electric the energy utility system: where has it been & where is it going?

TRANSCRIPT

The Energy Utility System:Where Has It Been and Where Is It Going?

Pamela Morgan

Graceful Systems LLC

October 9, 2014

2

The energy utility system today

WHEREis everything

going????

© 2014 Pamela Morgan

3

WHEREhas everything

been????

The road to what we(participants in the energy utility system)

experience today

© 2014 Pamela Morgan

4

Shared beliefs, expressed in norms, practices, decisions, regulations, and statutes, have a profound effect on the outcomes of the energy utility system. These beliefs form over time and, thus, it is useful to look back to see where we’ve been even as we speculate about where we are going.

A tiny bit of systems thinking

© 2014 Pamela Morgan

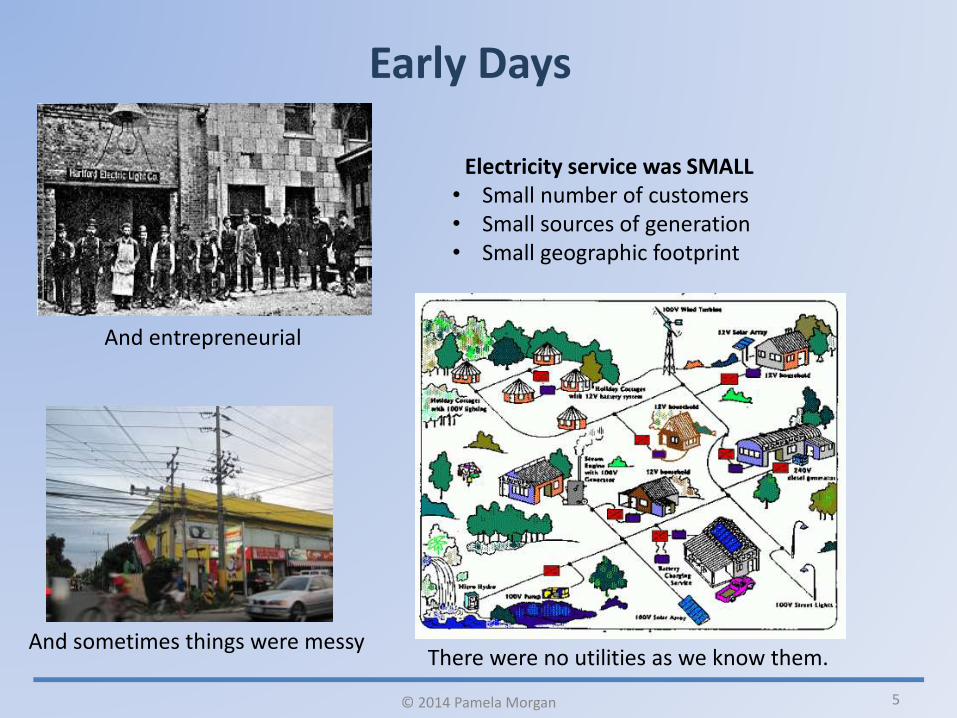

Early Days

5

Electricity service was SMALL• Small number of customers• Small sources of generation• Small geographic footprint

And sometimes things were messyThere were no utilities as we know them.

And entrepreneurial

© 2014 Pamela Morgan

Early Days

6

CITIES were in charge• Granted non-exclusive

franchises and rights of way

• Set rates• Dealt in graft and

corruption . . .

Then STATES took over• Insull’s “Blue Ribbon” panel

Obligation and exclusive right to serve

Rates set by independent state regulator to allow fair return on investment

• A popular solution Wisconsin and New York first

to adopt in 1907 Within 7 years, 43 states had

adopted

Beliefs formed:• Competition, particularly in distribution, is bad• Monopoly makes sense within a service territory• Cost of service regulation works

© 2014 Pamela Morgan

7

The 1920’s Got BIGGER:• More customers (prices dropped, uses

rose)• Larger generating stations (costs

dropped) • Greater areas covered with transmission

and distribution (costs dropped)• Larger, and more complex, organizations

Electric Utility

Holding Company

Stock Certificate

Beliefs formed:• Economies of scale are great• Electricity is more necessary than dangerous

Utilities, as we know them, came into being and . . .

© 2014 Pamela Morgan

8

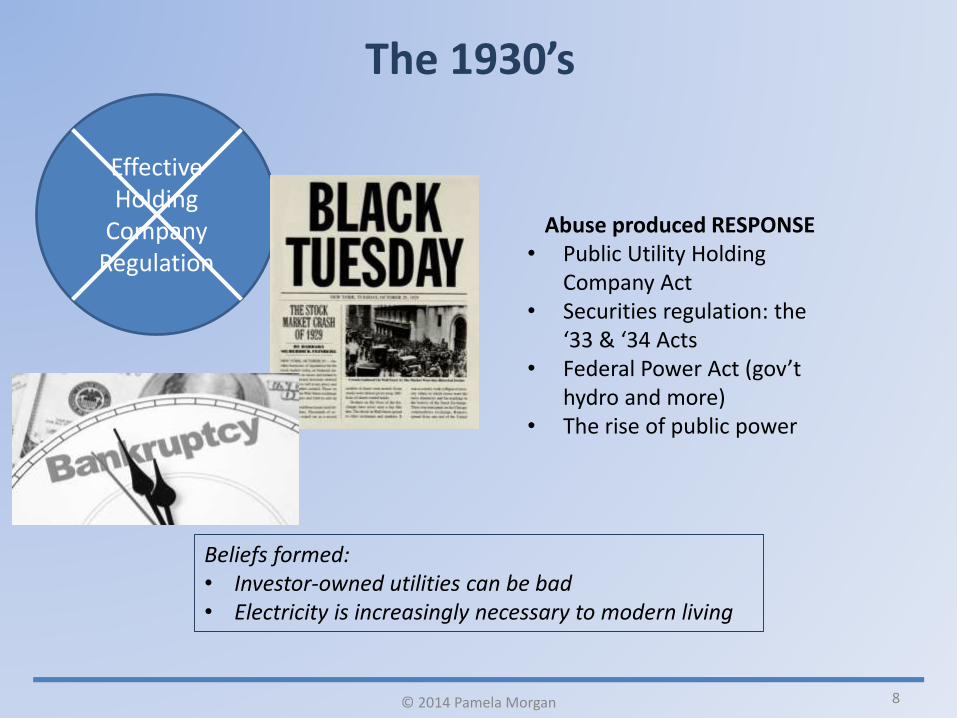

Effective Holding

Company Regulation

Abuse produced RESPONSE• Public Utility Holding

Company Act• Securities regulation: the

‘33 & ‘34 Acts• Federal Power Act (gov’t

hydro and more)• The rise of public power

The 1930’s

Beliefs formed:• Investor-owned utilities can be bad• Electricity is increasingly necessary to modern living

