclosure issues if they were to use electronic platforms. “Some people are creatures of habit, others have felt that they will be able to find better liquidity on the phone,” said Feerick. Over-the-counter derivatives, as their name suggests, are often bespoke. “There is always a reason for bespoke trades and by the nature of them they are not liquid, they are bespoke and they don’t lend themselves to electronic trading,” said Poynder.

There are also other challenges facing the growth of electronic trading. “The biggest challenge that we face, and that everybody faces, is that there are a lot of different scenarios [arising from regulation] that you could run depending on what the final protocols are,” said Ben MacDonald, global head of fixed income at Bloomberg in London. The final regulations could have an impact on the competitive landscape depending on how prescriptive the rules are. This creates uncertainty and it poses difficulties in

allocating resources. n

The Dodd-Frank regulatory reforms in the U.S. have

made electronic trading the way of the future,

whether anyone likes it or not. Though firms are not

obligated to move some of their derivatives trading

to electronic platforms until next year, those who are

heading the e-platform businesses are looking to capture

the market before end users have a swell of choices.

“It’s a chicken-or-the-egg problem,” said Ron karpovich,

managing director in e-commerce Royal Bank of

Scotland. “Is it now? Is it in the future? As one goes, the

rest will follow.”

Firms racing to beat the market on two fronts, with the

bet that the first and most flexible single-dealer cross-

asset electronic trading platforms are going to define

the way users trade for years to come. As such, firms are

looking for ways to lock in a target user base and keep

them with a competitive edge. uBS has rolled out a

first-of-its-kind platform for buyers and sellers of credit

default swaps to make markets on a bilateral basis.

RBS will soon launch cross-asset trading for its Agile

platform, which targets futures traders by giving them an

automated way to hedge gamma.

Firms are looking to capture the market before end

users have a swell of choices and many are

currently formulating platforms and keeping tight lipped about their form. “We know we’re

not the only firm out there selling electronic

trading,” said Daniel Ciment, head of

electronic trading solutions for the Americas

at JP Morgan. “As a leader in electronic

trading, we know that someone out there is

trying to take market share.”

Electronic trading has been a part of fx and equities

options trading for years, but Dodd-Frank is driving

firms to move some of over-the-counter derivatives

trading business online. “It will change the economics

on the trade, change the way we do business and

generate revenue,” said Jon Butler, head of equities &

U.S. Firms Bulk Up, Focus On NichesThe backdrop of the Dodd-Frank Act looms large on the U.S. landscape. Ahead of regulatory

deadlines, firms are looking to steal a march on each other. Kevin Dugan reports.

Daniel Ciment

16 ©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997.

MARCH 2012 | www.DeRivAtivesintelligenCe.CoM ELECTRONIC TRADING REPORT ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

structured retail technology and change at RBS. “But most

importantly it will require infrastructure to accommodate

all of the changes.”

To pave the way, banks have been building out their

electronic platform teams. “We’ve grown our team over

the last 12-18 months pretty significantly,” said JPMorgan’s

Ciment. A recruiter in New York who is familiar with the

electronic trading market said hiring for some firms has

been going on for even longer.

CLIEnT CALLS

Firms design electronic platforms to make trading easier

for clients. There are brainstorming sessions, solicitations

for client opinions, conference calls. Some platforms

are designed to bypass the traditional voice brokers and

screen watchers that end users have traditionally relied

on. “Electronic trading is all about being efficient and

doing more with less,” Ciment said.

The efficiency race has also set firms to focus on specific

areas of the market, and finding ways to capture market

share. This means developing platforms that are unique

to users’ needs in trading specific financial instruments.

In December, UBS launched such a platform, called the

Price Improvement Network-Fixed Income. “One strategy

we decided to pursue, among other things, is to be quite

aggressive and forward thinking

in developing a meaningful

electronic trading platform for

customers of CDS,” said Paul

Hamill, managing director of

matched principal trading at UBS.

It allows end users to hit or lift

prices on about 300 names, see

where the most liquidity is in the market, and give users

the ability to see where there is activity in the market.

“Customers know that they can trade with each other, so

it’s all-to-all and they never have to have [International

Swaps and Derivatives Association agreements] with each

other,” Hamill said. As of mid-February, the platform

had approximately 50 users, and about USD1.2 billion

has traded over about 200 trades. The platform is also

designed to adapt to where the markets have concentrated

the most liquidity in the future.

