electronic supplement to chapter...

TRANSCRIPT

ELECTRONIC SUPPLEMENT TO CHAPTER 7

Students sometimes find the material presented in this chapter difficult. Teachingexperience indicates that this difficulty often arises from lack of familiarity with

the basics of accounting for bond transactions. This supplement therefore presents a briefreview of bond accounting.

Chapter 7 in the text discusses consolidation working papers when the parent companyuses the equity method of accounting. This supplement repeats those illustrations for acomprehensive review of intercompany bond accounting using the complete equity, theincomplete equity, and cost methods of parent company accounting, following a discussionof basic accounting for bond transactions.

Exhibit E7-1 presents the complete equity method of accounting. Exhibit I7-1 presentsincomplete equity method accounting, Exhibit TI7-1 presents the traditional approach tothe incomplete equity method accounting (i.e., no initial conversion to complete equitymethod accounting). Exhibit C7-1 presents the cost method of accounting. Exhibit TC7-1presents the traditional approach to cost method accounting (i.e., no initial conversion toequity method accounting).

� � �

UNDERSTANDING BONDSWe can account for bonds using either a gross or a net approach. Under the gross method,we record bond investments or payables at their par value, with either an offsettingdecrease for bond discounts or a supplement for bond premiums. We report bond discountsand premiums in separate contra or adjunct accounts, respectively. Under the net method,we simply net discounts or premiums against the recorded bond investment or payableaccounts. The textbook uses a net approach because it more clearly highlights the financialstatement impact of these transactions.

This discussion reviews the basics of accounting for bonds payable, which repre-sent an important source of capital financing for many companies. Clearly understand-ing accounting for bonds will help you understand the problems posed by intercompanybond transactions in preparing consolidated financial statements. Specifically, thismaterial reviews journal entries for bonds payable (1) when originally recorded, (2) dur-ing the holding period, and (3) when redeemed, including early extinguishment of debtobligations.

A bond payable is a long-term debt security. Under the terms of a standard bond contract(an indenture), investors lend money to the issuer. The issuer agrees to repay the principal

Electronic Supplement to Chapter 7 1

C H A P T E R 7

2 ADVANCED ACCOUNTING

amount (the par value) at a future maturity date. Typically, firms issue bonds for long time periods,often 10 or 20 years or longer.

In addition to the principal repayment, the issuer agrees to make periodic cash interest paymentsto the investors. Most corporate bonds pay interest on a semiannual basis. The terms of the indenturedetermine the amount of the cash interest payments. Bonds pay interest based on the par value of thebond and the stated (or coupon) interest rate. For example, assume Barton Corporation issues a $10million, 8% bond that pays interest semiannually on June 30 and December 31. On each interestpayment date, Barton writes a check for $400,000, based on the stated terms ($10 million � 8% �1/2 year). Subsequent changes in the fair market price of the bonds or the effective interest rate donot change the cash interest payments.

Accounting for Issuance of Bonds PayableThe issuer records the bonds payable based on the selling price of the bond issue. The issuer alsorecords the receipt of cash proceeds from the bond issue.

Bonds always sell at fair market value. The issuer’s business and credit risk, the time period untilmaturity, and the general market rate of interest determine the fair market value of a bond. The marketrate of interest for a bond of a given risk level and term to maturity is known as the effective interest rate.

The effective interest rate changes over time due to changing economic conditions. For exam-ple, a company may diversify into several different lines of business, decreasing its overall operat-ing risk. The decrease in risk leads to a decrease in the effective interest rate. However, the bondindenture fixes the stated rate on a bond, which does not respond to changing economic conditions.Bond prices adjust for differences between the stated rate and the effective rate, so that the bondalways sells for its fair market value.

Bond prices adjust to fair market value as follows. If the stated interest rate is equal to the effec-tive interest rate, then the bond sells for its par value. If the stated interest rate is less than the effec-tive interest rate, then the bond sells for less than its par value, at a discount. If the stated interest rateis greater than the effective interest rate, then the bond sells for more than its par value, at a premium.

Investors seek to earn a fair rate of return on investments. We calculate rate of return by divid-ing the interest received by the cost of the investment. Consider a bond sold at a discount. Since theindenture fixes the cash payments for interest, the investors can earn the fair market rate of return(the effective interest rate) by reducing the price they pay for the bond. The bond indenture fixesthe numerator of the rate of return. The rate of return can only be changed by adjusting the denom-inator (the bond price).

EXAMPLE Acme Corporation decides to raise needed funds for a major plant expansion by issuing$8 million of five-year, 8% bonds on January 1, 2003. The bonds pay interest annually onDecember 31.

BONDS ISSUED AT PAR VALUE Assume that the effective interest rate is 8% on January 1, 2003. The bondshave a stated rate equal to the effective rate and sell for par value. You can verify that this is the fairmarket value of the bonds.

First, identify the future cash flows associated with the bond. There will be an $8 million out-flow at the end of five years for repayment of the par value. There will be annual payments of$640,000 each (an ordinary annuity), representing the cash payments for interest. We calculate thisby multiplying the stated interest rate (8%) times the principal amount of the bond ($8 million).

Next, calculate the present value of the future cash flows using the effective interest rate of 8% forthe five years until maturity. The present value of the $8 million principal repayment is $5,444,800.The present value of the $640,000 interest annuity is $2,555,328. The total present value of theremaining cash flows is $8,000,128. This amount equals the par value of $8 million. (There is a $128difference due to rounding.) The present value of the future cash flows is the fair market value of thebond. Acme makes the following journal entry to record the issuance of the bond:

Cash (+A) 8,000,000

Bonds payable (+L) 8,000,000

BONDS ISSUED AT MORE THAN PAR VALUE Assume that the effective interest rate is 6% on January 1, 2003.The bonds have a stated rate greater than the effective rate and should sell for a premium. You candetermine the price of the bonds.

Electronic Supplement to Chapter 7 3

The bond indenture specifies the future cash flows, which are identical to those discussed previ-ously for the bond sold at par value. Calculate the present value of these future cash flows using theeffective interest rate of 6% for the five years until maturity.

The present value of the $8 million principal repayment is $5,978,400. The present value of the$640,000 interest annuity is $2,695,936. The total present value of the remaining cash flows is$8,674,336. This is the fair market value of the bond. The bond sells for $8,674,336, a premium of$674,336 over par value. Investors pay more than par value because the bond offers stated interesthigher than the effective rate at the issue date. Acme makes the following journal entry to recordthe issue of the bond at a premium:

Cash (+A) 8,674,336

Bonds payable (+L) 8,674,336

BONDS ISSUED AT LESS THAN PAR VALUE Assume that the effective interest rate is 10% on January 1, 2003.The bonds have a stated rate less than the effective rate and sell for a discount. You can determinethe price of the bonds, as was done in the previous cases. The total present value of the cash flowsis $7,393,312. This amount is the fair market value of the bond. The bond sells for $7,393,312,reflecting a discount of $606,688 from par value. Investors pay less than face value because thebond offers stated interest lower than the effective rate at the issue date. Acme makes the followingjournal entry to record the issue of the bond at a discount:

Cash (+A) 7,393,312

Bonds payable (+L) 7,393,312

Accounting for Bonds at MaturityUnder terms of the bond indenture, the issuer repays the par value at the maturity date. This is inde-pendent of the original issue price of the bond. In all three of the previous cases, Acme repays the$8 million par value when the bond matures on December 31, 2007. The following journal entryrecords redemption of the bond:

Bonds payable (�L) 8,000,000

Cash (�A) 8,000,000

Accounting for Bonds During the Holding PeriodBONDS ISSUED AT PAR VALUE Acme makes annual interest payments beginning December 31,2003, continuing until the final payment on December 31, 2007. Acme bases the amount of cashinterest paid on the stated rate and par value. The cash payments are $640,000 each ($8,000,000 �8%). Acme calculates interest expense using the effective interest method. Under this method,Acme calculates the expense by multiplying the book value of the bond payable by the effectiveinterest rate. In this example, interest expense is also $640,000 ($8,000,000 � 8%). Acme makesthe following journal entries to record interest payments on December 31 each year.

