election dossier 2008 - doi-archived.gov.mt · 10 swot analysis..... 105 10.1 an overview of the...

TRANSCRIPT

Enemalta Corporation Dossier

Date 6th Mach 2008 Version 07

i

Table of Content Page No

1 INTRODUCTION ................................................................................................................. 1

1.1 Background .................................................................................................................................. 1 1.2 Organisational Set-Up of Enemalta Corporation ...................................................................... 2 1.2.1 Head Office structure .................................................................................................................. 2 1.2.1.1 CEO’s Office ............................................................................................................................ 2 1.2.1.2 Finance Department ................................................................................................................ 2 1.2.1.3 Human Resources and Corporate Services Department ........................................................ 2 1.2.1.4 Chief Information Office ........................................................................................................... 2 1.2.2 Electricity Division ....................................................................................................................... 3 1.2.3 Petroleum Division ...................................................................................................................... 3 1.2.4 Gas Division ................................................................................................................................ 3 1.3 Management Infrastructure ........................................................................................................ 3 1.3.1 Strategic Sourcing and Procurement .......................................................................................... 3 1.3.2 Programme, Services and Facilities Management ..................................................................... 4 1.3.2.1 Performance Management and Monitoring ............................................................................. 4 1.3.2.2 Service Call Centre .................................................................................................................. 5 1.3.3 Health and Estate Services Management .................................................................................. 5 1.3.4 Office of Strategy and Regulatory Affairs ................................................................................... 5 1.3.4.1 Quality Assurance Unit ............................................................................................................ 6 1.3.4.2 Research and Innovation Unit ................................................................................................. 6 1.3.5 Office of the Chief Information Officer ........................................................................................ 6 1.4 Unbundling the Corporation’s Organisation ............................................................................ 7

2 REGULATORY AND EU FRAMEWORK AT ENEMALTA CORPORATION ................................... 9

2.1 Introduction .................................................................................................................................. 9 2.2 The Enemalta Act ......................................................................................................................... 9 2.2.1 Recent amendments to the Enemalta Act .................................................................................. 9 2.3 The Electricity Supply Regulations (ESRs) ............................................................................. 10 2.4 Other relevant legislation .......................................................................................................... 10 2.5 Legal Issues and Enemalta’s Positioning ............................................................................... 10 2.5.1 Office of Fair Trading (OFT) ..................................................................................................... 10 2.5.2 Courts of Justice ....................................................................................................................... 11 2.5.3 Arbitration Centre ...................................................................................................................... 12 2.6 EU related Directives and Impacts on Enemalta Corporation .............................................. 12 2.6.1 Rules Concerning the Internal Market in Electricity .................................................................. 12 2.6.2 Environmental Matters .............................................................................................................. 14 2.6.2.1 Directive 2003/87/EC (L.N. 140/2005) : Greenhouse Gas Emissions Trading Scheme ....... 15 2.6.2.2 Directive 2001/80/EC (L.N. 329/2002): Large Combustion Plant .......................................... 15 2.6.2.3 Directive 2001/81/EC (L.N. 232/2004): National Emission Trading Scheme ........................ 15 2.6.2.4 Directive 1996/61/EC (L.N. 230/2004): Integrated Pollution Prevention and Control ........... 15 2.6.2.5 Directive 1997/265/EC ........................................................................................................... 16 2.6.2.6 Directive 1996/82/EC & Directive 2003/105/EC: Control of Major Accidents / Hazards. COMAH (Sevaso) Directive .................................................................................................................. 16 2.6.2.7 The 1999 Gothenburg Protocol ............................................................................................. 16 2.6.2.8 Renewable Sources of Energy .............................................................................................. 17 2.6.2.9 Energy Efficiency ................................................................................................................... 17 2.6.2.10 Draft Industrial Emissions Directive (IPPC Directive) .......................................................... 17

3 THE HUMAN RESOURCES FRAMEWORK OF ENEMALTA CORPORATION ............................. 19

ii

3.1 Overview ..................................................................................................................................... 19 3.2 Collective Agreements .............................................................................................................. 21 3.3 Side Agreements and Work Practices ..................................................................................... 23 3.3.1 Aviation Work Practice .............................................................................................................. 24 3.3.2 Generation Section Work Practice ........................................................................................... 25 3.3.3 Moving towards a Position Based Organisation ....................................................................... 25

4 THE FINANCIAL FRAMEWORK OF ENEMALTA CORPORATION ............................................ 28

4.1 An Overview of the Financial Framework of the Corporation ............................................... 28 4.2 The Finance Department of the Enemalta Corporation ......................................................... 29 4.2.1 Overview ................................................................................................................................... 29 4.2.2 Functions .................................................................................................................................. 29 4.2.3 Human resources ..................................................................................................................... 30 4.3 Funding strategy ........................................................................................................................ 31 4.4 Risk Management ...................................................................................................................... 32 4.4.1 Finance Committee ................................................................................................................... 32 4.4.2 Internal Audit Committee .......................................................................................................... 32 4.4.3 Fuel Procurement Advisory Committee .................................................................................... 32 4.4.4 Risk Management Committee .................................................................................................. 32 4.4.5 Fuel Procurement Committee ................................................................................................... 32 4.4.6 Tender Sub-Committee ............................................................................................................ 33 4.5 The Corporation’s Financial Position ...................................................................................... 33 4.5.1 Profit and Loss Analysis ........................................................................................................... 33 4.5.2 Cash flow, Loans and Debt Management ................................................................................ 34 4.6 Draft 2008 Estimates and 5 years forecast ............................................................................. 35 4.7 External Audits .......................................................................................................................... 36 4.8 Cost and Revenue Centres ....................................................................................................... 37 4.9 Internal audit .............................................................................................................................. 37 4.10 Dependency on Water Services Corporation ....................................................................... 37 4.10.1 The Debtor Portfolio ................................................................................................................ 38 4.10.2 Larger debtors ........................................................................................................................ 38 4.10.3 Credit issues and policy .......................................................................................................... 39 4.11 Applications for Financing Under the ERDF Funding Cohesion Policy: 2007-2012 ........ 40 4.11.1 Feasibility Study and Implementation of Prototype Offshore Renewable Energy Solution .... 40 4.11.2 400kWp Rooftop PV Project ................................................................................................... 40 4.11.3 Study on a Submarine Electricity Interconnection between Malta and Sicily ......................... 41 4.11.4 132kV and fibre-optic cables between Delimara PS and Marsa South Distribution Centre ... 41 4.11.5 Kappara 132kV Distribution Centre ........................................................................................ 41