Hamill said clients will be able to access PIN-FI through an

application programming interface for algorithmic trading.

When traders are required to go through swap execution

facilities for off-the-run instruments, like a legacy roll of

the Markit investment grade credit default swap index,

the platform is designed to consider different clients’

eligibility for which prices it has available.

RBS has also been looking to capture market share by

increasing the capabilities of its current platform, FX

Agile. UBS is planning on integrating other asset classes

on its Agile platform in order to give traders the ability to

monitor gamma, or correlation risk. “When you’re doing

cross-asset trading, you’re looking at correlation risk,”

Karpovich said.

Agile is designed to give futures traders greater ability to

set limits on gamma and, he said, hedge more efficiently.

“It’s a speed issue,” he said. A futures trader may hedge

gamma three or four times a

day. Agile allows the trader to set

up the parameters for gamma

and time and the number of

hedges can increase to 70 trades

a day. “The number increased

dramatically because it catches

every component. The system

looks at every small parameter in

price. It is a significantly better

hedging strategy by hedging much

more minutely.”

“The easy way to look at it is that gamma risk is correlated

to price,” Karpovich said. “So once you give us a gamma

number, we can hedge correlation. You can do that

with any two assets once you calculate the correlation.

It’s naturally cross-asset when you start working out

correlated prices.”

But launching novel electronic platforms for assets that

have not seen much, or any, electronic trading does not

come without its own risk. Some firms may not want to

open up a platform when markets might not be ready to

embrace electronic platforms just yet. “Regulations aside,

with equities it took 10 years to get fully electronic,”

Butler said. “There’s a big debate as to how fast it’s going

to happen in all asset classes.” n

“There’s a big debate as to how

fast it’s going to happen in all asset classes.”

— Jon Butler

“We know that someone out there is trying to take market share.”

— Daniel Ciment

MARCH 2012 | www.DeRivAtivesintelligenCe.CoM ELECTRONIC TRADING REPORT

©InstitutionalInvestorIntelligence2012.Reproductionrequirespublisher’spriorpermission.ToreceiveemailalertsoronlineaccesstoDerivativesIntelligence,call(800)437-9997. 17

ELECTRONIC TRADING REPORT MARCH 2012 | www.DeRivAtivesintelligenCe.CoM

A s interest rates begin their ascent from zero, Dodd-Frank is implemented and market conditions improve,

futures trading will become a more important portfolio tool for institutions. Many of the largest and most sophisticated investment managers, including top mutual fund companies and hedge funds, are expecting to either start trading futures or increase their futures trading levels.

Likewise, U.S. futures exchanges announced record volumes in 2011 and TABB Group expects this momentum to carry forward into 2012 (see Exhibit 1). Of the 12 million futures contracts traded per day in 2011, nearly 50% were executed by buy side traders. From just a few years ago until today, the percentage of trading by the buy-side continues to increase.

Rising volumes in the U.S. futures market is a clear indication of hedge fund speculators that are once again on the rebound, post-credit crisis. In addition, traditional investment managers facing increased competition from hedge funds and passive investment strategies are running more-complex portfolios. And pension funds are increasing their allocations to commodity trading advisors, as investing in futures has the potential to provide better alpha returns as well as capital preservation.

EvoLvInG PoRTFoLIo DEMAnDS

Going forward, the regulatory push for centrally cleared and exchange-traded instruments will add to volumes, as will provisions within the Dodd-Frank Act that are transitioning OTC swaps trading to more transparent swap execution facilities (SEFs). As swaps trading becomes more automated, the ability of traders to use interest rate futures and other

related instruments as part of overall strategies becomes attractive, especially for correlation and relative value strategies that look to profit from price changes in other asset classes.