© 2014 Pamela Morgan

9

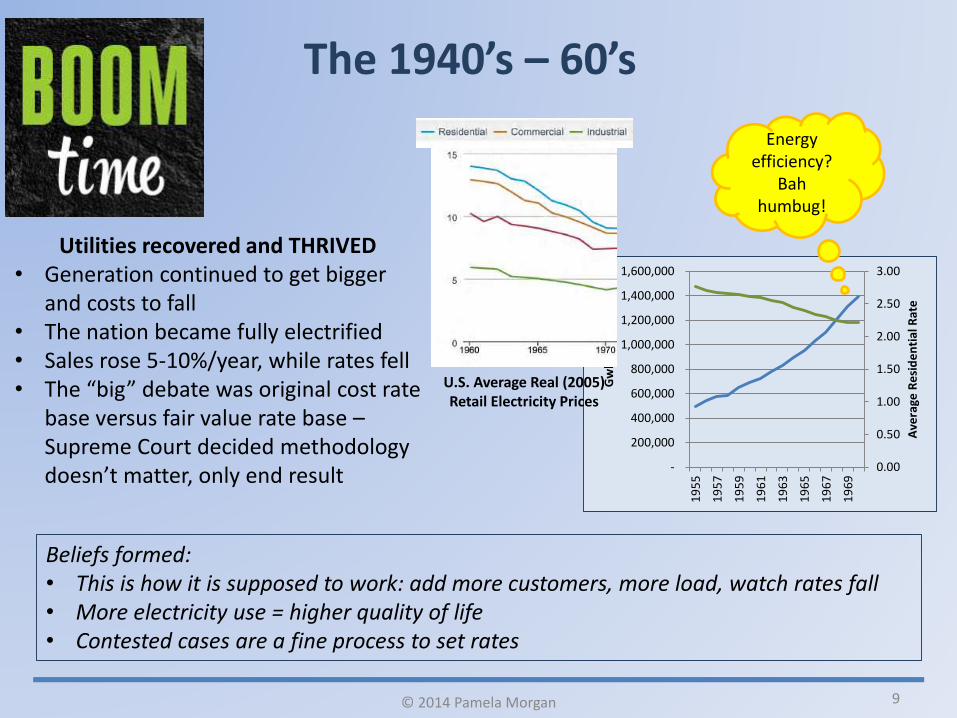

The 1940’s – 60’s

0.00

0.50

1.00

1.50

2.00

2.50

3.00

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

19

55

19

57

19

59

19

61

19

63

19

65

19

67

19

69

Ave

rage

Re

sid

en

tial

Rat

e

Gw

hrs

Utilities recovered and THRIVED• Generation continued to get bigger

and costs to fall• The nation became fully electrified• Sales rose 5-10%/year, while rates fell• The “big” debate was original cost rate

base versus fair value rate base –Supreme Court decided methodology doesn’t matter, only end result

Beliefs formed:• This is how it is supposed to work: add more customers, more load, watch rates fall• More electricity use = higher quality of life• Contested cases are a fine process to set rates

Energy efficiency?

Bah humbug!

U.S. Average Real (2005) Retail Electricity Prices

© 2014 Pamela Morgan

10

Exp

ect

ed

Ele

ctri

c Lo

ad

MW

s u

nd

er

Co

nst

ruct

ion

Infl

atio

n

Emp

loym

en

t an

d

Eco

no

my

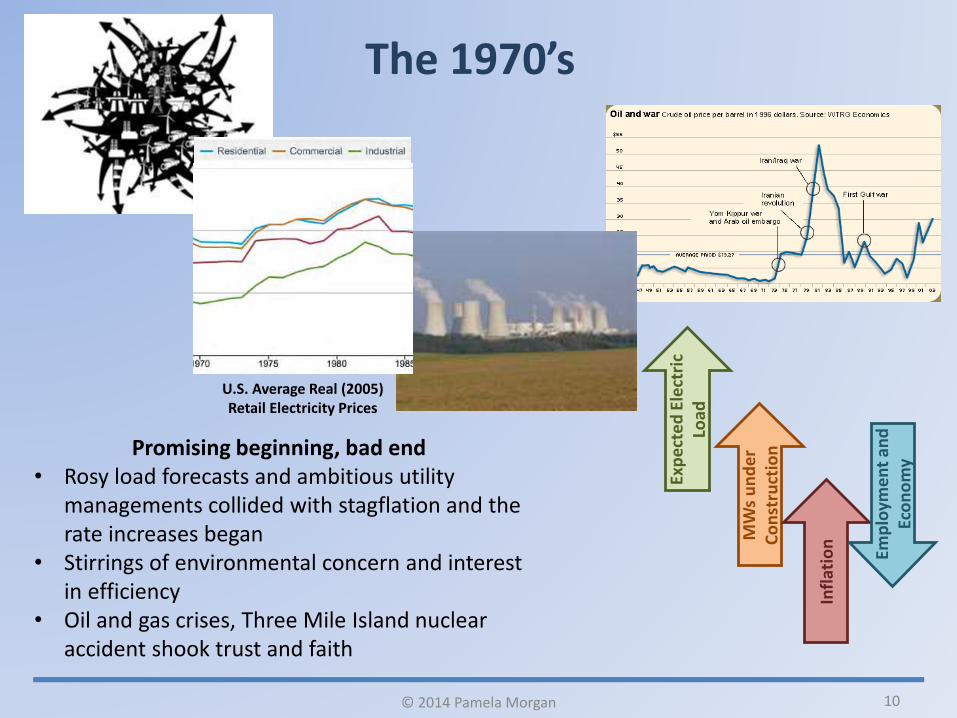

The 1970’s

Promising beginning, bad end• Rosy load forecasts and ambitious utility

managements collided with stagflation and the rate increases began

• Stirrings of environmental concern and interest in efficiency

• Oil and gas crises, Three Mile Island nuclear accident shook trust and faith

U.S. Average Real (2005) Retail Electricity Prices

© 2014 Pamela Morgan

11

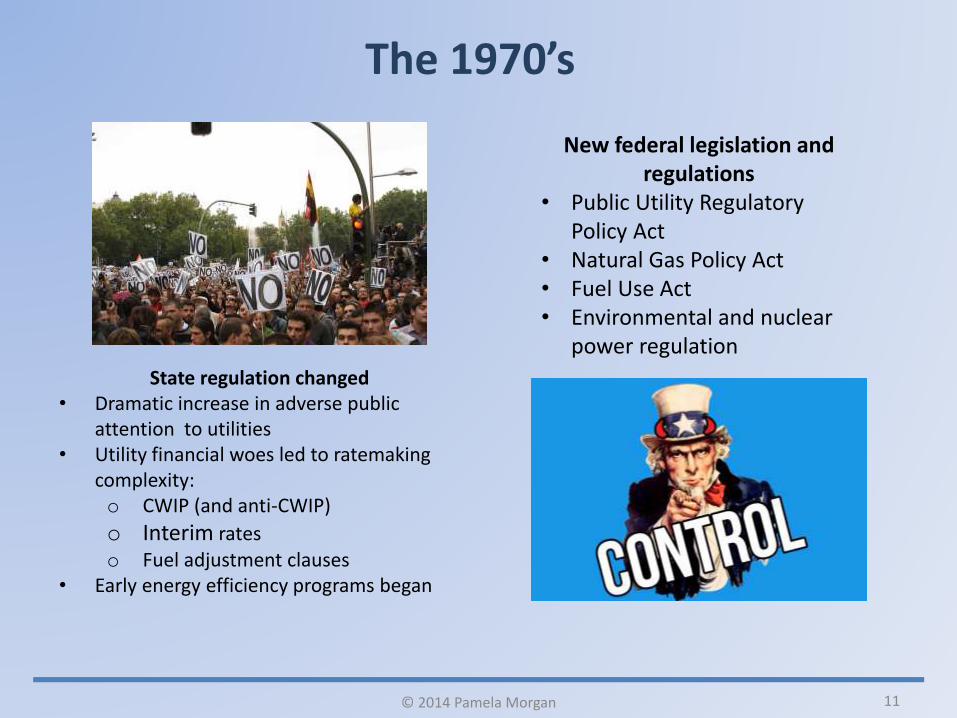

The 1970’s

New federal legislation and regulations

• Public Utility Regulatory Policy Act

• Natural Gas Policy Act• Fuel Use Act• Environmental and nuclear

power regulation

State regulation changed• Dramatic increase in adverse public

attention to utilities• Utility financial woes led to ratemaking

complexity:o CWIP (and anti-CWIP)