5 PRICING, TARIFFS, SURCHARGE AND HEDGING CONSIDERATIONS ..................................... 42

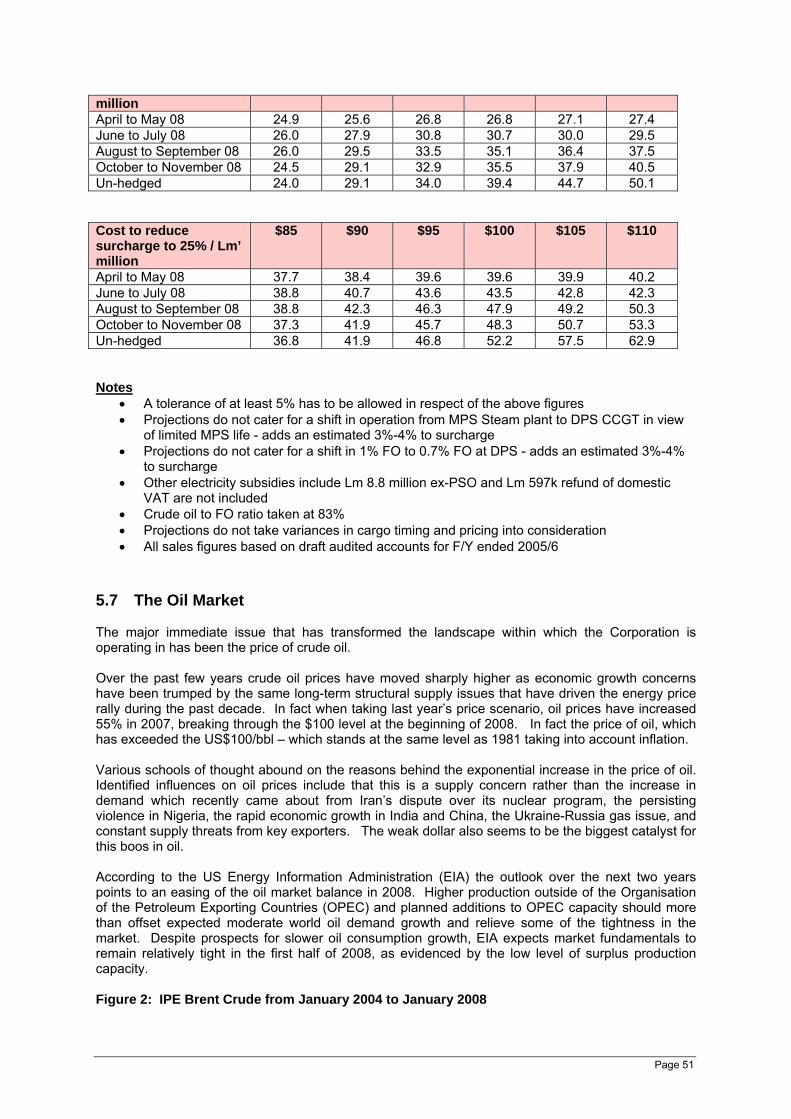

5.1 Pricing strategies ....................................................................................................................... 42 5.1.1 Tariffs ........................................................................................................................................ 42 5.1.1.1 Electricity Division .................................................................................................................. 42 5.1.1.2 Petroleum Division ................................................................................................................. 43 5.1.1.3 Gas Division ........................................................................................................................... 44 5.2 Contribution by Product ........................................................................................................... 44 5.3 Surcharge and Subventions ..................................................................................................... 46 5.4 Hedging ....................................................................................................................................... 47 5.4.1 Hedges in Place ........................................................................................................................ 48 5.5 Retailed Petroleum Product forecast ...................................................................................... 50 5.6 Surcharge forecasts .................................................................................................................. 50 5.7 The Oil Market ............................................................................................................................ 51

6 THE INFORMATION, TECHNOLOGY AND COMMUNICATIONS FRAMEWORK .......................... 54

iii

6.1 Introduction ................................................................................................................................ 54 6.2 The IUBS Solution ..................................................................................................................... 55 6.3 Information Systems Application within the Corporation ..................................................... 59 6.4 SCADA ........................................................................................................................................ 60 6.5 e-Services ................................................................................................................................... 61 6.6 ICT Infrastructure Backbone .................................................................................................... 62 6.7 ICT Literacy within the Corporation ......................................................................................... 64

7 THE ELECTRICITY DIVISION ............................................................................................. 65

7.1 Introduction ................................................................................................................................ 65 7.2 The Generation Set-Up .............................................................................................................. 65 7.2.3.1 Base Load Plant .................................................................................................................... 70 7.2.3.2 Two Shifting Plant .................................................................................................................. 71 7.2.3.3 Peak Plant ............................................................................................................................. 71 7.3 The Distribution Set-Up ............................................................................................................. 74 7.3.2 Distribution Operations ............................................................................................................. 77 7.3.2.2 Feeder Redundancy .............................................................................................................. 77 7.3.2.3 Redundancies of Power Transformers .................................................................................. 78 7.3.2.4 Switchgear ............................................................................................................................. 78 7.3.2.5 Load Growth Forecast ........................................................................................................... 79 7.3.2.6 Distribution substations .......................................................................................................... 80 7.4 Strategies to Meet Electricity Demand .................................................................................... 80 7.4.1 Enemalta Generation Plan........................................................................................................ 80 7.4.2 Transmission Plan .................................................................................................................... 83 7.4.3 The Sub-Sea Interconnector .................................................................................................... 86 7.4.4 Natural Gas Supply ................................................................................................................... 89

8 PETROLEUM DIVISION ..................................................................................................... 90

8.1 Introduction ................................................................................................................................ 90 8.2 The Installation Operations ...................................................................................................... 90 8.2.1 31st March 1979 Installation, Birzebbugia................................................................................. 90 8.2.2 Wied Dalam Depot .................................................................................................................... 92 8.2.3 Has-Saptan Installation ............................................................................................................. 93 8.2.4 Ras Hanzir Installation .............................................................................................................. 93 8.2.5 Luqa Airport Installation ............................................................................................................ 94 8.2.6 Security Oil Stocks .................................................................................................................... 95 8.3 Commercialisation of the Petroleum Division ........................................................................ 95

9 GAS DIVISION ................................................................................................................. 97

9.1 Introduction ................................................................................................................................ 97 9.2 The Installation Operations ...................................................................................................... 97 9.2.1 Stock of Cylinders ..................................................................................................................... 99 9.2.2 Production Process of Cylinders .............................................................................................. 99 9.2.3 Maintaining Supply of Gas ...................................................................................................... 100 9.3 Relocation of Qajjenza Plan .................................................................................................... 101 9.4 Distributors............................................................................................................................... 102 9.5 Commercialisation of the Gas Division ................................................................................. 102

10 SWOT ANALYSIS ......................................................................................................... 105

10.1 An Overview of the Corporation’s Strengths and Weaknesses ....................................... 105 10.1.1 Strengths............................................................................................................................... 105

iv

10.1.2 Weaknesses ......................................................................................................................... 105 10.2 An Overview of the Corporation’s Opportunities and Threats ......................................... 107 10.2.1 Opportunities ........................................................................................................................ 107 10.2.2 Threats .................................................................................................................................. 108

1 APPENDIX – ENEMALTA ACT 1977 ................................................................................. 1

2 APPENDIX – ELECTRICITY SUPPLY REGULATIONS ........................................................... 2

3 APPENDIX – MANAGEMENT ACCOUNTS AS AT 30 SEPTEMBER 2007 ............................... 3

4 APPENDIX – DRAFT ESTIMATES 2007/2008 .................................................................... 4

5 APPENDIX – 5 YEAR PROJECTIONS (2006-2011) ............................................................ 5

6 APPENDIX – ANNUAL REPORT AND FINANCIAL STATEMENTS 30 SEPTEMBER 2006 (DRAFT) ................................................................................................................................... 6

7 APPENDIX – BENGHAJSA LAND – IMPAIRMENT ISSUES .................................................... 7

8 APPENDIX – ANNUAL REPORT AND FINANCIAL STATEMENTS 30 SEPTEMBER 2005 (AUDITED) ................................................................................................................................ 8

9 APPENDIX – ELECTRICITY GENERATION PLAN 2006-2015 .............................................. 9

10 APPENDIX – TRANSMISSION PLAN 2006 - 2015 ............................................................ 10

11 APPENDIX – INVITATION TO TENDER: PETROLEUM DIVISION (TO BE HANDED OVER UPON REQUEST) ..................................................................................................................... 11