Interest expense (E, �SE) 640,000

Cash (�A) 640,000

Recognize interest expense ($8,000,000 � 8%).

The book value of a bond issued at par value remains the same over the life of the bond. Acmereports a bond payable balance of $8 million on its balance sheet every year until maturity. Notethat since the bond liability does not change over the life of the bond, the interest expense calcu-lated under the effective interest method is the same each period.

BONDS ISSUED AT A PREMIUM Acme still makes annual interest payments based on the stated rateand par value (i.e., $640,000 each). In the case of the bond issued at a premium, Acme makes thefollowing journal entry to record the December 31, 2003, interest payment:

Interest expense (E, �SE) 520,460

Bonds payable (�L) 119,540

Cash (�A) 640,000

[Bonds payable � 6%]

[$8,674,336 � 6% � $520,460]

4 ADVANCED ACCOUNTING

The interest expense does not equal the interest payment. Acme calculates interest expenseusing the effective interest method, by multiplying the book value of the bond payable by the effec-tive interest rate. The difference between the interest expense and the cash interest paymentreduces the book value of the bond liability. The bond payable balance must be reduced to $8 mil-lion by the maturity date. The entry to record the December 31, 2004, payment is as follows:

Interest expense (E, �SE) 513,288

Bonds payable (�L) 126,712

Cash (�A) 640,000

[Bonds Payable � 6%]

[($8,674,336 � $119,540) � 6%]

The following amortization table summarizes the journal entries made over the life of the bond.

Interest Cash Bond BondExpense Payment Payable Payable

Date DR CR DR Balance

January 1, 2003 — — — $8,674,336December 31, 2003 $520,460 $640,000 $119,540 8,554,796December 31, 2004 513,288 640,000 126,712 8,428,084December 31, 2005 505,685 640,000 134,315 8,293,769December 31, 2006 497,626 640,000 142,374 8,151,395December 31, 2007 489,084 640,000 150,916 8,000,479December 31, 2007 8,000,000 8,000,000 479*

*Rounding difference

BONDS ISSUED AT A DISCOUNT Acme still makes annual interest payments of $640,000 each, basedon the stated rate and the par value. In the case of the bond issued at a discount, Acme makes thefollowing journal entry to record the December 31, 2003, interest payment:

Interest expense (E, �SE) 739,331

Bonds payable (+L) 99,331

Cash (�A) 640,000

[(Bonds Payable) � 10%]

[($8,000,000 � $606,688) � 10% � $739,331]

As for a bond sold at a premium, interest expense does not equal the interest payment. Using theeffective interest method, Acme calculates interest expense by multiplying the bond liabilityamount by the effective interest rate. The total bond liability is $7,393,312. The entry to record theDecember 31, 2004, payment is as follows.

Interest expense (E, �SE) 749,264

Bonds payable (+L) 109,264

Cash (�A) 640,000

[(Bonds payable) � 10%]

[$8,000,000 � ($606,688 � $99,331) � 10%]

The following amortization table summarizes the journal entries made over the life of the bond.

Interest Cash Bond BondExpense Payment Payable Payable

Date DR CR CR Balance

January 1, 2003 — — — $7,393,312December 31, 2003 $739,331 $640,000 $99,331 7,492,643December 31, 2004 749,264 640,000 109,264 7,601,908December 31, 2005 760,191 640,000 120,191 7,722,098December 31, 2006 772,210 640,000 132,210 7,854,308December 31, 2007 785,431 640,000 145,431 7,999,739December 31, 2007 8,000,000 8,000,000 (261)*

*Rounding difference

Electronic Supplement to Chapter 7 5

1SFAS No. 4,“Reporting Gains and Losses from Extinguishment of Debt,” March 1975.

Straight-Line Premium or Discount AmortizationUnder GAAP, all interest calculations, including premium and discount amortization, should usethe effective interest method. However, firms may amortize premiums and discounts using thestraight-line method when differences from the effective interest method are immaterial. For sim-plicity, straight-line amortization of premiums and discounts is used throughout Chapter 7.

Using the prior example of a bond originally issued at a discount, Acme issued the bonds at aprice of $7,393,312, reflecting a discount of $606,688. Using straight-line amortization, Acmerecords the annual interest expense with the following journal entry:

Interest expense (E, �SE) 761,338

Bonds payable (+L) 121,338

Cash (�A) 640,000

The interest expense equals the cash payment plus the straight-line discount amortization. Acmemakes the same entry at each interest payment date.

Investment in BondsBond investors account for bonds in essentially the same manner as bond issuers. However, theinvestor is on the opposite side of the transaction. Investors will record an investment in bonds andinterest income, rather than the bonds payable and interest expense recorded by the issuer.

In addition to the basic accounting for bonds, investors may also be required to adjust the invest-ment balance for changes in fair value of bonds during the holding period. GAAP requires suchadjustments for bonds classified as either trading or available-for-sale securities.

Extinguishment of Debt ObligationsIssuers choosing to retire outstanding bonds may realize either a gain or a loss on the retirement.The fair value of a bond changes over time due to fluctuations in interest rates. A gain (loss) ariseswhen the fair value at the redemption date is less (greater) than the book value of the bondspayable. The issuer must pay fair value to repurchase the bonds.

Returning to the earlier example of a bond issued at a premium, Acme decides to retire its out-standing bonds payable on December 31, 2004. At that date, the bonds are priced to sell for$8,400,000. The amortization schedule shows that the book value of the bonds is $8,428,084.Acme records the early retirement with the following journal entry:

Bonds payable (�L) 8,428,084

Cash (�A) 8,400,000

Extraordinary gain on early

extinguishment of debt (Ga, �SE) 28,084

Acme classifies the gain or loss on extinguishment of debt as an extraordinary gain or loss inaccordance with the provisions of Statement of Financial Accounting Standards (SFAS) No. 4.1

PARENT COMPANY BONDS PURCHASED BY SUBSIDIARYChapter 7 provides an example of constructive retirement when a subsidiary purchases its parentcompany’s bonds. That example is repeated here to illustrate changes in consolidation techniqueswhen the parent company uses either the incomplete equity method or the cost method to accountfor its investment in the subsidiary.

Incomplete Equity and Cost MethodsTo illustrate, assume that Sue is a 70%-owned subsidiary of Pam, acquired at its $5,600,000 bookvalue on December 31, 2003, when Sue had capital stock of $5,000,000 and retained earnings of$3,000,000.

