electric utilities response to climate change environmental federation of oklahoma october 2, 2008...

TRANSCRIPT

Electric Utilities Response to Climate Change

Environmental Federation of Oklahoma

October 2, 2008

Michael MillerDirector, EnvironmentElectric Power Research Institute

2© 2007 Electric Power Research Institute, Inc. All rights reserved.

About EPRI

• Founded in 1973 as an independent, nonprofit center for public interest energy and environmental research.

• Objective, tax-exempt, collaborative electricity research organization

• Science and technology focus--development, integration, demonstration and applications

• Broad technology portfolio ranging from near-term solutions to long-term strategic research

Together…Shaping the Future of Electricity

3© 2007 Electric Power Research Institute, Inc. All rights reserved.

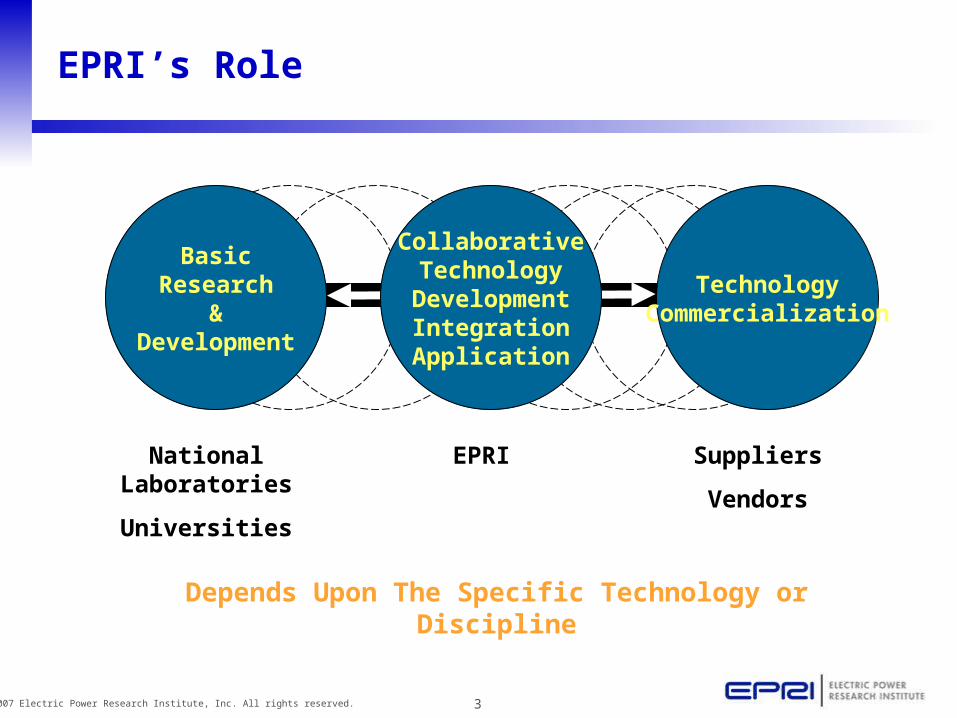

EPRI’s Role

Depends Upon The Specific Technology or Discipline

National Laboratories

Universities

Suppliers

Vendors

EPRI

BasicResearch

&Development

TechnologyCommercialization

CollaborativeTechnology

DevelopmentIntegrationApplication

4© 2007 Electric Power Research Institute, Inc. All rights reserved.

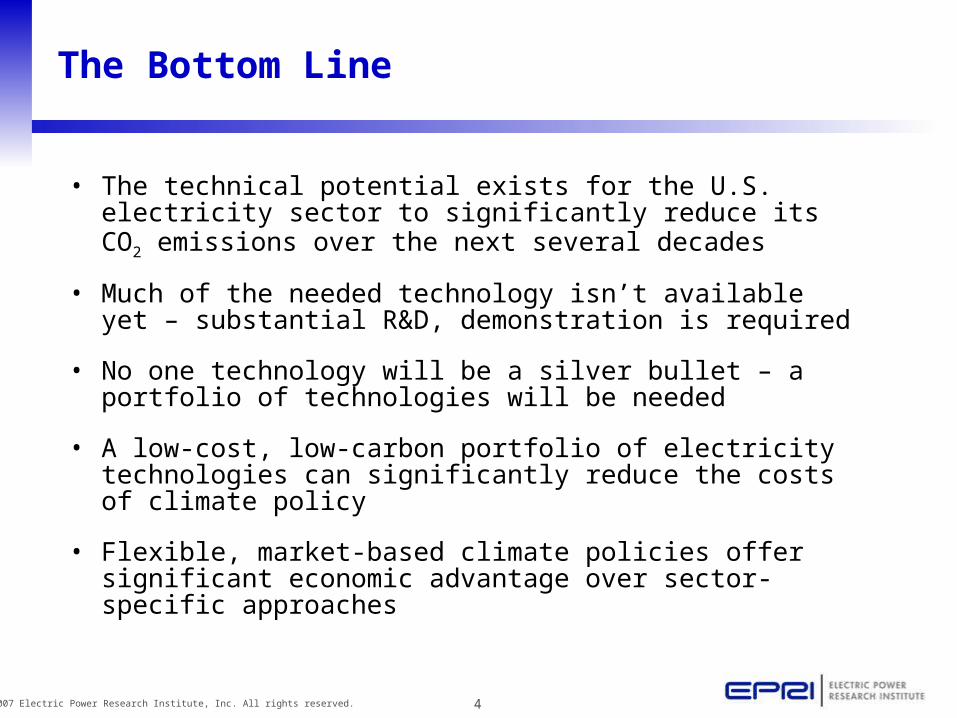

The Bottom Line

• The technical potential exists for the U.S. electricity sector to significantly reduce its CO2 emissions over the next several decades

• Much of the needed technology isn’t available yet – substantial R&D, demonstration is required

• No one technology will be a silver bullet – a portfolio of technologies will be needed

• A low-cost, low-carbon portfolio of electricity technologies can significantly reduce the costs of climate policy

• Flexible, market-based climate policies offer significant economic advantage over sector-specific approaches

5© 2007 Electric Power Research Institute, Inc. All rights reserved.