o Interim rateso Fuel adjustment clauses

• Early energy efficiency programs began

© 2014 Pamela Morgan

12

Actu

al Load

R A

T E

S

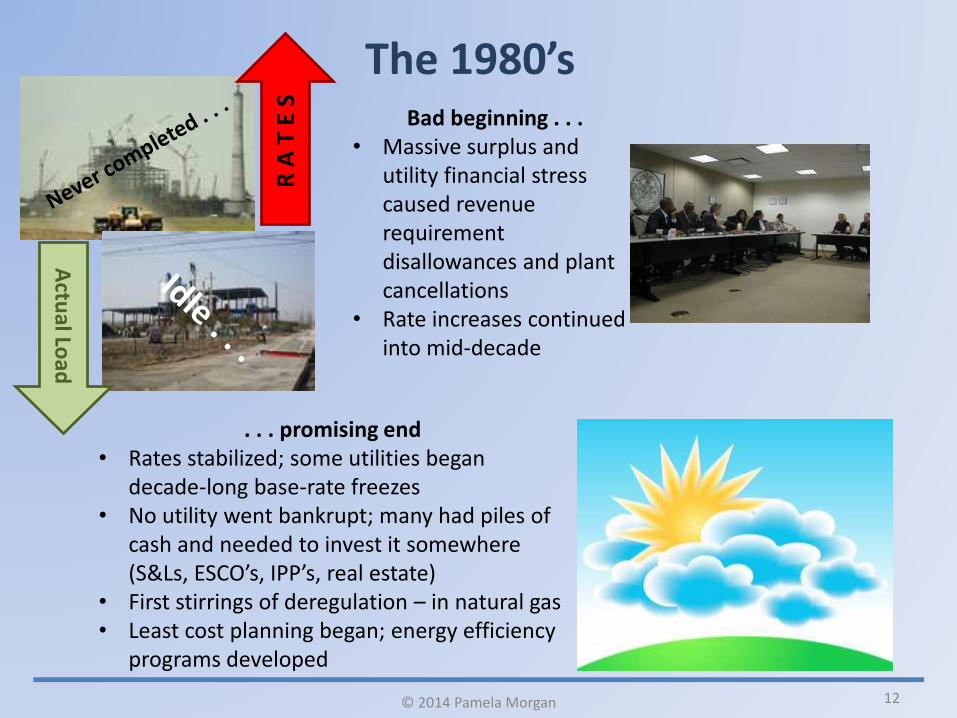

The 1980’s Bad beginning . . .

• Massive surplus and utility financial stress caused revenue requirement disallowances and plant cancellations

• Rate increases continued into mid-decade

. . . promising end• Rates stabilized; some utilities began

decade-long base-rate freezes• No utility went bankrupt; many had piles of

cash and needed to invest it somewhere (S&Ls, ESCO’s, IPP’s, real estate)

• First stirrings of deregulation – in natural gas• Least cost planning began; energy efficiency

programs developed

© 2014 Pamela Morgan

13

The 1970’s and 80’s

Beliefs formed:• Regulatory (and internal utility!) process is critical and more is usually better• Utilities may experience financial pain but regulators won’t let them go broke• Still, utilities can’t fully trust regulators and vice versa• Utility diversification is a mixed blessing (at best) and many pursuits don’t work out• The whole energy landscape is more complicated than anyone thought a while ago

but it is still possible to optimize electricity resources in planning and operations• Energy efficiency is good (but industrials would rather not pay for it . . . )

© 2014 Pamela Morgan

14

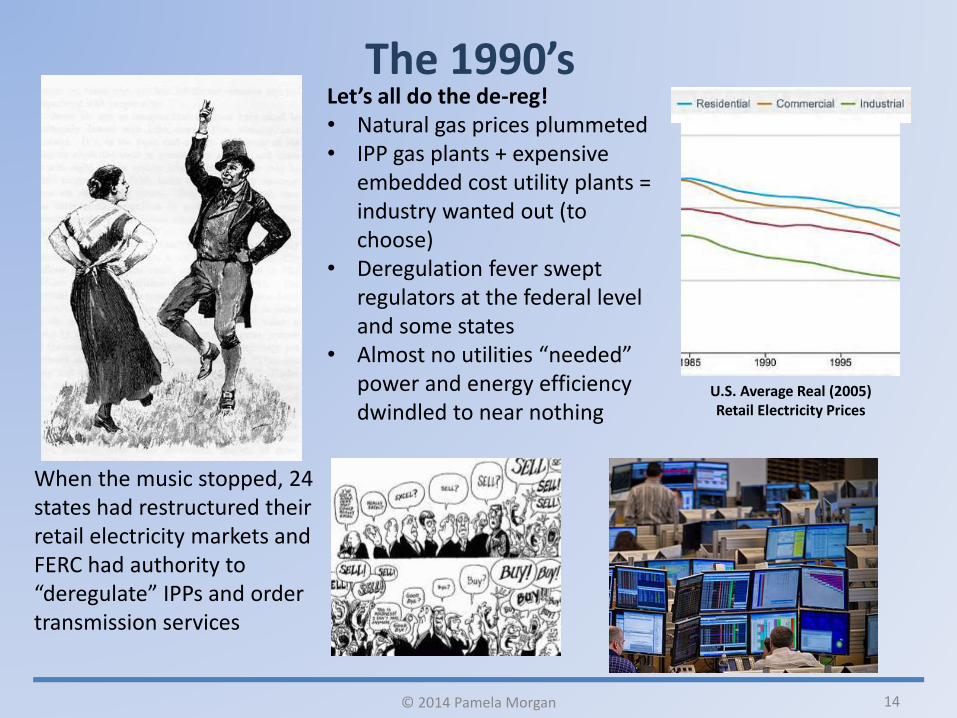

The 1990’s Let’s all do the de-reg!• Natural gas prices plummeted• IPP gas plants + expensive

embedded cost utility plants = industry wanted out (to choose)

• Deregulation fever swept regulators at the federal level and some states

• Almost no utilities “needed” power and energy efficiency dwindled to near nothing

When the music stopped, 24 states had restructured their retail electricity markets and FERC had authority to “deregulate” IPPs and order transmission services

U.S. Average Real (2005) Retail Electricity Prices

© 2014 Pamela Morgan

15

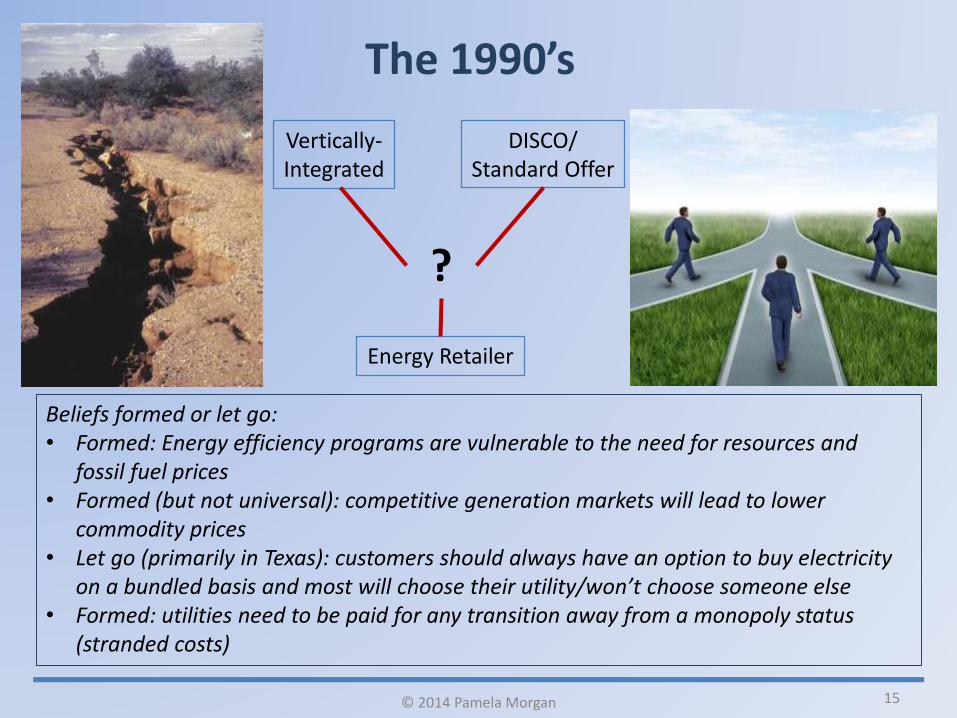

The 1990’s

DISCO/Standard Offer

Vertically-Integrated

Energy Retailer

?