Pam has $10,000,000 par of 10% bonds outstanding with a $100,000 unamortized premium onJanuary 1, 2005, at which time Sue Company purchases $1,000,000 par of these bonds for

6 ADVANCED ACCOUNTING

$950,000 from an investment broker. This purchase results in a constructive retirement of 10% ofPam’s bonds and a $60,000 constructive gain, computed as follows:

Book value of bonds purchased $1,010,000

[10% � ($10,000,000 par + $100,000 premium)]

Purchase price 950,000

Constructive gain on bond retirement $ 60,000

If Pam uses an incomplete equity method of accounting or the cost method in accounting for itsinvestment in Sue, Pam’s separate financial statements would show balances that differ from thoseillustrated under the equity method in Chapter 7 of the text as follows (amounts in thousands):

IncompleteEquity Equity CostMethod Method Method

Income StatementIncome from Sue $ 202 $ 154 —Pam’s net income 1,312 1,264 $1,110

Retained EarningsRetained earnings January 1, 2005 4,900 4,900 4,200Net income 1,312 1,264 1,110Retained earnings December 31, 2005 6,212 6,164 5,310

Balance SheetInvestment in Sue 6,502 6,454 5,600Retained earnings December 31, 2005 6,212 6,164 5,310

Assuming that Pam uses an incomplete equity method of accounting for its investment in Sueand has not adjusted for the constructive gain, the following working paper entry would adjustPam’s accounts to the equity method:

Incomplete Equity Method

Investment in Sue (+A) 48,000

Income from Sue (R, +SE) 48,000

The conversion entry that would be required if Pam uses the cost method would be as follows:

Cost Method

Investment in Sue (+A) 902,000

Retained earnings January 1, 2005 (+SE) 700,000

Income from Sue (R, +SE) 202,000

After entering the conversion entry (incomplete equity to equity or cost to equity) in the workingpapers, all other working paper entries to consolidate the financial statements of Pam and Sue for2005 are the same as those illustrated in Exhibit 7-1 (in Chapter 7 of the text) under the equity method.

SUBSIDIARY BONDS PURCHASED BY THE PARENTIncomplete Equity and Cost MethodsFor convenience, the facts of the Pro and Sky Corporation example from Chapter 7 are repeatedhere, followed by a discussion of the preparation of consolidated statements when Pro uses eitherthe incomplete equity or cost methods to account for its investment in Sky.

Pro Corporation owns 90% of the voting common stock of Sky Corporation. Pro purchased itsinterest in Sky a number of years ago at its book value of $9,225,000. Sky’s capital stock was$10,000,000 and its retained earnings were $250,000 on the acquisition date.

At December 31, 2003, Sky had $10,000,000 par of 10% bonds outstanding with an unamor-tized discount of $300,000. The bonds pay interest on January 1 and July 1 of each year and maturein five years on January 1, 2009.

On January 2, 2004, Pro Corporation purchases 50% of Sky’s outstanding bonds for $5,150,000cash. This transaction is a constructive retirement and results in a loss of $300,000 from the viewpoint

Electronic Supplement to Chapter 7 7

of the consolidated entity. The consolidated entity retires a liability of $4,850,000 (50% of the$9,700,000 book value of the bonds) at a cost of $5,150,000. We assign loss to Sky Corporation underthe theory that the parent company management acts as agent for Sky, the issuing company, in allintercompany bond transactions.

During 2004, Sky records interest expense on the bonds of $1,060,000 [($10,000,000 par �10%) + $60,000 discount amortization]. Of this interest expense, $530,000 relates to the intercom-pany bonds. Pro records interest income from its investment in bonds during 2004 of $470,000[($5,000,000 par � 10%) � $30,000 premium amortization].

The $60,000 difference between the interest expense and the interest income on the intercom-pany bonds reflects recognition of one-fifth of the constructive loss during 2004. At December 31,2004, the books of Pro and Sky have not recognized $240,000 of the constructive loss through pre-mium amortization (Pro’s books) and discount amortization (Sky’s books).

If Pro uses an incomplete equity method or the cost method to account for its investment in Sky,its separate financial statements for 2004 would contain amounts that differ from those under theequity method as follows (amounts in thousands):

IncompleteEquity Equity CostMethod Method Method

Income StatementIncome from Sky $ 459 $ 675 —Pro’s net income 5,000 5,216 $4,541

Retained EarningsRetained earnings January 1 13,000 13,000 12,100Net income 5,000 5,216 4,541Retained earnings December 31 18,000 18,216 16,641

Balance SheetInvestment in Sky 10,584 10,800 9,225Retained earnings December 31 18,000 18,216 16,641

An entry in the consolidation working papers to convert from an incomplete equity to the equitymethod of accounting for 2004 follows:

Income from Sky (�R, �SE) 216,000

Investment in Sky (�A) 216,000

The only difference between the incomplete and complete equity methods lies in the construc-tive loss, so the conversion entry only affects the year 2004. The amount is 90% of the $300,000constructive loss less 90% of the $60,000 piecemeal recognition of the loss.

If Pro uses the cost method, the cost-to-equity working paper conversion for the 2004 consoli-dation would be as follows:

Investment in Sky (+A) 1,359,000

Income from Sky (R, +SE) 459,000

Retained earnings January 1 (+SE) 900,000

When entering the conversion entry under the incomplete equity method or the cost method inthe working papers, the adjusted amounts of Pro reflect the equity method of accounting as a one-line consolidation. Subsequently, the remaining working paper entries to consolidate the state-ments of Pro and Sky will be the same as those illustrated in Exhibit 7-3 in Chapter 7, under theequity method.

CONSOLIDATION IN YEARS AFTER INTERCOMPANY BOND PURCHASE UNDER DIFFERENTASSUMPTIONS

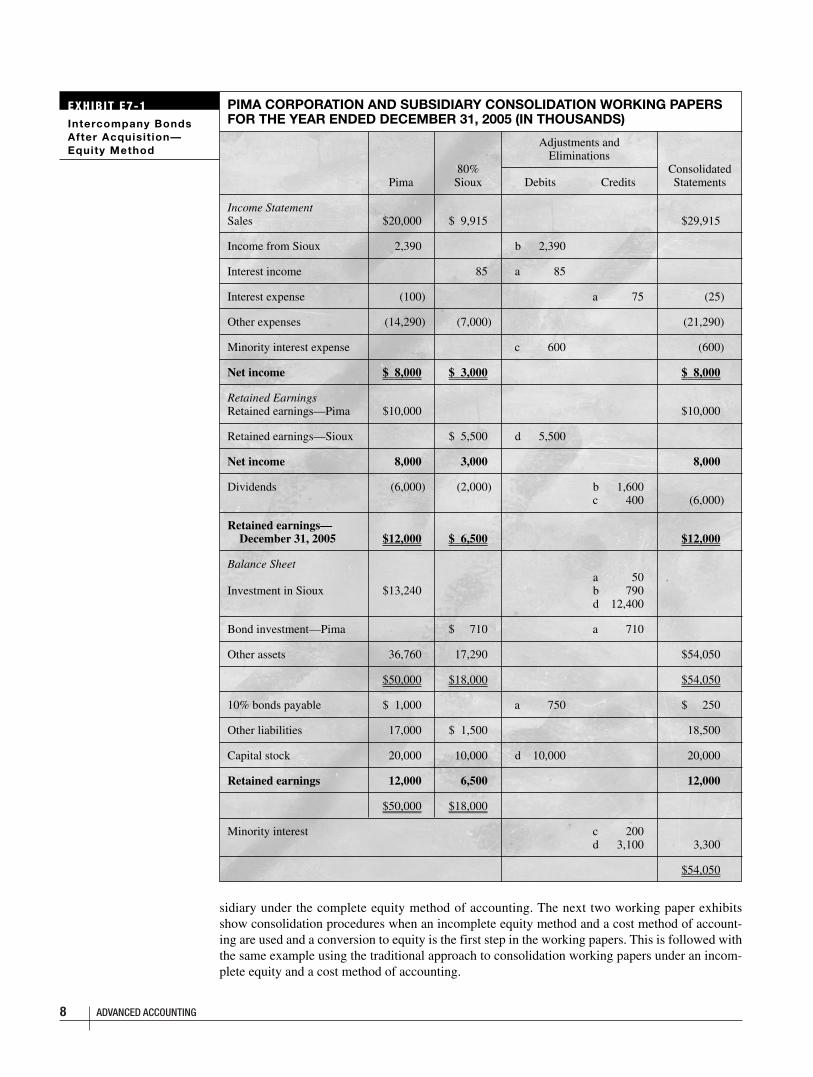

This section illustrates consolidation procedures in years after an intercompany bond purchaseunder several different parent company accounting assumptions. The first consolidation workingpaper (Exhibit E7-1) shows consolidation when the parent accounts for its investment in the sub-