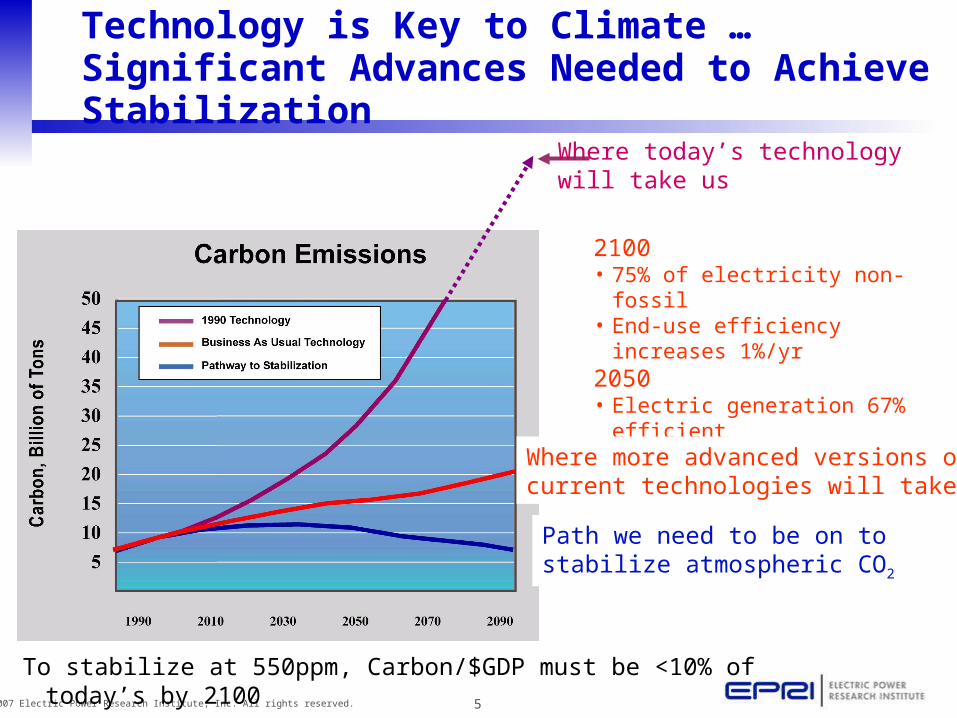

2100• 75% of electricity non-fossil• End-use efficiency increases 1%/yr2050• Electric generation 67% efficient• Passenger vehicles average 50mpg

Stabilization pathway

Technology is Key to Climate … Significant Advances Needed to Achieve Stabilization

To stabilize at 550ppm, Carbon/$GDP must be <10% of today’s by 2100

1300 GT C

480 GT C

Path we need to be on tostabilize atmospheric CO2

Where more advanced versions ofcurrent technologies will take us

Where today’s technologywill take us

6© 2008 Electric Power Research Institute, Inc. All rights reserved.

With accelerated electricity R&D, how quickly can the U.S. electric sector cut

its future CO2 emissions?

7© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2

Em

issi

on

s (m

illio

n m

etri

c to

ns)

U.S. Electricity Sector CO2 Emissions

• Base case from EIA “Annual Energy Outlook 2007”

– includes some efficiency, new renewables, new nuclear

– assumes no CO2 capture or storage due to high costs

Using EPRI deployment assumptions, calculate change in CO2 relative to EIA base case

8© 2007 Electric Power Research Institute, Inc. All rights reserved.

Technology Deployment Targets

Technology EIA 2007 Base Case EPRI Analysis Target*

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades

40% New Plant Efficiencyby 2020–2030

150 GWe Plant Upgrades

46% New Plant Efficiency by 2020; 49% in 2030

Carbon Capture and Storage (CCS)

NoneWidely Available and Deployed

After 2020

Plug-in Hybrid Electric Vehicles (PHEV)

None10% of New Vehicle Sales by

2017; +2%/yr Thereafter

Distributed Energy Resources (DER) (including distributed solar)

< 0.1% of Base Load in 2030 5% of Base Load in 2030

EPRI analysis targets do not reflect economic considerations, or potential regulatory and siting constraints.

9© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

EIA Base Case 2007

9% reduction in base load by 2030

Benefit of Achieving Efficiency Target

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades

40% New Plant Efficiency by 2020–2030

150 GWe Plant Upgrades

46% New Plant Efficiency by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

10© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. E

lec

tric

Se

cto

rC

O2

Em

iss

ion

s (

mil

lio

n m

etr

ic t

on

s) EIA Base Case 2007

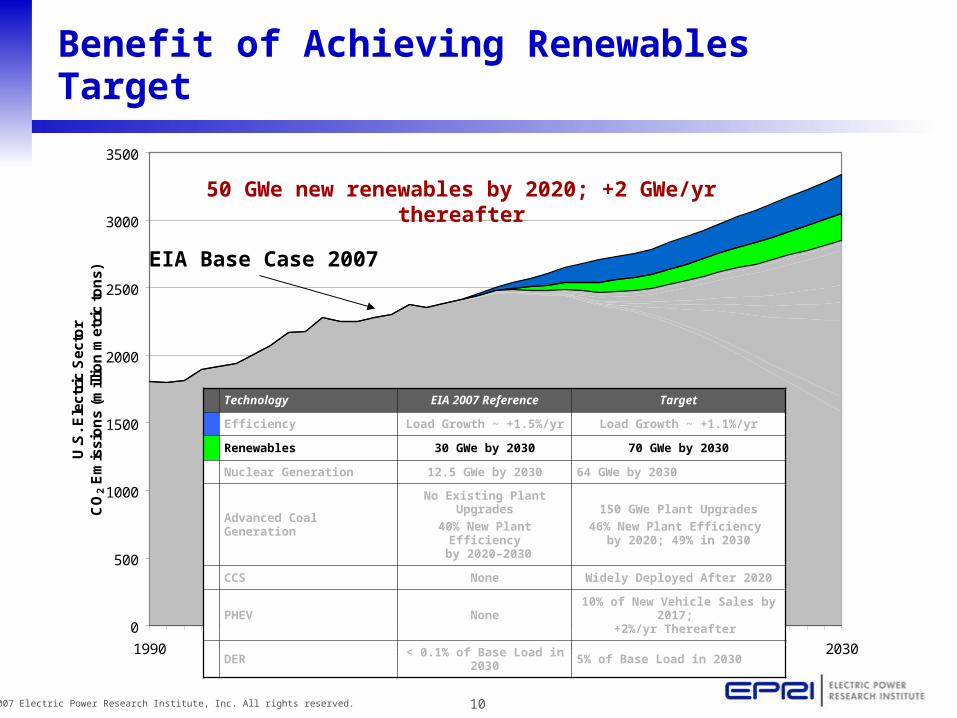

Benefit of Achieving Renewables Target

50 GWe new renewables by 2020; +2 GWe/yr thereafter

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades

40% New Plant Efficiency by 2020–2030

150 GWe Plant Upgrades

46% New Plant Efficiency by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

11© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

EIA Base Case 2007

Benefit of Achieving Nuclear Generation Target

24 GWe new nuclear by 2020; +4 GWe/yr thereafter

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades

40% New Plant Efficiency by 2020–2030

150 GWe Plant Upgrades

46% New Plant Efficiency by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

12© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

EIA Base Case 2007

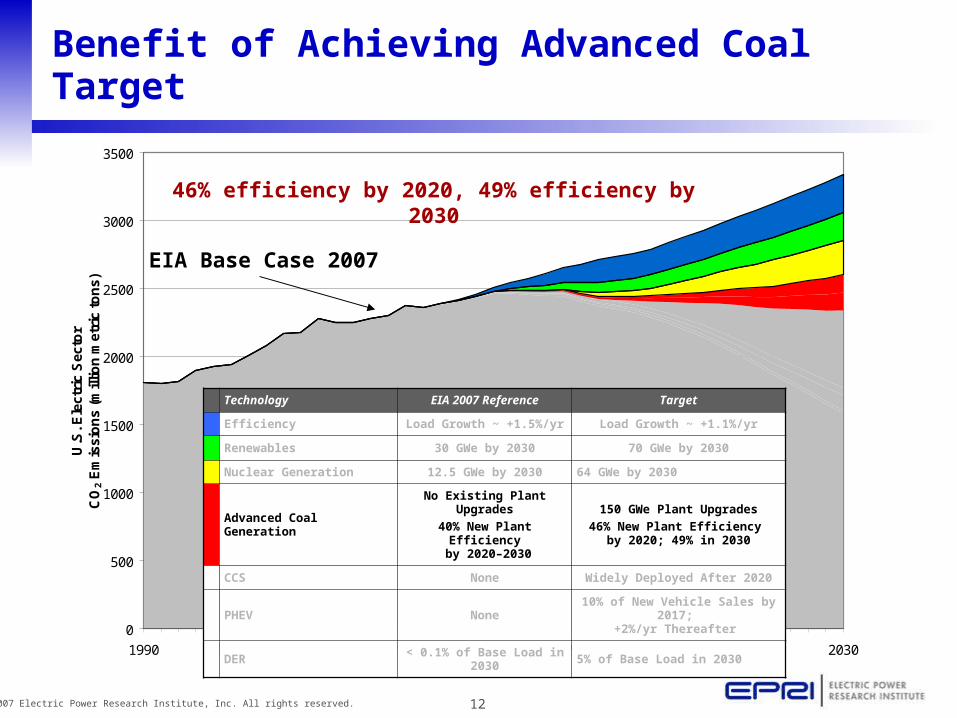

Benefit of Achieving Advanced Coal Target

46% efficiency by 2020, 49% efficiency by 2030

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades

40% New Plant Efficiency by 2020–2030

150 GWe Plant Upgrades

46% New Plant Efficiency by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

13© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

EIA Base Case 2007

Benefit of Achieving CCS Target

After 2020, all new coal plants capture and store 90% of their CO2 emissions

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades

40% New Plant Efficiency by 2020–2030

150 GWe Plant Upgrades

46% New Plant Efficiency by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

14© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

EIA Base Case 2007

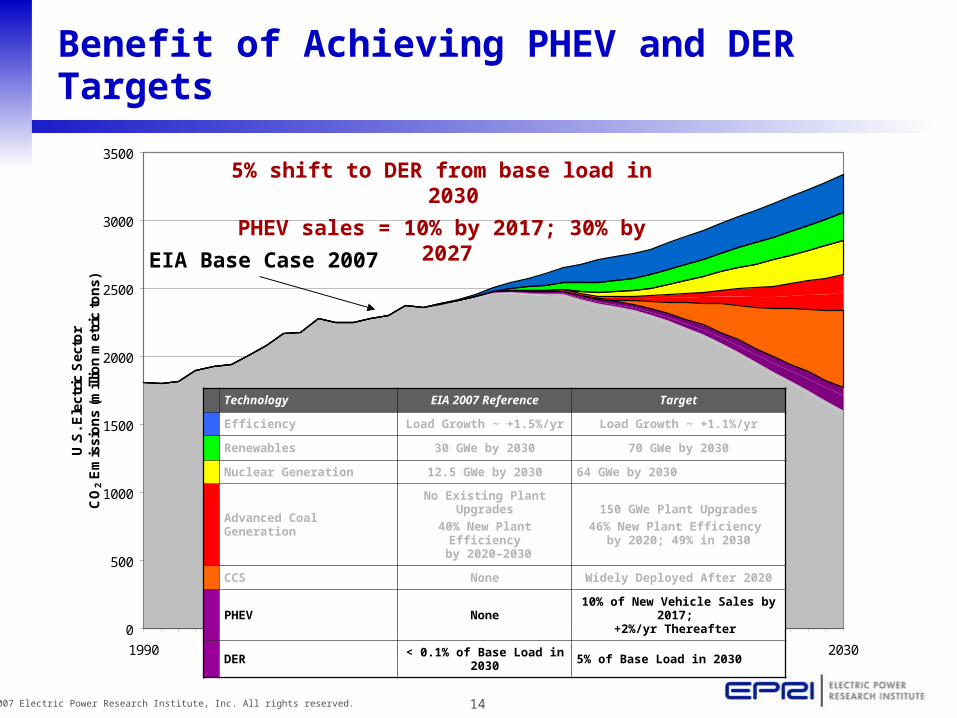

Benefit of Achieving PHEV and DER Targets

5% shift to DER from base load in 2030

PHEV sales = 10% by 2017; 30% by 2027

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades

40% New Plant Efficiency by 2020–2030

150 GWe Plant Upgrades

46% New Plant Efficiency by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

15© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

EIA Base Case 2007

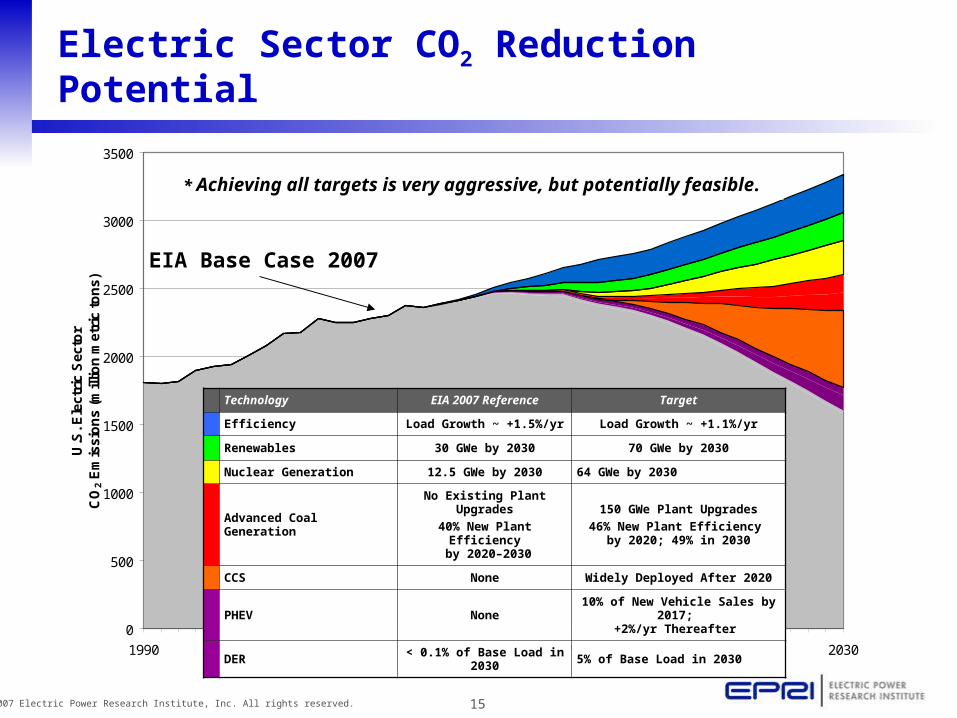

Electric Sector CO2 Reduction Potential

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades

40% New Plant Efficiency by 2020–2030

150 GWe Plant Upgrades

46% New Plant Efficiency by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None10% of New Vehicle Sales by 2017;

+2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

* Achieving all targets is very aggressive, but potentially feasible.

16© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

Technology EIA 2008 Reference Target

Efficiency Load Growth ~ +1.05%/yr Load Growth ~ +0.75%/yr

Renewables 55 GWe by 2030 100 GWe by 2030

Nuclear Generation 15 GWe by 2030 64 GWe by 2030

Advanced Coal Generation

No Heat Rate Improvement for Existing Plants

40% New Plant Efficiency by 2020–2030

1-3% Heat Rate Improvement for 130 GWe Existing Plants

46% New Plant Efficiency by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None10% of New Light-Duty Vehicle Sales

by 2017; 33% by 2030

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

Achieving all targets is very aggressive, but potentially feasible

AEO2007*

AEO2008*

AEO2008*

*Energy Information Administration (EIA) Annual Energy Outlook (AEO)

Impact of efficiency measures in Energy Independence and Security Act of 2007 (EISA2007)

Updated EPRI “Prism” for 2008

17© 2008 Electric Power Research Institute, Inc. All rights reserved.