Beliefs formed or let go:• Formed: Energy efficiency programs are vulnerable to the need for resources and

fossil fuel prices• Formed (but not universal): competitive generation markets will lead to lower

commodity prices• Let go (primarily in Texas): customers should always have an option to buy electricity

on a bundled basis and most will choose their utility/won’t choose someone else• Formed: utilities need to be paid for any transition away from a monopoly status

(stranded costs)

© 2014 Pamela Morgan

16

The 2000’s

Regulators (and sometimes legislatures or Congress) . . . regulated:

• Rates: retail, transmission etc.• Service: transmission, retail access

etc.• Market structure and behavior:

retail and wholesale• Energy efficiency, renewables, smart

grid mandates and incentives• Reliability• And more . . . .

Utilities . . . embraced being utilities• Filed rate cases with fervor• Wanted to make rate base

investments but with increasing levels of assurance of recovery

• Tried to say “customers” and not “ratepayers”

Retailers . . . shook out and grew

• What to sell• How to sell it

17

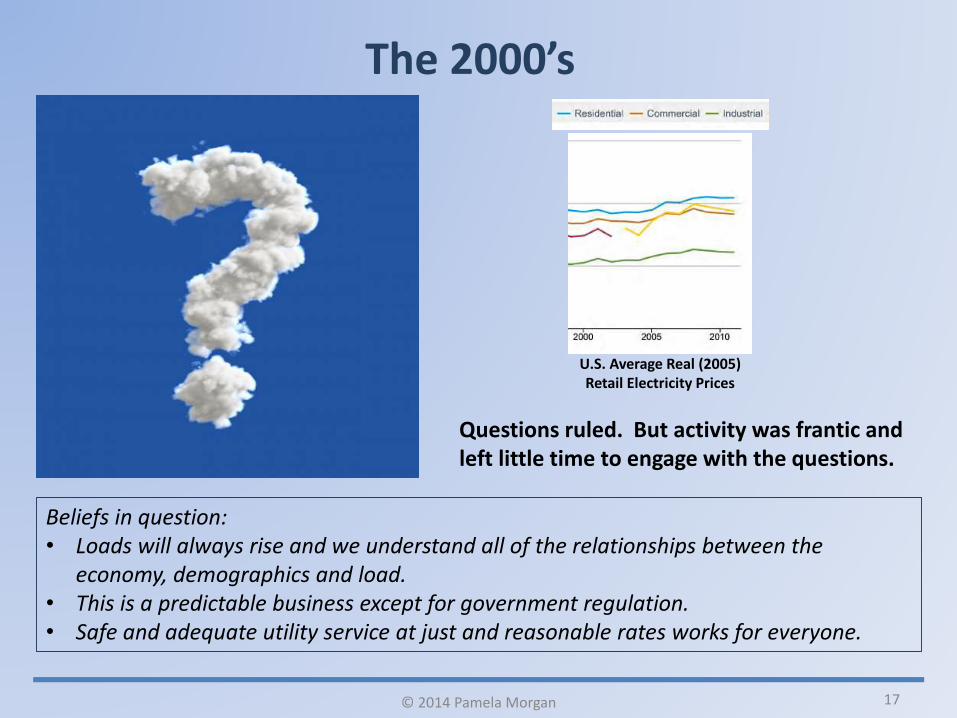

The 2000’s

Beliefs in question:• Loads will always rise and we understand all of the relationships between the

economy, demographics and load.• This is a predictable business except for government regulation.• Safe and adequate utility service at just and reasonable rates works for everyone.

Questions ruled. But activity was frantic and left little time to engage with the questions.

U.S. Average Real (2005) Retail Electricity Prices

© 2014 Pamela Morgan

18

The 2010’s

Hotbeds of regulatory activity . . .

ISSUES EVERYWHERE• Microgrids

• Demand response• Transmission

• EVs• Electricity Storage

• Smart grid• CO2 regulation and climate change

• New nukes• Technology – IT and other

• EE Cost-effectiveness• Net metering and the death spiral

• Your favorite

© 2014 Pamela Morgan

19

Is this where we are????

What beliefs do you think:

• Are forming?• Are expiring?

• Are in question?

© 2014 Pamela Morgan

20

THIS is what we have. Big Questions.

THIS is what we’d like to have.

But don’t.And won’t.

© 2014 Pamela Morgan

21

IF we are clear on the

important questions, we will more easily be able to make observations of events that pertain to those questions.

IF we make

observations of events that shed light on the questions, we might ultimately be able to discern patterns.

IF we discern patterns

and explore why those patterns are occurring, we might begin to understand the major reasons for what we see.

IF we understand

those reasons, we may be able to

FORESEE what is

coming.

© 2014 Pamela Morgan

22

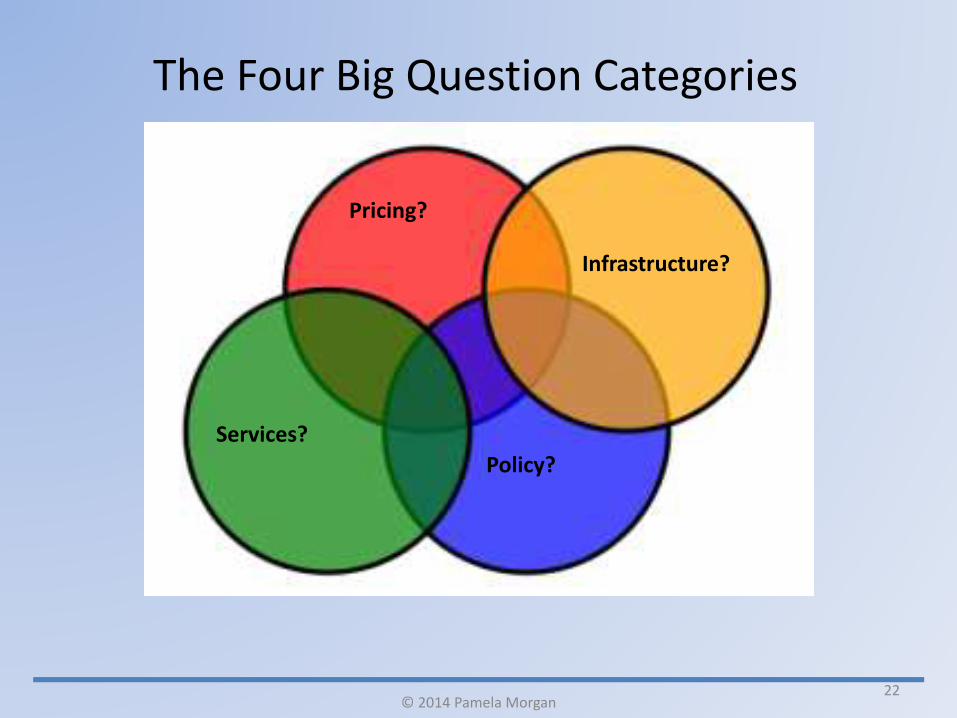

Policy?