8 ADVANCED ACCOUNTING

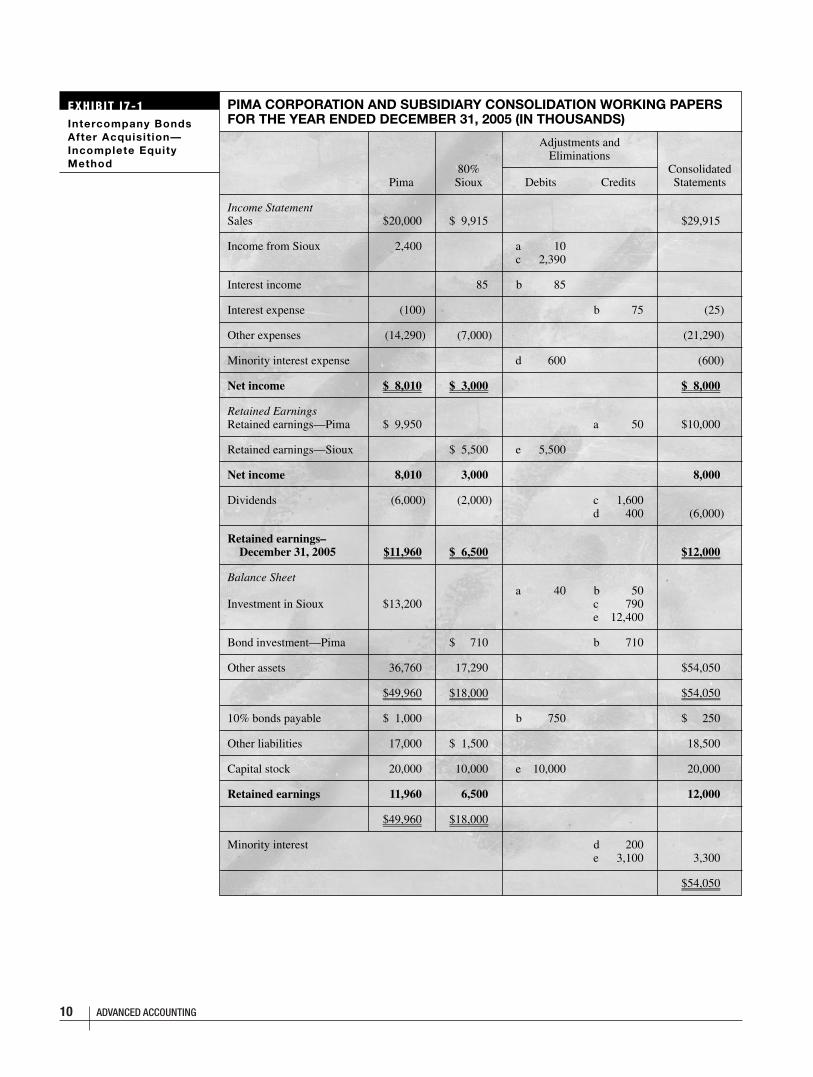

PIMA CORPORATION AND SUBSIDIARY CONSOLIDATION WORKING PAPERSFOR THE YEAR ENDED DECEMBER 31, 2005 (IN THOUSANDS)

Adjustments andEliminations

80% ConsolidatedPima Sioux Debits Credits Statements

Income StatementSales $20,000 $ 9,915 $29,915

Income from Sioux 2,390 b 2,390

Interest income 85 a 85

Interest expense (100) a 75 (25)

Other expenses (14,290) (7,000) (21,290)

Minority interest expense c 600 (600)

Net income $ 8,000 $ 3,000 $ 8,000

Retained EarningsRetained earnings—Pima $10,000 $10,000

Retained earnings—Sioux $ 5,500 d 5,500

Net income 8,000 3,000 8,000

Dividends (6,000) (2,000) b 1,600c 400 (6,000)

Retained earnings—December 31, 2005 $12,000 $ 6,500 $12,000

Balance Sheeta 50

Investment in Sioux $13,240 b 790d 12,400

Bond investment—Pima $ 710 a 710

Other assets 36,760 17,290 $54,050

$50,000 $18,000 $54,050

10% bonds payable $ 1,000 a 750 $ 250

Other liabilities 17,000 $ 1,500 18,500

Capital stock 20,000 10,000 d 10,000 20,000

Retained earnings 12,000 6,500 12,000

$50,000 $18,000

Minority interest c 200d 3,100 3,300

$54,050

EXHIBIT E7-1Intercompany BondsAfter Acquisit ion—Equity Method

sidiary under the complete equity method of accounting. The next two working paper exhibitsshow consolidation procedures when an incomplete equity method and a cost method of account-ing are used and a conversion to equity is the first step in the working papers. This is followed withthe same example using the traditional approach to consolidation working papers under an incom-plete equity and a cost method of accounting.

Electronic Supplement to Chapter 7 9

Pima Corporation acquired an 80% interest in Sioux Corporation on January 1, 2004, at its bookvalue of $12 million, when the stockholders’ equity of Sioux consisted of $10 million commonstock and $5 million retained earnings. The only intercompany transactions between the two com-panies occurred on December 31, 2004, when Sioux purchased 75% of Pima’s $1 million par, 10%outstanding bonds for $700,000. These bonds were issued at par and mature in five years onDecember 31, 2009.

During 2004, Sioux reported net income of $2.5 million and paid $2 million dividends.Under the equity method, Pima’s income from Sioux for 2004 is $2.05 million and its invest-ment in Sioux at December 31, 2004, is $12.45 million. The following table summarizescomparisons of Pima’s income from Sioux for 2004 and its investment in Sioux at December31, 2004, under the equity, incomplete equity, and cost methods of accounting (amountsin thousands):

IncompleteEquity Equity CostMethod Method Method

Income (dividends) from Sioux $ 2,050 $ 2,000 $ 1,600Investment in Sioux 80% 12,450 12,400 12,000

The $50,000 constructive gain on the intercompany purchase of bonds [($1,000,000 � 75%) �$700,000] creates the $50,000 differences in Pima’s income and investment in Sioux amountsunder the equity and incomplete equity methods. Pima’s (the parent company’s) bonds were con-structively retired, so we allocate no part of the gain to minority interests.

Pima’s dividend income under the cost method differs from income from Sioux under theincomplete equity method by $400,000, or 80% of Sioux’s $500,000 undistributed income from2004. Under the cost method, Pima’s investment in Sioux remains at its $12,000,000 cost onJanuary 1, 2004.