12 APPENDIX – STANDARD & POOR’S 2007 FULL REPORT ................................................ 12

v

Tables Page No Table 1: Years of Service with the Corporation ............................................................................... 19 Table 2: Enemalta Corporation Employees by Gender ................................................................... 19 Table 3: Classification of the Corporation’s employees ................................................................. 19 Table 4: Enemalta Corporation Aging Population ........................................................................... 19 Table 5: Instances of Negative Increment Reports ......................................................................... 20 Table 6: Membership Representation in Unions.............................................................................. 20 Table 7: Profit and Loss Analysis ..................................................................................................... 33 Table 8: Debt Position ........................................................................................................................ 34 Table 9: Cash generation, Capex and debt since 1994 ................................................................... 35 Table 10: Aged debtors (Lm).............................................................................................................. 38 Table 11: Larger Debtors .................................................................................................................... 39 Table 12: Electricity Tariffs ................................................................................................................ 42 Table 13: Retailed Petroleum Products ............................................................................................ 43 Table 14: LPG Prices .......................................................................................................................... 44 Table 15: Contribution by Division .................................................................................................... 44 Table 16: Fuel Costs, Surcharge and Government Subventions ................................................... 46 Table 17: Government’s Payment ..................................................................................................... 46 Table 18: Hedges done in recent years - Products ......................................................................... 48 Table 19: Electricity hedges in place ................................................................................................ 49 Table 20: Petroleum product hedges ................................................................................................ 49 Table 21: Petroleum Product forecast .............................................................................................. 50 Table 22: Surcharge forecast ............................................................................................................. 50 Table 23: Investment in ICT by the Corporation since 2004 ........................................................... 54 Table 24: Plant mix .............................................................................................................................. 66 Table 25: Installed generating plant at MPS ..................................................................................... 67 Table 26: Installed generating plant at DPS ..................................................................................... 68 Table 27: Expected Peak Loads (natural growth only) ................................................................... 68 Table 28: Expected Peak Loads (incl. planned developments) ...................................................... 69 Table 29: Transformer ratings in distribution centres .................................................................... 75 Table 30: Localities in each Region .................................................................................................. 76 Table 31: Peak Demand Growth Forecast ........................................................................................ 79 Table 32: Sale of Gas Between 26th January 2008 to 19th February 2008 ...................................... 98 Table 33: Hour Production of Gas Cylinders ................................................................................. 100

vi

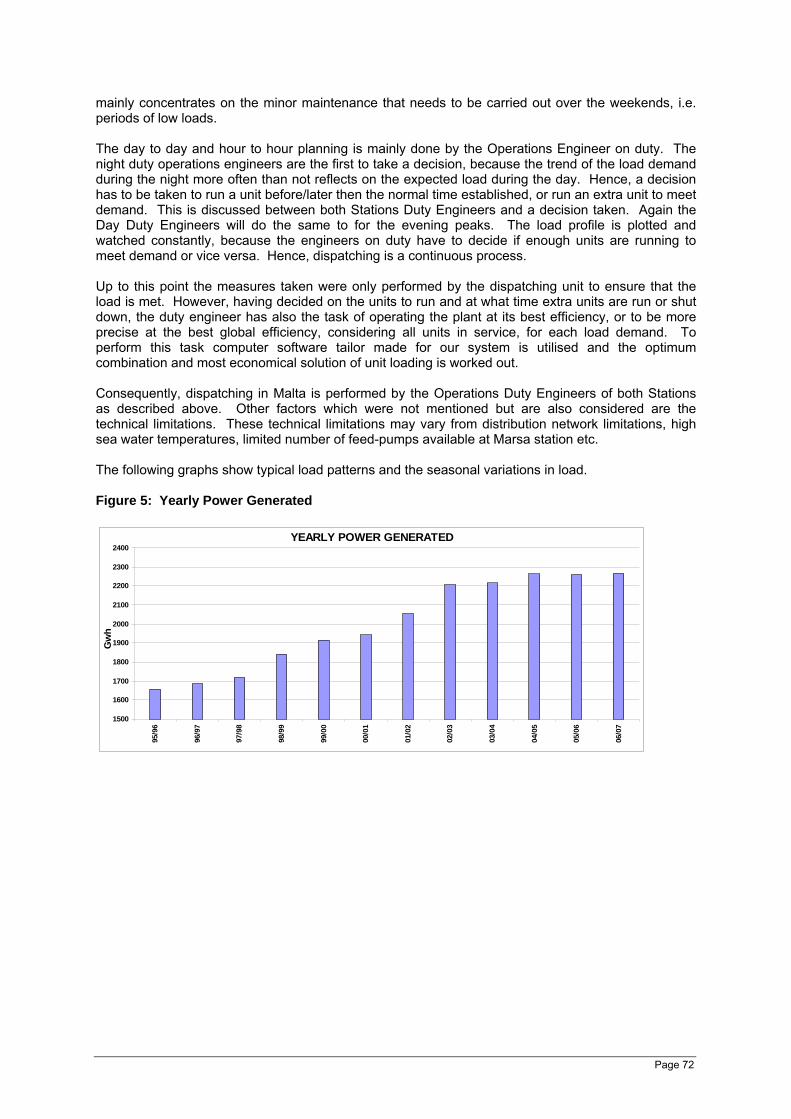

Figures Page No Figure 1: Organization Structure ........................................................................................................ 2 Figure 2: IPE Brent Crude from January 2004 to January 2008 .................................................... 51 Figure 3: Electricity consumption by Sector .................................................................................... 66 Figure 4: Power Generation in Gwh .................................................................................................. 66 Figure 5: Yearly Power Generated ................................................................................................... 72 Figure 6: Monthly Generated Power ................................................................................................ 73 Figure 7: Seasonal Variations in Peak Demand .............................................................................. 73 Figure 8: Power Generated ................................................................................................................ 73 Figure 9: Typical Daily Load Charts ................................................................................................. 74 Figure 10: Transmission System ....................................................................................................... 76 Figure 11: Power Generated in Gwh ................................................................................................. 82 Figure 12: Predicted Load .................................................................................................................. 82 Figure 13: Gas Cylinders Sales Between January 2004 and January 2008 .................................. 97 Figure 14: Gas Sales from 1st December 2007 to 19th February 2008 ............................................ 98 Figure 15: Total Number of Cylinders ............................................................................................... 99

Page 1

1 Introduction This Dossier is prepared in order to provide a new Government and a new Board of Directors with a comprehensive overview of the Corporation in terms of state of play, issues and recommendations. 1.1 Background Enemalta Corporation is a 100% Government entity established by an Act of Parliament (The Enemalta Act 1977 Chapter 272 of the Laws of Malta). Enemalta is vertically integrated and operates in three energy related divisions, namely electricity, petroleum and gas. A Head Office structures overseas the three operational activities. The Electricity Division was recently “unbundled” into generation and distribution, while Petroleum and Gas Divisions include of importation, storage and distribution activities of petroleum and LPG products. The Electricity Division utilizes the billing function of another fully owned Government entity (namely Water Services Corporation - WSC) while the Petroleum and Gas Divisions utilize 3rd party retailers and distributors as their interface with consumers. Enemalta is one of the largest organizations in Malta with turnover of Lm190 million, assets of Lm294 million, debts of Lm142 million and 1,700 employees. The Corporation is managed by a semi-executive Chairman (currently Ing Alexander Tranter) and a Board of Directors (all appointed by the Government). At executive level the Corporation is managed by a Chief Executive Officer (Mr. David Spiteri Gingell) and a Board of Management consisting of the Chief Finance Officer (Mr. Joseph Pandolfino), the Chief Technical officer (Ing Peter Grima) and the Chief HR & Corporate Services (Mr. Anthony Bonello). A position of Chief Information Officer is currently vacant as is the position of Chief Internal Auditor. Executive Management is supported by various Managers and Assistant Manager that are responsible for line activities (Generation, Distribution, Development, Petroleum and Gas) and support functions such as Finance, Legal, HR, Corporate Services and HR. At a lower level the Corporation employees a number of professional, technical, administrative and support staff. Enemalta is closely linked and significantly influenced by Government. It currently falls under the Ministry for IT & Investments and is primarily regulated by the Malta Resources Authority. Secondary ministries include the Ministry for Finance, the MRES and the MRAE, while Authorities such as MEPA and the ADT play influential roles. The Corporation is closely linked to the WSC in view of joint billing, the Department of Contracts for purchasing and more recently MITTS for IT related services. The Corporation is currently at a cross-road. Strategically Government has decided that Enemalta should focus on electricity and that its petroleum and gas businesses should be commercialized (i.e. sold). The divestment of petroleum and gas will allow the Corporation to focus its resources on the electricity segment that is also in a transitional stage, both due to EU directives in this area as well as the significant investments forecast for the coming years. The Corporation has an investment grade rating of BBB+ stable by Standards and Poor’s reflecting strong Government support, not a stand-alone basis.