Infrastructure?

Pricing?

Services?

The Four Big Question Categories

© 2014 Pamela Morgan

23

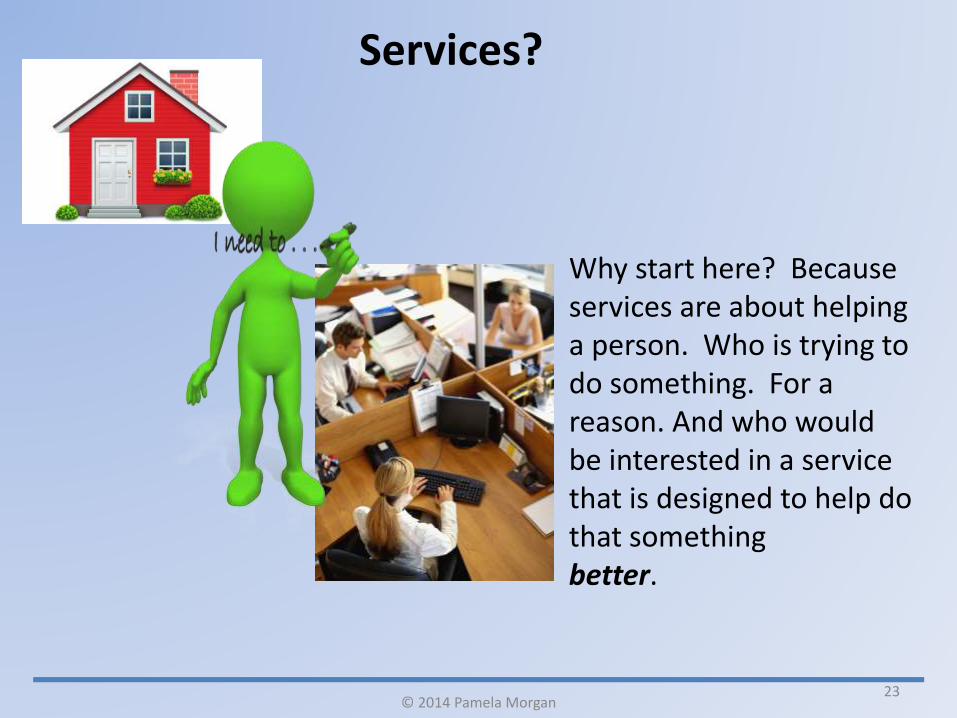

Services?

Why start here? Because services are about helping a person. Who is trying to do something. For a reason. And who would be interested in a service that is designed to help do that something better.

© 2014 Pamela Morgan

24

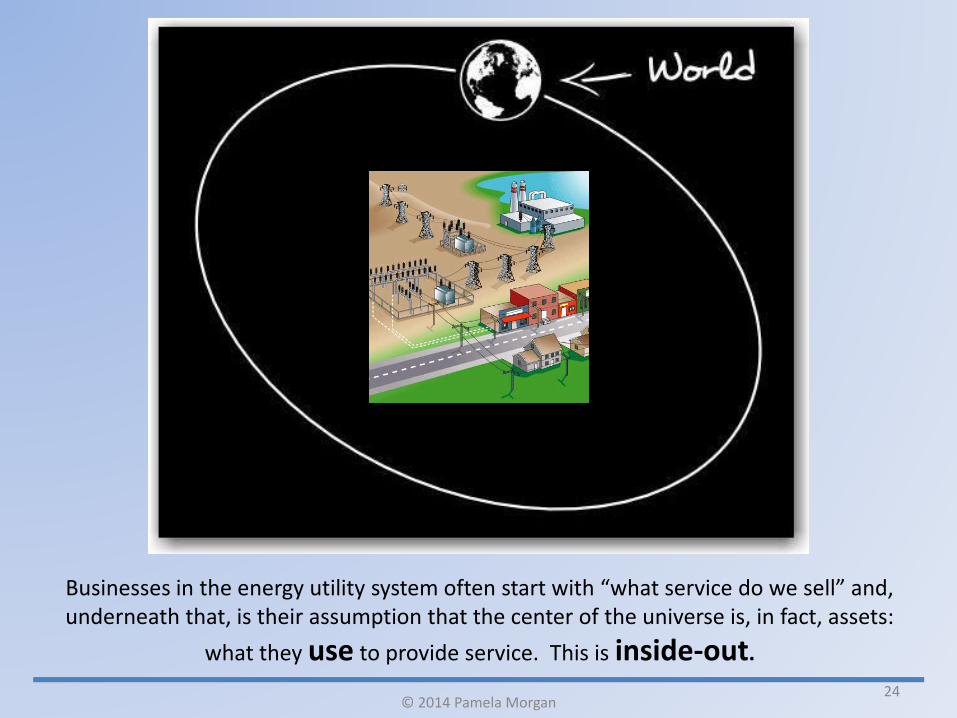

Businesses in the energy utility system often start with “what service do we sell” and, underneath that, is their assumption that the center of the universe is, in fact, assets:

what they use to provide service. This is inside-out.

© 2014 Pamela Morgan

25

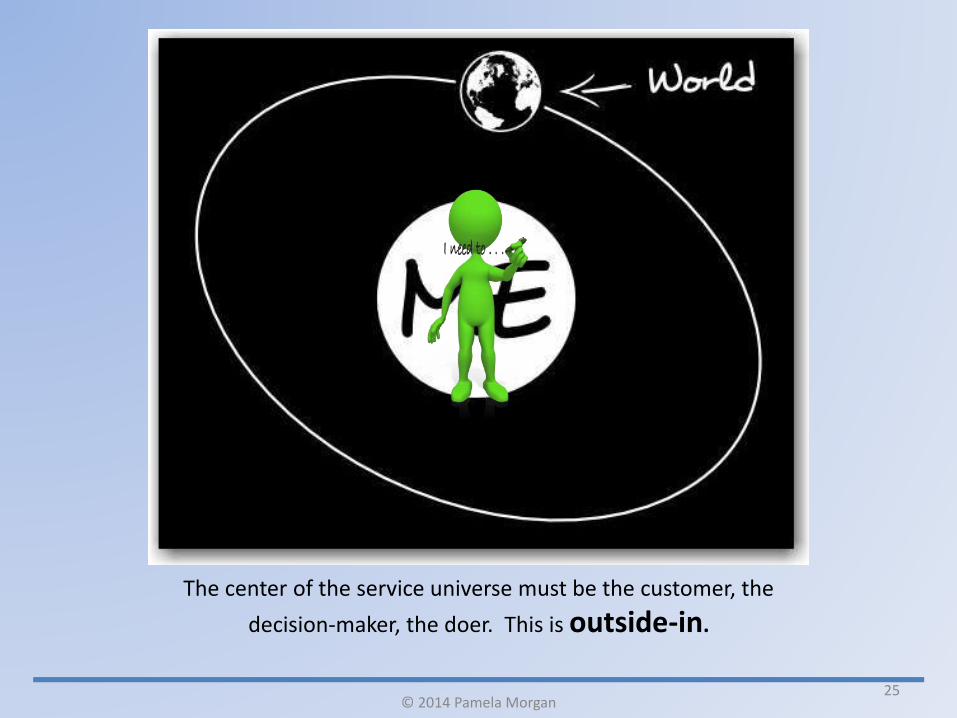

The center of the service universe must be the customer, the

decision-maker, the doer. This is outside-in.