During 2005, Sioux reported $3 million net income and paid $2 million dividends, and the onlyintercompany transactions between Pima and Sioux related to the $75,000 interest ($1,000,000par � 10% interest � 75% owned) that Pima paid to Sioux and the $1.6 million dividends thatSioux paid to Pima. Pima’s total interest expense for 2005 is $100,000, and Sioux’s interest incomeis $85,000, consisting of $75,000 nominal interest plus $10,000 discount amortization. The follow-ing table compares changes in Pima’s investment in Sioux from acquisition to December 31, 2005,under the equity, incomplete equity, and cost methods of parent company accounting (amountsin thousands):

IncompleteEquity Equity CostMethod Method Method

Investment balance January 1, 2004 $12,000 $12,000 $12,000Income from Sioux—2004 2,050 2,000 —Dividends received (1,600) (1,600) —

Investment balance December 31, 2004 12,450 12,400 12,000Income from Sioux—2005

Equity in Sioux’s income 2,400 2,400 —Piecemeal recognition of gain on bonds (10) — —Dividends (1,600) (1,600) —

Investment balance December 31, 2005 $13,150 $13,200 $12,000

This information is reflected in comparative consolidation working papers for Pima and Siouxfor 2005 in Exhibit E7-1 for the equity method (Exhibit E7-1 is the same as Exhibit 7-5 in the text),Exhibit I7-1 for the incomplete equity method, and Exhibit C7-1 for the cost method. Under theequity method of consolidation illustrated in Exhibit E7-1, Pima’s net income of $8 million equalsconsolidated net income, and its beginning and ending retained earnings equal the respective con-solidated retained earnings amounts.

The first working paper entry in Exhibit E7-1 eliminates intercompany interest income andinterest expense amounts, and intercompany bond investment and bond liability amounts, and

10 ADVANCED ACCOUNTING

EXHIBIT I7-1Intercompany BondsAfter Acquisit ion—Incomplete EquityMethod

PIMA CORPORATION AND SUBSIDIARY CONSOLIDATION WORKING PAPERSFOR THE YEAR ENDED DECEMBER 31, 2005 (IN THOUSANDS)

Adjustments andEliminations

80% ConsolidatedPima Sioux Debits Credits Statements

Income StatementSales $20,000 $ 9,915 $29,915

Income from Sioux 2,400 a 10c 2,390

Interest income 85 b 85

Interest expense (100) b 75 (25)

Other expenses (14,290) (7,000) (21,290)

Minority interest expense d 600 (600)

Net income $ 8,010 $ 3,000 $ 8,000

Retained EarningsRetained earnings—Pima $ 9,950 a 50 $10,000

Retained earnings—Sioux $ 5,500 e 5,500

Net income 8,010 3,000 8,000

Dividends (6,000) (2,000) c 1,600d 400 (6,000)

Retained earnings–December 31, 2005 $11,960 $ 6,500 $12,000

Balance Sheeta 40 b 50

Investment in Sioux $13,200 c 790e 12,400

Bond investment—Pima $ 710 b 710

Other assets 36,760 17,290 $54,050

$49,960 $18,000 $54,050

10% bonds payable $ 1,000 b 750 $ 250

Other liabilities 17,000 $ 1,500 18,500

Capital stock 20,000 10,000 e 10,000 20,000

Retained earnings 11,960 6,500 12,000

$49,960 $18,000

Minority interest d 200e 3,100 3,300

$54,050

Electronic Supplement to Chapter 7 11

EXHIBIT C7-1Intercompany BondsAfter Acquisit ion—CostMethod

PIMA CORPORATION AND SUBSIDIARY CONSOLIDATION WORKING PAPERSFOR THE YEAR ENDED DECEMBER 31, 2005 (IN THOUSANDS)

Adjustments andEliminations

80% ConsolidatedPima Sioux Debits Credits Statements

Income StatementSales $20,000 $ 9,915 $29,915

Dividend income 1,600 a 1,600

Income from Sioux c 2,390 a 2,390

Interest income 85 b 85

Interest expense (100) b 75 (25)

Other expenses (14,290) (7,000) (21,290)

Minority interest expense d 600 (600)

Net income $ 7,210 $ 3,000 $ 8,000

Retained EarningsRetained earnings—Pima $ 9,550 a 450 $10,000

Retained earnings—Sioux $ 5,500 e 5,500

Net income 7,210 3,000 8,000

Dividends (6,000) (2,000) c 1,600d 400 (6,000)

Retained earnings–December 31, 2005 $10,760 $ 6,500 $12,000

Balance Sheeta 1,240 b 50

Investment in Sioux $12,000 c 790e 12,400

Bond investment—Pima $ 710 b 710

Other assets 36,760 17,290 $54,050

$48,760 $18,000 $54,050

10% bonds payable $ 1,000 b 750 $ 250

Other liabilities 17,000 $ 1,500 18,500

Capital stock 20,000 10,000 e 10,000 20,000

Retained earnings 10,760 6,500 12,000

$48,760 $18,000

Minority interest d 200e 3,100 3,300

$54,050

12 ADVANCED ACCOUNTING

credits the investment in Sioux for the $50,000 constructive gain not recognized on the separatebooks of Pima and Sioux at the beginning of the period.

a Interest income (�R, �SE) 85,000

10% bonds payable (�L) 750,000

Interest expense (�E, +SE) 75,000

Bond investment–Pima (�A) 710,000

Investment in Sioux (�A) 50,000

The second working paper entry in Exhibit E7-1 eliminates the income from Sioux and 80%of dividends paid by Sioux and returns the investment in Sioux to its beginning-of-the-periodamount.

b Income from Sioux (�R, �SE) 2,390,000

Dividends (+SE) 1,600,000

Investment in Sioux 80% (�A) 790,000

The third working paper entry recognizes minority interest expense and the minority interestshare of dividends.

c Minority interest expense (E, �SE) 600,000

Dividends (+A) 400,000

Minority interest (+L) 200,000

The last working paper entry eliminates reciprocal investment and equity amounts and entersbeginning minority interest.

d Common stock—Sioux (�SE) 10,000,000

Retained earnings–Sioux (�SE) 5,500,000

Investment in Sioux (�A) 12,400,000

Minority interest (+L) 3,100,000

CONVERSION TO EQUITY APPROACH The four working paper entries presented in Exhibit E7-1 arealso used in consolidating the financial statements of Pima and Sioux under an incomplete equitymethod (Exhibit I7-1) and the cost method (Exhibit C7-1) after entering an initial conversion toequity entry in the working papers. The working paper entry in Exhibit I7-1 to convert from anincomplete equity method to the equity method is as follows:

a Income from Sioux (�R, �SE) 10,000

Investment in Sioux 80% (+A) 40,000

Retained earnings—Pima (+SE) 50,000

This working paper entry corrects Pima’s beginning retained earnings for the $50,000 constructivegain that was not recorded under an incomplete equity method, and it adjusts income from Siouxfor the $10,000 piecemeal recognition of the constructive gain that was not charged to investmentincome under the incomplete equity method. The $40,000 debit to investment in Sioux correctsthat account for the constructive gain for 2004, less piecemeal recognition for 2005, neither ofwhich was recorded under the incomplete equity method. The other working paper entries inExhibit I7-1 are the same as those illustrated for the equity method.

The consolidation illustrated in Exhibit C7-1 assumes that Pima uses the cost method inaccounting for its investment in Sioux and that the balance of its investment in Sioux accountequals the $12 million cost at January 1, 2004. Entry a in the working papers of Exhibit C7-1 con-verts the accounts of Pima to an equity basis for working paper purposes.