Page 2

1.2 Organisational Set-Up of Enemalta Corporation The Corporation consists of support services at Head Office and the three operational Divisions. 1.2.1 Head Office structure Head Office consists of the CEO’s office together with 3 main departments. 1.2.1.1 CEO’s Office The CEO Office includes the CEO and his PAs, together with a Special Projects. The Special Projects Office is responsible for the afore mentioned commercialisation process. There are another 36 staff employed in various other functions within the Corporation that report to the CEO. 1.2.1.2 Finance Department This department is responsible for financial management, procurement, credit control. There are 58 employees in this department. 1.2.1.3 Human Resources and Corporate Services Department This department is responsible for Industrial Relations, Personnel Administration, Training, and Corporate Services. This department has 163 staff. 1.2.1.4 Chief Information Office This Office is responsible for ICT support to both the core business and support functions. There are 18 employees in this Office. The organisation chart bellows depicts the Corporation’s structure: Figure 1: Organization Structure

Page 3

1.2.2 Electricity Division This Division is responsible for the generation of electricity through the Marsa Power Station and the Delimara Power Station; and distribution through its multi-tier high and low voltage cable network, and overhead lines, connected through Distribution Centres and Sub-Stations. The Electricity Division constitutes the largest organisational element of the Corporation. A detailed review of the Division is captured in Chapter 7. This Division has staff as follows: - Marsa Power Station 436 - Delimara Power Station 227 - Distribution 351 - Development 159. 1.2.3 Petroleum Division This Division is responsible for the procurement of fuel, diesel et al and for the supply of fuel in the inland market, Enemalta Corporation, and the Aviation Unit of the Corporation. This Division is effected by the liberalisation of the inland market introduced in October 2007. A detailed review of the Division is captured in Chapter 8. This Division has 163 staff. It is pertinent to note that the Government through the Privatisation Unit and MIMCOL is at ITT stage in the commercialisation process of this Division. An articulation of the commercialisation process is captured in Chapter 8.3 1.2.4 Gas Division This Division is responsible for the storage, filling and distribution of gas to Gas Distributors. Although this Division is small in terms of staff, it is a strategic division given that it must on a ‘just in time’ basis ensure a continuous supply of gas – for which demand has increased considerably over the past years. A detailed review of the Division is captured in Chapter 9. This Division has 39 employees. It is pertinent to note that the Government through the Privatisation Unit and MIMCOL is at an advanced stage in the commercialisation process of this Division. An articulation of the commercialisation process is captured in Chapter 9.5. 1.3 Management Infrastructure The Board of the Corporation in August 2007 discussed the management support infrastructure. The Board concluded that sustained efforts are required to establish a fundamental management support infrastructure backbone that reflects the complexity of the Corporation. The following are the essential organisational and management grafting that the Board agreed to implement. 1.3.1 Strategic Sourcing and Procurement The Corporation procures on a strategic and level of scale that is probably unrivalled in Malta. Despite this, the sourcing and procurement leadership must be strengthened. The Corporation is way too much bogged down to control expenditure below Lm2,500 that strategic procurement and sourcing is at times neglected. The understanding of how to work within the technicalities of the law, exploit the existing procurement legislation, secure the most appropriate procurement medium, and establish strategic partnership and a proper functioning relationship with the Department of Contracts is a critical requirement. Moreover the success of the transmission and generation plan, and ultimately the Corporation’s ability to manage the supply of electricity effectively is directly correlated to its ability to manage its strategic sourcing programme – the building of new generators or elements of the distribution network on time, within budget, and with the best maintenance and supporting framework. In this regard the Procurement Section should be set up as a separate Department to be titled Office of Strategic Sourcing and Procurement.

Page 4

Major Issue Consideration Establish an Office of Strategic Sourcing and Procurement. In addition the Corporation should either ameliorate its relationship with the Department of Contracts or else severe them completely. The Office of Strategic Sourcing and Procurement should also be responsible for stock management. Stock management is currently the responsibility of the core line departments. This, it is strongly argued, is not correct as it does not allow for checks and balances; and thus effective governance. Functionally re-aligning stock management to this new Office would require the establishment of management positions for the myriad of stock centres managed by the Corporation. Major Issue Consideration Functionally re-align responsibility for stock management with the Office of Strategic Sourcing and Procurement and establish appropriate designated responsibility holders for stock centres. 1.3.2 Programme, Services and Facilities Management The Corporation has no central capacity to coordinate, measure and secure delivery of services and projects. Whilst projects and services should be carried out by the core line departments, the centre should be in a position to ensure that projects are delivered on time, within budget and to the determined quality; and services are delivered to predetermined benchmarks. In this regard it is believed that an Office for Programme, Services and Facilities Management is constituted. The Office will report to the Chief Executive Officer. Major Issue Consideration Establish an Office of Programme, Services and Facilities Management. This Office will be supported by two primary functions: 1.3.2.1 Performance Management and Monitoring A Performance Management and Monitoring Unit within the Strategy and Communications Department with responsibility for:

- establishing an infrastructure for project and services monitoring; - ensuring projects plans are in placed and periodic project reports are issued; - ensuring that service KPIs and KPTs are in placed and measured; - identifying problem areas; - provide intelligence reporting; - introduce the Balanced Score Card Methodology within the Corporation. Major Issue Consideration Establish a Performance Management and Monitoring Unit.

Page 5

1.3.2.2 Service Call Centre The Corporation has no proper service call centre – that is directed to monitor incidents, provides interactive service, and acts as a first line of support. Whilst it may be argued that the Service Call Centre is an operational activity it is strongly believed that given the new culture that such a set-up will bring to the Corporation in terms of service delivery, benchmarks and monitoring that the Centre should at the outset be established under the sponsorship and championing of the Chief Executive Officer. Over the summer, the Corporation took steps to introduced limited call centre services beyond the existing Service Dispatch Centre. It is never the less argued that the role of the Service Call Centre should be broadened to enable the Call Centre to: - act the only port of call for electronic interactions with the Corporation; - act as first line of support vis-a-vis the management of immediate reaction to arising electricity

issues; - act as the intelligent interface between the client and the Corporation until such time that

Enemalta Corporation places all of its interactive client process on an e-services platform. Major Issue Consideration Establish a Service Call Centre. 1.3.3 Health and Estate Services Management Health and safety is crucial given the environment within which staff at the Corporation operate in. To the extent possible, the Corporation must be able to anticipate risks in order to take preventive measures, as against reacting once disasters occur. Whilst line departments must be responsible for operations maintenance and issue management, a governance function that is independent of the line should be in place. This exists in the form the Health and Safety Unit within the HR department. In this regard, it is argued that the profile of health management (defined to encompass health, safety, rescue, and fire) should be a key performance objective of the Corporate – and thus its profile raised. It is pertinent to add that in essence the Corporation has no corporate services. House keeping and estate services management (on a holistic basis) is non existent. Given the property owned by the Corporation the current state of play is not tenable. The end result is one of shabbiness (at best) and standards that fail to positively compare with the Public Service and other government entities let alone the private sector. Major Issue Consideration Establish an Office of Health and Estate Services Management. 1.3.4 Office of Strategy and Regulatory Affairs The Corporation has a weak strategic and planning infrastructure. In this regard preliminary steps have been taken by appointing an internal graduate officer to the position of Corporate Strategist. Further to this an EU and Regulatory Affairs Office is in place, which currently reports to the Chief Technical Officer. A far more robust structure needs to be put into place. In this regard, an Office if Strategy and Regulatory Affairs is to be appointed – where-in the Office will assume a proactive stance in terms of strategic and business planning as well as in undertaking horizon scanning in terms of regulatory changes and reforms.