What advanced electricity technologies will be needed in a carbon-constrained

world?

18© 2007 Electric Power Research Institute, Inc. All rights reserved.

Key Technology Challenges

• Expanded Advanced Light Water Reactor Deployment

• Enabling Efficiency, PHEVs, DER via the Smart Distribution Grid

• Enabling Intermittent Renewables via Advanced Transmission Grids

• Advanced Coal Plants with CO2 Capture and Storage

19© 2007 Electric Power Research Institute, Inc. All rights reserved.

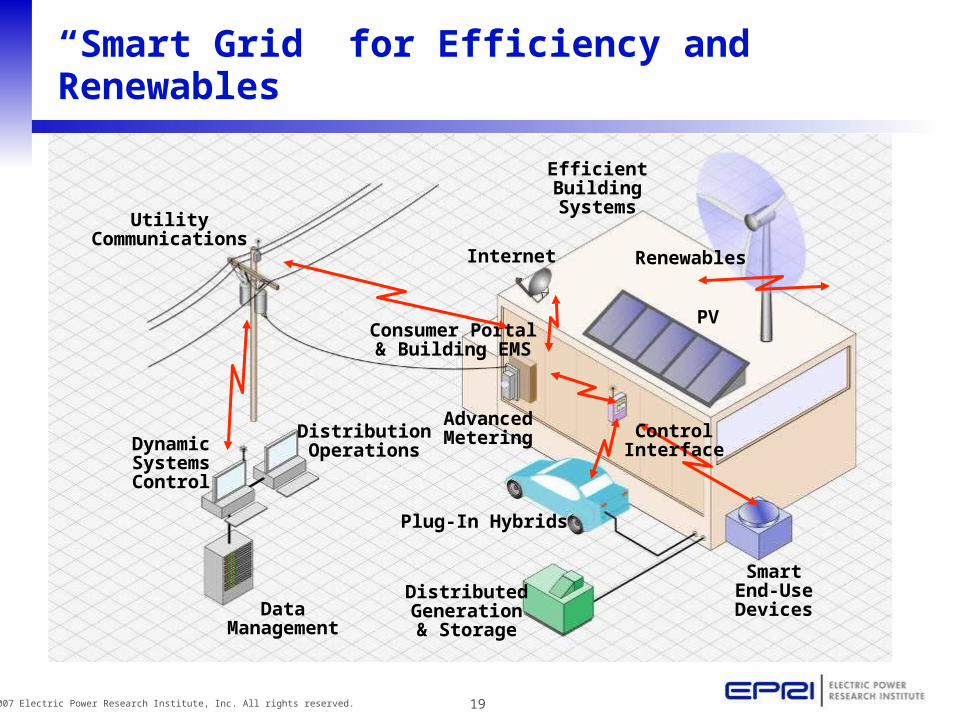

EfficientBuildingSystems

UtilityCommunications

DynamicSystemsControl

DataManagement

DistributionOperations

DistributedGeneration& Storage

Plug-In Hybrids

SmartEnd-UseDevices

AdvancedMetering

Consumer Portal& Building EMS

Internet Renewables

PV

“Smart Grid” for Efficiency and Renewables

ControlInterface

20© 2007 Electric Power Research Institute, Inc. All rights reserved.

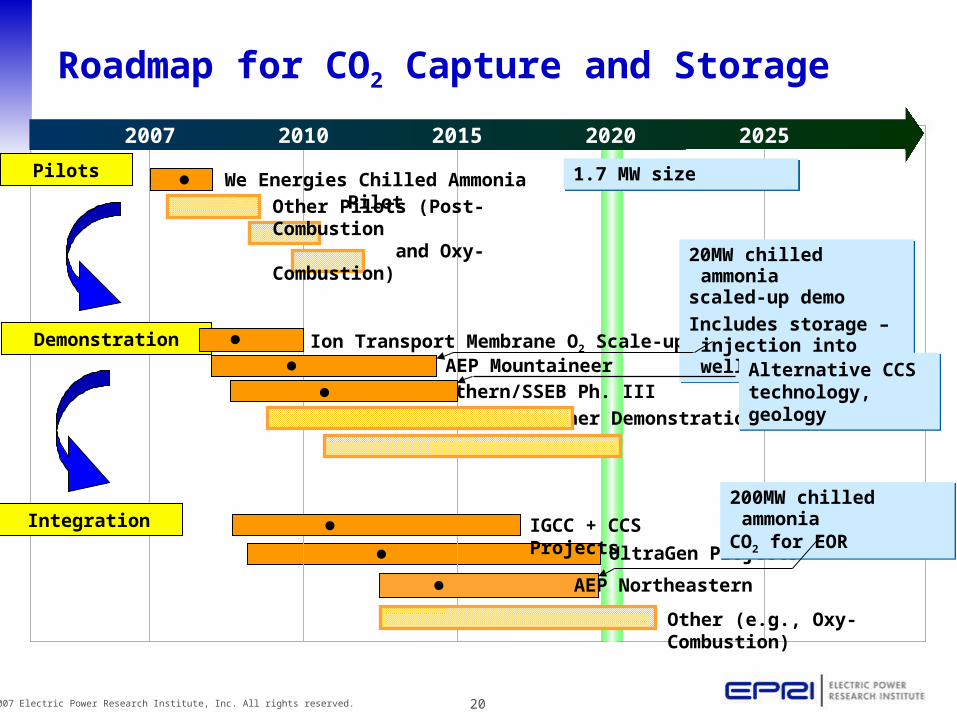

2005 2010 2015 20202007 2010 2015 20252020

We Energies Chilled Ammonia Pilot

Other Pilots (Post-Combustion and Oxy-Combustion)

●Pilots

Demonstration

Integration

Other Demonstrations

AEP MountaineerSouthern/SSEB Ph. III

●●

UltraGen Projects

Other (e.g., Oxy-Combustion)

●IGCC + CCS Projects●

Ion Transport Membrane O2 Scale-up●

AEP Northeastern●

20MW chilled ammoniascaled-up demo

Includes storage – injection into wells

20MW chilled ammoniascaled-up demo

Includes storage – injection into wells

Alternative CCS technology, geologyAlternative CCS technology, geology

200MW chilled ammonia

CO2 for EOR

200MW chilled ammonia

CO2 for EOR

1.7 MW size1.7 MW size

Roadmap for CO2 Capture and Storage

21© 2007 Electric Power Research Institute, Inc. All rights reserved.