A cost-to-equity conversion schedule is probably the best explanation of this working paperentry. After the conversion entry is entered in the working papers of Exhibit C7-1, the otherworking paper entries are the same as if the equity method had been used. Pima could also con-vert its separate accounts to the equity method by entering an equivalent entry before closing itsbooks for 2005. The conversion schedule is as follows (all amounts in thousands):

Electronic Supplement to Chapter 7 13

Pima’sBeginningRetained Investment IncomeEarnings in Sioux from Sioux Dividends

Prior Year’s Effect80% of $5,000,000 undistributed

income from 2004 $4,000 $ 4,000Constructive gain for 2004 500 500

Current Year’s EffectReclassify dividend income

as investment decrease (1,600) $(1,600)80% share of Sioux’s

$300,000,000 net income 2,400 $2,400Piecemeal recognition of gain

($50,000 / 5 years, or $85,000interest income � $75,000interest expense) (10) (10)

Conversion entry amounts $4,500 $ 5,290 $2,390 $(1,600)

TRADITIONAL APPROACH The financial statements of Pima and Sioux can be consolidated withoutan initial conversion to equity. Procedures under the traditional approach are shown in the next twoexhibits. Working papers for an incomplete equity method under the traditional approach are pre-sented in Exhibit TI7-1.

If Pima has accounted for its investment in Sioux using an incomplete equity method as shownin Exhibit TI7-1, the financial statements can be consolidated using the following set of workingpaper entries:

a 10% bonds payable (�L) 750,000

Bond investment—Pima (�A) 710,000

Retained earnings—Pima, January 1 (+SE) 40,000

To eliminate intercompany bond investment and bond liability amounts and correct Pima’s beginning-of-the-period retained earnings for the constructive gain.

b Interest income (�R, �SE) 85,000

Interest expense (�E, +SE) 75,000

Retained earnings (+SE) 10,000

To eliminate intercompany interest incomeand expense and adjust for piecemealrecognition of the constructive gain.

c Income from Sioux (�R, �SE) 2,400,000

Dividends (+SE) 1,600,000

Investment in Sioux (�A) 800,000

To eliminate investment income (as recorded by Pima),80% of Sioux’s dividends, and return the investment account to its beginning-of-the-period balance.

d Minority interest expense (E, �SE) 600,000

Dividends (+SE) 400,000

Minority interest (+L) 200,000

To record minority interest expense and minority share of dividends.

e Retained earnings—Sioux (�SE) 5,500,000

Capital stock—Sioux (�SE) 10,000,000

Investment in Sioux (�A) 12,400,000

Minority interest, January 1 (+L) 3,100,000

To eliminate reciprocal investment and equity amounts and enter beginning-of-the-period minority interest.

14 ADVANCED ACCOUNTING

PIMA CORPORATION AND SUBSIDIARY CONSOLIDATION WORKING PAPERSFOR THE YEAR ENDED DECEMBER 31, 2005 (IN THOUSANDS)

Adjustments andEliminations

80% ConsolidatedPima Sioux Debits Credits Statements

Income StatementSales $20,000 $ 9,915 $29,915

Income from Sioux 2,400 c 2,400

Interest income 85 b 85

Interest expense (100) b 75 (25)

Other expenses (14,290) (7,000) (21,290)

Minority interest expense d 600 (600)

Net income $ 8,010 $ 3,000 $ 8,000

Retained EarningsRetained earnings—Pima $ 9,950 a 40 $10,000

b 10

Retained earnings—Sioux $ 5,500 e 5,500

Net income 8,010 3,000 8,000

Dividends (6,000) (2,000) c 1,600d 400 (6,000)

Retained earnings–December 31, 2005 $11,960 $ 6,500 $12,000

Balance Sheetc 800

Investment in Sioux $13,200 e 12,400

Bond investment—Pima $ 710 a 710

Other assets 36,760 17,290 $54,050

$49,960 $18,000 $54,050

10% bonds payable $ 1,000 a 750 $ 250

Other liabilities 17,000 $ 1,500 18,500

Capital stock 20,000 10,000 e 10,000 20,000

Retained earnings 11,960 6,500 12,000

$49,960 $18,000

Minority interest d 200e 3,100 3,300

$54,050

EXHIBIT TI7-1Intercompany BondsAfter Acquisit ion—Incomplete EquityMethod (Tradit ionalApproach)

Electronic Supplement to Chapter 7 15

EXHIBIT TC7-1Intercompany BondsAfter Acquisit ion—CostMethod (Tradit ionalApproach)

PIMA CORPORATION AND SUBSIDIARY CONSOLIDATION WORKING PAPERSFOR THE YEAR ENDED DECEMBER 31, 2005 (IN THOUSANDS)

Adjustments andEliminations

80% ConsolidatedPima Sioux Debits Credits Statements

Income StatementSales $20,000 $9,915 $29,915

Dividend income 1,600 d 1,600

Interest income 85 c 85

Interest expense (100) c 75 (25)

Other expenses (14,290) (7,000) (21,290)

Minority interest expense e 600 (600)

Net income $ 7,210 $ 3,000 $ 8,000

Retained EarningsRetained earnings—Pima $ 9,550 a 400 $10,000

b 40c 10

Retained earnings—Sioux $ 5,500 f 5,500

Net income 7,210 3,000 8,000

Dividends (6,000) (2,000) d 1,600e 400 (6,000)

Retained earnings–December 31, 2005 $10,760 $ 6,500 $12,000

Balance SheetInvestment in Sioux $12,000 a 400 f 12,400

Bond investment—Pima $ 710 b 710

Other assets 36,760 17,290 $54,050

$48,760 $18,000 $54,050

10% bonds payable $ 1,000 b 750 $ 250

Other liabilities 17,000 $ 1,500 18,500

Capital stock 20,000 10,000 f 10,000 20,000

Retained earnings 10,760 6,500 12,000

$48,760 $18,000

Minority interest e 200f 3,100 3,300

$54,050

16 ADVANCED ACCOUNTING

Now assume that Pima has used the cost method in accounting for its investment in Sioux, andthat it consolidates the financial statements under the traditional approach without a conversion toequity. Working papers are presented in Exhibit TC7-1.

The working paper entries from Exhibit TC7-1 are reproduced for convenient reference asfollows:

a Investment in Sioux (+A) 400,000

Retained earnings—Pima, January 1 (+SE) 400,000

To take up 80% of Sioux’s increase instockholders’ equity between the date ofacquisition and the beginning of the currentperiod.

b 10% bonds payable (�L) 750,000

Bond investment—Pima (�A) 710,000

Retained earnings—Pima, January 1 (+SE) 40,000

To eliminate intercompany bond investmentand bond liability amounts and correctPima’s beginning-of-the-period retainedearnings for the constructive gain.

c Interest income (�R, �SE) 85,000

Interest expense (�E, +SE) 75,000

Retained earnings (+SE) 10,000

To eliminate intercompany interest incomeand expense and adjust for piecemealrecognition of the constructive gain.

d Dividend income (�R, �SE) 1,600,000

Dividends (+SE) 1,600,000

To eliminate dividend income and 80% ofSioux’s dividends.

e Minority interest expense (E, �SE) 600,000

Dividends (+SE) 400,000

Minority interest (+L) 200,000

To record minority interest expense andminority share of dividends.

f Retained earnings—Sioux (�SE) 5,500,000

Capital stock—Sioux (�SE) 10,000,000

Investment in Sioux (�A) 12,400,000

Minority interest, January 1 (+L) 3,100,000

To eliminate reciprocal investment and equityamounts and enter beginning-of-the-periodminority interest.