Page 6

Major Issue Consideration Establish an Office of Strategy and Regulatory Affairs. The Office will be supported by two primary functions: 1.3.4.1 Quality Assurance Unit The Corporation does not have a quality assurance function. ISO9001:2000 has been achieved in only one area of the Corporation – the Aviation Department. The need to introduce quality standards stems primarily from the fact that the application of such standards act as a leverage for process transformation, rationalisation and change. The marquee attained by the Corporation in becoming ISO compliant is, in essence, a secondary goal. The Corporation requires a Quality Assurance Unit that will seek to:

- improve operational safety, reliability and effectiveness of services aimed at maintaining its high competitiveness at present and in future;

- create the Corporate Quality Management System based on the EFQM methodology, complemented by ISO 9001:2000 certification;

- establish the Environmental Management Systems, meeting ISO 14000 certification for minimising environmental impacts;

- centralise any other quality measures underway at the Corporation within the Quality Assurance Unit.

Major Issue Consideration Establish a Quality Assurance Unit. 1.3.4.2 Research and Innovation Unit The Corporation has no locum of responsibility for research and innovation. Research and innovation in environment technologies as well as in alternative energy is of fundamental importance to the Corporation. Moreover the National Strategy for Research and Innovation approved by Cabinet last year designates the Corporation as strategic entity which should set capacity for Research and Innovation, and which should invest 0.25% of its budget or turnover whichever is the highest for such research and innovation. Major Issue Consideration Establish a Research and Innovation Unit. 1.3.5 Office of the Chief Information Officer The Office of the Chief Information Officer, together with a strategic HR department, should be the Corporation’s change agent. It is, however, currently structured as an ICT technical shop. The bias of the Office of the Chief Information Officer must be skewed towards change management.

Page 7

The Corporation is caught in a business process and culture time-wrap. For an aggressive process of change and transformation to be adopted skilled capacity within the Corporation must be grafted. Major Issue Consideration Re-orientate the Office of the Chief Information Officer into a business and transformation change agent by grafting the appropriate skills and capacity. 1.4 Unbundling the Corporation’s Organisation The Corporation has taken steps to meet relevant EU directive (LN511 of 2004) to unbundle its accounting in relation to distribution and generation; as well its other business and supporting operations. The unbundling of accounts has allowed for apportionment of costs and the elimination of cross-subsidisation across the various business units. The Corporation needs to determine whether it should also proceed with the unbundling of generation and distribution on an organisational basis. What would need to be undertaken is effective managerial and financial unbundling, whereby the management of the distribution system operates, in practice, isolated from the generation and supply operations. In order to achieve this: - The persons responsible for the management of the distribution system may not participate in

company structures of the integrated electricity undertaking responsible directly or indirectly for the day-to-day operation of the generation or supply of electricity.

- Appropriate measures must be taken to ensure that each operation is capable of operating

independently. - The distribution system operator must have effective and independent decision-making rights

with respects to assets necessary to operate, maintain and develop the network. The Corporation, as the ‘parent company’ would only exercise economic and management supervision rights e.g. approval of annual financial plan and ensuring that the operations of the distribution system do not exceed allocated budget. This would entail separate, distinct, management ‘cores’ including an independent financial controller, not only for the distribution system operator but also for generation and supply. Substantial restructuring of management – senior and intermediate – would therefore become necessary. Services such as human resources, legal, laboratory and other common operations can continue to operate as is – possibly with a proportion of the costs of each being allocated to the various divisions. An internal report carried out in 2006 recommends an organisation structure that seeks to secure such unbundling. The report recommends the constitution of a holding organisation which will be responsible for back-office and support functions and the divestment of the Electricity Division into two separate organisational structures: one for generation and one for distribution. The Corporation has not, to date, proceeded with this organisational re-design. A decision to re-design the organisation should not be limited solely to organisational structures and legal representation but rather with a holistic overview directed to create business units that are efficient, effective, economic and responsive to clients and the environment respectively.

Page 8

Major Issue Consideration The Corporation has designed options to organisationally unbundle distribution and generation to secure ring fenced separation of these structures in response to appropriate EU directives. Whilst a decision to proceed with such fundamental organisational re-design is yet be taken, the process of organisational change should not be limited solely to organisational structures and legal representation but rather with a holistic overview directed to create business units that are efficient, effective, economic and responsive to clients and the environment respectively.

Page 9

2 Regulatory and EU Framework at Enemalta Corporation 2.1 Introduction Enemalta is primarily governed by the Enemalta Act 1977 Chapter 272 of Laws of Malta. The Electricity Supply Regulations issued under the Enemalta Act are also very important since these regulate the Corporation’s relationship with its consumers. The Corporation is also subject to various others laws and EU directives that are briefly covered in this chapter. 2.2 The Enemalta Act Prior to the establishment of the Malta Resource Authority, the Enemalta Act was also the act that covered regulatory aspects of the various energy sectors. The Enemalta Act is currently largely intended to govern the operation of the Corporation. The main sections of the Enemalta Act are the following: - Part I. Preliminary - Part II. Constitution, Functions and Composition of Enemalta - Part III. Financial Provisions - Part IV. Transfer to Enemalta of certain undertakings - Part V. Management Committees and Officers and Servants of Enemalta - Part VI. Contracts and Power to acquire or dispose of property - Part VII. Miscellaneous Provisions A copy of the Enemalta Act is attached as Appendix 1. 2.2.1 Recent amendments to the Enemalta Act The Enemalta Act has been amended various times with the most recent amendment being done in September 2007. The amendments are premised on the fact that changes in the regulatory and operational set-up within the energy, gas and petroleum markets require a new legislative framework for the Corporation. The following are the main amendments: - On MRA’s advice new definitions relative to “energy audits”, “ energy efficiency”, “energy

service” etc have been introduced in the Enemalta Act with a view to directing the Corporation to foster a more efficient and intelligent use of energy and resources.

- Change of financial year end to reflect calendar year. - The widening of the Corporation’s functions so as to render the Corporation’s activities within

a market open to competition more flexible and wide ranging. - Further strengthened the obligation of the Corporation to abide by the requirements of the

Malta Resources Authority Act. - Established the office of Chief Executive Officer, who reports to the Board of Directors and is

be responsible for the executive and administrative conduct of the Corporation. - Board of Directors to be responsible for the formulation and the implementation of the policy

and the strategy of the Corporation. - In line with Government’s policy in this sector the requirement to establish a Works Council

has been introduced.

Page 10

- The said works council will be substituting the post of worker director. - Enemalta’s exemption from the payment of stamp duty has been removed. - Enemalta’s discretion to request overdraft has been raised from Lm200,000 to Lm1,000,000. - Enemalta’s procurement procedures have been specifically tied to LN 178 of 2005, Public

Procurement of Entities Operating in the Water, Energy, Transport and Postal Services Sectors Regulations, which deals specifically with the procurement of utilities. In fact enemalta (and wsc) is actually included in one of the schedules to this Legal Notice.