Another factor behind the increased adoption of futures is the need by portfolio managers to generate and retain

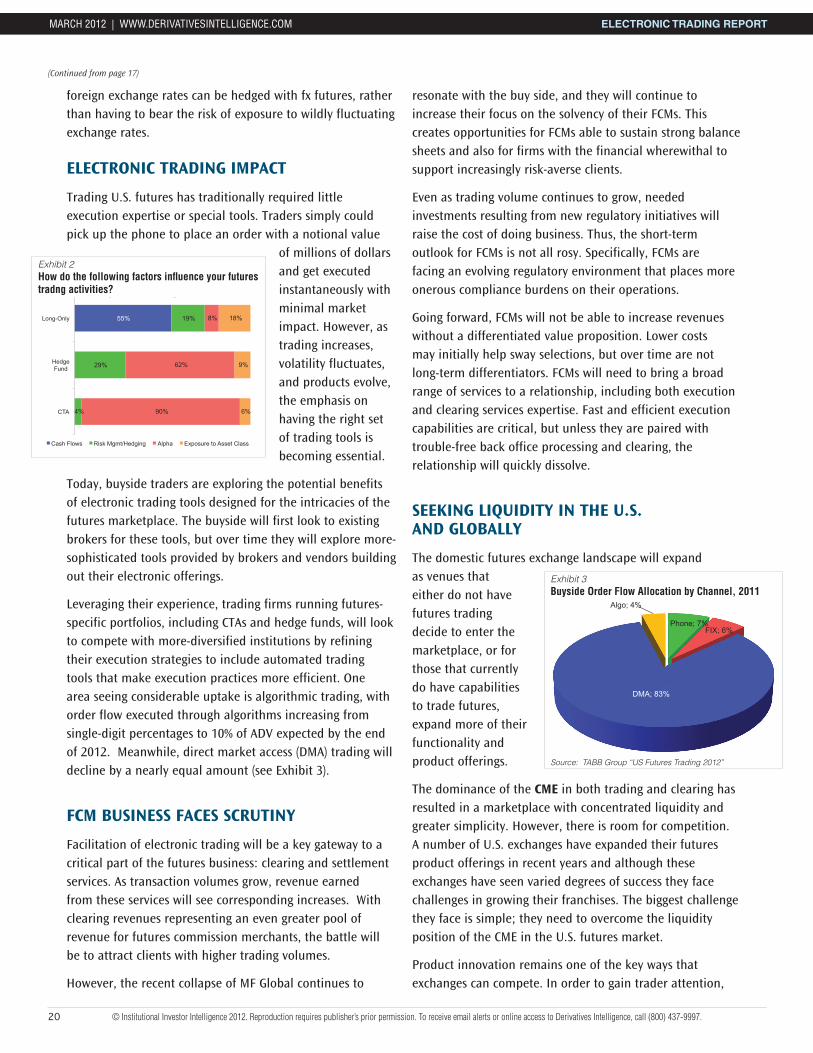

alpha. With a rise in ETFs and beta-replicating strategies, there is significant pressure on asset managers to increase returns as investors choose between active and passive management. Futures provide leverage and exposure to asset classes and markets that historically have not been in the active management sweet spot. The ease and flexibility of using futures to access these markets provide an efficient way for firms to expand their strategies (see Exhibit 2).

An additional incentive for the buyside is to better manage capital. Dodd-Frank opens up a world of opportunity for investment managers, especially for firms already trading OTC interest rate swaps. Interest rate futures will become both a complement and an enabler for strategies that have traditionally relied on OTC swaps for returns. Similarly, equity managers continue to struggle with putting cash inflows to work in today’s fragmented equity markets, and futures are an effective way to achieve this objective.

Futures are also gaining greater prominence among traditional asset managers as an effective hedging vehicle, and are becoming more important to managers looking to protect against unanticipated movements in asset prices. As volatility and market uncertainty become the new market norm, traders are gravitating toward a new crop of volatility products that can help manage this market environment. And as investment portfolios become global, fluctuations in

Futures On The Rise

U.S. futures usage is tipped to rise among hedge funds and mutual fund players. Market conditions and the regulatory drive to create open markets, such as with swaps, are key factors behind the prediction. Matt Simon, a senior analyst at TABB Group, outlines what is in store.

Millions of contracts traded on US exchanges

629

851

1,043

1,324

1,653

2,044

2,645

2,850

2,328

2,765

3,056

Total Other/Metals FX Commodities Energy Equity

3,354

2001-2008

CAGR 24%

2011-2012e

+10%

-18%

US Futures Trading Volume (2001-2012e) Exhibit 1 U.S. Futures Trading Volume (2001-2012e)

Source: Futures Industry Association, TABB Group

(Continued on page 20)

SponSored Article

Alpha Profiling – A Better Way for Institutional Traders to Choose Execution Strategies

By Henri Waelbroeck, Ph.D., Director of Research, Aritas Group, Inc.