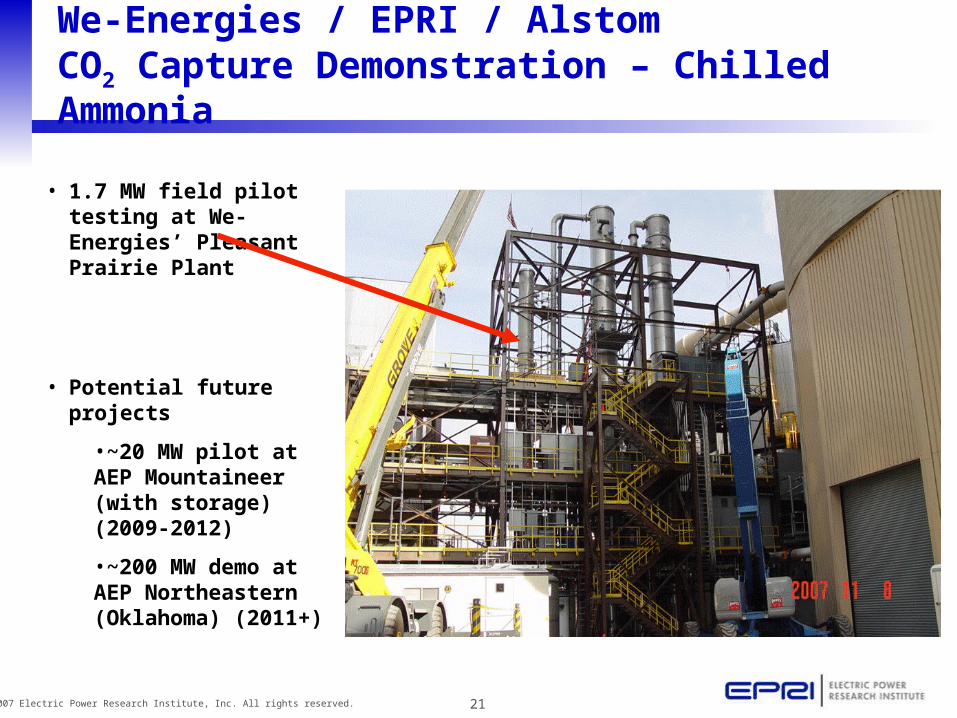

We-Energies / EPRI / Alstom CO2 Capture Demonstration – Chilled Ammonia

• 1.7 MW field pilot testing at We-Energies’ Pleasant Prairie Plant

• Potential future projects

•~20 MW pilot at AEP Mountaineer (with storage) (2009-2012)

•~200 MW demo at AEP Northeastern (Oklahoma) (2011+)

22© 2007 Electric Power Research Institute, Inc. All rights reserved.

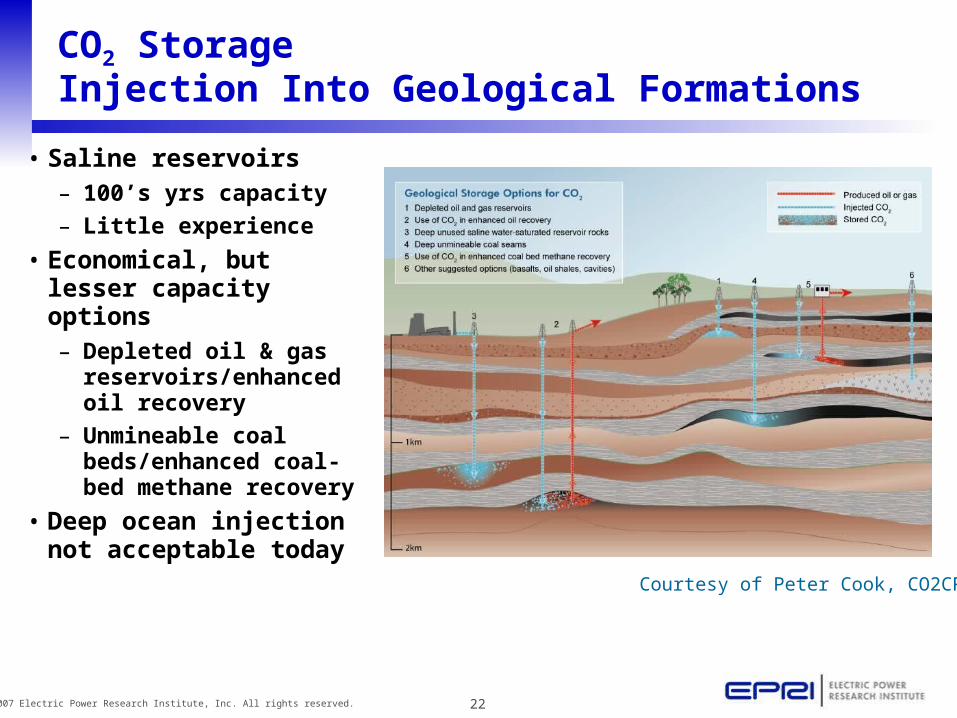

CO2 Storage Injection Into Geological Formations

• Saline reservoirs– 100’s yrs capacity

– Little experience

• Economical, but lesser capacity options– Depleted oil & gas

reservoirs/enhanced oil recovery

– Unmineable coal beds/enhanced coal-bed methane recovery

• Deep ocean injection not acceptable today

Courtesy of Peter Cook, CO2CRC

23© 2007 Electric Power Research Institute, Inc. All rights reserved.

Moving from Analysis to Action

Creating the Electricity Network of the Future

24© 2007 Electric Power Research Institute, Inc. All rights reserved.

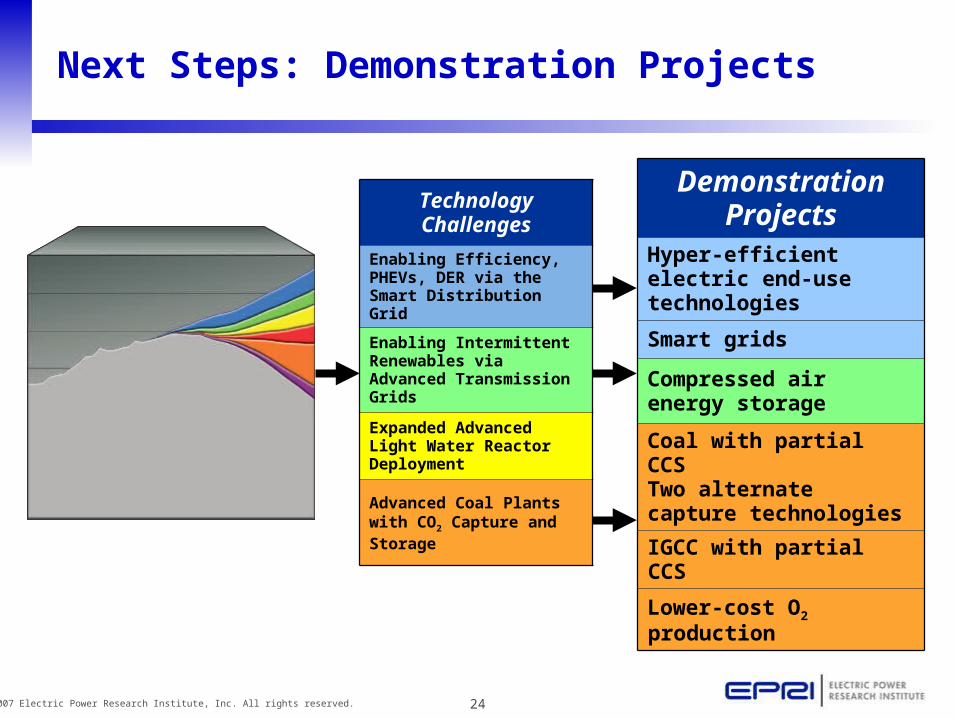

Demonstration Projects

Hyper-efficient electric end-use technologies

Smart grids

Compressed air energy storage

Coal with partial CCSTwo alternate capture technologies

IGCC with partial CCS

Lower-cost O2 production

Technology Challenges

Enabling Efficiency, PHEVs, DER via the Smart Distribution Grid

Enabling Intermittent Renewables via Advanced Transmission Grids

Expanded Advanced Light Water Reactor Deployment

Advanced Coal Plants with CO2 Capture and Storage

Next Steps: Demonstration Projects

25© 2007 Electric Power Research Institute, Inc. All rights reserved.