- The transfer of immovables by Enemalta has been linked to the Disposal of Government’s

Land Act. 2.3 The Electricity Supply Regulations (ESRs) The Electricity Supply Regulations govern the relationship between the Corporation and its consumers with respect to the provision of supply. Important aspects include application for services, supply and load requirements, fees, payments and responsibility for bills, tariffs, meters, readings, suspension and termination of services amongst other matters. A copy of the Electricity Supply Regulations is attached as Appendix 2. Major Issue Consideration The ESRs require an overhaul. 2.4 Other relevant legislation Apart from the Enemalta Act, other important primary legislation includes the following:

- Chapter 7 - Coal (Sale) Ordinance Chapter 22 - Water Supply Ordinance

- Chapter 25 - Petroleum (Importation, Storage and Sale) Ordinance - Chapter 81 - Utilities and Services (Regulation of Certain Works) Act - Chapter 356 - Development Planning Act - Chapter 423 - Malta Resources Authority Act - Chapter 424 - Occupational Health and Safety Authority Act - Chapter 435 - Environment Protection Act

Various secondary legislation that concern Enemalta include the EElleeccttrriicciittyy SSuuppppllyy RReegguullaattiioonnss,, Electricity Regulations (LN511/04), Commencement Notice of the Crude Oil and Petroleum Products (Minimum Security Stocks and Crisis Management) Regulations 2002 (LN 237 of 2002), Public Contracts Regulations 2005 (LN 177/2005) and Public Procurement of Entities in the Water, Energy, Transport and Postal Services Sectors Regulations 2005 (LN 178/2005) 2.5 Legal Issues and Enemalta’s Positioning The Corporation is involved in a number of Court cases and proceedings in other Courts which may have a significant impact, whether financial and / or operational, on the Corporation’s activities. The following list purports to delineate those which are believed to be important: 2.5.1 Office of Fair Trading (OFT)

i) Complaint on methodology followed to compute surcharge and on discrimination

relative to capping of certain entities such as hotels and factories.

Page 11

The OFT is investigating this complaint and has requested the Corporation to provide certain information which is presently being compiled. The Corporation has denied any discrimination in the calculation of the surcharge and the capping of activities which was introduced on direct instructions of Government as reflected in the 2005 Budget Speech.

Major Issue Consideration Should Enemalta lose this case it could potentially have to refund the surcharge above the cap to non-capped consumers. This would sum into the millions.

ii) Complaint by Attard Services Limited (ASL) / Shell relative to an allegation by the

said entities that the Corporation is creating a barrier for entry in the airport’s ground handling sector by imposing a fee, for the use of the infrastructure, which is not objective and transparent as requested by law. The Corporation, as comforted by a report compiled by PriceWaterhouseCoopers, is adamant that the fee requested is fair and reasonable.

Parallel to this case the Corporation has instituted Court proceedings in the First Hall of the Civil Court to impugn a decision of the Resources Appeals Board (as confirmed by the Court of Appeal) on the grounds of breach of the principle of Audi Alteram Partem and has filed a warrant for proihibitory injunction to suspend the execution of the said decision by the Malta Resources Authority.

2.5.2 Courts of Justice

(i) Pisani Brothers vs. Enemalta Corporation (Rent Regulation Board)

This case regards the rental of warehouses by plaintiff to the Corporation. Plaintiff contends that due to a change in use of premises and extensive structural changes the rent agreement should be rescinded. Parties to the case are attempting to solve case amicably. Plaintiff has forwarded his proposal in virtue of which he has offered either an outright sale of the premises for Lm400.000 or an increase in the rent to Lm12,000 pa. (current rent Lm500pa).

(ii) Ragonesi & Company Limited vs. Director of Contracts and Enemalta Corporation

(First Hall Civil Court)

Plaintiff has instituted two separate proceedings regarding alleged irregularities in the award of public tenders. Plaintiff is claiming damages due to the fact that he contends contract should have been awarded to his company. Court has been requested to establish amount of damages. The Corporation and Director of Contracts have strongly objected to these claims.

(iii) Baldacchino vs Kummissarju ta’ l-artijiet and Enemalta Corporation (Court of Appeal

Superior)

This case, which relates to a request for damages by plaintiffs against Government and the Corporation in view of the erection of the Delimara Power Station in the proximity of his residence, was decided on the 31st January 2007 and damages of Lm550,000 were awarded. The Government and the Corporation appealed the decision.

(iv) Attard Joseph vs Prim Ministru (First Hall):

Former Malta Electricity Board employees who were transferred to the Corporation filed this case against the Government and the Corporation. The claim is based on the fact that the said former government employees were not given the same benefits

Page 12

that are available to other employees and are claiming discrimination and compensation. The Corporation and the Government have strongly objected to these claims.

(v) Peralta vs Meilaq et (First Hall):

This case, which was filed in 1992, relates to the purchase of coal and amounts awarded may be significant as claim relates to over Lm200,000.

(vi) Ventura vs Fenech: (Court of Appeal Superior)

The case was decided in favour of the Corporation awarding a payment of approximately Lm244 000, with interests and expenses. Defendant filed an appeal to the decision. It is also worth noting that a number of cases filed by Micheal and Alfred Fenech against the Corporation (and vice-versa) in 1988 have been reappointed for hearing. The said cases relate to transactions in the petroleum markets and certain decisions may be significant although not exorbitant.

2.5.3 Arbitration Centre

i) General Soft Drinks vs Enemalta Corporation is involved in arbitral proceedings against General Soft Drinks Limited relative to the onus of bearing expenses related to the shifting of a vital underground electricity cable. The said exercise was estimated at Lm317,580.60, however one cannot exclude that the said estimate will vary due to unforeseen circumstances. In fact the arbitration proceedings which were filed in 2006 will decide who will be bearing costs and will not liquidate the said costs.

ii) Enemalta vs Regency

This case relates to recovery of dues for consumption of electricity within a development in Valletta amounting to Lm 92,000. 2.6 EU related Directives and Impacts on Enemalta Corporation 2.6.1 Rules Concerning the Internal Market in Electricity This Chapter also looks at the EU related Directives, the impacts on the Corporation, and actions taken by the Corporation where so relevant. The Corporation is subject to Directive 2003/54/EC concerning rules for internal market in electricity, as transposed into local legislation by the Electricity Regulations 2004, issued by MRA (Legal Notice 511 of 2004). Malta’s current situation under this Directive: i. Malta’s electricity system qualifies as a ‘small isolated system’, because of its annual

consumption and the fact that none of its consumption is obtained through interconnection with other systems. In fact Malta can import up to 5% of its consumption through interconnection and still qualify as a ‘small isolated system’.

ii. Under the current situation Enemalta’s generation sector is open to competition whilst its

distribution system remains classed as a natural monopoly and is not open to competition. iii. Malta is also currently eligible for derogations from a number of chapters and/or obligations

under Directive 2003/54/EC. Interconnectivity of more than 5% of consumption may render Malta subject to these new obligations.