© 2014 Pamela Morgan

26

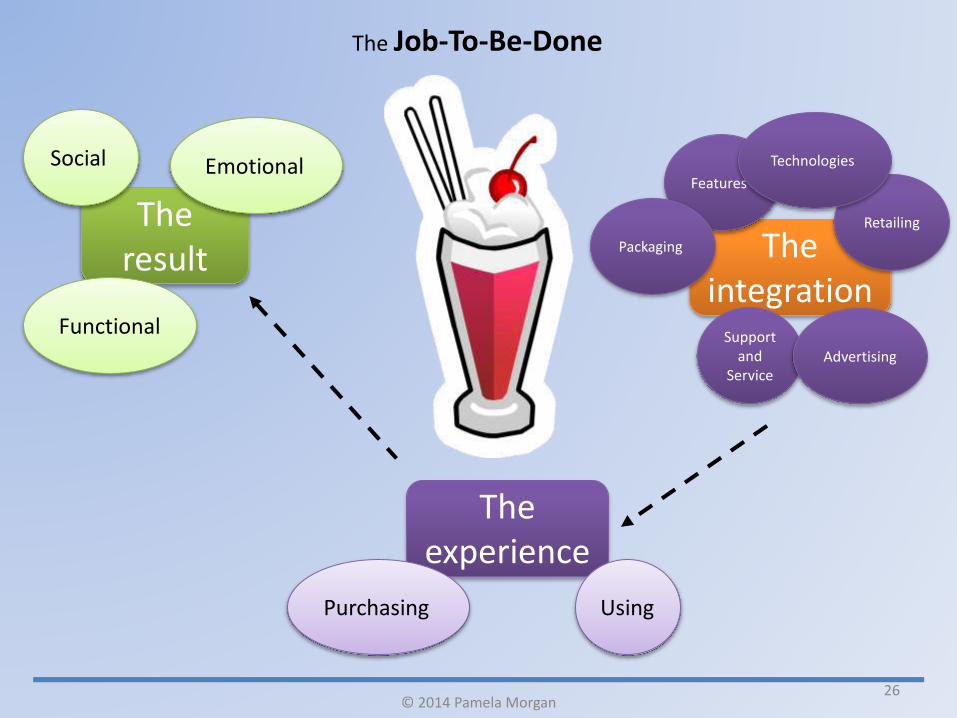

The Job-To-Be-Done

The result

EmotionalSocial

Functional

The experience

UsingPurchasing

The integration

Features

Retailing

Technologies

Packaging

Support and

ServiceAdvertising

© 2014 Pamela Morgan

27

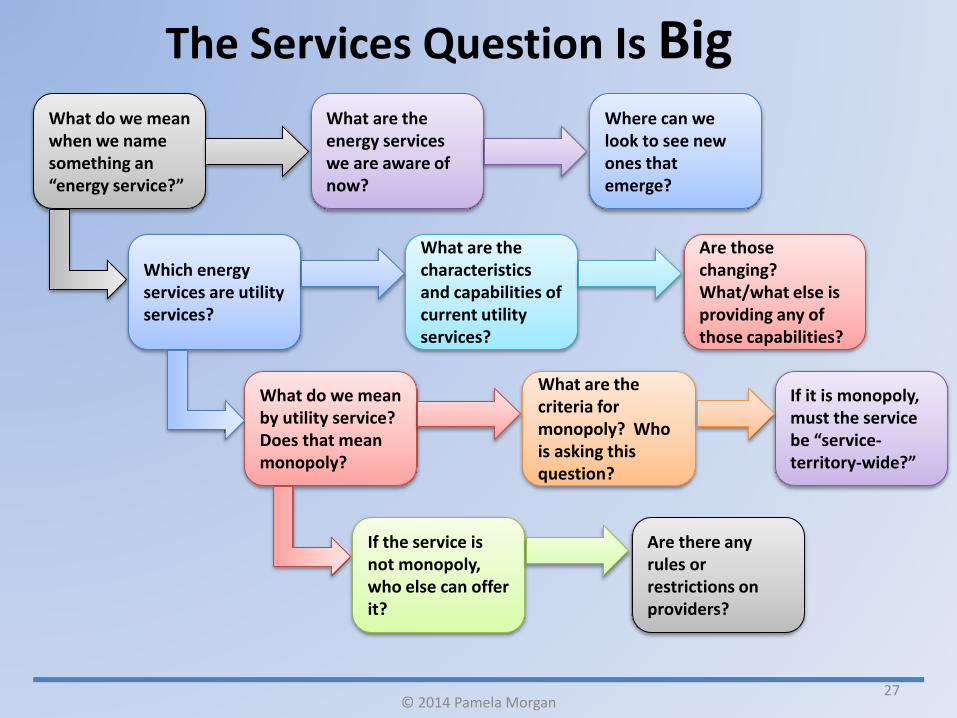

The Services Question Is BigWhat do we mean when we name something an “energy service?”

What are the criteria for monopoly? Who is asking this question?

What do we mean by utility service? Does that mean monopoly?

Which energy services are utility services?

If the service is not monopoly, who else can offer it?

Are those changing? What/what else is providing any of those capabilities?

What are the characteristics and capabilities of current utility services?

Where can we look to see new ones that emerge?

What are the energy services we are aware of now?

Are there any rules or restrictions on providers?

If it is monopoly, must the service be “service-territory-wide?”

© 2014 Pamela Morgan

28

Prices?

© 2014 Pamela Morgan

29

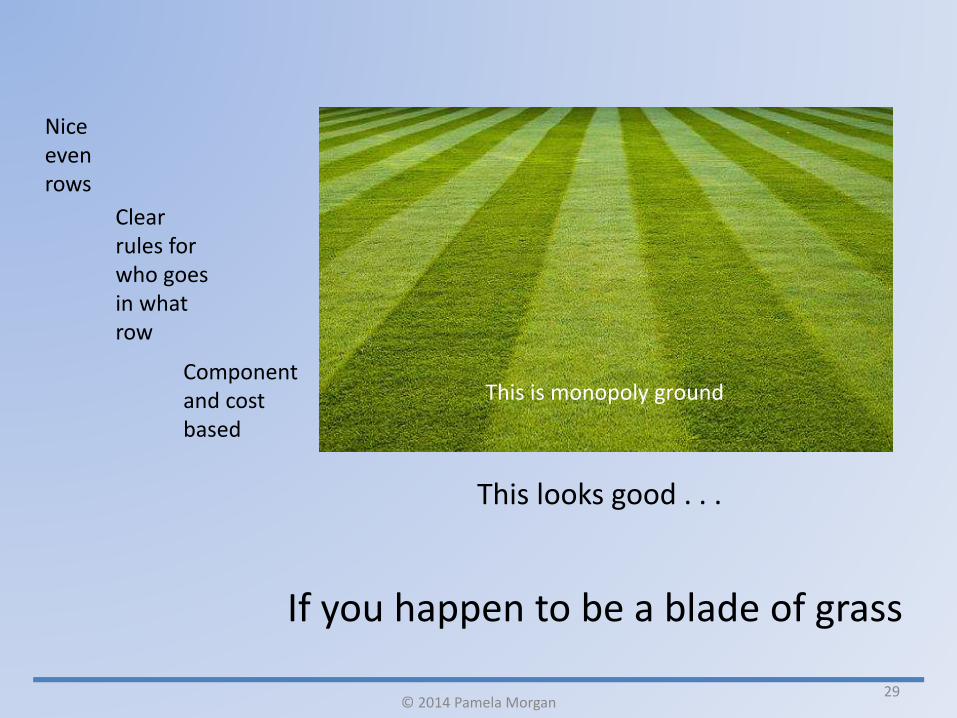

This is monopoly ground

Nice even rows

Clear rules for who goes in what row

Component and cost based

This looks good . . .