What is the potential value of these advanced electricity technologies to

the U.S. economy and to consumers?

26© 2007 Electric Power Research Institute, Inc. All rights reserved.

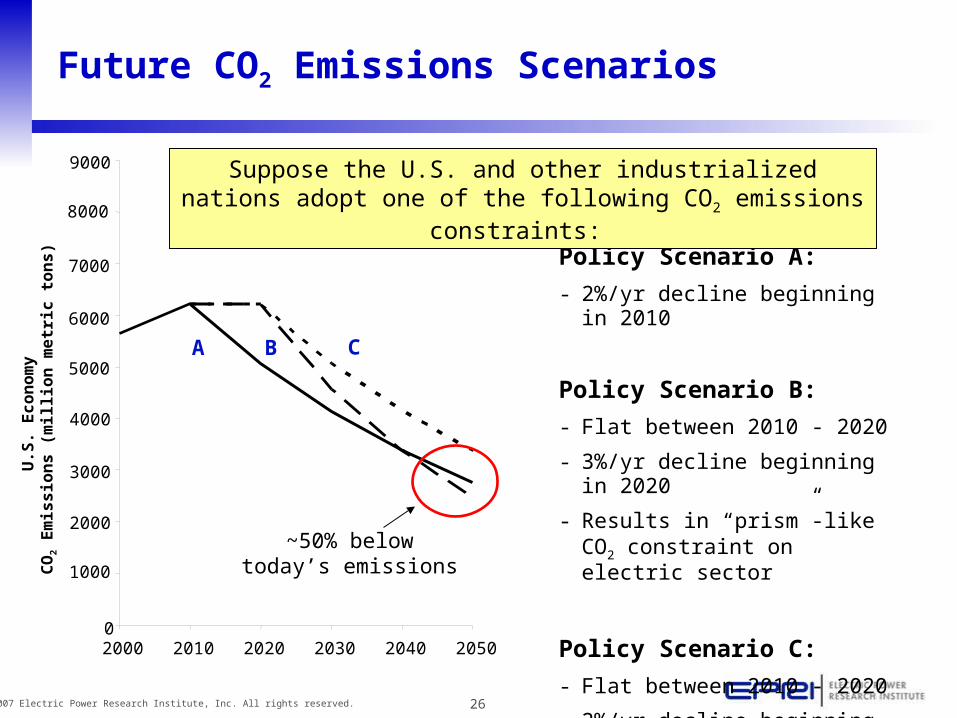

Future CO2 Emissions Scenarios

A CB

Policy Scenario A:

- 2%/yr decline beginning in 2010

Policy Scenario B:

- Flat between 2010 - 2020

- 3%/yr decline beginning in 2020

- Results in “prism”-like CO2 constraint on electric sector

Policy Scenario C:

- Flat between 2010 - 2020

- 2%/yr decline beginning in 2020

Suppose the U.S. and other industrialized nations adopt one of the following CO2 emissions constraints:

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2000 2010 2020 2030 2040 2050

U.S

. E

co

no

my

C

O2

Em

iss

ion

s (

mil

lio

n m

etr

ic t

on

s)

~50% belowtoday’s emissions

27© 2007 Electric Power Research Institute, Inc. All rights reserved.

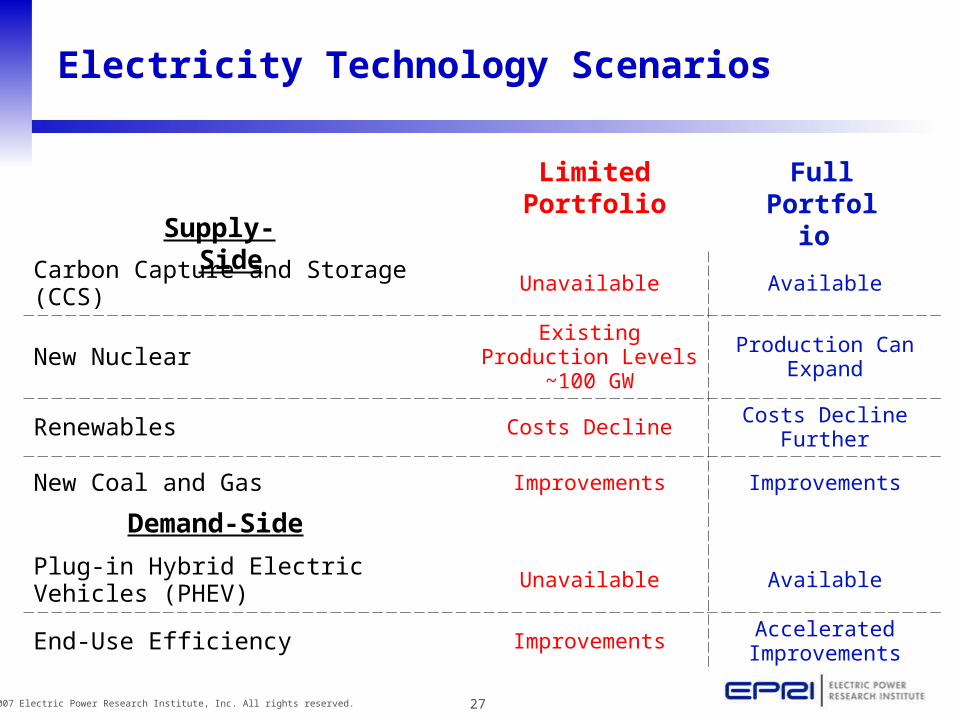

Electricity Technology Scenarios

Supply-Side

Carbon Capture and Storage (CCS) Unavailable Available

New Nuclear Existing Production Levels ~100 GW

Production Can Expand

Renewables Costs Decline Costs Decline Further

New Coal and Gas Improvements Improvements

Plug-in Hybrid Electric Vehicles (PHEV) Unavailable Available

End-Use Efficiency ImprovementsAccelerated

Improvements

Demand-Side

Limited Portfolio

Full Portfolio

28© 2007 Electric Power Research Institute, Inc. All rights reserved.