Page 13

Amendments to this Directive are currently under review. The Directive introduces a number of obligations to the different players in the business of electricity transmission and distribution: In terms of a Transmission System Operator (TSO) Malta does not have a significant (bulk) transmission system because its network is too small. In reality, there is only a distribution system and hence no transmission system operator has been designated. With or without an interconnector this situation is not expected to change under the current regulations. In terms of a Distribution System Operator Malta is obliged to designate a distribution system operator, which is the Corporation by virtue of Legal Notice 511 of 2004 - the Electricity Regulations. The obligation of financial unbundling of the Corporation’s accounts already exists. Accounts for generation and distribution are shown separately in order to ensure transparency allowing MRA to ensure/oversee fair competition practice. The issue of unbundling the Distribution System Operator to be independent from the generation organisational structure has been discussed in 04.3 above. In terms of third party access and market opening and reciprocity, the MRA is empowered to ensure the implementation of third party access to the distribution network based on published tariffs applicable to all eligible consumers and applied effectively and without discrimination between system users. These tariffs do not exist in either practice or fact. Refusal of access to third parties due to under-capacity is permitted, but the distribution system operator shall, against a reasonable fee, provide necessary information on measures that would be necessary to reinforce the network. Malta may decide (under Article 3 of Directive) not to apply the measure above insofar as its application would obstruct the performance, in law and in fact, of the obligations imposed on Enemalta insofar as the development of trade would not be affected to such an extent that it would be contrary to the interests of the community. The issue of market access is problematic in view of Malta’s application for a derogation from the liberalisation of supply – sale and resale of electricity – to consumers. What the Corporation could eventually end up facing is a multitude of suppliers – each selling to a number of consumers, electricity purchased from the Corporation itself. Malta has applied for derogation from obligation as already stated, but interconnectivity possibly renders the granting of such derogation dubious. The existence of independent suppliers would impact the Corporation’s operations. Of overall concern however remains the issue of tariffs – MRA has the responsibility of issuing tariff structures which, under competition / State-Aid laws must reflect actual cost. The Enemalta Act (Art. 20) itself has provisions which state that tariffs must reflect cost as well as such factors as resources for future development. The current tariff structure does not reflect actual costs let alone provide for investment into the development of the system. Major Issue Consideration The issue of tariffs which under competition and State-Aid laws must reflect actual true cost is a matter of concern. A competing generator - even selling directly, through direct lines to its subsidiaries and eligible customers, would certainly invoke the above issues. This problem could easily also apply to suppliers, who might not be able to operate competitively due to the fact that tariffs may not reflect actual costs. Competition issues would certainly have to be addressed following new entrants to the electricity market. The Commission’s package of 19 September puts forward two options for achieving the aim - agreed by EU leaders at their March 2007 summit - of ensuring effective separation of network operations from production and supply activities. The first, commonly known as ownership unbundling, involves forcing vertically-integrated energy companies to sell off their transmission businesses. The second, termed the Independent System Operator (ISO) approach, would allow firms to maintain ownership of

Page 14

their transmission assets but transfer management to a separate ISO, responsible for taking investment and commercial decisions. The arguments put forward against these proposals by the Franco-German led group of eight - including Austria, Bulgaria, Greece, Luxembourg, Latvia and the Slovak Republic - are varied and complex, but their basic claim is that they are unnecessary, that the two so-called ‘options’ are too alike to be considered real alternatives and, moreover, “ownership unbundling” runs counter to constitutional law and the freedom of movement of capital. As disquiet over the Commission proposals surfaced at a Council session of Energy Ministers on 3 December 2007, the Council President asked dissenting Member States to propose a workable alternative, which led to the 29 January 2008 “third way” proposals from the eight. This third way rests on two pillars, the first concerning how the internal governance and organisation of the TSO entity would be organised; and the second detailing how grid investments, market integration and the connection of new power plants would be fostered. The first pillar items set out how the assets, staff, financial resources and identity of the TSO would be separated from the parent. It also provides for a compliance regime to separate TSO top-management from that of the rest of the company. Regarding investment and new entry, the national regulatory authority “will have the power to oblige” a TSO to make necessary investments or to hold a tender where the TSO “is not willing” to build infrastructure as deemed necessary in the relevant national network development plan. Whilst these considerations do not apply to Malta, as it has no transmission system, the ever increasing powers of the Commission, the creation of an ‘Agency’ to regulate the national regulators and the increasing trend by the Commission to use “comitology” to modify and re-interpret Directives well beyond their original intent and scope are worrying as they could eventually be applied to Malta, either through ‘harmonisation’ of the definition of transmission and distribution or if a sole DSO becomes classed as equivalent to a TSO. Major Issue Consideration Whilst considerations relating to a Transmission Service Operator do not apply to Malta at present, concern exists that the Commission may in the future, through the use of ‘comitology’ modify or re-interpret the Directives in such a manner that the rules relating to the TSO will become applicable to Malta. 2.6.2 Environmental Matters Malta ratified the United Nations Framework Convention on Climate (UNFCCC) as a non-Annex I party on 17th March 1994, subsequently also ratifying the Kyoto Protocol on 11th November 2001. To date, Malta has maintained its non-Annex I party status, even after accession to the European Union (EU) on 1st May 2004. Under this status, it does not have any binding obligations to limit or reduce greenhouse gas emissions under the Protocol. Neither does it have any limitation or reduction targets under the ‘burden-sharing agreement’ (Council Decision 2002/358/EC of 25 April 2002 concerning the approval, on behalf of the European Community, of the Kyoto Protocol to the United Nations Framework Convention on Climate Change and the joint fulfilment of commitments thereunder, ) currently in effect. However, Malta is now bound to adopt and implement policies and measures under the EU environmental acquis.

Page 15

The following Directives impact the Corporation: 2.6.2.1 Directive 2003/87/EC (L.N. 140/2005) : Greenhouse Gas Emissions Trading Scheme

a) Reduction of GHG Emissions

The EU has set a target for a reduction of GHG emissions of 20% below 1990 levels by 2020. The emission levels allocated to the Corporation are to be established by the Second National Allocation Plan which is still being discussed with the EU Commission.

b) Emission Trading Scheme

Directive 2003/87/EC transposed by Emission Trading Scheme (LN 140/2005: European Community greenhouse gas emissions trading scheme regulations).

Capping of CO2 emissions from power plants in national allocation plans (NAPII) this is not finalised because it is dependant on the second National Allocation Plan being formally approved by the Commission.

2.6.2.2 Directive 2001/80/EC (L.N. 329/2002): Large Combustion Plant

a) Emission limits for large combustion plats

Directive 2061/80/EC on the limitation of emissions of certain pollutions into the air from large combustion plants, transposed into Maltese legislation by LN 329/2002.

This legislation sets limits on the amount of NOx and SO2 which may be emitted by generating plants. In the Corporation’s case these limits only apply for Delimara Power Station because for Marsa Power Station, the Corporation applied the facility granted by Article 21 (a) of the Directive where a written declaration was submitted not to operate the plant for more than 20,000 hours starting from first January 2008 and ending no later than 31 December 2015. Furthermore, in early 2008 the Government accepted the Corporation’s recommendations to redefine the scope of the definition of ‘diesel engines’ within the said LN; and a LN was issued in this regard

The Corporation whilst not compliant at present is in the process of complying with the limits through upgrading of its generating plant at Delimara Power Station.

2.6.2.3 Directive 2001/81/EC (L.N. 232/2004): National Emission Trading Scheme

a) National Emission Ceiling

LN 291/2002: National emission ceiling for certain atmospheric pollutants regulations). Directive 2001/81/EC transposed by. Emission ceiling for acidifying and eutrophying pollutants and ozone precursors. Enemalta will attempt to comply with the limits in accordance with these regulations, however this will require completion of the proposed modifications to the steam plant at Delimara Power Station.

2.6.2.4 Directive 1996/61/EC (L.N. 230/2004): Integrated Pollution Prevention and Control

a) Integrated pollution prevention and control

Directive 96/61 as amended; 2003/85 transposed by LN 234/2002 : Integrated pollution prevention and control regulations) which relates to consideration of climate

Page 16

change issues in policy-making and in environmental impact assessments and rules for the prevention and control of pollution including release of atmospheric pollutants, from large industrial establishments. Due consideration of the effect on emission of greenhouse gases arising from the implementation of policies and developments to be taken into account when formulating policies in other areas and assessing environmental impacts of major developments and measures. The Corporation is in process of applying for IPPC permits for both the Marsa Power Station and Delimara Power Station installations and this is being reviewed by MEPA.

2.6.2.5 Directive 1997/265/EC

The EMAS Directive is not binding on EU Members States and it has only been adopted by a few energy companies. The Corporation issued a request for proposals for consultancy services for arguing ISO-2001 Clarification in Environment Management Systems. Adjudication has been completed and the results have been submitted for review by the Tender Sub-Committee.