A S S I G N M E N T M A T E R I A L

W 7-1 On January 1, 2008, Pike Corporation sold $200,000 par value of 8% bonds in the bond market for$208,000. The bonds have interest payment dates of January 1 and July 1 and mature in 10 yearsfrom date of issue.

Sack Corporation, Pike’s 100% pooled subsidiary, purchased $100,000 par of Pike’s 8% bondsin the bond market for $95,000 on January 1, 2008. Both entities use straight-line amortization forbond investments and liabilities.

Comparative balance sheets for Pike and Sack corporations at December 31, 2008, are summa-rized as follows (in thousands):

Electronic Supplement to Chapter 7 17

Pike Sack

AssetsCash $ 83 $ 25Bond interest receivable — 4Other receivables 60 25Inventories 120 70Plant assets—net 250 180Investment in Sack stock 385.6 —Investment in Pike bonds — 96

Total assets $898.6 $400

EquitiesAccounts payable $ 28 $ 20Bond interest payable 8 —8% bonds payable 203.2 —Common stock $10 par 400 300Retained earnings 259.4 80

Total equities $898.6 $400

R E Q U I R E D : Prepare a consolidated balance sheet for Pike Corporation and Subsidiary at December 31,2008.

W 7-2 Comparative balance sheets for Phil Corporation and Sam Corporation at December 31, 2006, aresummarized as follows (in thousands):

Phil Sam

AssetsCash $ 25 $19.4Accounts receivable 32.2 25Inventories 30 16Plant and equipment 50 30Accumulated depreciation (10) (4)Investment in Sam stock (90%) 46 —Investment in Sam bonds 20.8 —

$194 $86.4Liabilities and EquityAccounts payable $ 25.5 $10Bonds payable (10%) — 36.4Common stock 100 30Retained earnings 68.5 10

$194 $86.4

A D D I T I O N A L I N F O R M AT I O N1. Phil acquired its 90% interest in Sam Corporation on December 31, 2003.

2. Phil uses the equity method of accounting but does not adjust for the excess of cost over book valueacquired or for intercompany profits.

3. The difference between Phil’s investment in Sam stock account and the underlying book value of Phil’sequity interest relates to undervalued plant and equipment that had an expected useful life of 10 years onJanuary 1, 2003.

4. Sam’s December 31, 2006, inventory includes $2,000 profit on goods acquired from Phil.

5. Phil acquired $20,000 par of Sam bonds on January 1, 2006. The bonds mature on December 31, 2010,and the premium is amortized by the straight-line method.

R E Q U I R E D : Prepare a consolidated balance sheet for Phil Corporation and Subsidiary at December 31,2006.

W 7-3 Pile Corporation acquired 100% of Scud Corporation’s outstanding common stock at its under-lying book value on January 1, 2004, when Scud’s equity consisted of $100,000 capital stock,$35,000 other paid-in capital, and $35,000 retained earnings. Scud’s assets and liabilities wererecorded at their fair values on this date.

18 ADVANCED ACCOUNTING

Pile uses the equity method in accounting for Scud but has made no adjustment relative to the inter-company bond holdings of Pile and Scud. Scud’s investment in Pile’s bonds consists of $50,000 parvalue of Pile’s 10% bonds that were purchased by Scud for $48,000 on January 2, 2004. These bondsmature on January 1, 2008, and have semiannual interest payment dates of July 1 and January 1. Thecombined income and retained earnings statements and balance sheets of Pile and Scud at and for theyear ended December 31, 2004, are summarized as follows (in thousands):

Pile Scud

Combined Income and Retained Earnings Statementsfor the Year Ended December 31, 2004Sales $150 $ 55Income from Scud 25 —Interest income — 5.5Cost of sales (73) (20)Depreciation expense (28) (9)Interest expense (9) —Other expenses (30) (6.5)

Net income 35 25Add: Beginning retained earnings 65 35Less: Dividends (10) (20)

Retained earnings December 31, 2004 $ 90 $ 40

Balance Sheet at December 31, 2004Cash $ 15 $ 9Accounts receivable 20 10Interest receivable — 2.5Inventories 60 10Land 70 20Plant and equipment—net 140 100Investment in Scud stock 175 —Investment in Pile bonds — 48.5

Total assets $480 $200Accounts payable $ 42 $ 25Interest payable 5 —10% bonds payable 103 —Capital stock, $10 par 200 100Other paid-in capital 40 35Retained earnings 90 40

Total equities $480 $200

R E Q U I R E D : Prepare consolidation working papers for Pile Corporation and Subsidiary for the year2004.

W 7-4 Plum Corporation purchased 90% of Star Corporation’s outstanding voting common stock at itsbook value for $207,000 cash on January 1, 2003, when Star’s stockholders’ equity consisted of$200,000 capital stock and $30,000 retained earnings. Financial statements for Plum and Star forthe year 2004 are as follows (in thousands):

Plum Star

Combined Income and Retained Earnings Statementfor the Year Ended December 31, 2004Sales $380 $210Income from Star 36 —Interest income — 12Gain on equipment 30 —Cost of sales (180) (140)Depreciation expense (58) (22)Operating expenses (78) (20)Interest expense (20) —

Net income 110 40Add: Retained earnings January 1, 2004 125 50Less: Dividends (60) (30)

Retained earnings December 31, 2004 $175 $ 60(Continued)

Electronic Supplement to Chapter 7 19

Plum Star

Balance Sheet at December 31, 2004Cash $ 49 $ 19Accounts receivable 110 60Interest receivable — 5Inventories 90 30Land 20 10Buildings—net 70 30Equipment—net 227 150Investment in Star stock 234 —Investment in Plum bonds — 96

Total assets $800 $400Accounts payable $115 $140Interest payable 10 —10% bonds payable 200 —Capital stock, $1 par 300 200Retained earnings 175 60

Total equities $800 $400

A D D I T I O N A L I N F O R M AT I O N1. Star Corporation sold inventory items to Plum for $60,000 during 2003, and one-half of this merchandise

was inventoried by Plum at year end. Star’s sales to Plum Corporation during 2004 were $90,000, andtwo-thirds of this merchandise was included in Plum’s year-end 2004 inventory. Star’s sales to Plum areat 150% of Star’s cost.

2. Star’s accounts receivable at December 31, 2004, included $30,000 due from Plum Corporation.

3. Plum Corporation sold equipment with a book value of $50,000 and a five-year remaining useful life toStar for $80,000 on July 1, 2004. This equipment remains in use by Star Corporation. Straight-line depre-ciation to the nearest month is applicable.

4. On January 1, 2004, Star Corporation paid $94,000 for $100,000 par of Plum Corporation’s five-year, 10%bonds. These bonds have interest payment dates of July 1 and January 1 and mature January 1, 2007.

5. Plum Corporation applies the equity method of accounting without considering intercompany transactions.

R E Q U I R E D : Prepare working papers to consolidate the financial statements of Plum Corporation andSubsidiary at and for the year ended December 31, 2004.