Policy Scenario B

Full Portfolio

8

7

6

5

4

3

2

1

02000 2010 2020 2030 2040 2050

Tri

llio

n k

Wh

per

Ye

ar

8

7

6

5

4

3

2

1

02000 2010 2020 2030 2040 2050

Tri

llio

n k

Wh

per

Ye

ar

Limited Portfolio

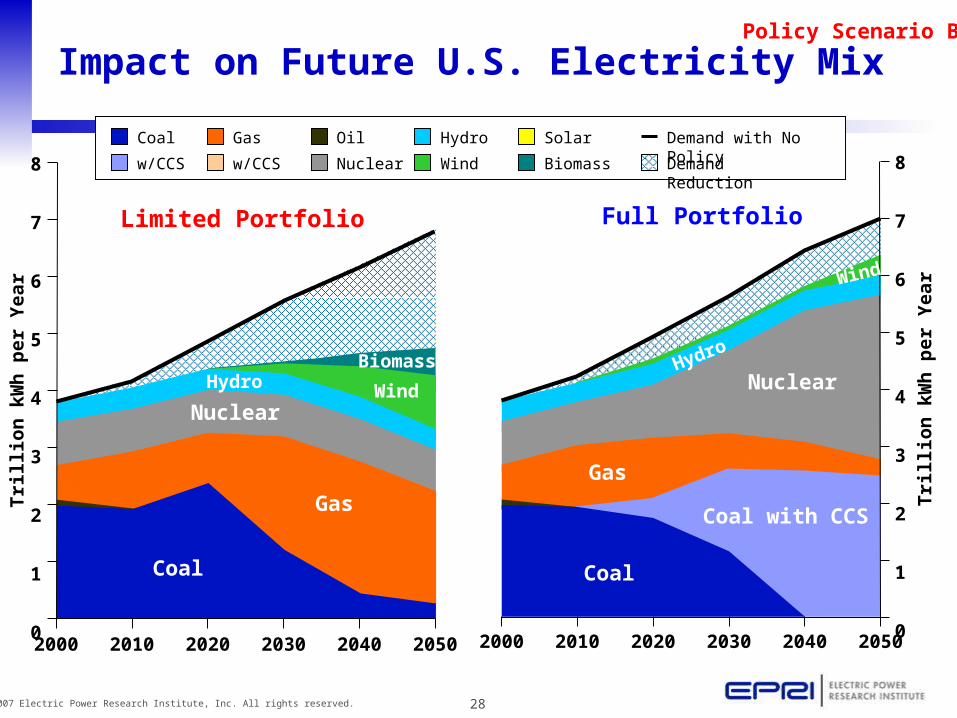

Impact on Future U.S. Electricity Mix

Coal

w/CCS

Gas

w/CCS Nuclear

Hydro

Wind

SolarOil

Demand Reduction

Demand with No Policy

Biomass

Coal Coal

Coal with CCSGas

Gas

Nuclear

NuclearHydro

Hydro Wind

Biomass

Wind

29© 2007 Electric Power Research Institute, Inc. All rights reserved.

Policy Scenario B

U.S. Electric Generation in 2030

Limited Portfolio

Total: 4,500 TWh

Full Portfolio

Total: 5,125 TWh

27%

43%

17%

22%

12%

28%

30%

13% 8%

Coal

w/CCS

Gas

w/CCS

Hydro

Other Renewables

30© 2007 Electric Power Research Institute, Inc. All rights reserved.

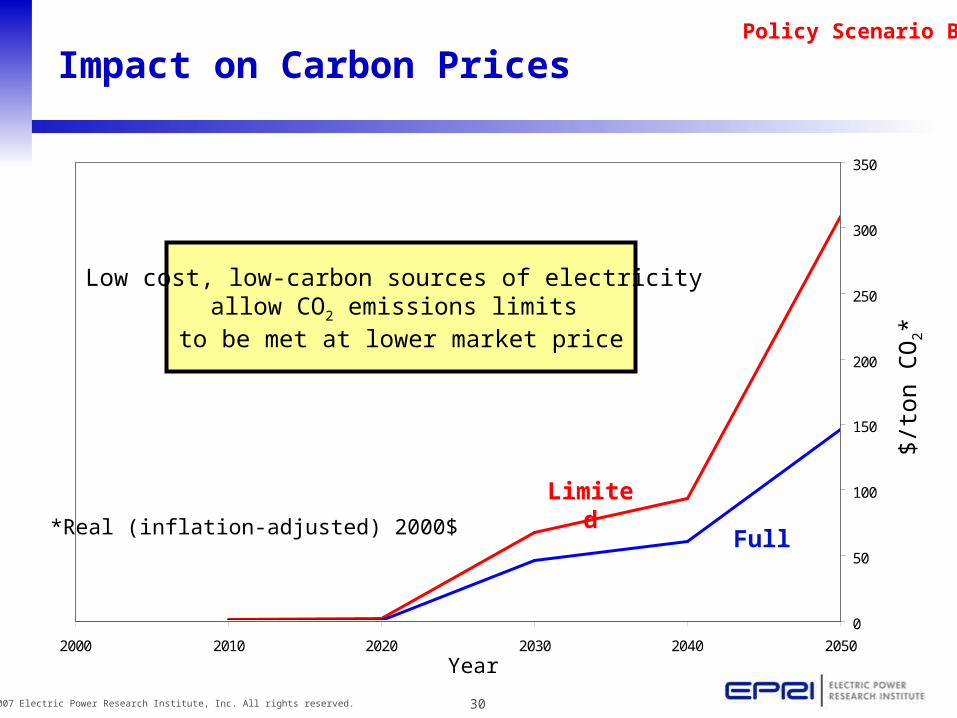

Policy Scenario B

2000 2010 2020 2030 2040 2050

0

50

100

150

200

250

300

350

Full

Limited

$/to

n C

O2*

*Real (inflation-adjusted) 2000$

Impact on Carbon Prices

Year

Low cost, low-carbon sources of electricity allow CO2 emissions limits

to be met at lower market price

31© 2007 Electric Power Research Institute, Inc. All rights reserved.

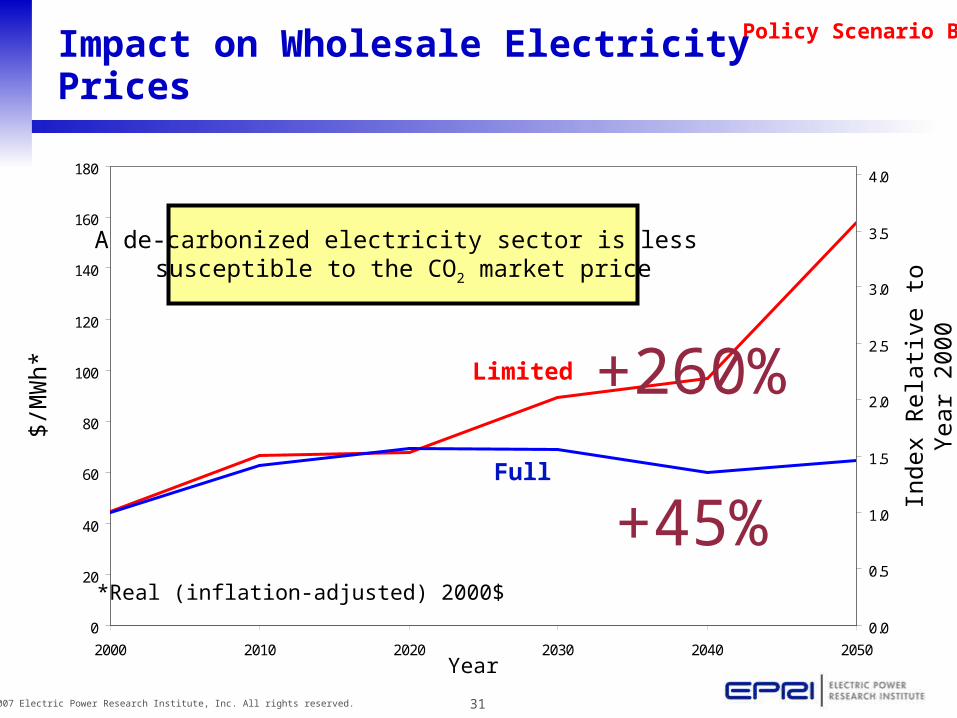

Policy Scenario B

0

20

40

60

80

100

120

140

160

180

2000 2010 2020 2030 2040 2050

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Impact on Wholesale Electricity Prices

Full

Limited

$/M

Wh*

Inde

x R

elat

ive

to Y

ear

2000

*Real (inflation-adjusted) 2000$

Year

A de-carbonized electricity sector is less susceptible to the CO2 market price

+260%

+45%

32© 2007 Electric Power Research Institute, Inc. All rights reserved.