2.6.2.6 Directive 1996/82/EC & Directive 2003/105/EC: Control of Major Accidents / Hazards.

COMAH (Sevaso) Directive

Directive 96/82/EC on the control of major-accident hazards as amended and extended by Directive 2003/105.

This Directive applies to Delimara Power Station, three installations at the Petroleum Division (B’Bugia, Has Saptan, Ras Hanzir) and the Gas division. Internal emergency plans for all these installations have been prepared and discussions are being held with the CPD for the finalisation of their external plans.

Malta had originally asked for a 4 year transition period for the gas plant, but withdrew this during negotiations, and decided to close down the Qajjenza Plant and to build a new plant in line with the Directive at Bengħajza

The decommissioning of Qajjenza is intertwined with the Gas Division commercialisation process which is discussed later in the Dossier.

No actual dates can be given because it all depends on when MEPA issues the necessary permit.

2.6.2.7 The 1999 Gothenburg Protocol

The 1999 Gothenburg Protocol, also known as the Convention on Long Range Transboundary Air Pollution, sets national emissions ceilings for Sulphur Dioxide, Nitrogen Oxides, Ammonia and VOC’s, based on a progressive reduction of emissions from 1990 levels. Allocations for Malta have not yet been determined. It also imposes limit values for emissions from power generating plant, which are similar to those of the Large Combustion Plant Directive, with the following exceptions. The provision for existing plant which is non compliant to the limit values given to operate for 20,000 hrs as from 1st January 2008 is not allowed. The limit values for existing plant come into force as soon as the protocol is ratified. The exclusion given to stationary diesel (compression ignition) engines from the provisions of the LCPD are not allowed in the case of NOx emissions, where a limit value of 600mg/Nm3 at 5% O2 content is stipulated for new plant.

Page 17

2.6.2.8 Renewable Sources of Energy The Commission presented Malta with a binding target for energy from renewable sources in final energy consumption of 10% by 2020 and a binding 10% target for the share of renewable energy in transport, etroleum and diesel. The Corporation is conducting studies on the use of wind energy. The Corporation, as is discussed later in the Dossier, has also applied for ERDF financing of a R&D&I marine generation prototype. 2.6.2.9 Energy Efficiency Demand-side management (LN 62/2002: Efficiency requirements for new hot-water boilers fired with liquid or gaseous fuels regulations; LN 63/2002: Energy Efficiency requirements for household electric refrigerators, freezers, and combinations regulations; LN 100/2002 : Energy Efficiency requirements for ballast for fluorescent lighting regulations) - all transposing relative EU Directives. The Commission has also taken measures to reduce demand and improve end-use efficiency such as energy efficiency measures in buildings (Directive 2002/91/EC, more energy efficient industrial practices (Regulation No 761/2001 allowing voluntary participation by organisations in a Community eco-management and audit scheme - EMAS), energy efficient appliances. 2.6.2.10 Draft Industrial Emissions Directive (IPPC Directive) This draft Directive seeks to incorporate various Directives within the IPPC Directive. These include the Large Combustion Plant Directive and the Waste Management Directive. The draft directive goes further and proposes the use of mandatory limits based on Best Available Technology (BAT). This is expected to be subject to widespread opposition from the industry. Enemalta does not agree in principle with the proposals as (a) it reflects a ‘one size fits all attitude’, and (b) the use of BAT is tied in to ‘best reference’ plants, which do not reflect the actual operating requirements of the different utilities.

The proposal for the new IPPC directive is expected to come into service as from 1 January 2016 (After the 20,000 hr period for old plant expires) and affects the various types of generating plant operated (or contemplated) by the Corporation as follows: Gas turbines: As from 1/1/2016 the proposed NOx limit for gas turbines has been lowered to 90mg/Nm3 from 120 mg/Nm3. There is also a limit on the emission of CO which has to be measured. These limits are also expected (proposed) to apply to Enemalta’s existing gas turbines for post 2015 operation. Diesel Engines: The phrase "plants powered by diesel...............shall not be covered by this directive" which excludes Diesel engines from the provisions of the LCPD has been removed. There are new limits inserted for gas engines. However, no limits have yet been proposed for diesel engines operating on liquid fuels. Boilers. For operation of DPS boilers post 2015, the limits are comparable to present day BAT. Operation of plant to present day LCPD limits will not be allowed after 1/1/2016. The impact on generation plant, and future demand, are uncertain due to: - The new Industrial Emissions Directive. - The NEC Directive 2020 targets.

Page 18

- The outcome of discussions on EU greenhouse gas reductions, renewable energy targets and EU. Emissions Trading Scheme phase 3.

- The potential for carbon capture and storage (CCS).

Page 19

3 The Human Resources Framework of Enemalta Corporation 3.1 Overview The Corporation is one of the largest employers in Malta. The current staff complement is that of 1,659 personnel – down from 1775 employees over 2005. Whilst figures may denote an extensive large number of employees, the fact is that the Corporation has a weak middle management structure and, as discussed earlier, limited management support infrastructure. The Corporation is static – and has been so for decades. Between 2005 and 2007 only 70 recruitments have taken place (18 in 2005; 30 in 2006; and 22 in 2007). To a large part the recruitment relates to new engineers – which is the strata that experiences the highest turnover. The Table below shows the years of service of the employees with the Corporation: Table 1: Years of Service with the Corporation Years of Service %

0 to 3 years 59 3.55% 4 to 10 years 126 7.59% 11 to 20 years 889 53.58% 21 to 30 years 522 31.46% 31 to 40 years 58 3.49% Over 41 years 5 0.30% The gender population within the Corporation is as shown in the following Table: Table 2: Enemalta Corporation Employees by Gender Males 1538 92.70%Females 121 7.86%

The Table below shows the classification of the Corporation’s employees. Table 3: Classification of the Corporation’s employees % Engineers 83 5% Other Professional 18 1.08% Technical 1342 80.89% Administration 216 13%

As shown in the Table below the Corporation has an aging population. Only 23.85% of the population is 35 years of age or younger. A considerable 12.8% is over 56 years of age; and 29.59% are between 46 and 55 years of age. Table 4: Enemalta Corporation Aging Population

Under 25 26-35 36-45 46-50 50-55 Over 56

All Personell 49 338 575 302 189 206 Percent 3.55 20.3 34.6 18.2 11.39 12.8

Generation 25 111 257 128 73 64

Percent 1.5 6.69 15.49 7.71 4.4 3.85

Page 20

Petroleum 1 25 50 50 23 13 Percent 0.06 1.5 3.01 3.01 1.38 0.78

Development 9 60 60 19 10 11

Percent 0.54 3.61 3.61 1.15 0.6 0.66

Distribution 8 77 101 61 37 60 Percent 0.48 4.64 6.08 3.67 2.23 3.61

Gas 0 5 8 6 6 14

0.3 0.48 0.36 0.36 0.84

The above has two impacts. First it will allow for a smooth attrition of staff at the same time that the Corporation moves onto modern technology which will require less employees to operate. Second, however, succession planning needs to be embarked upon embracing a 15 year horizon as the Corporation becomes devoid of skills and knowledge and expertise as well as an element of personnel that would need to be replaced. Promotions are insignificant – with only 109 promotions taking place over three years (35 in 2005, 19 in 2006, and 55 in 2007) – that is 6.5% of the Corporation staff. This is primarily the result that the Corporation is based on traditional organisational models – hierarchical and on a grade structure. The end result is that people move into dead-end positions relatively quick in their career and the issuance, or lack thereof, of call for applications becomes a major organisational political issue. Further to this, the Corporation has no mechanisms to award performance and to manage accountability. There is an increment review mechanism, which acts as a form of accountability check. The Table below shows the instances of ‘negative’ reports between 2005 and 2007: Table 5: Instances of Negative Increment Reports

No Increment Total Nr of Employees %

2005 419 1788 23% 2006 408 1730 23.50% 2007 307 1676 18.31%