If you happen to be a blade of grass

© 2014 Pamela Morgan

30

This is competitive ground

Niches, nooks and crannies

What the market will bear

Judgment based

This looks scary . . .

But welcoming for people with different jobs-to-be-done

© 2014 Pamela Morgan

31

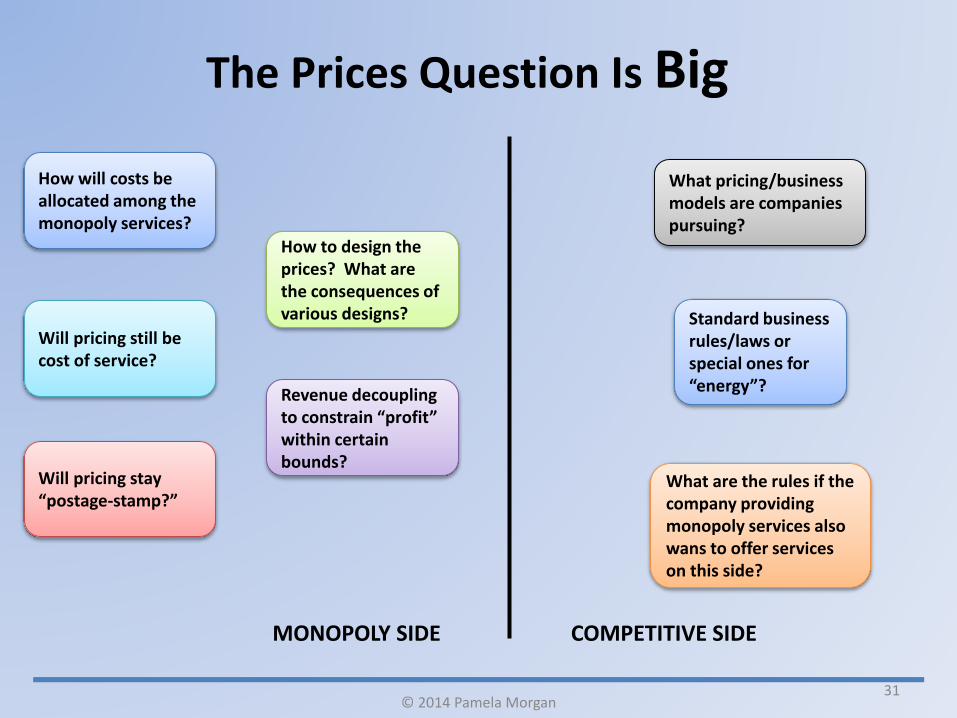

The Prices Question Is Big

How will costs be allocated among the monopoly services?

Will pricing still be cost of service?

How to design the prices? What are the consequences of various designs?

Revenue decoupling to constrain “profit” within certain bounds?

Will pricing stay “postage-stamp?”

MONOPOLY SIDE

What pricing/business models are companies pursuing?

What are the rules if the company providing monopoly services also wans to offer services on this side?

Standard business rules/laws or special ones for “energy”?

COMPETITIVE SIDE

© 2014 Pamela Morgan

32

Infrastructure?

© 2014 Pamela Morgan

MY STUFF IS MOST

IMPORTANT!!

NO!!!MY STUFF IS

MOST IMPORTANT

Whose STUFF will WIN?

IS that even the RIGHT question?

33

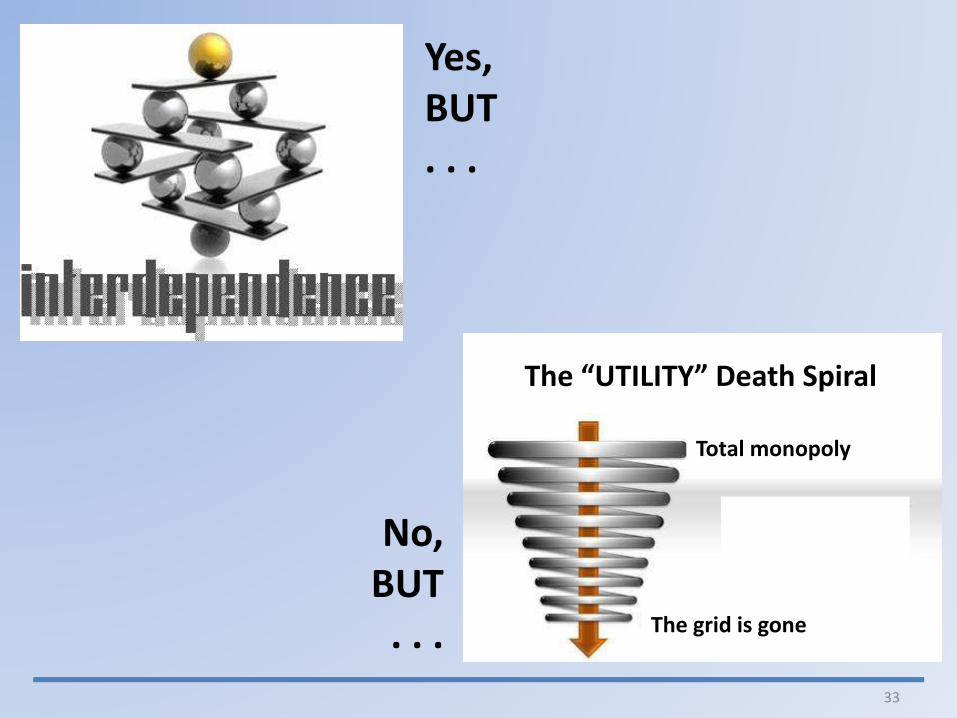

Yes, BUT . . .

No, BUT

. . .

The “UTILITY” Death Spiral

Total monopoly

The grid is gone

34© 2014 Pamela Morgan

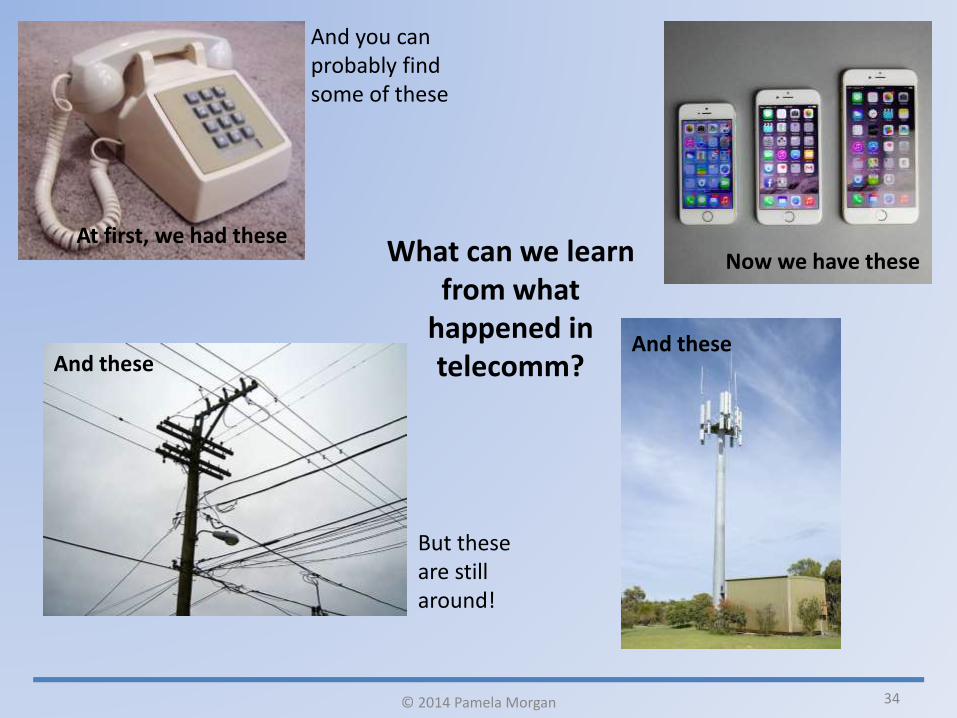

At first, we had these

And these

Now we have these

And these

But these are still around!