Policy Scenario B

Impact on Natural Gas Markets

0

5

10

15

20

25

30

2000 2010 2020 2030 2040 2050 2000 2010 2020 2030 2040 2050

Nat

ura

l G

as C

on

sum

pti

on

(T

CF

)

0

2

4

6

8

10

12

14

Nat

ura

l G

as W

ellh

ead

Pri

ce (

$/M

CF

)

Non-Electric Sector

Electric Sector

Price

Limited Portfolio Full Portfolio

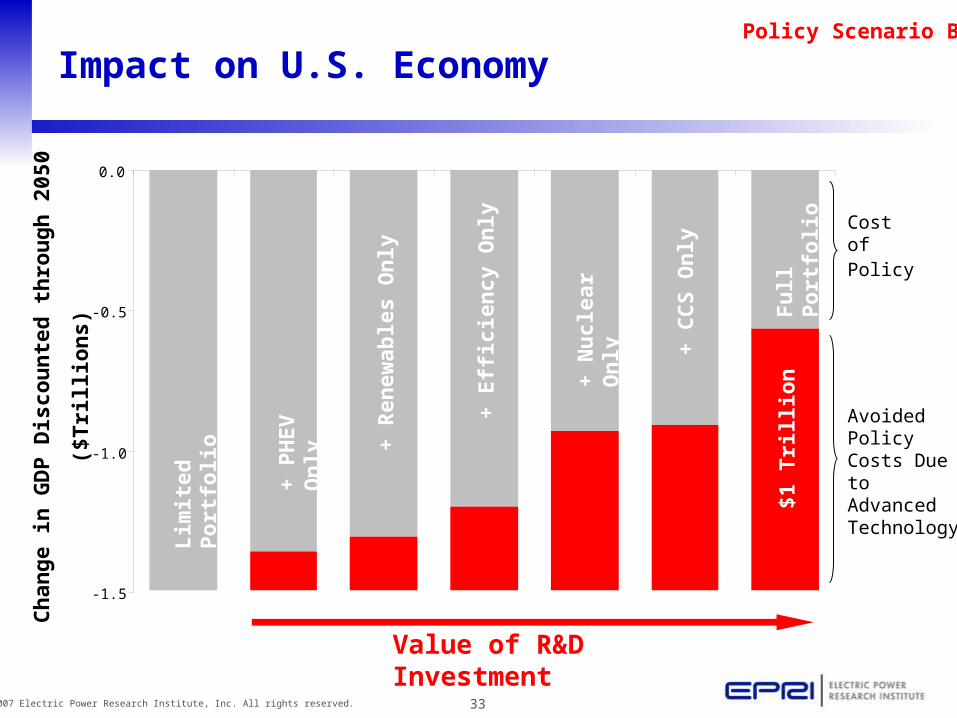

33© 2007 Electric Power Research Institute, Inc. All rights reserved.

Policy Scenario B

-1.5

-1.0

-0.5

0.0

Impact on U.S. EconomyC

han

ge

in G

DP

Dis

cou

nte

d t

hro

ug

h 2

050

($T

rilli

on

s)

Avoided Policy Costs Due to Advanced Technology

Cost of Policy

Fu

ll P

ort

folio

Lim

ited

Po

rtfo

lio

+ P

HE

V O

nly

+ R

enew

able

s O

nly

+ E

ffic

ien

cy O

nly

+ N

ucl

ear

On

ly

+ C

CS

On

ly

Value of R&D Investment

$1 T

rilli

on

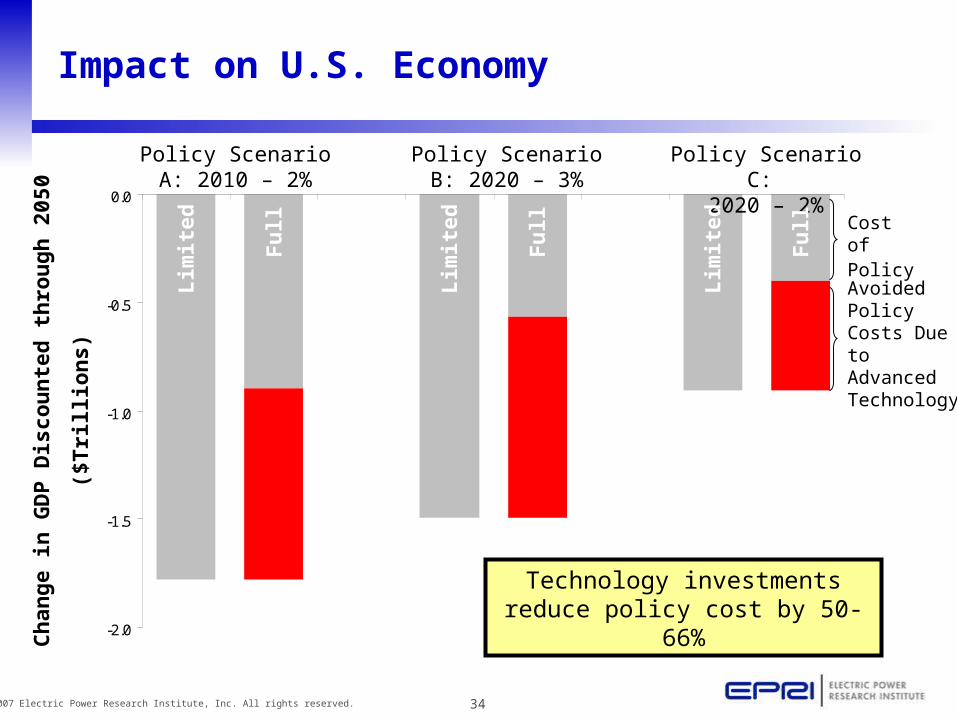

34© 2007 Electric Power Research Institute, Inc. All rights reserved.

-2.0

-1.5

-1.0

-0.5

0.0

Impact on U.S. EconomyC

han

ge

in G

DP

Dis

cou

nte

d t

hro

ug

h 2

050

($T

rilli

on

s)

Policy Scenario A: 2010 – 2%

Policy Scenario C: 2020 – 2%

Policy Scenario B: 2020 – 3%

Cost of Policy

Technology investments reduce policy cost by 50-66%

Fu

ll

Lim

ited

Fu

ll

Lim

ited

Fu

ll

Lim

ited

Avoided Policy Costs Due to Advanced Technology

35© 2007 Electric Power Research Institute, Inc. All rights reserved.

The Bottom Line (Again)

• The technical potential exists for the U.S. electricity sector to significantly reduce its CO2 emissions over the next several decades

• Much of the needed technology isn’t available yet – substantial R&D, demonstration is required

• No one technology will be a silver bullet – a portfolio of technologies will be needed

• A low-cost, low-carbon portfolio of electricity technologies can significantly reduce the costs of climate policy

• Flexible, market-based climate policies offer significant economic advantage over sector-specific approaches