New techniques in business intelligence have been empowering

businesses to turn their data into intelligent information and optimize their operations. This process has spurred a revolution over the past decade that has helped companies post record profits while keeping inflation in check. This trend is expected to accelerate over the next decade, as so-called big data solutions are deployed. The institutional trading desk is deeply engaged in this revolution. In this article, we will describe how the analysis of historical trading data and new techniques in Transaction Cost Analysis today are helping portfolio managers capture alpha, and soon will enable further gains through feedback on market timing, trade selection or substitution.

Trading desks for a long time have been well aware that there are differences in the order flow from different managers. While some managers tend to initiate orders with a high risk of adverse price moves that need to be executed with urgency, others are more likely to trade contrary to the flow to capture opportunities created by impatient traders on the other side; these require patient execution and should not suffer any implementation shortfall (IS). The root cause of the similarities and differences between portfolio managers lies in the coherence in thinking amongst industry participants. Whether acting from a common signal or following similar lines of reasoning, portfolio managers often respond to the same events, information, and opportunities in similar ways: broadly speaking, one group will hold consensus views while another group will hold

contrarian views. A particular portfolio manager may be more likely to be aligned with the consensus or contrarian view, and this characteristic is persistent on a timescale that is sufficient to enable the optimization of execution strategies.

Yet it would be wrong to describe all orders from a portfolio manager as sharing a common signature: a portfolio manager typically initiates orders for a number of different reasons; as these orders reach the market they encounter different environments – to understand the urgency of a trade requires knowledge of both the portfolio manager’s historical profile and the current market drivers. Indeed, for each portfolio manager one can identify several classes of orders. Orders within a class share similar attributes and a historically-consistent short-term alpha pattern. Market microstructure variables such as the order flow imbalance acquire a very different meaning when they are considered at or shortly after the start of a new institutional trade. The supply and demand imbalances that are revealed in the order flow observations at this particular time reflects on whether a particular portfolio manager is more likely to be aligned with or contrarian to the market consensus in this particular trade. The market is generally well-arbitraged, so order flow imbalances provide limited alpha in other circumstances, but the arrival of a new institutional trade represents private information for which arbitrage arguments do not apply.

Alpha profiling is a systematic statistical analysis aiming to identify classes of trade

arrival that share common features and for which the same execution strategy is optimal. In a simplified example, one might have to choose between only two execution strategies: a slow one, such as a VWAP algorithm, or a fast one such as a front-loaded IS algorithm. Looking at each trade in a historical dataset it is possible to estimate in hindsight what the cost would have been using one or the other strategy. One might find for example that trade arrivals on weak sector-relative momentum tend to have low urgency. More generally, data mining techniques use Bayesian classifiers to identify statistically significant associations; expert knowledge can be introduced as a second step to select rules that have an economic underpinning and therefore are more likely to generalize in the future. The factor universe comprises both attributes of the order arrival itself (size of the order, stock, side, PM instructions, for example) and market factors such as momentum, sector, the presence of news, etc.

Ultimately an alpha profiling system will partition the feature space into domains that are associated with low urgency trades and other domains that are associated with high urgency trades. In each domain, one can compute the historical average impact-free return as a function of time, called “alpha profile”, and marry an execution strategy to this statistical profile in order to minimize overall cost.

A practical implementation of alpha profiling must deal with more complex questions than simply the decision of whether to execute fast or slowly. A

SponSored Article

minimal set of design parameters must include:

• Execution speed; or equivalently, target completion time

• Front-loading / back-loading of the implementation schedule

• Granularity (execute continuously over time or in bursts as opportunities arise)

• Block exposure (accept or reject opportunities to cross)

• Sector-relative stability (slow on sector divergence?)

All of these strategy design items represent critical decisions, in that each one can cause an execution to be vastly more expensive than it should have been. The institutional trader is tasked with making these decisions today but must do so without quantitative tools that provide insight on the likely outcomes.