And you can probably find some of these

What can we learn from what

happened in telecomm?

35

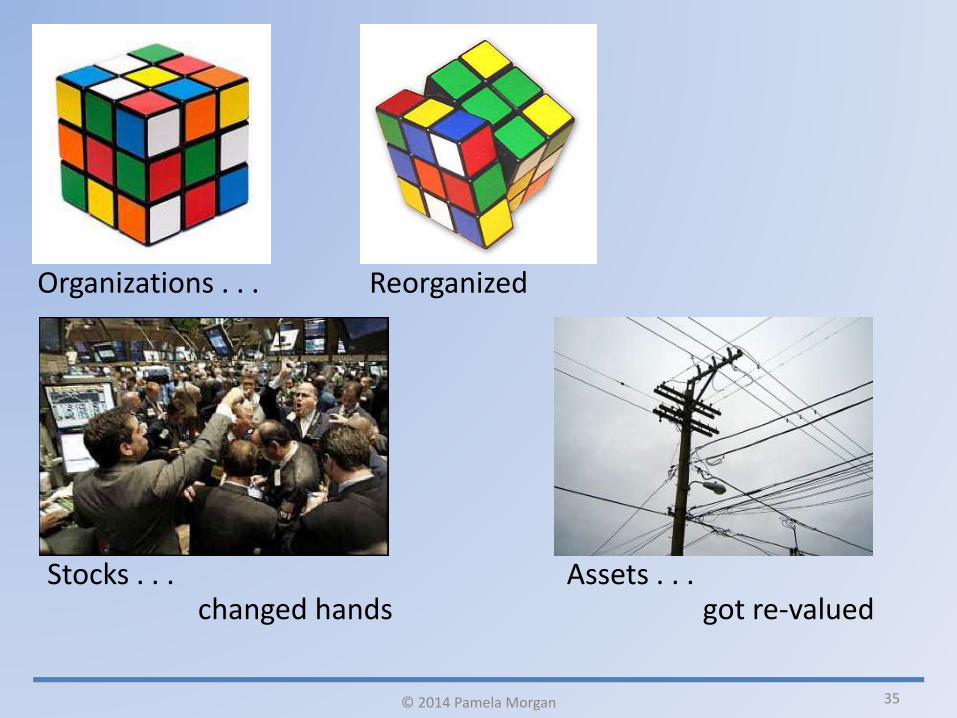

Organizations . . . Reorganized

Stocks . . . Assets . . . changed hands got re-valued

© 2014 Pamela Morgan

36© 2014 Pamela Morgan

The Infrastructure Question Is Big

What would Sam Insull do?

37

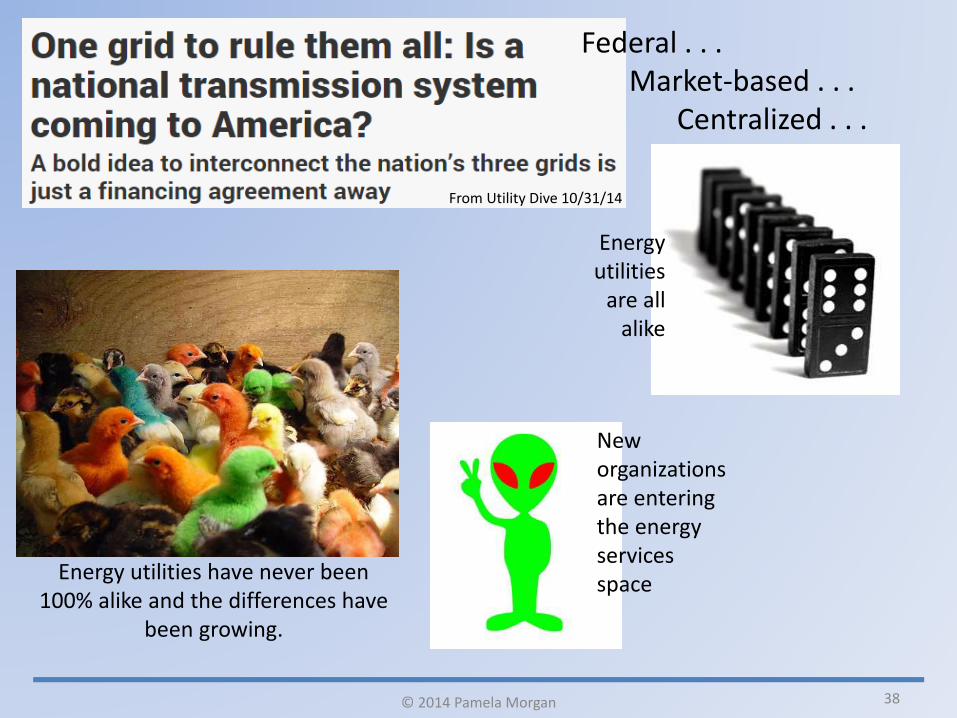

Policy?

CENTRAL CONTROL

© 2014 Pamela Morgan

38© 2014 Pamela Morgan

From Utility Dive 10/31/14

Energy utilities

are all alike

Energy utilities have never been 100% alike and the differences have

been growing.

Federal . . . Market-based . . .

Centralized . . .

New organizations are entering the energy services space

39

THE SOLUTION TOTHE PROBLEM? NOT

MAKING SPACE FOR TRIAL AND ERROR AND TRIAL . . . YES

The Policy Question Is Big

40

Mental models and beliefs will largely drive the answers that emerge for these questions. So, let’s review:

Early Days’ beliefs formed:• Competition, particularly in distribution, is bad• Monopoly makes sense within a service territory• Cost of service regulation works

1920’s beliefs formed:• Economies of scale are great• Electricity is more necessary than dangerous

1930’s beliefs formed:• Investor-owned utilities can be bad• Electricity is increasingly necessary to modern

living

1940’s – 60’s beliefs formed:• This is how it is supposed to work: add more

customers, more load, watch rates fall• More electricity use = higher quality of life• Contested cases are a fine process to set rates

1970’s – 80’s beliefs formed:• Regulatory (and internal utility!) process is critical

and more is usually better• Utilities may experience financial pain but

regulators won’t let them go broke• Still, utilities can’t fully trust regulators and vice

versa• Utility diversification is a mixed blessing (at best)

and many pursuits don’t work out• The whole energy landscape is more complicated

than anyone thought but it is still possible to optimize electricity resources in planning and operations

• Energy efficiency is good

1990’s beliefs formed or let go:• Formed: Energy efficiency programs are

vulnerable to the need for resources and fossil fuel prices

• Formed (but not universal): competitive generation markets will lead to lower commodity prices

• Formed: utilities need to be paid for any transition away from a monopoly status (stranded costs)

• Let go (primarily in Texas): customers should always have an option to buy electricity on a bundled basis and most will choose their utility/won’t choose someone else

© 2014 Pamela Morgan

41

2000’s beliefs in question:• Loads will always rise and we understand all of the relationships between the

economy, demographics and load.• This is a predictable business except for government regulation.• Safe and adequate utility service at just and reasonable rates works for everyone.

What will the energy utility industry do with its beliefs in the 2010’s?

And will it be the industry’s beliefs that guide the answers or ?

© 2014 Pamela Morgan

42

The energy utility system today

WHEREis everything

going????

© 2014 Pamela Morgan

43

What do YOU think?

© 2014 Pamela Morgan