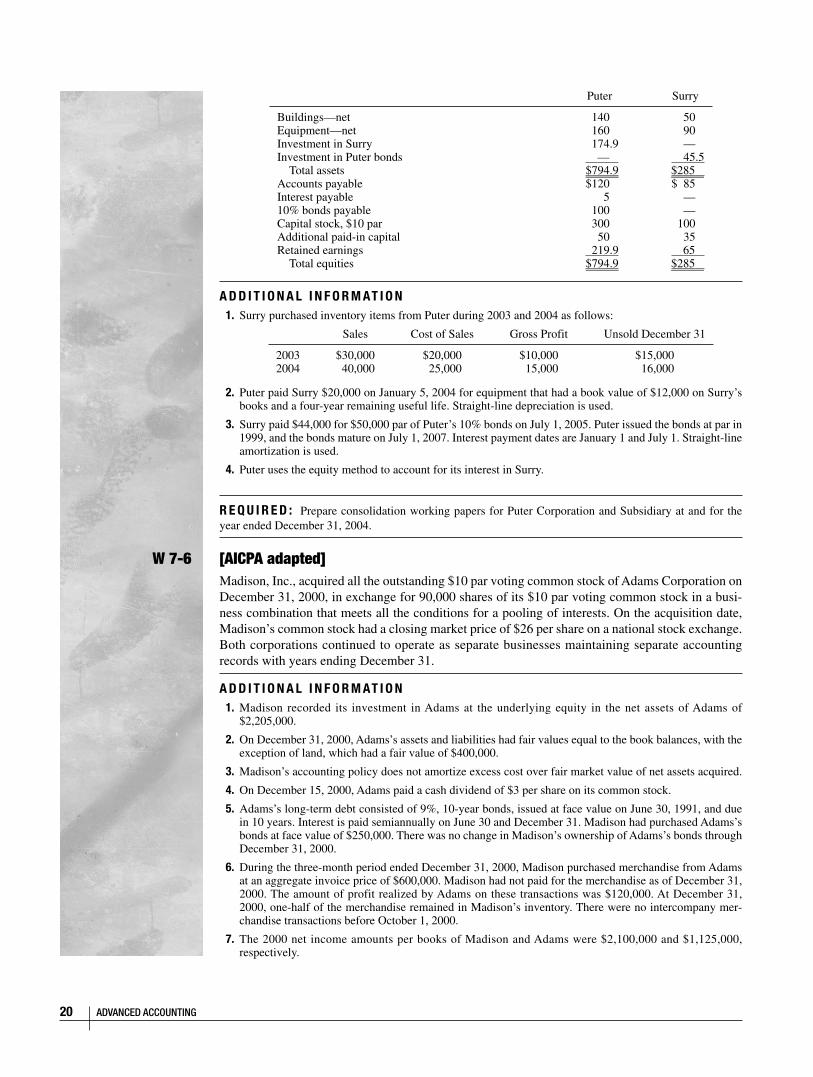

W 7-5 Puter Corporation acquired a 90% interest in Surry Corporation in 2001 in a pooling of interestsbusiness combination. The pooling was correctly recorded by Puter on the date of consummation.Financial statements for Puter and Surry Corporations at and for the year ended December 31,2004, are summarized as follows (in thousands).

Puter Surry

Combined Income and Retained Earnings Statementsfor the Year Ended December 31, 2004Sales $300 $100Income from Surry 50.3 —Interest income — 4Cost of sales (140) (45)Depreciation expense (15) (5)Operating expense (20) (4)Interest expense (10) —

Net income 165.3 50Add: Beginning retained earnings 114.6 35Deduct: Dividends (60) (20)

Retained earnings December 31, 2004 $219.9 $ 65

Balance Sheet at December 31, 2004Cash $ 90 $ 17Accounts receivable—net 110 35Interest receivable — 2.5Inventories 50 30Land 70 15

(Continued)

20 ADVANCED ACCOUNTING

Puter Surry

Buildings—net 140 50Equipment—net 160 90Investment in Surry 174.9 —Investment in Puter bonds — 45.5

Total assets $794.9 $285Accounts payable $120 $ 85Interest payable 5 —10% bonds payable 100 —Capital stock, $10 par 300 100Additional paid-in capital 50 35Retained earnings 219.9 65

Total equities $794.9 $285

A D D I T I O N A L I N F O R M AT I O N1. Surry purchased inventory items from Puter during 2003 and 2004 as follows:

Sales Cost of Sales Gross Profit Unsold December 31

2003 $30,000 $20,000 $10,000 $15,0002004 40,000 25,000 15,000 16,000

2. Puter paid Surry $20,000 on January 5, 2004 for equipment that had a book value of $12,000 on Surry’sbooks and a four-year remaining useful life. Straight-line depreciation is used.

3. Surry paid $44,000 for $50,000 par of Puter’s 10% bonds on July 1, 2005. Puter issued the bonds at par in1999, and the bonds mature on July 1, 2007. Interest payment dates are January 1 and July 1. Straight-lineamortization is used.

4. Puter uses the equity method to account for its interest in Surry.

R E Q U I R E D : Prepare consolidation working papers for Puter Corporation and Subsidiary at and for theyear ended December 31, 2004.

W 7-6 [AICPA adapted]Madison, Inc., acquired all the outstanding $10 par voting common stock of Adams Corporation onDecember 31, 2000, in exchange for 90,000 shares of its $10 par voting common stock in a busi-ness combination that meets all the conditions for a pooling of interests. On the acquisition date,Madison’s common stock had a closing market price of $26 per share on a national stock exchange.Both corporations continued to operate as separate businesses maintaining separate accountingrecords with years ending December 31.

A D D I T I O N A L I N F O R M AT I O N1. Madison recorded its investment in Adams at the underlying equity in the net assets of Adams of

$2,205,000.

2. On December 31, 2000, Adams’s assets and liabilities had fair values equal to the book balances, with theexception of land, which had a fair value of $400,000.

3. Madison’s accounting policy does not amortize excess cost over fair market value of net assets acquired.

4. On December 15, 2000, Adams paid a cash dividend of $3 per share on its common stock.

5. Adams’s long-term debt consisted of 9%, 10-year bonds, issued at face value on June 30, 1991, and duein 10 years. Interest is paid semiannually on June 30 and December 31. Madison had purchased Adams’sbonds at face value of $250,000. There was no change in Madison’s ownership of Adams’s bonds throughDecember 31, 2000.

6. During the three-month period ended December 31, 2000, Madison purchased merchandise from Adamsat an aggregate invoice price of $600,000. Madison had not paid for the merchandise as of December 31,2000. The amount of profit realized by Adams on these transactions was $120,000. At December 31,2000, one-half of the merchandise remained in Madison’s inventory. There were no intercompany mer-chandise transactions before October 1, 2000.

7. The 2000 net income amounts per books of Madison and Adams were $2,100,000 and $1,125,000,respectively.

Electronic Supplement to Chapter 7 21

8. The balances in retained earnings on December 31, 1999, were $1,600,000 and $275,000 for Madison andAdams, respectively.

On December 31, 2000, after nominal accounts were closed and immediately after acquisition, the condensedbalance sheets for both corporations were as follows:

Madison Adams

AssetsCash $ 750 $ 300Accounts receivable—net 1,950 750Inventories 2,100 950Land 500 200Depreciable assets—net 4,160 1,800Investment in Adams Corporation 2,205 —Long-term investments and other assets 785 350

Total assets $12,450 $4,350

Liabilities and Stockholders’ EquityAccounts payable and other current

liabilities $ 1,750 $ 945Long-term debt 1,500 1,200Common stock, $10 par 3,000 900Additional paid-in capital 1,370 175Retained earnings 4,830 1,130

Total liabilities and equity $12,450 $4,350

R E Q U I R E D1. Prepare consolidated balance sheet working papers for Madison and its subsidiary, Adams Corporation, as

of December 31, 2000.

2. Prepare a consolidated statement of retained earnings for the year ended December 31, 2000.