It is possible to assign execution parameters at trade start based on historical analysis, as we illustrated with the example of execution speed. However, some of the most valuable information is revealed after the start of trading. Indeed, if one believes that portfolio managers seldom act alone, there are likely to be other orders in the same or opposite direction that are sitting on order management systems and have not yet been expressed on the market. As a trade begins to execute, its impact on price automatically creates urgency for other orders on the same side that may have been waiting for price or liquidity opportunities. Or in the case of a contrarian trade, the discovery of hidden liquidity may foretell opportunities for further price improvement. A successful application of alpha profiling requires a “hypothesis validation” step where the initial trade classification is revisited after the early execution results have expressed themselves. If the new information

contradicts the original hypotheses, the trade may need to be re-assigned to a different execution plan.

Does the application of hypothesis validation in alpha profiling create unstable markets? The risk of instability certainly exists if strategies are poorly designed so that they reinforce coherence. For instance, one possible action plan in the case of coherent PM signals is to execute relatively fast, say at 20% of market volume… if several parties come to the same conclusion the competition for liquidity can cause price to overshoot its

target. Properly-designed alpha profiling systems must not only determine whether or not short-term alpha is likely to be present but also estimate its amount, in order to determine how many basis points of sector-relative price appreciation should be considered acceptable within a front-loading stage. If price overshoots this level, the strategy should realize that the expected alpha has been exhausted and automatically pull back to a more passive execution plan. A properly-designed execution framework incorporates the relative value safeguards that ensure stability. Ultimately, the role of the institutional trader remains vital to oversee the process and take control where needed, or to look for opportunities to add value in situations where unique

circumstances invalidate the quantitative analysis. With an interface that provides transparency and control, alpha profiling

places Artificial Intelligence at the service

of the trader, and not vice-versa.

What is the potential ROI for implementing an alpha profiling methodology? The answer depends on the particular portfolio manager. In the chart below we show IS results for Aritas’ Alpha Pro platform in 2011, for US and European markets separately. The IS results are compared to the estimated results of a 10% volume participation strategy.

The results point to savings of

approximately 10bps overall resulting from the implementation of an alpha profiling methodology. We have found this to vary quite a bit by manager, with some portfolio managers achieving savings of 40bps and others 2-3bps. The largest savings typically occur for accounts with very large orders and little-to-no short-term alpha, where a disciplined and patient approach provides the greatest benefits.

For further information about Aritas’ Alpha Pro, please visit http://aritasgroup.com/.

-40 -35 -30 -25 -20 -15 -10 -5 0

EU

US

Alpha Pro Results 2011

MAC

I/S

Exhibit 1. Average Alpha Pro realized shortfalls in the US and EU regions are shown compared to the estimated cost using a 10% participation strategy (Momentum-Adjusted Cost, or MAC). The average savings is approximately 10bps.

20 © Institutional Investor Intelligence 2012. Reproduction requires publisher’s prior permission. To receive email alerts or online access to Derivatives Intelligence, call (800) 437-9997.

MARCH 2012 | WWW.DERIVATIVESINTELLIGENCE.COM ELECTRONIC TRADING REPORT ELECTRONIC TRADING REPORT MARCH 2012 | WWW.DERIVATIVESINTELLIGENCE.COM

foreign exchange rates can be hedged with fx futures, rather than having to bear the risk of exposure to wildly fluctuating exchange rates.

ELECTRONIC TRADING IMPACT

Trading U.S. futures has traditionally required little execution expertise or special tools. Traders simply could pick up the phone to place an order with a notional value

of millions of dollars and get executed instantaneously with minimal market impact. However, as trading increases, volatility fluctuates, and products evolve, the emphasis on having the right set of trading tools is becoming essential.

Today, buyside traders are exploring the potential benefits of electronic trading tools designed for the intricacies of the futures marketplace. The buyside will first look to existing brokers for these tools, but over time they will explore more-sophisticated tools provided by brokers and vendors building out their electronic offerings.

Leveraging their experience, trading firms running futures-specific portfolios, including CTAs and hedge funds, will look to compete with more-diversified institutions by refining their execution strategies to include automated trading tools that make execution practices more efficient. One area seeing considerable uptake is algorithmic trading, with order flow executed through algorithms increasing from single-digit percentages to 10% of ADV expected by the end of 2012. Meanwhile, direct market access (DMA) trading will decline by a nearly equal amount (see Exhibit 3).

FCM BUSINESS FACES SCRUTINY